This paper studies the model risk of the Black-Scholes (BS) model in

pricing and risk-managing variable annuities motivated by its wide usage in the insurance industry.

Specifically, we derive a model-free decomposition of the no-arbitrage price

of the variable annuity into the BS model price in conjunction with three out-of-model adjustment terms.

This sheds light on all risk drivers behind the product, that is, spot price, realized volatility,

future smile, and sub-optimal withdrawal.

We further investigate the efficacy of the BS-based hedging strategy

given the market diverges from the model assumptions.

We disclose that the spot price risk can always be eliminated by the strategy

and the hedger’s cumulative P&L exhibits gradual slippage and instantaneous leakage.

We finally show that the pricing, risk and hedging models can be separated from each other

in managing the risks of variable annuities.

Keywords: Valuation Adjustment, Variable Annuities, Model Risk.

The views expressed in this article are the author’s own

and do not represent the opinions of any firm or institution.

1. Introduction

Variable annuities are long-term, equity-linked, and tax-deferred structure products

issued by insurance companies targeting retail customers.

The size of the U.S. variable annuities market is remarkable.

By the end of 2021, variable annuity net assets in the U.S. climbed to 2,130 billion dollars [11],

around two-thirds of the notional amount outstanding

of the entire U.S. OTC equity derivatives market with 3,567 billion dollars [7].

The pricing of variable annuities is a stochastic control problem

without analytical solution in general [2, 9, 10, 14]

and thus is fairly cumbersome even under the classical Black-Scholes (BS) model.

Despite extensive studies on various numerical methods for pricing variable annuities,

little understanding has been delivered in the literature regarding the impact of model misspecification

on the pricing and hedging of variable annuities.

This paper aims to bridge this gap by exploring tentative answers to the following questions

raised from different aspects.

•

From the perspective of pricing, the pricer needs to have a thorough understanding of how to determine

the volatility parameter in the BS model to conservatively price the product

to compensate for the potential model risk.

•

From the hedger’s perspective, a natural question: is it still viable

to conduct BS-Delta-hedging given the market diverges

from the model assumptions?

Does doing so reduce the risk or even escalate the problem?

•

From the viewpoint of risk management, it is important to pinpoint all

risk drivers behind the variable annuity. Then the insurer can decide which

risk to hedge, which risk to outsource, and which risk to take.

In response to the questions above, this paper makes several contributions to the literature.

As the primary contribution, we decompose the model-free no-arbitrage price of the variable annuity

into the BS model price in together with

(i) valuation adjustment for future realized volatility,

(ii) valuation adjustment for future implied volatility smile,

and (iii) valuation adjustment for sub-optimal withdrawal risk;

see Theorems 3.1 and 3.7 in Section 3.

We further show that the BS model enables the insurer to speculate

the volatility risks by marking up/down the volatility parameter.

As the second contribution, we investigate the efficacy of BS-based delta-hedging in the presence of model risk.

We find that the risk caused by the underlying asset’s price change

can always be eliminated by such a classical hedging strategy

regardless of whether the market behaves in accordance with the BS model’s assumptions or not.

Furthermore, there is even a chance that the hedger can benefit from taking the model risk; see Proposition 3.4.

This justifies the use of the BS model as a hedging tool to some extent.

However, such a hedging strategy does not come without any downsides.

We disclose that the hedger’s cumulative P&L exhibits gradual slippage throughout the contract’s lifetime

and instantaneous leakage across each withdrawal date; see Remark 3.5 in the sequel.

As the third contribution, we show that it is viable to separate the risk model from

the pricing model.

Specifically, on the one hand, the insurer may solely use the BS model as an extractor

for the spot price risk with the residual part further decoupled into three extra factors,

i.e., realized volatility, future implied volatility and sub-optimal withdrawal.

Such a way of risk attribution is exhaustive and can be constantly monitored;

see Remark 3.10.

On the other hand, the insurer may use a different pricing model to charge the premium

or estimate the hedging costs for the four risk factors.

Finally, we would like to stress that the notion of out-of-model-adjustment is not new

and has been well understood for European options

[1, 3, 5, 8] and cliquets [3].

However, it is a fairly challenging task to find a systematic way to decompose

the model-free price of any exotic derivative product

into a given model price plus adjustments that have financial meanings

and can shed light on different aspects of model risk.

For variable annuities, to the best of the author,

this paper is the first attempt to pursue this route.

The existing results mentioned above cannot be carried over here

because the variable annuity contains some unique risk features, and in particular,

it gives rise to the valuation adjustment for sub-optimal withdrawal risk

that is unseen in other products.

This distinguished risk profile stems from

the stochastic control problem involved in variable annuities.

The remainder of this article is structured as follows.

