Quantum computational finance: martingale asset pricing in a linear programming setting

Quantum computational finance: martingale asset pricing for incomplete markets

Abstract

A derivative is a financial security whose value is a function of underlying traded assets and market outcomes. Pricing a financial derivative involves setting up a market model, finding a martingale (“fair game”) probability measure for the model from the given asset prices, and using that probability measure to price the derivative. When the number of underlying assets and/or the number of market outcomes in the model is large, pricing can be computationally demanding. We show that a variety of quantum techniques can be applied to the pricing problem in finance, with a particular focus on incomplete markets. We discuss three different methods that are distinct from previous works: they do not use the quantum algorithms for Monte Carlo estimation and they extract the martingale measure from market variables akin to bootstrapping, a common practice among financial institutions. The first two methods are based on a formulation of the pricing problem into a linear program and are using respectively the quantum zero-sum game algorithm and the quantum simplex algorithm as subroutines. For the last algorithm, we formalize a new market assumption milder than market completeness for which quantum linear systems solvers can be applied with the associated potential for large speedups. As a prototype use case, we conduct numerical experiments in the framework of the Black-Scholes-Merton model.

1 Introduction

Consider the following simplified version of the “parable of the bookmaker” [BR96]. A bookmaker is taking bets on a horse race between two horses A and B. Assume that, without quoting any odds, the bookmaker has received bets on a win of horse A and bets on a win of horse B. The bookmaker’s desire is to have a sustainable business based on fees and not to use the money for gambling. What are the correct odds for the bookmaker to quote to the betters? The market has decided that horse A is half as likely to win over horse B, i.e., the implied probability of winning is vs. . Hence the bookmaker quotes the odds of , which means that if horse A wins each bet on horse A will turn into , while bets on horse B are lost. If horse B wins, each bet on horse B will turn into , while bets on horse A are lost. Given these odds for the bets taken, the bookmaker has a payoff of for each scenario, which is called risk neutral. Note that the result of zero payoffs for all scenarios is independent of the true probabilities of winning for A or B.

Financial markets show some similarities with the betting on horse races, and often involve highly complex scenarios and challenging computational problems. A significant part of computational finance involves the pricing of financial securities such as derivatives [Gla03, FS04, Hul12]. Some of these securities (often called over-the-counter, OTC, derivatives) are tailor-made between two parties, and thus the price of these instruments is not readily quoted on a liquid primary market [Čer09]. Such securities have complex payoffs that usually depend on underlying liquid assets, each introducing its own dynamics due to market and economic fluctuations. In that sense, these securities can be called exotic and illiquid. Exotic securities are usually not frequently traded to allow adequate price determination by the market itself. Pricing can become computationally expensive, especially when the number of underlying liquid assets is large and/or the pricing model takes into account a large number of possible market outcomes.

The Black-Scholes-Merton framework [BS73, Mer73, Hul12] allows for a concise formula for the price of a call option on a single stock and other options. The market model in the simplest formulation is a single risky stock driven by a random process (e.g., a Brownian motion) and one safe asset (“bond” or bank account). One can consider a generalized situation for markets with a large amount of underlying assets and a large sample space on which arbitrary driving processes are defined. The number of assets can be large, say all the stocks traded on the stock market and in addition simple frequently traded derivatives on these stocks. The size of the underlying sample space can also be large. Such a sample space could be given by the discretization of a continuous model space for a multidimensional random walk used in finance, or by the exact outcomes of the NCAA basketball playoffs (which have possibilities for teams) in a betting scenario. Large outcome spaces and the presence of many traded securities can make pricing hard in many cases and motivate the use of quantum computers. The risk-neutral pricing framework is employed in practice in stock, interest rate, and credit derivative markets. Given a liquid financial market trading a number of assets, the task is to price a new financial instrument which is not traded in the market. To price this instrument, so-called risk-neutral probability measures are extracted from the market variables. Such measures turn the discounted price process of each of the assets into a martingale and are used to compute the price of the derivative via an expectation value.

1.1 Main results

In this work, we discuss algorithms in quantum computational finance which can be used for the pricing of certain illiquid financial securities. We discuss quantum algorithms that can be used in incomplete markets with the potential for significant speedups over classical algorithms. The algorithms presented here are the first to extract the martingale measures from market data. This is akin to bootstrapping: the process of extracting information from market variables, a common practice among financial institutions. We describe in Section 2 the concepts of Arrow securities, price system, martingale measures, including the existence of martingale measures from a no-arbitrage assumption, and complete markets. In Section 3 we introduce a pricing framework where quantum linear programming algorithms can be employed. In this framework, the Arrow securities provide the basis for constructing a probability measure, called martingale measure, which encapsulates the market information and allows to find the price of new securities. The output of financially relevant results is usually a range of possible prices of the new asset.

In Section 4, we adapt to our settings the quantum algorithm for zero-sum games [AG19] which is asymptotically one of the fastest algorithms for solving linear programs in terms of query complexity. We give the conditions for which the quantum algorithm performs better than the classical one. We further explore in Section 4.3 the performances of the zero-sum game algorithm on market instances derived from Black-Scholes-Merton (BSM) models. Working in this model eases the space requirements of the input to be only , compared to in the general case. As an alternative to the zero-sum game algorithm, in Appendix E we discuss the usage of a quantum version of the simplex method for pricing. Simplex methods are often used for solving linear programs: they provide exponential worst-case complexity, but they can be very efficient in practice. We adapt a previous quantum algorithm for the simplex method and compare to the quantum zero-sum game algorithm.

In Section 5 we explore the use of quantum matrix inversion algorithms for pricing and extracting the martingale measure. We introduce the definition of a least-squares market, and prove that market completeness is a sufficient condition for having a least-square market (Theorem 6). As the converse is usually not true, a least-squares market is generally a weaker assumption than a complete market. We show that with appropriate assumptions on the data input, quantum linear systems solvers are able to provide the derivative price for least-squares markets with the potential of a large speedup over classical algorithms.

All the quantum algorithms assume quantum access to a matrix called payoff matrix (which we define formally in the main text) whose rows represent the assets traded in the market that we consider, and whose columns represent the possible events. If an event indexed by happens, the asset takes on the value . The current value of the assets are described in the vector . The performance of the different algorithms used in this work can be summarized informally as follows, (here is the condition number of the payoff matrix).

Results (Informal - Theorems 3, 16, 7).

Assume to have appropriate quantum access to a price vector of assets, the payoff matrix of a single-period market, and a derivative . Then, with a relative error

-

1.

we can estimate the range of implied present values of the derivative

-

•

with a quantum zero-sum games algorithm, with cost ,

-

•

with a quantum simplex algorithm with cost per iteration, a number of iterations proportional to the classical algorithm, and a final step of operations,

-

•

-

2.

if the market is a least-squares market (Definition 7) we can estimate the price of the derivative with a quantum matrix-inversion algorithm with cost .

Related works

Quantum speedups have been discussed for a large set of problems, including integer factoring, hidden subgroup problems, unstructured search [NC00], solving linear systems [HHL09] and for convex optimization [BS17, Van+20]. Financial applications are receiving increased attention. A quantum algorithm for Monte-Carlo asset pricing given knowledge of the martingale measure was shown in [RGB18]. Similarly, an algorithm for risk management [WE18] and further works on derivative pricing [Sta+19] with amplitude estimation and principal component analysis [Mar+21] were shown with proof-of-principle implementations on quantum hardware. More in-depth reviews are given in [OML19, Bou+20, Her+22]. Zero-sum games are a particular case of minmax games, specifically they are the minmax games. More general quantum algorithms for solving minmax games can be found in [LCW19, Theorem 7] [Li+21].

1.2 Preliminaries

Define . We use boldface for denoting a vector , where the -th entry of the vector is denoted by . With we denote the -th vector in a list of vectors. Denote by the non-negative real numbers. The Kronecker delta is for some integers . Define the simplex of non-negative, -normalized -dimensional vectors and its interior by

| (1) |

For a matrix , the spectral norm is , the Frobenius norm is , and the condition number is , where the pseudoinverse is denoted by . Denote by the -th row of the matrix. We use the notation to hide factors that are polylogarithmic in and the notation to hide factors that are polylogarithmic in and . We assume basic knowledge of quantum computing and convex optimization (in particular linear programming), and we use the same notation that can be found in [NC00] and [BV04].

We refer to Appendix B.2 for a compressed introduction to aspects of probability theory. In general, a probability space is given by a triple , see Definition 13 of Appendix B.2. Our first assumption is the existence of a sample space which is finite (and hence countable). We take the -algebra to be the set of all subsets of . For most of the paper, we do not require the knowledge of the probability measure , a setting which is called Knightian uncertainty [Kni21]. We only require the assumption that for all : it is reasonable to exclude singleton events from that have no probability of occurring. Equivalence of two probability measures and is if, for , if and only if . In our simplified context, this amounts to the statement that if, for , if and only if . Since we assume that , equivalent measures are all measures for which . We denote with the expectation value of the random variable with respect to the probability measure . We refer to Appendix B.2 for formal definitions in probability theory used in this work. In Appendix B.1 we recall some useful definition in linear programming and optimization, and in Appendix B.3 we report some useful definitions and subroutines in quantum numerical linear algebra.

