monthyear\monthname[\THEMONTH], \THEYEAR

At the Edge of a Cloud of Brownian Particles

Abstract

We study a simple model for the trajectory of a particle in a turbulent fluid, where a Brownian motion travels through a random Gaussian velocity field. We study the quenched law of the process and prove that in a weak environment setting, the fluctuations at the transition from weak to strong disorder are described by the KPZ equation. We conjecture the same is true without the assumption of a weak environment.

1 Introduction

In this paper we consider a model of turbulent advection describing particle trajectories in one dimensional turbulent fluids. The particles each have their own, independent molecular diffusive motion, and are also transported through a Gaussian random drift field which represents the effect of the fluid. The field is Brownian in time and smooth, but rapidly decorrelating, in space. Associated to this model is a stochastic flow of kernels, [LJR04], which can be thought of as the density of a cloud of particles in the fluid, or as the random transition density of a single particle running through a realisation of the drift field. Using this interpretation, it is possible to show the flow of kernels solve a stochastic partial differential equation (SPDE) similar to a Fokker-Planck equation for a Brownian motion with drift.

The model is an example of the compressible Kraichnan model for turbulence, see the review [FGmcV01], which models the trajectory of a particle in a turbulent fluid, where the fluid is represented by a random evolving velocity field that is white in time. In our case the spatial correlations are taken to be of short length and smooth in space, similar to the case considered in [GH04], where the authors showed that removing the molecular diffusivity, at the same time as reducing the correlation length of the velocity field, with a certain relation holding between the two, led to sticky interactions between pairs of particles in the limiting process. This result was extended for the model we consider, [War15], to a full description of the interactions between any number of particles in the limiting process.

In [DG21] Dunlap and Gu show that the fluctuations of the density of the flow of kernels are well approximated, at large times, by the product of the heat kernel and the stationary solution to the SPDE solved by the flow of kernels. We are instead interested in the fluctuations of the density in the tail. Barraquand and Le Doussal, [BD20] conjecture that, at a cetain distance from the origin, these fluctuations are governed by the Kardar-Parisi-Zhang equation (KPZ equation). We will show that this is indeed the case in a regime in which the strength of the environment is tending to zero. Further we conjecture that the KPZ equation also appears when the diffusivity of the molecular motion of the particles is taken to be small instead of the environment strength.

We now briefly recall the stochastic heat equation, its connection to the KPZ equation and describe some previous results on the universality of the KPZ equation. The stochastic heat equation (SHE) is the stochastic partial differential equation, driven by a space-time white noise , given below

| (1.1) |

The logarithm of the stochastic heat equation, , is the Cole-Hopf solution to the KPZ equation

| (1.2) |

The KPZ equation describes the interface for surface growth model and is the canonical model in the KPZ universality class [KPZ86]. In fact, the KPZ equation is also a universal object itself; this is known as weak KPZ universality and it has been shown that a large class of continuous surface growth models lie in this class [HQ18]. In addition, it has been shown that certain observables of some discrete models converge to the KPZ equation, via convergence to the stochastic heat equation. The earliest such result was for the height function of the weakly asymmetric exclusion process [BG97]. More recently convergence to the KPZ equation has been shown for the free energy of directed random polymers in the intermediate disorder limit [AKQ14]. Following this result weak KPZ universality has been shown for a generalisation of ASEP [CST18], for a class of weakly asymmetric non-simple exclusion processes [DT16], and for Higher-Spin Exclusion process [CT17] and the related Stochastic 6-vertex model [CGST20]. Most relevant for us, in [CG16] Corwin and Gu studied a discrete version of our model, where the random drift field appears instead as random transition probabilities for a nearest neighbour random walk on . They showed that the transition probabilities evaluated in the large deviation regime, after rescaling, converge to the solution to the stochastic heat equation.

Barraquand and Corwin, [BC17], showed that when the transition probabilities in the random walk model are chosen to be Beta distributed the model becomes exactly solvable. They then used their formulae to show that the tail probabilities of the Beta Random walk in a random environment have Tracy-Widom GUE fluctuations of size , placing the model in the universality class of the KPZ fixed point, called strong KPZ universality. The same result is expected to hold for the density of the transition probabilities evaluated at point in the tail, not just for the cumulative tail probabilities [TLD16].

