Optimal Stopping with Gaussian Processes

Abstract.

We propose a novel group of Gaussian Process based algorithms for fast approximate optimal stopping of time series with specific applications to financial markets. We show that structural properties commonly exhibited by financial time series (e.g., the tendency to mean-revert) allow the use of Gaussian and Deep Gaussian Process models that further enable us to analytically evaluate optimal stopping value functions and policies. We additionally quantify uncertainty in the value function by propagating the price model through the optimal stopping analysis. We compare and contrast our proposed methods against a sampling-based method, as well as a deep learning based benchmark that is currently considered the state-of-the-art in the literature. We show that our family of algorithms outperforms benchmarks on three historical time series datasets that include intra-day and end-of-day equity stock prices as well as the daily US treasury yield curve rates.

1. Background and Related Work

The question of when to profitably buy or sell an asset is a long-studied fundamental economic problem (Rothschild1974, 32, 31), one that is closely related to the mathematical problem of optimal stopping. While optimal stopping problems have a rich literature (Wald:1947, 42, 35), they have historically been solved analytically in restrictive settings where underlying quantities are independent and identically distributed (iid) (Bruss2000, 6, 16), with a known data-generating process.

Financial price time series such as stock prices display interesting structural properties such as mean-reversion that allow for explicit modeling (poterba1988mean, 26). Functional data analysis has long been used in modeling time series enabling long term predictions with the ability to work with irregularly sampled data (bengio_gaussian, 7). In time series modeling, approaches based on Gaussian Processes (GPs) allow long term forecasting in settings with small quantities of data for calibration and those with a need to estimate the covariance of predictions (Gaussian_time_series, 30, 17). GPs also come up in finance when studying mean reverting processes called Ornstein-Uhlenbeck (OU) processes which are GPs with an exponential kernel (gpml, 29). In (Duvenaud_thesis, 14), the author develops a range of methods for automatically choosing GP kernels based on structure observed in the data during training (processes learnt this way are called Deep GPs). In this work, we leverage the effectiveness of the functional form of GPs to provide an efficient solution to optimal stopping problems under minimal assumptions. Such general stopping problems are ubiquitous in finance, for example in the pricing of American options (McDonald86, 22, 35).

Contributions.

This work provides the following:

- (1)

-

(2)

Extension of our proposed algorithms to use Deep GPs, which have an advantage of not requiring the specification of a GP kernel beforehand.

-

(3)

Uncertainty quantification for the proposed optimal stopping value functions.

-

(4)

Empirical demonstrations of the effectiveness of our GP-based approach on historical data, namely, intra-day and end-of-day US stock prices and treasury yield curve rates, as well as on synthetic data drawn from an OU process. We demonstrate that our group of algorithms, while being more computationally efficient (exhibiting faster training times) also largely outperforms competing approaches in terms of optimality of the stopping rule.

Related Work.

From the financial literature, in (dourban2017optimal, 13), the authors solve the finite horizon optimal purchasing problem for items with a mean reverting price process, under the assumption the price series follows an AR(1)/discrete OU-process with known parameters and a convex holding cost. The work in (lipton2020closedform, 20) presents a closed form solution to this problem. In (Leung2015, 19, 21), the authors study optimal trading of a mean-reverting asset, under the assumption that the asset follows an OU process in continuous-time with infinite-horizon. In the classic work by (buy_and_hold, 36) on selling an asset following the Black-Scholes model, the optimal strategy is found to either sell immediately or wait until the end of the time horizon, depending on a “goodness” measure computable from the model parameters. A Bayesian optimal selling problem is solved in (Ming2013, 18) where offers come from one of a finite number of known distributions. (Sofronov2020, 37) tackles the setting of selling multiple identical assets against a background of sequential iid offer prices and known transaction costs.

From the machine learning literature, (Tsitsiklis1999, 39) tackle the problem of optimal stopping using Q-learning. The chosen domain is financial, dealing with pricing a synthetic multidimensional option. Work using “Zap” Q-learning by (Chen2019, 8) builds on this. The same experimental example is used and compared with the fixed point Kalman filter algorithm of (Choi2006, 9). The work by (dos, 2) views optimal stopping through the lens of deep learning, using backwards induction to fit a neural network at each timestep to approximate the true value function. This work is extended to high dimension problems in (becker_cheridito_jentzen_welti_2021, 3).

Optimal Stopping can be formulated (puterman2014markov, 27) as a Markov Decision Process (MDP) with time in the state space and with a highly restrictive action space. This specialised structure of the optimal stopping MDP renders the problem unsuitable for use with general MDP solvers, due to data sparsity and lack of influence of the decision-maker on the state transition process. In (DeisenrothACC, 12, 28), the authors address solving general MDPs using GPs. For (NIPS2003_7993e112, 28) the MDP dynamics and the value function are learned as GPs using policy iteration at finite number of “support points”. For optimal stopping problems the required number of support points would be prohibitively large, with being number of discretization points in “price” space and the time horizon. The GPDP algorithm presented in (DeisenrothACC, 12) would engender a similar computational burden when applied to the optimal stopping setting, with a distinct GP being trained for the value function at each time-step, and a -function for each (training input, time-step) pair.

The closest work to the present paper is (pmlr-v97-dai19a, 10), wherein the authors solve a hyperparameter optimisation problem by using a GP within a Bayesian Optimal Stopping scheme originally defined in (MULLER20073140, 23) to prune poorly performing hyperparameter configurations while training the corresponding neural network. This work uses a GP with a specific kernel (enforcing monotonicity) with a value function approximation based on Monte Carlo sampling. The GP based family of optimal stopping algorithms presented here uses a piecewise constant value-function approximation evaluated using Gaussian integrals to analytically estimate stopping value functions in a tractable fashion, with the underlying time-series being modelled by a GP. We further use Deep GPs to generalize the proposed algorithms when the GP kernel cannot be specified in advance.

1.1. Optimal Stopping

Following the notation in (ferguson2006optimal, 16), stopping rule problems are defined by two objects: a sequence of random variables whose joint distribution is assumed known, and a sequence of real-valued reward functions . Given these two objects, the stopping rule problem can be described as follows. You observe the sequence for as long as you wish. For each , after observing , you may stop and receive the known reward , or you may continue and observe . If you choose to continue (and not take any observations), you receive the constant amount, . If you never stop, you receive .

The goal is to choose a time to stop to maximise the expected reward. Let denote the (deterministic) stopping decision made at stage having observed , where denotes the decision to stop, and denotes the decision to continue. The observations and sequence of decisions determine the random time at which stopping occurs, where and means stopping never occurs. Our task is then to choose a stopping rule to maximise the expected return, defined as

We are interested in stopping rule problems with a finite horizon, those that require stopping after observing for some . They are obtained as a special case of the general problem above by setting .

