Multiscale Comparison

of Nonparametric Trend Curves

Marina Khismatullina111Corresponding author. Address: Erasmus School of Economics, Erasmus University Rotterdam, 3062 PA Rotterdam, Netherlands. Email: khismatullina@ese.eur.nl.

Erasmus University Rotterdam

Michael Vogt222Address: Institute of Statistics, Department of Mathematics and Economics, Ulm University, 89081 Ulm, Germany. Email: m.vogt@uni-ulm.de.

Ulm University

We develop new econometric methods for the comparison of nonparametric time trends. In many applications, practitioners are interested in whether the observed time series all have the same time trend. Moreover, they would often like to know which trends are different and in which time intervals they differ. We design a multiscale test to formally approach these questions. Specifically, we develop a test which allows to make rigorous confidence statements about which time trends are different and where (that is, in which time intervals) they differ. Based on our multiscale test, we further develop a clustering algorithm which allows to cluster the observed time series into groups with the same trend. We derive asymptotic theory for our test and clustering methods. The theory is complemented by a simulation study and two applications to GDP growth data and house pricing data.

Key words: Multiscale statistics; nonparametric regression; time series errors; shape constraints; strong approximations; anti-concentration bounds.

JEL classifications: C12; C14; C23; C38.

1 Introduction

The comparison of time trends is an important topic in time series analysis and has a wide range of applications in economics, finance and other fields such as climatology. In economics, one may wish to compare trends in real GDP (Grier and Tullock, 1989) or trends in long-term interest rates (Christiansen and Pigott, 1997) across different countries. In finance, it is of interest to compare the volatility trends of different stocks (Nyblom and Harvey, 2000). In climatology, researchers are interested in comparing the trending behaviour of temperature time series across different spatial locations (Karoly and Wu, 2005).

In this paper, we develop new econometric methods for the comparison of time trends. Classically, time trends are modelled stochastically in econometrics; see e.g. Stock and Watson (1988). Recently, however, there has been a growing interest in econometric models with deterministic time trends; see Cai (2007), Atak et al. (2011), Robinson (2012), Chen et al. (2012), Zhang et al. (2012) and Hidalgo and Lee (2014) among others. Following this recent development, we consider a general panel model with deterministic time trends. We observe a panel of time series for , where are real-valued random variables and are -dimensional random vectors. Each time series is modelled by the equation

| (1.1) |

for , where is a vector of unknown parameters, is a vector of individual covariates or controls, is an unknown nonparametric (deterministic) trend function defined on the rescaled time interval , is a fixed effect error term and is a zero-mean stationary error process. A detailed description of model \tagform@1.1 together with the technical assumptions on the various model components can be found in Section 2.

An important question in many applications is whether the nonparametric time trends in model \tagform@1.1 are all the same. This question can formally be addressed by a statistical test of the null hypothesis

against the alternative : for some and . The problem of testing versus is well studied in the literature. In a restricted version of model \tagform@1.1 without covariates, it has been investigated in Härdle and Marron (1990), Hall and Hart (1990), Degras et al. (2012) and Chen and Wu (2019) among many others. Test procedures in a less restricted version of model \tagform@1.1 with covariates and homogeneous parameter vectors ( for all ) have been derived, for instance, in Zhang et al. (2012) and Hidalgo and Lee (2014).

Even though many different approaches to test versus have been developed over the years, most of them have a serious shortcoming: they are very uninformative. More specifically, they only allow to test whether the trend curves are the same or not. But they do not give any information on which curves are different and where (that is, in which time intervals) they differ. The following example illustrates the importance of this point: Suppose a group of researchers wants to test whether the GDP trend is the same in ten different countries. If the researchers use a test which is uninformative in the above sense and this test rejects , they can only infer that there are at least two countries with a different trend. They do not obtain any information on which countries have a different GDP trend and where (that is, in which time periods) the trends differ. However, this is exactly the information that is relevant in practice. Without it, it is hardly possible to get a good economic understanding of the situation at hand. The main aim of the present paper is to construct a test procedure which provides the required information. More specifically, we construct a test which allows to make rigorous confidence statements about (i) which trend curves are different and (ii) where (that is, in which time intervals) they differ.

Very roughly speaking, our approach works as follows: Let be the rescaled time interval with midpoint and length . We call the location and the scale of the interval . For any given location-scale pair , let

be the hypothesis that the two trend curves and are identical on the interval . Our procedure simultaneously tests for a wide range of different location-scale pairs and all pairs . As it takes into account multiple scales , it is called a multiscale method. Our main theoretical result shows that under suitable technical conditions, the developed multiscale test controls the familywise error rate, that is, the probability of wrongly rejecting at least one null hypothesis . As we will see, this allows us to make simultaneous confidence statements of the following form for a given significance level :

| With probability at least , the trends and differ on any interval and for any pair for which is rejected. | (1.2) |

Hence, as desired, we can make confidence statements about which trend curves are different and where they differ.

To the best of our knowledge, there are no other test procedures available in the literature which allow to make simultaneous confidence statements of the form \tagform@1.2 in the context of the general model \tagform@1.1. We are only aware of two other multiscale tests for the comparison of nonparametric time trends, both of which are restricted to a strongly simplified version of model \tagform@1.1 without covariates. The first one is a SiZer-type test by Park et al. (2009), for which theory has only been derived in the special case of time series. The second one is a multiscale test by Khismatullina and Vogt (2021), which was developed to detect differences between epidemic time trends in the context of the COVID-19 pandemic. Notably, our multiscale test can be regarded as an extension of the approach in Khismatullina and Vogt (2021). In the present paper, we go beyond the quite limited model setting in Khismatullina and Vogt (2021) and develop multiscale inference methods in the general model framework \tagform@1.1 which allows to deal with a wide range of economic and financial applications. Moreover, we develop a clustering algorithm based on our multiscale test which allows to detect groups of time series with the same trend.

Our multiscale test is constructed step by step in Section 3, whereas its theoretical properties are laid out in Section 4. The clustering algorithm is introduced and investigated in Section 5. The proofs of all theoretical results are relegated to the technical Appendix. We complement the theoretical analysis of the paper by a simulation study and two application examples in Sections 6 and 7. In the first application example, we use our test and clustering methods to examine GDP growth data from different OECD contries. We in particular test the hypothesis that there is a common GDP trend in these countries and we cluster the countries into groups with the same trend. In the second example, we examine a long record of housing price data from different countries and compare the price trends in these countries by our methods.

2 The model framework

2.1 Notation

Throughout the paper, we adopt the following notation. For a vector , we write to denote its -norm and use the shorthand in the special case . For a random variable , we define its -norm by and write in the case .

Let () be independent and identically distributed (i.i.d.) random variables, write and let be a measurable function such that is a properly defined random variable. Following Wu (2005), we define the physical dependence measure of the process by

| (2.1) |

where is a coupled version of with being an i.i.d. copy of . Evidently, measures the dependency of the random variable on the innovation term .

2.2 Model

We observe a panel of time series of length for . Each time series satisfies the model equation

| (2.2) |

for , where is a vector of unknown parameters, is a vector of individual covariates, is an unknown nonparametric trend function defined on the unit interval with for all , is a (deterministic or random) intercept term and is a zero-mean stationary error process. As common in nonparametric regression, the trend functions in model \tagform@2.2 depend on rescaled time rather than on real time ; see e.g. Robinson (1989), Dahlhaus (1997) and Vogt and Linton (2014) for a discussion of rescaled time in nonparametric estimation. The condition is required for identification of the trend function in the presence of the intercept . We allow to be correlated with the covariates in an arbitrary way. Hence, can be regarded as a fixed effect error term. We do not impose any restrictions on the dependence between the fixed effects across . Similarly, the covariates are allowed to be dependent across in an arbitrary way. As a consequence, the time series in our panel can be correlated with each other in various ways. In contrast to and , the error terms are assumed to be independent across . Technical conditions regarding the model are discussed below. Throughout the paper, we restrict attention to the case where the number of time series in model \tagform@2.2 is fixed. Extending our theoretical results to the case where grows with the time series length is a possible topic for further research.

2.3 Assumptions

The error processes satisfy the following conditions.

-

(C1)

The variables allow for the representation , where , the variables are i.i.d. across , and is a measurable function such that is well-defined. It holds that and for some and a sufficiently large constant .

-

(C2)

The processes are independent across .

Assumption (C1) implies that the error processes are stationary and causal (in the sense that does not depend on future innovations with ). The class of error processes that satisfy condition (C1) is very large. It includes linear processes, nonlinear transformations thereof, as well as a large variety of nonlinear processes such as Markov chain models and nonlinear autoregressive models (Wu and Wu, 2016). Following Wu (2005), we impose conditions on the dependence structure of the error processes in terms of the physical dependence measure defined in \tagform@2.1. In particular, we assume the following:

-

(C3)

For each , is finite and with from (C1), where and .

For fixed and , the expression measures the cumulative effect of the innovation on the variables in terms of the -norm. Condition (C3) puts some restrictions on the decay of (as a function of ). It is fulfilled by a wide range of stationary processes . For a detailed discussion of (C1)–(C3) and some examples of error processes that satisfy these conditions, see Khismatullina and Vogt (2020).

The covariates are assumed to have the following properties.

- (C4)

-

(C5)

The matrix is invertible for each .

-

(C6)

For each and , it holds that is finite and for some with from (C4).

Assumption (C4) guarantees that the process is stationary and causal for each . Assumption (C6) restricts the serial dependence of the process for each in terms of the physical dependence measure.

We finally impose some assumptions on the relationship between the covariates and the errors and on the trend functions .

-

(C7)

The random variables and are uncorrelated, that is, .

-

(C8)

The trend functions are Lipschitz continuous on , that is, for all and some constant . Moreover, they are normalised such that for each .

Remark 2.1.

Conditions (C4)–(C6) can be relaxed to cover locally stationary regressors. For example, (C4) may be replaced by

- (C4′)

The other assumptions can be adjusted accordingly. We conjecture that our main theoretical results still hold in this case. However, the complexity of the technical arguments will increase drastically. Hence, for the sake of clarity, we restrict attention to stationary covariates .

3 The multiscale test

In this section, we develop a multiscale test for the comparison of the trend curves in model \tagform@2.2. More specifically, we construct a multiscale test of the null hypothesis

The test is designed to be as informative as possible: It does not only allow to say whether is violated. It also gives information on which types of violation occur. In particular, it allows to infer which trends are different and where (that is, in which time intervals) they differ.

Our strategy to construct the test is as follows: For any given location-scale point , let

be the hypothesis that and are identical on the interval . can be viewed as a local null hypothesis that characterises the behaviour of two trend functions locally on the interval , whereas is the global null hypothesis that is concerned with the comparison of all trends on the whole unit interval . We consider a large family of time intervals that fully cover the unit interval. More formally, we consider all intervals with , where is a set of location-scale points with the property that . Technical conditions on the set are given below. The global null can now be formulated as

This formulation shows that we can test by a procedure which simultaneously tests the local hypothesis for all and all .

In what follows, we design such a simultaneous test procedure step by step. To start with, we introduce some auxiliary estimators in Section 3.1. We then construct the test statistics in Section 3.2 and set up the test procedure in Section 3.3. Finally, Section 3.4 explains how to implement the procedure in practice.

3.1 Preliminary steps

If the fixed effects and the coefficient vectors were known, our testing problem would be greatly simplified. In particular, we could consider the model

which is a standard nonparametric regression equation. As and are not observed in practice, we construct estimators and and replace the unknown variables by the approximations

In what follows, we explain how to construct estimators of and .

In order to estimate the parameter vector for a given , we consider the time series of the first differences and . We can write

where . Since is Lipschitz by Assumption (C8), we can use the fact that to get that

| (3.1) |

This suggests to estimate by applying least squares methods to equation \tagform@3.1, treating as the regressors and as the response variable. As a result, we obtain the least squares estimator

| (3.2) |

In Lemma A.5 in the Appendix, we show that under our assumptions. Given , we next estimate the fixed effect term by

| (3.3) |

This is a reasonable estimator of for the following reason: For each , it holds that

since by the law of large numbers, due to Lipschitz continuity of and the normalisation , by Chebyshev’s inequality and .

In order to construct our multiscale test, we do not only require the variables and thus the estimators and . We also need an estimator of the long-run error variance for each . Throughout the paper, we assume that the long-run variance does not depend on , that is for all . For technical reasons, we nevertheless use a different estimator of for each . Let be an estimator of which is computed from the -th time series , that is, let be a function of the variables for . Our theory works with any estimator which has the property that for each , where slowly converges to zero, in particular, . We now briefly discuss two possible choices of .

Following Kim (2016), we can estimate by a variant of the subseries variance estimator, which was first proposed by Carlstein (1986) and then extended by Wu and Zhao (2007). Formally, we set

| (3.4) |

where is the length of the subseries and is the largest integer not exceeding . As per the optimality result in Carlstein (1986), we set . When implementing , we in particular choose . According to Lemma A.6 in the Appendix, is an asymptotically consistent estimator of with the rate of convergence .

The subseries estimator is completely nonparametric: it does not presuppose a specific time series model for the error process but merely requires to fulfill general weak dependence conditions. In practice, however, it often makes sense to impose additional structure on the error process . A very popular yet general error model is the class of processes. A difference-based estimator of the long-run error variance for this error model has been developed in Khismatullina and Vogt (2020) and can be easily adapted to the situation at hand. A detailed discussion of the estimator and a comparison with other long-run variance estimators can be found in Section 4 of Khismatullina and Vogt (2020).

3.2 Construction of the test statistics

A statistic to test the local null hypothesis for a given location-scale point and a given pair of time series can be constructed as follows: Let

| (3.5) |

be a weighted average of the differenced variables . In particular, let be local linear kernel weights of the form

| (3.6) |

where

for and is a kernel function with the following property:

-

(C9)

The kernel is non-negative, symmetric about zero and integrates to one. Moreover, it has compact support and is Lipschitz continuous, that is, for any and some constant .

The kernel average can be regarded as a measure of distance between the two trend curves and on the interval . We may thus use a normalized (absolute) version of the kernel average , in particular, the term

| (3.7) |

as a statistic to test the local null . Our aim is to test simultaneously for a wide range of location-scale points and all possible pairs of time series . To take into account that we are faced with a simultaneous test problem, we replace the statistics from \tagform@3.7 by additively corrected versions of the form

| (3.8) |

where . The scale-dependent correction term was first introduced in the multiscale approach of Dümbgen and Spokoiny (2001) and has been used in various contexts since then. We refer to Khismatullina and Vogt (2020) for a detailed discussion of the idea behind this additive correction.

In order to test the global null hypothesis , we aggregate the test statistics by taking their maximum over all location-scale points and all pairs of time series with . This leads to the multiscale test statistic

For our theoretical results, we suppose that the set of location-scale points is a subset of with and for some and which fulfills the following conditions:

-

(C10)

for some arbitrarily large but fixed constant , where denotes the cardinality of .

-

(C11)

, that is, with defined in (C1) and .

Assumptions (C10) and (C11) place relatively mild restrictions on the set : (C10) allows to be very large compared to the sample size . In particular, may grow as any polynomial of . (C11) allows to contain intervals of many different scales , ranging from very small intervals of scale to substantially larger intervals of scale .

