∎

The University of Texas at El Paso, 500 West University Avenue, Texas 79968, USA, 11email: sbchatla@utep.edu

Nonparametric inference for additive models estimated via simplified smooth backfitting ††thanks: The online version of this article contains supplementary material.

Abstract

We investigate hypothesis testing in nonparametric additive models estimated using simplified smooth backfitting (Huang and Yu, Journal of Computational and Graphical Statistics, 28(2), 386–400, 2019). Simplified smooth backfitting achieves oracle properties under regularity conditions and provides closed-form expressions of the estimators that are useful for deriving asymptotic properties. We develop a generalized likelihood ratio (GLR) (Fan, Zhang and Zhang, Annals of statistics, 29(1),153–193, 2001) and a loss function (LF) (Hong and Lee, Annals of Statistics, 41(3), 1166–1203, 2013) based testing framework for inference. Under the null hypothesis, both the GLR and LF tests have asymptotically rescaled chi-squared distributions, and both exhibit the Wilks phenomenon, which means the scaling constants and degrees of freedom are independent of nuisance parameters. These tests are asymptotically optimal in terms of rates of convergence for nonparametric hypothesis testing. Additionally, the bandwidths that are well-suited for model estimation may be useful for testing. We show that in additive models, the LF test is asymptotically more powerful than the GLR test. We use simulations to demonstrate the Wilks phenomenon and the power of these proposed GLR and LF tests, and a real example to illustrate their usefulness.

keywords: Generalized likelihood ratio, Loss function, Hypothesis testing, Local polynomial regression, Wilks phenomenon

1 Introduction

Additive models are popular structural nonparametric regression models and have been widely studied in the literature (Friedman & Stuetzle, 1981; Hastie & Tibshirani, 1990). For a random sample , we consider the following additive model:

| (1) |

where is a sequence of i.i.d. random variables with mean zero and finite variance and the additive components ’s are unknown smooth functions which are identifiable subject to the constraints, for .

Additive models do not suffer greatly from the curse of dimensionality because all of the unknown functions are one-dimensional. It is possible to estimate each additive component with the same asymptotic bias and variance of a theoretical estimate which uses the knowledge of other components. Mammen et al. (1999) demonstrates that this oracle property holds true when smooth backfitting is used for estimation. Alternative estimation methods include marginal integration (Tjøstheim & Auestad, 1994; Linton & Nielsen, 1995), backfitting (Buja et al., 1989; Opsomer, 2000), penalized splines (Wood, 2017) and simplified smooth backfitting (Huang & Yu, 2019). In this study, we concentrate on simplified smooth backfitting. Simplified smooth backfitting, in addition to achieving oracle properties under regularity conditions, provides closed-form expressions of the estimators, which are convenient for deriving asymptotic properties.

After fitting an additive model, we are often interested in some hypothesis testing problems, e.g. testing whether a specific additive component in (1) is significant, or whether it may be replaced by a parametric form. For simple hypothesis problems such as component significance, the existing penalized estimation methods (Meier et al., 2009; Lian et al., 2012; Horowitz & Huang, 2013; Lian et al., 2015) provide some quick answers. However, a hypothesis testing framework is necessary for rigorous treatment. The theory for nonparametric hypothesis testing is well developed for univariate nonparametric models (Ingster, 1993; Hart, 2013) but is somewhat limited for additive models. Härdle et al. (2004) propose a bootstrap inference procedure for generalized semiparametric additive models which is based on marginal integration (Linton & Nielsen, 1995). While their test statistic is asymptotically normal, convergence to normality is slow, so they propose a bootstrap approach to calculate its critical values. Roca-Pardiñas et al. (2005) study the testing of second-order interaction terms in generalized additive models. They propose a likelihood ratio test and an empirical-process test based on the deviance under the null and alternative hypotheses. The asymptotic distributions of their test statistics are unknown and are hard to derive, so they use a bootstrap procedure to approximate the null distribution.

Proceeding in this direction, Fan & Jiang (2005) propose a generalized likelihood ratio (GLR) test which is very simple to use. The GLR test compares the likelihood function under the null with the likelihood function under the alternative. Fan & Jiang (2005) derive the asymptotic properties of the GLR test statistic using classical backfitting (Opsomer, 2000) for model estimation. It is known that backfitting does not achieve oracle bias when the covariates are correlated. Moreover, the estimators of backfitting do not have closed-form expressions. Regardless of these drawbacks of backfitting, Fan & Jiang (2005) show that the GLR test exhibits Wilks phenomenon, which means that the null distribution is independent of the nuisance parameters – a much-desired property for likelihood ratio tests. However, their method is still limited in practice because of the disadvantages of backfitting. Better alternatives for model estimation include smooth backfitting, for which the properties of the GLR test still need to be investigated. This motivates us to study the properties of GLR test using simplified smooth backfitting for estimation.

While the GLR test has some appealing features and has been widely used in practice, it is still a nonparametric pseudo test because of the parametric assumptions on error distribution. Another promising alternative is loss function (LF) based testing framework (Hong & Lee, 2013) which is available for univariate nonparametric models (Model (1) with ). A loss function test compares the models under null and alternative by specifying a penalty for their difference. Many times, this is more relevant to decision-making under uncertainty because it provides the flexibility of choosing a loss function that mimics the objective of the decision-maker. Hong & Lee (2013) show that LF test is asymptotically more powerful than GLR test in terms of Pitman’s efficiency criterion and possesses both optimal power and Wilks properties. Moreover, all admissible loss functions are asymptotically equally efficient under a general class of local alternatives. In spite of all these advantages, the properties of LF test still need to be investigated for nonparametric additive models . To fill this void, we propose a LF test for additive model (1) and derive its asymptotic properties. More recently, although in a different context, Mammen & Sperlich (2022) proposed a backfitting test. Their test compares the nonparametric estimators obtained from smooth backftting in the norm. Using simulations they show that the backfitting test provides very good performance in finite samples. It is worth mentioning that, the proposed LF test in the study takes a similar form asymptotically.

The main contributions from this study are as follows. We develop GLR and LF based hypothesis testing frameworks for nonparametric additive model (1) using simplified smooth backfitting (Huang & Yu, 2019) for estimation. In Theorems 8.1 and 8.2, we show that both these test statistics follow a rescaled chi-square distribution asymptotically and achieve Wilks phenomenon. Unlike the GLR test in Fan & Jiang (2005), the proposed GLR and LF tests do not require undersmoothing to achieve Wilks phenomenon and the bandwidths that were well-suited for model estimation might also be useful for testing. We also construct new type of tests for additive models and establish the connections between GLR, LF and F-test statistics. Theorem 8.4 shows that GLR and LF test statistics achieve the optimal rate of convergence for nonparametric testing, where and is the order of local polynomial, according to Ingster (1993). Furthermore, in Theorem 8.5 we show that LF test is asymptotically more powerful than GLR test. Using simulations we validate our theoretical findings and illustrate that both GLR and LF tests are robust to error distributions to some extent.

The remainder of the paper is organized as follows. In Section 2, we introduce smoother matrices which are required for simplified smooth backfitting and outline the estimation algorithm. In Section 3, we formulate GLR and LF test statistics for nonparametric additive model. We derive the asymptotic null distributions for both test statistics and discuss their optimal power properties in Section 4. In Section 5, we evaluate the finite sample performances of both GLR and LF tests using a simulation study and a real example. We include proofs and additional numerical results in Supplementary Material.