2 Market models, martingale asset pricing, and fundamental theorems of finance

Consider Appendix A for some philosophical aspects of modeling financial markets. In this work, we consider a single-period model, which consists of a present time and a future time. The random variables of the future asset prices are defined on a sample space . We assume that is finite with elements. We consider a market with primary assets, which are risky assets and one safe asset. The risky assets could be stocks and possibly other financial instruments on these stocks, such as simple call options, e.g., , or options involving several stocks, e.g., , where is the strike price. The number of such possible options in principle scales with the number of subsets of the set of stocks , and hence can be quite large. The safe asset acts like a bank account and models the fact that money at different time instances has a different present value due to inflation and the potential for achieving some return on investment. Discount factors are used for comparing monetary values at different time instances. To simplify the notation, we assume in this work that the discount factors are , which corresponds to a risk-free interest rate of [FS04]. Hence, our bank account does not pay any interest. At the present time, the prices of all assets are known. The prices are denoted by for , where for the safe asset. We assume that we can buy and short-sell an arbitrary number and fractions of them at no transaction cost. The prices at the future time are given by the random variables , for , where is not random for the safe asset.

In our setting, risk-neutral pricing will have two conceptual steps. The first step finds probability measures under which the existing asset prices are martingales. Such probability measures are derived from the market prices of the existing assets, and are denoted by in the probability theory context, in the vector notation, and are elements of a set denoted by . Measures should be equivalent to the original probability measure , however, the algorithms here will achieve equivalency only approximately. As a second step, probability measures are used to determine the range of fair prices of the non-traded financial security by computing expectation values. In the remainder of this section, we discuss some background in financial asset pricing. In particular, we recall the concept of Arrow security, the martingale property of financial assets, the definition of arbitrage, and the existence of martingale probability measures.

Arrow security

The notion of an Arrow security [Len04, Var87] is useful in the pricing setting. Arrow securities are imaginary securities that pay one unit of currency, say , in case some event occurs and pay nothing otherwise. Albeit they are not traded in most of the markets, they have historical and theoretical relevance in finance and asset pricing. They allow us to express the future stock prices as a sum of Arrow securities multiplied by respective scaling factors. This separation then naturally leads to a matrix description of the problem of pricing a derivative.

Definition 1 (Arrow security [Var87]).

The Arrow security for is the random variable such that in the event the payoff of the security is:

Since Arrow securities are often not traded in the market, they do not have a price. Their prices may be inferred from the traded securities if these securities can be decomposed into Arrow securities. As we will see, pricing the Arrow securities amounts to finding a probability measure, which in turn can be used for pricing other assets. Arrow securities can be considered as a basis of vectors from which the other financial assets are expanded, as in the next definition. For this definition, we also require the concept of redundancy: here, a redundant asset is a primary asset which can be expressed as a linear combination of the other primary assets.

Definition 2 (Payoffs, payoff matrix, price system).

Let there be given one safe asset with current price of and payoff . Let there be given non-redundant assets with current price and future payoff for . We denote by the associated vector of asset payoffs and by the price vector. Define the payoff matrix such that the assets are expanded as

| (2) |

Finally, we call a price system.

The matrix specifies the asset price for each asset for each market outcome. An interpretation of a single row of the payoff matrix is as a portfolio that holds the amounts in Arrow security . Hence, the random variable is replicated with a portfolio of Arrow securities. However, because of the non-redundancy assumption, it cannot be replicated with the other primary assets. Non-redundancy implies that the matrix has always rank .

Martingale measure

Martingales are defined in Definition 16. For the asset prices, the martingale property means that the current asset prices are fair, that is, they reflect the discounted expected future payoffs. The martingale property is a property of a random variable relative to a probability measure. Martingale probability measures are often denoted by in the financial literature. We want to find such martingale probability measures which are equivalent to the original probability measure . In our setting, equivalency holds if for the new probability measure all probabilities are strictly positive. The probability measure is hence and denoted by . The martingale property of Definition 16 here reads as:

| (3) |

The corresponding probability measure is called equivalent martingale measure or risk-neutral measure, whose existence is discussed below. Finding a risk-neutral measure is equivalent to finding the prices of the Arrow securities. The expectation value of an Arrow security is the probability of the respective event,

| (4) |

Putting together the martingale property for the asset prices of Eq. (3), the expansion into Arrow securities of Eq. (2), and the property of the Arrow securities of Eq. (4) we obtain for the prices of the traded securities:

| (5) |

In matrix form this equation reads as . The set of solutions that are contained in the simplex is given by

| (6) |

Depending on the problem this set is either empty, contains single or multiple elements, or an infinite number of elements. The existence of a solution is discussed below via a no-arbitrage argument. If measures exist, they can be obtained with feasibility methods [BV04]. We note that linear programming formulations do not admit optimization over open sets, i.e., cannot work with strict inequality constraints. Thus we have to work with the closed convex set

| (7) |

As all algorithms in this work are approximation algorithms, the sets and will be considered the same, up to the error tolerance for all the components.

Existence of martingale measure

Now we discuss the existence of a martingale measure, a property that is closely related to the non-existence of arbitrage in the market. Arbitrage is the existence of portfolios that allow for gains without the corresponding risk. A standard assumption in finance is that the market model under consideration is arbitrage-free. No arbitrage implies the existence of a non-negative solution via Farkas’ lemma.

Lemma 1 (Farkas’ lemma [BV04]).

For a matrix and a vector exactly one of the two statements hold:

-

•

there exists a such that and ,

-

•

there exists a such that and .

Note that we are using a slightly modified version of Farkas’ Lemma (whose proof can be found in Appendix B.2), which usually considers only that and . Expressing Lemma 1 in words, in the first case the vector is spanned by a positive combination of the columns of . In the second case, there exists a separating hyperplane defined by a normal vector that separates from the convex cone spanned by the columns of . In the present financial framework, we can think of as a portfolio that is allocated in the different assets. Then, this lemma is immediately applicable to an arbitrage discussion.

Definition 3 (Arbitrage portfolios and no-arbitrage assumption).

An arbitrage portfolio is defined as a portfolio with non-positive present value and non-negative future value for all market outcomes , and at least one such that . The no-arbitrage assumption, denoted by (NA), states that in a market model such portfolios do not exist.

By this definition, expressed as a mathematical statement is

| (8) |

It is easy to see that

| (9) |

since the right hand side is a special case of . Then, if holds Farkas’ lemma implies that case (i) holds, as case (ii) is ruled out by the statement in Eq. (9). Since there exists a such , the set is by its definition not empty. In conclusion, it holds that

| (10) |

Together with the reverse direction, this result is a formulation of the “first fundamental theorem of asset pricing”. There are special cases for which , called complete markets. Before we define complete markets, we formalize the concept of financial derivatives.

Financial derivatives

A financial derivative in the context of this work is a new asset whose payoff can be expanded in terms of Arrow securities and which does not have a current price.

Definition 4 (Financial derivative [FS04]).

A derivative is a financial security given by a random variable . The derivative can be written as an expansion of Arrow’s securities with expansion coefficients , as:

| (11) |

We denote by the vector of arising from the random variable .

This definition includes the usual case when the derivative has a payoff that is some function of one or multiple of the existing assets. As an example, let the function be and the derivative be , for some asset . Then, we have the expansion in Arrow securities .

Complete markets

We define another common assumption for financial theory. Market completeness means that every possible payoff is replicable with a portfolio of the existing assets. Hence it is an extremal case where every derivative is redundant.

Definition 5 (Complete market [FS04, Definition 1.39]).

An arbitrage-free market model is called complete if every derivative (Definition 4) is replicable, i.e., if there exists a vector such that .

A fundamental result relates complete markets to the set of equivalent martingale measures . For complete markets, the martingale measure is unique.

Theorem 1 (Second fundamental theorem of asset pricing [FS04, Theorem 1.40]).

An arbitrage-free market model is complete if and only if .

Thus, there exists a unique martingale measure if and only if every financial derivative is redundant. In an incomplete market, derivatives usually cannot be replicated.

3 Risk-neutral pricing of financial derivatives as a linear program

For pricing a derivative, we use any risk-neutral probability vector , if the set is not empty. Lacking any other information or criteria any element in is a valid pricing measure. The derivative is priced by computing the expectation value of the future payoff under the risk-neutral measure , (discount factors are taken to be )

| (12) |

The price is an inner product between the pricing probability measure and the vector describing the random variable of the financial derivative. Since is convex [FS04], it follows that the set of possible prices of the derivative is a convex set, i.e., an interval. We can formulate as a convex optimization problem to evaluate the maximum and minimum price and , respectively, which are possible over all the martingale measures. We obtain two optimization programs:

| (13) | |||||

| (14) |

When the solution of the optimization problems is a broad range of prices, additional constraints can be added to narrow the range of admissible prices. We discuss a simple case study in Section 4.3, where for a highly incomplete market we can narrow the range of admissible prices of a derivative to its analytic price. In general, additional assets could be added to reduce the number of valid risk-neutral measures, and thus the range of admissible prices.

