\ul

Deep Learning Based Residuals in Nonlinear Factor Models: Precision Matrix Estimation of Returns with Low Signal-To-Noise Ratio

Abstract

This paper introduces a consistent estimator and rate of convergence for the precision matrix of asset returns in large portfolios using a non-linear factor model within the deep learning framework. Our estimator remains valid even in low signal-to-noise ratio environments typical for financial markets and is compatible with weak factors.

Our theoretical analysis establishes uniform bounds on expected estimation risk based on deep neural networks for an expanding number of assets. Additionally, we provide a new consistent data-dependent estimator of error covariance in deep neural networks.

Our models demonstrate superior accuracy in extensive simulations and the empirics.

Keywords: Deep neural networks, feedforward multilayer neural network, nonparametric regression, covariance matrix estimation, factor models

1 Introduction

The Great Financial Crisis 2008/09 and the COVID-19 Crisis 2020/21 revealed major problems and disadvantages of existing econometric models for economic forecasting and policy analysis. Especially during periods with high uncertainties these models commonly cause large prediction errors and lead to misleading policy recommendations. Recent research developments indicate that machine learning methods suit better in these circumstances: they can measure non-linear structures and sudden changes in the relations between economic variables. Deep neural networks, i.e., artificial neural networks with many hidden layers, as part of the most important machine learning techniques nowadays, received increasing attention in economics over the recent years. Their usefulness has been shown on several complex machine learning problems that concern e.g., natural language processing and image recognition. A detailed overview of applications of deep neural networks on observed data can be found e.g., in Schmidhuber (2015) and the literature cited therein. In an comprehensive empirical paper, Gu et al. (2020) compare the out-of-sample performance of various machine learning techniques in predicting the portfolio returns for the US market and show that most often neural network methods provide the best results. More recently, Gu et al. (2021) develop a non-linear conditional asset pricing model based on an extended autoencoder incorporating latent factors that depending on asset characteristics and illustrate its superiority in terms of the lowest pricing errors compared to standard methods commonly used in the finance literature.

In this paper, we provide a consistent estimator of the precision matrix of asset returns in large portfolios based on deep learning residuals formed from non-linear factor models, so that we can get better out-of-sample results for metrics like Sharpe-Ratio, variance of the portfolio. In light of the advantages of deep neural networks in terms of prediction accuracy compared to traditional econometric models testified in various empirical studies and research fields, there is an increasing interest in analyzing their large sample properties. Important theoretical contributions that deal with the approximation properties of deep neural networks in the nonparametric regression framework are provided e.g., by Schmidt-Hieber (2020a), Farrell et al. (2021) and Kohler and Langer (2021). For a general class of smooth non-linear functions Farrell et al. (2021) make a major contribution and provide upper risk bounds for deep learning estimators. Within a subcase for the class of composition based functions, which include (generalized) additive models, Schmidt-Hieber (2020a) shows that sparse deep neural networks do not suffer from the curse of dimensionality in contrast to traditional nonparametric estimation methods and achieve minimax rate of convergence in expected risk under the squared loss. Recently, Jiao et al. (2023) provide risk bounds on deep learning linear function estimators. Notably, their derived constant on the risk bounds is smaller compared to existing literature, enabling the establishment of bounds for approximately sparse factor structures. Their analysis relies on a rather abstract treatment of sparsity-approximate factors and finds more practical utility in domains like image processing and video analysis, where low-dimensional latent structures are prevalent.

One of the main disadvantages of machine learning techniques is that the typical application assumes a high signal-to-noise ratio. However, in asset pricing this is not the case. Table 3.1 of Nagel (2021) clearly illustrates that typical datasets on asset returns exhibit a low or very low signal-to-noise ratio. In our paper, we introduce a model in the framework of deep neural networks, which is also appropriate in a setting with very low signal-to-noise ratio and can be used to obtain a consistent estimator of the precision matrix of the returns, even with a growing number of assets in the portfolio. In order to establish this estimator, we investigate the theoretical properties of feedforward multilayer neural networks (multilayer perceptron) with rectifier linear unit (ReLu) activation function. Our modeling framework builds upon the research contributions of Farrell et al. (2021) and Schmidt-Hieber (2020a) offers convenient theoretical generalizations and extensions.

Specifically, we contribute to the deep learning literature with uniform results on the expected estimation risk. In our first contribution, we analyze the properties of the deep neural network estimator in case of incorporating a potential set of response variables compared to the current deep learning research that refers to univariate responses. Our results provide bounds on the expected risk and show that these upper bounds are uniform over the variables. Hence, our model framework offers considerable extensions in terms of functional composition of the true underlying model and estimation. In fact, we allow for different unknown functional forms in the nonparametric regression model across each variable . The advantage of concentrating on the theoretical framework of Farrell et al. (2021) lies in its straightforward applicability to factor models. In fact, we further contribute by building a bridge between our deep learning setting and non-linear factor models. One of the key issues in financial markets are the non-linearities due to interaction terms involving the covariates or factors explaining asset returns, as discussed in Section 3.6 of Nagel (2021). Our deep neural network factor model (DNN-FM) estimator and its theory can handle this type of non-linearities, which is also confirmed by the superior performance in extensive simulations and the empirical application.

Moreover, we extend our deep learning results to an additive model setting, similar to the framework in Schmidt-Hieber (2020a) and analyze the implications of imposing sparsity in the neural networks. It is important to note that our sparse deep neural network only incorporates a sparse structure in the parameters in the hidden layers. Hence, the input variables (factors) do not exhibit any sparsity. We provide the theory for our sparse deep neural network factor model (SDNN-FM) estimator, which shows that the SDNN-FM approach can avoid the curse of dimensionality arising from an increasing number of included factors and testify its strong performance compared to alternative machine learning techniques in simulations and our out-of-sample portfolio forecasting exercise. A non-linear additive structure for explaining asset returns is also used in Freyberger et al. (2020). The authors propose an adaptive group lasso structure and show in an empirical study based on data of the US stock market that the return to risk ratio of a portfolio constructed by a non-linear factor model can be considerably higher compared to the one resulting from a linear factor model.

In order to obtain an estimate of the data covariance matrix based on the deep neural network factor model (DNN-FM) and its sparse version (SDNN-FM), we require an efficient estimate for the residual covariance matrix. For this purpose, as our second contribution, we develop a novel data-dependent covariance matrix estimator of the innovations in deep neural networks. The estimator refers to a flexible adaptive thresholding technique, which is robust to outliers in the errors. We elaborate on the consistency of the estimator in -norm under rather mild assumptions. Furthermore, since the precision matrix of the returns of a high-dimensional portfolio is paramount for understanding various financial metrics, such as the Sharpe ratio, we provide consistency and rate of convergence results for the precision matrix estimated based on our DNN-FM and SDNN-FM. As our third contribution, we show that we obtain these consistency and rate of convergence results under a very low signal-to-noise ratio assumption. Specifically, we allow that the minimum eigenvalue of the covariance matrix of the non-linear factors is zero or local to zero and show its connection to a very low signal-to-noise ratio in the data. Furthermore, instead of using the Sherman-Morrison-Woodbury formula, which is commonly applied in the literature to obtain the precision matrix of the returns, we provide a new formula that uses matrix theory and is in line with a setting where the minimum eigenvalue of the covariance matrix of the factors is zero or local to zero. Moreover, we illustrate the direct connection between the low signal-to-noise ratio assumption and the weak factor setting. Hence, our deep neural network framework is suitable for measuring weakly influential factors.

Linear factor models are helpful in understanding the behavior of asset returns. Fan et al. (2011) and Fan et al. (2013) use linear observed and unobserved factors in a large portfolio of assets, respectively. They show that linear factor models can be combined with a sparse error covariance matrix to consistently estimate the precision matrix of asset returns even in high dimensions. These two papers are benchmarks and contributed to merging of factor model with high dimensional statistics literature in an important way. Fan et al. (2016) show that in case of ”almost” block diagonal covariance matrix of errors, there can be a sparse precision matrix of the errors, which is applicable in linear factor models. Recently, Callot et al. (2021) and Caner et al. (2023) estimate the precision matrix of returns via nodewise regression and with linear factor model based residual nodewise regression techniques, respectively. Caner (2023) proposed a new machine learning technique that may be suitable for buy and sell decisions for a single asset in a high dimensional generalized linear model with structured sparsity patterns.

Traditional factor models, as in Fama and French (1993) or Fan et al. (2011) assume rigid linear relations between the factors and the underlying observed variables. Especially during crisis periods, however, economic time series follow non-linear relations and are subject to sudden changes. Hence, the linearity assumption of standard factor models would be inappropriate to measure time series with these patterns. The structure of our deep neural network factor model (DNN-FM) and its sparse version (SDNN-FM) mitigate this limitation and allow for measuring non-linear and complex dynamic relations between the factors and economic variables. Our theoretical elaboration provides convergence results for the covariance and precision matrix estimators based on the deep neural network. In that general framework the rate of convergence of our estimators are not affected by number of assets in a portfolio unless that number is exponentially growing. Moreover, the convergence results depend on both the number of factors and the smoothness of the functions. In the subcase of non-linear additive functions we show that the convergence rate is not affected by the number of included factors.

The favorable large sample properties of the DNN-FM and SDNN-FM are confirmed by our Monte Carlo study based on various simulation designs. Specifically, both approaches consistently determine the true underlying function connecting the factors and observable variables, as the number of periods increases. Further, the estimators for the covariance and precision matrix of the returns are as well consistent. Compared to competing approaches, as e.g., the traditional static factor model, which are sensitive to an increase of the number of factors (i.e., their error rate deteriorate as increases), the convergence rates of the DNN-FM and SDNN-FM estimators are stable with respect to a raising number of factors.