2 Simplified Smooth Backfitting

In this section, we give a brief introduction to local polynomial regression (Fan & Gijbels, 1996) and describe simplified smooth backfitting algorithm, which includes smoother matrices, , of Huang & Chen (2008).

2.1 Smoother Matrix

Suppose , , are independent observations generated from the following model

| (2) |

where is a continuous response variable, is a continuous explanatory variable and denotes an error term with mean zero and finite variance. We choose local polynomial modeling approach (Fan & Gijbels, 1996). To estimate the conditional mean at a grid point , it considers a th order Taylor expansion , for in a neighborhood of .

Let be a design matrix with of length and for . Let be a weight matrix with as a nonnegative and symmetric probability density function, and where is a bandwidth. The local polynomial approach estimates , where , , as

| (3) |

where . Let , denote the solution vector to (3) and the dependence of on is suppressed for convenience in notation.

Suppose the support of is . Let

| (4) |

be the boundary corrected kernel function defined in Mammen et al. (1999). It is easy to note that for a fixed . The smoother matrix in Huang & Chen (2008) is based on integrating local least squares errors (3)

| (5) |

where is an - dimensional identity matrix and

| (6) |

is a smoother matrix in which the integration is taken element by element. Consequently, we may use as a fitted value for and its th element, takes the following form, for

| (7) |

where is the unit vector with as the th element. The estimator (7) involves double smoothing as it combines the fitted polynomials around . Therefore, at interior points , the estimator achieves bias reduction. While the bias of traditional local polynomial estimator is of order for odd , the bias of is of order for . In Section 2.2, we define simplified smooth backfitting estimators for additive model (1) analogous to (7). Huang & Chen (2008) and Huang & Chan (2014) discuss the properties of and they show that it is symmetric, asymptotically idempotent and asymptotically a projection matrix. Moreover, it is nonnegative definite and shrinking.

2.2 Estimation

Huang & Yu (2019)’s simplified smooth backfitting algorithm is analogous to the classical backfitting algorithm of Buja et al. (1989) and Hastie & Tibshirani (1990) in terms of component updates. The key difference is that it uses the univariate matrices in (6) as smoothers in backfitting algorithm.

Let and for . Let for , and , where is the vector of ones. Let which is same as without the column of ones. For any matrix , define and . Suppose is an univariate smoother matrix defined as in (6) for covariate with th order local polynomial approximation and bandwidth for .

We introduce the following spaces before stating the simplified smooth backfitting algorithm for model (1). Let be a space spanned by the eigenvectors of with eigenvalue 1. It includes polynomials of up to th order because , , and . Suppose is an orthogonal projection onto the space and is an orthogonal projection onto the space , . Then,

| (8) |

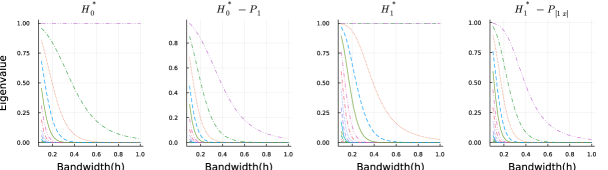

where and , and are defined similarly. Since the modified smoothers , , have eigenvalues in , by Proposition 3 in Buja et al. (1989), we obtain closed form expressions for backfitting estimators. For illustration, we plot the eigenvalues of the smoother and the modified smoother using local constant () and local linear terms () in Figure 1. While the local constant smoother has one eigenvalue equal to 1, the local linear smoother has two eigenvalues that are equal to 1. The modified smoother has eigenvalues in for bandwidths that are not too small.

The simplified smooth backfitting algorithm with modified smoothers for , and , is stated as follows:

-

1.

Initialize: with in the space of , .

-

2.

Cycle: , , since and .

-

3.

Continue step 2 until the individual functions do not change. The final estimator for the overall fit is .

Furthermore, we can write

for such that , . Then the final estimator for th additive component is , for . Since it follows that for . Consequently, the estimators ’s are identifiable.

Since the smoothers , , are symmetric and shrinking, using the results in Buja et al. (1989), Huang & Yu (2019) show that the above algorithm converges. We provide their results in the following:

-

•

It follows from Theorem 2 of Buja et al. (1989) that the normal equations

(9) are consistent for every .

- •

-

•

The solution is unique unless there is an exact concurvity which happens when there is a linear dependence among the eigenspaces corresponding to eigenvalue 1 of the ’s.

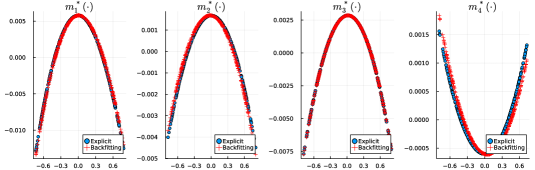

We now obtain explicit expressions for the estimators , . Let and . By Proposition 3 in Buja et al. (1989), we obtain . While these expressions provide estimators without requiring an iterative procedure, we still favor the backfitting algorithm because of its numerical stability. Furthermore, the backfitting approach is computationally simpler. Assume that a certain number of iterations is sufficient for convergence. In terms of computations, the explicit expressions cost operations whereas the backfitting algorithm only costs operations (Hastie & Tibshirani, 1990). However, this might not be a concern for small sample sizes. In Figure 2, we provide a comparison of the estimated functions using backfitting and explicit expressions for the model considered in Section 5.1. Both methods provide similar results. The computation times of backfitting and explicit expressions across different sample sizes are presented in Table 1. For small sample sizes, both approaches took about the same amount of time. However, solving explicit expressions is computationally costly than backfitting for large sample sizes. More information on the computer facilities can be found in Section 5.1.

| Backfitting(ms) | Explicit(ms) | |

|---|---|---|

| 200 | 664.8 | 682.6 |

| 400 | 2414 | 2514 |

| 800 | 8961 | 8650 |

| 1600 | 40717 | 40299 |

| 3000 | 169575 | 194010 |

| 6000 | 856743 | 1203930 |

At the convergence of simplified smooth backfitting algorithm, we obtain smooth backfitting estimates (or estimates at grid points) by performing a local polynomial regression of on partial residual . Formally,

| (10) |

for , , where is a unit vector with 1 at the th position and and are defined similar to and in (3).

Huang & Yu (2019) discuss the properties of estimators and for . They show that, estimator achieves asymptotic bias of order , for , in the interior range for . Similarly, asymptotic bias of is of order if or , and is of order if or , for , in the interior range.

3 Proposed Test Statistics

In this section, we define both GLR and LF test statistics for Model (1) which are computed using the simplified smooth backfitting in Section 2. For simplicity in presentation, we consider the following simple hypothesis testing problem:

| (11) |

which tests whether the th predictor makes any significant contribution to the dependent variable. This testing problem is a nonparametric null versus a nonparametric alternative. It is also possible to choose more complicated hypothesis testing problems such as composite hypotheses, and nonparametric null versus parametric alternatives. We discuss some of these in our numerical results in Section 5.

We now introduce some matrices which will be used in our asymptotic results. Let where as in (37). Define

| (12) | ||||

| (13) | ||||

| (14) |

where , , is the matrix of ones, and is an identity matrix of size .

