Time Consistency

for Multistage Stochastic Optimization Problems

under Constraints in Expectation

Abstract

We consider sequences — indexed by time (discrete stages) — of families of multistage stochastic optimization problems. At each time, the optimization problems in a family are parameterized by some quantities (initial states, constraint levels…). In this framework, we introduce an adapted notion of time consistent optimal solutions, that is, solutions that remain optimal after truncation of the past and that are optimal for any values of the parameters. We link this time consistency notion with the concept of state variable in Markov Decision Processes for a class of multistage stochastic optimization problems incorporating state constraints at the final time, either formulated in expectation or in probability. For such problems, when the primitive noise random process is stagewise independent and takes a finite number of values, we show that time consistent solutions can be obtained by considering a finite dimensional state variable. We illustrate our results on a simple dam management problem.

Keywords:

Multistage Stochastic Optimization; Time Consistency; Constraints in Expectation; Dynamic Programming

1 Introduction and motivation

The notion of time consistency has been introduced in the field of Economics [11], and developed in the context of risk measures [1, 14, 7, 6]. It has been studied in stochastic optimization, both from the stochastic programming [16, 13] and from the Markov Decision Process [15] points of view. Loosely speaking, time consistency means that strategies obtained by solving the problem at the very first stage do not have to be questioned later on. This definition has been used in [5] to establish links between the concept of state variable and the notion of time consistency. The aim in [5] was to highlight the role of information in time consistency. For example, considering a standard multistage stochastic optimization problem solvable by dynamic programming, it was shown that adding a probabilistic constraint involving the state at the final instant of the time span invalidates the time inconsistency property, in the sense that optimal strategies based on the usual state variable have to be reconsidered at each time stage. It was also shown that it was possible to devise an appropriate state variable, namely the probabilistic distribution of the state variable rather than the state variable itself, to formulate an equivalent problem enjoying the time consistency property. But this state is an infinite dimensional one, so that dynamic programming is usually not implementable. The aim of this article is to give deeper insights into the results established in [5] and to show that it is possible to regain time consistency on such problems by using an extended finite dimensional state variable.

The paper is organized as follows. In Sect. 2, we introduce the notion of universal solution for a family of optimization problems, and we define the notion of time consistency for a sequence of families of optimization problems. Then, we revisit the setting of a discrete time multistage stochastic optimization problem in the standard formulation, and we show that our definition of time consistency applies in this case. In Sect. 3, we add an expectation constraint on the final state to the standard multistage stochastic optimization problem, and we define families of optimization problems parameterized by both the initial state and the level of constraint. We prove that the feedback strategies — obtained by dynamic programming on an extended problem formulation with additional state and control variables — are time consistent. In Sect. 4, we present a toy problem for managing a dam subject to a final constraint in probability, and we give results obtained using the extended formulation. Finally, we draw some conclusions in Sect. 5.

2 Time consistency and multistage stochastic optimization

In §2.1, we introduce the notion of universal solution of a family of optimization problems and the notion of time consistency of a sequence of controls for an optimization data set. In §2.2, we show how these two notions apply in multistage stochastic optimization.

2.1 Universal solutions and time consistency

We start with general considerations on universal solutions and time consistency, before moving to more formal statements.

In optimization, the most natural notion of universal solution is the following. Let be a set of parameters and be a set of (decision) variables. Let be a family of functions333Adopting usage in mathematics, we follow Serge Lang and use “function” only to refer to mappings in which the codomain is numerical — that is, a set of numbers (i.e. a subset of or , or their possible extensions with ) — and reserve the term “mapping” for more general codomains. indexed by the parameter . An element is a universal solution for the family of functions when . In a different way, the most natural notion of time consistency in (mutistage) optimization is the following. Let be two integers, be the corresponding finite time span, and be a sequence of control sets. We introduce the truncation mapping (projection) at time , that is, and . Then, considering a sequence of functions , with , we say that time consistency holds when, for all ,

We now extend and mix these two notions in the case where the (cost) functions depend on both parameters and time.

Definition 1

We call optimization data set a family , , , , where (with two integers), a sequence of parameter sets, a sequence of control sets, a sequence of cost functions, with .

For any , we call truncated optimization data set at time the optimization data set .

The notion of universal solution for an optimization data set at time is the following.

Definition 2

Let be an optimization data set and let be given. We say that is a universal solution for the data set at time if it satisfies

| (1) |

where, for any , the optimization problem is defined by

| (2) |

The property of time consistency of a sequence of controls for an optimization data set is defined as follows.

