Inter-order relations between moments of a Student distribution, with an application to -quantiles

Abstract

This paper introduces inter-order formulas for partial and complete moments of a Student distribution with degrees of freedom. We show how the partial moment of order about any real value can be expressed in terms of the partial moment of order for in . Closed form expressions for the complete moments are also established. We then focus on -quantiles, which represent a class of generalized quantiles defined through an asymmetric -power loss function. Based on the results obtained, we also show that for a Student distribution the -quantile and the -quantile coincide at any confidence level in .

Keywords: expectiles, generalized quantiles, higher-order moments, partial moments, quantiles, risk measures.

1 Introduction

Partial moments play an important role in several areas of statistics and applied mathematics, including reliability modeling (Lata Gupta and

Gupta, 1983), insurance pricing (Denuit, 2002) and financial risk theory (Harlow and

Rao, 1989). Bawa (1975) was among the first ones to introduce partial moments in financial economics, Anthonisz (2012) and Yao

et al. (2021) subsequently investigated the use of (lower) partial moments in the context of asset pricing and portfolio optimization, respectively.

Unser (2000) examined investors’ risk perception in financial decision making using lower partial moments as a measure of perceived risk, while Antle (2010) considered partial moments as a flexible way to estimate the effects of biophysical and management processes on agricultural output distributions.

From a theoretical standpoint, their properties and recursive relationships have been investigated in, for instance, Winkler

et al. (1972), where several methods for determining partial moments are discussed or in Abraham

et al. (2007) who characterized different continuous distributions belonging to the exponential and Pearson families based on partial moments.

In this work, we are concerned with partial and complete moments of the Student distribution with arbitrary degrees of freedom . In both frequentist and Bayesian paradigms, the Student has thoroughly pervaded the statistical literature in those situations where heavy tails or outliers arise as a robust alternative to the normal distribution (Jonsson, 2011). These characteristics make it suitable for the analysis of data in the economic sciences and risk analysis; see, for instance, Lange

et al. (1989) and McNeil

et al. (2015). In particular,

results on the moments of a Student distribution with degrees of freedom have been obtained in Winkler

et al. (1972) where it was shown that the -th order partial moment about the origin can be expressed in terms of the -th order partial moment, provided that . More recently, Bernardi

et al. (2017) presented a recurrence formula by substituting repeatedly the partial moment of order in the characterization of the -th order partial moment illustrated in Gradshteyn and

Ryzhik (2007). In the literature, general expressions for central moments of skewed, truncated or folded Student distributions have also been derived by Nadarajah and

Ali (2004) and Kim (2008), for example. However, relationships for partial and complete higher-order moments about any arbitrary point of a Student distribution have not yet been determined.

This paper contributes to the existing literature in two ways. First, we show that for a Student distribution with degrees of freedom, the partial moment of order about any point can be expressed in terms of the partial moment of order times a multiplicative constant that depends on and . In addition, closed form expressions for the complete moments are also derived in terms of the Gamma and the hypergeometric functions. The proofs of these results involve concepts from combinatorial analysis as well as exploit fundamental properties of known special functions. To the best of our knowledge, this is the first time that inter-order relationships for partial and complete moments of the Student distribution are investigated, giving a simple way for calculating higher order moments from those of lower order.

The second contribution of the paper establishes inter-order relations of equality between -quantiles of the Student distribution. In the literature, -quantiles, introduced by Chen (1996) as a natural extension of quantiles, are an important class of statistical functionals defined as the minimizers of an expected asymmetric -power loss function. Indeed, for and for , they correspond respectively to quantiles and expectiles, which have been proposed by Newey and Powell (1987), based on asymmetric least-squares estimation as a “quantile-like” generalization of the mean. Basic properties of the -quantiles have been given by Chen (1996) and, in the context of generalized quantiles, Abdous and Rémillard (1995) provided sufficient conditions under which -quantiles (quantiles) and -quantiles (expectiles) coincide. More generally, both quantiles and expectiles, and in turn -quantiles, can be embedded in the wider class of M-quantiles of Breckling and Chambers (1988) which extend the ideas of M-estimation of Huber (1964) by introducing asymmetric influence functions to model the entire distribution of a random variable. Generalized quantile models have been implemented in a broad range of applications, such as multilevel modeling (Alfò et al. 2021 and Merlo et al. 2022), nonparametric regression (Pratesi et al. 2009), multivariate analysis (Merlo et al. 2022), economics and finance (Gneiting 2011, Bellini et al. 2014 and Daouia et al. 2019). In the latter context, -quantiles have received particular consideration as potential competitors to the most used risk measures in banking and insurance, namely Value at Risk and Expected Shortfall. Indeed, besides being elicitable (Lambert et al. 2008), they possess several interesting properties in terms of risk measures (see for instance Bellini 2012 and Bellini et al. 2014). Moreover, when , -quantiles are the only risk measure that is both coherent (Artzner et al. 1999) and elicitable (please see also Bellini et al. (2014) and Ziegel (2016) for a detailed analysis of expectiles as a risk measure).

In this paper, by exploiting the results derived on partial moments we show that for a Student distribution with degrees of freedom, the -quantile and the -quantile coincide for any (and the same holds for any affine transformation). This result generalizes the one in Koenker (1993) who showed that the Student distribution with 2 degrees of freedom, or any affine transformation thereof, is the unique distribution where -quantiles and -quantiles match each other, and in Bernardi et al. (2017) who proved that the -quantiles and -quantiles coincide for any .

