Treatment Effects with Multidimensional Unobserved Heterogeneity:

Identification of the Marginal Treatment Effect

††thanks: I am grateful to my advisor, Katsumi Shimotsu, for his continuous guidance and support. I am also thankful to Mark Henry, Hidehiko Ichimura, Sokbae Lee, Ryo Okui, Bernard Salanié and Takahide Yanagi for their insightful comments. Further, I benefited from comments of the seminar participants at The University of Tokyo and Tohoku University.

The author gratefully acknowledges the

support of JSPS KAKENHI Grant Number JP 23KJ0713 and the IAAE travel grant for the 2023 IAAE Conference in Oslo, Norway.

Abstract

This paper establishes sufficient conditions for the identification of the marginal treatment effects with multivalued treatments. Our model is based on a multinomial choice model with utility maximization. Our MTE generalizes the MTE defined in Heckman and Vytlacil (2005) in binary treatment models. As in the binary case, we can interpret the MTE as the treatment effect for persons who are indifferent between two treatments at a particular level. Our MTE enables one to obtain the treatment effects of those with specific preference orders over the choice set. Further, our results can identify other parameters such as the marginal distribution of potential outcomes.

Keywords: Identification, treatment effect, multidimensional unobserved heterogeneity, multivalued treatments, endogeneity, instrumental variable.

JEL classification: C14, C31

1 Introduction

Assessing heterogeneity in treatment effects is important for precise treatment evaluation. The marginal treatment effect (MTE) provides rich information on heterogeneity across economic agents regarding their observed and unobserved characteristics. Further, once the MTE is estimated, researchers can obtain other treatment effects, such as the average treatment effect (ATE), the average treatment effect on the treated (ATT), and local ATE (LATE).

In this paper, we consider the multivalued treatments. While the multivalued treatments complicate the identification of treatment effects, they are often used in many applications. For example, vocational programs provide various types of training to participants, and college choice involves numerous dimensions to respond to varied incentives. The literature has developed treatment effects with multivalued treatments, such as LATE (Angrist and Imbens, 1995), MTE (Heckman et al., 2006, 2008; Heckman and Vytlacil, 2007; Heckman and Pinto, 2018; Lee and Salanié, 2018) and instrumental variable quantile regression (Fusejima, 2024).

For the binary treatment models, Heckman and Vytlacil (1999) establish the local instrumental variable (LIV) framework to identify MTE. They assume individuals decide on their choices based on the generalized Roy model that is separable in terms of observed and unobserved variables. Vytlacil (2002) shows that the separable threshold-crossing model in the LIV approach plays the same role as the monotonicity assumption for identifying LATE (Imbens and Angrist, 1994).

For the identification of MTE with the multivalued treatments, we examine the multiple discrete choice model based on utility maximization. In this model, the value of each treatment is the sum of an observed term and an unobserved term that represents unobserved heterogeneity. This model is a generalization of the multiple logit model and has been extensively studied in economics since the seminal work of McFadden (1974). In theoretical research, Matzkin (1993) establishes sufficient conditions for the nonparametric identification of the discrete choice model. In applied research, Dahl (2002) employs this model to study the effects of self-selected migration on returns to college. Kline and Walters (2016) use the discrete multiple-choice model as a self-selection model to analyze the Head Start program’s cost-effectiveness.

We identify the MTE with multidimensional unobserved heterogeneity, which enables us to evaluate treatment effects from multiple perspectives. For instance, we consider three-valued treatments and set treatment 0 as the baseline. In this case, the model contains two-dimensional heterogeneity that consists of willingness to take treatment 1 and willingness to take treatment 2 against treatment 0. When we condition the MTE on a high value of the former heterogeneity and a low value of the latter heterogeneity, our identification result reveals the causal effects of those with the preference order treatment 1, treatment 0 and treatment 2 from top to bottom.

A comparison of our MTE with the MTE with binary treatment reveals several intriguing similarities and discrepancies. As a similarity, our identified MTE with multivalued treatments has multidimensional heterogeneity whose each element follows a uniform distribution on while Heckman and Vytlacil (2005) define the MTE with binary treatment conditional on unobserved heterogeneity that also uniformly ranges from 0 to 1. In this sense, our MTE generalizes the MTE in the binary treatment case defined by Heckman and Vytlacil (2005) to the multivalued treatment case. Additionally, as in the binary case, we can interpret the MTE as the treatment effect for persons indifferent between treatment 1 and 0 and treatment 2 and 0 at a specific level. On the other hand, two MTEs have different relationships between treatments and preference order. In the binary treatment case, the MTE corresponds to marginal changes in the treatment choice because an individual’s preference order exactly maps to his choice. However, in the multivalued treatment case, marginal changes in preference order do not necessarily correspond to the changes in treatments. Therefore, our MTE with the multivalued treatments represents marginal changes in preferences over the choice set.

