Trigonometrically approximated maximum likelihood estimation for stable law

Abstract.

A trigonometrically approximated maximum likelihood estimation for -stable laws is proposed.

The estimator solves the approximated likelihood equation,

which is obtained by projecting a true score function on the space spanned by trigonometric functions.

The projected score is expressed only by real and imaginary parts of the characteristic function and their derivatives, so that

we can explicitly construct the targeting estimating equation.

We study the asymptotic properties of the proposed estimator and show consistency and asymptotic normality.

Furthermore, as the number of trigonometric functions increases, the estimator converges to the exact maximum likelihood estimator,

in the sense that they have the same asymptotic law.

Simulation studies show that our estimator outperforms other moment-type estimators, and

its standard deviation almost achieves the Cramér–Rao lower bound.

We apply our method to the estimation problem for -stable Ornstein–Uhlenbeck processes

in a high-frequency setting. The obtained result demonstrates the theory of

asymptotic mixed normality.

Key words. characteristic function, stable distributions, Fisher

information matrix, maximum likelihood estimator, -stable Ornstein–Uhlenbeck processes.

2010 Mathematics Subject Classification:

Primary 60E07, 62E17; Secondary 62F12, 62E201. Introduction

This paper proposes a novel characteristic function (ch.f.)-based estimation method called the trigonometrically approximated maximum likelihood estimation (TMLE). Our approach relies on the approximation method of a score function in Brant [1], where the approximation is done by projecting a true score on the functional space spanned by trigonometric functions. By solving the approximated score equation, we conduct TMLE. Because the projected score is expressed by combinations of real and imaginary parts of the ch.f. and its derivatives, we can easily calculate the approximated score solely from the original ch.f. This method is effective for the class of distributions whose ch.f.’s are available in closed form but whose densities are not. An example is the class of infinitely divisible (ID) distributions, which provides finite dimensional distributions for fundamental stochastic processes such as Lévy processes and additive processes (see, e.g. Sato [44]).

Specifically we apply the proposed method to the estimation of stable laws, which hold a prominent position among ID distributions. For details and notable properties of stable laws, see Samorodnitsky and Taqqu [43], Nolan [38] and references therein. We show that the trigonometrically approximated maximum likelihood (TML) estimator converges to the true maximal likelihood (ML) estimator as the number of trigonometric functions increases. Therefore, TMLE takes over nice properties of the maximum likelihood estimation (MLE), such as asymptotic normality and efficiency. Furthermore, we extend TMLE to an estimation method suitable for the parameter estimation of -stable Ornstein–Uhlenbeck processes. In what follows, we briefly introduce the literature and explain features of our estimator by comparing it with previous estimation methods.

The parameter estimation based on the ch.f. was originally proposed by Press [41] and has been developed into various directions. A regression-type estimator was proposed by Koutrouvelis [24, 25] and further investigated by Kogan and Williams [22]. Paulson et al. [40] considered an estimator that minimizes the squared integrated distance between the true ch.f. and the empirical one. Heathcote [17] implemented the method and discussed its efficiency and robustness. Feuerverger and McDunnough [13, 14] showed that their moment-type estimator can attain arbitrary high efficiency. Notice that some of the estimation methods are applicable not only for stable laws but also for general distributions with explicit ch.f’s.

The estimator by [13, 14] can be viewed as the generalized method of moments (GMM) estimator [15]. In the econometric literature, the GMM estimator and its variants [16, 19, 21, 35, 39] are commonly used to achieve semiparametrically efficient estimation. However, they are suboptimal for the estimation of the stable law if they use only a fixed number of moment conditions, constructed from the ch.f. Indeed, to attain high efficiency in the GMM estimator of [13] the number of moment conditions should be increased. Kunitomo and Owada [26] showed that the empirical likelihood (EL) estimator is asymptotically normal and efficient if the number of moment conditions increases at a certain rate with the sample size.

Although the GMM-type estimators satisfy desirable properties, they have two deficiencies. First, the number of moment conditions can increase only at a slow rate. For instance, in the EL estimator it must increase at the rate for , where is the sample size. Thus, the EL estimator cannot achieve high efficiency in a finite sample. Second, previous studies [4, 45, 48] point out that the weight matrix of the optimal GMM estimator tends to be singular as the number of moment conditions increases. Therefore, the GMM-type estimators are infeasible when the number of moment conditions is relatively large compared to the sample size.

To overcome these problems, Carrasco and Florens [3] proposed a version of the GMM estimator that utilizes a continuum of moment conditions (hereafter, the CGMM estimator). See also [2, 4, 5]. The CGMM uses an uncountable number of moment conditions from the beginning, which may cause the degeneracy of a certain covariance operator. However, the degeneracy problem is avoided by introducing regularization. Thus, the number of moment conditions is not restricted by the sample size.

TMLE addresses the same issues with CGMM. As we will see in the next section, the TML estimator has a close relation with the optimally weighted GMM estimator. The number of trigonometric functions in TMLE plays the same role as the number of moment conditions in GMM estimation. Moreover, to obtain the approximated score function, we calculate a covariance matrix that is similar to the weight matrix of the optimal GMM. The novelty of TMLE is that the number of trigonometric functions can be increased regardless of the sample size to satisfy asymptotic normality and efficiency. Moreover, the covariance matrix of TMLE is non-singular even if its dimension is large. Furthermore, our simulation shows that the TML estimator outperforms the CGMM estimator in terms of finite sample efficiency.

As for the exact MLE, the asymptotic theory has been established earlier by DuMouchel [11] and recently elaborated by Matsui [28] under continuous parametrizations. Since the ch.f. is the Fourier transform of the density, the likelihood function can be obtained by numerically evaluating the inversion formula. However, one encounters several difficulties in practical implementation. So far the methods of implementation have been studied only intermittently. Started from an early work by DuMouchel [12], several attempts have been made, especially in the symmetric case (see references in Nolan [38, Section 4]). However, in the general non-symmetric case, there are only a few studies [33, 37].

There are two issues in implementing MLE: computational complexity and accuracy. There exists a clear trade-off relation between these two aspects. For example, to ease the computational burden of the inversion formula for the densities, Mittnik et al. [33] have examined MLE solely by the FFT-based approximation of density functions. However, that limits the accuracy, especially in the tail. Nolan [37] uses a precomputed spline approximation of stable densities in doing MLE, which is equipped as the program “STABLE”. The program is fast, but the values reported by it have limited accuracy in several regions due to technical difficulties in approximation (see also [42]). On the other hand, regarding the pursuit of accuracy, few papers have rigorously validated the accuracy of their implemented ML estimators. Assuming symmetry, Matsui [31] improved the accuracy of ML estimators and certified the accuracy by comparing the true Fisher information matrix with the empirical one calculated from simulated ML estimators, and have observed that the two are almost identical. To obtain high accuracy, a finite integral representation of Zolotarev [49] is used for the central part of the density and an infinite series expansion of the density is applied for the tail part. Although the procedure is highly accurate, its computational burden is quite large. Besides one has to determine the regions where the finite integral representation or the series expansion is appropriate.

Turning now to TMLE, since it uses the ch.f. and its derivatives only, we do not need numerical integrations nor series expansions of densities, so that it is computationally simple and light. Furthermore, it gives high accuracy. Our simulation result shows that the variance of the TML estimator almost achieves the Cramér–Rao lower bound. Thus, TMLE shares nice properties with MLE such as asymptotic efficiency, while it is computationally reasonably tractable. Finally and most importantly, the procedure given in TMLE is easy to extend to other contexts. Here we apply it to approximate the conditional ML estimator of -stable Ornstein–Uhlenbeck (OU) processes. Applications to ID distributions other than stable laws are also possible (cf. [46]). Since the class of ID distributions constitute marginal laws of Lévy processes, we may consider, for instance OU processes driven by Lévy processes, which have been studied intensively in recent years. In summary, the method of TMLE has potential application in various active areas.

The paper is organized as follows. After introducing several preliminaries in Section 2.1, we rigorously define TMLE in Section 2.2. The non-degeneracy of the covariance matrix for TMLE is also proved in this section. TMLE is compared with other related estimation methods in Section 2.3. Asymptotics such as consistency and asymptotic normality are obtained in Section 3. Subsection 3.1 treats the case where the number of trigonometric functions is fixed. As the number of trigonometric functions increases, the TML estimator is shown to converge to the ML estimator regardless of sample size (see Subjection 3.2), so that TMLE is proved to have asymptotic efficiency. Most proofs and auxiliary results for Section 3 are given in the Appendix. We briefly discuss efficiency in finite samples at the end of Section 3. In Section 4 we examine finite sample performance of TMLE by Monte Carlo simulation, which shows that the TML estimator outperforms other asymptotically efficient estimators. Indeed, we see that the standard deviation of TMLE almost achieves the Cramér–Rao bound. Extending the TMLE method, we consider the parameter estimation for -stable Ornstein–Uhlenbeck processes in Section 5, where we numerically observe that the asymptotic mixed normality holds for the mean reversion parameter and asymptotic normality holds for other parameters in a high-frequency setting.