Definition 3

Let be an optimization data set and let be a sequence of controls in . We say that the sequence of controls is time consistent for the optimization data set if, for any , the truncated subsequence of controls is a universal solution for the optimization data set at time .

Otherwise stated, given a universal solution for the data set at initial time , time consistency means that the subsequence is a universal solution for the data set at time , for any time .

2.2 Multistage stochastic optimization in the classical case

We study the standard case of a controlled dynamical system influenced by exogenous disturbances. The decision maker has to find strategies to drive the system so as to minimize some objective function over a certain time span.

Let be given a probability space . All random variables and all random processes are defined on , and we denote them using bold letters. We denote by the -field generated by a random variable .

We consider a positive integer and the finite time span , , ,, . We denote by the primitive (or exogenous) noise random process, where each random variable takes values in a measurable space . We denote by the control random process, where each random variable takes values in a measurable space , and by the state random process, where each random variable takes values in a measurable space . We consider a sequence of measurable mappings (dynamics), a sequence of measurable functions (instantaneous cost), and a measurable function (final cost).

The optimization problem we consider below consists in minimizing the expectation of a sum of costs depending on the state, the control and the noise variables over the finite time span . The state variable evolves with respect to the dynamics that depends on the current state, noise and control values. The problem starting at time is

| (3a) | ||||

| s.t. | (3b) | |||

| (3c) | ||||

| (3d) | ||||

By convention, for , the -field is the trivial -field . Under the measurability assumptions made, Problem (3) is well-defined as all functions take extended nonnegative values.

We make the following assumption.

Assumption 1 (Markovian setting)

The noise random variables are independent.

Using Assumption 1, it is well known [2] that there is no loss of optimality in looking for the optimal control at time of Problem (3) as a feedback strategy depending on the state variable , that is, as a measurable mapping (state feedback).

Let us embed Problem (3) in the framework developed in §2.1. For that purpose, we build an optimization data set

| (4) |

The discrete time span is , the sequence of parameter sets is , and the sequence of control spaces is , being the space of measurable mappings (state feedbacks). The sequence of cost functions

is defined by

| with | |||

Thanks to dynamic programming, we obtain the following result. The sequence of optimal strategies of Problem (3), obtained by solving the dynamic programming equation backward in time

| (5a) | ||||

| (5b) | ||||

| with | ||||

| (5c) | ||||

is time consistent, in the sense of Definition 3, for the optimization data set defined in Equation (4). Indeed, letting time be given, we build from the data set the family of optimization problems as in Equation (2), with Problem being

| (6) |

It is clear that Problem coincides with Problem (3). From the Bellman theory, we know that the sequence of strategies obtained by solving the dynamic programming equation (5) is such that, for any , the truncated sequence is an optimal solution of Problem (6) for any initial state . Thus, according to Definition 3, the sequence of controls is time consistent for the optimization data set .

Remark 4

The notion of time consistency crucially depends on the nature of the solutions of the family of optimization problem under consideration. As a matter of fact, consider Problem (3) and its solution in terms of feedback strategies: as already explained, there is no difficulty to apply the truncated sequence to Problem (6) since this truncated sequence is admissible for the problem starting at time . But consider again Problem (3) and its solution in terms of random variables. Problem (6) is equivalent to

| (7a) | ||||

| s.t. | (7b) | |||

| (7c) | ||||

| (7d) | ||||

We note that the truncated subsequence of is not even admissible for Problem 7 as it does not satisfy (7d). Indeed, each for is by construction (see Constraint (3d)) measurable with respect to the -field , , and thus does not satisfy Constraint (7d).

3 Multistage stochastic optimization with a final constraint in expectation

In §3.1, we modify the framework studied in §2.2 by adding to Problem (3) a constraint in expectation involving the final state , which leads to the optimization problem (8) below. In §3.2, we propose a reformulation of Problem (8) involving a finite dimensional state, and an optimization data set (including the initial state and the level of the expectation constraint) for which time consistency holds. In §3.3, we propose a dual problem formulation of Problem (8), and we illustrate the fact that such a reformulation is not time consistent.

3.1 Standard formulation

We use the notations defined in §2.2. We consider a measurable function , For convenience, we denote . The stochastic optimization problem starting at time with a final constraint in expectation at time is

| (8a) | ||||

| s.t. | (8b) | |||

| (8c) | ||||

| (8d) | ||||

| (8e) | ||||

with . Again, Problem (8) is assumed to be well-defined.