The main challenge of the identification is that the model properties prevent us from obtaining several marginal changes in treatments. In the binary treatment case, we set a threshold for selecting the treatment and take a derivative with respect to the threshold. This procedure identifies the MTE because the derivative with respect to the threshold exactly expresses a marginal change in the treatment. In the case of multivalued treatments, we set one specific treatment as the baseline and construct the multiple-choice model by comparing the other treatments with the baseline. For the identification, we set thresholds of the other treatments compared with the baseline and take derivatives with respect to these thresholds. In the case of the baseline treatment, this procedure identifies the conditional expectation because the derivative with respect to each threshold exactly expresses a marginal change in each treatment against the baseline. In the case of the other treatments, changing thresholds has indirect effects on all the other treatments and we cannot identify conditional expectations of those treatments by simply taking derivatives with respect to thresholds.

We solve the indirect effects by focusing on an area of each treatment that thresholds have only a direct effect. In this model, each treatment has one threshold that has both indirect and direct effects on that treatment. We remove the indirect effects of the threshold by an ingenuous transformation that enables us to substitute those indirect effects with the marginal changes in other thresholds. By removing indirect effects with those substitutes, we can extract the direct effect from the marginal change in the threshold and identify conditional expectations of all the treatments from the multiple discrete choice model.

By identifying conditional expectations of treatments, we can obtain several treatment effects, including the MTE. Because our result identifies conditional expectations of each treatment given unobserved heterogeneity, we can obtain the MTE with multivalued treatments by taking their differences. Further, we can also obtain the marginal distribution of potential outcomes, which leads to identifying the quantile treatment effects given multidimensional unobserved heterogeneity.

We also establish a sufficient condition for identifying the thresholds. In the case of multivalued treatments, the connection between thresholds and propensity scores is unclear, even though the propensity score is equal to the threshold in the binary case. We assume the existence of at least one instrument that significantly and negatively affects only one treatment. This assumption enables us to identify the thresholds and is also used by Lee and Salanié (2018) for the identification of thresholds.

In the existing literature on the identification of the MTE with multivalued treatments, Lee and Salanié (2018) investigate the identification of conditional expectations given unobserved variables based on multinomial choice models characterized by a combination of separable threshold-crossing rules. They assume the existence of continuous instruments and identify several causal effects with identified thresholds. Our result complements the applicability of their main theorem by introducing a novel identification strategy.

Heckman and Vytlacil (2007) and Heckman et al. (2008) expand the LIV approach to a model with multivalued treatments generated by a general unordered choice model. They study the identification conditions of several types of treatment effects including the marginal treatment effect of one specified choice versus another choice. They achieve the identification of the MTE by using an identification-at-infinity type argument. Our identification strategy does not depend on the large support assumption.

With the introduction of new treatment effects for multivalued treatments, Mountjoy (2022) studies the effect of enrollment in 2-year community colleges on upward mobility, such as years of education and future income. Because the main focus of his paper is the effect of policy changes for 2-year entry on the outcome of 2-year colleges, he defines new treatment effects with respect to the marginal change of the instrument pertained to 2-year entry. Our MTEs are based on unobserved heterogeneities that correspond to marginal changes in preferences between treatments and can express his treatment effects.

The remainder of this paper is organized as follows: Section 2 proposes the basic settings and notation used in this study. We construct the model through comparisons between treatments. In Section 3, we explain our MTE with the multivalued treatments through figures. We highlight the similarities and differences between our MTEs and the MTE in the binary case. After we show identification of the MTE, we add detailed explanations of our identification strategies. Section 4 establishes sufficient conditions for nonparametric identification of the thresholds. We relate our contributions to the literature in Section 5. Section 6 concludes. Proofs of the main results and some auxiliary results are collected in Appendix A.

Notation. Let denote “equals by definition,” and let a.s. denote “almost surely.” Let denote the indicator function. For random variables and , denotes the probability density function of . and denotes the distribution and quantile functions of given , respectively.

2 Model

Let denote the set of treatments and assume the set comprising of elements. Let be a potential outcome. takes the value one if the agent takes treatment . The observed outcome and treatment are expressed as and , respectively. The data contains covariates and instruments . Throughout this article, we condition on the value of and suppress it from the notation. Let the support of and be and , respectively.

Let denote the vector of functions of the instruments , that is, . Let be a vector of continuous random variables whose support is . For each , define . is a vector of unobserved heterogeneity and serves as a threshold for each when is given. Hence, is a separable threshold-crossing model as in the generalized Roy model.

We define MTE as

and analyze sufficient conditions for the identification. As in Heckman et al. (2006, 2008) and Heckman and Vytlacil (2007), we consider the discrete choice model based on utility maximization. This model setting enables us to interpret the above MTE as the treatment effect with unobserved heterogeneity of preferences over the choice set. For details, see Section 3.1.

2.1 Multiple Discrete Choice Model and Basic Assumptions

For each , we define as an unknown function that maps from to and define as an unobserved continuous random variable whose support is . By extending the definition of the treatment variable in the binary treatment model, we formulate the treatment decision as follows:

| (1) |

where for .

Intuitively, by interpreting and as unobserved and observed terms in an agent’s utility, this discrete multiple-choice model states that he makes a choice based on utility maximization. From this intuition, we regard model (1) as a straightforward generalization of the generalized Roy model.