In an out-of-sample portfolio forecasting application based on assets constituents of the S&P 500 stock index and concentrating on a global minimum variance portfolio setting, we show that the DNN-FM and SDNN-FM are superior in most cases compared to competing portfolio estimators that are commonly used in the literature. More precisely, they often lead to the lowest out-of-sample portfolio standard deviation (SD) and avoid large changes in the portfolio constellation. Consequently, both models provide low portfolio turnover rates and prevent high transaction costs. This generally leads to the highest out-of-sample Sharpe rations across different asset spaces compared to the competing methods when transaction costs are taken into account. The superiority in forecasting precision is particularly pronounced during turbulent times, such as during the Great Financial Crisis of 2008/09 and the COVID-19 Crisis. Hence, the flexibility of the deep learning estimators allows for capturing strong changes and high uncertainties in financial time series during volatile periods.

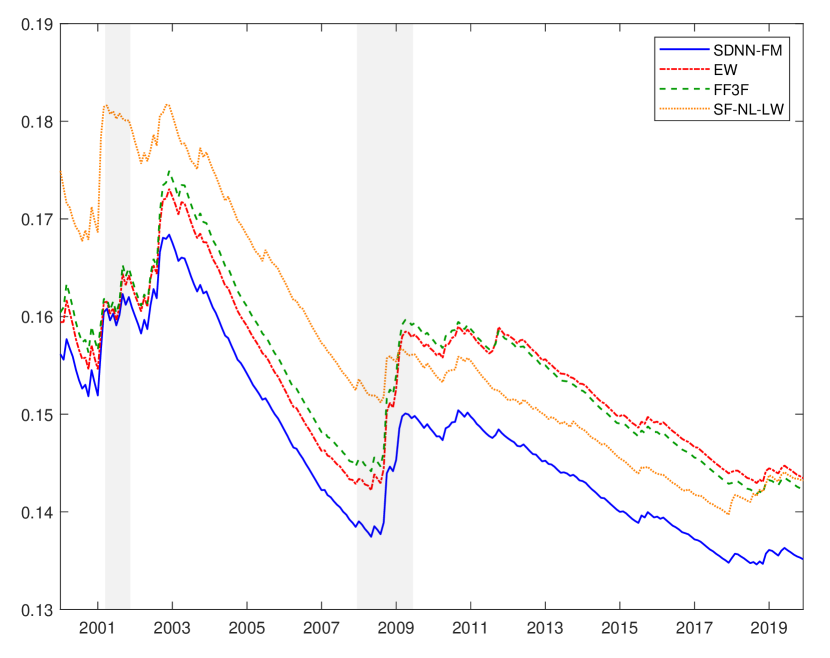

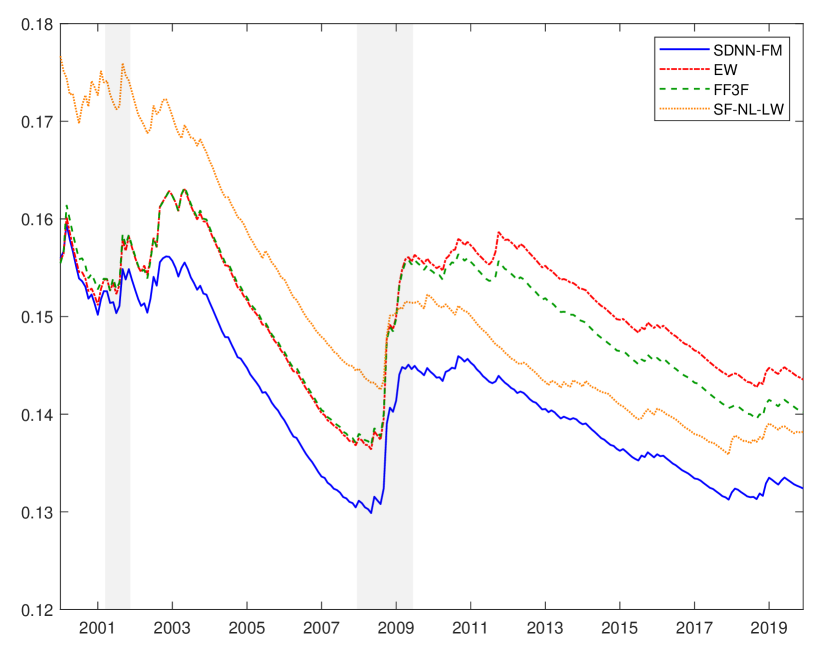

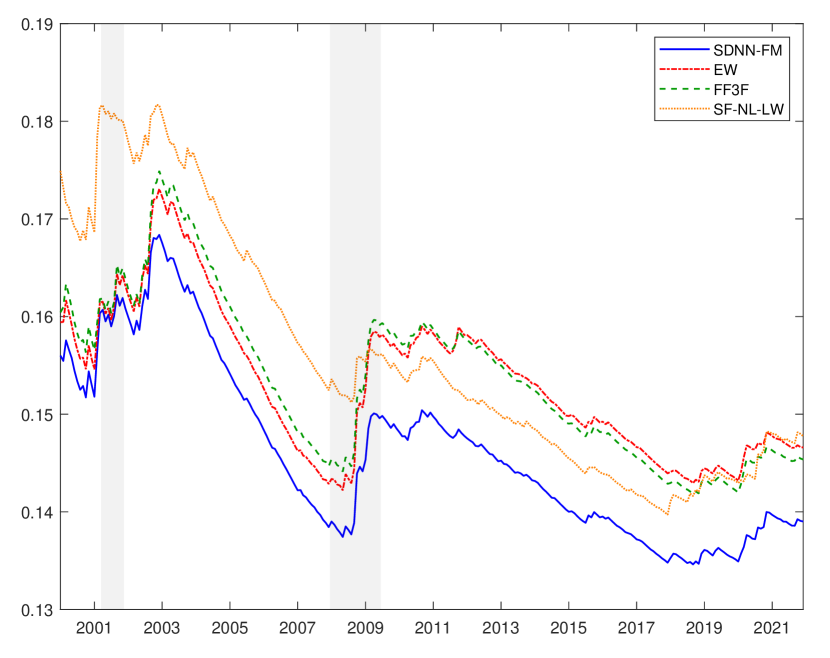

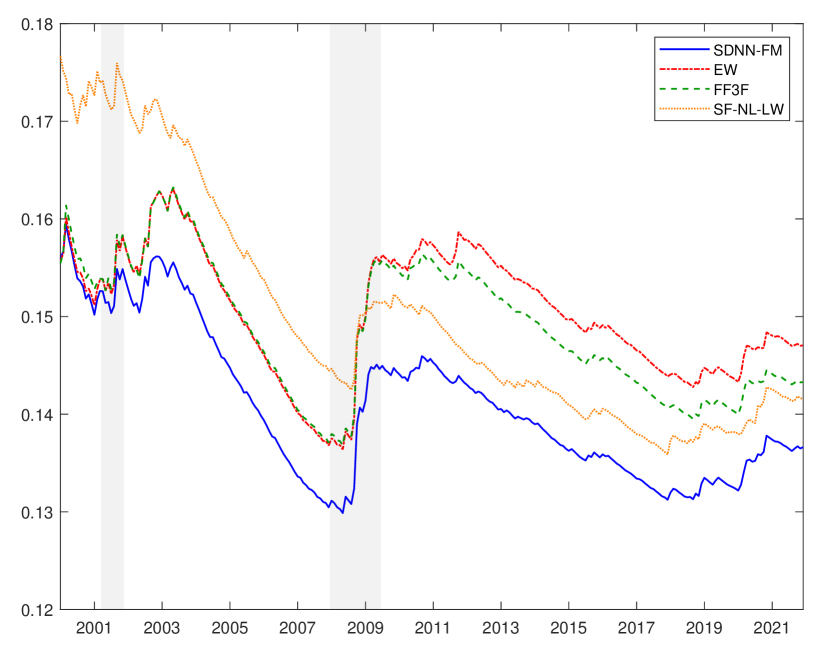

As an example, we illustrate the results of a comparison among our SDNN-FM, the equally weighted portfolio (EW), the Fama-French three factor (FF3F) model, and the single factor non-linear shrinkage method of Ledoit and Wolf (2017) (SF-NL-LW) in Figure 1. The y-axis shows the out-of-sample standard deviation (SD) of a large portfolio, and the x-axis denotes the out-of-sample periods that we analyze. We consider two sample periods, where the first sample excludes the COVID-19 Crisis and the second one includes the COVID-19 Crisis. represents the number of assets in the portfolio, and the NBER recession years for the dot-com Crisis 2001 and the Great Financial Crisis of 2008/09 are highlighted as vertical gray bars. The results are depicted in Figure 1, where panels LABEL:sub@fig_sd_sub_a and LABEL:sub@fig_sd_sub_b refer to the first sample without COVID-19 Crisis and panels LABEL:sub@fig_sd_sub_c and LABEL:sub@fig_sd_sub_d correspond to the second sample including the COVID-19 Crisis. The outcome at a specific period incorporates the out-of-sample returns until (e.g., the SD in December 2011 incorporates the out-of-sample returns from January 1996 until December 2011). The graphs illustrate that the advantage of the SDNN-FM in lowest out-of-sample portfolio standard deviation compared to the competing approaches are especially pronounced during and after the Great Financial Crisis 2008/09 and the COVID-19 Crisis 2020/21. These results confirm that our deep learning method is well suited for capturing high volatilities during turbulent episodes. Extensive results and more comparisons are given in Section 9.

