[R]First version: September 25, 2022. This version: March 23, 2022.

Efficient Wrong-Way Risk Modelling for Funding Valuation Adjustments

Abstract

Wrong-Way Risk (WWR) is an important component in Funding Valuation Adjustment () modelling. Yet, the standard assumption is independence between market risks and the counterparty defaults and funding costs. This typical industrial setting is our point of departure, where we aim to assess the impact of WWR without running a full Monte Carlo simulation with all credit and funding processes. We propose to split the exposure profile into two parts: an independent and a WWR-driven part. For the former, exposures can be re-used from the standard xVA calculation. We express the second part of the exposure profile in terms of the stochastic drivers and approximate these by a common Gaussian stochastic factor. Within the affine setting, the proposed approximation is generic, is an add-on to the existing xVA calculations and provides an efficient and robust way to include WWR in modelling. Case studies for an interest rate swap and a representative multi-currency portfolio of swaps illustrate that the approximation method is applicable in a practical setting. We analyze the approximation error and use the approximation to compute WWR sensitivities, which are needed for risk management. The approach is equally applicable to other metrics such as Credit Valuation Adjustment.

keywords:

Gaussian approximation , Wrong-Way Risk (WWR) , Funding Valuation Adjustment () , computational finance , risk management1 Introduction

Funding Valuation Adjustments () are used in financial derivatives pricing to include the funding costs of uncollateralized deals. When transactions are not fully collateralized, captures the funding cost of hedging the market risk of these transactions. Wrong-Way Risk (WWR) should be included in modelling, and can be understood as an increase in the funding risk due to increased market risk (exposure). For a qualitative discussion about , WWR, and its importance, see, for example, [27]. Going forward, WWR is referred to as WWR. As a starting point, assume that a Valuation Adjustment (xVA) calculation is in place where WWR is not included. We develop an efficient methodology to compute WWR, but avoid a full Monte Carlo simulation including additional risk factors driving the counterparty defaults and funding spread, similar to [17]. In this fashion, it is possible to assess WWR effects when the existing xVA calculation cannot simulate stochastic credit and funding correlated to the existing set of risk factors.

The existing literature focuses on WWR modelling and its efficient computation. Kenyon et al. tackle WWR with a model-independent approach by rewriting the xVA expressions into separate components to assess the various contributions to correlation effects [14]. Different WWR modelling approaches can be compared using this framework. Brigo and Pallavicini touch upon the topic in a symmetric funding case in a Monte Carlo BSDE setting [3]. Green indicates the natural choice is a stochastic funding spread, where the dependence with the underlying asset is introduced through Gaussian correlation [9], e.g., see also [25], with an idiosyncratic/systemic decomposition of the stochastic funding spread. Moni adds correlation among credit spreads, funding spreads and market risk factors using a polynomial delta-gamma approximation [17]. This approach avoids a full Monte Carlo simulation where the credit and funding spreads are also simulated. Alternatively, one can focus on extreme events like Turlakov [24] or consider worst-case like Singh and Zhang [22].

To put WWR in perspective, we compare it with Credit Valuation Adjustment () WWR. WWR is introduced through a dependence between exposure and default probabilities, which will increase the . Literature on WWR modelling for for non-credit derivatives can be divided into three approaches. 111For credit derivatives, a separate stream of literature exists, but in this paper we do not focus on this class of derivatives. Firstly, there is simulation, which models interest rates, default intensities and their dependence through either a deterministic relationship or a set of correlated SDEs [7, 12]. Secondly, a copula approach where the multivariate distribution of exposure and defaults is modelled through a copula [5, 6]. Finally, a worst-case method provides an upper bound for the without requiring exact knowledge of the dependence structure of exposures and default dynamics [8, 15]. These approaches could also be extended to WWR.

In this paper, we essentially follow Green [9] and Moni [17], but we propose a Gaussian WWR approximation, which allows for efficient and robust WWR computation in a generic fashion. We extend our previous work [27] by focusing on the quantitative computational challenges and avoiding simulating extra (correlated) dynamics for credit and funding spreads. We assume that all short-rate dynamics are of the affine form. Credit and funding spread dynamics are chosen and correlated to the existing risk factor dynamics that drive the exposure. We split the exposure profile into two parts: an independent and a WWR-driven part. For the first part, already computed exposures are used. We express the second part of the exposure profile in terms of the stochastic drivers, and approximate these by a common Gaussian stochastic factor. The approximation also provides intuition on WWR. We analyze the approximation quality and indicate in which situations the approximation works well. We use a brute-force Monte Carlo approach as a benchmark, where all risk factors are simulated. Case studies are presented for an uncollateralized interest rate (IR) swap, as well as a representative multi-currency portfolio of swaps. We show that the approximation method is applicable in a practical setting due to its generic nature. Hence, the approximation can be applied to portfolios, including other products and asset classes. The approach is introduced for , but is equally applicable to other metrics such as .

When computing , calculating the relevant sensitivities is particularly important from a risk-management perspective. The cross-gamma risk between funding spreads and exposure is a sensitivity which is introduced by including WWR in modelling. The effects are two-fold: the WWR premium is compensation for re-hedging at expensive moments and recognizing when to re-hedge to have low hedging costs [27]. Furthermore, the WWR sensitivities are needed in the xVA explain process [26] to keep the unexplained as low as possible. The proposed Gaussian approximation enables a fast approximation of the sensitivities so that hedges in the market can be set up early.

In Section 2, we introduce the modelling framework with the equation, correlation assumptions, funding spreads and WWR as in [27]. Then, in Section 3, we propose our Gaussian approximation. We analyze the approximation error in Section 4. Numerical experiments are presented in Section 5, and finally, in Section 6, we conclude.

2 FVA and Wrong-Way Risk

We re-iterate the equation, correlation assumptions, funding spread definitions and exposure split between the independent and WWR part, as in [27]. Funding costs and benefits are assumed to be asymmetric: when borrowing funds, a spread over the risk-free rate is paid, but when lending out funds, only the risk-free rate is earned. As a consequence , since . 222Here, and represent the Funding Cost Adjustment and Funding Benefit Adjustment, respectively. The framework is summarized in Section 2.1.

In Section 2.2, we extend the framework to prepare for the Gaussian approximation of the WWR exposure from Section 3. We use Taylor series expansions of the interest rate (IR) discount factors and credit adjustment factors that appear in the exposure formulae.

2.1 The setup

We assess the impact of WWR on the for a portfolio of uncollateralized derivatives, , between counterparty and institution , with maturity . Values are denoted from ’s perspective. The borrowing spread, , is an instantaneous spread over the risk-free rate , and will be the funding costs used to compute . Default times , , are modelled as the first jump of a Cox process [2], driven by hazard rate .

We look at the processes and , and their correlation structure with the IR risk factor , introduced via correlated Brownian increments. Next, the equation is given and split into an independent and a WWR part. The same split is done for the corresponding exposures. Furthermore, we assume a funding spread of a particular form, such that exposures can be rewritten to a convenient form in Section 2.2.

2.1.1 Default processes, model dynamics and correlations

We work with affine short-rate dynamics [2] for interest rate and hazard rates and , where the integrated dynamics fit in the following generic setup:

| (2.1) |

Here, and . Furthermore, , , and are deterministic quantities. Respectively, and are stochastic and integrated stochastic processes, with .

We introduce a dependence between the credit and IR processes through correlated Brownian increments in , as in [18], rather than using a copula, as in [4]. For IR derivatives, the main WWR driver will be the dependence between the funding spread and the IR exposure [27]. Hence, we choose to work with independent defaults of the counterparties and . This will slightly restrict correlations between the other risk factors for the correlation matrix to remain symmetric positive definite. Survival probabilities can be factorized due to this independent default assumption, which we will use in Section 2.1.2.

The correlation assumptions can also be formulated in terms of the Brownian motions of the stochastic processes:

Correlations , , can be calibrated to historical data or can be mapped to alternative data in the case of illiquid counterparties [9]. The latter correlation, , is zero due to the independent default assumption.

Remark (Credit derivatives).

Default times and are assumed to be conditionally independent on , i.e., . This assumption cannot be justified when considering credit derivatives, where the dependence between counterparties is a crucial component that must be captured in any modelling approach. Therefore, credit derivatives cannot be handled straight away, even though dynamics for the credit processes are already specified.

2.1.2 FVA equation

For the of portfolio , the following expression can be derived, see [27], under the assumption of conditional independence of defaults, and using the instantaneous spread :

(2.2)

(2.3)

where denotes the time value of the time Expected Positive Exposure, which is a credit- and funding-adjusted discounted positive exposure. 333In typical notation, the credit and funding components are not part of the , but they are included here for ease of notation.

Furthermore, filtration is the ‘standard’ default-free filtration; is the enriched filtration with all available market information; is the filtration generated by the default time for , see [2].

Furthermore, .

From Equation (2.2) it is clear that if one of the parties defaults before , funding only needs to take place up to the default date. This translates into credit adjustment factors and for the potential default of and , which can be interpreted as survival probabilities. These credit adjustment factors can change the magnitude significantly, with increased effects for lower credit quality. Hence, including default times and in the definition and modelling is an important consideration. including these credit adjustment factors is also known as ‘contingent’ and is consistent with a closeout based on the risk-free value [10]. In addition, these credit adjustment factors influence the dependence structure, introducing additional WWR effects. Therefore, including or excluding the default times is also relevant from a hedging perspective.

Remark (Asymmetric funding assumption).

The assumption of asymmetric funding can be made to avoid double counting of funding benefits from and [10]. In general, this assumption leads to a recursive and non-linear pricing equation, where the derivative price depends on the future funding requirement, such that the xVA is the solution of a BSDE [21]. The consequence is that can no longer be considered as an additive xVA term. However, the BSDE formulation is not strictly needed unless the closeout is on the risky pre-default value [1]. Therefore, we can safely assume asymmetric funding. When funding and borrowing rates are equal (symmetric funding), the pricing equation is no longer recursive and becomes additive.

2.1.3 Splitting the FVA equation

Going forward, we write for ease of notation. For exposure in Equation (2.3), we consider a generic form:

| (2.4) |

where , and depend on the modelling assumptions, and are defined in Section 2.1.4.

This expression can be rewritten by decomposing it into covariances:

(2.5)

The overall exposure is then split into an independent exposure, , and a WWR exposure, , which is driven by the correlation assumptions and captures cross-dependence.

Rather than decomposing into covariances, the expectation could be decomposed into correlations and the corresponding standard deviations, see [14].

However, for us it appears more convenient to work with the covariance decomposition.

2.1.4 Funding spread

When choosing a funding spread, a key requirement is that it is in line with the ability of a financial institution to fund itself in the market. A stochastic funding spread takes into account the credit of , through hazard rate . We assume the information on ’s credit is extracted from the CDS market. Instantaneous borrowing spread is now defined as [9]:

| (2.7) |

with a deterministic loss given default , which is a standard assumption [19]. For a stochastic loss given default, additional WWR will be introduced, but this is outside the scope of this paper as it is not common practice. We assume in Equation (2.7) is stochastic, with model dynamics of the form (2.1). Furthermore, is correlated with the other underlyings, which results in WWR. We split the borrowing spread into a deterministic part, , and a stochastic part, , as in Equation (2.1):

| (2.8) |

A (deterministic) liquidity adjustment could be added to Equation (2.7) to reflect the bond-CDS basis in the borrowing spread. This adjustment will naturally be absorbed by in Equation (2.8), and none of the results to follow will change.

For the current choice of funding spread, in Equation (2.5) is defined as

so that

with Zero Coupon Bond (ZCB) . Due to the independence assumption from Section 2.1.1, and are independent. Furthermore, , and , such that is simply the discounted positive exposure, which is readily available from an existing xVA calculation.

2.2 FVA exposure for a given funding spread

Given the funding spread definition, the functions , and have an explicit form. The independent and WWR exposure from Equation (2.5) can be rewritten using these functional forms. We use Taylor series approximations to rewrite these expressions in a convenient form with the stochastic drivers and as introduced in Equation (2.1). This step is done to prepare for the Gaussian approximation in Section 3.

2.2.1 Taylor series approximations

The affine dynamics from Section 2.1.1 imply that the ZCB under the model of choice can be written as

| (2.9) |

where and . We introduce the notation for a deterministic factor, to split into a deterministic and stochastic part:

| (2.10) |

with and as defined in Equation (2.1). can be interpreted as a discount factor for . This modelling framework is flexible regarding various choices for the affine short-rate dynamics. We keep the derivations generic and express the results in terms of the stochastic processes and their integrated version . For notational convenience, the product of deterministic factors is denoted as

| (2.11) |

Next, we denote the Taylor series expansion of as

| (2.12) |

Combining the other notation from this section with the Taylor expansion yields:

| (2.13) | ||||

| (2.14) |

These two expansions will be used in the approximations that follow in Sections 2.2.2 and 2.2.3.

2.2.2 Independent exposure

Combining the funding spread assumption from Equation (2.8) with the notation in Section 2.2.1, independent exposure from Equation (2.5) is written as

| (2.15) |

where the second term captures the dependence between the credit randomness driving the borrowing spread and the default probabilities.

Using the Taylor expansion from Equation (2.14) with , which is a first-order expansion, gives us:

(2.16)

where is the truncation error from cutting off the Taylor series expansion:

| (2.17) |

An approximation for is obtained by omitting the term in Equation (2.16). The corresponding approximation error results from truncating the Taylor series expansion, by discarding the product . The choice of means that no calibration needs to be performed for this approximation parameter.

2.2.3 WWR exposure

In a similar fashion as the independent exposure, WWR exposure from Equation (2.5) can be rewritten:

| (2.18) |

If IR and credit are independent, then clearly .

We take the WWR exposure from Equation (2.18) and apply the modelling choices from Section 2.1.1, the funding spread from Equation (2.8) together with the two Taylor expansions from Equations (2.13) and (2.14) with , resulting in:

(2.19)

(2.20)

where and are as in Equation (2.11).

In Equation (2.20), we have defined the generic truncation error , which is the result of truncating multiple Taylor series.

An approximation for is obtained by omitting in Equation (2.19).

See A for a derivation of the WWR exposure.

First, contains the scaled truncation errors, , where

| (2.21) |

Error results from removing the terms , which corresponds to the Taylor series expansion of , combined with the deterministic part of the funding spread, i.e., . Error is a consequence of omitting the product , which corresponds to the Taylor series expansion of , combined with the stochastic part of the funding spread, i.e., . The choice of means that no calibration needs to be performed for this approximation parameter.

