Sandwiched Volterra Volatility model:

Markovian approximations and hedging

2Department of Business and Management Science, NHH Norwegian School of Economics, Bergen

)

Abstract

We consider stochastic volatility dynamics driven by a general Hölder continuous Volterra-type noise and with unbounded drift. For such models, we consider the explicit computation of quadratic hedging strategies. While the theoretical solution is well-known in terms of the non-anticipating derivative for all square integrable claims, the fact that these models are typically non-Markovian provides a concrete difficulty in the direct computation of conditional expectations at the core of the explicit hedging strategy. To overcome this difficulty, we propose a Markovian approximation of the model which stems from an adequate approximation of the kernel in the Volterra noise. We study the approximation of the volatility, the prices as well as the optimal mean-square hedge and provide the corresponding error estimates. We complete the work with numerical simulations performed with different methods.

Keywords: stochastic volatility, sandwiched process, Hölder continuous noise, hedging, Monte Carlo methods

MSC 2020: 91G30; 60H10; 60H35; 60G22

Acknowledgements. The present research is carried out within the frame and support of the ToppForsk project nr. 274410 of the Research Council of Norway with title STORM: Stochastics for Time-Space Risk Models.

1 Introduction

A significant number of modern financial market models is characterized by the absence of the Markov property. Such a choice of modeling framework is substantiated by a number of empirical studies indicating presence of long memory in the market volatility. For instance, [15, 16] described the long-range dependence and volatility clustering effects which led to the development of models based on fractional Brownian motion with Hurst index such as [12, 13, 14]. Other empirical studies (see e.g. [28]) conclude that Hölder regularity of volatility is strictly less than and this statement gave birth to another class of non-Markovian “rough volatility” models such as rough Bergomi [8], SABR [25], Stein & Stein [29] or Heston [22] models. A substantial advantage of such models in comparison to the Markovian ones is the ability to grasp the implied volatility surface far more accurately and reproduce e.g. the power law of at-the-money volatility skew (see [4, 23, 24] or [40, Theorem 1]).

Another example of a non-Markovian market model – which the underlying model in this paper – is the Sandwiched Volterra Volatility (SVV) model introduced in [19]. Namely, we consider the financial market composed of the two primary assets:

-

(i)

a risk-free bond (or bank account) with the price , , where is deterministic;

-

(ii)

a risky asset , the risk-free dynamics of which is given by

(1.1) (1.2) where and are given constants, is a standard 2-dimensional Brownian motion, , is a Hölder continuous Gaussian Volterra process. The discounted price of will be denoted by

(1.3)

The drift in (1.2) is unbounded and has an explosive growth to whenever and explosive decay to whenever , where are two deterministic Hölder continuous functions. This structure ensures that the volatility process is sandwiched between and , i.e.

| (1.4) |

The property (1.4) guarantees that the volatility stays strictly positive and that the price has moments of all orders. Note that the latter feature turns out to be crucial from the financial perspective: as noted in [5, Section 8], “several actively traded fixed-income derivatives require at least solutions to avoid infinite model prices”. And still, it is often absent even in classical stochastic volatility models such as the standard Heston model [5, Proposition 3.1]. Another advantage of (1.1)–(1.3) is the flexibility in the driving noise. In this work, can be an arbitrary Hölder continuous Gaussian Volterra process which allows to reproduce multiple empirical phenomena: for example, taking

gives long memory if and roughness if covering both modeling paradigms mentioned above. Furthermore, the setting of Gaussian Volterra processes is general enough to combine them as advocated in e.g. [3, Section 7.7] or [26].

While absence of Markovianity in stochastic volatility models is well supported by empirical evidence, we have to highlight that it also brings substantial difficulties from the point of view of stochastic methods, especially in optimization problems. As an example, consider a mean-square hedging problem of the form

| (1.5) |

where the financial claim and the infimum is taken over all -adapted -integrable strategies with being the filtration generated by . From the theoretical perspective, the problem (1.5) is well understood: for martingale discounted prices , the existence of the solution to (1.5) is guaranteed by the celebrated Galtchouk-Kunita-Watanabe decomposition theorem (see e.g. [36, 37]). Furthermore, if is additionally square integrable, [17] gives the explicit representation of the optimal hedging strategy: according to [17, Theorem 2.1], the solution to (1.5) can be written as the non-anticipating derivative defined as the -limit of simple processes

| (1.6) |

where denotes the mesh of the partition . Formula (1.6) is explicit in the sense that the hedge is written only in terms of the discounted price model, the information flow of reference, and the claim . This formula is in the spirit of the Clarck-Haussmann-Ocone (CHO) formula (see e.g. [35, 21]) but we stress that (1.6) has several important advantages. Namely, the CHO formula exploits the Malliavin derivative which is tailored for specific noises (e.g. Brownian motion) and claims falling in the domain of the Malliavin operator. In turn, formula (1.6) is available for all square integrable claims and all square integrable martingales as discounted prices. Nevertheless, the practical use of (1.6) is still limited in many long memory and rough volatility models including the SVV model (1.2)–(1.3) due to the absence of the Markov property. Indeed, analytical expressions for are usually impossible to obtain whereas dependence of on the past significantly complicates numerical computation of the conditional expectations in (1.6) by e.g. Monte Carlo methods.

In this paper, we tackle this problem by constructing a Markovian approximation to the SVV model (1.1)–(1.3) and then exploit it for the numerical computation of conditional expectations in (1.6). By doing this, we produce an algorithm for the computation of quadratic hedging strategies. The core of our approximation method lies in the following observation: since non-Markovianity in (1.1)–(1.3) comes from integrating the kernel , we produce an approximation of with a sequence of degenerate kernels

where and are functions, so that the -dimensional process

given by

| (1.7) | ||||

is Markovian w.r.t. the filtration . Note that a similar idea was already utilized in [10] for the Riemann–Liouville fractional Brownian motion, in [1] for the rough Heston, and in [9] for the fractionally integrated standard Heston models, as well as in [2] in the context of optimal control in more general stochastic Volterra systems.

However, there are two main challenges related to application of such an approach in the setting (1.1)–(1.3). First of all, the drift in (1.2) is unbounded which creates substantial technical difficulties in estimating the error between the original model and its approximation. Second, in order to ensure existence and uniqueness of from (1.7), it is necessary to demand that the Hölder regularity of the process is the same as the one of the original noise or higher.

In this paper, we deal with the first challenge by using the pathwise bounds for sandwiched processes developed in [20] whereas the second issue is addressed by imposing more restrictive requirements on the approximating sequence . As examples, we provide explicit sequences for the rough fractional and the general Hölder continuous kernels. Once obtained the approximation of the discounted price , we plug it into (1.6) and prove the –convergence of

| (1.8) |

to the optimal hedge when .

Note that the conditional expectations in (1.8) simplify as

with and being two measurable functions. Therefore, the problem of searching for the optimal hedge boils down to computation of and . We use numerical schemes for the SVV model from [18, 19] and provide two Monte Carlo algorithms to estimate these conditional expectations: the Nested Monte Carlo and the Least Squares Monte Carlo.

The paper is organized as follows. Section 2 contains the detailed descriprion of the SVV model (1.1)–(1.3) and gathers some necessary known results. Section 3 provides estimates of an error between the original model and obtained by replacing the kernel in the volatility with a general approximant . In Section 4, we describe the actual construction of the Markovian approximation and illustrate the approach with two examples of rough fractional and general Hölder continuous kernels. Section 5 concentrates on the mean-variance hedging problem (1.5), the description of two Monte Carlo approaches for computation of the non-anticipating derivative as well as simulations.

2 Market modeling with the SVV and quadratic hedging

Hereafter we specify the model (1.1)–(1.3) on the complete probability space in more detail and then collect some fundamental results for the upcoming discussion and recall the concept of non-anticipating derivative within quadratic hedging. Before proceeding to the main content, let us introduce some notation used in the sequel.

Notation.

- 1.

-

2.

In what follows, by we will denote any positive deterministic constant the exact value of which is not important in the context. Note that may change from line to line (or even within one line).

-

3.

Throughout the paper, will denote a standard space of square-integrable random variables. For a given square-integrable martingale , the Hilbert space of stochastic processes such that

will be denoted by .

2.1 Stochastic volatility process

First of all, we describe the driving noise in (1.2). Consider a function : that satisfies the following assumption.

Assumption (K).