3.1 The Generalized Likelihood Ratio Test

We define the GLR test statistic analogous to Fan & Jiang (2005). Since the distribution of is unknown, pretend that the error distribution is normal, , to obtain the likelihood. However, we note that normality assumption is not needed to derive asymptotic properties for GLR statistic. In Section 5.1, we show that asymptotic distribution of GLR statistic is robust to error distribution to some extent. Now, the log-likelihood under model (1) is

Replacing , , , with their estimates , , yields

where . This likelihood function attains maximum for which implies that . Similarly, the log-likelihood for is , with , and , , are the estimators of under , using the simplified smooth backfitting algorithm with the same set of bandwidths. Now, we define the GLR test statistic as

| (15) |

and reject the null hypothesis when is large. From Lemma 1 (Supplementary Material), we obtain that

for and defined in (38) and (39), respectively. This motivates us to consider the following F-type of test (Huang & Davidson, 2010)

| (16) |

where denotes the trace. Theorem 8.1 shows the statistic (42) indeed follows F distribution asymptotically.

3.2 The Loss Function Test

The LF testing framework (Hong & Lee, 2013) compares models under and via a loss function . This is more relevant to decision-making under uncertainty in some applications. We write the discrepancy between the models as

| (17) |

where and are the th predicted values for the models under and , respectively. Similar to Hong & Lee (2013), we consider a specific class of functions called the generalized cost-of-error function defined as , where is twice continuously differentiable with , and .

We define the LF test statistic as

| (18) |

where is the residual sum of squares under alternative and is the remainder term in the Taylor expansion of . We reject the null hypothesis when is large.

Interestingly, when the estimated additive functions under and are approximately equal, that means, for and , we obtain

The form of the statistic is similar to the backfitting based test statistic proposed in Mammen & Sperlich (2022) as

| (19) |

where is the distribution of . For more discussion of similar tests please refer to Mammen & Sperlich (2022).

4 Asymptotic Results

In this section, we develop asymptotic theory for the GLR and the LF test statistics defined in Section 3 under model (1). We derive the asymptotic null distributions of these test statistics when the testing problem is of the form (11) and discuss Wilks phenomenon and optimal power properties. For simplicity in theoretical arguments we assume that all the data points are interior , (Huang & Yu, 2019). However, we remark that, under the conditions of Theorems 8.1 and 8.2, the additional bias terms introduced by the boundary points are of smaller order. Therefore, our theory holds when the data include boundary points.

We list some of the assumptions required for our theoretical results in the following.

(A.1)

The densities of are Lipschitz-continuous and bounded away from 0 and have bounded support for . The joint density of and , , for , is also Lipschitz continuous and have bounded support.

(A.2)

The kernel is a bounded symmetric density function with bounded support and satisfies Lipschitz condition. The bandwidth and , , as .

(A.3)

The th derivative of , , exists.

(A.4)

The error has mean 0, variance , and finite fourth moment.

(A.5)

The loss function has a unique minimum at , and is monotonically nondecreasing as . Furthermore, is twice continuously differentiable at with , , , and for any near .

The Assumptions (A.6), (A.7) and (A.9) are standard for additive models in the nonparametric smoothing literature; for example, they are similar to Fan & Jiang (2005); Huang & Chan (2014); Huang & Yu (2019). Assumption (A.8) is required for simplified smooth backfitting to achieve bias reduction. For example, similar assumptions are found in Huang & Chan (2014); Huang & Yu (2019). Assumption (A.10) is from Hong & Lee (2013) and it is required for the loss function.

4.1 Asymptotic Null Distributions of GLR and LF Tests

Let and for . Let , be a matrix and are the elements of . Denote the convolution of with by , where for . Let,

where is the th, , element of defined in (38), is the length of the support of the density of . In practice, the above asymptotic expressions are not required to compute the quantities and . We can compute them directly from the matrix defined in (38) which provides a good approximation.

Hereafter, the notations “” and “” stand for convergence in distribution and probability, respectively. The following theorem describes the Wilks type of result for the GLR test conditional on the sample space .

Theorem 4.1

Theorem 8.1 gives the asymptotic null distribution of the GLR test statistic for the testing problem (11) under . In our opinion, the asymptotic expression for is complicated and might not be necessary.

Remark 1

The factors and in Theorem 8.1 do not depend on the nuisance parameters and nuisance functions. Therefore, the GLR test statistic achieves the Wilks phenomenon that its asymptotic distribution does not depend on nuisance parameters and nuisance functions. Theorem 8.1 is different from Theorem 1 of Fan & Jiang (2005) because it uses simplified smooth backfitting instead of backfitting for estimation of additive components.

Remark 2

Theorem 8.1 shows that the bias is negligible under the condition which is different from the condition in Theorem 1 of Fan & Jiang (2005). Suppose , then the proposed GLR test achieves Wilks phenomenon for the bandwidths of order for odd , which are the optimal bandwidths used for estimation in Fan & Jiang (2005), while their GLR test statistic does not. To see this, consider , then , the first condition holds where as the second condition does not hold.

We now derive the asymptotic null distribution of the LF test statistic. Let where is the th, , element of defined in (40). Define

Denote where is the loss function given in Section 3.2. The following theorem describes the Wilks type of result for the LF test statistic conditional on the sample space .

Theorem 4.2

Remark 3

Theorem 8.2 shows that the factors and do not depend on the nuisance parameters and nuisance functions. Therefore, like the GLR statistic, the LF test statistic also enjoys Wilks phenomenon that its asymptotic distribution does not depend on nuisance parameters and nuisance function. Further, since Wilks phenomenon is achieved for optimal bandwidths , for odd , , undersmoothing may not be necessary.

Remark 4

The LF test statistic includes an extra scaling constant , which is the curvature of the loss function. When is correctly specified, the asymptotic distribution of the scaled statistic does not depend on it. However, the choice of is irrelevant if the conditional bootstrap method (Supplementary Material) is used to simulate the null distribution. We further validate this using simulations in Section 5.1. We also provide more discussion on the efficiency of loss functions in Theorem 8.3.

Unlike GLR test statistic, the LF test statistic includes only the second-order term in the Taylor expansion because the first-order term vanishes to 0 under . For univariate nonparametric model (1) with , Hong & Lee (2013) argue that not having first-order term could be one reason for LF test to be asymptotically more powerful than GLR test. In Theorem 8.5 we show that similar result holds for the nonparametric additive model (1). We now discuss the optimal power properties of the proposed test statistics in the following section.

4.2 Power of GLR and LF Tests

We consider the framework of Fan et al. (2001) and Fan & Jiang (2005) to study the power of GLR and LF tests. Assume that , so that the second term in both and is of smaller order than and , respectively. We note that the optimal bandwidth for the testing problem (11) is (to be shown later in Theorem 8.4), which satisfies the condition . Under these assumptions, Theorems 8.1 and 8.2 lead to the following approximate level tests for GLR and LF test statistics, respectively

Let be a class of functions such that any satisfy the following regularity conditions as stated in Fan & Jiang (2005):

| (25) | ||||

for some constants and . Let with . Define a class of functions,

| (26) |

for a given , where is the th derivative of and is some positive constant. Consider the contiguous alternative of the form

| (27) |

where and .

The following theorem is useful to approximate the power of GLR and LF tests under the contiguous alternative (73).

Theorem 4.3

Suppose and for some constant . Suppose , for .