Furthermore, contains scaled truncation errors, , where

| (2.22) |

Similarly, contains the scaled truncation errors , with

| (2.23) |

Both errors and are from the truncation of the infinite summations to , and thus discard the terms of the corresponding full Taylor series. The choice of an appropriate value for is discussed in Section 5.3. So far, all the truncation errors are at the exposure level and are generic, regardless of the choice of portfolio .

3 Gaussian approximation for WWR exposure

In Section 2, we have obtained an expression for the WWR exposure using the affine dynamics, correlation assumptions, funding spread and Taylor series expansions. Next, we propose an efficient and generic approximation of the expectations in Equation (2.19). The distributions of the various processes are approximated by normal distributions. This significantly simplifies the equations while preserving the dependence structure in an approximate fashion, allowing for a useful approximation of the WWR exposure. Furthermore, the approximation preserves intuition on WWR from a modelling perspective.

We choose dynamics that fit the framework from Section 2.1.1. The Hull-White dynamics (HW1F) with constant volatility are used for IR process . For Bilateral Credit Valuation Adjustment (BCVA) WWR modelling, a CIR model is often used for the credit processes [3, 4]. Hence, the CIR++ dynamics [2] with constant volatility are used for the credit process of each counterparty . See B for the full specification of the model dynamics. We are interested in the integrated model dynamics, such that both drift and diffusion appear in integrated form.

The stochastic processes for IR, defined in Equation (2.1), follow normal distributions, i.e., and . Hence, the use of a Gaussian approximation is justified for the IR processes, as both processes are already Gaussian.

The CIR++ model has a scaled non-central chi-square distribution, with fatter tails than a normal distribution. When the Feller condition is satisfied, both tails of the density will decay fast [20], such that it can be well approximated by a Gaussian. 444Under some market conditions, the Feller condition can be too restrictive in the sense that the model cannot generate enough volatility to fit the market [16]. In this case, jumps could be added to the model to increase the generated volatility. Still, information from the tails is lost in the approximation. However, it is challenging to calibrate these tails properly due to insufficient market data. Therefore, the Gaussian approximation is also justified for the credit processes. The Gaussian approximation might lead to a small probability of negative values of the credit distribution. As the approximation is only applied to the joint distributions required for WWR, and not to the marginals distributions used to compute the independent part of the exposure, this is an acceptable consequence of the Gaussian approximation.

Remark (Black-Karasinski for credit).

Alternatively to the CIR++ dynamics, the Black-Karasinski (BK) dynamics can be used to model the default intensity, where positive rates are guaranteed due to the lognormal distribution. The main drawback of these dynamics is that there is no analytic ZCB formula, and the dynamics do not belong to the affine class. Turfus proposes an analytic approximation of the ZCB price by truncating an infinite power series of the rate, which preserves positivity [23]. This approximation is done under the assumption of a small deviation of rates from the forward curve. Due to the lack of affinity of the BK dynamics, and the need for an approximation to obtain an analytic ZCB price, these dynamics are not considered in this paper.

3.1 Gaussian approximation for stochastic processes

The essence of the proposed WWR approximation is to approximate all relevant stochastic processes by a single normally distributed variable. Currently, follows a normal distribution. Hence, we approximate all stochastic processes in terms of , without loss of generality.

As and are both normal with zero mean, can be expressed as times a scaling factor:

(3.1)

Here, we have introduced the notation for the ratio of variances.

The CIR++ model has dynamics which follow a scaled non-central chi-square distribution.

Thus, and are not Gaussian for .

We propose to approximate by a normally distributed variable, and then rewrite this in terms of :

(3.2)

where for the WWR exposures, the correlations enter the approximation.

Remark (Correlation).

As written in Equation (3.2), the Gaussian approximation is applied to the marginal distributions. However, for WWR exposures, not the marginal distributions but the joint distributions are relevant. These define the WWR exposures in the form of cross-moments. Therefore, correlation should enter the equations, because the Brownian motions are correlated, i.e., . For example, when the marginal of is approximated using Equation (3.2), the cross-moment with will be approximated as

where the dependence structure is preserved in an approximate fashion. The marginals are unaffected, as is computed in the existing xVA calculation, where WWR is not included. The error size mainly depends on how close is to a normal distribution.

3.2 WWR exposure approximation

The WWR exposure in Equation (2.19) forms the starting point of the proposed WWR approximation.

The individual terms in the Taylor summation yield expressions of the form .

The essence of the WWR exposure approximation is to apply the stochastic process approximations from Section 3.1, which results in:

(3.3)

with from Equation (2.1).

The first term in Equation (3.3) accounts for the linear correlation effects, while the second term covers the non-linear correlation effects.

We introduced the following notation for simplicity and to help identify the WWR exposure drivers:

| (3.4) | ||||

| (3.5) | ||||

| (3.6) | ||||

| (3.7) |

where represents the main WWR effect resulting from the stochastic component of the funding spread. The factor corresponds to the WWR from the credit adjustment effects, where is a second-order cross-effect between the funding spread and the credit adjustment factors. Both and are linear in correlations, while is non-linear in the correlations. This is in line with [27], where linear correlation effects were identified as the main WWR drivers, while the non-linear correlation effects were of second order.

Furthermore, represents the overall Gaussian approximation error:

| (3.8) |

and is given in Equation (2.20). An approximation of the WWR exposure (3.3) is obtained by omitting and .

In summary, Equation (3.3) provides a generic expression for the WWR exposure of portfolio . Once is specified, two approaches can be taken. The first is a generic one, where we use the fact that and are available on a path level from the existing xVA calculation (without any WWR). The expectations , , can then be computed as an average over these existing paths. Alternatively, in some specific cases, can be written as a function of , such that can be approximated analytically. An example of the latter approach for an IR swap is given in Section 3.4.

The WWR approximation is flexible and allows one to quickly compute the WWR exposure for various counterparties. This property can also be exploited when one wants to see how the WWR numbers would change if the credit quality of one of the relevant parties changed. For example, consider the hypothetical case of an identical trade with a new counterparty . The first step for any approach would be to calibrate the model dynamics and correlation to the (historical) market data. For the WWR approximation, only and are required, which can be computed analytically, and no simulation is required. These results can directly be substituted into Equation (3.3), where all other components can be reused from the simulations which have already been performed.

3.3 Understanding WWR effects using the approximation

The representation of the WWR exposure in Equation (3.3) helps us identify under what conditions the various model components generate either WWR or RWR. As noted in Section 3.1, by definition, . Recall that can be interpreted as a discount factor. By construction, , and by definition, .

Consider the example where is an uncollateralized IR receiver swap, and . Then, , , , which implies

For ease of notation, we define

If is a receiver swap, then 555The ’th term determines the sign, the rest of the terms are decaying in magnitude due to the factor in , see Equation (3.7). One can examine the ’th term in the sum, decompose the payoff and eventually come to the conclusion that . , and . Hence, in this example, the term in Equation (3.3) gives rise to WWR, i.e.,

The and terms however give rise to RWR, i.e.,

So, the stochastic component of the funding spread generates WWR, while the credit adjustment effects (direct and cross) generate RWR in this example of a receiver swap with negative IR-credit correlations. This is in line with the findings from [27].

Whether the net result is WWR or RWR depends on the correlations, credit parameters, IR parameters and product type [27]. The proposed approximation helps us to understand this in both a qualitative and quantitative sense. As , we have that with , see B.1. Given model parameters and , the variance will be largest at the portfolio’s maturity . One can then verify that will be small enough to claim that generally . In this case, .

Furthermore, the third term in Equation (3.3) is of a lower order than the first two terms, as is small. 666See the analytic expression for in Equation (B.1) in B.2. Hence, the first term in Equation (3.3) is dominant in determining whether there is net WWR or RWR. This first term accounts for the linear correlation effects, which we already identified as the main WWR driver. In particular, the net WWR will depend on the sign of , which depends on correlations, credit parameters and IR parameters. This quantity can be computed analytically given a calibrated set of model dynamics and is payoff-independent. The type of payoff will determine the sign of , which, combined with the sign of , will indicate whether there is net WWR or RWR. The proposed WWR approximation thus helps to identify the WWR/RWR drivers of exposures, as only a set of calibrated model dynamics and a few straightforward calculations are required. Hence, we can conclude that the approximation preserves some form of WWR intuition.

3.4 Analytic WWR exposure approximation for an IR swap

Here, a detailed example of the WWR exposure approximation is presented for the case where is a single uncollateralized IR swap. In this case, can be expressed in terms of , such that an analytic approximation of the WWR exposure is obtained. In Section 3.4.1, is written as a function of stochastic process . Next, in Section 3.4.2, the results are combined to simplify the expectations of the form , which appear in Equation (3.3).

3.4.1 IR swap formula

Consider an IR swap under a single yield curve setup starting at , maturing at with intermediate payment dates , . To apply the Gaussian approximation from Section 3, the IR swap value needs to be written differently than the conventional formulations. In C.1, the value of an IR swap with strike and notional is expressed in terms of :

| (3.9) | ||||

| (3.14) | ||||

| (3.18) |

3.4.2 WWR approximation for an IR swap

In Equation (3.19), is expressed as a function of .

In D, the moments of a normal and generic truncated normal random variable are given in Results 1 and 2, respectively.

Using these analytic results, we write and , where is the CDF of .

Combining these moments with the results from Equation (3.19), the expectations of the form in Equation (3.3) can be written in terms of these analytic moments:

(3.20)

This expression can be computed fully analytically, provided that is known.

Product-level truncation error manifests itself after the application of the Gaussian approximation. It is the error due to the truncation of the infinite summations of in to , see Equation (3.20). The choice of an appropriate value for is discussed in Section 5.3.

The final step is to substitute the payoff-dependent expectation from Equation (3.20) into the WWR exposure approximation (3.3). Then, is the overall product-level truncation error after the Gaussian approximation is performed:

| (3.21) |

In Section 5, we will demonstrate that for sufficiently large, the error is negligible compared to and .

3.5 Scope of products and asset classes in the generic case

The Gaussian approximation method presented in Section 3.1 is based on a HW1F dynamics for IR and CIR++ dynamics for credit. The approximation in Equation (3.3) is generic and is applicable to any portfolio of IR derivatives. Here, we rely on the availability of from the xVA calculation without WWR. Therefore, any derivative that can be priced in the original xVA calculation can also be in the portfolio when approximating the WWR exposure.

The FX extension is trivial as this happens in exactly the same way as the non-WWR FX extension of xVA. The only thing one must keep in mind is that only the IR-credit relationship is captured in the approximation. Whether or not this is acceptable depends on the business model of a financial institution. Furthermore, extending to other asset classes, e.g., inflation, proceeds in a similar fashion. Also, the extension to a multi-curve framework is not a problem, and the HW1F model for IR can easily be replaced by a multi-factor IR model.

3.5.1 Special cases of fully analytical approximations

As seen in Section 3.4 for the IR swap, for some cases it is possible to find an analytical WWR approximation 777Up to the numerical computation of .. If this is desired, a portfolio of derivatives allows for an analytic WWR approximation if it can be written in terms of , such that allows for an analytic approximation. Linear IR derivatives which can be written as a monotonically decreasing function of are already covered. This can be extended to all linear IR derivatives that are not of this particular form at the cost of some additional computations. Vanilla options on linear IR derivatives are also covered. For example, consider a swaption payoff exposure: . Hence, the exposure of vanilla options on linear derivatives collapses to the exposure of the underlying derivative itself, which is covered in our framework. For exotic derivatives, like non-linear derivatives, which are not vanilla options on linear derivatives, it is less trivial to see if they allow for an analytic WWR approximation. Fortunately, there is always the generic approach which covers all derivatives that can be priced in the original xVA calculation.

To extend to FX derivatives, one would need two additional SDEs: a foreign short-rate process for IR and an FX process to convert currency into . The original IR process is then denoted as . Furthermore, correlations need to be imposed between all the processes, again with the assumption of independent counterparties. For both IR processes, we use the HW1F model as before. The dynamics will be given under the risk-neutral measure. When setting up a Monte Carlo simulation, all processes must be under the same measure [9]. Hence, we use a change of measure and write the dynamics under the risk-neutral measure. This will lead to an additional term in the drift, which is a quanto correction term, see B.1. For the FX process, , we choose log-normal dynamics, see B.3. Next, we write this in integrated form, and express it as , where , with . The three stochastic processes , , are correlated normals with zero mean. Then, is normal with zero mean and a variance where the correlations are included.

Next, we examine an FX derivative, for example, an FX forward contract with maturity . This payoff can be written in terms of the quantities , and . In turn, these quantities can be expressed in terms of the corresponding integrated drift and integrated stochastic processes. Using the Gaussian approximation for the stochastic processes from Section 3.1, can be approximated in terms of . Further manipulations result in an expression of in terms of . See E for a detailed derivation of this example. Using this expression, we decompose the expressions in terms of moments of a normal and truncated normal distribution. This approach can easily be extended to all linear FX derivatives.

4 Error analysis

In the proposed WWR approximation, various errors appear. First, from Equation (2.20) is a truncation error from the truncated Taylor series expansions. Next, from Equation (3.8) is the Gaussian approximation error. Finally, for specific derivatives , a product-level truncation error is introduced in Equation (3.21). In general, there are two types of errors: truncation errors and Gaussian approximation errors.

Here, we dive further into the two error types. The goal is to find out when the approximations are working well and when not; and to find error bounds where possible. In particular, we look at the impact of various model parameters on the quality of the approximations, including extreme conditions. In this way, it becomes apparent when the approximation can safely be used and when some more caution is required.

4.1 Truncation error

First, we examine from Equation (2.20), where the contributing terms all contain Taylor sums of the form . Here, are stochastic integrals with for all . The variance grows through time, as is the integrated stochastic part of the dynamics . Consider a portfolio with maturity . If the error for is sufficiently small, then the same holds for with . Therefore, only is considered in the error analysis.

The terms of in Equation (2.20) all contain an expectation of the form

, which we aim to bound in the norm.

The Cauchy-Schwarz inequality gives

| (4.1) |

First term

For the first term in the RHS of Equation (4.1), we use that , i.e., s.t. . Hence,

| (4.2) |

Next, we use the correlation definition for two correlated random variables and to obtain the following inequality:

| (4.3) |

with correlation and .

Using this result, we can bound in Equation (4.2), as follows:

| (4.4) |

Second term

Since the approximation is generic, the second term at the RHS in Equation (4.1), which is the product-specific component of the error, can be computed straightaway from the available grid of simulated future portfolio values. Hence, we write

| (4.5) |

In the example of an IR swap, see Section 3.4, an analytic bound can be derived, such that . See C.3 for a derivation of in this case.