2. Trigonometrically approximated maximum likelihood estimation

2.1. Preliminary

We work on a continuous parametrization of the stable law (cf. [49, 36]) whose ch.f. is given by

| (2.1) | ||||

where , and are parameters. The parameter vector is denoted by . Moreover, we denote the parameter space and its interior by and , respectively. Because the expression (2.1) is continuous in , the case may not be necessary. By the inversion formula, we see that the density satisfies the condition for a location-scale family.

We use the following notations throughout. Denote real and imaginary parts of the ch.f. respectively by and , that is, . As usual and denote the first and the second derivatives of with respect to (w.r.t.) , respectively. Moreover, denotes the vector of partial derivatives of w.r.t. . The second-order partial derivatives w.r.t. and are denoted by

that is, all derivatives treated are interchangeable in our case (cf. [28, Section 2]).

2.2. Trigonometrically approximated likelihood estimation

As described in the introduction, we utilize the approximated score function proposed by Brant [1], which we call the trigonometrically approximated score function (TSF for short). By solving the approximated score equation by TSF, we define TMLE. The key idea is that TSF is the projection of the true score function onto a subspace spanned by trigonometric functions. The projected score has a nice expression given solely by the ch.f. and its derivatives.

In what follows, we precisely explain the procedure. Let be a Hilbert space with inner product

| (2.2) |

Notice that the expectation is taken w.r.t. , the density of , and both and depend on ; for convenience we abbreviate in these notations. For a given set of points such that for , we prepare a vector of trigonometric functions

and its expectation

| (2.3) |

The elements of vector are linearly independent and span a subspace of . Generally, constitutes a non-orthogonal basis.

Next we project the score onto the subspace spanned by centered trigonometric functions . The projected score satisfies

with some coefficient , where denotes the orthogonal complement of the space spanned by . By taking the inner product of both sides with , we obtain

with

where the inner product of vectors is taken elementwise. Here under exchangability of expectation and derivative, is expressed by a derivative matrix 111This is denominator-layout notation (the Hessian formulation, the gradient) where a vector-by-vector derivative is given by the transpose of Jacobian.:

| (2.4) |

The elements of are given by

| (2.5) | ||||

Thus TSF is constructed by

| (2.6) |

It is easy to see that

| (2.7) |

which will be shown to converge to the true Fisher information matrix as in the proof of Theorem 3.4.

Now we write the empirical TSF by

and define the TML estimator as an element of the set

| (2.8) |

with some compact set . Since the existence of exact zeros of the empirical TSF is not always assured in a small sample, if there are no roots, we choose one of local minimum values of as the estimator. Although there might exist multiple local minima, we can appropriately choose a consistent sequence, as we will discuss shortly.

Remark 2.1.

Interestingly the expectation of the derivative of w.r.t. satisfies

under certain regularity conditions. The relation corresponds to the second definition of the Fisher information matrix.

As one can see, the procedure of TMLE is applicable to any laws with explicit ch.f.’s.

Thus TMLE could be a powerful statistical tool for the class of ID distributions,

whose ch.f is given by the Lévy–Khintchine representation e.g. [44, Section 8].

Finally, we discuss the non-degeneracy of . One may wonder if an arbitrary choice of evaluation points of results in the singularity of . In fact, we avoid this by the condition for . Recall that is constructed by the projection on a space spanned by trigonometric functions. The idea behind this is to choose such that trigonometric functions keep linear independence. In the following lemma we show that the rows of are linearly independent for and the inverse of the Grammian matrix is positive definite.

Lemma 2.2.

Suppose that for all .

For any

and for any choice of such that for ,

the rows of are linearly independent for

, namely .

is positive definite.

2.3. Comparison with GMM and other related estimators

The TML estimator has a close similarity to the GMM estimator. Based on moment conditions , the optimally weighted two-step GMM estimator is defined by

| (2.9) |

where is a consistent estimator for . Typically, is obtained by

| (2.10) |

where is a preliminary consistent estimator of . The first-order condition of the minimization problem yields

| (2.11) |

Comparing with (2.6), we see that the two estimators are closely related, although their derivations are quite different: the TML estimator is obtained by the projection of the true score on trigonometric functions, while the GMM estimator is constructed based on the moment conditions. One clear difference is that we treat as a function of in the estimator of TMLE (2.6), and do not use a predetermined matrix.

Some studies pointed out that the GMM estimator is infeasible when the grid of is too fine, because the weight matrix becomes singular [2, 4, 45, 48]. There might be some confusion regarding this argument. Even though the GMM estimator is infeasible if (2.10) is used, can be estimated by because the explicit form of is available for the stable law, cf. (2.2). We do not need to estimate the variance by its sample analog. We call the GMM estimator using as the weight matrix the explicit GMM estimator. Lemma 2.2 shows that is non-singular as long as evaluation points are properly chosen. Therefore, the explicit GMM estimator is indeed feasible no matter how fine the grid is. Notice, however, that the non-degeneracy of the weight matrix does not imply that explicit GMM can utilize an arbitrary large number of moment conditions to satisfy desirable asymptotic properties. We will discuss this issue in the next section (Remark 3.8).

We explain other related estimators, which are compared with TML estimator in the simulation.

The asymptotics of these estimators are discussed in the next section.

Other related estimators

The CGMM estimator is based on a continuum (continuous function) of moment conditions

, where

(see [3, 4] for a detailed definition).

More precisely, for a suitably chosen covariance operator , it minimizes

w.r.t. , where is a norm

and .

Thus the CGMM estimator can be viewed as a continuous version of (2.9) (notice that

plays a role of ). The idea behind is to pursuit efficiency by capturing more information ([3, Sec. 5.2]).

A problem of CGMM is that an estimate of optimal is not invertible in general.

This is dealt with a regularization parameter introduced in the estimation of .

The EL estimator [26] also relies on the moment conditions and

maximizes the empirical likelihood subject to the moment conditions. Similar to the GMM estimator

it suffers from a severe problem of degeneracy if moment conditions are too many, because it is a one-step estimator that implicitly

estimates the optimal weight matrix.

We cannot use as the weight matrix for the EL estimator.

Remark 2.3.

The models considered by [45] and [2] are different from ours. They treat more complicated financial models such as affine price models. It is not certain if is non-singular for distributions other than the stable law when the grid of evaluation points is fine. Moreover, the condition of our lemma is violated if symmetric grid points are selected as in [45].

3. Asymptotics of trigonometric approximated maximum likelihood estimation

This section investigates asymptotic properties of TMLE. The asymptotics of TMLE with arbitrary fixed evaluation points are studied in Subsection 3.1. In Subsection 3.2 we consider the case where the number of points increases. We show that the TML estimator converges to the ML estimator in the sense that they have the same asymptotic law. The asymptotics of other related estimators are discussed at the end of this section.

3.1. Asymptotics of TMLE when the number of points is fixed

The TML estimator with fixed evaluation points could be regarded as a -estimator, and we exploit theorems from van der Vaart [47, Theorems 5.41 and Theorem 5.42]. The following is the first main result.

Theorem 3.1.

Let be any compact subset of and let be a true parameter. Suppose that evaluation points of satisfy for and for all . Then the probability that has at least one root tends to as , and there exists a sequence of roots such that in probability. Moreover, every consistent sequence of roots satisfies

| (3.1) |

In particular, the sequence is asymptotically normal with mean zero and covariance matrix .

Theorem 3.1 does not rule out the existence of multiple roots. However, non-uniqueness of solutions is not a serious problem because we can utilize existing consistent estimators for such as the quantile-based estimator of McCulloch[32]. We can find the consistent root by choosing the root closest to a preliminary consistent estimator (see p.70 of [47]).

The proof of Theorem 3.1 is given in Appendix A.2. Here we make a remark about the idea behind the proof.

Remark 3.2.