- (i)

- (ii)

Theorem 8.3 shows that when , , the alternative distributions are independent of the nuisance functions , , and this helps us to compute the power of the tests via simulations over a large range of bandwidths with nuisance functions fixed at their estimated values.

It is interesting to note that the noncentrality parameters in part (ii) of Theorem 8.3 are independent of the curvature parameter of the loss function . This implies that, as discussed in Hong & Lee (2013), all loss functions satisfying Assumption (A.10) are asymptotically equally efficient under in terms of Pitman’s efficiency criterion [Pitman (2018), Chapter 7].

The maximum of the probabilities of type II errors is

| (28) |

where and are the probabilities of type II errors at the alternative . Use to denote either or and to denote or . As mentioned in Fan et al. (2001) and Fan & Jiang (2005), the minimax rate of or is defined as the smallest such that:

-

(a)

for every , , and for any , there exists a constant such that , and

-

(b)

for any sequence , there exists and such that for any , and .

The following theorem provides the rate with which the alternatives can be detected by GLR and LF tests. The convergence rate depends on bandwidth.

Theorem 4.4

Remark 5

For the class of alternatives in (26), the rate of convergence for nonparametric hypothesis testing according to the formulations of Ingster (1993) and Spokoiny et al. (1996) is where is the smoothness parameter. Since in this study, the GLR and LF tests are asymptotically optimal based on their rates given in Theorem 8.4. Our rates are different from the rates in Theorem 5 of Fan & Jiang (2005) because of different smoothness parameter considered in their study. For this reason, the optimal bandwidth for testing in our study which is also different from in Fan & Jiang (2005).

Remark 6

Based on Theorems 8.1 and 8.2, the assumption on bandwidths , , is required to ensure Wilks property for both GLR and LF tests. This is true for a collection of bandwidths which includes the optimal bandwidths used in backfitting (Fan & Jiang, 2005). With our method, the bandwidths well suited for curve estimation might also be useful for testing.

We now show that the LF test is asymptotically more powerful than the GLR test. For ease of exposition, we assume that , . Without loss of generality, let which satisfy the condition in Theorem 8.3. We now compare the relative efficiency between the LF test statistic and the GLR test statistic under the class of local alternatives

| (29) |

where and . While Theorem 8.4 shows that the GLR and the LF tests achieve optimal rate of convergence in the sense of Ingster (1993) and Spokoiny et al. (1996), Theorem 8.5 provides that under the same set of regularity conditions, the LF test is asymptotically more powerful than the GLR test under in (29).

Theorem 4.5

Remark 7

Theorem 8.5 shows that the Pitman’s relative efficiency of the LF test over the GLR test is larger than 1 for , , which means that the LF test is asymptotically more efficient than the GLR test. Given the complicated expressions of and , the extension of Theorem 8.5 to general , is not straightforward. We defer this for future research.

Remark 8

The result in Theorem 8.5 does not imply that the GLR test is not useful. The GLR test is a natural extension of classical Likelihood Ratio test with many desirable features and has been widely used in the literature. As stated in Hong & Lee (2013), same bandwidths and same kernel functions are required for the relative efficiency of over to hold. Therefore, it might be possible that both test statistics achieve similar efficiencies under different bandwidths and kernel functions. In our simulations in Section 5.1, we observe that the statistic achieves larger powers than the statistic .

Remark 9

The result in Theorem 8.5 is new to the literature. While Theorem 4 in Hong & Lee (2013) discuss the asymptotic relative efficiency of over for Nadaraya-Watson estimator in an univariate model, the proposed Theorem 8.5 discuss the relative efficiency for similar type of estimators using , , in additive models.

5 Numerical Comparison of GLR and LF Tests

In this section, we evaluate the performance of GLR and LF tests in finite samples. Using simulations, we demonstrate the Wilks phenomenon and examine the effect of error distribution on the performances of GLR and LF tests. Local linear smoothing with Gaussian kernel is considered in all the simulations. We use software Julia (Bezanson et al., 2017) to carry out simulations and data analysis. We also illustrate the usefulness of the proposed statistics using Boston housing data. Additional results are presented in Section S3.2 of supplementary Material.

5.1 Simulations

We mimic the simulation designs in Fan & Jiang (2005) and Huang & Yu (2019). Consider the additive model,

| (30) |

where , , , , and is distributed as . For the covariates , , and , we first simulate normally distributed random variables , , and with mean and covariance , and project them back on to using the transformation , .

We consider the null hypothesis and treat , and as nuisance functions. For comparison purpose, we implement the GLR test in Fan & Jiang (2005) which is based on classical backfitting; hereafter, denoted as GLR(FJ) and the corresponding test statistic as . We also implement the backfitting based test (19) proposed in Mammen & Sperlich (2022); hereafter, denoted as SB. The SB statistic in (19) is approximated using Riemann sum as

where is the th order statistic of . An R (R Core Team, 2021) package wsbackfit (Roca-Pardinas et al., 2021) is used to estimate the additive component and kernel density estimate which uses the bandwidth considered for .

We compute the optimal bandwidths using the following cross-validation procedure which is defined similar to Nielsen & Sperlich (2005).

-

1.

Fit the additive model for initial values of bandwidths.

-

2.

For any direction (covariate), consider the corresponding partial residual as a response variable and use an Akaike Information Criterion based smoothing parameter selection method (Hurvich et al., 1998) to determine the optimal bandwidth in univariate local linear regression.

-

3.

Refit the model with the updated bandwidths and proceed to the step 2 choosing a different direction.

-

4.

Obtain, the optimal bandwidths at the convergence of the above procedure.

To demonstrate Wilks phenomenon for GLR, LF, and F tests, we choose three levels of bandwidths and , and . Similarly, we consider three levels of to show that the proposed tests do not depend on the nuisance function :

where . For LF statistic, we consider the following class of LINEX functions (Hong & Lee, 2013):

| (31) |

where is an asymmetric loss function for each pair of parameters . The magnitude of , which is a shape parameter, controls the degree of asymmetry. The parameter is a scale factor.

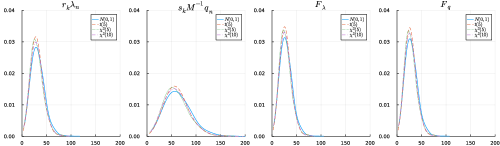

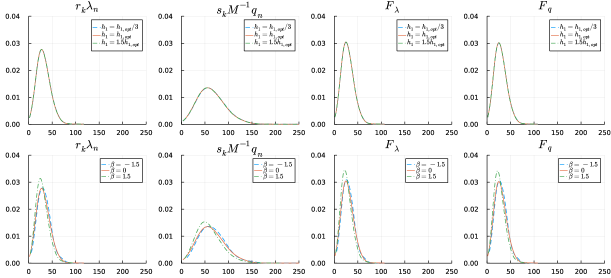

We draw 1000 samples of 100 observations from (30) and for each sample, we compute the scaled GLR, LF, and F test statistics. The distributions of scaled GLR, LF, and F test statistics among 1000 simulations are obtained via a kernel estimate using the rule of thumb bandwidth , where is the standard deviation of the test statistics. Figure 3 shows the estimated densities for the scaled GLR and LF, and F test statistics. Plots in the top row show that the null distributions of scaled GLR and LF statistics follow a chi-squared distribution over a wide range of bandwidth values for . It is interesting to note that , and . Due to the extra scaling constant , the distribution of seems like a scaled version of the distribution of . Both F statistics, and , are computed using the , and matrices defined in (38,39,40); the results also illustrate that they provide a good approximation. Similarly, plots from the bottom row demonstrate the Wilks phenomenon for scaled GLR, LF, and F test statistics, as their null distributions are nearly the same for three different choices of the nuisance functions for . For LF test, we consider the LINEX loss function (31) with the choice and .