Recent related papers merging the deep learning literature with asset pricing applications offer substantial advances in the empirical literature. Feng et al. (2022) analyze latent factors based on a structural model that benefits from deep learning estimation. Their well-designed model establishes connections between factor loadings, factors, and the deep learning literature. The analysis encompasses the asset returns and pricing errors. Notably, they adopt a sparse approach for selecting weights in deep neural networks, akin to our SDNN-FM model. Their asset return model is linear in factors and is empirically estimated, incorporating deep learning generated factors. Remarkably, their empirical findings demonstrate that factors generated based on deep learning techniques lead to enhanced Sharpe Ratios in portfolios. Chen et al. (2023) utilize the no-arbitrage condition to estimate stochastic discount factor (SDF) weights and the optimal instrument function. They employ recurrent neural networks, including Long-Short-Term-Memory estimates, to obtain hidden macro variable estimates. Subsequently, feed-forward neural networks are employed to estimate SDF and the optimal function of hidden macro variables and firm characteristics. Their study employs a generative adversarial network structure, analyzing the problem from both structural and empirical perspectives. In contrast, our research focuses on the econometric theory, specifically exploring the integration of non-linear factors with deep neural networks. Moreover, one objective is to consistently estimate the precision matrix of asset returns and analyze the rate of convergence.

The remainder of the paper is organized as follows. In Section 2, we introduce the deep neural network framework used for estimating nonparametric regressions and provide our main theoretical findings. In Section 3, we introduce a novel estimator for the covariance and precision matrix for the idiosyncratic errors of the deep neural network factor model by means of a robust adaptive threshold estimator and prove its consistency. Moreover, we elaborate on the consistency of the corresponding covariance matrix estimator of the returns in Section 4. Section 5 introduces the precision matrix estimator of the returns based on the DNN-FM and shows the consistency of the estimator. Section 6 provides the non-linear additive function case in a sparse deep neural network. Details on the implementation are discussed in Section 7. In Section 8, we present Monte-Carlo evidence on the finite sample properties of our DNN-FM and SDNN-FM approaches in estimating the unknown function, which connects the factors with the observable variables, as well as the corresponding covariance and precision matrix. In Section 9 we analyze the empirical performance of our methods in an out-of-sample portfolio forecasting exercise. Section 10 summarizes the main findings. The proofs are provided in the Appendix.

2 Deep Learning

In this section, we combine the work of Farrell et al. (2021) with non-linear factor models. We extend their results to multivariate output variables. Assume the following nonparametric regression model for

| (1) |

where denotes the -th response variable for the -th observation. The regressors are iid across , and incorporate observed variables of dimension , where each . 111Currently, we are working on a paper, which extends the modeling framework by relaxing the iid assumption on the regressors and allowing for a time series structure. Also is not growing with , it is a positive integer-constant and . Let be a zero mean noise component, which is iid across , for all . Define the -dimensional covariance matrix of the errors as , where is a vector of dimension . is an unknown function, and for each , it may be of a different functional form, but . Moreover, we assume that is independent of for a given . can be a nondecreasing function of .To save from notation, we do not subscript with . Also, the number of factors is constant, and does not vary with .

2.1 Multilayer Neural Networks

In order to estimate the unknown function , we rely on multilayer (deep) feedforward neural networks.222The ”Deepness” in the neural network will arise from multiple hidden layers to estimate , for . ”Learning” comes from estimating and correcting errors in the network parameters via an algorithm (stochastic gradient descent), which will be relegated to the literature, and will not be discussed here. For further information see e.g., Goodfellow et al. (2016). We are concerned about the statistical properties of deep learning, specifically multilayer feedforward neural networks. In the following, we briefly describe the model architecture. As it is common in nonparametric problems, we start with the regressors, and aim to determine the response . In order to achieve that we have to estimate the unknown function in (1) connecting with . In the deep learning framework, the estimation of is carried out within hidden layers, which are incorporated between the input layer containing the regressors and the output layer that includes the response. Let , and represents the number of hidden layers. A given hidden layer is composed of hidden units , which are defined for each layer , and each function , with and . These units are transformed by an activation function: at each layer. We impose a rectifier linear unit (ReLu) activation function for

which censors all negative real numbers to zero, and keeps all positive. The choice for this activation function is motivated by several factors. First, the partial derivative of the ReLu function is either zero or one, which facilitates computations. Moreover, the ReLu activation function can pass a signal without any change through all layers, i.e. it has the projection property. For each , we assume the same number of layers .

We formally define the network architecture by the parameters , where the number of hidden layers represents the depth of the network, and corresponds to the number of units at each layer , which constitutes the width of the network. Note that we allow for a different width vector for the estimator of each function . Specifically, , which is a vector, where is the number of inputs and defines the number of units in the output layer. The remaining quantities , represent the number of units in hidden layers , respectively. In this paper, we impose one output variable, hence , and the number of inputs is for each .

In the following, we provide a simple example of a multilayer feedforward neural network illustrated by the directed acyclic graph in Figure 2. The neural network incorporates two regressors and one response . Moreover, it contains two hidden layers () with three units at each hidden layer, i.e., .

The first connection arises from the regressors, which are collected in the input layer to the first hidden layer. Each regressor is connected forward with each unit in the first hidden layer. Moreover, at each hidden unit the regressors are multiplied with weights and an intercept is added. Hence, for the first unit in the first hidden layer three parameters need to be estimated. The remaining units follow an identical structure. In all this, the ReLU activation function is used to estimate the parameters at each unit. In our example, nine parameters have to be estimated in total, and three ReLU units are in the first hidden layer.

In a second step, each unit in the first hidden layer is connected with each unit in the second hidden layer. More specifically, the outputs from the first hidden layer are used as inputs to each unit at the second hidden layer. Each of those inputs is multiplied with the corresponding weights, an intercept is added and the the ReLU activation function is applied. For our example, we need to estimate 12 parameters, formed by three weights and an intercept at each unit in second hidden layer.

Finally, in the output layer, we use the least squares loss and regress on all three responses from the second hidden layer and an intercept. This adds four additional parameters that have to be estimated. Hence, in total we need to estimate 25 parameters, if the regressor vector is -dimensional and if we incorporate two hidden layers with three units each. For a general multilayer deep neural network architecture, let denote the total number of parameters to be estimated for each . A straightforward calculation shows that .

2.2 Estimator

Let represent the multilayer perceptron architecture. To save from notation let . We define the estimator as the empirical minimizer, representing the feedforward deep neural network estimator described above with unbounded weights and without any sparsity constraint on the weights, as follows

| (2) |

where is a positive constant for each . This type of estimator is a subcase of estimators with general loss functions, see Farrell et al. (2021). In the following, we formalize an assumption about the data.

Assumption 1.

Assume that for each , , are iid across . is continuously distributed. We set , for , , where is a positive constant for each .

This assumption is a minor extension of Assumption 1 in Farrell et al. (2021) to a case with many functions (outcomes), and hence we allow for bounded outcomes but with differing bounds for each . In Section 6, we relax this restriction. The restriction on bounded outcomes is necessary to have Lipschitz continuity of the least squares loss and to be able to apply Lemma 2 and Lemma 5 of Farrell et al. (2021) in the proofs. For the second assumption, we need the following definition. The formal definition of the Sobolev ball

where

and is the weak derivative, and is the essential supremum, and .

Assumption 2.

For each , let , where each function has the same smoothness parameter .

Assumptions 1 and 2 are standard and used in Farrell et al. (2021). The width of all layers will grow at the same rate for a given . Hence, the number of parameters to be estimated in the deep neural network only changes up to constants when we estimate functions. Theorem 1 provides risk bounds for a specification with multiple outcome variables in the deep learning literature.

Theorem 1.

Under Assumptions 1 and 2, where the number of hidden units at each layer grow at the same rate , for , and the depth of the neural network is , we obtain

-

(i)

For large enough

with and , where is a positive constant.

-

(ii)

With , (i) holds with probability approaching one.

Remarks on Theorem 1.

- 1.

-

2.

Define the quantity

(3) In the following, we analyze the rates in Theorem 1 (i). We start with considering a exponentially growing number of outcomes, i.e., and set . If , then we have . If we still consider , however , we get . Hence, we obtain two different cases when the number of outcomes is growing exponentially in . The first case leads to the rate , when the number of regressors is small. The second case yields with a larger (but constant) number of factors the rate . When , , then . We obtain the same rate , if . Moreover, when is a fixed number and not growing with , the rate is .

In order to simplify the interpretation in the subsequent technical elaboration and to conform with our empirical application in Section 9 considering a out-of-sample portfolio forecasting experiment, we denote the response variables as asset returns and the regressors as observed factors, for and , where represents the number of assets and denotes the number of periods. However, it is important to note that the results are still valid for general types of responses and regressors.

3 Covariance and Precision Matrix Estimate for Errors

In this section, we analyze the large sample properties of the error covariance and precision matrix estimates based on the deep neural network. We start with denoting as the -th element of the error covariance matrix , with .

Subsequently, we provide two maximal inequalities: the first one for the estimation of the error covariance matrix with infeasible sample average via Bernstein’s inequality, and the second one provides a centered absolute version of the first maximal inequality.

Lemma 1.

We use the following assumption linking the number of assets to the sample size .

Assumption 3.

as .

