Splitting Method for Support Vector Machine with Lower Semi-continuous Loss

Mingyu Mo, Qi

Abstract:

In this paper, we study the splitting method based on alternating direction method of multipliers for support vector machine in reproducing kernel Hilbert space with lower semi-continuous loss function. If the loss function is lower semi-continuous and subanalytic, we use the Kurdyka-Lojasiewicz inequality to show that the iterative sequence induced by the splitting method globally converges to a stationary point. The numerical experiments also demonstrate the effectiveness of the splitting method.

Keywords: support vector machine, lower semi-continuous loss function, reproducing kernel Hilbert space, splitting method, Kurdyka-Lojasiewicz inequality.

Mathematics Subject Classification: 68Q32, 49J52.

1 Introduction

Support vector machine (SVM) is a well-known model for binary classification in machine learning. The basic idea of SVM is to find a function in a kernel-based function space to achieve the smallest regularized empirical risk such that the classification rule is constructed by the decision function and the sign function. The SVM is already achieved in reproducing kernel Hilbert spaces (RKHS) and convex loss functions (See [24]). After the success of the SVM in the RKHS with the convex loss functions, people continue to investigate whether the SVM in the RKHS can be feasible for nonconvex loss functions. Recently, different nonconvex loss functions are proposed and used for traditional SVM (see [6, 9, 15, 18, 19, 22, 29]). But the algorithms of the SVM in the RKHS with the general nonconvex loss function are still lack of study. If the loss function is convex, then it is lower semi-continuous (L.S.C.) while the lower semi-continuity can not imply the convexity. Moreover, the SVM in the RKHS with the L.S.C. and nonconvex loss functions can perform better than the convex loss functions in manny cases (see Section 5). Currently, people are most interested in the infinite-dimensional spaces for applications of machine learning such that the learning algorithm can be chosen from the enough large amounts of suitable solutions. In this paper, we consider the SVM in the infinite-dimensional RKHS with the L.S.C. loss function (See Section 2).

To construct the SVM in the RKHS, we will find a minimizer from Optimization (2.1). In this paper, we show that Optimization (2.1) has a minimizer in a finite-dimensional space spanned by the reproducing kernel basis related to the training data points. Thus Optimization (2.1) can be equivalently transferred to a finite-dimensional Optimization. Based the equivalent Optimization, we discuss the splitting method for Optimization (2.1) based on alternating direction method of multipliers (ADMM). By the splitting method, we obtain two subproblems which are computable easily. Moreover, the convergence of ADMM is already guaranteed well for the convex Optimizations (see [5]) and some special nonconvex Optimizations by the Kurdyka-Lojasiewicz (KL) property (see [11, 14]). To complete the proof, we reexchange the convergence theorems in [11, 14] and verify the convergence of the splitting method for Optimization (2.1) if the loss function is L.S.C. and subanalytic for the global convergence to a stationary point and the error bound.

This paper is organized as follows. We introduce the notations and preliminary materials of the SVM in Section 2. Next, we study the representer theorem for the L.S.C. loss functions and discuss how to solve Optimization (2.1) by the splitting method in Section 3. Moreover, we discuss the global convergence and convergent rates of splitting method for L.S.C. and subanalytic loss function in Section 4. Finally, we look at the numerical examples of the different loss functions and RKHSs for the synthetic data and the real data in Section 5.

2 Notations and Preliminaries

In this section, we review some notations and preliminaries of SVM. We denote the set of positive integers as and the -dimensional Euclidean space as respectively. For the sample space and the label space , the training data is composed of input data and output data . We will find a mapping related to such that is a good approximation of the response to an arbitrary . For the rest of this paper, the symbol always refers to column vector, so denotes row vector.

The SVM is an important class of mappings . The basic idea of traditional SVM is to find a hyperplane in that classifies all the training data in correctly and creates the biggest margin. Thus we construct by the hyperplane and the sign function. However, the hyperplane to separate may not exist and we can only accept the hyperplane that misclassifies some training data. To help us define what we mean by ”good”, we introduce the loss function of the SVM to find the hyperplane and its equivalent optimization is a optimization with an offset term in a RKHS consisting all linear functions on with the linear reproducing kernel (See [24, 1.3 History of SVMs and Geometrical Interpretation]). Obviously, the RKHS is a finite-dimensional kernel-based function space which is isometrically isomorphic to . Generally speaking, the SVM is to find a function on that achieves the smallest regularized empirical risk in a given RKHS such that the classification rule is constructed by the decision function and the sign function.

Since the RKHS is only a finite-dimensional space, in the rest of this paper, we shall discuss the SVM in some special infinite-dimensional spaces with different kinds of kernels. Generally speaking, a Hilbert space of functions equipped with the complete inner product and the reproducing kernel is called an RKHS if it satisfies the following two conditions

(i) for all ,

(ii) for all and all .