Model (1) has been studied extensively in economics since the seminal work of McFadden (1974). Matzkin (1993) establishes sufficient conditions for the nonparametric identification of the utility functions and the joint distribution function of unobserved random terms. The multinomial choice model has also been used in applied research. Dahl (2002) uses this model to study the effects of self-selected migration on the return to college. Kline and Walters (2016) adopt the discrete multiple-choice model as a self-selection model and analyze the Head Start program’s cost-effectiveness in the presence of substitute preschools. Kirkeboen et al. (2016) examine the effect of types of education on the gains in earnings. They find that the estimated payoffs are consistent with agents choosing fields based on the discrete multiple-choice model.

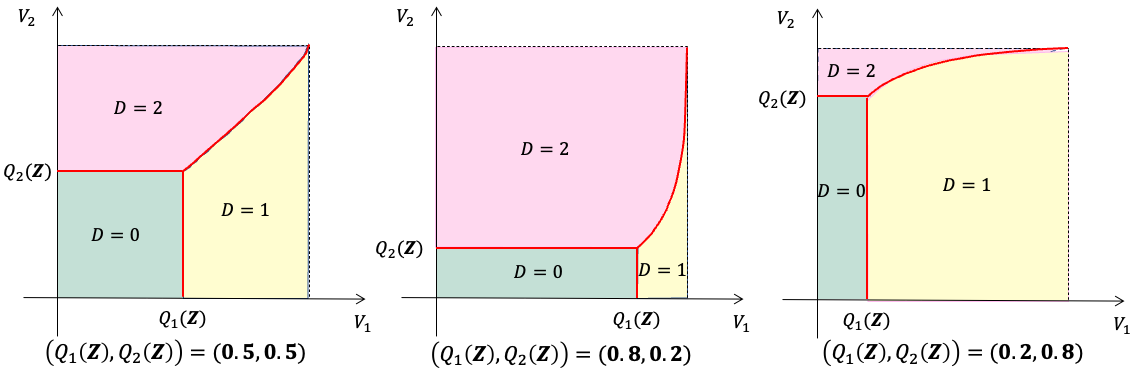

For the identification of the MTE, we construct a model through a combination of threshold-crossing models based on model (1). We consider case of three alternatives, namely treatment 0, 1 and 2. Without loss of generality, we regard treatment 0 as the baseline and set almost surely. We construct a model with three alternatives using two indicator functions. Assume and are continuously distributed. Let

Set

Note that

and a similar argument gives

Two indicator functions, and , correspond to comparisons of the utilities between treatment 0 and 1, and treatment 0 and 2, respectively. From model (1), individuals take treatment 0 when the utility of treatment 0 is the highest among all the alternatives. Therefore, we obtain .

We introduce an indicator function that compares the utilities between treatment 1 and 2. Define

By trivial calculation, we obtain

| (2) |

Hence, we have by definition. A similar argument reveals .

This model is depicted in Figure 1. In this setting, treatment 0 has the form of the double hurdle model, namely if and only if and as in Lee and Salanié (2018). Even though the double hurdle model essentially expresses the binary treatment case, we successfully specify and by introducing and construct the multiple-choice model based on utility maximization. Hence, our model is not covered by Lee and Salanié (2018). For details, see Section 5.1.

We introduce basic assumptions frequently required in the literature on program evaluation.

Assumption 2.1.

and are measurable sets.

Assumption 2.2 (Conditional Independence of Instruments).

, , and are jointly independent of .

Assumption 2.3 (Continuously Distributed Unobserved Heterogeneity in the Selection Mechanism).

The joint distribution of is absolutely continuous with respect to the Lebesgue measure on .

Assumption 2.4 (The Existence of the Moments).

For , , where is a measurable function defined on the support of , which can be discrete, continuous, or multidimensional.

Assumption 2.1 ensures the existence of probability of each treatment, that is, . This assumption guarantees that each treatment variable is a random variable. Assumption 2.2 corresponds to the exogeneity of instruments, which plays a vital role in the identification in the literature using instrumental variables. We guarantee the existence of the probability density function of by Assumption 2.3. Through the argument of change of variables, we can also ensure the joint density of . Assumption 2.4 ensures the existence of the moments for each alternative. Otherwise, we cannot define conditional expectations of potential outcomes or identify MTE. The assumptions above often appear in the literature on treatment effects with endogeneity. For instance, Assumptions 2.1, 2.2, and 2.3 correspond to Assumptions 2.1, 2.2, and 3.2 of Lee and Salanié (2018), respectively. Assumption 2.4 generalizes Assumption (A-3) of Heckman et al. (2008).

3 Identification

3.1 MTE with the Multivalued Treatments

In this paper, we study the identification of the following conditional expectations

where we define as the points where we evaluate treatment effects. When we set and take the difference between two conditional expectations, we identify the following MTE:

| (3) |

By definition, each element of has a uniform distribution on and refer to the quantiles of the distributions of and , respectively. Hence, and mean the willingness to choose treatment 1 and 2 compared to treatment 0. For instance, a low value of implies an individual is less likely to take treatment 1 than treatment 0.