Note that the results in Lemma 2 are used to obtain the consistency of the covariance and precision matrix estimators of the returns. We have the following assumption that sets a lower bound on a demeaned second moment of the errors.

Assumption 4.

In the following, we specify the covariance matrix of the errors and its thresholding counterpart. Set . The sample estimator is given by

where is the vector of residuals based on the deep neural network estimator. Also define the -th element of as , for and . We provide a new robust-adaptive thresholding estimator for the error covariance matrix estimation in deep learning, which is robust to outliers in the data, i.e., it is robust to large residuals. To that end, we define, for and

| (4) |

Our adaptive thresholding estimator is represented as the matrix , where the -th element of is computed as

The rate is determined by the expression

| (5) |

where is a positive constant. Note that the above thresholding estimator is different from the one used in Fan et al. (2011), where they use a norm based definition for , unlike our norm based definition. The thresholding estimator in Fan et al. (2011) is not suitable for merging theory of deep learning with non-linear factor based residuals for precision matrix estimation. By using a new based robust data dependent threshold in (4) we solve this problem, as can be seen in our proofs.

Moreover, we define a sparsity pattern in the covariance matrix of the errors as

where represents the maximum number of nonzero elements across the rows of the error covariance matrix.

The following theorem establishes the consistency of the adaptive thresholding estimator for the covariance matrix of errors, by using the residuals resulting from the deep learning estimator in (2).

Theorem 2.

Remarks. 1. Note that the rate of is given by . Under Assumption 3, two possibilities arise that determine the dominant rate between and . The first possibility is the case of an very high number of assets, where , with . In this scenario, we have . For all other possibilities of under Assumption 3, the rate is given by . It is worth noting that this rate is not affected by the number of assets , but rather affected by the number of factors , which is constant.

2. Negligible tail probabilities are written explicitly in our proofs, and they depend on number of assets, sample size and the number of factors.

4 Covariance Matrix Estimator for the Returns

In this section, we show that the covariance matrix of the asset returns can be estimated consistently based on the deep neural network estimator in (2). We start with specifying the true covariance matrix of the returns and the corresponding estimator. In that respect, we consider the following nonparametric model for each period

where is a -dimensional vector of asset returns,

denotes the unknown function relating the observed factors of dimension with the asset returns and the idiosyncratic innovations are given by the -dimensional vector . Define the covariance matrix of the returns as

Subsequently, we define each component of and start with the covariance matrix for the functions of the factors given by

which is a matrix. The -th element of is

Moreover, we define the corresponding estimator for as follows

with , which is a vector, and

The following lemma proves the consistency of the estimate for the covariance matrix function of factors in a non-linear nonparametric model based on the deep neural network estimator (2). As far as we know, this is a new result in the deep learning literature. It is important to note that we allow for the large dimensional setting .

The estimator for the covariance matrix of the returns based on the deep neural network in (2) is given by

where we estimate the covariance matrix of the innovations using our adaptive thresholding estimator introduced in Section 3. We establish the following theorem for the consistency of the covariance matrix of returns based on the deep neural network. To the best of our knowledge this is a novel result in the deep learning literature.

Remarks on Theorem 3.

-

1.

The sparsity of the error covariance matrix does not play any role in the estimation error, i.e., the estimation error is not affected by .

-

2.

The rate of convergence corresponds to

Hence, the rate is affected by the number of factors, , jointly with smoothness coefficient , or by the number of assets . In the case of a very large number of assets, e.g., , with , the rate of convergence is given by . For all remaining specifications of that satisfy Assumption 3, we obtain a rate .

5 Precision Matrix Estimator for the Returns

In this section, we provide an explicit expression for the precision matrix for the returns. We start with introducing a formula for the inverse of the sum of two square matrices and both of dimension , where is a nonsingular matrix, and can be any square matrix

| (6) |

which is from p. 348-349, Fact 3.20.8 of Bernstein (2018). Set and . Since , where is a nonsingular matrix, we obtain the following expression for the precision matrix

| (7) |

It is important to note that even with being singular, the inverse, exists. In the same way, since is nonsingular, with probability approaching one as shown in Lemma A.4(ii), the estimate for the precision matrix of the returns based on the deep neural network in (2) is

| (8) |

In the following, we provide two assumptions that will be essential for proving the consistency of the precision matrix estimator based on the deep neural network.

Assumption 5.

-

(i)

with is a positive constant, and with and with .

-

(ii)

with a positive constant, and , with , or .

-

(iii)

is symmetric.

The following assumption replaces Assumption 3 and introduces a sparsity assumption.

Assumption 6.

, and .

Assumption 5(i) is standard in large asymptotic framework, and commonly used in the literature, for the covariance matrices and , which are both of dimension . Hence, the maximum eigenvalue of the covariance matrix of the errors is growing with at the rate but slower than itself. In that sense we control the rate of the noise. Moreover, in Assumption 5(ii) the maximum eigenvalue of the covariance matrix of the factors is upper bounded by a multiple of . This is also an extension of the linear-additive factor models in Fan et al. (2011) to flexible non-linear factor models considered here. The minimum eigenvalue of the covariance matrix of the factors is either zero, or local to zero, reflecting the large dimensional problems resulting in singularity-near-singularity. Assumption 5(iii) is technical in nature and helps us to derive a lower bound on minimum eigenvalue of a certain matrix in Lemma A.3(i). For example if and are commuting, this assumption is satisfied, see p.604, Fact 7.6.16(i) of Bernstein (2018). Assumption 6 restricts unlike all the previous results. The main reason for this restriction is: to get a positive lower bound on the minimum eigenvalue of covariance matrix of the functions of factors. There is a tradeoff between number of factors , and the number of assets as seen in Assumption 6.

5.1 Signal-to-Noise Ratio and Weak Factor Issues

In the following, we show a key aspect of our Assumptions 5(i) and (ii). Specifically, we will demonstrate that our assumptions allow for low signal-to-noise ratio, which is one of the main characteristics of the stock market. In order to analyze the implications, we consider a vector, , with , which simplifies the theoretical elaboration below. We propose the following measure to quantify the signal-to-noise ratio in the deep neural network for a large portfolio of assets

| (9) |

Note that in (9) we can have the lower bound

| (10) |

where we use the Rayleigh inequality-quotient on p.343 of Abadir and Magnus (2005) for both the numerator and denominator. Moreover, we use Assumptions 5(i) and (ii) for the last inequality. Based on Assumption 5(ii), we know that the ratio is either zero or converging to zero. Hence, this result clearly shows that we allow for a low signal-to-noise ratio (as well as none). The lowest signal-to-noise ratio according to our definition in (9) is 0, which corresponds to the case, where there is only pure noise. If is zero or converging to zero (low signal-to-noise setup), the signal-to-noise ratio can be either 0 or converging to 0 from above. It is important to note that in a setting with low signal-to-noise ratio, which is implied by Assumptions 5(i) and (ii), the widely used Sherman-Morrison-Woodbury formula cannot be used, as it requires computing the inverse of , which is singular-near singular in this setting. Hence, by introducing the new formula for the precision matrix of the returns in (7), we provide an expression that is compatible with a setting of low signal (i.e., the minimum eigenvalue of the covariance matrix of non-linear factors is zero or local to zero).

Now we provide an upper bound for signal-to-noise ratio and tie this upper bound to our discussion of weak factors below. In (9), an upper bound on signal-to-noise ratio is

| (11) |

Note that the signal-to-noise ratio can be between the lower and upper bounds, and we show below that the upper bound can be smaller and even collapse to zero under a modification of Assumption 5. However, note that our standard set of assumptions in Assumption 5 allow for a signal-to-noise ratio of zero or converging to zero by the minimum eigenvalue condition.

In the following, we analyze two cases that conform with the weak factor framework.

Case 1. Based on Assumptions 5(i) and (ii), our deep learning framework allows for measuring weak factors. Compared to the pervasiveness assumption conventionally imposed in the standard linear factor models (see e.g., Bai and Ng (2002) and Fan et al. (2011)), which implies that the largest eigenvalues in diverge with the fast rate , the weak factor assumption incorporates factors that considerably less influential.444See, e.g. Chudik et al. (2011), Onatski (2012), Uematsu and Yamagata (2022), Bai and Ng (2023), and the references therein, who analyze the implications of weak factors in the linear factor model framework. Specifically, in the weak factor setting, the largest eigenvalues of diverge with a rate, which is substantially slower than . We analyze this case in the proofs after the proof of Theorem 4. To get some intuition, let us replace Assumption 5(ii) by the following weak factor assumption

Assumption W.5(ii).

| (12) |

with a positive constant, and , but , and , with , or .

Hence, this new assumption offers an alternative to Assumption 5(ii) and assumes a divergent largest eigenvalue for the non-linear factor covariance matrix, however it grows at a slower rate than the number of assets . Hence, Assumption W.5(ii) is more amenable for the weak factor scenario. Moreover, we obtain the following lower and upper bounds on signal-to-noise ratio

| (13) |

Hence, by taking , the lower bound will collapse to zero, and upper bound still diverges, however at a slower rate compared to the setting with Assumption 5(ii), as shown by equation (11). We cover a large number of possibilities regarding the signal-to-noise and factor models with (13).

Case 2. In the second case, we consider a setting with very weak factors, which implies that the largest eigenvalue of the covariance matrix of the non-linear factors converges to zero. Hence, similar as the lower bound, the upper bound on the signal-to-noise ratio collapses to zero as well. In order to see this, we change Assumption 5(ii) to the following specification, which incorporates a environment with very weak factors (this replaces Assumption W.5(ii))

Assumption VW.5(ii).

| (14) |

with a positive constant, and , and , with , or .