3.3 The test procedure

Let be the collection of all location-scale points and all pairs of time series under consideration. Moreover, let be the set of tuples for which is true. For a given significance level , our multiscale test is carried out as follows:

-

(i)

For each tuple , we reject the local null hypothesis if

where the critical value is constructed below such that the familywise error rate (FWER) is controlled at level . As usual, the FWER is defined as the probability of wrongly rejecting for at least one tuple . More formally, it is defined as

for a given significance level and we say that the FWER is controlled at level if .

-

(ii)

We reject the global null hypothesis if at least one local null hypothesis is rejected. Put differently, we reject if

We now construct a critical value which controls the FWER at level . Let be the -quantile of the multiscale statistic under the global null . Since

with denoting the probability under , this choice of indeed controls the FWER at the desired level. However, this choice is not computable in practice. We thus replace it by a suitable approximation: Suppose we could perfectly estimate and , that is, and for all . Then under , the test statistics would simplify to

| (3.9) |

where denotes the empirical average of the variables . Replacing the error terms in \tagform@3.9 by normally distributed variables leads to the statistics

| (3.10) |

with

| (3.11) |

where are independent standard normal random variables for and and, as before, we use the shorthand . With this notation, we define

| (3.12) |

which can be regarded as a Gaussian version of the test statistic under the null (in the idealized case with and for all ). We now choose to be the -quantile of .

Remark 3.1.

Importantly, this choice of can be computed by Monte Carlo simulations in practice: under our assumption that the long-run variance does not depend on (i.e. ), we can rewrite the statistics from \tagform@3.10 as

This shows that the distribution of these statistics and thus the distribution of the multiscale statistic only depend on the Gaussian variables for and . Consequently, we can approximate the distribution of – and in particular its quantiles – by simulating values of the Gaussian random variables . In Section 3.4, we explain in detail how to compute Monte Carlo approximations of the quantiles .

3.4 Implementation of the test in practice

In practice, we implement the test procedure as follows for a given significance level :

-

Step 1.

Compute the -quantile of the Gaussian statistic by Monte Carlo simulations. Specifically, draw a large number (say ) of samples of independent standard normal random variables for . For each sample , compute the value of the Gaussian statistic , and store these values. Calculate the empirical -quantile from the stored values . Use as an approximation of the quantile .

-

Step 2.

For each with and each , reject the local null hypothesis if . Reject the global null hypothesis if at least one local hypothesis is rejected.

-

Step 3.

Display the test results as follows. For each pair of time series , let be the set of intervals for which we reject . Produce a separate plot for each pair ( which displays the intervals in . This gives a graphical overview over the intervals where our tests finds a deviation from the null.

Remark 3.2.

In some cases, the number of intervals in may be quite large, rendering the visual representation of the test results outlined in Step 3 cumbersome. To overcome this drawback, we replace with the subset of minimal intervals . As in Dümbgen (2002), we call an interval minimal if there is no other interval such that . Notably, our theoretical results remain to hold true when the sets are replaced by . See Section 4 for the details.

4 Theoretical properties of the multiscale test

To start with, we investigate the auxiliary statistic

| (4.1) |

where

and

with and . By construction, it holds that under . Hence, the auxiliary statistic is identical to the multiscale test statistic under the global null . Consequently, in order to determine the distribution of the test statistic under , it suffices to study the auxiliary statistic . The following theorem shows that the distribution of is close to the distribution of the Gaussian statistic introduced in \tagform@3.12.

Theorem 4.1 is key for deriving theoretical properties of our multiscale test. Its proof is provided in the Appendix.

Remark 4.2.

The proof of Theorem 4.1 builds on two important theoretical results: strong approximation theory for dependent processes (Berkes et al., 2014) and anti-concentration bounds for Gaussian random vectors (Nazarov, 2003). It can be regarded as a further development of the proof strategy in Khismatullina and Vogt (2020) who developed multiscale methods to test for local increases/decreases of the nonparametric trend function in the univariate time series model . We extend their theoretical results in several directions: we consider the case of multiple time series and work with a more general model which includes covariates and a flexible fixed effect error structure.

With the help of Theorem 4.1, we now examine the theoretical properties of our multiscale test developed in Section 3. The following proposition shows that our test of the global null has correct (asymptotic) size.

Proposition 4.3.

Suppose that the conditions of Theorem 4.1 are satisfied. Then under , we have

The next proposition characterises the power of the test against a certain class of local alternatives. To formulate it, we consider a sequence of pairs of functions and that depend on the time series length and that are locally sufficiently far from each other.

Proposition 4.4.

Let the conditions of Theorem 4.1 be satisfied. Moreover, assume that for some pair of indices and , the functions and have the following property: There exists with such that for all or for all , where is any sequence of positive numbers with . Then

We now turn attention to the local null hypotheses . As already defined above, let be the collection of location-scale points and pairs of time series under consideration. Moreover, let be the set of tuples for which is true. Since we test simultaneously for all , we would like to bound the probability of making at least one false discovery. More formally, we would like to control the family-wise error rate

at level , where is the set of intervals for which the null hypothesis is rejected. The following result shows that our test procedure asymptotically controls the FWER at level .

Proposition 4.5.

Let the conditions of Theorem 4.1 be satisfied. Then for any given ,

The statement of Proposition 4.5 can obviously be reformulated as follows:

Consequently, we can make the following simultaneous confidence statement:

| With (asymptotic) probability at least , the trends and differ on any interval and for all pairs for which is rejected. | (4.2) |

Put differently:

| With (asymptotic) probability at least , for any pair with , the two trends and differ on all intervals . | (4.3) |

Remark 4.6.

According to \tagform@4.3, the graphical device introduced in Section 3.4 which depicts the intervals in comes with the following statistical guarantee: we can claim with (asymptotic) confidence at least that the trends and differ on all the depicted intervals. As for all and , this guarantee remains to hold true when the sets are replaced by the sets of minimal intervals .

5 Clustering

Consider a situation in which the null hypothesis is violated. Even though some of the trend functions are different in this case, part of them may still be the same. Put differently, there may be groups of time series which have the same time trend. Formally speaking, we define a group structure as follows: There exist sets or groups of time series with and such that for each ,

where are group-specific trend functions. Hence, the time series which belong to the group all have the same time trend . Throughout the section, we suppose that the group-specific trend functions have the following properties:

-

(C12)

For each , is a Lipschitz continuous function with . In particular, for all and some constant that does not depend on . Moreover, for any , the trends and differ in the following sense: There exists with such that for all or for all , where .

In many applications, it is natural to suppose that there is a group structure in the data. In this case, a particular interest lies in estimating the unknown groups from the data at hand. In what follows, we combine our multiscale methods with a clustering algorithm to achieve this. More specifically, we use the multiscale statistics calculated for each and as distance measures which are fed into a hierarchical clustering algorithm.

To describe the algorithm, we first need to introduce the notion of a dissimilarity measure: Let and be two sets of time series from our sample. We define a dissimilarity measure between and by setting

| (5.1) |

This is commonly called a complete linkage measure of dissimilarity. Alternatively, we may work with an average or a single linkage measure. We now combine the dissimilarity measure with a hierarchical agglomerative clustering (HAC) algorithm which proceeds as follows:

Step (Initialisation): Let denote the -th singleton cluster for and define to be the initial partition of time series into clusters.

Step (Iteration): Let be the clusters from the previous step. Determine the pair of clusters and for which

and merge them into a new cluster.

Iterating this procedure for yields a tree of nested partitions , which can be graphically represented by a dendrogram. Roughly speaking, the HAC algorithm merges the singleton clusters step by step until we end up with the cluster . In each step of the algorithm, the closest two clusters are merged, where the distance between clusters is measured in terms of the dissimilarity . We refer the reader to Section 14.3.12 in Hastie et al. (2009) for an overview of hierarchical clustering methods.

When the number of groups is known, we estimate the group structure by the -partition produced by the HAC algorithm. When is unknown, we estimate it by the -partition , where is an estimator of . The latter is defined as

where we write for short and is the -quantile of defined in Section 3.3.

The following proposition summarises the theoretical properties of the estimators and , where we use the shorthand for .

This result allows us to make statistical confidence statements about the estimated clusters and their number . In particular, we can claim with asymptotic confidence at least that the estimated group structure is identical to the true group structure. The proof of Proposition 5.1 can be found in the Appendix.

Our multiscale methods do not only allow us to compute estimators of the unknown groups and their number . They also provide information on the locations where two group-specific trend functions and differ from each other. To turn this claim into a mathematically precise statement, we need to introduce some notation. First of all, note that the indexing of the estimators is completely arbitrary. We could, for example, change the indexing according to the rule . In what follows, we suppose that the estimated groups are indexed such that . Proposition 5.1 implies that this is possible without loss of generality. Keeping this convention in mind, we define the sets

and

for . An interval is contained in if our multiscale test indicates a significant difference between the trends and on the interval for some and . Put differently, if the test suggests a significant difference between the trends of the -th and the -th group on the interval . We further let

be the event that the group-specific time trends and differ on all intervals . With this notation at hand, we can make the following formal statement whose proof is given in the Appendix.

Proposition 5.2.

Under the conditions of Proposition 5.1, the event

asymptotically occurs with probability at least , that is,

According to Proposition 5.2, the sets allow us to locate, with a pre-specified confidence, time intervals where the group-specific trend functions and differ from each other. In particular, we can claim with asymptotic confidence at least that the trend functions and differ on all intervals .333This statement remains to hold true when the sets of intervals are replaced by the corresponding sets of minimal intervals.

6 Simulations

In this section, we investigate our testing and clustering methods by means of a simulation study. The simulation design is as follows: We generate data from the model , where the number of time series is set to and we consider different time series lengths . For simplicity, we assume that the fixed effect term is equal to in all time series and we only include a single regressor in the model, setting the unknown parameter to for all . For each , the errors follow the AR(1) model , where and the innovations are i.i.d. normally distributed with mean and variance . Similarly, for each , the covariates follow an AR() process of the form , where and the innovations are i.i.d. normally distributed with mean and variance . We assume that the covariates and the error terms are independent from each other for all and . To generate data under the null , we let for all without loss of generality. To produce data under the alternative, we define with and set for all . Hence, all trend functions are the same except for which is an increasing linear function. Note that the normalisation constraint is directly satisfied in this case. For each simulation exercise, we simulate data samples.

| nominal size | |||

|---|---|---|---|

| 0.01 | 0.05 | 0.1 | |

| 100 | 0.009 | 0.045 | 0.087 |

| 250 | 0.013 | 0.063 | 0.117 |

| 500 | 0.013 | 0.057 | 0.112 |

| nominal size | |||

|---|---|---|---|

| 0.01 | 0.05 | 0.1 | |

| 100 | 0.033 | 0.122 | 0.199 |

| 250 | 0.209 | 0.434 | 0.549 |

| 500 | 0.741 | 0.891 | 0.947 |

| nominal size | |||

|---|---|---|---|

| 0.01 | 0.05 | 0.1 | |

| 100 | 0.105 | 0.270 | 0.376 |

| 250 | 0.635 | 0.840 | 0.901 |

| 500 | 0.994 | 0.999 | 0.999 |

| nominal size | |||

|---|---|---|---|

| 0.01 | 0.05 | 0.1 | |

| 100 | 0.275 | 0.512 | 0.628 |

| 250 | 0.933 | 0.986 | 0.993 |

| 500 | 1.000 | 1.000 | 1.000 |

Our multiscale test is implemented as follows: The estimators and of the unknown parameters and are computed as described in Section 3.1. Since the errors follow an AR() process, we estimate the long-run error variance by the difference-based estimator proposed in Khismatullina and Vogt (2020), setting the tuning parameters and to and , respectively. In order to construct our test statistics, we use an Epanechnikov kernel and the grid with

We thus consider intervals which contain data points. The critical value of our test is computed by Monte Carlo methods as described in Section 3.4, where we set .

The simulation results for our multiscale test can be found in Table 2, which reports its actual size under , and in Table 2, which reports its power against different alternatives. Both the actual size and the power are computed as the number of simulations in which the test rejects the global null divided by the total number of simulations. Inspecting Table 2, one can see that the actual size is fairly close to the nominal target in all the considered scenarios. Hence, the test has approximately the correct size. Inspecting Table 2, one can further see that the test has reasonable power properties. For the smallest slope and the smallest time series length , the power is only moderate, reflecting the fact that the alternative with is not very far away from the null. However, as we increase the slope and the sample size , the power increases quickly. Already for the slope value , we reach a power of for and for all nominal sizes .

We next investigate the finite sample performance of the clustering algorithm from Section 5. To do so, we consider a very simple scenario: we generate data from the model , that is, we assume that there are no fixed effects and no covariates. The error terms are specified as above. Moreover, as before, we set the number of time series to and we consider different time series lengths . We partition the time series into groups, each containing time series. Specifically, we set , and , and we assume that for all and all . The group-specific trend functions , and are defined as , and . In order to estimate the groups , , and their number , we use the same implementation as before followed by the clustering procedure from Section 5.

| nominal size | |||

|---|---|---|---|

| 0.01 | 0.05 | 0.1 | |

| 100 | 0.055 | 0.188 | 0.298 |

| 250 | 0.713 | 0.922 | 0.939 |

| 500 | 0.994 | 0.979 | 0.956 |

| nominal size | |||

|---|---|---|---|

| 0.01 | 0.05 | 0.1 | |

| 100 | 0.009 | 0.045 | 0.077 |

| 250 | 0.640 | 0.825 | 0.845 |

| 500 | 0.992 | 0.978 | 0.956 |

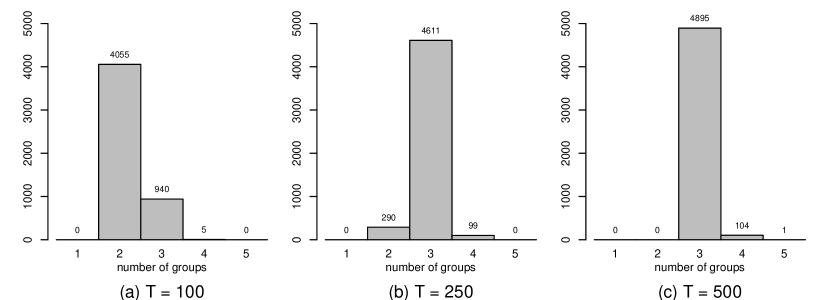

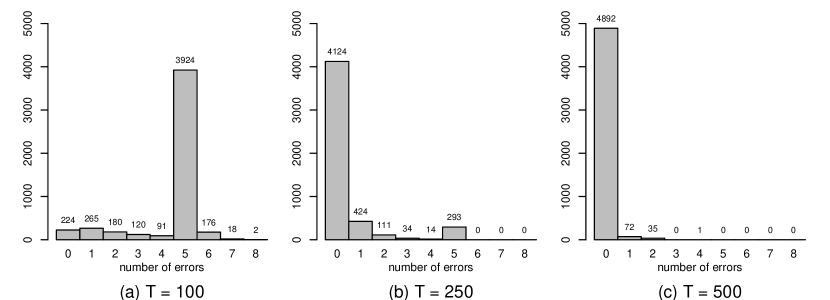

The simulation results are reported in Table 2. The entries in Table 2(a) are computed as the number of simulations for which divided by the total number of simulations. They thus specify the empirical probabilities with which the estimate is equal to the true number of groups . Analogously, the entries of Table 2(b) give the empirical probabilities with which the estimated group structure equals the true one . The results in Table 2 nicely illustrate the theoretical properties of our clustering algorithm. According to Proposition 5.1, the probability that and should be at least asymptotically. For the largest sample size , the empirical probabilities reported in Table 2 can indeed be seen to exceed the value as predicted by Proposition 5.1. For the smaller sample sizes and , in contrast, the empirical probabilities are substantially smaller than . This reflects the asymptotic nature of Proposition 5.1 and is not very surprising. It simply mirrors the fact that for the smaller sample sizes and , the effective noise level in the simulated data is quite high.