With this paper, we give new insights on the properties of the Student distribution and, at the same time, we contribute in the context of risk management to the framework of Bellini and

Di Bernardino (2017), Li and Wang (2022) and Fiori and

Rosazza Gianin (2022) for comparing general pairs of risk measures and determining when these coincide.

The rest of the paper is organized as follows. Section 2 introduces the notation and the mathematical background that will be used in our analysis. In Section 3 we present the first important result of the paper deriving inter-order formulas for partial and complete moments of arbitrary order for a Student distribution. Finally, in Section 4 we introduce the -quantiles and provide a symmetry characterization of -quantiles of the Student distribution. The proofs of the main results are collected in the Appendix.

2 Mathematical background

We start by introducing some basic mathematical notation. Let denote the set of positive integers, and the positive real line; will always be an element of . The binomial coefficient if defined by for , where is the factorial with the convention . We denote and the positive and negative part of , respectively. Given an atomless probability space , represents the space of random variables with finite -moment, . and denote, respectively, the space of measurable and bounded random variables. Given a continuous real-valued random variable , we denote and its density and distribution functions. To improve readability the subscript may be omitted when no confusion is likely to arise. For , the upper and lower partial moments of order about any point are denoted as follows

| (1) |

and

| (2) |

In this paper we make extensive use of some special functions: the Gamma, the Beta and the hypergeometric functions. These functions are widely discussed in every book on special functions. Among many others we cite Abramowitz and Stegun (1972), Askey (1975), Temme (1996) and Mathai and Haubold (2008). Here, we briefly introduce the hypergeometric function with its most relevant properties.

To this end, we first recall the notion of Pochhammer’s symbol:

with the convention . Note that for , one has , where denotes the Gamma function of the positive real number . For , it is immediate to verify

Then, the hypergeometric function is defined by the series

| (3) |

with . The radius of convergence of the series is the unity, but it may be extended under weak conditions. For instance, when the analytic continuation of the hypergeometric function can be obtained when (or ) and , see Temme (1996). The series terminates if either or is a nonpositive integer, in which case the function reduces to a polynomial and the convergence is guaranteed for any . Indeed, when or is equal to , with , the function is a polynomial of degree in , that is:

The hypergeometric function satisfies a great variety of relations. First we observe that it is symmetric in and , giving . Another useful property which will be often used throughout the paper is the following Euler’s transformation (Temme 1996, p. 110). For (or equivalently from the symmetry in with respect to and ) and :

| (4) |

where denotes the argument of the real number .

The last property of the hypergeometric function that we need is:

| (5) | |||

for , and the Gamma functions well defined (Temme 1996, p. 120). In this contribution we will briefly encounter the generalized hypergeometric function defined as

The radius of convergence of this series is unity for , while it is for . The parameters can be commuted as well as the parameters . Furthermore if for some and , then

3 Relations between moments of the Student distribution

In this section we present innovative results for the partial and complete moments of the Student distribution. Let be a random variable with Student distribution with degrees of freedom, i.e., , with density function given by

In order to introduce our results, we recall the expressions for the moments of centered around zero. Specifically, the raw moments are well defined for any order and can be calculated as

| (6) |

The raw moments of odd order are null because the density function is an even function.

In the following, a closed form expression for the complete moments of order centered in is derived. This result can be found in the working paper by Kirkby et al. (2019) based on the unpublished note by Winkelbauer (2012). Here, we derive the same formulas with a different proof.

Proposition 3.1.

Let be a random variable with Student distribution with degrees of freedom. For and :

| (7) |

where is the hypergeometric function defined in (3).

Proof.

See the Appendix A.1. ∎

Remark 3.2.

Note that , therefore Proposition 3.1 for returns the expression for the raw moments of order provided in (6). Moreover, for both odd and even the first term of the hypergeometric function is a nonpositive integer, implying that the function is a polynomial and the convergence is guaranteed for any and .

A useful property of upper and lower partial moments of the Student distribution that will be needed for the main theorems can be proved by the following lemma.

Lemma 3.3.

Let be a random variable with Student distribution with degrees of freedom and let :

-

(1)

For the following equation holds:

(8) -

(2)

For

(9)

Proof.

For the proof see Appendix A.2. ∎

Thanks to Lemma 3.3, in the following theorem we derive an interesting link between the central moments of order with that of order for any .

Theorem 3.4.

Let be a random variable with Student distribution with degrees of freedom. For and , the following equation for the central moments about the point holds:

-

1.

For odd:

(10) -

2.

For even:

(11)

Proof.

For the proof see Appendix A.3. ∎

Theorem 3.4 provides an original inter-order relation between moments of the Student distribution.

Remark 3.5.

It is worth noting that Theorem 3.4 also establishes an expression for the raw moments of . Indeed, for , we have that

| (12) |

In the next results, we show that a similar relation holds also for the upper and lower partial moments.

Theorem 3.6.

Let be a random variable with Student distribution with degrees of freedom. For and , the following equation for the upper partial moments holds:

| (13) |

Proof.

Corollary 3.7.

