[acronym]long-short

Bilevel Optimization for Feature Selection in the Data-Driven Newsvendor Problem

Breno Serrano∗

School of Management, Technical University of Munich, Germany, breno.serrano@tum.de

Stefan Minner

School of Management and Munich Data Science Institute, Technical University of Munich, Germany, stefan.minner@tum.de

Maximilian Schiffer

School of Management and Munich Data Science Institute, Technical University of Munich, Germany, schiffer@tum.de

Thibaut Vidal

Department of Mathematical and Industrial Engineering, Polytechnique Montréal, Canada,

Department of Computer Science, Pontifical Catholic University of Rio de Janeiro, Brazil, thibaut.vidal@polymtl.ca

Abstract. We study the feature-based newsvendor problem, in which a decision-maker has access to historical data consisting of demand observations and exogenous features. In this setting, we investigate feature selection, aiming to derive sparse, explainable models with improved out-of-sample performance. Up to now, state-of-the-art methods utilize regularization, which penalizes the number of selected features or the norm of the solution vector. As an alternative, we introduce a novel bilevel programming formulation. The upper-level problem selects a subset of features that minimizes an estimate of the out-of-sample cost of ordering decisions based on a held-out validation set. The lower-level problem learns the optimal coefficients of the decision function on a training set, using only the features selected by the upper-level. We present a mixed integer linear program reformulation for the bilevel program, which can be solved to optimality with standard optimization solvers. Our computational experiments show that the method accurately recovers ground-truth features already for instances with a sample size of a few hundred observations. In contrast, regularization-based techniques often fail at feature recovery or require thousands of observations to obtain similar accuracy. Regarding out-of-sample generalization, we achieve improved or comparable cost performance.

Keywords. Feature Selection; Bilevel Optimization; Newsvendor; Mixed Integer Programming.

∗ Corresponding author

Declarations of interest: none

1 Introduction

The newsvendor problem and its variants have served as fundamental building blocks for models in inventory and supply chain management. In the classical newsvendor problem, a decision-maker optimizes the inventory of a perishable product that has a stochastic demand with a known distribution. However, having complete knowledge of the demand distribution is a strong assumption that does not hold in practice: often, the only information available is a limited set of historical data. Against this background, data-driven approaches became popular and strive to use past demand data to inform the newsvendor’s ordering decisions.

In this context, we study the feature-based newsvendor problem (cf. Beutel & Minner 2012, Ban & Rudin 2019) in which the decision-maker has access not only to historical demand observations but also to a set of feature variables—often referred to as contextual information or covariates—that may provide partial information about future realizations of the uncertain demand. Companies nowadays have large amounts of data that are used to train machine learning models with the aim of improving operational decisions. In practice, such models often suffer from overfitting to the training data, or lack explainability, which is crucial, e.g., when dealing with high-stakes decisions. In this setting, selecting a subset of the available features can lead to sparser, more explainable models with improved out-of-sample performance. Against this background, we investigate the challenge of feature selection (cf. Molina et al. 2002, Kuhn & Johnson 2019): given a data set with a possibly large set of feature variables, we aim to learn a linear decision function for the feature-based newsvendor that can generalize to out-of-sample data, utilizing only relevant features.

The goal of this paper is to propose an approach to feature selection based on bilevel optimization. We search for a subset of features that leads to a minimal out-of-sample cost measured on a held-out data set, when used for training a linear decision function for the feature-based newsvendor. In the remainder of this section, we first review related literature before we detail our contribution and describe the organization of this paper.

1.1 Related Works

Our work relates to the fields of data-driven optimization for the newsvendor problem, and more broadly to prescriptive analytics, machine learning, and bilevel programming. We briefly review the most related papers in the following.

Newsvendor problem. Research on the newsvendor problem often assumed a decision-maker with full knowledge about the demand distribution, and considered various settings, e.g., with different objectives or utility functions (Chen et al. 2007, Wang & Webster 2009), pricing policies (Petruzzi & Dada 1999), and multi-product or multi-period settings (Lau & Lau 1996, Kogan & Lou 2003). For general surveys on newsvendor models and extensions, we refer the interested reader to Khouja (1999), Qin et al. (2011) and Choi (2012). In practice, the decision-maker often has only a finite set of demand observations and cannot estimate the true underlying distribution, which motivated works on the distribution-free newsvendor problem. In this context, the seminal work of Scarf (1958) derived the optimal order quantity that maximizes profit against the worst-case demand distribution, assuming that only the mean and variance of demand are known. For a review on the distribution-free newsvendor and extensions thereof, we refer to Gallego & Moon (1993), Moon & Gallego (1994), and Yue et al. (2006). Later works on this problem variant assumed additional information about the demand distribution, such as percentiles (Gallego et al. 2001), symmetry, and unimodality (Perakis & Roels 2008).

In contrast to working with moments or distributional parameters, data-driven approaches build directly upon a sample of available data that reflects realizations of the underlying uncertainty. In this context, a common solution approach is sample average approximation (SAA) (cf. Kleywegt et al. 2002, Shapiro 2003). Levi et al. (2007) applied SAA for the single-period featureless newsvendor problem and established upper bounds on the number of samples required to achieve a specified relative error. In this course, Levi et al. (2015), Cheung & Simchi-Levi (2019), and Besbes & Mouchtaki (2021) further improved upon previous SAA bounds. Besbes & Muharremoglu (2013), Sachs & Minner (2014), and Ban (2020) studied the impact of demand censoring, i.e., a problem variant in which only sales observations are available but excess demand is not recorded. They derived upper and lower bounds on the difference between the cost achieved by a policy and the optimal cost with knowledge of the demand distribution. Adopting a robust optimization perspective, Bertsimas & Thiele (2005) proposed a data-driven approach that can be reformulated as a linear program (LP) and trades off higher profits for a decrease in the downside risk. Robust optimization approaches were also investigated by Bertsimas & Thiele (2006) and See & Sim (2010) for a multi-period inventory problem. Finally, many authors applied data-driven distributionally robust approaches for dealing with uncertainty in the context of multi-item newsvendor problems (see, e.g., Ben-Tal et al. 2013, Hanasusanto et al. 2015, Wang et al. 2016, and Bertsimas et al. 2018).

Despite numerous extensions to the newsvendor problem, most data-driven approaches consider only demand data but no feature variables to be available. However, ignoring the presence of features can lead to inconsistent decisions as shown in Ban & Rudin (2019). In the following, we review papers that also consider the presence of features in the context of data-driven optimization.

Data-driven optimization. Beyond the newsvendor problem, some recent works have studied the integration of estimation and optimization. In particular, Bertsimas & Kallus (2020) proposed a framework for feature-based stochastic optimization problems based on a weighted SAA approach, in which the weights are generated by machine learning methods, such as -nearest neighbors regression, local linear regression, classification and regression trees, or random forests. Elmachtoub & Grigas (2021) focused on problems with a linear objective and used features to learn a prediction model for the stochastic cost vector. They proposed a modified loss function that directly leverages the structure of the optimization problem instead of minimizing a standard prediction error, such as the least squares loss. Despite this modification, their approach still handles prediction and optimization as separate tasks and does not integrate them into a one-step process. Mandi et al. (2020) further adapted the approach from Elmachtoub & Grigas (2021) to solve some hard combinatorial problems, e.g., by proposing tailored warm-starting techniques.

In the context of the feature-based newsvendor, Beutel & Minner (2012) integrated estimation and optimization by learning a decision function that predicts ordering decisions directly from features, opposed to first estimating the demand and then optimizing the inventory level. The proposed model formulation is an LP that solves an Empirical Risk Minimization (ERM) problem over a training data set. Oroojlooyjadid et al. (2020) and Zhang & Gao (2017) applied neural networks to the newsvendor problem, proposing specific loss functions that consider the impact of inventory shortage and holding costs. Huber et al. (2019) provided an empirical evaluation of different data-driven approaches for the feature-based newsvendor and compared their performance against model-based approaches, which model the uncertainty through a demand distribution assumption. Their experiments on real-world data showed that data-driven approaches outperform their model-based counterparts in most cases.