Section 2 gives a brief recap on the pricing of the variable annuity

as a stochastic control problem.

Section 3 presents the main result of the paper:

the out-of-model adjustment formula.

Section 4 gives numerical studies

and finally Section 5 concludes the paper.

2. Variable Annuities

2.1. Notations

•

Consider a set of equally-spaced withdrawal dates with .

•

Let be the time- value of the state variable associated with the contract (investment account, benefit base, etc) valued in . To ease the notations, in the sequel, we denote shorthand and .

Remark 2.1.

is not necessarily a scalar process. For the clarity of presentation, this paper concentrates on the one-dimensional case, which however is not essential to our argument for proving the main results.

•

Denote as the transition map of the state variable across an event date,

with being the feasible set of the withdrawal policy.

That is,

where is the policyholder’s withdrawal amount at

and is some state-dependent constraint.

•

Between two withdrawal dates, the state variable evolves according to

where is some random driver

(e.g. the cumulative return of the underlying asset over ).

•

Let and be the terminal and intermediate payoff functions, respectively.

•

Let be the risk-free rate and denote by the risk-neutral measure.

Let be the information up to time .

2.2. Bellman Equation – Model-free Case

The pricing of variable annuities is typically formulated as a discrete-time stochastic control problem

and accordingly, the value function at withdrawal time is recursively given by the following Bellman equation:

(2.1)

where

(2.2)

with

and ;

see e.g. [2, 9, 10, 14].

can be thought of as the value of the contract right after the policyholder’s withdrawal at

with the post-withdrawal state .

Between two event dates, the value function satisfies

(2.3)

As a remark, with the convention that the contract inception time is not a withdrawal date, the above equation holds for when .

2.3. Bellman Equation – Black-Scholes Case

In a BS world, the price function of the variable annuity is recursively given by

(2.4)

where

(2.5)

and in between two withdrawal dates solves the following BS-type PDE:

It is worth stressing the difference between and :

the former is a value function and while the latter is a stochastic process

which is not necessarily a function of the state variable due to the existence of other (latent) risk factors generating the filtration .

Similarly, given a realized value of , is still a random variable

(parameterized by ) while is deterministic.

The primary thrust of the article is to characterize the discrepancy between and .

3. Out-of-Model Adjustments

This section is devoted to presenting the main results of the article.

To get some flavours of the problem,

we start with a two-period case in the subsequent Section 3.1.

3.1. Valuation Adjustments

Theorem 3.1(Out-of-Model Adjustments).

Let and denote the BS implied variance of an European option with payoff as of time (see also Definition E.3 in Appendix E).

Suppose the assumptions in Appendix B hold.

Then

(3.1)

where

(3.2)

(3.3)

and denotes the quadratic variation process of .

Remark 3.2(Realized & Implied Volatility Risks).

Theorem 3.1 discloses two different risks that are not priced in the BS model.

•

Realized Volatility Risk The first valuation adjustment (VA) term (3.2) is contributed by the discrepancy between

the BS variance parameter and the realized variance of the underlying.

Should the underlying price behave in accordance with the BS model, this VA term would vanish.

•

Future Smile Risk The second VA term (3.3) is caused by the difference between BS variance

and the implied variance of the European option with payoff

at a future time point .

The latter is determined by the entire volatility smile as of and for this reason,

we refer to this risk source as the future-smile risk.

In an ideal BS world, all European options have the same implied variance and thus this VA term disappears.

To summarize, we have

The two VA terms vanish should the model’s assumptions be satisfied.

Remark 3.3.

Evaluating the two VA terms calls for the knowledge of the true model, which is a formidable task.

Nonetheless, gauging their signs is relatively easier:

(1)

The VA for the future realized volatility risk is positive (resp. negative) if the the BS model variance underestimates (resp. overestimates) the realized variance over ;

(2)

The VA for the future smile risk is positive (resp. negative) if the the BS model variance underestimates (resp. overestimates) the implied variance .

The critical insight from the above is that the

insurer has the freedom of under-pricing or over-pricing the variable annuity by marking up/down the BS variance parameter .

In other words, intentionally or not, should the insure decide to choose the BS model to price the variable annuity,

she essentially speculates the realized volatility and future smile risks.

3.2. P&L Slippage and Leakage

The previous discussion reveals that the BS model fails to price in Gamma and future smile risks.

Next, we study the impact of the use of BS as a hedging tool on the insurer’s cumulative P&L.

Consider the following situation: the BS model is not in line with the market’s dynamics

but the insurer pretends it to be and delta-hedges her exposure to the variable annuity.

Specifically, the hedging strategy is given as follows.