Let be a random variable with Student distribution with degrees of freedom. For and , the following equation for the lower partial moments holds:

| (14) |

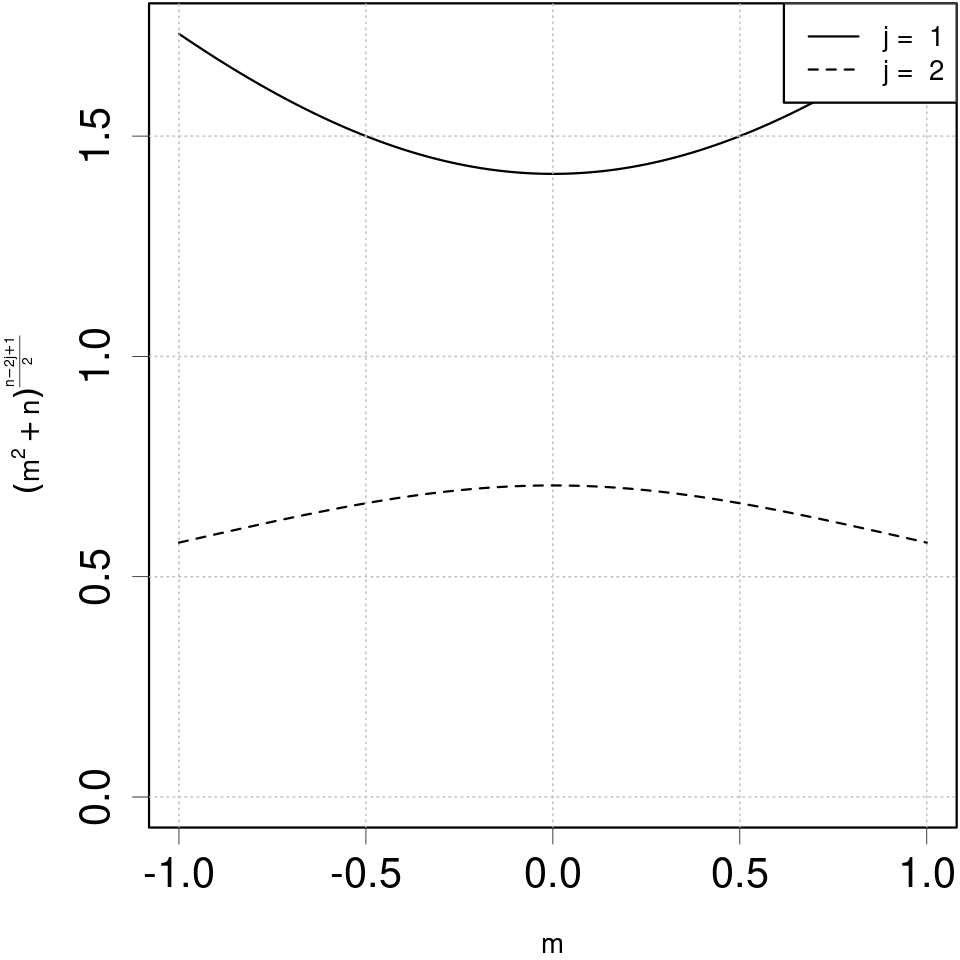

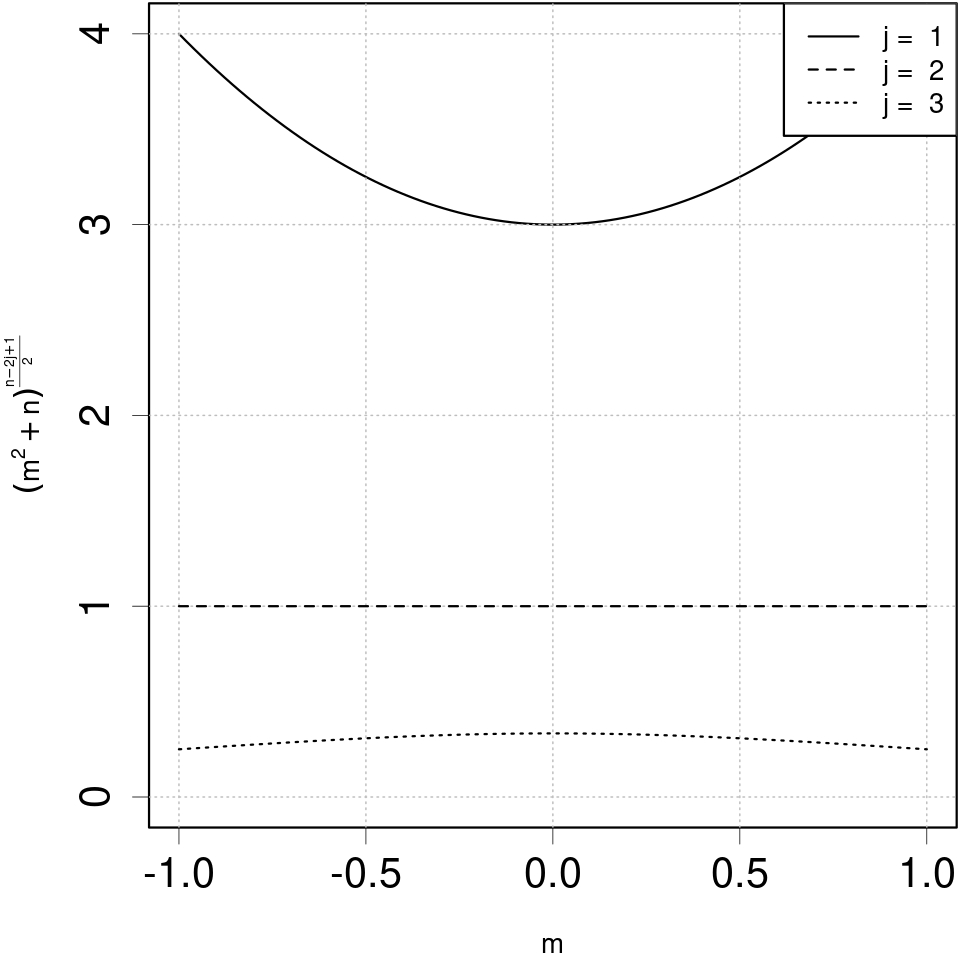

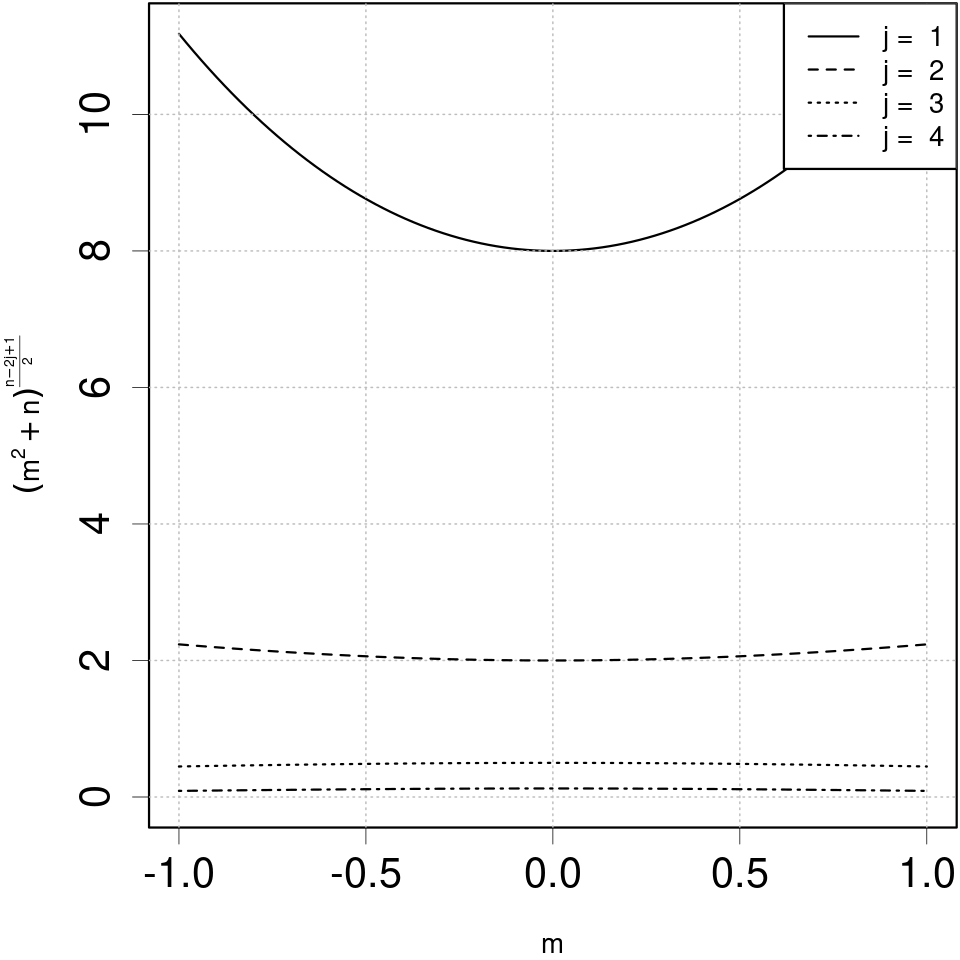

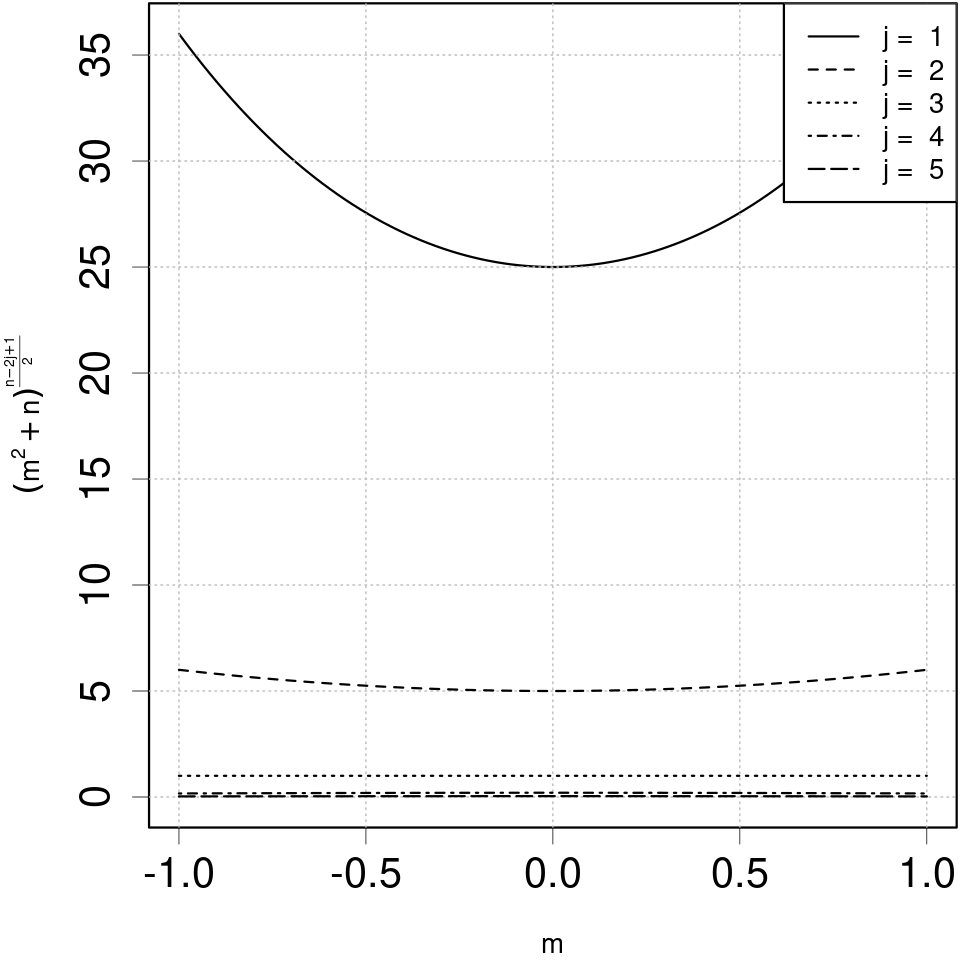

From another perspective, Theorem 3.6 and Corollary 3.7 assert that for a Student distribution with degrees of freedom the ratio between the upper (lower) partial moment of order and that of order is a deterministic function of . Figure 1 depicts the function for various values of and . As it can be observed, this is an even convex function of when the exponent is positive and concave otherwise. We can also see that in both cases the global minimum (maximum) is at . Evidently, if and is odd, this is a constant function equal to 1.

4 On the -quantiles for the Student distribution

In this section we formally introduce the -quantiles and present our second major contribution on identity relations between the -quantiles of a Student distribution. Specifically, consider the asymmetric power loss function , , where . For , the -quantile of a random variable at level , denoted by , is defined as:

| (15) |

