Chaotic Hedging with Iterated Integrals and Neural Networks

Abstract.

In this paper, we extend the Wiener-Ito chaos decomposition to the class of diffusion processes, whose drift and diffusion coefficient are of linear growth. By omitting the orthogonality in the chaos expansion, we are able to show that every -integrable functional, for , can be represented as sum of iterated integrals of the underlying process. Using a truncated sum of this expansion and (possibly random) neural networks for the integrands, whose parameters are learned in a machine learning setting, we show that every financial derivative can be approximated arbitrarily well in the -sense. Since the hedging strategy of the approximating option can be computed in closed form, we obtain an efficient algorithm that can replicate any integrable financial derivative with short runtime.

Key words and phrases:

Hedging, Chaos Expansion, Martingale Representation, Iterated Integrals, Machine Learning, Universal Approximation, Neural Networks, Reservoir Computing, Affine Diffusions, Polynomial Diffusions1. Introduction

We address the problem of pricing and hedging a financial derivative within a financial market consisting of risky assets, whose prices are modelled by a diffusion process with drift and diffusion coefficient of linear growth. This includes in particular affine and some polynomial diffusion processes (see [Duffie et al., 2000], [Cuchiero, 2011], and [Filipović and Larsson, 2016]). While in complete markets, every financial derivative can be perfectly replicated using one pricing measure, the hedging problem in incomplete markets needs to be addressed with an additional criteria, for example, “mean-variance hedging” (see e.g. [Duffie and Richardson, 1991], [Schweizer, 1992], and [Pham et al., 1998]), “super-replication” (see e.g. [El Karoui and Quenez, 1995], [Cvitanić et al., 1999], [Cheridito et al., 2005], and [Acciaio et al., 2016]), “quadratic hedging” (see e.g. [Schweizer, 1999] and [Pham, 2000]), or “utility indifference pricing and hedging” (see e.g. [Musiela and Zariphopoulou, 2004] and [Carmona, 2009]).

Our “chaotic hedging” approach solves the hedging problem by minimizing a given loss function and is therefore similar to the idea of “quadratic hedging”. The numerical algorithm relies on the so-called chaos expansion of a financial derivative, which can be seen as Taylor formula for random variables, and has been applied for option pricing (see [Lacoste, 1996] and [Lelong, 2018]) and for solving stochastic differential equations (SDEs) (see [Xiu and Karniadakis, 2002]). Moreover, by proving a universal approximation result for random neural networks, we are able to efficiently learn the financial payoff. We refer to other successful neural networks applications in finance (see e.g. [Han et al., 2018], [Bühler et al., 2019], [Sirignano and Cont, 2019], [Cuchiero et al., 2020], [Eckstein et al., 2020], [Eckstein et al., 2021], [Neufeld and Sester, 2022], [Neufeld et al., 2022], and [Schmocker, 2022]). Altogether, this paper introduces a fast two-step approximation of any sufficiently integrable financial derivative, by first using a truncation of its chaos expansion, and then learning (random) neural networks for each order of the expansion. The algorithm can be also applied to high-dimensional options and returns the hedging strategy of the approximation in closed form.

The main idea of this paper relies on the chaos expansion of a financial derivative. In the Brownian motion case, the so-called Wiener-Ito chaos decomposition (see [Ito, 1951, Theorem 4.2]) yields an expression for every square-integrable functional of the Brownian path as infinite sum of iterated integrals of the given Brownian motion. This was later extended to the compensated Poisson process (see [Ito, 1956, Theorem 2]) and Azéma martingales (see [Émery, 1989, Proposition 6]). Moreover, [Løkka, 2004], [Jamshidian, 2005], [Di Nunno et al., 2008], and [Di Tella and Engelbert, 2016a] proved the chaos expansion for particular martingales with independent increments. However, to the best of our knowledge, a chaos expansion with respect to a diffusion process with stochastic covariation and non-independent increments has not yet been established in the literature. Opposed to the classical Wiener-Ito chaos decomposition, we omit the orthogonality in the chaos expansion and use the direct sum (instead of the orthogonal sum) together with the so-called “time-space harmonic Hermite polynomials” in order to span the chaotic subspaces. Moreover, by extending the Kailath-Segall formula in [Segall and Kailath, 1976], we are able to express every -integrable functionals, , as iterated integrals of the underlying diffusion process, which yields an analogue of the classical Wiener-Ito chaos decomposition in this more general setting with possible drift process.

It is well-known that whenever the underlying stochastic process is a Brownian motion, the chaos expansion can be used to obtain a martingale representation result, which ensures the existence of a hedging strategy for each square-integrable functional of the Brownian path, see e.g. [Karatzas and Shreve, 1998, Section 3.4]. This has been extended to the compensated Poisson process (see e.g. [Ikeda and Watanabe, 1989, Theorem II.6.7]), Azéma martingales (see [Émery, 1989]), and other martingales with independent increments (see [Nualart and Schoutens, 2000], [Løkka, 2004], [Davis, 2005], [Jamshidian, 2005], and [Di Tella and Engelbert, 2016b]). In our setting, we are able to retrieve a similar representation, but with respect to the diffusion process, which relies on the -closedness of stochastic integrals (see [Grandits and Krawczyk, 1998] and [Delbaen et al., 1997]). This leads us in the martingale case (i.e. without drift) to a martingale representation result similar to [Soner et al., 2011, Theorem 6.5].

The machine learning application of this paper consists of learning the integrands of the iterated integrals in the chaos expansion. More precisely, we first approximate a financial derivative by truncating the infinite sum of iterated integrals from its chaos expansion, and then replace the deterministic integrands by neural networks. This provides us with a parametric family of financial derivatives, whose optimal coefficients can be learned by minimizing a loss function in the sense of “quadratic hedging”.

In addition, we extend our universal approximation result for financial derivatives to random neural networks with randomly initialized weights and biases, which is inspired by the works on extreme learning machines and random features (see e.g. [Huang et al., 2006], [Rahimi and Recht, 2007], [Grigoryeva and Ortega, 2018], [Gonon et al., 2022], and [Gonon, 2022]). In this case, the optimization procedure reduces to the training of the linear readout, which can be performed, e.g., by a simple linear regression. This can be solved within few minutes, also for high-dimensional financial derivatives.

Altogether, our “chaotic hedging” approach provides a “global” universal approximation result for financial derivatives by using the -norm. This is more general than other universal approximation results for financial applications (see e.g. [Lyons et al., 2019], [Benth et al., 2022], [Lyons et al., 2020], [Acciaio et al., 2022], and [Cuchiero et al., 2022b]), where the approximation holds true on a compact subset of the sample path space. Other “global” universal approximation results have been found in [Király and Oberhauser, 2019], [Schmocker, 2022], and [Cuchiero et al., 2023]. However, in this paper, we exploit the chaos expansion of a given financial derivative to learn its hedging strategy.

1.1. Outline

In Section 2, we introduce the setting of this paper and provide the main theoretical results, including the chaos expansion, the corresponding (semi-) martingale representation result, and the theoretical approximation results for financial derivatives. Subsequently, we illustrate in Section 3 how these theoretical results can be applied to learn the hedging strategy of various options in different markets. Finally, all proofs of the theoretical results are given in Section 4.

1.2. Notation

As usual, and denote the sets of natural numbers, whereas and represent the real and complex numbers (with complex unit ), respectively, where , for . Moreover, denotes the Euclidean space equipped with the norm , whereas represents the vector space of matrices equipped with the Frobenius norm . Hereby, denotes the cone of symmetric non-negative definite matrices and represents the identity matrix.

In addition, for , with , represents the Borel -algebra of , whereas denotes the space of continuous functions . Furthermore, for and , we denote by the Banach space of -measurable functions with finite norm , whereas for , the inner product turns into a Hilbert space. Moreover, we abbreviate .

2. Setting and Main Results

Throughout this paper, we consider a financial market with finite time horizon consisting of risky assets, whose vector of price processes follows a stochastic process with continuous sample paths and values in a subset .

2.1. Setting

On a given probability space , we fix an -dimensional Brownian motion endowed with the natural -augmented filtration generated by such that , and let and be continuous. We assume that is an -valued strong solution (see [Karatzas and Shreve, 1998, Definition 5.2.1]) of the stochastic differential equation (SDE) , with , i.e. is -adapted, and for every and , it holds -a.s. that

| (1) |

where , -a.s.

Definition 2.1.

An -valued strong solution of (1) is called a (time-inhomogeneous) diffusion process on with drift coefficient and diffusion coefficient defined by

for . Moreover, we say that the drift and diffusion coefficient (shortly “coefficients”) are of linear growth if there exists some such that

for all .

Remark 2.2.

By [Karatzas and Shreve, 1998, Thereom 5.2.9], (1) admits a strong solution if, e.g., and satisfy a Lipschitz and linear growth condition, i.e. there exists a constant such that for every and , it holds that

Moreover, (1) admits by the Yamada conditions in [Yamada and Watanabe, 1971] a strong solution (see also [Ikeda and Watanabe, 1989, Theorem IV.3.2] and [Altay and Schmock, 2016, Theorem 2.1 & Remark 2.7] for ) if there exists and with , non-decreasing, concave, and continuous, non-decreasing, for all , , and for all , such that for every with and , it holds that

Example 2.3 (Polynomial Diffusions).