(H1) At time , the insurer sells a variable annuity contract and chooses to value it by the BS model with a BS variance parameter . Accordingly, the premium received by the issuer is which is used to finance her hedging strategy.

(H2) Over the time horizon , the insurer continuously delta-hedges her exposure with two commitments:

(C1) the insurer freezes the variance parameter

because the implied volatility of the variable annuity is not quoted in the market;

(C2) for the same reason as the above, the insurer always marks her position to the model price .

(H3) At time , the variable annuity degenerates into an European option whose implied variance

can be observed from the market quotes for vanilla options111

Given a market for vanilla call options with all strikes,

one can pin down the BS implied variance/volatility for any European option with convex payoff [3]..

Accordingly, the insurer can mark the value of the contract be .

Now the problem of interest is to understand how the insurer’s mark for P&L varies as time progresses from to . The following proposition sheds light on this.

Proposition 3.4.

Suppose the assumptions in Appendix B hold.

Let be the value of the insurer’s hedges as of time .

The cumulative profit and loss marked by the insurer is given by

(3.4)

where

(3.5)

Furthermore, the cumulative profit and loss realized by the insurer as of is given by

(3.6)

where

(3.7)

Remark 3.5(P&L Slippage and Leakage).

Proposition 3.4 discloses two P&L impacts with different natures brought by the use of the BS-based hedging strategy.

•

Slippage Before time , as time progresses,

the insurer can gradually feel the mis-hedging of the BS model

because she can observe exposure to Gamma risk (Eq. (3.5)) in her marked P&L (Eq. (3.4))

which shouldn’t have come into place had the market behaved in accordance with the BS model.

We refer to the term (3.5) as the P&L slippage

to stress this incremental bleeding.

•

Leakage Recall from (H3) that at time the insurer can observe the fair market price of the variable annuity and her final P&L reads (3.4).

By comparing Eqs. (3.4) and (3.4), the insurer sees a sudden mark up/down for her position across

caused by the second term in Eq. (3.6). To stress this discontinuity in P&L(t) across , we refer to the term (3.7) as the P&L leakage.

Remark 3.6.

In the classical BS paradigm,

the model’s assumptions are supposed to be fulfilled by the market

and thus the Gamma risk enters into the hedger’s P&L only when the hedging frequency is discrete.

Proposition 3.4 reveals that the Gamma exposure is generally inevitable

even if we assume continuous hedging due to the presence of model risk.

In a more realistic situation, we shall expect extra P&L and valuation adjustment terms taking into account

the impact of discrete re-balancing.

The conclusion of Proposition 3.4 is not surprising:

we have shown in Theorem 3.1 that the fair price contains two VA terms on top of the BS model price,

which implies that if the insurer only charges the BS model price as the premium

it might overestimate/underestimate the entire hedging cost as reflected by the P&L slippage and leakage terms illustrated in the above.

Nevertheless, the insurer does not necessarily lose/make money depending on the relative order between the parameter

and implied/realized variance; see Remark 3.3.

3.3. Multi-period Case

The following theorem generalizes Theorem 3.1 to the case with multiple withdrawal dates.

where are given in Eqs. (E.6)–(E.8) of Appendix E.

Remark 3.8(Sub-optimal Withdrawal Risk).

With respect to the two-period case (see Eq. (3.1)),

Eq. (3.8) discloses one extra valuation adjustment term

which stems from the fact that the optimal withdrawal strategy associated with

the “true” model is only suboptimal under the BS model; see Eq. (E.8)

for a concise definition of the sub-optimal withdrawal risk.

Generally speaking,

it is not surprising that the optimal withdrawal strategy of any given model

is not in line with the one observed from the market due to the existence of model risk.

Such a disagreement has been attributed to the irrationality of the policyholder

or tax considerations in the literature; see

[6, 13, 12] and the references therein.

This article provides an alternative explanation, that is, the model mis-specification risk.

The following corollary directly follows from the above theorem.

where the expressions of and are relegated to Definition E.5

of Appendix E for the clarity of presentation.

Remark 3.10(Exhaustive Risk Attribution).

The primary message delivered by the above corollary is that

the P&L of the variable annuity can be exhaustively attributed to four drivers

(i) spot price222To be precise, we refer

to P&L that is solely caused by the first-order-change of the underlying asset price

as the spot price risk. The second-order effect is attributed to the future realized volatility.,

(ii) future realized volatility, (iii) future implied volatility

and (iv) sub-optimal withdrawal.

It is also worth noting the last two terms are missing in the classical attribution analysis

based on the BS greeks.

Generally speaking, for any given model,

should it diverge from the market,

the classical greeks-based-attribution is incomplete, which is reflected by unexplained profit/loss.

