Non-Gaussian Process Regression

Abstract

Standard GPs offer a flexible modelling tool for well-behaved processes. However, deviations from Gaussianity are expected to appear in real world datasets, with structural outliers and shocks routinely observed. In these cases GPs can fail to model uncertainty adequately and may over-smooth inferences. Here we extend the GP framework into a new class of time-changed GPs that allow for straightforward modelling of heavy-tailed non-Gaussian behaviours, while retaining a tractable conditional GP structure through an infinite mixture of non-homogeneous GPs representation. The conditional GP structure is obtained by conditioning the observations on a latent transformed input space and the random evolution of the latent transformation is modelled using a Lévy process which allows Bayesian inference in both the posterior predictive density and the latent transformation function. We present Markov chain Monte Carlo inference procedures for this model and demonstrate the potential benefits compared to a standard GP.

1 Introduction

Gaussian processes (GPs) are stochastic processes which are widely used in nonparametric regression and classification problems to represent probability distributions over functions [1]. They allow Bayesian inference in a space of functions such that consistent uncertainty measures over predictions are obtained rather than only point estimates.

In its simplest form a GP defines a distribution over functions through its particular mean and covariance (kernel) functions which determine the smoothness, stationarity and periodicity of a random realisation in the function space. As a prior distribution in Bayesian inference, using a zero mean GP reflects the lack of information in the values and trend of the function. In this case the covariance function, which defines the similarity between any two points in the input space, fully characterises the properties of the random function space.

The design of kernel functions that are able to represent a wide range of characteristics and make consistent generalisations is a fundamental area of research. Some recent work in this area include modelling the kernel via spectral densities that are scale-location mixtures of Gaussians [2], and similarly using Lévy process priors over adaptive basis expansions for the spectral density [3]. Spectral kernels are generalised to non-stationary kernels in [4]. For stationary time series models, a prior over nonparametric kernels can be defined through a separate GP [5].

Extensions to the standard GP model can be made by directly modelling the covariance matrix as a stochastic process [6], assuming heteroscedastic noise on the observations and carrying out variational inference [7], or learning nonlinear transformations of the observations such that the latent transformed observations are modelled well by a GP [8, 9]. Nonstationarity in the measurement process can be expressed as a product of multiple GPs [10] and heavy-tailed observations may be modelled through the Student-t process where the predictive kernel function depends on the values of the observations [11], unlike the standard GP where the kernel is determined only by the values of the input set. Particularly relevant extensions of GP models are presented in [12] where the input space is locally modelled by separate GPs, and string GPs [13] introduce link functions between local GPs such that the global process is still a GP and provides efficient inference methods on large data sets. In [14, 15] a latent space is defined between the inputs and observations through a separate GP and a class of bounded functions in , respectively. In [16] the inputs are assumed to be unobserved and integrated out using a variational approach which leads to deep GPs [17].

By designing expressive covariance functions or stacking multiple GPs in structured arrangements, the GP framework produces accurate predictive models in numerous application domains. However, these models are limited by their Gaussianity assumption such that the local patterns learned through these models are highly dependent on particular observations instead of learning the overall dynamics of the data generating system. A more natural and interpretable way to define complex relationships may be to assume that the underlying random function is non-Gaussian which yields more sparse representations [18] as discussed in Section 4.

In this work, we present a novel approach to modelling non-Gaussian dynamics by constructing a non-Gaussian process (NGP) such that the observations form a conditional GP that is conditioned on a latent input transformation function that is separately modelled as a Lévy process. Building on the definition of a stationary kernel, the latent layer between the input and output spaces represent the random distances between any two points on an input space. In order to define the distribution of random distances without referring to a specific origin, and in order to maintain monotonicity of the input space transformation, the latent space of transformation functions is modelled by a special class of Lévy process called a subordinator that is non-negative and non-decreasing. Such a process is characterised by the distribution of its stationary and independent increments which as a result defines a probability distribution over the distance between any two input values. Making random monotonic transformations of input values allow the kernel to adapt to the local characteristics of an input space or in other words to the varying rate of change in the observations and the learned subordinator provides uncertainty estimates over the variation of the observed process everywhere on its domain. In this paper we focus principally upon 1-dimensional GPs for the sake of brevity, but we emphasise that our approach can be readily extended to multiple dimensions, as described throughout the text and illustrated in the experimental results.

NGPs are related to continuous-time stochastic volatility models studied in the mathematical finance literature to model the behaviour of a stochastic process which has a randomly distributed variance [19]. The time-change operation defined for continuous-time stochastic processes is a standard approach to building stochastic volatility models. A common example is the time-changed Brownian motion where the time-change is chosen to be a subordinator and the time-changed motion produces a Lévy process [20]. In such a model, the process is conditionally a Brownian motion i.e. the integral of a white-noise GP. Similarly, our construction of a stationary NGP follows a GP conditioned on the latent values of a subordinator, thus it is a time-changed GP. Particular non-Gaussian behaviour can be expressed through the characterisation of a subordinator, examples include the stable law, normal-tempered stable, and generalised hyperbolic (including Student-t) processes. Hence, NGPs provide a flexible and expressive probabilistic framework for nonparametric learning of functions.

In Section 2 we briefly review the GP regression framework, introduce the time-change operation and define NGPs. An inference method for NGP regression is presented in Section 3 following an introduction to shot-noise simulation methods for Lévy processes. In Section 4, we present the results of applying NGP regression on representative synthetically generated non-Gaussian data sets to visually highlight their dynamics and compare the results to alternative GPs. Furthermore, a multidimensional example using a data set available in TensorFlow is presented using two different characterisations of a NGP. Lastly in Section 5, we discuss future extensions to our work that are aimed at extending the applicability of the model presented in Section 4.

2 Models

In this section, we briefly present the standard GP regression framework and introduce the time-change operation which results in a non-Gaussian process (NGP). The series representation of a Lévy process [21] reviewed in Section 2.2 is central to the inference methodology studied in Section 3.

2.1 Gaussian process regression

A stochastic process is defined by the probability distribution of all possible finite subsets of its values, where is a -dimensional input space. In the case of GPs, for any finite set of inputs the corresponding values of the function has a multivariate Gaussian distribution [22] characterised by its mean and covariance kernel functions where . Given a set of inputs the mean function forms a vector and the kernel function forms a positive-definite covariance matrix . The resulting multivariate Gaussian distribution can be extended to any input following the Kolmogorov extension theorem [23] which produces the interpretation of the stochastic process as a random function such that .

In the standard GP regression setting, it is assumed that noisy observations of a function are made such that where are a sequence of independent and identically distributed Gaussian noise. Following a Bayesian approach, a prior distribution on the function space is defined such that where any marginal has a Gaussian distribution. In general referring to any particular marginal of is not necessary since a GP is defined for all points in and the finite distribution is understood from the context. Since the likelihood is a product of Gaussians, the posterior distribution over the function space can be analytically found to be a GP with a particular mean and kernel function where both functions are defined for any finite set of inputs as shown in [1]. The posterior GP is denoted as .

2.2 Time-change

In this section, the classical time-change operation is introduced in one dimension of time and the operation is generalised to multidimensional input spaces using subordinated Gaussian fields [24, 25, 26].

Let be an isotropic stochastic process which has uniformly distributed variance. The operational time can be interpreted as a linear representation of change such that the derivative is proportional to a deterministic constant. Hence the variance of scales proportionally to time intervals. Random evolution in variance may be obtained by considering a representation of change that is random and nonlinear.