In this work, the random variables represent asset prices at times instants . For the case where we want to find the best time and price at which to sell the asset, the reward function represents the asset price at time . Then, the goal of the stopping problem is to find the maximum expected (selling) price and the time of reaching that price. For the case where we want to find the best time and price to buy the asset, the reward function represents the negative of the asset price at time . Then, the goal of the stopping problem is to find the minimum expected (buying) price and the time of reaching that price. For the sake of clarity, we develop our technique for the former case of finding the best time and price at which to sell an asset. Since the selling decision is made at a single time step, we ignore transaction costs of asset trading in this work. Note that our developed methods are capable of solving any optimal stopping problem even though the discussion in this paper is focused on finding the best time to sell (or buy) an asset. This would require passing the GP model for random variables through the reward functions while computing the stopping value functions.

1.2. Dynamic Programming

In principle, finite horizon stopping problems may be solved by the method of backward induction. Since we must stop at time , we first find the optimal rule at time . Upon knowing the optimal rule at , we find the optimal rule at time , and so on back to the initial time using the Principle of Optimality (bellman1954theory, 4). Define to be the maximum reward one can obtain starting from time after having observed . Then, , and inductively for :

| (1) | ||||

We compare the reward for stopping at time namely , with the reward we expect to get by continuing and using the optimal rule for stages through . Our optimal reward is therefore the maximum of these two quantities. And, it is optimal to stop at if , and to continue otherwise. The value of the stopping rule problem is .

One can see that even for finite horizon stopping problems with a known distribution over , finding a solution is non-trivial with the main difficulty being the determination of the value functions (1). This bottleneck can be alleviated by the assumption of a distributional form for the reward function as in the next subsection.

1.3. Gaussian Processes

In this work, we model the asset price (consequently the stopping reward function) as a function of time with a Gaussian Process (GP) prior. A stochastic process is said to be Gaussian if and only if for every finite set of indices , the variable is a multivariate Gaussian random variable (gpml, 29). A GP is entirely specified by its mean function , and its covariance function . The covariance function or kernel is symmetric and positive definite. By convention, the mean function and we say . We also assume a Gaussian likelihood for the asset price , that is, , where is a (small) variance. Equivalently, where is Gaussian noise with variance .

Given training data comprising asset prices at time instants , we infer the distribution of at a new time instant as follows. Let be the vector of observed values, be the kernel matrix with elements and be the vector with elements . Then, one can show that the distribution of at a new time instant is Normal, with mean and variance given by

| (2) | ||||

| (3) |

The presence of the matrix inverse in (2)-(3) results in a computation time of that can be arduous for applications with . We bypass this limitation of GPs in this work by clustering samples in the training set, and fitting a GP to the centroid (most representative sample) of each cluster. The computational complexity is further reduced by clustering an initial warm start period of data.

1.4. Deep Gaussian Processes

While GPs are attractive for modeling structured time series data using an appropriate kernel, the quality of their fit depends on the knowledge of this structure beforehand. For mean reverting time series, the fact that the series shows mean reversion is used to fit a GP with an exponential kernel. In cases when such structural information is not known beforehand, the common approach is to fit multiple GPs each with a different kernel and to pick one that performs best on a validation set. On the other hand, deep Gaussian Processes (denoted DGPs henceforth) constitute a model for time series where the kernel is learned from the data as described in Chapter 5 of (Duvenaud_thesis, 14). DGPs model a distribution on functions constructed by composing functions drawn from GP priors. They are effectively a deep version of regular GPs where the outputs of a vector of GPs is fed into the inputs of the next vector of GPs (damianou2013deepgp, 11). One can think of a DGP as a neural network with multiple hidden layers with each hidden unit constituting a GP with a predefined kernel, such as a Radial Basis Function (RBF), rational quadratic or linear kernel (kern_cook, 15). The weights of the DGP are fit (typically) using variational inference using the training data.