Even under the Markovian Assumption 1, the presence of Constraint (8e) makes it difficult to write a dynamic programming equation for solving Problem (8) starting at time . Indeed Constraint (8e) is not a pointwise constraint at the final stage , so that we do not know how to incorporate it easily in the dynamic programming equation. In §3.3, using an indirect way of proceeding, we show that it is possible to obtain an optimal solution of Problem (8) starting at time in terms of feedback strategies depending on the state . But these feedbacks are implicitly parameterized by both the initial state and the constraint level , so that they do not satisfy the time consistency property for a data set in which the parameter at time is the initial state (see §3.3 for further details).

A partial answer to the question of time consistency of the solution of Problem (8) starting at time has been given in [5]. Indeed, as detailed in [5], Problem (8) can be written in an equivalent way as a deterministic distributed optimal control problem in which the state variable is the probability distribution of , the dynamics of which is given by the Fokker-Planck equation. This deterministic problem can be solved by dynamic programming, which thus produces a sequence of strategies (with the mapping defined over probability distributions on and taking values in [3]), which is time consistent for a data set in which the parameter at time is the initial state probability distribution. But these optimal strategies depend on the specific value in the right-hand side of the expectation constraint, and thus have to be recomputed if this value changes. Moreover, the computation of the Bellman functions involves an infinite dimensional state, so that it is generally not tractable.

Our goal is to obtain a solution for Problem (8) starting at time which, on the one hand is computable in practice (that is, involves a finite dimensional state), and on the other hand is time consistent for a data set (to be specified) in which the parameter at time consists of both the initial state and the constraint level . More precisely, we want to compute a solution for Problem (8) starting at time which is optimal for any value of both the initial state in (8b) and the final constraint level in (8e). Moreover, for any , this solution after truncation has to be a universal solution (Definition 2) for the parameters for Problem (8) starting at . As already explained in Remark 4, time consistency is not available for a solution in terms of random variables. We now present a reformulation of Problem (8) involving a finite dimensional state, whose solution in terms of state feedback strategies meets the goal described in this paragraph.

3.2 Formulation with martingale-type constraints

Following the same path as in [4], but in a discrete time context, we show that Problem (8) is equivalent to a multistage stochastic optimization problem subject to an almost sure contraint on the final state (see also [9, 10, 12]). For that purpose, we introduce a new state process and a new control process . The random variables and take their values respectively in spaces and , all identical to the space where is the codomain of the function introduced at the beginning of §3.1: for all . Now, we consider the optimization problem starting at time

| (9a) | ||||

| subject, for all , to dynamic constraints | ||||

| (9b) | ||||

| (9c) | ||||

| to measurability constraints | ||||

| (9d) | ||||

| (9e) | ||||

| to martingale-type constraints | ||||

| (9f) | ||||

| and to almost sure final constraint | ||||

| (9g) | ||||

Note that, in this formulation, the control variable taken at time does not depend on the noise (Decision–Hazard framework), whereas the control variable , also taken at time , does depend on the noise (Hazard–Decision framework). At time , the martingale-type constraint (9f) introduces a coupling between all the realizations of the decision random variable . In the sequel, for all , we denote by the -field generated by the sequence of random variables:

| (10) |

By convention, .

3.2.1 Equivalence with the standard formulation

The link between the multistage stochastic optimization control problem (9) incorporating a martingale-type constraint and the initial problem (8) is given by the following proposition.

Proposition 5

Proof. Let be a solution of Problem (8). We define the random processes and by

| (12a) | |||

| (12b) | |||

The random vector is well defined (hence so is ) and is integrable. Indeed, as the function is assumed nonnegative in §3.1 and using Inequality (8e), we get . As , the random vector is integrable, hence in (12a) is the difference between two random vectors in , hence is well defined, and is integrable.

By construction, the two processes and satisfy the constraints (9c)–(9e)–(9f). Moreover, we have that

| (by (12b)) | ||||

| (by telescoping sum using (12a)) |

and hence, by (8e) and (11), we get that

so that Constraint (9g) is also fulfilled. We deduce that is admissible for Problem (9). Suppose that there would exist a solution of Problem (9) with a strictly lower cost value than . From the dynamics (9c), we would have

so that by repeated uses of (9f). Taking the expectation in (9g) would lead thus to

Then, would be admissible for Problem (8) with a strictly lower cost value than the optimal solution , which contradicts the assumed optimality of . We conclude that is an optimal solution of Problem (9).