In the following, we discuss the maximizing program Eq. (13), as the minimizing program is treated equivalently. We make explicit the LP formulation of the problem in Eq. (13). The first step is to replace the open set with the closed set . In that sense, we do not find probability measures that are strictly equivalent to . However, the probability measures in are arbitrarily close to the equivalent probability measures in . We use vector notations and the price system to write the linear program

| (15) |

From Appendix C, we see that the dual of the maximizing program is given by a linear program for the vector as

| (16) |

The financial interpretation is the following. The dual program finds a portfolio of the traded assets which minimizes today’s price . The portfolio attempts to replicate (or “hedge”) the derivative future payoff. Ideal replication would mean , i.e, the payoff of the portfolio of assets is exactly the derivative outcome for all market outcomes. The linear program attempts to find a portfolio that “superhedges” the derivative in the sense that .

In the following Lemma we show how to recast the pricing LP in standard form (as per Definition 9 in the Appendix). Note that we also require the parameters defining the LP to assume values in the interval . For this, we need to assume the knowledge of the following quantities.

Assumption 1 (Assumptions for conversion to standard form LP).

Assume the following.

-

•

Knowledge of , the maximum payoff of the derivative under any event.

-

•

Knowledge of , the maximum entry of the payoff matrix .

Lemma 2 (Normalized standard form LP for Equation 15).

Given Assumption 1, the optimization problem in Eq. (15) can be written as a linear program in standard form as

| (17) |

for , , and .

Proof.

First, use the assumption to normalize the derivative and the payoff matrix . Define , and and , for which . Then, we split the equality constraint into two inequality constraints and . We can now write the extended problem

| (22) |

∎

Note that scaling and by does not change the value of the optimal solution of the LP, but we need to multiply the solution of the LP by to obtain the result of the problem in Eq. (15). As before, the dual of this problem is given by a linear program for the vector as

| (23) |

The financial interpretation is similar to the above. The portfolio is constrained to have only non-negative allocations, but we have assets to invest in with prices and , which allows taking long and short positions. We again find the minimum price of the portfolio that also “superhedges” the derivative via .

4 Quantum zero-sum games algorithm for risk-neutral pricing

A matrix game is a mathematical representation of a game between two players (here called Alice and Bob) who compete by optimizing their actions over a set of strategies. For such a game, let the possible actions of the two players be indexed by and , respectively, and, in the zero-sum setting, let the game be defined by a matrix . The players select the strategy and , and the outcome of a round is for the first player and for the second. One player’s gain is the other’s loss, hence the name zero-sum game. The randomized (or “mixed”) strategies for the players are described by a vector in the simplex for Alice and for Bob, i.e., probability distributions over the actions. If is the strategy of Alice and is the strategy for Bob, the expected payoff for Alice is . Jointly, the goal of the players can be formalized as a min-max problem as:

| (24) |

The optimal value of a game is defined as

| (25) | |||||

This optimal value is always achieved for a pair of optimal strategies . A strategy is called -optimal if . There is a bijection between zero-sum games and linear programs. Following Ref. [AG19, Lemma 12], we can reduce the LP of Lemma 2 to a zero-sum game. In our scenario, the optimal solution is in as and by construction as a probability measure. The problem is solved by binary search on a feasibility problem obtained from the LP. The feasibility problem is deciding if the optimal solution is or , for a parameter . Note that this interval, for our problem, is restricted to , as the normalized value of a derivative is non-negative. After manipulating the LP, one can formulate the decision problem solved at each round of the binary search. Below, we state a version of Ref. [AG19, Lemma 12], made specific to our problem.

Lemma 3 (Zero-sum game for derivative pricing).

Consider the LP in standard form from Lemma 2, with optimal value OPT and optimal strategy , and its dual in Eq. (23) with optimal solution . Let be such that and . For an , the primal LP can be cast as the following LP

| (26) |

where the matrix is defined as

| (36) |

where and , and are column vectors of the appropriate size. Finding the optimal value of the LP in Eq. (26) with additive error suffices to correctly conclude either or for the original LP.

In the previous decision problem, if then adding the constraint to the primal in Lemma 2 will not change the optimal value of the primal. In our case, we know that

| (37) |

Likewise, if then adding the constraint will not change the optimal value of the dual program. The LP in Eq. (26) can be solved via a zero-sum game algorithm, which we choose to be the quantum algorithm from Ref. [AG19]. Solving this linear program obtains a solution vector , a number , and a number from which information on the actual price of the derivative can be obtained. We have two cases: If , then the option price is . If , then the option price is . Performing a binary search on will suffice to estimate the price of the derivative to the desired accuracy.

4.1 Quantum input model

We discuss the input model of our quantum algorithm: an oracle for the price system, and a way of obtaining quantum sampling access to probability distributions. We assume access to the price system and the derivative in the standard quantum query model [BC12] as follows.

Oracle 1 (Zero-sum game pricing oracles).

In most practical cases such as conventional European options, the query access to the derivative can be obtained from a quantum circuit computing the function used to compute the derivative and query access to the payoff matrix . We also define quantum vector access as a black box that builds quantum states proportional to any vector (in our context and ).

Definition 6 (Quantum vector access).

Let with sparsity , and . We say that we have quantum vector access to -dimensional vectors if for any we can construct a unitary in time that performs the mapping

in time, where is an sub-normalized arbitrary quantum state.

There are different ways of building this quantum access. Given quantum query access to the entries of the vector , we can perform the controlled rotation . Moreover, the state with negligible garbage state can be constructed efficiently using pre-computed partial sums and the quantum circuits developed in [GR02, KP20a, KP17]. We refer to Definition 17 for a definition of this type of data structure that can be used with a single vector. In [Ara+21] there is a depth circuit for creating arbitrary quantum states of the form where is a qubit state entangled with the first register [Sun+21]. The quantum access to a vector can be implemented by a quantum random access memory (QRAM) [RML14a, GLM08a, GLM08, De ̵+09]. A QRAM requires quantum switches that are arranged as a branching tree of depth and width to access the memory elements. As shown in [GLM08a, GLM08], the expected number of switches that are activated in a memory call is even though all switches participate to a call in parallel. More discussion on the architecture can be found in [Aru+15, Han+19].

4.2 Quantum algorithm

The quantum algorithm for zero-sum games uses amplitude amplification and quantum Gibbs sampling to achieve a speedup compared to the classical algorithm. We discuss the run time of the classical algorithm for solving LP based on the reduction to a zero-sum game at the end of this section. The quantum computer is used to sample from certain probability distributions created at each iteration. The result [AG19, Lemma 8] is used to prepare the quantum states

| (38) |

via amplitude amplification and polynomial approximation techniques, relying on the oracle access to the matrix . Measuring these quantum states then retrieves classical bit strings corresponding to an index with probability and , respectively. These samples are then used in the steps and , for classically updating the solution vector. The rest of the algorithm remains classical. We state here the main result from [AG19]. An -feasible solution to our LP problem means that we can find a solution such that the constraint is relaxed to .

Theorem 2 (Dense LP solver [AG19, Theorem 13]).

Assume to have suitable quantum query access to a normalized LP in standard form as in Lemma 2, with (defined in Lemma 3) known, along with quantum vector access as in Definition 6 to two vectors . For , there exists a quantum algorithm that finds an -optimal and -feasible with probability using quantum queries to the oracles, and the same number of gates.

Theorem 2, can be directly adapted to the martingale pricing problem to obtain a quantum advantage for the run time, see Algorithm 1. Theorem 2, and the embedding in Lemma 3 imply the following theorem. Here, we discuss how to obtain a relative error for the derivative price.

Theorem 3 (Quantum zero-sum games algorithm for martingale pricing).

Let be a price system with payoff matrix and price vector , and let be a derivative. Assume to have quantum access to the matrix and the vectors and through Oracle 1, and two vectors , and through quantum vector access as in Definition 6. Under Assumption 1, for , Algorithm 1 estimates with absolute error and with high probability using

quantum queries to the oracles, and the same number of gates. The algorithm also returns quantum access to an -feasible solution as in Definition 6.

Proof.

From quantum access to the vectors and , and knowing and we can obtain quantum access to and using quantum arithmetic circuits (see for example [RG17]). From the given oracles and quantum arithmetic circuits, we can derive quantum access to an oracle for the matrix in Eq. (36). It follows from these observations that one query to the entries of costs queries to the oracles in the input. Note that the updating query access to the matrix (Line 30) takes constant time, as we do not need to modify the whole matrix .

In order to estimate the value of the zero-sum game (Line 24) with error and probability greater than we use classical sampling. As stated in [AG19, Claim 2], we require independent samples from and similarly independent samples from . Then, is an estimate of with absolute error . As each repetition of the ZSG algorithm does not return the right value of the game , but only an estimate with absolute error , the condition on for the precision of the binary search of [AG19, Lemma 12] has to be modified to account for this case. This leads to the conditional statements in Line 25 and Line 27. ∎

Note that the original algorithm of Theorem 2 results in an absolute error for , for the normalized problem, which then results in an absolute error of for the value of the derivative.

Theorem 4 (Quantum zero-sum games algorithm for martingale pricing, relative error).

Proof.