Regarding feature selection, Ban & Rudin (2019) extended the model of Beutel & Minner (2012) by including a regularization term to the objective function, which penalizes the complexity of the solution, thereby favoring the selection of fewer features. However, feature selection is not the main focus of Ban & Rudin (2019), and an open challenge remains regarding the specification of the regularization parameter, for which heuristics are often employed. In this work, we avoid regularization by formalizing the task of feature selection as a bilevel optimization problem for which we provide a tractable single-level reformulation.

Bilevel optimization in machine learning. Bilevel optimization has been applied in the field of machine learning for hyperparameter optimization (Bennett et al. 2006, 2008, Franceschi et al. 2018, Mackay et al. 2019) and feature selection (Agor & Özaltın 2019). In particular, Bennett et al. (2006, 2008) proposed a bilevel program for optimizing the hyperparameters of a \glsxtrlongSVR model. They reformulated the model into a single-level \glsxtrlongNLP and employed off-the-shelf solvers based on \glsxtrlongSQP (Fletcher & Leyffer 2002). Franceschi et al. (2018) also proposed a bilevel programming approach for hyperparameter optimization, highlighting connections to meta-learning, and solved it with a gradient-based method.

Only Agor & Özaltın (2019) addressed feature selection as a bilevel optimization problem in the context of classification models, e.g., Lasso-based logistic regression and support vector machines. However, their bilevel formulations do not apply to our problem setting, since the feature-based newsvendor combines aspects from supervised learning, i.e., regression, and data-driven optimization. Moreover, the solution method of Agor & Özaltın (2019) consists of a tailored genetic algorithm, which does not provide solution-quality guarantees. In contrast, our methodology is based on mixed integer linear programming (MILP) and allows to optimally solve the proposed bilevel programming formulations.

1.2 Contribution

We close the research gaps outlined above by proposing a novel bilevel optimization model that directly incorporates feature selection into solving the data-driven newsvendor problem. Specifically, our contribution is fourfold. First, we introduce a bilevel program designed for feature selection, which we denote the Bilevel Feature Selection (BFS) model. In contrast to regularization-based methods, which penalize the norm of the solution vector, BFS captures the more intuitive notion of selecting a subset of features that minimizes an estimate of the out-of-sample cost, measured on a held-out validation set. We reformulate the bilevel program into a single-level optimization problem, which we solve to optimality with off-the-shelf optimization solvers. Second, we extend the BFS model to accommodate cross-validation strategies, which further improves its solution quality. Third, to illustrate the drawback of regularization-based methods for feature selection, we present a bilevel program, which we refer to as Bilevel Hyperparameter Optimization (BHO), that searches for the optimal hyperparameter for the regularized ERM model (cf. Ban & Rudin 2019). BHO formally describes the optimization model that established hyperparameter optimization methods implicitly solve by means of heuristics, such as grid search, random search, or Bayesian optimization. Fourth, we conduct extensive numerical experiments, using synthetic instances with correlated features. We compare the proposed BFS models against regularization-based methods in terms of out-of-sample performance and ground-truth feature recovery. We further compare the methods’ behavior under demand misspecification, assuming a nonlinear demand model. Our results show that the proposed BFS approach consistently achieves higher accuracy in feature recovery. In most cases, we also observe an improvement in out-of-sample cost performance, i.e., a decrease in test cost.

1.3 Organization

The remainder of this paper is structured as follows. In Section 2, we review the model formulations for the classical newsvendor and the feature-based newsvendor problem. Section 3 presents the BHO and the BFS models, and consecutively extends the BFS to cross-validation. Section 4 describes our experimental design, and Section 5 presents the results comparing the proposed method against state-of-the-art techniques based on regularization. Section 6 concludes this paper and gives an outlook on future research.

2 Fundamentals

In the classical newsvendor problem, a risk-neutral decision-maker sets the order quantity of a product before observing its uncertain demand. Here, the objective is to minimize the expected cost:

| (1) |

where is the order quantity, is the random variable representing the uncertain demand,

| (2) |

is the cost of ordering units and observing demand , based on the per unit shortage cost for lost profits and unit holding cost , corresponding to the procurement cost of unsold products discounted by their unit salvage value. If the demand distribution is known, then the optimal decision is given at the quantile of its cumulative distribution function.

In practice, the demand distribution is often not known. We consider the feature-based newsvendor problem, in which the decision-maker has access to historical demand data and contextual information given by a set of feature variables (cf. Beutel & Minner 2012). Here, the uncertain demand and feature variables follow an (unknown) joint probability distribution . The decision-maker’s objective is to minimize the expected cost conditioned on the observed features:

| (3) |

One approach to solve the feature-based newsvendor is to separate the estimation and optimization problems, i.e., one first estimates the conditional demand distribution from historical data and then optimizes the order quantity based on new feature observations. One drawback of this approach is that the first step’s estimation problem does not account for the asymmetry in the newsvendor cost function, related to under- and over-predicting demand. To address this issue, Beutel & Minner (2012) proposed to integrate estimation and optimization into a one-step process, by introducing a linear decision function that maps feature observations directly to ordering decisions. To learn the optimal coefficients of the decision function, one minimizes the empirical cost over a data set with demand and feature observations.

Let be a data set indexed by , where is an -dimensional feature vector and is a scalar demand observation. Let denote the set of feature indices. We assume that represents the feature-independent intercept term, for all . In this setting, Beutel & Minner (2012) consider a linear decision function of the form:

| (4) |

where is the parameter vector, whose values are learned by minimizing the empirical cost on data set . Upon observing new feature values, the decision-maker can then directly decide upon the order quantity instead of first estimating the uncertain demand.

Since the learned decision function may overfit to the in-sample data set , it is common practice in machine learning to evaluate the out-of-sample generalization on a separate test data set . To avoid overfitting and improve the out-of-sample generalization, Ban & Rudin (2019) proposed an extension of Beutel & Minner (2012) by integrating a regularization term into the loss function. Accordingly, the objective comprises a trade-off between minimizing the empirical in-sample cost and the regularization term, with a constant hyperparameter balancing these two terms:

| (ERM-) | (5) | |||||

| s.t. | (6) | |||||

where is the regularization hyperparameter and is the -norm of the vector . Depending on the choice of in the regularization, the resulting model may be a MILP, an LP, or a \glsxtrlongSOCP, for , , and -norm regularization, respectively. Effectively, regularization enables feature selection by penalizing the complexity of the solution, thereby favoring sparse solution vectors.

3 Methodology

We start this section presenting the BHO model, which incorporates hyperparameter fitting in (ERM-). Then, we introduce the BFS model as an alternative bilevel program that avoids regularization.

3.1 Bilevel Hyperparameter Optimization (BHO)

In Section 2, we assumed the hyperparameter as introduced in (ERM-) to be given. However, identifying constitutes a challenge in itself as a respective misspecification can significantly reduce cost performance. To parametrize correctly, one may utilize existing techniques for hyperparameter optimization, which partition the original data set into a training set and a validation set . On the training set, one learns the model parameters for a fixed hyperparameter value. Using the validation set, one can then assess the cost of the trained model for a variety of hyperparameter values, to finally choose the value that leads to a minimum cost on the validation set. Next, we present the BHO formulation, which models the search for the optimal hyperparameter as a bilevel optimization problem.

