Simultaneous Estimation and Group Identification for Network Vector Autoregressive Model with Heterogeneous Nodes

Xuening Zhu1, Ganggang Xu2, and Jianqing Fan3,4

1Fudan University, China;

2University of Miami, USA;

3Capital University of Economics and Business, China

4Princeton University, USA

Abstract

Individuals or companies in a large social or financial network often display rather heterogeneous behaviors for various reasons. In this work, we propose a network vector autoregressive model with a latent group structure to model heterogeneous dynamic patterns observed from network nodes, for which group-wise network effects and time-invariant fixed-effects can be naturally incorporated. In our framework, the model parameters and network node memberships can be simultaneously estimated by minimizing a least-squares type objective function. In particular, our theoretical investigation allows the number of latent groups to be over-specified when achieving the estimation consistency of the model parameters and group memberships, which significantly improves the robustness of the proposed approach. When is correctly specified, valid statistical inference can be made for model parameters based on the asymptotic normality of the estimators. A data-driven criterion is developed to consistently identify the true group number for practical use. Extensive simulation studies and two real data examples are used to demonstrate the effectiveness of the proposed methodology.

KEY WORDS: Heterogeneity, Latent group structure, Network autoregressive model, Network time series.

1 Introduction

High dimensional time series harvested from large network platforms such as social networks and financial networks has become increasingly available in recent years. Much research interest has been devoted to model dynamics of the associated network time series. Examples include Sewell and Chen (2015); Zhu et al. (2017, 2019b) and references therein. While abundant literature is available for network time series data, one remaining challenge is how to account for the commonly encountered nodal heterogeneity. For example, in a social network, users with different education or social-economic backgrounds may have rather different posting behaviors and may interact differently with members from other social groups. There has been scarce work on modeling such heterogeneous network effects in the literature, including the spatial autoregression model studied in Dou et al. (2016) and the feature screening of network nodes proposed in Zhu et al. (2019a). However, both works can only model the heterogeneous network effect on an individual node level. In this work, we propose a network autoregression model with a latent group structure (GNAR) for jointly modeling the time series data collected from all potentially heterogeneous network nodes.

Consider a network with nodes indexed by , whose relationships are recorded through an adjacency matrix , where if the th node follows the th node and otherwise. By convention, we set for all . For the th node, we observe a time series of continuous variable, denoted by , together with a set of node specific covariates . In particular, we remark that the first entry of the vector is always , which corresponds to the intercept term. To account for the network heterogeneity, we assume that the network nodes can be clustered into groups with homogenous within-group regression effect and use to denote the group membership of the th node. The GNAR model can be expressed as

| (1.1) |

where with being the out-degree of node , and ’s are independent and identically distributed random noises with a mean and variance . All model parameters as well as the node membership ’s will be estimated.

The key assumption of the GNAR model is that nodes from the same group, say group , share similar characteristics such as the node-specific momentum effect () and covariate-related fixed-effect (). The interactions between nodes from two groups, say , share the same group-level network effect parameter . Such assumptions are reasonable for many popular networks such as social networks. From the estimation point of view, the GNAR model strikes a good balance between the model flexibility and complexity. In the special case with , the GNAR model reduces to the network vector autoregression (NAR) model proposed in Zhu et al. (2017), which may not be flexible enough since it requires homogeneous network effects, momentum effects, and fixed-effects. In the other extreme case with , the GNAR model becomes the classic first-order vector autoregression (VAR) type model with covariates, for which the number of parameters will quickly explode as increases.

Another popular strategy to model high dimensional time series is to impose some structural assumptions on the autoregression coefficient matrix of the VAR model. Examples include assuming that the autoregression coefficient matrix is sparse (Basu et al., 2015; Zhu, 2020; Nicholson et al., 2020) or has a low rank structure (Negahban and Wainwright, 2011; Basu et al., 2019; Wang et al., 2022). However, the aforementioned approaches do not incorporate the observed network structure for the model estimation and therefore can be less efficient when such information is available, which is demonstrated through simulation studies in Section 4.2. In addition, we remark that the model (1.1) assumes that individuals are influenced in a similar way by friends of the same type they follow in a network. Although this assumption is reasonable for sparse networks, it is difficult to hold true in densely connected networks. In such situations, alternative high-dimensional VAR models (e.g., Basu et al., 2019) may be more suitable.

Recently, modeling heterogeneity among individuals by imposing group structures has received considerable attention in panel data literature. For example, Bonhomme and Manresa (2015) considered grouped time-varying fixed effects for linear panel model and Bester and Hansen (2016) demonstrated that grouped individual fixed effects may improve the model estimation. Ando and Bai (2016) introduced grouped factor structure for linear panel data models. Su et al. (2016) proposed a Classifier Lasso (C-Lasso) procedure for simultaneous group identification and parameter estimation of panel data models. Zhang et al. (2019) studied clustering of panel data using quantile regression. More recently, Liu et al. (2020) revisited the estimation and inference for the grouped panel data model with a possibly over-specified number of groups. Similar structures are also used in Fang et al. (2020). As we shall elaborate further, due to the existence of the network structure and the time-invariant covariates in model (1.1), the theoretical investigation of the GNAR model faces additional challenges compared to existing panel data models.

1.1 Comparison to existing works

A simplified version of model (1.1) is considered in Zhu and Pan (2020), where they assume that for any ’s, which is less realistic for network data. We wish to remark that our work is fundamentally different from Zhu and Pan (2020). Firstly, the model in Zhu and Pan (2020) is essentially a finite Gaussian mixture model, for which group membership estimation consistency of network nodes cannot be established. In contrast, our work treats nodal group memberships as parameters that can be consistently estimated. Secondly, the asymptotic normality in Zhu and Pan (2020) is established under the assumption that the true nodal memberships are known while our theory takes into account the potential group membership estimation errors. Thirdly, Zhu and Pan (2020) assumes that the number of latent groups is known. In our work, not only do we allow to be over-specified but also give a data-driven method for consistently choosing . Finally, our much stronger theoretical results are established without imposing restrictive assumptions on the network structure as those in Zhu and Pan (2020); see Conditions 3 and 7 for details. This further significantly expands the applicability of the proposed method.

Our work is also significantly different from the community network autoregression (CNAR) model recently proposed in Chen et al. (2022), where they utilize the concept of “community” that arises from the community detection literature (Rohe et al., 2011; Lei and Rinaldo, 2015). Although the “group” structure in our work appears to share some similarities with “community”, they are fundamentally different. The “community” is typically determined by the connectivities among different network nodes, and the community structure is used to model the generating mechanism of the network structure, and the network structure is assumed to be random in Chen et al. (2022). In contrast, for our GNAR model, the network structure is treated as deterministic over time, which is a reasonable framework for many applications and has been frequently used, see, e.g., Fox et al. (2016); Farajtabar et al. (2017); Zhu et al. (2017, 2019b). Furthermore, unlike the “community” in Chen et al. (2022), the groups of network nodes in our GNAR model are primarily determined by node-specific characteristics, i.e., ’s and ’s. In addition, we consider time invariant covariates instead of time dependent covariates in Chen et al. (2022). Therefore, while modeling network time series data with similar structures, the research focus and theoretical challenges in our work is fundamentally different from those in Chen et al. (2022).

Our theoretical findings appear to have a similar flavor as those in Liu et al. (2020). However, the technical proofs are significantly different, primarily due to the introduction of (1) the network effects ’s, and (2) the time-invariant covariates ’s in model (1.1). Firstly, in Liu et al. (2020), once the model parameters are estimated, the estimated membership does not depend on values of other ’s owning to the independence between different individuals in panel data. However, because of ’s in model (1.1), even when model parameters are given, the estimated will inevitably depend on the estimated memberships of its connected nodes. The interplay between ’s significantly complicated our theoretical investigations compared to those in Liu et al. (2020). Secondly, for panel data considered in Liu et al. (2020), all model parameters related to an individual can be consistently estimated by using only the time series data from the th individual given a sufficiently large . However, this is not the case when we have time-invariant covariates ’s, in which case the fixed effects ’s can only be consistently estimated by pooling data from all nodes in Group . This is especially difficult since the true group memberships are unknown. To address these two challenges, we developed a new set of technical tools in the proof. As a result, although our Theorem 1 only establishes convergence rates in probability, which is weaker than the almost sure convergence obtained in Liu et al. (2020), it does provide more insights on how the network structure impacts the convergence rates. To establish asymptotic normality, we also proposed a refinement algorithm for the estimated group memberships that is not needed in Liu et al. (2020).

1.2 Main Contributions and Organization

The main contributions of our work can be summarized as follows. First, we propose a highly interpretable GNAR model that is suitable for modeling multivariate time series observed on a network with heterogeneous nodes. Second, we give detailed conditions under which both model parameters and node memberships in the GNAR model can be consistently estimated, even if the number of groups is over-specified. Third, we propose an information criterion that can consistently choose the true number of groups when . Lastly, we show that, under suitable conditions, if the number of groups is correctly specified, the estimated model parameters converge to a multivariate normal distribution at a convergence rate of , which enables valid statistical inference based on the proposed GNAR model.

The rest of the paper is organized as follows. Section 2 gives details on the proposed methodology including model description, computational algorithm, and sufficient conditions to establish estimation consistency when the number of latent groups is over-specified. Section 3 establishes the asymptotic normality of the model parameter estimators when is correctly specified. Extensive simulation studies are conducted in Section 4 and real data applications are given in Section 5. Details on the initialization of the proposed algorithm is given in the Appendix. All technical proofs and additional simulation studies are collected in the supplementary material.

Notations. Denote by the identity matrix with dimension. Define and . For an arbitrary vector , denote the -norm as and -norm as . For any set , denote as its cardinality. Finally, denotes the Frobenius norm of matrix .

2 Model Estimation

For a given number of groups , denote the membership vector as . Define with , and with for . Correspondingly, the true parameters are defined as , , and with , where is the true number of groups. The membership vector as well as parameters and can be estimated by minimizing the following quadratic loss function

| (2.1) |

where , for If is known, the optimization of with respect to and is convex and has a closed-form solution. However, we need to estimate jointly with other parameters, which makes the optimization of (2.1) non-convex. In the next subsection, we give an iterative algorithm to minimize (2.1).