The function : is a Volterra kernel, i.e. whenever , and the following conditions hold:

-

(K1)

is square integrable, i.e.

and, moreover,

-

(K2)

there exists a constant such that, for any ,

where is a constant, possibly dependent on .

By means of , we now define a Gaussian Volterra process as

| (2.1) |

and immediately remark that

-

1)

(K1) ensures that the stochastic integral in (2.1) is well-defined for all ,

-

2)

(K2) guarantees (see e.g. [7, Theorem 1 and Corollary 4]) that has a modification that is Hölder continuous of any order . Moreover, for any , the positive random variable such that

(2.2) can be chosen to have moments of all orders. In what follows, such Hölder continuous modification as well as with all the moments will be used.

In this paper, we mostly deal with difference kernels in the Volterra noise . Before proceeding further, let us give two relevant examples.

Example 2.1.

(Hölder continuous kernels) Let for some function . Assume also that is -Hölder continuous for some . Then

i.e. (K2) is satisfied and the process

has a modification that is Hölder continuous up to the order . Furthermore, if additionally , then it is easy to see that

i.e. has a modification that is Hölder continuous up to the order .

Example 2.2.

(Fractional kernel) Let with . The process

is called the Riemann-Liouville fractional Brownian motion (RL-fBm) and it is well-known (see e.g. [39, Lemma 3.1]) that, for any ,

for some constant . Thus (K2) holds and the RL-fBm has a modification that is Hölder continuous up to the order .

For a given pair , : such that , , and any , , we introduce the notation for the set

Consider a stochastic process defined by (1.2), where the initial value and the drift satisfy the following assumption.

Assumption (Y).

There exist -Hölder continuous functions , : , , , with being the same as in (K2) such that

-

(Y1)

is deterministic and ,

-

(Y2)

: is continuous and, moreover, for any

where and are given constants,

-

(Y3)

where , are given constants and ,

-

(Y4)

the partial derivative with respect to the spacial variable exists, is continuous and

for some and .

According to [20], Assumptions (K) and (Y) together ensure that the SDE (1.2) has a unique solution that is sandwiched, i.e.

| (2.3) |

This and other relevant results from [20] regarding the process (1.2) are summarized in the following statement.

2.2 Price process

Let Assumptions (K) and (Y) hold, be a Gaussian Volterra process (2.1), and be the sandwiched process (1.2) such that (2.3) holds for some functions . We now consider the model introduced in Section 1 with a risk-free asset and a risky asset defined by (1.1), where is some deterministic constant and . Clearly, the process defined by (1.3) satisfies the SDE

| (2.5) |

where, for notational simplicity, we denote . Moreover, the following Theorem holds.

Theorem 2.4.

Remark 2.5.

Theorem 2.4 implies that is a square integrable martingale w.r.t. the filtration generated jointly by and .

Remark 2.6.

We stress that (2.6) does not hold in general even in classical stochastic volatility models such as the Heston model (see e.g. [5]). This has repercussions in the possibilities of numerical simulations as well as in various applications such as pricing hedging or portfolio optimization. In our case, the existence of moments of all orders is achieved thanks to the boundedness of .

We conclude the Subsection with a result on regularity of the probability laws of and presented in [19].

Theorem 2.7.

[19, Theorem 3.8] For any , the law of (and consequently of ) has continuous and bounded density.

2.3 Quadratic hedging: some considerations

Let Assumptions (K) and (Y) hold, be defined by (1.1) and . In what follows, we discuss mean-square hedging problem and in this Subsection we provide some known theoretical background for that. We are interested in European options with rather complicated payoffs covering both classical contracts (such as standard call options) and exotic ones with discontinuities in (digital, supershare, binary, truncated payoff options and so on). Namely, the payoff function : satisfies the following assumption.

Assumption (F).

The payoff function : can be represented as

where

-

(i)

is globally Lipschitz, i.e. there exists such that

-

(ii)

: is of bounded variation over , i.e.

where

and the supremum above is taken over all and all partitions .

In what follows, we will need to approximate the discounted price by a random variable with “better” properties and then compare with . In order to do that, the following Theorem will be used.

Theorem 2.8.

Let satisfy Assumption (F) and , , . Then

-

1)

there exists a constant depending only on and such that

-

2)

if has bounded density , then

(2.7) -

3)

if has bounded density , then there exists a constant depending only on , , and the density such that

Proof.

Item 1) is obvious and follows directly from the Lipschitz condition for . Item 2) is proved in [6, Theorem 2.4]. Item 3) is simply a combination of 1) and 2). ∎

Next, consider a quadratic hedging problem of minimizing the functional defined by (1.5) over all -adapted stochastic processes . By Theorem 2.4, the discounted price is a square integrable martingale w.r.t. the filtration and hence [17] states that the unique minimizer of is equal to the non-anticipating derivative of w.r.t. . We give the necessary details regarding the non-anticipating derivatives below.

Let and be a square-integrable martingale w.r.t. a filtration . For an arbitrary partition of with the mesh , denote

| (2.8) | ||||

Definition 2.9.

Consider a monotone sequence of partitions , such that as . The -limit

| (2.9) |

is called the non-anticipating derivative of w.r.t. .

The next result shows that is well-defined and gives the orthogonal -projection of on the subspace of stochastic integrals w.r.t. . By this, it is easy to see that the linear operator is actually the dual of the Itô integral.

Theorem 2.10.

Notation.

Since the limit (2.9) does not depend on the particular choice of partition , we will use the notation

meaning that the limit in is taken along an arbitrary sequence of monotone partitions with the mesh going to zero.

Corollary 2.11.

- 1)

-

2)

Consider an arbitrary partition . The proof of [17, Theorem 2.1] implies that the pre-limit sum

(2.10) (2.11) is the -orthogonal projection of onto the subspace generated by stochastic integrals of simple processes

(2.12) w.r.t. . Note that admissible portfolios in real markets are exactly of this type since there is no technical possibility of real “continuous” trading.

3 Effects of a change of Volterra kernels

The very definition of the non-anticipating derivative describing the hedging portfolio provides a natural approximation of it. Indeed, simple processes given by (2.10) converge in to and each is itself the optimal hedge in the corresponding class of simple processes (2.12). However, computation of the conditional expectations in (2.11) is a challenging task that becomes even more complicated since the Volterra noise from (1.2) may have memory (and thus is in general not Markovian). The numerical computation of conditional expectations in a non-Markovian context is a renowned crucial problem in this context of hedging and represents a true obstacle for effective implementation. In order to tackle this problem, one may try to obtain a finite-dimensional Markovian approximation to the process which would significantly simplify numerical algorithms. Our approach is to replace the kernel in (2.1) with an appropriate approximation in that allows to obtain a Markovian structure. In this, we have taken inspiration from [1], but in our case the drift in (1.2) is unbounded and thus we need to obtain new methods for error estimation.

In this Section we study a general kernel approximation to and provide all the necessary technical estimates for the corresponding approximations: first of the stochastic volatility process and prices (see Subsection 3.1) and then of the very hedging strategies (see Subsection 3.2). We emphasize that the study of the estimates for hedging strategies is rather involved and is specialized to the family of kernels of difference type, i.e.

3.1 General approximation error estimates

As noted above, we want to replace the kernel with its appropriate -approximations , , and then consider stochastic processes and defined by

| (3.1) |

and

| (3.2) |

However, we need to make sure that the solution to (3.2) exists, i.e. Theorem 2.3 holds, for all . Moreover, we will need that bounds of the type (2.4) hold for each with constants , that do not depend on . In order to ensure that, we introduce the following assumption.

Assumption (Km).

The sequence of kernels is such that each function : is a Volterra kernel, i.e. whenever , and

-

(Km1)

for each , is square integrable, i.e.

and, moreover,

-

(Km2)

for each and with being from (K2),

where is a constant that possibly depends on but does not depend on .

As in Section 2, we see here that Assumption (Km1) guarantees that each has a continuous modification that satisfies the -Hölder property for all while (Km2) guarantees that moments of Hölder seminorms of and are in fact uniformly bounded in . The corresponding result is presented in the next lemma.

Lemma 3.1.

Proof.

Fix an arbitrary , choose such that and denote

with . By the Garsia-Rodemich-Rumsey inequality (see [27] and [20, Lemma 1.1]), for any and ,

and, moreover, the proof of [7, Theorem 1] implies that , for each .

