Semiparametric Estimation of Optimal Dividend Barrier for Spectrally Negative Lévy Process

Abstract

We disucss a statistical estimation problem of an optimal dividend barrier when the surplus process follows a Lévy insurance risk process. The optimal dividend barrier is defined as the level of the barrier that maximizes the expectation of the present value of all dividend payments until ruin. In this paper, an estimatior of the expected present value of all dividend payments is defined based on “quasi-process” in which sample paths are generated by shuffling increments of a sample path of the Lévy insurance risk process. The consistency of the optimal dividend barrier estimator is shown. Moreover, our approach is examined numerically in the case of the compound Poisson risk model perturbed by diffusion.

1 Introduction

In risk theory, surplus process is a very important model for understanding how the capital or surplus of an insurance company evolves over time. The classical model for the surplus process is the so-called “Cramér-Lundberg insurance risk model”. In this model, the insurance company collects premiums at a fixed rate from its customers. On the other hand, a customer can make a claim causing the surplus to jump downwards. The claim frequency follows a Poisson process, and the claim sizes are assumed to be independent and identically distributed (i.i.d.). A natural generalization of the Cramér-Lundberg model is a spectrally negative Lévy process also called “Lévy insurance risk model”, which has been studied in many actuarial literature, such as Feng (2011), Feng and Shimizu (2013), Kyprianou (2014) and so on. Thanks to the Lévy insurance risk model, we can grasp many realistic social phenomena in the surplus process such as the fluctuation of premium income, the effect of investment result, the effect of the small claim and so on. In this paper, we also suppose that the surplus of an insurance company follows the Lévy insurance risk process.

In risk theory, the central topics are the ruin time or ruin probability, but there is a dividend problem as one of the application. In the dividend problem introduced by De Finetti (1957) (especially, the so-called “constant barrier strategy”), assuming that there is a horizontal barrier of level , such that when an insurance company’s surplus reaches level , dividends are paid continuously such that the surplus stays at level until it becomes less than . The optimal strategy is to maximize the expectation of the present value of all dividend payments and the “optimal dividend barrier” is defined as a barrier of level where the maximization can be achieved. B’́uhlmann (1970), Lin (2003), Gerber et al. (2006), Li (2006), Loeffen (2008) derived the optimal dividend barrier explicitly in some special models such as the Cramér-Lundberg model with exponential claim amount distribution. On the other hand, Kyprianou (2014) discussed a stochastic control problem for the optimal dividend strategy when the surplus process follows the Lévy insurance risk process. In these papers, the main concern is the property from a probabilistic point of view, but there is a limited contribution in the statistical point of view. From the statistical point of view in ruin theory, a ruin probability by Croux and Veraverbeke (1990) and Shimizu (2009), a Gurber-Shiu function by Feng and Shimizu (2013) and an optimal dividend problem in the Cramér-Lundberg model by Shiraishi and Lu (2018) are discussed, respectively. In this paper, we discuss the statistical estimation problem in the Lévy insurance risk process.

Considering the optimal dividend problem in a statistical estimation framework, it can be reduced to an M-estimation problem if we can define our optimal dividend barrier estimator as a maximizer of an objective function which corresponds to an estimator of the expectation of the present value of all dividend payments. Note that, for the usual M-estimator, the objective function sometimes called a contrast estimator is defined by a sample mean of i.i.d. random variables. In the same way, our contrast estimator would be defined by a sample mean of the present value of all dividend payments. However, since the present value of all dividend payments is path dependent, in order to construct the contrast estimator, we need to provide a number of independent copy of sample paths; consequently, it is impossible to observe multiple sample paths. In addition, in practical point of view, it is reasonable to assume that the surplus of a insurance portfolio is observable discretely not continuously, such as hourly, daily, monthly and so on. To overcome these problems, we introduce “quasi-process”, that is, an approximation of the true Lévy insurance risk process. The quasi-process is composed by rearranging the increments of discretely observed data, thus, it is possible to generate multiple sample paths by changing the permutation. Essentially, it takes advantage of the exchangeability of the increments in the Lévy insurance risk process. Generating multiple quasi-process, it is possible to provide a number of (approximated) present value of all dividend payments, which implies that a contrast estimator can be defined. In our estimation procedure, the complexity of an estimator is characterized in the class of functions. In other words, our procedure is applicable not only to optimal dividend problem but also to many statistical inference problems defined as an M-estimation problem.