For , let be a one-dimensional Brownian motion and let be an -valued solution of (1) with time-homogeneous drift and diffusion coefficient , i.e.

| (2) |

for . Hereby, the state space depends on , which we require to satisfy , for all . For and , with , it follows by choosing (see [Altay and Schmock, 2016, Remark 2.7]) and inserting the inequality for any , that

Hence, (2) admits by Remark 2.2 a strong solution, which shows that is a diffusion process, called a polynomial diffusion in the sense of [Filipović and Larsson, 2016, Definition 2.1]. Moreover, in the case of vanishing drift (i.e. ), there are in particular three relevant cases:

| e.g. Brownian motion (BM), | (3a) | |||||

| (3b) | ||||||

| e.g. Jacobi process. | (3c) | |||||

If or is compact (e.g. (3c)), the diffusion coefficient is of linear growth. Moreover, conditional moments and higher order correlators can be computed with [Filipović and Larsson, 2016, Theorem 3.1] and [Benth and Lavagnini, 2021, Theorem 4.5], respectively.

In the remaining part of this section, we prove that an -valued time-inhomogeneous diffusion process with drift and diffusion coefficient of linear growth admits moments of all orders and is exponentially integrable. The proofs are all contained in Section 4.

Lemma 2.4.

Let be a time-inhomogeneous diffusion process with coefficients of linear growth with constant . Then, for every , it holds that

| (4) |

Moreover, for every and , we have that

| (5) |

Next, we denote by the vector space of left-continuous functions with right limits (LCRL). Moreover, for a given -valued diffusion process with as well as every and -measurable function , we define

| (6) |

Hence, by using [Fraňková, 1991, Lemma 1.5+1.7], i.e. that every LCRL function in is -measurable and bounded, we can estimate the -norm.

Lemma 2.5.

Let be a diffusion process with coefficients of linear growth, and let . Then, every is -measurable and bounded. Moreover, there exists a constant such that for every it follows that

where .

On , we define the equivalence relation “” by if and only if , for any . Moreover, by a slight abuse of notation, we sometimes write as function, which in fact refers to the equivalence class . Then, we introduce the following quotient space of deterministic LCRL integrands.

Definition 2.6.

For a diffusion process , whose coefficients are of linear growth, and , we define as the quotient space equipped with defined in (6).

Remark 2.7.

The space has also been introduced in [Föllmer and Schweizer, 1991, Equation 2.8], [Delbaen et al., 1997, Definition 2.3], [Grandits and Krawczyk, 1998, Definition 2.4+2.5], and [Protter, 2005, p. 165] for (stochastic) -predictable integrands instead of deterministic integrands.

Next, we show that is in fact an (incomplete) normed vector space, on which we define the following operators returning the stochastic integral and its quadratic variation.

Lemma 2.8.

Let be a diffusion process with coefficients of linear growth, and let . Then, is a normed vector space.

Definition 2.9.

For , we introduce the operators and defined by

which return the stochastic integral and its quadratic variation of a function .

Remark 2.10.

While we show in Lemma 2.11 that the operators and are well-defined and bounded, we first observe that is well-defined as stochastic integral. Indeed, the drift part is well-defined as Lebesgue integral. On the other hand, since every is by definition left-continuous, and is itself continuous, the integrand is left-continuous and -adapted, thus -predictable and locally bounded. Hence, is well-defined as stochastic integral, which shows that the process is also well-defined.

Moreover, for every and , we introduce the processes and , which represent the stochastic integral and its quadratic variation at each time .

Lemma 2.11.

Let be a diffusion process and let . Then, there exists a constant such that for every , it holds that

| (7a) | ||||

| (7b) | ||||

with , where denotes the constant of the classical upper Burkholder-Davis-Gundy inequality with exponent .

In the following, we now use the operators and returning the stochastic integral and its quadratic variation to obtain the chaos expansion.

2.2. Abstract Chaos Expansion

In this section, we introduce the time-space harmonic Hermite polynomials, which are obtained from the classical (probabilist’s) Hermite polynomials defined by

| (8) |

for and (see [Abramowitz and Stegun, 1970, Section 22] for more details).

Definition 2.12.

The time-space harmonic Hermite polynomials are defined by

for and .

Example 2.13.

The first Hermite polynomials and time-space harmonic Hermite polynomials up to order four are given by and

for .

Remark 2.14.

In the usual setting of Malliavin calculus introduced in [Malliavin, 1978] with being a one-dimensional Brownian motion, the linear operator is defined as isonormal process such that is a Gaussian random variable, for all (see [Nualart, 2006, Definition 1.1.1]). Then, [Nualart, 2006, Lemma 1.1.1] shows the orthogonality relation

This relation still holds true for martingales with deterministic quadratic variation, which are by [Dambis, 1965] and [Dubins and Schwarz, 1965] deterministic time changes of Brownian motion. However, as soon as the quadratic variation of is stochastic or any additional drift is added, the random variables might no longer be orthogonal in .

Now, we define the chaotic subspaces of , which are the generalization of the orthogonal chaotic subspaces in classical Malliavin calculus used in [Nualart, 2006, Theorem 1.1.1].

Definition 2.15.

For every , the -th chaotic subspace is defined as

| (9) |

where are the time-space harmonic Hermite polynomials from Definition 2.12.

Next, we show that every chaotic subspace , , is well-defined as vector subspace of .

Lemma 2.16.

For every and , it holds that .

Moreover, we denote by “” the direct sum, which is the sum over finite tuples defined by

In the classical Wiener-Ito chaos decomposition with , the orthogonal sum is used instead of the direct sum because the random variables are orthogonal in , see also Remark 2.14. However, as soon as becomes stochastic or any drift is added, the chaotic subspaces will no longer be orthogonal to each other in .

Theorem 2.17 (Chaos Expansion).

Let be a time-inhomogeneous diffusion process with coefficients of linear growth, and let . Then, is dense in .

The chaos expansion in Theorem 2.17 provides the theoretical foundation for the following machine learning application, where we learn a financial derivative and its hedging strategy.

2.3. Chaos Expansion with Iterated Integrals

In this section, we introduce iterated integrals of a diffusion process , whose drift and diffusion coefficient is of linear growth. By using the time-space harmonic Hermite polynomials, we obtain the chaos expansion with respect to iterated integrals.

For every , we define , with . Moreover, for every , let be the vector space of linear functionals acting on multilinear forms , i.e. we define the linear functional by

for each multilinear form . Hence, we can express every tensor as , for some , , , , where the representation might not be unique. From this, we define the linear functional by

| (10) |

for each multilinear form , where the value of the sum in (10) is independent of the representation of , see also [Ryan, 2002, Chapter 1]. On the vector space , we define the so-called projective tensor norm

In the next lemma, we show that is a norm.

Lemma 2.18.

For every and , is a normed vector space. Moreover, it holds for every that .

Remark 2.19.

For , we recover from Lemma 2.8, i.e. .

In the following, denotes the vector space of -measurable random variables.

Definition 2.20.

For , the -fold iterated integral is the operator defined by , for , and for and of the form , , by

as well as , for .

While we prove in Lemma 2.22 and Lemma 2.23 that is a linear, bounded, and continuous operator, and that does not depend on the representation of , we first show that is well-defined as iterated stochastic integrals.

Remark 2.21.

For , we introduce the stochastic process defined by

such that , where is by Remark 2.10 well-defined as stochastic integral. By abbreviating , we iteratively define for every the process by

such that . Hereby, is well-defined as stochastic integrals of with respect to , for , because every integrand is left-continuous and -adapted, thus -predictable and locally bounded.

Lemma 2.22.

The operator is linear. Moreover, for every with representations and , it holds that , -a.s.

Next, we show that the linear operator is well-defined and bounded, thus continuous. For this purpose, we derive an upper Burkholder-Davis-Gundy type of inequality for iterated integrals of a semimartingale, which is similar to [Carlen and Kree, 1991, Theorem 1].

Lemma 2.23.

Let be a diffusion process with coefficients of linear growth, let and . Then, there exists a constant such that for every , it holds that

| (11) |

with , where , , denotes the constant of the classical upper Burkholder-Davis-Gundy inequality with exponent .

Next, we consider for every and the vector subspace of diagonal tensors in . For this purpose, we define the vector subspace

and show that the iterated integral of such a diagonal tensor can be expressed with the time-space harmonic Hermite polynomials in Definition 2.12. This relies on the Kailath-Segall formula, which was shown for -integrable martingales in [Segall and Kailath, 1976], but still holds true for semimartingales.

Lemma 2.24 (Kailath-Segall).

Let be a diffusion process with coefficients of linear growth, let and . Then, it follows for every and that

where denote the time-space harmonic Hermite polynomials.

Remark 2.25.

Finally, we prove the following chaos expansion for financial derivatives, which is obtained from the abstract chaos expansion in Theorem 2.17 together with the Kailath-Segall formula in Lemma 2.24.

Theorem 2.26 (Chaos Expansion).

Let be a diffusion process with coefficients of linear growth, and let for some . Then, for every there exists some and a sequence of functions , with for all , such that

| (12) |

2.4. (Semi-) Martingale Representation

By using the chaos expansion in Theorem 2.26, we derive the following (semi-) martingale representation theorem. For every , we introduce the space consisting of -dimensional -predictable stochastic processes which satisfy

Then, we observe that holds -a.s. true, which implies that is well-defined, for all . Moreover, we define the vector subspace

Moreover, we call an equivalent probability measure an equivalent local martingale measure (ELMM) for if is a local martingale under . Then, by assuming the existence of such an ELMM , we first prove a representation with respect to the semimartingale under .