It remains to prove that . Take any , and observe that Minkowski integral inequality, Gaussian distribution of and (Km2) yield

and thus

which ends the proof. ∎

Next, consider a family of sandwiched process , , defined by equations of the form 3.2. Note that the conditions of Theorem 2.3 are met for all , i.e. each is well-defined. Since constants , in (2.4) depend only on , the shape of and that can be chosen jointly for all , we have that

| (3.4) |

Moreover, the following result is true.

Lemma 3.2.

Proof.

The next result gives a pathwise estimate of distance between and .

Theorem 3.3.

Proof.

Fix and consider a uniform partition , , of the interval such that the mesh satisfies the condition

| (3.6) |

for from (Y4). Denote and observe that

Note that, for each , there exists between and such that

and thus

| (3.7) | ||||

Observe that each by (3.6) and denote

. By multiplying the left- and right-hand sides of (3.7) by , we obtain:

i.e.

Next, observe that, by (Y4) and (3.6), for any

Note that converges as and hence is bounded w.r.t. , therefore there exists a (non-random) constant that does not depend on , or such that

Using this, one can easily deduce that

| (3.8) | ||||

Next, fix an arbitrary and observe that (2.4) and (Y2) imply

for all . Therefore, by Lemma 3.2,

| (3.9) | ||||

where is from Lemma 3.2 and has all the moments. Moreover, (3.4) and the same argument as above yield that

| (3.10) |

with being from Lemma 3.2. Finally, using Abel summation-by-parts formula, one can write:

| (3.11) | ||||

Random variables lie between and , hence

and thus it is easy to see by (Y4) that

where is, as always, a deterministic constant that does not depend on , or . Therefore,

where

∎

We are now ready to study the error estimates for the approximations of the prices. For this, we first present a result on the moments of the approximating processes. Let us consider the price process given by (1.1) and denote

For all , we define the approximated price processes as

| (3.12) | ||||

where is given in (3.1). We also define the approximation for the discounted process in (1.3) as

| (3.13) |

Note that Theorem 2.4 immediately implies that for each and all

However, in the sequel we will require a slightly stronger result summarized in the following Lemma.

Proof.

It is sufficient to prove the result for . By Theorem 2.4 and continuity of , we can see that

| (3.14) | ||||

Since thanks to Theorem 2.3,

| (3.15) | ||||

Next, consider the process

Note that

and, since is bounded, is a uniformly integrable martingale due to Novikov’s condition. The Burkholder–Davis–Gundy inequality yields

| (3.16) | ||||

Since, by the Novikov criterion, , we can write

hence

| (3.17) |

Therefore, using (3.14), (3.15) and (3.17), we immediately obtain that

with being a constant that does not depend on and this finally proves the required result. ∎

We are now finally ready to proceed to the main result of the Subsection.

Theorem 3.5.

Proof.

Item 1. For any , (1.1), (3.12) and the continuity of imply

whence

By the Burkholder-Davis-Gundy inequality,

| (3.18) | ||||

Let us focus on the last summand of (3.18). Using the fact that

we have

| (3.19) | ||||

Studying again the last summand of (3.19), we obtain by Theorem 3.3 that there exist random variables , , such that (3.5) holds and

| (3.20) | ||||

Also, by [19, Theorem 2.6],

so the Hölder inequality as well as the Gaussianity of the random variable yield

| (3.21) | ||||

Additionally, (3.5) together with [19, Theorem 2.6] imply that

hence

| (3.22) | ||||

Therefore, taking into account (3.18)–(3.22), we see that there exists a constant that does not depend on or the particular choice of such that

| (3.23) | ||||

and item 1) now follows from the Gronwall’s inequality.

Theorem 3.5 can be easily reformulated in terms of the discounted prices. Namely, the following Corollary holds.

3.2 Error estimates for the non-anticipating derivative

Earlier on, we investigated the error between the original discounted price and the price obtained by replacing the kernel in the volatility. Hereafter, we give the error estimates between the non-anticipating derivative of w.r.t. and the non-anticipating derivative of w.r.t. .

Throughout this Subsection, we always assume that Assumptions (K) and (Y) hold, the sequence of kernels satisfies Assumption (Km) and , , , are all difference kernels, i.e.

We also recall that the payoff function that we consider satisfies Assumption (F). To allow for compact writing, we denote

where is from (1.1).

The main results rely also on some technical lemmas which we present separately.

Lemma 3.7.

Proof.

We only give the proof for the process ; the one for is identical. By the very definition of and Itô lemma, we have

| (3.24) | ||||

We remark that the above relies on the boundedness of and the moments of .

Let now be fixed. Note that, with probability 1,

| (3.25) |

and

whence, by the boundedness of ,

Next, by the Novikov criterion, the process

is a martingale, and hence, for ,

Therefore,

and we can now write

| (3.26) |

Lemma 3.8.

Proof.

Using uniform boundedness of and , the Burkholder-Davis-Gundy and Jensen inequalities as well as Theorem 3.3, one can write:

where the random variable does not depend on or . Now, since

by Corollary 3.6, it is clear that

Next, (2.6) in Theorem 2.4 implies that there exists a constant that does not depend on or such that

which yields

Similarly, by (2.6) and (3.5) we can write

which finalizes the proof. ∎

We are now ready to prove the main results of this Subsection. Recall that the payoff function satisfies Assumption (F), . Consider and observe that for any

| (3.27) |

by Lemma 3.4. Denote also and and consider the non-anticipating derivatives given by Definition 2.9:

where the limit is taken in and, for a given partition ,

| (3.28) |

with

| (3.29) |

Lemma 3.9.

Proof.

Fix and denote . It is easy to see that

| (3.30) | ||||

Now we will deal with each of the above summands separately.

Step 1: estimation of By Lemma 3.7, there exist constants , (not depending on the partition or ) such that

and

Hence, using Hölder inequality and (2.6), one can write

| (3.31) | ||||

where can be chosen to not depend on or the partition.

Step 2: estimation of By Hölder inequality, Lemma 3.7, Lemma 3.8 and (3.27),

| (3.32) | ||||

where does not depend on or the partition.

Step 3: estimation of Using Hölder’s inequality and (3.27), one can verify that

| (3.33) | ||||

By the Burkholder–Davis–Gundy and Hölder inequalities, uniform boundedness of and (2.6),

| (3.34) | ||||

Further, one can verify using Itô formula that

| (3.35) | ||||

We study the last two summands separately. It is clear that

| (3.36) | ||||

Taking into account that processes and satisfy the stochastic differential equations

boundedness of , uniform boundedness of as well as the same argument as in Theorem 3.5 imply that there exists a constant such that

whereas, again like in the proof of Theorem 3.5, we have

Plugging these estimates in (3.36), we obtain that

Next, for the second summand of (3.35) we have

| (3.37) | ||||

Using the same argument as in (3.34), one can verify that there exists a constant (not depending on or the partition) such that, for all ,

| (3.38) |

Moreover, using (2.6) and Theorem 3.3, it is easy to show that for any

whence

| (3.39) | ||||

Next, by Lemma 3.8, for all ,

| (3.40) |

Plugging the estimates (3.38)–(3.40) into (3.37), we finally obtain that there exists a constant (not depending on or the partition) such that

Taking into account all of the above, we can finally write

and whence we have the estimate

which finalizes the proof. ∎

Theorem 3.10.

Let Assumptions (K), (Y) and (Km) hold, the payoff function satisfies Assumption (F), the kernels and , , have the form

and , . Then the following statements hold.

-

1)

There exists a constant that does not depend on such that, for any partition with the mesh ,

(3.41) where and are defined by (3.28). In particular, if the partition is uniform, i.e. and ,

(3.42) -

2)

If is such that

then

Proof.

By Theorem 2.7, the random variable has continuous and bounded density, whence conditions of Theorem 2.8 are fulfilled and

where the constant does not depend on or the partition. Furthermore, by Lemma 3.9,

which gives item 1).

To prove item 2), first note that

as . Whence

By this, the proof is complete. ∎

We remark that that the exponent appears in (3.41) and (3.42) exclusively due the estimate (2.7) of Theorem 2.8 that corresponds to the (possibly discontinuous) component of . If , i.e. when

Theorem 3.10 can be reformulated as follows.

Theorem 3.11.

Let Assumptions (K), (Y) and (Km) hold, the payoff function be globally Lipschitz, and , , have the form

and , . Then the following statements are true.