This paper is organized as follows. Section 2 defines the surplus process following the Lévy insurance risk process and the true optimal dividend barrier as a maximizer of the expectation of the present value of all dividend payments. We define the quasi-process from discretely observed data and show its weak convergence in Section 3. Then, the optimal dividend barrier estimator is also defined. Section 4 shows the consistency of the optimal dividend barrier estimator. To do so, the uniform consistency for the contrast estimator in the function set is shown based on the empirical process theory. In Section 5, we examine our approach numerically. When the surplus process follows the compound Poisson risk model perturbed by diffusion discussed in Li (2006), it is numerically confirmed that our proposed estimator converges in probability to the true optimal dividend barrier as observe interval goes to and the size of permutation set goes to infinity. We place all the proofs of the theorems and lemmas in Section 6.

2 Optimal Dividend Barrier

Given a stochastic basis with a filtration , we consider a Lévy process starting at of the form

| (1) |

where , , is a Wiener process and is a pure-jump Lévy process, independent of , with the characteristic exponent

When and , is called a subordinator, that is, a special class of Lévy processes taking values in and having non-decreasing paths. Let be a space of càdlàg functions on , and the subset be also a space of càdlàg functions on , restricted as follows:

For all , has the form (1), where and is a subordinator with .

Then, the belongs to the class of spectrally negative Lévy processes with for all (see, e.g., Sato (1999)). In this paper, we suppose that is an insurance risk process where is the insurer’s initial surplus, is a given premium rate per unit time, with the net profit condition , and is the aggregate claims process.

Let , where is a known positive value. For an insurance risk process and , we introduce a process by and

where . Note that is called the dividend strategy consisting of a process with initial value zero, which has paths that are left-continuous, non-negative, non-decreasing and adapted to the filtration of insurance risk process defined by (1). Let be the family of dividend strategies, and for each , write for the time of ruin under the dividend strategy . Here we call the controlled risk process and the time of ruin for the controlled risk process (see, e.g., Kyprianou (2014)); represents the cumulative dividends that the insurer has paid out until the time under a dividend strategy which the dividend payments are continued while the controlled risk process attains up to the time of ruin (see, e.g., Loeffen (2008)). The expected present value of all dividend payments, with discounting at rate , associated with the dividend strategy is given by

| (2) |

Loeffen (2008) and Yin et al. (2015) discussed the concavity for under some conditions. We suppose that is a bounded, infinitely differentiable, and strictrly concave function with respect to . Then, for any , there exists such that for all satisfying , it follows . We assume the proper proerty for in our main theorem (Theorem 4.1). \colorblack In insurance risk theory, the expected present value of a ruin-related ‘loss’ up to time of ruin is often discussed (e.g., Feng (2011) and Feng and Shimizu (2013)). Among them, the dividend problem discussed in De Finetti (1957) consists of solving the stochastic control problem which corresponds to a optimization problem

| (3) |

In this paper, we consider statistical estimation problem for when we observe an insurance risk process discretely.

3 Estimation of Optimal Dividend Barrier

Let be the Borel field on generated by the Skorokhod topology. We denote a distribution of on by and write

for a measurable function . Suppose that for a , random elements are independent copies of process , and denote its empricial measure as

where is the delta measure concentrated on . In practice, it is often impossible to observe the independent copies of and to observe the sample path continuously. To overcome these problems, we consider a construction of “multiple quasi-processes” from a discrete sample path. Suppose that we observe a discrete sample path from a insurance risk process , where the discrete sample path consists of with

Let be a vector of increments with , and let

be a family of all the permutations of . Since , , are i.i.d. for each , is exchangeable, that is, for any permutation ,

has the same distribution as .

Definition 1

For given and , a stochastic process given by

is said to be a quasi-process of for a permutation .

Note that a path of the quasi-process belongs to (but not to ), a right continuous step function that has a jump at () with the amplitude .

For the discrete sampling scheme, we impose the following assumption.

Assumption (High-Frequency sampling in the Long Term; HFLT)

and as .