Define a non-negative, non-decreasing stochastic process such that it randomly maps time instances while preserving their order, therefore changing the time. A time-changed stochastic process is then defined as where the evolution of is governed by instead of . In other words, the change in will have variance proportional to , instead of where . Assuming that is Gaussian, this operation enables large deviations from Gaussian behaviour to occur when is large, while retaining a conditionally Gaussian form.

The random evolution of can be modelled as a subordinator that take values in such that it has independent and stationary increments with no fixed discontinuities [27, 28]. Thus, a subordinator increases non-linearly with a certain statistical distribution defined by the random number of discontinuities and their random magnitudes. A Lévy process in having no drift or Brownian motion is defined through its characteristic function ([29], Corollary 15.8) where is a Lévy measure that satisfies ([28], p.72). The Lévy measure is defined on the random magnitudes of discontinuities, called jumps, and denotes the expected number of jumps per unit time whose magnitudes belong to some subset of the jump space [30].

By the Lévy-Itô decomposition, a pure jump Lévy process (i.e. containing no Brownian motion) may be expressed using a stochastic integral as

| (1) |

where is a bivariate point process having mean measure on which can be conveniently expressed using a Poisson random measure as

| (2) |

where are i.i.d. uniform random variables which give the times of arrival of jumps, are the sizes of the jumps and is Dirac measure centered at time and jump size . Substituting into Eq. (1) leads to a representation of a Lévy jump process as an infinite series

| (3) |

The almost sure convergence of this series to is proved in [21]. Therefore, by sampling pairs of jump times and sizes , a realisation of a Lévy process may be obtained.

The standard formulation of the time-change operation on can be extended to -dimensional input spaces by considering the Poisson random measure representation of a Lévy process. A homogeneous Poisson process expressing the jump times can be generalised to any number of dimensions where we define arbitrary inputs [31]. The independence properties of a Lévy measure allow the definition on the unit time interval to be extended to unit -dimensional volumes by appropriately scaling the rate of the process [32]. For multidimensional input transformations a subordination field on is a -dimensional stochastic process such that each of its dimensions is a subordinator. Thus the -th dimension of an input vector is mapped to where denotes the subordinator on . Therefore a distance can be randomly transformed as . Hence, the choice of a Lévy measure characterise the distribution of the random distances over the input space. The notation introduced for the multidimensional treatment of subordination is omitted for brevity in the following sections as it is straightforward to extend the model into multidimensional input spaces.

2.3 Non-Gaussian processes

A non-Gaussian process (NGP) prior on functions can be obtained by randomly transforming the inputs using a subordinator and carrying out GP regression on the transformed input space. The resulting posterior distribution follows a non-Gaussian stochastic process. Given a set of input-output pairs consider a latent input transformation such that is mapped to where is a subordinator. The associated prior on the transformation function is then defined as and the conditional prior over is where , and is a stationary kernel function e.g. squared exponential or Matérn. The joint distribution over the product space of and , characterises the NGP prior.

The conditional GP structure of a NGP induces a posterior mean and kernel function that can be evaluated analytically, i.e. . The conditional likelihood is of particular interest in this framework since it is a measure of how well the data is represented by the model given a random transformation and it can also be evaluated analytically.

The NGP posterior distribution over the function space is found as

where is the posterior distribution of the subordinator process. Inferring and hence is analytically intractable, however using approximate inference methods allow for straightforward extensions of the model and fully Bayesian inference as discussed in the following.

3 Sampling and Inference

In this section, we review shot-noise simulation methods for simulating Lévy processes based on series representations [21]. We describe a novel Metropolis-Hastings-within-Gibbs (MH-in-Gibbs) algorithm [33, 34] to obtain samples from the posterior distribution of a subordinator and estimate a non-Gaussian process posterior .

3.1 Shot-noise simulation methods

The jump magnitudes shown in Eq. (3) of a Lévy process cannot be directly simulated because there may be an infinite number of jumps in any finite interval. One way to obtain approximate samples from such an infinite sequence is to consider ordering the jump magnitudes by size and simulating large jumps while ignoring or approximating the residual error as discussed in [35, 21, 36, 32, 37]. Once the ordered jump sizes have been obtained, the corresponding jump positions may be simulated independently from a uniform distribution on where , are some lower and upper bounds, or sequentially in space from a homogeneous Poisson process if preferred.

Consider a bivariate point process that has the same form as Eq. (2) where the jump magnitudes are expressed as the output of a function where are the epochs of a unit rate Poisson process, i.e. the cumulative sum of exponential random variables with unit rate, independent of . Similar to the standard inverse CDF method for random variate generation, the upper tail mass of a Lévy measure can be inverted to produce jump magnitudes of a subordinator by passing epochs of a homogeneous Poisson process through the inverse Lévy measure . The corresponding function is non-increasing thus is an ordered sequence representing random jump sizes. Note that the epochs of a homogeneous Poisson process are analogous to uniformly distributed random variables in and the mapping theorem states that the resulting points form a Poisson point process on [31]. converges almost surely to as the sequence is simulated indefinitely [21] and approximations of the point process may be obtained through finite samples.

The explicit evaluation of the inverse tail measure in general is not possible. The Lévy measures considered in this paper possess a density function denoted as such that . The approach taken in this work is to simulate from a tractable dominating point process having Lévy measure such that for which can be explicitly evaluated. The resulting jump magnitudes belonging to are then thinned with probability as in [38] to obtain the desired approximate jump magnitudes of a subordinator.

As a motivating example in this paper, we consider tempered stable (TS) processes which are commonly used in mathematical finance to model stochastic volatility [39]. We note that our methodology is equally applicable to other subordinator processes for which shot noise simulation methods can be applied [37, 40]. A TS process exhibits both -stable and Gaussian trends depending on the distance it travels. For short distances the stable characteristics prevail and the TS process produces larger jumps compared to a Gaussian process. For longer distances the tempering causes a TS process to produce Gaussian trends [41]. Thus, a TS process is a natural extension to Gaussian processes.

| (4) |

where is the tail parameter and is the tempering parameter. The corresponding tail probability may be calculated in terms of gamma functions but it cannot be analytically inverted and numerical approximations are needed [43]. Instead, we adopt a thinning approach where the Lévy density is factorised into a -stable subordinator process with Lévy density [44, 40] and a tempering function . The tail mass of a stable process can be found to be and inverting this function produces the simulation function . Given points from a stable point process with density , individually selecting (thinning) points with probability results in a tempered stable process. The associated sampling algorithm is shown in Alg. 1 for reference.

-

1.

Assign ,

-

2.

Generate the epochs of a unit rate Poisson process, ,

-

3.

For ,

-

•

Compute ,

-

•

With probability , accept and assign .

-

•

Algorithm 1 generates the jumps that correspond to a TS process in . Since the jumps of a Lévy process are independent and stationary it is straightforward to adjust the interval. For instance, setting the rate of the underlying Poisson process produced in the second stage of Alg. 1 to the length of the interval produces the associated TS process. Similarly, for -dimensional input spaces the jumps on a -dimensional hypercube can be simulated by setting the rate to the associated volume [32].

3.2 Approximate inference

Since a stochastic process is defined as an infinite collection of random variables, designing direct sampling methods from the posterior based on batch Monte Carlo methods is a difficult task. Instead a more appropriate approach to high dimensional problems is to use a Gibbs sampler which approximates samples from a multivariate probability distribution or in this case a stochastic process. The latent random variables are grouped into smaller and more manageable collections, then each collection is iteratively updated conditioned on the previous samples and observations. The sequence of samples from such an algorithm can be considered as a Markov chain where the stationary distribution is the high dimensional posterior distribution that was targeted. For a short tutorial on Gibbs sampling see [45].