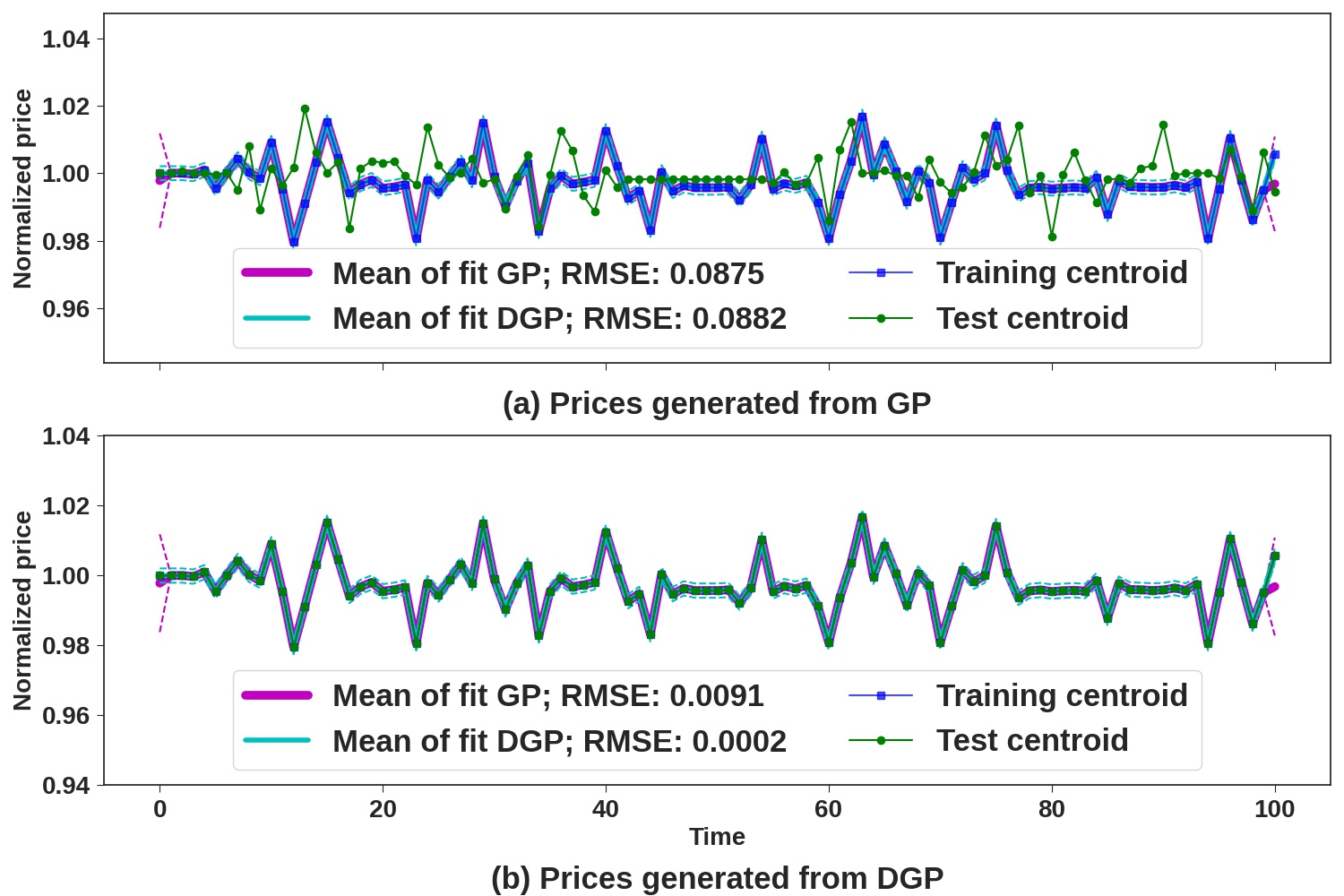

The main advantage of DGPs over GPs for modeling structured time series is that the exact knowledge of the structural form is not as necessary for DGPs as it is for GPs. Loosely speaking, the effective kernel in DGPs is learnt from data as opposed to being pre-specified for GPs. To illustrate this, we generate two sets of synthetic asset price data and partition each into training and test sets. The first set is generated from a GP with an exponential kernel. We fit a GP and DGP to the most representative sample (or centroid) of the training set and examine the GP mean function and root mean squared error (RMSE) in prediction over the test set in Figure 1 (a). We see that the RMSE in predictions over the test set for both fits are fairly close to each other. For the second data set, we generate data from a DGP with a single hidden layer. We compare the RMSE in predictions for a GP and a DGP fit to the centroid of the training set in Figure 1 (b). In this case, we see that while the RMSE of the fit DGP is small, that for the fit GP is much larger. This shows that a DGP model (when trained properly111To ensure proper training of the DGP models, we made sure their predictive performance on the training data set improved during training.) does similarly or better than a GP model fit to the same data. Moreover, a GP model may not have the capacity to fit data generated from a DGP model due to its kernel limitations. Thus, DGPs allow for automated kernel fitting while enjoying similar structural properties and computational advantages as GPs. Going ahead, we adopt both models in designing our optimal stopping algorithms. The Deep GP package (dgp_package, 34) is used to construct and train our DGP models.

2. Problem Setup

We are interested in forecasting for the best time and price to sell an asset given historical asset prices. Let be training data with being the asset price at time in sample . We build upon the idea that intra-day and end-of-day asset prices are mean reverting and hence, model them using a GP. Assuming that this structural information helps us compute the value function in (1), we compute the stopping policy as the decision to continue (holding the asset) or to stop (and sell the asset) in (1). Given new (test) asset price series up until steps in the day, we wish to use the optimal policy to find the best time and price to sell the asset.

2.1. Approximations to the value function

To make the problem more tractable, we make two assumptions to compute the value function. We first assume that the value function in (1) depends only on the asset price at the current time instant and the training data as

| (4) |

This is to say that the maximum asset price going forward from time is a function of only the asset price at time , and previously observed asset price data.

The second approximation is to assume that the value function conditioned on the training data is piecewise constant in asset price . Partition the real line into disjoint intervals , with being the collection of all such intervals222We are currently working on renouncing the bins and estimating a continuous stopping value function as a direct extension to this work.. Note that and are the lower and upper limits respectively for a bin , and write the bin center as . Then, we have

| (5) |

where . The approximation in (5) becomes an exact equality as . 333We found it sufficient to pick bins of equal length to cover the range .

Using assumptions (4) and (5) in (1), we have

| (6) |

If , putting (6) back into (1) gives

| (7) |

with the boundary condition where .

Note that the GP (or DGP) model assumption makes the computation of the integral in (7) simple using Gaussian distribution functions. The corresponding (approximately) optimal policy is given as

| (8) |

where denotes that it is optimal to sell the asset at time if the current asset price lies in bin . Likewise, denotes that it optimal to hold the asset. Note that we have decomposed the problem of finding the best time and price to sell the asset into a series of stopping decisions specifying the action to take at every time based on the asset price.

2.2. Metric to measure quality of stopping policy

Now that we are theoretically able to find a stopping policy as in (8), we need a metric to quantify its performance. Define the suboptimality of a policy over a price series as

| (9) |

(9) captures the difference in the true maximum asset price, and the predicted maximum price resulting from policy . Clearly, with lower values characterising better stopping policies. When the prices are given in $ amounts, as computed above is also in $ amount. When comparing suboptimality values across assets, it is helpful to express in basis points (denoted bps henceforth). We compute the suboptimality in bps by dividing the suboptimality in $ by the arithmetic mean of sample asset prices in $, and multiplying the result by .

2.3. Uncertainty quantification

One of the main advantages of using a GP as a model for time series is the predictive uncertainty that comes along with it. Using the fact that the price series is modeled as a GP (or DGP), we can express the price random variable as . Since we further bin the asset prices, we introduce the following random variable for bins :

This allows us to express the value function for each bin in a probabilistic way paving the way to estimate the uncertainty of the value function. If we define , and , the probability mass function (PMF) of is

| (10) |

Intuitively, the distribution in (10) is a folded version of the binned price distribution as any value smaller than gets a zero probability. (10) can be directly used to evaluate measures of uncertainty (e.g. variance) for the value function.

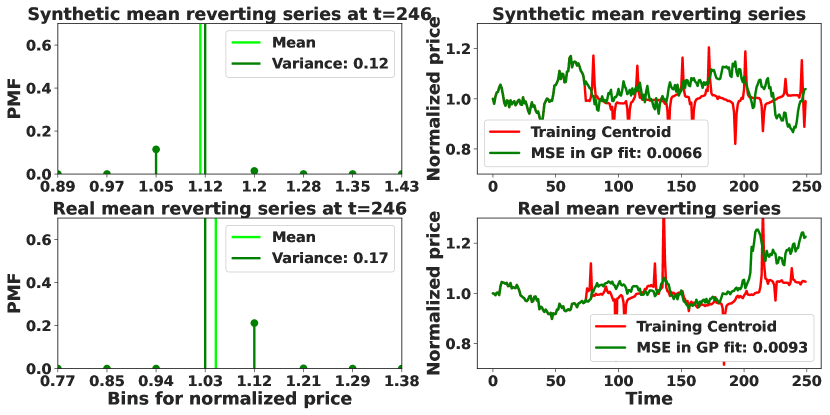

Figure 2 is a plot of the PMF of the value function (10) at a chosen time , along with the asset prices used to fit the GP model. The top row of plots corresponds to fitting a GP model to synthetically generated asset prices from a GP with an exponential kernel. The bottom row corresponds to fitting a GP model to real asset prices that are seen to be mean reverting. The right column of plots shows the training centroid over which the GP model is fit, and the test sample along with the mean squared error (MSE) in the GP fit over the test sample. Intuitively, one would expect the GP model to be a better fit for the synthetically generated data than the real asset price data. And, we see that the quality of GP fit translates into the variance in the value function.

3. Approach

Our method works by fitting a GP (or DGP) to pre-processed training data to evaluate the term inside the integral in (7).

3.1. Time Series Clustering

We preprocess the training set by partitioning it into clusters as with each cluster containing training samples over the initial time period . Define the log return (or simply return) of an asset with price at time as

where is a pre-defined time scale for computing returns. The standard deviation of asset returns is a measure of asset volatility. The clustering method takes in log returns of asset price time series as input and clusters them by grouping time series with similar volatility together. The reason for this clustering stems from the fact that asset prices can exhibit different levels of volatility based on market regimes as well as seasonal fluctuations across different assets (getreal, 41). This also enables us to pick the most relevant cluster to compute our optimal stopping policy when presented with new (test) asset prices.