In particular, for any , the corresponding norm and the corresponding metric are complete. On the other hand, the reproducing kernel of an RKHS is uniquely determined. By [26, Theorem 10.3 and 10.4], is symmetric and positive definite (see [24, Definition 4.15]). In some cases, can be symmetric and strictly positive definite, for instance, Gaussian kernels, Matérn kernels and so on. In particular, the value can often be interpreted as a measure of dissimilarity between the input values and .

For more flexible kernels such as those of Gaussian kernels, which belong to the most important kernels in practice, the offset term has neither a known theoretical nor an empirical advantage. In addition, the theoretical analysis is often substantially complicated by offset term. Thus, we decide to exclusively consider the SVM in the RKHS without an offset term. Let us fix such an RKHS and a real number , the SVM in the RKHS finds a minimizer of

(2.1)

where is a loss function and is the regularization term used to penalize with the large RKHS norm. In the following, we will interpret as the loss of predicting by if is observed, that is, the smaller the value is, the better predicts in the sense of . We denote the minimizer of Optimization (2.1) as . Next we use to construct the SVM in the RKHS as follows.

(2.2)

Moreover, the classification rules constructed by different minimizers of Optimization (2.1) have no difference in performance. In conclusion, we just need to find a minimizer of Optimization (2.1). Next we discuss the solution of Optimization (2.1) and splitting method for Optimization (2.1) in Section 3.

3 Representer Theorem and Splitting Method

In this section, we discuss how to solve Optimization (2.1) by splitting method. First we discuss the solution of Optimization (2.1). The loss function is the key factor of the SVM in the RKHS, because it not only determines the sensitivity to the noise of training data but also affects the sparsity of the SVM in the RKHS. For binary classification, the most straightforward loss function is the 0-1 loss function, which is an ”ideal” loss function (see [7]). However, 0-1 loss function is bounded, nonconvex and L.S.C. but discontinuous. Trying to optimize 0-1 loss function directly leads to a L.S.C. and nonconvex optimization problem which is unable to deal with by traditional optimization theory and algorithm. Therefore, a number of surrogate loss functions are proposed in the literature, such as convex loss function, that is, is a convex function for all and . Besides convexity, we can define other loss functions in a similar way, such as continuity, smoothness, lower semi-continuity, etc. Specially, if is convex, then is L.S.C. But the lower semi-continuity can not imply the convexity.

Generally speaking, loss functions can be divided into two categories: convex loss functions and nonconvex loss functions. Convex loss functions including Hinge loss, square loss are the most commonly used. If is a convex loss function, then the classical representer theorem [24, Theorem 5.5] assures that Optimization (2.1) has a unique minimizer such that

where denotes the set of all finite linear combinations of .

A remarkable consequence of the representation above is the fact that is contained in a known finite- dimensional space, even if the space itself is substantially larger. Thus, the convex loss functions are viewed as highly preferable in many publications because of their computational advantages (unique minimizer, ease-of-use, ability to be efficiently optimized by convex optimization tools, etc.).

However, the convexity also offer poor approximations to 0-1 loss function. Therefore, different nonconvex loss functions, such as ramp loss, truncated logistic loss, truncated least square loss, truncated least square loss, bi-truncated loss, generalized exponential loss, generalized logistic loss and Sigmoid loss are proposed and used in SVM (see [6, 9, 15, 18, 19, 22, 29]). These loss functions mentioned above and 0-1 loss functions are L.S.C. and nonconvex. Recently, [12, Corollary 4.1] generalizes the classical representer theorem to the L.S.C. loss function. Moreover, by the preliminary numerical experiments, we find that the SVM in the RKHS with the L.S.C. and nonconvex loss functions may be better than the convex loss functions (see Section 5). Thus, we will discuss the SVM in the RKHS with the L.S.C. loss functions. Before we show our main result, we need some concepts and properties of .

From [27, Definition 2.1], an RKHS can be seen as the two-sided reproducing kernel Banach space. On the other hand, the Riesz Representation Theorem assures that the dual space of is isometrically isomorphic to , that is, , which ensures that is reflexive. Hence, by [8, Definition 2.2.27] and reflexity of , it shows that the predual space of is . Moreover, since is also strictly convex and smooth, we obtain the following formula of Fréchet derivative (see [27, Remark 2.24])

(3.1)

where denotes the Fréchet derivative. In particular, for a differentiable real function, represents the gradient.

Proposition 3.1.

If is lower semi-continuous, then Optimization (2.1) has a minimizer such that

Proof.

Since is an reproducing kernel Banach space which has a predual space , from the condition (i) in the definition of the RKHS, we have that

Therefore, [12, Corollary 4.1] ensures that Optimization (2.1) has a minimizer such that

If is L.S.C. and nonconvex, then Optimization (2.1) may have more than one minimizers. Moreover, Proposition 3.1 guarantees that at least one of minimizers is contained in . Thus, we focus on find the minimizer in .