2.1 An Optimization Algorithm

Note that the loss function (2.1) can be written as

| (2.2) |

where the vector with and for any . It is straightforward to see that ’s can be estimated separately when is given. Specifically, let and be the design matrix and the response vector obtained by stacking all ’s and ’s with and , respectively. Then for a given , the minimizer of is of the following form

| (2.3) |

Based on (2.1) and (2.3), we propose the following iterative algorithm to minimize with rerespect to and jointly.

-

(a)

Obtain an initial membership estimator using the -means algorithm given in the Appendix. Use and (2.3) to find initial estimators and .

-

(b)

Update group memberships: in the th iteration, update each entry of sequentially, where is the membership estimator in the th step. Specifically, the group membership of node is updated by

(2.4) where , Repeat (2.4) for until no change can be made for .

-

(c)

Update the parameter estimates: fix the group membership , and obtain the updated parameter estimates and using (2.3).

-

(d)

Repeat (b)–(c) until the convergence criterion is met.

The above optimization algorithm is a -means type algorithm which consists of two major steps. The first step is that we update the group memberships given the model parameters. The second step is that we update the model parameters given the group memberships. The algorithm framework is adopted by several group panel data models in recent literature (Ando and Bai, 2016, 2017; Zhang et al., 2019; Liu et al., 2020). The main difference between our algorithm and the other approaches mainly lies in the first step due to introducing the network structure. Specifically, in the first step, when updating , we need to fix group memberships of all nodes that follow the node due to the existence of the network effect parameters ’s in (2.1). On the contrary, in classical group panel data models, one can update the group membership separately for since the independence is typically assumed among the individuals. For a given initial membership estimator , the above algorithm converges rather fast. However, since is non-convex, it is important to search the solution with multiple initial values to escape from local minimums. In the Appendix, we propose an algorithm to search for multiple ’s using a set of -means algorithms, which works sufficiently well for all our numerical examples. We prove that the algorithm can attain local convergence, where the details are given in Appendix LABEL:appen:local_conv in the supplementary material.

2.2 Conditions for Estimation Consistency

The GNAR model (1.1) can be written in a vector form as following

| (2.5) |

where , , , and is an matrix whose th entry is for and for . We next give sufficient conditions for estimation consistency.

Suppose that the true number of latent groups is and the true group memberships are given by with . For each node , we denote as the set of the nodes that the node follows.

Condition 1.

(Distribution) Assume that , , are independent identically distributed (i.i.d.) zero-mean sub-Gaussian random variables with a scale factor , that is for any . Assume that ’s are fixed covariates satisfying .

Condition 2.

(True Parameters) Assume that (a) ; (b) there exists a constant such that .

Condition 3.

(Network Structure A) For any , define proportions and . Assume that there exist and such that and as , and that there exists a constant such that .

Condition 1 assumes that the innovations follow a sub-Gaussian distribution, which is commonly used in high dimensional data analysis (Wang et al., 2013; Lugosi and Mendelson, 2019; Fan et al., 2021). Condition 2 (a) is a mild sufficient condition to ensure the stationarity of the vector autoregression model (2.5), which is similar to the stationarity condition of Zhu et al. (2017). Condition 2 (b) requires that true parameters from different latent groups are sufficiently apart from each other, as similarly required by Liu et al. (2020). Condition 3 assumes that there are sufficiently number of nodes in each latent group, which is needed for consistent estimation of ’s and ’s. It also poses assumptions on the network structure, which basically requires that there are sufficient number of connected edges between any two groups to ensure consistent estimation of network effect parameters for . In addition, we provide local convergence result of the proposed numerical algorithm. The details are given in Appendix LABEL:appen:local_conv.

Condition 4.

(Parameter Space) Assume that there exists a constant such that .

Condition 5.

(Fixed-effect Identifiability) Let for . For any subset with , it holds as , where and are positive constants.

Condition 4 assumes that the parameter space is compact, which is a standard condition in statistical theory. Condition 5 is a sufficient condition for the identifiability of fixed-effect parameters , . It asserts that a sufficiently large set of nodes (i.e., greater than ) from any true group should contain sufficient information to uniquely identify the corresponding fixed-effect vector . Note that Condition 5 trivially holds if there is only an intercept term in the fixed-effect, in which case for any . In particular, when , our theory still holds with .

As we shall show in the next subsection, the convergence rate of model parameters is consequently affected by the value of .

2.3 Estimation Consistency with an Over-specified

We now establish the estimation consistency when . Denote be the minimizer of (2.1) with . To this end, we define the estimated groups as for and a mapping as

| (2.6) |

In other words, gives the true membership of majority of nodes being assigned to for any . The membership error rate can be consequently defined as

| (2.7) |

We remark that gives the percentage of the nodes that are majority in all estimated groups, which is commonly referred to as the clustering purity (Schütze et al., 2008).

Denote by and as the average and maximum of the out-degree of all network nodes. For a given , we define the following quantity

| (2.8) |

It readily follows that . For a sufficiently large , (2.8) implies that only a small fraction of nodes can follow more than network nodes. In this sense, serves as a measure of the network connectivity upper bound for a given to ensure estimation consistency, and it is involved in the consistency result as stated in the following Theorem.

Theorem 1.

The proof is given in the supplementary material.

Theorem 1 (a) asserts that the fraction of network nodes that are assigned to an incorrect group approaches as , In particular, ignoring the term, the rate of convergence in part (a) is mainly controlled by rather than . This is consistent with our observations in the simulation study, where an increase in results in a large reduction in while a larger only yields a marginal decrease or even an increase of . The convergence rates given in Theorem 1 (b)–(c) are of the same form, suggesting that to compensate for the impacts of network effects as well as the network dependence structure, one needs a larger by a factor of (assuming ) to ensure estimation consistency compared to the case when all nodes are isolated without any followers. Consequently, the result is different from existing results from the panel data literature when the individuals are typically treated as independent such as Liu et al. (2020). Particularly, the network structure related quantities (i.e., ) are not incorporated. Moreover, compared to the network data setting considered by Zhu and Pan (2020), we remark that while our theoretical results are more sophisticated, our theory imposes much fewer restrictions on the network structure, see Conditions 3 and 7 for details.

2.4 Consistent Selection of

Although the consistency results in Theorem 1 can apply to any , it is still of practical interest to identify the true value of since a smaller can improve the model interpretability and estimation accuracy. In particular, as we will show in Section 3, valid statistical inference can be performed if is consistently identified. This motivates us to design a data-driven selection criterion for .

With a slight abuse of notations, denote as the estimated model parameters and group memberships when the number of groups is specified as . The optimal is chosen by minimizing the following group information criterion (GIC)

| (2.9) |

where is a tuning parameter. In the following theorem, we show that if is appropriately chosen, the GIC can identify the true number of groups consistently.

Theorem 2.

The proof is given in the supplementary material.

The GIC is designed in the similar fashion of the BIC in the model selection literature (Chen and Chen, 2008; Zou and Zhang, 2009; Wang et al., 2013). Some discussion on the condition is in order. In our proof of Theorem 2, we manage to show that if , one has that for some constant . In panel data models, it is typically true that for some constant if , see, e.g., Liu et al. (2020). The difference is due to the existence of the network effects ’s in (2.1), in which case the bias caused by the smaller parameter space (due to a smaller ) is offset by the extra flexibility arising from the network effects, leading to the extra term in . As a result, we require in contrast to suggested in, e.g., Liu et al. (2020).

3 Model Inference

We next investigate the asymptotic distribution of the model parameter estimators. Compared to Section 2, we need to further assume as in Liu et al. (2020) and the following additional identifiability condition to Condition 2.

Condition 6.

(Group Identifiability) There exists a positive constant such that .

Condition 7.

(Network Structure B) For any , there exist a constant such that .

Condition 6 requires that two latent groups either have different momentum effect parameters, i.e., ’s, or different fixed-effect parameters, i.e., ’s, that can separate any two nodes in the network. Recall that we require that always includes the intercept term. Specifically, if (i.e., for ), Condition 6 reduces to . In more general cases, it is slightly more restrictive than the Condition 2 but still reasonable for many applications. Condition 7 is a slightly more restrictive condition on the network structure than Condition 3, which is the price to pay to achieve the asymptotic normality of parameter estimators. It implies that the number of nodes with bounded out-degrees should be of the order , suggesting that the network density should not be too high. Our Lemma LABEL:lem:Sig_g_lowerbound in the supplement also shows that Condition 7 ensures all diagonal elements of the matrix in Theorem 4 to be greater than a constant , which is necessary for to be strictly positive definite as assumed. Compared to the network structure conditions of Zhu and Pan (2020), both Conditions 3 and 7 are much simpler and more transparent.

3.1 Membership Refinement

To establish the asymptotic normality, we further propose an algorithm to refine the estimated group memberships. Denote by the group memberships of the nodes that the node follows and , for . Then the loss function corresponding to the node , i.e., in (2.1), can also be written as a function of and , denoted by . Note that does not only depend on its own membership but also memberships of its neighbors . As a result, the minimizer of the loss function (2.1), denoted as , does not necessarily minimize each , which creates a hurdle for analyzing the asymptotic distribution of . To circumvent this difficulty, we propose a refinement of the estimated memberships using an approximate node-specific profile loss function. Specifically, let with ’s being the corresponding entries in obtained from minimizing (2.1). Given , is the collection of all possible estimated network effects between the node and the nodes it follows (i.e., ), obtained by exhausting membership assignments to nodes and nodes in . The approximate node-specific profile loss function of is defined as

The definition of eliminates the impacts of membership estimates for nodes in when determining , which facilitates our technical proofs. Define the optimal , and if is much smaller than , then we have reason to switch from the original estimated membership to . Consequently, we define the refined estimated membership as following

| (3.1) |

Intuitively, (3.1) asserts that one should only switch the membership from to if the reduction of the loss at the node is more than of the minimum possible profile loss. We shall show in the next subsection that such a refinement strategy ensures the asymptotic normality of the resulting parameter estimators.

Remark 1.

Our simulation study in Section 4.1 shows that the refined estimator performs slightly worse than the unrefined estimator in most case scenarios, although the differences are rather small. Given this observation, we wish to remark that the membership refinement algorithm serves as more of a device that facilitates our theoretical investigations and can be skipped in the practical use of the proposed method.

3.2 Asymptotic Normality

In this section, we establish asymptotic normality for model parameter estimators when . The first challenge is to obtain a stronger convergence result for the membership mis-classification rate than Theorem 1 (a). Denote by the refined estimated memberships using (3.1), and , as the estimated clusters. The following Theorem gives the uniform consistency of the parameter estimators as well as the group membership estimators.

