Randomized low-rank approximation

of monotone matrix functions111This work has been supported by the SNSF research project Fast algorithms from low-rank updates, grant number: 200020_178806. Institute of Mathematics, EPF Lausanne, 1015 Lausanne, Switzerland. E-mails: david.persson@epfl.ch, daniel.kressner@epfl.ch

Abstract

This work is concerned with computing low-rank approximations of a matrix function for a large symmetric positive semi-definite matrix , a task that arises in, e.g., statistical learning and inverse problems. The application of popular randomized methods, such as the randomized singular value decomposition or the Nyström approximation, to requires multiplying with a few random vectors. A significant disadvantage of such an approach, matrix-vector products with are considerably more expensive than matrix-vector products with , even when carried out only approximately via, e.g., the Lanczos method. In this work, we present and analyze funNyström, a simple and inexpensive method that constructs a low-rank approximation of directly from a Nyström approximation of , completely bypassing the need for matrix-vector products with . It is sensible to use funNyström whenever is monotone and satisfies . Under the stronger assumption that is operator monotone, which includes the matrix square root and the matrix logarithm , we derive probabilistic bounds for the error in the Frobenius, nuclear, and operator norms. These bounds confirm the numerical observation that funNyström tends to return an approximation that compares well with the best low-rank approximation of . Furthermore, compared to existing methods, funNyström requires significantly fewer matrix-vector products with to obtain a low-rank approximation of , without sacrificing accuracy or reliability. Our method is also of interest when estimating quantities associated with , such as the trace or the diagonal entries of . In particular, we propose and analyze funNyström++, a combination of funNyström with the recently developed Hutch++ method for trace estimation.

1 Introduction

Matrix functions appear in many areas of applied mathematics, such as differential equations [22, 25, 45], network analysis [12, 13], statistical learning [2, 50], nuclear norm estimation [48, 49], and matrix equations [37]. Given a symmetric matrix with spectral decomposition , and a function defined on the eigenvalues of , the matrix function is defined as

Explicitly computing via this definition requires operations using standard algorithms [18], which becomes prohibitively expensive for larger .

Quite a few applications of matrix functions only require quantities associated with instead of the full matrix function. Notable examples include the trace and the diagonal elements of , which can be estimated with Monte Carlo methods [6, 7, 10, 21, 48, 49]. In recent years, there has been increased attention to the use of randomized low-rank approximation techniques in this context, for estimating these quantities [29, 43] or as a variance reduction technique for Monte Carlo methods [9, 27, 33, 35]. These techniques facilitate matrix-vector products (mvps) with random vectors to construct cheap, yet accurate, approximations of matrices with small numerical rank, see [17, 20, 34, 47] for examples. Applied to a matrix function, randomized low-rank approximation requires to perform mvps with , a nontrival task for large . Usually only itself can be accessed directly via mvps and one needs to resort to approximate methods, such as Lanczos [24, Chapter 13] and block Lanczos methods [15]. As the error of Lanczos is linked to polynomial approximations of [40, Proposition 6.3], one may observe slow convergence for “difficult” functions , for example when has a singularity close to the eigenvalues of . To avoid this, one could resort to rational approximation such as rational Krylov subspace methods [19], but these methods require the solution of a (shifted) linear system with in every iteration, which comes with challenges on its own. Even when Lanczos converges quickly and only requires a few iterations to reach the desired accuracy, the corresponding cost for approximating can still be significantly more expensive than obtaining a randomized low-rank approximation of itself.

For certain functions it is possible to obtain a low-rank approximation of directly from a low-rank approximation of , a key observation that potentially allows us to completely bypass the need for performing mvps with . The following basic lemma provides a first result in this direction, for the special case of best low-rank approximations (with respect to a unitarily invariant norm).

Lemma 1.1.

Given a symmetric positive semi-definite (SPSD) matrix consider the best rank- approximation , where is a diagonal matrix containing the largest eigenvalues of on the diagonal and contains an orthonormal basis of the corresponding eigenvectors. Then, for monotonically increasing it holds that is a best rank- approximation of . If, in addition, then .

Proof.

By the spectral decomposition of , we can write , with diagonal and orthonormal . Because the first term is a best low-rank approximation, none of the eigenvalues of is larger than any of the eigenvalues of . Because of monotonicity, the same statement holds for the relation between the eigenvalues of and . Using the spectral decomposition , this implies the first claim of the lemma. The final claim is a consequence of , since . ∎

The result of Lemma 1.1 is constrained to best rank- approximations and does not extend to the quasi-optimal rank- approximations of usually returned by (randomized) numerical algorithms. One still hopes that

| (1) |

is small when is small for a unitarily invariant norm . A similar idea was used in [43], which analyzes approximations of the form see also [29].

In this work, we will derive bounds for the approximation (1) when is an operator monotone function satisfying . A function is called operator monotone if for symmetric implies [8, p.112], where means that is SPSD; see [26, Definition 7.7.1]. Trivially, any operator monotone function is monotonically increasing, but the converse is not true. For example, the functions and are monotonically increasing on but not operator monotone. Examples of operator monotone functions include and for ; see [8, Sec. V.1]. In the following, we briefly highlight a few of the numerous applications for these functions.

Matrix square root

Matrix square roots of SPSD matrices play an important role in sampling from Gaussian distributions. If and then , and a possible choice is [36]. Having a low-rank approximation of at hand allows us to cheaply sample from . Moreover, the mean-squared error remains small for an accurate approximation :

The same technique can be used to sample from a general elliptical distribution [31].222For a general elliptical distribution the mean-squared error equals where is a constant depending on the elliptical distribution.

Matrix logarithm

The matrix function frequently appears in statistical learning [16]. In these applications one typically aims at estimating , a task that greatly benefits from low-rank approximation of .

Effective dimension

The effective dimension , also called statistical dimension, is defined as

This quantity appears in kernel learning [1, 4, 5] and inverse problems [32]. The effective dimension can once again be estimated using trace estimation, and low-rank approximation is again beneficial. Another important quantity is the diagonal of ; its entries are called the Ridge leverage scores.

1.1 Contributions

In this work we present funNyström, a new and simple method to obtain a randomized low-rank approximation of for an SPSD matrix and an increasing function satisfying . In a nutshell, our method returns , where is a Nyström approximation [17] of . A major advantage of funNyström is that it only requires mvps with and not with . Furthermore, our method can be made single-pass, meaning that we only need to access the entries of once. This property does not hold for the Nyström approximation applied to ; the Lanczos method for approximating the involved mvps with usually requires several iterations and thus repeatedly accesses .

For operator monotone we derive (probabilistic) bounds on

| (2) |

for different unitarily invariant norms , including the Frobenius norm , the nuclear norm , and the operator norm . The bounds predict that funNyström achieves similar accuracy compared to the (much more expensive) alternative of applying randomized low-rank approximation to . Let us emphasize that its inexpensiveness makes funNyström also relevant when only quantities like the trace instead of the full matrix function are needed. Our bounds not only improve and generalize the error bounds in [43] on trace estimation for but they also show how funNyström can be used to improve the recently developed Hutch++ algorithm [33] for trace estimation in the context of matrix functions.

The numerical experiments reported in this work confirm our theoretical findings; compared to existing methods funNyström requires fewer mvps with to obtain a low-rank approximation or trace estimate for , without sacrificing accuracy or reliability.