By Proposition 3.1, Optimization (2.1) in the RKHS can be equivalently transferred to Optimization (2.1) in . Next we show that Optimization (2.1) in also can be equivalently transferred to a finite-dimensional Optimization in . We denote the kernel matrix of as

and is symmetric and positive definite. For each , there exists a unique vector such that has the finite representation

which ensures that

Therefore, it is easy to check that

(3.2)

is an isometric isomorphism from

onto . On the other hand, combining the property of inner product with the reproducing property in the RKHS, it holds that

(3.3)

So Optimization (2.1) can be equivalently transferred to the following Optimization in

(3.4)

We denote the minimizer of Optimization (3.4) as , it follows that

This ensures that we employ the finite suitable parameters to reconstruct the SVM in the RKHS.

By this idea, we consider to find an algorithm based on Optimization (3.4) to compute Optimization (2.1) easily. At present, we mainly use the subdifferential, proximal operator and Fenchel conjugate of loss function to design algorithms for SVM, such as subgradient method, Lagrange multipliers method and sequential minimal optimization (SMO). These classical numerical algorithms are suitable for solving convex and smooth programs. Since is continuous, the lower semi-continuity of guarantees the lower semi-continuity of for all which ensures that is L.S.C.. On the other hand, it is clear that is continuous. In conclusion, Optimization (3.4) is L.S.C. finite-dimensional Optimization which may be nonsmooth or nonconvex. Many classical numerical algorithms are not suitable for Optimization (3.4) when is L.S.C.

The ADMM algorithm, as one of splitting techniques, has been successfully exploited in a wide range of structured regularization optimization problems in machine learning. ADMM can even be used to minimize nonsmooth or nonconvex function, which solves optimization problem by breaking them into smaller pieces. Moreover, Paper [25] discusses how to use ADMM for the traditional SVM with the 0-1 loss function. For the general L.S.C. functions and kernels, we observe that the subproblems in ADMM for Optimization (3.4) can be transferred into some Optimizations in and a well-posed linear system, each of which are thus easier to handle. In summary, we discuss the splitting method based on ADMM for Optimization (2.1). Moreover, if the sample size is small to moderate, then the preliminary numerical experiments show that the splitting method is a fast algorithm for Optimization (2.1) (see Section 5). Hence, we will study how to solve Optimization (2.1) by the splitting method. For notational convenience, let

To describe the algorithm, we first reformulate Optimization (3.4) as

(3.5)

Recall that the augmented Lagrangian function is defined as:

where the Lagrangian multiplier and denotes -norm in Euclidean space. The splitting method is presented as follows. Suppose that the algorithm is initialized at , its iterative scheme is

(S-1)

(S-2)

(S-3)

(S-4)

where is an iteration counter. Since (S-1) only depends on and (S-2) only depends on , by combining the linear and quadratic terms in , we equivalently transfer (S-1) and (S-2) to

(S-1’)

(S-2’)

By definition, it is easy to check that (S-1’) is L.S.C. and (S-2’) is continuous. Moreover, (S-1’) and (S-2’) is coercive (see [1, Definition 2.13]), that is,

Thus, Weierstrass Theorem [1, Theorem 2.14] assures that (S-1’) and (S-2’) both have a solution. As a consequence, the splitting method above is well-defined and an infinite iterative sequence is generated. Moreover, can be seen as an infinite iterative sequence to approximate the minimizer of Optimization (2.1).

Next, we discuss how to solve subproblems (S-1’) and (S-2’). As for (S-1’), since and can be split of the variable into subvectors, that is,

we equivalently transfer an Optimization in to some Optimizations in , that is,

(S-1”)

In other words, we solve (S-1’) in -dimensional space by breaking it into Optimizations (S-1”) in 1-dimensional space and each of them is easier to handle. To illustrate above, we give a simple example. Assume that is Hinge loss, that is,

By simple algebra, if , then

where . On the other hand, if , then

For the general L.S.C. loss function , the solution set of (S-1”) may not be a singleton. For example, assume that is ramp loss, that is,

Similarly, by simple algebra, if and , then

if and , then

In this case, we choose one of the elements in the solution set as .

As for (S-2’), since is symmetric and strictly positive definite and , it is clear that (S-2’) is nonnegative, convex and continuously differentiable. Moreover, is a minimizer of (S-2’) and thus a stationary point, that is,

By rearranging terms, is the solution of the following well-posed linear system

(S-2”)

where is the identity matrix with and order . Since is symmetric and strictly positive definite, we can use conjugate gradient method to obtain (See [13, 4.7.3 Conjugate Gradient Methods]).

