Asymmetric Laplace scale mixtures for the distribution of cryptocurrency returns

Abstract

Recent studies about cryptocurrency returns show that its distribution can be highly-peaked, skewed, and heavy-tailed, with a large excess kurtosis. To accommodate all these peculiarities, we propose the asymmetric Laplace scale mixture (ALSM) family of distributions. Each member of the family is obtained by dividing the scale parameter of the conditional asymmetric Laplace (AL) distribution by a convenient mixing random variable taking values on all or part of the positive real line and whose distribution depends on a parameter vector providing greater flexibility to the resulting ALSM. Advantageously with respect to the AL distribution, the members of our family allow for a wider range of values for skewness and kurtosis. For illustrative purposes, we consider different mixing distributions; they give rise to ALSMs having a closed-form probability density function where the AL distribution is obtained as a special case under a convenient choice of . We examine some properties of our ALSMs such as hierarchical and stochastic representations and moments of practical interest. We describe an EM algorithm to obtain maximum likelihood estimates of the parameters for all the considered ALSMs. We fit these models to the returns of two cryptocurrencies, considering several classical distributions for comparison. The analysis shows how our models represent a valid alternative to the considered competitors in terms of AIC, BIC, and likelihood-ratio tests.

keywords:

Cryptocurrencies, Econophysics, Asymmetric Laplace distribution, Scale mixture, Heavy-tailed distributions.1 Introduction

In the recent years, cryptocurrencies have grown to be alternative investments for investors looking to hedge against stock market crashes and optimize their earnings. As a matter of fact, many established cryptocurrencies are currently in the market, and over the years many of these assets have appreciated radically. This justifies the growing number of studies about the distributional peculiarities of cryptocurrency returns. However, from this literature, it is not yet possible to infer formal and rigorous “stylized facts” for the distribution of these returns. Nevertheless, some common findings are already known. Without going into details about the cryptocurrencies considered in each work we will cite, these findings show that cryptocurrency returns – as usual for financial returns in general – are clearly non-normally distributed (Bariviera et al., 2017, Zhang et al., 2018, and Takaishi, 2018); instead, their distribution can be highly peaked, skewed, and leptokurtic (Chu et al., 2015, Osterrieder, 2017, Zhang et al., 2018, and Szczygielski et al., 2020), with high levels of excess kurtosis (always greater than 3 in the analyses by Chan et al., 2017, Zhang et al., 2018, Bariviera et al., 2017, Phillip et al., 2018, Szczygielski et al., 2020, and Punzo & Bagnato, 2021a).

The asymmetric Laplace (AL) distribution could be a good candidate to accommodate all these findings; unfortunately, its skewness and kurtosis can only assume values in the intervals and , respectively (refer to Section 2.1), and this limits its performance when fitted to the empirical distribution of cryptocurrency returns. To overcome these issues, we introduce the family of asymmetric Laplace scale mixtures (refer to Section 2). The underlying idea consists in dividing the scale parameter, of the conditional AL distribution, by a convenient mixing random variable, whose distribution takes values on all or part of the positive real line and depends on a parameter vector further governing the shape of the unconditional mixture. This confers more flexibility to the conditional AL distribution, allowing for a larger range of values for skewness excess kurtosis, without modifying its peculiar peaked shape. As an alternative, our proposal can be seen as a generalization of the (symmetric) Laplace scale mixture proposed in Punzo & Bagnato (2021a) to allow for skewness.

For illustrative purposes, in Section 3 we consider seven members of our family obtained by choosing convenient mixing distributions. The mixing distributions we choose have the advantage to produce a compound model having a closed-form probability density function (pdf); this advantage should not to be undervalued since, as emphasized by Shevchenko (2010), simple closed form expressions for the pdf of compound models are often not available.

As usual in the literature, we consider the maximum likelihood (ML) approach to estimate the parameters of our models. To obtain these estimates, in Section 4 we describe an expectation-maximization (EM) algorithm which is general enough to be easily extended to mixing distributions beyond those considered in this paper. From the updates of the parameters of the nested AL distribution, obtained in the M-step of the algorithm, we also show how the influence of observations associated to large absolute distances is automatically reduced (downweighted) in the estimation phase.

In Section 5, we summarize the results of an analysis where our models are fitted to the returns of two cryptocurrencies (Bitcoin EUR and TRON EUR). We consider several classical symmetric distributions as competitors. The analysis shows how the proposed models provide a significant improvement with respect to the considered competitors in terms of AIC, BIC and likelihood-ratio tests.

We conclude the paper, in Section 6, with further insights and possible future works related to the proposed models.

2 Asymmetric Laplace scale mixture

2.1 Preliminaries: the asymmetric Laplace distribution

As well-documented in Kotz et al. (2012), various skewed versions of the Laplace distribution have appeared in the literature. Among them, the asymmetric Laplace (AL) distribution by Kozubowski & Podgorski (2000) is the reference one; for details about its properties and advantages, see Kotz et al. (2012, pages 134–136). The classical and simplest parameterization of the pdf of the AL distribution – given in Equation (3.0.8) of Kotz et al. (2012) – is

| (1) |

where , and are location, scale, and asymmetry parameters, respectively; if has the pdf in (1), then we compactly write . The parameter is scale invariant while coincides with the mode of the distribution. Furthermore, if , then we obtain the classical (symmetric) Laplace distribution; in this case we write .

The moments of greatest practical interest of , namely the mean, variance, skewness, and kurtosis, are respectively given by

| (2) | ||||

| (3) | ||||

| (4) | ||||

| (5) |

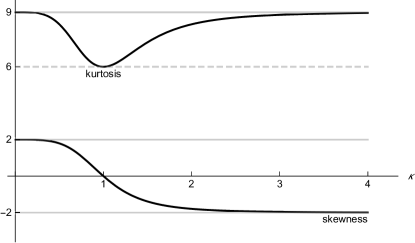

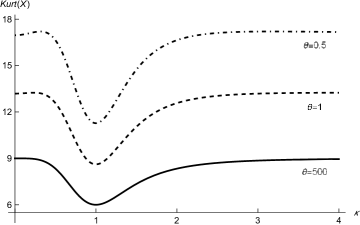

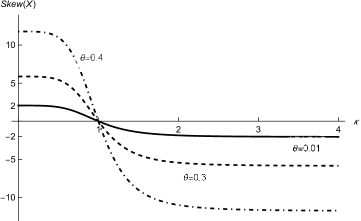

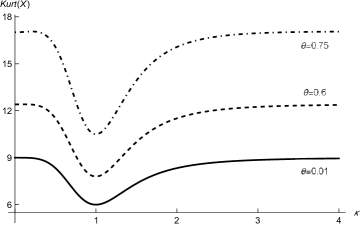

Among them, the mean in (2) is the only one depending on all the parameters of the AL distribution. The mean is given by the mode plus a term whose sign depends on the asymmetry parameter ; this term can be negative (for ), null (for ), or positive (for ). The variance does not depend on the mode and it is given by – which is half of the variance of – multiplied by a positive factor only depending on . Instead, skewness and kurtosis only depend on , and their behavior as a function of is displayed in Figure 1.

The skewness lies in the interval ; as increases, the corresponding value of decreases monotonically. As for the kurtosis, the AL distribution is leptokurtic and varies from 6 – the value we have for the symmetric Laplace distribution () – to 9 (the greatest value attained when either or ). For further details about moments and related quantities of , see Kotz et al. (2012, Section 3.1.5).

2.2 Probability density function

In Definition 1 we introduce the asymmetric Laplace scale mixture in terms of its pdf.

Definition 1 (Probability density function).

A random variable is said to have the asymmetric Laplace scale mixture (ALSM) distribution with location , scale , asymmetry parameter and tailedness , in symbols , if its pdf is given by

| (6) |

where is the mixing probability density (or mass) function of , with support , depending on the vector of parameters ; in symbols, .

According to (6), the distribution of can be thought of as a composite distribution constructed by taking a finite/infinite set of AL component distributions with the same location and asymmetry parameter , but with a different scale . The component AL distributions are not taken uniformly from the set, but according to a set of “weights” determined by the distribution of (random counterpart of ). In the context of modelling currency returns, the mixing variable could be interpreted as a shock that arises from new information and impacts the volatility of the market. The resulting mixture is not itself an AL distribution due to a more flexible tail behavior governed by the tailedness parameter . However, the distribution preserves the characteristic towering peak of the AL distribution. Note that, if is degenerate in 1 (), then reduces to . While, if , then reduces to the Laplace scale mixture distribution proposed by Punzo & Bagnato (2021a).