Theorem 3.

The proof is given in the supplementary material.

Theorem 3 can be viewed as an enhanced version of Theorem 1 for the special case with , which states that under some regularity conditions, all group memberships can be correctly estimated (subject to a label permutation) with a probability tending to as . Similar results have also been established in the panel data literature (e.g., Liu et al., 2020). However, similar to Theorem 1, special care must be paid to the network structure in our work by considering the network structure related factors as and .

Making use of Theorem 3 (b), the following Theorem establishes the asymptotic normality of model parameter estimators when .

Theorem 4.

Let be defined by (2.3) with the refined membership and be the corresponding true parameter vector (after an appropriate label permutation). Define with as in (2.3) by plugging in the true membership . Assume that , Conditions in Theorem 3 hold, and that is strictly positive definite. Then, it holds that

where .

The proof is given in the supplementary material.

Theorem 4 states that for each , is consistent for with an asymptotic covariance matrix given by . The asymptotic covariance is the same as the oracle estimator (2.3) which knows the group membership in advance. In practice, we can estimate using the refined memberships . Specifically, we use , where and . In addition, we estimate by . By Condition 3, we have that , which suggests that diverges in the same order of . Theorem 4 enables us to conduct valid statistical inference for model parameters, including the momentum effects (’s), the network effects (’s), and the fixed-effects (’s). which is supported by the numerical results given in Section 4.

4 Simulation Studies

To demonstrate the finite sample performance of the proposed method, we conduct a number of simulation studies with different network structures and parameter settings using model (1.1). For all settings, the time-invariant covariate ’s are independently generated from a multivariate normal distribution with . The innovation term ’s are independently sampled from . For each network structure, we consider two settings with and , and sample the memberships of the network nodes from multinomial distribution with a for and for respectively. We consider two network structures.

1. Stochastic Block Model (SBM). For this network structure, the nodes are partitioned into communities. If nodes and belong to the same community, the chance of them being connected is set as , otherwise the chance reduces to . This corresponds to the challenging case where the exact recovery of the communities are not possible (Abbe et al., 2020). For different network sizes , we set respectively.

2. Power-Law Distribution Network. In this network, the node in-degrees () follow a power-law distribution, which is suitable for social networks where the majority of nodes have few followers but a small percent of nodes have a large number of followers. Following Clauset et al. (2009), we generate the network structure as follows. First, for each node , we generate by and set the in-degree of the node as . Next, for the th node, we randomly pick nodes as its followers.

| 1 | 2 | 3 | - | - | - | 1 | 2 | 3 | - | - | - | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 0.3 | -0.2 | - | 0.4 | -0.8 | 0.8 | 0.15 | 0.2 | -0.1 | 0.2 | -1.2 | 0.4 |

| 2 | 0.1 | 0.3 | - | 0.6 | -0.32 | 1.2 | 0.1 | 0.3 | -0.2 | 0.4 | -0.8 | 0.8 |

| 3 | - | - | - | - | - | - | 0.15 | 0.1 | 0.3 | 0.6 | -0.32 | 1.2 |

For each of the two network structures, the performances of the proposed method are evaluated under three parameter settings. In Scenario 1, we specify the true parameters as in Table 1 respectively for and . In Scenario 2, we set , in which case the groups only differ in network effect parameters ’s and fixed-effect parameters ’s. Lastly, in Scenario 3, we set and groups only differ in network effect parameters ’s and momentum parameters ’s.

4.1 Estimation and Inference when

When , we consider both of the unrefined and refined estimators. Denote the estimates obtained from the proposed algorithm as , , and for the th simulation run and let , , and be the corresponding estimates after the refinement. The group membership estimation error rate is computed as , where is obtained by applying definition (2.7) to the th simulation run. The estimation accuracy can be directly measured by the root mean squared error (RMSE) of , , and after a suitable label permutation. For example, for , the RMSE is defined as RMSE. To evaluate the performance of statistical inference using Theorem 4, we construct confidence interval for each model parameter based on the refined estimates. Taking as an example, in the th simulation run, we construct confidence interval for as CI, where is the estimated asymptotic standard error based on Theorem 4. The average error in coverage probability (AEcp) for all components in is then calculated as AE. The AEcp’s for and are similarly defined. Finally, for a direct comparison, we compute the same measures for the oracle estimators obtained when the true group memberships are known, denoted as , , and .

| Oracle Estimator | GNAR without Refinement | GNAR with Refinement | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 100 | 3.94 (0.45) | 1.61 (1.50) | 4.93 (1.85) | 4.20 (1.20) | 1.67 (2.30) | 5.10 (2.45) | 2.90 | 4.20 (1.20) | 1.67 (2.30) | 5.10 (2.45) | 2.90 | |

| 200 | 2.76 (0.45) | 1.14 (1.10) | 3.45 (1.20) | 2.84 (0.85) | 1.17 (1.50) | 3.52 (1.70) | 0.86 | 2.84 (0.85) | 1.17 (1.50) | 3.52 (1.70) | 0.86 | ||

| 300 | 2.24 (1.30) | 0.90 (1.10) | 2.77 (0.60) | 2.26 (1.35) | 0.92 (0.90) | 2.81 (0.85) | 0.31 | 2.26 (1.35) | 0.92 (0.90) | 2.81 (0.85) | 0.31 | ||

| 2 | 200 | 100 | 2.33 (0.60) | 1.06 (1.20) | 3.30 (0.65) | 2.48 (1.40) | 1.09 (0.70) | 3.35 (0.80) | 2.28 | 2.47 (1.40) | 1.09 (0.70) | 3.35 (0.80) | 2.28 |

| 200 | 1.63 (0.75) | 0.72 (2.20) | 2.29 (1.00) | 1.66 (0.65) | 0.75 (1.50) | 2.32 (0.35) | 0.62 | 1.66 (0.65) | 0.75 (1.50) | 2.32 (0.35) | 0.62 | ||

| 300 | 1.32 (1.00) | 0.62 (0.50) | 1.91 (0.70) | 1.32 (0.75) | 0.63 (0.40) | 1.93 (0.80) | 0.22 | 1.32 (0.75) | 0.63 (0.40) | 1.93 (0.80) | 0.22 | ||

| 300 | 100 | 2.01 (0.60) | 0.85 (1.10) | 2.69 (1.60) | 2.10 (1.95) | 0.90 (0.90) | 2.78 (1.30) | 2.51 | 2.10 (1.95) | 0.90 (0.90) | 2.78 (1.30) | 2.51 | |

| 200 | 1.38 (0.85) | 0.60 (1.30) | 1.89 (0.70) | 1.40 (0.85) | 0.61 (1.10) | 1.90 (0.65) | 0.74 | 1.40 (0.85) | 0.61 (1.10) | 1.90 (0.65) | 0.75 | ||

| 300 | 1.12 (0.45) | 0.48 (0.80) | 1.52 (0.80) | 1.13 (0.50) | 0.49 (0.50) | 1.52 (0.90) | 0.26 | 1.13 (0.50) | 0.49 (0.50) | 1.52 (0.90) | 0.26 | ||

| 100 | 100 | 12.87 (0.60) | 2.77 (0.53) | 7.38 (0.80) | 15.07 (3.00) | 2.98 (1.73) | 8.07 (1.57) | 3.08 | 15.50 (3.98) | 3.04 (2.33) | 8.21 (1.97) | 3.28 | |

| 200 | 8.99 (0.96) | 1.93 (1.27) | 5.18 (0.77) | 9.35 (1.02) | 1.98 (1.47) | 5.34 (1.00) | 0.78 | 9.41 (1.11) | 1.98 (1.40) | 5.38 (1.00) | 0.82 | ||

| 300 | 7.52 (0.69) | 1.52 (0.53) | 4.18 (0.90) | 7.61 (0.69) | 1.55 (0.87) | 4.23 (0.97) | 0.27 | 7.63 (0.71) | 1.55 (0.87) | 4.24 (0.97) | 0.28 | ||

| 3 | 200 | 100 | 6.93 (0.64) | 1.84 (0.53) | 4.92 (0.83) | 7.83 (3.09) | 1.95 (1.27) | 5.16 (1.37) | 2.92 | 8.17 (4.33) | 2.03 (3.20) | 5.32 (1.97) | 3.19 |

| 200 | 4.73 (0.40) | 1.27 (0.73) | 3.45 (0.50) | 4.92 (0.73) | 1.30 (0.47) | 3.52 (0.87) | 0.77 | 4.96 (0.93) | 1.31 (0.87) | 3.53 (1.03) | 0.83 | ||

| 300 | 3.89 (0.53) | 1.08 (0.47) | 2.90 (0.87) | 3.95 (0.40) | 1.09 (1.00) | 2.92 (0.87) | 0.30 | 3.96 (0.38) | 1.09 (1.00) | 2.92 (0.90) | 0.30 | ||

| 300 | 100 | 5.37 (1.11) | 1.42 (0.40) | 3.87 (1.10) | 5.93 (1.89) | 1.51 (0.40) | 4.10 (1.03) | 2.90 | 6.16 (3.51) | 1.69 (3.73) | 4.37 (2.67) | 3.21 | |

| 200 | 3.85 (0.60) | 1.02 (0.93) | 2.77 (0.60) | 3.94 (0.93) | 1.05 (0.67) | 2.84 (0.77) | 0.78 | 3.98 (1.40) | 1.07 (1.00) | 2.87 (0.93) | 0.82 | ||

| 300 | 3.13 (0.80) | 0.83 (0.53) | 2.25 (0.63) | 3.16 (0.84) | 0.85 (0.33) | 2.27 (0.77) | 0.27 | 3.17 (0.87) | 0.85 (0.33) | 2.28 (0.67) | 0.28 | ||

| Oracle Estimator | GNAR without Refinement | GNAR with Refinement | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 100 | 4.27 (0.90) | 1.62 (0.40) | 4.44 (0.50) | 6.09 (10.10) | 2.20 (11.00) | 5.90 (8.55) | 10.32 | 6.09 (10.10) | 2.20 (11.00) | 5.90 (8.55) | 10.32 | |

| 200 | 3.07 (0.60) | 1.20 (0.30) | 3.18 (0.55) | 3.88 (5.80) | 1.40 (4.30) | 3.61 (3.65) | 6.35 | 3.88 (5.80) | 1.40 (4.30) | 3.61 (3.65) | 6.35 | ||