The TML estimator could be regarded as a -type estimator whose estimating equation approximates the first-order condition of MLE. If the estimator converges to a local minimum/maximum of the likelihood function, then consistency fails. We can avoid this at least locally through the condition see Lemma 2.2, that is, the condition that for sufficiently large samples, the Hessian of TMLE derivative of w.r.t. is positive definite in a neighborhood of true parameter cf. Remark 2.1 . Thus asymptotically and locally we can choose a unique zero which maximizes the likelihood function.

3.2. Asymptotics of TMLE when the number of points goes to infinity

We show that the TML estimator converges to the ML estimator in the sense that they have the same asymptotic law (Theorem 3.6). Throughout this subsection, we take equally spaced evaluation points and study the limit behavior of TMLE when the number increases to infinity, while the interval length goes to zero.

Referring to Brant [1], we first describe that TSF can be regarded as a two-step approximation of the true score function. From this one can grasp how the limit operation and works, which is also useful to follow the proofs. The first step is based on a wrapping of ,

| (3.2) |

from which we construct a wrapped version of the score function ( vector)

| (3.3) |

Notice that both and are periodic functions with period . By letting we obtain convergences and (Lemmas B.1 and B.2).

The second approximation step is the projection of into the subspace of that is spanned by trigonometric functions, as done in Section 2. Here, is the space on , whose inner product is given by

Now setting in the previous definitions (2.3) and (2.4), we obtain

Thus the projection coincides with TSF with equidistant evaluation points. Since is periodic, its projection on trigonometric functions will be close to itself for a sufficiently large . We can rigorously prove the convergence as (Proposition B.5). Therefore, we obtain as and .

Remark 3.3.

Notice that TSF is originally obtained by the projection of the true score function into the subspace of the space spanned by . The equivalence of the two procedures follows from the same logic as that the Fourier coefficients of a wrapped function are equivalent to the Fourier transform of at the corresponding points see also [1, p.993], that is, for ,

In the proofs of this subsection, we implicitly use properties of Fourier series expansion of the wrapped version e.g. Theorems B.3 and B.4. Thus we take equidistant points on and consider .

It is not straight forward to extend Theorem 3.1 to the case of and . The difficulty stems from the fact that the proof of the theorem evaluates the second-order derivatives of with respect to , which is quite complicated when and . Instead we apply [47, Theorem 5.7], the assertion of which is weaker than that of Theorem 3.1 but assures that sequences of (approximate) zeros of include a consistency sequence.

Let be a closed ball with center and radius . We have the following theorem.

Theorem 3.4.

Let be any compact subset of and be a true parameter. Then, for any and , there exists a sufficiently small such that any sequence of estimators satisfying for all sufficiently large and converges in probability to . The result holds even when if .

The problem of TMLE is that potentially has multiple local minima. However, asymptotically has a unique minimum in a neighborhood of . The theorem states that if we restrict the parameter space in a neighborhood of , then any sequence of estimators that satisfies is consistent for .

Theorem 3.4 immediately implies the existence of a consistent sequence of TMLE. Indeed, let for a sufficiently small . Then, from the proof of Theorem 3.4, we see that satisfies , and thus that is consistent. We emphasize that the introduction of is only for theoretical exposition. By the existence of a preliminary consistent estimator, we can obtain a consistent sequence of TMLE without knowing .

Remark 3.5.

Similarly as in the fixed-points case,

we can choose a sequence of consistent roots of .

Practically, we use a variant of the Newton–Raphson algorithm with a consistent initial value.

See Section 4 for the detail.

We observe in the proof that under the condition of and in Theorem 3.4,

converges to the true score as .

By this fact, consistency of is kept even in the limit .

The condition of Theorem 3.4 depends on an unknown true parameter and .

Because can be arbitrarily small, there exists such that for any .

Then, the condition is satisfied if although using too many evaluation points is computationally demanding.

In actual implementation the dependence on is not a major issue, see Remark 3.7.

Notice that the condition of and for consistency is included in

that for asymptotic normality, see Theorem 3.6.

Next we study the asymptotic normality and efficiency of the TML estimator, taking the consistent sequence of TMLE. For this purpose, first, we evaluate the distance between the score of TML and that of MLE , which can be depending on (Lemma B.6). Then, we evaluate the distance between and , whose expressions are given by scores and respectively, and show that it converges to in probability.

Theorem 3.6.

Let be any compact set on and be a true parameter. Denote the ML estimator and the consistent TML estimator respectively by and . If and such that holds for of Theorem 3.4, then ; thus, has the same asymptotic distribution as .

Theorem 3.6 states that the TML estimator is asymptotically normal and efficient because it inherits the asymptotic properties of the ML estimator [28]. As far as we know, our result is the first to rigorously establish the asymptotic normality and efficiency of the estimator based on the countable points of the ch.f. Here we see the difference between our result and previous results.

Previous studies show that the asymptotic variance of the GMM estimator, which is obtained under fixed and , can be arbitrarily close to the Crámer–Rao lower bound when is large and is small ([13, 48]). In other words, they employ a sequential asymptotic framework, where the limit w.r.t. is taken first and then the limit w.r.t. and is taken. However, the sequential asymptotic theory does not provide a good approximation to the finite sample distribution in general. If the number of moment conditions is too large, the GMM estimator does not satisfy asymptotic normality (see, for instance, [10] and references therein).

Kunitomo and Owada [26] showed that the EL estimator satisfies asymptotic normality if the number of moment conditions grows slowly depending on the sample size. However, their asymptotic framework is also different from ours. Their proof consists of two steps. First, they choose for fixed , and prove that the EL estimator converges in distribution to a normal distribution if satisfies with , so that is not independent of the sample size . Then, they show that the asymptotic variance converges to the Crámer–Rao lower bound as . Therefore, they do not specify the condition for the relation between and under which the EL estimator is asymptotically normal and efficient.

We close this section with a brief discussion of finite sample behaviors. As stated above the number of moment conditions is limited by sample size for both GMM and EL estimators. Since the number should be increased for efficiency, those estimators could not be optimal in finite samples. The CGMM estimator avoids this deficiency and can exploit a full continuum of moment conditions. However, similar to the GMM estimator, it has the estimation step of the optimal covariance operator. In view of simulations, this step causes some efficiency loss. Notice that the EL estimator skips this step since it estimates both the parameter vector and the optimal weight all at once. Taking above facts into consideration, we consider TMLE. In the TML estimator, and can be arbitrarily small and large respectively, regardless of the sample size. Moreover even if is sufficiently large, no singularity is observed, that is, it just converges to the ML estimator as and . Notice that in view of the form (2.6), the explicit weight matrix includes , and thus TMLE implicitly estimates the weight matrix simultaneously with .

Remark 3.7.

The condition on and in Theorem 3.6 depends on the unknown parameter . In actual implementation, the dependence on is not a major issue. Our simulation shows that a use of evaluation points is sufficient for efficient estimation for any value of . Using many more evaluation points does not improve the efficiency of the estimator when . This is probably because the estimation error of MLE dominates the approximation error of TSF when is not so large.

Remark 3.8.

The explicit GMM estimator is well defined even when we increase the evaluation number of ch.f. depending on . In particular we could take the equally spaced points as done in the TML estimator. However, it remains to be seen whether the asymptotic efficiency beyond a sequential framework holds in the limit of and . Indeed for the continuous version of GMM see [13, Equation (5.1)], which could be regarded as the limit of and , it is shown that the optimal weight is not always integrable [13, Equation (5.9)], and indeed we could not obtain it. Although it is not explicitly mentioned in [13], by ignoring the integrability and proceeding with some calculations, the first-order condition of explicit GMM with the optimal weight leads to the likelihood equation. We stay with only two certain facts: The score of explicit GMM is expressed by a combination of trigonometric functions and thus it has a more distance to the score of MLE than that of TMLE does, If we estimate by the explicit GMM with iteratively it becomes close to the TML estimator. Indeed, in a small simulation study, which is not reported here, we could not find a clear difference in the mean square errors between the TML estimator and the explicit GMM using with a consistent estimator.

4. Simulation results

The performance of ch.f.-based estimators is examined in this section. We compare the TML estimator with the EL estimator and the CGMM estimator. See Subsection 2.3 for definitions and relations of these estimators. All of the estimators are asymptotically efficient under certain conditions.

To find a root of for TMLE, we utilize the method of scoring algorithm, which is a variant of the Newton–Raphson algorithm. The method replaces the derivative of the objective function with its expected value in the iteration process; that is, given a preliminary estimator , the sequence is renewed by

where () is a scalar that adjusts the step length. The procedure is computationally stable because the positive definiteness of is guaranteed by Lemma 2.2. If the initial value of the iteration is -consistent and , then the one-step estimator is asymptotically equivalent to the TML estimator ([47, Theorem 5.45]). However, we iterate the procedure until the sequence converges.