2 funNyström: Randomized low-rank approximation of matrix functions

Let denote an Gaussian random matrix, that is, its entries are i.i.d. standard normal random variables. Given an SPSD matrix , we consider the Nyström approximation

| (3) |

where denotes the Moore-Penrose pseudoinverse of a matrix and is a small integer, say, or .

Since is SPSD, we can compute its square root to obtain

The singular value decomposition (SVD) of the factor, , yields a (truncated) spectral decomposition with . Using the assumption , it follows that

Algorithm 1 implements this idea. Some remarks on our implementation of the algorithm:

- •

-

•

To mitigate numerical issues when in line 8 is highly ill-conditioned, in our implementation we truncate eigenvalues in smaller than to .

input: SPSD . Rank . Number of subspace iterations . Increasing function satisfying .

output: Spectral decomposition of

For , the loop in line 3 of Algorithm 1 becomes empty and Algorithm 1 requires a single pass over . Moreover, the mvps with , which usually constitute the dominant cost of the method, can be carried out entirely in parallel.

There is a variant of Algorithm 1 that uses the randomized SVD of instead of the Nyström approximation. This variant first computes an orthonormal basis of and then constructs a (truncated) spectral decomposition of . This variant requires mvps with . For the same number of mvps, Algorithm 1 can carry out an additional subspace iteration. The corresponding Nyström approximation is often significantly better than the one obtained from the randomized SVD with subspace iterations [17, 20, 34]. Therefore, for the case of an SPSD matrix using the Nyström approximation is often preferred.

3 Error bounds for operator monotone functions

In this section, we will derive bounds for the approximation error (2) in the Frobenius norm, nuclear norm, and the operator norm. Each of these three norm settings is of importance on its own in applications. For example, the Frobenius norm error dictates the mean square error when approximating samples from elliptical distributions and the variance of the stochastic trace estimator after using a low-rank approximation to reduce the variance of the estimator [33]. The nuclear norm is important when approximating with , since by the operator monotonicity of the nuclear norm error simplifies to the trace error; see Section 3.1 and Section 3.3 for details and Section 5 for applications of our bounds in trace estimation. Finally, the operator norm is often the most natural norm to consider when represents a (discretized) linear operator.

The following setting will be assumed for the main results presented in this section.

Setting 3.1.

For SPSD with eigenvalues , consider the spectral decomposition

| (4) |

where and . We assume and let

-

•

denote the spectral gap;

-

•

be an oversampling parameter;

-

•

be an Gaussian random matrix;

-

•

for ;

-

•

be the rank- Nyström approximation defined in (3) for ;

-

•

be operator monotone and .

Some remarks on Setting 3.1:

-

•

By the unitary invariance of Gaussian random vectors, and are independent Gaussian random matrices. This implies that holds almost surely, in which case .

-

•

The assumption has been made for convenience. When then the approximation results derived in this work become trivial because, with probability one, and the approximation error (2) is 0 in this case.333To see this, recall , where is the orthogonal projector onto . However, as argued in the proof of [20, Theorem 9.1], if then almost surely. Thus, almost surely. Consequently, almost surely.

- •

3.1 General results

We start our analysis by collecting preliminary results that do not depend on the choice of norm. For this purpose, let us recall from [17, Lemma 1] that we can write

| (5) |

where we let denote the orthogonal projection onto the range of a matrix . This implies

Combined with operator monotonicity, it follows that is approximated from below:

| (6) |

The following results hold for any unitarily invariant norm .

Lemma 3.1.

Consider SPSD matrices satisfying . Then

-

(i)

;

-

(ii)

for any increasing function ;

-

(iii)

for any operator monotone function .

Proof.

(i) Let and denote the th largest eigenvalues of and , respectively. By [26, Corollary 7.7.4 (c)], for . By Fan’s dominance theorem [8, Theorem IV.2.2], this implies .

(ii) Because of the monotonicity and non-negativity of , and hence the arguments from (i) apply.

(iii) This is a consequence of a result by Ando [3, Theorem 1]. ∎

Lemma 3.1 (ii) combined with (6) yields . The following result establishes a lower bound on in terms of the projected matrix function.

Lemma 3.2.

Under Setting 3.1 we have

| (7) |

Proof.

The following bound will be useful for relating the approximation errors of the matrix and the matrix function.

Lemma 3.3.

Under Setting 3.1 the function is decreasing and we have

Proof.

Because is a differentiable concave function we have . Letting and using gives . Hence, . The second part follows from noticing that for . ∎

3.2 Frobenius norm error bounds

In this section we will establish the following probabilistic bounds for the approximation error (2) in the Frobenius norm.

Theorem 3.4.

Under Setting 3.1 suppose that . Then

Theorem 3.5.

For our error bounds for Algorithm 1 are comparable to existing bounds [20, Theorem 10.5 and 10.7] for the direct (and much more expensive) application of the randomized SVD to .444For , by replacing in Theorem 3.4 and 3.5 with we achieve the same bounds as in [20, Theorem 10.5 and 10.7] up to constants. In the context of trace estimation, Theorem 3.5 allows us to replace the randomized SVD by Algorithm 1 in Hutch++ [33]; see Section 5 for details. Our bounds are only valid for ; in Appendix B we present (structural) bounds valid for any and for general Schatten norms but under a stronger assumption on .

3.2.1 Structural bound

Before applying probabilistic arguments, we derive a structural bound that holds for any sketching matrix such that has full rank. We begin with a simple error bound.

Lemma 3.6.

Under Setting 3.1 we have the inequality

Proof.

Lemma 3.6 combined with Lemma 3.2 allow us to bound the Frobenius norm approximation error by a projection error:

| (8) |

On the other hand, because is the best projection of the (co-)range of on the range of and we also have

| (9) |

Thus, the approximation error is sandwiched between the errors of orthogonal projections of onto and . Note that the definition is valid for any , even rational . Therefore, by (8) and (9) and (a consequence of )

which in turn implies

| (10) | ||||

where is an orthonormal basis of . This means that the error from Algorithm 1 will never exceed the error produced by the randomized SVD, using the same number of mvps with . Similar comments for can be found in [17, 20, 30, 34].

We now proceed with the main structural bound.

Lemma 3.7.

Under Setting 3.1 and assuming we have

Proof.

Letting , the inequality (8) states that . Setting with the orthogonal factor from the spectral decomposition (4), we have [20, Proposition 8.4] and thus

Setting

we note that and, in turn, . Consequently, and therefore

| (11) |

3.2.2 Probabilistic bounds

Next, we proceed with turning Lemma 3.7 into the probabilisitic bounds of Theorems 3.4 and 3.5. For this purpose we need the following results, which are common in the literature on randomized low-rank approximation; see, e.g., [20, Sec. 10.1] and [17, Lemma 7].

Lemma 3.8.

Let and be independent Gaussian matrices. If is a matrix and , then

| (15) |

Let and , then

| (16) |

holds with probability .

Proof of Theorem 3.4.

3.2.3 Improved bounds for the matrix square root

Although the square root satisfies the conditions of Setting 3.1 and the analysis above applies, it turns out that simpler and stronger bounds can be derived in this case. By Lemma 3.6 we have

Because of we have . This allows us to apply [17, Theorem 4] and obtain that

Compared to the structural bound of Lemma 3.7, this bound holds already for , it improves the exponent of as well as the constants. Expectation and deviation bounds can be easily derived using Lemma 3.8.