Lemma 2.27 ([Grandits and Krawczyk, 1998, Lemma 4.5]).

Let be a diffusion process, let with , and assume that there exists an ELMM for with density . Then, is closed in if and only if there exists some such that for every , it holds that

| (13) |

Theorem 2.28 (Semimartingale Representation).

Let be a diffusion process with coefficients of linear growth, and let with . Moreover, assume that there exists an ELMM for with density , and suppose that (13) holds true. Then, for every there exists a -dimensional and -predictable process such that

Theorem 2.28 yields sufficient conditions for the representation of a random variable , for , with respect to the semimartingale diffusion process, which relies on the -closedness of , see [Grandits and Krawczyk, 1998] and [Delbaen et al., 1997] for more details.

Moreover, if is a local martingale diffusion, i.e. a diffusion process with , for all , we obtain the following martingale representation result.

Corollary 2.29 (Martingale Representation).

Let be a local martingale diffusion, whose diffusion coefficient is of linear growth, and let . Then, for every there exists a -dimensional and -predictable process such that

| (14) |

Remark 2.30.

The classical martingale representation expresses an -integrable random variable in terms of a stochastic integral with respect to Brownian motion, where the integrand is unique (see [Karatzas and Shreve, 1998, Problem 3.4.17]). This result was extended in [Dudley, 1977, Abstract] to any -measurable random variable without integrability condition, where, however, is not unique anymore. Hence, Corollary 2.29 can be seen as generalization of [Dudley, 1977, Abstract] to diffusion processes with coefficients of linear growth. Moreover, [Soner et al., 2011, Theorem 6.5] derived a similar result when is -a.s. invertible, for all .

2.5. Approximation of Financial Derivatives by Neural Networks

In this section, we approximate a financial derivative with the help of the chaos expansion in Theorem 2.26. More precisely, we first approximate by a truncated sum of iterated integrals, and then replace the integrands of the iterated integrals by tensor-valued neural networks, to obtain a parametric family of random variables. The numerical method returns the hedging strategy of the learned option in closed form.

For a general introduction to neural networks defined on Euclidean spaces and their universal approximation property, we refer to [Cybenko, 1989], [Hornik, 1991], and [Pinkus, 1999]. Moreover, results about approximation rates of neural networks can be found in [Bölcskei et al., 2019].

Definition 2.31.

For and , a diagonal tensor is called an -valued (resp. tensor-valued) neural network if for every it holds that

| (15) |

for some , , and . In this case, the vectors and are called the weights and biases, respectively, whereas the numbers are called the linear readouts. Moreover, is called an activation function.

Definition 2.32.

For and , we define as the set of all -valued neural networks, whereas for , we set .

Remark 2.33.

For the approximation of a financial derivative , we use finitely many iterated integrals and replace the integrands by tensor-valued neural networks.

Definition 2.34.

Let be a tuple of tensor-valued neural networks , for all . Then, we define the financial derivative generated by as

Remark 2.35.

Now, we use the properties of neural networks to approximate any tensor in , for and . For this purpose, we first introduce a property related to the activation function.

Definition 2.36.

A function is called activating if is dense in with respect to the uniform topology.

Remark 2.37.

A function is activating if it satisfies one of the following sufficient conditions:

-

(i)

bounded and sigmoidal (see [Cybenko, 1989, Theorem 1 & Lemma 1]),

-

(ii)

discriminatory, i.e. if for every finite signed Radon measure satisfying for all , it follows that (see [Cybenko, 1989, Theorem 1]),

-

(iii)

bounded and non-constant (see [Hornik, 1991, Theorem 2]),

-

(iv)

non-polynomial (see [Pinkus, 1999, Theorem 3.1]).

Now, we use this property of the activation function to lift the universal approximation property of deterministic neural networks to the normed vector space .

Proposition 2.38.

Let be a diffusion process with coefficients of linear growth, let be activating, let and . Then, is dense in , i.e. for every and there exists some such that .

This version of the universal approximation property of neural networks presented in Proposition 2.38 allows us to get an approximation result for financial derivatives , where .

Theorem 2.39 (Universal Approximation).

Let be a diffusion process with coefficients of linear growth, let be activating, and let for some . Then, for every there exists some and such that satisfies .

Next, we show that the weights and biases of the tensor-valued neural networks in the approximating financial derivative can be initialized randomly and only the linear readouts need to be trained to obtain a similar approximation result as in Theorem 2.39. This generalizes the works on extreme machine learning and random features (see e.g. [Huang et al., 2006], [Rahimi and Recht, 2007], and [Gonon et al., 2022]).

For this purpose, we fix an activation function and two real-valued random variables defined on another probability space . Moreover, for the next results, we impose the following condition on the distribution of .

Assumption 2.40.

The random variables admit a joint density function which is strictly positive and satisfies for every that

Example 2.41.

Assumption 2.40 is satisfied for example if is bounded (e.g. sigmoid function ) or if there exist some such that , for all , and and have moments of all orders (e.g. ReLU function and ).

Now, for every , the map is called a random tensor-valued neural network if for every and , it holds that

where and are independent and identically distributed (i.i.d.) random variables, and where the map consists of some and an event , for all .

We denote by the set of random -valued neural networks, with , and show that is contained in every Bochner space (see [Hytönen et al., 2016, Definition 1.2.15]), for all , where is the -completion of .

Proposition 2.42.

Let Assumption 2.40 hold true, let , and let . Then, for every , we have .

By the strong law of large numbers for Banach space-valued random variables in [Hytönen et al., 2016, Theorem 3.3.10], we obtain the following universal approximation result for random neural networks.

Proposition 2.43.

Let be a diffusion process with coefficients of linear growth, let be activating, let Assumption 2.40 hold true, and let for some and . Then, for every and there exists some such that .

As a consequence of Proposition 2.43, we obtain the following approximation result for financial derivatives , with , which is similar to Theorem 2.39 but now with random neural networks instead of deterministic neural networks.

Corollary 2.44 (Random Universal Approximation).

Let be a diffusion process with coefficients of linear growth, let be activating, let Assumption 2.40 hold true, and let for some . Then, for every and there exists some and such that satisfies .

Next, we show that the hedging strategy of a financial derivative generated by tensor-valued neural networks can be computed in closed form. In case of random neural networks, the result can still be applied because for and .

Theorem 2.45 (Hedging Strategy).

Theorem 2.45 provides us with an explicit formula in (17) for the hedging strategy of a financial derivative of the form , where .

Remark 2.46.

The universal approximation results in Theorem 2.39 (for deterministic neural networks) and in Corollary 2.44 (for random neural networks) extend the following results in the literature:

-

(i)

To learn a financial derivative, the so-called “signature” has been applied in [Lyons et al., 2019], [Kalsi et al., 2020], [Lyons et al., 2020], [Perez Arribas et al., 2020], [Cuchiero et al., 2022a],[Cartea et al., 2022], [Cuchiero et al., 2022b], [Cuchiero et al., 2023], and the references therein. The signature appears in the theory of rough paths (see [Lyons et al., 1998]) and satisfies a similar universality as neural networks but for path space functionals. Moreover, since the signature of a diffusion process is given as the iterated integrals with constant integrand equal to one, Theorem 2.39 can be related to the results cited above. However, in our “chaotic hedging” approach, the iterated integrals can be computed directly with the time-space harmonic Hermite polynomials (see Lemma 2.24). In addition, by using the -norm, the universal approximation result in Theorem 2.39 holds globally true and not only on a compact subset of the space of sample paths from the diffusion process.

-

(ii)

The random universal approximation result in Corollary 2.44 is similar to [Gonon, 2022, Corollary 5.4], where random neural networks with the ReLU activation function have been used to learn European option prices in the Black-Scholes model.

3. Numerical Examples

In the following, we show how the theoretical results of this paper can be applied to solve the hedging problem. For a time-inhomogeneous diffusion process with coefficients of linear growth, the universal approximation result with random neural networks in Corollary 2.44 holds true. Hence, we apply the following steps to approximate the hedging strategy of a financial derivative , :

-

(1)

For , generate discretized sample paths of , , where is a discretization of , and compute for every the corresponding option payoff .

-

(2)

Choose some (the order of the chaos expansion), some (the sizes of the networks in each order), and a function which is activating (see Definition 2.32).

-

(3)

For every , , and randomly initialize and on the probability space , which means that we fix some . Hereby, the distribution of should satisfy Assumption 2.40.

-

(4)

Let and define for every and the random neurons .

-

(5)

Compute for every , , and the stochastic integral and its quadratic variation at time , e.g. with the Euler-Maruyama scheme for and the Euler scheme for .

- (6)

-

(7)

Define for every the financial derivative generated by , where .

-

(8)

Minimize the empirical -norm by optimizing over and , for and . This can be obtained by a linear regression.

- (9)

Remark 3.1.

If deterministic neural networks instead of random neural networks are applied, we use Theorem 2.39, omit the -dependence in (1)-(9), and replace (3)+(4) and (8) above by the following:

-

(3)+(4)

Let and initialize for every and deterministic neural neurons of the form for some .

-

(8)

Minimize the empirical -norm by optimizing over and the network parameters , for , , and .

However, the training of deterministic neural networks is a non-convex optimization problem with an iterative algorithm (e.g. (stochastic) gradient descent or the Adam algorithm, see [Goodfellow et al., 2016]), which might lead to a long or unstable training performance.