Conversely, let be an optimal solution of Problem (9). As shown in the first part of the proof, we have , so that is admissible for Problem (8). Suppose that there would exist a solution of Problem (8) with a strictly lower cost value than . Then, the quadruplet obtained by constructing and by (12) would give a strictly lower cost value for Problem (9) than , which would be absurd. We conclude that is an optimal solution of Problem (8).

Let us make a few comments about Problem (9).

-

•

The nice features of the equivalent formulation (9) of Problem (8) are double. On the one hand, the initial constraint (8e) in expectation is replaced by an almost sure constraint (9g) on the final state, hence paving the way to use dynamic programming to solve Problem (9). On the other hand, the parameter defining the right-hand side of the constraint (8e) in expectation in formulation (8) becomes a component (9c) of the initial state in Problem (9), thus leading to time consistency as a consequence of dynamic programming.

-

•

The conditional expectation can be interpreted as the “perception of the risk constraint (8e)” at time . From the very definition of , we have that

from which we deduce that the control corresponds to the variation of this perception between time and time . The additional state in (9c) is thus the cumulative variation of the risk contraint perception up to time . Therefore, this new added state seems to be the minimal information which has to be added to the standard state in order to recover a dynamic programming principle.

- •

3.2.2 Extended dynamic programming equation and time consistency

The interest of Problem (9) is highlighted by the following theorem.

Theorem 6

Suppose that the primitive noise random process = , , takes a finite number of values, and that the following induction (Bellman equation)

| (13a) | ||||

| (13b) | ||||

is well-defined in the sense that all the functions are measurable, for .

We deduce from Equation (13) that there is no loss of optimality in looking for the optimal control at time of Problem (9) as induced by a measurable mapping , and for the optimal control at time as induced by a measurable mapping .

Let us embed Problem (9) starting at time in the framework developed in §2.1. The finite time span is , the sequence of parameter sets is , the sequences of control spaces are made of two sequences, with the space of measurable mappings defined on and taking values in , and with the space of measurable mappings defined on and taking values in . Notice that there exists an additional set , where the final state of the system takes values, but that this set is not part of the sequence of parameter sets. The sequence of cost functions , with

is defined by

| if , and by | ||||

From the optimization data set and for a given , we build, as in Definition 2, the family of optimization problems , with Problem being

| (14) |

Optimal strategies and obtained by solving for Problem (14) using the dynamic programming equation (13) are such that, for any , and is an optimal solution of Problem (14) for any initial state .

We deduce that solving Problem (9) dy dynamic programming fully answers the goal of time consistency enounced at the end of §3.1. Indeed, for all , the subsequence of optimal strategies is a universal solution for the family of optimization problems (14). By Proposition 5, a solution of Problem induces a solution of Problem (8) starting at time with initial state and final constraint level .

3.3 Formulation with dualized constraint

We finish this section by presenting a way to solve Problem (8) using Lagrangian duality, and we show that the dualized problem does not display time consistency.

3.3.1 Dualized formulation

By dualizing the expectation constraint (8e) in Problem (8) with a given (fixed) multiplier , we obtain the following problem444For the sake of simplicity, we suppose that the function , introduced at the beginning of §3.1, is bounded to ensure integrability in (15a)

| (15a) | ||||

| s.t. | (15b) | |||

| (15c) | ||||

| (15d) | ||||

| By weak duality, we have that the optimal value of this problem is a lower bound of the optimal value of Problem (8) for any value . In some cases, Problems (15) and (8) are equivalent as specified by the following theorem. | ||||

Theorem 7

Proof. The result is a direct consequence of the extension of Everett’s Theorem given in Appendix A.

3.3.2 Discussion about time consistency

Since Problem (15) falls within the standard dynamic programming framework, there is no loss of optimality to look for the optimal controls of Problem (15), and hence of Problem (8), as feedback strategies depending on the state variable .

However, we do not claim that the optimal feedbacks obtained by this argument have any specific properties in terms of time consistency. Indeed, assume as in Theorem 7 that there exists a such that . The parameter implicitly depends on both the initial condition and the constraint level , so that the optimal feedbacks of Problem (15), which are parameterized by , are accordingly implicitly parameterized by the pair and therefore do not satisfy the property of time consistency. Moreover, if we write an optimization problem similar to Problem (15) starting at an initial time with this value

| (16a) | ||||

| s.t. | (16b) | |||

| (16c) | ||||

| (16d) | ||||

there is no reason that the optimal solution of Problem (16) satisfies the constraint , that is, there is no reason to satisfy the relation . Of course, it may exists some such that , but usually .