If we want model (6) to embed as a special or limiting case, we need to consider a mixing random variable degenerating in 1 under a convenient choice of . This is commonly required to models that aim to make more flexible the behavior of the tails of a conditional distribution (as, e.g., the well-known normal scale mixture model). This allows to use inferential procedures such as the likelihood-ratio test to compare the ALSM with the nested AL distribution (cf. Section 5).

2.3 Representations

The ALSM admits the following useful representations as mixture of normal distributions (Proposition 1) and as mixture of AL distributions (Proposition 2).

Proposition 1 (Mixture of normal distributions).

admits the representation

| (7) |

where is standard normal () and is standard exponential (). Note that , , and are independent.

Proposition 2 (Mixture of AL distributions).

admits the representation

| (8) |

where is independent of .

2.4 Moments

2.5 Absolute moments

2.6 Mean, variance, skewness, and kurtosis

Mean, variance, skewness, and kurtosis of can be obtained from (8) and from the corresponding moments of . These moments can be expressed as a function of convenient moments of , which depend on , in the following way:

| (12) |

| (13) |

| (14) |

| (15) |

As we can note, the mean depends on all the parameters of the ALSM distribution, the variance does not depend on , while skewness and kurtosis only depend on and .

2.7 Mode

In Theorem 1 we show that the ALSM distribution is unimodal hump-shaped, with mode in ; the result is a slight modification of Theorem 1 in Punzo et al. (2018) and Punzo & Bagnato (2021a).

Theorem 1.

The pdf of is unimodal hump-shaped in .

Proof. The first derivative, with respect to , of is

where

Hence, for , for , and for . Using these results and recalling that for , the theorem is straightforwardly proven. ∎

3 Examples of asymmetric Laplace scale mixtures

The ALSM family of distributions is extremely flexible. In this section we introduce some members of the family obtained under a convenient choice of the mixing probability density (or mass) function . These members satisfy two requirements: 1) the existence of a closed-form pdf for the ALSM and 2) the peculiarity to nest under a suitable choice of .

3.1 Two-point asymmetric Laplace distribution

A simple but effective special case of model (6) is obtained if we consider the following mixing two-point (TP) distribution

| (16) |

where and . The probability mass function of is

| (17) |

where ; in symbols, . Using (17), model (6) becomes

| (18) |

Hereafter, we will refer to the resulting distribution as two-point asymmetric Laplace (TP-AL).

If , then the th moment of is

| (19) |

If we put in (11)–(15) the first four raw moments computed according to (19), mean, variance, skewness and kurtosis of the TP-AL distribution become

| (20) |

| (21) |

| (22) |

and

| (23) |

With respect to , which can be considered as the reference distribution for the model (for a discussion about the concept of reference distribution, see Davies & Gather, 1993), the additional parameters and have an interpretation of practical interest.

- –

-

is the proportion of points from the reference distribution. For applications of model (18) in robustness studies, it could be natural to assume, and we will do that hereafter, that , i.e., at least half of the observations come from the reference distribution (Hennig, 2002, p. 250, Punzo & McNicholas, 2016, Mazza & Punzo, 2019, Templ et al., 2019 and Punzo & Bagnato, 2021a).

- –

-

denotes the degree of contamination and, because of the assumption , it can be meant as the increase in variability due to the points which do not come from the reference distribution; hence, it is an inflation parameter.

Model (18) reduces to when and , and can also be seen as the natural asymmetric counterpart of the contaminated Laplace distribution introduced by Punzo & Bagnato (2021a). For this reason, we will also refer to the TP-AL distribution as contaminated asymmetric Laplace distribution.

An interesting characteristic of model (18) is the possibility to determine whether a generic observation comes or not from the reference distribution via the a posteriori probability

| (24) |

Specifically, will be considered coming from the reference distribution if the probability in (24) is greater than 1/2.

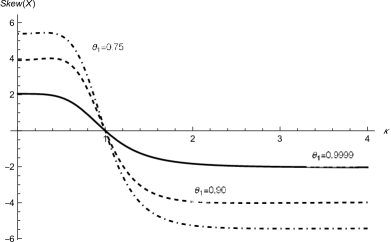

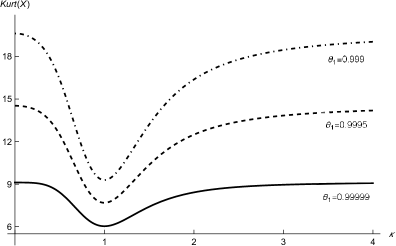

Figure 2 shows examples of behaviors of and , as functions of , at various levels of , with .

From Figure 2(a) we realize that: 1) values of close to 1 tend to produce the plot of we obtained for (refer to Figure 1); and 2) as decreases (to a minimum value of 0.5), the range of possible values of increases. Similarly, from Figure 2(b) we realize that, fixed : 1) large values of (with a maximum of 1) tend to produce the plot of we obtained for (refer to Figure 1); and 2) kept fixed, the lower the value (with a minimum of 0.5), the higher the kurtosis. This means that the curve obtained for acts as a lower bound.

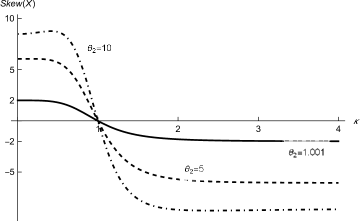

Figure 3 shows examples of behaviors of and , as functions of , at various levels of , with .

From Figure 3(a) we realize that: 1) values of close to 1 tend to produce the plot of we obtained for (refer to Figure 1); and 2) as grows, the range of possible values of increases. Similarly, from Figure 3(b) we realize that: 1) small values of (with a minimum of 1) tend to produce the plot of we obtained for (refer to Figure 1); and 2) kept fixed, the higher the value , the higher the kurtosis. This means that the curve obtained for acts as a lower bound.

3.2 Shifted exponential Laplace distribution

Let

| (25) |

with rate parameter , be the pdf of the shifted exponential, in symbols . When the pdf in (25) is considered as mixing density in model (6), the pdf of the ALSM becomes

| (26) |

We will refer to the resulting distribution as shifted exponential asymmetric Laplace (SE-AL). Model (26) reduces to when . Moreover, if , then we obtain the SE-Laplace distribution, proposed by Punzo & Bagnato (2021a), as a special case.

If , then the th raw moment of is

| (27) |

where is the exponential integral function. By substituting in (12)–(15) the first four raw moments computed according to (27), mean, variance, skewness and kurtosis of the SE-AL distribution become

| (28) |

| (29) |

| (30) |

and

| (31) |

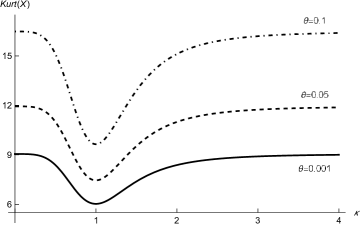

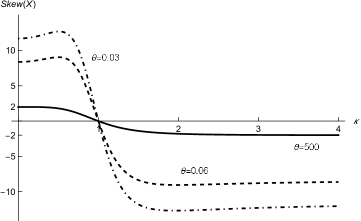

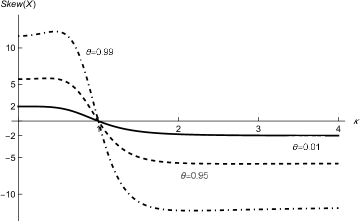

Figure 4 shows examples of behaviors of and , as functions of , at various levels of .

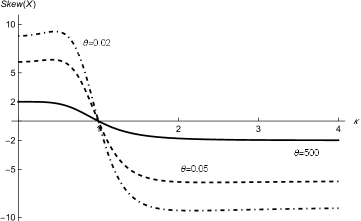

From Figure 4(a) we realize that: 1) large values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) as decreases, the range of possible values of increases. Moreover, to “significantly” modify the behavior of with respect to the case, we need low values of (in the examples, and ). Similarly, from Figure 4(b) we realize that: 1) large values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) kept fixed, the lower the value , the higher the kurtosis. This means that the curve obtained for acts as a lower bound. Also in this case, to “significantly” modify the behavior of with respect to the case, we need low values of (in the examples, and ).