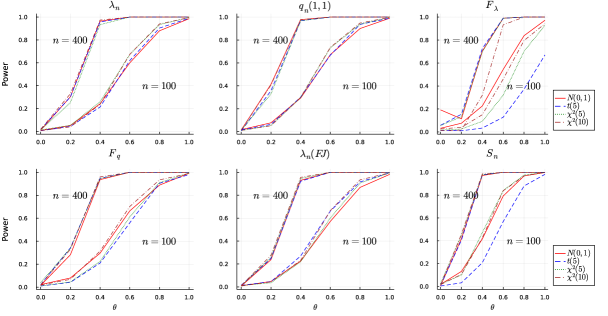

For power comparison among GLR, LF, F, GLR(FJ), and SB tests, we evaluate the power for a sequence of alternative models indexed by ,

| (32) |

where , gives the null model and makes the alternative reasonably far away from the null model. For each given value of , we consider Monte Carlo replicates for calculation of the critical values via conditional bootstrap method which is described in Section S3 of Supplementary Material. The rejection percentage values are computed based on simulations. When , the alternative is identical to the null hypothesis and the power is approximately equal to the significance level or . Furthermore, to illustrate the influence of different error distributions on the power of GLR, LF, and F tests, we consider model (30) with different error distributions of , namely, , , and . The distributions of test statistics among 1000 simulations are provided in Figure 8 in Supplementary Material. The estimated densities are approximately similar across different error distributions.

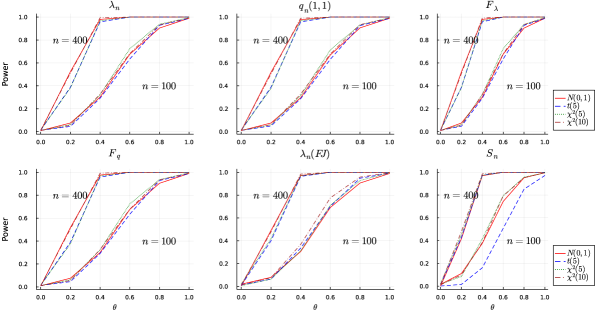

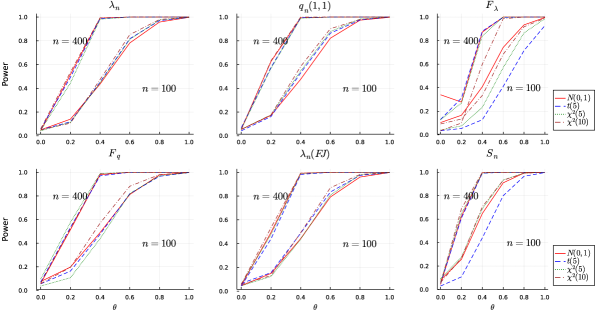

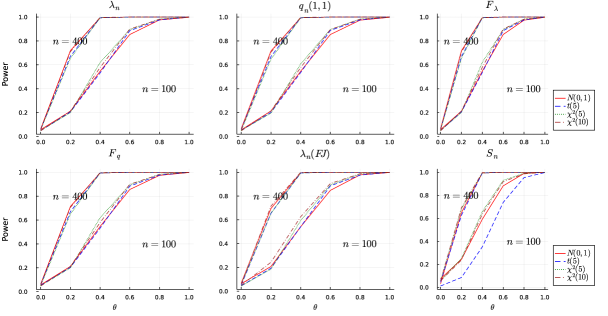

The power of GLR, LF, F, GLR(FJ), and SB tests for the alternative model sequence in (32) at the significance level is provided in Figure 4 for and . Figure 4 illustrates that both GLRT and LFT differentiate the null and alternative hypotheses with high power while not being sensitive to error distributions. When , the alternative is identical to the null and hence, the power should be approximately equal to (); this is evident from the results. This gives an indication that Monte Carlo approach yields the correct estimator of the null distribution. Based on Theorem 8.4, we consider the bandwidths that are optimal for testing , . Here is the standard deviation of . One important observation is that the results for the statistic exhibit some variation. However, in Figure 5 where the optimal bandwidths for model estimation (cross-validation) are considered, we observe that performs very similar to other statistics. We note that the optimal bandwidths are larger than ; it seems is not stable for smaller bandwidths due to approximation. Overall, Figures 4 and 5 illustrate that the proposed methods in the study work well with the finite samples and comparable to other existing methods in the literature.

We also provide the power comparison of the above methods at 1% level of significance. The results are available in Figures 9 and 10 in Supplementary Material. The findings remain similar.

5.2 Boston Housing Data Analysis

To demonstrate the usefulness of the proposed GLR and LF tests, we consider the Boston housing data. This data include the information collected by the U.S Census Service regarding housing in the area of Boston Mass, and originally published in Harrison Jr & Rubinfeld (1978). It contain the median values of 506 homes along with 13 sociodemographic and related variables. This data has been previously used in the literature to benchmark different algorithms and to illustrate different methodologies. For example, please see Belsley et al. (2005), Breiman & Friedman (1985), Opsomer & Ruppert (1998) and Fan & Jiang (2005). For the sake of easy comparison, we consider the same dependent and independent variables used in Fan & Jiang (2005).

-

•

MV, median value of owner-occupied homes in $1,000’s

-

•

RM, average number of rooms per dwelling

-

•

TAX, full-value property tax rate

-

•

PTRATIO, pupil/teacher ratio by town school district

-

•

LSTAT, proportion of population that is of “lower status” .

Opsomer & Ruppert (1998) and Fan & Jiang (2005) analyze this data by considering the following four-dimensional additive model,

| (33) |

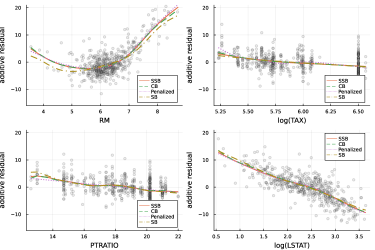

where , , , and . We use simplified smooth backfitting algorithm in Section 2.2 with local linear smoothing to estimate model (33) after six outliers are removed. To alleviate the effect of sample size on -value, we take a random sample observations for hypothesis testing. The optimal bandwidths are selected using the cross-validation procedure described in Section 5.1 which uses the AIC to find optimal bandwidth in each direction. For comparison, we also fit model (33) using classical backfitting in Fan & Jiang (2005), smooth backfitting (Mammen & Sperlich, 2022; Roca-Pardinas et al., 2021) with wsbackfit package in R, and penalized splines approach with mgcv package in R (Wood & Wood, 2015; R Core Team, 2021).