In order to achieve a relative error we can run a standard procedure. For an integer , run Algorithm 1 with precision parameter set to and success probability at least . For a given , this will return an estimate such that with success probability at least . Next, conditioned on the event that the algorithm succeeds, check the estimate for . If that does hold, we re-run the algorithm with precision and success probability . This obtains an estimate such that with success probability by the union bound. For the run time, we evaluate , and hence . Set and . If the above criterion does not hold, we increase . The procedure will halt because by assumption . The number of iterations is given by the first such that , which is bounded by . By repeating enough times we can make sure that the total success probability is high. We obtain the estimate with relative error in the price with high probability and with a run time . ∎

Along with the price with relative error, this algorithm returns also a -feasible solution . This solution could be used to price other derivatives . Doing so will often result in an error as large as .

Classical zero-sum games algorithm and condition for quantum advantage

The classical algorithm requires a number of iterations to achieve the relative error for . The cost of the computation for a single iteration is dominated by the update of the two vectors and of size and , respectively. Hence, the classical run time of the algorithm is .

Now we focus on a condition that allows for the quantum algorithm to be faster than the classical counterpart. The run time of the algorithms depends on the parameter , which we can relate to the number of assets required to hedge a derivative.

Remark 1.

Consider the context of Lemma 2 and its dual formulation. For any vector , note that . In addition, if , we have . In our setting, where is the optimal portfolio and is the number of assets in the optimal portfolio, we hence can use .

To obtain an advantage in the run time of the quantum algorithm we have to presuppose the following for .

Theorem 5.

If the derivative requires asset allocations to be replicated, where , then Algorithm 1 performs less queries to the input oracles compared to the classical algorithm.

Proof.

Since the number of iterations is the same, we focus on the query complexity of a single iteration. To find the upper bound for which up to logarithmic factors still allows for a speedup, we need to find such that . Thus,

| (39) |

By Remark 1, we have an advantage in query complexity if the number of assets in the optimal portfolio is bounded by . ∎

4.3 Linear programming martingale pricing with the Black-Scholes-Merton model

We show a simple example motivated by the standard Black-Scholes-Merton (BSM) framework. In our example the payoff matrix can be efficiently computed, and hence access to large amounts of additional data is not required. The consequence is that instead of having quantum access to directly, for example from a QRAM of size , we only require access to data of size . Moreover, we show an example of how an additional constraints in the LP can regularize the model, so to narrow the range of admissible price. For a call option, which we consider in this example, the price can be computed analytically. We show how to make the range of prices of the solutions of our linear programs comparable to the analytic value of the derivative.

In the BSM model, the market is assumed to be driven by underlying stochastic processes (factors), which are multidimensional Brownian motions. Multi-factor models have a long history in economics and finance [Bai03]. The dimension and other parameters of the model, like drift and volatility, can be estimated from past market data [Bjö09, May95, BBF04]. An advantage of modeling the stocks with the BSM model is that it often allows to solve analytically the pricing problem for financial derivatives.

Pricing with a measure change

An importation notion in pricing is the change of measure from the original measure to the martingale measure. The change of measure is described by the Radon-Nikodym derivative, which denoted by the random variable . We formulate the problem of pricing a derivative, given that we have an initial probability measure via a vector and consider the measure change to a new probability measure via the vector . The Radon-Nikodym derivative in this context is an for which

| (40) |

The martingale property for the assets under and the pricing of a derivative are formulated as

| (41) | |||||

| (42) |

Hence, using for the Hadamard product (element-wise product) between vectors, and , we obtain the linear program for the maximization problem of Eq. (13) of the Radon-Nikodym derivative

| (43) |

The minimization problem is obtained similarly.

Discretized Black-Scholes-Merton model for a single time step.

We perform our first drastic simplification and set the number of risky assets to be . This makes the market highly incomplete but simplifies the modeling. While the Brownian motion stochastic process has a specific technical definition, in the single-period model a Brownian motion becomes a Gaussian random variable. Hence, we assume here that we have a single Gaussian variable driving the stock. Let be the Gaussian random variable, also denoted by distributed under the measure . The future stock price is modeled as a function of . In BSM-type models, asset prices are given by a log-normal dependency under ,

| (44) |

using today’s price , the volatility , and the drift .

The stock price is not a martingale under , which can be checked by evaluating . However, it can be shown that under a change of probability measure, the Gaussian random variable can be shifted such that the resulting stock price is a martingale. The following lemma is a simple version of Girsanov’s theorem for measure changes for Gaussian random variables.

Lemma 4 (Measure change for Gaussian random variables [Shr05]).

Let under a probability measure . For define . Then, under a probability measure , where this measure is defined by .

In standard Black-Scholes theory, we use to obtain under where

| (45) |

We can check that satisfies the key property of a martingale as , with . Many financial derivatives can be priced in the Black-Scholes-Merton model by analytically evaluating the expectation value under of the future payoff. We use this analytically solvable model as a test case for the linear programming formulation. In order to fit this model into our framework, we need to discretize the sample space. In contrast to the standard BSM model, we take a truncated and discretized normal random variable centered at on the interval . We take the sample space to be and . The size of the space is . The probability measure for , is , where . In analogy to the BSM model, we define the payoff matrix of future stock prices as

| (46) |

where . An important property of this example is that each , can be computed in time and space via Eq. (46). For settings with more than a single asset , if we have more than one, say , Gaussian random variables driving the assets, we expect this cost to be .

Call option.

We define the simple case of an European call option. The European call option on the risky asset gives the holder the right but not the obligation to buy the asset for a predefined price, the strike price. Hence, the future payoff is defined as

| (47) |

where is the strike price. Using the stock prices from Eq. (46), for a specific event the payoff under is

| (48) |

Numerical tests.