3.3 Unimodal gamma asymmetric Laplace distribution

Let

| (32) |

with , be the pdf of the unimodal gamma distribution (Chen, 2000) with mode in . In symbols, ; see also Bagnato & Punzo (2013). When the pdf in (32) is considered as mixing density in model (6), the pdf of the ALSM becomes

| (33) |

We refer to model (33) as unimodal gamma asymmetric Laplace (UG-AL) distribution. Model (33) reduces to when . Moreover, if , then we obtain the UG-Laplace distribution, proposed by Punzo & Bagnato (2021a), as a special case.

If , then the th raw moment of is

| (34) |

which exists if . By substituting in (12)–(15) the first four raw moments in (34), mean, variance, skewness and kurtosis of the UG-AL distribution become

| (35) |

| (36) |

which exists if ,

| (37) |

which exists if , and

| (38) |

which exists if .

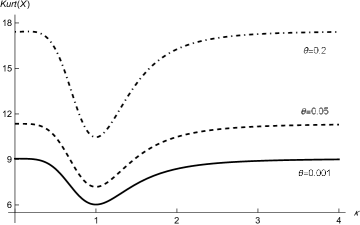

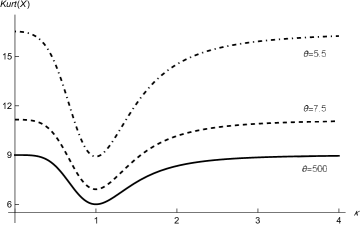

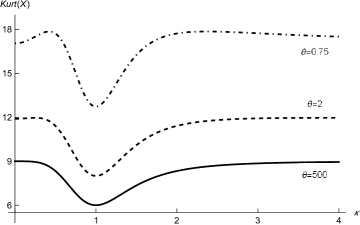

Figure 5 shows examples of behaviors of and , as functions of , at various levels of .

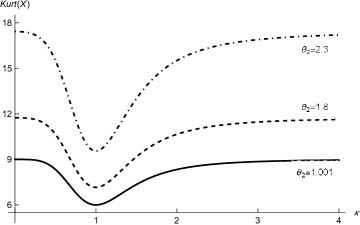

From Figure 5(a) we realize that: 1) small values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) as grows from 0 to 1/2, the range of possible values of increases. Similarly, from Figure 5(b) we realize that: 1) small values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) kept fixed, as grows from 0 to 1/3, the kurtosis increases. This means that the curve obtained for acts as a lower bound.

For completeness, and in analogy with the genesis of the distribution as a normal scale mixture, in A we give an alternative parameterization of the UG-AL distribution using a mixing gamma distribution with shape and rate equal to .

3.4 Inverse Gaussian asymmetric Laplace distribution

Let

| (39) |

with , be the pdf of the reparameterized inverse Gaussian distribution, introduced by Punzo (2019), with mode in ; see also Punzo et al. (2018). If has the pdf in (39), then we compactly write . When the pdf in (39) is considered as mixing density in model (6), the pdf of the ALSM becomes

| (40) |

We call inverse Gaussian asymmetric Laplace (IG-AL) the resulting distribution. Model (40) reduces to when . Moreover, if , then we obtain the IG-Laplace distribution, proposed by Punzo & Bagnato (2021a), as a special case.

When , the th raw moment of is

| (41) |

where is the modified Bessel function of the third kind; for details, see Abramowitz & Stegun (1965) and Watson (1995). By substituting in (12)–(15) the first four raw moments in (41), mean, variance, skewness and kurtosis of the IG-AL distribution become

| (42) |

| (43) |

| (44) |

and

| (45) |

Figure 6 shows examples of behaviors of and , as functions of , at various levels of .

From Figure 6(a) we realize that: 1) small values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) as grows, the range of possible values of increases. Similarly, from Figure 6(b) we realize that: 1) small values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) kept fixed, as grows, the kurtosis increases. This means that the curve obtained for acts as a lower bound.

3.5 Power-function asymmetric Laplace distribution

Let

| (46) |

with shape parameter , be the pdf of the (standard) power-function distribution, in symbols , special case of the beta distribution ; see Johnson & Kotz (1970a, Chapter 25) and Ahsanullah & Kabir (1974). When the pdf in (46) is considered as mixing density in model (6), the pdf of the ALSM simplifies as

| (47) |

where is the lower incomplete gamma function. We refer to the resulting distribution as power-function asymmetric Laplace (PF-AL). Model (47) reduces to when . Moreover, if , then we obtain the PF-Laplace distribution, proposed by Punzo & Bagnato (2021a), as a special case.

When , the th raw moment of – to be substituted in (12)–(15) to obtain mean, variance, skewness and kurtosis of the PF-AL distribution – is

| (48) |

which exists for . Thanks to (48), we have

| (49) |

which exists if ,

| (50) |

which exists if ,

| (51) |

which exists if , and

| (52) |

which exists if .

Figure 7 shows examples of behaviors of and , as functions of , at various levels of .

From Figure 7(a) we realize that: 1) large values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) as decreases (to a minimum value of 3), the range of possible values of increases. Moreover, to “significantly” modify the behavior of with respect to the case, we need low values of (in the examples, and ). Similarly, from Figure 7(b) we realize that: 1) large values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) kept fixed, the lower the value (with a minimum of 4), the higher the kurtosis. This means that the curve obtained for acts as a lower bound. Also in this case, to “significantly” modify the behavior of with respect to the case, we need low values of (in the examples, and ).

3.6 Pareto asymmetric Laplace distribution

Let

| (53) |

with , be the pdf of a Pareto distribution with unitary scale and shape ; in symbols, . When the pdf in (53) is considered as mixing density in model (6), the pdf of the ALSM simplifies as

| (54) |

We refer to the resulting distribution as Pareto asymmetric Laplace (P-AL). Model (54) reduces to when .

When , the th raw moment of is

| (55) |

By substituting in (12)–(15) the first four raw moments in (55), mean, variance, skewness and kurtosis of the P-AL distribution become

| (56) |

| (57) |

| (58) |

and

| (59) |

Figure 8 shows examples of behaviors of and , as functions of , at various levels of .

From Figure 8(a) we realize that: 1) a large value of produces, as a limiting case, the plot of we obtained for (refer to Figure 1); and 2) as decreases, the range of possible values of increases. Moreover, to “significantly” modify the behavior of with respect to the case, we need low values of (in the examples, and ). Similarly, from Figure 8(b) we realize that: 1) a large value of produces, as a limiting case, the plot of we obtained for (refer to Figure 1); and 2) kept fixed, the lower the value , the higher the kurtosis. This means that the curve obtained for acts as a lower bound. Also in this case, to “significantly” modify the behavior of with respect to the case, we need low values of (in the examples, and ).

3.7 Uniform asymmetric Laplace distribution

When a uniform distribution on , , is chosen as mixing distribution, in symbols , the pdf of the ALSM becomes

| (60) |

We will refer to the resulting distribution as uniform asymmetric Laplace (U-AL) or, in analogy with Punzo & Bagnato (2021b), as tail-inflated asymmetric Laplace distribution. Model (60) reduces to when .

When , the th raw moment of is

| (61) |

By substituting in (12)–(15) the first four raw moments in (61), mean, variance, skewness and kurtosis of the U-AL distribution become

| (62) |

| (63) |

| (64) |

and

| (65) |

Figure 9 shows examples of behaviors of and , as functions of , at various levels of .

From Figure 9(a) we realize that: 1) small values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) as grows, the range of possible values of increases. Moreover, to “significantly” modify the behavior of with respect to the case, we need values of close to 1 (in the examples, and ). Similarly, from Figure 9(b) we realize that: 1) small values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) kept fixed, as grows, the kurtosis increases. This means that the curve obtained for acts as a lower bound.

4 Maximum likelihood estimation

Several estimators of the parameters of the ALSMs may be considered. Among them, maximum likelihood (ML) estimators are most attractive because of their large sample properties.

Given a sample from the pdf in (6), the log-likelihood function of the ALSM is

| (66) |

The first order partial derivatives of (66), with respect to , are

The values of , , , and that maximize are the ML estimates , , , and and satisfy the condition .