Figures 2 and 2 give more insight into what happens for and . Figure 2 shows histograms of the simulated values of , while Figure 2 depicts histograms of the number of classification errors produced by our algorithm. By the number of classification errors, we simply mean the number of incorrectly classified time series, which is formally calculated as

with being the set of all permutations of . The histogram of Figure 2 for clearly shows that our method underestimates the number of groups ( in cases out of ). In particular, it fails to detect the difference between two out of three groups in a large number of simulations. This is reflected in the corresponding histogram of Figure 2 which shows that there are exactly classification errors in of the simulation runs. In most of these cases, the estimated group structure coincides with either , or . In summary, we can conclude that the small empirical probabilities for in Table 2 are due to the algorithm underestimating the number of groups. Inspecting the histograms for , one can see that the performance of the estimators and improves significantly, even though the corresponding empirical probabilities in Table 2 are still somewhat below the target .

7 Applications

7.1 Analysis of GDP growth

In what follows, we revisit an application example from Zhang et al. (2012). The aim is to test the hypothesis of a common trend in the GDP growth time series of several OECD countries. Since we do not have access to the original dataset of Zhang et al. (2012) and we do not know the exact data specifications used there, we work with data from the following common sources: Refinitiv Datastream, the OECD.Stat database, Federal Reserve Economics Data (FRED) and the Barro-Lee Educational Attainment dataset (Barro and Lee, 2013). We consider a data specification that is as close as possible to the one in Zhang et al. (2012) with one important distinction: In the original study, the authors examined OECD countries (not specifying which ones) over the time period from the fourth quarter of 1975 up to and including the third quarter of 2010, whereas we consider only countries (Australia, Austria, Canada, Finland, France, Germany, Japan, Norway, Switzerland, UK and USA) over the same time span. The reason is that we have access to data of good quality only for these 11 countries. In the following list, we specify the data for our analysis.444All data were accessed and downloaded on 7 December 2021.

-

•

Gross domestic product (): We use freely available data on Gross Domestic Product – Expenditure Approach from the OECD.Stat database (https://stats.oecd.org/Index.aspx). To be as close as possible to the specification of the data in Zhang et al. (2012), we use seasonally adjusted quarterly data on GDP expressed in millions of 2015 US dollars.555Since the publication of Zhang et al. (2012), the OECD reference year has changed from 2005 to 2015. We have decided to analyse the latest version of the data in order to be able to make more accurate and up-to-date conclusions.

-

•

Capital (): We use data on Gross Fixed Capital Formation from the OECD.Stat database. The data are at a quarterly frequency, seasonally adjusted, and expressed in millions of US dollars. In contrast to Zhang et al. (2012), who use data on Capital Stock at Constant National Prices, we choose to work with gross fixed capital formation due to data availability. It is worth noting that since accurate data on capital stock is notoriously difficult to collect, the use of gross fixed capital formation as a measure of capital is standard in the literature; see e.g. Sharma and Dhakal (1994), Lee and Huang (2002) and Lee (2005).

-

•

Labour (): We collect data on the Number of Employed People from various sources. For most of the countries (Austria, Australia, Canada, Germany, Japan, UK and USA), we download the OECD data on Employed Population: Aged 15 and Over retrieved from FRED (https://fred.stlouisfed.org/). The data for France and Switzerland were downloaded from Refinitiv Datastream. For all of the aforementioned countries, the observations are at a quarterly frequency and seasonally adjusted. The data for Finland and Norway were also obtained via Refinitiv Datastream, however, the only quarterly time series that are long enough for our purposes are not seasonally adjusted. Hence, for these two countries, we perform the seasonal adjustment ourselves. We in particular use the default method of the function

seasfrom theRpackageseasonal(Sax and Eddelbuettel, 2018) which is an interface to X-13-ARIMA-SEATS, the seasonal adjustment software used by the US Census Bureau. For all of the countries, the data are given in thousands of persons. -

•

Human capital (): We use Educational Attainment for Population Aged 25 and Over collected from http://www.barrolee.com as a measure of human capital. Since the only available data is five-year census data, we follow Zhang et al. (2012) and use linear interpolation between the observations and constant extrapolation on the boundaries (second and third quarters of 2010) to obtain the quarterly time series.

For each of the countries in our sample, we thus observe a quarterly time series of length , where and with , and . Without loss of generality, we let . Each time series is assumed to follow the model , or equivalently,

| (7.1) |

for , where is a vector of unknown parameters, is a country-specific unknown nonparametric time trend and is a country-specific fixed effect.

In order to test the null hypothesis with in model \tagform@7.1, we implement our multiscale test as follows:

-

•

We choose to be the Epanechnikov kernel and consider the set of location-scale points , where

We thus take into account all locations on an equidistant grid with step length and all scales with . The choice of the grid is motivated by the quarterly frequency of the data: each interval spans quarters, i.e., years. The lower bound on the scales in is motivated by Assumption (C11), which requires that (given that all moments of exist).

-

•

To obtain an estimator of the long-run error variance for each , we assume that the error process follows an AR() model and apply the difference-based procedure of Khismatullina and Vogt (2020) to the augmented time series with . We set the tuning parameters and of the procedure to and , respectively, and choose the AR order by minimizing the Bayesian Information Criterion (BIC), which yields for Australia, Canada and the UK and for all other countries.666We also calculated the values of other information criteria such as FPE, AIC and HQ which, in most of the cases, resulted in the same values of .

-

•

The critical values are computed by Monte Carlo methods as described in Section 3.4, where we set .

Besides these choices, we construct and implement the multiscale test exactly as described in Section 3.