4 Numerical experiments

We illustrate numerically whether time consistency holds true or not on a simple dam management problem developed in §4.1. In §4.2, we provide a numerical resolution of the problem with dualized expectation constraint (as seen in §3.3). In §4.3, we provide a numerical resolution by extended dynamic programming (as seen in §3.2).

4.1 A dam management problem

We consider here a basic dam model for a management problem. Let denote a positive integer (horizon) and be the optimization time span, and let be a probability space. For any time in , we consider the following real valued random variables:

-

•

, the water storage volume in the dam at the beginning of time interval ,

-

•

, the decided amount of water to be turbinated during time interval , set at the beginning of the time interval , and constrained to belong to an interval ,

-

•

, the amount of water inflow in the dam during time interval .

Let (resp. ) denotes the minimum (resp. maximum) water volume of the dam, and let be the dam volume at time . The decision can be implemented only if there is enough water in the dam, that is, the turbinated water during a time interval cannot exceed the quantity of water present in the dam. Then, the real amount of turbinated water during the time interval is

The maximal dam volume is taken into account by accepting reservoir overflow: if the forthcoming water volume is greater than , then the dam water surplus spills out. The dam dynamics is written accordingly:

The turbinated water during the time interval produces electricity which is sold at a given price . We assume that the sequence of prices is deterministic. The dam revenue to be maximized is thus

Compared to classical dam management model, we do not add an explicit final cost, but we rather constrain the final level of water in the dam at the end of the time span by a risk contraint. Indeed, we consider a probability constraint on the dam water volume at final time , namely

where the water level and the probability level are given real numbers. Ultimately, the problem we have to solve is

| (17a) | ||||

| s.t. | (17b) | |||

| (17c) | ||||

| (17d) | ||||

| (17e) | ||||

| (17f) | ||||

We recall that the probability constraint (17f) can be rewritten as an expectation constraint

| (18) |

where is the Heaviside step function:

We assume that the water inflows are independent random variables with a known probability distribution on the interval .

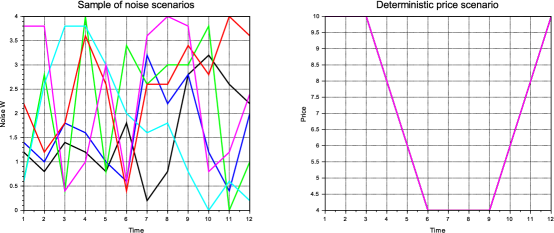

To numerically solve Problem (17), we use the following parameter values: final time ; initial state ; state bounds ; control bounds ; noise bounds ; price sequence ; final dam water level ; required probability level . Moreover, we assume that the variables , and take discrete values within their respective bounds, with respective discretization steps equal to , and . The optimization problem thus corresponds to the control of a discrete state space Markov chain. The discrete probability distribution of each random variable is uniform. We represent on Figure 2 some selected trajectories of the noise process and the sequence of the deterministic prices . These noise trajectories are used in the sequel to illustrate the behavior of the different optimization algorithms.

4.2 Resolution of the problem with dualized expectation constraint

The method used here to solve Problem (17) is based on the duality argument described in §3.3. The probability constraint (17f) is dualized with associated multiplier , which leads, in the cost function (17a), to an added term of the form:

Instead of guessing the parameter value leading to the constraint level , we solve the dual problem

| (19) |

with

| (20a) | ||||

| under constraints (17b)–(17c)–(17d)–(17e). | (20b) | |||

The Uzawa algorithm consists in maximizing the dual function using a projected gradient algorithm. At iteration of the algorithm, knowing the value of the multiplier, we perform the three following steps.

-

•

Compute , that is, solve the minimization problem (20) with ; this minimization is performed using dynamic programming (1-dimensional state variable), hence furnishing optimal feedbacks and optimal state variables .

- •

-

•

Update the multiplier by a projected gradient step:

For the problem under consideration, and despite the potential nonconvexity induced by the final probability constraint (17f), the Uzawa algorithm converges in about 10 iterations, leading to an optimal multiplier value . Once the algorithm has converged, we obtain the optimal feedback sequence by solving Problem (20) by dynamic programming with . Then, we simulate the dynamics of the dam along some noise trajectories using these optimal feedbacks . The results given in Table 1 are obtained by simulating 10,000 noise trajectories, and illustrates the adequacy between optimization and simulation.