The ML fitting of most of the models in our family is simplified considerably by the application of the expectation-maximization (EM) algorithm (Dempster et al., 1977) which is, indeed, the classical approach to find ML estimates for parameters of distributions which are defined as a mixture. The TP-AL and the U-AL distributions are the exceptions; indeed, they require convenient variants of the EM algorithm. For the TP-AL distribution, in analogy with other contaminated models available in the literature (Punzo & McNicholas, 2016, Punzo, 2019, Morris et al., 2019, Tomarchio & Punzo, 2020 and Punzo & Tortora, 2021), we illustrate in E the application of the expectation-conditional maximization (ECM) algorithm (Meng & Rubin, 1993), a well-known extension of the EM algorithm (see McLachlan & Krishnan, 2007, Chapter 5, for details). The ECM algorithm replaces the M-step of the EM algorithm by a number of computationally simpler conditional maximization (CM) steps. The expectation-conditional maximization either (ECME) algorithm (Liu & Rubin, 1994) generalizes the ECM algorithm by conditionally maximizing on some or all of the CM-steps the incomplete-data log-likelihood. We illustrate this algorithm, to fit the U-AL distribution, in F.

For the application of the EM algorithm and, more in general, of any of its variant, it is convenient to view the observed data as incomplete. The complete data are , where the missing variables are defined so that

independently for , and

Because of this conditional structure, the complete-data likelihood function can be factored into the product of the conditional densities of given the and the joint marginal densities of , i.e.

Accordingly, the complete-data log-likelihood function can be written as

| (67) |

where

| (68) |

and

| (69) |

with

and

So, while is shared by all the ALSMs, is distribution-dependent and – by only focusing on the distributions for which the EM algorithm is considered – is given by

| (70) |

for the SE-AL distribution,

| (71) |

for the UG-AL distribution,

| (72) |

for the IG-AL distribution,

| (73) |

for the PF-AL distribution, and

| (74) |

for the PAR-AL distribution.

Working on , the EM algorithm iterates between two steps, one E-step and one M-step, until convergence. We detail these steps below for a generic iteration of the algorithm, as well as for all the considered ALSMs apart from the TP-AL and U-AL distributions (see E and F). As in Melnykov & Zhu (2018, 2019), quantities/parameters marked with one dot will correspond to the previous iteration and those marked with two dots will represent the estimates at the current iteration.

4.1 E-step

The E-step requires the calculation of

| (75) |

the conditional expectation of given the observed data , using for . In (75) the two terms on the right-hand side are ordered as the two terms on the right-hand side of (67). As well-explained in McNeil et al. (2005, p. 82), in order to compute we need to replace any function of the latent mixing variables which arise in (68) and (69) by the quantities , where the expectation, as highlighted by the superscript, is taken using for , . To calculate these expectations we can observe that the conditional pdf of satisfies , up to some constant of proportionality.

Below we detail the E-step for the considered ALSMs.

4.1.1 Shifted exponential asymmetric Laplace distribution

For the SE-AL distribution we have

| (76) |

where

and

denotes the pdf of a gamma distribution with shape and rate . This means that has a left-truncated gamma distribution (see, e.g., Coffey & Muller, 2000), on the interval , with shape and rate , whose pdf is given in (76); in symbols

| (77) |

The function arising from (68) and (70) is . Thanks to (77) we obtain

where

is the Misra function (Misra, 1940), further generalization of the generalized exponential integral function (Abramowitz & Stegun, 1965).

4.1.2 Unimodal gamma asymmetric Laplace distribution

For the UG-AL distribution we have

| (78) |

This means that has a gamma distribution with shape and rate , whose pdf is given in (78); in symbols

| (79) |

The functions arising from (68) and (71) are and . Thanks to (79) we obtain

and

where denotes the digamma function.

In B.1 we report the analogous material for the reparameterized UG-AL distribution obtained considering the classical gamma as mixing distribution.

4.1.3 Inverse Gaussian asymmetric Laplace distribution

4.1.4 Power-function asymmetric Laplace distribution

For the PF-AL distribution we have

| (81) |

where

This means that has a right-truncated gamma distribution (see, e.g., Coffey & Muller, 2000), on the interval , with shape and rate , whose pdf is given in (81); in symbols

| (82) |

The functions arising from (68) and (73) are and . Thanks to (82) we obtain

and

where is the generalized hypergeometric function (Dwork, 1990).

4.1.5 Pareto asymmetric Laplace distribution

4.2 M-step

The M-step requires the calculation of as the value of that maximizes . According to the right-hand side of (75), and can be maximized separately with respect to the parameters they involve, with the maximization of being independent of the ALSM considered. is also the function to be maximized in the first CM-step of the ECME algorithm related to the U-AL distribution to obtain the updates of , and .

can be maximized following an approach similar to the one used to find ML estimators for the parameters of the AL distribution (see, e.g., Kotz et al., 2001). To find , , and we can proceed as follows.

- Step 1:

- Step 2:

-

Set as defined in D.2 and use the results in D.1 to find solutions for and . In particular, there are three scenarios in Step 2.

- –

-

If , then as in the situation i) in D.1 the solutions of and do not exist. In this case the ML estimates for the ALSM can not be found by using the EM algorithm;

- –

-

If , then as in the situation ii) in D.1 the solutions of and do not exist. As before the ML estimates for the ALSM can not be found by using the EM algorithm.

- –

We provide below details about the maximization of for each ALSM.

4.2.1 Shifted exponential asymmetric Laplace distribution

For the SE-AL,

is the log-likelihood function of independent observations from a shifted exponential distribution with parameter . Therefore, from the standard theory about the exponential distribution (see, e.g., Johnson & Kotz, 1970b, Chapter 19), the update for is

4.2.2 Unimodal gamma asymmetric Laplace distribution

For the UG-AL distribution, a closed-form update for does not exist. The function to maximize is

| (85) |

whose derivative, with respect to , is

| (86) |

The update for can be obtained numerically either by maximizing (85) over or by finding the root (over ) of the equation obtained equating (86) to zero.

In B.2 we provide the analogous quantities for the reparameterized UG-AL distribution which uses the classical gamma as mixing distribution.

4.2.3 Inverse Gaussian asymmetric Laplace distribution

For the IG-AL distribution, a closed-form update for does not exist. The function to maximize is

| (87) |

where does not need to be calculated since no parameters are related to it. The derivative, with respect to , is

| (88) |

As for the UG-AL distribution, the update for can be obtained numerically either by maximizing (87) over or by finding the root (over ) of the equation obtained equating (88) to zero.

4.2.4 Power-function asymmetric Laplace distribution

For the PF-AL distribution, the function to be maximized to obtain the update for is

The closed-form update for is

4.2.5 Pareto asymmetric Laplace distribution

For the PAR-AL,

is the log-likelihood function of independent observations from a Pareto distribution. Therefore, from the standard theory about the Pareto distribution (see, e.g., Rytgaard, 1990), the update for is

4.2.6 Uniform asymmetric Laplace distribution

For the U-AL distribution the update of is computed at the second CM-step of the ECME algorithm by maximizing the observed-data log-likelihood function over .