provided the expectation exists. For , corresponds to the quantile at level of and (15) has a unique solution only if the distribution of is strictly increasing in a neighborhood of . When , corresponds to the level expectile introduced by Newey and Powell (1987). Expectiles have gained major attention in quantitative risk management as an important alternative to the well known VaR and ES risk measures. See for instance Emmer et al. (2015) for a comparison of these three risk measures, Delbaen et al. (2016) and the reference therein for a characterization of expectiles as the unique example of a coherent elicitable risk measure and Bellini and Di Bernardino (2017) for an empirical analysis of expectiles. Quantiles and expectiles with correspond respectively to the median and the mean of . For , -quantiles can be defined as the unique solution of the following first order condition:

| (16) |

The main advantage of using (16) is that it is well defined for random variables with -th finite moments, while (15) requires also the -th moment to be finite.

In what follows, we show that for a random variable having a Student distribution with degrees of freedom the -quantile and the -quantile coincide for any level .

Theorem 4.1.

Let be a Student random variable with degrees of freedom. For the following equation holds:

| (17) |

Proof.

From Theorem 4.1 follows an important property of the -quantiles of a Student distribution. Specifically, the -quantile not only minimizes the asymmetric power loss function of order but it also minimizes the one of order for and for any . Their symmetry characterization is reflected by the fact that, for a given number of degrees of freedom , the -quantile (quantile) and -quantile coincide, the -quantile (expectile) tallies with the -quantile, and so forth for every pair of - and -quantiles.

In the next corollary we extend this result to any affine transformation of the Student distribution.

Corollary 4.2.

Let be any affine transformation of a random variable with Student distribution with degrees of freedom, that is . For any ,

Proof.

The proof follows immediately by noting that for any and . ∎

Theorem 4.1 and Corollary 4.2 extend the work of Koenker (1992) who originally showed that the class of distributions for which the -quantiles and -quantiles coincide, corresponds to a rescaled Student distribution with 2 degrees of freedom. Moreover, in the special case , the equality in Theorem 4.1 reduces to the expression derived in Bernardi

et al. (2017), which shows that the -quantile and the quantile coincide for any level . With our results we further generalize these works by providing a characterization of the symmetry of the -quantiles for the Student distribution with degrees of freedom for any .