We introduce variables to model the inventory shortage and variables to model the surplus inventory at the end of period . In the following bilevel programming formulation, the upper-level (UL) problem searches for an optimal regularization value that minimizes cost on the validation set . In turn, the lower-level (LL) problem solves the feature-based newsvendor, as stated in (ERM-), on the training set :

| (BHO- UL) | (7) | |||||

| s.t. | (8) | |||||

| (9) | ||||||

| (10) | ||||||

| (11) | ||||||

where is the set of optimal solutions to the lower-level problem, parameterized by :

| (BHO- LL) | (12) | |||||

| s.t. | (13) | |||||

| (14) | ||||||

| (15) | ||||||

The upper-level objective (7) minimizes the newsvendor cost on the validation set and the lower-level objective (12) minimizes the regularized newsvendor cost on the training set . Constraints (8) and (13) define the inventory shortage for period and , respectively, given the decision function parametrized by . Constraints (9) and (14) define the surplus inventory at period and . Constraints (10), (11), and (15) define the variable domains.

So far, we define the BHO formulation in (7)–(15) for a general -norm, which leads to a different model for different . In the following, we illustrate some properties of BHO under the special case of the -norm regularization, which minimizes the number of non-zero elements in the vector. In this case, we introduce the binary variable to indicate whether coefficient is non-zero. The lower-level problem can then be formulated as a mixed integer program (MIP):

| (BHO- LL) | (16) | ||||

| s.t. | (13)–(15) | ||||

| (17) | |||||

| (18) | |||||

where Constraints (13)–(15) define the shortage and surplus inventory and Constraints (17) enforce that if the corresponding feature is not selected.

The BHO formulation (7)–(15) generalizes many common methods for hyperparameter optimization. To avoid the high computational effort of solving the BHO model to optimality, existing methods relax the assumption that can take any value in , and consider a finite support set instead (Bergstra & Bengio 2012, Bergstra et al. 2013). For example, suppose the values in are equally spaced along a grid, i.e., a line segment, then the resulting model corresponds to the well-known grid search method. If the values in are randomly selected in a closed region, then the formulation describes the random search method. Other approaches, e.g., based on Bayesian optimization, would perform an adaptive search, iteratively selecting a value for the upper-level variable and then optimizing the lower-level problem. The iterative selection of new values for depends on the validation performance of previously selected points. In essence, current methods for hyperparameter optimization, such as the examples described above, are heuristics that avoid solving the BHO model to optimality.

3.2 Bilevel Feature Selection (BFS)

To remedy the drawback of BHO, we introduce a bilevel programming formulation specifically designed for feature selection. Instead of penalizing the number of selected features, we propose a more intuitive model, in which the upper-level problem selects a subset of features that minimize the empirical cost on a validation set. We then reformulate the resulting model into a single-level problem, which is computationally more tractable, and finally compare the proposed BFS and BHO models.

Consider our original data set , which we partition into a training set and a validation set . We introduce binary variables , for , to indicate whether feature is marked as relevant () or not (). In the upper-level, BFS selects a subset of features that minimizes the empirical cost on the validation set . The lower-level problem then learns the optimal coefficients of the decision function in the training set by solving the ERM model using only the features selected in the upper-level. We formulate the resulting upper-level problem as follows:

| (BFS UL) | (19) | ||||

| s.t. | (8)–(10) | ||||

| (20) | |||||

| (21) | |||||

where is the set of optimal solutions to the lower-level problem:

| (BFS LL) | (22) | ||||

| s.t. | (13)–(15) | ||||

| (23) | |||||

The upper and lower-level objectives (19) and (22) minimize the newsvendor cost on the validation set and training set , respectively. Constraints (8)–(10) and (13)–(15) define the shortage and surplus inventory. Constraints (20)–(21) define the variable domains and Constraints (23) ensure that if feature is not selected.

We reformulate Model (19)–(23) by substituting the lower-level problem by its Karush-Kuhn-Tucker (KKT) conditions (cf. Cao & Chen 2006, Fontaine & Minner 2014). We introduce the dual variables , and corresponding to constraints (13) and (14) of the lower-level problem. The equivalent single-level (SL) optimization problem can then be expressed by using indicator constraints:

| (BFS SL) | (24) | ||||

| s.t. | (8)–(10), (13)–(15), (20), (23) | ||||

| (25) | |||||

| (26) | |||||

| (27) | |||||

| (28) | |||||

| (29) | |||||

As before, Constraints (8)–(10) and (13)–(15) define the shortage and surplus inventory. Constraints (20) and (23) model the selection of features. Constraint (25) represents the optimality condition of the lower-level problem, by comparing its primal objective value with the corresponding dual objective value. Constraints (26) and (27) are the dual constraints of the lower-level problem associated with primal variables and for . Constraints (28) are the dual constraints related to the primal variables for , and Constraints (29) define the domain of the dual variables. The single-level reformulation has variables and constraints.

The BFS model shares some similarities with the BHO model. Both models have the same upper-level objective and the lower-level objectives differ only in the presence of the regularization term. We provide an overview of the main properties of both models in Table 1. The main advantage of the BFS model regarding tractability is due to the existence of binary variables being limited to the upper-level problem. Consequently, we can reformulate the BFS model into a MILP and leverage the power of today’s optimization software to find optimal solutions.

| Formulation | BHO (-norm reg.) | BFS | |

|---|---|---|---|

| Upper-level | Objective | minimize validation cost | minimize validation cost |

| Variables | |||

| Lower-level | Objective | minimize training cost + regularization | minimize training cost |

| Variables | |||

Moreover, the following results show that the optimal cost of the BFS model is a lower bound to the optimal cost of the BHO model when adopting -norm regularization.

Lemma 1.

Given a fixed selection of features for both BHO and BFS, i.e., (assuming that is feasible for both problems), solving the remaining problems for the rest of the decision variables yields optimal solutions with costs .

Proof.

By fixing , the regularization term in the lower-level objective becomes constant and does not influence the optimal solution. Therefore, we can ignore regularization and the lower-level problem of the BHO becomes equal to the lower-level problem of the BFS, leading to as the optimal solution. Since the upper-level objectives are equal in both models, the optimal costs will be equal: . ∎

Proposition 1.

The optimal cost of the BFS model is a lower bound for the optimal cost of the BHO model with -norm regularization: .

Proof.

Let be the optimal selection of features according to BHO with cost . Suppose that is a solution to BFS, such that . We can always improve the cost of BFS by setting in the upper-level problem. Because of Lemma 1, this will result in a new solution with cost . ∎

3.3 Bilevel Feature Selection with Cross-Validation (BFS-CV)

Cross-validation strategies often improve the generalization ability of machine learning models and prevent overfitting by using data re-sampling methods. Accordingly, we extend the BFS model to cross-validation instead of simple hold-out validation. We consider training-validation splits of the data and search for the set of features that minimize the average cost over all validation sets. For each , we consider a subset of observations sampled from the original data set . Analogously to BFS, we partition the set into a training set and a validation set . We introduce variables and to model the inventory shortage and surplus, respectively, at the end of period for each training-validation split . We then learn the model parameters using the corresponding training set , and select features by minimizing the average validation cost over all validation sets for . The resulting problem is a bilevel program with lower-level problems:

| (BFS-CV UL) | (30) | |||||

| s.t. | (31) | |||||

| (32) | ||||||

| (33) | ||||||

| (34) | ||||||

| (35) | ||||||

where is the set of optimal solutions corresponding to the lower-level problem:

| (BFS-CV LL) | (36) | |||||

| s.t. | (37) | |||||

| (38) | ||||||

| (39) | ||||||

| (40) | ||||||

Constraints (31)–(33) and (37)–(39) define the shortage and surplus inventory for period and , respectively for each split . Constraints (34) and (35) define the variable domains and Constraints (40) ensure that if feature is not selected for the training-validation split .

The above model can accommodate different cross-validation strategies, such as -fold, random permutations (Shuffle & Split), or Leave-P-Out cross-validation (see, e.g., Arlot & Celisse 2010, Hastie et al. 2009). Each particular choice of cross-validation strategy corresponds to a different approach for constructing the subsets and partitioning the data into and . Moreover, the special case with corresponds to the previously introduced BFS model.