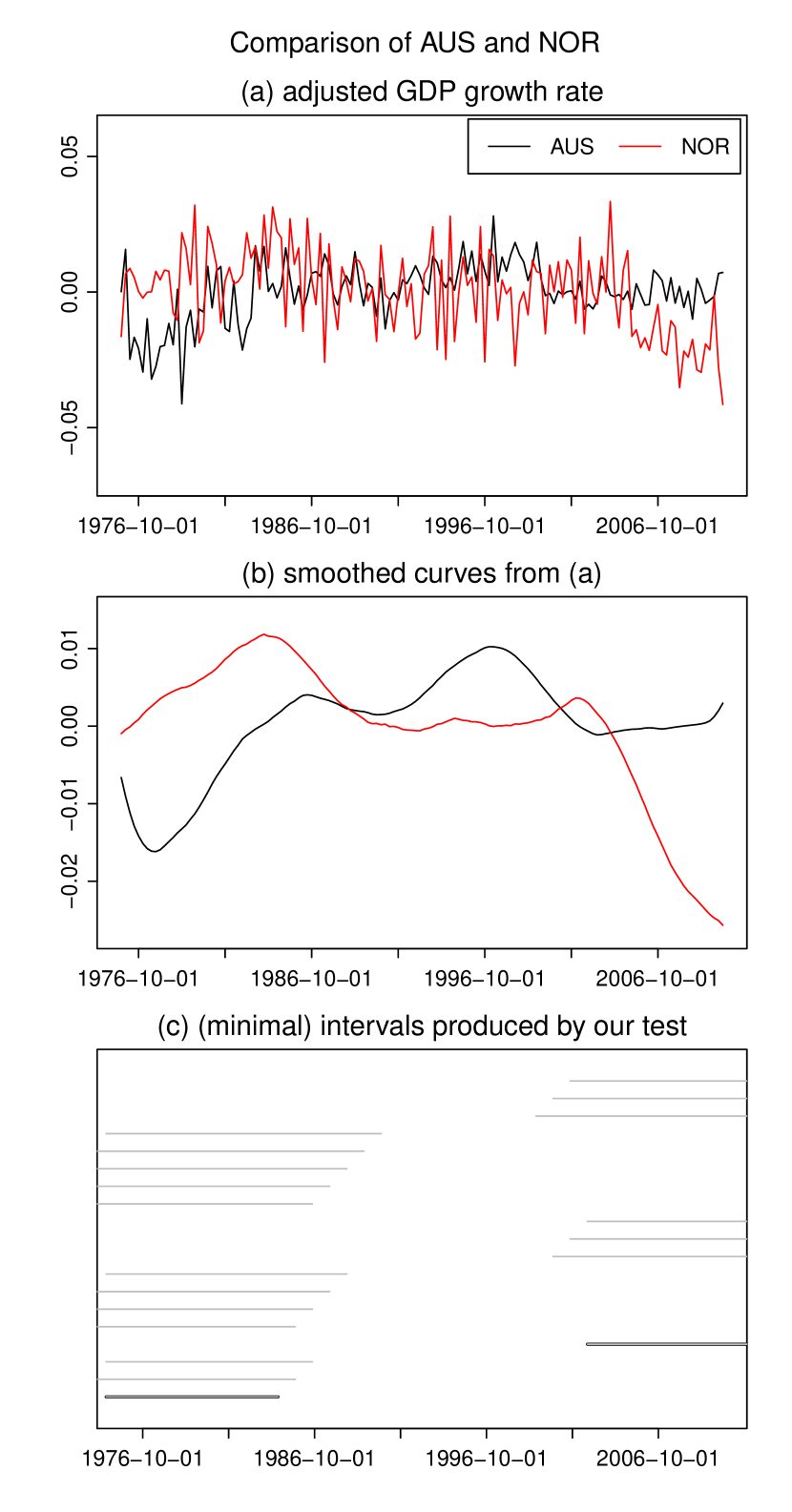

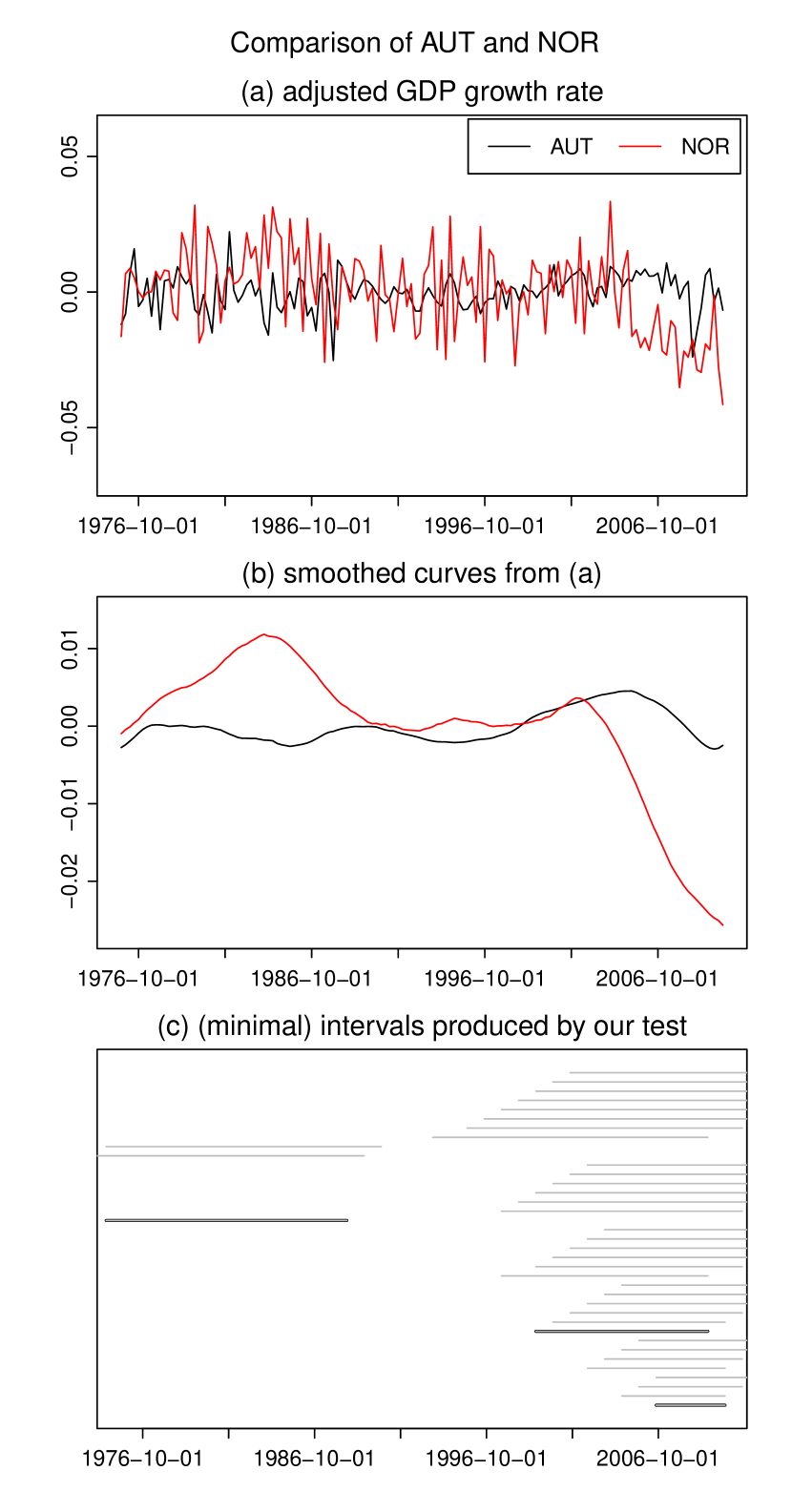

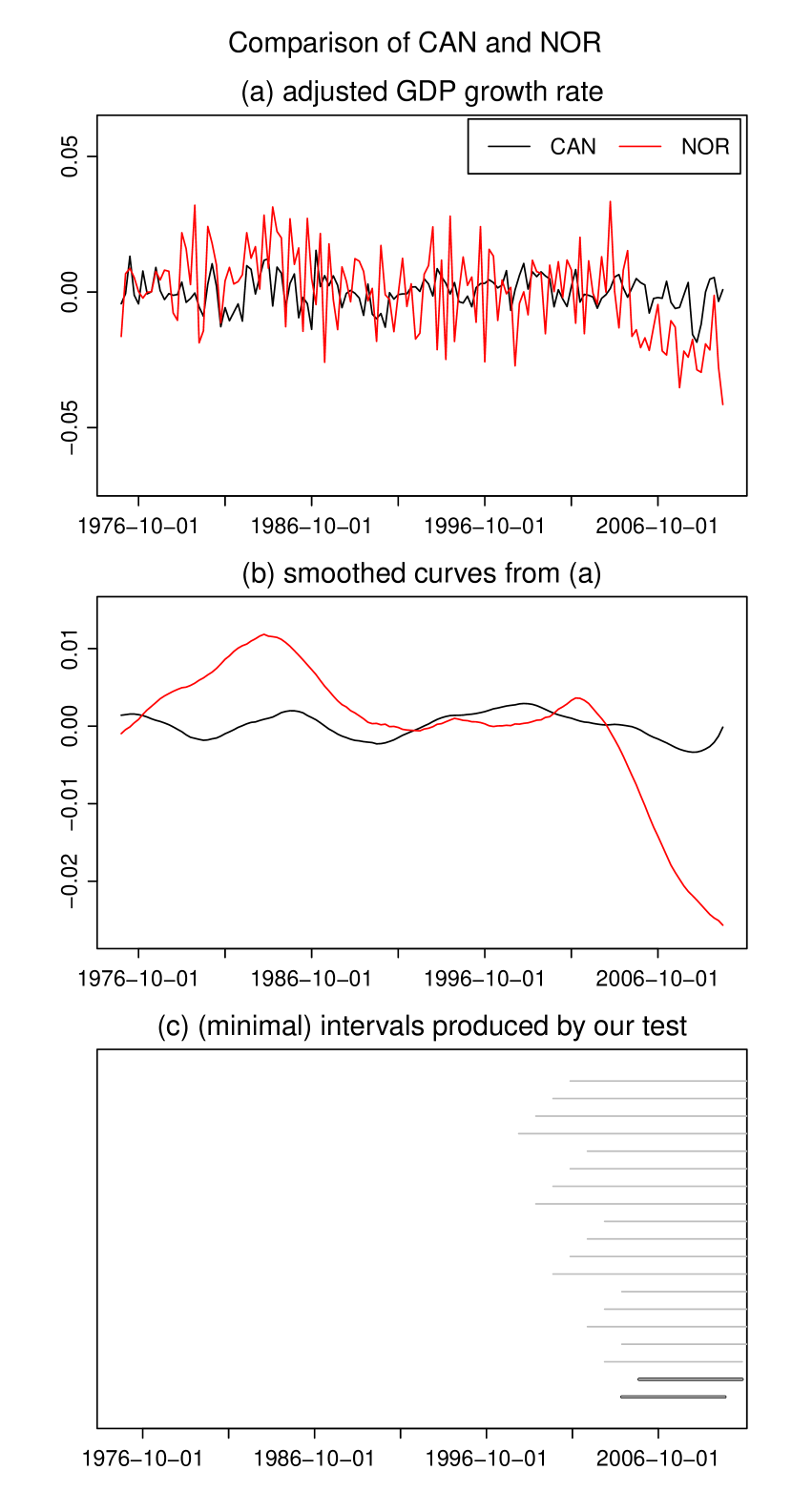

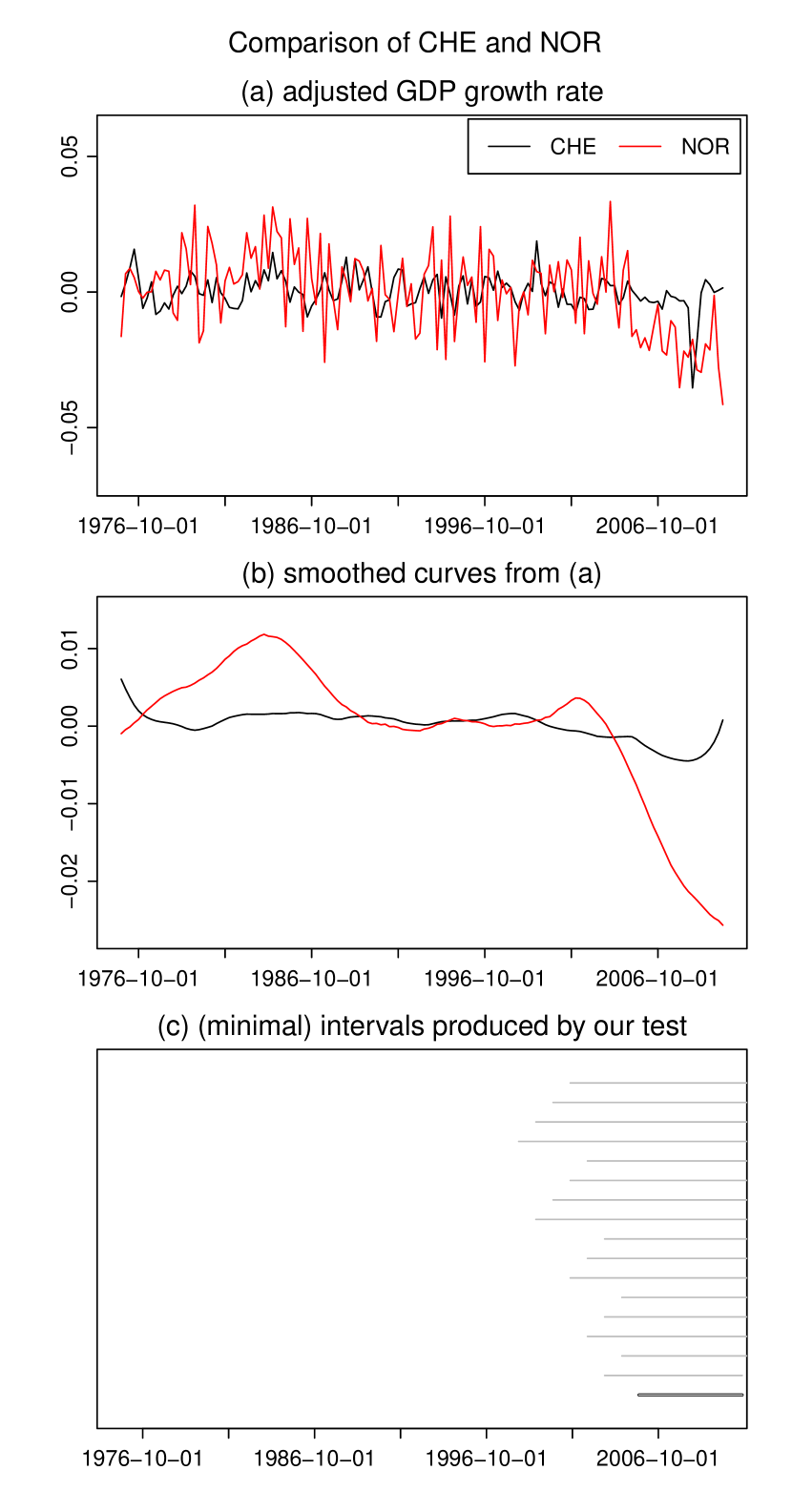

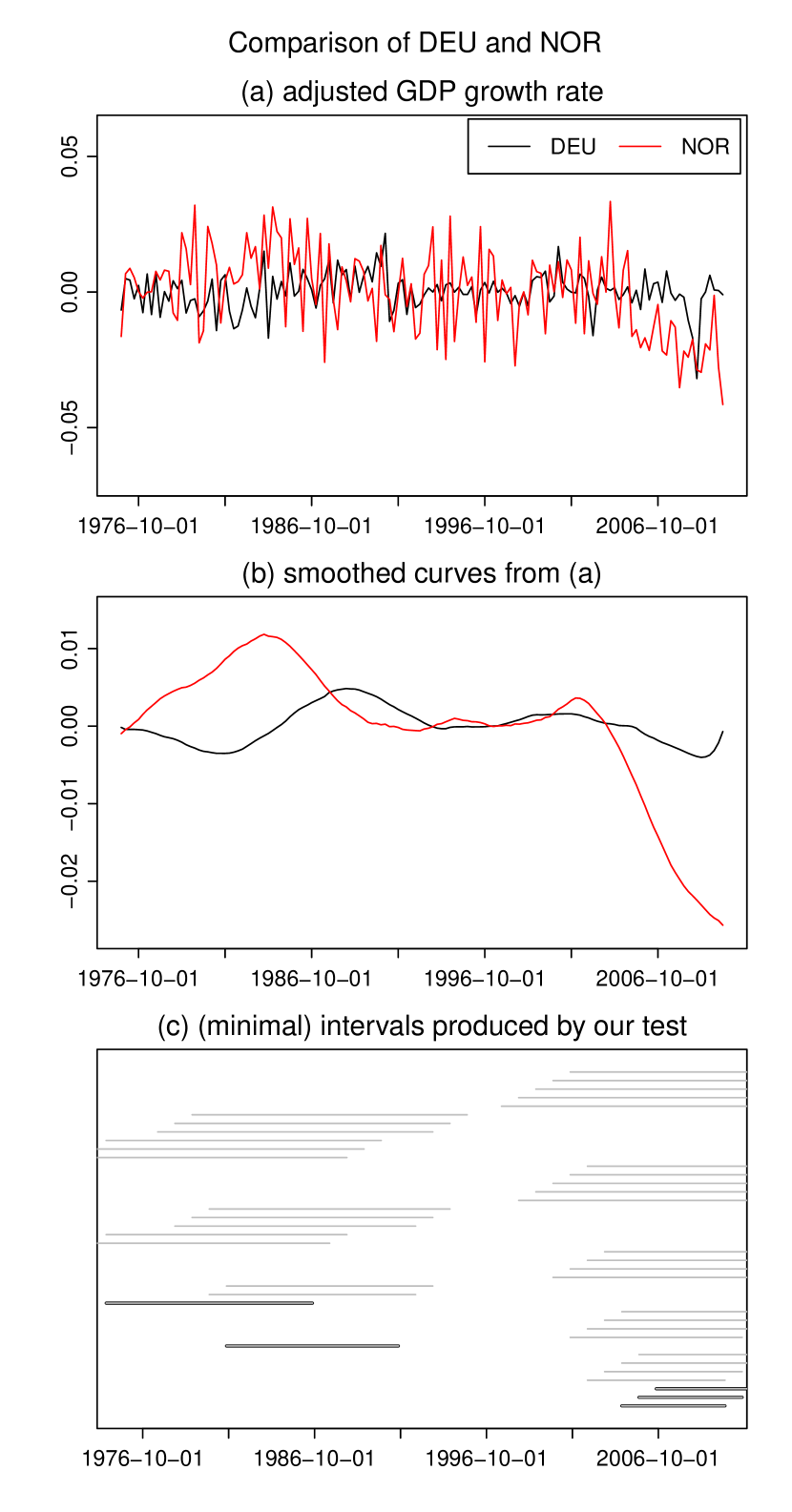

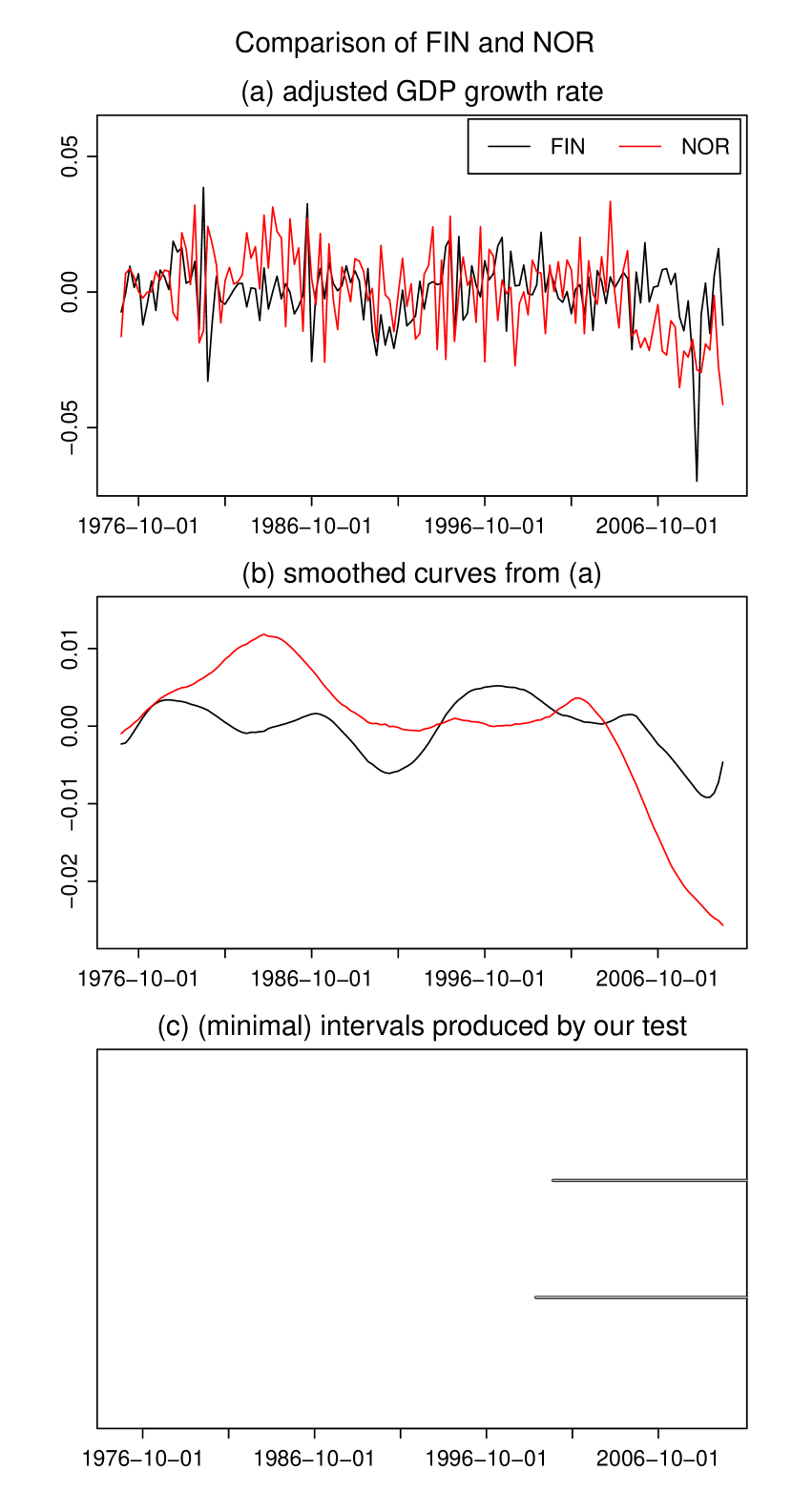

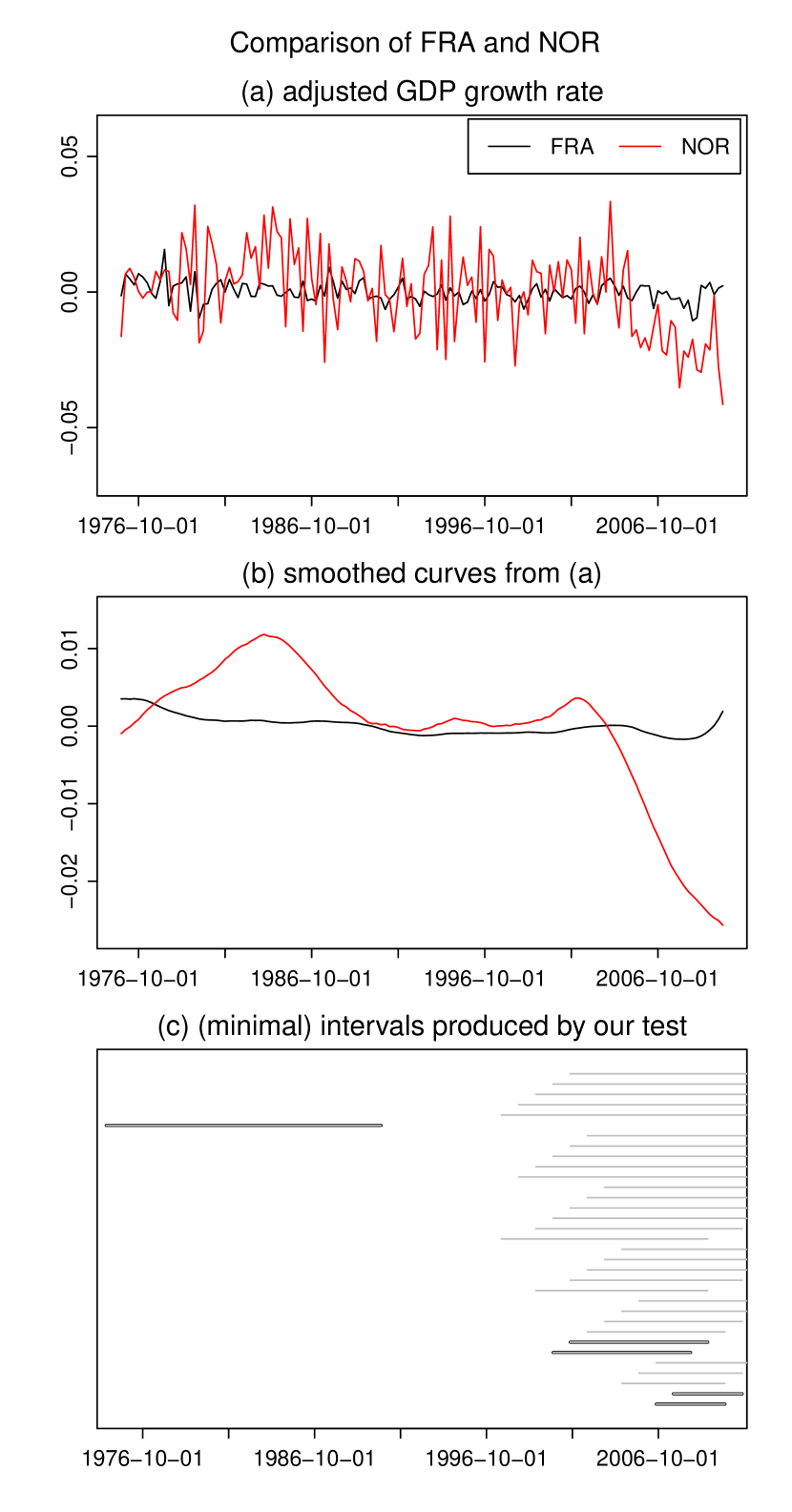

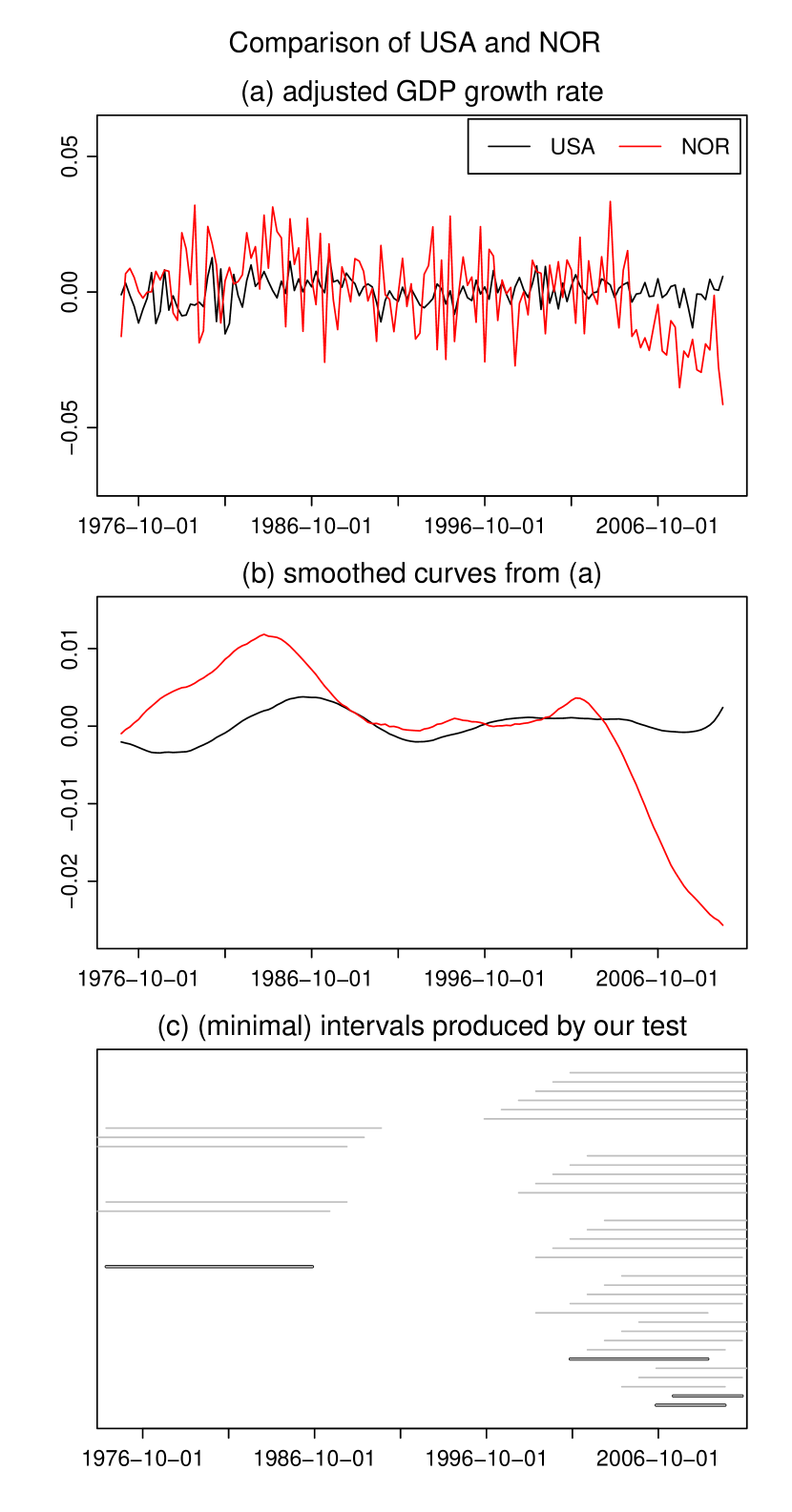

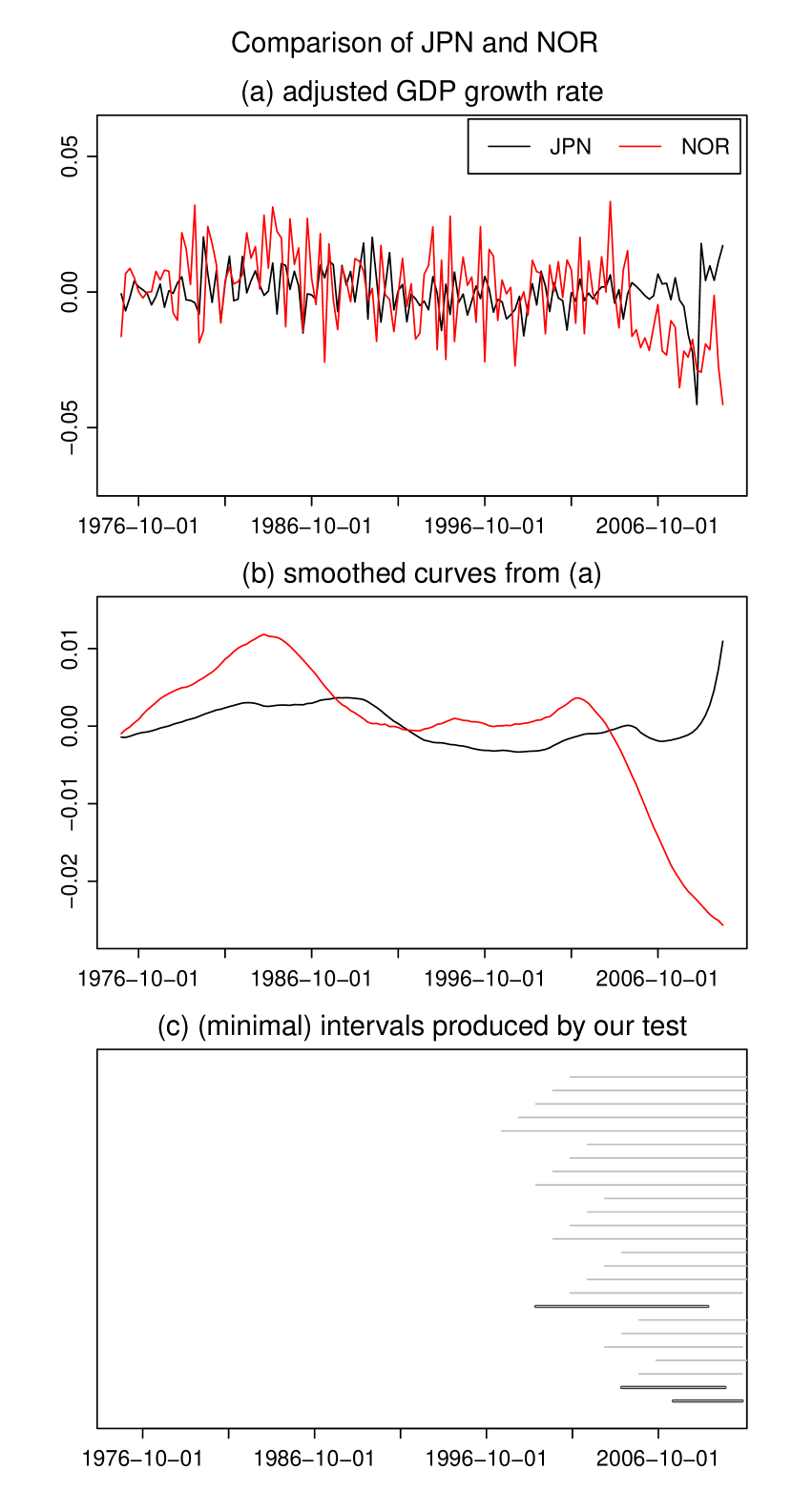

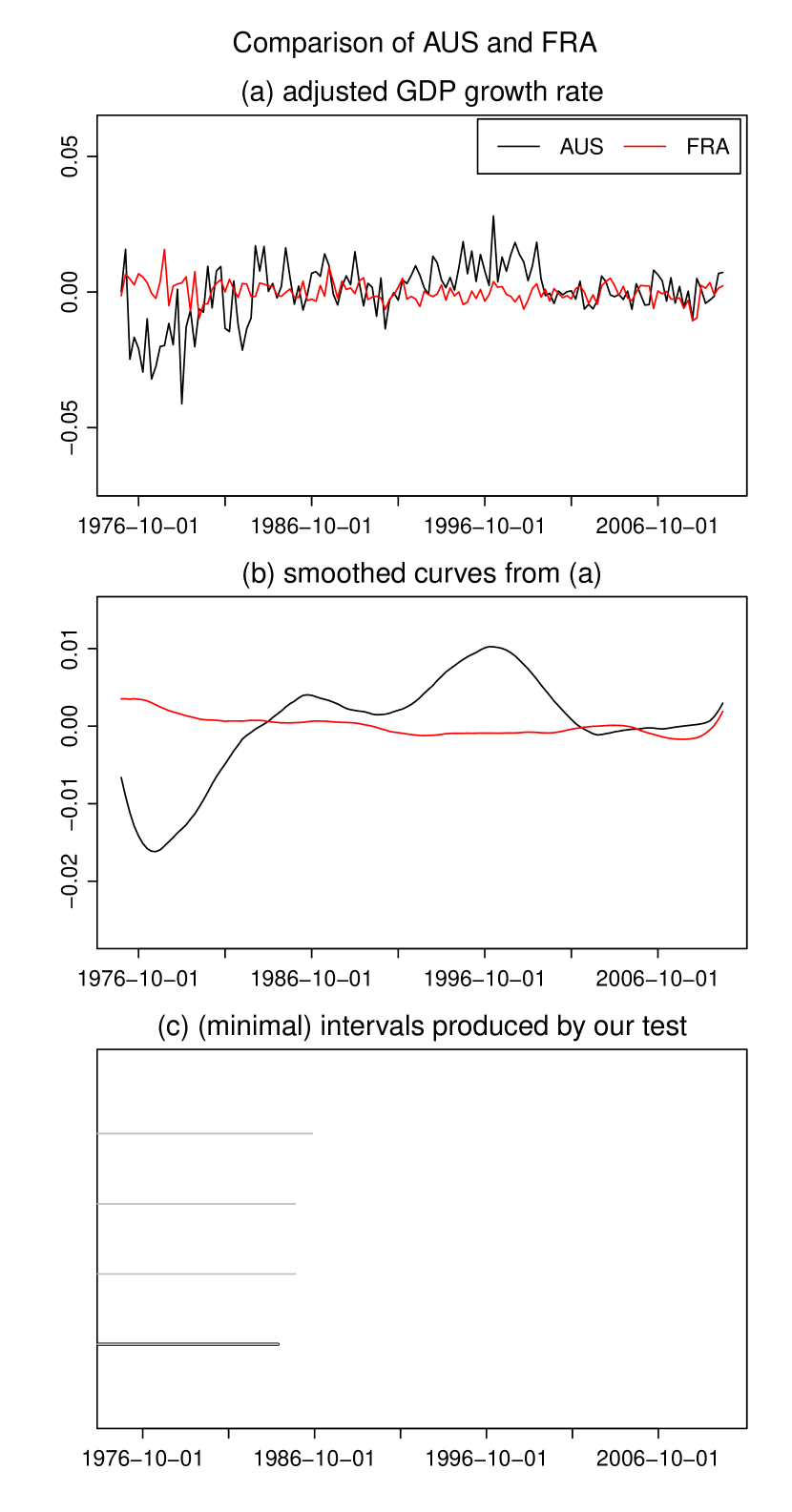

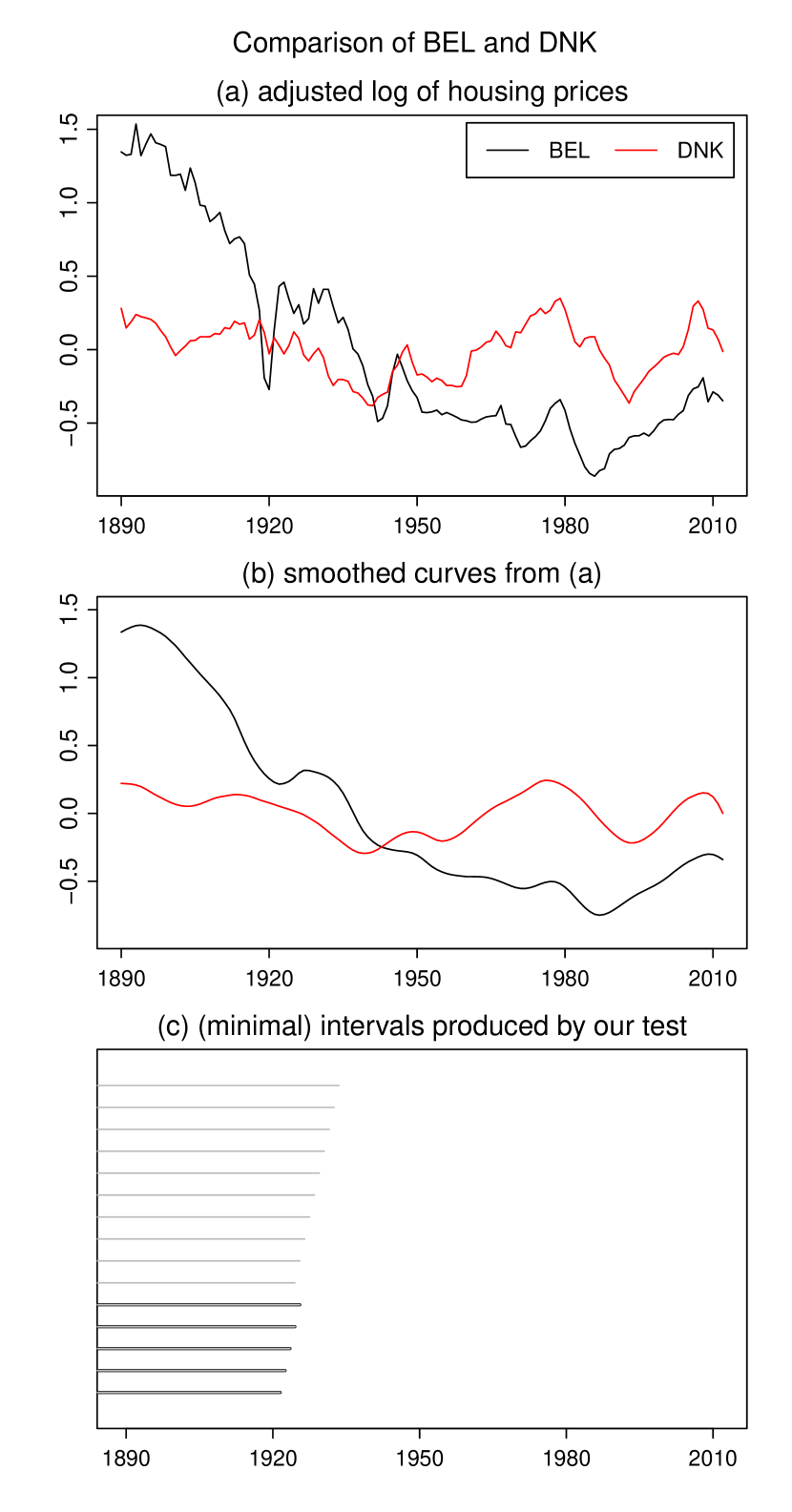

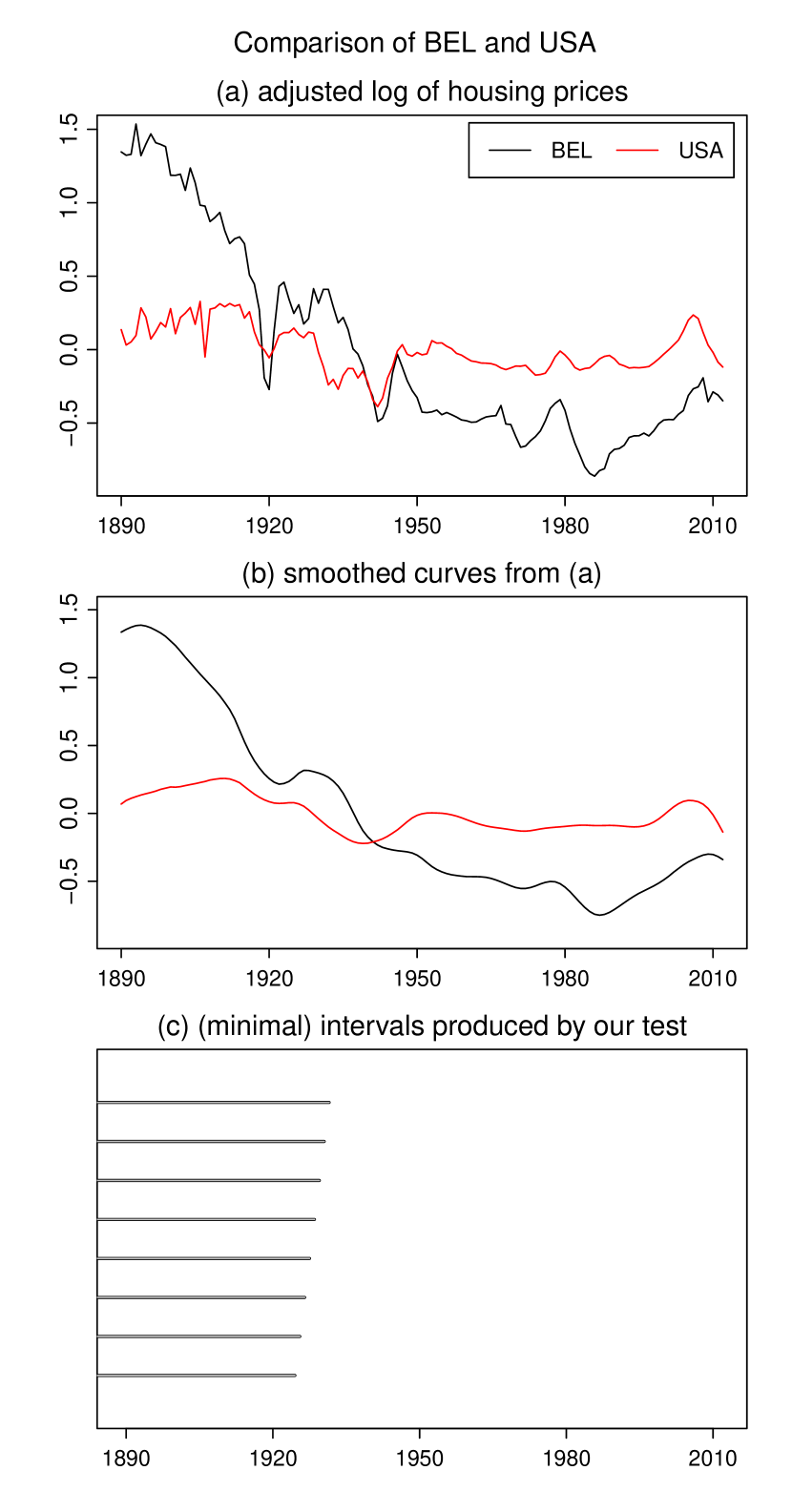

The thus implemented multiscale test rejects the global null hypothesis at the usual significance levels . This result is in line with the findings in Zhang et al. (2012) where the null hypothesis of a common trend is rejected at level . The main advantage of our multiscale test over the method in Zhang et al. (2012) is that it is much more informative. In particular, it provides information about which of the countries have different trends and where the trends differ. This information is presented graphically in Figures 6–13. Each figure corresponds to a specific pair of countries and is divided into three panels (a)–(c). Panel (a) shows the augmented time series and for the two countries and that are compared. Panel (b) presents smoothed versions of the time series from (a), in particular, it shows local linear kernel estimates of the two trend functions and , where the bandwidth is set to quarters (that is, to in terms of rescaled time) and an Epanechnikov kernel is used. Panel (c) presents the results produced by our test