We leverage a clustering algorithm called Dynamic Time Warping (DTW) that seeks to find a minimal-distance alignment between times series that is robust to shifts or dilations in time, unlike the classical Euclidean metric (dtw_original, 33, 5). For a pair of series of lengths and , there exists an algorithm that solves DTW using dynamic programming (tslearn, 38). After partitioning the training set into clusters, we summarize each cluster with a centroid time series that is meant to capture the essence of the series in each cluster. We compute the DTW centroids using the DTW Barycenter Averaging Algorithm (DBA) proposed in (dtw_barycenter, 25). We plug-and-play these time series clustering and centroid computation methods from the Tslearn package (tslearn, 38). Note that corresponds to summarizing all of the data in with a single centroid.

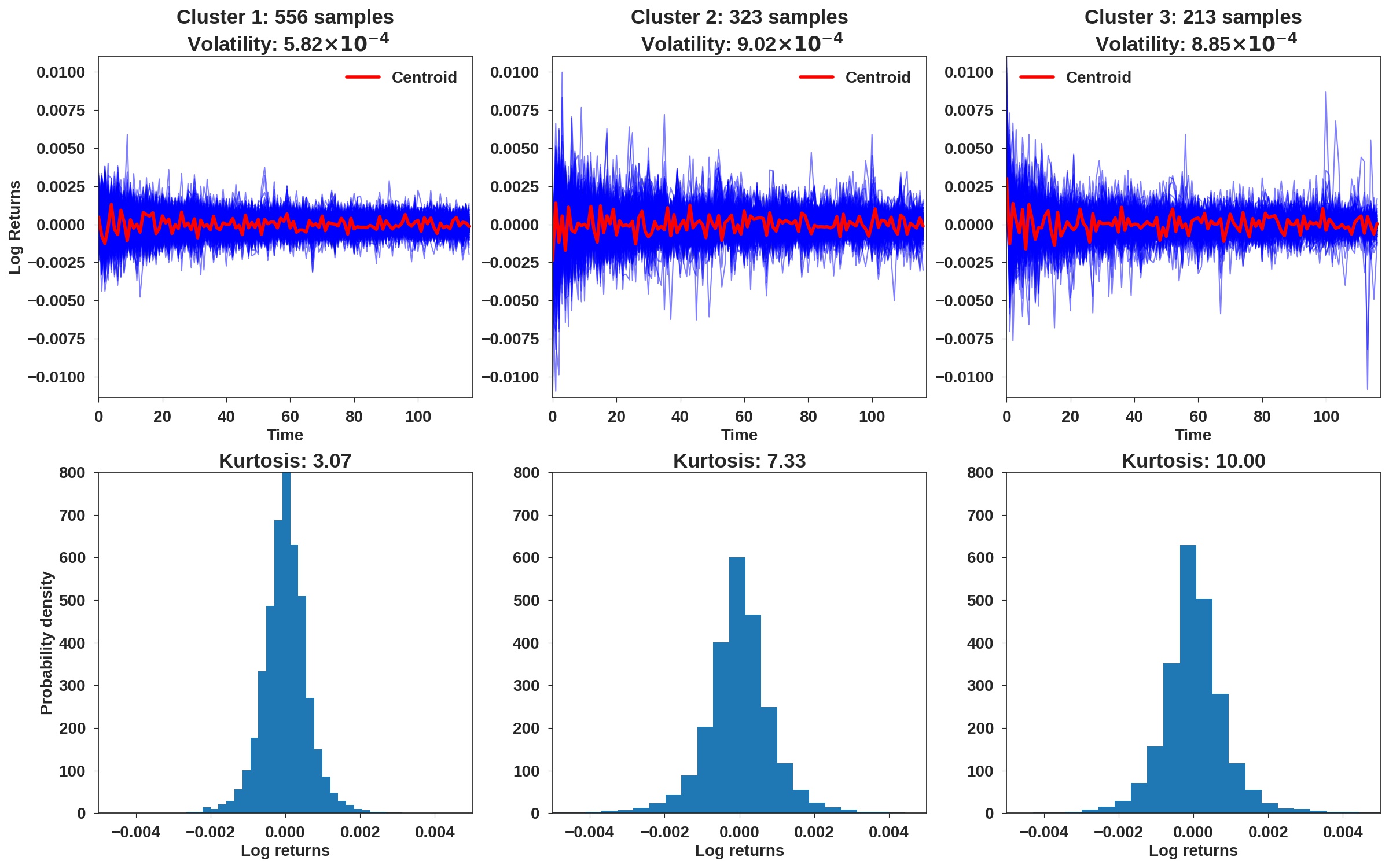

Figure 3 shows an example of DTW clustering of log returns with clusters. While the first row plots log returns along with the centroid of each cluster, the second row shows histograms of log returns. We also measure the volatility (or standard deviation) of returns in each cluster, and observe a distinction in volatility between clusters. Another stylized metric of interest for financial time series is the kurtosis or tailedness of returns distributions (getreal, 41). A large kurtosis value signifies higher deviation of the returns distribution from a Gaussian distribution. And, we observe that while cluster 1 has low kurtosis meaning that it is fairly close to a Gaussian distribution, clusters 2 and 3 have higher kurtosis.

3.2. Algorithms

After clustering the training data and computing the centroids of each cluster, we fit a GP (or DGP) to these centroids. This GP (or DGP) fit is used to compute the value function and stopping policy as in (7)-(8) for each cluster. When presented with (test) asset price series up until steps in the day, we first assign a cluster to based on the clustering on the training data. This helps us assign the test series to a cluster with similar statistical properties such as volatility. We then use the stopping policy of that cluster to find the best time and price to sell for the test series. Our algorithm is called Gaussian Process based Optimal Stopping (GPOS) and is presented in Algorithm 1.

Note that GPOS does not change the GP (or DGP) fit after observing the new test series. This can result in poor performance when the test series is rather different from the training set. To handle such cases, we propose an adaptive version of GPOS that re-fits the GP (or DGP) upon observing time steps of the new test series, while using past information for the remaining time steps of . This is given in Algorithm 2 where the computation of the value function and stopping policy are done only after observing the test series, with the training set used for clustering and filling up the centroids after time steps.

3.3. Benchmarks

Sample Optimal Stopping.

We propose an intuitive benchmark for optimal stopping algorithms that computes the stopping policy without using any structural information about the time series (such as mean reversion). We call it Sample Optimal Stopping (SOS) since it computes approximations to the value function (1) using the asset price samples in set . Define the value function for sample at time to be the highest asset price seen at/after :

| (11) |

and the average value function for the set at time as

| (12) |

(12) estimates the (true) value function used to compute the stopping policy as when the price lies in bin .