Analogously to BFS, Bilevel Feature Selection with cross-validation (BFS-CV) can be reformulated into a single-level MILP:

| (BFS-CV SL) | (41) | ||||

| s.t. | (31)–(34), (37)–(40) | ||||

| (42) | |||||

| (43) | |||||

| (44) | |||||

| (45) | |||||

| (46) | |||||

Constraints (42) represents the optimality condition of the lower-level problem, for each training-validation split . Constraints (43) and (44) are the dual constraints of the lower-level problem associated with primal variables and for for . Constraints (45) are the dual constraints related to the primal variables for , and Constraints (46) define the domain of the dual variables. The single-level reformulation has variables and constraints.

4 Experimental Design

To benchmark our approaches, we perform extensive computational experiments on synthetic instances. The goals of our computational experiments are fourfold.

-

1.

We evaluate the performance of a MILP approach for the proposed BFS and BFS-CV models in terms of feature selection and generalization to out-of-sample data;

-

2.

We compare the performance of our approach against existing regularization-based methods;

-

3.

For each method, we compare the performance of hold-out validation against cross-validation;

-

4.

We analyze the effect of different instance parameters on each method’s performance.

We implemented all methods in C++, using CPLEX 20.1 to solve the respective MILP formulations. All experiments were performed on machines with Intel Core i7-6700 CPU at 3.40 GHz, with 16 GB of RAM, and Ubuntu 16.04.6 LTS operating system, under a time limit of 900 seconds. We provide the source code and data at [to be disclosed after peer-review].

4.1 Instances

We adapt the experimental setup from Zhu et al. (2012) and consider a linear demand model with additive noise:

| (47) |

where is an -dimensional vector representing the ground-truth coefficients. The feature variables are drawn from a multivariate Gaussian distribution with mean zero and covariance matrix with entries , for . The noise term follows a Gaussian distribution . We set negative demand values to zero.

We generate instances varying the number of samples from 40 to 2000 and the number of features from 8 to 14. For each configuration, we generate 20 instances to account for variability in the distributions. Additionally, we generate a separate test set with 1000 observations associated with each instance, following the same distributions.

Furthermore, we analyze the impact of demand misspecification, i.e., when the demand is not linearly related to the features. We investigate the following nonlinear demand model (cf. Zhu et al. 2012):

| (48) |

where for a homoscedastic case and for a heteroscedastic case.

We solve the proposed BFS and BFS-CV models and compare the results against regularization-based methods from the literature. Since our motivation for feature selection is to provide more explainable decisions, we focus on methods based on linear decision functions, which are intrinsically more explainable. We consider the ERM model of Ban & Rudin (2019) with and -norm regularization and use grid search with 50 break-points to calibrate the regularization parameter. We run each considered method once using a hold-out validation set and once with Shuffle & Split cross-validation (CV). For hold-out validation, we use half of the samples in each instance as a training set and the other half as a validation set, following the setting in Zhu et al. (2012). For cross-validation, we perform re-sampling iterations, where we sample a subset of size , for each .

4.2 Performance metrics

We assess the ability of each method to recover the ground-truth feature vector, adopting the accuracy measure:

| (49) |

where is the indicator function, is the estimated binary feature vector, and is the ground-truth vector, defined as if , i.e., feature is non-informative, otherwise . Our definition of accuracy is analogous to the one commonly adopted for binary classification, where represents the class assigned to feature .

Additionally, we analyze the cost performance of applying the learned decision functions to out-of-sample data. We therefore evaluate the out-of-sample cost on a separate test data set with 1000 observations. We report the test cost values of each method in terms of its percentage deviation relative to the test cost achieved by BFS-CV on the same configuration:

| (50) |

where is the average newsvendor cost of method calculated on the test set. Deviation values greater than zero indicate that BFS-CV improves upon method regarding test cost performance, while values below zero indicate that method achieves lower test cost than BFS-CV.

5 Results

First, we present results concerning instances generated by the linear demand model, and then discuss results on instances with nonlinear demand.

5.1 Linear demand model

We analyze how instance size, number of features, noise level, shortage cost, and holding cost affect the performance of each method. Unless otherwise stated, we use a setting with samples, features, a shortage cost of , and a holding cost of as reference configuration. For the noise term, we consider as reference configuration for the Gaussian distribution. We provide results regarding computation times in A.

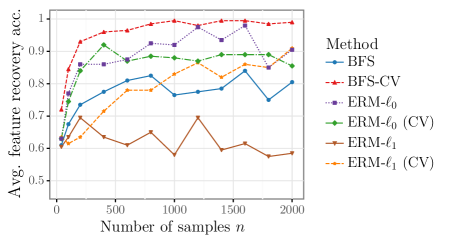

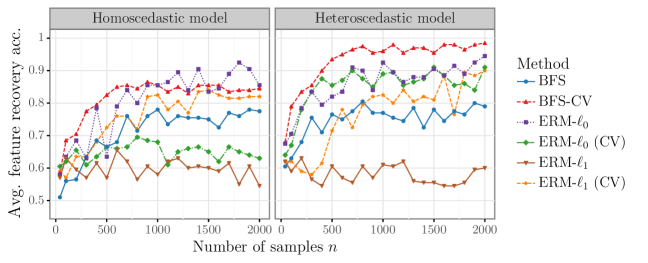

Instance size. Figure 1 reports the feature recovery accuracy of the different methods for a varying number of samples , averaged over randomly generated instances. In general, BFS-CV achieves the highest accuracy among all methods and faster convergence for increasing , with accuracy values above already for instances with samples. In contrast, existing methods often yield accuracy values below and fail to recover the ground-truth features accurately, even for instances with a larger number of samples. We confirm these results at significance level by pairwise Wilcoxon signed-rank tests, and refer to B for details on the respective p-values.

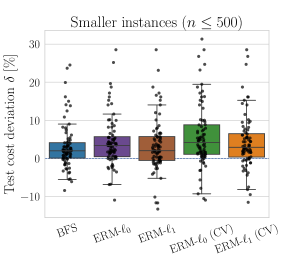

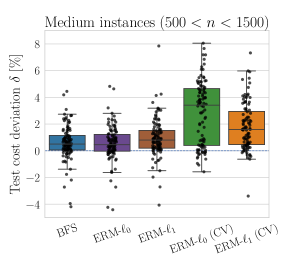

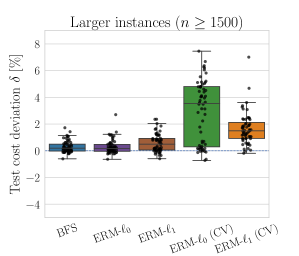

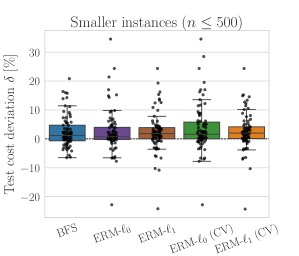

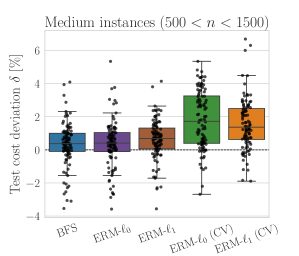

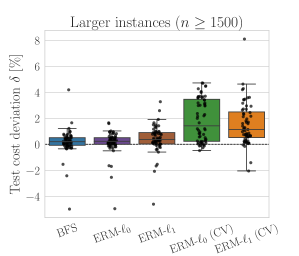

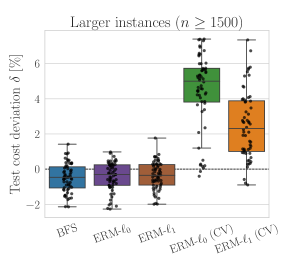

Besides feature recovery, we evaluate the out-of-sample cost performance of each method. Figure 2 shows the distribution of percentage deviations, where a positive deviation indicates that BFS-CV is superior to the respective other method. We split the results in three different plots based on the sample size , classifying each instance as small, medium, or large. BFS-CV outperforms the other methods in most cases, as the lower quartiles are always above or close to zero. For smaller instances, test cost deviations can be as high as in the best case. As we increase , all methods present improving test cost performance and the variance in the test cost distribution decreases. Yet, BFS-CV is still superior to the other methods in the wide majority of cases. For large instances, all methods present mostly positive test cost deviations, with values ranging from to .