for the significance level : it depicts in grey the set of all the intervals for which the test rejects the local null . The set of minimal intervals is highlighted in black. According to \tagform@4.3, we can make the following simultaneous confidence statement about the intervals plotted in panels (c) of Figures 6–13: we can claim, with confidence of about , that there is a difference between the functions and on each of these intervals.

Out of pairwise comparisons, our test detects differences for pairs of countries . These cases are presented in Figures 6–13. In cases (Figures 6–13), one of the involved countries is Norway. Inspecting the trend estimates in panels (b) of Figures 6–13, the Norwegian trend estimate can be seen to exhibit a strong downward movement at the end of the observation period, whereas the other trend estimates show a much less pronounced downward movement (or even a slight upward movement). According to our test, this is a significant difference between the Norwegian and the other trend functions rather than an artefact of the sampling noise: In all cases, the test rejects the local null for at least one interval which covers the last years of the analysed time period (from the first quarter in up to the third quarter in ). Apart from these differences at the end of the sampling period, our test also finds differences in the beginning, however, only for part of the pairwise comparisons.

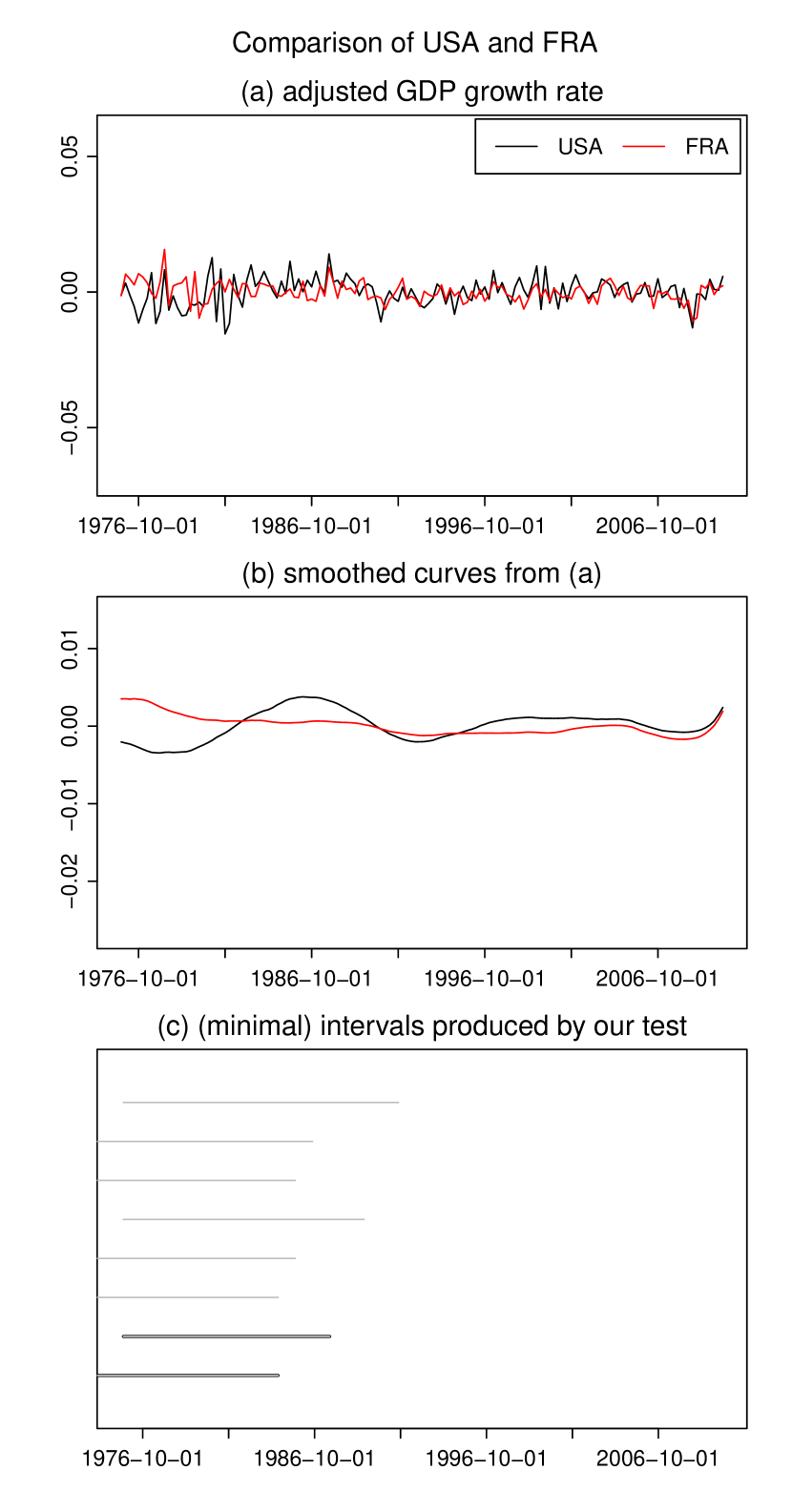