MTE (3) provides rich information about treatment effects conditioned on individuals’ preferences over the choice set. The MTE characterizes preferences among all the alternatives through the values of . For example, when we identify MTE with a low value of and a high value of , we can interpret this MTE as the average treatment effect in those who are more likely to take treatment 2 and less likely to take treatment 1 compared to treatment 0, i.e., their preferences would be treatment 2, treatment 0 and treatment 1 from top to bottom.

As another interpretation, MTE (3) is the average treatment effect for individuals who would be indifferent between treatment 1 and 0, and treatment 2 and 0 at . Under Assumption 2.2, we can illustrate this interpretation in the following equation,

Note that each unobserved heterogeneity only focuses on comparing two treatments, treatment 1 and 0, and treatment 2 and 0. Therefore, MTE (3) corresponds to the marginal changes in treatment 1 and 0, and treatment 2 and 0.

Comparing MTE (3) with the MTE in the binary treatment case provides useful insights. Heckman and Vytlacil (2005) define as the receipt of the treatment and characterize the decision rule as the generalized Roy model, that is,

where is an unknown function, which maps from to , and is an unobserved continuous random variable. As a normalization, they innocuously assume that and is the quantile of the willingness to participate in the treatment. Heckman and Vytlacil (2005) then define MTE with binary treatment as

| (4) |

where . In our definition of MTE with multivalued treatments, precisely corresponds to in the binary treatment case. Therefore, MTE (3) is a natural generalization of MTE with binary treatment to the multivalued treatment case.

Heckman and Vytlacil (2005) show that treatment effects such as ATE and ATT can be expressed as a function of their MTE. Similarly, in our model, treatment effects such as ATE and ATT can be expressed as a function of our MTE.

MTE (3) has a different interpretation from MTE (4) due to the existence of the multivalued treatments. In the binary case, whether an individual takes treatment or not precisely corresponds to his preference for its treatment. However, in the multivalued treatment case, the preference orders over the choice set have additional information over revealed treatments. For example, if an individual’s best treatment is treatment 2, her preference order of the choice set is treatment 2, 0, 1 or treatment 2, 1, 0. When marginally changes through , this change corresponds to the binary choice between treatment 2 and 0 or treatment 2 and 1, but the change in does not affect the preference between treatment 1 and 0. On the other hand, when marginally changes and remains fixed, her choice may remains in treatment 2 because only affects the change in preference between treatment 1 and 0. Therefore, marginal changes in and correspond to not marginal changes in treatments but marginal changes in preferences between treatment 1 and 0, and treatment 2 and 0, respectively. MTE (3) is the treatment effect depicting the marginal changes in preferences over the choice set.

3.2 Illustration

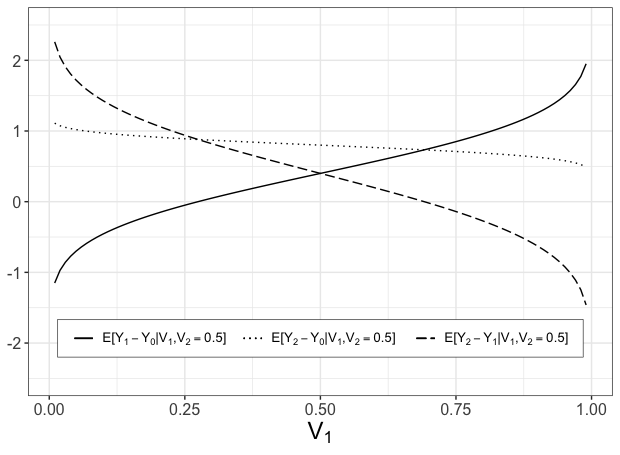

We illustrate figures of three MTEs, and given is fixed at . We depict the MTEs in the following two cases:

3.2.1 Case 1: are not independent of the outcome variable

Case 1 examines the three MTEs when is correlated with the outcome variable , i.e.

In this case, increases and decreases with because people are more likely to choose treatment 1 than treatment 0 at the high value of . Even though does not directly affect the difference between treatment 2 and 0, the MTE decreases slightly with , reflecting the combined effect of the decrease in and the increase in .

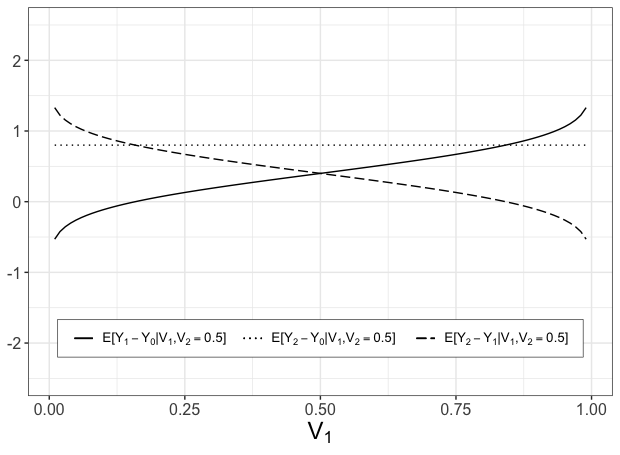

3.2.2 Case 2: is independent of and given

Case 2 analyzes the three MTEs when is independent of and given , i.e.