3.3 Nuclear norm error bounds

In this section we state and prove the following probabilistic bounds for the approximation error (2) in the nuclear norm.

Theorem 3.9.

Under Setting 3.1 suppose that and . Then

Theorem 3.10.

Because of the nuclear norm of simplifies to the trace. Hence, Theorem 3.9 and Theorem 3.10 provide bounds on the error of the trace approximation

Similar bounds appear in [43] for ; see Section 5 for further discussion.

3.3.1 Structural bound

We now proceed with deriving a structural bound for the nuclear norm error.

Lemma 3.11.

Under Setting 3.1 and assuming we have

Proof.

As in the proof of Lemma 3.7, we set . Applying Lemma 3.2 for the nuclear norm yields

Using the factorization , one obtains

Being a composition of operator monotone functions, the function is operator monotone [8, Exercise V.1.10]. Applying the inequality (13) from the proof of Lemma 3.7 to instead of yields

where the final equality follows from because is decreasing. ∎

3.3.2 Probabilistic bounds

As in the case of the Frobenius norm, we use the results of Lemma 3.8 to turn Lemma 3.11 into the probabilistic bounds of Theorems 3.9 and 3.10.

Proof of Theorem 3.9.

3.3.3 Improved bounds for the matrix square-root

3.4 Operator norm error bounds

Finally, we present bounds for the error (2) in the operator norm.

Theorem 3.12.

Under Setting 3.1 suppose that and . Then

For conciseness we only state an expectation bound. From the proof of Theorem 3.12, it follows that a deviation bound can be obtained from a deviation bound on the quantity ; see, e.g., [20, Theorem 10.8] for such a bound.

3.4.1 Structural bound

We first state a structural bound that holds in any unitarily invariant norm . The proof of this lemma is included in Appendix A.

Lemma 3.13.

Under Setting 3.1, assume that and let . Then

The result of Lemma 3.13 simplifies for the operator norm because

Corollary 3.14.

Under Setting 3.1 and assuming , one has

3.4.2 Probabilistic bounds

In order to obtain the expectation bound of Theorem 3.12 from Corollary 3.14 we make use of the following result established in [14, Appendix B].

Lemma 3.15.

Let and be independent Gaussian matrices. If is a matrix, then

| (17) |

3.4.3 Improved bounds for the matrix square-root

4 Numerical Experiments

In this section, we verify the performance of funNyström numerically. All experiments have been performed in MATLAB (version 2020a) on a MacBook Pro with a 2.3 GHz Intel Core i7 processor with 4 cores. Scripts to reproduce all figures in this paper are available at https://github.com/davpersson/funNystrom.

We compare the approximation returned by funNyström with the following references. Applying Nyström directly to with an Gaussian random matrix yields the rank- approximation

| (18) |

This assumes that mvps with are carried out exactly. If each mvp with needed in (18) is approximated using iterations of the Lanczos method, one obtains a different approximation, which will be denoted by .

Given an approximation of , we will measure the relative error for some norm .

4.1 Test matrices

In the following, we describe the test matrices used in our experiments.

4.1.1 Synthetic matrices

We consider synthetic matrices with prescribed algebraic and exponential eigenvalue decays. Let and be diagonal matrices with diagonal entries

for parameters and . Letting denote the orthogonal matrix generated by the MATLAB-command gallery(’orthog’,n,1), we set

| (19) |

Unless specified otherwise, we choose .

4.1.2 Gaussian process covariance kernels

We consider two classes of matrices that arise from the discretization of the squared exponential and Matérn Gaussian process covariance kernels [44]. For this purpose, we generate i.i.d. data points and set

| (20) | |||

| (21) |

for , and parameters . Note that is the modified Bessel function of the second kind. Computing , where is a matrix arising from discretizing a covariance kernel, is an important task in Bayesian optimization and maximum likelihood estimation for Gaussian processes [16, 50].

4.1.3 Bayesian inverse problem

Motivated by the numerical experiments in [2, 11, 43], this test matrix arises from a Bayesian inverse problem. Consider the parabolic partial differential equation

| (22) | ||||

for and and . We place 49 sensors at for to take measurements of at these sensor locations at times . We gather all measurements in a vector .

Discretizing (22) in space using finite differences on equispaced grid yields an ordinary differential equation of the form

| (23) | ||||

The solution to (23) is . Let contain the values of corresponding to sensor locations at times . Then, by linearity, we can write for a matrix .

Assume that , the discretization error is negligible, and that the measurements are distorted by some noise so that

It is well known that the posterior distribution of is given by with

see [46]. Now let

| (24) |

Then, is related to the expected information gain from the posterior distribution relative to the prior distribution [2]. For fine discretization grids, the matrix , and thus , cannot be formed explicitly. Instead, one only implicitly performs mvps with via solving (23).