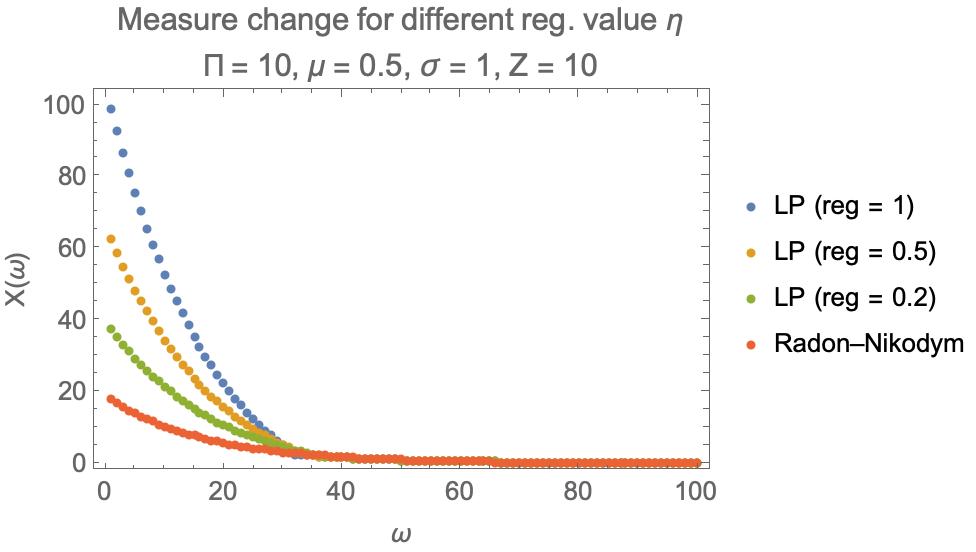

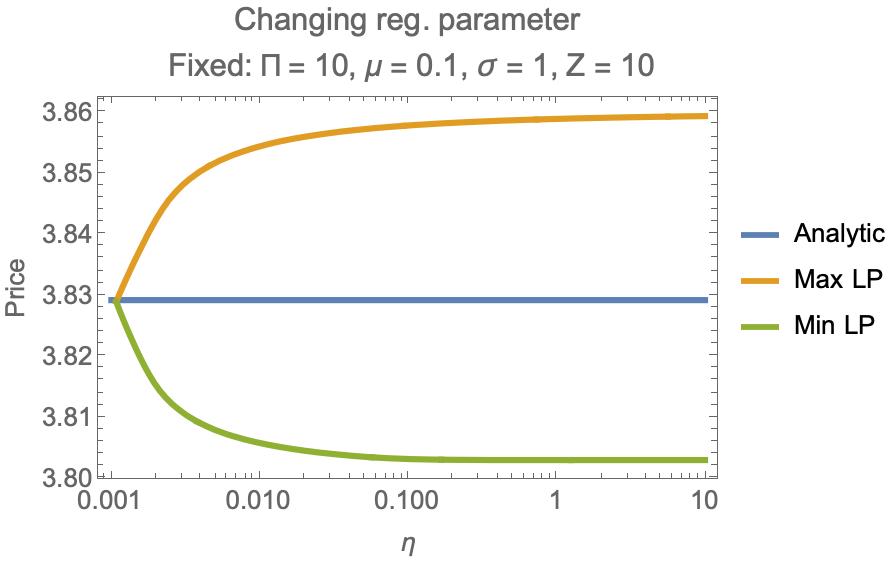

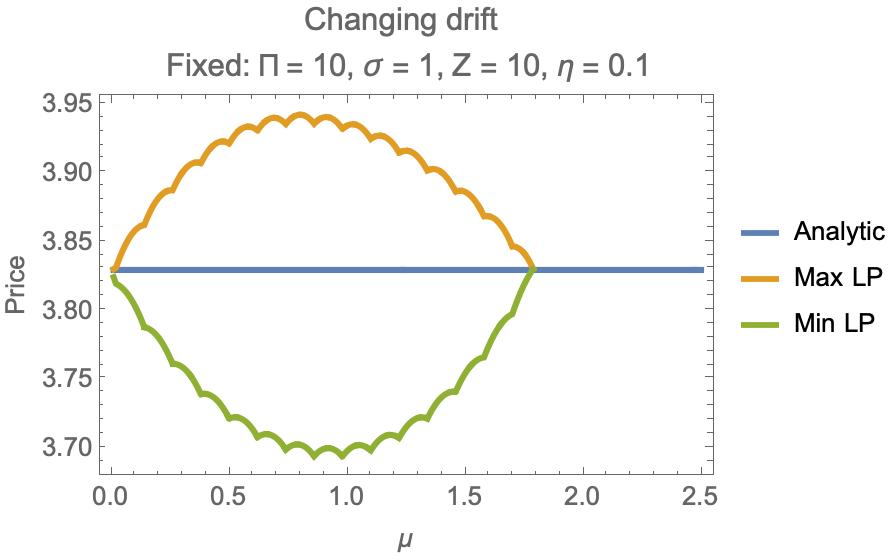

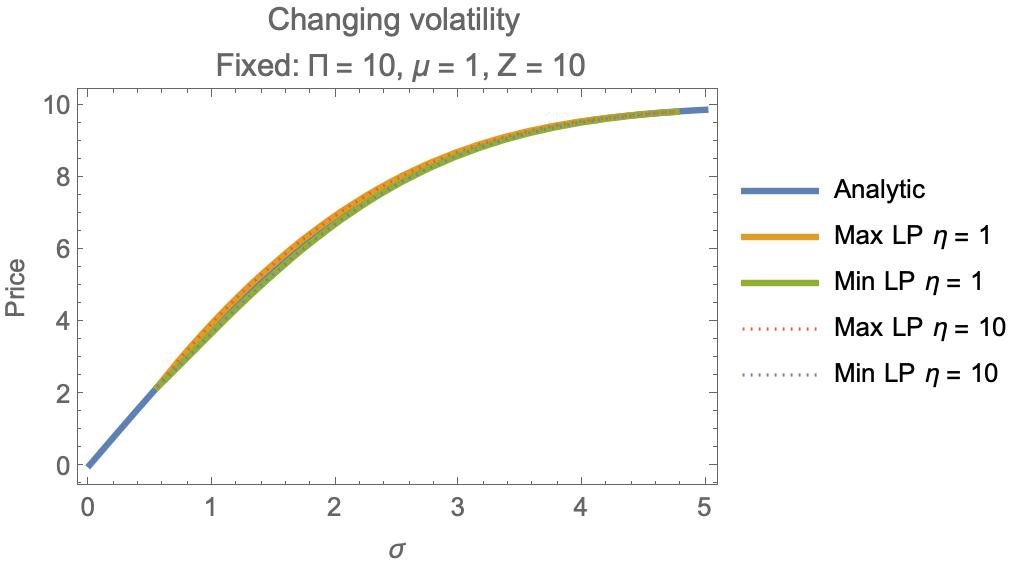

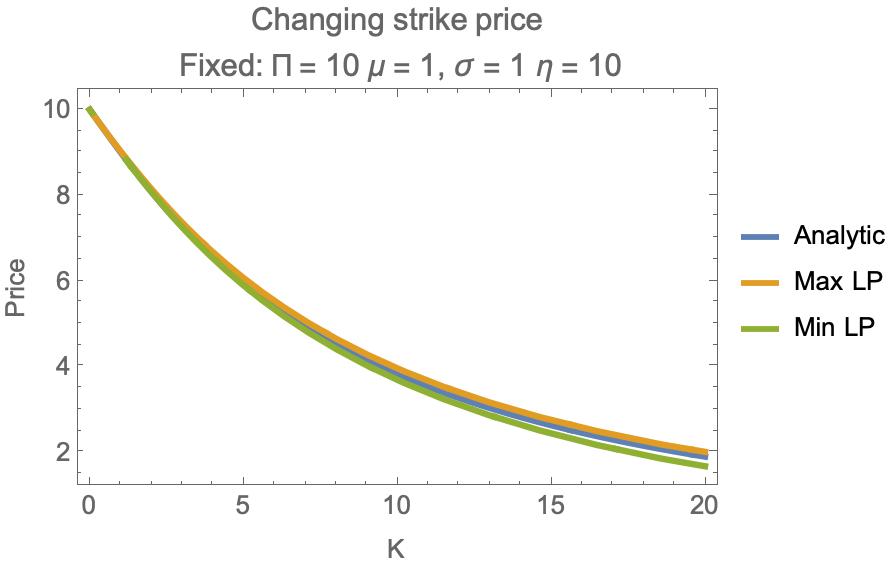

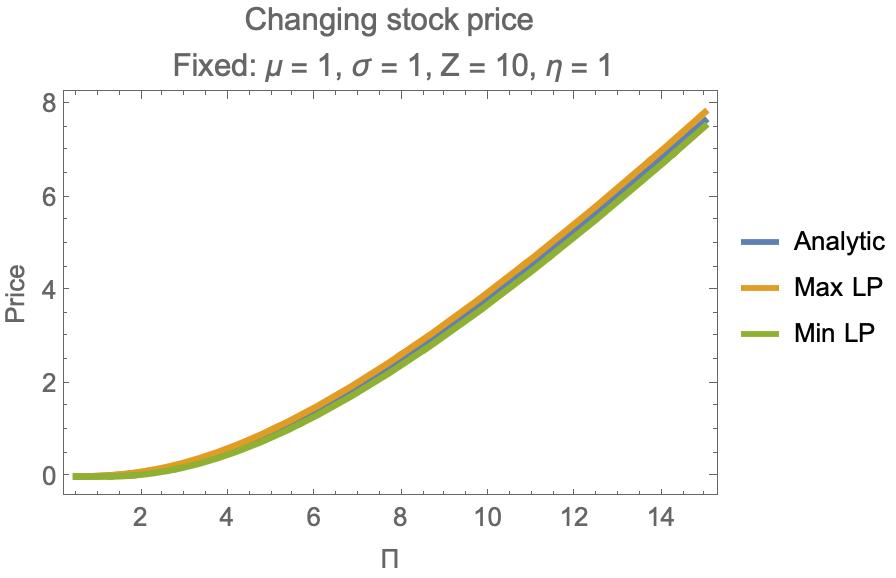

We now test this approach for the call option, using the linear program in Eq. (43), its minimization form, and the payoff matrix Eq. (46). In Appendix D we present the main numerical results. We compare the approach to the analytical price derived from the Black-Scholes-Merton model. Our optimization framework allows for a much larger set of Radon-Nikodym derivatives (all entry-wise positive -dimensional vectors) than the set implied from the BSM framework. We observe that this freedom allows for a large range of prices corresponding to idiosyncratic solutions for the measure change. To find solutions closer to the Black-Scholes measure change, we develop a simple regularization technique. This regularization is performed by including a constraint for the slope of into the LP, see Appendix D. The regularization leads to a narrowing of the range of admissible prices. We find that for a broad enough range of parameters, the analytic price of the derivative is contained in the interval of admissible prices given by the maximization and minimization linear programs of Eq. (43). The regularization is successful in recovering the BSM price for strong regularization parameter. In that sense, this linear programming framework contains the BSM model and allows to model effects beyond the BSM-model.

Instead of using the regularization, there could be other approaches to narrow the range between admissible prices. An approach founded in the theory is to complete the market with assets for which we know the price analytically/from the market. When there are more benchmark assets, we expect the range of prices to narrow. In the limit of a complete market, every derivative has a unique price. We leave this approach for future work.

Towards a quantum implementation.

The requirement for an efficient quantum algorithm is to have query access to oracles (as in Oracle 1) for the vectors. For the payoff matrix we can build efficient quantum circuits, without requiring large input data. To create the mapping , we have to have classical access to input quantities such as drift and volatility, quantum access to the prices, and apply the arithmetic operations in Eq. (46). Following the same reasoning, since the vector is efficiently computable from the matrix , we can build efficient query access to its entries. We remark that such efficient computation can hold also for more complicated models (i.e., models that are more complicated than log-normal such as Poisson jump processes or Levy heavy-tailed distributions).

5 Quantum matrix inversion for risk-neutral pricing

Taking insight from the fact that the sought-after measure is a vector satisfying the linear system , we consider in this section the quantum linear systems algorithm ([HHL09], and successive improvements [Gil+19, CGJ19]) for solving the pricing problem. Given the right assumptions about the data input and output, one could hope to obtain an exponential speedup for the pricing problem. However, the quantum linear systems algorithm cannot directly be used to find positive solutions for an underdetermined linear equations system [RML14]. The constraint involves constraints of the form , which all have to be enforced. We may be able to apply the quantum linear systems algorithm if we demand a stronger no-arbitrage condition, as will be discussed in the present section. With quantum linear systems algorithms we can prepare a quantum state that is proportional to , where is a price system and is the pseudo-inverse of the matrix . A well-known fact (which we recall in Theorem 10 in the Appendix) is that the pseudo-inverse of finds the minimum norm solution to a linear system of equations. Unfortunately, this solution can lie outside the positive cone, and thus outside , so we need a stronger no-arbitrage condition to guarantee finding a valid probability measure. We have to assume that one of the valid probability measures in - whose existence follows from the no-arbitrage assumption of Definition 3 - is indeed also the minimum -norm solution. A market satisfying this condition we call a least-square market.