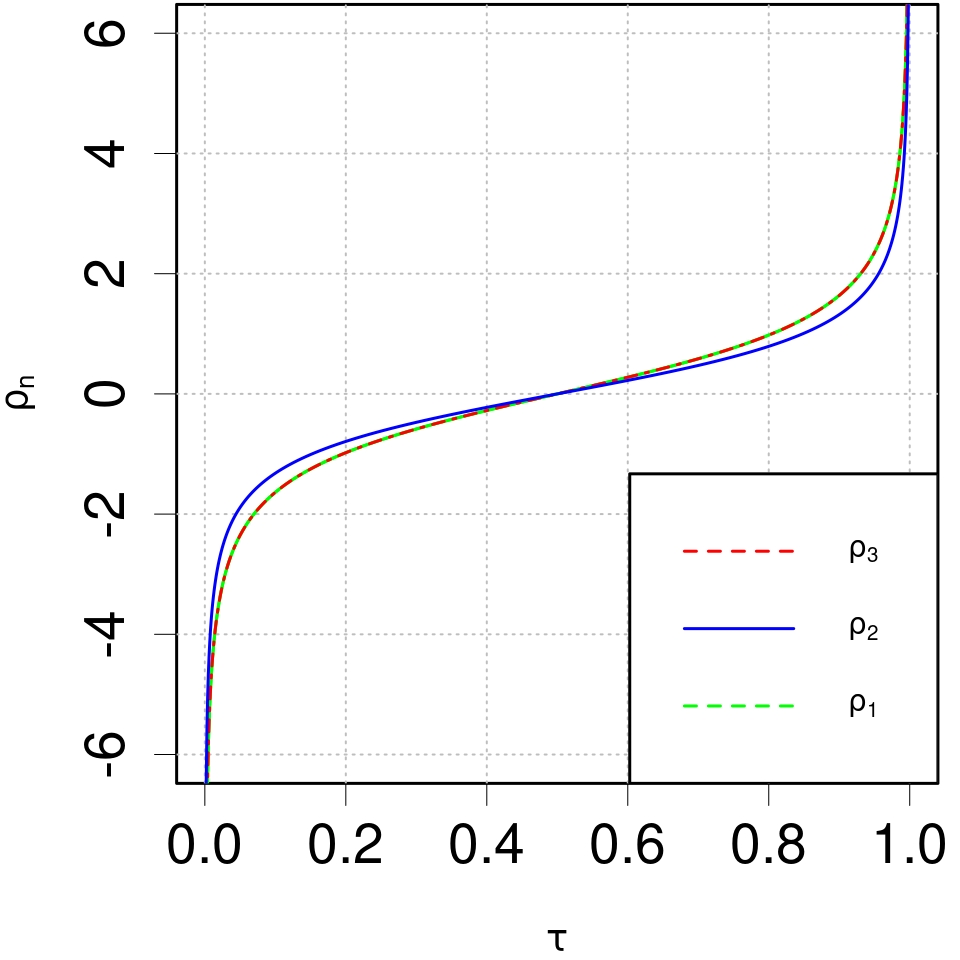

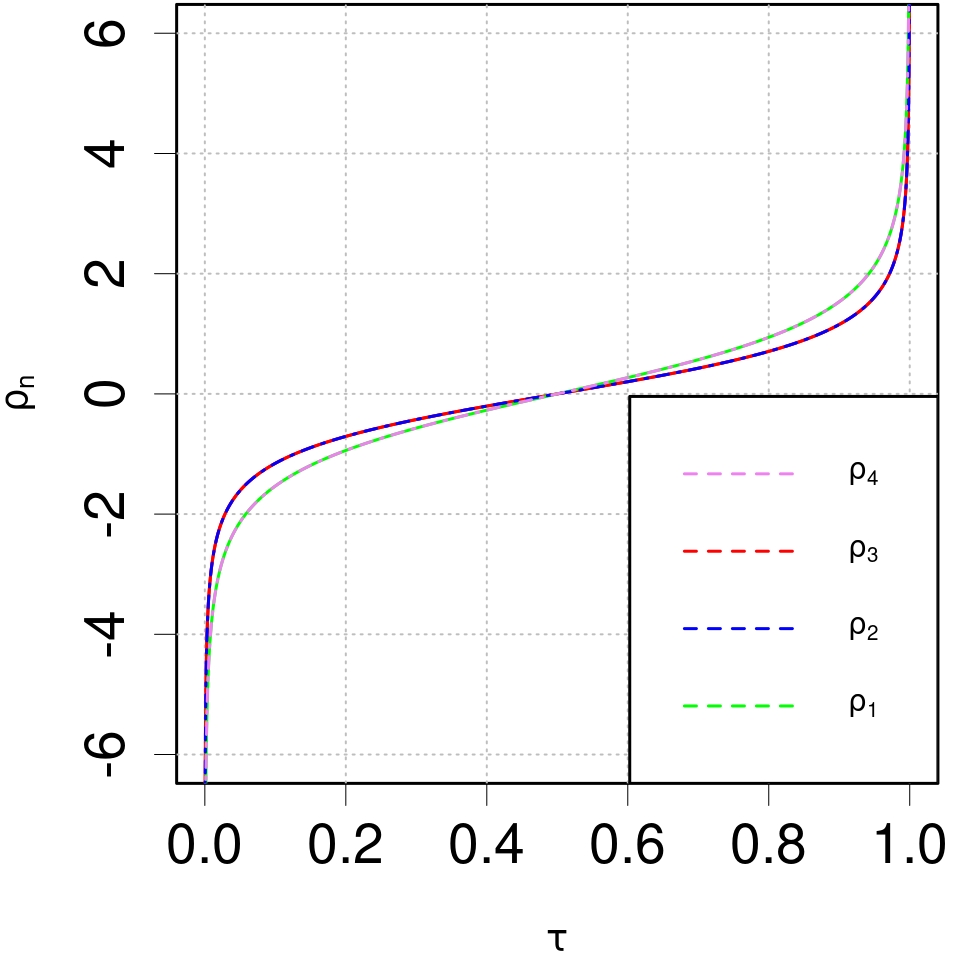

Figure 2 illustrates the behavior of the -quantile for of a Student distribution with (left) and (right) degrees of freedom with respect to . It is worth noticing that the -quantiles are monotonically increasing, with a symmetry point for due to the symmetry of the Student centered around zero. Moreover, by looking at the plot on the left, it is possible to see that (green) coincides with (red) for all . Similarly, in the right-hand picture we have that (green) is equal to (pink) and (blue) coincides with (red) for all .

Appendix A Appendix

A.1 Proof Proposition 3.1

Proposition 3.1 Let be a random variable with Student distribution with degrees of freedom. For and :

| (19) |

where is the hypergeometric function defined in (3).

Proof.

By using the binomial expansion and the linearity of the expectation we can decompose the term , as:

Note that for and all the moments are finite. We first assume that is even. The term is not zero only for even, therefore the index is changed to obtain:

One can now substitute the values of from (6) and express the binomial coefficient in terms of the Gamma function to get:

| (20) |

where in the last equation we multiplied and divided by . One can now apply the Legendre duplication formula for the Gamma function, , to the following terms:

By substituting the above formulas in (20), recalling the definition of the Pochhammer symbol and that , one gets

Since the first term of the hypergeometric function is a nonpositive integer, the convergence of the function is guaranteed for any value of and .