To obtain the TML and EL estimators, we need to determine a vector of grid points for . The TML estimator uses equidistant points . The EL estimator uses 11 points when and 6 points when . The selection of the grid points for the EL estimator is similar to that of [26]. We use only 6 points when because our simulation showed that the EL estimator with 11 grid points performs poorly when .

For the minimization procedure for CGMM, because solving the original minimization problem of [3] is computationally involved, we utilize Proposition 3.4 of [2], which gives a simpler yet equivalent minimization problem. To evaluate the integrals used in the objective function, we adopt the Gauss–Hermite formula. Recall that the problem of CGMM is that an estimate of is not invertible, and we need the regularization to estimate . The regularization parameter is set to be in our simulation. Although we repeated the estimation using different values of the regularization parameter, the result was insensitive to this choice in this finite sample simulation.

The simulation is conducted using R software with package libstableR. The data generating process takes six different values of and two different values of . The values of and are fixed to and , respectively. As the initial value of all estimators, we use the quantile-based estimator of McCulloch [32], which is consistent and easy to calculate but not necessarily efficient.

Table 1 reports the result of 1000 repetitions with 1000 observations. The mean, standard deviation, skewness, and kurtosis are reported. We see that all estimators are nearly unbiased. Moreover, except for a few cases, we do not see a clear deviation from a normal distribution in term of the skewness and kurtosis. However, the standard deviation is quite different among estimators. The TML estimator dominates other two estimators for all cases even though its computational burden is quite small. The CGMM estimator performs poorly especially when the true value of is small. In contrast, the EL estimator performs rather poorly when the true value of is large.

| QMLE | ELE | CGMM | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.5 | 0 | Mean | 0.5001 | -0.0023 | 1.0000 | -0.0009 | 0.5000 | -0.0029 | 0.9980 | 0.0008 | 0.5006 | -0.0027 | 0.9996 | -0.0013 |

| Sd | 0.0191 | 0.0455 | 0.0773 | 0.0266 | 0.0245 | 0.0582 | 0.0827 | 0.0305 | 0.0584 | 0.1286 | 0.1092 | 0.0444 | ||

| Skew | 0.1126 | -0.0615 | 0.4498 | -0.1202 | 0.1309 | 0.0033 | 0.3717 | 0.0900 | 0.0106 | 0.0222 | 0.0715 | 0.0665 | ||

| Kur | 2.9610 | 3.0564 | 3.5118 | 2.8604 | 3.0749 | 3.1392 | 3.2826 | 3.1535 | 3.1382 | 3.1803 | 2.9802 | 3.0663 | ||

| 0.5 | Mean | 0.4995 | 0.4997 | 1.0038 | 0.0009 | 0.4980 | 0.5019 | 1.0042 | 0.0011 | 0.5002 | 0.4996 | 1.0010 | 0.0021 | |

| Sd | 0.0181 | 0.0387 | 0.0752 | 0.0366 | 0.0232 | 0.0543 | 0.0778 | 0.0400 | 0.0584 | 0.1282 | 0.1094 | 0.0546 | ||

| Skew | 0.0128 | -0.0277 | 0.1693 | 0.2090 | 0.1800 | 0.0950 | 0.2312 | 0.2377 | 0.1184 | 0.1164 | -0.0054 | 0.0166 | ||

| Kur | 2.8393 | 2.8909 | 3.0163 | 3.2009 | 2.7689 | 2.9204 | 3.0465 | 3.2012 | 3.0269 | 2.9172 | 2.8122 | 3.0560 | ||

| 0.7 | 0 | Mean | 0.7000 | -0.0016 | 1.0032 | 0.0002 | 0.7008 | -0.0039 | 0.9958 | 0.0018 | 0.7001 | -0.0071 | 0.9928 | 0.0020 |

| Sd | 0.0240 | 0.0436 | 0.0575 | 0.0337 | 0.0301 | 0.0552 | 0.0609 | 0.0365 | 0.0598 | 0.1051 | 0.0785 | 0.0490 | ||

| Skew | 0.0809 | 0.0572 | 0.0975 | -0.0026 | 0.2372 | 0.0630 | 0.2889 | -0.0138 | 0.1167 | 0.0224 | 0.1172 | -0.0165 | ||

| Kur | 2.8056 | 2.8497 | 3.0761 | 2.9722 | 3.0582 | 3.0206 | 3.0453 | 3.0562 | 2.9967 | 2.7643 | 2.88841 | 2.9925 | ||

| 0.5 | Mean | 0.7023 | 0.4997 | 0.9987 | 0.0012 | 0.7017 | 0.4988 | 0.9993 | 0.0004 | 0.7035 | 0.5041 | 0.9969 | 0.0011 | |

| Sd | 0.0243 | 0.0399 | 0.0549 | 0.0409 | 0.0303 | 0.0500 | 0.0580 | 0.0442 | 0.0607 | 0.1042 | 0.0723 | 0.0553 | ||

| Skew | 0.2565 | -0.0634 | 0.3667 | 0.3090 | 0.1111 | -0.1013 | 0.1919 | 0.0458 | -0.0167 | 0.1035 | 0.1691 | 0.2004 | ||

| Kur | 2.9837 | 2.8447 | 3.0964 | 3.2816 | 2.7998 | 2.8292 | 2.8247 | 2.8587 | 2.8587 | 3.2082 | 3.2045 | 3.3522 | ||

| 1.0 | 0 | Mean | 1.0018 | -0.0004 | 1.0038 | 0.0006 | 1.0025 | -0.0004 | 1.0036 | 0.0002 | 1.0005 | 0.0009 | 1.0030 | 0.0007 |

| Sd | 0.0353 | 0.0568 | 0.0453 | 0.0492 | 0.0396 | 0.0639 | 0.0466 | 0.0492 | 0.0611 | 0.0936 | 0.0524 | 0.0547 | ||

| Skew | 0.1197 | -0.0608 | 0.1635 | 0.1755 | 0.0158 | -0.0283 | 0.1766 | 0.1077 | -0.0337 | -0.0345 | 0.1477 | 0.1223 | ||

| Kur | 3.0653 | 3.3013 | 2.8804 | 2.9999 | 2.8650 | 2.9374 | 2.8817 | 3.0077 | 2.6764 | 3.1695 | 2.8678 | 2.8860 | ||

| 0.5 | Mean | 1.0003 | 0.4995 | 1.0002 | 0.0002 | 1.0025 | 0.5003 | 0.9997 | 0.0002 | 1.0009 | 0.5024 | 0.9991 | -0.0006 | |

| Sd | 0.0345 | 0.0478 | 0.0434 | 0.0477 | 0.0384 | 0.0583 | 0.0446 | 0.0493 | 0.0603 | 0.0930 | 0.0502 | 0.0562 | ||

| Skew | 0.0915 | -0.1710 | 0.0779 | 0.0943 | 0.0296 | -0.0994 | 0.1300 | 0.1252 | 0.0966 | 0.0847 | 0.1006 | 0.1239 | ||

| Kur | 2.8549 | 2.8708 | 2.8244 | 3.0870 | 2.9937 | 3.0937 | 2.8579 | 3.1045 | 2.9499 | 3.1468 | 2.8947 | 2.9264 | ||

| 1.3 | 0 | Mean | 1.3011 | -0.0027 | 1.0000 | 0.0001 | 1.3015 | -0.0040 | 1.0002 | 0.0009 | 1.3006 | -0.0031 | 0.9986 | -0.0003 |

| Sd | 0.0449 | 0.0744 | 0.0372 | 0.0523 | 0.0508 | 0.0821 | 0.0380 | 0.0533 | 0.0619 | 0.1011 | 0.0399 | 0.0560 | ||

| Skew | -0.0304 | 0.0089 | 0.0887 | -0.0614 | -0.0008 | 0.1513 | 0.0864 | -0.0081 | -0.1612 | 0.0679 | 0.0605 | 0.0072 | ||

| Kur | 2.9152 | 2.9449 | 2.9022 | 3.0298 | 2.8310 | 3.2701 | 2.8996 | 2.9636 | 3.1164 | 2.9232 | 3.0110 | 2.9021 | ||

| 0.5 | Mean | 1.3014 | 0.5002 | 0.9996 | 0.0003 | 1.3025 | 0.4983 | 1.0003 | 0.0015 | 1.3034 | 0.5012 | 0.9995 | 0.0015 | |