| 300 | 2.55 (0.50) | 0.96 (0.40) | 2.57 (1.00) | 3.05 (5.45) | 1.12 (4.30) | 3.41 (3.55) | 5.26 | 3.05 (5.45) | 1.12 (4.30) | 3.41 (3.55) | 5.26 | ||

| 2 | 200 | 100 | 2.74 (0.85) | 1.17 (0.30) | 3.08 (0.25) | 3.91 (12.15) | 1.59 (10.00) | 4.04 (7.25) | 10.55 | 3.90 (12.10) | 1.59 (10.10) | 4.04 (7.30) | 10.55 |

| 200 | 1.91 (0.50) | 0.82 (0.40) | 2.17 (0.55) | 2.30 (6.65) | 0.91 (3.10) | 2.41 (2.50) | 6.41 | 2.30 (6.65) | 0.91 (3.10) | 2.41 (2.50) | 6.41 | ||

| 300 | 1.58 (0.80) | 0.67 (0.50) | 1.77 (0.45) | 1.74 (2.75) | 0.73 (3.40) | 1.89 (2.45) | 4.62 | 1.74 (2.75) | 0.73 (3.40) | 1.89 (2.45) | 4.62 | ||

| 300 | 100 | 2.23 (1.00) | 0.93 (0.80) | 2.49 (1.00) | 3.37 (12.25) | 1.30 (10.50) | 3.41 (7.20) | 9.72 | 3.37 (12.25) | 1.30 (10.50) | 3.41 (7.25) | 9.72 | |

| 200 | 1.60 (0.60) | 0.65 (0.70) | 1.72 (0.70) | 2.12 (7.15) | 0.82 (4.60) | 2.38 (3.15) | 6.50 | 2.12 (7.10) | 0.82 (4.60) | 2.38 (3.15) | 6.50 | ||

| 300 | 1.32 (0.50) | 0.53 (0.50) | 1.40 (0.90) | 1.70 (6.85) | 0.67 (3.70) | 2.21 (3.35) | 5.26 | 1.70 (6.85) | 0.67 (3.70) | 2.21 (3.35) | 5.26 | ||

| 100 | 100 | 12.21 (0.84) | 2.62 (0.53) | 7.40 (0.70) | 29.41 (22.38) | 3.91 (10.87) | 17.49 (15.43) | 15.16 | 29.22 (22.53) | 3.95 (10.93) | 17.47 (15.77) | 15.21 | |

| 200 | 8.59 (0.51) | 1.93 (0.73) | 5.32 (0.70) | 17.06 (14.31) | 2.43 (5.40) | 10.08 (8.87) | 8.22 | 16.95 (14.13) | 2.45 (5.73) | 10.06 (8.83) | 8.21 | ||

| 300 | 7.07 (1.00) | 1.58 (0.93) | 4.44 (1.73) | 11.85 (9.62) | 1.81 (3.67) | 7.00 (6.73) | 5.26 | 11.82 (9.51) | 1.83 (3.80) | 6.93 (6.57) | 5.22 | ||

| 3 | 200 | 100 | 6.53 (0.71) | 1.85 (0.53) | 4.88 (0.43) | 10.98 (15.33) | 2.59 (11.13) | 7.19 (9.27) | 11.51 | 11.16 (16.29) | 2.61 (11.47) | 7.23 (9.83) | 11.63 |

| 200 | 4.65 (0.71) | 1.31 (1.40) | 3.46 (0.70) | 6.16 (7.18) | 1.45 (2.73) | 4.03 (3.63) | 5.26 | 6.23 (7.44) | 1.45 (3.20) | 4.04 (3.57) | 5.29 | ||

| 300 | 3.82 (0.82) | 1.06 (0.47) | 2.77 (0.77) | 4.70 (5.80) | 1.12 (1.80) | 3.19 (2.30) | 3.35 | 4.71 (5.78) | 1.13 (1.73) | 3.19 (2.33) | 3.34 | ||

| 300 | 100 | 5.30 (0.87) | 1.45 (0.93) | 3.97 (0.73) | 8.18 (13.62) | 2.01 (9.53) | 5.67 (8.37) | 10.39 | 8.28 (13.93) | 2.03 (9.47) | 5.74 (8.63) | 10.53 | |

| 200 | 3.72 (0.56) | 1.01 (0.53) | 2.77 (0.83) | 4.90 (7.96) | 1.19 (3.53) | 3.84 (4.37) | 5.72 | 4.94 (8.22) | 1.20 (3.67) | 3.87 (4.80) | 5.74 | ||

| 300 | 3.05 (0.67) | 0.82 (0.87) | 2.26 (0.80) | 3.66 (4.49) | 0.93 (2.67) | 2.93 (2.97) | 3.71 | 3.70 (4.87) | 0.94 (2.87) | 2.93 (2.87) | 3.70 | ||

| Oracle Estimator | GNAR without Refinement | GNAR with Refinement | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 100 | 7.59 (0.60) | 1.63 (0.60) | 2.81 (0.75) | 11.47 (13.80) | 2.28 (13.30) | 3.47 (5.80) | 13.45 | 11.47 (13.80) | 2.28 (13.30) | 3.47 (5.80) | 13.45 | |

| 200 | 5.51 (1.40) | 1.10 (0.60) | 2.00 (0.75) | 6.34 (4.20) | 1.31 (5.60) | 2.15 (1.90) | 5.23 | 6.34 (4.20) | 1.31 (5.60) | 2.15 (1.90) | 5.23 | ||

| 300 | 4.52 (0.55) | 0.92 (0.30) | 1.60 (0.80) | 4.83 (1.10) | 0.99 (2.10) | 1.65 (1.25) | 2.21 | 4.83 (1.10) | 0.99 (2.10) | 1.65 (1.25) | 2.21 | ||

| 2 | 200 | 100 | 5.18 (0.50) | 1.08 (1.20) | 1.96 (0.40) | 7.86 (14.20) | 1.89 (20.90) | 2.43 (6.25) | 12.80 | 7.86 (14.20) | 1.89 (20.90) | 2.43 (6.25) | 12.80 |

| 200 | 3.65 (1.15) | 0.75 (0.50) | 1.36 (0.70) | 4.24 (4.00) | 0.92 (5.30) | 1.45 (2.15) | 5.12 | 4.24 (4.00) | 0.92 (5.30) | 1.45 (2.15) | 5.12 | ||

| 300 | 2.97 (0.95) | 0.61 (0.90) | 1.13 (0.90) | 3.16 (1.30) | 0.65 (2.20) | 1.16 (1.35) | 2.18 | 3.16 (1.30) | 0.65 (2.20) | 1.16 (1.35) | 2.18 | ||

| 300 | 100 | 4.30 (0.65) | 0.87 (0.80) | 1.56 (0.80) | 6.60 (15.75) | 1.72 (25.50) | 1.95 (6.15) | 12.78 | 6.60 (15.75) | 1.72 (25.50) | 1.95 (6.15) | 12.78 | |

| 200 | 3.05 (1.10) | 0.63 (0.90) | 1.09 (0.65) | 3.51 (4.75) | 0.78 (6.20) | 1.18 (1.60) | 4.97 | 3.51 (4.75) | 0.78 (6.20) | 1.18 (1.60) | 4.97 | ||

| 300 | 2.46 (0.55) | 0.50 (0.30) | 0.90 (0.70) | 2.57 (1.35) | 0.55 (1.60) | 0.93 (0.70) | 2.08 | 2.57 (1.35) | 0.55 (1.60) | 0.93 (0.70) | 2.08 | ||

| 100 | 100 | 21.24 (0.67) | 2.76 (0.27) | 4.76 (0.90) | 42.53 (23.29) | 6.62 (26.60) | 6.50 (9.17) | 18.64 | 42.18 (23.04) | 6.62 (26.73) | 6.50 (9.20) | 18.70 | |

| 200 | 15.08 (0.89) | 1.88 (0.27) | 3.32 (0.40) | 18.83 (4.42) | 2.42 (6.93) | 3.66 (2.13) | 4.56 | 18.85 (4.44) | 2.42 (6.87) | 3.66 (2.17) | 4.58 | ||

| 300 | 12.41 (0.67) | 1.55 (0.53) | 2.74 (0.80) | 13.49 (1.71) | 1.74 (2.80) | 2.84 (1.17) | 1.76 | 13.50 (1.73) | 1.74 (2.80) | 2.84 (1.17) | 1.77 | ||

| 3 | 200 | 100 | 13.69 (0.73) | 1.82 (0.73) | 3.03 (0.80) | 23.95 (18.44) | 3.33 (20.00) | 4.09 (8.70) | 14.71 | 23.75 (17.93) | 3.32 (19.93) | 4.10 (8.70) | 14.78 |

| 200 | 9.60 (0.76) | 1.27 (0.20) | 2.14 (0.77) | 11.39 (3.80) | 1.58 (6.07) | 2.32 (1.83) | 4.73 | 11.37 (3.84) | 1.59 (6.07) | 2.33 (1.87) | 4.75 | ||

| 300 | 7.81 (0.69) | 1.06 (1.13) | 1.79 (1.00) | 8.38 (1.31) | 1.15 (2.33) | 1.84 (1.50) | 1.89 | 8.38 (1.31) | 1.15 (2.33) | 1.84 (1.53) | 1.89 | ||

| 300 | 100 | 10.71 (0.42) | 1.49 (0.87) | 2.46 (0.83) | 18.33 (17.89) | 2.62 (18.47) | 3.31 (8.63) | 13.93 | 18.13 (17.29) | 2.61 (18.73) | 3.32 (8.83) | 13.99 | |

| 200 | 7.57 (0.60) | 1.09 (1.80) | 1.77 (0.53) | 8.92 (3.71) | 1.34 (6.73) | 1.94 (2.17) | 4.55 | 8.91 (3.69) | 1.34 (6.80) | 1.94 (2.17) | 4.56 | ||

| 300 | 6.15 (1.13) | 0.87 (0.53) | 1.44 (0.70) | 6.52 (1.67) | 0.96 (3.13) | 1.49 (1.10) | 1.87 | 6.52 (1.69) | 0.96 (3.20) | 1.49 (1.13) | 1.87 | ||

Summary statistics based on simulation runs are given in Tables 3–4 for the SBM network. Simulation results for the power-law network yield rather similar conclusions and are given in the supplementary material. First, Tables 3–4 suggest that as either or increases, the parameter estimation accuracy consistently improves and approaches the estimation accuracy of the oracle estimators. However, the group membership estimation error rate only gains a significant reduction when increases, which is consistent with our theoretical findings in Theorem 1 (a). As increases, the overall performance of the proposed method is much better with a than , which is as expected. Second, we can see that in Scenarios 2-3, the ’s are much higher compared to those of Scenario 1 because group separations are much greater in Scenario 1. The important message from Scenarios 2-3 is that even if two groups only differ in either momentum parameters or fixed-effect parameters, they can be consistently separated using the proposed method given large enough and .