-

1)

There exists a constant that does not depend on such that for any partition with the mesh

where and are defined by (3.28). In particular, if is uniform, i.e. and ,

(3.43) -

2)

If is such that

then

4 Markovian approximation of the SVV model

So far, we have obtained estimates of errors in the approximation of the volatility process, the prices and the optimal hedge generated by changing the kernel, without any requirements of Markovianity. We now move to a more specific problem of constructing kernels , , providing a Markovian structure.

4.1 General construction

Let Assumptions (K) and (Y) hold. Assume that there exists a sequence of kernels such that

-

(i)

satisfies Assumption (Km);

-

(ii)

, ;

-

(iii)

each has the form

Consider now the sequence of processes given by (3.13). Corollary 3.6 implies that

We can also see that the -dimensional process given by

| (4.1) | ||||

is Markovian w.r.t. the filtration generated by . In particular, conditional the expectations of the type (2.11) can be rewritten for the process as

which significantly simplifies their actual computation. The difficulty here lies in finding an explicit sequence of kernels , , satisfying conditions (i)–(iii) above. In the remaining part of the Section, we provide such approximating sequences for some widely used kernel types, namely rough fractional and Hölder continuous kernels.

4.2 Rough fractional kernels

Let and

| (4.2) |

i.e. is a RL-fBm as discussed in Example 2.2. For such a kernel, an appropriate sequence of -approximations is presented in [1, Section 3]. Namely, let be a measure on defined as

where is such that

| (4.3) |

Denote

| (4.4) |

By [1, Lemma 5.2], the sequence satisfies Assumption (Km) and, moreover, by [1, Proposition 3.3],

Then, by item 2) of Corollary 3.6, for any

The values satisfying (4.3) can be chosen in several ways. In [1, Subsection 3.2], it is suggested to put

| (4.5) |

In this case,

where is a positive constant that depends only on the Hurst parameter . In this case, Theorem 3.10 and Theorem 3.11 read as follows.

Corollary 4.1.

Remark 4.2.

Putting , , we obtain that each process of the form

from (4.1) is an Ornstein-Uhlenbeck process satisfying the SDE

4.3 Hölder continuous kernels

Assume that with and for some , i.e.

| (4.8) |

Example 4.3.

The fractional kernel

with is Hölder continuous of order and thus fits in the framework of this Subsection. However, note that the corresponding RL-fBM has higher regularity and is -Hölder continuous for all .

Let be the corresponding Bernstein polynomial of order defined as

| (4.9) | ||||

By [34, Proposition 2],

where is the same as in (4.8) for all . Since , and we can write for any

where does not depend on , i.e. Assumption (Km) holds. Moreover, [34, Theorem 1] gives the estimate

which implies that

and whence for any

by Corollary 3.6. In particular, Theorem 3.10 and Theorem 3.11 imply the following result.

Corollary 4.4.

Remark 4.5.

Remark 4.6.

Note that each process

is Hölder continuous of any order , i.e. the solution to the SDE

exists and is unique for any value in (Y3).

5 Monte Carlo approximation of the optimal hedge and simulations

We complete our study with simulations. In order to simulate paths of sandwiched processes, we use the drift-implicit Euler approximation scheme from [18]. The original and the approximated discounted price processes and are simulated just like in [19]. We also present simulations of the hedging strategies for a standard European call option. Note that algorithms presented below also work for exotic contracts with discontinuous payoffs, but slower convergence rates require longer computations. All simulations were performed in R programming language on the system with Intel Core i9-9900K CPU and 64 Gb RAM.

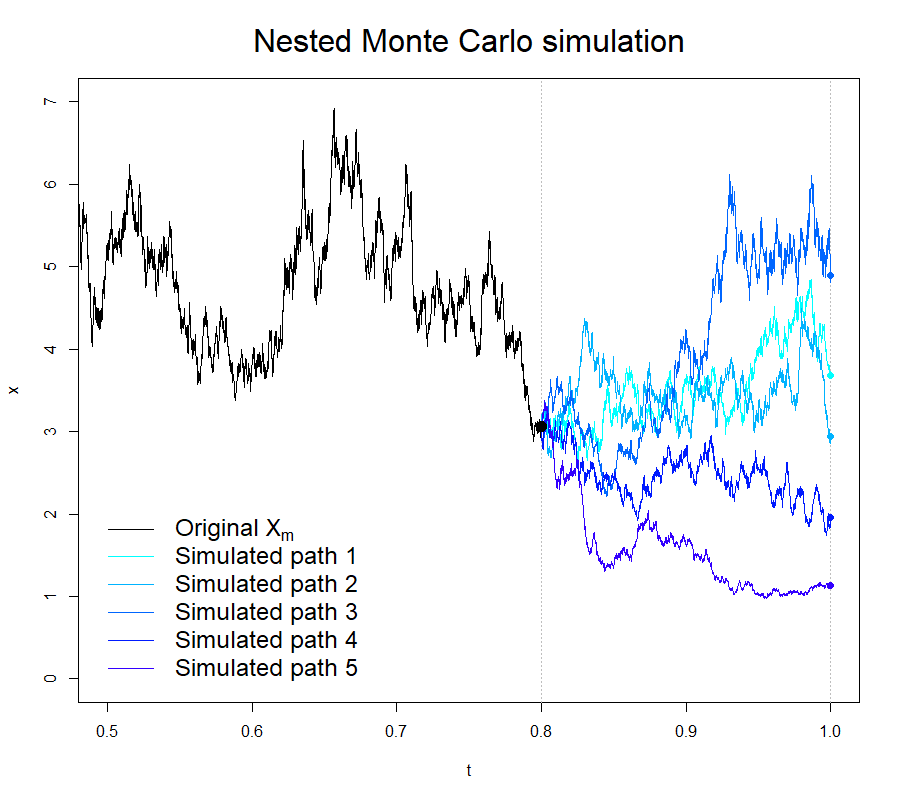

5.1 Nested Monte Carlo method

A straightforward way to compute the conditional expectations

is the Nested Monte Carlo (NMC) approach that can be summarized as follows (see also Fig. 1):

-

1)

given , , , …, , simulate independent trajectories , ;

-

2)

for each trajectory, compute and , ;

-

3)

put

Example 5.1.