Barraquand and Rychnovsky, [BR20], found similar results exist for sticky Brownian motions and the associated Howitt-Warren flows; once again taking advantage of exact solvability in a special case. Further they conjectured the Howitt-Warren flows ( [HW09]) converge, under rescaling, to the stochastic heat equation, based on the convergence of the moments. Note that by [War15] this special case of the sticky flow is not the same one that arises in the limit of our model, but it is reasonable to expect the results to hold more generally.

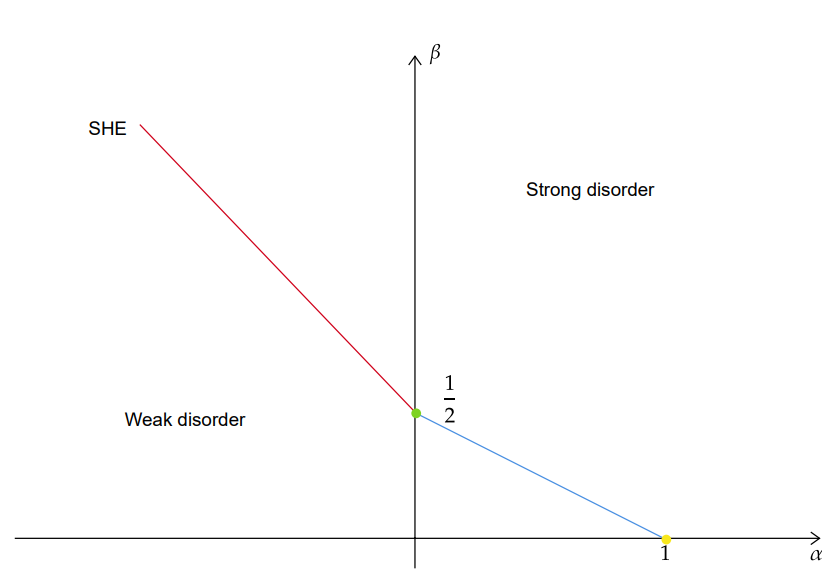

In this paper we show that the flow of kernels associated with our model converges to the solution to the stochastic heat equation, when the strength of the random environment and its correlation length are both taken to zero, with a certain relationship holding between the two. This result is similar to the result of Corwin and Gu, [CG16], for the discrete random walk model. We will also consider the behaviour of the second moment of the kernel in more general regimes; Figure 1 shows the behavior we find to hold when the distance from the origin and the ratio of the strength of environment to molecular diffusivity vary. The stochastic heat equation occurs (or is conjectured to occur) at a transition between weak and strong disorder regimes. In the former the kernels converge to the deterministic heat equation. In the latter the kernels converge to zero. This is analogous to the behaviour of the partition function of a random polymer, [Com17].

1.1 The Model

Suppose that is a centred Gaussian field with covariance , where is positive-definite. Let , we are interested in the solutions to the SDE

| (1.3) |

In the above SDE, is a Brownian motion on independent of and both stochastic integrals are understood in the Itô sense. As mentioned in the introduction, this is a simplified model for a particle trajectory in a turbulent fluid. The fluid is represented by the noise, , and is the molecular diffusivity of the particle itself. Existence and uniqueness of solutions is proved in [Kun94b, Theorem 3.4.1]. In fact, by [Kun94b, Theorem 4.5.1] the solution exists as a stochastic flow, , such that for any , the process solves the SDE started from at time . The solution is distributed as a Brownian motion with diffusivity , which can be checked directly by calculating the quadratic variation and recalling Lévy’s characterisation of Brownian motion. Alternatively, the solution can be thought of as a Brownian motion with diffusivity , running through the time dependent Gaussian random field , which we can think of as a random velocity field. We then consider the transition probabilities of the process conditional on :

| (1.4) |

Note that the family of kernels depend only on the field , and form a stochastic flow of kernels as introduced by Le Jan and Raimond in [LJR04]. Further, because is itself a Brownian motion, if we average over the law of we get the heat kernel,

| (1.5) |

Here, denotes the heat kernel with diffusivity , the density of which we will denote by .