| Sd | 0.0439 | 0.0652 | 0.0366 | 0.0527 | 0.0504 | 0.0754 | 0.0377 | 0.0542 | 0.0593 | 0.1087 | 0.0403 | 0.0587 | ||

| Skew | 0.0393 | -0.0369 | 0.1030 | 0.0184 | -0.0080 | -0.0293 | 0.1208 | 0.0148 | 0.0620 | -0.0295 | 0.1192 | 0.0673 | ||

| Kur | 2.9720 | 2.7660 | 2.8661 | 3.1141 | 3.1213 | 2.9781 | 2.9181 | 3.0627 | 2.9224 | 2.8581 | 2.8740 | 3.0668 | ||

| 1.6 | 0 | Mean | 1.6004 | 0.0004 | 0.9990 | -0.0016 | 1.6052 | 0.0008 | 1.0001 | -0.0019 | 1.5995 | -0.0039 | 0.9987 | -0.0002 |

| Sd | 0.0491 | 0.1137 | 0.0318 | 0.0560 | 0.0605 | 0.1345 | 0.0321 | 0.0586 | 0.0552 | 0.1479 | 0.0332 | 0.0613 | ||

| Skew | -0.0663 | 0.0843 | 0.1365 | -0.0923 | 0.5137 | -0.0980 | 0.0637 | -0.0865 | -0.1163 | 0.0493 | 0.1434 | -0.1285 | ||

| Kur | 2.8879 | 3.2288 | 2.8530 | 3.0718 | 4.9116 | 2.9819 | 3.2748 | 3.0262 | 2.9319 | 3.1401 | 2.8545 | 3.1150 | ||

| 0.5 | Mean | 1.6006 | 0.5033 | 0.9986 | -0.0009 | 1.6023 | 0.5111 | 0.9983 | 0.0000 | 1.6009 | 0.5033 | 0.9986 | -0.0003 | |

| Sd | 0.0485 | 0.1008 | 0.0315 | 0.0553 | 0.0608 | 0.1303 | 0.0334 | 0.0610 | 0.0565 | 0.1483 | 0.0333 | 0.0607 | ||

| Skew | 0.0094 | 0.0804 | 0.0905 | -0.0294 | 0.0124 | 0.4189 | 0.2196 | 0.0206 | -0.0258 | 0.0723 | 0.1685 | -0.0662 | ||

| Kur | 2.9767 | 2.9599 | 2.9079 | 3.0665 | 2.8251 | 3.3305 | 2.9167 | 3.3463 | 3.1096 | 3.3187 | 2.8926 | 3.2160 | ||

| 1.9 | 0 | Mean | 1.9025 | 0.0160 | 0.9998 | -0.0018 | 1.9022 | 0.0041 | 0.9986 | -0.0012 | 1.8957 | 0.0052 | 0.9985 | -0.0020 |

| Sd | 0.0390 | 0.3478 | 0.0267 | 0.0531 | 0.0452 | 0.4375 | 0.0286 | 0.0611 | 0.0425 | 0.5299 | 0.0297 | 0.0650 | ||

| Skew | -0.0739 | 0.0623 | -0.0295 | -0.0352 | -0.5660 | -0.0011 | 0.1676 | -0.0335 | -0.2156 | -0.0312 | 0.1440 | -0.1065 | ||

| Kur | 2.9590 | 3.9513 | 2.9083 | 3.0549 | 2.9949 | 3.1632 | 2.9147 | 3.0477 | 2.8248 | 2.4583 | 2.8669 | 2.9937 | ||

| 0.5 | Mean | 1.9012 | 0.5317 | 0.9994 | -0.0009 | 1.8997 | 0.5259 | 0.9980 | 0.0026 | 1.8917 | 0.4707 | 0.9981 | -0.0012 | |

| Sd | 0.0376 | 0.3027 | 0.0266 | 0.0532 | 0.0451 | 0.3659 | 0.0282 | 0.0596 | 0.0423 | 0.4651 | 0.0296 | 0.0642 | ||

| Skew | -0.1684 | -0.3778 | 0.0187 | -0.0131 | -0.6621 | -0.6294 | 0.1596 | 0.0285 | -0.2116 | -0.8586 | 0.1379 | -0.0667 | ||

| Kur | 2.8764 | 3.4267 | 3.0886 | 3.1041 | 3.3209 | 3.6659 | 2.9539 | 2.9691 | 2.8167 | 3.4851 | 2.8465 | 2.9645 | ||

| 0.5 | 0 | 0.800 | 0.772 | 0.978 | 0.913 |

|---|---|---|---|---|---|

| 0.5 | 0.821 | 0.805 | 0.969 | 0.974 | |

| 0.7 | 0 | 0.956 | 0.952 | 1.018 | 1.006 |

| 0.5 | 0.924 | 0.883 | 1.001 | 1.006 | |

| 1.0 | 0 | 0.988 | 0.965 | 1.009 | 0.955 |

| 0.5 | 0.997 | 0.992 | 1.005 | 1.006 | |

| 1.3 | 0 | 0.999 | 1.003 | 1.026 | 1.009 |

| 0.5 | 0.999 | 1.006 | 1.006 | 1.015 | |

| 1.6 | 0 | 0.995 | 0.988 | 1.017 | 0.996 |

| 0.5 | 0.986 | 0.997 | 1.003 | 1.008 | |

| 1.9 | 0 | 0.913 | 0.824 | 0.987 | 1.002 |

| 0.5 | 0.922 | 0.886 | 0.983 | 0.999 |

Table 2 reports the ratio of the standard deviation of the ML estimator to that of the TML estimator under the same setting as that for Table 1. Thus, larger values indicate higher efficiency of TMLE. Because MLE is computationally demanding, we use the theoretical standard deviation calculated by Nolan [38]. The simulation generally supports our theory. The TML estimator is on par with the ML estimator for between 1.0 and 1.6. However, for a smaller we observe a slight degradation in the performance.

Remark 4.1.

The performance of the CGMM estimator may be improved if the

regularization parameter is determined

in a date-driven way cf. [5].

Although the result is not reported here, we also investigated the performance of the TML estimator by using 11 grid points.

The TML and the EL estimators have similar means and standard deviations in that case.

This is not surprising, because two estimators are first-order equivalent if the same grid points are used.

However, in a finite sample, the EL estimator performs poorly if a large number of grid points is used.

If the parameter regions are close to the boundaries, such as or , some elements of

the Fisher information matrix are known to diverge to see [11, 34, 29].

It will be interesting to see what happens for these estimators in such situations, and we will pursue this in future work.

In finite samples, the optimal choice of the grid points in the EL and TML estimators will depend on the true value of .

If is small, the estimators with more grid points around the origin often perform better. Further study of

this topic will also be part of future work.

5. Extensions to estimation of stable OU-processes

As an extension, we estimate the parameters of -stable Ornstein–Uhlenbeck processes based on discrete observations with an interval . By letting with/without , we can consider both high and low frequently observed processes. Let be a symmetric -stable Lévy process with , where is the scale parameter. Then a stationary version has the form

| (5.1) |

Notice that (5.1) satisfies the stochastic differential equation

and that due to the independent increments of , the process is a Markov process (see, e.g. [43, Sec. 3.6] for the definition and properties of -stable Ornstein–Uhlenbeck processes). For this type of Markov processes, several estimation methods based on the ch.f. have been established. One finds a detailed review in [48, Sec. 2.2.2] (see also [45, 6, 2]). All of them are variants of the GMM estimator based on the conditional ch.f. Our estimator also relies on the conditional ch.f., but it appears as the result of projection of the conditional score function on trigonometric functions.

We see our estimator more closely. Write the conditional likelihood equation

where is our targeting parameter vector. Here and are respectively the conditional density of given and its derivative vector. We approximate the likelihood equation by projecting the conditional score onto the subspace spanned by . The estimator is obtained as a zero of this approximated equation. We call this estimation trigonometrically approximated conditional MLE (TCMLE for short).

We present the exact form of TCMLE. In the definition (5.1) since the last two terms are independent, the conditional ch.f. is written as

A conditional version of at given , is provided by

where is a vector of evaluation points of the ch.f. Accordingly we have

where

The quantity corresponding to is defined by

where denotes the expectation operator deduced from the conditional density . Now we obtain the trigonometrically approximated conditional score function as

so that the corresponding empirical score is given by

The TCML estimator is the solution of .

Remark 5.1.