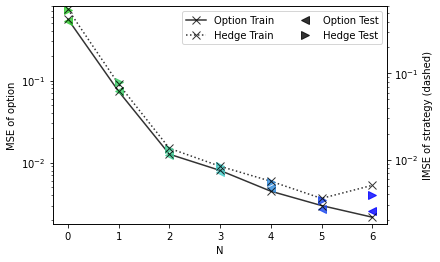

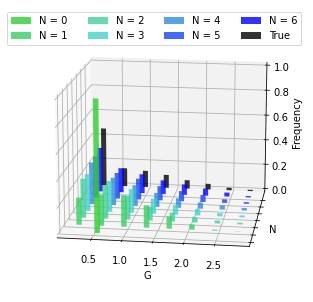

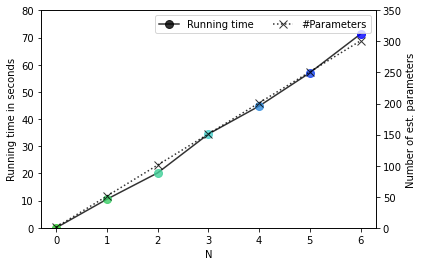

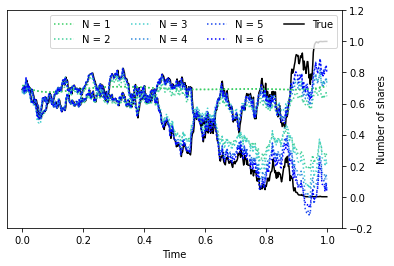

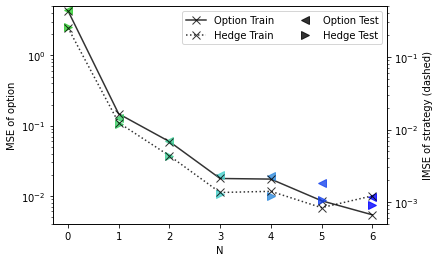

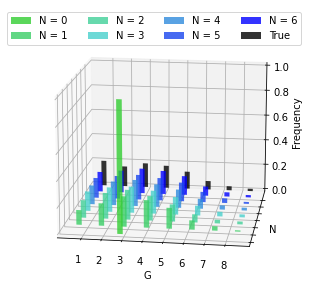

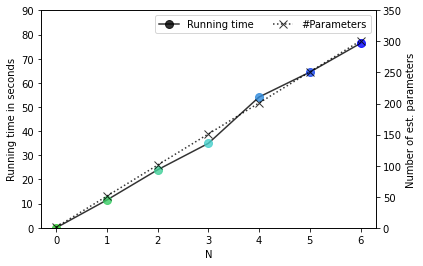

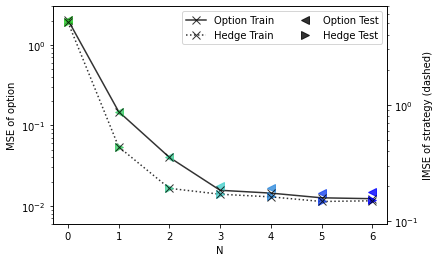

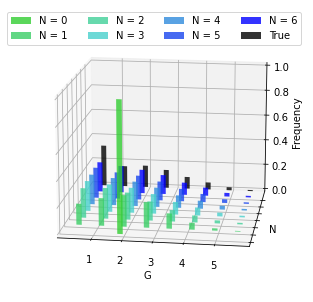

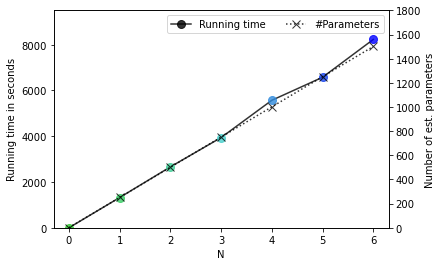

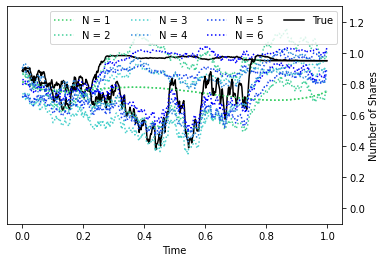

In the following numerical experiments111All numerical experiments have been implemented in Python on an average laptop (Lenovo ThinkPad X13 Gen2a with Processor AMD Ryzen 7 PRO 5850U and Radeon Graphics, 1901 Mhz, 8 Cores, 16 Logical Processors). The code can be found under the following link: https://github.com/psc25/ChaoticHedging, we use random neural networks to reduce the training time, which allows us to learn the hedging strategy of a financial derivative within few minutes (see Figure 1(c), Figure 2(c), and Figure 3(c)). Unless otherwise specified, we generate sample paths of discretized over an equidistant time grid , with , which are split up into / for training and testing. In addition, we choose and as different orders, where the random neural networks are of size with the sigmoid activation function .

Moreover, by using Malliavin calculus (see [Nualart, 2006]) or the affine structure with Fourier techniques (see [Duffie et al., 2000] and [Carr and Madan, 1999]), we compute the true hedging strategy of the financial derivative . This allows us to compare the hedging strategy of the approximation with the true hedging strategy of .

3.1. European Option with Brownian Motion

In the first example (see Figure 1), we consider a one-dimensional Brownian motion and learn for the European call option

| (18) |

with strike price . By the Clark-Ocone formula in [Clark, 1970] and [Ocone, 1984] (see also [Di Nunno et al., 2008, Theorem 4.1]), the true hedging strategy of is given by , for all , where denotes the Malliavian derivative of (see [Di Nunno et al., 2008, Definition 3.1] and [Nualart, 2006, Definition 1.2.1]). Using the chain rule of the Malliavin derivative in [Nualart, 2006, Proposition 1.2.4], it follows for every that and thus

| (19) |

where denotes the cumulative distribution function of the standard normal distribution.

3.2. Asian Option in Local Volatility Model

In the second example (see Figure 2), we consider an Asian option in the CEV model (see [Cox, 1975]), where the price process with follows

for , with , , and . Hereby, is a diffusion process with drift and diffusion coefficient of linear growth. Then, we learn the Asian option

| (20) |

with strike price . By using similar Fourier arguments as in [Carr and Madan, 1999], we have

| (21) |

where and denotes the characteristic function of under the unique ELMM . Hence, the true hedging strategy is obtained by taking the derivative in (21) with respect to and applying the fractional fast Fourier transform (FFT) in [Chourdakis, 2005] to compute the integrals. Hereby, the characteristic function is calculated with the affine transform formula in [Duffie et al., 2000, Section 2.2] and the time-integral extension in [Keller-Ressel, 2009, Section 4.3].

3.3. Basket Option in Affine Model

In the third example (see Figure 3), we learn a Basket option written on stocks with Brownian motions. More precisely, we consider for the affine SDE

for , where and , , for some , . The parameters are sampled according to , , , and , for all . In this case, is a diffusion process with drift and diffusion coefficient of linear growth. Then, we learn the Basket option

| (22) |

with strike price and . By using similar Fourier arguments as in [Carr and Madan, 1999], we conclude that

| (23) |

where and , for and an ELMM. Hence, the true hedging strategy is given as the gradient of (23) with respect to , where the integrals are computed as in Section 3.2. Now, the sample size and the size of the random neural networks are increased to and , respectively.

(a) Learning performance

(b) Payoff distribution on test set

(c) Running time and number of parameters

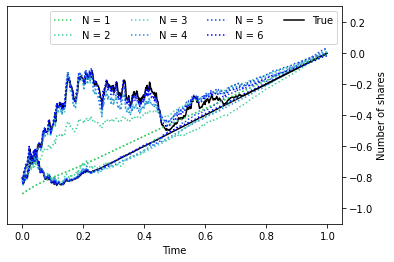

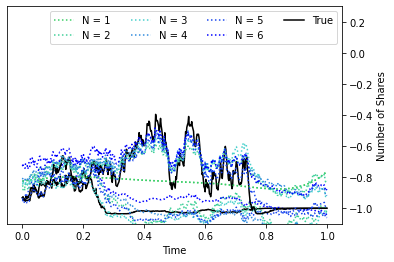

(d1) and for two samples of test set

(d2) and for two samples of test set

![[Uncaptioned image]](/html/2209.10166/assets/python/itint_rand_am_hedgetest_3.png)

(d3) and for two samples of test set

![[Uncaptioned image]](/html/2209.10166/assets/python/itint_rand_am_hedgetest_4.png)

(d4) and for two samples of test set

![[Uncaptioned image]](/html/2209.10166/assets/python/itint_rand_am_hedgetest_5.png)

(d5) and for two samples of test set

![[Uncaptioned image]](/html/2209.10166/assets/python/itint_rand_am_hedgetest_6.png)

(d6) and for two samples of test set

![[Uncaptioned image]](/html/2209.10166/assets/python/itint_rand_am_hedgetest_7.png)

(d7) and for two samples of test set

![[Uncaptioned image]](/html/2209.10166/assets/python/itint_rand_am_hedgetest_8.png)

(d8) and for two samples of test set

![[Uncaptioned image]](/html/2209.10166/assets/python/itint_rand_am_hedgetest_9.png)

(d9) and for two samples of test set

![[Uncaptioned image]](/html/2209.10166/assets/python/itint_rand_am_hedgetest_10.png)

(d10) and for two samples of test set

4. Proofs

In this chapter, we provide all the proofs of the previous results in chronological order.