When and is acquired, we can obtain by (S-3). However, we have a simpler one in mind that accomplishes the same goal. Substituting (S-3) into (S-2”) and rearranging terms, we have that

(S-3’)

In conclusion, the splitting method of Optimization (2.1) can be represented as follows:

Algorithm 1 Splitting Method for SVM in RKHS with L.S.C Loss Function

Input: initial value , the training data , loss function , kernel matrix , regularization parameter , Lagrange multiplier and stopping threshold .

fordo

(1) Choose in .

(2) Let , , .

fordo

(2-1) Set .

(2-2) Set .

(2-3) Set .

ifthen stop.

end forOutput: The approximate solution as .

(3) Set .

(4) Set .

ifthen stop.

end for

Output: The approximate solution .

In Section 4, we verify that if is L.S.C. and subanalytic and is sufficiently large, globally converges to a stationary point of Optimization (2.1). In particular, if is convex, then is globally convergent to the minimizer . If is L.S.C. and nonconvex, then may converge to a stationary point not a minimizer. Hence, it is better to solve Optimization (2.1) repeatedly by selecting some initial values randomly and choosing the minimizer of these outputs as the approximate solution of Optimization (2.1). Finally, we construct the classification rule by , that is,

We will complete the convergence analysis of Algorithm 1 in Section 4.

4 Convergence Analysis

In this section, we discuss the convergence of inspired from the work [11, 14] and use similar line of arguments therein. To ensure the convergence, we need the following assumption of loss function.

Assumption 4.1(Loss Function).

For any and ,

(i) is lower semi-continuous and subanalytic on .

(ii) is not the stationary point of in the sense of limiting subdifferential, that is, . (see [20, Definition 8.3])

Subanalytic functions are quite wide, including semi-algebraic, analytic and semi-analytic functions (see [10, 6.6 Analytic Problems]). More precisely, polynomial functions and piecewise polynomial functions are subanalytic functions. However, subanalyticity does not even imply continuity. Moreover, some margin-based loss functions (see [24, 2.3 Margin-Based Losses for Classification Problems]) satisfy Assumption 4.1, such as the least square loss, the Hinge loss, the truncated least squares loss, logistic loss and so on.

Theorem 4.1.

Suppose that Assumption 4.1 holds and Algorithm 1 is initialized at . If is symmetric and strictly positive definite and , then converges to a stationary point of Optimization (2.1).

Before we verify our main result, we need two lemmas about .

Lemma 4.2.

If the conditions in Theorem 4.1 holds, then there exists such that the following descent inequality holds

Proof.

From (S-1), we know that is the minimizer of , that is,

Combining [16, 1.4.14 Proposition] with (3.2), it shows that there exists such that

Let . Thus and the following descent inequality holds

The proof is complete.

∎

Moreover, Lemma 4.2 shows that is monotonically decreasing, that is, for any ,

(4.6)

Moreover, since is symmetric and strictly positive definite, the minimum eigenvalue of is which is its largest possible strong convexity parameter. Hence, [1, Example 5.19 and Theorem 5.24 (iii)] show that

Since and , the two inequalites above and (S-3’) provide that

(4.7)

It means that is bounded which ensures is also bounded by (S-3’). Furthermore, (S-3) shows that

is bounded. In conclusion, is bounded. Let be the set of subsequential limits of . [21, Theorem 3.6 and 3.7] show that is nonempty compact, and

By Lemma 4.2, (4.6) and (4.7), it follows that is monotonically decreasing and bounded. Hence, [21, Theorem 3.24] shows the convergence of .

For any , there exists a subsequence that converges to . Since is L.S.C. and the other term of is continuous, we have that is lower-continuous. Hence, the lower semi-continuity of at and the convergence of show that

(4.9)

Conversely, since is the minimizer of , it shows that

(4.10)

From the continuity of with respect to and , it holds

First, Lemma 4.2 and Lemma 4.3 (ii) show that for any , . We consider the following two cases:

(I) If there exists an integer for which , then for any . Since is monotonically decreasing, we see that

Since , for any , Lemma 4.2 shows that which ensures that is convergent.

(II) If for any integer , then we verify the convergence of by KL property of . Combining with the nonnegativity and subanalyticity of and , [23, (I.2.1.9)] shows that is subanalytic. Moreover, [2, 3, 28] assures that is a KL function on , that is, has the KL property at each point in (see [4, Section 2.4]). Clearly, by definition, is a KL function on . Hence, [4, Lemma 3.6] assures that there exist , and a nonnegative continuous concave function related to KL property such that

(i) and is continuously differentiable on with positive derivatives;

(ii) if and , then

where denotes the limiting subdifferential (see [20, Definition 8.3]). From Lemma 4.3 (i) and (4.8), it suffices to show that for and above, there exists an integer such that for any , we have

(4.14)