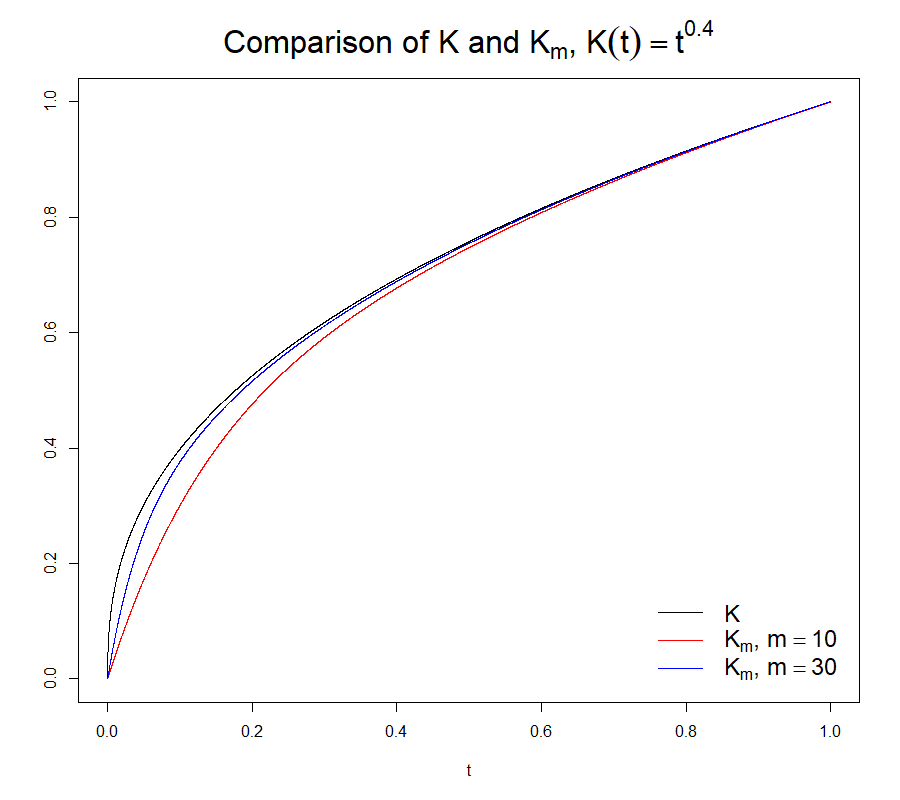

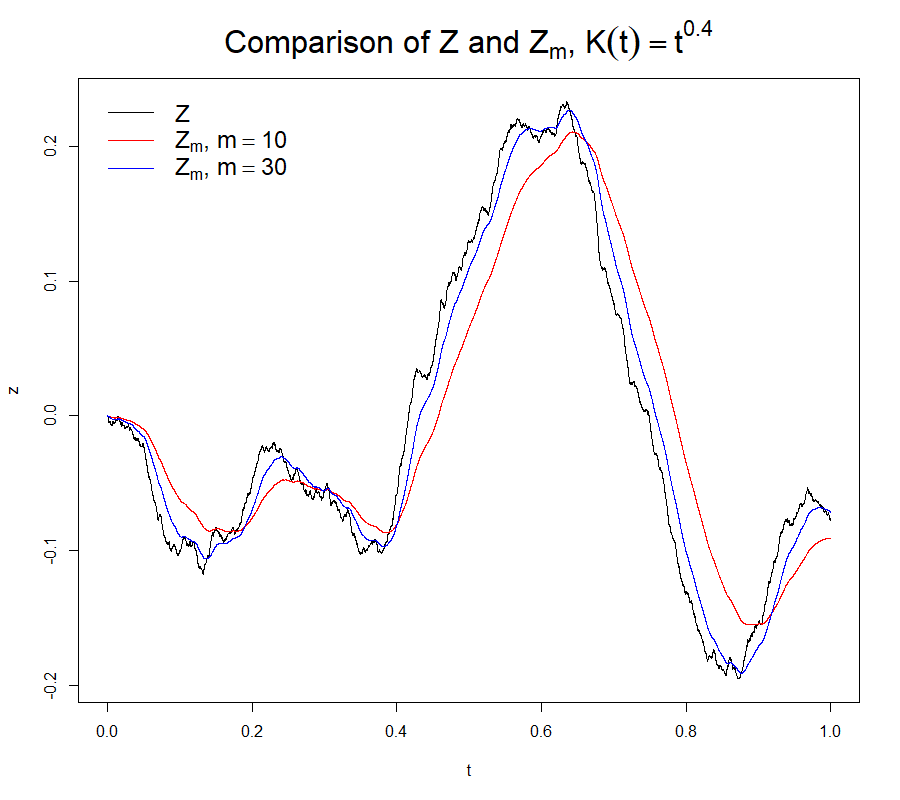

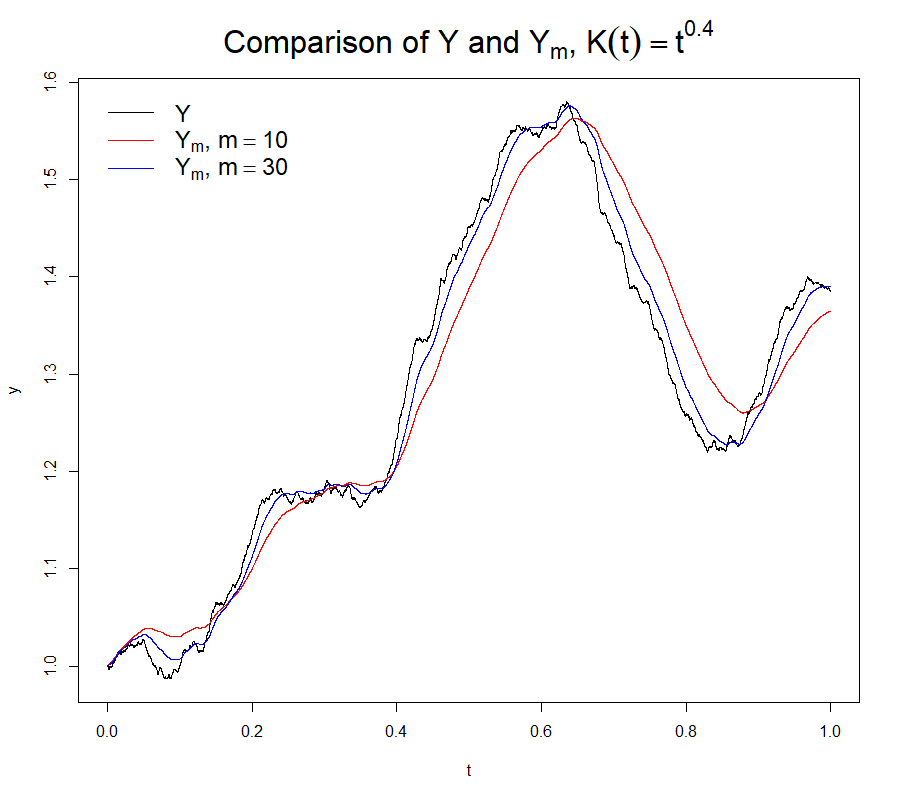

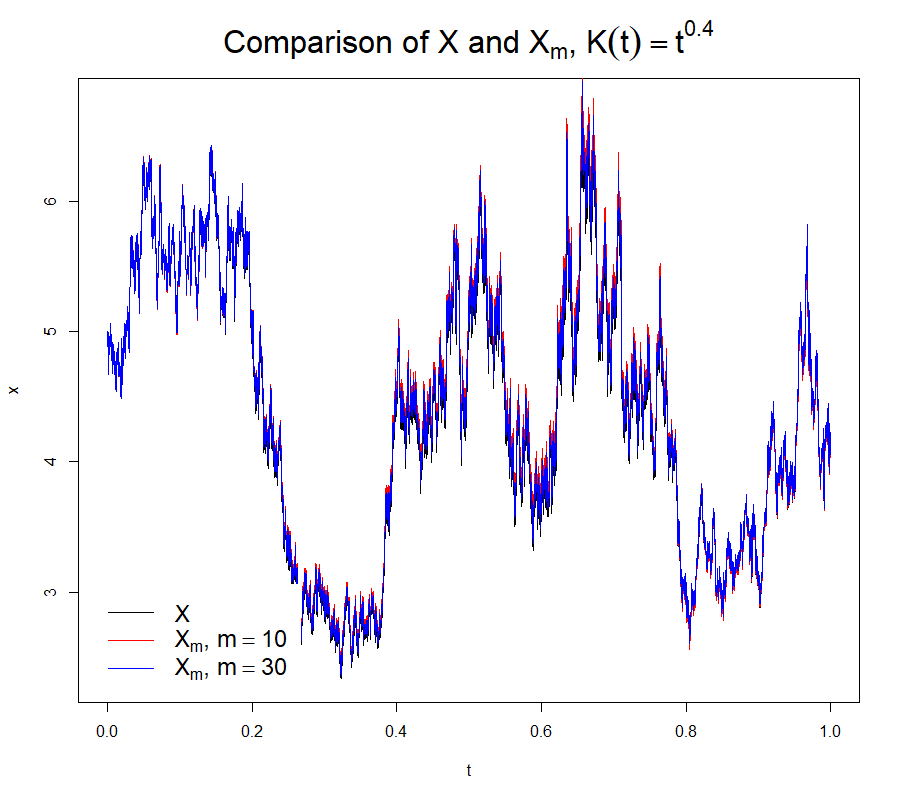

(Hölder continuous kernel) Consider the SVV model

with , , , and . The approximation is constructed using the Bernstein polynomials as described in Subsection 4.3.