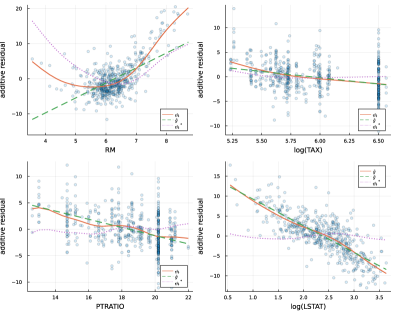

Figure 6 shows the estimated additive functions along with the partial residuals. The simplified smooth backfitting algorithm estimates the additive functions as a sum of two functions i.e. and , where is the purely nonparametric part and is the parametric part corresponding to the eigenvectors of eigenvalue 1 of the smoother . For comparison, Figure 7 includes the fits from gam() function in mgcv package in R, from sback() function in wsbackfit package in R, and from the classical backfitting of Fan & Jiang (2005). Figure 7 shows that the fits from the these methods are very similar. From both Figures 6 and 7 we find that the additive components for all the variables except exhibit the following parametric forms:

| (34) |

This confirms with the observations of Opsomer & Ruppert (1998) and Fan & Jiang (2005).

We use the proposed GLR and LF statistics to test whether the semiparametric null model (34) holds against the additive alternative model (33). For the LF test statistic, we consider the family of LINEX loss functions (31) with parameters . For comparison, we include the results for the GLR test in Fan & Jiang (2005), which we refer as GLR(FJ). Further, we also include the results from the backfit test (SB) defined in Mammen & Sperlich (2022). For convenience, the test statistic for SB method is computed as

where is the th order statistic of , is the corresponding parametric part. The null distributions of the test statistics , , , , , and are necessary to compute their -values. Therefore, we use the conditional bootstrap method described in Supplementary Material to obtain the null distributions of the test statistics. The optimal bandwidths are computed using the procedure described in Section 5.1.

Table 2 provides the -values for statistics , , , , , and with the following five different bandwidths and using bootstrap replications to compute null distributions. These results indicate that the semiparametric model (34) is appropriate for this dataset within the additive models. For smaller bandwidths (undersmoothing) there is some evidence to reject the null hypothesis which is not surprising. For larger bandwidths, the estimated additive functions look more like parametric models and therefore the evidence is in favor of the null hypothesis. For the optimal bandwidths considered for estimation, the proposed GLR and LF tests conclude that semiparametric additive model is appropriate at and significance levels, respectively. This result also validates our finding that the LF test is asymptotically more powerful than the GLR test. The -values of the statistic are the smallest among all. We note that the optimal bandwidths are computed using simplified smooth backfitting and the same are used for GLR(FJ) as well.

| Bandwidth | |||||||||

|---|---|---|---|---|---|---|---|---|---|

To sum up, the results in this section indicate that both GLR and LF tests are very useful in practical applications. While their performances are sensitive to the choice of bandwidth, it is not straightforward to find optimal bandwidths for these statistics. Additionally, the finite sample performance of LF test is mildly sensitive to the choice of the loss function. Therefore, in practice, it is advisable to use both frameworks for a given hypothesis testing problem. This helps minimizing errors associated with hypothesis testing.

6 Summary and Conclusions

In this study, we develop a hypothesis testing framework for additive models using GLR and LF tests where simplified smooth backfitting is used for model estimation. While the properties of GLR test are available in the literature for additive models estimated via classical backfitting (Opsomer, 2000), it is not the case for additive models estimated with simplified smooth backfitting (Huang & Yu, 2019). Similarly, the results for the LF test are not available for additive models. We fill this void by proposing inference methods using GLR and LF tests when a model uses simplified smooth backfitting for estimation. Under some regularity conditions, we show both the test statistics achieve Wilks phenomenon and have optimal power properties. Furthermore, LF test is asymptotically more powerful than GLR test. This result is a new addition to the existing literature. The numerical performance of test statistics is also very similar across different bandwidths, and robust to different error distributions to some extent.

One possible direction for future research is to propose similar testing frameworks for generalized additive models. The LF test is asymptotically more powerful than the GLR test in linear additive models. It will be interesting to see whether the same result holds in generalized additive models.

Acknowledgements.

The author would like to thank the associate editor and two anonymous referees for their constructive feedback, which resulted in major changes to the paper’s presentation. The author would also like to thank Prof. Li-Shan Huang for offering a postdoctoral position and for sharing her research on simplified smooth backfitting, which provided the required framework for this article. The author gratefully acknowledges the support from grants 107-2811-M-007-014, 105-2118-M-007-006-MY2, and 107-2811-M-007-1047 by the Ministry Of Science and Technology (MOST) in Taiwan (R.O.C).References

- (1)

- Belsley et al. (2005) Belsley, D. A., Kuh, E. & Welsch, R. E. (2005), Regression diagnostics: Identifying influential data and sources of collinearity, Vol. 571, John Wiley & Sons.

-

Bezanson et al. (2017)

Bezanson, J., Edelman, A., Karpinski, S. & Shah, V. B.

(2017), ‘Julia: A fresh approach to

numerical computing’, SIAM review 59(1), 65–98.

https://doi.org/10.1137/141000671 - Breiman & Friedman (1985) Breiman, L. & Friedman, J. H. (1985), ‘Estimating optimal transformations for multiple regression and correlation’, Journal of the American statistical Association 80(391), 580–598.

- Buja et al. (1989) Buja, A., Hastie, T. & Tibshirani, R. (1989), ‘Linear smoothers and additive models’, The Annals of Statistics 17(2), 453–510.

- de Jong (1987) de Jong, P. (1987), ‘A central limit theorem for generalized quadratic forms’, Probability Theory and Related Fields 75(2), 261–277.

- Fan & Gijbels (1996) Fan, J. & Gijbels, I. (1996), Local polynomial modelling and its applications: monographs on statistics and applied probability 66, Vol. 66, CRC Press.

- Fan & Jiang (2005) Fan, J. & Jiang, J. (2005), ‘Nonparametric inferences for additive models’, Journal of the American Statistical Association 100(471), 890–907.

- Fan et al. (2001) Fan, J., Zhang, C. & Zhang, J. (2001), ‘Generalized likelihood ratio statistics and wilks phenomenon’, Annals of statistics 29(1), 153–193.

- Friedman & Stuetzle (1981) Friedman, J. H. & Stuetzle, W. (1981), ‘Projection pursuit regression’, Journal of the American statistical Association 76(376), 817–823.

- Härdle et al. (2004) Härdle, W., Huet, S., Mammen, E. & Sperlich, S. (2004), ‘Bootstrap inference in semiparametric generalized additive models’, Econometric Theory 20(2), 265–300.

- Harrison Jr & Rubinfeld (1978) Harrison Jr, D. & Rubinfeld, D. L. (1978), ‘Hedonic housing prices and the demand for clean air’, Journal of environmental economics and management 5(1), 81–102.

- Hart (2013) Hart, J. (2013), Nonparametric smoothing and lack-of-fit tests, Springer Science & Business Media.

- Hastie & Tibshirani (1990) Hastie, T. & Tibshirani, R. (1990), Generalized Additive Models, Chapman & Hall/CRC Monographs on Statistics & Applied Probability, Taylor & Francis.

- Hong & Lee (2013) Hong, Y. & Lee, Y.-J. (2013), ‘A loss function approach to model specification testing and its relative efficiency’, Annals of Statistics 41(3), 1166–1203.

- Horowitz & Huang (2013) Horowitz, J. L. & Huang, J. (2013), ‘Penalized estimation of high-dimensional models under a generalized sparsity condition’, Statistica Sinica 23, 725–748.