Definition 7 (Least-squares market).

An arbitrage-free market model is called a least-squares market if .

Under this assumption, the pseudo-inverse is guaranteed to find a positive solution to . This assumption is obviously stronger than the no-arbitrage assumption (Assumption 3), which only implies that . However, it is not as strong as assuming market completeness, see Definition 5, which means that every possible payoff is replicable with a portfolio of the assets. We now state an intermediate result for the rank of .

Lemma 5.

Let be a price system, as in Definition 2. The market model is complete if and only if and the matrix has full rank.

Proof.

If the market is complete, any contingent claim is attainable. For a contingent claim let be a replicating portfolio so that . Since can be any vector in , the column space of must have dimension equal to . Since we assume non-redundant assets, it must hold that and has full column rank. Now assume that has full rank and that the number of assets is equal to the number of events (i.e. ). Having full rank implies that the matrix is invertible, and thus is the unique replicating portfolio. ∎

From the second fundamental theorem of asset pricing (Theorem 1), there exists a unique martingale measure if and only if every financial derivative is redundant, i.e., replicable via a unique portfolio of traded assets. If the market is not complete, a derivative is in general not replicated. The next theorem states that market completeness is a stronger assumption than the assumption of a least-square market.

Theorem 6.

Let be a price system, as in Definition 2. If the market model is complete, it is also a least-squares market.

Proof.

Market completeness, via Theorem 1, implies that , so there exists a unique measure such that and . Market completeness, via Lemma 5, implies that the matrix is square and has full rank. Define the pseudo-inverse solution as . Since , and the assets are non-redundant, satisfies and is the unique solution to the equation system. Thus, must also have the property of being in and . ∎

Market completeness is usually a rather strong hypothesis, while least-square market includes a broader set of markets. Both the market completeness and the weaker least-squares market conditions enable the use of quantum matrix inversion for finding a martingale measure. Even weaker conditions may also suffice for the use of quantum matrix inversion. For instance, markets where some is -close to may be also be good candidates. Another case could arise in the situation where there is a vector in the null space of such that . We leave the exploration of weaker assumptions for future work.

In this part of the work, we assume block-encoding access to [Gil+19].

Definition 8 (Block-encoding).

Let . We say that a unitary is a ( block encoding of if

Often the shorthand -block encoding is used which does not explicitly mention the number of ancillary qubits. An -block encoding can be obtained with a variety of access models [KP20a, CGJ19]. Note that the matrix is in general not sparse, as most events will not lead to zero stock prices. To satisfy Definition 8 and the hypothesis of Theorem 11, we use the standard trick of obtaining a symmetric version of by creating an extended matrix with in the upper-right corner and in the bottom-left corner, and everywhere else. In the following, we assume w.l.o.g that and are power of (if they are not, we can always pad the matrix and the vectors with s) and we do not introduce a new notation for the padded quantities.

Under the assumption that the matrix can be efficiently accessed in a quantum computer, we can prepare a quantum state for the martingale measure in time to accuracy [HHL09, CKS17, CGJ19, Gil+19]. Using the quantum state for the probability measure, one can then price the derivative by computing an inner product with another quantum state representing the derivative. This will result in a run time that will depend linearly in the precision required in the estimate of the value of the derivative and further scaling factors given by the normalization of the vector representing the derivative and the martingale measure as a quantum state.

Theorem 7 (Quantum pseudo-inverse pricing in incomplete least-squares markets).

Let be the price system of a least-squares market with the extended payoff matrix satisfying and . Let be a -block-encoding of matrix , and assume to have quantum access as Definition 17 to the extended price vector and the extended derivative vector . Let and , where is the projector into the column space of . For and , there is a quantum algorithm that estimates with relative error and high probability using queries to the oracles.

Proof.

With , the price of the derivative can be rewritten as:

| (49) |

It is simple to check (using the triangle inequality) that to estimate with relative error it suffices to estimate and with relative error , as we have exact knowledge of and (due to the availability of Definition 17). The idea is to use Theorem 11 for the ability to prepare the state , estimate the normalizing factor, and then perform a swap test between and . Using , and Theorem 11 we can prepare a state close to , with a run time poly-logarithmic factor in the precision. Let , , and the cost in terms of elementary gates for having quantum access to , , and . Producing with Theorem 11 has a cost in terms of elementary gates of

| (50) |

Estimating with relative error has a cost of according to Theorem 12. We now estimate with relative error the value with a standard trick which requires calls to the unitaries generating and . Prepare the state

| (51) |

and then use amplitude estimation (Theorem 14) to estimate the probability of measuring in the first qubit, which is . To obtain a relative error of on we set . Thus, the number of queries to the unitaries preparing the two states is . The total run time is the sum of the two estimations but the inner product estimation has an additional factor of at the denominator, and therefore dominates the run time. Repeating the algorithm for a logarithmic number of times achieves a high success probability via the union bound. The final run time is . ∎

Interestingly, when the market is complete, the factor is just , so we can think of this parameter as a “measure” of market incompleteness, which is reflected in the run time of our algorithm (and can be estimated with amplitude estimation). In addition, if we want to recover an approximation of the risk-neutral measure . Obtaining an estimate of allows to price derivatives classically.

Theorem 8 (Estimation of the martingale measure).

Consider the same settings as Theorem 7. For , there is a quantum algorithm that returns a classical description of , such that a derivative can be priced as follows. Given a derivative we can estimate with relative error using queries to the oracles.

Proof.

Let be the -norm unit vector obtained through tomography (Theorem 13 in the appendix) on the quantum state with error . As in Theorem 7, we can take that with negligible error. Let our estimate of with error . Let be the estimate of the vector . For pricing a derivative, rewrite . Using Cauchy-Schwarz, we can also bound . Thus, we want to find and such that . From triangle inequality it is simple to check that . With , we obtain that . The run time for obtaining is and the run time for amplitude estimation is . ∎

In conclusion, assuming a least-square market (Definition 7) - which is weaker condition than the assumption of market completeness - there may exist special situations when there is the potential for an exponential speedup using the quantum linear systems algorithm.

6 Discussion and conclusions

The study of quantum algorithms in finance is motivated by the large amount of computational resources deployed for solving problems in this domain. This work explored the use of quantum computers for martingale asset pricing in one-period markets, with specific focus on incomplete markets. Contrary to other works in quantum finance, our algorithms are not directly based on quantum speedups of Monte Carlo subroutines [Mon15], albeit they use similar subroutines (e.g., amplitude amplification and estimation). One algorithm discussed here is based on the quantum zero-sum games algorithm (Theorem 3), one is based on the pseudoinverse algorithm (Theorem 7), and one is based on the quantum simplex method (Theorem 16). They all output a price with relative error. The martingale measure obtained from the zero-sum game and the simplex algorithm returns a value that maximizes (or minimizes) the price over the convex set of martingale measures. Moreover, the quantum zero-sum game algorithm returns an -feasible measure, which is to be interpreted as a solution where every constraint is satisfied up to a tolerance . Theorem 8 and Theorem 17 allow to extract the martingale measure using the quantum simplex method and quantum pseudoinverse algorithm. We studied the conditions under which the quantum zero-sum game is better than the classical analogue and under which the simplex method is expected to beat the the zero-sum game method.

In the quantum algorithms based on matrix inversion and the simplex method, there is a factor (for ) in the run times. In many cases, this factor could be bounded by economic reasoning. For instance, put/call options that only with very small probability, say , give a non-zero payoff, are usually not traded or modeled. Most common derivatives have a large enough number of events when they have some pay-out. Hence, the run time cost introduced by the factor is not expected to grow polynomially with and . We can draw similar conclusions for the factor for some derivatives. For example, a put option with a strike price of of a stock which trades at a market value of , described by a BSM with and has a price of dollars. The value of (using the discretizations used in the experiments of this work) is , making the value of .

We remark again that all algorithms will not return an equivalent martingale measure per Definition 14. The output of the zero-sum games algorithm will be sparse, which follows directly from the total number of iterations. However, this algorithm is still good enough to return an approximation of the derivative price with the desired precision. The quantum algorithms based on the simplex and the pseudo-inverse algorithm are able to create quantum states that are -close to an equivalent martingale measure.

In this work, we propose a new class of market models called least-square markets (Definition 7). This market condition, which is weaker than market completeness, is particularly interesting for quantum algorithms, as it may allow for large speedups in martingale asset pricing using the quantum linear systems algorithm. It remains to be seen if the market condition can be weakened further for a broader application of the quantum linear systems algorithm.

Along with the future research directions already discussed in the manuscript, we propose to study quantum algorithms for risk-neutral asset pricing in a parametric setting, i.e., when it is assumed that the martingale probability measure comes from a parameterized family of probability distributions. It is also interesting to estimate the quantum resources for the algorithms proposed in this manuscript in real-world settings (i.e., in a realistic market model for which the parameters , , and have been estimated from historical data, realistic assumptions on a given hardware architectures like error correction codes, noise models, and connectivity, and so on). We also leave as future work the study of other algorithms based on other quantum subroutines for solving linear programs, like interior-point methods [KP20, CM20].