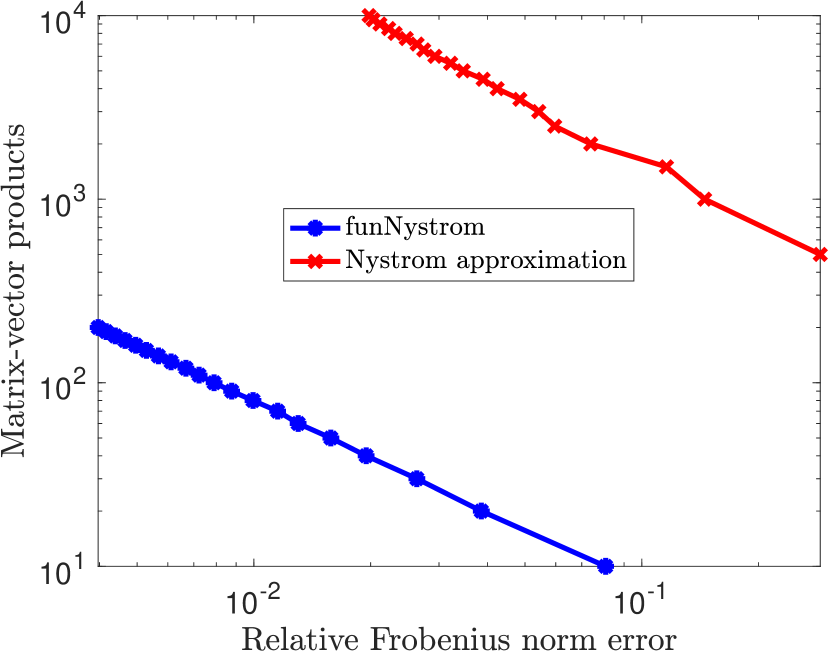

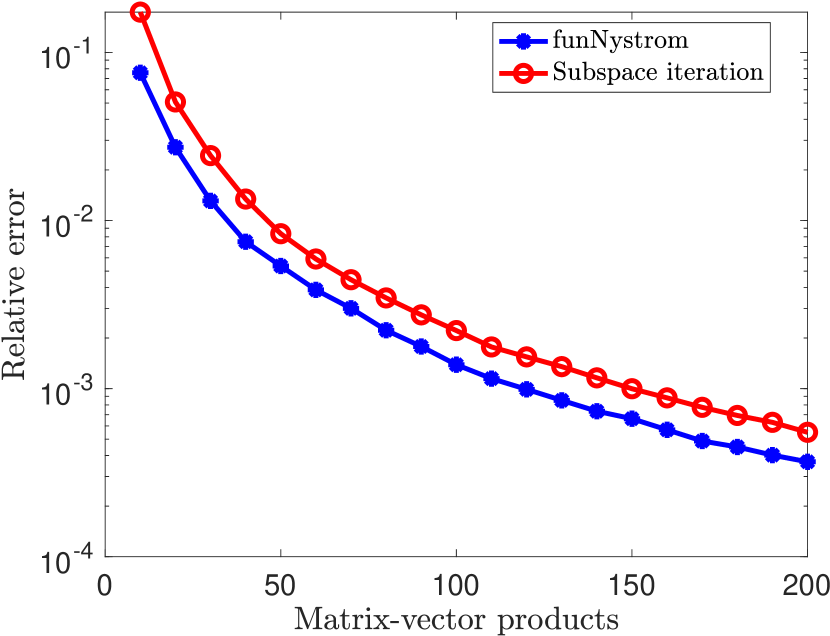

4.2 Comparing number of mvps

Recall that Algorithm 1 requires mvps with to compute . In contrast, the approximation – obtained via applying Nyström to – requires mvps with . The choice of , the number of Lanczos iterations, needs to be chosen in dependence of such that the impact on the overall accuracy remains negligible. For the purpose of our numerical comparison, we have precomputed the matrix obtained without the additional Lanczos approximation and choose such that

| (25) |

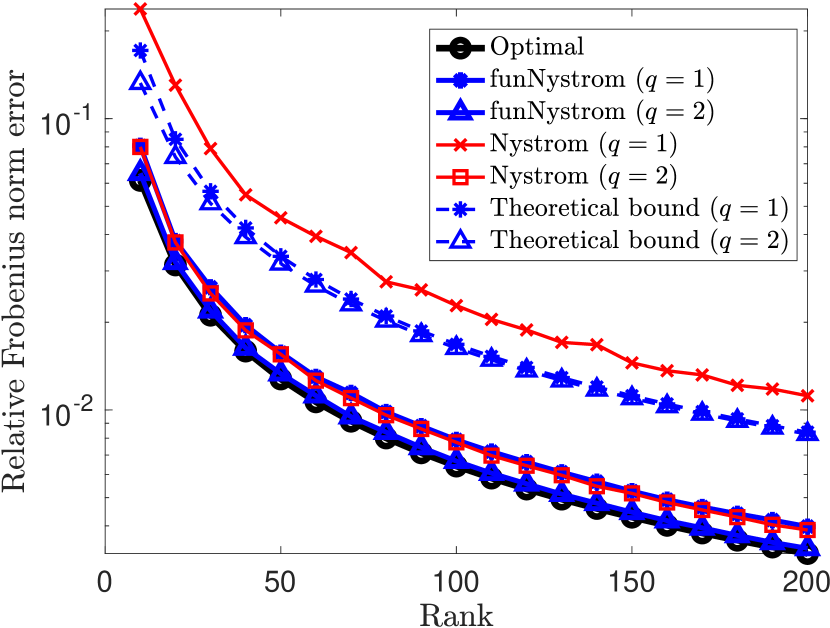

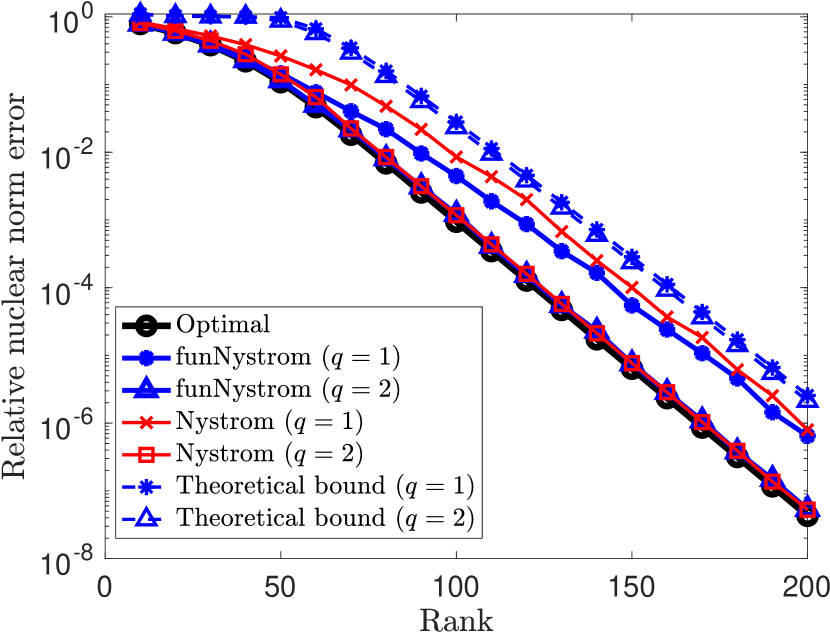

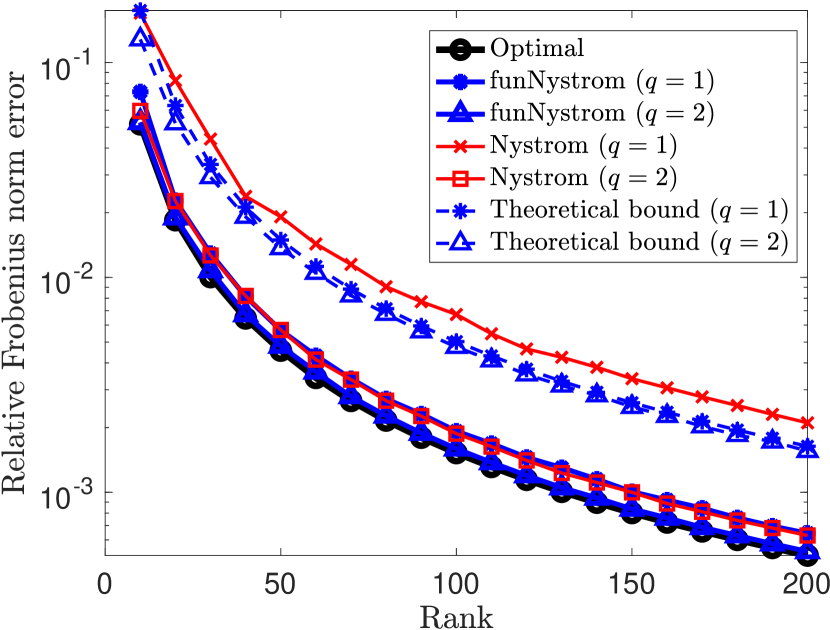

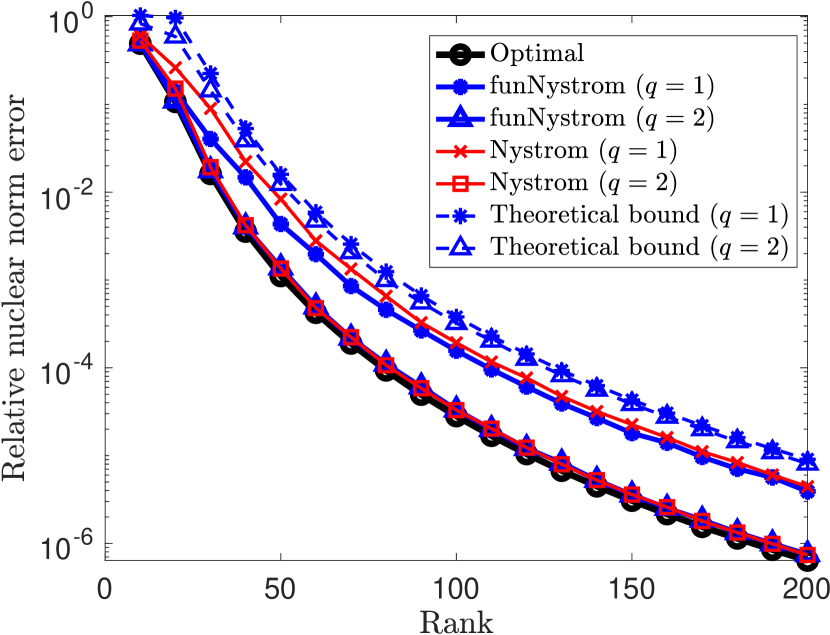

In practice, is not available and one needs to employ heuristic and potentially less reliable criteria. In our implementation we increase by 5 until (25) is satisfied. The results obtained for are reported in Figure 1. Clearly, Algorithm 1 needs fewer mvps; the difference can be up to three orders of magnitude.