A Gibbs sampler approximating samples from can be implemented by simulating the associated bivariate random points that define the jump size and position on small disjoint intervals conditioned on the previous sample points in and observations. Progressively simulating these points such that the whole input space is covered leads to approximate samples from the target distribution. Let be a random length sequence of jump positions and magnitudes associated with the -th sample in a Monte Carlo procedure. For any interval new jump position and magnitudes can be simulated with a rate determined by the distance while removing the points associated with the same interval from . The resulting sample path is denoted as before accepting or rejecting it as the -th sample .

While Gibbs sampling reduces the complexity of sampling a stochastic process for each small interval, direct sampling from the conditional posterior for each interval is still intractable in general. Thus for each interval a Metropolis-Hastings algorithm is used yielding a MH-within-Gibbs sampling algorithm [34]. The proposal density for the MCMC sampling procedure is which produces new bivariate points (jump sizes and times) on some interval conditioned on all points in as described in Alg. 2.

For each realisation of the subordinator , the conditional likelihood may be used as a weight in a Markov chain Monte Carlo sampler since it is proportional to the posterior distribution and we are proposing from . As discussed in Section 2.3 the conditional likelihood may be analytically found given the values of . Then given a sample and proposal , the acceptance probability for the proposal is

| (5) |

-

1.

Initialise by simulating from the associated bivariate point process using Alg. 1,

-

2.

Analytically evaluate , which define the conditional GP posterior , and the conditional likelihood ,

-

3.

For times, iterate over where ,

-

(a)

Using and the points associated with , sample a proposed sample path using Alg. 2,

-

(b)

Evaluate , and ,

-

(c)

With probability the proposal is accepted and , otherwise reject and set .

-

(a)

The MH-within-Gibbs sampling procedure is described in Alg. 3. The resulting samples are individually associated with conditional GP posterior functions that are completely defined through their mean and covariance functions. Such a collection forms a Gaussian mixture distribution and the mean and covariance of the corresponding mixture density can be obtained as

| (6) |

and

| (7) |

where is the number of samples and , define the posterior mean and covariance of the random function . It is straightforward to obtain the corresponding predictive density by adding the observation noise matrix to each covariance matrix sample . Using a constant noise matrix corresponds to the assumption that the observation likelihood model is Gaussian [1]. This assumption can be relaxed by sampling a noise matrix for each individual sample to consider non-Gaussian likelihood models such as scale mixture of normals which includes the Student-t and Laplace distributions [46]. This results in doubly non-Gaussian behaviour which is highly expressive while retaining interpretation of individual components of the behaviour.

Following a similar approach the hyperparameters , and of the subordinator process may be included in the sampling procedure by considering an appropriate prior distribution over their values. Hence these parameters may be marginalised out using the Monte Carlo procedure, which leaves the same number of kernel parameters that define a standard GP. This approach works successfully and will be reported in a future publication. Furthermore, a nonparametric kernel may be included in this framework by considering a prior distribution on stationary kernel functions and sampling a kernel function for each proposed sample. Some examples of nonparametric kernel design can be found in [2, 5, 47].

A straightforward extension of Alg. 3 to multidimensional input spaces can be achieved by assuming that individual subordinator dimensions are independent a priori. The simulation steps defined by Alg. 1 and 2 can be independently applied to each dimension and the other steps remain unchanged, replacing step 3. (b) with the multidimensional GP likelihood.

4 Experimental Results

In this section, we present the results of applying NGP regression to non-Gaussian data sets and compare the results with alternative standard GP regression settings. In order to emphasise the differences in non-Gaussian and Gaussian processes, we first use a synthetically generated data set that displays non-Gaussian behaviour that is representative of a tempered stable process as the observations display local deviations from Gaussian behaviour while long-range dependencies remain Gaussian. Afterwards, in order to demonstrate the generalisation of a NGP to multidimensional input spaces a two dimensional example problem is presented using a toy data set available in TensorFlow [48] on diamond prices.

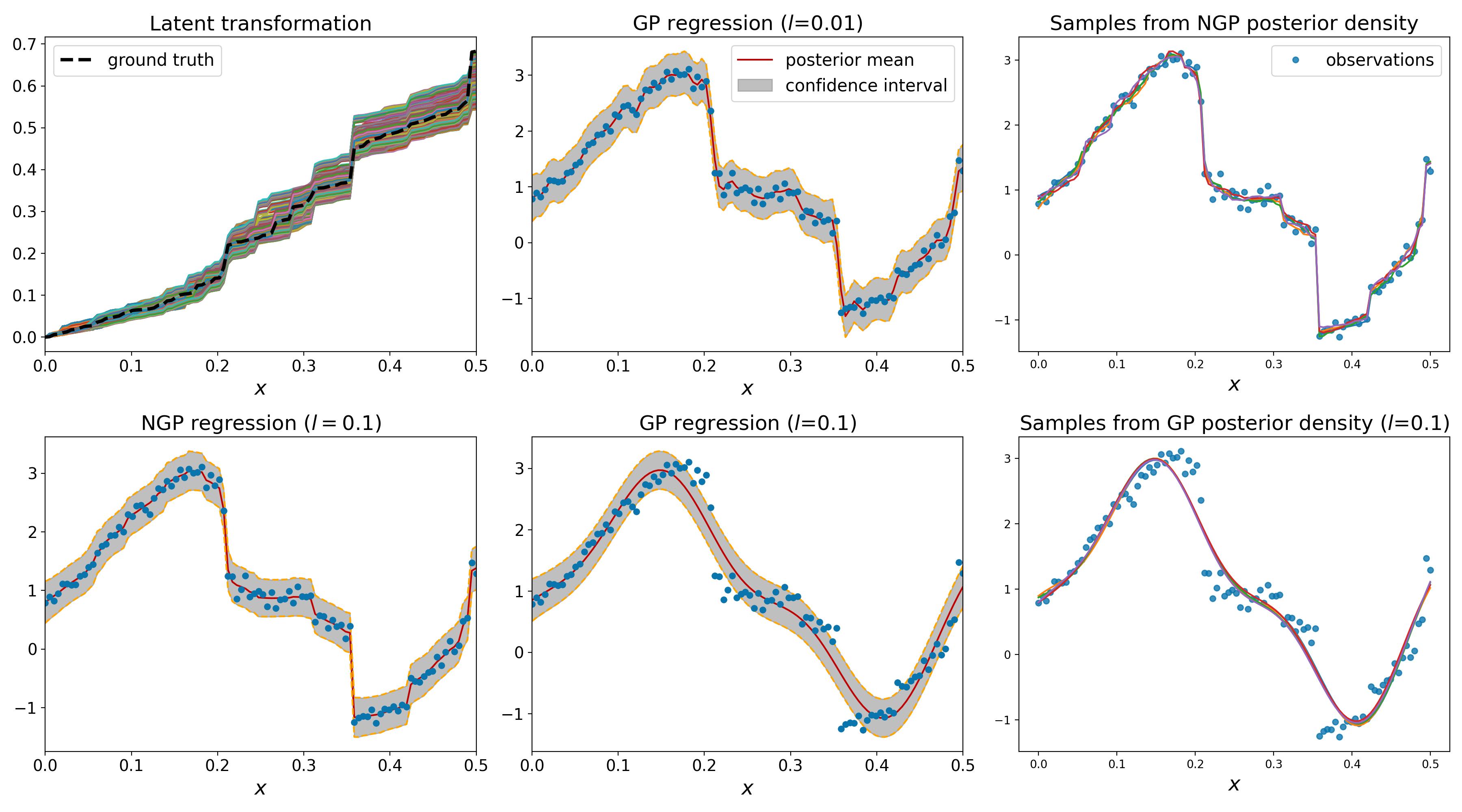

Any stationary kernel function can be used to define the conditional kernel function in NGP regression. Initially a squared exponential (SE) kernel is selected for the conditional GP since it is one of the most widely used examples. In order to demonstrate the ability of a NGP in identifying local characteristics, a length-scale is used and an observation set defined on a small region of the input space is simulated from a NGP prior. The latent transformation space in this example is generated as a TS subordinator with and and the observations have i.i.d. noise with standard deviation . The observations and results are shown in Fig. 1.