3.4. Separating Risk, Hedging, and Pricing Models

Now we comment on the impacts of the model risk of the BS model from several aspects.

•

Firstly and foremost, Remark 3.3 reveals that

the BS model enables the insurer to speculate the future implied and realized volatility

via marking up/down the parameter .

This distorts the incentives of the insurer and is undesirable from the regulator’s perspective.

•

From the perspective of pricing, the problem with the BS model is more about its lack of flexibility.

There is only one degree of freedom (the parameter ) that can be utilized by the pricer to

mark up/down the realized volatility and future smile risks simultaneously.

In other words, the insurer is not able to control the two risks separately

despite that realized and implied volatility don’t behave in line with each other in reality [3]

and have different impacts on the insurer’s P&L (see Remark 3.5).

•

From the viewpoint of hedging, the hedger’s perception of the P&L is misled by the BS model.

We recall from Remark 3.5

that the presence of the future smile risk causes an instantaneous jump across the contract event date.

This is very annoying:

it is likely that the hedger’s positive cumulative P&L is suddenly skewed up by leakage term (3.7).

•

Remark 3.10

reveals that the BS model can be used as a decent tool for risk attribution analysis.

Specifically, it precisely pinpoints all risk drivers behind the variable annuity;

see Remark 3.10.

4. Numerical Examples

This section conducts some numerical experiments to study the efficacy of the BS-delta-hedging

given the market does not respect the BS model assumptions.

4.1. Contract Specification

The specification of contract-related payoff functions is relegated to Appendix A

for the clarity of the presentation.

We confine our attention into the two-period case considered by Section 3.1 with .

4.2. Dynamics of the Market

For illustration purposes, we postulate the market follows the Heston-type stochastic volatility model given by

with .

We adopt the Heston parameters given in the following table.

Table 1. Heston parameters used for numerical experiments.

Parameter

Value

0.0

0.1

0.1

0.04

0.04

-0.69

In our numerical experiments,

we simulate the Heston process at equally-spaced time points

with , and step size .

Further denote as the value of in -th simulated path.

In the consequent numerical experiments, we simulate 100 scenarios in total,

which is sufficient for illustrating the main conclusion.

4.3. Efficacy of the BS-Hedging

We recall from Eqs. (3.4) and (3.6) that

the cumulative P&L of the BS-hedging strategy is given by

where

Then the cumulative P&L at time along the -th simulated path is approximately given by:

where is recursively defined by

with and

see Eq. (A.1) of Appendix A

for the expression of .