|

|

|

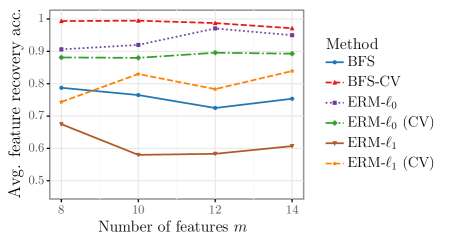

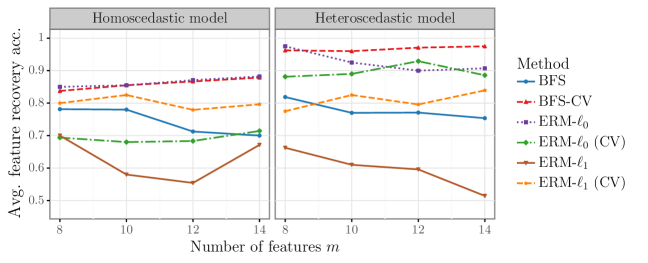

Number of features. Figure 3 shows average feature recovery accuracy values, where we now fix the number of samples to and vary the number of features . For all methods, the number of features does not strongly affect the accuracy performance. Notably, BFS-CV achieves average accuracy values consistently above , being superior to the other methods, as confirmed by pairwise Wilcoxon tests.

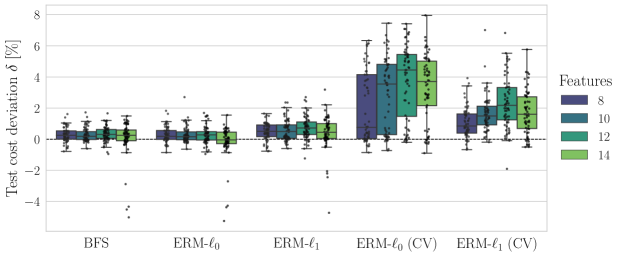

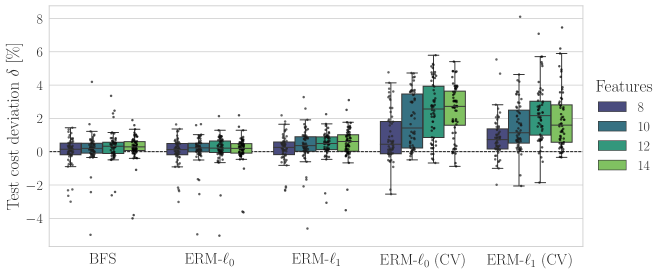

Regarding test cost performance, Figure 4 shows the distribution of test cost deviations. We focus on large instances () in this analysis, which have lower variance, so that we can isolate the impact of on the test cost. For BFS, ERM-, and ERM-, the number of features has no strong influence on the test cost deviations. In contrast, the performance of ERM- (CV) and ERM- (CV) shows increasing deviation values for increasing . In the majority of cases, BFS-CV outperforms the other considered methods.

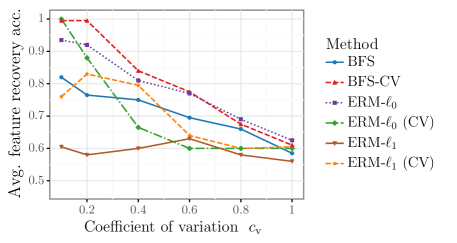

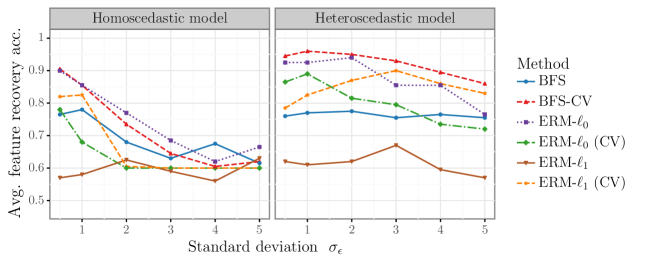

Noise level. We vary the coefficient of variation and report the average feature recovery accuracy for each method in Figure 5. As we increase the level of noise, it becomes harder to recover the informative features and the accuracy of all methods deteriorates. For , BFS-CV achieves the highest accuracy among the considered methods. Outside this range, BFS-CV is outperformed by ERM- (CV) for and by ERM- for , respectively. Still, BFS-CV generally attains comparatively high accuracy, being superior to most other methods.

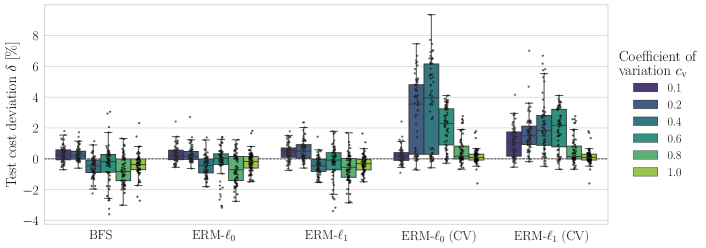

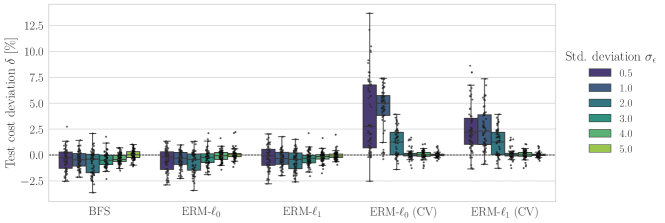

Figure 6 illustrates the impact of different noise levels on test cost performance, considering large instances (). Methods BFS, ERM-, and ERM- mostly outperform BFS-CV for . In such cases, test cost deviations range from to , indicating that BFS-CV achieves comparable results even when its performance is inferior to other methods. Methods ERM- (CV) and ERM- (CV) perform comparatively worse, with mostly positive deviations and larger variance in the distribution.

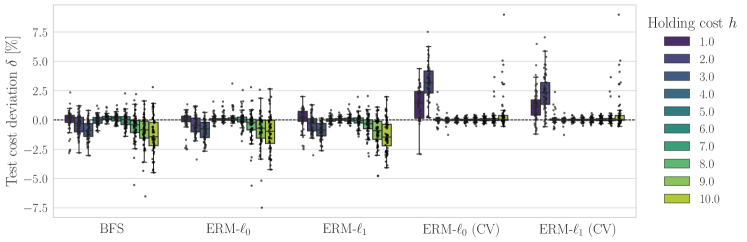

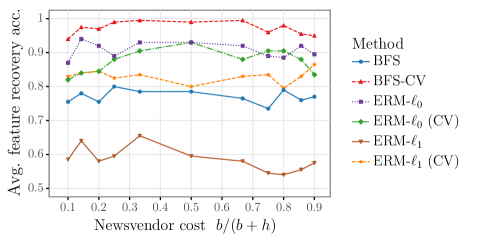

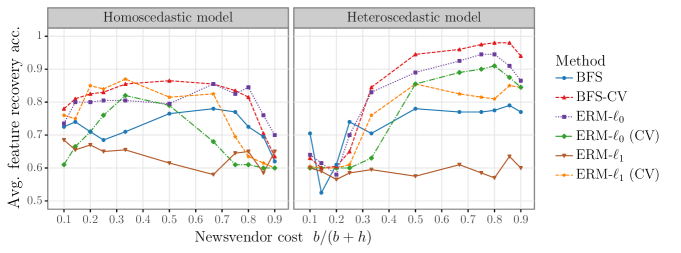

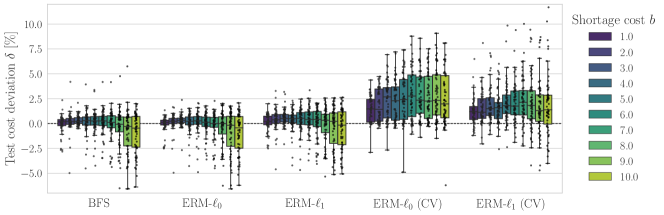

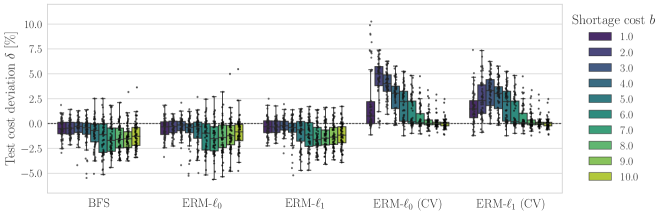

Shortage and holding costs. Figure 7 displays results on the accuracy performance as a function of the newsvendor ratio , by varying . In general, BFS-CV has accuracy values consistently above and outperforms the other methods.