Let . From the concavity of , we get that

Multiplying on both side and using (4.14), we obtain that

(4.15)

By [20, 8.8 Exercise (c) and 10.5 proposition], it follows that

where

(4.16)

Invoking the optimality condition for (S-1’) and (4.2), we have that

(4.17)

From (4), (4.17) and (S-3), we obtain further that

Hence, , which ensures that

(4.18)

From [16, 1.4.14 Proposition], (4.4) and (3.2), we see that there exists such that

Inserting the inequality above into , and , we verify that

(4.19)

Combining (4.18) with (4), we have that there exists such that

(4.20)

Since , by rearranging terms, whenever , Lemma 4.2, (4.15) and (4.20) assure that

By rearranging terms, we obtain further that

Summing up the above relation from , since and ,, we see that

(4.21)

Hence, we denote . Thus . For any , there exists an integer such that for any ,

Therefore, is a Cauchy sequence. Since is a Hilbert space which is a complete metric space, it means that is convergent.

Combining (I) with (II), we conclude that converges to . Moreover, the sequence converges to and . Next we verify that is a stationary point of Optimization (2.1). First, (S-3) shows that

(4.22)

which ensures that

By the definition of , Lemma 4.3 (ii) and the continuity of , we find that

By [20, proposition 8.7] and (4.17), passing to the limit above along , it follows that

On the other hand, we suppose that . Thus (4.24) and (S-3’) assure that and . Moreover, (4.24) shows that

(4.25)

Since can be split of the variable into subvectors, Assumption 4.1 (ii) and [20, proposition 10.5] and [20, D. Rescaling] assure that

(4.26)

Clearly, (4.25) and (4.26) are contradiction. Hence, , which ensures that . Thus, (3.1) assures that

(4.27)

Therefore, [17, Definition 1.77 and Proposition 1.107], (4.25) and (4.28) show that

that is, is a stationary point of Optimization (2.1). The proof is complete.

∎

Next we analyze the convergent rates of . By [4, Example 5.3] and [2, Theorem 3.1], we know that has the following form

Moreover, we have the following theorem about convergent rates.

Proposition 4.4.

If the conditions in Theorem 4.1 hold, then we have the following estimations:

(i) If , then there exists an integer such that for , .

(ii) If , then there exists an integer , and such that for ,

(iii) If , then there exists an integer and such that for ,

Proof.

First we consider the case that . Suppose that satisfying the case (II) in Theorem 4.1. First, the definition of , we have that

(4.28)

Moreover, (4.20) and (4.28) assure that when is sufficient largely,

(4.29)

On the other hand, by the definition of , we have that . Hence, (4.17) shows that

(4.30)

Clearly, (4.29) and (4.30) are contradiction. Therefore, satisfies the case (I) in Theorem 4.1, that is, there exists an integer such that whenever , . Item (i) holds.

Next we consider the case that . It is easy to check that if satisfies the case (I) in Theorem 4.1, the assertion holds. If satisfies the case (II) in Theorem 4.1, then . Passing to the limit along the sequence , the triangle inequality and (4.21) ensure that for any

Let . Thus . Combining with two inequalities above, we have that

(4.32)

Moreover, the definition of ensures that there exists an integer such that for any , we have that

If , then . We denote . If , then (4.32) shows that

(4.33)

This implies that . Let and . Thus , and . Combining (4.31) with (4.33), we show that

Item (ii) holds.

If , then . Whenever , it follows that

Let . First we assume that , it holds that

Combining with two inequalities above, we find that

Next we assume that . Since , we have . This ensures that

Let . Thus , and

(4.34)

Since , summing up the above relation from and rearranging terms, (4.31) and (4.34) show that there exists such that if ,

Item (iii) follows immediately. The proof is complete.

∎

5 Numerical Examples

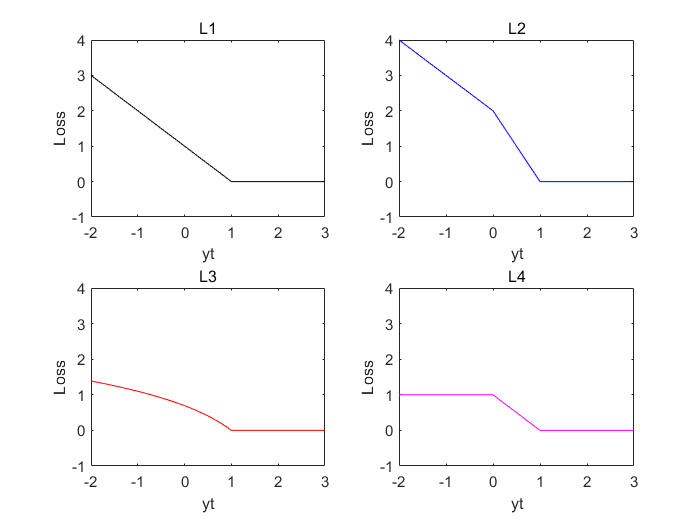

In this section, we test Algorithm 1 by the synthetic data and the real data. We choose some training data and testing data, loss functions and kernels to test Algorithm 1. For simplicity, let , , and be four loss functions used in our experiments, that is,

and

Here are the graphs of these support vector loss functions above.