Figures 13 and 13 present the results of the pairwise comparison between Australia and France and between the USA and France, respectively. In both cases, our test detects differences between the GDP trends only in the beginning of the considered time period. In the case of Australia and France, it is clearly visible in the raw data (panel (a) in Figure 13) that there is a difference between the trends, whereas this is not so obvious in the case of the USA and France. According to our test, there are indeed significant differences in both cases. In particular, we can claim with confidence at least 95%, that there are differences between the trends of the USA and France (of Australia and France) up to the fourth quarter in 1991 (the fourth quarter in 1986), but there is no evidence of any differences between the trends from 1992 (1987) onwards.

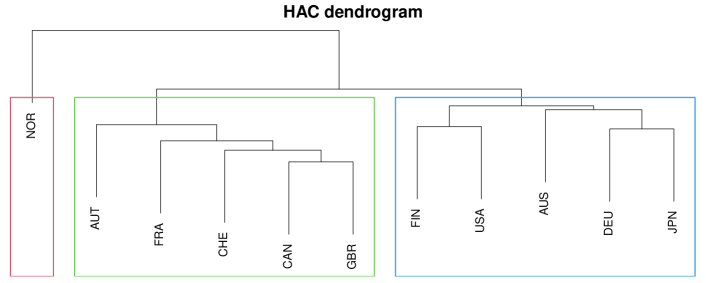

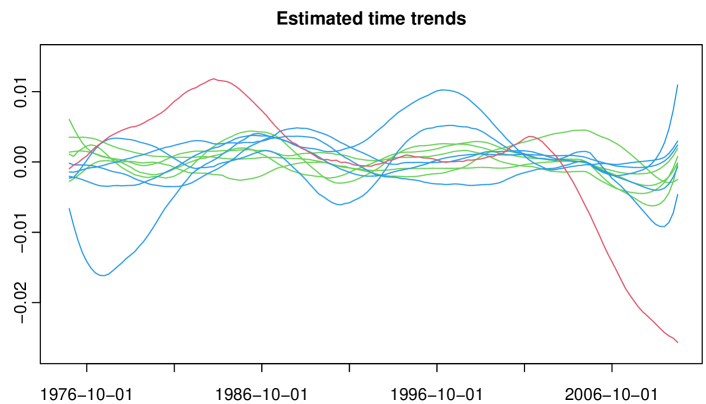

We next apply our clustering techniques to find groups of countries that have the same time trend. We implement our HAC algorithm with and the same choices as detailed above. The dendrogram that depicts the clustering results is plotted in Figure 15. The number of clusters is estimated to be . The rectangles in Figure 15 indicate the clusters. In particular, each rectangle is drawn around the branches of the dendrogram that correspond to one of the three clusters. Figure 15 depicts local linear kernel estimates of the GDP time trends (calculated from the augmented time series with bandwidth and Epanechnikov kernel). Their colour indicates which cluster they belong to.