5 Data and results

5.1 Data

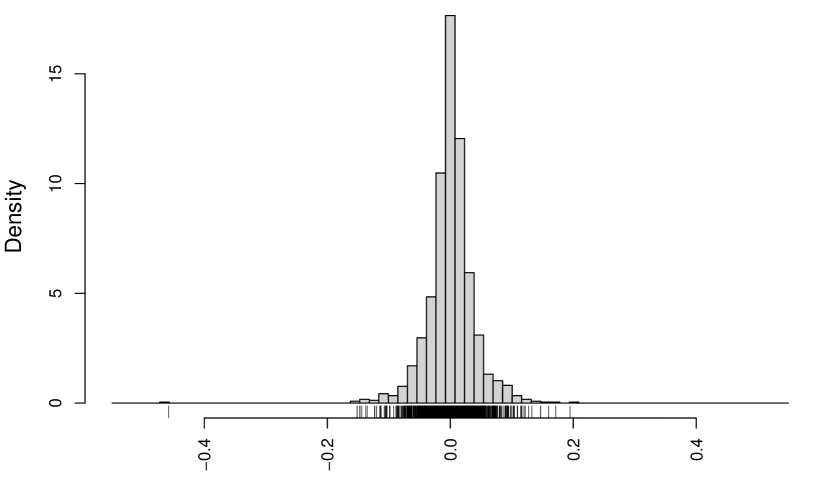

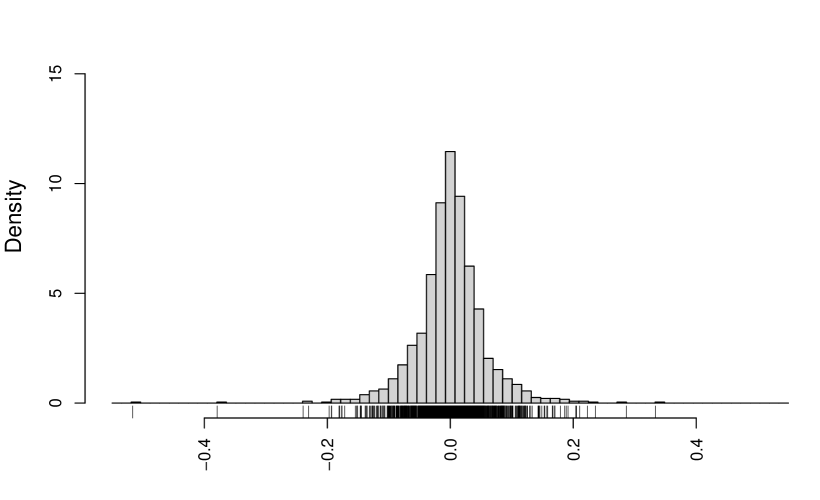

We downloaded the daily adjusted close prices of the following two cryptocurrencies: Bitcoin EUR (BTC-EUR) and TRON EUR (TRX-EUR). All prices are in Euro. The data were downloaded from https://finance.yahoo.com/cryptocurrencies. The period under investigation goes from 1 April 2018 to 31 May 2022. Returns are estimated by taking logarithmic differences.

We conduct the whole analysis in R (R Core Team, 2018), and the codes needed to replicate the analysis are available upon request. Table 1 shows some descriptive statistics of the considered cryptocurrency returns. Table 1 also reports the -values of the D’Agostino test of skewness and of three commonly employed tests of normality: Anderson-Darling, Jarque-Bera and Shapiro-Wilk (see Yap & Sim, 2011, for a comparison). In the following we will compare the -values with the classical 0.05 significance level. Regardless of the considered cryptocurrency, mean and median are very close to zero. TRX-EUR has a slightly larger variability, as measured by the standard deviation and range. All the return distributions are skewed (according to the D’Agostino test, regardless of the considered significance level) and, in agreement with the literature, they are clearly non-normal regardless of both the considered normality test and significance level considered (-values very close to 0). Finally, the return distributions are highly leptokurtic with an excess kurtosis of 15.966 for BTC-EUR and of 8.249 for TRX-EUR.

| BTC-EUR | TRX-EUR | |

|---|---|---|

| 1521 | 1521 | |

| Mean | 0.001 | 0.001 |

| Median | 0.001 | 0.001 |

| St. Dev. | 0.038 | 0.057 |

| Skewness | -1.079 | -0.434 |

| Kurtosis | 18.966 | 11.249 |

| Minimum | -0.458 | -0.516 |

| Maximum | 0.195 | 0.334 |

| D’Agostino test (-value) | 0.000 | 0.000 |

| Anderson-Darling test (-value) | 0.000 | 0.000 |

| Jarque-Bera test (-value) | 0.000 | 0.000 |

| Shapiro-Wilk test (-value) | 0.000 | 0.000 |

The histograms of the cryptocurrency returns appear in Figure 10; to make the comparison easier, the histograms share the same axes range. Regardless of the considered cryptocurrency, we observe the shape typical of the asymmetric Laplace distribution. Indeed, the distributions have high peaks near zero and appear to have tails heavier than those of the normal distribution. However, the empirical kurtoses in Table 1 are not included in , the interval of kurtoses allowed by the asymmetric Laplace distribution (refer to Figure 1). In particular, they are larger.

5.2 Results

Motivated by the findings above, especially those related to shape, skewness and kurtosis of the empirical distributions, we fit our ALSMs to the considered cryptocurrency returns. For the sake of comparison, we also fit several parametric distributions defined on the whole real line. We take the competing models among those implemented in the gamlss package (Rigby & Stasinopoulos, 2005) for R. In detail, we consider the following distributions, given in alphabetic order using the nomenclature by Rigby et al. (2019): exponential Gaussian (exGAUS), generalized (GT), Gumbel (GU), Johnson’s SU (JSU), logistic (LO), NET (NET), normal (NO), normal family (NOF), power exponential (PE), reverse Gumbel (RG), sinh-arcsinh (SHASH), sinh-arcsinh original (SHASHo), skew normal type 1 (SN1), skew normal type 2 (SN2), skew power exponential type 1 (SEP1), skew power exponential type 2 (SEP2), skew power exponential type 3 (SEP3), skew power exponential type 4 (SEP4), skew Student (SST), skew type 1 (ST1), skew type 2 (ST2), skew type 4 (ST4), skew type 5 (ST5), and family (TF). Moreover, for the sake of completeness, and motivated by the results in Chu et al. (2015) and Chan et al. (2017), we also fit the generalyzed hyperbolic (GH) and some of its special cases which are not implemented in the gamlss package, namely hyperbolic (H), variance gamma (VG), and normal inverse Gaussian (NIG) distributions. These models are fitted via the fit.ghypuv() function of the ghyp package. This yields a total of 36 competing models. We estimate the parameters of all the models under consideration via the ML approach.

To compare models with the same number of parameters, in terms of goodness-of-fit, we use the log-likelihood (in addition to the criteria described below). We accomplish the comparison of models with differing number of parameters, as usual, via the Akaike information criterion (AIC; Akaike, 1974) and the Bayesian information criterion (BIC; Schwarz, 1978) that, in our formulation, need to be maximized because they are multiplied by . Moreover, we use the likelihood-ratio (LR) test to compare each Laplace-based model (alternative model) with the nested asymmetric Laplace distribution (null model). In particular, the LR test can be used to determine whether the alternative model is a significant improvement over the asymmetric Laplace distribution. The test statistic is

where , , and are the ML estimates of , , and , respectively, and where and are the maximized log-likelihood values under the null and alternative models, respectively. Under the null hypothesis of no improvement, using Wilks’ theorem, LR can be approximated by a random variable with number of degrees of freedom given by the difference in the number of estimated parameters between the alternative and the null model, and this allows us to compute a -value.

Tables 2–3 present the model comparison separately for each cryptocurrency. To easy the reader in comparing the performance of the considered parametric models, the tables also give rankings induced by AIC, BIC, and LR tests (limited to the AL-based models).