Shimizu and Shiraishi (2022) showed the followings under HFLT.

Theorem 3.1

Under Assumption 1, we have, for any sequence of permutations ,

For a given size , let be a set of i.i.d. samples drawn uniformly from , i.e., for a given ,

Based on , we introduce two empirical measures and by

Next, we propose an estimator of defined by (3) based on the empirical measure of the quasi-process.

Definition 2

Given a vector of increments and permutation sets , we denote a maximum contrast estimator of defined by (3) as

where

For the moments of , we have following result.

Lemma 1

Under Assumption 1, we have, for any and ,

4 Asymptotic Results

Our main result in this paper is to provide the consistency for defined in Definition 2.

To do so, we assume that a size of permutation sets satisfies followings.

Assumption (Size of permutation sets)

as .

We recall that the empirical measure of the quasi-process is asymptotically equivalent in law with based on the independent copy of the process . Moreover, we introduce a sequence of a family of measurable functions on , where is a family of measurable functions for each , given by

| (4) |

where and for all and . Here is an identical permutation, i.e., . For the class , we denote by the covering number of which is the minimum number of -balls needed to cover , where an -ball around a function being the set , with being the -norm. In addition, we denote by the bracketing number which is the minimum number of -brackets in needed to ensure that every lines in at least one bracket, where an -bracket in is a pair of functions with and . For the covering number and bracketing number, we have following result.

Lemma 2

Under Assumptions 1 and 2, we have, for any

This lemma implies that both of the covering number and bracketing number diverge slower than . This result is applied for the proof of uniformly consistency below. The following result is due to a slight modification by Kosorok (2008; Theorem 8.15).

Lemma 3

Under Assumptions 1 and 2, we have

This lemma shows that two measure and are asymptotically equivalent on the function space . On the other hand, the true optimal dividend barrier defined by (3) is a maximizer of , where . Hence, we have to evaluate the difference between and defined by (2) and (4) based on the measure . The following lemma is also applied for the proof of our main result.

Lemma 4

Under Assumptions 1 and 2, we have

By Lemmas 3 and 4, we can show the consistency for , as follows.

Theorem 4.1

Suppose that Assumptions 1 and 2 are hold, and that there exists such that, for any ,

| (5) |

black Then, is weakly consistent to , i.e.,

5 Numerical Results

In this section, we present simulation results to evaluate the finite-sample performance of the proposed estimator of the optimal dividend barrier based on the discrete sample from spectrally negative Lévy processes. We consider the following data generating process (DGP), sampling scheme, permutation set and discount rate.

-

•

DGP (Brownian motion compound Poisson process): Let , where , is a standard Brownian motion, and is a compound Poisson process. The Poisson process has intensity . We set . The jump size is a sequence of i.i.d. random variables having exponential distribution with parameter , that is, .\colorblack

-

•

Sampling scheme: We consider the sampling interval and the terminal (fixed), which implies that sample size is , respectively.

-

•

Permutation set: We consider the subset of permutation set with , where the suffix is independently selected with same probability from .

-

•

Discount rate: We set .

5.1 Quasi Process

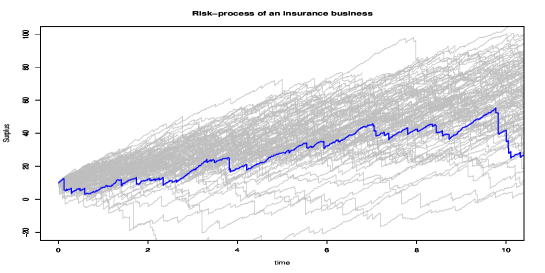

We first examine the finite sample performance of the quasi-process for each and . Figure 1 shows 100 sample paths for the risk process of an insurance business defined above. It looks that we can not know the distribution of only from one sample path without any additional assumption. In this study, we consider such a situation. When we suppose that only one sample path is observed discretely, we would like to know its distribution. In Figure 1, the blue line is observed discretely.