Figure 1: For the graphs of the loss functions , , and , we replace to because of the symmetry of and .

We see that is convex Hinge loss, is a nonconvex linear piecewise loss function, is a nonconvex piecewise logarithmic loss function and is a nonconvex ramp loss function. These four loss functions satisfy Assumption 4.1. On the other hand, let be Gaussian kernel, that is,

and be Matérn 1-norm kernel, that is,

where denotes 1-norm in Euclidean space. Moreover, these two kernels are symmetric and strictly positive definite. Next we introduce our test results on synthetic data and real data.

5.1 Examples on Synthetic Data

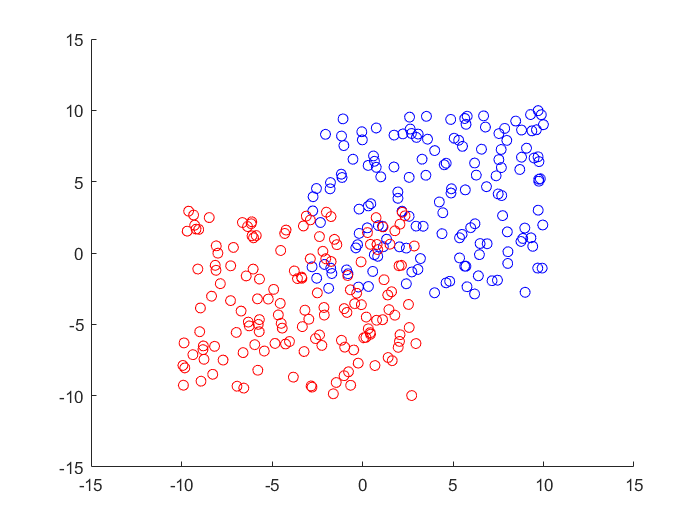

We sample from labeled by and labeled by randomly to obtain different training sets and testing sets. The data labeled by are equal to the data labeled by in each training set or testing set. Here is an example of sampling. In the following figures, two subdatasets are colored in blue and red.

(a) Training Set

(b) Testing Set

Figure 2: Example of Sampling .

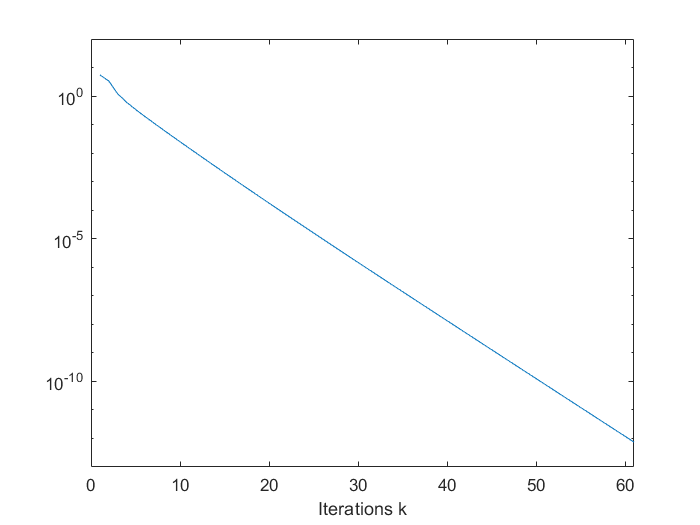

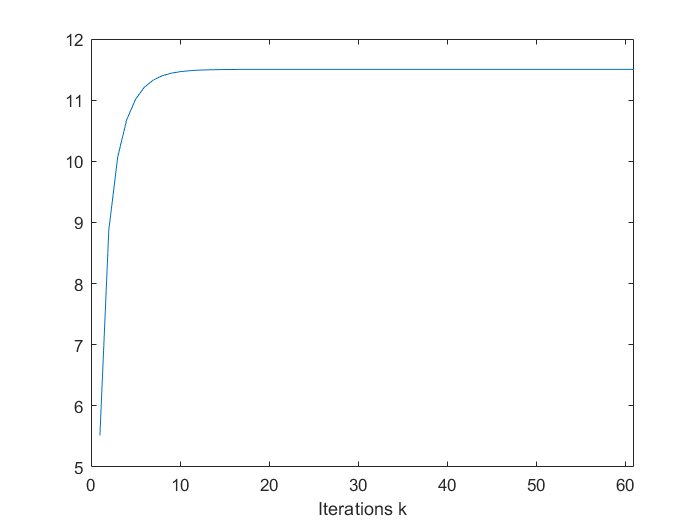

First, we show the convergence of Algorithm 1 for the nonconvex loss function . Some parameters and results of the numerical experiment represent as follows.