In this setting, the largest eigenvalue of the covariance matrix of the non-linear factor model can converge to zero, which implies that all factors can be very weak. This gives rise to a collapsing signal-to-noise ratio to zero. In (13), with , , the signal-to-noise ratio collapses to zero. For the case that the rate of the largest eigenvalue is , we obtain the same results for precision matrix estimation of the returns as in the case of very weak factors. Hence, we only briefly cover that scenario after the proof of Theorem 4 in the Appendix A.

The proof of consistency and rate of convergence of the estimate of the precision matrix of returns this very-weak factor case will be presented after the proof of Theorem 4. Hence, the weak factor setting conforms with the case of a low or very low signal-to-noise ratio as elaborated in the previous paragraph. Moreover, empirical evidence testifies that the weak factor assumption better explains the spectral properties of financial and macroeconomic datasets (see, e.g., Trzcinka (1986) and Ludvigson and Ng (2009)). Hence, our model setting is better suited to measure the spectral structure of datasets incorporating assets returns compared to standard linear factor models that rely on the pervasiveness assumption.

5.2 Main Theorem

The following theorem shows the consistency of the precision matrix of the returns under our standard set of assumptions. We proceed with a new proof due to the non-linear nature of the factors.

Remarks on Theorem 4.

-

1.

Our rate both depends on both the number of assets and the number of factors , where the rate deteriorates with larger portfolios and an increasing number of factors. We can only allow for as shown by Assumption 6. This is due to non-linear nature of the factor model and Assumption 5. Note that our rate does not depend on which control the minimum signal to noise ratio as in (10).

-

2.

It is also difficult to compare our rate with any known linear model in terms of rates of convergence, without putting any structure on the non-linearity. We cover a general non-linear unknown function with observed factors, and estimate it with deep neural networks.

-

3.

Since , based on Assumption 6 we have that . Hence, simplifies to

-

4.

We analyze the implications of a weak factor or a very weak factor assumption on the results for Theorem 4 in a separate paragraph after the proof of Theorem 4 in Appendix A. Specifically, we establish the Corollaries A.1 and A.2, which show that the rate of convergence of the precision matrix estimator improves compared to the rate derived in Theorem 4 and depends linearly in . This is due to the fact that the precision matrix estimator is no longer affected by the fast diverging eigenvalues of the covariance matrix of the non-linear factors, which increase with the rate implied by the standard strong factor assumption. However, for the consistency of the estimator we still require .

6 Additive Non-linear Factor Models

In this part of the paper, we make some simplifying assumptions and show that the curse of dimensionality due to the number of factors may disappear in an additive but still non-linear-unknown function model.

6.1 The Additive Model

In the finance literature, asset returns are governed by common factors. The following model is used in Fan et al. (2011):

| (15) |

for all , where represents the number of assets in the portfolio, and denotes the time span of the portfolio. The number of factors is , and , and the number of factors do not vary with , and is constant. The factors are observed. represents the -th factor at time period , and depicts the factor loading corresponding to the -th asset and -th factor. The model described above defines a linear relation between the factors and returns through the factor loadings. However, a more flexible relationship between asset returns and factors can be put forward. Instead of the linear model specification in (15), we assume that the returns evolve through the following model

| (16) |

with

| (17) |

where represents the true but unknown function relating the factors to the returns for each asset. corresponds to the unknown function of factor for the -th factor at time period . The model specification (16) enhances the flexibility in the relationship between the factors and assets to a large extent, compared to the rigid all linear additive formulae (15). We want to estimate with sparse deep learning, for each . The additive-flexible model (16) is related to Section 4 and equation (12) of Schmidt-Hieber (2020a). We can specify the true function as the composite of two functions as follows

| (18) |

where

which is a vector. Then

For each and

where represents ball of Hölder functions with radius , see p.1880, 1885 of Schmidt-Hieber (2020a). These Hölder functions are functions with partial derivative up to order exist and are bounded, and the partial derivative of order are Hölder, and represents the largest integer strictly smaller than . Since , and Hölder ball definition-domain is slightly different there is a different notation in Assumption 2. The technical definition of Hölder functions is relegated to Appendix B.1. Furthermore we impose that true composite function belongs to the following function space

| (19) |

where we define the function space in Appendix B.1. This function space, , consists of composite of Hölder functions.

6.2 S-sparse Deep Neural Networks

Our empirical minimizer satisfies the following sparsity and bounded parameter requirements in the deep neural network. Schmidt-Hieber (2020a) introduces them in equation (4) of his paper and requires two important restrictions. Schmidt-Hieber (2020a) argues that non-sparse deep neural networks can result in overfitting hence large out-of-sampling errors. We analyze this last statement both theoretically, but also with simulation, and most importantly in out-of-sample asset pricing example from the US Stock Market. There are two key aspects of deep-sparse neural networks. First, the parameters will be bounded by one, and second the network will be sparse. Note that also by imposing a sparse deep neural network estimator with bounded weights we try to understand how sparsity especially play a role in the theory in deep networks. Sparsity in our proof is used to control the covering numbers for the function space as shown in Step 1b of the proof of Theorem 5. In Remark 8 of Theorem 5 we show relaxing of these restrictions does not change risk upper bound up to a slowly varying function in .

The first restriction can be formally depicted as follows: For each

| (20) |

This restriction is necessary to ensure the practical applicability of the neural networks. Statistical results using large parameters/weights are usually not observed, see Goodfellow et al. (2016). To be specific, Schmidt-Hieber (2020a) argues that computational algorithms use random, nearly orthogonal matrices as initial weights. Hence, the initial weights are bounded by one, and the model training leads to trained weights, which are close to the initial values. Therefore, it seems reasonable to set a bound of one for the weights.

In the next step, we introduce our sparsity assumption, which is crucial to prevent overfit caused by a probable large number of hidden units in each layer. For each function , we impose the same number of hidden units where , where we have inputs for each function and the output is scalar. Let be the number of nonzero entries of , respectively. The s-sparse deep neural networks are given in Schmidt-Hieber (2020a), subject to (20) and

| (21) |

where the output dimension is one and the functions are uniformly bounded by , which is a positive constant. Clearly, the sparsity is different for each . In order to simplify the notation, we represent as . The sparsity structure imposed on the neural networks weights are additionally valuable for the consistency of the of deep learning estimators compared to model specifications that only rely on the implicit regularization introduced by the stochastic gradient decent algorithm during the computational stage. This point is conjectured explicitly, and an example is provided on p. 1916 of Schmidt-Hieber (2020b).

6.3 Theory

We start with Assumptions that are necessary for the sparse deep neural network. In contrast to the large sample elaboration on the dense deep neural network in Section 2, we will not assume bounded outcomes in the sparse DNN framework. However, we strengthen other assumptions such as sparsity of the neural network parameters. The Sparse Deep Neural Network (SDNN-FM) factor model estimator is defined as

Let be the rate of the approximation error for the true function by the sparse deep neural network estimator for each , described in Appendix B.1 and (B.3).

Assumption 7.

Assume that are iid zero mean with unit variance across with subgaussian distribution and Orlicz norm, , which is a positive constant. Let the minimum eigenvalue of the covariance matrix of errors be , where is a positive constant. are iid across and independent from for each .

Assumption 7 is subgaussian noise extension of the gaussian noise assumption imposed in Schmidt-Hieber (2020a).

Assumption 8.

Assumption 9.

- (i)

-

(ii)

The optimal number of hidden layers is growing with sample size:

-

(iii)

The number of hidden units-minimum across all hidden layers- should exceed the following lower bound ,

-

(iv)

The sparsity of the network parameters can grow with n, for each for each .

Assumptions 8 and 9 are used to approximate the true function, by the sparse deep learning estimator . Assumption 8 specifies the true composite function. Assumption 9(i)-(ii) put an upper bound on the functions, and specifies the number of layers . The number of layers is an increasing function of . The number of units at each layer is specified in Assumption 9(iii) and provides a lower bound of this quantity. Hence, the number of units increase with , and form a wide layer. The sparsity restriction is specified in Assumption 9(iv). Given the specification of the rate , the sparsity assumption shows that , with . Assumptions 8-9 are directly taken from Schmidt-Hieber (2020a), and see p.1885 of Schmidt-Hieber (2020a) for non-linear-additive functions. In the following, we provide the upper bound on the risk for our functions that are estimated by deep learning.

Remarks.

-

1.

By , in which case the right side in (i) can be written as

-

2.

The results in Theorem 5 indicate that we require a large number of layers, and the number of units at each hidden layer cannot be small, in order to obtain a good function approximation. These restrictions are specified in Assumption 9. However, for a better prediction we need fewer layers as observed by our result in Theorem 5. Hence, there is a tradeoff in the selection of the optimal number of layers. While the depth of the neural network is essential for achieving a better function approximation, the question arises: how deep should the network be? Theorem 5 in Schmidt-Hieber (2020a) emphasizes the importance of deep layers in obtaining an improved function approximation.

-

3.

The results of Theorem 5 further show that the upper bound is uniform over . This is due to Assumption 9(iv). Moreover, we also allow that the true functional forms are different. However, they have the same Hölder smoothness. Concerning the deep learning estimators, we have the same number of layers and units for each estimate but their sparsity patterns can vary.

-

4.