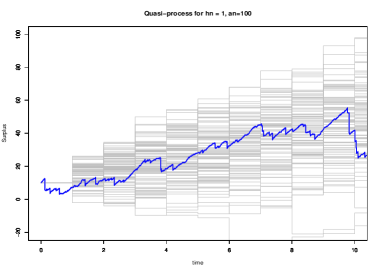

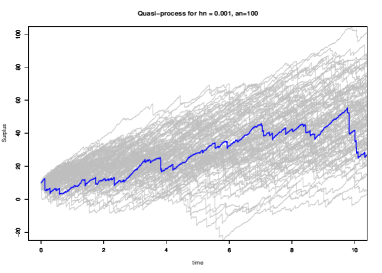

Under the sampling scheme defined above, we can construct a number of sample paths of the quasi-process from one sample path. Then, we can approximate the distribution of based on these sample paths. In Figure 2, the blue line is a observed (but discretely) sample path from the stochastic process (this is the same as Figure 1). From this sample path, we construct sample paths of the quasi-process based on Definition 1. Each sample path depends on the observed sample path and the permutation . The top figure shows the case of and , and the bottom figure shows the case of and . It looks that the top figure is not, but the bottom figure is well approximated the distribution of . This phenomenon comes from the exchangeability of the increments of the Lévy processes and if the sampling interval is sufficiently small and the size of permutation set is sufficiently large, we can well approximate the distribution of even from only one sample path.

5.2 Maximum Contrast Estimator

Next, we examine the behavior of the objective function . Given a sample path of the quasi-process , we can construct as a function of the parameter . Since each sample path of the quasi-process is locally constant on time , we can write

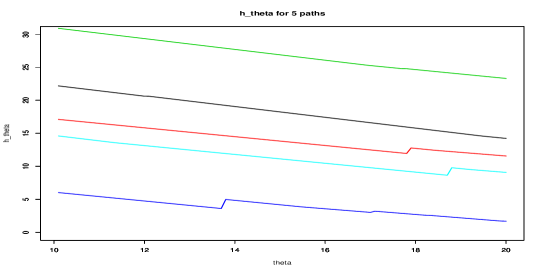

where with . Figure 3 shows the plots of for five sample paths of the quasi-process . In this figure, the horizontal axis represents the magnitude of and the vertical axis represents the magnitude of . Under a fixed sample path, it can be seen that is a locally decreasing function with some positive jumps. The locally decreasing property is that the total dividend amount tends to decrease as the dividend barrier increases while the ruin time is fixed. On the other hand, the existence of positive jump shows that the total dividend amount increases discontinuously since the ruin time is extended at some .

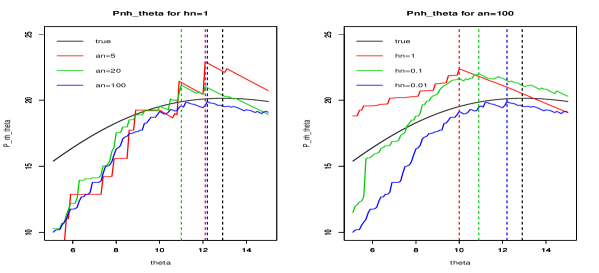

Figure 4 shows the behavior of the contrast function for some and . The left figure shows plots of the contrast function for the size of permutation set under fixed sampling interval , and the dotted line shows its maximization point. It can be seen that the function approaches the true function as increases which implies that the maxmization point tends to the true maximation point, that is, our proposed estimator converges to the true optimal dividend barrier . On the other hand, the right figure shows plots of the contrast function for under fixed . It can be seen that the function approaches the true function as decreases which implies that our estimator converges to the true optimal dividend barrier. In both figures, the black line represents the true objective function (see, e.g., Li (2006)). These figures confirm the validity of the theoretical result in Theorem 4.1.