| Model | par | Log-lik | AIC | Rank | BIC | Rank | LR -value | Rank |

|---|---|---|---|---|---|---|---|---|

| AL | 3 | 3020.921 | 6035.842 | 18 | 6019.861 | 15 | ||

| TP-AL | 5 | 3027.713 | 6045.426 | 7 | 6018.790 | 17 | 0.001 | 6 |

| SE-AL | 4 | 3026.311 | 6044.621 | 8 | 6023.313 | 7 | 0.001 | 5 |

| UG-AL | 4 | 3027.701 | 6047.402 | 4 | 6026.094 | 5 | 0.000 | 3 |

| IG-AL | 4 | 3027.388 | 6046.776 | 5 | 6025.467 | 6 | 0.000 | 4 |

| PF-AL | 4 | 3028.167 | 6048.334 | 2 | 6027.026 | 3 | 0.000 | 2 |

| P-AL | 4 | 3025.807 | 6043.614 | 13 | 6022.306 | 12 | 0.002 | 7 |

| U-AL | 4 | 3047.685 | 6087.370 | 1 | 6066.062 | 1 | 0.000 | 1 |

| exGAUS | 3 | 2818.553 | 5631.105 | 31 | 5615.124 | 32 | ||

| GH | 5 | 3025.958 | 6041.917 | 16 | 6015.281 | 18 | ||

| GT | 4 | 3027.728 | 6047.455 | 3 | 6026.147 | 4 | ||

| GU | 2 | 2593.517 | 5183.034 | 35 | 5172.380 | 35 | ||

| H | 4 | 3020.920 | 6033.841 | 20 | 6012.532 | 20 | ||

| JSU | 4 | 3018.886 | 6029.773 | 21 | 6008.464 | 21 | ||

| LO | 2 | 2962.209 | 5920.419 | 29 | 5909.765 | 29 | ||

| NET | 2 | 2988.639 | 5969.277 | 28 | 5947.969 | 28 | ||

| NIG | 4 | 3021.583 | 6035.167 | 19 | 6013.858 | 19 | ||

| NO | 2 | 2816.573 | 5629.146 | 32 | 5618.491 | 31 | ||

| NOF | 3 | 2816.573 | 5627.146 | 33 | 5611.164 | 33 | ||

| PE | 3 | 3026.119 | 6046.239 | 6 | 6030.257 | 2 | ||

| RG | 2 | 1909.950 | 3815.899 | 36 | 3805.245 | 36 | ||

| SHASH | 4 | 3025.711 | 6043.422 | 14 | 6022.113 | 13 | ||

| SHASHo | 4 | 3025.522 | 6043.044 | 15 | 6021.735 | 14 | ||

| SN1 | 3 | 2816.573 | 5627.146 | 34 | 5611.164 | 34 | ||

| SN2 | 3 | 2820.347 | 5634.693 | 30 | 5618.712 | 30 | ||

| SEP1 | 4 | 3026.126 | 6044.253 | 11 | 6022.944 | 10 | ||

| SEP2 | 4 | 3026.146 | 6044.292 | 10 | 6022.984 | 9 | ||

| SEP3 | 4 | 3026.120 | 6044.241 | 12 | 6022.932 | 11 | ||

| SEP4 | 4 | 3026.208 | 6044.416 | 9 | 6023.108 | 8 | ||

| SST | 4 | 3012.351 | 6016.702 | 27 | 5995.394 | 27 | ||

| ST1 | 4 | 3012.427 | 6016.853 | 23 | 5995.545 | 23 | ||

| ST2 | 4 | 3012.360 | 6016.719 | 26 | 5995.411 | 26 | ||

| ST4 | 4 | 3012.363 | 6016.725 | 25 | 5995.417 | 25 | ||

| ST5 | 4 | 3012.363 | 6016.726 | 24 | 5995.418 | 24 | ||

| TF | 3 | 3012.320 | 6018.641 | 22 | 6002.659 | 22 | ||

| VG | 4 | 3024.470 | 6040.940 | 17 | 6019.631 | 16 |

| Model | par | Log-lik | AIC | Rank | BIC | Rank | LR -value | Rank |

|---|---|---|---|---|---|---|---|---|

| AL | 3 | 2383.212 | 4760.423 | 20 | 4744.442 | 8 | ||

| TP-AL | 5 | 2388.481 | 4766.963 | 5 | 4740.327 | 18 | 0.005 | 5 |

| SE-AL | 4 | 2386.362 | 4764.723 | 11 | 4743.415 | 11 | 0.012 | 6 |

| UG-AL | 4 | 2387.646 | 4767.293 | 4 | 4745.984 | 5 | 0.003 | 3 |

| IG-AL | 4 | 2387.405 | 4766.810 | 6 | 4745.501 | 6 | 0.004 | 4 |

| PF-AL | 4 | 2388.365 | 4768.731 | 3 | 4747.422 | 4 | 0.001 | 2 |

| P-AL | 4 | 2385.815 | 4763.630 | 14 | 4742.322 | 13 | 0.022 | 7 |

| U-AL | 4 | 2409.962 | 4811.925 | 1 | 4790.617 | 1 | 0.000 | 1 |

| exGAUS | 3 | 2213.975 | 4421.950 | 30 | 4405.969 | 30 | ||

| GH | 5 | 2388.037 | 4766.073 | 7 | 4739.438 | 20 | ||

| GT | 4 | 2388.430 | 4768.861 | 2 | 4747.552 | 3 | ||

| GU | 2 | 1902.159 | 3800.318 | 35 | 3789.663 | 35 | ||

| H | 4 | 2383.211 | 4758.423 | 21 | 4737.114 | 22 | ||

| JSU | 4 | 2384.976 | 4761.952 | 18 | 4740.644 | 17 | ||

| LO | 2 | 2333.869 | 4663.738 | 29 | 4653.084 | 29 | ||

| NET | 2 | 2360.386 | 4712.772 | 28 | 4691.463 | 28 | ||

| NIG | 4 | 2386.959 | 4765.918 | 8 | 4744.610 | 7 | ||

| NO | 2 | 2202.754 | 4401.507 | 31 | 4390.853 | 31 | ||

| NOF | 3 | 2202.626 | 4399.253 | 34 | 4383.271 | 34 | ||

| PE | 3 | 2385.124 | 4764.247 | 12 | 4748.266 | 2 | ||

| RG | 2 | 1587.234 | 3170.468 | 36 | 3159.814 | 36 | ||

| SHASH | 4 | 2386.467 | 4764.933 | 10 | 4743.625 | 10 | ||

| SHASHo | 4 | 2386.468 | 4764.935 | 9 | 4743.627 | 9 | ||

| SN1 | 3 | 2202.754 | 4399.507 | 33 | 4383.526 | 33 | ||

| SN2 | 3 | 2203.538 | 4401.075 | 32 | 4385.094 | 32 | ||

| SEP1 | 4 | 2385.688 | 4763.376 | 16 | 4742.068 | 15 | ||

| SEP2 | 4 | 2385.830 | 4763.660 | 13 | 4742.351 | 12 | ||

| SEP3 | 4 | 2385.763 | 4763.526 | 15 | 4742.218 | 14 | ||

| SEP4 | 4 | 2385.322 | 4762.644 | 17 | 4741.335 | 16 | ||

| SST | 4 | 2380.241 | 4752.482 | 23 | 4731.174 | 23 | ||

| ST1 | 4 | 2380.229 | 4752.458 | 24 | 4731.149 | 24 | ||

| ST2 | 4 | 2380.222 | 4752.444 | 25 | 4731.136 | 25 | ||

| ST4 | 4 | 2380.207 | 4752.414 | 27 | 4731.106 | 27 | ||

| ST5 | 4 | 2380.218 | 4752.435 | 26 | 4731.127 | 26 | ||

| TF | 3 | 2380.206 | 4754.412 | 22 | 4738.430 | 21 | ||

| VG | 4 | 2384.530 | 4761.061 | 19 | 4739.752 | 19 |

For the BTC-EUR, Table 2 shows that both AIC and BIC indicate one of our models, the U-AL, as the best one. Furthermore, six out of the seven models we propose (all except P-AL) are in the first eight positions according to the AIC (GT and PE occupy the third and sixth positions, respectively) while five out of our seven models (all except P-AL and TP-AL) are in the first six positions according to the BIC (PE and GT occupy the second and fourth positions, respectively). These findings are further corroborated by the ranking induced by the LR-test, with the U-AL in the first position and the TP-AL and P-AL in the penultimate and last position, respectively. Moreover, at the 5% significance level, all our models represent a significant improvement over the asymmetric Laplace.

For the TRX-EUR (refer to Table 3) we observe similar results. The U-AL is still the best model for AIC, BIC and LR test. Moreover, based on the -values from the LR test, all our models still represent a significant improvement over the asymmetric Laplace at the 5% significance level.

A final interesting aspect to be noted is that, regardless of the considered cryptocurrency, the Gumbel-based models (RG and GU) are the worst models according to AIC and BIC.

6 Conclusions and future works

In this paper we further corroborate some recent findings about the cryptocurrency return distribution; in particular, we confirm it can be highly-peaked, skewed, and heavy-tailed, with a large excess kurtosis. To account for all these peculiarities, in a modeling perspective, we propose the asymmetric Laplace scale mixture (ALSM) family of distributions and, for illustrative purposes, we consider seven different members of this family. Advantageously with respect to the nested asymmetric Laplace distribution, the members of our family allow for a wider range of skewness values and for a larger excess kurtosis. These improvements allows the ALSM to be a convenient model for the distribution of cryptocurrency returns.

However, the novelty of the paper is not limited to the five illustrated models and the usefulness of our family is not restricted to cryptocurrencies. Indeed, other members of the family may be easily defined and other financial contexts, like those outlined in Kotz et al. (2012, Chapter 8), may benefit from the use of ALSMs.

References

- Abramowitz & Stegun (1965) Abramowitz, M., & Stegun, I. A. (1965). Handbook of Mathematical Functions: With Formulas, Graphs, and Mathematical Tables volume 55 of Applied Mathematics Series. New York: Dover Publications.

- Ahsanullah & Kabir (1974) Ahsanullah, M., & Kabir, A. B. M. L. (1974). A characterization of the power function distribution. The Canadian Journal of Statistics, 2, 95–98.