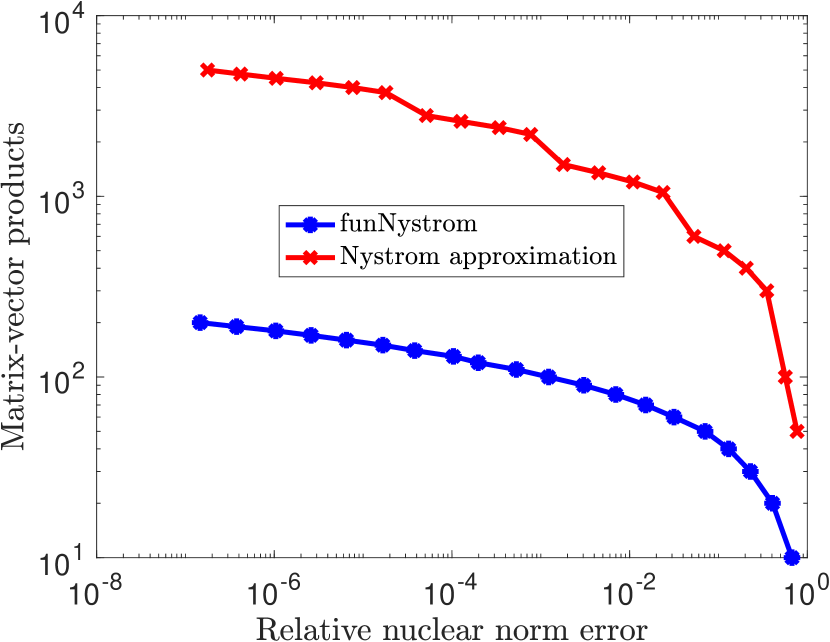

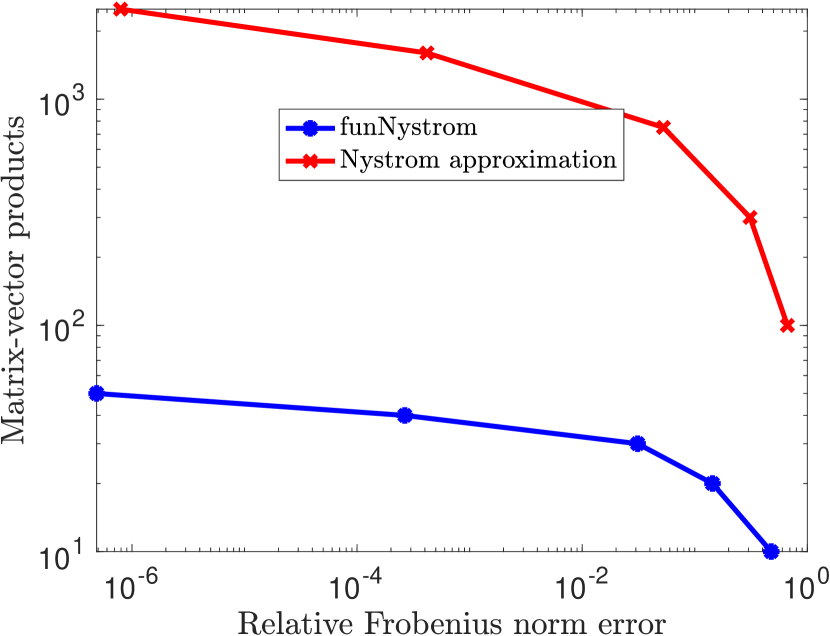

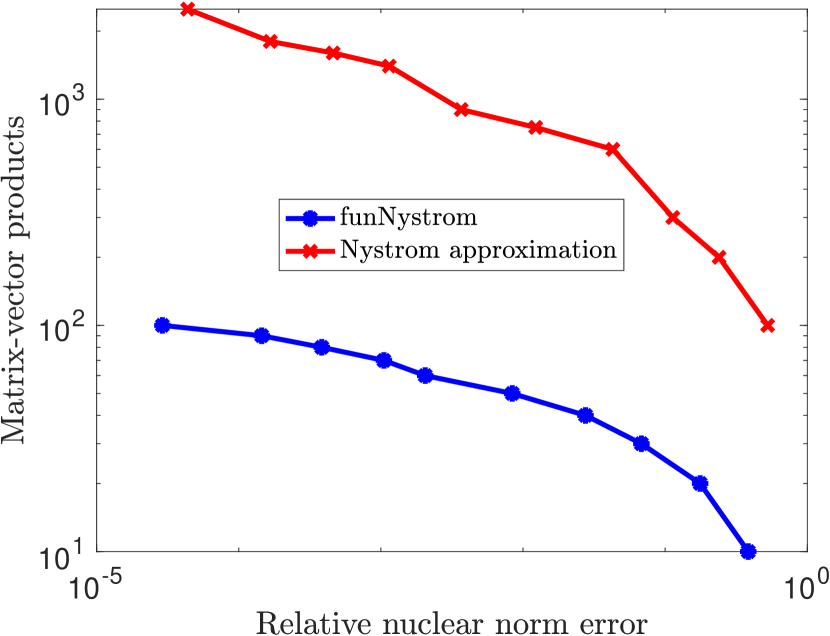

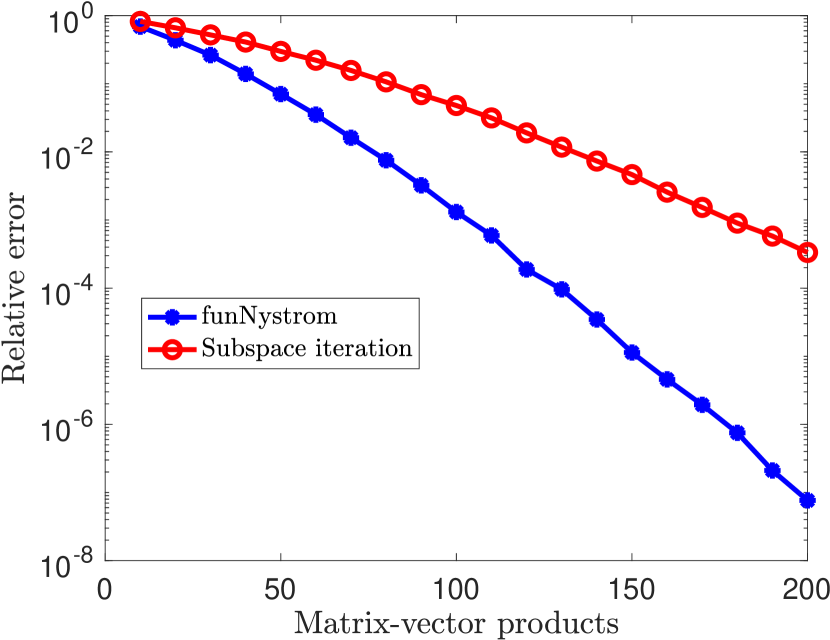

4.3 Comparing accuracy

In Figure 2, we compare the approximation error of Algorithm 1 with the (significantly more expensive) approximation . It can be observed that Algorithm 1 is never worse than , and sometimes even better. This suggests that even when mvps with can be performed very efficiently, Algorithm 1 may still be the preferred choice. In the figures we also plot the expectation error bounds from Section 3.2.3 and Theorem 3.9 for choices of and that minimize the right-hand side of the error bound. For our bounds recover the empirical error up to a factor less than 10. For the performance of Algorithm 1 is sometimes significantly better than our bounds predict, suggesting that there is room to tighten the bounds for .

4.4 Fast computation of mvps

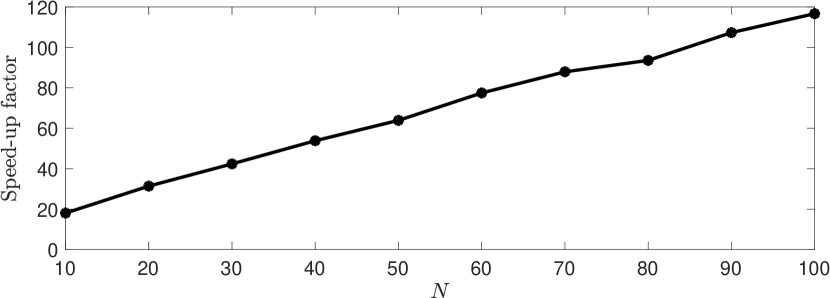

In this section we show that Algorithm 1 can be used to compute fast mvps with . We let and defined in (19) with and . We let be the matrix containing the first columns of the identity matrix. Hence, computing requires mvps with . We compare the computation times of the following two methods for approximating :

-

1.

Approximating using the Lanczos method with iterations. This comes at a computational cost of . The implementation we use for the Lanczos method is the same implementation used for the numerical expriments in [33], which approximates the mvps with simultaneously by vectorizing all computations, rather than approximating the mvps subsequently. This significantly speeds up the computation.

-

2.

Computing using Algorithm 1 and approximate . This comes at a computational cost of .

If we let and be wall-clock time to approximate mvps with using the Lanczos method and low-rank approximation respectively, the speed-up factor will be

if we keep and constant and assume .

In our numerical experiments we set . This choice of parameters yields a similar relative error for both methods and for all , where is the approximation to . We set . The results are presented in Figure 3, which confirm the speed-up factor.

5 Application to trace estimation

In this section, we discuss how funNyström can be used to approximate , the trace of , under Setting 3.1.

5.1 Trace estimation via low-rank approximation

When an matrix admits an excellent rank- approximation for , it is sensible to approximate by . Setting , this motivates the approximation

| (26) |

where denotes the output of Algorithm 1 with . Using that we get

Hence, Theorem 3.9 and Theorem 3.10 yield probabilistic bounds for the error of this trace approximation.