•

Gaussian kernel , where .

•

The nonconvex loss function .

•

.

•

, and .

•

we choose initial values randomly in .

From (4.22), we can show the convergence of by . By definition of , (3.1) and (3.2), we have that

In the following two picture, we show the convergence of Algorithm 1 by .

(a)

(b)

Figure 3: Convergence of Algorithm 1 with Nonconvex Loss Function .

Figure 3 shows that for the training data and parameters, Algorithm 1 converges in 61 iterations. This shows the effectiveness of Algorithm 1. Next, we use different sizes of training set and testing set to test Algorithm 1. Some parameters and results of the numerical experiment represents as follows.

•

Gaussian kernel , where .

•

The nonconvex loss function .

•

.

•

, and .

•

we choose 20 initial values randomly in .

Table 1: Comparison of Different Sizes of Data.

Training Data

Testing Data

Time(s)

Training Accuracy

Testing Accuracy

100

40

3.546

98%

85%

200

80

7.302

94%

87.5%

300

120

10.524

93.7%

90%

400

160

14.833

93%

87.5%

500

200

18.343

93.2%

90%

600

240

21.813

92.7%

87.1%

700

280

27.469

92.4%

89.3%

800

320

33.776

92.1%

90.9%

900

360

44.653

90.3%

90%

1000

400

56.510

92.3%

89%

Table 5.2 shows that solving Optimization (2.1) by Algorithm 1 is feasible in terms of running time and accuracy. Next we will show that choosing different kinds of loss functions and kernels have different accuracy.

Now we sample from the area and randomly to obtain a training set with points and a testing set with points. Some parameters of these experiments represent as follows.

•

The kernels and , where and .

•

The loss functions , , and .

•

, and .

•

Choose initial values randomly in .

In each experiment, we will choose a loss function and a kernel. The results of these experiments represent as follows.

Table 2: Numerical Results of Using Different Loss Functions and Kernels.

Loss Function

Kernel

Training Accuracy

Testing Accuracy

95.7%

95%

95.7%

95%

92%

93.7%

94.7%

93%

From Table 2, it is easy to see that the nonconvex loss function performs better than , and in these experiments. It shows that the SVM in the RKHS with the nonconvex loss function is better than the SVM in the RKHS with the convex loss functions for some cases. Next, we introduce the numerical experiment results on a real-world benchmark dataset.

5.2 Examples on UCI Machine Learning Repository

The vinho verde data in UCI machine learning repository has two kinds of wine samples. We will identify them based on physicochemical tests. There are 11 input variables about them, which are fixed acidity, volatile acidity, citric acid, residual sugar, chlorides, free sulfur dioxide, total sulfur dioxide, density, pH, sulphates and alcohol. We have 2000 wine samples in training set, and a half of them are labeled by +1 and the others are labeled by -1. Moreover, we have 718 wine samples in testing set, and a half of them are labeled by +1 and the others are labeled by -1. Next, we introduce some parameters of these experiments as follows.

•

The kernels and , where and .

•

The loss functions , , and .

•

, and .

•

Choose initial values randomly in .

In each experiment, we will choose a loss function and a kernel and we have the following results.

Table 3: Numerical Results on Vinho Verde Data.

Loss Function

Kernel

Training Accuracy

Testing Accuracy

99,9%

100%

99.9%

99.9%

100%

100%

100%

100%

From Table 3, we check that performs better than , and . It shows that in some cases the nonconvex loss function is more suitable than the convex loss function, which is our motivation of this paper.

In Section 5, we demonstrate the effectiveness of solving Optimization (2.1) by Algorithm 1. In addition, we give some examples to show that in some cases, the SVM in the RKHS with the nonconvex loss functions are better than the SVM in the RKHS with the convex loss functions. Therefore, we should reconsider not only convex loss function but also nonconvex loss function.

Acknowledgments. This program is supported by the National Natural Science Foundation of China under grant #12071157, #12026602 and the Natural Science Foundation of Guangdong #2019A1515011995 and #2020B1515310013.

References

[1]

A. Beck.

First-Order Methods in Optimization.

SIAM, Philadelphia, 2017.

[2]

J. Bolte, A. Daniilidis and A. Lewis.

The Lojasiewicz inequality for nonsmooth subanalytic functions with

applications to subgradient dynamical systems.

SIAM J. Optimiz. 17 (2007), 1205-1223.

[3]

J. Bolte, A. Daniilidis, A. Lewis and M. Shiota.

Clarke subgradients of stratifiable functions.

SIAM J. Optimiz. 18 (2007), 556-572.