5.3 Simulation result

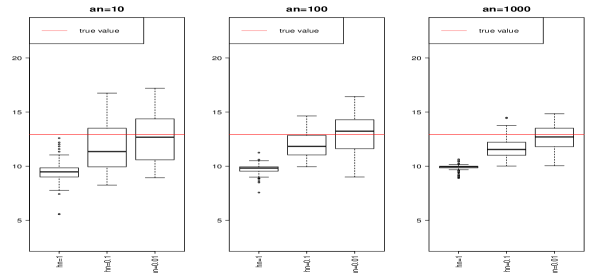

Now, we examine mean, standard deviation (std), bias, and MSE for and . We generate replications for each run of the simulations. Figure 5 shows the box-plot for estimated values for each and . The left figure is the case of , the middle figure is the case of , and the right figure is the case of . In each figure, the left box is the case of , the middle box is the case of , and the right box is the case of . The red line shows the true value . In view of the median (and mean) of the estimated values, it can be seen that the value converges to the true value as increases and decreases. On the other hand, in view of the dispersion, it looks that the estimated values shrink as increases. However, when is not sufficiently small, it seems that the estimated values converges to a value different from the true value. This phenomenon indicates that it is a warning that an asymptotic bias will occur unless the sampling interval is sufficiently small.

Table 1 shows mean , std , bias , and MSE of the estimated values for , and . It can be seen that the mean converges to the true value, and the MSE converges to as increases and decreases. Note that the bias tends to have negative value which implies that the distribution of the estimator tends to be asymmetric. From the insurer’s point of view, this phenomenon is a warning because setting a lower dividend barrier poses a risk to insures.

| mean | std | bias | MSE | ||

|---|---|---|---|---|---|

| 1 | 9.482 | 1.039 | -3.45 | 13.03 | |

| 10 | 0.1 | 11.778 | 2.106 | -1.16 | 5.78 |

| 0.01 | 12.560 | 2.126 | -0.37 | 4.66 | |

| 1 | 9.681 | 0.489 | -3.25 | 10.85 | |

| 100 | 0.1 | 12.009 | 1.290 | -0.92 | 2.52 |

| 0.01 | 12.964 | 1.558 | 0.02 | 2.42 | |

| 1 | 9.895 | 0.260 | -3.04 | 9.33 | |

| 1000 | 0.1 | 11.680 | 0.998 | -1.25 | 2.58 |

| 0.01 | 12.680 | 1.183 | -0.25 | 1.46 |

6 Proofs

This section shows proofs of lemmas and theorems.

6.1 Proof of Lemma 1

From the definition, we can write

where and is a sequence of i.i.d. random variables. From (1), we have

It is easy to see . Since , we have

which imply that for . By the Taylor expansion, we have

Therefore, we have

6.2 Proof of Lemma 2

By definition, for any and . Note that if , we define . This implies that we can divide into (), where with

For a fixed , it can be seen that for any if , which implies that

In addition, since (), where , we can write

which implies that

Since and , we have for any

Note that the -size of the brackets is bounded by , which imples that

Therefore, from Assumption 2, it follows that

From the relationship between bracketing number and covering number (cf., Kosorok (2008; Lemma 9.18)), we have

6.3 Proof of Lemma 3

By the symmetrization result (cf., Kosorok (2008; Theorem 8.8)), we can write

where is a sequence of independent Rademacher random variables which are independent of and satisfy , and are the expectations with respect to , respectively. \colorblack For any fixed , and , let be a sequence of finite -balls in over (i.e., is a subset of and for any , and ). For each , we fix (satisfying if ) which is a representative such that for any

black which implies that

| (6) |

black Let and . Then,

from Jensen’s inequality. On the other hand, based on the nondecreasing, nonzero convex function , we introduce the Orlicz-norm

for which . Applying the maximal inequality (cf., Kosorok (2008; Lemma 8.2)), we have

where the constant depends only on , which implies that the left-hand-side of (6) is bounded by

black up to a constant. By Hoeffiding’s inequality (cf., Kosorok (2008; Lemma 8.7)), we have

for any and each , where . Hence, from Kosorok (2008; Lemma 8.1) and Jensen’s inequality,

which, together with Lemma 1, implies that

uniformly in . From this and Lemma 2, converges to as and . ∎

6.4 Proof of Lemma 4

From the definition, we can write for any

where . For the term , Lemma 1 yields

| (7) |

for any fixed . Denoting and , the first term of the right hand side of (7) is bounded by

black Let be a space of càdlàg functions on . We now consider the Skorokhod topology , where is the Skorokhod metric defined by

for any (cf., Billingsley (1999)). Note that is the class of strictly increasing, continuous mappings of onto itself, for any , is the identity map on and . On this topology, we define a map by

Then, it is easy to see that

which implies that is continuous on . Therefore, by using the continuous mapping theorem, Theorem 1 implies