It is known from [DG21] that the family of probability kernels have continuous densities, , with respect to the Lebesgue measure which solve the stochastic partial differential equations

| (1.6) |

together with the initial condition , where is the Dirac delta. In the above equation, is the (formal) time derivative of , so that it is white in time and smoothly correlated in space. By solution, we mean it is a generalised solution in the sense of [Kun94a], which we describe now by briefly recalling [DG21, Proposition 2.1]. The process , considered as a time-indexed family of tempered distributions on , is the unique solution to (1.6). That is, for every and every Schwartz function the following equality holds almost surely for every

| (1.7) |

Here, the stochastic integral is interpreted in the Itô sense.

The same SPDE, in a slightly different formulation, was derived for the flow of kernels (1.4) in [LJR04, Section 5]. The solution to the SPDE can be constructed directly in terms of a Wiener chaos expansion, [LJR02, Theorem 3.2]. Note that (1.6) is similar to the Fokker-Planck equation for a Brownian motion with diffusivity moving through a velocity field ; however, the coefficient of the Laplacian part is instead of because of the Itô correction coming from the stochastic integral.

1.2 The Stochastic Heat Equation as a Limit

We are interested in the fluctuations of at large times far from the origin. Hence, we look first at the effect of diffusive rescaling on the kernel. Define for ,

Then it is a straightforward calculation to show that is a solution to the transport SPDE (1.1) in which is replaced by its rescaled version , which has spatial covariance function . If we take then converges to the solution to the Heat equation, as we will see in Proposition 1.3. This convergence is only in a weak sense in the space variable; Dunlap and Gu, [DG21], show that there is a non-trivial random fluctuation when the pointwise behaviour is considered.

Rather than just considering in the diffusive regime, we are also interested in the moderate deviation regime, where and Barraquand and Le Doussal, [BD20], conjectured the SHE would appear. Thus, we introduce the rescaled quantity, , given by

| (1.8) |

where is a parameter which we will vary with to control the distance from the origin. The prefactor is motivated by fixing the expectation of :

In the most part, we will set and consider . According to Lemma 3.1 below, is the solution to the SPDE,

| (1.9) |

where, here, is a shifted version of the noise, . The covariance of the shifted noise is given by , so that is equal in distribution to the discussed at the start of the section.

If is chosen to depend on in an appropriate manner, namely , then approaches a multiple of the Dirac delta distribution, and thus approaches a space-time white noise as . Le Doussal and Barraquand, [BD20], argue that taking in (1.9) will lead to the final term vanishing, suggesting the limit could be the stochastic heat equation.

One can also consider the moments of . First consider the moments of , which have a representation in terms of solutions to (1.3). More precisely, if and are two solutions to , each driven by independent Brownian motions and but the same Gaussian velocity field, then for any

Notice that is a diffusion with generator

| (1.10) |

To see that this representation is useful, we can note that it can be used to show the convergence towards the heat equation, in the weak spatial sense, simply by showing that converges towards a Brownian motion on with diffusivity as ; we will do this later in propositions 1.3 and 2.2. There is a similar representation for the moments of ,

| (1.11) |

where is a diffusion with generator

being the Kronecker delta.

By taking , and once again converge to independent Brownian motions, and if we simultaneously take , then the right hand side of (1.11) approaches

| (1.12) |

where and are independent Brownian motions with diffusivity , is the local time at of the process and . This is exactly the form of the second moment for the stochastic heat equation, (1.1). Note that, importantly, this prediction for the coefficient, , of the noise is different from that which one would obtain simply by neglecting the transport noise in (1.9). The latter would be , which is strictly smaller. We can extend this argument by showing the convergence of the higher moments as well. However, the distribution of the stochastic heat equation is not determined by its moments, and unfortunately, we do not have any proof of the convergence of to a solution to the stochastic heat equation.

We consider a more general setup where we change the balance between the effects of the environment and the molecular diffusivity as we vary . More precisely, we consider solving (1.9) with noise having covariance , where is a fixed positive definite function, as before. We can also let the molecular diffusivity, , depend on and then . Two regimes are of interest, in addition to case considered previously, where and . The weak environment setting, where tends to and tends to some as ; and the weak diffusivity, where tends to and tends to as .

In the weak environment setting, we will prove the convergence of towards the solution to the stochastic heat equation when is chosen such that converges to a (non-zero) constant. In fact, we can couple the sequence of solutions, , to (1.9) to the limiting solution of the stochastic heat equation. This is achieved by constructing the driving noises from a common space-time white noise, through appropriate mollifications.