The NGP predictive posterior density shown in the first column of Fig. 1 clearly identifies some local changes in the variance that match with large jumps observed in the latent transformation posterior samples above. Furthermore, for input differences on the order of the density retains close to Gaussian behaviour. The posterior sample paths on the latent transformation space identify how fast the SE kernel decays to zero around different regions in . Large jump sizes break the correlation between local points and the associated observations are treated as statistically independent. From this perspective, if the model correctly identifies large jumps this shows that it discovers some observations contain more information about their local region than a stationary GP can encode. Hence, the sample paths provide an expressive probabilistic layer for interpreting non-Gaussian behaviour.

Two alternative GP regression results are presented in the second column of Fig. 1. Firstly, using the ground truth value of , a smooth approximation of the predictive posterior density can be obtained. Alternatively, a GP with a higher marginal likelihood can be obtained by optimising the length-scale. In order to adapt to large deviations in some regions of the optimisation results in a smaller value of . This can be considered as a trade-off between in-sample performance and the generalisation capability of the model. As gets smaller each observation is modelled as almost statistically independent and there are no long distance dependencies between inputs. Such a representation will likely be an overfitted model that does not have any generalisation capability and interpolations will produce white-noise. NGP regression provides a more sparse representation of the random function in the sense that it only defines local statistical independence assumptions if the observations show non-Gaussian behaviour and otherwise retain long distance dependencies.

Our Gibbs sampler defines a grid of disjoint intervals and iterates over the whole space times. After initial samples are discarded for burn-in the average log conditional likelihood of the remaining samples is found to be with a standard deviation of . In comparison the log conditional likelihood of the data generating process is found as which suggests that the NGP does not overfit. The log marginal likelihood of the GPs with and are found as and , respectively. The mean acceptance probability for each step in Alg. 3 is found as . The confidence intervals in regression results show standard deviations. Lastly, on the right column we show samples from the NGP posterior density and its smooth approximation.

Given the results above the two main aspects that require further attention are the design of a sensible prior distribution on the latent transformation space and the initialisation of the Gibbs sampler. The tempered stable (TS) subordinator is characterised by three parameters, , and , that represent the tail heaviness, tempering and scale. The expected value and variance of the subordinator process on an input space is a function of these parameters and the length (or measure) of . In order to produce results that are comparable with Gaussian process (GP) regression, the expected value of the subordinator process is set to the length of , i.e. given an interval the expected value is . As discussed in Section 2.2, if the observed input points are assumed to lie on a Euclidean space, the change in the covariance scales linearly according to . On the latent transformation space, this corresponds to an identity map in . Setting the expected value to the length of the input set expresses a preference towards regular Gaussian behaviour and the deviations from the identity map provide insight into the characteristics of the observed data set.

Note again that the shot-noise simulation methods studied in Section 3.1 produce approximate sample paths from a Lévy process since the infinite series described by Eq. (3) have to be truncated to a finite number of terms. The convergence of the series is found in practice to be faster for smaller values of and parameters. The number of terms that are required to obtain a sufficiently close estimate can be adaptively found using probabilistic asymptotic bounds and will be presented in future extensions of our work. However, a simple way to ensure the required convergence is to increase the number of terms produced as gets larger. In practice for , producing terms in Alg. 1 is found to work well.

The initialisation of the Gibbs sampler in practice is one of the central issues in designing Markov chain Monte Carlo methods. In Alg. 3, the sampling method depends on the number and size of small disjoint intervals . As the size of is decreased, the acceptance rates for the Gibbs sampler increase and convergence can be achieved in a few number of iterations of the whole input space. However, this also results in an increased number of intervals and each iteration requires more computation and time. Our strategy to initialise the Gibbs sampler is to obtain a crude estimate of the latent transformation function by running the same algorithm on a few number of intervals and set the initial state of the Gibbs sampler to the jump magnitudes and positions that correspond to the last sample path. The chain can then be simulated starting from this state and only a few samples have to be discarded as burn-in. Alternatively, a simpler initialisation is to generate linearly spaced points with equal magnitudes that represent the identity map corresponding to a GP regression setting. This alternative initialisation can be particularly useful for dataset that display close to Gaussian behaviour.

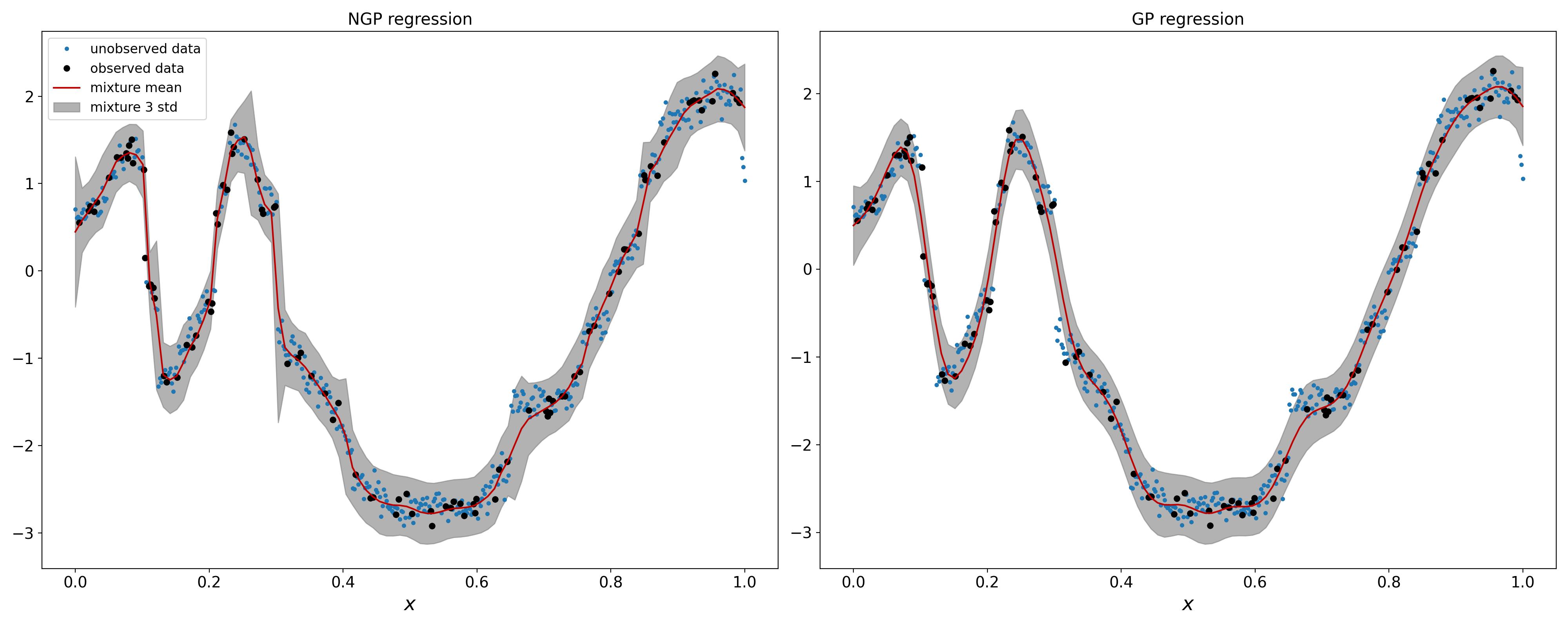

It is straightforward to change the particular choice of a kernel function without any changes in our presented algorithms. In Fig. 2 an example regression problem is presented using the conditional kernel function specified as the Matérn kernel. The Matérn kernel decays slower than a squared exponential kernel and therefore can be used to model long range dependencies. Particular parameter values of the Matérn kernel correspond to the covariance of certain stochastic differential equations as described in [49]. The results are again compared with a GP regression setting to highlight the differences. The smoothness parameter is chosen as and the length-scale is . The subordinator parameters are identical to the previous example in Fig. 1. A dataset of size is generated on from the NGP prior and a set of size is randomly selected as the observations. In this case, the unobserved elements in the dataset serve as the test set. For the NGP regression, most unobserved data points lie inside the confidence intervals while the GP regression misses these points around local deviations. The log conditional likelihood of the NGP and the marginal likelihood of the GP models are and respectively.