From the definition of the weak convergence, it follows that

as for any . Since from Lemma 1, we have as and . In the same way, we have as and . \colorblack For the term , Lemma 1 yields

for any fixed . Then, there exits a constant such that

| (8) | |||

| (9) |

as . Note that (8) is shown by and , and (9) is shown by from Theorem 1 and . Hence, as and . Therefore, we have

as and , uniformly in .∎

6.5 Proof of Theorem 2

Lemmas 3 and 4 imply that

as . Combining this and (5), we immediately have the conclusion from van der Vaart (1998; Theorem 5.7).∎

Acknowledgements.

The autors would like to thank the Editors for their constructive comments. The first author was partially supported by JSPS KAKENHI Grant Number JP21K03358 and JST CREST JPMJCR14D7, Japan. The second author was supported by JSPS KAKENHI Grant Number JP21K11793.References

- B’́uhlmann (1970) Bühlmann, H. (1970). Mathematical Methods in Risk Theory. Springer-Verlag, Berlin; Heidelberg; New York.

- Billingsley (1999) Billingsley, P. (1999). Convergence of probability measures. 2nd ed. John Wiley Sons, New York.

- Croux and Veraverbeke (1990) Croux, K. and Veraverbeke, N. (1990). Nonparametric estimators for the probability of ruin. Insurance: Mathematics and Economics, 9, 127-130.

- De Finetti (1957) De Finetti, B. (1957). Su un’impostazione alternativa della teoria collettiva del rischio. Transactions of the XVth international congress of Actuaries, 2, 433-443.

- Feng (2011) Feng, R. (2011). An operator-based approach to the analysis of ruin-related quantities in jump diffusion risk models. Insurance: Mathematics and Economics, 48, 304-313.

- Feng and Shimizu (2013) Feng, R. and Shimizu, Y. (2013). On a generalization from ruin to default in a Lévy insurance risk model. Methodol. Comput. Appl. Probab., 15, 773-802.

- Gerber et al. (2006) Gerber, H.U., Shiu, E.S.W., and Smith, N. (2006). Maximizing dividends without bankruptcy. Astin Bullitain, 36, 5-23.

- Lin (2003) Lin, X.S., Willmot, G.E., and Drekic, S. (2003). The classical risk model with a constant dividend barrier: analysis of the Gerber-Shiu discounted penalty function. Insurance: Mathematics and Economics, 33, 551-566.

- Li (2006) Li, S. (2006). The distribution of the dividend payment in the compound Poisson risk model perturbed by diffusion. Scandinavian Actuarial Journal, 2006, 73-85.

- Loeffen (2008) Loeffen, R. L. (2008). On Optimality of the Barrier Strategy in De Finetti’s Dividend Problem for Spectrally Negative Lévy Processes. The Annals of Applied Probability, 18, 1669-1680.

- Kosorok (2008) Kosorok, M. (2008). Introduction to empirical processes and semiparametric inference. Springer Science Business Media.

- Kyprianou (2014) Kyprianou, A.E. (2014). Fluctuations of Lévy processes with applications. 2nd ed. Springer, Heidelberg.

- Sato (1999) Sato, K. (1999). Lévy processes and infinitely divisible distributions. Cambridge University Press, Cambridge.

- Shimizu (2009) Shimizu, Y. (2009). A new aspect of a risk process and its statistical inference. Insurance: Mathematics and Economics, 44, 70-77.

- Shimizu and Shiraishi (2022) Shimizu, Y. and Shiraishi, H. (2022). M-Estimation based on quasi-processes from discrete samples of Lévy process. arXiv:2112.08199.

- Shiraishi and Lu (2018) Shiraishi, H. and Lu, Z. (2018). Semiparametric estimation in the optimal dividend barrier for the classical risk model. Scandinavian Actuarial Journal, 9, 845-862.

- van der Vaart (1998) van der Vaart, A.W. (1998). Asymptotic Statistics. Cambridge University Press, Cambridge.

- Yin et al. (2015) Yin, C., Yuen, K.C. and Shen, Y. (2015). Convexity of ruin probability and optimal dividend strategies for a general Lévy process. The Scientific World Journal, 2015.