Let be a cylindrical Brownian motion on , and suppose that can be written as for a symmetric mollifier . Denote and , so that . Define , so that is a centred Gaussian field that is Brownian in time with spatial covariance function . In the following theorem, we will consider solutions to (1.9), , in the weak environment setting where is taken to be converging to as tends to . Note that whilst we have coupled the solutions, , they are no longer connected by the diffusive scalings and shifts that we discussed earlier.

Theorem 1.1.

Suppose that and as . Let be the solution to the SPDE

| (1.13) |

where is constant. Then, for any , as tends to zero, the following convergence holds in

where denotes the solution to the stochastic heat equation,

| (1.14) |

The convergence in , established in Theorem 1.1, implies convergence in distribution of as random elements of . If we adjust the definition of to account for the weak environment ( noting this makes depend on ) then (1.8) holds as an equality in distribution, and we have the following corollary.

Corollary 1.2.

Suppose that solves

where . Let be chosen so that as . Then,

converges in distribution as a random element of to , where solves the SHE with parameters and .

This extends simply to multiple times, and it is natural to expect that in fact is converging as a process. We have not established the tightness needed to prove this however.

Turning to the weak diffusivity regime, we can once again argue at the level of the moments and show that if we set and suppose that tends to slowly enough that tends to infinity as tends to , and we choose such that is converging to a positive constant, , then the second moment of converges to (1.12), this time with . We will justify this prediction for at the end of Section 2.1. The nature of this convergence is expected to be quite different from in the weak environment setting. Firstly, some smoothing in the spatial variable will be needed to control oscillations in . Secondly, if the pair converges in distribution (possibly down some subsequence) then the limit of the noises is not the noise driving the limiting SHE.

We summarize our predictions for general choices of and in Figure 1. Let

where we suppose that the above limits exist and that is positive.

The next two results concern the behaviour of in the weak disorder regime, which in Figure 1 corresponds to the region below the line segments.

Proposition 1.3.

Suppose we are in the setting of the preamble to Theorem 1.1. Suppose further that is bounded and tends to as . For any and we have

As previously, denotes the density of the heat kernel.

Notice that the above result involves spatial averaging; we expect that there are random fluctuations of the type described by Dunlap and Gu, [DG21], which mean that pointwise convergence fails. However, in the weak environment setting these fluctuations vanish in the limit, and we obtain the following result.

Proposition 1.4.

Suppose we are in the setting of the preamble to Theorem 1.1. Suppose further that and as . Then, for each , the following convergence holds in

In the strong disorder regime, corresponding to the region above the line segments in Figure 1, the asymptotic behaviour of the kernels is expected to be quite different. We give a first result in this direction, showing convergence to zero; however the argument is only valid when , so that there is a region in Figure 1 on the right which is not covered. The proof is an adaptation of an argument from Liggett [Lig04], see also [CSY03].

Proposition 1.5.

Suppose we are in the setting of the preamble to Theorem 1.1. Suppose further that is bounded and tends to infnity as . Then, for each , the following convergence holds in probability

2 The 2-Point Motion

2.1 The general case

Before we move on to the main part of the proof of Theorem 1.1, we will show that the second moments of can be written in terms of a two-dimensional diffusion, which we will call the two-point motion associated to .

Proposition 2.1.

Suppose that is the solution to (1.9). Let be the diffusion in with generator

where is the Kronecker delta. Then we have the equality

| (2.1) |

Proof.

As a consequence of (1.8) and the definition of the underlying flow of kernels, (1.4), we have

where the process has the generator given in line (1.10). The stated equality follows by applying Girsanov’s theorem with change of measure given by the Doléans-Dade exponential of the process , and then defining the process as , for . ∎

Note that both and are distributed as Brownian motions on with diffusivity plus an additional drift, which is the same for both processes. In fact, as the process converges in distribution to two-dimensional Brownian motion, which we will now prove. We will then use this result to show that converges in a weak sense towards the heat kernel.

Proposition 2.2.

Proof.

We apply [EK09, Theorem 8.2]; this proves the convergence of finite dimensional distributions by considering the behaviour of the generator. We will use the following estimate, which we derive below. There is a constant depending only on and such that

| (2.2) |

For any , the occupation times formula gives

where is the local time. If we apply Jensen’s inequality to the right hand side, we get

where . One can easily show that for each , there is a constant , depending only on , such that, for any , . Thus, we have that for all

In the above inequality, is a new constant that depends only on and ; the second inequality is a consequence of the assumption that , where for . In particular, this means that the main contribution to the integral comes from small enough that looks quadratic. Our assumption that implies (2.2).