| Uzawa optimization | Monte Carlo simulation |

|---|---|

| Bellman value at : | Monte Carlo cost: |

| Required probability: | Estimated probability: |

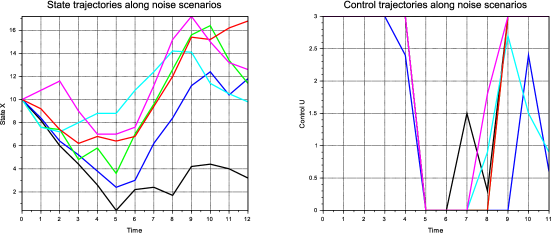

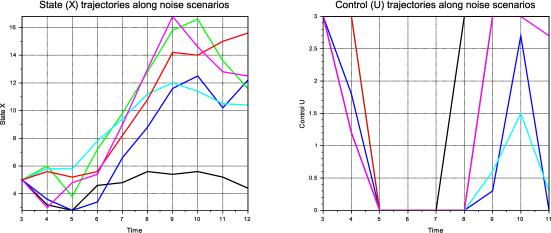

On Figure 3, we represent the dam water level and control trajectories over obtained by simulating with the optimal feedbacks along the noise trajectories depicted on Figure 2. We observe that the optimization “gives up” for certain trajectories (the lowest one to the left of Figure 3) to reach the final level appearing in the constraint in probability: we turbine as much water as possible, leaving the state evolve towards the minimum level . This observation is conform to the expected behavior of an optimization problem with a probability constraint.

Finally, we can use the optimal feedbacks to simulate the dam starting at any initial time from any given initial state . For example starting at time from the initial state and simulating the optimal feedbacks along 10,000 scenarios leads to the results given in Table 2. As expected, the final constraint level reached in this last simulation is not equal to the required level , which illustrates that time consistency does not hold true for the problem formulation with dualized constraint.

| Monte Carlo simulation |

|---|

| Monte Carlo cost: |

| Estimated probability: |

4.3 Resolution by extended dynamic programming

We now use the equivalent formulation of Problem (17) incorporating an additional state process , an additional control process and an almost sure contraint on the final state. As it has been explained in §3.2, the expression of the new dynamics, here 1-dimensional, is

and the form of the final constraint is

The equivalent problem for the case study under consideration is

| (21a) | ||||

| s.t. | (21b) | |||

| (21c) | ||||

| (21d) | ||||

| (21e) | ||||

| (21f) | ||||

| (21g) | ||||

| (21h) | ||||

From Proposition 5, we have that Problems (17) and (21) are equivalent under the condition

Moreover, the special form (21h) of the final constraint makes it possible to bound the variables and . Indeed, from the proof of Proposition 5, we deduce from the expression (12a) of the optimal control with that it is sufficient to search for the control in . Moreover, the optimal state being obtained by a telescoping sum, it is sufficient to search for the state in . Problem (21) can be solved by dynamic programming with the extended state variable , which corresponds to a dynamic programming equation with a 2-dimensional state variable. Then, we simulate the dynamics of the dam — using the same 10,000 noise trajectories as those previously used to obtain Table 1 — with the optimal feedbacks given by dynamic programming with the extended state variable . The associated results are given in Table 3. We observe a good adequacy between optimization and simulation, and we observe that the costs are pretty much identical between Table 1 and Table 3.

| Extended Dynamic Programming | Monte Carlo Simulation |

|---|---|

| Bellman value at : | Monte Carlo cost: |

| Initial state : | Estimated probability: |

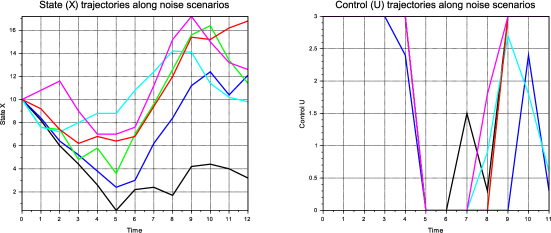

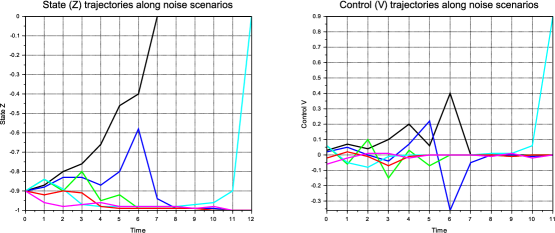

Some simulation trajectories are represented on Figure 4 and Figure 5. Figure 4 gives the same information (dam water level and control trajectories over ) as the one presented for the duality based algorithm in §4.2, whereas Figure 5 depicts trajectories of the optimal state process and the optimal control process . We observe that the results depicted on Figure 3 (duality method) and on Figure 4 (extended dynamic programming method) are very close (with tiny differences induced by numerical resolution), which illustrates the equivalence between Problem (17) and Problem (21).