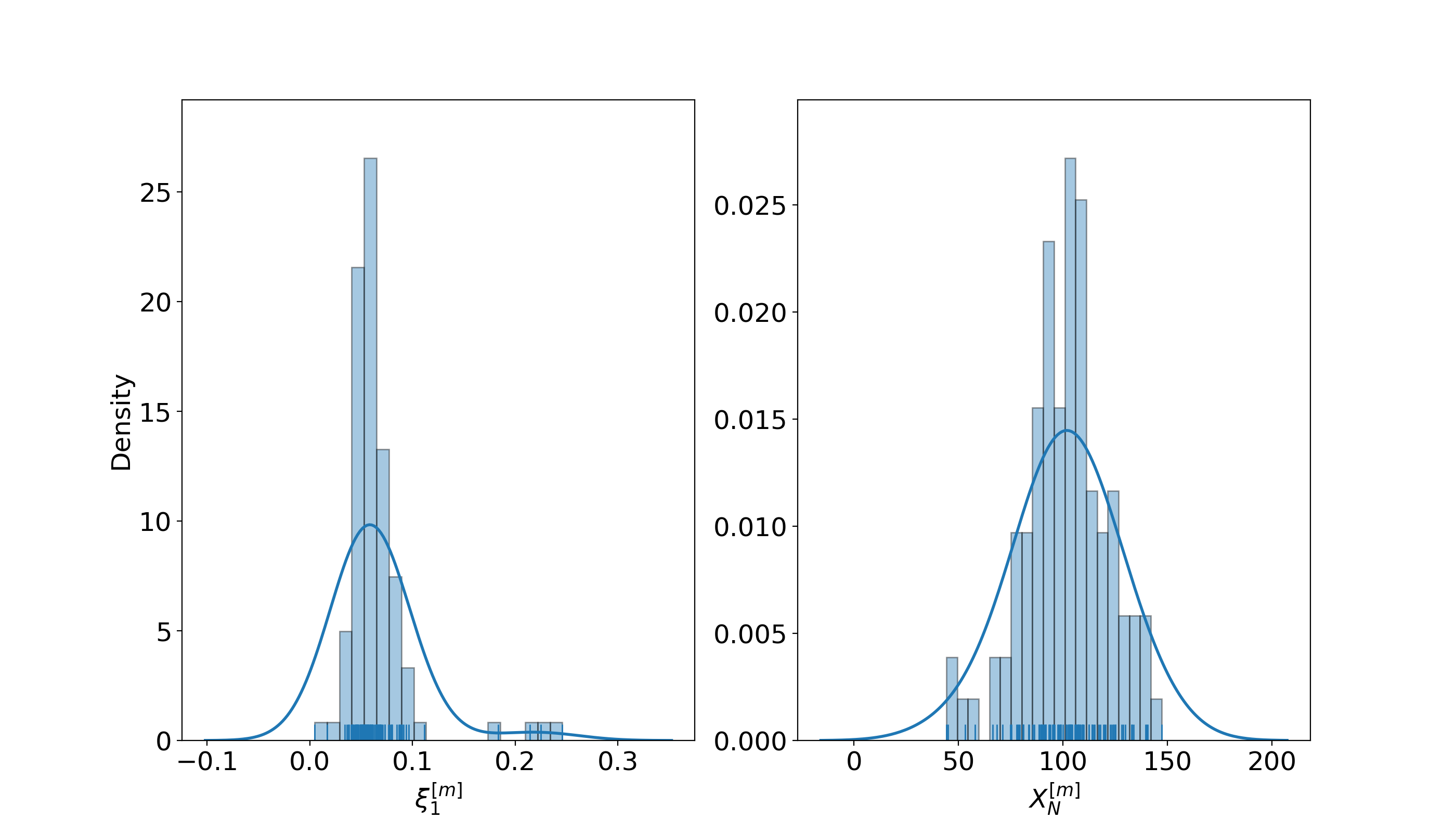

Figure 1 displays the histograms of the simulated values

of the BS implied variance of the contract

and the underlying asset price at respectively.

We can see that the implied variance at a future time point is random

under the Heston model:

it can lie arbitrarily above or below any given BS variance parameter

and thus introduces the future smile risk and P&L leakage; see Remark 3.5.

Figure 1. Histograms of implied variance of the contract and the underlying price at .