(a) Kernels and

(b) Volterra noises and

(c) Volatility processes and

(d) Price processes and

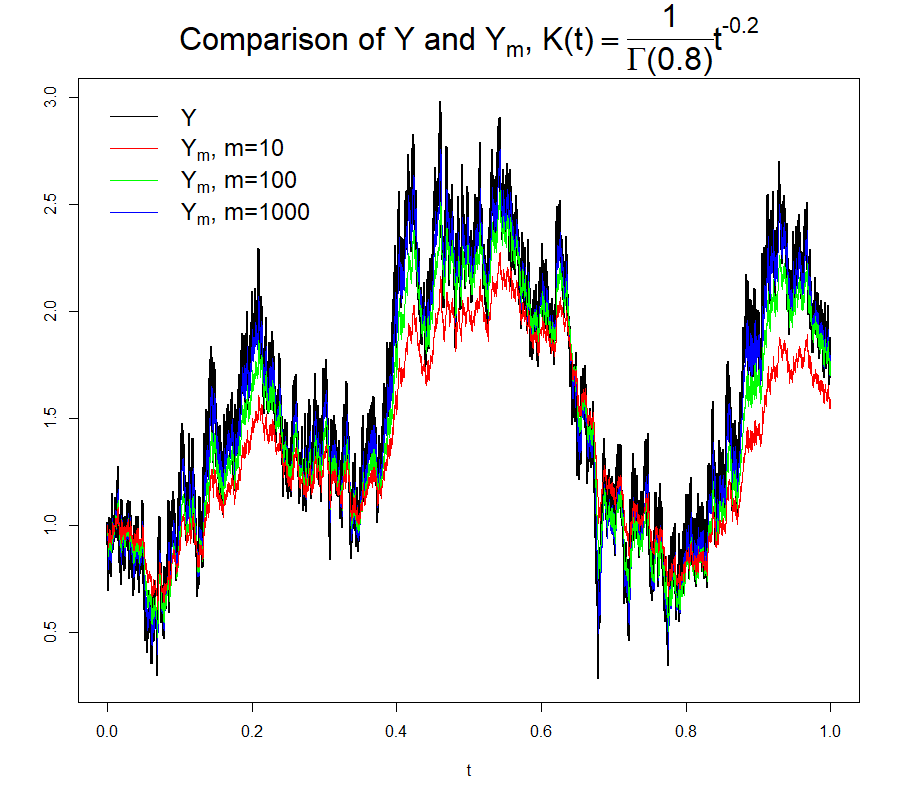

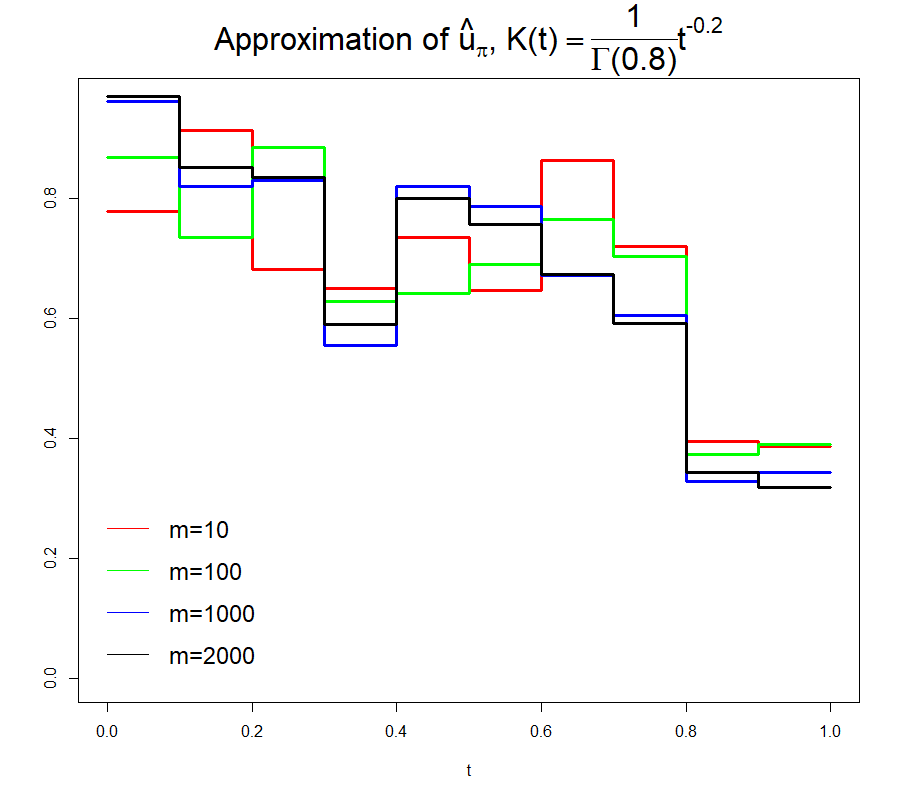

Figure 2 illustrates approximation of the SVV model; original kernel and generated sample paths of the corresponding processes are depicted in black whereas approximations using the Bernstein polynomials are depicted in red (of order ) and blue (of order ). Note that the path of simulated using the original noise (black) is not visible on Figure 2(d) due to the high degree of overlapping with the approximations (red and blue trajectories). Figure 3 contains a path of the process

| (5.1) |

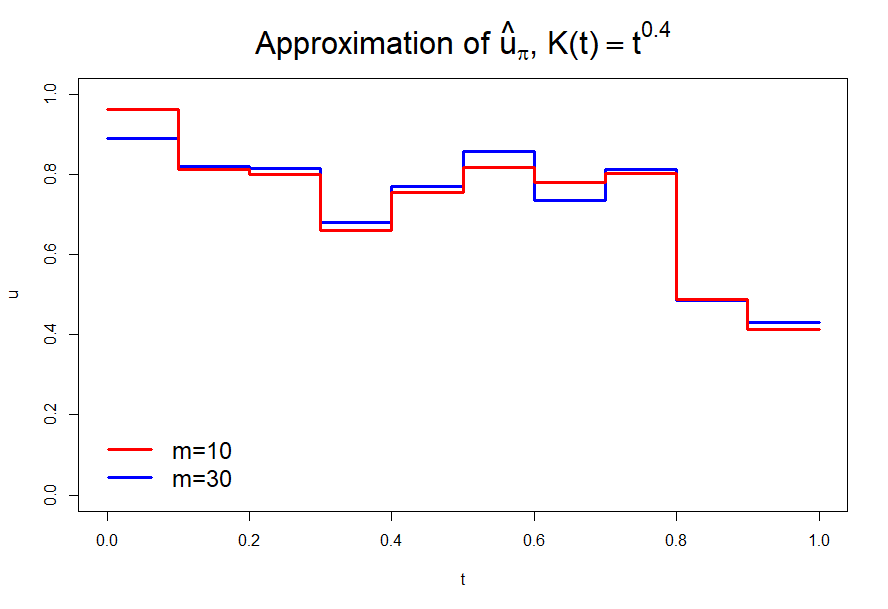

with the European call payoff function and the values , , , …, coming exactly from the trajectory depicted on Figure 2. In order to estimate

100000 simulations were used for each .

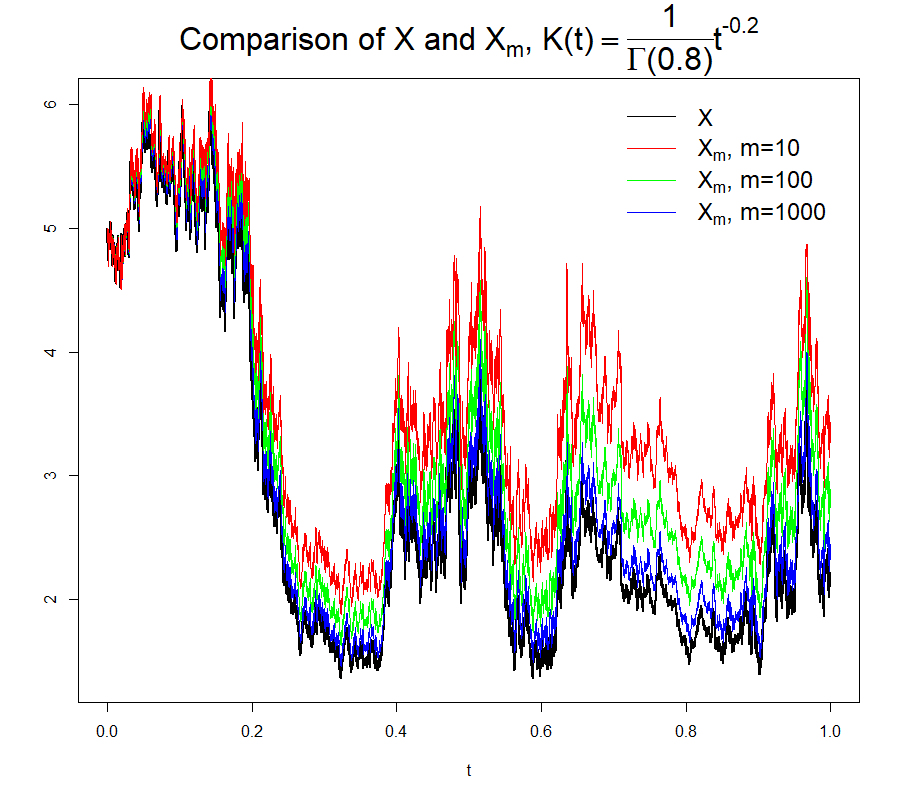

Example 5.2.