The results in Figures 15 and 15 show that there is one cluster which consists only of Norway (plotted in red). As we have already discussed above and as becomes apparent from Figure 15, the Norwegian trend exhibits a strong downward movement at the end of the sampling period, whereas the other trends show a much more moderate downward movement (if at all). This is presumably the reason why the clustering procedure puts Norway in a separate cluster. The algorithm further finds two other clusters, one consisting of the 5 countries Australia, Finland, Germany, Japan and the USA (plotted in blue in Figures 15 and 15) and the other one consisting of the 5 countries Austria, Canada, France, Switzerland and the UK (plotted in green in Figures 15 and 15). Visual inspection of the trend estimates in Figure 15 suggests that the GDP time trends in the blue cluster exhibit more pronounced decreases and increases than the GDP time trends in the green cluster. Hence, overall, the clustering procedure appears to produce a reasonable grouping of the GDP trends.

7.2 Analysis of house prices

We next analyse a historical dataset on nominal annual house prices from Knoll et al. (2017) that contains data for advanced economies covering years from to . In our analysis, we consider 8 countries (Australia, Belgium, Denmark, France, Netherlands, Norway, Sweden and USA) over the time period 1890–2012. The data for all these countries except one (Belgium) contain no missing values, and for Belgium there are only five missing observations777The missing values in the Belgium time series span five years during World War I. which we impute by linear interpolation. The time series of the other countries contain more than missing values each, which is why we exclude them from our analysis.

We deflate the nominal house prices with the corresponding consumer price index (CPI) to obtain real house prices (). Variables that can potentially influence the average house prices are numerous, and there seems to be no general consensus about what the main determinants are. Possible determinants include, but are not limited to, demographic factors such as population growth (Holly et al. 2010, Wang and Zhang 2014, Churchill et al. 2021); fundamental economic factors such as real GDP (Huang et al. 2013, Churchill et al. 2021), interest rate and inflation (Abelson et al. 2005, Otto 2007, Huang et al. 2013, Jordà et al. 2015); urbanisation (Chen et al. 2011, Wang et al. 2017); government subsidies and regulations (Malpezzi 1999); stock markets (Gallin 2006); etc. In our analysis, we focus on the following determinants of the average house prices: real GDP (), population size (), long-term interest rate () and inflation () which is measured as change in CPI. Most other factors (such as government regulations, construction costs, and real wages) vary rather slowly over time and can be captured by time trend, fixed effects and slope heterogeneity. Data for CPI, real GDP, population size and long-term interest rate are taken from the Jordà-Schularick-Taylor Macrohistory Database888See Jordà et al. (2017) for a detailed description of the variable construction., which is freely available at http://www.macrohistory.net/data/ (accessed on 13 January 2022).

In summary, we observe a panel of time series of length for each country , where and . For each , the time series is assumed to follow the model , or equivalently,

| (7.2) |

for , where is a vector of unknown parameters, is a country-specific unknown nonparametric time trend and is a fixed effect.

The inclusion of a nonparametric trend function in model \tagform@7.2 is supported by the literature. Ugarte et al. (2009), for example, model the trend in average Spanish house prices by means of splines. Winter et al. (2022) include a long-term stochastic trend component when describing the dynamic behaviour of real house prices in advanced economies. Including a nonparametric trend function when modelling the evolution of house prices is also the main conclusion in Zhang et al. (2016), where it is shown that the time series of logarithmic US house prices is trend-stationary, i.e., can be transformed into a stationary series by subtracting a deterministic trend.

We implement the multiscale test from Section 3 in the same way as in the previous application example with one minor modification: we let with

We thus take into account all locations on an equidistant grid with step length and all scales with . This implies that each interval with spans years. The lower bound is motivated by Assumption (C11). As in Section 7.1, we assume that for each , the error process follows an AR() model and we estimate the long-run variances by the difference-based estimator from Khismatullina and Vogt (2020) with tuning parameters and equal to and , respectively. We choose by minimizing the BIC. For out of countries the order determined by BIC999Applying other information criteria such as FPE, AIC and HQ yields exactly the same results in these cases. is equal to . For the sake of simplicity, we thus assume that for all .

We are now ready to apply our test to the data. The overall null hypothesis is rejected at levels and . The detailed test results for the significance level are presented in Figures 19–19. As in Section 7.1, each figure corresponds to the comparison of a pair of countries for which our test detects differences between the trends. Panel (a) shows the augmented time series and for the two countries and under consideration. Panel (b) presents smoothed versions of the time series from (a) with the bandwidth window covering years. Panel (c) presents the test results for the level . As before, the set of intervals for which our test rejects and the set of minimal intervals are depicted in grey and black, respectively. According to \tagform@4.3, we can make the following simultaneous confidence statement about the intervals plotted in panels (c) of Figures 19–19: we can claim, with confidence of about , that there is a difference between the trends and on each of these intervals.

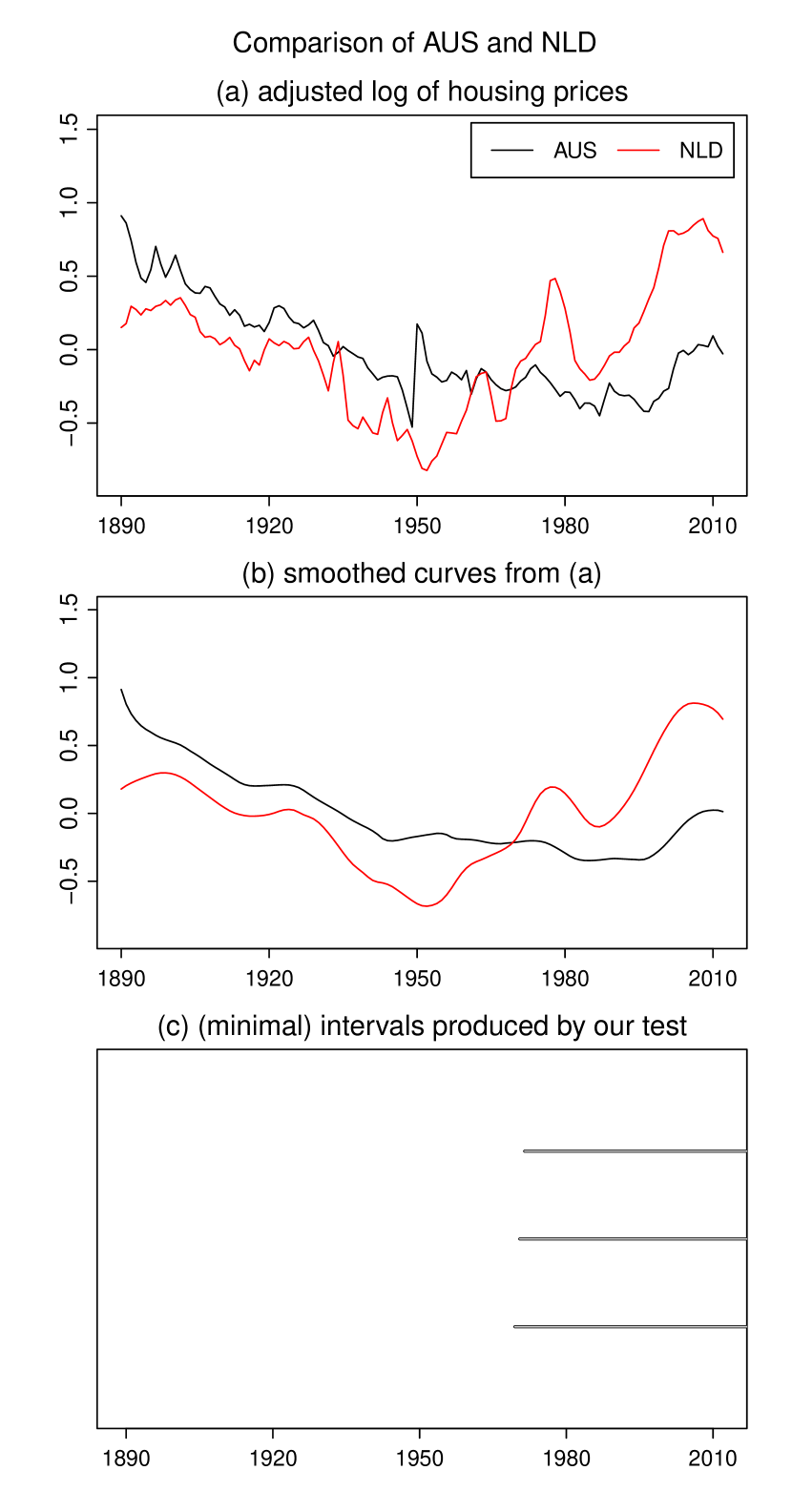

Overall, our findings are in line with the observations in Knoll et al. (2017), where the authors find considerable cross-country heterogeneity in the house price trends. The authors note that before World War II, the countries exhibit similar trends in real house prices, while the trends start to diverge sometime after World War II. This fits with our findings in Figures 19 and 19 which show that our test detects differences between the trends of Australia and the Netherlands (of Belgium and the Netherlands) starting only from 1968 (1966) onwards. Contrary to Knoll et al. (2017), however, our test also finds significant differences in the first half of the observed time period, specifically, between the time trends of Belgium and Denmark and of Belgium and the USA (Figures 19 and 19, respectively). This discrepancy in the results is most certainly due to the fact that the method used in Knoll et al. (2017) does not account for effects of other factors such as GDP or population growth, while our test allows us to include various determinants of the average house prices in model \tagform@7.2.

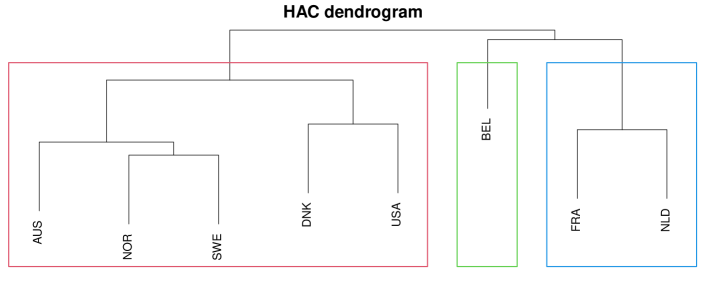

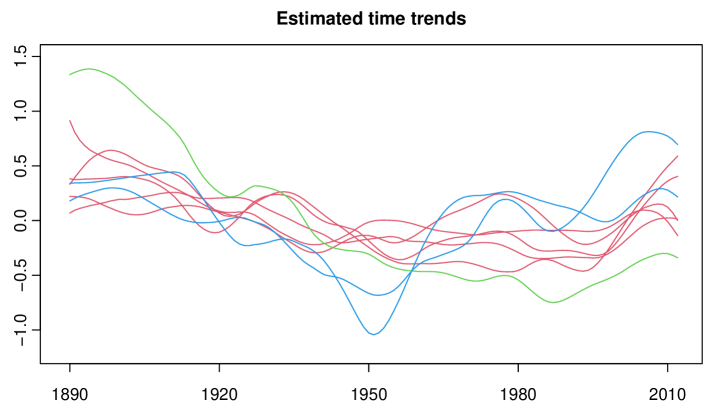

We next apply the clustering procedure from Section 5 to the data. As in the previous application example, we set . The results are displayed in Figures 21 and 21. Specifically, Figure 21 shows the dendrogram with the results of the HAC algorithm and Figure 21 presents local linear kernel estimates of the trend curves (calculated with a bandwidth window of years and an Epanechnikov kernel). The number of clusters is estimated to be . As before, the coloured rectangles in Figure 21 are drawn around the countries that belong to the same cluster and the same colours are used to display the trend estimates in Figure 21.

Inspecting the results, we can see that there is one cluster consisting only of Belgium (plotted in green). Figure 21 suggests that the Belgium time trend indeed evolves somewhat differently from the other trends in the first years of the observed time period. The algorithm further detects a cluster that consists of two countries: France and the Netherlands (plotted in blue). The time trends of these two countries display some kind of dip around 1950, which is not present in the time trends of the other countries. Overall, our algorithm thus appears to produce a reasonable clustering of the house price trends.

Acknowledgements

Financial support by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation), Germany – grant VO 2503/1-1, project number 430668955 – is gratefully acknowledged.

References

- Abelson et al. (2005) Abelson, P., Joyeux, R., Milunovich, G. and Chung, D. (2005). Explaining house prices in Australia: 1970–2003. Economic Record, 81 S96–S103.

- Atak et al. (2011) Atak, A., Linton, O. and Xiao, Z. (2011). A semiparametric panel model for unbalanced data with application to climate change in the United Kingdom. Journal of Econometrics, 164 92–115.

- Barro and Lee (2013) Barro, R. J. and Lee, J. W. (2013). A new data set of educational attainment in the world, 1950–2010. Journal of Development Economics, 104 184–198.

- Berkes et al. (2014) Berkes, I., Liu, W. and Wu, W. B. (2014). Komlós-Major-Tusnády approximation under dependence. Annals of Probability, 42 794–817.

- Cai (2007) Cai, Z. (2007). Trending time-varying coefficients time series models with serially correlated errors. Journal of Econometrics, 136 163–188.

- Carlstein (1986) Carlstein, E. (1986). The use of subseries values for estimating the variance of a general statistic from a stationary sequence. Annals of Statistics, 14 1171–1179.

- Chen et al. (2012) Chen, J., Gao, J. and Li, D. (2012). Semiparametric trending panel data models with cross-sectional dependence. Journal of Econometrics, 171 71–85.

- Chen et al. (2011) Chen, J., Guo, F. and Wu, Y. (2011). One decade of urban housing reform in China: urban housing price dynamics and the role of migration and urbanization, 1995–2005. Habitat International, 35 1–8.

- Chen and Wu (2019) Chen, L. and Wu, W. B. (2019). Testing for trends in high-dimensional time series. Journal of the American Statistical Association, 114 869–881.

- Chernozhukov et al. (2017) Chernozhukov, V., Chetverikov, D. and Kato, K. (2017). Central limit theorems and bootstrap in high dimensions. Annals of Probability, 45 2309–2352.

- Christiansen and Pigott (1997) Christiansen, H. and Pigott, C. (1997). Long-term interest rates in globalised markets.

- Churchill et al. (2021) Churchill, S. A., Baako, K. T., Mintah, K. and Zhang, Q. (2021). Transport infrastructure and house prices in the long run. Transport Policy, 112 1–12.

- Dahlhaus (1997) Dahlhaus, R. (1997). Fitting time series models to nonstationary processes. Annals of Statistics, 25 1–37.

- Degras et al. (2012) Degras, D., Xu, Z., Zhang, T. and Wu, W. B. (2012). Testing for parallelism among trends in multiple time series. IEEE Transactions on Signal Processing, 60 1087–1097.

- Dümbgen (2002) Dümbgen, L. (2002). Application of local rank tests to nonparametric regression. Journal of Nonparametric Statistics, 14 511–537.

- Dümbgen and Spokoiny (2001) Dümbgen, L. and Spokoiny, V. G. (2001). Multiscale testing of qualitative hypotheses. Annals of Statistics, 29 124–152.

- Gallin (2006) Gallin, J. (2006). The long-run relationship between house prices and income: evidence from local housing markets. Real Estate Economics, 34 417–438.

- Grier and Tullock (1989) Grier, K. B. and Tullock, G. (1989). An empirical analysis of cross-national economic growth, 1951–1980. Journal of Monetary Economics, 24 259–276.