Notice that similarly to the i.i.d. case, GMM-type estimators again encounter the singularity problem in the covariance matrix (2.10) as the number of the grid points increases, see [3] cf. [48, Sec. 2.2.2]. Thus one needs to increase the grid number depending on sample sizes or needs a regularization parameter for the optimal covariance operator. Although we do not have a rigorous theoretical result for the non-i.i.d. case, in view of numerical simulations, we do not observe such a singularity in TCMLE.

Hereafter, we will examine the finite sample performance of our estimator in high frequency settings. In the literature asymptotic theories for quasi-MLE have been established for OU processes driven by more general locally stable Lévy processes, especially for [27, 8, 9]. The main tool is locally asymptotic stable property of the processes. The joint asymptotic distribution of all parameters has been derived by [9, Theorem 3.2]. Since TMLE converges to MLE as , for reasonably large and small TCMLE should approximate this asymptotic distribution also. We briefly explain this asymptotic in order to compare it with our simulation results.

Assume that we observe on with frequency , that is, we observe a discretized process with . Let and then as

where is the standard normal r.v. independent of and

Here are some constants depending on . In other words, has asymptotic mixed normality. If numerical simulations replicate this asymptotic mixed normality, then the validity of TCMLE would be assured.

| Mean | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sd | ||||||||||||

| Skew | ||||||||||||

| Kur | ||||||||||||

| Mean | ||||||||||||

| Sd | ||||||||||||

| Skew | ||||||||||||

| Kur | ||||||||||||

| Mean | ||||||||||||

| Sd | ||||||||||||

| Skew | ||||||||||||

| Kur | ||||||||||||

| Mean | ||||||||||||

| Sd | ||||||||||||

| Skew | ||||||||||||

| Kur | ||||||||||||

Monte Carlo simulations of TCMLE for parameters of -stable OU processes with frequency (top two rows) and (bottom two rows). For the first and third rows we take and for the second and fourth rows . The estimation procedures are repeated times. Here is a modified version of , see (5.3) for definition. In each cell statistical characteristics of estimators are presented.

In our simulation, we set and so that a path of process on is observed in different times. We repeated the estimation procedure times in three different cases and with . We uses equidistant points for evaluation of empirical conditional ch.f.

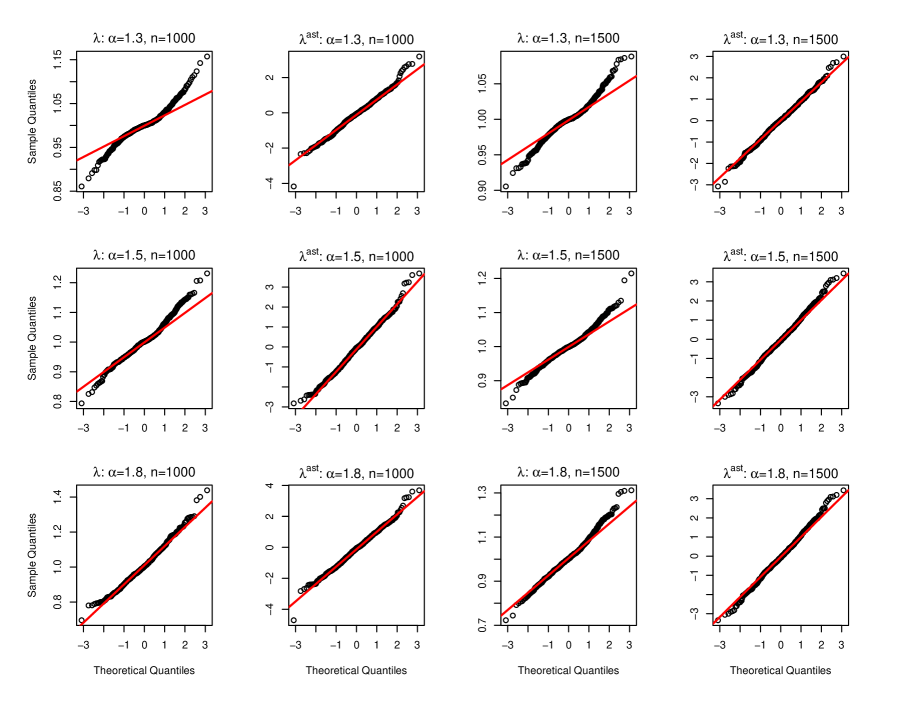

The results are summarized in Table 3, where statistics are presented similarly as before. Judging from the mean values, all estimators are unbiased, while obviously the standard deviations of are smaller than . The standard deviations for are smaller than those for . In view of skewness and kurtosis, asymptotic normality follows for and (We check QQ-plots also, though we do not present here), though these values for show quite different values. Values of are studied in detail bellow. We find difficulty in confirming orders directly, since accuracy of the asymptotic scale matrix depends on both and . Alternatively by observing the asymptotic mixed normality for we see that TCMLE properly functions.

Thus, we consider skewness, kurtosis, and QQ-plots for a version

| (5.3) |

where is the mean of samples of . The values of are presented in Table 3. Since the original sometimes takes huge outliers (mostly negative), we present further modified values of , that is, we remove several very small values. In cases and we remove outlier, and in cases , we remove outliers. Notice that skewness and kurtosis are sensitive to outliers, and the two characteristics of often show worse values than those of ; for instance, in , and then skewness, kurtosis are and respectively.

In Figure 1, we present QQ-plots of and for and sample sizes . Similarly to Table 3, outliers of are removed. In view of these graphs, is well-rescaled, and plots for almost show normality. Judging from these facts we conclude that the theory of asymptotic mixed normality for is depicted correctly with TCMLE.

Appendix A Supplementary results and proofs for Section 3.1

A.1. Proof of Lemma 2.2

It suffices to take with non-zero in (2.4) and prove that rows of are linearly independent. We take a similar approach as in the proof of [28, Theorem 3.1], where the non-singularity of the Fisher information matrix is shown for the stable law. Let and we show that

| (A.1) |

implies by indirect proof. Assume (A.1) for , then

holds. Therefore, the complex vectors

are linearly dependent with real coefficients . For convenience we omit the parameter in and and functions of them.

For , we define , so that we have , where

Now we look for . If these sums are zero, then

In view of the real parts of and ,

should hold for . This is impossible unless . Moreover, from and , we have

which is impossible unless .

Notice that at ,

the above equation reduces to , and thereby the result is kept.

Thus, we obtain , which is a

contradiction.

Let . Since

trigonometric functions in constitute a basis on

(see e.g. [7, Theorem 1]), they are linearly

independent.

Thus, for any if and

only if , cf. [23, p.9]. This implies

that is non-deterministic as a function

of for . Now for any it follows from Fubini

that

since the support of is the whole real line and is continuous in . Thus, is positive definite.

Remark A.1.

We could not remove the condition . Indeed, we take

such that and , and , and then

holds for all .

In view of [7, Theorem 1], we do not necessarily use the same set of points

for both and . We might obtain a better estimator with two different sets of evaluation points.

A.2. Proof of Theorem 3.1

We will check the conditions of [47, Theorem 5.41] where there corresponds to here. Since the conditions of [47, Theorems 5.41 and 5.42] are the same, the existence of a consistent root follows from Theorem 5.42, while asymptotic normality and (3.1) directly follow from Theorem 5.41.

In view of (2.6), is twice continuously differentiable for every because the ch.f. is three times continuously differentiable w.r.t. on . Note that in [28], the derivatives of w.r.t. are obtained up to the second order. In a similar manner we could obtain the third-order derivatives even in the complicated case of .

From (2.6) and (2.7), and follow. Write the first-order derivative matrix ( denominator layout) as

where each row is a vector and the element of is

| (A.2) | ||||

Thus exists and is non-singular according to Lemma 2.2 (cf. Remark 2.1).

From the form of the first-order partial derivative (A.2), it is not difficult to observe

| (A.3) |

where and are continuous matrix functions in . Since is compact and is integrable, we could find a dominant integrable function for each element of (A.3). Now due to [47, Theorem 5.42], there exists a consistent sequence of roots , and by [47, Theorem 5.41] this sequence satisfies asymptotic normality together with (3.1).

Appendix B Supplementary results and proofs for Section 3.2

For the proofs of Theorem 3.4 (Subsection B.1) and Theorem 3.6 (Subsection B.2), we need supplementary results. We use two theorems from [1] (Theorems B.3 and B.4), and the following lemmas and a proposition. Throughout this section, let , etc. be generic positive constants whose values are not of interest. For a given function , we denote by the periodic function:

The first lemma is an easy application of Lemma 6.2 in [1].