The sparsity in the neural network can be achieved by active regularization at each layer through an elastic net penalization, or an iterative pruning approach as suggested on p. 1882 of Schmidt-Hieber (2020a), and p. 1917 of Schmidt-Hieber (2020b), respectively. Lemma 5 of Schmidt-Hieber (2020a) combined with our Lemma B.3 and Step 1b in the proof of Theorem 5(i) shows that the sparsity in the network parameters at each layer is essential for a better prediction. The implicit regularization induced by the stochastic gradient descent algorithm will not be sufficient, and the consistency of the deep neural network estimator may be not achieved as shown in pp. 1916-1917 of Schmidt-Hieber (2020b). We also analyze these issues of sparse versus non-sparse networks in an empirical out-of-sample portfolio exercise for the US Stock Market. Moreover, we consider different simulation studies, which aim at comparing the two approaches in an in-sample estimation analysis.

-

5.

An important aspect concerns the consistency of the deep neural network estimator, which is not affected by number of factors, . This is due to additive structure of the model, the novel proofs in Schmidt-Hieber (2020a) and our proof for the subgaussian noise in Theorem 5. The quantities and correspond to the rates of convergence associated with the risk of the deep learning estimator and the fact of using assets in the portfolio, respectively.

-

6.

Theorem 5(ii) is a novel result in the literature and shows the implications of the size of the portfolio and the number of factors on the convergence rate of the deep learning estimate for the true underlying function that relates the factors to the returns. Our result extends the contributions of Schmidt-Hieber (2020a) to the estimation of multiple functions. Hence, we obtain the additional rate due to estimation of different functions.

-

7.

In the subsequent analysis, we examine which rate may be the slowest among and . Suppose that and . We obtain as the slower rate as long as , which is true if . Hence, regardless of , when , we obtain the rate with . If we consider , with and , a similar reasoning applies, leading to the rate . The same logic applies to the case of , with . However, it is important to note that if , it is not clear which rate will be slowest. The rate depends on the tradeoff between the smoothness coefficient , and the number of assets .

-

8.

A non-sparse approach, allowing for unbounded weights in deep neural network estimation, has been explored in Kohler and Langer (2021) using Theorem 1a. Their approach yields similar rates of convergence to those presented in Schmidt-Hieber (2020a) for the additive non-linear case, up to a slowly varying function in . However, it remains unclear how this approach can be extended to handle multiple outcomes, as established in our paper. In contrast, our paper provides a general framework through Theorem 1, which does not rely on a sparsity assumption, boundedness of the weights, or the assumption of a composite true function. Notably, Kohler and Langer (2021) still rely on the assumption of a composite true function.

Subsequently, we set up rates that will be used in the following theorem. Let

| (22) |

and

where the last equality is due to .

Moreover, let us denote the estimate of the precision matrix of errors by using the sparse deep neural network estimator in a non-linear additive model by . The main difference from , which corresponds to the error precision matrix of the dense deep neural network in (2), concerns the implied residuals that are obtained from the sparse deep neural network estimator. Moreover, the covariance matrix estimator is subject to the same thresholding formula, however in the threshold is replaced with the quantity . Denote and as the covariance and precision matrix of the returns in a non-linear additive model estimated by the sparse deep neural network. The following theorem establishes the consistency of the estimate of precision matrix of the errors and returns for a non-linear additive model setting estimated by the sparse deep neural network.

Theorem 6.

Remarks on Theorem 6.

- 1.

-

2.

Theorem 6(iii) is a new result that provides a consistent deep learning based non-linear factor model estimate of the precision matrix of the returns. It is important to note that the estimation error does not depend on the number of factors. However, it is affected by the sparsity () in the covariance matrix of errors, the number of assets , and the estimation error rate , which is used for the estimator of the error covariance matrix. Hence, we can only allow for , however we still have when .

-

3.

Issues that are related to signal-to-noise ratio and weak factors are the same as in Section 5.

7 Implementation

In the following, we discuss the implementation details of our deep neural network factor model with fully connected units (DNN-FM) in Section 2 and our sparse deep neural network factor model (SDNN-FM) with sparsely connected units introduced in Section 6, which are crucial for the performance of the models.

In order to train and validate our models on different sets of data, we split our in-sample data into two distinct subsets, which correspond to the training and validation dataset, respectively. This data division is essential to reduce the overfitting. More precisely, only the data in the training set is used to estimate the DNN-FM and SDNN-FM for a specific set of hyperparameters. The validation set serves as proxy for an out-of-sample test of the model and is used to optimize the hyperparameters. In our implementation, we use the first 80% of the in-sample data for training the model, whereas the remaining 20% are used for the model validation.

In order to explicitly incorporate sparsity in the weights of our SDNN-FM we use three regularization methods. These methods reduce the effective number of parameters to be estimated in the neural network. Specifically, we augment the objective function by a -norm penalty on the weights of the neural network, which sets elements of the weight matrices to zero. Hence, the -norm penalty induces sparsity in the parameters of the neural network and allows for disregarding uninformative weights. The strength of the penalty is controlled by a tuning parameter, which we select based on the validation set. Furthermore, we use Dropout, introduced by Srivastava et al. (2014) as a second technique to reduce overfitting in the neural network. The Dropout technique randomly disables a prespecified number of units and their corresponding connections in each layer of the neural network during the training process. This reduces the occurrence of complex co-adaptations between the units on the training data. These co-adaptations generally lead to a close adjustment of the neural network to the training data, which compromises its ability to generalize to new data that has not been seen during training. Hence, Dropout mitigates this problem and improves the out-of-sample performance. In our implementation, we randomly disable 20% of the units in each layer during the training process. As a third regularization technique, we adopt Early Stopping. During each step of an iterative optimization algorithm (e.g., stochastic gradient decent (SGD)) the neural network parameters are adjusted such that the fitting error based on the training data is minimized. While the training error decreases in each iteration, this is not true for the validation error, which is used as a proxy for the out-of-sample error. Early Stopping keeps track of the validation error and terminates the optimization as soon as the validation error starts to increase. For both SDNN-FM and DNN-FM we use the Early Stopping rule. Hence, the difference between these two methods arise from incorporating -norm regularization and Dropout in the SDNN-FM. Clearly, we need Early Stopping for both non-sparse and sparse deep neural network estimation, to avoid an increase of the out-of-sample validation error.

In order to optimize the DNN-FM and SDNN-FM, we refer to the adaptive moment estimation algorithm (Adam) introduced by Kingma and Ba (2014), which offers an efficient adaptation of the stochastic gradient decent (SGD) algorithm. More precisely, compared to SGD it provides an adaptive learning rate by using the information of the first and second moments of the gradient.

We estimate the covariance matrix of the residuals of the DNN-FM based on our novel thresholding procedure introduced in Section 3. Specifically, we use as threshold level, where is specified in (4) and is set to . To estimate the covariance matrix of the innovations for the SDNN-FM, we also rely on our thresholding procedure, however use the SDNN-FM residuals as elaborated in Section 6 to build and is set to the same level as so that DNN-FM and SDNN-FM differences can be only due to sparse number of parameters estimated in hidden layers, and possible data generating processes.

8 Simulation Evidence

The aim of this section is threefold. First, we verify our theorems. Second, we compare-contrast our DNN-FM, SDNN-FM methods with the ones that are widely used in the literature tied to machine learning. Third, we analyze the performance of our methods under low signal-to-noise ratio and weak factor setup.

8.1 Monte Carlo designs and Models

To evaluate our theoretical findings, we analyze three Monte Carlo designs. For the first design, we consider the following data generating process (DGP)

| (23) |

where defines an indicator function that is equal to one if the boolean argument in braces is true. Moreover, the coefficients and the explanatory variables are drawn from the standard normal distribution, for , and .555We run the same study with fixed coefficients and obtain similar results as in the random coefficients design. Therefore, we omitted these simulation results, however they can be obtained from the authors upon request. This DGP is more aligned with SDNN-FM since it comprises a non-linear additive structure. The innovations are generated according to the following process, which is similar to the DGP used in Bai and Liao (2016).

| (24) | ||||

where are iid , for , and are independently drawn from , for . Hence, the process (24) implies some cross-sectional correlations between the innovations and yields a banded covariance matrix .

Compared to the standard static factor model specification, the process in (23) additionally incorporates non-linearities through the term . Hence, we expect that the traditional static factor model estimated with principal component analysis may have greater difficulties in capturing these non-linearities compared to our deep neural network factor models.