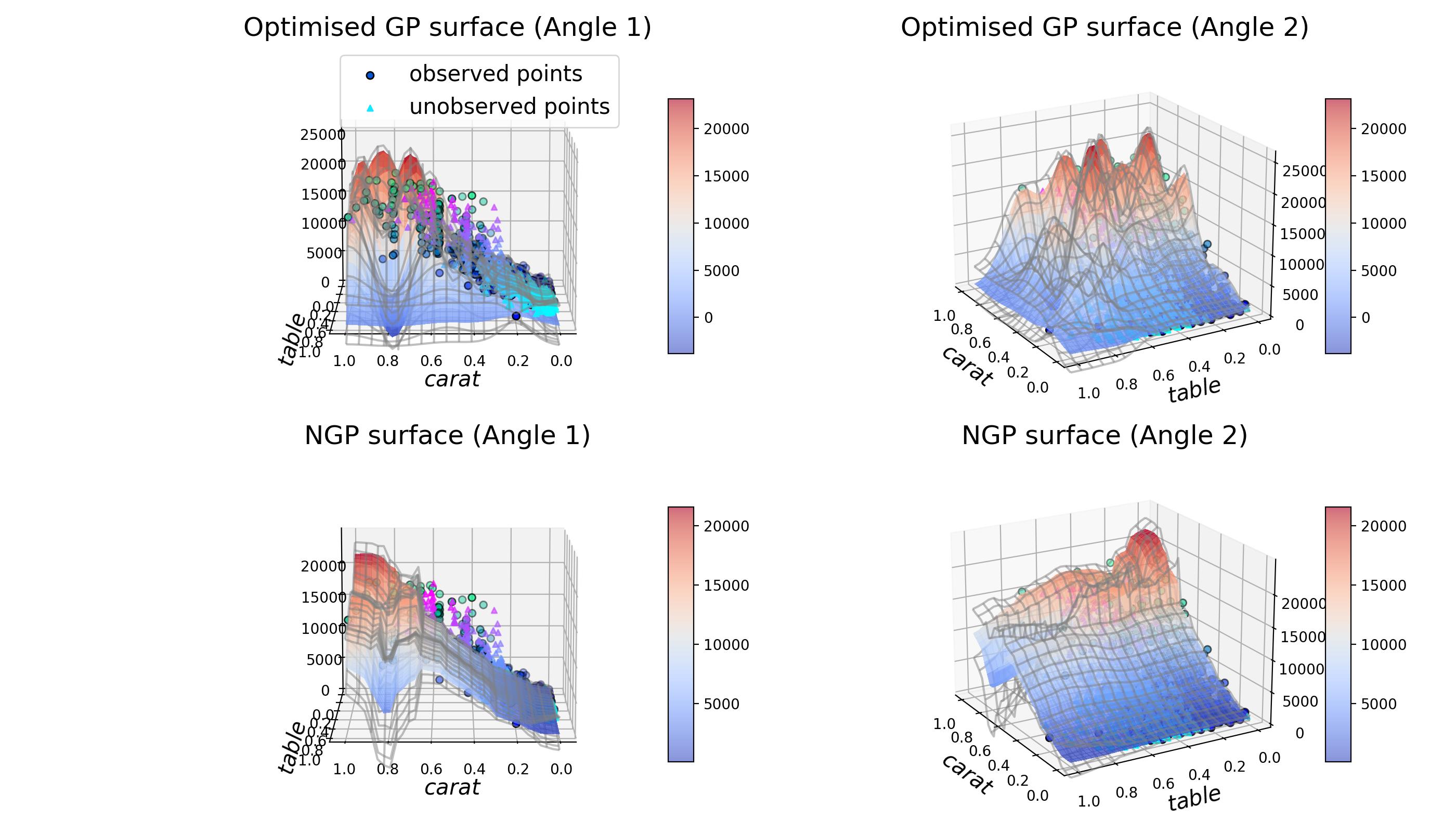

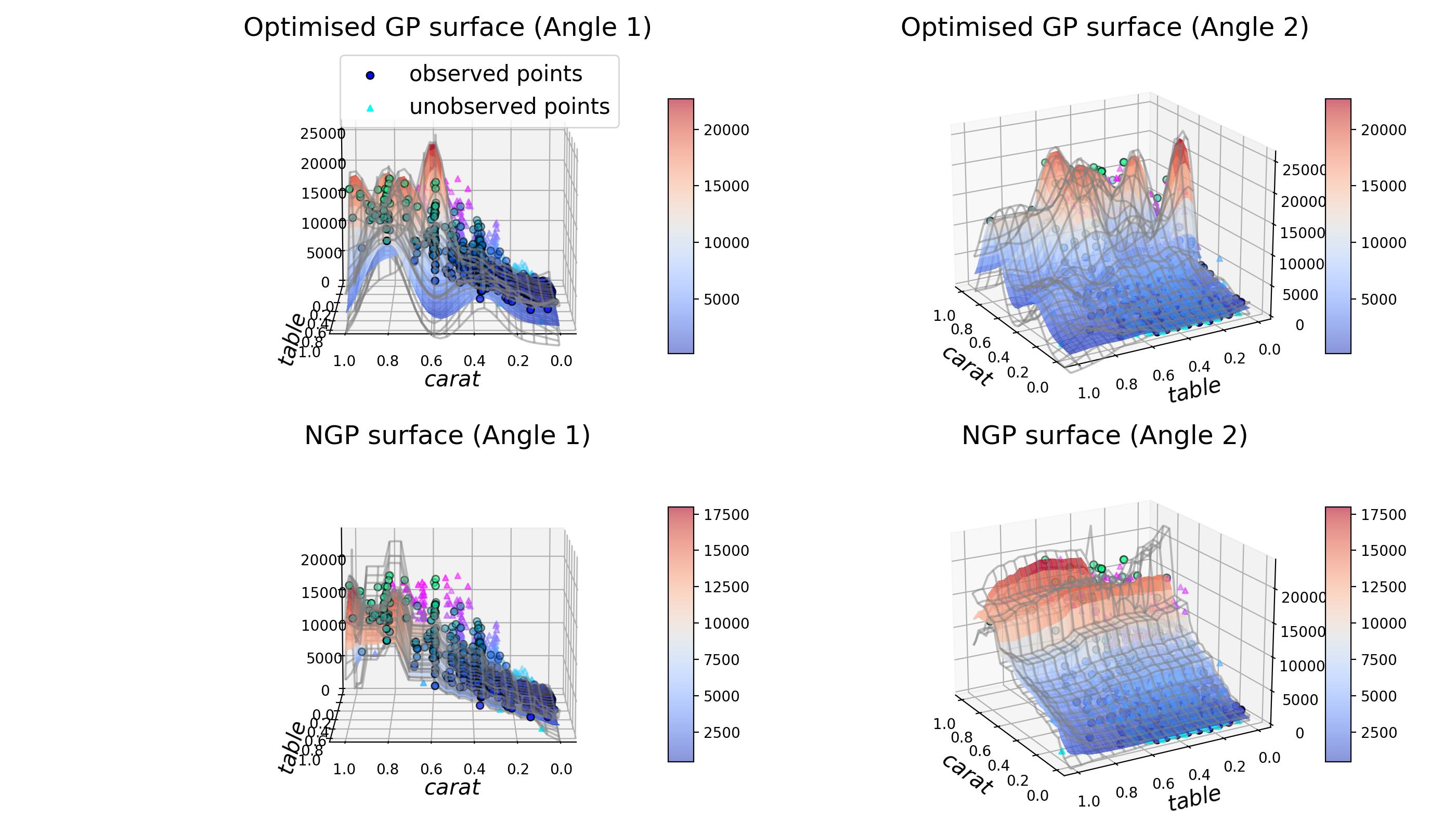

Lastly for the multidimensional case an example regression model for diamond prices is presented. The features used in this task are the carat of a diamond which is a measure of its weight and the percentage length of its table which is the largest flat facet of the diamond and affects how the diamond interacts with light. For ease of visualisation, both input dimensions are linearly transformed to lie between .

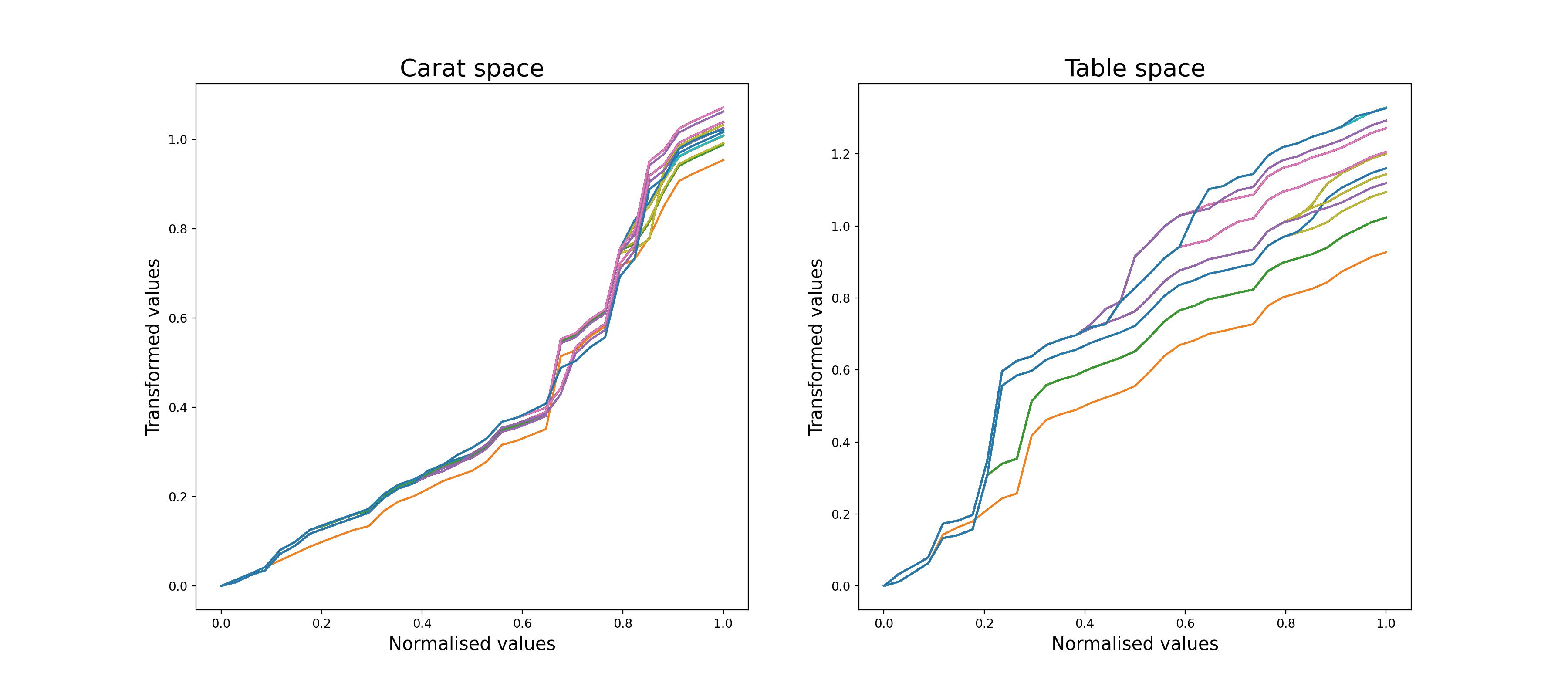

The experiment is designed such that a randomly selected input-output pairs are chosen as the training set and the learned posterior surface is compared against another randomly selected pairs. In order to emphasise that our framework works for any choice of Lévy process with a measure that possesses a density function, the experiment is run separately using a TS subordinator as well as a gamma subordinator. The required simulation algorithm for the gamma subordinator is presented in [21, 37].

Figures 3 and 4 show the results of NGP regression using a TS subordinator. The GP surfaces shown in Fig. 2 suggest that the standard GP framework is unable to recover a meaningful relationship between the input dimensions and observations. While it may make accurate predictions around observed points, on unobserved regions of the input space the posterior surface rapidly decays to the prior distribution. The NGP surface clearly identifies a relationship between the carat of a diamond and its price. The price of a diamond increases as its carat increase and there is a nonlinear increase in price around normalised carat values. The nonlinearity can be identified in Fig. 4 and the corresponding uncertainty of price values around the nonlinear increase can be seen in Fig. 3. While this is a toy example, the discovered relationship between the carat of a diamond and its price is reasonable and intuitive. Similarly, the NGP surface suggests that the percentage length of the table of a diamond does not influence the price of a diamond for small carat values but has an inverse relationship for larger carats.

The same experiment is performed using a gamma subordinator and an independently sampled training set, the results are presented Figures 5 and 6. Similar conclusions can be made using the gamma subordinator. However note that the gamma subordinator is characterised by the flat intervals shown in Fig. 6 and there may be other applications that are more appropriate for such a posterior surface.