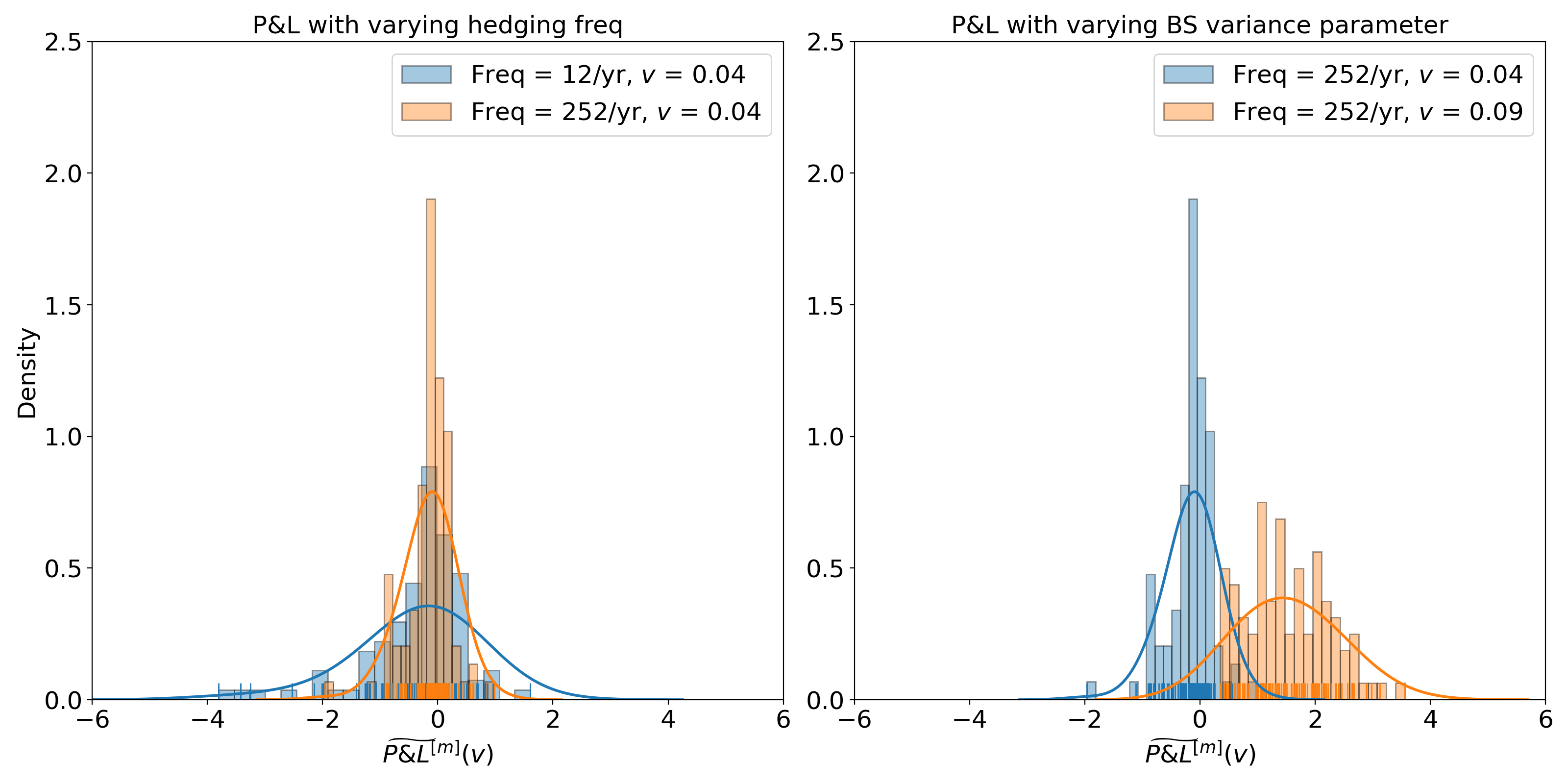

Figure 2 plots the histograms of the cumulative P&L at

with varying hedging frequency (daily vs monthly) and BS variance parameter

( vs ).

We have two observations. Firstly, as one increases the hedging frequency

from monthly to daily, the P&L becomes more stable,

as reflected by the more spiked shape of the density plot.

Such a variance reduction is due to the fact that the BS-Delta-hedging eliminates the spot price risk.

Secondly, as the hedger marks up the BS variance parameter ,

it is more likely to get positive cumulative P&L.

This is in line with the conclusion of Proposition 3.4:

both P&L leakage and slippage terms are monotone in ;

furthermore, they are positive should dominate the implied and realized variance over the course of the hedging.

Figure 2. Histograms of the cumulative P&L at .

To sum up, despite that the market disagrees with the BS model assumptions,

the hedger can always stabilize her final P&L by increasing hedging frequency

and even benefit from the mis-hedging (model risk) by speculatively marking up the BS variance parameter.

5. Concluding Remarks

We have shown that the fair value of the variable annuity can be decomposed into four parts

(i) BS model price,

(ii) valuation adjustment for future realized volatility,

(iii) valuation adjustment for future implied volatility smile,

(iv) and valuation adjustment for sub-optimal withdrawal risk.

This discloses that the risk of the variable annuity

can be exhaustively attributed to four corresponding factors.

The insurer can conservatively price (ii) and (iii) simultaneously

by marking up the variance parameter

but has no control over (iv).

This paper also shows that the impact of model risk on the cumulative P&L of

the classical BS-based-hedging strategy

is reflected in two different ways: gradual slippage and instantaneous leakage.

There is even a chance that the hedger can benefit from taking the model risk.

Furthermore, the P&L caused by spot price can always be eliminated by the strategy,

which is immune to the model risk.

It is worth stressing that the primary thrust of this article is delineating the risk profile of variable annuities

rather than promoting or criticizing the BS model.

The BS model plays the role of an extractor for the spot price risk

and our out-of-model adjustment formula further anatomizes the residual model risk.

Pinpointing all risk drivers paves the way to systematically access the advantages and limitations of more advanced models

(local volatility model, stochastic volatility model, stochastic local volatility model, etc)

in pricing and risk-managing variable annuities.

Specifically, one may scrutinize how a given model prices in each risk segment

and accordingly, underprice/overprice the product as a whole.

This is left as a future research avenue.

Generally speaking, one may decompose the model-free price into any given model price

plus out-of-model adjustments.

It will be fruitful to explore different decomposition formulas on top of different models.

However, the more fundamental question is:

does such a decomposition decouples the risks with different natures

and allow the pricer to control them individually by marking up/down some free parameter?

Our choice of the BS model as the extractor does not have no special significance.

A more fancy model does not necessarily give better pricing and risk-management of

the variable annuity due to the less transparency of the model risk.

Putting it another way, the simpler the model is, the better grasp of the model risk is.

Acknowledgements

The author is grateful to the inspiring discussions with Dr. Xi Tan and Professor Chengguo Weng.

For the clarity of illustration,

we consider a simple variable annuity contract specified as follows.

Transition of investment account across withdrawal date Across each withdrawal date, the investment account balance is reduced

by the withdrawal amount and accordingly,

Intermediate payoff function Given the withdrawal amount at , the policyholder’s reward is given by

where is withdrawal penalty.