In this case,the MTE does not depend on and is equal to for any . Conditional independence of implies that the comparison in preference between treatment 1 and 0 does not affect treatment effect . Furthermore, the difference in two other MTEs becomes constant because holds for any .

3.3 Identification Result

We introduce assumptions to identify the MTE with multivalued treatments. Assumption 3.1 is a technical assumption for the proof of the identification, such as continuity and differentiability.

Assumption 3.1.

-

(1).

For , and are twice differentiable at .

-

(2).

For , and are continuous on .

-

(3).

-

(a)

For , is finite.

-

(b)

The conditional density functions satisfy the following:

-

(a)

Assumption 3.1 (1) guarantees the existence of derivatives for each conditional expectation. This condition implicitly assumes that the value of is movable while is fixed and vice versa. We require Assumption 3.1 (3) to exchange differentiation and integration. Assumption 3.1 (3a) holds when is bounded for each .

Conditional on the assumption that and are identified, we can identify the conditional expectations , and by partially differentiating conditional expectations and for .

Theorem 3.1.

For any and such that , we can obtain and by using estimation methods such as local polynomial regression. Note that the density of at is identified as . For (b) and (c), the second and third terms on the right hand side correct indirect effects that we discuss in the following.

The identification result of the conditional expectations enables us to identify measures of treatment effects.111In the binary treatment case, by using the identification results of the conditional expectations, Carneiro and Lee (2009) propose a semiparametric estimator of the MTE. Brinch et al. (2017) also employ the results to identify MTE with discrete instruments. For example, if we set as we did previously, we obtain

If we let for , we can identify

If and are invertible, we identify the quantile treatment effect by taking the difference between the two, that is,

where .

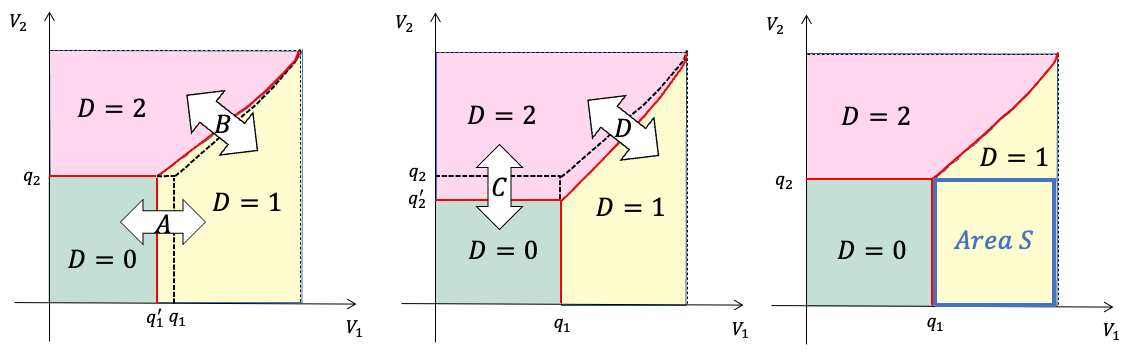

Our identification strategy consists of the marginal changes in conditional expectations and proper corrections for indirect effects caused by a nonlinear threshold. We can identify without being troubled by a nonlinear threshold. For instance, when is fixed, the change in corresponds exactly to the flow between treatment 0 and 1 over the values of in (flow A in Figure 4). Further, taking its derivative at provides the flow between treatment 0 and 2 at (flow C in Figure 4). Therefore, we can identify by taking derivatives of and with respect to and as in the binary case.

However, a nonlinear threshold in this model complicates identifications of the conditional expectations about treatments 1 and 2. In order to identify expectations about treatment 1 and treatment 2 conditional on and , we need to take derivatives of and for and with respect to and as in the case of treatment 0. Because marginal changes in and only indirectly affect the preference between treatment 1 and 2, we need to deal with indirect changes between treatment 1 and 2.

For instance, when identifying the conditional expectations of treatment 1, we first study area S in Figure 4. Because is larger than and is smaller than , this area represents those who have the preference order of treatment 1, 0, 2 from top to bottom. When decreases through , people with treatment 0 will move into area S (flow A in Figure 4), while this change in does not affect preferences over treatment 0 and 2. Moreover, when slightly decreases through , people in area S will change their preference orders from treatment 1, 0, 2 to treatment 1, 2, 0. Therefore, confining to area S, we can identify by taking derivatives of and with respect to and as in treatment 0.

A decrease in generates another flow, flow B in Figure 4. We must remove the marginal changes in treatment 1 caused by flow B. In this case, when decreases through , some individuals taking treatment 1 will move to treatment 2 (flow D in Figure 4), but there is no flow from treatment 1 to treatment 0 because the change in does not affect preferences over treatment 1 and 0. We can remove the marginal change between treatment 1 and treatment 0 by substituting flow D for flow B. Then, we can obtain the marginal changes generated by in area S by subtracting flow B from the marginal changes generated by in treatment 1. Therefore, we achieve the identification of .