Lemma B.1.

Let and be periodic functions respectively based on and . Then, for any , we have

where are positive constants that depend on neither nor .

Proof.

Since the proof is a slight modification of that for [1], we only state the difference in the condition. For sufficiently large , we clearly have . In view of Lemma 2.1 in [28], and are continuous in and satisfy

for sufficiently large , where the orders of left are uniform in . We replace the tail condition (6.1) of [1, Lemma 6.2] with the above bounds, and then the results follow from the reproduction of the proof. ∎

As stated before Theorem 3.6, we evaluate the distance between and through the two-step approximation; we will evaluate the distance between and in Lemma B.2 and that between and in Proposition B.5. In this regard we define several notations. Denote the -th element of by for , namely,

Similarly, denote the -th component of and respectively by and for . Notice that in the proofs, we often omit when the corresponding proof holds uniformly in . In such a case we make a caution in the beginning.

Lemma B.2.

For every , converges to uniformly in as .

Proof.

Since the proof is valid for all , we omit subscript of and write to indicate elements of them for convenience. Since

| (B.1) |

we evaluate

Since is unimodal and the support is , holds on . Indeed for sufficiently large . Due to Proposition 2.3 of [28], . Now in view of Lemma B.1 the left hand-side converges uniformly in as . ∎

The next proposition relies on [1, Theorems 6.5 and 6.6], and for convenience we state them.

Theorem B.3 (Theorem 6.5 in [1]).

Let be a differentiable function of period , such that for all . Then there exists a trigonometric polynomial of degree , , satisfying

where is an absolute constant.

Notice that Theorem B.3 is based on [20, Theorem 1, p.2], where one could see more precisely that does not depend on any specialization of the corresponding functions.

Theorem B.4 (Theorem 6.6 in [1]).

Let be continuous, and let and be th degree trigonometric polynomials in such that

| (B.2) |

and

| (B.3) |

Then

Proposition B.5.

There exists such that when we could take an upper bound with which hold uniformly in , and . Moreover, for any ,

| (B.4) |

where is a positive constant which does not depend on and .

Proof.

By the periodicity, it is enough to show that there exists such that . For convenience we omit subscript of and write, for instance, and since the proof is valid for all . Accordingly in and and their derivatives is also abbreviated. Firstly we consider . We evaluate

The numerator of is dominated by

where in the last step we use Lemma B.1. Similarly the numerator of is bounded by

Next the denominator is evaluated. It follows by the definition that

We recall that for sufficiently large , there exists a uniform constant in such that . Thus, if , so that , we have

for sufficiently small . Hence on , which yields

| (B.5) |

Now, correcting the above results, we obtain

Then due to the tail behaviors of and in Lemma 2.1 in [28], for some small it is easy to find a uniform bound which does not depend on , , and even . We specially notice that and for sufficiently large . Thus, we prove the existence of such that for all .

For the inequality (B.4), we rely on Theorem B.4 and will check its conditions (B.2) and (B.3). In our case, and . Due to Theorem B.3 and the result just proved, (B.2) holds with , where is an unspecified trigonometric polynomial. For (B.3) let and we obtain

where the second inequality follows from the fact that is the projection of on . Now we get (B.4) through Theorem B.4. ∎

B.1. Proof of Theorem 3.4

Proof of Theorem 3.4.

Because can be arbitrarily small without loss of generality, we assume that . Thus, we confine our parameter space to and show that any sequence such that and also satisfies .

Let . Then, by [47, Theorem 5.7], it is enough to show that there exist such that for any

| (B.6) |

and that

| (B.7) |

Notice that the TML estimator is included in the class of estimators we consider. Indeed, let . Then we see easily from (B.7) that .

For any given and , the condition (B.6) follows from Lemma 2.2 and continuity of . In case , we have for all if , which is established at the end of the proof . Because is continuous and positive definite at (see the proof of [28, Theorem 3.1]), we establish the first condition even when .

The condition (B.7) is satisfied if each element of is continuous in for every and is bounded by an integrable function (the envelope condition) [47, p.46]. As the proof is similar for any elements, we only establish the result for , the third element of . It is clear that is continuous in for any fixed and . Moreover, it follows from Proposition B.5 and Lemma B.2 that uniformly over if and . Since is continuous in , so is even when . For the envelope condition, we use the following inequality

| (B.8) |

The second term, which is periodic with period , has the same bound as that of Proposition B.5. Thus, if , it is bounded for any . For the first term, we have

| (B.9) |

The first part satisfies for sufficiently large (see [28, Proposition 2.3]). Since is periodic, we consider the bound of on .

The interval is further divided into two regions: and , where the constant is chosen such that holds for all and all . This is possible due to the tail property of stable laws (see, e.g. [43, Proposition 1.2.15]). Here, are constants that do not depend on . Since the tail of is bounded by , which is decreasing on , the numerator of is bounded on by

while the denominator has the lower bound on . Thus,

| (B.10) |

This together with the bound for yields

| (B.11) |

on . Since is periodic, the bound holds for all . Thus we obtain

Finally we prove . Since the proofs are similar, we only show the convergence for the information of , that is, . Since pointwise in , in view of

it suffices to show that has an integrable dominant function w.r.t. the measure . Observe that

where the second term has the bound (B.4). For the first term, we notice that (B.11) holds for all sufficiently small and the bound does not depend on (see the derivation process also). Thus, there exists a such that for all , if , holds. Hence has a dominant integrable function. ∎

B.2. Proof of Theorem 3.6

We first show -consistency of by using a similar argument with the proof of [47, Theorem 5.21]. Here we use the fact that can be arbitrarily close to the score function of the ML estimator, and establish the result by using the properties of . The condition on and assures us that and are close enough for our purpose. To obtain the asymptotic distribution of , we show that , where is the ML estimator. This result implies that the TML and ML estimators are first-order equivalent.

Before the proof we need the following lemma which gives a moment bound for the stochastic distance of and . The bound is proved to be a function of and . The proof is rather technical, and we fully exploit the two-step approximation scheme of Section 3.2.

Lemma B.6.

Let . Then for arbitrary small ,

Proof.

The left hand-side is bounded by

We evaluate each element in the last sum and decompose them into the following three integrals,

For we observe that is periodic and has the bound in (B.4). Thus taking in (B.4), we obtain .

Turning to , in view of (B.1) it suffices to evaluate

| (B.12) | ||||

Although is treated in the proof of Theorem 3.4, we use another bound here. Recall that is decreasing. Since , the numerator has a bound

for a sufficiently small . In the meanwhile, the denominator has a uniform lower bound on , and on it satisfies

where the constant is the one in the proof of Theorem 3.4. Thus, we have

and since , we further obtain

| (B.15) |

Now,

Concerning , we observe that on ,

| (B.16) |

while by similar calculations to that of ,

Thus, except for constants, has the same uniform bound as (B.15). Now collecting above results, we reach

We again use the bound (B.12) for . For of we recall the argument in the proof of Theorem 3.4. Define

and then

Notice that is periodic and by exactly the same way as that for , has the bound on (cf. (B.11)). Since for large , . Due to (B.16) together with , we further obtain . Thus

Therefore, we obtain the result. ∎

Now we are ready to prove Theorem 3.6.

Proof of Theorem 3.6.

We start to see . Let be the ML estimator and let . Then, as . By the definition of and the consistency of both and , we observe that

Due to Lemma B.6 and the condition on , the right-hand side converges to as .

Next we prove

| (B.17) |

where is the function (This corresponds to [47, (5.22)]). Write the left-hand side as

where is a function . We study in first. Observe that for any ,

as , where we borrow the logic of the previous proof in the last step. In a similar manner, other quantities in and converge to in probability. For the quantity , we use the continuous differentiability of the score of MLE: for every . In view of Lemma 2.1, in [28] each element of the matrix is continuous in and in the tail for all , where a matrix norm. Hence , and the Lipschitz condition for given in [47, Theorem 5.21] is satisfied, where there is replaced with here. Then due to [47, Example 19.7], the functions form a Donsker class (see also the proof of [47, Theorem 5.21]) and by [47, Lemma 19.24], .