Terminal payoff function At maturity, the policyholder can receive the balance of the investment account

or the guaranteed withdrawal amount, whichever is larger.

Thus, the terminal payoff is given by

Throughout Section 4, we adopt the set of parameters in the table below.

Table 2. Product parameters used for numerical experiments

where denotes the BS put option price with spot price ,

strike , time-to-expiry and BS-variance parameter .

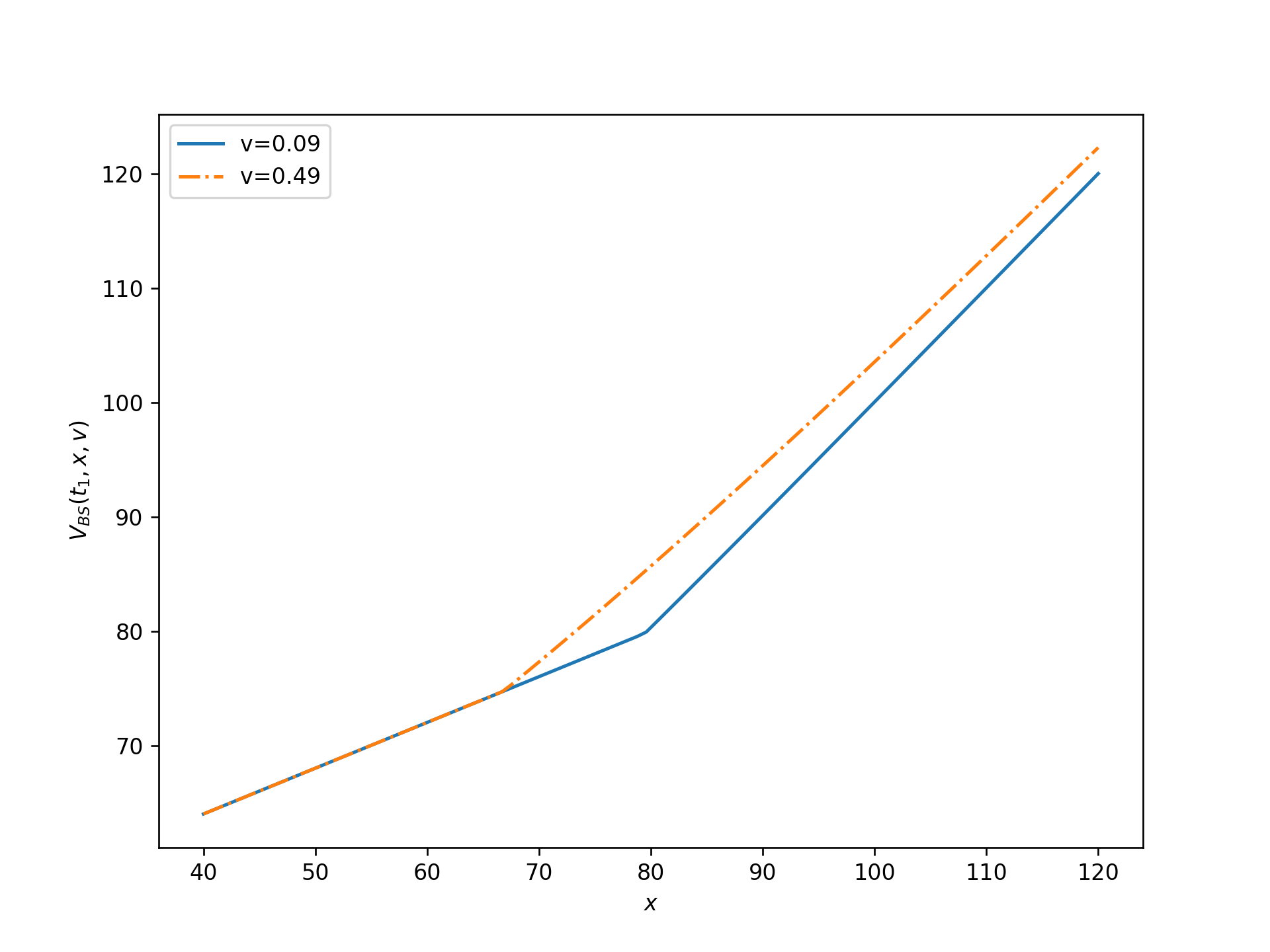

The plot of the value function is displayed in Figure 3

from which we can see how sensitive the function is to the BS variance parameter.

When the market does not follow the BS model, we recall from Proposition 3.4

that the fair value of the contract is given

by the above BS value function with replaced by the prevailing implied variance at

which can lies arbitrarily above or below .