It is instructive to compare our results with the bounds from [43] for the special case . In particular, Theorem 1 from [43] states that

| (27) | ||||

where is an orthonormal basis for , and

Constructing requires a total of mvps with . On the other hand, within the same budget one obtains the more accurate low-rank approximation . This also translates into tighter probabilistic bounds for trace estimation. To see this, note that Theorem 3.9 gives

The difference between (27) and this bound satisfies

for .555We use for small . Because and usually , this shows that we obtain a much tighter bound for our method compared to [43]. Similarly, it can be shown that our deviation bounds are tighter than those in [43]. Similar bounds for exist in [23, Theorem A.1]. By an identical argument we can show that our bounds are tighter than those in [23].

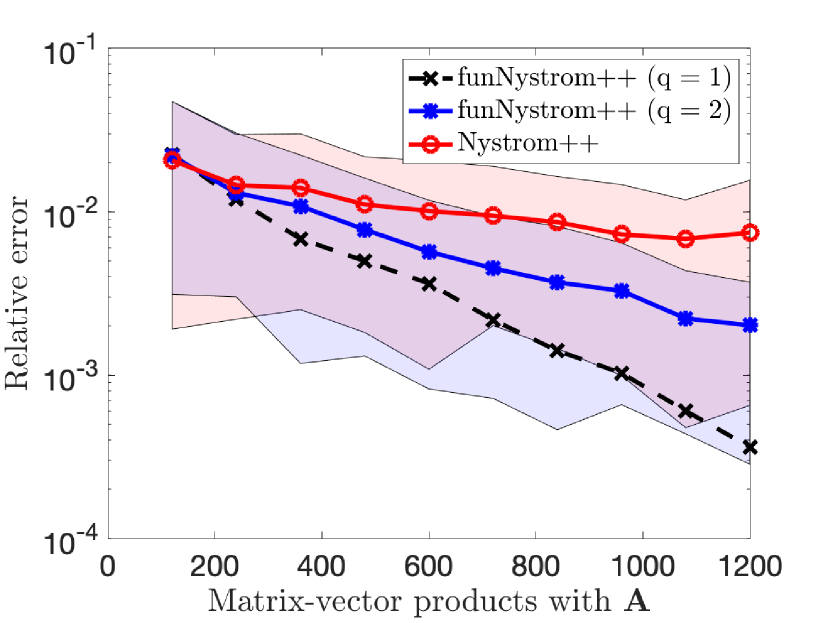

In Figure 4 we compare our approach, funNystrom combined with (26), with the method presented in [43] to approximate . We choose for both methods, since we have observed that increasing the rank of the low-rank approximation often yields a more accurate low-rank approximation than increasing . A budget of mvps allows one to choose in Algorithm 1 while one can only choose in the method from [43]. This explains the better performance of funNystrom observed in Figure 4; a similar observation has been made in [35, Section 3].

5.2 funHutch++

A popular way to approximate the trace of an SPSD matrix is to apply a stochastic estimator of the form

| (28) |

for an random matrix ; in the following, we assume that is Gaussian random. To achieve a relative error of (that is, with high probability) one generally needs to choose ; see [10, 11, 38, 39, 48, 49]. Hutch++ [33, Algorithm 1] reduces this number to by combining (28) with (randomized) low-rank approximation. More specifically, given a budget of mvps with , Hutch++666Hutch++ as presented in [33] uses Rademacher matrices instead of Gaussian random matrices. In order to remain consistent with the rest of this paper we choose all random matrices to be Gaussians, which incurs no significant difference in the theory or numerical performance of Hutch++. spends mvps to construct a rank- approximation based on the randomized SVD [20]. The remaining mvps are used to estimate the trace of the difference using (28).

In [35, Section 3] a variant called Nyström++ is presented, which – instead of the randomized SVD – constructs a rank- Nyström approximation using mvps. The remaining mvps are used to computed the correction . Nyström++ retains the property of Hutch++ that only mvps are needed to obtain a relative error of , and it often provides better numerical performance. We refer to [9, 27] for further variants of Hutch++.