7 Acknowledgements

We thank Nicolò Cangiotti for pointing us to useful citations in history of probability theory. Research at CQT is funded by the National Research Foundation, the Prime Minister’s Office, and the Ministry of Education, Singapore under the Research Centres of Excellence programme’s research grant R-710-000-012-135. We also acknowledge funding from the Quantum Engineering Programme (QEP 2.0) under grant NRF2021-QEP2-02-P05.

References

- [AG19] J. Apeldoorn and A. Gilyén “Quantum algorithms for zero-sum games”, 2019

- [Ara+21] Israel F Araujo, Daniel K Park, Francesco Petruccione and Adenilton J Silva “A divide-and-conquer algorithm for quantum state preparation” In Scientific reports 11.1 Nature Publishing Group, 2021, pp. 1–12

- [Aru+15] Srinivasan Arunachalam et al. “On the robustness of bucket brigade quantum RAM” In New Journal of Physics 17.12 IOP Publishing, 2015, pp. 123010

- [Bai03] Jushan Bai “Inferential theory for factor models of large dimensions” In Econometrica 71.1 Wiley Online Library, 2003, pp. 135–171

- [BBF04] Henri Berestycki, Jérôme Busca and Igor Florent “Computing the implied volatility in stochastic volatility models” In Communications on Pure and Applied Mathematics: A Journal Issued by the Courant Institute of Mathematical Sciences 57.10 Citeseer, 2004, pp. 1352–1373

- [BC12] Dominic W. Berry and Andrew M. Childs “Black-box Hamiltonian Simulation and Unitary Implementation” In Quantum Info. Comput. 12.1-2 Paramus, NJ: Rinton Press, Incorporated, 2012, pp. 29–62

- [Bjö09] Tomas Björk “Arbitrage theory in continuous time” Oxford university press, 2009

- [Bou+20] Adam Bouland et al. “Prospects and challenges of quantum finance” In arXiv preprint arXiv:2011.06492, 2020

- [BR96] Martin Baxter and Andrew Rennie “Financial calculus: an introduction to derivative pricing” Cambridge University Press, 1996

- [Bra+02] Gilles Brassard, Peter Hoyer, Michele Mosca and Alain Tapp “Quantum amplitude amplification and estimation” In Contemporary Mathematics 305 Providence, RI; American Mathematical Society; 1999, 2002, pp. 53–74

- [BS17] Fernando G… Brandao and Krysta Svore “Quantum speed-ups for semidefinite programming” In FOCS 17 Proceedings of the 45th Annual IEEE Symposium on Foundations of Computer Science, 2017 IEEE Computer Soc.

- [BS73] Fischer Black and Myron Scholes “The Pricing of Options and Corporate Liabilities” In Journal of Political Economy 81, 1973, pp. 637–654

- [BV04] S. Boyd and L. Vandenberghe “Convex Optimization” Cambridge University Press, 2004

- [Čer09] Aleš Černý “Mathematical techniques in finance” Princeton University Press, 2009

- [CGJ19] Shantanav Chakraborty, András Gilyén and Stacey Jeffery “The Power of Block-Encoded Matrix Powers: Improved Regression Techniques via Faster Hamiltonian Simulation” In 46th International Colloquium on Automata, Languages, and Programming (ICALP 2019), 2019 Schloss Dagstuhl-Leibniz-Zentrum fuer Informatik

- [CKS17] A. Childs, R. Kothari and R. Somma “Quantum Algorithm for Systems of Linear Equations with Exponentially Improved Dependence on Precision” In SIAM Journal on Computing 46.6, 2017, pp. 1920–1950

- [CM20] Pablo AM Casares and Miguel Angel Martin-Delgado “A quantum interior-point predictor–corrector algorithm for linear programming” In Journal of physics A: Mathematical and theoretical 53.44 IOP Publishing, 2020, pp. 445305

- [Cox46] Richard T Cox “Probability, frequency and reasonable expectation” In American journal of physics 14.1 American Association of Physics Teachers, 1946, pp. 1–13

- [De ̵+09] Francesco De Martini et al. “Experimental quantum private queries with linear optics” In Physical Review A 80.1 APS, 2009, pp. 010302

- [FS04] H. Föllmer and A. Schied “Stochastic Finance: An Introduction in Discrete Time” Walter de Gruyter, 2004

- [Gil+19] András Gilyén, Yuan Su, Guang Hao Low and Nathan Wiebe “Quantum singular value transformation and beyond: exponential improvements for quantum matrix arithmetics” In Proceedings of the 51st Annual ACM SIGACT Symposium on Theory of Computing, 2019, pp. 193–204

- [Gla03] Paul Glasserman “Monte Carlo Methods in Financial Engineering” Springer-Verlag, 2003

- [GLM08] V. Giovannetti, S. Lloyd and L. Maccone In Phys. Rev. A 78, 2008, pp. 052310

- [GLM08a] V. Giovannetti, S. Lloyd and L. Maccone In Phys. Rev. Lett. 100, 2008, pp. 160501

- [GR02] L. Grover and T. Rudolph “Creating superpositions that correspond to efficiently integrable probability distributions” In arXiv:quant-ph/0208112, 2002

- [Han+19] Connor T Hann et al. “Hardware-efficient quantum random access memory with hybrid quantum acoustic systems” In Physical Review Letters 123.25 APS, 2019, pp. 250501

- [Her+22] Dylan Herman et al. “A Survey of Quantum Computing for Finance” In arXiv preprint arXiv:2201.02773, 2022

- [HHL09] Aram W Harrow, Avinatan Hassidim and Seth Lloyd “Quantum algorithm for linear systems of equations” In Physical review letters 103.15 APS, 2009, pp. 150502

- [Hul12] John C. Hull “Options, futures, and other derivatives” Prentice Hall, 2012

- [KF57] Andreĭ Nikolaevich Kolmogorov and Sergeĭ Vasil’evich Fomin “Elements of the theory of functions and functional analysis” Courier Corporation, 1957

- [KLP19] Iordanis Kerenidis, Jonas Landman and Anupam Prakash “Quantum Algorithms for Deep Convolutional Neural Networks” In International Conference on Learning Representations, 2019

- [Kni21] Frank Hyneman Knight “Risk, uncertainty and profit” Houghton Mifflin, 1921

- [KP17] Iordanis Kerenidis and Anupam Prakash “Quantum Recommendation Systems” In 8th Innovations in Theoretical Computer Science Conference (ITCS 2017) 67, Leibniz International Proceedings in Informatics (LIPIcs) Dagstuhl, Germany: Schloss Dagstuhl, 2017, pp. 49:1–49:21

- [KP20] Iordanis Kerenidis and Anupam Prakash “A quantum interior point method for LPs and SDPs” In ACM Transactions on Quantum Computing 1.1 ACM New York, NY, USA, 2020, pp. 1–32

- [KP20a] Iordanis Kerenidis and Anupam Prakash “Quantum gradient descent for linear systems and least squares” In Physical Review A 101.2 APS, 2020, pp. 022316

- [LCW19] Tongyang Li, Shouvanik Chakrabarti and Xiaodi Wu “Sublinear quantum algorithms for training linear and kernel-based classifiers” In International Conference on Machine Learning, 2019, pp. 3815–3824 PMLR

- [Len04] Yvan Lengwiler “Microfoundations of financial economics: an introduction to general equilibrium asset pricing” Princeton University Press Princeton, 2004

- [Li+21] Tongyang Li, Chunhao Wang, Shouvanik Chakrabarti and Xiaodi Wu “Sublinear classical and quantum algorithms for general matrix games” In Proceedings of the AAAI Conference on Artificial Intelligence 35.10, 2021, pp. 8465–8473

- [LP11] Antonio Lijoi and Igor Prünster “A conversation with Eugenio Regazzini” In Statistical Science 26.4 Institute of Mathematical Statistics, 2011, pp. 647–672

- [Mar+21] Ana Martin et al. “Toward pricing financial derivatives with an ibm quantum computer” In Physical Review Research 3.1 APS, 2021, pp. 013167

- [May95] Stewart Mayhew “Implied volatility” In Financial Analysts Journal 51.4 Taylor & Francis, 1995, pp. 8–20

- [Mer73] Robert C. Merton “Theory of Rational Option Pricing” In The Bell Journal of Economics and Management Science 4.1, 1973, pp. 141–183

- [Mon15] Ashley Montanaro “Quantum speedup of Monte Carlo methods” In Proc. R. Soc. A 471, 2015, pp. 0301

- [Nan19] Giacomo Nannicini “Fast quantum subroutines for the simplex method” In arXiv preprint arXiv:1910.10649, 2019

- [Nan21] Giacomo Nannicini “Fast quantum subroutines for the simplex method” In Integer Programming and Combinatorial Optimization: 22nd International Conference, IPCO 2021, Atlanta, GA, USA, May 19–21, 2021, Proceedings 22, 2021, pp. 311–325 Springer

- [NC00] M.. Nielsen and I.L. Chuang “Quantum computation and quantum information” Cambridge University Press, 2000

- [OML19] Roman Orus, Samuel Mugel and Enrique Lizaso “Quantum computing for finance: Overview and prospects” In Reviews in Physics 4, 2019, pp. 100028