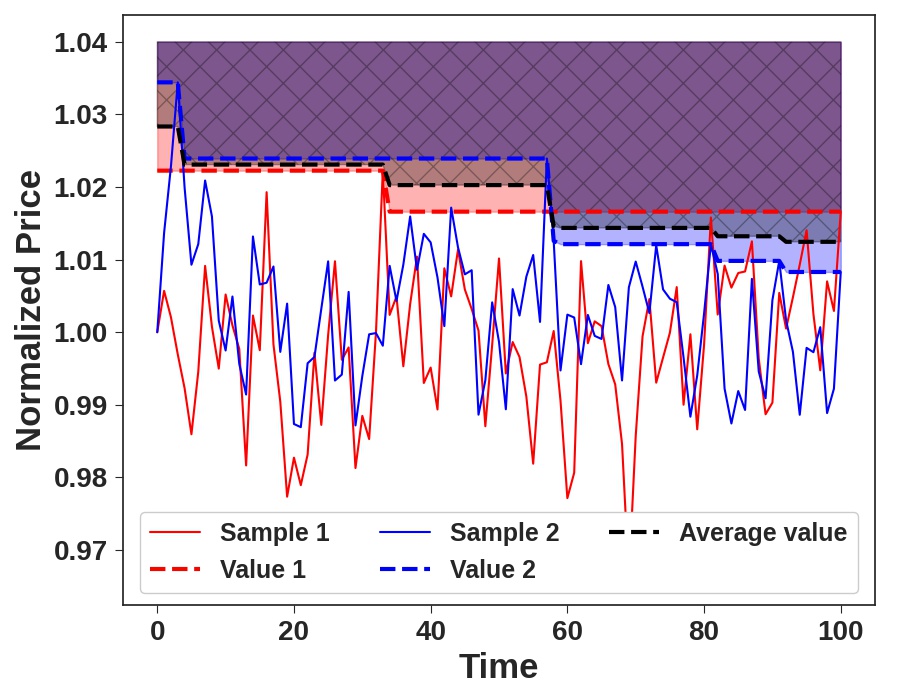

Figure 4 plots (11) and (12) in dashed lines along with asset prices in solid lines for a training set with samples and time horizon . The shaded (or hatched) region above each value function denotes the stopping policy that dictates that the asset be sold upon observing a price higher than the corresponding value. And, be held otherwise.

Deep Optimal Stopping.

We use a deep learning-based optimal stopping benchmark (denoted DOS for Deep Optimal Stopping) that is trained to learn the stopping policies given samples of the time series data and is now considered state-of-the-art in the optimal stopping literature (dos, 2). As in our framework, the authors decompose the problem of finding the best time to stop (and sell the asset) into a series of stopping decisions to be made at every time step (called the stopping policy in our notation). They model this stopping policy at every time instant with a neural network (NN) that is fit to minimize the difference between the left and right sides of (1). To have a fair comparison between our algorithms and DOS, we retain the pre-processing part including clustering the training data before learning the stopping policy within each cluster. An important note is that DOS learns as many NNs as there are time steps , so that the stopping policy at a time step is given by a different NN than that at other time steps.

4. Experiments

In this section, we compare the performance of our algorithms GPOS and A-GPOS, against that of SOS and DOS using the suboptimality metric (9)444The NN configuration for DOS was chosen as in section 4.1 in their paper (dos, 2) for the Bermudan max call option (, and ). For the DGPs, the choice was by trial and error to maximize predictive performance during training. We refrain from sharing code at the submission phase to retain anonymity.. We also include performance metrics for Deep GP based Optimal Stopping (denoted DGPOS henceforth) which corresponds to fitting Deep GP models in line 4 of Algorithm 1. Similarly, denote Adaptive Deep GP based Optimal Stopping by A-DGPOS reflecting fitting a Deep GP in line 6 of Algorithm 2. Each algorithm is tried out on price series clustered using the DTW clustering algorithm described in Section 3.1.

We consider four datasets including synthetic mean reverting time series generated from GPs, intra-day equity stock prices from early 2019, end-of-day equity stock prices from 2000 until 2020 and daily US treasury rates from 1990 until 2020. We do a 70-30 training and test split after randomly shuffling our normalized price data, and consider the stopping problem of finding the best time to sell the asset during a certain time horizon after observing its prices over the initial one third of the time horizon.

4.1. Synthetic Data Experiments

We generate synthetic time series following an Ornstein–Uhlenbeck (OU) process which is a mean-reverting process popularly studied in financial literature (nongaussianou, 1, 24). An OU process is a stochastic process with the following mean and covariance functions