Overall error bound

Plugging Equations (4.2) and (4.5) into Equation (4.1) yields the following generic bound

(4.6)

where the remaining expectation depends on the specific error under consideration, e.g., , and is bounded in Equation (4.4).

The error bound in Equation (4.6) clearly shows an exponential decay of the error, so only a few terms will be needed for a high-precision approximation.

This is only relevant if the higher order (cross-)moments in Equation (4.4) are finite.

In F, the obtained error bound is applied to from Equation (2.21), to obtain an explicit form of the error bound.

Looking at Equation (4.6), given a portfolio and a number of terms in the Taylor approximation, the error will be driven by , which is bounded in Equation (4.4) based on higher-order moments of and . Since both and are in several cases composed of multiple stochastic integrals 888For , , , . For , , , . For , , ., the leading order of the error will be the higher-order (cross-)moments of these stochastic integrals. For simplicity of the argument, we focus on .

As observed before, as increases, the distributions of will increase in magnitude; a pattern which the error will follow, depending on the shape of the exposure . For example, for an IR swap, the exposure decays towards maturity, which dampens the effect of an increased truncation error for larger . Furthermore, given a fixed value of mean reversion parameter in the model dynamics, increased volatility will result in an increase in error. Alternatively, for a fixed value of , a lower magnitude of will increase the error, where the effect is larger for larger values of .

More details on the impact of the model parameters will be given in Section 5.3, where also the interplay with the Gaussian approximation error is discussed.

4.2 Gaussian approximation error

In Section 3.1, the Gaussian approximations of the stochastic processes that appear in the exposure formula are introduced. When computing cross-moments, stochastic processes are approximated in terms of times a scaling factor, which depends on the ratio of the variances and the correlation between the two variables. For the integrated stochastic processes, recall that . When approximating WWR exposure, this results in Gaussian approximation error as defined in Equation (3.8).

The Gaussian approximation is done after truncating the Taylor series, so it is only applied to the first terms in the Taylor series. Furthermore, it is applied in the context of cross-moments, i.e., the marginal distributions are left untouched. Covariance, being a linear measure of joint variability, looks at the first-order relationship between two variables. Since it is at first order, the dependence can be summarized through a set of correlated Gaussians, replacing the original joint distributions. The information that is lost in this step mainly relates to the tails. However, as we are looking at first-order dependence, it is key to get the bulk of the distribution correct, and it is justified to lose some information from the tails. Further justification of the loss of tail information is already given at the start of Section 3. This will provide practitioners with an intuitive and fast way to get further intuition on WWR exposures.

Naturally, the further away the distribution of is from a Gaussian, the worse the approximation will be. Here, the (a)symmetry of the original distribution plays a role, as well as the fatness of the tails. Though it is difficult to control this error at a portfolio level, at a lower level, it can be quantified. The error may be measured by comparing the CDF of to a corresponding normal distribution with equivalent variance, i.e., . A way to measure the distance between the two CDFs is the summed squared distance between the two, which is an -norm. If an empirical CDF of is available, this is equivalent to computing the Cramer-von Mises test statistic. Alternatively, a Wasserstein distance can be used.

More details of the impact of the model parameters will be given in Section 5.3, where also the interplay with the truncation error is discussed.

5 Numerical results

To demonstrate the effectiveness of the proposed WWR approximation, various examples with different portfolio compositions are considered. A Monte Carlo simulation is used for the benchmark numbers, with paths and dates per year. Algorithm 1 summarizes the calculation procedure.

-

1.

for a generic portfolio, is computed through Monte Carlo;

-

2.

for an IR swap, is approximated using Equation (3.20).

We use market data that is representative of the market situation in April 2020, following the market stress in March 2020 [27]. At that time, interest rates were negative and continued to drop, and credit quality was deteriorating for all ratings. In particular, we use yield curves with low or negative interest rates, and credit curves corresponding AAA and BBB ratings. The detailed set of model inputs can be found in B.4.

The IR-credit correlations are chosen manually, but we focus on negative correlations to match the WWR scenario for receiver swaps in case of a negative correlation between IR and funding spreads. For the stochastic funding spread assumption, this implies negative IR-credit correlations. This adverse relationship between IR and credit is also understood through the empirical evidence that in case of an IR drop, credit spreads will widen in response to a flight-to-quality by investors. These market moves are typically observed during a bear market (financial downturn). In general, the lower the credit quality of a party, the higher the IR-credit correlation is in the absolute sense. The reverse of this argument holds for financially good times: if the default frequency goes down, credit spreads will go down, while at the same time, the central bank might raise IR to counter inflation. In practical settings, one cannot handpick correlation values, but a historical calibration can be performed based on the correlation between time series. For example, the correlation can be calibrated by taking the terminal correlation between the swap rate and CDS par rate as generated by the model setup, and match that to the historical correlation between those quantities.

When presenting and WWR numbers, the percentage of w.r.t. , i.e., , is denoted by ‘’. Furthermore, ‘ RD’ refers to the relative difference w.r.t. the Monte Carlo result, i.e., . This puts the WWR approximation error in the perspective of the overall exposure size, summarized in the numbers. The runtime (in seconds) refers to the extra computing time to compute the WWR according to the specified method.

In Section 5.1, the performance of the approximation is assessed in the case of a single IR swap. Then, in Section 5.2, we examine the practically relevant case of a multi-currency portfolio of IR swaps. The approximation errors are analyzed in Section 5.3. Finally, the approximation of WWR sensitivities is discussed in Section 5.4.

5.1 Single IR swap

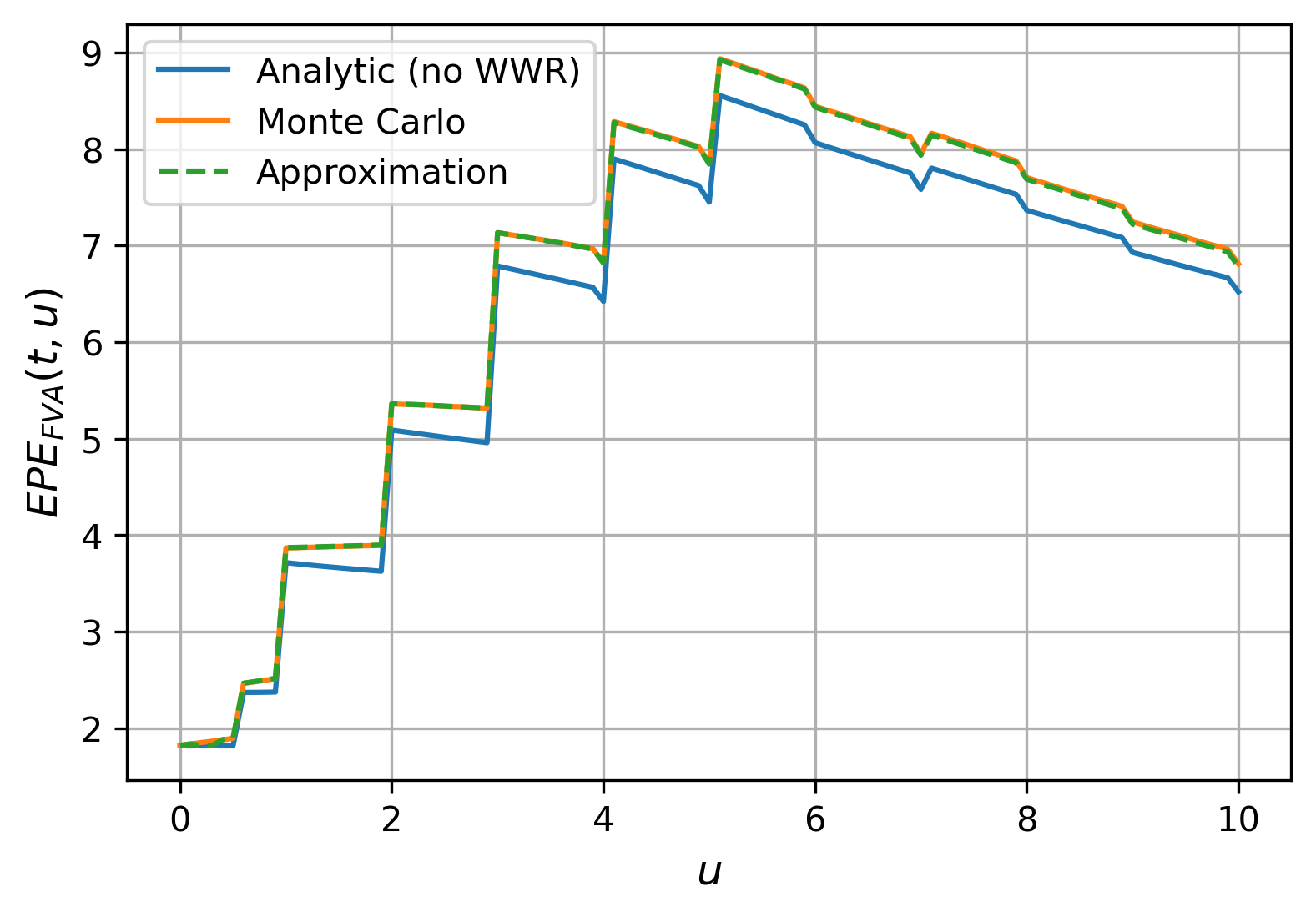

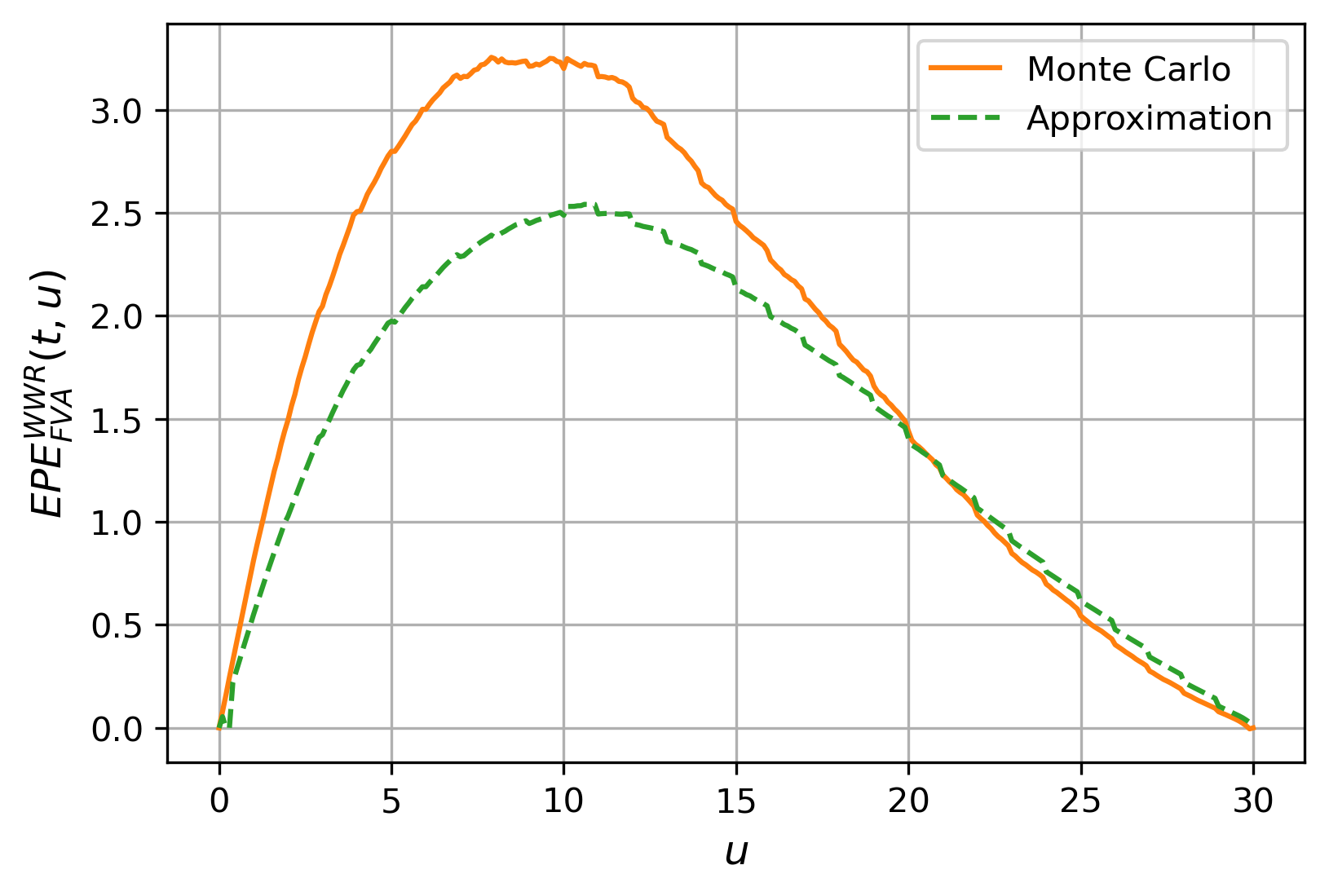

The first example is that of a single receiver IR swap , expiring in year and maturing in years, paying yearly coupons on both legs, with zero margin on the floating leg, based on a notional such that the value can be interpreted as a basis point value. The model parameters used in this example are given in B.4.1. For a receiver swap, the aforementioned market conditions are an example of WWR, with an adverse relationship between IR and credit. For a single IR swap, the fully analytic WWR exposure approximation from Section 3.4 can be used.