Estimate (2.2) allows us to apply [EK09, Theorem 8.2] by controlling the difference between the action of the generator (2.1) and the Laplacian. The Theorem gives us convergence of the finite dimensional distributions. The proof is concluded by noting that since, for any , and are both marginally Brownian motions with diffusivity the sequence of processes is tight. ∎

Proposition 1.3, i.e. converges to the heat kernel in a weak sense, is an immediate consequence of the above proposition.

Proof of Proposition 1.3.

Moving the discussion to the weak diffusivity regime, we will explain the predictions we made in the introduction for the coefficients of the limiting stochastic heat equation. Recall that in the weak diffusivity regime, we assume that tends to more slowly than , as tends to . We also assume that converges to a positive constant . The occupations times formula gives

| (2.3) |

where the equality under the brace is due to Taylor’s expansion and . Proposition 2.2 shows that the process converges in distribution to a Brownian motion ; if we assume that the local times, , are converging jointly with to , then (2.3) suggests the following convergence should hold as

This is the form of the second moment for the stochastic heat equation, with the coefficients as predicted in the Introduction. This convergence can be made rigorous, see the thesis [Bro22] for details.

2.2 In a Weak Environment

In the weak environment setting, we can make stronger statements about the limiting behaviour of the by looking at the behaviour of the density of the law of the two-point motion. In fact, we will only need to look at the difference between the two-point motions, which is a one-dimensional diffusion. One explanation for the better behaviour in this setting is that the diffusion coefficient in the generator of this difference is converging to a constant function pointwise, rather than only pointwise almost everywhere, as happens in the other two regimes. As a consequence of Proposition 2.1, we can make the following statement about the process .

Proposition 2.3.

The process is a diffusion with generator

| (2.4) |

Let be the transition density of , that is let . The existence of this density is standard, see for example [Bor17]. In the following, we collect some necessary estimates on , which hold uniformly in . In the rest of this section, we’ll fix a constant and deal with a finite time window .

Proposition 2.4.

Suppose that is a bounded sequence, there are constants such that for any , , and

Proof.

We aim to apply the result [Aro67, Theorem 1], which provides a Gaussian estimate for fundamental solutions to elliptic PDEs. To begin, we will show that satisfies a PDE. Denote , and define . Note that for each , is a continuous and strictly increasing function, and so has a well defined inverse. Let be the process defined by , then it is a diffusion with generator . If we denote the transition density of by , then since is bounded above and below uniformly over all , we can apply the result in [Aro67, Theorem 1] to get that there are constants such that for all , , and

However, it is easy to see that , so that we in fact have the estimate

| (2.5) |

The claimed estimate then follows from the fact that for all and . In particular, the claim follows after noting

∎

The above estimate can be used to prove that converges to a multiple of the stochastic heat equation in the weak environment setting. In order to study itself, we must look at , which we define through the following equality, which we impose for any

| (2.6) |

We can also rewrite the expectation on the left-hand side in terms of the difference of the two-point motion, . This yields the equality

From which it is easily deduced that . Suppose that , we can apply Itô’s formula, which shows us that satisfies the following PDE

| (2.7) |

As before, the function is defined by

To simplify some notation we will introduce notation for the mass of , which in most of the cases we consider we will assume to be convergent as tends to .

We can estimate the difference between and its smoothing in terms of as follows.

| (2.8) |

Thus, we just need equicontinuity of , as a sequence of functions depending on , to get the desired upgrade for the convergence. We will begin proving this by considering the case.

Proposition 2.5.

Suppose that converges to as tends to , then for any the sequence of functions formed by is equicontinuous on .

Proof.

From inequality (II.1.10) proved in [Str88, Theorem II.3.1] and the fact that , we get that forms an equicontinuous sequence of functions on . is equicontinuous because of the upper and lower bounds on , whereas is equicontinous because of our assumption that is null. The lower bounds on then imply that is equicontinuous. Thus, the equality shows that is also equicontinuous. ∎

We will use this result to prove the equicontinuity for , but first we need a pointwise estimate on .

Proposition 2.6.

Suppose that and are bounded for , then there is a constant such that for all , and

Proof.