Finally, the differences between the unrefined and refined estimators appear to be rather small. In particular, when , no membership switch was executed based on Algorithm (3.1) since the clustering is relatively easier in this case. When , the refined memberships appear to have slightly higher clustering errors in most case scenarios with only a few exceptions. Nevertheless, in all case scenarios, the AEcp values are rather small for both unrefined and refined estimators, suggesting that all confidence intervals have right nominal coverage probability when and are large. We can observe that the performances of the proposed estimators gradually approach those of the oracle estimators as and increase. This leads to further supports our theoretical findings in Theorem 4.

4.2 Estimation and Group Selection when

In this section, we evaluate the performance of the proposed method when the number of groups is mis-specified. The true number of groups is fixed at . Under this case, to measure the estimation accuracy, we use the following criteria. For the estimation of and , we define RMSE and RMSE. For , we define RMSE, which evaluates the estimation accuracy of the autoregression matrix defined in model (2.5). Furthermore, we also evaluate the selection accuracy for number of groups using the GIC criterion proposed in (2.9), for which we set the tuning parameter as , where is the 90% quantile of nodal out-degrees . We compute the model selection rate (MSR) as MSR, for any given , where denotes the selected number of groups with the GIC in the th simulation run. Specifically, MSR(3) corresponds to the percentage that the GIC correctly identifies the true group number .

For comparisons, we investigate the performances of several existing methods on the data generated from our model (1.1), including the sparse VAR model by Basu et al. (2015), and the grouped network autoregression model by Zhu and Pan (2020). For the sparse VAR model, we use the fitVAR function in the R package sparsevar. However, since the sparse VAR model in Basu et al. (2015) does not include time-invariant covariates as the model (1.1), we apply the method proposed in Basu et al. (2015) to centered time series () to eliminate the impacts of ’s, and focus on the estimation of and . For the grouped network autoregression model proposed in Zhu and Pan (2020), we implement both the EM algorithm (EM) and the two-step estimation method (TS), for which we set . Summary statistics based on simulation runs are given in Table 5.

| Scenario 1 | Scenario 2 | Scenario 3 | |||||||||||||||

| Method | MSR | MSR | MSR | ||||||||||||||

| (RMSE) | (%) | (RMSE) | (%) | (RMSE) | (%) | ||||||||||||

| 100 | 200 | Oracle | 0.84 | 0.85 | 2.57 | - | - | 0.88 | 0.90 | 2.50 | - | - | 1.58 | 0.84 | 1.54 | - | - |

| GNAR-2 | 3.72 | 6.32 | 21.29 | 0.0 | 26.0 | 2.60 | 5.35 | 1.25 | 50.8 | 23.4 | 4.70 | 4.00 | 22.90 | 0.0 | 28.5 | ||

| GNAR-3 | 0.92 | 0.95 | 2.87 | 100.0 | 0.5 | 2.28 | 1.76 | 1.66 | 49.2 | 4.3 | 1.58 | 0.99 | 5.44 | 96.8 | 4.3 | ||

| GNAR-4 | 1.87 | 1.97 | 6.20 | 0.0 | 0.7 | 4.18 | 2.74 | 2.50 | 0.0 | 4.6 | 2.93 | 1.62 | 9.10 | 3.2 | 6.5 | ||

| GNAR-5 | 2.70 | 2.68 | 8.54 | 0.0 | 1.2 | 5.33 | 3.55 | 2.97 | 0.0 | 6.1 | 4.13 | 2.17 | 13.63 | 0.0 | 9.6 | ||

| GNAR- | 0.92 | 0.95 | 2.87 | - | - | 2.44 | 3.58 | 1.45 | - | - | 1.62 | 1.01 | 5.56 | - | - | ||

| EM(G=3) | 11.19 | 3.21 | 12.12 | - | 6.7 | 10.19 | 3.14 | 2.48 | - | 7.9 | 9.45 | 1.60 | 20.85 | - | 20.7 | ||

| TS (G=3) | 9.70 | 14.19 | 37.63 | - | 22.5 | 10.52 | 6.04 | 2.48 | - | 22.3 | 8.56 | 20.04 | 59.73 | - | 40.2 | ||

| SparseVAR(1) | 12.03 | 14.93 | - | - | - | 11.96 | 14.92 | - | - | - | 12.12 | 15.15 | - | - | - | ||

| 100 | 300 | Oracle | 0.68 | 0.67 | 2.07 | - | - | 0.71 | 0.73 | 2.04 | - | - | 1.30 | 0.69 | 1.27 | - | - |

| GNAR-2 | 3.68 | 6.26 | 21.23 | 0.0 | 26.0 | 2.25 | 5.15 | 1.03 | 15.6 | 22.5 | 4.58 | 4.01 | 22.38 | 0.0 | 28.0 | ||

| GNAR-3 | 0.71 | 0.71 | 2.17 | 100.0 | 0.2 | 1.54 | 1.09 | 1.31 | 84.4 | 1.9 | 1.04 | 0.78 | 3.58 | 98.2 | 2.4 | ||

| GNAR-4 | 1.47 | 1.61 | 5.09 | 0.0 | 0.2 | 3.10 | 1.90 | 1.98 | 0.0 | 1.9 | 2.00 | 1.33 | 6.18 | 1.8 | 3.7 | ||

| GNAR-5 | 2.07 | 2.23 | 7.12 | 0.0 | 0.6 | 4.02 | 2.55 | 2.36 | 0.0 | 2.8 | 2.95 | 1.77 | 9.61 | 0.0 | 5.9 | ||

| GNAR- | 0.71 | 0.71 | 2.17 | - | - | 1.65 | 1.72 | 1.27 | - | - | 1.06 | 0.79 | 3.63 | - | - | ||

| EM(G=3) | 11.16 | 2.96 | 11.37 | - | 5.6 | 10.18 | 2.00 | 1.98 | - | 3.6 | 9.38 | 1.39 | 20.08 | - | 20.0 | ||

| TS (G=3) | 9.93 | 12.38 | 32.34 | - | 20.3 | 10.24 | 5.43 | 1.78 | - | 20.2 | 8.54 | 18.94 | 56.23 | - | 37.9 | ||

| SparseVAR(1) | 10.45 | 11.66 | - | - | - | 10.47 | 11.64 | - | - | - | 10.60 | 11.75 | - | - | - | ||

| 200 | 200 | Oracle | 0.55 | 0.60 | 1.81 | - | - | 0.57 | 0.65 | 1.81 | - | - | 1.16 | 0.62 | 1.13 | - | - |

| GNAR-2 | 2.76 | 6.29 | 19.61 | 0.0 | 29.0 | 2.87 | 6.20 | 0.97 | 10.0 | 29.1 | 4.60 | 4.12 | 24.04 | 0.0 | 33.3 | ||

| GNAR-3 | 0.64 | 0.72 | 2.14 | 100.0 | 0.5 | 1.85 | 1.56 | 1.20 | 90.0 | 4.4 | 1.59 | 0.72 | 6.10 | 99.0 | 5.8 | ||

| GNAR-4 | 1.29 | 1.74 | 5.02 | 0.0 | 0.7 | 3.40 | 2.50 | 1.82 | 0.0 | 5.1 | 2.77 | 1.22 | 9.43 | 1.0 | 8.9 | ||

| GNAR-5 | 1.91 | 2.66 | 7.33 | 0.0 | 1.3 | 4.63 | 3.61 | 2.31 | 0.0 | 7.0 | 3.79 | 1.99 | 13.12 | 0.0 | 12.0 | ||

| GNAR- | 0.64 | 0.72 | 2.14 | - | - | 1.95 | 2.02 | 1.18 | - | - | 1.60 | 0.72 | 6.13 | - | - | ||

| EM(G=3) | 10.00 | 3.87 | 13.58 | - | 9.5 | 9.26 | 2.91 | 1.82 | - | 8.6 | 8.23 | 1.32 | 21.85 | - | 25.2 | ||

| TS (G=3) | 9.18 | 14.76 | 40.06 | - | 27.1 | 9.70 | 7.19 | 1.53 | - | 27.4 | 8.05 | 17.89 | 56.46 | - | 49.1 | ||

| SparseVAR(1) | 13.10 | 16.69 | - | - | - | 13.12 | 16.70 | - | - | - | 13.17 | 16.98 | - | - | - | ||

| 200 | 300 | Oracle | 0.45 | 0.51 | 1.51 | - | - | 0.47 | 0.52 | 1.43 | - | - | 0.94 | 0.51 | 0.95 | - | - |

| GNAR-2 | 2.69 | 6.19 | 19.35 | 0.0 | 28.8 | 2.49 | 5.97 | 0.79 | 0.0 | 28.3 | 4.46 | 4.19 | 23.61 | 0.0 | 32.8 | ||

| GNAR-3 | 0.47 | 0.55 | 1.62 | 100.0 | 0.2 | 1.18 | 0.90 | 0.96 | 100.0 | 1.9 | 1.08 | 0.57 | 4.17 | 99.4 | 3.8 | ||

| GNAR-4 | 0.98 | 1.44 | 4.13 | 0.0 | 0.3 | 2.43 | 1.66 | 1.44 | 0.0 | 2.1 | 1.93 | 0.93 | 6.55 | 0.6 | 5.8 | ||

| GNAR-5 | 1.47 | 2.23 | 5.85 | 0.0 | 0.5 | 3.40 | 2.60 | 1.82 | 0.0 | 3.3 | 2.77 | 1.49 | 9.39 | 0.0 | 8.1 | ||

| GNAR- | 0.47 | 0.55 | 1.62 | - | - | 1.18 | 0.90 | 0.96 | - | - | 1.09 | 0.57 | 4.18 | - | - | ||

| EM(G=3) | 10.00 | 3.72 | 13.15 | - | 8.7 | 9.25 | 1.73 | 1.42 | - | 3.9 | 8.22 | 1.21 | 21.49 | - | 24.6 | ||

| TS (G=3) | 9.39 | 12.94 | 35.35 | - | 24.9 | 9.46 | 6.47 | 1.23 | - | 24.7 | 8.09 | 17.32 | 54.57 | - | 47.1 | ||

| SparseVAR(1) | 11.19 | 13.20 | - | - | - | 11.19 | 13.19 | - | - | - | 11.26 | 13.19 | - | - | - | ||

We first focus on the performance of the GNAR estimator. From Table 5, we can observe that when the model is under-fitted (), the RMSE is much larger than when it is over-fitted () and the RMSE does not significantly decrease when both increase. This is in line with the fact that the under-fitted model leads to a significant model estimation bias. When is over-specified (i.e., ), we observe that the both RMSE and clustering error rate are larger than those from the model with a correctly specified . That is due to the inflated model estimation uncertainty when the number of model parameters increases. It may also be caused by the greater misclassification error with a larger . In the meantime, the RMSE and still decrease with an over-specified as the sample size ( and ) increases, which corroborates with the theoretical results in Theorem 1. Finally, the MSR values are all close to for Scenario 1 and 3. For Scenario 2, although it requires a much larger sample size and , the MSRs also reach when are sufficiently large. This observation supports the selection consistency results given by Theorem 2. In fact, in all case scenarios, when is chosen by GIC as , the resulting RMSEall’s are very close to those with a fixed .