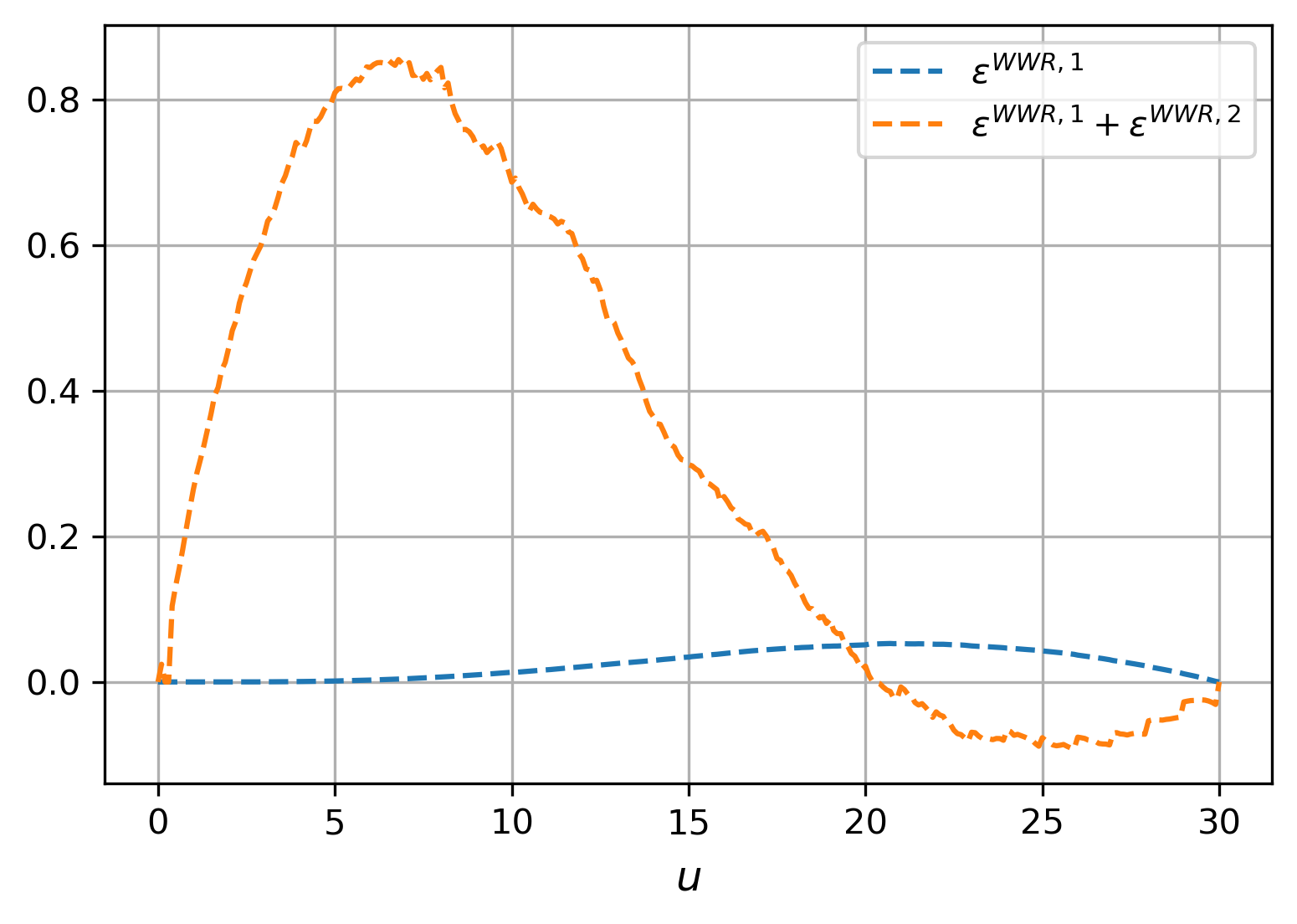

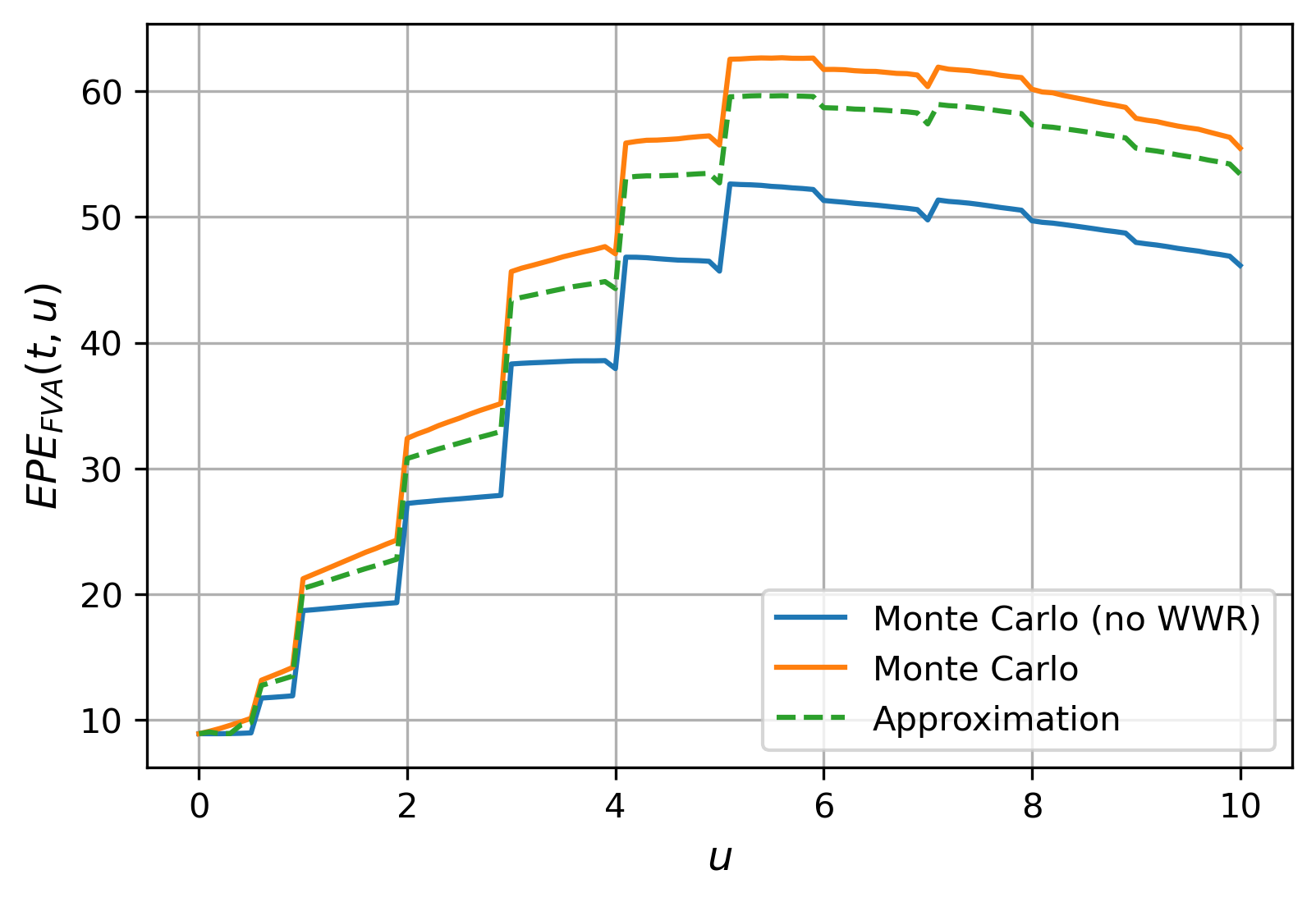

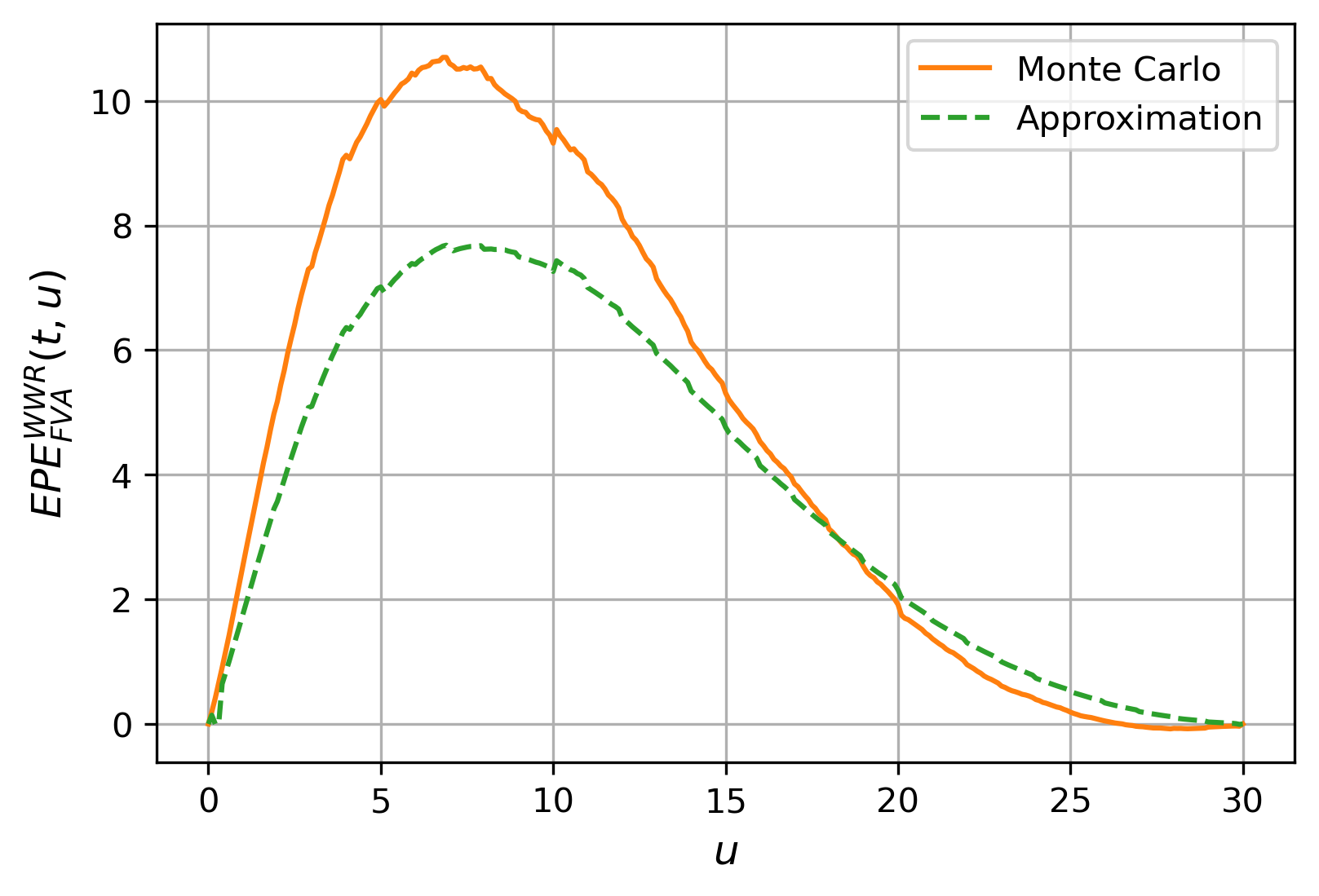

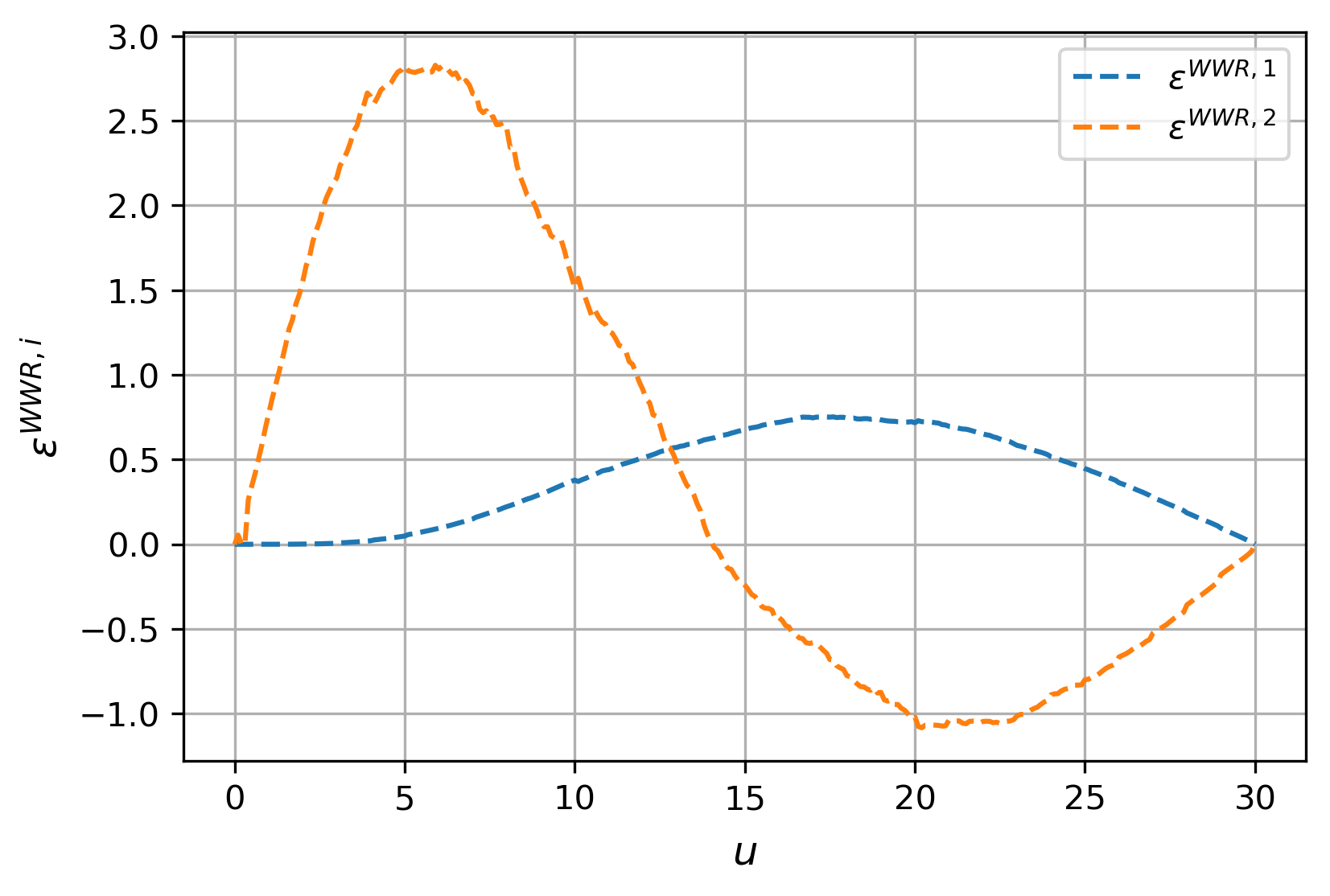

The various exposures (for the first out of years) and approximation errors are presented in Figure 1. From Figure 1(a), one can immediately conclude that the WWR component of the exposure needs to be included in the computation. The approximation captures the same WWR pattern as the Monte Carlo benchmark, albeit at a slightly different scale, which is also visible from Figure 1(b). This is the result of the overall approximation error as plotted in Figure 1(c). This figure also shows that the Taylor series approximation and the Gaussian approximation cancel out to some degree. Furthermore, the product-specific Taylor approximation from Section 3.4, which allows WWR exposures to be computed analytically, is of high quality. All in all, in the presented example, the WWR exposure approximation is of high quality.