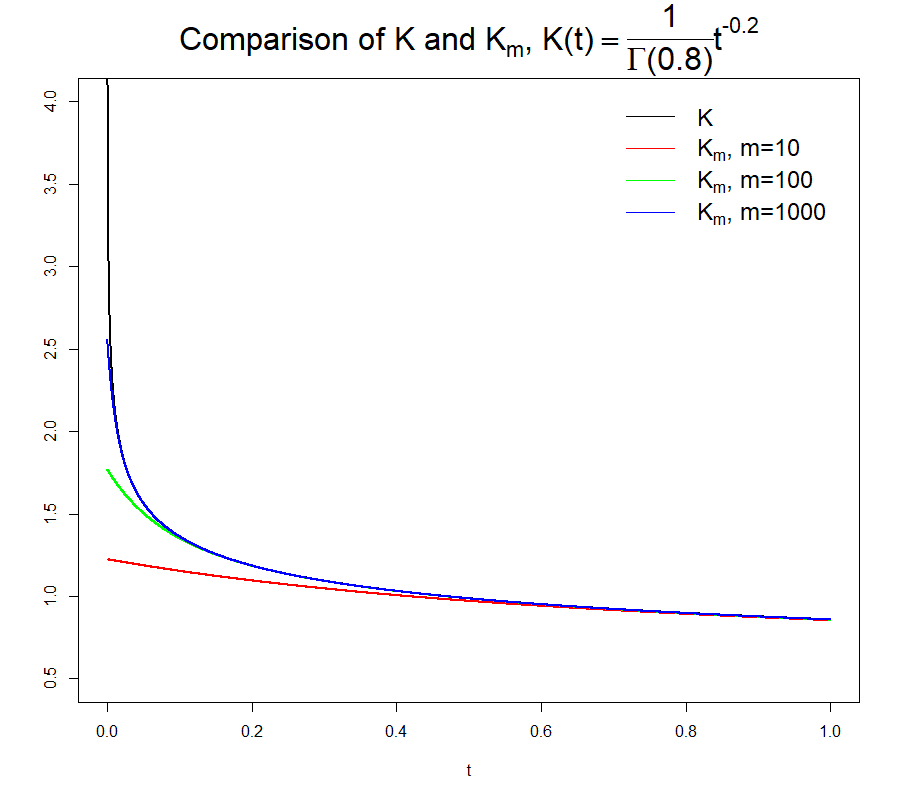

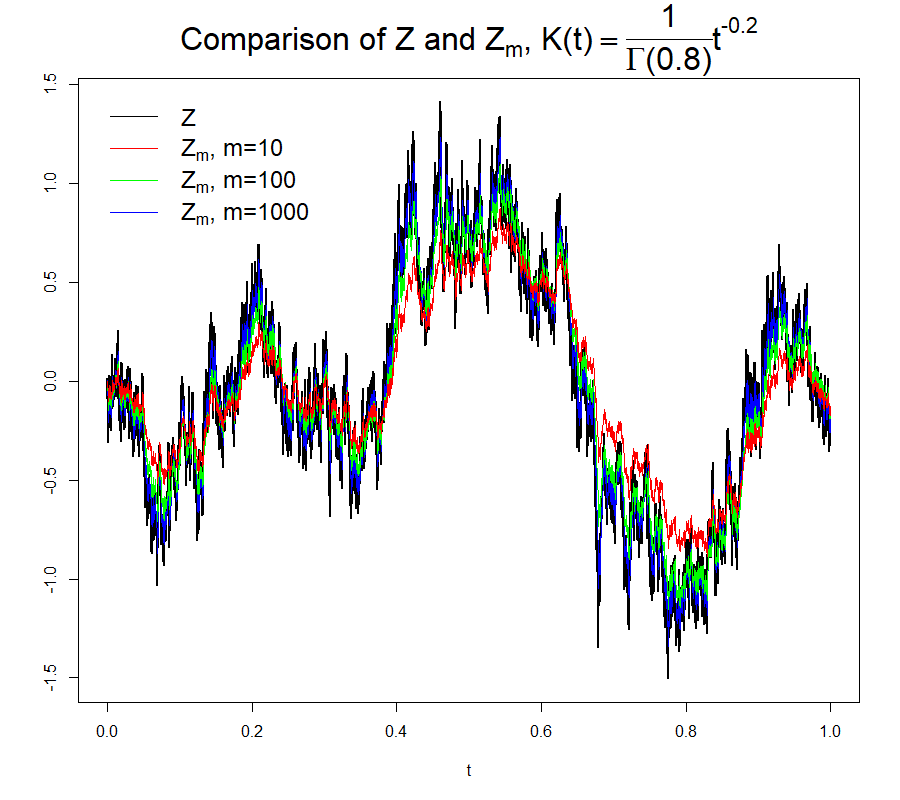

(Rough kernel) Consider the SVV model

with , , , and . The approximation is constructed by approximating the Volterra noise by a linear combination of standard Ornstein-Uhlenbeck processes as described in Subsection 4.2.

(a) Kernels and

(b) Volterra noises and

(c) Volatility processes and

(d) Price processes and

Just as in Example 5.1, Figure 4 illustrates approximation of the SVV model; original kernel and generated sample paths of the corresponding processes are depicted in black whereas approximations are depicted in red ( summands), green ( summands) and blue ( summands). Note that rough volatility requires much higher values of in order to ensure a decent level of approximation in comparison to Example 5.1.

Figure 5 contains a path of the process

| (5.2) |

, where the payoff function and the values , , , …, are exactly the ones from the trajectory depicted on Figure 4. In order to estimate

100000 simulations were used for each .

5.2 Least squares Monte Carlo method

Despite its simplicity and clear theoretical justification, the nested Monte Carlo approach has a substantial disadvantage: it takes long to compute and thus requires powerful computational resources in order to be used in practice. In order to overcome this issue, one can use the Least Squares Monte Carlo (LSMC) method instead:

-

1)

simulate independent realizations

;

-

2)

for each path, evaluate

and

;

-

3)

apply an appropriate non-parametric regression (with a mean squared error loss function) to the generated “dataset” treating

as “input” and

as “output” variables. The resulting estimates , of the regression functions are then used to calculate on the interval .

Remark 5.3.

Example 5.4.

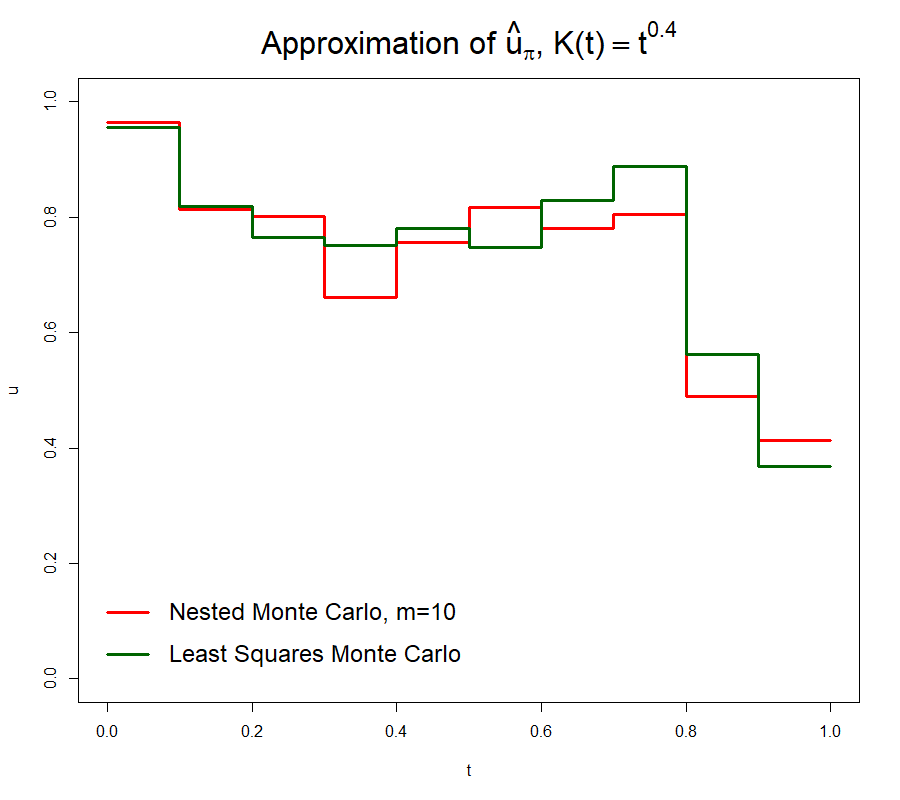

Fig. 6 contains approximations of the optimal hedging strategy constructed for the path of from Example 5.1 that corresponds to . In order to obtain the dark green line, we simulated the “dataset” containing the “input” variables

together with the corresponding “output” variables

with for each . In order to compute , , we used the idea from [31] and utilized a neural network with 3 hidden layers and 20 nods in each layer. The red line is exactly the path of for from Fig. 3 and is treated as a reference.