[4]

J. Bolte, S. Sabach and M. Teboulle.

Proximal alternating linearized minimization for nonconvex and

nonsmooth problems.

Math. Program. 146 (2014), 459-494.

[5]

S. Boyd, N. Parikh, E. Chu, B. Peleato, J. Eckstein, et al.

Distributed optimization and statistical learning via the alternating

direction method of multipliers.

Found. Trends. Mach. Le. 3 (2011), 1-122.

[6]

J. Brooks.

Support Vector Machines with Ramp Loss and the Hard Margin Loss.

Oper. Res. 59 (2011), 467-479.

[7]

C. Cortes and V. Vapnik.

Support Vector Network.

Mach. Learn. 20 (1995), 273-297.

[8]

H. Dales, F. Dashiell, A. Tau and D. Strauss.

Banach Spaces of Continuous Functions as Dual Spaces.

Springer, Switzerland, 2016.

[9]

Y. Feng, Y. Yang, S. Huang, S. Mehrkanoon and J. Suykens.

Robust Support Vector Machines for Classification with Nonconvex and Smooth Losses.

Neural Comput. 28 (2016), 1217-1247.

[10]

F. Facchinei and J. Pang.

Finite-Dimensional Variational Inequalities and Complementarity Problems,

vol.I.

Springer, Berlin, 2003.

[11]

K. Guo, D. Han and T. Wu.

Convergence of alternating direction method for minimizing sum of two

nonconvex functions with linear constraints.

Int. J. Comput. Math. 94 (2016), 1-18.

[12]

L. Huang, C. Liu, L. Tan and Q. Ye.

Generalized representer theorems in Banach spaces.

Anal. Appl. 19 (2021), 125-146.

[13]

D. Kincaid and W. Cheney.

Numerical Analysis: Mathematics of Scientific Computing, 3rd Edition.

American Mathematical Society, Providence, 2002.

[14]

G. Li and T. Pong.

Global convergence of splitting methods for nonconvex composite

optimization.

SIAM J. Optimiz. 25 (2015), 2434-2460.

[15]

D. Liu, Y. Shi, Y. Tian and X. Huang.

Ramp loss least squares support vecotr machine.

J. Comput. Sci-Neth. 14 (2016), 61-68.

[16]

R. Megginson.

An Introduction to Banach Space Theory.

Springer-Verlag, New York, 1998.

[17]

B. Mordukhovich.

Variational Analysis and Generalized Differentiation. I: Basic Theory.

Grundlehren Series (Fundamental Principles of Mathematical Sciences), Springer, Berlin, 2006.

[18]

S. Park and Y. Liu.

Robust Penalized Logistic Regression with Truncated Loss Functions.

Can. J. Stat. 39 (2011), 300-323.

[19]

F. Pérez-Cruz, A. Navia-Vázquez, A. Figueiras-Vidal and A. Artés-Rodríguez.

Empirical risk minimization for support vector classifiers.

IEEE Trans. Neural Netw. 14 (2003), 296-303.

[20]

R. Rockafellar and R. Wets.

Variational Analysis.

Springer Berlin Heidelberg, Berlin, 1998.

[21]

W. Rudin.

Principles of mathematical analysis.

McGraw-Hill, Inc, New York, 1976.

[22]

X. Shen, L. Niu, Z. Qi. and Y. Tian,

Support Vector Machine Classifier with Truncated Pinball Loss.

Pattern Recogn., 68 (2017), 199-210.

[23]

M. Shiota.

Geometry of Subanalytic and Semialgebraic Sets.

Birkhäuser, Boston, 1998.

[24]

I. Steinwart and A. Christmann.

Support Vector Machines.

Springer-Verlag, New York, 2008.

[25]

H. Wang, Y. Shao, S. Zhou, C. Zhang and N. Xiu.

Support vector machine classifier via L0/1 soft-margin loss.

IEEE T. Pattern Anal. 2021, doi:10.1109/TPAMI.2021.3092177, in press.

[26]

H. Wendland.

Scattered Data Approximation.

Cambridge University Press, Cambridge, 2005.

[27]

Y. Xu and Q. Ye.

Generalized Mercer kernels and reproducing kernel Banach spaces.

Mem. Am. Math. Soc. 258 (2019), 1-122.

[28]

Y. Xu and W. Yin.

A block coordinate descent method for regularized multiconvex

optimization with applications to nonnegative tensor factorization and

completion.

SIAM J. Imaging Sci. 6 (2013), 1758–1789.

[29]

L. Yang and H. Dong.

Support Vector Machine with Truncated Pinball Loss and its Application in Pattern Recognition.

Chemometr. Intell. Lab. 177 (2018), 89-99.

[30]

C. Zalinescu.

Convex Analysis in General Vector Spaces.

World Scientific Publishing, River Edge, 2002.