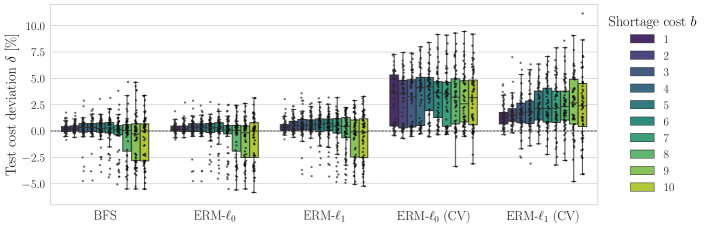

Figure 8 shows results on test cost performance of each method as a function of , for large instances (), where we fixed , corresponding to newsvendor ratios . ERM- (CV) and ERM- (CV) generally perform worse than BFS-CV, since the deviation values are often positive. For all considered methods, we observe that the test cost deviations range from to and the variance increases with increasing . We observed similar results for cases with .

5.2 Nonlinear demand model

Demand may not be linearly related to the features. Therefore, we investigate how each method performs under nonlinear demand models, considering homoscedastic and heteroscedastic settings. In the following, we only present results regarding accuracy performance. Results on test cost performance did not provide new insights, since we observed similar patterns as in the case of linear instances (see C). Unless otherwise stated, we use the same reference configuration as in the previous section.

Instance size. Due to the nonlinear structure of the demand models, Figure 9 shows considerably lower accuracy values compared to instances with linear demand. For heteroscedastic instances, BFS-CV outperforms existing methods, with accuracy values above already for samples. For the homoscedastic case, all methods present inferior accuracy compared to the heteroscedastic case. In this setting, BFS-CV and ERM- present comparable performance, superior to the other considered methods.

Number of features. Figure 10 shows the average feature recovery accuracy for varying , for both homoscedastic and heteroscedastic demand. Similarly as for instances with linear demand, the number of features does not strongly influence the accuracy performance for nonlinear instances.

Noise level. For the heteroscedastic case, BFS-CV outperforms existing methods (Figure 11). In this setting, varying the standard deviation does not strongly affect the accuracy performance. For homoscedastic instances, all methods present inferior accuracy compared to heteroscedastic instances. Here, ERM- is superior to other methods for most values of , but BFS-CV often presents comparable accuracy.

Shortage and holding costs. In Figure 12, for heteroscedastic instances, BFS-CV has superior accuracy than other methods when . We observe that all methods perform poorly when the newsvendor ratio is below 0.3. In particular, the considered methods often do not recover any features when , leading to accuracy values between 0.5 and 0.65. For the homoscedastic case, the accuracy of all methods decreases with increasing newsvendor ratios, with values often below 0.8. In this setting, BFS-CV is superior to most methods, but is outperformed by ERM- when and by ERM- (CV) when .

One comment on these results is in order. Applying a linear decision function to nonlinear data may naturally lead to poor results, due to the inconsistent dependency structure with respect to the features. In some cases, we observed that all methods fail to achieve reasonable accuracy in feature recovery. However, for the vast majority of settings that we considered, BFS-CV presented good performance, outperforming the other methods. One possibility for dealing with such nonlinear instances would be to include additional features by considering nonlinear transformations of the original features, which we leave for future research.

6 Conclusion

We have presented a novel formulation based on bilevel optimization for incorporating feature selection in the feature-based newsvendor problem. The proposed BFS models provide an intuitive approach specifically designed for the task of feature selection, in which the upper-level problem directly selects the subset of relevant features. Our experimental results on synthetic data show that the proposed methods can accurately recover ground-truth informative features, leading to more explainable inventory decisions in comparison to previous methods.

There are many possibilities for follow-up works. First, research on tailored solution methods for BFS and BFS-CV, e.g., based on decomposition strategies for mixed integer programming, may allow to improve the scalability of the proposed methods when dealing with a large number of features. Next, other classes of data-driven optimization problems may benefit from an extension of the proposed methodology. As an example, the newsvendor problem also captures the fundamental trade-offs emerging in decisions related to capacity planning. Accordingly, an extension of the proposed BFS models may be applied to select features in stochastic, data-driven variations of such problems. Finally, from a broader perspective, incorporating concepts from machine learning into data-driven optimization problems may lead to crucial advances for both fields. As exemplified in this work, feature selection is one among possibly many machine learning tasks that can be integrated into the decision-making process, especially given the growing need for more explainable decisions.

Acknowledgments

This research has been funded by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) - Projektnummer 277991500. This support is gratefully acknowledged.

References

- Agor & Özaltın (2019) Agor, J., & Özaltın, O. Y. (2019). Feature selection for classification models via bilevel optimization. Computers & Operations Research 106:156–168.

- Arlot & Celisse (2010) Arlot, S., & Celisse, A. (2010). A survey of cross-validation procedures for model selection. Statistics Surveys 4:40–79.

- Ban (2020) Ban, G.-Y. (2020). Confidence intervals for data-driven inventory policies with demand censoring. Operations Research 68(2):309–326.

- Ban & Rudin (2019) Ban, G.-Y., & Rudin, C. (2019). The big data newsvendor: Practical insights from machine learning. Operations Research 67(1):90–108.

- Ben-Tal et al. (2013) Ben-Tal, A., Den Hertog, D., De Waegenaere, A., Melenberg, B., & Rennen, G. (2013). Robust solutions of optimization problems affected by uncertain probabilities. Management Science 59(2):341–357.

- Bennett et al. (2006) Bennett, K. P., Hu, J., Ji, X., Kunapuli, G., & Pang, J.-S. (2006). Model selection via bilevel optimization. In Proceedings of the IEEE International Joint Conference on Neural Networks (IJCNN). (pp. 1922–1929).

- Bennett et al. (2008) Bennett, K. P., Kunapuli, G., Hu, J., & Pang, J.-S. (2008). Bilevel optimization and machine learning. In J. M. Zurada, G. G. Yen, & J. Wang (Eds.), Computational Intelligence: Research Frontiers: IEEE World Congress on Computational Intelligence (WCCI), Hong Kong, China. Springer, Berlin, Heidelberg (pp. 25–47).

- Bergstra & Bengio (2012) Bergstra, J., & Bengio, Y. (2012). Random search for hyper-parameter optimization. Journal of Machine Learning Research 13(10):281–305.

- Bergstra et al. (2013) Bergstra, J., Yamins, D., & Cox, D. (2013). Making a science of model search: Hyperparameter optimization in hundreds of dimensions for vision architectures. In S. Dasgupta, & D. McAllester (Eds.), Proceedings of the 30th International Conference on Machine Learning. Atlanta, Georgia, USA: PMLR, volume 28 of Proceedings of Machine Learning Research (pp. 115–123).

- Bertsimas et al. (2018) Bertsimas, D., Gupta, V., & Kallus, N. (2018). Robust sample average approximation. Mathematical Programming 171(1):217–282.