4 Identification of thresholds

In this section, we consider the identification results of and that enable us to estimate MTE with the results in Theorems 3.1. While the propensity score plays a role as a threshold in deciding on the treatment in the binary case, has more complicated relationships with the propensity scores , and . Because each marginal distribution of and is uniformly distributed on , and correspond to the probability that treatment 0 is preferable to treatment 1 and the probability that treatment 0 is preferable to treatment 2, respectively. Hence, we cannot directly identify from , and because propensity scores only reveal the probabilities of each treatment given . 222If we have the data of preferences over the choice set as in the case of Kirkeboen et al. (2016), we can directly identify .

We provide a sufficient condition for the nonparametric identification of and that enables us to estimate MTE with the results in Theorems 3.1. A sufficient condition requires the existence of at least one instrument that significantly and negatively affects only one utility. Let denote the -th component of . Let be all the instruments except for the -th component.

Assumption 4.1.

For , there exists at least one element of , say , and at least one value , such that, given any ,

and is constant for .

Assumption 4.1 imposes a type of exclusion restriction. Conditional on all the regressors except , one can vary independently. Moreover, we assume the existence of one value such that, as approaches , the value of the function becomes sufficiently small given any .

Theorem 4.1.

The strategy for the identification of in Theorem 4.1 deeply depends on the reduction to the binary treatment setting. As converges to , for instance, approximately approaches to 1, which implies that the individuals take treatment 0 or treatment 1. Hence, we identify as in the binary case.

Assumption 4.1 is similar to assumptions for identifying thresholds in the existing literature. Lee and Salanié (2018) establish the general identification result of conditional expectations given that is known. They study the identification of for some choice models, using the information of these models. Especially, they impose a similar large support assumption for the identification of in a double hurdle model. Because treatment 0 has the form of a double hurdle model, Theorem 4.1 can be considered as the identification result of thresholds in a double hurdle model, as in Theorem 4.2 in Lee and Salanié (2018).

5 Comparison with the Existing Literature

In this section, we briefly review the existing literature regarding the identification of MTE with the multivalued treatments and compare them with our results.

5.1 Lee and Salanié (2018)

Lee and Salanié (2018) employ the following model:

where

| (5) |

and is an integer. Let be the set , and let be the set of all the subsets of . Model (5) can express any decision model that comprises sums, products, and differences of their indicator functions .

In their Section 5.2, Lee and Salanié (2018) apply their main theorem to the multiple discrete choice model. Example 5.2 of Lee and Salanié (2018) analyzes three treatments, . They define

| (6) |

Subsequently, they define

| (7) |

Based on the comparison among utilities as we did in Section 2, they define treatments as follows:

- •

iff and ,

- •

iff and ,

- •

iff and .

Evidently, this corresponds to the decision rule based on model (1).

Lee and Salanié (2018) argue that their main theorems (Theorem 3.1 and Theorem A.1) can identify the MTE if are identified and their Assumptions 2.1–2.2 and 3.2–3.4 hold. From this result, they state that we can identify MTE without monotonicity. Moreover, because they identify the MTE via multidimensional cross-derivatives, they do not rely on the identification-at-infinity strategy.

The following discussion shows that the model in Section 5.2 of Lee and Salanié (2018) may not be sufficient to identify the MTE. When we set , by construction we have

This equality suggests that even if is absolutely continuous with respect to the Lebesgue measure on , its support is not equal to as in Figure 5. Consequently, cannot satisfy Assumption 3.2 in Lee and Salanié (2018), which requires that the joint distribution of be absolutely continuous on and that its support be equal to .

Our model can be regarded as a double hurdle model for treatment 0. However, in a double hurdle model with three choices, we cannot define some treatments through two thresholds. For example, when treatment 0 has the form of a double hurdle model, the information in and is not sufficient to determine whether the agent receives either treatment 1 or treatment 2. As a result, we cannot identify the MTE with the multivalued treatments. With the introduction of , we successfully specify and in our model. Our model cannot be expressed in the form of model (5), however, because includes the nonlinear transformation of and . Consequently, Theorem 3.1 in Lee and Salanié (2018) is not sufficient to identify the corresponding conditional expectations of or in our model.

5.2 Heckman and Vytlacil (2007) and Heckman et al. (2008)

Heckman and Vytlacil (2007) and Heckman et al. (2008) expand the LIV approach to model (1). They study the identification conditions of three treatment effects: the treatment effect of one specific choice versus the next best alternative, the treatment effect of one specific group of choices versus the other group and the treatment effect of one specified choice versus another choice.

Heckman and Vytlacil (2007) and Heckman et al. (2008) establish sufficient conditions for the identification of the following MTE:

| (8) |

for any and , such that . To identify MTE (8), they impose a large support assumption in Theorem 8 (Heckman and Vytlacil, 2007) and Theorem 3 (Heckman et al., 2008). This large support assumption implies that one utility function, , can take a sufficiently negative value as in Assumption 4.1. Under the large support assumption, they succeed in reducing the model with three alternatives to a binary case and they achieve the identification of MTE (8).

While we impose Assumption 4.1 for the identification of thresholds, our identification strategy does not depend on the large support assumption. As a result, we achieve the identification of the MTE with two-dimensional unobserved heterogeneity . Moreover, while their MTEs are conditioned on unobserved heterogeneity , we do not require the information of distributions for heterogeneity.