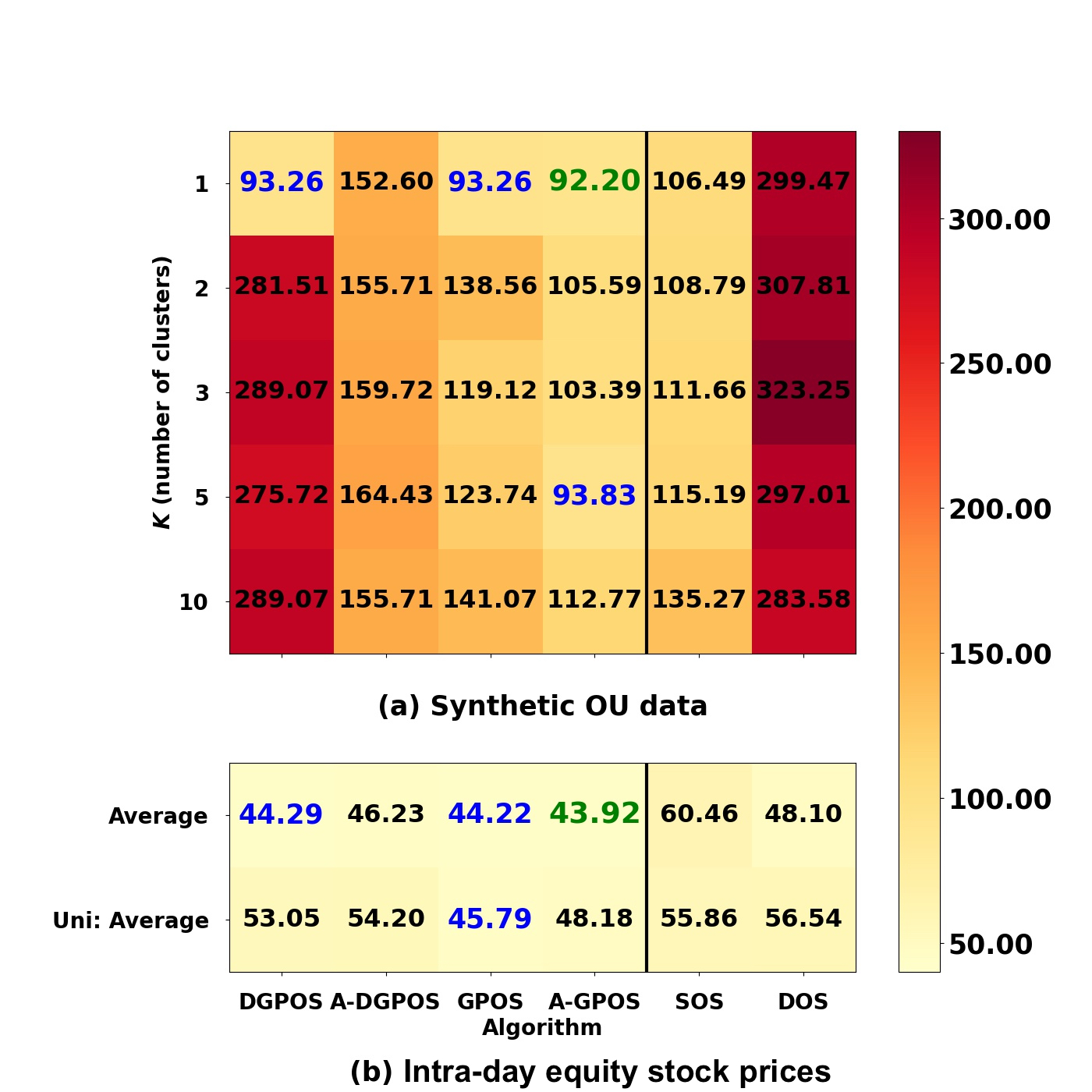

where is the mean reversion parameter, is a drift term and is a variance parameter. OU processes are a special type of Gaussian processes, those with an exponential kernel (gpml, 29). We generate samples of synthetic OU series from the same GP with different seeds. Figure 6 (a) shows suboptimality values with each row corresponding to a different number of clusters . We see that Adaptive GPOS with no clustering does the best, with GPOS and Deep GPOS doing the next best in suboptimality. As expected for synthetic data generated from a GP, algorithms using a GP model with the same kernel structure perform slightly better than those using DGP models.

4.2. Historical Price Data Experiments

We look at three historical price datasets – intra-day and end-of-day equity stock prices for nearly two dozen stocks, and 1 Yr US treasury rates. Since we have access to prices of more than one asset within each dataset, we devise a universal model for prices across assets by fitting a GP to (centroids of) clusters of normalized prices from all assets. Intuitively, this would correspond to clustering assets with different characteristics such as volatility, into different clusters.

Intra-day equity stock prices.

We have intra-day equity stock prices measured every minute in a trading day for 26 out of the 30 underlying stocks of the Dow Jones Industrial Average (DJIA) in early 2019. The goal of the stopping problem is to find the best time to sell an asset during the trading day, given initial price data for the first one third of the day. Figure 6 (b) is a matrix of suboptimality values with clusters where the first row displays the average suboptimality of stopping algorithms across the 26 stocks considered. We are able to compute the average across stocks using an arithmetic mean of suboptimality values for each stock since we express suboptimality in bps. And, the second row displays the average suboptimality of the universal model across all stocks. We see that our proposed algorithms beat the benchmarks with adaptive GPOS doing the best, and with DGP based algorithms being within 5% of the best.

End-of-day equity stock prices.

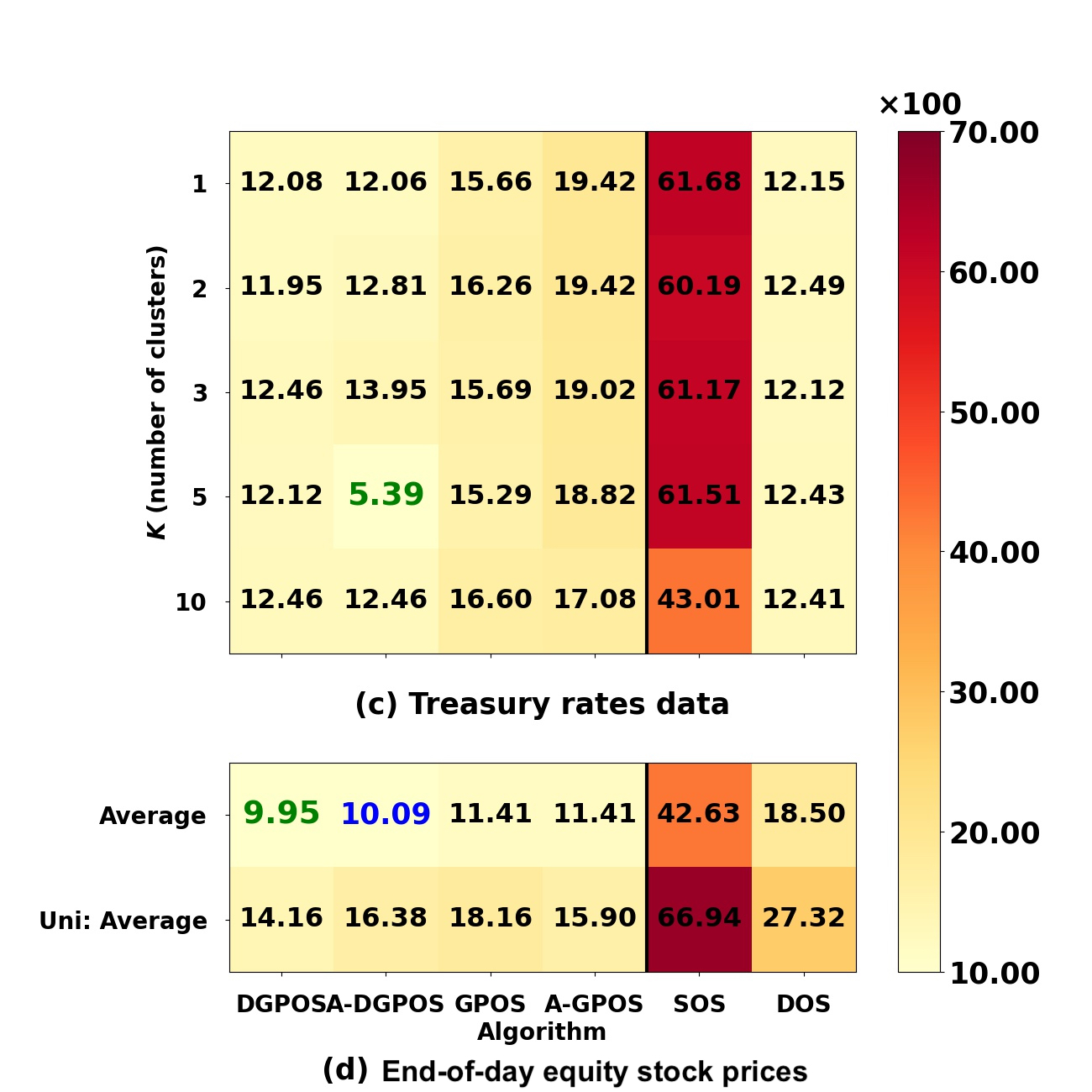

We examine prices of 23 out of the 30 underlying stocks of the DJIA that traded from 2000 to 2020 at the end of every business day. The goal of the stopping problem is to find the best time to sell an asset during a year, given prices for the first one third of the year. Figure 6 (d) shows suboptimality (divided by 100) with clusters where the first row displays average suboptimality of algorithms across all stocks. And, the second row displays average suboptimality of the universal model across all stocks. We see that our proposed algorithms beat the benchmarks with DGPOS doing the best.