In order to verify the robustness of our simulation results, we consider two additional Monte Carlo designs. The second Monte Carlo design relies on a similar DGP as in Farrell et al. (2021). Specifically, we simulate the data according to the following process

| (25) |

where incorporates independent standard normally distributed random variables and the idiosyncratic innovations follow the process in (24). Moreover, denotes a non-linear multivariate transformation function, which incorporates second-degree polynomials and pairwise interactions and more in line with DNN-FM and what we observe in financial data. Hence, this simulation design enhances the non-linear influence of on the response compared to the first design in (23). The coefficient vectors and are both of dimension and drawn from and , respectively, and they represent the columns in matrices which are of dimension .

| Signal | Noise | Signal-to-Noise Ratio | Eigmin | Eigmax | Eigmin | Eigmax \bigstrut | |

| \bigstrut | |||||||

| 1 | 2.08 | 1.73 | 1.21 | -2.16E-14 | 99.72 | 0.03 | 5.82 \bigstrut[t] |

| 3 | 5.36 | 1.75 | 3.06 | -2.81E-14 | 119.91 | 0.03 | 5.78 |

| 5 | 8.37 | 1.74 | 4.81 | -3.26E-14 | 133.74 | 0.03 | 5.81 |

| 7 | 10.67 | 1.73 | 6.17 | -3.59E-14 | 144.75 | 0.03 | 5.78 \bigstrut[b] |

| \bigstrut | |||||||

| 1 | 1.90 | 1.74 | 1.09 | -3.59E-14 | 199.68 | 0.02 | 6.35 \bigstrut[t] |

| 3 | 4.84 | 1.72 | 2.80 | -4.39E-14 | 227.13 | 0.01 | 6.22 |

| 5 | 8.08 | 1.73 | 4.67 | -5.08E-14 | 245.50 | 0.02 | 6.31 |

| 7 | 10.97 | 1.74 | 6.31 | -5.64E-14 | 260.92 | 0.02 | 6.26 \bigstrut[b] |

| \bigstrut | |||||||

| 1 | 1.84 | 1.75 | 1.05 | -5.66E-14 | 399.81 | 0.01 | 6.67 \bigstrut[t] |

| 3 | 4.85 | 1.73 | 2.80 | -6.81E-14 | 438.71 | 0.01 | 6.72 |

| 5 | 8.24 | 1.75 | 4.72 | -7.71E-14 | 462.72 | 0.01 | 6.75 |

| 7 | 11.35 | 1.73 | 6.55 | -8.57E-14 | 484.49 | 0.01 | 6.74 \bigstrut[b] |

-

•

Note: The first column (signal) corresponds to the informational content explained by the covariance matrix of the factors measured by , where each element in the vector is and the second column (noise) measured by is the variation explained by the innovations. Eigmin , Eigmax are the smallest and largest eigenvalues of and Eigmin , Eigmax are the smallest and largest eigenvalues of , respectively. All the quantities correspond to averages across the 500 simulation repetitions.

Based on the third simulation design, we analyze the finite sample properties of our deep learning approaches for the case that the DGP incorporates weak factors. More precisely, we generate the data according to process (25), however introduce sparsity in the -dimensional coefficient matrices and . Given that for any matrix , denotes the -norm of , counting the non-zero elements in , we set the cardinalities of each row of are as follows:666All the cardinalities are rounded to the smaller integer. , for , , for , , for and , for , where we randomly select the positions of the non-zero elements in and . Moreover, similar as for the second design, we draw the non-zero coefficients in and from and , respectively. The time dimension is set to 60, 120 and 240 for all simulations. Moreover, we consider several dimensions for and . Specifically, and . The number of replications is 500.

In the following, we analyze the signal-to-noise ratio characteristics and spectral properties of the true covariance matrix of the functions of the factors and the covariance matrix of the innovations for each of the three simulation designs. Table 1 shows that the first DGP incorporates settings with a low signal-to-noise ratio (for ) and high ratios for . In addition, it corresponds to a strong factor setting as the largest eigenvalue of increases with the rate . The characteristics for the second DGP are reported in Table 2. The results illustrate that the signal-to-noise ratio is substantially smaller compared to the first simulation design. Hence, the second DGP is well suited for analyzing environments with a very low signal-to-noise ratio (), low signal-to-noise ratio () and higher signal-to-noise ratios (). Moreover, the process also refers to a strong factor framework, since the largest eigenvalue of diverges with the rate . Finally, Table 3 reports the properties of the third DGP. Based on the evolution of the largest eigenvalue of , we can see that this process perfectly represents the weak factor framework. In fact, compared to strong factor setting, the largest eigenvalue diverges with a considerable slower rate than . Moreover, the signal-to-noise ratio is very low and stays on a stable level even for increasing number of factors .

Hence, our analysis shows that all three Monte Carlo designs are well suited for measuring the performance of our deep learning models and the competing approaches for settings with a very low signal-to-noise ratio. It is important to note that in all three setting, we have that is rank deficient, where the -th eigenvalues, for , are zero or close to zero. This is due to the fact that all DGPs follow a (non-linear) factor structure.

| Signal | Noise | Signal-to-Noise Ratio | Eigmin | Eigmax | Eigmin | Eigmax \bigstrut | |

| \bigstrut | |||||||

| 1 | 0.50 | 1.70 | 0.29 | -3.10E-15 | 17.03 | 0.03 | 5.80 \bigstrut[t] |

| 3 | 1.77 | 1.72 | 1.03 | -4.38E-15 | 22.34 | 0.03 | 5.85 |

| 5 | 3.33 | 1.73 | 1.93 | -4.70E-15 | 26.61 | 0.02 | 5.79 |

| 7 | 5.27 | 1.72 | 3.07 | -3.81E-15 | 31.04 | 0.03 | 5.82 \bigstrut[b] |

| \bigstrut | |||||||

| 1 | 0.50 | 1.76 | 0.29 | -4.72E-15 | 33.68 | 0.01 | 6.32 \bigstrut[t] |

| 3 | 1.74 | 1.72 | 1.01 | -6.87E-15 | 40.73 | 0.02 | 6.29 |

| 5 | 3.36 | 1.73 | 1.94 | -8.01E-15 | 46.20 | 0.01 | 6.28 |

| 7 | 5.23 | 1.73 | 3.03 | -8.64E-15 | 51.32 | 0.01 | 6.26 \bigstrut[b] |

| \bigstrut | |||||||

| 1 | 0.53 | 1.74 | 0.30 | -7.15E-15 | 66.77 | 0.01 | 6.80 \bigstrut[t] |

| 3 | 1.78 | 1.74 | 1.02 | -1.06E-14 | 76.71 | 0.01 | 6.72 |

| 5 | 3.40 | 1.74 | 1.96 | -1.29E-14 | 83.53 | 0.01 | 6.71 |

| 7 | 5.26 | 1.74 | 3.02 | -1.43E-14 | 90.03 | 0.01 | 6.76 \bigstrut[b] |

-

•

Note: The first column (signal) corresponds to the informational content explained by the covariance matrix of the factors measured by , where each element in the vector is and the second column (noise) measured by is the variation explained by the innovations. Eigmin , Eigmax are the smallest and largest eigenvalues of and Eigmin , Eigmax are the smallest and largest eigenvalues of , respectively. All the quantities correspond to averages across the 500 simulation repetitions.

| Signal | Noise | Signal-to-Noise Ratio | Eigmin | Eigmax | Eigmin | Eigmax \bigstrut | |

| \bigstrut | |||||||

| 1 | 0.07 | 1.72 | 0.04 | -5.84E-16 | 2.44 | 0.02 | 5.85 \bigstrut[t] |

| 3 | 0.13 | 1.73 | 0.08 | -6.44E-16 | 2.69 | 0.02 | 5.75 |

| 5 | 0.19 | 1.71 | 0.11 | -6.15E-16 | 2.76 | 0.03 | 5.77 |

| 7 | 0.22 | 1.73 | 0.13 | -5.57E-16 | 2.79 | 0.03 | 5.83 \bigstrut[b] |

| \bigstrut | |||||||

| 1 | 0.05 | 1.74 | 0.03 | -8.98E-16 | 3.41 | 0.02 | 6.27 \bigstrut[t] |

| 3 | 0.10 | 1.74 | 0.06 | -9.92E-16 | 3.62 | 0.02 | 6.28 |

| 5 | 0.12 | 1.75 | 0.07 | -9.47E-16 | 3.66 | 0.01 | 6.31 |

| 7 | 0.14 | 1.73 | 0.08 | -9.22E-16 | 3.72 | 0.02 | 6.25 \bigstrut[b] |

| \bigstrut | |||||||

| 1 | 0.04 | 1.75 | 0.02 | -1.23E-15 | 4.65 | 0.01 | 6.71 \bigstrut[t] |

| 3 | 0.07 | 1.73 | 0.04 | -1.30E-15 | 4.80 | 0.01 | 6.72 |

| 5 | 0.08 | 1.75 | 0.05 | -1.31E-15 | 4.92 | 0.01 | 6.72 |

| 7 | 0.09 | 1.75 | 0.05 | -1.27E-15 | 4.83 | 0.01 | 6.76 \bigstrut[b] |

-

•

Note: The first column (signal) corresponds to the informational content explained by the covariance matrix of the factors measured by , where each element in the vector is and the second column (noise) measured by is the variation explained by the innovations. Eigmin , Eigmax are the smallest and largest eigenvalues of and Eigmin , Eigmax are the smallest and largest eigenvalues of , respectively. All the quantities correspond to averages across the 500 simulation repetitions.

We compare the precision of our deep neural network factor models (DNN-FM and SDNN-FM) with methods that are commonly used in the literature. The following models are included in the simulation study:

-

•

SFM-POET: The static factor model with observed factors, where the covariance matrix of the idiosyncratic errors is estimated based on the principal orthogonal complement thresholding method (POET) from Fan et al. (2013).

-

•

DNN-FM: Our non-linear nonparametric factor model estimated based on deep neural network in Section 2.

-

•

SDNN-FM: Our non-linear nonparametric factor model estimated based on the s-sparse deep neural network in Section 6.

-

•

NL-LW: The non-linear shrinkage estimator of Ledoit and Wolf (2017).

-

•

SF-NL-LW: The single factor non-linear shrinkage estimator of Ledoit and Wolf (2017).

-

•

RN-FM: Residual nodewise regression estimation of factor models by Caner et al. (2023).

8.2 Simulation results

The simulation results for the first Monte Carlo design in (23) are illustrated in Tables 4 to 6. Table 4 provides the results of the static linear factor model with observed factors (SFM-POET) and our deep learning factor models (DNN-FM, SDNN-FM) in estimating the unknown true function in (23), which connects the factors with the response variables . The non-linear (NL-LW, SF-NL-LW) shrinkage estimators of Ledoit and Wolf only provide estimates for the covariance and precision matrix of the returns. For this reason, these methods are not included in Table 4. We also use the linear shrinkage estimator of Ledoit and Wolf (2003) in an earlier version of this paper, however as other methods lead to much better results, hence we omitted the linear shrinkage method from Tables 5 and 6.