- Hall and Hart (1990) Hall, P. and Hart, J. D. (1990). Bootstrap test for difference between means in nonparametric regression. Journal of the American Statistical Association, 85 1039–1049.

- Härdle and Marron (1990) Härdle, W. and Marron, J. S. (1990). Semiparametric comparison of regression curves. Annals of Statistics, 18 63–89.

- Hastie et al. (2009) Hastie, T., Tibshirani, R. and Friedman, J. (2009). The Elements of Statistical Learning. New York, Springer.

- Hidalgo and Lee (2014) Hidalgo, J. and Lee, J. (2014). A CUSUM test for common trends in large heterogeneous panels. In Essays in Honor of Peter C. B. Phillips. Emerald Group Publishing Limited, 303–345.

- Holly et al. (2010) Holly, S., Pesaran, M. H. and Yamagata, T. (2010). A spatio-temporal model of house prices in the USA. Journal of Econometrics, 158 160–173.

- Huang et al. (2013) Huang, M., Li, R. and Wang, S. (2013). Nonparametric mixture of regression models. Journal of the American Statistical Association, 108 929–941.

- Jordà et al. (2015) Jordà, Ò., Schularick, M. and Taylor, A. M. (2015). Betting the house. Journal of International Economics, 96 S2–S18.

- Jordà et al. (2017) Jordà, Ò., Schularick, M. and Taylor, A. M. (2017). Macrofinancial history and the new business cycle facts. NBER Macroeconomics Annual, 31 213–263.

- Karoly and Wu (2005) Karoly, D. J. and Wu, Q. (2005). Detection of regional surface temperature trends. Journal of Climate, 18 4337–4343.

- Khismatullina and Vogt (2020) Khismatullina, M. and Vogt, M. (2020). Multiscale inference and long-run variance estimation in non-parametric regression with time series errors. Journal of the Royal Statistical Society: Series B, 82 5–37.

- Khismatullina and Vogt (2021) Khismatullina, M. and Vogt, M. (2021). Nonparametric comparison of epidemic time trends: the case of COVID-19. Journal of Econometrics.

- Kim (2016) Kim, K. H. (2016). Inference of the trend in a partially linear model with locally stationary regressors. Econometric Reviews, 35 1194–1220.

- Knoll et al. (2017) Knoll, K., Schularick, M. and Steger, T. (2017). No price like home: global house prices, 1870-2012. American Economic Review, 107 331–53.

- Lee (2005) Lee, C.-C. (2005). Energy consumption and GDP in developing countries: a cointegrated panel analysis. Energy Economics, 27 415–427.

- Lee and Huang (2002) Lee, C.-H. and Huang, B.-N. (2002). The relationship between exports and economic growth in East Asian countries: a multivariate threshold autoregressive approach. Journal of Economic Development, 27 45–68.

- Malpezzi (1999) Malpezzi, S. (1999). A simple error correction model of house prices. Journal of Housing Economics, 8 27–62.

- Nazarov (2003) Nazarov, F. (2003). On the maximal perimeter of a convex set in with respect to a Gaussian measure. In Geometric Aspects of Functional Analysis. Springer, 169–187.

- Nyblom and Harvey (2000) Nyblom, J. and Harvey, A. (2000). Tests of common stochastic trends. Econometric Theory, 16 176–199.

- Otto (2007) Otto, G. (2007). The growth of house prices in Australian capital cities: what do economic fundamentals explain? Australian Economic Review, 40 225–238.

- Park et al. (2009) Park, C., Vaughan, A., Hannig, J. and Kang, K.-H. (2009). SiZer analysis for the comparison of time series. Journal of Statistical Planning and Inference, 139 3974–3988.

- Robinson (1989) Robinson, P. M. (1989). Nonparametric estimation of time-varying parameters. In Statistical Analysis and Forecasting of Economic Structural Change. Springer, 253–264.

- Robinson (2012) Robinson, P. M. (2012). Nonparametric trending regression with cross-sectional dependence. Journal of Econometrics, 169 4–14.

- Sax and Eddelbuettel (2018) Sax, C. and Eddelbuettel, D. (2018). Seasonal adjustment by X-13ARIMA-SEATS in R. Journal of Statistical Software, 87 1–17.

- Sharma and Dhakal (1994) Sharma, S. C. and Dhakal, D. (1994). Causal analyses between exports and economic growth in developing countries. Applied Economics, 26 1145–1157.

- Stock and Watson (1988) Stock, J. H. and Watson, M. W. (1988). Testing for common trends. Journal of the American Statistical Association, 83 1097–1107.

- Ugarte et al. (2009) Ugarte, M. D., Goicoa, T., Militino, A. F. and Durbán, M. (2009). Spline smoothing in small area trend estimation and forecasting. Computational Statistics & Data Analysis, 53 3616–3629.

- Vogt and Linton (2014) Vogt, M. and Linton, O. (2014). Nonparametric estimation of a periodic sequence in the presence of a smooth trend. Biometrika, 101 121–140.

- Wang et al. (2017) Wang, X.-R., Hui, E. C.-M. and Sun, J.-X. (2017). Population migration, urbanization and housing prices: evidence from the cities in China. Habitat International, 66 49–56.

- Wang and Zhang (2014) Wang, Z. and Zhang, Q. (2014). Fundamental factors in the housing markets of China. Journal of Housing Economics, 25 53–61.

- Winter et al. (2022) Winter, J. d., Koopman, S. J. and Hindrayanto, I. (2022). Joint decomposition of business and financial cycles: evidence from eight advanced economies. Oxford Bulletin of Economics and Statistics, 84 57–79.

- Wu (2005) Wu, W. B. (2005). Nonlinear system theory: another look at dependence. Proc. Natn. Acad. Sci. USA, 102 14150–14154.

- Wu and Wu (2016) Wu, W. B. and Wu, Y. N. (2016). Performance bounds for parameter estimates of high-dimensional linear models with correlated errors. Electronic Journal of Statistics, 10 352–379.

- Wu and Zhao (2007) Wu, W. B. and Zhao, Z. (2007). Inference of trends in time series. Journal of the Royal Statistical Society: Series B, 69 391–410.

- Zhang et al. (2016) Zhang, J., de Jong, R. and Haurin, D. (2016). Are US real house prices stationary? New evidence from univariate and panel data. Studies in Nonlinear Dynamics & Econometrics, 20 1–18.

- Zhang et al. (2012) Zhang, Y., Su, L. and Phillips, P. C. (2012). Testing for common trends in semi-parametric panel data models with fixed effects. The Econometrics Journal, 15 56–100.

Appendix A Appendix

In what follows, we prove the theoretical results from Sections 4 and 5. We use the following notation: The symbol denotes a universal real constant which may take a different value on each occurrence. For , we write . For , we let denote the integer value of and the smallest integer greater than or equal to . For any set , the symbol denotes the cardinality of . The expression means that the two random variables and have the same distribution. Finally, we sometimes use the notation to express that .

Auxiliary results

Let be a stationary time series process with for some and . Assume that can be represented as , where are i.i.d. variables and is a measurable function. We first state a Nagaev-type inequality from Wu and Wu (2016).

Definition A.1.

Let and . The dependence adjusted norm of the process is given by .

Proposition A.2 (Wu and Wu (2016), Theorem 2).

Assume that with and . Let , where are real numbers with . Then for any ,

where are constants that only depend on and .

The following lemma is a simple consequence of the above inequality.

Lemma A.3.

Let for some and . Then

Proof of Lemma A.3..

Let be a fixed number. We apply Proposition A.2 to the sum with for all . The assumption implies that . Hence, for chosen sufficiently large, we get

for all . This means that . ∎

Let and . By Assumptions (C1) and (C4), and . We further define

where , and with and . The next result gives bounds on the physical dependence measures of the processes and .

Lemma A.4.

Proof of Lemma A.4..

We only prove the first statement. The second one follows by analogous arguments. By the definition of the physical dependence measure and the Cauchy-Schwarz inequality, we have with that

where , and are coupled processes with , and being i.i.d. copies of , and . From this and Assumptions (C1), (C3), (C4) and (C6), it immediately follows that . ∎

We now show that the estimator is -consistent for each under our conditions.

Proof of Lemma A.5..

The estimator can be written as

where , and . Hence,

| (A.1) |

In what follows, we show that

| (A.2) | ||||

| (A.3) | ||||

| (A.4) |

Lemma A.5 follows from applying these three statements together with standard arguments to formula \tagform@A.1.

Since by (C7) and for some , and all by Lemma A.4, the claim \tagform@A.2 follows upon applying Lemma A.3. Another application of Lemma A.3 yields that

As is invertible, we can invoke Slutsky’s lemma to obtain \tagform@A.3. By assumption, is Lipschitz continuous, which implies that for all and some constant . Hence,

where we have used that by Markov’s inequality. This yields \tagform@A.4. ∎

Lemma A.6.

Proof of Theorem 4.1

We first summarize the main proof strategy, which splits up into five steps, and then fill in the details. We in particular defer the proofs of some intermediate results to the end of the section.

Step 1

To start with, we consider a simplified setting where the parameter vectors are known. In this case, we can replace the estimators in the definition of the statistic by the true vectors themselves. This leads to the simpler statistic

where

and is computed in exactly the same way as except that all occurrences of are replaced by . By assumption, with . For most estimators of including those discussed in Section 4, this assumption immediately implies that as well. In the sequel, we thus take for granted that the estimator has this property.

We now have a closer look at the statistic . We in particular show that there exists an identically distributed version of which is close to the Gaussian statistic from \tagform@3.12. More formally, we prove the following result.

Proposition A.7.

There exist statistics with the following two properties: (i) has the same distribution as for any , and (ii)

where and is a Gaussian statistic as defined in \tagform@3.12.

The proof makes heavy use of strong approximation theory for dependent processes. As it is quite technical, it is postponed to the end of this section.

Step 2

In this step, we establish some properties of the Gaussian statistic . Specifically, we prove the following result.

Proposition A.8.

It holds that

where .

Roughly speaking, this proposition says that the random variable does not concentrate too strongly in small regions of the form with converging to . The main technical tool for deriving it are anti-concentration bounds for Gaussian random vectors. The details are provided below.

Step 3

We now use Steps 1 and 2 to prove that

| (A.5) |

Step 4

In this step, we show that the auxiliary statistic is close to in the following sense.

Proposition A.9.

It holds that

with .

The proof can be found at the end of this section.

Step 5

We finally show that

| (A.6) |

Details on Steps 1–5

Proof of Proposition A.7.

Consider the stationary process for some fixed . By Theorem 2.1 and Corollary 2.1 in Berkes et al. (2014), the following strong approximation result holds true: On a richer probability space, there exist a standard Brownian motion and a sequence such that for each and

| (A.8) |

where denotes the long-run error variance. We apply this result separately for each . Since the error processes are independent across , we can construct the processes in such a way that they are independent across as well.

We now define the statistic in the same way as except that the error processes are replaced by . Specifically, we set

where

and the estimator is constructed from the sample in the same way as is constructed from . Since and , we have that as well. In addition to , we introduce the Gaussian statistic

and the auxiliary statistic

where and the Gaussian variables are chosen as . With this notation, we obtain the obvious bound

In what follows, we prove that

| (A.9) | ||||

| (A.10) |

which completes the proof.

First consider . Straightforward calculations yield that

| (A.11) |

where the last line follows from the fact that . Using summation by parts (that is, with ), we further obtain that

where

and for all pairs by construction. From this, it follows that

| (A.12) |

with . Straightforward calculations yield that

Applying the strong approximation result \tagform@A.8, we can infer that

Moreover, standard arguments show that . Plugging these two results into \tagform@A.12, we obtain that

which in view of \tagform@A.11 yields that . This completes the proof of \tagform@A.9.

Next consider . It holds that

| (A.13) |

where the last line is due to the fact that . We can write , where

with for all and . This shows that are centred Gaussian random variables with bounded variance for all and . Hence, standard results on the maximum of Gaussian random variables yield that

| (A.14) |

where we have used that is fixed and for some large but fixed constant by Assumption (C10). Plugging this into \tagform@A.13 yields , which completes the proof of \tagform@A.10. ∎

Proof of Proposition A.8..

The proof is an application of anti-concentration bounds for Gaussian random vectors. We in particular make use of the following anti-concentration inequality from Nazarov (2003), which can also be found as Lemma A.1 in Chernozhukov et al. (2017).

Lemma A.10.

Let be a centred Gaussian random vector in such that for all and some constant . Then for every and ,

where the constant only depends on .

To apply this result, we introduce the following notation: We write and , where for some large but fixed by our assumptions. For and , we further let

along with and , where . Under our assumptions, it holds that and for all , and . We next construct the random vector by stacking the variables in a certain order (which can be chosen freely) and construct the vector in an analogous way. Since the variables are normally distributed, is a Gaussian random vector of length .

Proof of Proposition A.9.

Straightforward calculations yield that

Since and , we further get that

and

where the difference of the kernel averages does not include the error terms (they cancel out) and can be written as

Hence,

| (A.15) |

where

We examine these three terms separately.

We first prove that

| (A.16) |

From the proof of Proposition A.7, we know that there exist identically distributed versions of the statistics with the property that

| (A.17) |

Instead of \tagform@A.16, it thus suffices to show that

| (A.18) |

Since for any constant ,

and by \tagform@A.17, we get that

| (A.19) |

Moreover, since as already proven in \tagform@A.14, we can make the probability on the right-hand side of \tagform@A.19 arbitrarily close to by choosing the constant sufficiently large. Hence, for any , we can find a constant such that for sufficiently large . This proves \tagform@A.18, which in turn yields \tagform@A.16.

We next turn to . Without loss of generality, we assume that is real-valued. The vector-valued case can be handled analogously. To start with, we have a closer look at the term . By construction, the kernel weights are unequal to if and only if . We can use this fact to write

Note that

| (A.20) | ||||

Denoting by the number of integers between and (with the obvious bounds ) and using \tagform@A.20, we can normalize the kernel weights as follows:

Next, we apply Proposition A.2 with the weights to obtain that

| (A.21) |

for any , where is the dependence adjusted norm introduced in Definition A.1 and by Assumption (C6). From \tagform@A.21, it follows that for any ,

| (A.22) |

where the constant depends neither on nor on . In the last equality of the above display, we have used the following facts:

-

(i)

by Assumption (C6).

-

(ii)

(which follows from (i)).

-

(iii)

for the following reason: By \tagform@A.20, it holds that and thus for all , and . This implies that for all , and . As a result,

Since by Assumption (C4), the bound in \tagform@A.22 converges to as for any fixed . Consequently, we obtain that

| (A.23) |

Using this together with the fact that (which is the statement of Lemma A.5), we arrive at the bound

We finally turn to . Straightforward calculations yield that . Moreover, by Lemma A.3 and by Lemma A.5. This immediately yields that

To summarize, we have shown that

This immediately implies the desired result. ∎

Proof of Proposition 4.3

We first show that

| (A.24) |

We proceed by contradiction. Suppose that \tagform@A.24 does not hold true. Since by definition of the quantile , there exists such that . From the proof of Proposition A.8, we know that for any ,

Hence,

for small enough. This contradicts the definition of the quantile according to which . We thus arrive at \tagform@A.24.

Proof of Proposition 4.4

To start with, note that for some sufficiently large constant we have

| (A.25) |

Write with