Finally, we can use the optimal feedbacks obtained when solving Problem (21) by dynamic programming to simulate the dam starting at any initial time from any given initial state . For example starting at time from the initial state — using the same values than those used in §4.2 — and simulating the optimal feedbacks along 10,000 scenarios leads to the results given in Table 4: the final probability level to be reached is by construction equal to , and the Monte Carlo simulation induces a very similar level of probability, which numerically illustrates that the time consistency property is fulfilled. The associated simulation trajectories are represented on Figure 6, using the same noises trajectories as those that had been used to obtain Figure 3.

| Extended Dynamic Programming | Monte Carlo Simulation |

|---|---|

| Bellman value at : | Monte Carlo cost: |

| Initial state : | Estimated probability: |

5 Conclusion

In this paper, we have proposed a formal definition of time consistency for families of optimization problems, by introducing the notion of universal solution. With this, we have shown that — for the class of problems where risk is modeled in the form of constraints in probability or in expectation — the property of time consistency depends on the notion of state that one chooses, which must be suited to the problem studied. In particular, we have shown that, even if the “right” notion of state for the class of multistage stochastic optimization problems with a final expectation state constraint was of infinite dimension (the conditional probability distribution of the state), it is possible to display a state of finite dimension, so that solving the problem by dynamic programming becomes conceivable again.

Acknowledgements:

This paper builds upon results obtained by Pierre Girardeau during his PhD thesis [9], supervised by the three authors.

Appendix A An extension of Everett’s theorem

A result due to Everett (see [8]) links the solution of an optimization problem under constraint and the one of the related dualized optimization problem. We give here a slight extension, which relaxes an assumption of Everett’s theorem.

Let be a set and let be a subset of . Let be a (mulivalued) function. We deal with the following optimization problem

| (22) |

hence subject to a finite number of inequality constraints.

Theorem 9

Let be given. We consider , solution of the optimization problem

| (23) |

and we set . We introduce the set defined by

| (24) |

Proof. Let be a solution of Problem (23) and let . We have

| (by definition of ) | ||||

| (by definition of ) | ||||

| (by definition of in (24)) | ||||

| (as ) | ||||

| (by weak duality) | ||||

| (by (22)) |

Since is such that by definition of the set in (24), we deduce that is admissible for Problem (22), and hence is an optimal solution of this problem.

Appendix B Dynamic programming for the optimization problem involving martingale-type constraints

We prove in §B.2 that Problem (9) can be solved by dynamic programming under the additional assumption that, for any time in , the random variable can take only a finite number of values. The proof is based on a so-called interchange (between minimization and integration) lemma given in §B.1.

B.1 An interchange Lemma

Lemma 10

Let , , , and be measurable spaces, and let be a measurable extended real function. Let be a probability space555All random variables are defined on , and we denote them using bold letters.. Given three random variables , and taking values in , and respectively, we consider the optimization problem defined by

| (25a) | ||||

| (25b) | ||||

| (25c) | ||||

where the minimization is done over couples of random variables and .

We define the function by

| (26) | ||||

where the minimization is done over variables and random variables .

We suppose that the two random variables and are independent, that they each take a finite number of values, and that the random variable is -measurable, that is, . Then, the optimal value of Problem satisfies the following interchange formula

| (27) |

Proof. Letting and be the sets of values taken by, respectively, the random variables and , we denote

| (28) | ||||

| (29) |

Now, since is a -measurable random variable and from the measurability constraints on the random variables and in Equation (25b), we can represent these random variables as follows:

| (30) |

We have just expressed the fact that the set of -measurable random variables taking values in a set is in bijection with the product space if the random variable takes different values.

We start the proof by using Equation (30) to establish the following equalities

| (31a) | ||||

| (31b) | ||||

| (31c) | ||||

All the manipulations below are easy to check, and are justified because all quantities take extended nonnegative values.

Using Equations (30) and (31c), for any -measurable random variable , we have the equivalence

| (35) |

Using again Equations (30) and (31), we obtain that the optimization Problem (25) is equivalent to the following optimization problem

| (36a) | ||||

| (36b) | ||||

The optimization problem (36) trivially splits into a family of independent optimization problems, Problem being defined by

| (37a) | ||||

| (37b) | ||||

and the value of Problem (36) is the weighted sum of the values of the family of problems :

We notice that in (37) is exactly in (26), so that the above equation gives (27).