In order to get the desired estimate, we use Duhamel’s principle to get an integral equation for in terms of . In particular, Duhamel’s principle tells us that

| (2.9) |

One can easily check, assuming all the involved functions are sufficiently nice, that the solution to the above integral equation is also a solution to (2.7). One can also verify the above equation by applying Itô’s formula in the definition of with a suitable test function, and then taking a limit. We will use this equality to derive an inequality to which we can apply Gronwall’s inequality.

Applying (2.4), we get that

| (2.10) |

We can rewrite this in terms of the normalised version of to get

The inequality follows by estimating by its supremum and noting that , which is bounded in . Iterating this inequality, and allowing the constants to change between lines, we get

The proof is concluded by applying Gronwall’s inequality and making some additional simplifications. To check we can apply the inequality we just need to show that the integral on the right hand side is always finite. Note that an bound on provides an estimate through Equation (2.10), but an bound is easily provided by setting in Equation (2.6). ∎

Proposition 2.7.

Suppose that converges to as tends to , and that is bounded, then, for each , the sequence is equicontinuous.

Proof.

We will use Equation (2.9) once more. Fix and let be arbitrary, then for any , Proposition 2.5 tells us that there exists a such that for all we have

| (2.11) | ||||

| (2.12) |

If we apply Propositions 2.6 and 2.4, then we see that this is bounded above by

The statement follows by noting that we are allowed to choose to be sufficiently small. ∎

We conclude this section with a proof of Proposition 1.4, which follows directly from the convergence of .

Proof of Proposition 1.4.

First note that

Hence, we only need to prove the convergence of towards . We already have equicontinuity and boundedness of from propositions 2.7 and 2.10; thus, the Arzela-Ascoli theorem implies that the sequence is relatively compact in , where is arbitrarily chosen. From Equation (2.9), we get the inequality

Applying Propositions 2.4 and 2.10, and using that is a null sequence, we see that the right hand side vanishes. Finally, we note that propositions 2.4 and 2.5 prove that, for each , is relatively compact as a sequence in on . Due to Proposition 2.2, the process converges in distribution to a Brownian motion with diffusivity , combining this with the above relative compactness proves uniform convergence on compact sets of towards . ∎

3 The Mild Equation

In the following, we will use the notation for

| (3.1) |

We will also use the notation below for stochastic integrals with respect to .

| (3.2) |

The second inequality is a consequence of the coupling between the fields that we chose in the setup of Theorem 1.1. Note that we have the isometry

| (3.3) |

It is important to note here that is not normalised to have unit mass, so that for a fixed function , converges to as tends to . However, under the choice of made in Theorem 1.1, the function has mass , which is converging to a positive constant. We can derive the SPDE for , (1.9), directly from the SPDE for .

Lemma 3.1.

With and defined as in Section 1.1, we have that for each

| (3.4) | ||||

| (3.5) |

Proof.

Let and define . By definition, we have . Thus, a straightforward calculation using Equation (1.1) and the stochastic and deterministic Fubini theorems leads to the equality

Noticing that , we get the desired equation with in place of . As discussed in Section 1.1, we replace by its shifted version, which has the same distribution, to get the result as stated.

∎

From Equation (1.9), one can derive the following mild equation for . For any

| (3.6) |

The solution to the stochastic heat equation,

satisfies its own mild equation. For any

We will use these two mild equations to prove Theorem 1.1.

3.1 Proof of Theorem 1.1

The proof of Theorem 1.1 relies on a Gronwall argument that will yield the following inequality.

Proposition 3.2.

There are constants such that for every and

| (3.7) |

Before the proof of this statement, we will first derive an estimate to which we can apply Gronwall’s inequality, and then collect some lemmas to get an estimate of the form in the proposition.

Also note that the estimate in Proposition 3.2 shows that the norm tends to faster than . as . This is necessary for the estimate to be meaningful because of the fact that the mass of is proportional to .

Lemma 3.3.

There is a constant such that for all and

| (3.8) |

Proof.