4.1. Proof of Results in Section 2.1: Stochastic Integral and Quadratic Variation

Proof of Lemma 2.4.

For every , we define the stopping time . Moreover, we fix some and in the following. By applying Ito’s formula with respect to the smooth function , it follows for every , -a.s., that

| (24) | ||||

Hereby, we observe by applying the Burkholder-Davis-Gundy inequality (with constant ) and using the linear growth condition of that

which shows that is a martingale with , for all . Hence, by taking the expectation in (24), and using the Cauchy-Schwarz inequality, Fubini’s theorem, the linear growth condition of and , the inequalities , for any , for any , , and Jensen’s inequality, it follows for every that

| (25) | ||||

where is continuous with , for all . From this, we define with , for all . By the inverse function theorem, there exists a continuously differentiable inverse , with , for all , implying that is strictly increasing. Moreover, since for all , as , and for all , as , we observe for every that

which shows that , for all . Then, by using (25) together with the non-linear Gronwall inequality in [Bihari, 1956, Equation 6-8] and that , it follows for every , , and that

where the right hand-side does not depend on . Since converges -a.s. to , as , Fatou’s lemma implies for every and that

which shows the inequality in (4).

In order to show (5), fix some . Then, by using (4), Stirling’s inequality, i.e. for any , and that , it follows that

Hence, by the root test, converges absolutely. Similarly, by using (4), Stirling’s inequality, i.e. for any , and that , it follows that

Hence, by the root test, converges absolutely. Finally, by using the monotone convergence theorem, Jensen’s inequality, and (4) with implying that , it follows for every that

which completes the proof. ∎

Proof of Lemma 2.5.

First, we use the linear growth of and , the inequalities and for any and , and Lemma 2.4 to conclude that

| (26) | ||||

Now, we fix some . By [Fraňková, 1991, Lemma 1.5], is a uniform limit of -valued piecewise constant functions. Since the latter are -measurable, we conclude that is also -measurable. Moreover, by using [Fraňková, 1991, Lemma 1.7], it follows that is bounded, which implies that . Hence, by using Jensen’s inequality for the time integral of a convex function, Jensen’s inequality for the expectation of a concave function (if ) or Jensen’s inequality for the time integral of a convex function (if ), Fubini’s theorem, and (26), we conclude that

which completes the proof. ∎

Proof of Lemma 2.8.

For two functions and some , it follows that and . Hence, we only need to show that is a norm. By definition, is absolutely homogeneous, and since we consider as quotient space with respect to the kernel of , the norm is positive definite. In order to show the triangle inequality, let . Then, by applying the Cauchy-Schwarz inequality twice, it holds -a.s. that

Hence, by using for any , it follows that

Finally, by applying Minkowski’s inequality, we conclude that

which completes the proof. ∎

Proof of Lemma 2.11.

Lemma 4.1.

Let be a diffusion process with coefficients of linear growth with constant , and let . Then, it holds for every that

| (27a) | ||||

| (27b) | ||||

where does not depend on . Moreover, for every with , we have for every that

| (28) |

In addition, for every with , we have for every that

| (29) |

Proof.

In order to show (27a), we first define the sequence of stopping times by , for . Now, we fix some and . Then, by applying Ito’s formula on the smooth function , it follows for every , -a.s., that

| (30) | ||||

Hereby, we observe by applying the Burkholder-Davis-Gundy inequality (with constant ) and using the linear growth condition of that

which shows that is a martingale with , for all . Hence, by taking the expectation in (30), using the linear growth condition of and , Hölder’s inequality (with exponents and , respectively) together with Jensen’s inequality, the inequalities and for any , Lemma 2.4, the inequalities and for any , and defining , it follows for every that

| (31) | ||||

where is continuous with , for all . From this, we define with , for all . By the inverse function theorem, there exists a continuously differentiable inverse function with , for all , implying that is strictly increasing. Moreover, since , for all , we observe for every that

which shows that , for all . Then, by using (31) together with the non-linear Gronwall inequality in [Bihari, 1956, Equation 6-8] and that , it follows for every , , and that

where the right-hand side does not depend on . As converges -a.s. to , as , Fatou’s lemma implies for every and that

which shows the inequality in (27a).

In order to show (27b), let and define for every the stopping time . Then, by Ito’s formula, it follows for every , -a.s., that . Moreover, by using the linear growth condition of , Hölder’s inequality (with exponents ) together with Jensen’s inequality, that for any , Lemma 2.4, and for any , it holds for every that

| (32) | ||||

where is continuous with , for all . From this, we define satisfying , for all . By the inverse function theorem, there exists a continuously differentiable inverse with , for all , implying that is strictly increasing. Moreover, for every , we have

which shows that , for all . Then, by using (32) together with the non-linear Gronwall inequality in [Bihari, 1956, Equation 6-8] and that , it follows for every , , and that

where the right-hand side does not depend on . Since converges -a.s. to , as , Fatou’s lemma implies for every and that

which proves the inequality in (27b).

In order to show (28), let with . Then, by using (27a) and Stirling’s inequality, i.e. for any , it follows that

Hence, by the root test, converges absolutely. Similarly, by using (27a), Stirling’s inequality, i.e. for any , and that , it follows that

Hence, by the root test, converges absolutely. Thus, by using the monotone convergence theorem, Jensen’s inequality, and (27a) with implying that , it follows for every that

On the other hand, for (29), let with . Then, by using (27b) and Stirling’s inequality, i.e. for any , it follows that

Hence, by the root test, converges absolutely. Thus, the monotone convergence theorem, Jensen’s inequality, and (27b) with implying that , shows for every that

which completes the proof. ∎

4.2. Proof of Results in Section 2.2

4.2.1. Auxiliary Results: Time-Space Harmonic Hermite Polynomials

In the following, we show some properties of the time-space harmonic Hermite polynomials introduced in Definition 2.12.

Lemma 4.2.

The time-space harmonic Hermite polynomials satisfy for every and that

| (33a) | ||||

| (33b) | ||||

| (33c) | ||||

(resp. ). Moreover, it holds for every that

| (34a) | ||||

| (34b) | ||||

Remark 4.3.

Proof of Lemma 4.2.

In order to show (33a), we use the chain rule and [Abramowitz and Stegun, 1970, Equation 22.8.8], i.e. for any , to conclude for every that

For (33b), we apply the product rule, use again for any , and the recurrence relation in [Abramowitz and Stegun, 1970, Equation 22.7.14], i.e. for any , to conclude for every that

Moreover, implies for every that

which proves (33c). For (34a), we define the function , for which (8) implies . Then, Taylor’s theorem around shows for every that

which yields . Hence, for every , we have

On the other hand, for (34b), we use the explicit expression of in [Abramowitz and Stegun, 1970, Equation 22.3.11] given by , for all and , where , for . Then, by using the definition of the time-space harmonic Hermite polynomials in Definition 2.12, it follows for every that

| (35) |

Moreover, we observe that if and only if , for all . Hence, by using (35) and reordering the sums, we conclude for every and that

Finally, by taking the limit , it follows that

which completes the proof. ∎

The following lemma is a modification of [Jamshidian, 2005, Proposition 5.1] to this setting of , with , where we show that polynomial increments of are dense in , which was similarly applied in [Nualart and Schoutens, 2000, Proposition 2] for Lévy processes.

Lemma 4.4.

Let be a diffusion process with coefficients of linear growth, and let . Then,

is dense in with , where .

Proof.

Let such that with convention . Now, we assume by contradiction that is not dense in . Then, there exists by Hahn-Banach a non-zero continuous linear functional , which vanishes on . By Riesz representation, can be represented with some such that , for all , which implies that , for all . Thus, it suffices to show that , which contradicts that is non-zero.

Since the -augmentation of is equal to , we have

where . Then, it follows by [Brézis, 2011, Theorem 4.12] that is dense in , where denotes the space of continuous functions with compact support. By mollification, every can be uniformly approximated by smooth functions, which implies that is dense in (see [Brézis, 2011, Corollary 4.23]), where denotes the space of smooth functions with compact support (see [Rudin, 1991, Example I.1.46]). Thus, it suffices to show that for all , , and .

Now, for every fixed and , we define the distribution and let be its Fourier transform in the sense of distributions (see [Rudin, 1991, Definition 7.14]), where denotes the Fourier transform of . Then, by Fubini’s theorem, it follows for every that

| (36) |

where we define the function . Next, we show that is constant. For this purpose, we apply Hölder’s inequality, the Cauchy-Schwarz inequality, and the generalized Hölder inequality (with exponents ) to conclude for every that

where , for . Then, by using Lemma 2.4, there exists some such that , which implies that , for all . From this, we see that the function is holomorphic on . Hence, the restriction is real analytic and satisfies

for all and . Since is analytic, is hence constant equal to , which implies together with (36) that , for all . Then, is by [Rudin, 1991, Example II.7.16] a scalar multiple of the Dirac delta, i.e. , for all . However, by choosing , we have , which implies , for all . Finally, since and were chosen arbitrarily, it follows that for all , , and , which implies that and completes the proof. ∎

Proof of Lemma 2.16.

Let . For , this follows immediately. For , we use the explicit expression of the time-space harmonic Hermite polynomials derived in (35) to conclude for every that

where , for . By using this, Minkowski’s inequality, and Lemma 2.11, it follows for every that

Hence, by definition of in (9), we conclude that . ∎

4.2.2. Proof of Theorem 2.17

Proof of Theorem 2.17.