- [RG17] Lidia Ruiz-Perez and Juan Carlos Garcia-Escartin “Quantum arithmetic with the quantum Fourier transform” In Quantum Information Processing 16.6 Springer, 2017, pp. 152

- [RGB18] Patrick Rebentrost, Brajesh Gupt and Thomas R. Bromley “Quantum computational finance: Monte Carlo pricing of financial derivatives” In Phys. Rev. A 98, 2018, pp. 022321

- [RML14] P. Rebentrost, M. Mohseni and S. Lloyd In Physical Review Letters 113, 2014, pp. 130503

- [RML14a] Patrick Rebentrost, Masoud Mohseni and Seth Lloyd “Quantum support vector machine for big data classification” In Physical review letters 113.13 APS, 2014, pp. 130503

- [Shr05] Steven Shreve “Stochastic calculus for finance I: the binomial asset pricing model” Springer Science & Business Media, 2005

- [Sta+19] Nikitas Stamatopoulos et al. “Option Pricing using Quantum Computers” In arXiv:1905.02666, 2019

- [Str+93] Gilbert Strang, Gilbert Strang, Gilbert Strang and Gilbert Strang “Introduction to linear algebra” Wellesley-Cambridge Press Wellesley, MA, 1993

- [Sun+21] Xiaoming Sun et al. “Asymptotically optimal circuit depth for quantum state preparation and general unitary synthesis” In arXiv preprint arXiv:2108.06150, 2021

- [Tao11] Terence Tao “An introduction to measure theory” American Mathematical Society Providence, RI, 2011

- [Van+20] Joran Van Apeldoorn, András Gilyén, Sander Gribling and Ronald Wolf “Quantum SDP-solvers: Better upper and lower bounds” In Quantum 4 Verein zur Förderung des Open Access Publizierens in den Quantenwissenschaften, 2020, pp. 230

- [Var87] Hal R Varian “The arbitrage principle in financial economics” In Journal of Economic Perspectives 1.2, 1987, pp. 55–72

- [WE18] Stefan Woerner and Daniel J. Egger “Quantum Risk Analysis” In arXiv:1806.06893, 2018

- [Wil14] David P. Williamson “ORIE 6300: Mathematical Programming I - Lecture 7” Cornell University, 2014

- [Wil16] David P. Williamson “ORF523 Convex and Conic Optimization - Lecture 5” Princeton University, 2016

- [YZ05] Raphael Yuster and Uri Zwick “Fast sparse matrix multiplication” In ACM Transactions On Algorithms (TALG) 1.1 ACM New York, NY, USA, 2005, pp. 2–13

Appendix A Aspects of market modeling

We briefly discuss three aspects of modeling markets, the sample space, the payoffs, and the no-arbitrage assumption. First, an important question in probability theory is where the sample space comes from [LP11, Cox46]. There is a “true” underlying , which describes the sample space affecting the financial assets. Each element would describe a state of the whole financial market or the outcome of a tournament. Especially in finance, this space is rarely observed or practical and one assumes certain models for the financial market. Such a model contains events which shall described by a sample space , which we work with here. An example of this space are the trajectories of a binomial stochastic process.

Second, a similar question as for the sample space arises regarding the availability of the payoffs (introduced below in Definition 2). There exists a “true” mapping which relates elements in to the financial asset prices. There will be some relation between the state of the financial market and the stock price of a company. As mentioned, usually one works with some model sample space . Hence, one considers a matrix with relates events to price outcomes. Such a matrix can in some cases be generated algorithmically or from historical data. We discuss an example in Section 4.3 motivated by the Black-Scholes-Merton model.

Third, consider the notion of arbitrage which is the existence of investments that allow for winnings without the corresponding risk, see Definition 3 in our context. The scope of the discussion on arbitrage depends if one considers the “true” setting or the model setting . For the “true” market, one often assumes the efficient market hypothesis. While strongly debatable, the efficient market hypothesis states that all the information is available to all market participants and instantaneously affects the prices in the market. In other words, the market has arranged the current asset prices in a way that arbitrage does not exist. Of course, the existence of certain types of hedge funds and speculators proves that such an assumption is not realistic, especially on short time scales. However, it is often a reasonable first approximation for financial theory. In the model, the absence of arbitrage is a requirement rather than an assumption. If one assumes that the underlying true market is arbitrage-free (efficient-market hypothesis), then the model market should also be designed in an arbitrage-free way. If a model admits arbitrage opportunities, one needs to consider a better model. While the task of finding appropriate models for specific markets is outside the scope of this work, we show an example in Section 4.3.

Appendix B Further notions and preliminary results

B.1 Linear programming and optimization

We introduce the standard form of a LP. For an inequality vector with we mean that for all .

Definition 9 (Standard form of linear program (LP) [BV04]).

For a matrix where , , a linear program in standard form is defined as the following optimization problem:

Note that a minimization problem can be turned into a maximization problem simply by changing to . It is often the case that an LP problem is formulated in a non-standard form, i.e. when we have inequality constraints different than or the equality constraint . It is usually simple to convert a LP program in non-standard form into a LP in standard form. For instance, an equality constraint can be cast into two inequality constraint as and .

Farkas’ Lemma is a standard result in optimization [Wil14, Wil16]. We present here a version slightly adjusted to our needs. Specifically, we need the vector to be strictly greater than in each component. This is needed because we need a probability measure to be equivalent (as in Definition 14) to the original probability measure (which is non-zero on the singletons of our -algebra). We state two theorems that we will use in the proof of Farkas’ Lemma. The first, is a lemma to the separating hyperplane theorem, while the second is about closedness and convexity of a cone.

Lemma 6 ([BV04, Example 2.20]).

Let be a closed convex set and a point not in . Then and can be strictly separated by a hyper plane, i.e.

The previous lemma states that a point and a closed convex set can be strictly separated by a hyperplane: strict separation - i.e. having strict inequalities in both directions - is not always possible for two closed convex sets [BV04, Exercise 2.23]. Note that the direction of the inequalities can be changed by considering instead of .

Lemma 7.

Let . Then is closed and convex.

Theorem 9 (Farkas’ Lemma).

Let , and . Then, only one of the following two proposition holds:

-

•

.

-

•

.

Proof.

We first show that both conditions cannot be true at the same time. We do this by assuming that both propositions holds true, and we derive a contradiction. By using the definition of in the second inequality, it is simple to obtain that , which is a contradiction. The last inequality follows the positivity of an inner product between two vectors with strictly positive entries.

Let us assume that the first case does not hold, then we prove that the second case must necessarily hold. We do this using Corollary 6. Let be the columns of , and be the cone generated by the columns of . By assumption, . For closedness and convexity of , required by Corollary 6, see Lemma 7. From the Corollary we have that , and such that and . Now we argue that by ruling out the possibility of it being positive or negative. Since the origin is part of the cone (i.e. ), we have that cannot be bigger than . But cannot be negative either. Indeed, if there is a for which there must be another point in the cone (for ) for which , which contradicts Corollary 6, and thus . In conclusion, if , then for all the columns of holds that and . ∎

We conclude this section with a standard result in linear algebra.

Theorem 10 ([Str+93]).

Let a linear system of equations for a matrix with singular value decomposition , where , is a diagonal matrix with on the diagonal, and . The least-square solution of smallest norm exists, is unique, and is given by

Where is the square matrix having on the diagonal if , and otherwise.

B.2 Random variables, measurable spaces

Definition 10 (-algebra [Tao11, KF57]).

Let be a set, and be a subset of the power set of (or equivalently a collection of subsets of ). Then is a -algebra if

-

•

(Empty set) .

-

•

(Complement) .

-

•

(Countable unions) is closed under countable union, i.e., if , then .

Observe that thanks to the de Morgan law, we can equivalently define the sigma algebra to be closed under countable intersection.

Definition 11.

Let be a set, and a -algebra. The tuple is a measurable space (or Borel space).

Definition 12 (Measurable function [Tao11]).

Let , and two different measurable space. A function is said to be measurable if for every

A measurable function is a function between the underlying sets of two measurable spaces that preserves the structure of the spaces: the pre-image of any measurable set is measurable. This is a very similar definition of a continuous function between topological spaces: the pre-image of any open set is open.

Definition 13 (Probability space).

The tuple is a probability space if

-

•

is a -algebra.

-

•

is a measurable function such that

-

–

and .

-

–

Let be a set of disjoints elements of . Then is countably additive.

-

–

.

-

–

We say commonly that is the set of outcomes of the experiment, and is the set of events. That is, a probability space is a measure space whose measure of is .

Definition 14 (Equivalence between probability measures).

Let two probability space with the same and . We say that and are equivalent if and only if

Two equivalent measures agree on the possible and impossible events. Next, we recall the definition of and the formalism of random variable.

Definition 15 (Random variable).

A (real-valued) random variable on a probability space is a measurable function .

Usually the definition of a martingale is in the context of stochastic processes, but in the case of a discrete market in one time step, we can use a simplified definition.

Definition 16 (Martingale).

Let be two random variables on the same probability space. They are a martingale if

-

•

.

-

•

.

B.3 Quantum subroutines

We need few results from previous literature in quantum linear algebra.

Theorem 11 (Pseudoinverse state preparation [CGJ19]).