B.2 Proof of Theorem 6

Proof. For any we consider the minimization Problem defined by666For , the value of Problem is simply .

| (38a) | ||||

| (38b) | ||||

| and, for all , | ||||

| (38c) | ||||

| (38d) | ||||

| (38e) | ||||

| where the sequence of value functions, with , appearing in the cost function (38a) is given by the Bellman recursion (13). To simplify the notation, we denote by the set of random variables and satisfying the constraints (38b) – (38c) – (38d) – (38e). We recall that, by Equation (10), represents the -field generated by for all . | ||||

We are now going to prove, by backward induction, that the value of Problem (9) with is equal to the value of Problem in (38) for any .

First, the value of Problem (9), with , is equal to the value of Problem in (38) for . Indeed, the criterion (38a) in Problem (38), satisfies, for ,

| (as is defined by (13a)) | |||

Thus, we obtain that Problem (38) for is the same as Problem (9) with , the only difference being that the almost sure final constraint (9g) has been moved in the final cost in (38a).

Second, we prove by backward induction that the value of Problem (9) is equal to the value of Problem for any . For this purpose, assuming that the value of Problem (9) is equal to the value of Problem , we prove that it is also equal to the value of Problem . We immediately get that

| (39) | |||

because all quantities take extended nonnegative values.

Now, we apply Lemma 10 to the inner minimization, with , , and with the function , and deduce that

because in (26) is exactly in (13b). Combined with Equation (39), this leads to

We conclude that the value of Problem (9) is equal to the value of Problem , so that we have by induction that the value of Problem (9) is equal to the value of Problem in (38) for any .

References

- [1] P. Artzner, F. Delbaen, J.-M. Eber, D. Heath, and H. Ku. Coherent multiperiod risk-adjusted values and Bellman’s principle. Annals of Operations Research, 152(1):5–22, July 2007.

- [2] D. P. Bertsekas. Dynamic Programming and Optimal Control, Vol. I. Athena Scientific, Belmont, Massachusets, second edition, 2005.

- [3] D. P. Bertsekas and S. E. Shreve. Stochastic Optimal Control: The Discrete-Time Case. Athena Scientific, Belmont, Massachusetts, 1996.

- [4] B. Bouchard, R. Elie, and N. Touzi. Stochastic target problems with controlled loss. SIAM Journal on Control and Optimization, 48(5):3123–3150, 2009.

- [5] P. Carpentier, J.-P. Chancelier, G. Cohen, M. De Lara, and P. Girardeau. Dynamic consistency for stochastic optimal control problems. Annals of Operation Research, 200(1):247–263, 2012.

- [6] P. Cheridito, F. Delbaen, and M. Kupper. Dynamic monetary risk measures for bounded discrete-time processes. Electronic Journal of Probability, 11(3):57–106, 2006.

- [7] K. Detlefsen and G. Scandolo. Conditional and dynamic convex risk measures. Finance and Stochastics, 9(4):539–561, October 2005.

- [8] H. Everett. Generalized Lagrange multiplier method for solving problems of optimum allocation of resources. Operations research, 11:399–417, 1963.

- [9] P. Girardeau. Résolution de grands problèmes en optimisation stochastique dynamique et synthèse de lois de commande. PhD thesis, Université Paris-Est, december 2010. http://www.theses.fr/2010PEST1026.

- [10] G. Granato. Optimisation de lois de gestion énergétiques des véhicules hybrides. PhD thesis, École Polytechnique, december 2012.

- [11] P. J. Hammond. Consistent plans, consequentialism, and expected utility. Econometrica, 57(6):1445–1449, 1989.

- [12] L. Pfeiffer. Two approaches to stochastic optimal control problems with a final-time expectation constraint. Appl Math Optim, 77:377–404, 2018.

- [13] G. C. Pflug and A. Pichler. Time-inconsistent multistage stochastic programs: Martingale bounds. European Journal of Operational Research, 249(1):155–163, 2016.

- [14] F. Riedel. Dynamic coherent risk measures. Stochastic Processes and their Applications, 112(2):185 – 200, 2004.

- [15] A. Ruszczynski. Risk-averse dynamic programming for Markov decision processes. Mathematical Programming, 125:235–261, 2010.

- [16] A. Shapiro. On a time consistency concept in risk averse multistage stochastic programming. Operations Research Letters, 37(3):143 – 147, 2009.