Fix some and let such that with convention . Now, we assume by contradiction that is not dense in . Then, there exists by Hahn-Banach a non-zero continuous linear functional vanishing on . By Riesz representation, can be represented with some such that , for all , and thus , for all . Therefore, it suffices to show that , which contradicts the assumption that is non-zero.

Now, we fix some , , , and , and define the tuple

where . Moreover, we choose some with and , where the constant was introduced in Lemma 4.1. In addition, we define the subsets and be of . Then, we consider for every fixed the simple function defined by

for , where denotes the -th unit vector of . Since , Lemma 2.5 implies that , for all . Moreover, we have

where . Similarly, for with , we observe that

where . In addition, by using the definition of in (9), it follows that , which implies that , for all . Hence, by defining , we conclude for every that

| (37) |

Hereby, the polynomial converges by Lemma 4.2 pointwise to the function , as , and for every and , it holds that

| (38) |

Moreover, implies and . Hence, we can apply Lemma 4.1 to conclude that

| (39) |

Then, by using the generalized Hölder inequality (with exponents ), it follows that

Moreover, it holds by (38) that , -a.s., for all , where the latter is integrable. Thus, we can apply dominated convergence on (37) to conclude that

| (40) |

From this, we define the function , where is a random function. Then, it follows from (40) that , for all .

Now, we show by induction on that the -th partial derivative of with respect to each but different direction , for , evaluated at , is equal to the expected -th partial derivative of with respect to each but different direction, evaluated at , which means that we can interchange expectation and partial derivatives such that

| (41) | ||||

In order to prove (41), we choose some with , and define by , which implies that , and thus . Then, we conclude by the generalized Hölder inequality (with exponents ), the inequalities and for any , that together with (39), and Lemma 4.1 that

where . Hence, the family of random variables

| (42) |

is by de la Vallée-Poussin’s theorem in [Klenke, 2014, Theorem 6.19] uniformly integrable. Since is continuous on , we can apply Vitali’s convergence to conclude for every and every sequence with that , i.e. for every and there exists with . This implies that

| (43) |

for all and sequences with .

Now, we prove the induction initialization that is continuous on and , for all . To this end, we apply the fundamental theorem of calculus and use Fubini’s theorem to conclude that

for all and such that . This and (43) imply for every and every sequence with that

| (44) | ||||

Since is continuous on and (42) is uniformy integrable, Vitali’s convergence theorem implies for every and every sequence with that

| (45) | ||||

This and (44) show the induction initialization that , for all , and is continuous on .

Next, we prove the induction step, i.e. if for some , the function is continuous on and for every , it holds that

| (46) |

then is also continuous on and (46) still holds true with replacing . To see this, we use the induction hypothesis, apply the fundamental theorem of calculus, and Fubini’s theorem such that

for all and such that . Using this and the same arguments as in (44) and (45), we conclude that

for all and sequences with . This together with (45) establishes the induction step such that (46) is true with instead of .

Finally, by taking in (46) and using that satisfies , for all , we have

Moreover, it holds that . Hence, by using that the linear span of polynomial increments of the form , for , , , and , is by Lemma 4.4 dense in , it follows that . This contradicts however the assumption that is non-zero, which shows that is dense in . ∎

4.3. Proof of Results in Section 2.3

4.3.1. Auxiliary Results: Iterated Integrals

Proof of Lemma 2.22.

In order to show that is linear, we define the multilinear map . Then, there exists by the universal property of the tensor product (see [Ryan, 2002, Proposition 1.4]) a linear map such that , for all . However, since , for all , we have on , which shows that is also linear.

For the second part, by linearity of , it suffices to show that , -a.s., for each representation of . For some fixed , we define the multilinear form . Then, it follows for every representation of that

Since the value of is independent of the representation of , it follows by choosing that . However, because was chosen arbitrarily, we obtain , -a.s., which completes the proof. ∎

Proof of Lemma 2.23.

For , (11) follows from Lemma 2.11 and since , for all . For , let and define . For fixed , Hölder’s inequality (with exponents ) implies that

| (47) | ||||

Similarly, by the Burkholder-Davis-Gundy inequality (with exponent and constant ) and Hölder’s inequality (with exponents ), it follows that

| (48) | ||||

Hence, by using Minkowski’s inequality as well as (47) and (48), it follows for every that

| (49) | ||||

By applying this argument iteratively backwards for , and using that , for all , it follows with the help of Lemma 2.11 that

| (50) | ||||

For the general case of , we fix and assume that is a representation of such that . Then, it follows by using Minkowski’s inequality and (50) that

Since was chosen arbitrarily, we obtain the conclusion in (11). ∎

Proof of Lemma 2.24.

We follow the proof of [Segall and Kailath, 1976, Theorem 1]. For , we define for every the process , with and . First, we show the Kailath-Segall identity, i.e. it holds for every and , -a.s., that

| (51) |

which is by definition true for . In order to show the induction step, we assume that (51) holds true for with . Then, by applying Ito’s formula on the function twice, it follows for every , -a.s., that

Moreover, by using the induction hypothesis , and the fact that , we conclude for every , -a.s., that

Hence, by adding on both sides, the Kailath-Segall identity in (51) follows for each . Moreover, we recall that the rescaled time-space harmonic Hermite polynomials satisfy by Lemma 4.2 the recurrence relation

for all , with and . Therefore, by choosing and , we see that satisfies the same recurrence as in (51), which implies the desired result. ∎

4.3.2. Proof of Theorem 2.26

Proof of Theorem 2.26.

As is by Theorem 2.17 dense in , there exists some of the form , with and , for all , such that

| (52) |

By Definition 2.15, every can be written as linear combination of random variables of the form with , which implies that , for some , and . From this, we define for every the function . Then, Lemma 2.24 and linearity of show

-a.s., for all . This proves together with (52) the conclusion in (12). ∎

4.4. Proof of Results in Section 2.4

4.4.1. Auxiliary Results: Iterated Integral is a martingale under ELMM

Lemma 4.5.

Let be a diffusion process, let with , and assume that there exists an ELMM for with density . Then, for every and , the process is a martingale under .

Proof.

First, we observe for some that is a local martingale under . Moreover, by applying Hölder’s inequality and Lemma 2.23, we conclude that

which shows that is a true martingale under . ∎

4.4.2. Proof of Theorem 2.28 and Corollary 2.29

Proof of Theorem 2.28.

For every , we apply Theorem 2.26 with to obtain some , and , for , such that

| (53) |

Hereby, we can write , for some , , and . Now, for every , , and , we define by , for and , which is -adapted and left-continuous, thus -predictable and locally bounded. Then, by Minkowski’s inequality, Hölder’s inequality (with exponents ), iteratively applying (49) as in the proof of Lemma 2.23, and using Lemma 2.11, it follows that

which shows that , and thus , for all , , and . Hence, by using that is a vector space, we conclude that , for all .

Now, let be the ELMM with . Then, every process is by Lemma 4.5 a martingale under , which implies that . Hence, by Minkowki’s inequality, Hölder’s inequality, and (53), it follows for every that

Hence, converges to in , as . However, since is by Lemma 2.27 closed in , there exists some satisfying (14). ∎

Proof of Corollary 2.29.

Since is a -local martingale, is an ELMM with trivial density for with . Moreover, by the Burkholder-Davis-Gundy, is for every a martingale. Then, by the lower Burkholder-Davis-Gundy inequality (with constant ) and Doob’s inequality (with constant ), it follows for every that

which shows that the condition in (13) is satisfied. Hence, the assumptions of Theorem 2.28 are fulfilled, which immediately yields the representation in (14). ∎

4.5. Proof of Results in Section 2.5

4.5.1. Auxiliary Results: Universal Approximation

Lemma 4.6.

Let and . Then, it follows for every that and that

Proof.

Let for some . Since is -measurable, it follows for every that is -measurable. Moreover, we observe that

which shows that for all . In addition, by using the inequality for any and , it follows that

which completes the proof. ∎

Proposition 4.7.

Let be a diffusion process with coefficients of linear growth, let be activating, and let . Then, is dense in , i.e. for every and there exists some such that .

Proof.

Fix some and let for some . Then, by using that is defined as (equivalence classes of) LCRL functions in , it follows from Lemma 2.5 that and that . Hence, by using Lemma 4.6, we conclude that for all . Moreover, by applying [Rudin, 1987, Theorem 3.14] to every , , there exists some such that

| (54) |

where is the constant of Lemma 2.5. Now, for every , we use that is activating, i.e. that is dense in with respect to the uniform topology to conclude that there exists some such that

| (55) |

From this, we define the -valued neural network . Hence, by using Lemma 2.5 (with constant ), Lemma 4.6 (with ), Minkowski’s inequality, (54), and (55), it follows that

Since and were chosen arbitrarily, it follows that is dense in . ∎

Proof of Proposition 2.38.

Fix some and let with representation , for and , such that

| (56) |

which exists as is a representation of . Then, for every , we apply Proposition 4.7 to obtain some such that

which implies that . Using this, the telescoping sum , the triangle inequality, and Lemma 2.18, it follows that

| (57) | ||||

Finally, by defining , it follows by combining (56) and (57) with the triangle inequality that

Since and were chosen arbitrarily, is dense in . ∎

4.5.2. Proof of Theorem 2.39

Proof of Theorem 2.39.