Function estimation

| SFM-POET | DNN-FM | SDNN-FM | SFM-POET | DNN-FM | SDNN-FM \bigstrut | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 60 | 50 | 7.05 | 3.67 | 3.87 | 5 | 60 | 50 | 6.17 | 2.46 | 2.88 \bigstrut[t] |

| 60 | 100 | 8.62 | 4.68 | 5.08 | 60 | 100 | 7.27 | 3.03 | 3.90 | ||

| 60 | 200 | 9.95 | 5.12 | 6.36 | 60 | 200 | 8.66 | 3.70 | 5.62 | ||

| 120 | 50 | 6.84 | 3.49 | 3.68 | 120 | 50 | 6.16 | 1.88 | 2.64 | ||

| 120 | 100 | 7.97 | 4.15 | 4.41 | 120 | 100 | 6.84 | 2.15 | 3.31 | ||

| 120 | 200 | 9.41 | 5.24 | 6.06 | 120 | 200 | 9.00 | 2.69 | 5.52 | ||

| 240 | 50 | 5.90 | 3.16 | 3.27 | 240 | 50 | 5.24 | 1.52 | 2.12 | ||

| 240 | 100 | 9.11 | 4.42 | 4.88 | 240 | 100 | 6.66 | 1.87 | 3.02 | ||

| 240 | 200 | 9.49 | 4.71 | 5.33 | 240 | 200 | 8.17 | 2.38 | 4.17 \bigstrut[b] | ||

| 3 | 60 | 50 | 6.84 | 2.74 | 3.30 | 7 | 60 | 50 | 5.74 | 2.67 | 2.80 \bigstrut[t] |

| 60 | 100 | 7.02 | 2.88 | 3.81 | 60 | 100 | 8.23 | 3.74 | 4.65 | ||

| 60 | 200 | 9.20 | 3.79 | 5.66 | 60 | 200 | 9.46 | 4.69 | 6.25 | ||

| 120 | 50 | 5.68 | 2.09 | 2.54 | 120 | 50 | 5.80 | 1.76 | 2.62 | ||

| 120 | 100 | 6.27 | 2.43 | 3.15 | 120 | 100 | 6.77 | 2.11 | 3.47 | ||

| 120 | 200 | 8.30 | 3.07 | 4.69 | 120 | 200 | 7.61 | 2.36 | 5.05 | ||

| 240 | 50 | 6.72 | 2.04 | 2.77 | 240 | 50 | 4.90 | 1.24 | 1.95 | ||

| 240 | 100 | 8.13 | 2.71 | 3.79 | 240 | 100 | 6.99 | 1.66 | 3.25 | ||

| 240 | 200 | 8.29 | 2.79 | 4.25 | 240 | 200 | 8.06 | 1.94 | 4.14 \bigstrut[b] |

The quantities in Table 4 relate to the error metric used in Theorem 1 and Theorem 5, which corresponds to the maximum difference between the estimated and true function. The results indicate that our DNN-FM and SDNN-FM uniformly provide more precise function estimates compared to the SFM-POET. Consequently, these methods are better suited for measuring non-linear transformations of the observed factors and complex transferring mechanisms between the factors and the observed variables. As predicted by the theory, the estimation error of DNN-FM and SDNN-FM converges to zero as increases, e.g., for the DNN-FM with and , the error rate decreases from 4.69 () to 1.94 (). This result is valid for different dimensions of the number of factors and number of variables . Moreover, the error rates of SFM-POET are sensitive to an increase in the number of factors and occasionally rise as gets large. In contrast to that the error rates of DNN-FM and SDNN-FM are in most of the cases unaffected by an increase of , e.g., for the SDNN-FM with , the error rate gradually decreases from 3.27 () to 1.95 (). This result is in line with the theory in Theorem 5. Generally, the error rates of the DNN-FM are smaller compared to the SDNN-FM. This result is anticipated as our simulation study focuses on an in-sample analysis and the DNN-FM with fully connected units offers a more precise function approximation. However, this is not necessarily valid for an out-of-sample analysis, as the DNN-FM might be overfitting compared to a deep neural network with sparsely connected units.

Covariance matrix estimation

| SFM-POET | DNN-FM | SDNN-FM | NL-LW | SF-NL-LW | RN-FM \bigstrut | |||

|---|---|---|---|---|---|---|---|---|

| 1 | 60 | 50 | 2.13 | 1.37 | 1.68 | 1.32 | 1.38 | 2.00 \bigstrut[t] |

| 60 | 100 | 2.62 | 1.71 | 2.11 | 1.60 | 1.74 | 2.24 | |

| 60 | 200 | 3.10 | 2.01 | 2.61 | 1.90 | 2.05 | 2.66 | |

| 120 | 50 | 2.20 | 1.31 | 1.68 | 1.30 | 1.33 | 1.76 | |

| 120 | 100 | 2.72 | 1.64 | 2.13 | 1.57 | 1.59 | 2.27 | |

| 120 | 200 | 3.18 | 1.90 | 2.57 | 1.87 | 2.08 | 2.61 | |

| 240 | 50 | 2.25 | 1.18 | 1.53 | 1.32 | 1.35 | 1.44 | |

| 240 | 100 | 2.77 | 1.47 | 1.96 | 1.57 | 1.59 | 2.14 | |

| 240 | 200 | 3.24 | 1.73 | 2.38 | 1.86 | 1.89 | 2.56 \bigstrut[b] | |

| 3 | 60 | 50 | 1.46 | 0.91 | 1.28 | 1.60 | 1.64 | 1.83 \bigstrut[t] |

| 60 | 100 | 1.73 | 1.10 | 1.53 | 1.89 | 2.00 | 1.77 | |

| 60 | 200 | 2.02 | 1.29 | 1.89 | 2.17 | 2.35 | 2.04 | |

| 120 | 50 | 1.53 | 0.78 | 1.26 | 1.54 | 1.56 | 1.48 | |

| 120 | 100 | 1.80 | 0.95 | 1.52 | 1.80 | 1.80 | 1.70 | |

| 120 | 200 | 2.09 | 1.15 | 1.87 | 2.11 | 2.23 | 1.97 | |

| 240 | 50 | 1.57 | 0.68 | 1.16 | 1.51 | 1.53 | 1.17 | |

| 240 | 100 | 1.85 | 0.83 | 1.38 | 1.79 | 1.78 | 1.66 | |

| 240 | 200 | 2.15 | 1.01 | 1.67 | 2.12 | 2.11 | 1.95 \bigstrut[b] | |

| 5 | 60 | 50 | 1.15 | 0.77 | 1.04 | 1.60 | 1.63 | 1.58 \bigstrut[t] |

| 60 | 100 | 1.36 | 0.90 | 1.23 | 1.94 | 1.98 | 1.59 | |

| 60 | 200 | 1.58 | 1.07 | 1.50 | 2.27 | 2.27 | 1.79 | |

| 120 | 50 | 1.18 | 0.61 | 1.01 | 1.57 | 1.58 | 1.30 | |

| 120 | 100 | 1.39 | 0.76 | 1.22 | 1.83 | 1.85 | 1.54 | |

| 120 | 200 | 1.61 | 0.90 | 1.48 | 2.19 | 2.20 | 1.72 | |

| 240 | 50 | 1.22 | 0.52 | 0.95 | 1.55 | 1.55 | 1.07 | |

| 240 | 100 | 1.43 | 0.64 | 1.11 | 1.82 | 1.81 | 1.51 | |

| 240 | 200 | 1.66 | 0.76 | 1.29 | 2.14 | 2.11 | 1.75 \bigstrut[b] | |

| 7 | 60 | 50 | 1.01 | 0.71 | 0.89 | 1.58 | 1.61 | 1.48 \bigstrut[t] |

| 60 | 100 | 1.16 | 0.84 | 1.06 | 1.88 | 1.91 | 1.51 | |

| 60 | 200 | 1.33 | 0.95 | 1.27 | 2.24 | 2.27 | 1.66 | |

| 120 | 50 | 0.99 | 0.53 | 0.87 | 1.53 | 1.54 | 1.22 | |

| 120 | 100 | 1.15 | 0.64 | 1.04 | 1.85 | 1.86 | 1.45 | |

| 120 | 200 | 1.33 | 0.74 | 1.26 | 2.21 | 2.22 | 1.56 | |

| 240 | 50 | 1.03 | 0.44 | 0.83 | 1.50 | 1.51 | 1.00 | |

| 240 | 100 | 1.20 | 0.54 | 0.97 | 1.83 | 1.83 | 1.40 | |

| 240 | 200 | 1.37 | 0.64 | 1.07 | 2.20 | 2.21 | 1.57 \bigstrut[b] |

-

•

Note: The quantities in the table refer to the error metric used in Theorem 3 and Theorem 6(ii), which corresponds to the maximum matrix norm of the difference between the estimated covariance matrices , and the true covariance matrix . The deep neural network factor model (DNN-FM) and sparse deep neural network factor model (SDNN-FM) are compared to the static factor model with observed factors and POET estimator from Fan et al. (2013) (SFM-POET), the non-linear shrinkage estimator (NL-LW), the single factor non-linear shrinkage estimator (SF-NL-LW) of Ledoit and Wolf (2017) and the residual nodewise regression estimation of factor models by Caner et al. (2023).