- Bertsimas & Kallus (2020) Bertsimas, D., & Kallus, N. (2020). From predictive to prescriptive analytics. Management Science 66(3):1025–1044.

- Bertsimas & Thiele (2005) Bertsimas, D., & Thiele, A. (2005). A data-driven approach to newsvendor problems. Technical Report, Massachusetts Institute of Technology Cambridge, MA.

- Bertsimas & Thiele (2006) Bertsimas, D., & Thiele, A. (2006). A robust optimization approach to inventory theory. Operations Research 54(1):150–168.

- Besbes & Mouchtaki (2021) Besbes, O., & Mouchtaki, O. (2021). How big should your data really be? Data-driven newsvendor: Learning one sample at a time. Available at SSRN 3878155.

- Besbes & Muharremoglu (2013) Besbes, O., & Muharremoglu, A. (2013). On implications of demand censoring in the newsvendor problem. Management Science 59(6):1407–1424.

- Beutel & Minner (2012) Beutel, A.-L., & Minner, S. (2012). Safety stock planning under causal demand forecasting. International Journal of Production Economics 140(2):637–645.

- Cao & Chen (2006) Cao, D., & Chen, M. (2006). Capacitated plant selection in a decentralized manufacturing environment: A bilevel optimization approach. European Journal of Operational Research 169(1):97–110.

- Chen et al. (2007) Chen, X., Sim, M., Simchi-Levi, D., & Sun, P. (2007). Risk aversion in inventory management. Operations Research 55(5):828–842.

- Cheung & Simchi-Levi (2019) Cheung, W. C., & Simchi-Levi, D. (2019). Sampling-based approximation schemes for capacitated stochastic inventory control models. Mathematics of Operations Research 44(2):668–692.

- Choi (2012) Choi, T.-M. (2012). Handbook of newsvendor problems: Models, extensions and applications, volume 176. Springer, New York.

- Elmachtoub & Grigas (2021) Elmachtoub, A. N., & Grigas, P. (2021). Smart “predict, then optimize”. Management Science 68(1):9–26.

- Fletcher & Leyffer (2002) Fletcher, R., & Leyffer, S. (2002). Nonlinear programming without a penalty function. Mathematical Programming 91(2):239–269.

- Fontaine & Minner (2014) Fontaine, P., & Minner, S. (2014). Benders decomposition for discrete–continuous linear bilevel problems with application to traffic network design. Transportation Research Part B: Methodological 70:163–172.

- Franceschi et al. (2018) Franceschi, L., Frasconi, P., Salzo, S., Grazzi, R., & Pontil, M. (2018). Bilevel programming for hyperparameter optimization and meta-learning. In J. Dy, & A. Krause (Eds.), Proceedings of the 35th International Conference on Machine Learning. Stockholm, Sweden: PMLR, volume 80 of Proceedings of Machine Learning Research (pp. 1568–1577).

- Gallego & Moon (1993) Gallego, G., & Moon, I. (1993). The distribution free newsboy problem: Review and extensions. Journal of the Operational Research Society 44(8):825–834.

- Gallego et al. (2001) Gallego, G., Ryan, J. K., & Simchi-Levi, D. (2001). Minimax analysis for finite-horizon inventory models. IIE Transactions 33(10):861–874.

- Hanasusanto et al. (2015) Hanasusanto, G. A., Kuhn, D., Wallace, S. W., & Zymler, S. (2015). Distributionally robust multi-item newsvendor problems with multimodal demand distributions. Mathematical Programming 152(1):1–32.

- Hastie et al. (2009) Hastie, T., Tibshirani, R., Friedman, J. H., & Friedman, J. H. (2009). The elements of statistical learning: Data mining, inference, and prediction, volume 2. Springer, New York.

- Huber et al. (2019) Huber, J., Müller, S., Fleischmann, M., & Stuckenschmidt, H. (2019). A data-driven newsvendor problem: From data to decision. European Journal of Operational Research 278(3):904–915.

- Khouja (1999) Khouja, M. (1999). The single-period (news-vendor) problem: Literature review and suggestions for future research. Omega 27(5):537–553.

- Kleywegt et al. (2002) Kleywegt, A. J., Shapiro, A., & Homem-de Mello, T. (2002). The sample average approximation method for stochastic discrete optimization. SIAM Journal on Optimization 12(2):479–502.

- Kogan & Lou (2003) Kogan, K., & Lou, S. (2003). Multi-stage newsboy problem: A dynamic model. European Journal of Operational Research 149(2):448–458.

- Kuhn & Johnson (2019) Kuhn, M., & Johnson, K. (2019). Feature engineering and selection: A practical approach for predictive models. Chapman and Hall/CRC.

- Lau & Lau (1996) Lau, H.-S., & Lau, A. H.-L. (1996). The newsstand problem: A capacitated multiple-product single-period inventory problem. European Journal of Operational Research 94(1):29–42.

- Levi et al. (2015) Levi, R., Perakis, G., & Uichanco, J. (2015). The data-driven newsvendor problem: New bounds and insights. Operations Research 63(6):1294–1306.

- Levi et al. (2007) Levi, R., Roundy, R. O., & Shmoys, D. B. (2007). Provably near-optimal sampling-based policies for stochastic inventory control models. Mathematics of Operations Research 32(4):821–839.

- Mackay et al. (2019) Mackay, M., Vicol, P., Lorraine, J., Duvenaud, D., & Grosse, R. (2019). Self-tuning networks: Bilevel optimization of hyperparameters using structured best-response functions. In International Conference on Learning Representations (ICLR). New Orleans, Louisiana, USA.

- Mandi et al. (2020) Mandi, J., Demirović, E., Stuckey, P. J., & Guns, T. (2020). Smart predict-and-optimize for hard combinatorial optimization problems. Proceedings of the AAAI Conference on Artificial Intelligence 34(2):1603–1610.

- Molina et al. (2002) Molina, L., Belanche, L., & Nebot, A. (2002). Feature selection algorithms: A survey and experimental evaluation. In Proceedings of the IEEE International Conference on Data Mining (ICDM). Maebashi City, Japan (pp. 306–313).

- Moon & Gallego (1994) Moon, I., & Gallego, G. (1994). Distribution free procedures for some inventory models. Journal of the Operational Research Society 45(6):651–658.

- Oroojlooyjadid et al. (2020) Oroojlooyjadid, A., Snyder, L. V., & Takáč, M. (2020). Applying deep learning to the newsvendor problem. IISE Transactions 52(4):444–463.

- Perakis & Roels (2008) Perakis, G., & Roels, G. (2008). Regret in the newsvendor model with partial information. Operations Research 56(1):188–203.

- Petruzzi & Dada (1999) Petruzzi, N. C., & Dada, M. (1999). Pricing and the newsvendor problem: A review with extensions. Operations Research 47(2):183–194.

- Qin et al. (2011) Qin, Y., Wang, R., Vakharia, A. J., Chen, Y., & Seref, M. M. (2011). The newsvendor problem: Review and directions for future research. European Journal of Operational Research 213(2):361–374.

- Sachs & Minner (2014) Sachs, A.-L., & Minner, S. (2014). The data-driven newsvendor with censored demand observations. International Journal of Production Economics 149:28–36.

- Scarf (1958) Scarf, H. (1958). A min-max solution of an inventory problem. In K. Arrow, S. Karlin, & H. Scarf (Eds.), Studies in the Mathematical Theory of Inventory and Production. Stanford University Press, Stanford (pp. 201–209).

- See & Sim (2010) See, C.-T., & Sim, M. (2010). Robust approximation to multiperiod inventory management. Operations Research 58(3):583–594.

- Shapiro (2003) Shapiro, A. (2003). Monte carlo sampling methods. In A. Ruszczynski, & A. Shapiro (Eds.), Stochastic Programming, volume 10 of Handbooks in Operations Research and Management Science. Elsevier, Amsterdam (pp. 353–425).

- Wang & Webster (2009) Wang, C. X., & Webster, S. (2009). The loss-averse newsvendor problem. Omega 37(1):93–105.