Among the competing methods, the SparseVAR(1) appears to have the worst estimation accuracies in terms of RMSEν,all and RMSEβ,all, which is not surprising considering that the number of parameters to be estimated is of the order . Even with regularization, the estimation uncertainty can still be rather high. Between the EM and TS methods, it appears that the EM method consistently outperforms the TS method in terms of both estimation accuracy and clustering error . Finally, comparing the EM method to the proposed GNAR algorithm, we can see that the clustering errors are consistently higher for the EM method, especially in Scenario 1 and Scenario 3. Consequently, the estimation accuracies of the EM method also appear to be significantly worse than the GNAR estimator with either or chosen by the GIC. This observation suggests that if the network effects ’s in model (1.1) are misspecified as those in Zhu and Pan (2020), both model estimation and membership clustering will be negatively impacted.

4.3 Performance under Misspecified Models

In this section, we investigate the robustness of the GNAR model by studying its performance when the model is misspecified. For comparisons, we generate the data from the low-rank and structured vector auto-regressive model (LS-VAR, Basu et al., 2019) , where is a low-rank matrix and is a sparse matrix. Compared to the GNAR model (2.5), this model does not include any time-invariant covariates but employs an autoregressive coefficient matrix of a specific structure.

In the following we consider two specifications for the matrix. In Case I, we consider a sparse structure of . In Case II, we consider a low-rank+sparse structure of . First, we consider a purely sparse case with in Case I. The sparse matrix is generated as , where is a sparse matrix with around nonzero entries generated from a standard normal distribution and is the coefficient matrix generated from the GNAR model with under Scenario 3 in Section 4.1. The constant is chosen such that the spectral norm of is , and the ratio . We then apply the GNAR method and regularized estimation method proposed by Basu et al. (2019) for LS-VAR to estimate the coefficient matrix with various and . The number of groups in the GNAR model is selected using the GIC (2.9). For the method proposed by Basu et al. (2019), we use the fista.LpS function in R package LSVAR. The tuning parameters used by the fista.LpS function are selected by minimizing the prediction error on a testing dataset with using a model fitted by the remaining time points. After the tuning parameters are chosen, we refit the LS-VAR model with the whole data set. Summary statistics based on simulations are presented in Table 6, where we compute the relative estimation error (REE) as with being the estimated transition matrix in th simulation run.

In our simulation settings, the GNAR model is only correctly specified when while the LS-VAR model is always correct. Table 6 shows that when , the LS-VAR model performs much better than the GNAR model, suggesting that when the model misspecification is severe, the GNAR model produces large biases that make it much less accurate than more general models such as the LS-VAR model. However, when the model misspecification is not severe (e.g., or more), the GNAR may still outperform the LS-VAR model due to the benefit of the exploration of homogeneity. Such an observation suggests that the proposed GNAR model has some degree of robustness against model misspecification in the purely sparse case.

| LS | GNAR | LS | GNAR | LS | GNAR | LS | GNAR | LS | GNAR | ||

| Case I: Purely Sparse Structure | |||||||||||

| 50 | 200 | 24.7 | 114.1 | 36.2 | 103.7 | 48.0 | 74.3 | 51.4 | 45.8 | 43.4 | 25.4 |

| 50 | 400 | 17.1 | 115.6 | 25.2 | 104.8 | 33.8 | 73.5 | 37.0 | 45.1 | 33.4 | 23.7 |

| 100 | 200 | 37.7 | 100.8 | 55.8 | 94.3 | 61.1 | 75.0 | 56.1 | 46.2 | 49.8 | 24.3 |

| 100 | 400 | 27.0 | 100.6 | 41.5 | 93.8 | 46.0 | 74.2 | 42.4 | 44.3 | 34.9 | 21.1 |

| Case II: Low-rank+Sparse Structure | |||||||||||

| 50 | 200 | 79.9 | 106.5 | 82.6 | 92.6 | 86.3 | 73.0 | 68.5 | 46.4 | 45.7 | 23.3 |

| 50 | 400 | 61.5 | 101.9 | 68.0 | 88.3 | 68.8 | 68.8 | 51.8 | 42.9 | 33.4 | 18.2 |

| 100 | 200 | 94.6 | 112.1 | 94.8 | 99.8 | 96.3 | 79.4 | 80.3 | 50.2 | 46.7 | 22.8 |

| 100 | 400 | 79.4 | 106.3 | 82.7 | 94.2 | 84.9 | 74.1 | 63.2 | 46.4 | 33.7 | 19.0 |

Next, in Case II, we investigate the setting when is not purely sparse (i.e., ). In this case, we define , where is a symmetric matrix with and nonzero singular values as , and is generated the same way as in the purely sparse case. The constant is chosen such that the spectral norm of is , and the ratio . In these settings, the GNAR model estimators ignore the low-rank part and therefore are always biased except for the case . We can see from Table 6 that, the REEs of the GNAR model are rather similar to the purely sparse case. On the contrary, the REEs of the LS-VAR model deteriorate. One possible explanation is that to correctly recover the low-rank structure, the required should be much larger than those in the purely sparse case for a given . Therefore, the estimation variance of the LS-VAR estimators becomes the dominant source of the estimation error, even exceeding the estimation bias of the GNAR estimators. It is reasonable to anticipate that for a given , the performance of the LS-VAR estimator will improve as increases but the performance of the GNAR will stay roughly the same for . Nevertheless, for finite and , the GNAR model may still have good performance as long as the model is not severely misspecified.

5 Real Data Examples

5.1 Financial Contagion Analysis of Stock Market

In this section, we study a data set that collects information on companies listed in the Chinese A share market in 2020. It is common that many listed companies share a set of same shareholders and hence stock prices of these companies may correlate with each other. The shareholder network captures important inter-corporate dependence and has been an important research topic in financial risk management. Companies with shared ownerships may have similar stock return volatilities, as suggested by some empirical work. See, for example, Anton and Polk (2014) demonstrate that the degree of shared ownerships is significantly associated with cross-sectional volatility of the stock returns. Li et al. (2021) show that the information transmission between large shareholders has some significant impacts on stock volatility. For this reason, we construct a financial network based on the shared ownerships among these companies as follows. For each company, we define its major shareholders as its top 10 shareholders with more than equity shares. For a given company , if more than of its total equity shares are held by major shareholders of company , we set and otherwise set . Furthermore, any company that is not connected with other companies is eliminated from the financial network. As a result, we obtain a financial network with nodes. The same type of network structure has been widely used in the literature, e.g., Zhu et al. (2019b); Chen et al. (2022). However, we wish to comment that other types of the network can be constructed, which can be subsequently used in the GNAR model.

For company , we define the response variate as the log-realized weekly return volatility for weeks as following

where stands for the closing stock price of company on the th trading day of week , for . A similar measure has been used in Diebold and Yılmaz (2014) to study the network connectivity among financial firms.

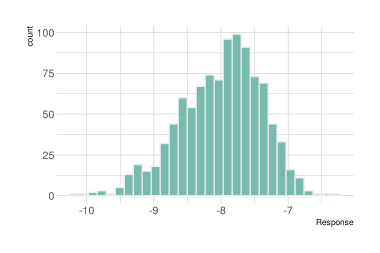

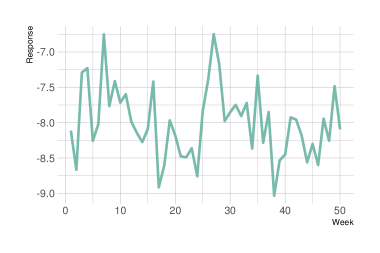

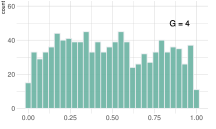

The left panel of Figure 1 presents the histogram of temporal averages of the responses for all companies and the right panel visualizes the weekly time series on the cross-sectional average of the responses of all companies (i.e., ), where we can observe relatively higher volatility levels during weeks 5–10 and around the 27th week. To characterize the dynamic pattern of the stock return volatilities, motivated by Fama and French (2015), we consider the following 6 covariates: SIZE (log-transformed market value), BM (book to market ratio), PR (increased profit ratio compared to the last year), AR (increased asset ratio compared to the last year), LEV (log-transformed leverage ratio), and CFM (cash flow divided by market value of the firm). Lastly, all covariates are standardized to be mean 0 and variance 1 for later analysis.

5.1.1 Group Choice and Model Diagnosis

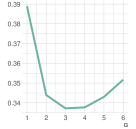

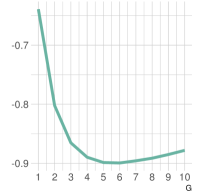

To apply the GNAR model to the aforementioned dataset, the first task is to choose the number of groups . By setting as in the simulation study (recall that is the 90% quantile of nodal out-degrees ), the resulting GIC values indicate that we should select groups, while might also be acceptable according to the left panel of Figure 2.