5.3 Mountjoy (2022)

Mountjoy (2022) studies the effect of enrollment in 2-year community colleges on upward mobility, such as years of education and future income. With three valued treatments, he disentangles the treatment effect of 2-year college entry versus the other two treatments into two parts: the treatment effect between 2-year college entry and no college and the treatment effect between 2-year and 4-year entry. Using a novel identification approach, he identifies and estimates those treatment effects with the multivalued treatments.

Let and denote no-college treatment, 2-year college entry treatment, and 4-year college entry treatment. He define and as continuous instrumental variables specific to and , respectively and assume and depend on two instruments, i.e., , and . The observed outcome is expressed as .

Because Mountjoy (2022) is interested in a special case of the marginal treatment effect, that is, the effect of marginal policy changes for 2-year entry on the outcome of 2-year colleges, he defines new MTEs with respect to the marginal change of . Under regularity conditions, he defines and identifies the following two treatment effects with interesting decomposition.

| (9) | ||||

| (10) | ||||

where he defines

MTEs (9) and (10) reflect the marginal change between treatments induced by the marginal change in .

Our MTEs are based on unobserved heterogeneities and , which refer to the preferences of treatment 1 and treatment 2 over treatment 0, respectively. Therefore, MTE (3) corresponds to the marginal change in preferences over the choice set and is entirely different from MTEs (9) and (10). While Mountjoy (2022) does not introduce a decision model, we set utilities of 2-year and 4-year entry as like model (1). Let and denote observed terms of utilities for a 2-year college and a 4-year college, and and denote unobserved terms of utilities for a 2-year college and a 4-year college, respectively. Then, the MTEs in Mountjoy (2022) can be expressed in terms of our MTEs as follows,

where we define

6 Conclusion

We study the identification of MTE with multivalued treatments. Our model is based on a multinomial choice model with utility maximization. We establish sufficient conditions for the identification of the marginal treatment effects with multidimensional unobserved heterogeneity, which reveals treatment effects conditioned on the willingness to participate in treatments against a specific treatment. Our MTE generalizes the MTE defined in Heckman and Vytlacil (2005) in binary treatment models and our identification strategy does not depend on the large support assumption required by Heckman and Vytlacil (2007) and Heckman et al. (2008). We also establish a sufficient condition for identifying thresholds. One possible extension is the identification of the MTE with the general multivalued treatments.

References

- Angrist and Imbens (1995) Angrist, J. D. and Imbens, G. W. (1995), “Two-stage least squares estimation of average causal effects in models with variable treatment intensity,” Journal of the American statistical Association, 90, 431–442.

- Brinch et al. (2017) Brinch, C., Mogstad, M., and Wiswall, M. (2017), “Beyond LATE with a discrete instrument,” Journal of Political Economy, 125, 985–1039.

- Carneiro and Lee (2009) Carneiro, P. and Lee, S. (2009), “Estimating distributions of potential outcomes using local instrumental variables with an application to changes in college enrollment and wage inequality,” Journal of Econometrics, 149, 191–208.

- Dahl (2002) Dahl, G. B. (2002), “Mobility and the return to education: Testing a Roy model with multiple markets,” Econometrica, 70, 2367–2420.

- Fusejima (2024) Fusejima, K. (2024), “Identification of multi-valued treatment effects with unobserved heterogeneity,” Journal of Econometrics, 238, 105563.

- Heckman and Pinto (2018) Heckman, J. J. and Pinto, R. (2018), “Unordered Monotonicity,” Econometrica, 86, 1–35.

- Heckman et al. (2006) Heckman, J. J., Urzua, S., and Vytlacil, E. (2006), “Understanding Instrumental Variables in Models with Essential Heterogeneity,” The Review of Economics and Statistics, 88, 389–432.

- Heckman et al. (2008) — (2008), “Instrumental Variables in Models with Multiple Outcomes: the General Unordered Case,” Annales d’Économie et de Statistique, 151–174.

- Heckman and Vytlacil (2005) Heckman, J. J. and Vytlacil, E. (2005), “Structural Equations, Treatment Effects, and Econometric Policy Evaluation,” Econometrica, 73, 669–738.

- Heckman and Vytlacil (1999) Heckman, J. J. and Vytlacil, E. J. (1999), “Local Instrumental Variables and Latent Variable Models for Identifying and Bounding Treatment Effects,” Proceedings of the National Academy of Sciences of the United States of America, 96, 4730–4734.

- Heckman and Vytlacil (2007) — (2007), “Chapter 71 Econometric Evaluation of Social Programs, Part II: Using the Marginal Treatment Effect to Organize Alternative Econometric Estimators to Evaluate Social Programs, and to Forecast their Effects in New Environments,” in Handbook of Econometrics, eds. Heckman, J. J. and Leamer, E. E., Elsevier, vol. 6, pp. 4875–5143.

- Imbens and Angrist (1994) Imbens, G. W. and Angrist, J. D. (1994), “Identification and Estimation of Local Average Treatment Effects,” Econometrica, 62, 467–475.

- Kirkeboen et al. (2016) Kirkeboen, L. J., Leuven, E., and Mogstad, M. (2016), “Field of study, earnings, and self-selection,” The Quarterly Journal of Economics, 131, 1057–1111.