Note that the Nested approach described in Example 5.1 required 63231 seconds to simulate a path of corresponding to a single realization of whereas the Least Squares modification took roughly 6 days to simulate the initial dataset and about 5 hours to fit the neural network. Once ready, the actual computations were conducted almost instantly.

Remark 5.5.

The neural network architecture in Example 5.4 is not optimal. It is fairly clear from Fig. 6: even though the LSMC Monte Carlo estimate preserves in general the shape of the reference optimal hedge simulated using the NMC approach, the difference between the two is still quite substantial. We emphasize that performance of the NMC method heavily depends on the chosen non-parametric regression method, and therefore a separate investigation on performance of different regression approaches is required.

Remark 5.6.

Similar method can theoretically be applied for the SVV model with a rough fractional kernel. However, as noted in Example 5.2, one may need a very high dimensionality of the “input” variables vector (over 1000) which requires a dataset with possibly unrealistically huge number of observations.

References

- [1] Abi Jaber, E., and El Euch, O. Multifactor approximation of rough volatility models. SIAM journal on financial mathematics 10, 2 (2019), 309–349.

- [2] Abi Jaber, E., Miller, E., and Pham, H. Linear-quadratic control for a class of stochastic Volterra equations: Solvability and approximation. The annals of applied probability 31, 5 (2021).

- [3] Alòs, E., and Garcia Lorite, D. Malliavin calculus in finance: Theory and practice. CRC Press, London, England, 2021.

- [4] Alòs, E., León, J. A., and Vives, J. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Finance and stochastics 11, 4 (2007), 571–589.

- [5] Andersen, L. B. G., and Piterbarg, V. V. Moment explosions in stochastic volatility models. Finance Stoch. 11, 1 (2007), 29–50.

- [6] Avikainen, R. On irregular functionals of SDEs and the Euler scheme. Finance and stochastics 13, 3 (2009), 381–401.

- [7] Azmoodeh, E., Sottinen, T., Viitasaari, L., and Yazigi, A. Necessary and sufficient conditions for Hölder continuity of Gaussian processes. Statistics & Probability Letters 94 (2014), 230 – 235.

- [8] Bayer, C., Friz, P., and Gatheral, J. Pricing under rough volatility. Quantitative finance 16, 6 (2016), 887–904.

- [9] Bäuerle, N., and Desmettre, S. Portfolio optimization in fractional and rough Heston models. SIAM journal on financial mathematics 11, 1 (2020), 240–273.

- [10] Carmona, P., and Coutin, L. Fractional Brownian motion and the Markov property. Electronic communications in probability 3 (1998), 95–107.

- [11] Carriere, J. F. Valuation of the early-exercise price for options using simulations and nonparametric regression. Insurance, mathematics & economics 19, 1 (1996), 19–30.

- [12] Chronopoulou, A., and Viens, F. G. Estimation and pricing under long-memory stochastic volatility. Annals of finance 8, 2–3 (2012), 379–403.

- [13] Comte, F., Coutin, L., and Renault, E. Affine fractional stochastic volatility models. Annals of finance 8, 2–3 (2012), 337–378.

- [14] Comte, F., and Renault, E. Long memory in continuous-time stochastic volatility models. Mathematical Finance 8, 4 (1998), 291–323.

- [15] Cont, R. Long range dependence in financial markets. In Fractals in Engineering. Springer-Verlag, 2005, p. 159–179.

- [16] Cont, R. Volatility clustering in financial markets: Empirical facts and agent-based models. In Long Memory in Economics. Springer Berlin Heidelberg, 2006, p. 289–309.

- [17] Di Nunno, G. Stochastic integral representations, stochastic derivatives and minimal variance hedging. Stoch. Stoch. Rep. 73, 1-2 (2002), 181–198.

- [18] Di Nunno, G., Mishura, Y., and Yurchenko-Tytarenko, A. Drift-implicit Euler scheme for sandwiched processes driven by Hölder noises. To appear in Numerical Algorithms (2022).

- [19] Di Nunno, G., Mishura, Y., and Yurchenko-Tytarenko, A. Option pricing in Volterra Sandwiched Volatility model. arXiv:2209.10688 [q-fin.MF] (2022).

- [20] Di Nunno, G., Mishura, Y., and Yurchenko-Tytarenko, A. Sandwiched SDEs with unbounded drift driven by Hölder noises. To appear in Advances in Applied Probability 55 (2023).

- [21] Di Nunno, G., Øksendal, B., and Proske, F. Malliavin calculus for Lévy processes with applications to finance. Springer, Berlin, Heidelberg, 2009.

- [22] El Euch, O., and Rosenbaum, M. The characteristic function of rough Heston models. Mathematical Finance. An International Journal of Mathematics, Statistcs and Financial Economics 29, 1 (2019), 3–38.

- [23] Fukasawa, M. Asymptotic analysis for stochastic volatility: martingale expansion. Finance and stochastics 15, 4 (2011), 635–654.

- [24] Fukasawa, M. Volatility has to be rough. Quantitative finance 21, 1 (2021), 1–8.

- [25] Fukasawa, M., and Gatheral, J. A rough SABR formula. Frontiers of Mathematical Finance 1, 1 (2022), 81.

- [26] Funahashi, H., and Kijima, M. A solution to the time-scale fractional puzzle in the implied volatility. Fractal and fractional 1, 1 (2017), 14.

- [27] Garsia, A., Rodemich, E., and Rumsey, H. A real variable lemma and the continuity of paths of some Gaussian processes. Indiana Univ. Math. J. 20 (1970), 565–578.

- [28] Gatheral, J., Jaisson, T., and Rosenbaum, M. Volatility is rough. Quantitative finance 18, 6 (2018), 933–949.

- [29] Harms, P., and Stefanovits, D. Affine representations of fractional processes with applications in mathematical finance. Stochastic processes and their applications 129, 4 (2019), 1185–1228.

- [30] Krah, A.-S., Nikolić, Z., and Korn, R. A least-squares Monte Carlo framework in proxy modeling of life insurance companies. Risks 6, 2 (2018), 62.

- [31] Krah, A.-S., Nikolić, Z., and Korn, R. Least-squares Monte Carlo for proxy modeling in life insurance: Neural networks. Risks 8, 4 (2020), 116.

- [32] Krah, A.-S., Nikolić, Z., and Korn, R. Machine learning in least-squares Monte Carlo proxy modeling of life insurance companies. Risks 8, 1 (2020), 21.

- [33] Longstaff, F. A., and Schwartz, E. S. Valuing american options by simulation: A simple least-squares approach. The review of financial studies 14, 1 (2001), 113–147.

- [34] Mathé, P. Approximation of Hölder continuous functions by Bernstein polynomials. The American mathematical monthly: the official journal of the Mathematical Association of America 106, 6 (1999), 568–574.

- [35] Nualart, D. The Malliavin calculus and related topics, 2 ed. Springer, Berlin, Germany, 2006.

- [36] Pham, H. On quadratic hedging in continuous time. Mathematical methods of operations research 51, 2 (2000), 315–339.

- [37] Schweizer, M. A guided tour through quadratic hedging approaches. In Handbooks in Mathematical Finance: Option Pricing, Interest Rates and Risk Management, E. Jouini, J. Cvitanic, and Musiela, Eds. Cambridge University Press, 2001, p. 538–574.

- [38] Tsitsiklis, J. N., and Van Roy, B. Regression methods for pricing complex American-style options. IEEE transactions on neural networks 12, 4 (2001), 694–703.

- [39] Wang, R., and Xiao, Y. Exact uniform modulus of continuity and Chung’s LIL for the generalized fractional Brownian motion. Journal of theoretical probability (2022).

- [40] Zhu, Q., Loeper, G., Chen, W., and Langrené, N. Markovian approximation of the rough Bergomi model for Monte Carlo option pricing. Mathematics 9, 5 (2021), 528.