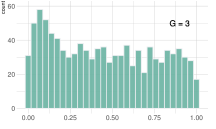

To assess the goodness-of-fit of the GNAR models with or , we propose to use the Ljung-Box test (Ljung and Box, 1978) to check the serial dependence of the residual time series on each network node. If the GNAR model fits the data sufficiently well, it is expected that the set of residual time series on all network nodes should be close to a set of independent white noise processes. We compute the -values of the Ljung-Box test for a white noise process based on the residual time series collected from each stock and visualize the distribution of -values from all stocks with a histogram, where a large number of small -values may suggest a lack of fit. From the middle (GNAR with ) and right (GNAR with ) panels of Figure 2, we can see that the -values for are more uniformly distributed than those for , suggesting a better model fit using GNAR with .

Deliberating on the GIC score and the diagnostic plots of the model fit, we choose to fit the GNAR model with to the stock data.

5.1.2 Clustering Results with

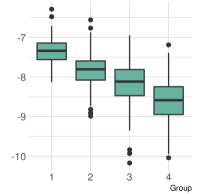

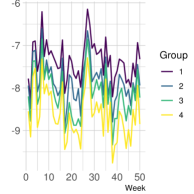

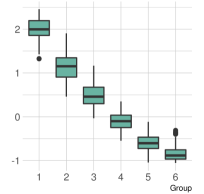

The temporal averages of the responses for different companies are depicted in the left panel of Figure 3, where we can see that the first group is of higher volatility levels than the other 3 groups. The right panel of Figure 3 visualizes the cross-sectional averages of the responses within the groups, which shows different dynamic patterns for the four groups.

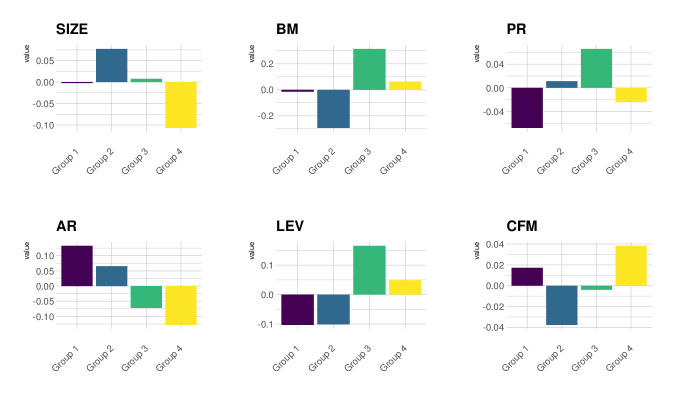

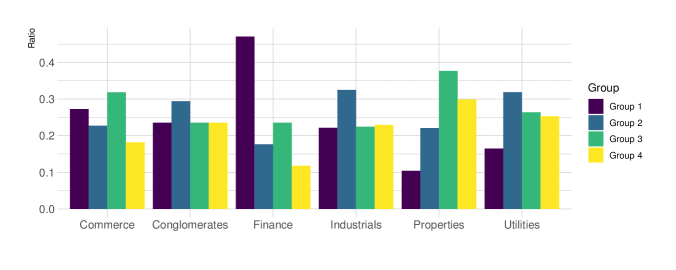

To shed more light on the differences among these groups, Figure 4 visualizes the average covariate values of different groups. Specifically, the firms in the second group have the largest size while Group 4 has small size firms. Group 3 has the largest BM, PR, and LEV values.

Lastly, we summarize the industry information of companies in each group in Figure 5. These companies can be roughly categorized into six major industries (Commerce, Conglomerates, Finance, Industries, Properties, and Utilities) according to the information released by China Securities Regulation Commission (CSRC) in 2012. We can see that most companies in the Finance are clustered in Group 1. Most companies in industrials and Utilities are clustered into Group 2 while most companies in Properties are in Group 3. Note that companies in the Industrials category typically have large market values, which explains why the averaged SIZE is the highest for Group 2 in Figure 4.

5.1.3 Model Interpretations

The model estimation results are given in Table 7. First, we observe that the momentum effect is the highest in Group 3 and the lowest in Group 2. This suggests that stock return volatilities of companies in Group 3 are highly influenced by its historical performance. Furthermore, the within-group network effects of all groups are rather similar and positive except Group 3, indicating a volatility spillover effect within each group. Regarding the between-group network effects, we can see that Groups 1, 2 and 4 positively influence each other with significant between-group network effects. In contrast, Group 3 receives negative influences from the other groups.

| Group 1 | Group 2 | Group 3 | Group 4 | |

| Proportion | 0.215 | 0.302 | 0.250 | 0.234 |

| Group 1 | 0.095 * () | 0.082 * () | 0.100 * () | 0.072 * () |

| Group 2 | 0.054 * () | 0.069 * () | 0.080 * () | 0.077 * () |

| Group 3 | -0.075 * () | -0.093 * () | -0.022 (0.052) | -0.064 * () |

| Group 4 | 0.047 * () | 0.035 * (0.005) | 0.047 * () | 0.066 * () |

| Momentum | 0.242 * () | 0.089 * () | 0.433 * () | 0.192 * () |

| Intercept | -4.854 * () | -6.659 * () | -5.115 * () | -6.573 * () |

| SIZE | -0.107 * () | -0.123 * () | -0.093 * () | -0.136 * () |

| BM | -0.108 * () | -0.247 * () | -0.118 * () | -0.252 * () |

| PR | -0.015 (0.259) | 0.024 * (0.021) | 0.018 * (0.023) | 0.069 * () |

| AR | -0.028 * (0.009) | -0.039 * () | -0.059 * () | -0.034 * (0.023) |

| LEV | 0.070 * () | 0.079 * () | 0.089 * () | 0.078 * () |

| CFM | -0.062 * () | -0.099 * () | -0.057 * () | -0.072 * () |

Finally, we comment on the estimated coefficients of the covariates. First, the volatility levels have negative relationships with the market values (SIZE) of the firms across all groups. This confirms the phenomenon that firms with larger sizes tend to perform better when exposed to financial risk than smaller firms (Diebold and Yılmaz, 2014; Huang et al., 2021). The BM, AR and CFM value are also shown to have significant negative effects on the volatility level across all groups. On the contrary, the LEV tends to have a positive effect on the volatilities and the PR values are also shown to have a positive influence on most groups.

5.2 Model Prediction

Lastly, we compare the prediction performance of the GNAR model with the LS-VAR model (Basu et al., 2019). Specifically, we use the first weeks for model training and the following weeks for model testing. For the GNAR model, we use groups. For the LS-VAR model, we choose the tuning parameters by minimizing the prediction RMSE on the testing dataset, which is defined as . Since the LS-VAR does not allow time-invariant covariates used in the GNAR model, we center the observations by with for . As a result, the PRMSE values for the GNAR model and LS-VAR model are 1.16 and 1.20, respectively. Although the difference is relatively small, the proposed GNAR model is able to achieve slightly lower prediction error with fewer model parameters.

5.3 User Activity Analysis with Sina Weibo

In this section, we illustrate the use of the proposed methodology with a dataset collected from Sina Weibo, a Twitter-type online social network platform in China. The dataset includes active users, whose posting activities are recorded for days. The network structure is obtained using the observed following-followee relationships among the users.

To gauge the users’ activity levels, we follow Zhu et al. (2017) to define the response with being the number of posts of the th user in the th day. To remove the time-varying trend, we center the response variable as . To further explain the variations of ’s among different network nodes, we collect seven node-specific covariates: Gender (male = 1, female = 0), Tenure (number of years since the user’s registration), Beijing (equals to 1 if the user locates in Beijing and 0 otherwise), Shanghai (equals to 1 if the user locates in Shanghai and 0 otherwise), Description (the length of user self-description), Weibo (logarithm of accumulated number of posts), and Public (equals to 1 if the user is a public account and 0 otherwise).

5.3.1 Group Choice and Clustering Results

We start by choosing the number of groups using the GIC criterion defined in (2.9) with a , where is the 90% quantile of nodal out-degrees . As illustrated in the left panel of Figure 6, the GIC value is minimized at , although is also acceptable. One notable feature is that the GIC achieves significant reductions by increasing from to , suggesting that there indeed exists certain level heterogeneity among network users. This provides some justifications for the proposed method that introduce latent groups among the network nodes.

5.3.2 Model Interpretations

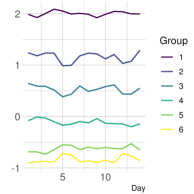

Next, we obtain the parameter estimates and group membership assignments by minimizing (2.1), which are summarized in Table 8 and Figure 6. In Figure 6, The middle panel indicates clear different individual activity levels for users in different groups, and the right panel reveals rather consistent separations for overall group activity level over time. In particular, Groups 2 and 3 tend to be less active during weekends while the other three groups do not exhibit such a pattern.

| Group 1 | Group 2 | Group 3 | Group 4 | Group 5 | Group 6 | |

|---|---|---|---|---|---|---|

| Proportion | 0.086 | 0.109 | 0.134 | 0.200 | 0.221 | 0.249 |

| Group 1 | 0.332 * () | 0.042 (0.691) | 0.150 (0.316) | -0.231 (0.151) | 0.215 (0.185) | -0.247 (0.053) |

| Group 2 | 0.492 * () | 0.746 * () | 0.643 * () | -0.226 (0.257) | 0.506 * (0.009) | 0.105 (0.520) |

| Group 3 | 0.453 * () | 0.197 (0.132) | 0.190 (0.318) | -0.312 (0.091) | -0.154 (0.370) | -0.103 (0.467) |

| Group 4 | 0.194 * () | 0.290 * (0.018) | 0.106 (0.496) | -0.155 (0.337) | 0.187 (0.181) | -0.061 (0.605) |

| Group 5 | -0.090 * (0.047) | 0.053 (0.597) | -0.167 (0.201) | 0.454 * () | 0.050 (0.669) | 0.119 (0.262) |

| Group 6 | -0.062 (0.112) | -0.044 (0.575) | -0.301 * (0.005) | 0.289 * (0.010) | 0.286 * (0.003) | 0.200 * (0.013) |

| Momentum | 0.523 * () | 0.293 * () | 0.338 * () | 0.286 * () | 0.234 * () | 0.157 * () |

| Intercept | 0.731 * () | -0.044 (0.549) | -0.288 * () | -0.563 * () | -0.606 * () | -0.812 * () |

| Gender | 0.021 (0.126) | 0.041 * (0.015) | -0.034 * (0.048) | 0.037 * (0.008) | 0.031 * (0.011) | 0.016 (0.116) |

| Tenure | 0.023 * (0.015) | 0.106 * () | 0.067 * () | 0.057 * () | 0.060 * () | 0.025 * () |

| Beijing | 0.037 * (0.009) | 0.201 * () | 0.086 * () | 0.015 (0.403) | -0.038 * (0.013) | -0.026 * (0.016) |

| Shanghai | -0.005 (0.824) | 0.259 * () | 0.114 * () | 0.076 * () | -0.286 * () | 0.284 * () |

| Description | -0.011 (0.054) | -0.013 * (0.024) | 0.018 * (0.003) | 0.028 * () | 0.032 * () | 0.006 (0.081) |

| -0.004 (0.244) | 0.013 * (0.005) | 0.010 (0.052) | 0.010 * (0.020) | -0.004 (0.243) | 0.010 * () | |

| Public | 0.046 * (0.023) | 0.135 * () | 0.066 * (0.009) | 0.135 * () | 0.027 (0.092) | 0.005 (0.662) |