- Kline and Walters (2016) Kline, P. and Walters, C. R. (2016), “Evaluating public programs with close substitutes: The case of Head Start,” The Quarterly Journal of Economics, 131, 1795–1848.

- Lee and Salanié (2018) Lee, S. and Salanié, B. (2018), “Identifying Effects of Multivalued Treatments,” Econometrica, 86, 1939–1963.

- Matzkin (1993) Matzkin, R. (1993), “Nonparametric identification and estimation of polychotomous choice models,” Journal of Econometrics, 58, 137–168.

- McFadden (1974) McFadden, D. (1974), “Conditional logit analysis of qualitative choice behavior,” Frontiers in Econometrics, 105–142.

- Mountjoy (2022) Mountjoy, J. (2022), “Community colleges and upward mobility,” American Economic Review, 112, 2580–2630.

- Vytlacil (2002) Vytlacil, E. (2002), “Independence, Monotonicity, and Latent Index Models: An Equivalence Result,” Econometrica, 70, 331–341.

Appendix

Appendix A Proofs and Auxiliary Results

A.1 Proof of Theorem 3.1

Proof of Theorem 3.1.

We first show part (a), namely,

| (A.1) |

Let and denote a vector of thresholds and heterogeneity . Define as the indicator for treatment 0, i.e. . Set . Under the assumptions of the theorem, for any in the range of , we obtain

| (A.2) |

where the third equality holds by Assumption 2.2. Hence, for any in the range of , we have

| (A.3) |

where and . From Fubini’s theorem, the right hand side (RHS) of (A.3) is written as

It follows from Assumption 3.1 (2) and the Leibniz integral rule that, for any

Furthermore, because is finite from Assumption 3.1 (3a), and is integrable with respect to , we can exchange differentiation and integral to obtain

| (A.4) |

By applying the Leibniz integral rule to the above equation with respect to , we have

| (A.5) |

We proceed to show the identification result of the density of , namely,

| (A.6) |

From a similar argument to (A.2), under the assumptions of the theorem, for any in the range of , we obtain

Therefore, from the same argument as the one leading to (A.5), (A.6) holds. The required result (A.1) follows from (A.5) and (A.6).

We move on to the proof of part (b). Let denote the indicator for treatment 1, i.e. . From a similar argument to (A.2), under the assumptions of the theorem, for any in the range of , we obtain

| (A.7) |

where . From Fubini’s theorem, the RHS of (A.7) is written as

| (A.8) |

For treatment a, b and c, let denote the preference order, treatment a, b and c. Let denote the support of , and let denote the support of with the preference order . In the following, let and denote arbitrary points of neighborhoods of and , respectively.

We decompose the domain of integration in (A.8) into two areas, , and ,

| (A.9) | ||||

where

and correspond to and , respectively.

First, we examine the effect of a marginal change in on . Because we can exchange the order of differentiation and integration as in the case of treatment 0, we obtain

| (A.10) |

Second, we examine the effect of a marginal change in on . It follows from Assumption 3.1 (1), (2) and the Leibniz integral rule that, for any ,

Through the argument of the change of variables, we have

Because and are finite from Assumption 3.1 (3), we can exchange the order of differentiation and integration. Therefore, we obtain

| (A.11) |

We derive an alternate expansion of the RHS of (A.11). First, we use change of variable. When we set , by definition, we obtain . It holds from (A.11) that

| (A.12) |

Second, we express (A.12) as a function of a partial derivative of with respect to . It follows from Assumption 3.1 (2) and the Leibniz integral rule that, for any ,

As in the case of (A.11), we can exchange the order of differentiation and integration. Hence, differentiating the second line of (A.9) with respect to gives

| (A.13) |

In conjunction with (A.11), we obtain

| (A.14) |

We show the likelihood ratio is identifiable through the following equality,

| (A.15) |

For the proof of (A.15), first, we take the derivatives of . From a similar argument to (A.2), under the assumptions of the theorem, we have

Hence, as in (A.9), (A.10), (A.11) and (A.13), we have

| (A.16) | ||||

| (A.17) |

From the same argument as the one leading to (A.4), we have

| (A.18) |

Therefore, the required result(A.15) follows from (A.16), (A.17) and (A.18).

From (A.9), (A.10), (A.14) and (A.15), we obtain

where we define

for any and such that . Especially, when we evaluate and at , we denote

respectively. Differentiating this with respect to gives

Therefore, in conjunction with (A.6), the required result follows.

For part (c), we follow the same argument as the proof of part (b), replacing with and with , respectively. Then, we obtain the following equality

Taking its derivative with respect to gives

In conjunction with (A.6), the required result follows.

∎

A.2 Proof of Theorem 4.1

Proof of Theorem 4.1.

By definition,

where . Because we define

by Assumption 4.1, we obtain

Therefore, as ,

Hence, it follows from the dominated convergence theorem (DCT) and Fubini’s theorem that

giving the stated result for .

For , similar to the proof for , we have

From Assumption 4.1, we obtain

Therefore, as ,

Hence, it follows from the DCT and Fubini’s theorem that:

∎