- Wang et al. (2016) Wang, Z., Glynn, P. W., & Ye, Y. (2016). Likelihood robust optimization for data-driven problems. Computational Management Science 13(2):241–261.

- Yue et al. (2006) Yue, J., Chen, B., & Wang, M.-C. (2006). Expected value of distribution information for the newsvendor problem. Operations Research 54(6):1128–1136.

- Zhang & Gao (2017) Zhang, Y., & Gao, J. (2017). Assessing the performance of deep learning algorithms for newsvendor problem. In D. Liu, S. Xie, Y. Li, D. Zhao, & E.-S. M. El-Alfy (Eds.), Neural Information Processing. Springer, Cham (pp. 912–921).

- Zhu et al. (2012) Zhu, L., Huang, M., & Li, R. (2012). Semiparametric quantile regression with high-dimensional covariates. Statistica Sinica 22(4):1379–1401.

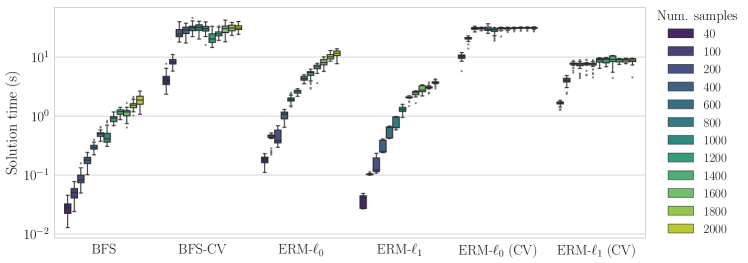

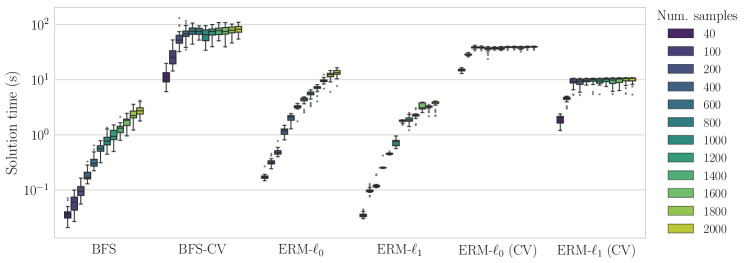

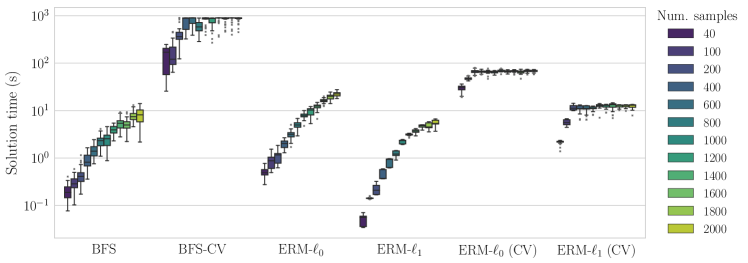

Appendix A Computation times

In this section, we report the computation times of the different methods considered in the experiments. Figures 13, 14, 15, and 16 show how the solution times scale with the number of samples , respectively for features. Here, we consider instances with linear demand model and we fix shortage cost to , the holding cost to , and the noise level to .

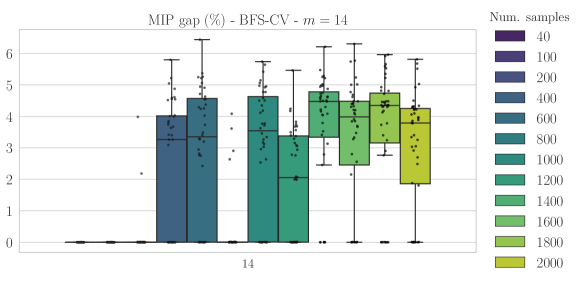

Considering instances with a larger number of features (), BFS-CV cannot solve all instances to optimality within the specified time limit. Accordingly, Figure 17 illustrates the distribution of the optimality gaps (in percentage values) for instances with features. In this case, optimality gaps are often below .

Appendix B Complementary results

In the following, we report the p-values of the non-parametric one-sided Wilcoxon signed-rank test, with null hypothesis that the median difference in accuracy between the BFS-CV and other methods is negative. Tables 2 and 3 report p-values for instances with linear and nonlinear demand, respectively.

| Figure | BFS | ERM- | ERM- (CV) | ERM- | ERM- (CV) |

|---|---|---|---|---|---|

| Figure 1 | 2.31E-35 | 8.73E-12 | 6.88E-23 | 2.25E-38 | 1.23E-32 |

| Figure 3 | 2.53E-14 | 7.76E-04 | 4.14E-10 | 2.32E-14 | 1.95E-13 |

| Figure 5 | 3.45E-07 | 8.89E-02 | 1.08E-11 | 1.06E-15 | 4.47E-13 |

| Figure 7 | 2.00E-32 | 6.56E-08 | 3.96E-23 | 1.77E-37 | 5.02E-27 |

| Figure | Noise | BFS | ERM- | ERM- (CV) | ERM- | ERM- (CV) |

|---|---|---|---|---|---|---|

| Figure 9 | Homoscedastic | 8.20E-33 | 3.15E-01 | 1.77E-53 | 4.49E-55 | 2.81E-19 |

| Heteroscedastic | 8.92E-56 | 1.92E-12 | 1.02E-29 | 7.49E-65 | 9.00E-49 | |

| Figure 10 | Homoscedastic | 4.45E-08 | 7.87E-01 | 2.66E-13 | 2.01E-12 | 2.37E-05 |

| Heteroscedastic | 6.90E-13 | 3.32E-02 | 8.34E-08 | 9.35E-15 | 2.25E-11 | |

| Figure 11 | Homoscedastic | 2.47E-02 | 9.86E-01 | 5.60E-11 | 7.19E-10 | 6.27E-07 |

| Heteroscedastic | 3.05E-16 | 1.72E-03 | 9.18E-15 | 5.51E-20 | 6.52E-08 | |

| Figure 12 | Homoscedastic | 2.58E-13 | 3.98E-01 | 6.28E-25 | 2.51E-22 | 2.21E-09 |

| Heteroscedastic | 4.86E-13 | 6.03E-02 | 4.44E-17 | 1.72E-26 | 1.59E-16 |

Appendix C Test cost results for nonlinear instances

We present results regarding test cost performance for instances with nonlinear demand model. This section follows the same structure as Section 5.2 of the main paper.

C.1 Instance size

Regarding the impact of instance size , Figures 18 and 19 show test cost results for instances with heteroscedastic and homoscedastic demand, respectively.

|

|

|

|

|

|

C.2 Number of features

Figures 20 and 21 show the impact of the number of features on test cost results for large instances () with heteroscedastic and homoscedastic demand, respectively.

C.3 Noise level

Figures 22 and 23 show the impact of noise level on test cost results for large instances () with heteroscedastic and homoscedastic demand, respectively.

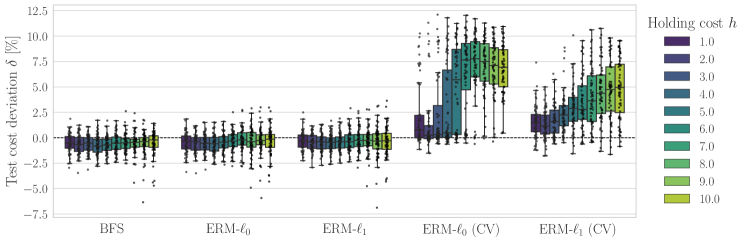

C.4 Shortage cost

Figures 24 and 25 show the impact of shortage cost on test cost results for large instances () with heteroscedastic and homoscedastic demand, respectively.

C.5 Holding cost

Figures 26 and 27 show the impact of holding cost on test cost results for large instances () with heteroscedastic and homoscedastic demand, respectively.