Table 1 reports the numbers and WWR runtimes corresponding to the exposures from Figure 1. Naturally, the high approximation quality is preserved when looking at numbers. The WWR contribution, being roughly of the overall exposure, is non-negligible. Also, looking at the runtimes, the approximation yields a significant speedup of more than 20 times compared to the benchmark methodology to compute the WWR component. Hence, next to being of high quality, the approximation is also fast, and the approximation runtime does not scale in the number of derivatives. In this particular example, the analytic approximation from Section 3.4 is used. Hence, the computation of is analytical, and therefore slightly faster as the generic approach where this expectation is computed as a Monte Carlo average over the existing set of simulated paths.

| RD | Runtime (sec) | ||||

|---|---|---|---|---|---|

| Analytic (no WWR) | 122.3386 | 0.0000 | 0.0000 | 0.0000 | 0.00 |

| Monte Carlo | 127.0546 | 4.7160 | 3.8549 | 0.0000 | 6.48 |

| Approximation | 126.5516 | 4.2130 | 3.4437 | -0.0040 | 0.27 |

5.2 Multi-currency portfolio of IR swaps

The encouraging results for the single IR swap motivate us to look at a practically relevant example. Therefore, we consider a portfolio of swaps in multiple currencies, similarly as in [11, Section 3.2], i.e., portfolio in domestic currency , with also trades in foreign currencies . In this case, dynamics are required for , and for every foreign currency two processes are needed: and . Naturally, all these processes are correlated with each other, as well as with the credit processes. The portfolio contains swaps in domestic currency , and swaps in foreign currency for each of the foreign currencies, and is then denoted as:

| (5.2) |

Here, swap is in foreign currency at time , and is then converted to domestic currency using the FX rate at that date, i.e., .

For the modelling, we use HW1F for the IR processes, and a GBM process for the FX rates. See B for the model dynamics in the form introduced in Section 2.1.

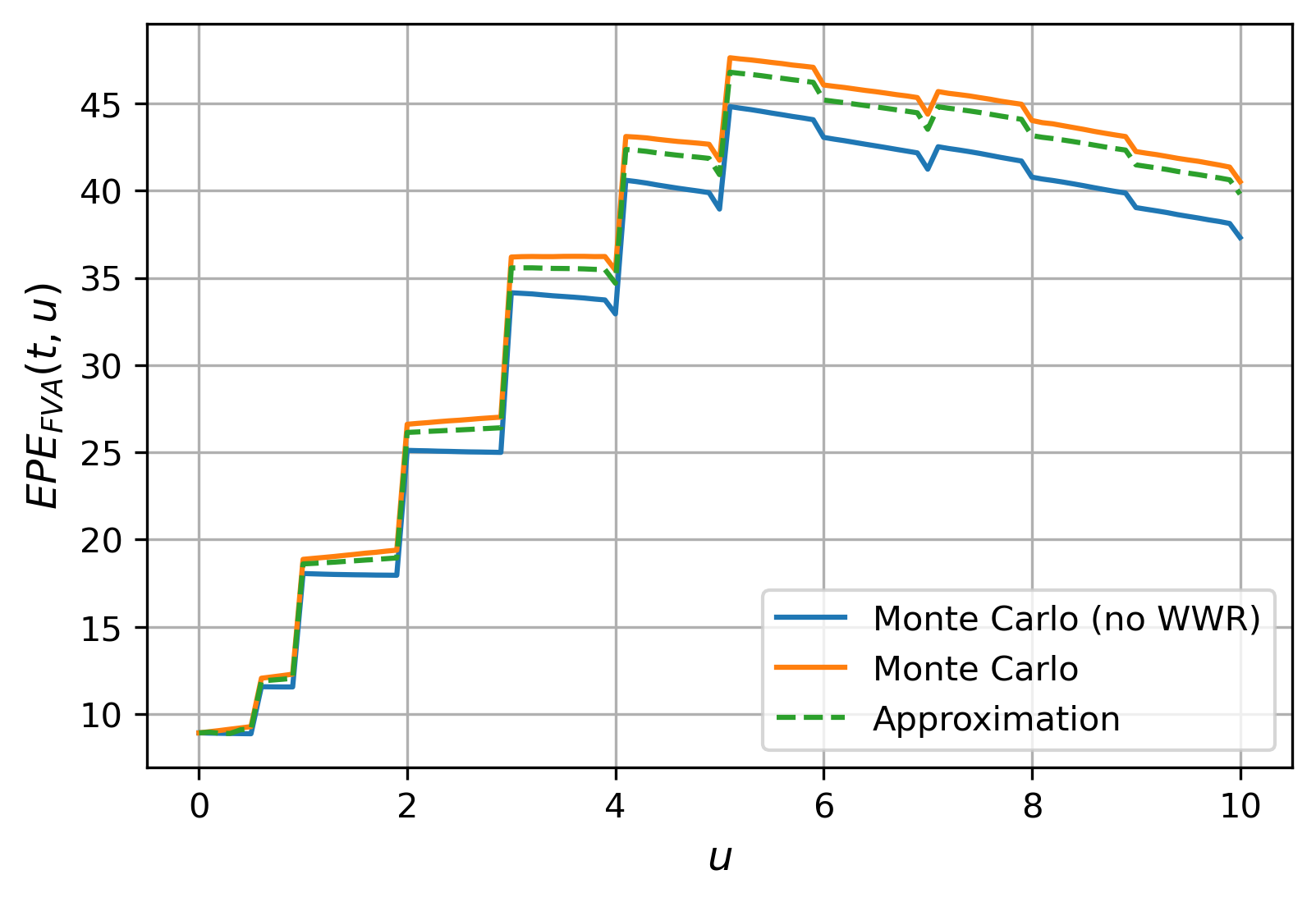

As an example, consider the currencies (EUR, USD, GBP) , such that the following processes are involved: , , , , , , . The example portfolio consists of two swaps in each currency, i.e., . The notional is 10k for all swaps, such that the results can be expressed in basis points, similarly to the single IR swap case. The model parameters used in this example are given in B.4.2. All swaps are receiver swaps, have a maturity of 30 years, with a yearly frequency, and either an expiry 1 year or 10 years from now. In this case, the generic approximation from Section 3.2 is used, where expectations , , are computed using Monte Carlo simulation, since everything has been pre-computed in the xVA calculation where no WWR is present.

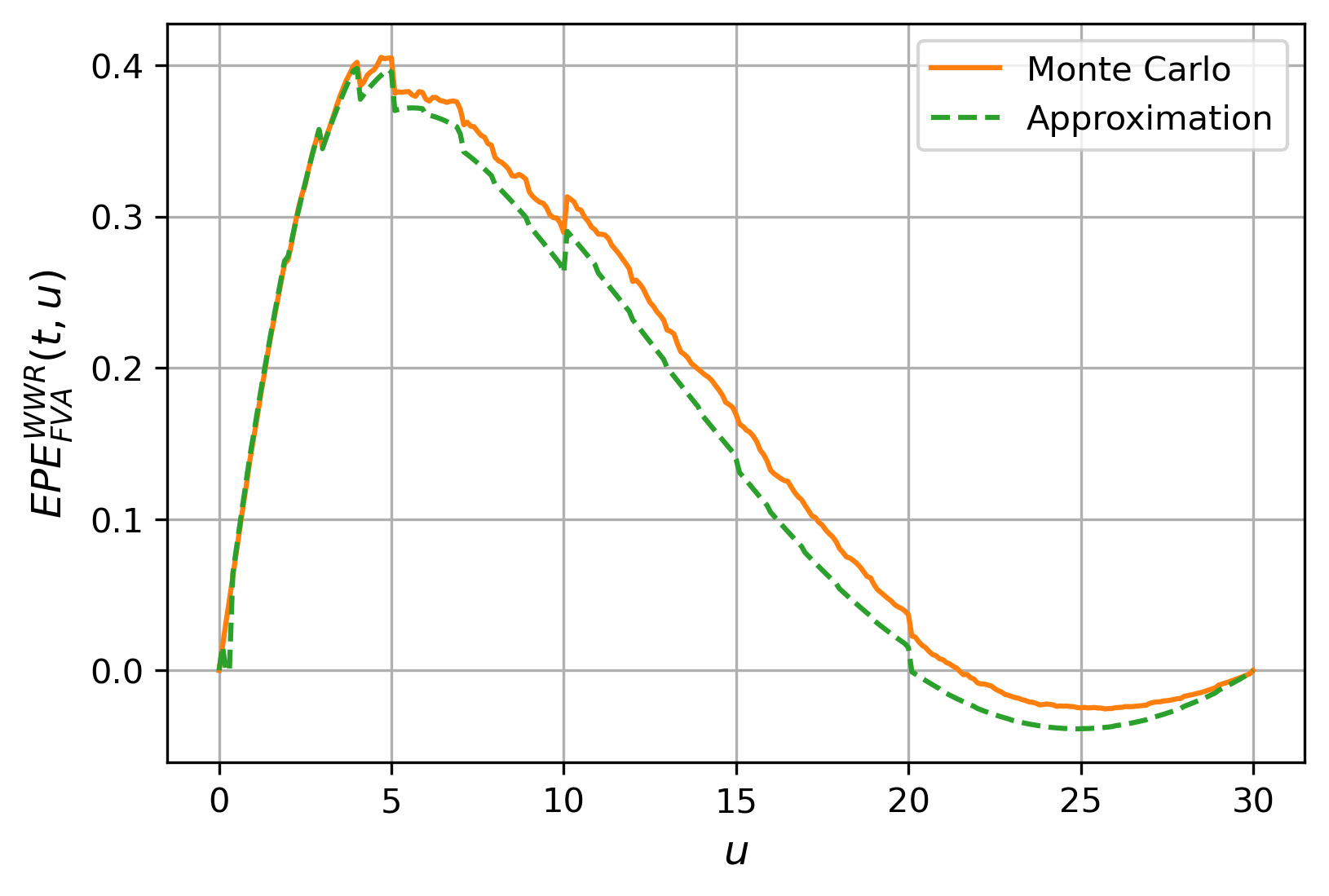

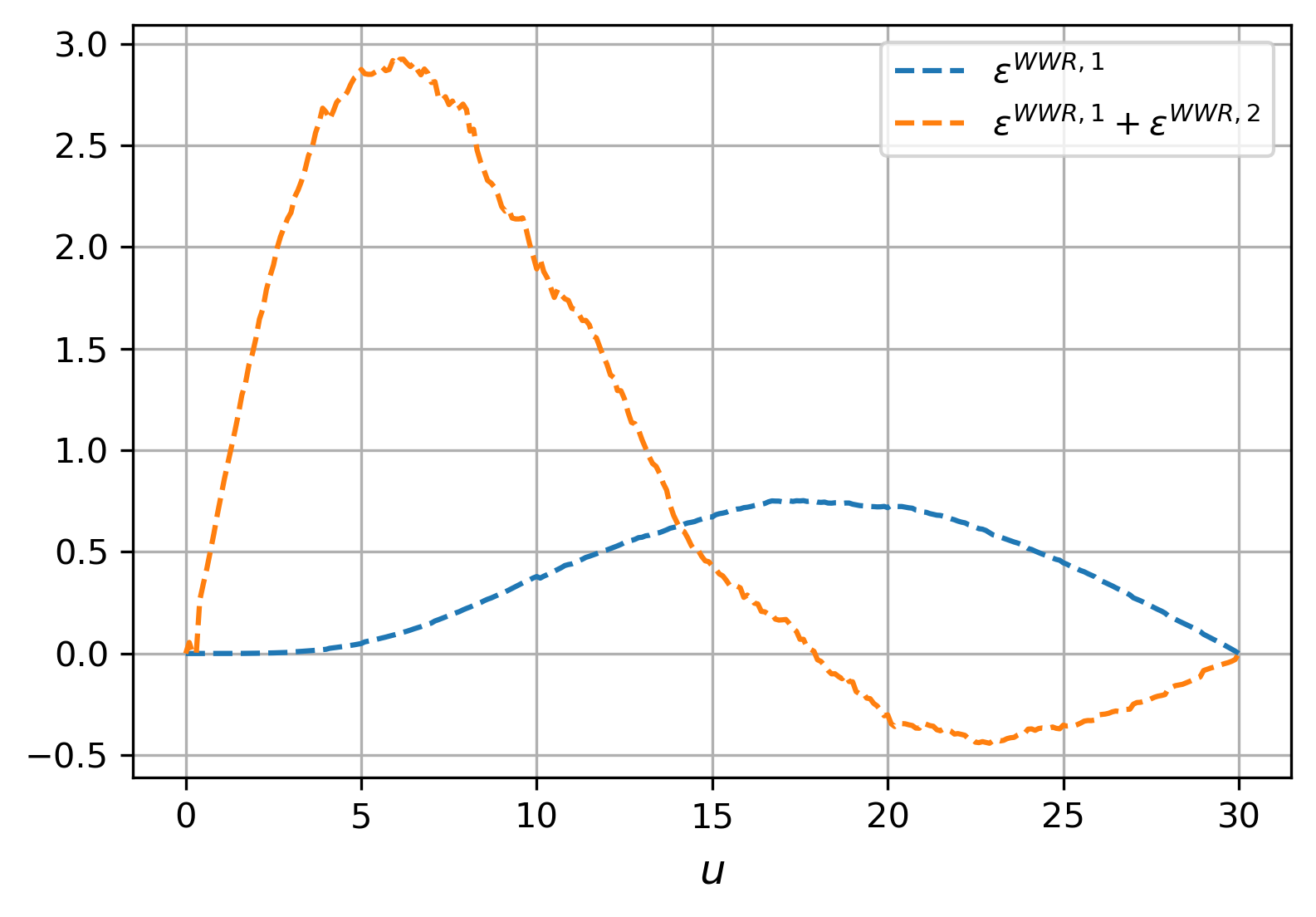

The various exposures and approximation errors are presented in Figure 2. Again, the WWR is non-negligible, and the approximation captures the global pattern of the WWR, despite a larger difference in WWR exposure compared to the single IR swap case, see Figure 2(b). The majority of the increase in overall approximation error can be attributed to the Gaussian approximation error , see Figure 2(c).