From Table 8, we can observe some interesting dynamic patterns among the six groups. Firstly, Group 1 appears to be the most self-excited group who has the largest momentum effect (i.e. 0.523). In the meantime, Group 1 also appears to be the most influential group in the sense that 5 out of , are statistically significant, suggesting users in other groups tend to be influenced by users in Group 1. Secondly, Group 2 has the largest within-group network effect (i.e., 0.746) but has little impact on activities of other groups except for Group 4. Activities of users in Group 2 are also heavily influenced by activities of other groups. For example, Group 2 receives significant positive network influence from Group 3 but its impact on Group 3 is not significant, which implies an asymmetric influential pattern. Lastly, the activities of Group 6 appear to be positively related to Groups 4–5, but not to the most influential Group 1.

For the fixed-effects, we observe that the male users tend to be more active in Groups 2, 4, 5 but less active in Group 3. The users with longer tenure tend to be more active in all groups. For the location related covariates, we observe that the users located in Beijing of Groups 1–3 are more active while users in Shanghai of Groups 2, 3, 4, 6 tend to be more active. Lastly, the activity levels of Groups 3, 4 and 6 are positively related to their historical accumulated Weibo posts and the public accounts tend to be more active in Groups 1–4.

5.3.3 Model Diagnosis and Improvement

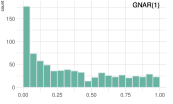

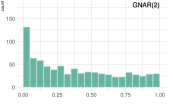

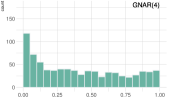

Following the same idea in Section 5.1.1, we use the histograms of the -values of the Ljung-Box tests to access the goodness of fit. From the left panel of Figure 7, we can see that the distribution of -values is far from a uniform distribution, suggesting a lack of fit with the proposed GNAR model to the Weibo data. Therefore, the model interpretations given in sections 5.2.1-5.2.2 should be treated with caution.

In our further attempts to improve the model fit, we implemented the following GNAR() model as a direct extension of the proposed GNAR model (1.1),

| (5.1) |

It is straightforward to see that when , the above model reduces to model (1.1). We apply the GNAR(2) and the GNAR(4) to the Weibo data, whose diagnostic plots are given in Figure 7. We can observe that, by increasing from to , the diagnostic plot indeed becomes closer to a uniform distribution but fails to fully address the lack-of-fit issue. To further improve the model, more relevant covariates including some time-dependent covariates may be collected, which will be pursued in a separate work.

6 Concluding Remarks

In this work, we propose a network vector autoregression model with a latent group structure. The flexibility of the model enables us to capture the individuals’ heterogeneous momentum effects and network interactions. Group memberships and model parameters are estimated simultaneously through the minimization of a least-square type loss function, and the theoretical properties of the resulting estimators are investigated. Furthermore, a data-driven criterion is designed to consistently select the number of groups. The usefulness of the proposed model is illustrated through simulation studies and two real data examples.

To conclude the article, we discuss several interesting future research topics. First, one immediate extension of the current work is to investigate theoretical properties of the GNAR() model suggested in (5.1), including the asymptotic normality, choice of , and the goodness-of-fit tests. Second, the group structure in the proposed model is primarily determined by node-specific characteristics but not by interactions among different nodes. It will be interesting to combine the proposed group structure with some community detection methods for a more practical model. Third, the fixed effects are assumed to be parametric and time-invariant. It is desirable to extend the current setting to include nonparametric and/or time-varying fixed effects. Lastly, the covariates considered in our work are of finite dimension. However, in practice high dimensional features can be collected. Feature screening and selection techniques can be developed to uncover the most informative features.

References

- Abbe et al. (2020) Abbe, E., Fan, J., Wang, K., and Zhong, Y. (2020), “Entrywise eigenvector analysis of random matrices with low expected rank,” Annals of statistics, 48, 1452.

- Ando and Bai (2016) Ando, T. and Bai, J. (2016), “Panel data models with grouped factor structure under unknown group membership,” Journal of Applied Econometrics, 31, 163–191.

- Ando and Bai (2017) — (2017), “Clustering huge number of financial time series: A panel data approach with high-dimensional predictors and factor structures,” Journal of the American Statistical Association, 112, 1182–1198.

- Anton and Polk (2014) Anton, M. and Polk, C. (2014), “Connected stocks,” The Journal of Finance, 69, 1099–1127.

- Basu et al. (2019) Basu, S., Li, X., and Michailidis, G. (2019), “Low rank and structured modeling of high-dimensional vector autoregressions,” IEEE Transactions on Signal Processing, 67, 1207–1222.

- Basu et al. (2015) Basu, S., Michailidis, G., et al. (2015), “Regularized estimation in sparse high-dimensional time series models,” The Annals of Statistics, 43, 1535–1567.

- Bester and Hansen (2016) Bester, C. A. and Hansen, C. B. (2016), “Grouped effects estimators in fixed effects models,” Journal of Econometrics, 190, 197–208.

- Bonhomme and Manresa (2015) Bonhomme, S. and Manresa, E. (2015), “Grouped patterns of heterogeneity in panel data,” Econometrica, 83, 1147–1184.

- Chen et al. (2022) Chen, E. Y., Fan, J., and Zhu, X. (2022), “Community network auto-regression for high-dimensional time series,” Journal of Econometrics, to appear.

- Chen and Chen (2008) Chen, J. and Chen, Z. (2008), “Extended Bayesian information criteria for model selection with large model spaces,” Biometrika, 95, 759–771.

- Clauset et al. (2009) Clauset, A., Shalizi, C. R., and Newman, M. E. (2009), “Power-law distributions in empirical data,” SIAM Review, 51, 661–703.

- Diebold and Yılmaz (2014) Diebold, F. X. and Yılmaz, K. (2014), “On the network topology of variance decompositions: Measuring the connectedness of financial firms,” Journal of econometrics, 182, 119–134.

- Dou et al. (2016) Dou, B., Parrella, M. L., and Yao, Q. (2016), “Generalized Yule–Walker estimation for spatio-temporal models with unknown diagonal coefficients,” Journal of Econometrics, 194, 369–382.

- Fama and French (2015) Fama, E. F. and French, K. R. (2015), “A five-factor asset pricing model,” Journal of Financial Economics, 116, 1–22.

- Fan et al. (2021) Fan, J., Ke, Y., and Liao, Y. (2021), “Augmented factor models with applications to validating market risk factors and forecasting bond risk premia,” Journal of Econometrics, 222, 269–294.

- Fang et al. (2020) Fang, G., Xu, G., Zhu, X., Guan, Y., et al. (2020), “Group network Hawkes process,” arXiv preprint arXiv:2002.08521.

- Farajtabar et al. (2017) Farajtabar, M., Wang, Y., Gomez-Rodriguez, M., Li, S., and Zha, H. (2017), “COEVOLVE: A joint point process model for information diffusion and network evolution,” Journal of Machine Learning Research, 18, 1–49.

- Fox et al. (2016) Fox, E. W., Short, M. B., Schoenberg, F. P., Coronges, K. D., and Bertozzi, A. L. (2016), “Modeling e-mail networks and inferring leadership using self-exciting point processes,” Journal of the American Statistical Association, 111, 564–584.

- Huang et al. (2021) Huang, C., Deng, Y., Yang, X., Cao, J., and Yang, X. (2021), “A network perspective of comovement and structural change: Evidence from the Chinese stock market,” International Review of Financial Analysis, 76, 101782.

- Lei and Rinaldo (2015) Lei, J. and Rinaldo, A. (2015), “Consistency of spectral clustering in stochastic block models,” The Annals of Statistics, 43, 215–237.

- Li et al. (2021) Li, J., Zhang, Y., and Wang, L. (2021), “Information transmission between large shareholders and stock volatility,” The North American Journal of Economics and Finance, 58, 101551.

- Liu et al. (2020) Liu, R., Shang, Z., Zhang, Y., and Zhou, Q. (2020), “Identification and estimation in panel models with overspecified number of groups,” Journal of Econometrics, 215, 574–590.

- Ljung and Box (1978) Ljung, G. M. and Box, G. E. (1978), “On a measure of lack of fit in time series models,” Biometrika, 65, 297–303.

- Lugosi and Mendelson (2019) Lugosi, G. and Mendelson, S. (2019), “Sub-Gaussian estimators of the mean of a random vector,” The annals of statistics, 47, 783–794.

- Negahban and Wainwright (2011) Negahban, S. and Wainwright, M. J. (2011), “Estimation of (near) low-rank matrices with noise and high-dimensional scaling,” The Annals of Statistics, 39, 1069–1097.

- Nicholson et al. (2020) Nicholson, W. B., Wilms, I., Bien, J., and Matteson, D. S. (2020), “High Dimensional Forecasting via Interpretable Vector Autoregression.” .

- Rohe et al. (2011) Rohe, K., Chatterjee, S., Yu, B., et al. (2011), “Spectral clustering and the high-dimensional stochastic blockmodel,” The Annals of Statistics, 39, 1878–1915.

- Schütze et al. (2008) Schütze, H., Manning, C. D., and Raghavan, P. (2008), Introduction to information retrieval, vol. 39, Cambridge University Press Cambridge.

- Sewell and Chen (2015) Sewell, D. K. and Chen, Y. (2015), “Latent space models for dynamic networks,” Journal of the American Statistical Association, 110, 1646–1657.

- Su et al. (2016) Su, L., Shi, Z., and Phillips, P. C. (2016), “Identifying latent structures in panel data,” Econometrica, 84, 2215–2264.