- Huang & Chan (2014) Huang, L.-S. & Chan, K.-S. (2014), ‘Local polynomial and penalized trigonometric series regression’, Statistica Sinica 24, 1215–1238.

- Huang & Chen (2008) Huang, L.-S. & Chen, J. (2008), ‘Analysis of variance, coefficient of determination and f test for local polynomial regression’, The Annals of Statistics 36(5), 2085–2109.

- Huang & Davidson (2010) Huang, L.-S. & Davidson, P. W. (2010), ‘Analysis of variance and f-tests for partial linear models with applications to environmental health data’, Journal of the American Statistical Association 105(491), 991–1004.

- Huang & Yu (2019) Huang, L.-S. & Yu, C.-H. (2019), ‘Classical backfitting for smooth-backfitting additive models’, Journal of Computational and Graphical Statistics 28(2), 386–400.

- Hurvich et al. (1998) Hurvich, C. M., Simonoff, J. S. & Tsai, C.-L. (1998), ‘Smoothing parameter selection in nonparametric regression using an improved akaike information criterion’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 60(2), 271–293.

- Ingster (1993) Ingster, Y. I. (1993), ‘Asymptotically minimax hypothesis testing for nonparametric alternatives. i, ii, iii’, Math. Methods Statist 2(2), 85–114.

- Lian et al. (2012) Lian, H., Chen, X. & Yang, J.-Y. (2012), ‘Identification of partially linear structure in additive models with an application to gene expression prediction from sequences’, Biometrics 68(2), 437–445.

- Lian et al. (2015) Lian, H., Liang, H. & Ruppert, D. (2015), ‘Separation of covariates into nonparametric and parametric parts in high-dimensional partially linear additive models’, Statistica Sinica 25, 591–607.

- Lin & Bai (2010) Lin, Z. & Bai, Z. (2010), Probability inequalities of random variables, in ‘Probability Inequalities’, Springer, pp. 37–50.

- Linton & Nielsen (1995) Linton, O. & Nielsen, J. P. (1995), ‘A kernel method of estimating structured nonparametric regression based on marginal integration’, Biometrika 82(1), 93–100.

- Mammen et al. (1999) Mammen, E., Linton, O. & Nielsen, J. (1999), ‘The existence and asymptotic properties of a backfitting projection algorithm under weak conditions’, The Annals of Statistics 27(5), 1443–1490.

- Mammen & Sperlich (2022) Mammen, E. & Sperlich, S. (2022), ‘Backfitting tests in generalized structured models’, Biometrika 109(1), 137–152.

- Meier et al. (2009) Meier, L., Van de Geer, S. & Bühlmann, P. (2009), ‘High-dimensional additive modeling’, The Annals of Statistics 37(6B), 3779–3821.

- Nielsen & Sperlich (2005) Nielsen, J. P. & Sperlich, S. (2005), ‘Smooth backfitting in practice’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 67(1), 43–61.

- Opsomer (2000) Opsomer, J. D. (2000), ‘Asymptotic properties of backfitting estimators’, Journal of Multivariate Analysis 73(2), 166–179.

- Opsomer & Ruppert (1998) Opsomer, J. D. & Ruppert, D. (1998), ‘A fully automated bandwidth selection method for fitting additive models’, Journal of the American Statistical Association 93(442), 605–619.

- Pitman (2018) Pitman, E. J. (2018), Some basic theory for statistical inference: Monographs on applied probability and statistics, CRC Press.

-

R Core Team (2021)

R Core Team (2021), R: A Language and

Environment for Statistical Computing, R Foundation for Statistical

Computing, Vienna, Austria.

https://www.R-project.org/ - Roca-Pardiñas et al. (2005) Roca-Pardiñas, J., Cadarso-Suárez, C. & González-Manteiga, W. (2005), ‘Testing for interactions in generalized additive models: application to so 2 pollution data’, Statistics and Computing 15(4), 289–299.

-

Roca-Pardinas et al. (2021)

Roca-Pardinas, J., Rodriguez-Alvarez, M. X. & Sperlich, S.

(2021), wsbackfit: Weighted Smooth

Backfitting for Structured Models.

R package version 1.0-5.

https://CRAN.R-project.org/package=wsbackfit - Spokoiny et al. (1996) Spokoiny, V. G. et al. (1996), ‘Adaptive hypothesis testing using wavelets’, Annals of Statistics 24(6), 2477–2498.

- Tjøstheim & Auestad (1994) Tjøstheim, D. & Auestad, B. H. (1994), ‘Nonparametric identification of nonlinear time series: projections’, Journal of the American Statistical Association 89(428), 1398–1409.

- Wood (2017) Wood, S. N. (2017), Generalized additive models: an introduction with R, CRC press.

- Wood & Wood (2015) Wood, S. & Wood, M. S. (2015), ‘Package ‘mgcv”, R package version 1, 29.

Supplementary Material

Introduction

This article develops a hypothesis testing framework for additive models. For a random sample , we consider

| (35) |

where is a sequence of i.i.d. random variables with mean zero and finite variance . Each additive component function , , is assumed to be an unknown smooth function and identifiable subject to the constraint, . For simplicity in presentation, the following hypothesis testing problem is considered

| (36) |

which tests whether the th covariate is significant or not.

For readability, we repeat some notations and definitions that are provided in the main document. Let and for . Let for , and , where is the vector of ones. Let which is same as without the column of ones. For any matrix , define and .

The following definitions are needed for the theoretical results. Let be a space spanned by the eigenvectors of with eigenvalue 1. It includes polynomials of up to th order because , , and . Suppose is an orthogonal projection onto the space and is an orthogonal projection onto the space , . Then,

| (37) |

where and , and are defined similarly. Let where and for , as in (37).

Define

| (38) | ||||

| (39) | ||||

| (40) |

where , and , is the matrix of ones, and is an identity matrix of size .

6.1 Generalized Likelihood Ratio test:

The GLR test statistic is defined as

| (41) |

where and are the residual sum of squares under the null and alternative, respectively, and reject the null hypothesis when is large. Analogously, the following F-type of test (Huang & Davidson 2010) is also developed

| (42) |

where denotes the trace.

6.2 Loss Function test:

The LF test statistic is defined as

| (43) |

where and are the fitted values of the models under null and alternative, respectively, is the residual sum of squares under alternative and is the remainder term in the Taylor expansion of . We reject the null hypothesis when is large. The corresponding F-type of test statistic is define as

| (44) |

for defined in (40).

7 Assumptions

We repeat the assumptions that are outlined in the main document.

(A.6)

The densities of are Lipschitz-continuous and bounded away from 0 and have bounded support for . The joint density of and , , for , is also Lipschitz continuous and have bounded support.

(A.7)

The kernel is a bounded symmetric density function with bounded support and satisfies Lipschitz condition. The bandwidth and , , as .

(A.8)

The th derivative of , , exists.

(A.9)

The error has mean 0, variance , and finite fourth moment.

(A.10)

The loss function has a unique minimum at , and is monotonically nondecreasing as . Furthermore, is twice continuously differentiable at with , , , and for any near .

8 Required Lemmas and Proofs

The explicit expressions for the estimators , are provided as follows. Let

| (45) |

By Proposition 3 in Buja et al. (1989), we obtain . Therefore, the fitted response under the alternative can be written as

| (46) |

Analogously, the fitted response under the null can be written as

| (47) |

The following lemma simplifies the expressions for the .