When looking at the approximation error in terms of the difference, Table 2 shows that the relative difference is roughly . We are approximating the WWR that the full model generates based on the chosen model dynamics. It is key to understand that this reference WWR is not a ‘true’ market value to begin with but a consequence of model choices. Despite not capturing all the WWR from the reference, the approximation gives a useful and practical indication of the amount of WWR in a portfolio. Especially due to the fast computation when compared with the Monte Carlo benchmark.

| RD | Runtime (sec) | ||||

|---|---|---|---|---|---|

| Monte Carlo (no WWR) | 658.4338 | 0.0000 | 0.0000 | 0.0000 | 0.00 |

| Monte Carlo | 713.0611 | 54.6272 | 8.2965 | 0.0000 | 7.59 |

| Approximation | 703.2882 | 44.8544 | 6.8123 | -0.0137 | 0.47 |

The approximation errors presented for this directional portfolio of linear derivatives can be considered as a lower bound for portfolios with more complicated derivatives. Given that xVA makes all derivatives non-linear, the presented portfolio is a simple but relevant one, as many of these portfolios exist in practice.

5.3 Error analysis

In the various Taylor approximations, a truncation point need to be chosen, i.e., and in Equation (2.20), and in Equation (3.20) in the case of a fully analytic WWR approximation for an IR swap.

Choice of

The use of is hard-coded in Section 2.2.3, and results in a first-order approximation of the credit adjustment factors, i.e., . Consecutively, the Gaussian approximation is applied to these terms of the Taylor approximation. The Gaussian approximation will be worse for higher-order Taylor terms if the distribution of the approximated variable is far from normal. This implies that the approximation quality cannot be improved by increasing . By , the Gaussian approximation is limited to first-order terms, limiting the Gaussian approximation error . At the same time, the Taylor truncation error will be larger in absolute sense for lower . Therefore, there is a tradeoff between and when choosing . In some cases, for example, when the IR volatility dominates, and the credit volatilities are low, yields a slightly improved overall approximation than . However, since the credit distributions are typically not that close to Gaussian, the choice of , leading to a first-order approximation, is appropriate and no calibration of this approximation parameter is required.