5 Discussion

NGP regression with a tempered stable subordinator presented in this work may be applied to datasets where there are local deviations from Gaussian behaviour but the overall trend of the function closely follows a GP. Using alternative characterisations of the subordinator, varying degrees of non-Gaussian behaviour can be modelled in a NGP regression framework as briefly demonstrated in Section 4. Some practical examples of subordinator processes are gamma processes [21] and inverse Gaussian processes [50, 51] which both lead to analytical probability density functions unlike the TS process. This fact can be utilised to design better proposal densities for a MCMC procedure. However given any Lévy density a similar formulation to Section 3.1 can be readily designed and used for inference as studied in Section 3.2. A particularly interesting case is the generalised inverse-Gaussian process which can capture various degrees of semi-heavy-tailed behaviour, including the gamma and inverse Gaussian processes [52, 37].

As shown in the two dimensional example in Section 4 the model can be extended to include multiple inputs by transforming each input dimension independently using a subordination field as discussed in Sections 2.2 and 3.2. Independent realisations of the Markov chain result in slightly different posterior densities over the space of subordinator functions. Jump magnitudes that are significantly larger than the length-scale may lead to similar independence assumptions on the observation space. The posterior density over the observations is less sensitive to variations in the subordinator functions. This suggests that there might be alternative representations that lead to similar behaviour in the observation space and the approximate inference procedure converges to a locally optimum posterior density. An improved estimate may be obtained by independently running a parallel MCMC algorithm based on our method and averaging over the samples. Another straightforward extension to our Gibbs sampler shown in Alg. 3 is to randomly sample an interval for each iteration such that the random intervals are ergodic.