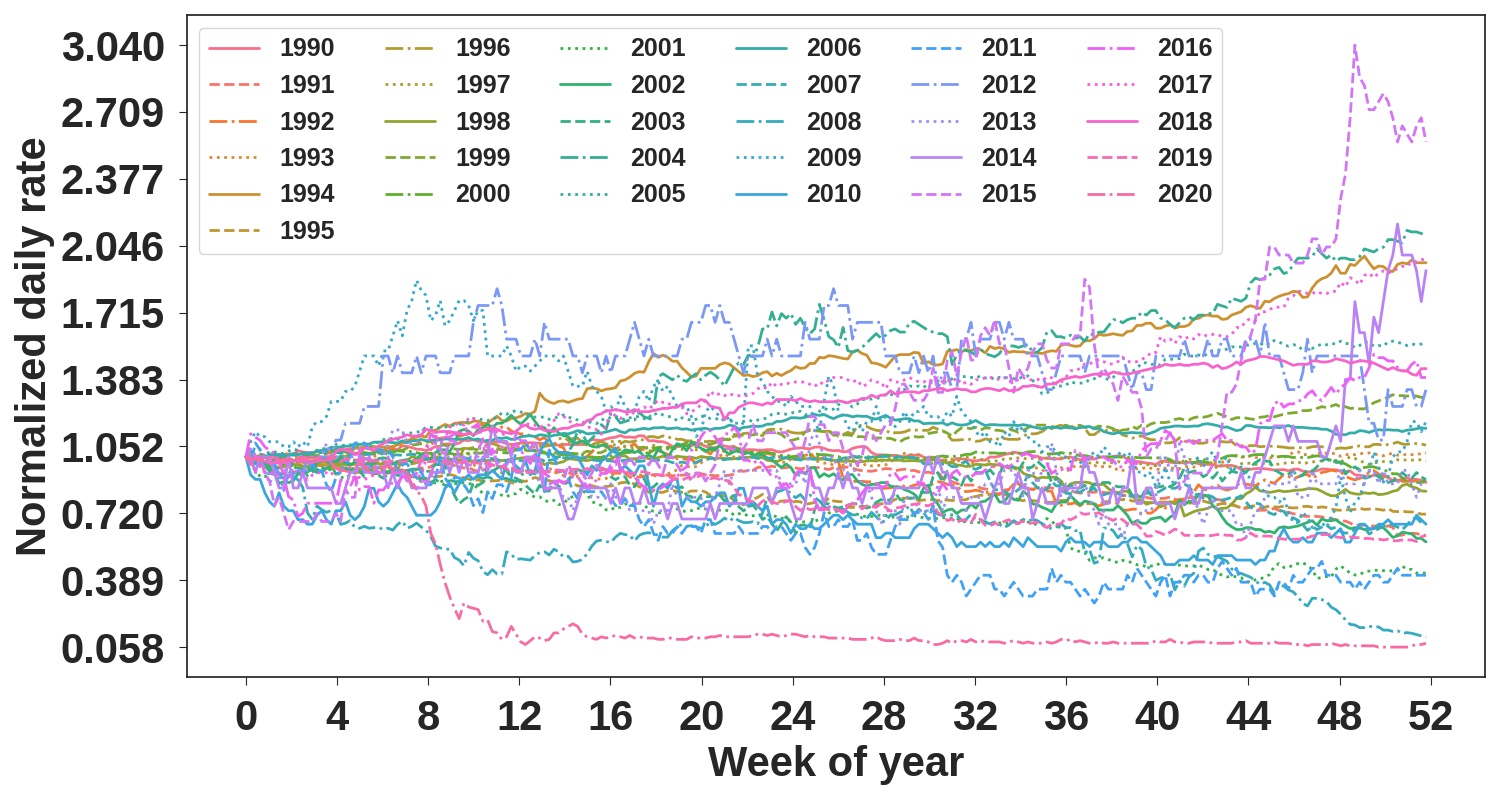

Treasury rates data.

We look at daily yield curve rates for the 1Yr Treasury from 1990 to 2020 for the US Treasury publicly available at (tsy_rates_data_source, 40). The goal of the stopping problem is to predict for the day in the year when rates would reach their maximum, given initial rates data for about one third of the year. Figure 5 is a plot of the treasury rates normalized by their initial values in the year with each curve representing a year of data. We clearly observe trends in the rates data that require the use of a non-stationary kernel (one that depends on absolute time index) for a GP that is to be fit to this data555Notice the visible non-stationarity in year 2020 due to the COVID rate regulation!. That is to say that a GP with a exponential kernel would perform poorly on the treasury rates data while doing well on the previous asset price data. Recollect that the DGP came up as the result of trying to overcome such a pre-defined kernel choice for GP models. Figure 6 (c) shows the suboptimality of our proposed algorithms (divided by 100) with rows specifying the number of clusters . As expected, we see that adaptive DGPOS performs better than GP based methods (without a specially picked kernel) while beating both benchmarks.

5. Discussion and Conclusion

We propose a family of algorithms to generate stopping rules for time series that can be modeled using Gaussian Processes. We utilize the Gaussian Process structure to design an analytical approach to compute stopping value functions (and their distributions) and stopping policies. We compare and contrast our family of algorithms with a sampling based benchmark as well as one from the deep learning literature. We demonstrate better performance over the benchmarks on three historical financial time series data sets. We also note that our algorithms are more computationally efficient than the benchmarks.

Acknowledgements.

This paper was prepared for informational purposes by the Artificial Intelligence Research group of JPMorgan Chase & Co. and its affiliates (“JP Morgan”), and is not a product of the Research Department of JP Morgan. JP Morgan makes no representation and warranty whatsoever and disclaims all liability, for the completeness, accuracy or reliability of the information contained herein. This document is not intended as investment research or investment advice, or a recommendation, offer or solicitation for the purchase or sale of any security, financial instrument, financial product or service, or to be used in any way for evaluating the merits of participating in any transaction, and shall not constitute a solicitation under any jurisdiction or to any person, if such solicitation under such jurisdiction or to such person would be unlawful.References

- (1) Ole E Barndorff-Nielsen and Neil Shephard “Non-Gaussian Ornstein–Uhlenbeck-based models and some of their uses in financial economics” In Journal of the Royal Statistical Society: Series B (Statistical Methodology) 63.2 Wiley Online Library, 2001, pp. 167–241

- (2) Sebastian Becker, Patrick Cheridito and Arnulf Jentzen “Deep optimal stopping” In Journal of Machine Learning Research 20 MIT Press, 2019, pp. 74

- (3) Sebastian Becker, Patrick Cheridito, Arnulf Jentzen and Timo Welti “Solving high-dimensional optimal stopping problems using deep learning” In European Journal of Applied Mathematics 32.3 Cambridge University Press, 2021, pp. 470–514

- (4) Richard Bellman “The theory of dynamic programming” In Bulletin of the American Mathematical Society 60.6 American Mathematical Society, 1954, pp. 503–515