Now applying the delta method to the last quantity, we find from (B.17) that

where is the Fisher information, that is, the derivative of at (Here corresponds to in [47, Theorem 5.21]). Since is invertible (see the beginning of the proof for Theorem 3.4), we have

This implies is -consistent, so that . Thus we obtain

Finally, by the asymptotic linear representation of the ML estimator [28, Theorem 3.1], we have

Again by Lemma B.6 the left is . ∎

Appendix C Supplement for Section 5

Exact forms of derivative vectors of the conditional ch.f. with are given. For convenience we define and present expressions for , which are

References

- [1] Brant, R. (1984) Approximate likelihood and probability calculations based on transforms. The Annals of Statistics 12, 989–1005.

- [2] Carrasco, M., Chernov, M., Florens, J.P. and Ghysels, E. (2007). Efficient estimation of general dynamic models with a continuum of moment conditions. Journal of Econometrics 140, 529–573.

- [3] Carrasco, M. and Florens, J.P. (2000) Generalization of GMM to a continuum of moment conditions. Econometric Theory 16, 797–834.

- [4] Carrasco, M. and Florens, J.P. (2002) Efficient GMM estimation using the empirical characteristic function. Working paper; Department of Econometrics: University of Rochester.

- [5] Carrasco, M. and Kotchoni, R. (2017) Efficient estimation using the characteristic function. Econometric Theory 33, 479–526.

- [6] Chacko, G. and Viceira, L.M. (2003) Spectral GMM estimation of continuous-time processes. Journal of Econometrics 116, 259–292.

- [7] Christensen, O. and Christensen, K.L. (2006) Linear independence and series expansions in function spaces. The American Mathematical Monthly 113, 611–627.

- [8] Clément, E. and Gloter, A. (2019) Estimating functions for SDE driven by stable Lévy processes. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques 55, (2019), 1316–1348.

- [9] Clément, E. and Gloter, A. (2020) Joint estimation for SDE driven by locally stable Lévy processes. Electronic Journal of Statistics 14, 2922–2956.

- [10] Donald S.G., Imbens, G.W. and Newey, W.K. (2003) Empirical likelihood estimation and consistent tests with conditional moment restrictions, Journal of Econometrics 117, 55–93.

- [11] DuMouchel, W.H. (1973) On the asymptotic normality of the maximum-likelihood estimate when sampling from a stable distribution. The Annals of Statistics 1, 948–957.

- [12] DuMouchel, W.H. (1975) Stable distributions in statistical inference: 2. Information from stably distributed samples. Journal of the American Statistical Association 70, 386–393.

- [13] Feuerverger, A. and McDunnough, P. (1981) On the efficiency of empirical characteristic function procedures. Journal of the Royal Statistical Society. Series B (Methodological) 43, 20–27.

- [14] Feuerverger, A. and McDunnough, P. (1981) On some Fourier methods for inference. Journal of the American Statistical Association 76, 379–387.

- [15] Hansen, L.P. (1982) Large sample properties of generalized method of moments estimators. Econometrica 50, 1029–1054.

- [16] Hansen, L.P., Heaton, J. and Yaron, A. (1996) Finite-sample properties of some alternative GMM estimators. Journal of Business & Eonomic Statistics 14, 262–280.

- [17] Heathcote, C.R. (1977) The integrated squared error estimation of parameters. Biometrika 64, 255–264.

- [18] Heyde, C. C. (1997) Quasi-Likelihood And Its Application: A General Approach to Optimal Parameter Estimation, Springer, New York.

- [19] Imbens, G. W., Spady, R. H. and Johnson, P. (1997) Information theoretic approaches to inference in moment condition models Econometrica 66. 333–357.

- [20] Jackson, D. (1930) Theory of Approximation. A.M.S. Colloq. Pub. 11.

- [21] Kitamura, Y. and Stuzer, M. An information-theoretic alternative to generalized method of moments estimation Econometrica 65, 861–874.

- [22] Kogon, S.M. and Williams, D.B. (1998). Characteristic function based estimation of stable distribution parameters. In: A Practical Guide to Heavy Tails: Statistical Techniques and Applications, Birkhäuser, Boston, 311–338.

- [23] Kolmogorov A.N. and Fomin S.V. (2012) Elements of the Theory of Functions and Functional Analysis [Two Volumes in One], Martino Publishing, Eastford.

- [24] Koutrouvelis, I.A. (1980) Regression-type estimation of the parameters of stable laws. Journal of the American Statistical Association 75, 918–928.

- [25] Koutrouvelis, I.A. (1981) An iterative procedure for the estimation of the parameters of stable laws. Communications in Statistics-Simulation and Computation 10, 17–28.

- [26] Kunitomo, N. and Owada, T. (2006). Empirical likelihood estimation of Lévy processes. Graduate School of Economics, University of Tokyo Discussion Paper.

- [27] Masuda, H. (2019). Non-Gaussian quasi-likelihood estimation of SDE driven by locally stable Lévy process. Stochastic Processes and their Applications 129, 1013–1059.

- [28] Matsui, M. (2020) Asymptotics of maximum likelihood estimation for stable law with continuous parameterization. Communications in Statistics - Theory and Methods (online)

- [29] Matsui, M. (2005) Fisher information matrix of general stable distributions close to the normal distribution. Mathematical Methods of Statistics 14, 224–251.

- [30] Matsui, M. and Takemura, A. (2006) Some improvements in numerical evaluation of symmetric stable density and its derivatives. Communications in Statistics - Theory and Methods 35, 149–172.

- [31] Matsui, M. and Takemura, A. (2008) Goodness-of-fit tests for symmetric stable distributions – empirical characteristic function approach. Test 17, 546–566.

- [32] McCulloch, J.H. (1986) Simple consistent estimators of stable distribution parameters. Communications in Statistics - Simulation andComputation 15, 1109–1136.

- [33] Mittnik, S., Doganoglu, T., and Chenyao, D. (1999). Maximum likelihood estimation of stable Paretian models. Mathematical and Computer Modelling 29, 275–293.

- [34] Nagaev, A.V. and Shkol’nik, S.M. (1988) Some properties of symmetric stable distributions close to the normal distribution. Theory of Probability & Its Applications 33, 139–144.

- [35] Newey, W. K. and Smith, R. J. Higher order properties of GMM and generalized empirical likelihood estimators. Econometrica 72, 219–255.

- [36] Nolan, J.P. (1998) Parameterizations and modes of stable distributions. Statistics & Probability Letters 38, 187–195.

- [37] Nolan, J.P. (2001) Maximum likelihood estimation and diagnostics for stable distributions. In: Lévy Processes: Theory and Applications (O. E. Barndorff-Nielsen et al. eds.), Birkhäuser, Boston, 379–400.

- [38] Nolan, J. P. (2020). Univariate Stable Distributions: Models for Heavy Tailed Data. Springer, Cham.

- [39] Qin, J. and Lawless, J. (1994) Empirical Likelihood and General Estimating Equations. The Annals of Statistics 22, 300–325.

- [40] Paulson, A.S., Holcomb, E.W. and Leitch, R.A. (1975) The estimation of the parameters of the stable laws. Biometrika 62, 163–170.

- [41] Press, S.J. (1972) Estimation in univariate and multivariate stable distributions. Journal of the American Statistical Association 67, 842–846.

- [42] Royuela-del-Val, J., Simmross-Wattenberg, F., and Alberola-López, C. (2017). libstable: Fast, Parallel, and High-Precision Computation of -Stable Distributions in R, C/C++, and MATLAB. Journal of Statistical Software 78, 1–23

- [43] Samorodnitsky, G. and Taqqu, M.S. (1994) Stable Non-Gaussian Random Processes. Stochastic Models with Infinite Variance. Chapman and Hall, London.

- [44] Sato, K. (1999) Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press, Cambridge.

- [45] Singleton, K.J. (2001) Estimation of affine asset pricing models using the empirical characteristic function. Journal of Econometrics 102, 111–141.

- [46] Sueishi, N. and Nishiyama, Y. (2005) Estimation of Levy Processes in Mathematical Finance: A Comparative Study. In: MODSIM 2005 International Congress on Modelling and Simulation. (Zerger, A. and Argent, R.M. eds.) Modelling and Simulation Society of Australia and New Zealand, December 2005, 953–959.

- [47] van der Vaart, A.W. (2000) Asymptotic Statistics (Cambridge Series in Statistical and Probabilistic Mathematics). Cambridge University Press, Cambridge.

- [48] Yu, J. (2004) Empirical characteristic function estimation and its applications. Econometric Reviews 23, 93–123.

- [49] Zolotarev, V.M. (1986) One-Dimensional Stable Distributions. AMS Translation of Mathematics Monographs, 65, American Mathematics Society, Providence. (Transl. of the original 1983 Russian)