Using NGP regression produces a generative model conditioned on a dataset where samples from both the posterior density over the input transformation and the predictive density over the observations can be generated. A probabilistic representation of a latent layer between the input and output spaces may lead to new insights about the underlying data generating mechanism. Furthermore, our construction of a NGP using the time-change operation may potentially be extended to any probabilistic setting for interpreting non-Gaussian behaviour. For example, Lévy fields can be used to model the first layer of a deep GP architecture. Our model is especially appropriate for applications in decision making where a reliable uncertainty estimate over predictions is critical and the data does not follow a simple stationary Gaussian behaviour. Some examples of such problems may be found in the field of reinforcement learning [53, 54, 55]. Note that while NGP regression provides an interpretable representation of data, future research is required on the assessment of the reliability of these representations on particular application domains. A relevant discussion on the deployment of interpretable machine learning systems in real world settings can be found in [56].

References

- [1] C. E. Rasmussen and C. K. I. Williams “Gaussian Processes for Machine Learning” MIT Press, 2006

- [2] Andrew Wilson and Ryan Adams “Gaussian Process Kernels for Pattern Discovery and Extrapolation” In Proceedings of the 30th International Conference on Machine Learning 28.3, Proceedings of Machine Learning Research Atlanta, Georgia, USA: PMLR, 2013, pp. 1067–1075 URL: https://proceedings.mlr.press/v28/wilson13.html

- [3] Phillip A Jang, Andrew Loeb, Matthew Davidow and Andrew G Wilson “Scalable Levy Process Priors for Spectral Kernel Learning” In Advances in Neural Information Processing Systems 30 Curran Associates, Inc., 2017 URL: https://proceedings.neurips.cc/paper/2017/file/02b1be0d48924c327124732726097157-Paper.pdf

- [4] Yves-Laurent Kom Samo and Stephen Roberts “Generalized spectral kernels” In arXiv preprint arXiv:1506.02236, 2015

- [5] Felipe Tobar, Thang D Bui and Richard E Turner “Learning Stationary Time Series using Gaussian Processes with Nonparametric Kernels” In Advances in Neural Information Processing Systems 28 Curran Associates, Inc., 2015 URL: https://proceedings.neurips.cc/paper/2015/file/95e6834d0a3d99e9ea8811855ae9229d-Paper.pdf

- [6] Andrew Gordon Wilson and Zoubin Ghahramani “Generalised Wishart Processes” arXiv, 2011 DOI: 10.48550/ARXIV.1101.0240

- [7] Miguel Lázaro-Gredilla and Michalis Titsias “Variational Heteroscedastic Gaussian Process Regression” In Proceedings of the 28th International Conference on Machine Learning, ICML 2011, 2011, pp. 841–848

- [8] Edward Snelson, Zoubin Ghahramani and Carl Rasmussen “Warped Gaussian Processes” In Advances in Neural Information Processing Systems 16 MIT Press, 2003 URL: https://proceedings.neurips.cc/paper/2003/file/6b5754d737784b51ec5075c0dc437bf0-Paper.pdf

- [9] Miguel Lázaro-Gredilla “Bayesian Warped Gaussian Processes” In Advances in Neural Information Processing Systems 25 Curran Associates, Inc., 2012 URL: https://proceedings.neurips.cc/paper/2012/file/d840cc5d906c3e9c84374c8919d2074e-Paper.pdf

- [10] Ryan Prescott Adams and Oliver Stegle “Gaussian Process Product Models for Nonparametric Nonstationarity” In Proceedings of the 25th International Conference on Machine Learning, ICML ’08 Helsinki, Finland: Association for Computing Machinery, 2008, pp. 1–8 DOI: 10.1145/1390156.1390157

- [11] Amar Shah, Andrew Wilson and Zoubin Ghahramani “Student-t Processes as Alternatives to Gaussian Processes” In Proceedings of the Seventeenth International Conference on Artificial Intelligence and Statistics 33, Proceedings of Machine Learning Research Reykjavik, Iceland: PMLR, 2014, pp. 877–885 URL: https://proceedings.mlr.press/v33/shah14.html

- [12] Carl Rasmussen and Zoubin Ghahramani “Infinite Mixtures of Gaussian Process Experts” In Advances in Neural Information Processing Systems 14 MIT Press, 2001 URL: https://proceedings.neurips.cc/paper/2001/file/9afefc52942cb83c7c1f14b2139b09ba-Paper.pdf

- [13] Y-LK Samo and Stephen J Roberts “String and membrane Gaussian processes” In Journal of Machine Learning Research 17 Journal of Machine Learning Research, 2016

- [14] Alexandra M. Schmidt and Anthony O’Hagan “Bayesian Inference for Non-Stationary Spatial Covariance Structure via Spatial Deformations” In Journal of the Royal Statistical Society. Series B (Statistical Methodology) 65.3 [Royal Statistical Society, Wiley], 2003, pp. 743–758 URL: http://www.jstor.org/stable/3647549

- [15] Jasper Snoek, Kevin Swersky, Rich Zemel and Ryan Adams “Input Warping for Bayesian Optimization of Non-Stationary Functions” In Proceedings of the 31st International Conference on Machine Learning 32.2, Proceedings of Machine Learning Research Bejing, China: PMLR, 2014, pp. 1674–1682 URL: https://proceedings.mlr.press/v32/snoek14.html

- [16] Michalis Titsias and Neil D. Lawrence “Bayesian Gaussian Process Latent Variable Model” In Proceedings of the Thirteenth International Conference on Artificial Intelligence and Statistics 9, Proceedings of Machine Learning Research Chia Laguna Resort, Sardinia, Italy: PMLR, 2010, pp. 844–851 URL: https://proceedings.mlr.press/v9/titsias10a.html

- [17] Andreas Damianou and Neil D. Lawrence “Deep Gaussian Processes” In Proceedings of the Sixteenth International Conference on Artificial Intelligence and Statistics 31, Proceedings of Machine Learning Research Scottsdale, Arizona, USA: PMLR, 2013, pp. 207–215 URL: https://proceedings.mlr.press/v31/damianou13a.html

- [18] Michael Unser and Pouya D. Tafti “An Introduction to Sparse Stochastic Processes” Cambridge University Press, 2014 DOI: 10.1017/CBO9781107415805

- [19] Eric Ghysels, Andrew C. Harvey and Eric Renault “Stochastic volatility” In Statistical Methods in Finance 14, Handbook of Statistics Elsevier, 1996, pp. 119–191 DOI: https://doi.org/10.1016/S0169-7161(96)14007-4

- [20] AED Veraart and M Winkel “Time change” In Encyclopedia of Quantitative Finance Wiley, 2010, pp. 1812–1816 DOI: 10.1002/9780470061602.eqf19026

- [21] J. Rosiński “Series Representations of Lévy Processes from the Perspective of Point Processes” In Lévy Processes: Theory and Applications Boston, MA: Birkhäuser Boston, 2001, pp. 401–415 DOI: 10.1007/978-1-4612-0197-7˙18

- [22] David J. C. MacKay “Information Theory, Inference, and Learning Algorithms” Copyright Cambridge University Press, 2003

- [23] Bernt Øksendal “Stochastic Differential Equations: An Introduction with Applications” Springer, Paperback, 2014