Fix some and let for some . By Theorem 2.26, there exists and a sequence , with for all , such that

| (58) |

Moreover, for every , we obtain by applying Proposition 2.38 some such that , where was introduced in Lemma 2.23. From this, we define with . Hence, by using (58), Minkowksi’s inequality, and the Burkholder-Davis-Gundy type of inequality in Lemma 2.23, it follows that

which completes the proof. ∎

4.5.3. Auxiliary Results: Random Universal Approximation

Proof of Proposition 2.42.

First, we observe that is as -completion of a Banach space, which we claim to be separable. Indeed, by the Stone-Weierstrass theorem, the countable set is dense in with respect to the uniform topology. Hence, by following the arguments in the proof of Proposition 4.7, we can use to approximate the components of any LCRL function in with respect to . Then, by similar arguments as in Proposition 2.38, we conclude that the countable set

is dense in .

Now, we observe that random tensor-valued neural networks are linear combinations of maps of the form , with some and

where denotes the function . Hence, it suffices to show that , for some fixed and for all , to obtain the conclusion. By the definition of the Bochner space in [Hytönen et al., 2016, Definition 1.2.15], this means that we need to prove that the map is -strongly measurable (see [Hytönen et al., 2016, Definition 1.1.14]) and satisfies , for all .

In order to prove that the map is -strongly measurable, we define the sequence of -valued random variables by

with

for and . Hence, by multilinearity of the tensor product, the map is a -simple function (see [Hytönen et al., 2016, Definition 1.1.13]), for all . Now, we show that converges pointwise to with respect to . For this purpose, we fix some and . Moreover, we introduce the notation and define the constant . Then, it follows for every , and that

In addition, we observe for every and that

| (59) |

which shows that for all and . Similarly, it follows for every and that

| (60) | ||||

which shows that for all and . Moreover, since is continuous, thus uniformly continuous on , there exists some such that for every with , it holds that

| (61) |

where is the constant of Lemma 2.5. From this, we choose some with . Then, it follows for every that

Hence, by using (61) together with (59) and (60), it follows for every that

Thus, by using this, Lemma 2.5 (with constant ), and Lemma 4.6 (with ), we conclude for every , , and that

Since was chosen arbitrarily, it follows that converges pointwise to with respect to , as . Hence, for every and every there exists some such that for every , it holds that

which implies that , for all . Then, by using the telescoping sum , the triangle inequality, and Lemma 2.18, it follows for every that

| (62) | ||||

Since was chosen arbitrarily, we conclude that converges pointwise to , as , which shows that is -strongly measurable.

Proposition 4.8.

Let be a diffusion process with coefficients of linear growth, let be activating, and let for some . Then, for every and there exists some such that .

Proof.

Fix some and , and let for some . Since is activating, there exists by Proposition 4.7 a deterministic neural network of the form , with , , , and such that

| (63) |

Hereby, we can assume without loss of generality that for all . Now, we define for every and a random neural network by

| (64) |

with

where and , where with

which implies for any , and where

since for any by Assumption 2.40. Note that and implies that for any and . Moreover, for every and , the i.i.d. sequence of -valued random variables in (64) belongs by Proposition 2.42 to , where (see also Remark 2.19).

Now, we show that there exists some such that for every the expectation of the random neural networks defined in (64) is -close to the function with respect to the -norm. For this purpose, we define for every , , and the closed subsets

satisfying for all , and . Since is continuous, thus uniformly continuous on the compact set , there exists some such that for every with , it holds that

| (65) |

where is the constant of Lemma 2.5. Now, we choose some such that . Then, it follows for every , , , and that

Hence, by combining this with (65), it follows for every and that

Thus, by using [Hytönen et al., 2016, Proposition 1.2.2], Lemma 2.5 (with constant ) and Lemma 4.6 (with ), that , that and that for any and , it follows for every that

| (66) | ||||

This shows that for every the expectation is indeed -close to the function in the -norm.

Now, we approximate the constant random variable by the average of the i.i.d. sequence defined in (64). More precisely, for every , we apply the strong law of large numbers for Banach space-valued random variables in [Hytönen et al., 2016, Theorem 3.3.10] to conclude for every that

| (67) |

In order to generalize the convergence to , we define for every the sequence of non-negative random variables by , . Then, by using the triangle inequality of , Minkowski’s inequality, [Hytönen et al., 2016, Proposition 1.2.2], that in (64) is identically distributed, that for any by Proposition 2.42, it follows for every and that

Since the right-hand side is finite and does not depend on , we conclude for every that . Hence, for every , the family of random variables is by de la Vallée-Poussin’s theorem in [Klenke, 2014, Theorem 6.19] uniformly integrable. Then, by using (67), i.e. that , -a.s., as , together with Vitali’s convergence theorem, it follows for every that indeed

From this, we conclude that for every there exists some such that

| (68) |

Finally, by defining , it follows by combining (63), (66), and (68) with the triangle inequality and Minkowski’s inequality that

which completes the proof. ∎

Proof of Proposition 2.43.

Fix some and let with representation for some , , and , such that

| (69) |

which exists as is a representation of . Then, for every , we apply Proposition 4.8 to obtain some such that

| (70) |

Thus, by applying the triangle inequality and Minkwoski’s inequality, we conclude that

| (71) | ||||

Hence, by using the telescoping sum , Minkowski’s inequality, Lemma 2.18, Hölder’s inequality, Jensen’s inequality, (71), and (70), it follows for every that

| (72) | ||||

Finally, by defining , it follows by combining (69) and (72) with the triangle inequality and Minkowski’s inequality that

which completes the proof. ∎

4.5.4. Proof of Corollary 2.44 and Theorem 2.45

Proof of Corollary 2.44.

Fix some and , and let for some . By Theorem 2.26, there exists and a sequence , with for all , such that

| (73) |

Then, for every , we apply Proposition 2.43 to obtain some with

| (74) |

where was introduced in Lemma 2.23. From this, we define the map with and show that . Indeed, since is by Proposition 2.42 -strongly measurable and since is by Lemma 2.22 and Lemma 2.23 linear and bounded, thus continuous and therefore measurable, it follows by [Hytönen et al., 2016, Corollary 1.1.11] that is also -strongly measurable. Moreover, by applying Minkowski’s inequality and using Lemma 2.23, we conclude that

which shows that indeed . Finally, by combining (73) and (74) with Minkowksi’s inequality, and using Lemma 2.23, it follows that

which completes the proof. ∎

Proof of Theorem 2.45.

First, we derive for every and the hedging strategy of . For this purpose, we use Lemma 2.24, Ito’s formula applied on , Lemma 4.2 (i.e. the identities (33a), (33b), and (33c)), that -a.s., and that -a.s., to conclude -a.s. that

| (75) | ||||

Now, in order to show (16), we conclude by using and (75) that, -a.s.,

which completes the proof. ∎

References

- [Abramowitz and Stegun, 1970] Abramowitz, M. and Stegun, I. A. (1970). Handbook of mathematical functions with formulas, graphs, and mathematical tables. Applied mathematics series / National Bureau of Standards 55, Print. 9. Dover, New York, 9th edition.

- [Acciaio et al., 2016] Acciaio, B., Beiglböck, M., Penkner, F., and Schachermayer, W. (2016). A model-free version of the fundamental theorem of asset pricing and the super-replication theorem. Mathematical Finance, 26(2):233–251.

- [Acciaio et al., 2022] Acciaio, B., Kratsios, A., and Pammer, G. (2022). Designing universal causal deep learning models: The geometric (hyper)transformer. Preprint arXiv:2201.13094.

- [Altay and Schmock, 2016] Altay, S. and Schmock, U. (2016). Lecture notes on the Yamada-Watanabe condition for the pathwise uniqueness of certain stochastic differential equations. Lecture Notes, TU Vienna.

- [Benth et al., 2022] Benth, F. E., Detering, N., and Galimberti, L. (2022). Neural networks in Fréchet spaces. Annals of Mathematics and Artificial Intelligence.

- [Benth and Lavagnini, 2021] Benth, F. E. and Lavagnini, S. (2021). Correlators of polynomial processes. SIAM Journal on Financial Mathematics, 12(4):1374–1415.

- [Bihari, 1956] Bihari, I. (1956). A generalization of a lemma of Bellman and its application to uniqueness problems of differential equations. Acta Mathematica Academiae Scientiarum Hungarica, 7:81–94.

- [Bölcskei et al., 2019] Bölcskei, H., Grohs, P., Kutyniok, G., and Petersen, P. (2019). Optimal approximation with sparsely connected deep neural networks. SIAM Journal on Mathematics of Data Science, 1:8–45.

- [Brézis, 2011] Brézis, H. (2011). Functional Analysis, Sobolev Spaces and Partial Differential Equations. Universitext. Springer, New York.

- [Bühler et al., 2019] Bühler, H., Gonon, L., Teichmann, J., and Wood, B. (2019). Deep hedging. Quantitative Finance, 19(8):1271–1291.

- [Carlen and Kree, 1991] Carlen, E. and Kree, P. (1991). -estimates on iterated stochastic integrals. The Annals of Probability, 19(1):354–368.

- [Carmona, 2009] Carmona, R. (2009). Indifference Pricing: Theory and Applications. Princeton University Press.

- [Carr and Madan, 1999] Carr, P. and Madan, D. B. (1999). Option valuation using the fast Fourier transform. Journal of Computational Finance, 2:61–73.