Choice of

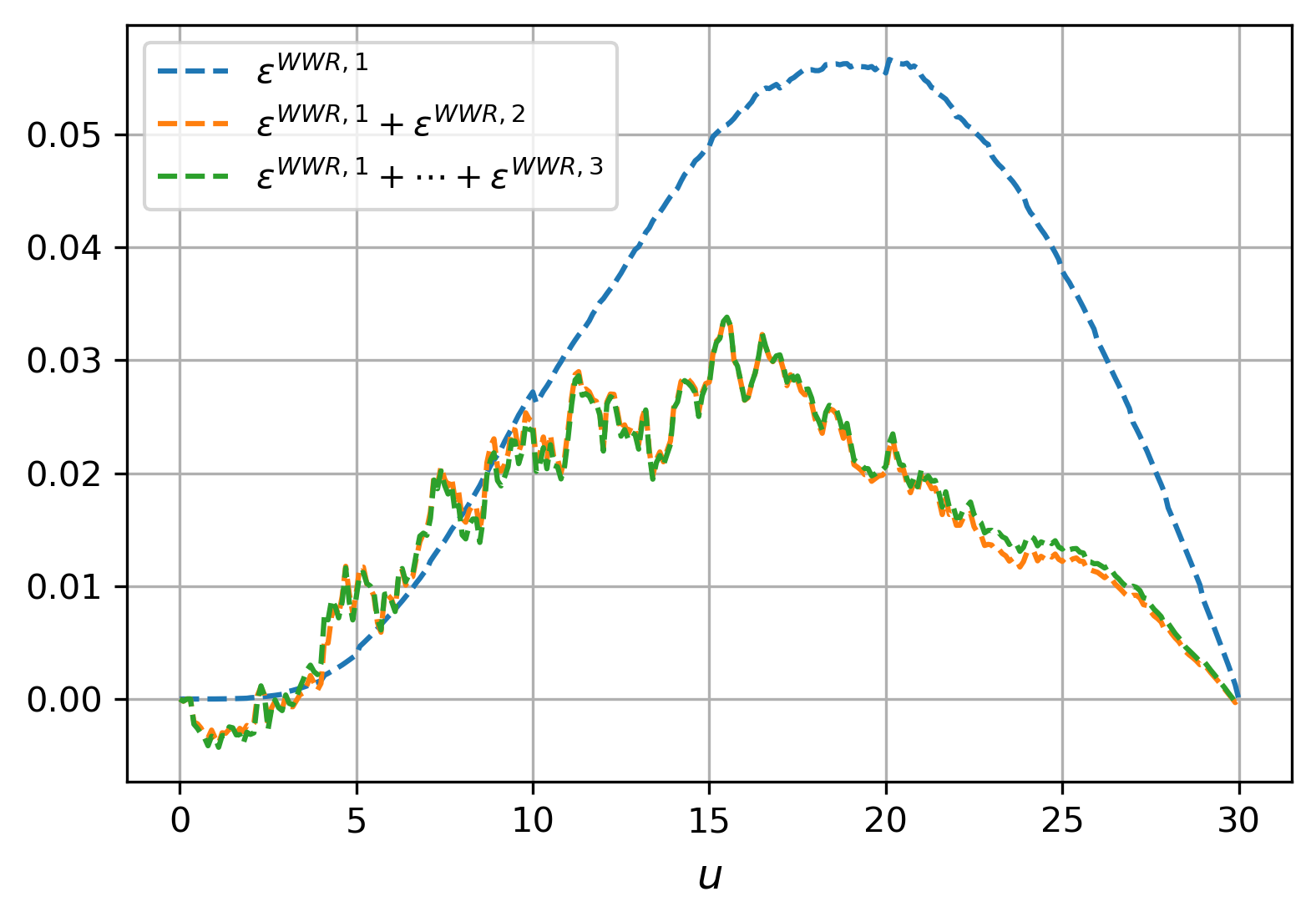

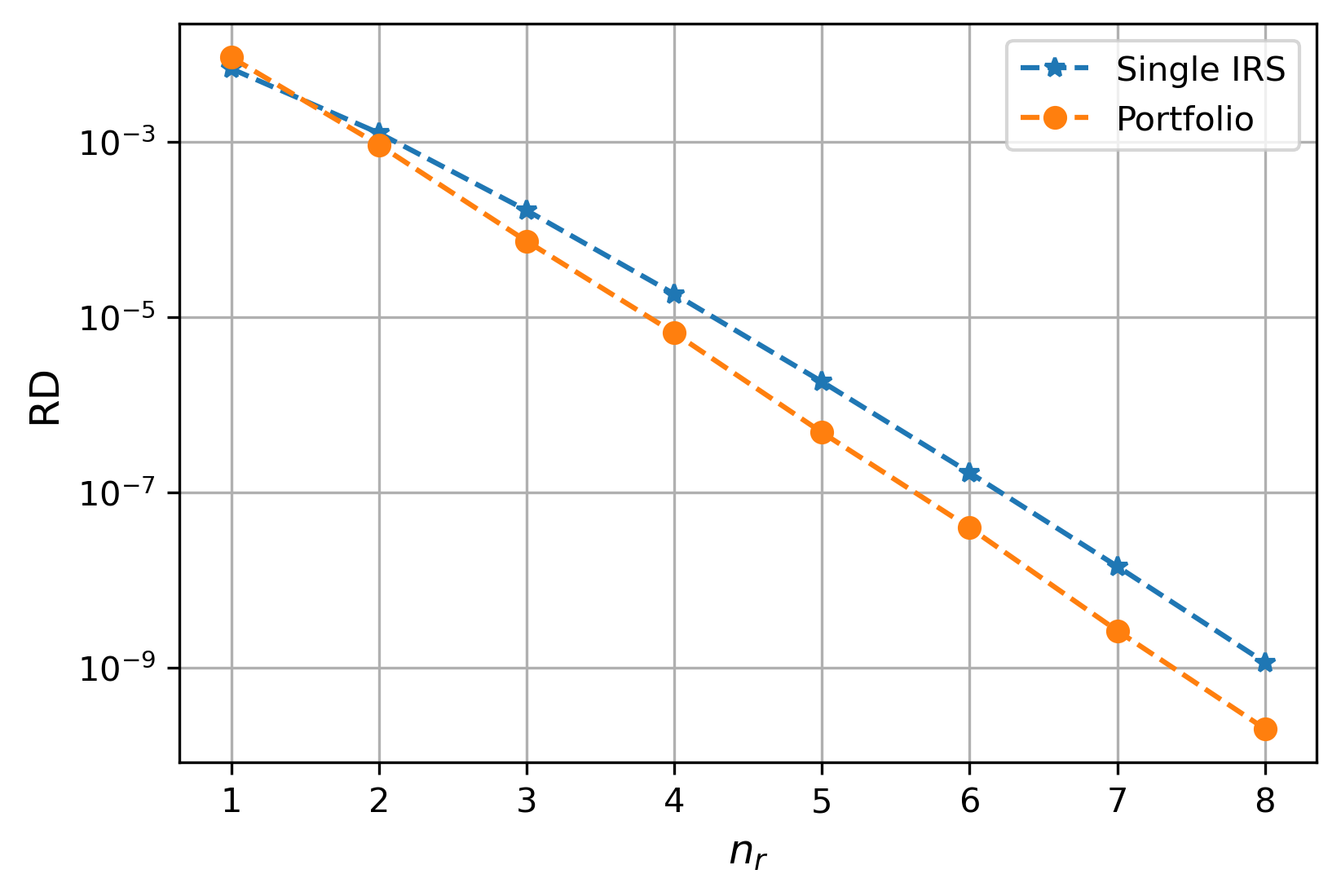

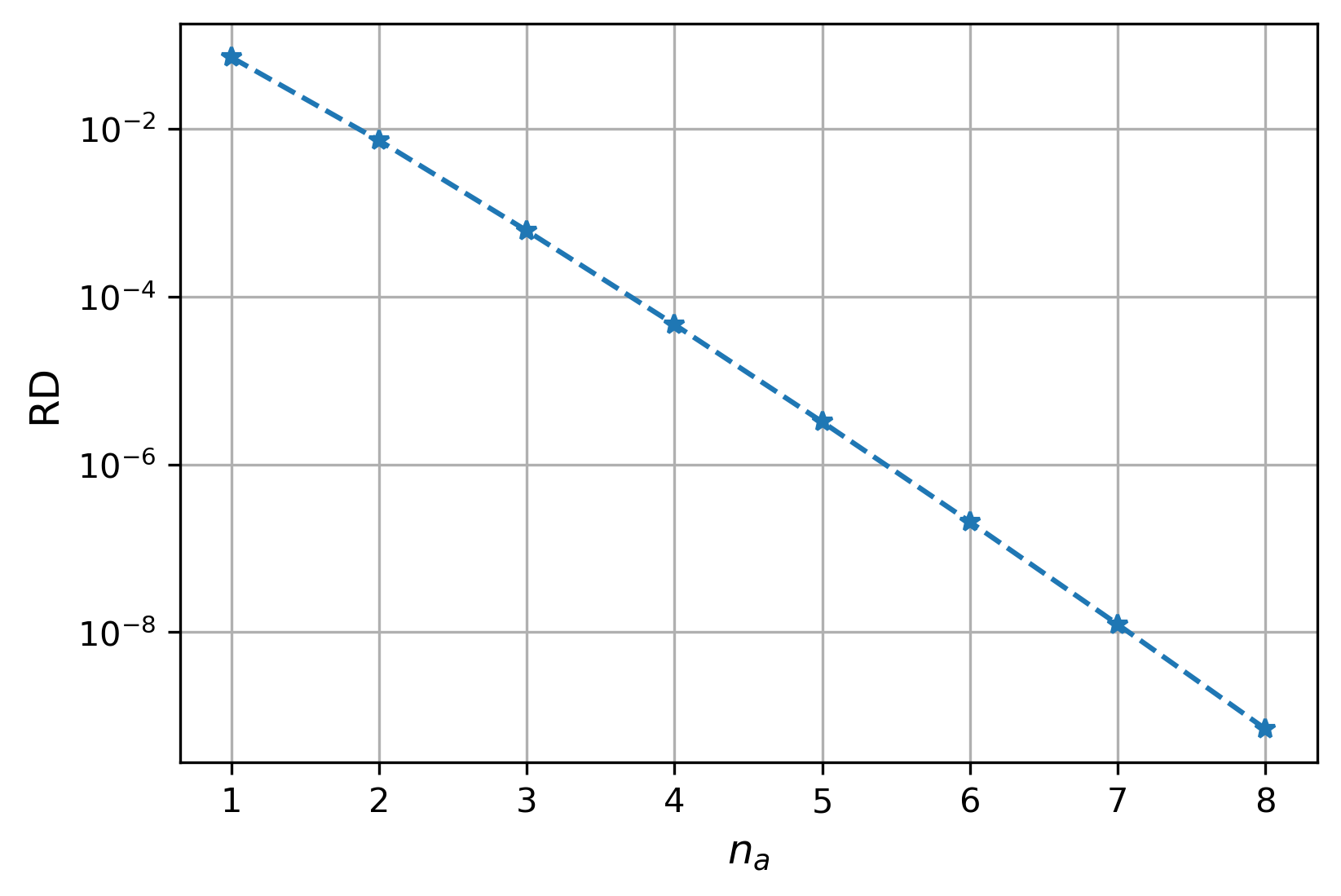

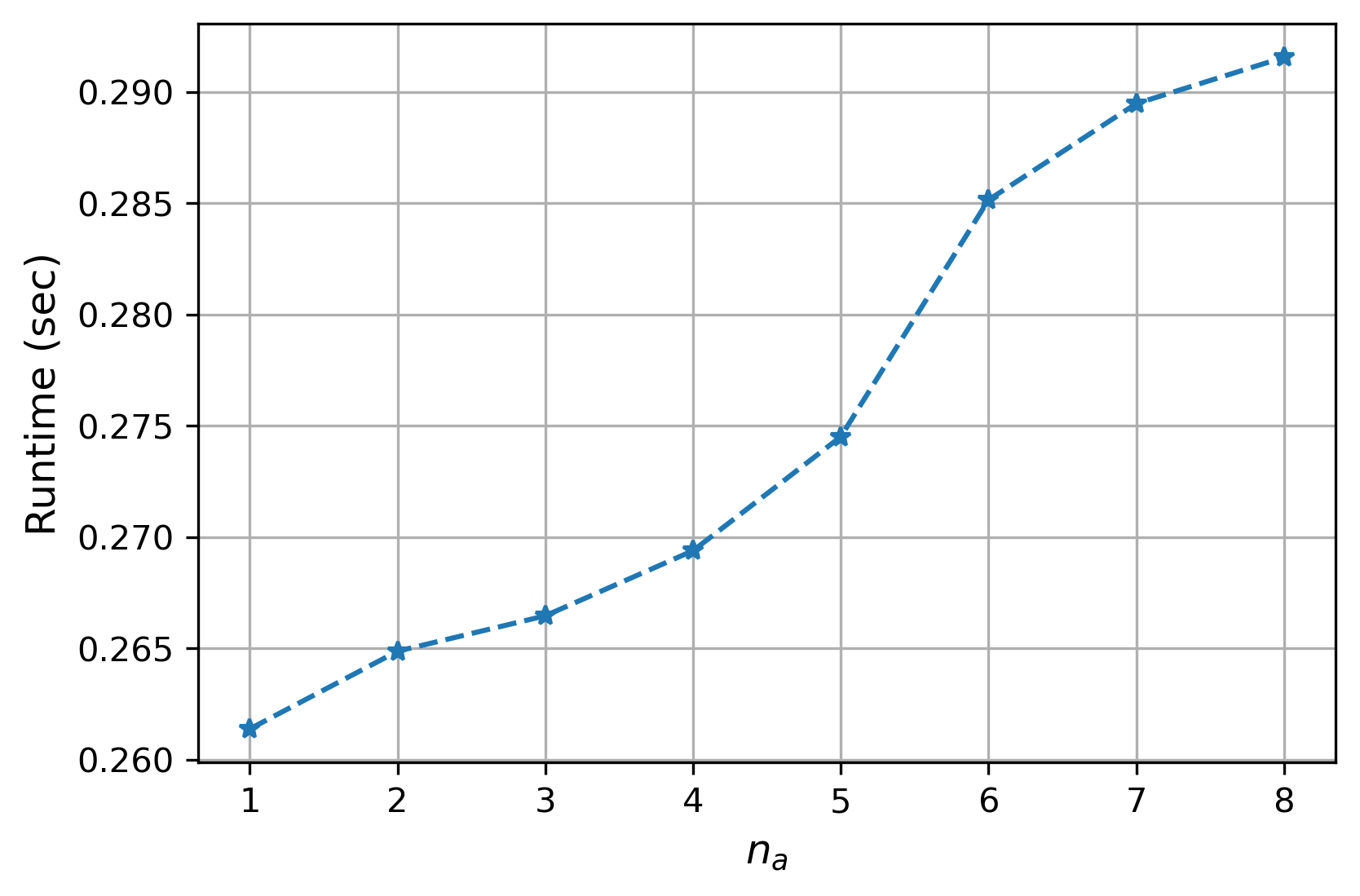

Given , from Equation (2.19) is the next truncation point that needs to be chosen. Since represent the truncation of the Taylor approximation involving , and given that is normally distributed, no tradeoff with the Gaussian approximation needs to be considered. In the results presented so far, has been used. From Figure 3 it is clear that the choice of is suitable, given the tradeoff between accuracy and speed, and no further significant improvement in accuracy can be achieved. Alternatively, the number of terms can be made adaptive by imposing a stopping criterion on the contribution of the ’th term, but this will only lead to marginal improvement of accuracy. In both cases, no calibration of the approximation parameter is required.

Choice of

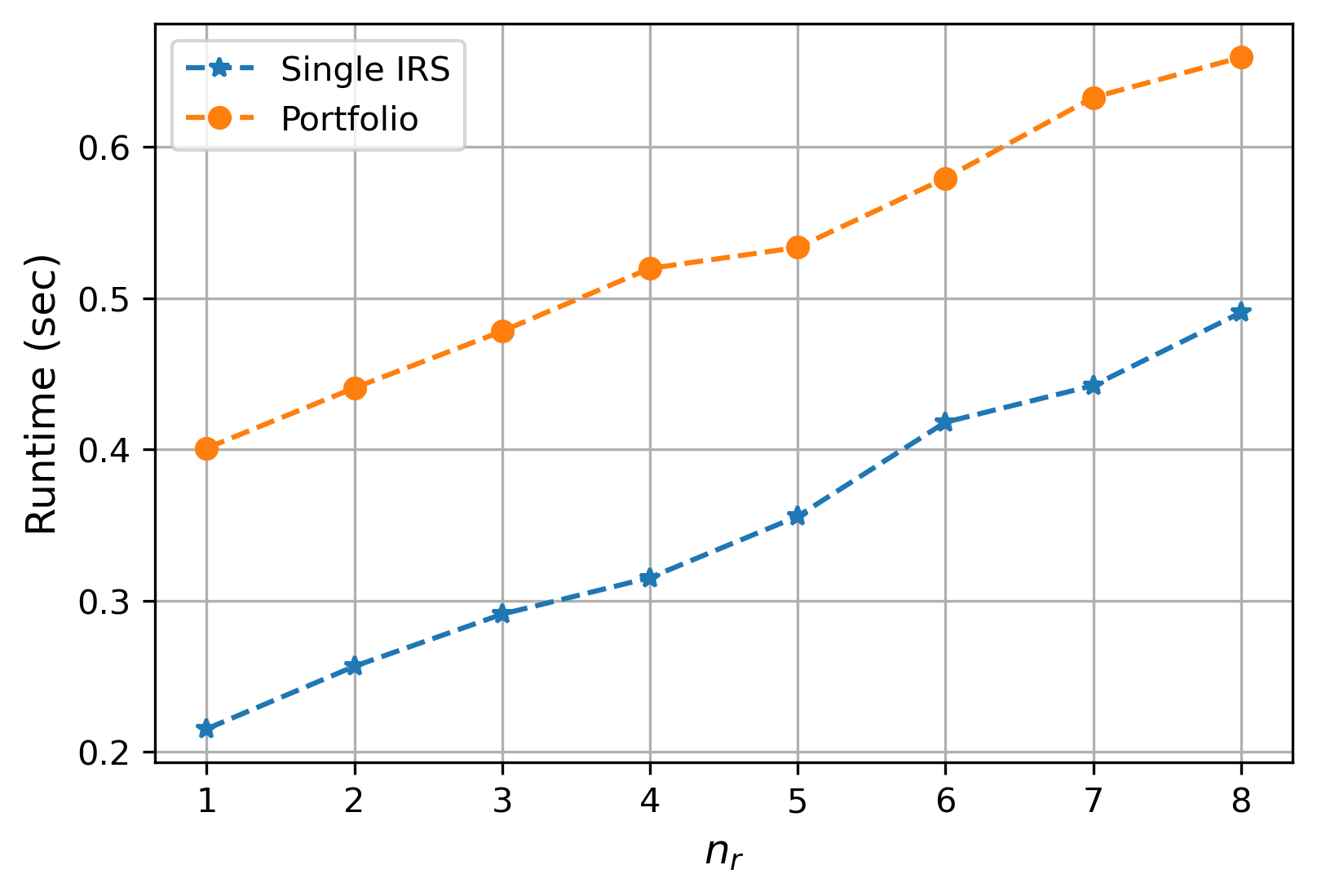

For the fully analytic approximation for an IR swap from Section 3.4, an additional truncation of a Taylor series is done in Equation (3.20) at the ’th term. As this involves the truncation of , and since is Gaussian, no tradeoff with the Gaussian approximation needs to be considered. In the results presented so far, has been used. From Figure 4 it is clear that the choice of is suitable. Compared to from Figure 3, the impact on the approximation runtime is much smaller. Recall from Figure 1(c) that has negligible impact on the overall approximation error. Alternatively to , the number of terms can be made adaptive in a similar fashion as .

Impact of model parameters

From Section 4 it is clear that in some situations the approximation performs less well. The distributions of will increase in magnitude as increases, a pattern which the Taylor truncation error will follow. However, for exposure profiles that decay towards maturity, for example, for (a portfolio of) IR swaps, the increased truncation error for dates closer to maturity is dampened. Looking solely at the truncation error, increased credit volatility and will result in an increased error, and lower mean-reversion and will also increase the truncation error. On the other hand, the Gaussian approximation error is larger when the distribution of deviates from a Gaussian, where the symmetry and tails of the distribution play a role. For the Gaussian approximation, as opposed to the truncation error, larger values of and lead to less normality in the credit distributions, increasing the error. As for the truncation error, for increased credit volatilities and , the credit distributions deviate from Gaussian, such that the Gaussian approximation error increases. This effect is especially visible for higher values of combined with low , since the credit of institution enters through both the funding spread and the credit adjustment factor, whereas ’s credit enters only through the latter. Furthermore, for larger IR volatility, the amount of WWR increases, and the overall approximation error increases along with it. Finally, increased IR-credit correlation magnitudes also result in larger approximation errors.

In stressed market scenarios, the approximation has its limitations, but as the analysis above illustrates, there is a sufficient level of understanding what the impact would be of various market stresses. In Figure 5 a stressed scenario is considered for the same portfolio as in Section 5.2. The model parameters used in this example are given in B.4.3. In comparison with Figure 2, the error pattern is comparable, but with a different scaling. A part of this scaling is explained by the larger degree of WWR that is present in this example.

In terms of , see Table 3, the approximation error has indeed also increased, but is still at an acceptable level for the approximation to be practically relevant, especially given the large degree of WWR that is captured.

| RD | Runtime (sec) | ||||

|---|---|---|---|---|---|

| Monte Carlo (no WWR) | 795.4959 | 0.0000 | 0.0000 | 0.0000 | 0.00 |

| Monte Carlo | 935.8899 | 140.3940 | 17.6486 | 0.0000 | 7.83 |

| Approximation | 908.3324 | 112.8365 | 14.1844 | -0.0294 | 0.53 |

5.4 Sensitivities

Next to the values, the relevant hedge ratios are required from a risk-management point of view. When computing these sensitivities w.r.t. market inputs, the modelling assumptions play a significant role, impacting first-order delta and vega risks, and adding cross-gamma risks between the risk factors.

Using a Monte Carlo simulation to calculate , the corresponding sensitivities w.r.t. the various risk drivers can be computed efficiently using Algorithmic Differentiation (AD) techniques. However, for a transparent implementation, some institutions resort to Finite Difference (FD) approximations, which require at least one recalculation of the entire Monte Carlo calculation chain for each sensitivity. We approximate the sensitivities using FD, both for the Monte Carlo benchmark and the Gaussian approximation. The latter also allows for several semi-analytic sensitivities, but for the proof of concept, we employ the generic FD method.

Following from Equation (2.6), the sensitivity of w.r.t. risk factor is given by

| (5.3) |

With the WWR approximation, like for value, only the WWR component of the sensitivities, i.e., , is approximated using the Gaussian approximation. The other part of the required sensitivity, , is taken from the current xVA calculation, where independence between the funding spread and the market risks is assumed. In this way, the WWR approximation error will not affect the ‘independent part’ of the sensitivities.

From a risk-management and hedging perspective, the most relevant first-order risks are the deltas and vegas. The IR and FX risks are the most relevant, as xVA desks at financial institutions are likely to hedge these.

In addition to the first-order risks, the cross-gamma risks are insightful, especially for WWR effects. These cross-gamma effects are always present, even if correlations are zero, but with non-zero correlations, they become more relevant. Especially the cross-gamma risks with funding risk and market risk are essential: the funding risk increases if the market risk (exposure) increases. Cross-gamma risks are difficult to hedge, but computing them will at least give us insight into this risk for a portfolio under consideration.

| Monte Carlo | Approximation | RD | ||

| Value | 658.43 | 54.63 | 44.85 | -0.0137 |

| IR delta EUR | -32680.74 | -1629.76 | -1627.51 | 0.0001 |

| IR delta USD | -25311.11 | -925.64 | -801.76 | 0.0047 |

| IR delta GBP | -34115.96 | -1154.91 | -1042.12 | 0.0032 |

| FX delta EUR/USD | 202.14 | 16.70 | 10.22 | -0.0296 |

| FX delta EUR/GBP | 221.77 | 15.83 | 10.18 | -0.0238 |

| Credit delta I | -4360.76 | 80.68 | 65.84 | -0.0035 |

| Credit delta C | 932.22 | 79.04 | 67.02 | -0.0119 |

| IR vega EUR | 729.18 | 170.16 | 212.04 | 0.0466 |

| IR vega USD | 793.98 | 146.77 | 76.29 | -0.0749 |

| IR vega GBP | 1014.62 | 166.41 | 87.63 | -0.0667 |

| FX vega EUR/USD | 21.10 | -29.75 | -12.12 | 2.0380 |

| FX vega EUR/GBP | 19.56 | -39.78 | -16.16 | 1.1682 |

| Credit vega I | -4.55 | 872.67 | 800.98 | -0.0826 |

| Credit vega C | 0.02 | -215.31 | -207.46 | 0.0365 |

| IR EUR / credit I cross-gamma | 328215.00 | -2410.00 | -2372.00 | 0.0001 |

| IR EUR / credit C cross-gamma | -44484.00 | -2358.00 | -2430.00 | -0.0015 |

To measure the performance of the approximated WWR sensitivities, the relative difference of the complete sensitivity from the approximation is computed w.r.t. the Monte Carlo benchmark result. In Table 4 the sensitivities corresponding to the multi-currency portfolio example from Section 5.2 are presented. The Gaussian approximation correctly determines the sign of the WWR part of the sensitivity in all cases. The IR deltas, most important for hedging, are of high quality. This is expected, as in the approximation from Equation (3.3), is taken outside the expectation in the exposure formula, and no Gaussian approximation is applied to this factor. Only is affected when computing an IR delta, but the effect is limited in this example. The IR vega approximation errors go up to 8%, but the approximation captures the tendency of the WWR sensitivities well. Also, the cross-gamma sensitivities between IR and credit are remarkably close.

Furthermore, the FX deltas are approximated at an acceptable level. The FX vegas are close to zero, as the portfolio does not include FX derivatives. Therefore, the high values of the RD metric are not an issue.

Like the IR deltas, the credit deltas are well approximated in this case. The credit vegas have similar error magnitudes as the IR vegas.