- Akaike (1974) Akaike, H. (1974). A new look at the statistical model identification. IEEE Transactions on Automatic Control, 19, 716–723.

- Askey & Daalhuis (2010) Askey, R. A., & Daalhuis, A. B. O. (2010). Generalized hypergeometric functions and Meijer -function.

- Bagnato & Punzo (2013) Bagnato, L., & Punzo, A. (2013). Finite mixtures of unimodal beta and gamma densities and the -bumps algorithm. Computational Statistics, 28, 1571–1597.

- Bariviera et al. (2017) Bariviera, A. F., Basgall, M. J., Hasperué, W., & Naiouf, M. (2017). Some stylized facts of the Bitcoin market. Physica A: Statistical Mechanics and its Applications, 484, 82–90.

- Chan et al. (2017) Chan, S., Chu, J., Nadarajah, S., & Osterrieder, J. (2017). A statistical analysis of cryptocurrencies. Journal of Risk and Financial Management, 10, 1–24.

- Chen (2000) Chen, S. X. (2000). Probability density function estimation using gamma kernels. Annals of the Institute of Statistical Mathematics, 52, 471–480.

- Chu et al. (2015) Chu, J., Nadarajah, S., & Chan, S. (2015). Statistical analysis of the exchange rate of bitcoin. PLOS One, 10, e0133678.

- Coffey & Muller (2000) Coffey, C. S., & Muller, K. E. (2000). Properties of doubly-truncated gamma variables. Communications in Statistics-Theory and Methods, 29, 851–857.

- Davies & Gather (1993) Davies, L., & Gather, U. (1993). The identification of multiple outliers. Journal of the American Statistical Association, 88, 782–792.

- Dempster et al. (1977) Dempster, A. P., Laird, N. M., & Rubin, D. B. (1977). Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 39, 1–38.

- Dwork (1990) Dwork, B. (1990). Generalized hypergeometric functions. Clarendon Press.

- Hennig (2002) Hennig, C. (2002). Fixed point clusters for linear regression: computation and comparison. Journal of Classification, 19, 249–276.

- Johnson & Kotz (1970a) Johnson, N. L., & Kotz, S. (1970a). Continuous Univariate Distributions volume 2. New York: John Wiley & Sons.

- Johnson & Kotz (1970b) Johnson, N. L., & Kotz, S. (1970b). Continuous Univariate Distributions volume 1. New York: John Wiley & Sons.

- Kotz et al. (2001) Kotz, S., Kozubowski, T., & Podgórski, K. (2001). The Laplace distribution and generalizations: a revisit with applications to communications, economics, engineering, and finance. 183. Springer Science & Business Media.

- Kotz et al. (2012) Kotz, S., Kozubowski, T. J., & Podgorski, K. (2012). The Laplace Distribution and Generalizations: A Revisit with Applications to Communications, Economics, Engineering, and Finance. SpringerLink : Bücher. Birkhäuser Boston.

- Kozubowski & Podgorski (2000) Kozubowski, T. J., & Podgorski, K. (2000). Asymmetric laplace distributions. Mathematical Scientist, 25, 37–46.

- Liu & Rubin (1994) Liu, C., & Rubin, D. B. (1994). The ECME algorithm: a simple extension of EM and ECM with faster monotone convergence. Biometrika, 81, 633–648.

- Mazza & Punzo (2019) Mazza, A., & Punzo, A. (2019). Modeling household income with contaminated unimodal distributions. In A. Petrucci, F. Racioppi, & R. Verde (Eds.), New Statistical Developments in Data Science (pp. 373–391). Cham, Switzerland: Springer volume 88 of Springer Proceedings in Mathematics & Statistics.

- McLachlan & Krishnan (2007) McLachlan, G., & Krishnan, T. (2007). The EM algorithm and extensions volume 382 of Wiley Series in Probability and Statistics. (2nd ed.). New York: John Wiley & Sons.

- McNeil et al. (2005) McNeil, A., Frey, R., & Embrechts, P. (2005). Quantitative Risk Management: Concepts, Techniques and Tools. Princeton Series in Finance. Princeton University Press.

- Melnykov & Zhu (2018) Melnykov, V., & Zhu, X. (2018). On model-based clustering of skewed matrix data. Journal of Multivariate Analysis, 167, 181–194.

- Melnykov & Zhu (2019) Melnykov, V., & Zhu, X. (2019). Studying crime trends in the USA over the years 2000–2012. Advances in Data Analysis and Classification, 13, 325–341.

- Meng & Rubin (1993) Meng, X.-L., & Rubin, D. B. (1993). Maximum likelihood estimation via the ECM algorithm: A general framework. Biometrika, 80, 267–278.

- Misra (1940) Misra, R. D. (1940). On the stability of crystal lattices. II. Mathematical Proceedings of the Cambridge Philosophical Society, 36, 173–182.

- Morris et al. (2019) Morris, K., Punzo, A., McNicholas, P. D., & Browne, R. P. (2019). Asymmetric clusters and outliers: Mixtures of multivariate contaminated shifted asymmetric laplace distributions. Computational Statistics & Data Analysis, 132, 145–166.

- Osterrieder (2017) Osterrieder, J. (2017). The statistics of bitcoin and cryptocurrencies. In Proceedings of the 2017 International Conference on Economics, Finance and Statistics (ICEFS 2017). Atlantis Press volume 26 of Advances in Economics, Business and Management Research.

- Phillip et al. (2018) Phillip, A., Chan, J. S. K., & Peiris, S. (2018). A new look at cryptocurrencies. Economics Letters, 163, 6–9.

- Punzo (2019) Punzo, A. (2019). A new look at the inverse Gaussian distribution with applications to insurance and economic data. Journal of Applied Statistics, 46, 1260–1287.

- Punzo & Bagnato (2021a) Punzo, A., & Bagnato, L. (2021a). Modeling the cryptocurrency return distribution via Laplace scale mixtures. Physica A: Statistical Mechanics and its Applications, 563. doi:10.1016/j.physa.2020.125354.

- Punzo & Bagnato (2021b) Punzo, A., & Bagnato, L. (2021b). The multivariate tail-inflated normal distribution and its application in finance. Journal of Statistical Computation and Simulation, 91, 1–36.

- Punzo et al. (2018) Punzo, A., Bagnato, L., & Maruotti, A. (2018). Compound unimodal distributions for insurance losses. Insurance: Mathematics and Economics, 81, 95–107.

- Punzo & McNicholas (2016) Punzo, A., & McNicholas, P. D. (2016). Parsimonious mixtures of multivariate contaminated normal distributions. Biometrical Journal, 58, 1506–1537.

- Punzo & Tortora (2021) Punzo, A., & Tortora, C. (2021). Multiple scaled contaminated normal distribution and its application in clustering. Statistical Modelling, 21, 332–358.

- R Core Team (2018) R Core Team (2018). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing Vienna, Austria. URL: https://www.R-project.org/.

- Rigby & Stasinopoulos (2005) Rigby, R. A., & Stasinopoulos, D. M. (2005). Generalized additive models for location, scale and shape. Journal of the Royal Statistical Society: Series C (Applied Statistics), 54, 507–554.

- Rigby et al. (2019) Rigby, R. A., Stasinopoulos, M. D., Heller, G. Z., & De Bastiani, F. (2019). Distributions for Modeling Location, Scale, and Shape: Using GAMLSS in R. Chapman & Hall/CRC The R Series. CRC Press. URL: https://books.google.it/books?id=Tu-yDwAAQBAJ.

- Rytgaard (1990) Rytgaard, M. (1990). Estimation in the pareto distribution. ASTIN Bulletin: The Journal of the IAA, 20, 201–216.

- Schwarz (1978) Schwarz, G. (1978). Estimating the dimension of a model. The Annals of Statistics, 6, 461–464.

- Shevchenko (2010) Shevchenko, P. V. (2010). Calculation of aggregate loss distributions. The Journal of Operational Risk, 5, 3–40.

- Szczygielski et al. (2020) Szczygielski, J. J., Karathanasopoulos, A., & Zaremba, A. (2020). One shape fits all? A comprehensive examination of cryptocurrency return distributions. Applied Economics Letters, 27, 1567–1573.

- Takaishi (2018) Takaishi, T. (2018). Statistical properties and multifractality of Bitcoin. Physica A: Statistical Mechanics and its Applications, 506, 507–519.