- [Cartea et al., 2022] Cartea, Á., Pérez Arribas, I., and Sánchez-Betancourt, L. (2022). Double-execution strategies using path signatures. SIAM Journal on Financial Mathematics, 13(4):1379–1417.

- [Cheridito et al., 2005] Cheridito, P., Soner, H. M., and Touzi, N. (2005). The multi-dimensional super-replication problem under gamma constraints. Annales de l’Institut Henri Poincaré C, Analyse non linéaire, 22(5):633–666.

- [Chourdakis, 2005] Chourdakis, K. (2005). Option pricing using the fractional FFT. Journal of Computational Finance, 8(2):1–18.

- [Clark, 1970] Clark, J. M. (1970). The representation of functionals of Brownian motion by stochastic integrals. The Annals of Mathematical Statistics, 41(4):1282–1295.

- [Cox, 1975] Cox, J. C. (1975). Notes on option pricing I: Constant elasticity of diffusions. Unpublished Draft, Stanford University.

- [Cuchiero, 2011] Cuchiero, C. (2011). Affine and polynomial processes. PhD thesis, ETH Zurich.

- [Cuchiero et al., 2022a] Cuchiero, C., Gazzani, G., and Svaluto-Ferro, S. (2022a). Signature-based models: theory and practice. Preprint arXiv:2207.13136.

- [Cuchiero et al., 2020] Cuchiero, C., Khosrawi, W., and Teichmann, J. (2020). A generative adversarial network approach to calibration of local stochastic volatility models. Risks, 8(4).

- [Cuchiero et al., 2022b] Cuchiero, C., Primavera, F., and Svaluto-Ferro, S. (2022b). Universal approximation theorems for continuous functions of càdlàg paths and Lévy-type signature models. Preprint arXiv:2208.02293.

- [Cuchiero et al., 2023] Cuchiero, C., Schmocker, P., and Teichmann, J. (2023). Global universal approximation of functional input maps on weighted spaces. Working Paper.

- [Cvitanić et al., 1999] Cvitanić, J., Pham, H., and Touzi, N. (1999). Super-replication in stochastic volatility models under portfolio constraints. Journal of Applied Probability, 36(2):523–545.

- [Cybenko, 1989] Cybenko, G. (1989). Approximation by superpositions of a sigmoidal function. Mathematics of Control, Signals and Systems, 2(4):303–314.

- [Dambis, 1965] Dambis, K. E. (1965). On the decomposition of continuous submartingales. Theory of Probability & Its Applications, 10(3):401–410.

- [Davis, 2005] Davis, M. H. (2005). Martingale representation and all that. In Abed, E., editor, Advances in Control, Communication Networks, and Transportation Systems: In Honor of Pravin Varaiya, pages 57–68. Birkhäuser, Boston, MA.

- [Delbaen et al., 1997] Delbaen, F., Monat, P., Schachermayer, W., Schweizer, M., and Stricker, C. (1997). Weighted norm inequalities and hedging in incomplete markets. Finance and Stochastics, 1:181–227.

- [Di Nunno et al., 2008] Di Nunno, G., Øksendal, B., and Proske, F. (2008). Malliavin Calculus for Lévy Processes with Applications to Finance. Springer Science + Business Media, Berlin Heidelberg.

- [Di Tella and Engelbert, 2016a] Di Tella, P. and Engelbert, H.-J. (2016a). The chaotic representation property of compensated-covariation stable families of martingales. Annals of Probability, 44(6):3965–4005.

- [Di Tella and Engelbert, 2016b] Di Tella, P. and Engelbert, H.-J. (2016b). The predictable representation property of compensated-covariation stable families of martingales. Theory of Probability & Its Applications, 60(1):19–44.

- [Dubins and Schwarz, 1965] Dubins, L. E. and Schwarz, G. (1965). On continuous martingales. Proceedings of the National Academy of Sciences of the United States of America, 53(5):913–916.

- [Dudley, 1977] Dudley, R. M. (1977). Wiener functionals as Ito integrals. The Annals of Probability, 5(1):140–141.

- [Duffie et al., 2000] Duffie, D., Pan, J., and Singleton, K. (2000). Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 68(6):1343–1376.

- [Duffie and Richardson, 1991] Duffie, D. and Richardson, H. R. (1991). Mean-variance hedging in continuous time. The Annals of Applied Probability, 1(1):1–15.

- [Eckstein et al., 2021] Eckstein, S., Guo, G., Lim, T., and Obłój, J. (2021). Robust pricing and hedging of options on multiple assets and its numerics. SIAM Journal on Financial Mathematics, 12(1):158–188.

- [Eckstein et al., 2020] Eckstein, S., Kupper, M., and Pohl, M. (2020). Robust risk aggregation with neural networks. Mathematical Finance, 30(4):1229–1272.

- [El Karoui and Quenez, 1995] El Karoui, N. and Quenez, M.-C. (1995). Dynamic programming and pricing of contingent claims in an incomplete market. SIAM Journal on Control and Optimization, 33(1):29–66.

- [Émery, 1989] Émery, M. (1989). On the Azéma martingales. Séminaire de probabilités de Strasbourg, 23:66–87.

- [Filipović and Larsson, 2016] Filipović, D. and Larsson, M. (2016). Polynomial diffusions and applications in finance. Finance and Stochastics, 20(4):931–972.

- [Föllmer and Schweizer, 1991] Föllmer, H. and Schweizer, M. (1991). Hedging of contingent claims under incomplete information. In Davis, M. H. A. and Elliott, R. J., editors, Applied Stochastic Analysis, volume 5 of Stochastics Monographs, pages 389–414. Gordon and Breach, London/New York.

- [Fraňková, 1991] Fraňková, D. (1991). Regulated functions. Mathematica Bohemica, 116(1):20–59.

- [Gonon, 2022] Gonon, L. (2022). Random feature neural networks learn Black-Scholes type PDEs without curse of dimensionality. Preprint arXiv:2106.08900.

- [Gonon et al., 2022] Gonon, L., Grigoryeva, L., and Ortega, J.-P. (2022). Approximation bounds for random neural networks and reservoir systems. Preprint arXiv:2002.05933, Forthcoming in: Annals of Applied Probability.

- [Goodfellow et al., 2016] Goodfellow, I., Bengio, Y., and Courville, A. (2016). Deep Learning. MIT Press.

- [Grandits and Krawczyk, 1998] Grandits, P. and Krawczyk, L. (1998). Closedness of some spaces of stochastic integrals. Séminaire de probabilités de Strasbourg, 32:73–85.

- [Grigoryeva and Ortega, 2018] Grigoryeva, L. and Ortega, J.-P. (2018). Echo state networks are universal. Neural Networks, 108:495–508.

- [Han et al., 2018] Han, J., Jentzen, A., and E, W. (2018). Solving high-dimensional partial differential equations using deep learning. Proceedings of the National Academy of Sciences, 115(34):8505–8510.

- [Hornik, 1991] Hornik, K. (1991). Approximation capabilities of multilayer feedforward networks. Neural Networks, 4(2):251–257.

- [Huang et al., 2006] Huang, G.-B., Zhu, Q.-Y., and Siew, C.-K. (2006). Extreme learning machine: Theory and applications. Neurocomputing, 70(1):489–501. Neural Networks.

- [Hytönen et al., 2016] Hytönen, T., van Neerven, J., Veraar, M., and Weis, L. (2016). Analysis in Banach Spaces, volume 63 of Ergebnisse der Mathematik und ihrer Grenzgebiete. 3. Folge. Springer, Cham.

- [Ikeda and Watanabe, 1989] Ikeda, N. and Watanabe, S. (1989). Stochastic differential equations and diffusion processes. North-Holland mathematical library vol. 24. North-Holland, Amsterdam, 2nd edition.

- [Ito, 1951] Ito, K. (1951). Multiple Wiener integral. Journal of the Mathematical Society of Japan, 3(1):157–169.

- [Ito, 1956] Ito, K. (1956). Spectral type of the shift transformation of differential processes with stationary increments. Transactions of the American Mathematical Society, 81(2):253–263.

- [Jamshidian, 2005] Jamshidian, F. (2005). Chaotic expansion of powers and martingale representation. Finance 0506008, University Library of Munich, Germany.

- [Kalsi et al., 2020] Kalsi, J., Lyons, T., and Pérez Arribas, I. (2020). Optimal execution with rough path signatures. SIAM Journal on Financial Mathematics, 11(2):470–493.

- [Karatzas and Shreve, 1998] Karatzas, I. and Shreve, S. (1998). Brownian Motion and Stochastic Calculus. Springer Science + Business Media, Berlin Heidelberg, 2nd corrected ed. 1998. corr. 6th printing 2004 edition.

- [Keller-Ressel, 2009] Keller-Ressel, M. (2009). Affine Processes – Theory and Applications in Finance. PhD thesis, TU Vienna.

- [Király and Oberhauser, 2019] Király, F. J. and Oberhauser, H. (2019). Kernels for sequentially ordered data. Journal of Machine Learning Research, 20(31):1–45.

- [Klenke, 2014] Klenke, A. (2014). Probability Theory: A Comprehensive Course. Universitext. Springer London, London, 2nd edition.

- [Lacoste, 1996] Lacoste, V. (1996). Wiener chaos: a new approach to option hedging. Mathematical Finance, 6(2):197–213.

- [Lelong, 2018] Lelong, J. (2018). Dual pricing of American options by Wiener chaos expansion. SIAM Journal on Financial Mathematics, 9(2):493–519.