- (5) Donald J Berndt and James Clifford “Using dynamic time warping to find patterns in time series.” In KDD workshop 10.16, 1994, pp. 359–370 Seattle, WA, USA:

- (6) F. Bruss “Sum the odds to one and stop” In The Annals of Probability 28.3 Institute of Mathematical Statistics, 2000, pp. 1384–1391

- (7) Nicolas Chapados and Yoshua Bengio “Augmented Functional Time Series Representation and Forecasting with Gaussian Processes” In Advances in Neural Information Processing Systems 20 Curran Associates, Inc., 2008

- (8) Shuhang Chen, Adithya M. Devraj, Ana Busic and Sean P. Meyn “Zap -Learning for Optimal Stopping Time Problems” In CoRR abs/1904.11538, 2019 arXiv:1904.11538

- (9) David Choi and Benjamin van Roy “A Generalized Kalman Filter for Fixed Point Approximation and Efficient Temporal-Difference Learning” In Discrete Event Dynamic Systems 16.2, 2006, pp. 207–239

- (10) Zhongxiang Dai, Haibin Yu, Bryan Kian Hsiang Low and Patrick Jaillet “Bayesian Optimization Meets Bayesian Optimal Stopping” In Proceedings of the 36th International Conference on Machine Learning 97, Proceedings of Machine Learning Research PMLR, 2019, pp. 1496–1506

- (11) Andreas Damianou and Neil D Lawrence “Deep gaussian processes” In Artificial intelligence and statistics, 2013, pp. 207–215 PMLR

- (12) Marc P. Deisenroth, Jan Peters and Carl E. Rasmussen “Approximate dynamic programming with Gaussian processes” In 2008 American Control Conference, 2008, pp. 4480–4485

- (13) Alon Dourban and Liron Yedidsion “Optimal Purchasing Policy For Mean-Reverting Items in a Finite Horizon” In arXiv preprint arXiv:1711.03188, 2017

- (14) David Duvenaud “Automatic model construction with Gaussian processes.” Doctoral thesis, 2005 URL: https://doi.org/10.17863/CAM.14087

- (15) David Duvenaud “The Kernel Cookbook: Advice on Covariance functions” [Online; accessed 24-January-2022], https://www.cs.toronto.edu/~duvenaud/cookbook/, 2005

- (16) Thomas S Ferguson “Optimal stopping and applications” UCLA, Los Angeles, CA, USA, 2006

- (17) Yunseong Hwang, Anh Tong and Jaesik Choi “Automatic Construction of Nonparametric Relational Regression Models for Multiple Time Series” In Proceedings of The 33rd International Conference on Machine Learning 48, Proceedings of Machine Learning Research New York, New York, USA: PMLR, 2016, pp. 3030–3039

- (18) Yen-Ming Lee and Sheldon M. Ross “Bayesian selling problem with partial information” In Naval Research Logistics (NRL) 60.7, 2013, pp. 557–570

- (19) Tim Leung, Xin Li and Zheng Wang “Optimal Multiple Trading Times Under the Exponential OU Model with Transaction Costs” In Stochastic Models 31.4 Taylor & Francis, 2015, pp. 554–587

- (20) Alexander Lipton and Marcos Lopez Prado “A closed-form solution for optimal mean-reverting trading strategies” In CoRR abs/2003.10502, 2020

- (21) Phong Luu, Jingzhi Tie and Qing Zhang “A Threshold Type Policy for Trading a Mean-Reverting Asset with Fixed Transaction Costs” In Risks 6.4, 2018

- (22) Robert McDonald and Daniel Siegel “The Value of Waiting to Invest” In The Quarterly Journal of Economics 101.4 Oxford University Press, 1986, pp. 707–728

- (23) Peter Müller et al. “Simulation-based sequential Bayesian design” Special Issue: Bayesian Inference for Stochastic Processes In Journal of Statistical Planning and Inference 137.10, 2007, pp. 3140–3150

- (24) Elisa Nicolato and Emmanouil Venardos “Option pricing in stochastic volatility models of the Ornstein-Uhlenbeck type” In Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics 13.4 Wiley Online Library, 2003, pp. 445–466

- (25) François Petitjean, Alain Ketterlin and Pierre Gançarski “A global averaging method for dynamic time warping, with applications to clustering” In Pattern recognition 44.3 Elsevier, 2011, pp. 678–693

- (26) James M Poterba and Lawrence H Summers “Mean reversion in stock prices: Evidence and implications” In Journal of financial economics 22.1 Elsevier, 1988, pp. 27–59

- (27) Martin L Puterman “Markov decision processes: discrete stochastic dynamic programming” John Wiley & Sons, 2005

- (28) Carl Rasmussen and Malte Kuss “Gaussian Processes in Reinforcement Learning” In Advances in Neural Information Processing Systems 16 MIT Press, 2004

- (29) Carl Edward Rasmussen and Christopher K.. Williams “Gaussian Processes for Machine Learning” The MIT Press, 2005

- (30) S. Roberts et al. “Gaussian processes for time-series modelling” In Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences 371.1984, 2013, pp. 20110550

- (31) Donald B. Rosenfield, Roy D. Shapiro and David A. Butler “Optimal Strategies for Selling an Asset” In Management Science 29.9 INFORMS, 1983, pp. 1051–1061

- (32) Michael Rothschild “Searching for the Lowest Price When the Distribution of Prices Is Unknown” In Journal of Political Economy 82.4 University of Chicago Press, 1974, pp. 689–711

- (33) H. Sakoe and S. Chiba “Dynamic programming algorithm optimization for spoken word recognition” In IEEE Transactions on Acoustics, Speech, and Signal Processing 26.1, 1978, pp. 43–49

- (34) SheffieldML “Deep GP package” [Online; accessed 25-January-2022], https://github.com/SheffieldML/PyDeepGP, 2016

- (35) Albert Shiryaev “Optimal Stopping Rules” Springer Science & Business Media, 2007

- (36) Albert Shiryaev, Zuoquan Xu and Xun Yu Zhou “Thou shalt buy and hold” In Quantitative Finance 8.8 Routledge, 2008, pp. 765–776

- (37) Georgy Sofronov “An Optimal Decision Rule for a Multiple Selling Problem with a Variable Rate of Offers” In Mathematics 8.5, 2020

- (38) Romain Tavenard et al. “Tslearn, A Machine Learning Toolkit for Time Series Data” In Journal of Machine Learning Research 21.118, 2020, pp. 1–6

- (39) J.. Tsitsiklis and B. van Roy “Optimal stopping of Markov processes: Hilbert space theory, approximation algorithms, and an application to pricing high-dimensional financial derivatives” In IEEE Transactions on Automatic Control 44.10, 1999, pp. 1840–1851 DOI: 10.1109/9.793723

- (40) U.S. Department of the Treasury “U.S. Treasury rates” [Online; accessed 22-December-2021], https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yieldAll

- (41) Svitlana Vyetrenko et al. “Get real: Realism metrics for robust limit order book market simulations” In Proceedings of the First ACM International Conference on AI in Finance, 2020, pp. 1–8

- (42) Abraham Wald “Sequential Analysis” John WileySons, 1947