Consider now the case odd.

The term is not zero only for odd, therefore the index is changed to obtain:

One can now substitute the values of from (6) and express the binomial coefficient in terms of the Gamma function to get:

| (21) |

where in the last equation we multiplied and divided by . Again, we apply the Legendre duplication formula for the Gamma function to the following terms:

By substituting the above formulas in (21), one gets

where in the last step we multiplied and divided by . Recalling that , we find:

as desired. Since the first term of the hypergeometric function is a nonpositive integer, the convergence of the function is guaranteed for any value of and . ∎

A.2 Proof of Lemma 3.3

Lemma 3.3 Let be a random variable with Student distribution with degrees of freedom and let :

-

(1)

For the following equation holds:

(22) -

(2)

For

(23)

Proof.

- (1)

-

(2)

Consider the case . For we apply a change of variable: and use again formula 3.254(2) in Zwillinger and Jeffrey (2015), to get

It follows that for

and

where in the third equality we applied again the Euler’s transformation and the symmetry of the hypergeometric function.

∎

A.3 Proof Theorem 3.4

Theorem 3.4 Let be a random variable with Student distribution with degrees of freedom. For and , the following equation for the central moments about the point holds:

-

1.

For odd:

(26) -

2.

For even:

(27)

Proof.

-

1.

We know that is odd and first consider the case odd, from which it follows that and are even. From the expression (7) for an even power, we get:

and

Using the symmetry of the hypergeometric function and applying the Euler’s transformation to concludes the proof.

For even, and are odd. Using again the expression (7) for an odd power, one gets

and

Using again the symmetry of the hypergeometric function and applying the Euler’s transformation to concludes the proof.

-

2.

For even, we first consider even. Since is even and is odd, using (7) we find

(28) and

(29) where in the last equality we used the Euler’s transformation for the hypergeometric function. Furthermore, for Lemma 3.3 and formula 3.254(2) in Zwillinger and Jeffrey (2015) provide

(30) Our goal is then to show that

(31) using the property in (5) of the hypergeometric functions. From (28), (29) and (30), (31) becomes

We first note that for and the hypergeometric functions above have the correct terms as the ones required by the property in (5). Therefore, we are left to show that the multiplicative coefficients associated to the two hypergeometric functions on the right-hand side correspond. For the first multiplicative term, the desired result follows from

where in the last step we used the Legendre duplication formula for the Gamma function. Moving on to the second multiplicative coefficient we have:

where in the last equality we used that .

∎

References

- Abdous and Rémillard (1995) Abdous, B. and B. Rémillard (1995). Relating quantiles and expectiles under weighted-symmetry. Ann. Inst. Statist. Math. 47(2), 371–384.

- Abraham et al. (2007) Abraham, B., N. U. Nair, and P. Sankaran (2007). Characterization of some continuous distributions by properties of partial moments. J. Korean Statist. Soc. 36(3), 357–365.

- Abramowitz and Stegun (1972) Abramowitz, M. and I. A. Stegun (1972). Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables. Tenth Printing., Volume 55. US Government printing office.

- Alfò et al. (2021) Alfò, M., M. F. Marino, M. G. Ranalli, N. Salvati, N. Tzavidis, et al. (2021). M-quantile regression for multivariate longitudinal data with an application to the Millennium Cohort Study. J. R. Stat. Soc. Ser. C. Appl. Stat. 70(1), 122–146.

- Anthonisz (2012) Anthonisz, S. A. (2012). Asset pricing with partial-moments. J. Bank. Financ. 36(7), 2122–2135.

- Antle (2010) Antle, J. M. (2010). Asymmetry, partial moments, and production risk. Am. J. Agric. Econ. 92(5), 1294–1309.

- Artzner et al. (1999) Artzner, P., F. Delbaen, J.-M. Eber, and D. Heath (1999). Coherent measures of risk. Math. Finance 9(3), 203–228.

- Askey (1975) Askey, R. (1975). Orthogonal polynomials and special functions. Society for Industrial and Applied Mathematics, Philadelphia, Pa.

- Bawa (1975) Bawa, V. S. (1975). Optimal rules for ordering uncertain prospects. J. Financ. Econ. 2(1), 95–121.

- Bellini (2012) Bellini, F. (2012). Isotonicity properties of generalized quantiles. Stat. Probab. Lett. 82(11), 2017–2024.

- Bellini and Di Bernardino (2017) Bellini, F. and E. Di Bernardino (2017). Risk management with expectiles. Eur. J. Finance 23(6), 487–506.

- Bellini et al. (2014) Bellini, F., B. Klar, A. Müller, and E. Rosazza Gianin (2014). Generalized quantiles as risk measures. Insurance Math. Econom. 54, 41–48.

- Bernardi et al. (2017) Bernardi, M., V. Bignozzi, and L. Petrella (2017). On the -quantiles for the Student distribution. Stat. Probab. Lett. 128, 77–83.

- Breckling and Chambers (1988) Breckling, J. and R. Chambers (1988). -quantiles. Biometrika 75(4), 761–771.

- Chen (1996) Chen, Z. (1996). Conditional -quantiles and their application to the testing of symmetry in non-parametric regression. Stat. Probab. Lett. 29(2), 107–115.

- Daouia et al. (2019) Daouia, A., S. Girard, and G. Stupfler (2019). Extreme M-quantiles as risk measures: From to optimization. Bernoulli 25(1), 264–309.

- Delbaen et al. (2016) Delbaen, F., F. Bellini, V. Bignozzi, and J. F. Ziegel (2016). Risk measures with the CxLS property. Finance Stoch. 20(2), 433–453.