When for SPSD and a monotonically increasing function satisfying , we can derive a cheaper version of Nyström++ by letting and thus considering the approximation

see also Algorithm 2. The first part of this approximation bypasses the need for performing mvps with .

input: SPSD . Rank . Number of subspace iterations . Number of samples in stochastic trace estimator . Increasing function satisfying .

output: An approximation .

The second part of the approximation still requires to perform or approximate such mvps via, e.g., the Lanczos method. Note that Algorithm 2 coincides with Nyström++ for . The following theorem extends the theoretical result on Hutch++ from [33, Theorem 1.1] to Algorithm 2.

Theorem 5.1.

Let be operator monotone with , SPSD, and . Then one can choose such that the output of Algorithm 2 satisfies for any the error bound

with probability at least .

Proof.

Let for . Applying Theorem 3.5, with and using , it follows that

holds with probability at least . Thus, by [33, Lemma 3.1] we have with probability at least that

Following the arguments in the proof of [35, Theorem 3.4], there are constants such that for , we have

with probability at least . Setting completes the proof. ∎

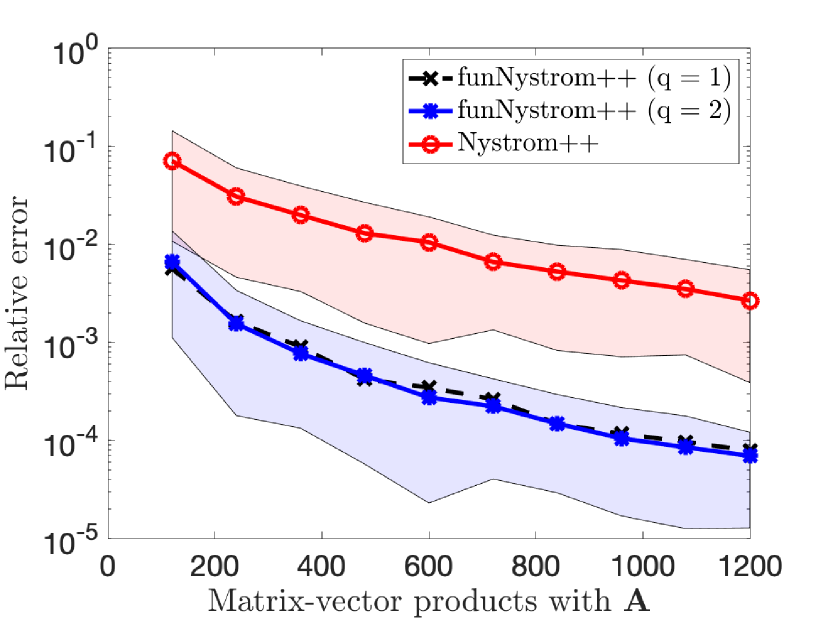

We compare Algorithm 2 with Nyström++ from [35]. For Algorithm 2 we let , , and for Nyström++ we set . We approximate mvps with using 10 iterations of the Lanczos method. Hence, for both the Nyström++ algorithm and Algorithm 2 we perform mvps with . The obtained results are presented in Figure 5. They indicate that Algorithm 2 with and can perform significantly better than Nyström++. It is interesting to note that our algorithms performs well for even though this choice is not covered by the result of Theorem 5.1.

6 Conclusion

funNyström is a new and simple method for obtaining a low-rank approximation to for an SPSD matrix . The experimental and theoretical evidence presented in this work seems to suggest that funNyström is currently the method of choice for an operator monotone function with . In contrast to standard randomized methods applied to , our method does not require exact or approximate matrix-vector products with . We have demonstrated that also other quantities associated with matrix functions, such as the trace, can be cheaply computed via funNyström.

Acknowledgments

We thank the referees and Arvind Saibaba for helpful comments on this work.

References

- [1] A. Alaoui and M. W. Mahoney, Fast randomized kernel ridge regression with statistical guarantees, in Advances in Neural Information Processing Systems, vol. 28, 2015.

- [2] A. Alexanderian, N. Petra, G. Stadler, and O. Ghattas, A-optimal design of experiments for infinite-dimensional Bayesian linear inverse problems with regularized -sparsification, SIAM J. Sci. Comput., 36 (2014), pp. A2122–A2148.

- [3] T. Ando, Comparison of norms and , Math. Z., 197 (1988), pp. 403–409.

- [4] H. Avron, K. L. Clarkson, and D. P. Woodruff, Faster kernel ridge regression using sketching and preconditioning, SIAM J. Matrix Anal. Appl., 38 (2017), pp. 1116–1138.

- [5] , Sharper bounds for regularized data fitting, in Approximation, randomization, and combinatorial optimization. Algorithms and techniques, vol. 81 of LIPIcs. Leibniz Int. Proc. Inform., Schloss Dagstuhl. Leibniz-Zent. Inform., Wadern, 2017, pp. Art. No. 27, 22.

- [6] R. A. Baston and Y. Nakatsukasa, Stochastic diagonal estimation: probabilistic bounds and an improved algorithm, arXiv preprint arXiv:2201.10684, (2022).

- [7] C. Bekas, E. Kokiopoulou, and Y. Saad, An estimator for the diagonal of a matrix, Appl. Numer. Math., 57 (2007), pp. 1214–1229.

- [8] R. Bhatia, Matrix analysis, vol. 169 of Graduate Texts in Mathematics, Springer-Verlag, New York, 1997.

- [9] T. Chen and E. Hallman, Krylov-aware stochastic trace estimation, arXiv preprint arXiv:2205.01736, (2022).

- [10] A. Cortinovis and D. Kressner, On randomized trace estimates for indefinite matrices with an application to determinants, Foundations of Computational Mathematics, (2021), pp. 1–29.

- [11] E. Dudley, A. K. Saibaba, and A. Alexanderian, Monte Carlo estimators for the Schatten -norm of symmetric positive semidefinite matrices, Electron. Trans. Numer. Anal., 55 (2022), pp. 213–241.

- [12] E. Estrada, Characterization of 3D molecular structure, Chemical Physics Letters, 319 (2000), pp. 713–718.

- [13] E. Estrada and D. J. Higham, Network properties revealed through matrix functions, SIAM Rev., 52 (2010), pp. 696–714.

- [14] Z. Frangella, J. A. Tropp, and M. Udell, Randomized Nyström preconditioning, arXiv preprint arXiv:2110.02820, (2021).

- [15] A. Frommer, K. Lund, and D. B. Szyld, Block Krylov subspace methods for functions of matrices II: Modified block FOM, SIAM J. Matrix Anal. Appl., 41 (2020), pp. 804–837.

- [16] J. Gardner, G. Pleiss, K. Q. Weinberger, D. Bindel, and A. G. Wilson, Gpytorch: Blackbox matrix-matrix gaussian process inference with gpu acceleration, in Advances in Neural Information Processing Systems, vol. 31, 2018.

- [17] A. Gittens and M. W. Mahoney, Revisiting the Nyström method for improved large-scale machine learning, J. Mach. Learn. Res., 17 (2016), pp. Paper No. 117, 65.

- [18] G. H. Golub and C. F. Van Loan, Matrix computations, Johns Hopkins Studies in the Mathematical Sciences, Johns Hopkins University Press, Baltimore, MD, fourth ed., 2013.