To avoid direct evaluation of the derivative of , we adopt the likelihood ratio method

[4] to compute

(A.1)

where

and denotes the expectation under which

Figure 3. BS value function with varying variance parameters.

Appendix B Technical Assumptions

Throughout this paper, we impose the following technical assumptions.

Consider a filtered probability space

satisfying the usual conditions.

Assumption B.1.

where

is the set of admissible controls.

Assumption B.2.

There exists s.t.

the supremum in Bellman equation (2.1) is attained at for .

Assumption B.3.

The investment account of the variable annuity is tied to a tradable asset

and accordingly, its value between two consecutive withdrawal dates is given by

where is the price process of the underlying asset.

Assume that is a continuous semi-martingale

and does not pay dividends.

Then we have

(B.1)

with being the risk-neutral measure.

Remark B.4.

The zero-dividend assumption can be removed by replacing in Eq. (B.1)

by with being the dividend yield.

Assumption B.5.

The value function under the BS model defined via Eq. (2.4)

is convex in . Specially, when , the terminal payoff is a convex function.

Remark B.6.

The above assumption ensures the BS-implied variance in the sequel Definition

E.3 is well-defined.

The BS value function of the variable annuity is convex under very mild conditions;

see e.g. [2, 9, 10, 14].

The convexity is a sufficient condition for the existence of the implied variance

and thus can be further relaxed.

Let be the value of the insurer’s hedges as of time .

In accordance with the setup of the hedging strategy (H1)–(H3), the hedges are made up of the underlying asset and cash position :

which satisfies the self-financing condition:

(D.1)

and the initial cost constraint .

In the sequel, we prove Eqs. (3.4) and (3.6) consequently.

The first equality of Eq. (3.4) follows by (H2).

By Itô’s lemma, we get

Furthermore, combining Eqs. (E.11) and (E.12) implies

that .

Putting (a)-(c) together implies Eq. (E.13) holds for .

(2)

Now by induction we assume Eq. (E.13) holds for .

Plugging Eq. (E.13) into Eq. (2.2) gives

where the last equality follows by

Eqs. (E.3), (E.10) and (E.12).

The above display in conjunction with Eq. (2.1) gives

where the second equality is by Eq. (E.4)

and the last equality follows by Eqs. (E.9) and (E.11)

in together with Lemma E.4.

This proves Eq. (E.13) for .

The above display in conjunction with Eq. (E.14) proves Theorem 3.7.

∎

References

[1]

Leif BG Andersen and Vladimir V Piterbarg.

Interest Rate Modeling Volume III: Products and Risk

Management.

Atlantic Financial Press, 2010.

[2]

Parsiad Azimzadeh and Peter A Forsyth.

The existence of optimal bang-bang controls for gmxb contracts.

SIAM Journal on Financial Mathematics, 6(1):117–139, 2015.

[3]

Lorenzo Bergomi.

Stochastic volatility modeling.

CRC press, 2015.

[4]

Mark Broadie and Paul Glasserman.

Estimating security price derivatives using simulation.

Management science, 42(2):269–285, 1996.

[5]

Peter Carr and Dilip Madan.

Towards a theory of volatility trading.

Option Pricing, Interest Rates and Risk Management, Handbooks in

Mathematical Finance, 22(7):458–476, 2001.

[6]

Zhang Chen, Ken Vetzal, and Peter A Forsyth.

The effect of modelling parameters on the value of gmwb guarantees.

Insurance: Mathematics and Economics, 43(1):165–173, 2008.

[8]

Jim Gatheral.

The volatility surface: a practitioner’s guide.

John Wiley & Sons, 2011.

[9]

Yao Tung Huang and Yue Kuen Kwok.

Regression-based monte carlo methods for stochastic control models:

Variable annuities with lifelong guarantees.

Quantitative Finance, 16(6):905–928, 2016.

[10]

Yao Tung Huang, Pingping Zeng, and Yue Kuen Kwok.

Optimal initiation of guaranteed lifelong withdrawal benefit with

dynamic withdrawals.

SIAM Journal on Financial Mathematics, 8(1):804–840, 2017.

[12]

Christian Knoller, Gunther Kraut, and Pascal Schoenmaekers.

On the propensity to surrender a variable annuity contract: an

empirical analysis of dynamic policyholder behavior.

Journal of Risk and Insurance, 83(4):979–1006, 2016.

[13]

Thorsten Moenig and Daniel Bauer.

Revisiting the risk-neutral approach to optimal policyholder

behavior: A study of withdrawal guarantees in variable annuities.

Review of Finance, 20(2):759–794, 2016.

[14]

Zhiyi Shen and Chengguo Weng.

Pricing bounds and bang-bang analysis of the polaris variable

annuities.

Quantitative Finance, 20(1):147–171, 2020.