- Denuit (2002) Denuit, M. (2002). S-convex extrema, Taylor-type expansions and stochastic approximations. Scand. Actuar. J. 2002(1), 45–67.

- Emmer et al. (2015) Emmer, S., M. Kratz, and D. Tasche (2015). What is the best risk measure in practice? A comparison of standard measures. J. Risk 18(2), 31–60.

- Fiori and Rosazza Gianin (2022) Fiori, A. M. and E. Rosazza Gianin (2022). Generalized PELVE and applications to risk measures. Eur. Actuar. J., 1–33.

- Gneiting (2011) Gneiting, T. (2011). Making and evaluating point forecast. J. Amer. Statis. Assoc. 106(494), 746–762.

- Gradshteyn and Ryzhik (2007) Gradshteyn, I. S. and I. M. Ryzhik (2007). Table of integrals, series, and products (Seventh ed.). Elsevier/Academic Press, Amsterdam. Translated from the Russian, Translation edited and with a preface by Alan Jeffrey and Daniel Zwillinger.

- Harlow and Rao (1989) Harlow, W. V. and R. K. Rao (1989). Asset pricing in a generalized mean-lower partial moment framework: Theory and evidence. J. Financial Quant. Anal. 24(3), 285–311.

- Huber (1964) Huber, P. J. (1964). Robust estimation of a location parameter. Ann. Math. Stat., 73–101.

- Jonsson (2011) Jonsson, F. (2011). On the heavy-tailedness of Student’s -statistic. Bernoulli 17(1), 276–289.

- Kim (2008) Kim, H.-J. (2008). Moments of truncated Student- distribution. J. Korean Statist. Soc. 37(1), 81–87.

- Kirkby et al. (2019) Kirkby, J. L., D. Nguyen, and D. Nguyen (2019). Moments of Student’s -distribution: A unified approach. arXiv preprint arXiv:1912.01607.

- Koenker (1992) Koenker, R. (1992). When are expectiles percentiles? Econometric Theory 8, 423–424.

- Koenker (1993) Koenker, R. (1993). When are expectiles percentiles? Econometric Theory 9(3), 526–527.

- Lambert et al. (2008) Lambert, N. S., D. M. Pennock, and Y. Shoham (2008). Eliciting properties of probability distributions. In Proceedings of the 9th ACM Conference on Electronic Commerce, pp. 129–138. ACM.

- Lange et al. (1989) Lange, K. L., R. J. Little, and J. M. Taylor (1989). Robust statistical modeling using the distribution. J. Amer. Statist. Assoc. 84(408), 881–896.

- Lata Gupta and Gupta (1983) Lata Gupta, P. and R. C. Gupta (1983). On the moments of residual life in reliability and some characterization results. Comm. Statist. Theory Methods 12(4), 449–461.

- Li and Wang (2022) Li, H. and R. Wang (2022). PELVE: Probability equivalent level of VaR and ES. J. Econom..

- Mathai and Haubold (2008) Mathai, A. M. and H. J. Haubold (2008). Special Functions for Applied Scientists, Volume 4. Springer.

- McNeil et al. (2015) McNeil, A. J., R. Frey, and P. Embrechts (2015). Quantitative risk management: concepts, techniques and tools - Revised edition. Princeton University Press.

- Merlo et al. (2022) Merlo, L., L. Petrella, N. Salvati, and N. Tzavidis (2022). Marginal M-quantile regression for multivariate dependent data. Comput. Stat. Data. Anal., 107500.

- Merlo et al. (2022) Merlo, L., L. Petrella, and N. Tzavidis (2022). Quantile mixed hidden Markov models for multivariate longitudinal data: An application to children’s Strengths and Difficulties Questionnaire scores. J. R. Stat. Soc. Ser. C. Appl. Stat. 71(2), 417–448.

- Nadarajah and Ali (2004) Nadarajah, S. and M. M. Ali (2004). A skewed truncated distribution. Math. Comput. Model. Dyn. Syst. 40(9-10), 935–939.

- Newey and Powell (1987) Newey, W. K. and J. L. Powell (1987). Asymmetric least squares estimation and testing. Econometrica 55(4), 819–847.

- Pratesi et al. (2009) Pratesi, M., M. G. Ranalli, and N. Salvati (2009). Nonparametric M-quantile regression using penalised splines. J. Nonparametr. Stat. 21(3), 287–304.

- Temme (1996) Temme, N. M. (1996). Special Functions: An introduction to the classical functions of mathematical physics. John Wiley & Sons.

- Unser (2000) Unser, M. (2000). Lower partial moments as measures of perceived risk: An experimental study. J. Econ. Psychol. 21(3), 253–280.

- Winkelbauer (2012) Winkelbauer, A. (2012). Moments and absolute moments of the normal distribution. arXiv preprint arXiv:1209.4340.

- Winkler et al. (1972) Winkler, R. L., G. M. Roodman, and R. R. Britney (1972). The determination of partial moments. Manag. Sci. 19(3), 290–296.

- Yao et al. (2021) Yao, H., J. Huang, Y. Li, and J. E. Humphrey (2021). A general approach to smooth and convex portfolio optimization using lower partial moments. J. Bank. Financ. 129, 106167.

- Ziegel (2016) Ziegel, J. F. (2016). Coherence and elicitability. Math. Finance 26(4), 901–918.

- Zwillinger and Jeffrey (2015) Zwillinger, D. and A. Jeffrey (2015). Table of integrals, series, and products. Elsevier.