- [24] R. L. Dobrushin “Gaussian and their Subordinated Self-similar Random Generalized Fields” In The Annals of Probability 7.1 Institute of Mathematical Statistics, 1979, pp. 1 –28 DOI: 10.1214/aop/1176995145

- [25] Robin Merkle and Andrea Barth “On Some Distributional Properties of Subordinated Gaussian Random Fields” In Methodology and Computing in Applied Probability Springer ScienceBusiness Media LLC, 2022 DOI: 10.1007/s11009-022-09958-x

- [26] Robin Merkle and Andrea Barth “Subordinated Gaussian random fields in elliptic partial differential equations” In Stochastics and Partial Differential Equations: Analysis and Computations Springer, 2022, pp. 1–49

- [27] W. Feller “An introduction to probability theory and its applications”, Wiley mathematical statistics series v. 2 Wiley, 1966

- [28] J. Bertoin “Lévy Processes”, Cambridge Tracts in Mathematics, 121 Cambridge University Press, 1997

- [29] O. Kallenberg “Foundations of Modern Probability” Springer-Verlag, 2002

- [30] Tankov, P. and Cont, R. “Financial Modelling with Jump Processes, Second Edition”, Chapman and Hall/CRC Financial Mathematics Series Taylor & Francis, 2015

- [31] Kingman, J.F.C. “Poisson Processes”, Oxford Studies in Probability Clarendon Press, 1992

- [32] Robert L. Wolpert and Katja Ickstadt “Simulation of Lévy Random Fields” In Practical Nonparametric and Semiparametric Bayesian Statistics New York, NY: Springer New York, 1998, pp. 227–242 DOI: 10.1007/978-1-4612-1732-9˙12

- [33] W. K. Hastings “Monte Carlo sampling methods using Markov chains and their applications” In Biometrika 57.1, 1970, pp. 97–109 DOI: 10.1093/biomet/57.1.97

- [34] Siddhartha Chib and Edward Greenberg “Understanding the Metropolis-Hastings Algorithm” In The American Statistician 49.4 [American Statistical Association, Taylor & Francis, Ltd.], 1995, pp. 327–335 URL: http://www.jstor.org/stable/2684568

- [35] T. S. Ferguson and M. J. Klass “A Representation of Independent Increment Processes without Gaussian Components” In The Annals of Mathematical Statistics 43.5 Institute of Mathematical Statistics, 1972, pp. 1634 –1643 DOI: 10.1214/aoms/1177692395

- [36] R.L. Wolpert and K. Ickstadt “Poisson/gamma random field models for spatial statistics” In Biometrika 85.2, 1998, pp. 251–267 DOI: 10.1093/biomet/85.2.251

- [37] Simon Godsill and Yaman Kındap “Point process simulation of generalised inverse Gaussian processes and estimation of the Jaeger integral” In Statistics and Computing 32.1, 2021, pp. 13 DOI: 10.1007/s11222-021-10072-0

- [38] P. A. W Lewis and G. S. Shedler “Simulation of nonhomogeneous Poisson processes by thinning” In Naval Research Logistics Quarterly 26.3, 1979, pp. 403–413 DOI: 10.1002/nav.3800260304

- [39] Peter Carr, Hélyette Geman, Dilip B. Madan and Marc Yor “Stochastic Volatility for Lévy Processes” In Mathematical Finance 13.3, 2003, pp. 345–382 URL: https://EconPapers.repec.org/RePEc:bla:mathfi:v:13:y:2003:i:3:p:345-382

- [40] Simon Godsill, Marina Riabiz and Ioannis Kontoyiannis “The Lévy State Space Model” In 2019 53rd Asilomar Conference on Signals, Systems, and Computers, 2019, pp. 487–494 DOI: 10.1109/IEEECONF44664.2019.9048715

- [41] Jan Rosiński “Tempering stable processes” In Stochastic Processes and their Applications 117.6, 2007, pp. 677–707 DOI: https://doi.org/10.1016/j.spa.2006.10.003

- [42] N. Shephard and O. E. Barndorff-Nielsen “Normal Modified Stable Processes”, 2001 URL: https://ideas.repec.org/p/oxf/wpaper/72.html

- [43] Junichi Imai and Reiichiro Kawai “On finite truncation of infinite shot noise series representation of tempered stable laws” In Physica A-statistical Mechanics and Its Applications 390, 2011, pp. 4411–4425

- [44] G. Samorodnitsky and M. S. Taqqu “Stable non-Gaussian random processes : stochastic models with infinite variance” CRC Press, 1994

- [45] Alan E Gelfand “Gibbs sampling” In Journal of the American statistical Association 95.452 Taylor & Francis, 2000, pp. 1300–1304

- [46] O. Barndorff-Nielsen, J. Kent and M. Sørensen “Normal Variance-Mean Mixtures and z Distributions” In International Statistical Review / Revue Internationale de Statistique 50.2 [Wiley, International Statistical Institute (ISI)], 1982, pp. 145–159 URL: http://www.jstor.org/stable/1402598

- [47] Wessel P. Bruinsma, Martin Tegnér and Richard E. Turner “Modelling Non-Smooth Signals With Complex Spectral Structure” In Proceedings of the 25th International Conference on Artificial Intelligence and Statistics, Proceedings of Machine Learning Research PMLR, 2022 eprint: https://arxiv.org/abs/2203.06997

- [48] Hadley Wickham “ggplot2: Elegant Graphics for Data Analysis” Springer-Verlag New York, 2016 URL: https://ggplot2.tidyverse.org

- [49] Peter Whittle “Stochastic-processes in several dimensions” In Bulletin of the International Statistical Institute 40.2 INT STATISTICAL INSTITUTE 428 PRINSES BEATRIXLAEN, VOORBURG, NETHERLANDS, 1963, pp. 974–994

- [50] T. H. Rydberg “The normal inverse Gaussian Lévy process: simulation and approximation” In Communications in Statistics. Stochastic Models 13.4 Taylor & Francis, 1997, pp. 887–910 DOI: 10.1080/15326349708807456

- [51] O. E. Barndorff-Nielsen “Processes of normal inverse Gaussian type” In Finance and Stochastics 2.1, 1997, pp. 41–68 URL: https://ideas.repec.org/a/spr/finsto/v2y1997i1p41-68.html

- [52] E Eberlein and E. A. Hammerstein “Generalized Hyperbolic and Inverse Gaussian Distributions: Limiting Cases and Approximation of Processes” In Seminar on Stochastic Analysis, Random Fields and Applications IV Basel: Birkhäuser Basel, 2004, pp. 221–264

- [53] Malte Kuss and Carl Rasmussen “Gaussian Processes in Reinforcement Learning” In Advances in Neural Information Processing Systems 16 MIT Press, 2003 URL: https://proceedings.neurips.cc/paper/2003/file/7993e11204b215b27694b6f139e34ce8-Paper.pdf

- [54] Yaakov Engel, Shie Mannor and Ron Meir “Reinforcement Learning with Gaussian Processes” In Proceedings of the 22nd International Conference on Machine Learning, ICML ’05 Bonn, Germany: Association for Computing Machinery, 2005, pp. 201–208 DOI: 10.1145/1102351.1102377

- [55] Marc Peter Deisenroth, Dieter Fox and Carl Edward Rasmussen “Gaussian Processes for Data-Efficient Learning in Robotics and Control” In IEEE Trans. Pattern Anal. Mach. Intell. 37.2 USA: IEEE Computer Society, 2015, pp. 408–423 DOI: 10.1109/TPAMI.2013.218

- [56] Finale Doshi-Velez and Been Kim “Considerations for evaluation and generalization in interpretable machine learning” In Explainable and interpretable models in computer vision and machine learning Springer, 2018, pp. 3–17