- [19] S. Güttel, Rational Krylov approximation of matrix functions: numerical methods and optimal pole selection, GAMM-Mitt., 36 (2013), pp. 8–31.

- [20] N. Halko, P. G. Martinsson, and J. A. Tropp, Finding structure with randomness: probabilistic algorithms for constructing approximate matrix decompositions, SIAM Rev., 53 (2011), pp. 217–288.

- [21] E. Hallman, I. C. Ipsen, and A. Saibaba, Monte carlo methods for estimating the diagonal of a real symmetric matrix, arXiv preprint arXiv:2202.02887, (2022).

- [22] T. F. Havel, I. Najfeld, and J.-x. Yang, Matrix decompositions of two-dimensional nuclear magnetic resonance spectra, Proceedings of the National Academy of Sciences, 91 (1994), pp. 7962–7966.

- [23] E. Herman, A. Alexanderian, and A. K. Saibaba, Randomization and reweighted -minimization for A-optimal design of linear inverse problems, SIAM J. Sci. Comput., 42 (2020), pp. A1714–A1740.

- [24] N. J. Higham, Functions of matrices, Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA, 2008. Theory and computation.

- [25] , The scaling and squaring method for the matrix exponential revisited, SIAM Rev., 51 (2009), pp. 747–764.

- [26] R. A. Horn and C. R. Johnson, Matrix analysis, Cambridge University Press, Cambridge, second ed., 2013.

- [27] S. Jiang, H. Pham, D. Woodruff, and R. Zhang, Optimal sketching for trace estimation, in Advances in Neural Information Processing Systems, vol. 34, 2021, pp. 23741–23753.

- [28] E.-Y. Lee, Extension of Rotfel’d theorem, Linear Algebra Appl., 435 (2011), pp. 735–741.

- [29] H. Li and Y. Zhu, Randomized block Krylov subspace methods for trace and log-determinant estimators, BIT, 61 (2021), pp. 911–939.

- [30] P.-G. Martinsson, Randomized methods for matrix computations, in The mathematics of data, vol. 25 of IAS/Park City Math. Ser., Amer. Math. Soc., Providence, RI, 2018, pp. 187–229.

- [31] A. J. McNeil, R. Frey, and P. Embrechts, Quantitative risk management, Princeton Series in Finance, Princeton University Press, Princeton, NJ, revised ed., 2015.

- [32] M. Meier and Y. Nakatsukasa, Randomized algorithms for Tikhonov regularization in linear least squares, arXiv preprint arXiv:2203.07329, (2022).

- [33] R. A. Meyer, C. Musco, C. Musco, and D. P. Woodruff, Hutch++: Optimal stochastic trace estimation, in Symposium on Simplicity in Algorithms (SOSA), SIAM, 2021, pp. 142–155.

- [34] Y. Nakatsukasa, Fast and stable randomized low-rank matrix approximation, arXiv preprint arXiv:2009.11392, (2020).

- [35] D. Persson, A. Cortinovis, and D. Kressner, Improved variants of the Hutch++ algorithm for trace estimation, SIAM J. Matrix Anal. Appl., 43 (2022), pp. 1162–1185.

- [36] G. Pleiss, M. Jankowiak, D. Eriksson, A. Damle, and J. Gardner, Fast matrix square roots with applications to Gaussian processes and Bayesian optimization, Advances in Neural Information Processing Systems, 33 (2020), pp. 22268–22281.

- [37] J. D. Roberts, Linear model reduction and solution of the algebraic riccati equation by use of the sign function, International Journal of Control, 32 (1980), pp. 677–687.

- [38] F. Roosta-Khorasani and U. Ascher, Improved bounds on sample size for implicit matrix trace estimators, Found. Comput. Math., 15 (2015), pp. 1187–1212.

- [39] F. Roosta-Khorasani, G. J. Székely, and U. M. Ascher, Assessing stochastic algorithms for large scale nonlinear least squares problems using extremal probabilities of linear combinations of gamma random variables, SIAM/ASA J. Uncertain. Quantif., 3 (2015), pp. 61–90.

- [40] Y. Saad, Iterative methods for sparse linear systems, SIAM, Philadelphia, PA, second ed., 2003.

- [41] , Numerical methods for large eigenvalue problems, vol. 66 of Classics in Applied Mathematics, SIAM, Philadelphia, PA, 2011.

- [42] A. K. Saibaba, Randomized subspace iteration: analysis of canonical angles and unitarily invariant norms, SIAM J. Matrix Anal. Appl., 40 (2019), pp. 23–48.

- [43] A. K. Saibaba, A. Alexanderian, and I. C. F. Ipsen, Randomized matrix-free trace and log-determinant estimators, Numer. Math., 137 (2017), pp. 353–395.

- [44] M. Seeger, Gaussian processes for machine learning, International journal of neural systems, 14 (2004), pp. 69–106.

- [45] R. B. Sidje and W. J. Stewart, A numerical study of large sparse matrix exponentials arising in markov chains, Computational Statistics & Data Analysis, 29 (1999), pp. 345–368.

- [46] A. M. Stuart, Inverse problems: a Bayesian perspective, Acta Numer., 19 (2010), pp. 451–559.

- [47] J. A. Tropp, A. Yurtsever, M. Udell, and V. Cevher, Fixed-rank approximation of a positive-semidefinite matrix from streaming data, in Advances in Neural Information Processing Systems, vol. 30, 2017.

- [48] S. Ubaru, J. Chen, and Y. Saad, Fast estimation of via stochastic Lanczos quadrature, SIAM J. Matrix Anal. Appl., 38 (2017), pp. 1075–1099.

- [49] S. Ubaru and Y. Saad, Applications of trace estimation techniques, in International Conference on High Performance Computing in Science and Engineering, Springer, 2017, pp. 19–33.

- [50] J. Wenger, G. Pleiss, P. Hennig, J. P. Cunningham, and J. R. Gardner, Reducing the variance of Gaussian process hyperparameter optimization with preconditioning, arXiv preprint arXiv:2107.00243, (2021).

Appendix A Proof of Lemma 3.13

To prove the structural bound of Lemma 3.13 for an arbitrary unitarily invariant norm , we make use of the following auxiliary result.

Lemma A.1 ([28, Theorem 2.1]).

Let be concave. Then given a partitioned SPSD matrix with square and , one has

Proof of Lemma 3.13.

From (5) it follows that

where we set and . Combined with Lemma 3.1, this gives

As in the proof of Lemma 3.7, we set Using , we obtain and, in turn, . Using Lemma 3.1 (ii), this gives

| (29) |

Exploiting the block structure (12) of the SPSD matrix and applying Lemma A.1 yields

The proof is completed using the inequalities

which are derived from the inequalities in (12) with the same arguments used for (29). ∎

Appendix B Structural bounds for general Schatten norms

The Schatten- norm for is a unitarily invariant norm defined as the norm of the vector of singular values of a matrix. It includes the Frobenius norm (), the nuclear norm (), as well as the operator norm (). Deriving a structural bound from the result of Lemma 3.13 for general is not straightforward; the result for crucially depends on Lemma 3.15, for which we do not know an extension for general . To circumvent this difficulty, the bound involves , the right derivative of at , which needs to be assumed finite.

Theorem B.1.

Under Setting 3.1, assume that and . Then

Proof.

Since is concave its maximal derivative is assumed at . Together with , this implies for any square matrix . In particular,

Applying Lemma 3.13 yields

| (30) |

which already establishes the result for .