- Templ et al. (2019) Templ, M., Gussenbauer, J., & Filzmoser, P. (2019). Evaluation of robust outlier detection methods for zero-inflated complex data. Journal of Applied Statistics, 47, 1144–1167.

- Tomarchio & Punzo (2020) Tomarchio, S. D., & Punzo, A. (2020). Dichotomous unimodal compound models: Application to the distribution of insurance losses. Journal of Applied Statistics, 47, 2328–2353.

- Watson (1995) Watson, G. N. (1995). A treatise on the theory of Bessel functions. Cambridge university press.

- Yap & Sim (2011) Yap, B. W., & Sim, C. H. (2011). Comparisons of various types of normality tests. Journal of Statistical Computation and Simulation, 81, 2141–2155.

- Zhang et al. (2018) Zhang, W., Wang, P., Li, X., & Shen, D. (2018). Some stylized facts of the cryptocurrency market. Applied Economics, 50, 5950–5965.

Appendix A Gamma asymmetric Laplace distribution

Let

| (89) |

with , be the pdf of the gamma distribution with shape and rate equal to . In symbols, . When the pdf in (89) is considered as mixing density in model (6), the pdf of the ALSM becomes

| (90) |

Although the pdf in (90) is a simple reparameterization of the pdf of the UG-AL model given in (33), for the sake of clarity/confusion we prefer referring to the resulting model as gamma asymmetric Laplace (G-AL). Model (90) reduces to when .

When , the th raw moment of is

| (91) |

which exists when . By substituting in (12)–(15) the first four raw moments in (91), mean, variance, skewness and kurtosis of the G-AL distribution become

| (92) |

which exists if ,

| (93) |

which exists if ,

| (94) |

which exists if , and

| (95) |

which exists if .

Figure 11 shows examples of behaviors of and , as functions of , at various levels of .

From Figure 11(a) we realize that: 1) large values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) as decreases (to a minimum value of 6), the range of possible values of increases. Moreover, to “significantly” modify the behavior of with respect to the case, we need low values of (in the examples, and ). Similarly, from Figure 11(b) we realize that: 1) large values of tend to produce the plot of we obtained for (refer to Figure 1); and 2) kept fixed, the lower the value (with a minimum of 8), the higher the kurtosis. This means that the curve obtained for acts as a lower bound. Also in this case, to “significantly” modify the behavior of with respect to the case, we need low values of (in the examples, and ).

Appendix B E- and M-steps for the G-AL distribution

For the G-AL distribution we have

| (96) |

B.1 E-step

B.2 M-step

Appendix C Method of moments

In the method of moments (MM) applied to the estimation of the parameters of the ALSM distribution, we relate the (unknown) population moments in (12)–(15) to their sample counterparts

Apart from the TP-AL distribution, where is bidimensional, for all the other models it is unidimensional. For these models, with the aim to find the MM estimates of , , , and , we have to solve a system of four equations. In doing that, it is important to remember that the four equations involve a different number of parameters (refer to Section 2.4). So, it is convenient to first find the estimates and by solving the system of the two equations and . To search for the roots of the system of the two nonlinear equations, we use the nleqslv() function included in the nleqslv package. Moreover, to ensure the existence of the moments we have to impose (if necessary) suitable constraints for (refer to Section 3). Then, based on (13), we solve the equation as a function of with and replaced by and , respectively; this leads to

| (100) |

where the quantities , with , are estimates of obtained using . Finally, based on (12), we solve the equation as a function of with , and replaced by , and , respectively; this leads to

| (101) |

Appendix D M-Step details

With the aim to maximize we consider the following two cases:

- • Case 1,

-

only is known;

- • Case 2,

-

all parameters are unknown.

D.1 Case 1

Maximizing is the same as maximizing which, when the value of is known, reduces to

| (102) |

where is defined as

| (103) |

with

| (104) |

The parameter could be: i) , ii) , or iii) . If i) holds, then all sample values are greater or equal to ; this means that

Thus,

| (105) |

where

| (106) |

Therefore, (102) takes the form

| (107) |

Fix and differentiate (107) with respect to to obtain

| (108) |

The derivative (108) is positive for and negative for , where

As a consequence, for any fixed , (107) is maximized by . Then, for all and , we have

| (109) |

where is a function of only and it is decreasing on , with the least upper bound being equal to

Since these values are not admissible, formally the M-step solutions of and do not exist in this case. However, as and , the conditional in (6) tends to .

If we are in the case ii), then all sample values are lower or equal to . This means that

Thus,

| (110) |

Then, (102) takes the form

| (111) |

Fix and differentiate (111) with respect to to obtain

| (112) |

The derivative (112) is positive for and negative for , where

Therefore, for any fixed , (111) is maximized by . Hence, for all and , we have

| (113) |

where is a function of only and it is increasing on , with the limit being equal to

Since these values are not admissible, formally the M-step solutions of and do not exist in this case. However, as and we have that the conditional in (6) tends to a “reversed” shifted exponential distribution with pdf

| (114) |

Under case iii), that is when , we can find the solutions for and through the following equations of derivatives of :

| (115) |

These equations are equivalent to

| (116) |

which lead to the following unique and explicit solutions for and :

| (117) |

D.2 Case 2

The function to maximize, when all the parameters are unknown, is

| (118) |

where

| (119) |

We proceed by first fixing the value of and then applying the same results obtained under the Case 1 in D.1.

If , thanks to (109), we conclude that for any and

Similarly, when , we can use (113) and conclude that

When , then we use the result in iii) of D.1. In particular we have

| (120) |

where the quantities and are obtained as in (117). Substituting these values into the right-hand side of (120) we obtain

where

| (121) |

Maximizing (121) is equivalent to minimize the function

| (122) |

It turns out that the minimum of , on the set

is given by one on the values

| , . |

This follows from the fact that is continuous on the closed interval and concave down on each of the subintervals , (see Lemma 3.5.2 in Kotz et al., 2001).

Appendix E ECM algorithm for the two-point asymmetric Laplace distribution

To have closed-form updates for the parameters , , , and of the TP-AL distribution, at each iteration of the fitting algorithm, we make two changes at the EM algorithm described in Section 4. The first one is related to the use of the expectation-conditional maximization (ECM) algorithm (Meng & Rubin, 1993). The second change is related to the use of the missing variable

which is a linear transformation of the missing variable in (16). With the latter change, the complete-data are given by and the complete-data likelihood can be written as

Simple algebra yields the following complete-data log-likelihood

| (123) |

where

| (124) |

and

| (125) |

Working on the complete-data log-likelihood in (123) as for the EM, the ECM algorithm iterates between three steps, one E-step and two CM-steps, until convergence. The two CM-steps are obtained by partitioning in the two subsets and . These steps, for the generic iteration of the algorithm, are detailed below.

E-step

CM-step 1

The first CM-step requires the calculation of as the value of that maximizes . The update for is calculated independently by maximizing with respect to , subject to the constraint on this parameter. Simple algebra yields

The updates of , , and are obtained by the maximization of . It is straightforward to realize that these estimates are analogous to those given in Section 4.2 with the only difference that

CM-step 2

In the second CM-step, at the same iteration, is chosen to maximize . Simple algebra yields the closed-form update

Appendix F ECME algorithm for the uniform asymmetric Laplace distribution

To fit the U-AL distribution we use the ECME algorithm. In our case, it iterates between three steps, one E-step and two CM-steps, until convergence. The two CM-steps arise from the partition of as and . From an operational point of view, the only difference with respect to the EM algorithm is the second CM-step, where we directly maximize the (observed-data) log-likelihood function instead of the complete-data one. We detail the three steps, for the generic iteration of the algorithm, below.

E-step

To calculate the expectations involved in the E-step (refer to Section 4.1), we observe that

| (127) |

where

This means that has a doubly-truncated gamma distribution (see, e.g., Coffey & Muller, 2000), on the interval , with shape and rate , whose pdf is given in (127); in symbols

| (128) |

The function arising from (68) is . Thanks to (128) we obtain

CM-step 1

The first CM-step proceeds as the M-step of the EM algorithm, but limited to the update of , , and by maximizing ; refer to Section 4.2.

CM-step 2

The update of is obtained at the second CM-step by maximizing over , namely the observed-data log-likelihood function in (66) with , , and fixed at , , and , respectively.