As expected, under stressed market conditions, like in Section 5.3, the sensitivity approximation error increases. More caution must thus be taken in this case, yet the tendency of the WWR sensitivity is well captured by the approximation. Especially the IR deltas are performing well, with maximum errors of around 2.5%. The IR vega error increases to 10%. For the credit sensitivities and the cross-gammas, the sensitivity approximation errors increase. As credit risks are more challenging to hedge due to limited liquidity in some of the credit markets, this is less of an issue.

The approximation allows for efficient sensitivity calculations. For example, for the IR deltas this efficiency becomes apparent. For the benchmark method, for each pillar on the yield curve, a new Monte Carlo simulation would need to be undertaken. Due to the semi-analytic nature of the Gaussian approximation, these extra simulations are not required. This speed-up in computing the WWR sensitivities can give an institution an edge over the rest of the market when setting up hedging positions.

6 Conclusion

In summary, the proposed WWR approximation provides a practical, robust and efficient method to compute WWR when the existing xVA calculation cannot simulate stochastic credit and funding processes which are correlated to the market risk factors. The approximation avoids simulation of these additional processes, and is therefore also faster than the Monte Carlo benchmark method. Furthermore, the approximation runtime does not scale in the number of derivatives in the portfolio. Within the affine setting, the approximation is generic, does not require any calibration of approximation parameters, and is applicable to a wide variety of derivatives and asset classes. Only the WWR exposure is approximated, so it is an add-on to the xVA calculation in place at financial institutions, where the original exposures without WWR are left untouched. In specific cases, the approximation gives rise to analytical expressions at the cost of one additional Taylor series approximation. This has been demonstrated for the example of a single IR swap. The approximation has been demonstrated for the practically relevant example of a multi-currency portfolio of multiple IR swaps. This approximation error can be considered a lower bound for portfolios with more complicated derivatives. After analyzing the various approximation errors, a good understanding is established of their behaviour and interplay. The proposed approximation has its limitations under stressed market conditions, but at the same time the approximation allows for insights in the effect of different market stresses on the approximation error. Recall that the quantity that is being approximated is not a ‘true market quantity’, but the WWR resulting from a series of modelling choices. Therefore, the WWR approximation is relevant from a practical perspective, giving a fast method to assess the impact of portfolio-level WWR. While the approach is applied to the calculation of , it is equally applicable to other metrics such as .

Acknowledgements

This work has been financially supported by Rabobank.

References

- [1] M. Bichuch, A. Capponi, and S. Sturm. Robust XVA. Mathematical Finance, pages 1–44, March 2020.

- [2] D. Brigo and F. Mercurio. Interest Rate Models - Theory and Practice With Smile, Inflation and Credit. Springer–Verlag, second edition, 2006. ISBN 978-3-540-22149-4.

- [3] D. Brigo and A. Pallavicini. Nonlinear consistent valuation of CCP cleared or CSA bilateral trades with initial margins under credit, funding and wrong-way risks. Journal of Financial Engineering, 1(1):1–60, May 2014.

- [4] D. Brigo, A. Pallavicini, and V. Papatheodorou. Arbitrage-free valuation of bilateral counterparty risk for interest-rate products: impact of volatilities and correlations. Mathematical Finance, 14(6):773–802, July 2011.

- [5] J. Cerny and J. Witzany. A copula approach to credit valuation adjustments for swaps under wrong-way risk. The Journal of Credit Risk, 25(1):31–43, March 2018.

- [6] U. Cherubini. Credit valuation adjustment and wrong way risk. Quantitative Finance Letters, 1(1):9–15, June 2013.

- [7] Q. Feng and C. Oosterlee. Computing Credit Valuation Adjustment for Bermudan Options with Wrong Way Risk. International Journal of Theoretical and Applied Finance, 20(8), December 2017.

- [8] P. Glasserman and L. Yang. Bounding wrong-way risk in CVA calculation. Mathematical Finance, 28(1):268–305, January 2018.

- [9] A. Green. XVA: Credit, Funding and Capital Valuation Adjustments. John Wiley & Sons, first edition, November 2015. ISBN 978-1-118-55678-8.

- [10] J. Gregory. The xVA Challenge - Counterparty Risk, Funding, Collateral, Capital and Initial Margin. John Wiley & Sons, fourth edition, July 2020. ISBN 978-1-119-50897-7.

- [11] L. Grzelak. Sparse grid method for highly efficient computation of exposures for xVA. Applied Mathematics and Computation, 434, December 2022.

- [12] J. Hull and A. White. CVA and Wrong-Way Risk. Financial Analysts Journal, 68(5):58–69, September 2012.

- [13] F. Jamshidian. An Exact Bond Option Formula. Journal of Finance, 44(1):205–209, March 1989.

- [14] C. Kenyon, M. Berrahoui, and B. Poncet. Data-driven WWR for CVA and FVA. Risk, October 2022.

- [15] C. Kenyon and A. Green. Option-Based Pricing of Wrong Way Risk for CVA. SSRN Electronic Journal, October 2016.

- [16] R. Lichters, R. Stamm, and D. Gallagher. Modern Derivatives Pricing and Credit Exposure Analysis. Palgrave Macmillan, first edition, 2015. ISBN 978-1-137-49483-2.

- [17] C. Moni. Adding Stochastic Credit and Funding to XVA Calculations. SSRN Electronic Journal, November 2014.

- [18] L. G. Munoz. CVA, FVA (and DVA?) with stochastic spreads. A feasible replication approach under realistic assumptions. December 2013.

- [19] D. O’Kane. Modelling Single-name and Multi-name Credit Derivatives. John Wiley & Sons, 2008. ISBN 978-0-470-51928-8.

- [20] C. Oosterlee and L. Grzelak. Mathematical Modeling and Computation in Finance. World Scientific, first edition, November 2019. ISBN 978-1-78634-794-7.

- [21] A. Pallavicini, D. Perini, and D. Brigo. Funding Valuation Adjustment: a consistent framework including CVA, DVA, collateral, netting rules and re-hypothecation. arXiv Electronic Journal, December 2011.

- [22] D. Singh and S. Zhang. Distributionally Robust XVA via Wasserstein Distance: Wrong Way Counterparty Credit and Funding Risk. arXiv Electronic Journal, May 2020.

- [23] C. Turfus and A. Shubert. Two-factor Black-Karasinski pricing kernel. Risk, June 2020.

- [24] M. Turlakov. Wrong-way risk, credit and funding. Risk, 26(3):69–71, March 2013.

- [25] N. Valsecchi. Funding Value Adjustment and Wrong-Way Risk: the Interest Rate Swap case. Master’s thesis, Department of Mathematics, Politecnico di Milano, April 2021.

- [26] T. van der Zwaard, L. Grzelak, and C. Oosterlee. A computational approach to hedging Credit Valuation Adjustment in a jump-diffusion setting. Applied Mathematics and Computation, 391, February 2021.

- [27] T. van der Zwaard, L. Grzelak, and C. Oosterlee. Relevance of Wrong-Way Risk in Funding Valuation Adjustments. Finance Research Letters, 49, October 2022.

Appendix A FVA exposure derivation

Using the modelling choices from Section 2.1.1 together with the funding spread from Equation (2.8), we write:

Applying this to the WWR exposure from Equation (2.18) yields:

| (A.1) |

The remaining unknown term in Equation (A.1) is rewritten in a similar fashion:

With these results, WWR exposure from Equation (A.1) changes into:

Finally, we apply the second part of Taylor expansion (2.13), which means we truncate the summation at the -th term:

| (A.3) |

where:

| (A.4) | ||||

| (A.5) |

Appendix B IR and credit dynamics

B.1 IR dynamics

For the IR process we choose the HW1F (G1++) dynamics with constant volatility:

This fits the framework we introduced in Section 2.1.1, where

and both follow a normal distribution with mean and respectively, and variances

In the case of a multi-currency portfolio, the domestic IR is denoted as , which adheres to the equations above. For foreign IR, , use a similar model:

Here, denotes the Brownian motion of process under the risk-neutral measure.

When setting up a Monte Carlo simulation, all processes must be under the same measure [9]. Hence, we use a change of measure and write the dynamics under the risk-neutral measure. This will lead to an additional term in the drift, which is a quanto correction term:

In this case,

where further information on the FX process is given in B.3.

B.2 Credit dynamics

In literature on WWR modelling for BCVA purposes, a CIR type model is commonly used [3, 4]. Hence, for the credit process we choose a CIR++ credit dynamics with constant volatility for each counterparty :

When the Feller condition is satisfied, we are not affected by potential issues around the origin, see [20] for more information. This model dynamics fits the framework introduced in Section 2.1.1, where

Conditional on , follows a scaled non-central chi-square distribution [20]:

Processes and have mean and respectively, and variance

Furthermore, the following analytic expression can be derived for the term, which is needed when computing .

| (B.1) |

B.3 FX dynamics

For the FX process, , which to converts currency into , we use log-normal dynamics:

The integrated form reads

The three stochastic processes , , are correlated normals with zero mean. Here, is normal with zero mean and a variance where the correlations are included.

Conditional on time , has mean and variance

B.4 Model parameters

B.4.1 Single IR swap example

-

1.

: , , , EUR1D yield curve;

-

2.

: , , , , , AAA-rating curve;

-

3.

: , , , , , BBB-rating curve;

-

4.

Correlation: , , .

B.4.2 Multi-currency portfolio of IR swaps example

-

1.

Currencies: EUR, USD, GBP;

-

2.

: , , , 1D yield curves;

-

3.

FX: , ;

-

4.

: , , , , , AAA-rating curve;

-

5.

: , , , , , BBB-rating curve;

-

6.

Correlation: , , , , , .

B.4.3 Multi-currency portfolio of IR swaps stressed example

-

1.

Currencies: EUR, USD, GBP;

-

2.

: , , , 1D yield curves;

-

3.

FX: , ;

-

4.

: , , , , , AAA-rating curve;

-

5.

: , , , , , BBB-rating curve;

-

6.

Correlation: , , , , , .

Appendix C IR swap

C.1 Payoff

Consider an IR swap under a single curve setup starting at , maturing at with intermediate payment dates , . The value of the swap with strike and notional is then:

| (C.1) | ||||

| (C.4) |

Using the assumptions from Section 2.1.1, we can express the swap value in terms of :

| (C.5) | ||||

| (C.9) |

Swap valuation formula (C.5) only holds if , meaning before the first reset date of the swap, i.e., . As soon as , the valuation changes, especially after several coupon payments have been made. For with , the following valuation holds:

| (C.10) |

We can combine Equations (C.5–C.10) into the following generic result for the swap value:

| (C.11) | ||||

| (C.14) |

C.2 Probability of positive value

We are interested in the case , with given in Equation (C.11). To find the values of for which this holds, we rewrite Equation (C.11) as a monotonically decreasing function. Consider the two different cases for in (C.14):

-

1.

, hence , so . Then, starting from Equation (C.5),

(C.15) -

2.

, hence , so . Then,

(C.16)

We combine Equations (C.15–C.16) as follows:

| (C.17) | ||||

| (C.20) |

where in Equation (C.17) we now explicitly write the dependence of on .

Similarly to Jamshidian’s trick for swaption pricing [13], we choose numerically such that . With , is equivalent to , where

Recall . Then, for all the function is monotonically decreasing in . In Equation (C.9), for all .

For a payer swap (i.e., when ), is a monotonically increasing function in as it is a sum of monotonically increasing functions. Alternatively, for a receiver swap (i.e., when ), is a monotonically decreasing function in as it is a sum of monotonically decreasing functions.

Using the monotonicity we can write the following for the indicator when the swap value is positive:

| (C.21) |

From this, we have a straightforward expression of the positive swap value probability:

| (C.22) |

where is the standard normal CDF. In the last step, we have used the assumption that is normally distributed , which results from using the HW1F model.

C.3 Error bound

For the second term in Equation (4.1), which is the product-specific component of the error, we use

| (C.23) |

to obtain .

Using the IR swap notation from Equation (C.11), together with the Cauchy-Schwarz inequality for sums, i.e., , we get

| (C.24) |

where in the last step we have written the expression in a generic form for ease of the analysis that follows. Here, and are deterministic, and the sum over is finite.

Furthermore, we know that . Recall that for . This, combined with Equation (C.24), yields:

| (C.25) |

where constant can be computed analytically.

Appendix D Moments of (truncated) normal random variables

Here, some results on the moments of (truncated) normal random variables are given, which are used in Section 3.4.2 for the IR swap WWR exposure approximation. In particular, consider and , where and is computed numerically as explained in C.2. The moments of a normal and generic truncated normal random variable are given in Result 1 and 2, respectively.

Result 1.

Recall the result about the central moments of a normally distributed random variable :

| (D.3) |

where is the double factorial function.

Result 2.

Let and where . Define . Then, there is a recursive formulation for , with and :

| (D.4) |

where and are the normal PDF and CDF, respectively.

Furthermore, moments can be written as

| (D.5) |

Appendix E Extension for linear FX derivatives

E.1 FX forward contract

Consider a linear FX payoff, e.g., an FX forward contract with payoff at time :

Value is in the domestic currency . Define the FX forward , which is a martingale under the forward measure:

Using standard risk-neutral pricing, and assuming unit notional, i.e., , write:

E.2 in terms of stochastic processes

Recall that in the current setup we can write:

Using the above, the following expression for the FX forward is obtained:

where is defined such that equality holds, and contains all deterministic terms.

The next step is to write in terms of stochastic processes , and . Hence, first look at the case where :

Using approximation , this can be rewritten as

Here, can only be zero if . For simplicity, from now on assume that . Denoting and combining with the above yields

| (E.4) |

This is a convenient formulation to work with, as is deterministic and given in terms of the model parameters.

As a result, can be written as

Thus, is written in terms of , where we used the proposed stochastic process approximation technique. For non-pure linear IR derivatives, this approximation step will be necessary.

Finally, the previous derivations are used to obtain an expression for in terms of :

From this, the expressions are again decomposed in terms of moments of a normal and truncated normal distribution. The current example is for an FX forward contract, but this approach can easily be extended for all linear FX derivatives. Recall that the current example has been illustrated for HW1F for foreign and domestic IR processes, and GBM for the FX process.

Appendix F Specific truncation error example

Here, we apply the error bound given in Equation (4.6) to from Equation (2.21). This error term is chosen as this is the main driver of . We split as follows

| (F.1) |

where .

First term

For the first expectation in Equation (F.1), we apply the bound from Equation (4.6) with , and . Thus, we first need to look at the bound for expectation from Equation (4.4).

For , using the binomial formula , and the independence of and , we write for :

| (F.2) |

where for now we only need the case where .