Lemma 1

Proof

As shown in Huang & Yu (2019), the diagonal elements of and , , are of order and the off-diagonal elements are of order . Similarly, the elements of are of order for . Since the elements of are of smaller order, we can write

| (50) | ||||

where is the identity matrix and is the matrix of 1’s of size . Since , it follows that . Therefore,

Consequently, we write (46) as

| (51) |

where the last step uses the fact that . Let be the parametric projection matrix of the first components defined similar to (37). Based on the properties of the projection matrices, we obtain

| (52) |

where defined in (40). Combination of (51) and (52) and some rearrangement of terms yields

Observe that , for . The elements of are of smaller order than the elements of since the latter has eigenvalues in . Therefore,

Similar computations yield

Hence,

Proof

Theorem 8.1

Proof

: Recall that

| (59) |

Proof of 57:

(i) Asymptotic Expression for :

Using the notation from Lemma 1, we write

| (60) |

where

| (61) |

and . With the help of Lemma 2, we can bound the bias term by . We write

| (62) |

Since the leading terms of in (61) come from , we obtain . Combination of Assumption (A.9) and Chebyshev inequality yields . After some algebra,

where is the length of the support of the density of . It remains to show that converges to normal in distribution. Note that and

where

Application of Proposition 3.2 of de Jong (1987) yields

| (63) |

(ii) Asymptotic Expression for : By the definition of ,

The arguments analogous to Lemma 2 yields

Note that, under the condition (A.7), . Thus, it remains to show that . From the proof of Lemma 1, we obtain

which follows from the Chebyshev inequality and using the arguments analogous to the derivation of variance for (62).

(iii) Conclusion : By part(i), part(ii) and definition of , we have

where . Therefore, (63) implies

If for , then which is dominated by . Then as .

Proof of (58):

By virtue of Lemma 1, the GLR test statistic is defined as

for and defined in (61). As discussed in Huang & Davidson (2010), for type statistics,

| (64) |

the distribution is warranted if and are both projection matrices (symmetric and idempotent) and they are orthogonal to each other. Clearly, both and are not projection matrices and not orthogonal to each other. However, following Huang & Chen (2008), we show these properties hold asymptotically. It is straightforward to show both and are asymptotically idempotent. Now it remains to show that they are asymptotically orthogonal. Observe

Based on the definition of asymptotic orthogonality in Huang & Chen (2008), we claim and are asymptotically orthogonal. Therefore,

because as and .

Theorem 8.2

Proof

Proof of (65):

Consider the LF test statistic in (43)

where is the loss function defined in Assumption (A.10) and is the th, , element of . The arguments analogous to Lemma 1 yield that , under ,

Note that the dominant orders for the elements ’s come from . Therefore, diagonal elements ’s are of order and the off-diagonal elements , , are of order . By Taylor series expansion of loss function in the neighborhood of , we obtain

where , , and lies between and . Assumption (A.10) implies . Therefore

| (67) |

where each . The idea is to show that the first term in (67) converges to normal distribution and the third term is of smaller order. Using the relation , we obtain

| (68) |

where is some positive constant and the exact value of it can be calculated using the expression in page 101 of Lin & Bai (2010). Note that, the first term in (67) can be written as

| (69) |

After some algebra, we obtain

Application of Chebyshev inequality yields that where . Now it remains to show that converges to normal in distribution. Observe that and

where and . We note that the leading terms of

Therefore, application of Proposition 3.2 of de Jong (1987) yields

| (70) |

By plugging (68) and (69) in (67), we obtain

Since and , we have,

| (71) |

where . Therefore, combination of (70) and (71) yields

If for , then which is dominated by . Then as .

Proof of (66): Recall

By Taylor’s expansion, as in part(a), the numerator can be written as where is the remainder term which is of order . As in part (b) of Theorem 8.1, we show that is asymptotically an idempotent matrix and and are asymptotically orthogonal. Hence, the LFT statistic is

| (72) |

which implies that, as in part(b) of Theorem 8.1, we have

as and .

For the following theorem, we consider the contiguous alternative of the form

| (73) |

where and .

Theorem 8.3

Suppose and for some constant . Suppose , for .

- (i)

- (ii)

Proof

Part (i): Under (73), the arguments analogous to Lemma 1 yields,

where , defined in (26) and is the vector of ones of size . Similarly,

Observe that, same set of arguments yield and . Consider,

| (74) | |||||

straightforward computations yield

Plugging the above results and the value from Theorem 8.1 in (74), we obtain

| (75) |

where , , are same as defined in Theorem 8.1,

The proof follows by proceeding similar to Theorem 8.1.

Theorem 8.4

Proof

The proof uses arguments analogous to Theorem 5 in Fan & Jiang (2005). We provide proof only for the GLR test and similar arguments can be used to prove the LF test. Under the contiguous alternative , it follows from (i) of Theorem 8.3,

| (77) |

where and . Since the probability of the type II error at is defined as , it implies that

with

and

Note that and and hence . Analogous arguments to Lemma B.7 of Fan & Jiang (2005) lead to

We choose . This implies, , , and . Hence, for and , it follows that only when . This implies and the possible minimum value of in this setting is . When , for any , there exists a constant such that uniformly in . Then

We note that only when . The function attains the minimum value

at . With simple algebra, in this setting, we obtain the corresponding minimum value of at for some constant .

Theorem 8.5

Proof

Pitman’s asymptotic relative efficiency of the LF test over the GLR test is the limit of the ratio of the sample sizes required by the two tests to have the same asymptotic power at the same significance level, under the same local alternative [Pitman (2018), Chapter 7]. Suppose and are the sample sizes required for the LF test and the GLR test, respectively. The Pitman’s asymptotic relative efficiency of to is defined as

under the condition that and have the same asymptotic power under the same local alternatives in the sense that

Given , , we have , where . Hence,

| (78) |

From Theorem 8.3(i), we have

under , where with is defined in Theorem 8.1. Also, from Theorem 8.3(ii), we have

under , where with is defined in Theorem 8.2. To have the same asymptotic power, the noncentrality parameters must be equal which means or

| (79) |

Combination of (78) and (79) yields, for , ,

Now, we show for any positive kernels with . It is sufficient to show that

From Jensen’s inequality and Fubini’s theorem we obtain

| (80) |

Triangle inequality and (80) yields that

| (81) |

Combination of (81) and (80) yields

Hence, the LF test is asymptotically more efficient than the GLR test.

Numerical Comparison- Extra results

Conditional Bootstrap

-

(a)

Fix the bandwidths at their estimated values and then obtain the estimates of additive functions under both null and unrestricted additive models.

-

(b)

Compute , , , , , and the residuals , , from the unrestricted model.

-

(c)

For each , draw a bootstrap residual from the centered empirical distribution of and compute , where , and are the estimated additive functions under the restricted model in step (a). This forms a conditional bootstrap sample .

-

(d)

Using the bootstrap sample in step (c) and bandwidths in step (a), obtain , , , , , .

-

(e)

Repeat steps (c) and (d) for a total of times, where is large number. We then obtain a sample of statistics.

-

(f)

Compute the bootstrap values for all the statistics. Reject at a prespecified significance level if and only if . Repeat this process for the all the above statistics.