From the previous section, for the difference between and , we have

Thus, we have

| (3.9) | ||||

| (3.10) |

This is not yet in a suitable form for Gronwall’s inequality. However, if we choose , and then integrate out the variable, inequality (3.9) becomes

| (3.11) | ||||

We will show that the first term after the inequality can be bounded above by

We will also show that the second term after the inequality in (3.11) tends to as . This, together with bounds on the norms of and , will allow us to apply Gronwall’s inequality to (3.11) and prove Proposition 3.2. Recall that , so that we may rewrite as follows

By rearranging the convolutions and using the convolution property of the heat kernel, we get that the above expression is equal to

| (3.12) |

Young’s inequality gives us the estimate

For each there is a such that we have the following inequality

The last inequality is a consequence of the assumption that for , where , and the assumption that is bounded in . Another consequence is that for some constant . Hence, line (3.12) is bounded above by

Applying this to (3.11) yields the desired estimate. ∎

So that we just need a good estimate on the second and third lines of (3.8). Then, we can apply Gronwall’s inequality and get a meaningful estimate. Note the that the second line of (3.8) is bounded above by

| (3.13) |

In the following lemma, we provide estimates on the norms of and .

Lemma 3.4.

There are constants such that for all

Proof.

For the second inequality we can square and integrate the mild equation for to get

The desired inequality follows by iterating the inequality derived above, and then applying Gronwall’s inequality.

This result allows us to estimate the second line in (3.8), we now move on to estimating the third line.

Lemma 3.5.

There is a constant such that for every with and

Proof.

Some simple rearrangements using that give the equality

We will apply a combination of the following two bounds.

Thus, we see that the right hand side in the lemma is bounded, for any , by

Which, by the Cauchy-Schwartz inequality, is bounded above by

| (3.14) |

We recall that we assumed is bounded, so that we can apply Lemma 3.4 to get the following upper bound on (3.14), for a new constant .

| (3.15) |

where is the Beta function. Note that , which is bounded above for all by , for some constant . Thus, Line (3.15) is bounded above by

where, once again, the constant has changed between lines. If we set , which we can do for , then we get the desired upper bound. ∎

Proof of Proposition 3.2.

Thus, applying Lemmas 3.4 and 3.5 to (3.8), we get the inequality (for a new constant )

| (3.16) | ||||

| (3.17) |

Where for the last inequality, we have repeated our estimate for the Beta function and set . If we apply this inequality, we can see

Applying this bound to (3.17), we can apply Grönwall’s inequality. Which, after some elementary simplifications, yields the desired inequality. ∎

Proof.

Proof of Theorem 1.1 As a consequence of the previous proposition, we have proved that if then

We also have that for each , in , this follows from estimates in [BC95]. Therefore,

where is the normalised version of . We now just need to show that the mollified version of is close to itself. From the triangle inequality, we have

| (3.18) |

Theorem 1.1 tells us that the latter term on the right hand side tends to as , and we discussed the former term in the previous section. Recall from (2.8) that we only need to control the the following increment of to get the desired convergence.

Since both and have compact support, we only need to apply Proposition 2.7 to finish the proof. ∎

4 Proof of Proposition 1.5

Let be the solution to the SPDE (1.9). Then is a martingale with quadratic variation

Applying Itô’s formula and taking expectations gives

Now, similarly to previous sections, assume the covariance can be expressed as

with for a positive and symmetric function . Then, for any , by the Cauchy-Schwartz inequality,

Let , so that , and the right-hand side above can be written as

Since whenever , we deduce that

Taking expectations, and using Jensen’s inequality finally gives

Express as where has unit mass. Then integrating the inequality gives

| (4.1) |

Now we can move on to the proof of Proposition 1.5.

Proof of Proposition 1.5.

The idea is to use the estimate (4.1) to deduce that tends to zero with .

First notice that Jensen’s inequality and the initial condition implies that

We can write

as

where and are independent random variables, the distribution of having density and being a Gaussian with variance . Consequently the second term on the RHS of (4.1) can be made arbitraily small, for all by choosing large enough.

The hypothesis that ensures that for any fixed , which in turn implies that, for a fixed , the first term on the RHS of (4.1) is tending to zero.

∎

Acknowledgement. D.B. was supported by EPSRC grant No. EP/W522594/1.

References

- [AKQ14] Tom Alberts, Konstantin Khanin, and Jeremy Quastel. The intermediate disorder regime for directed polymers in dimension . The Annals of Probability, 42(3):1212 – 1256, 2014.

- [Aro67] D. G. Aronson. Bounds for the fundamental solution of a parabolic equation. Bulletin of the American Mathematical Society, 73(6):890 – 896, 1967.

- [BC95] Lorenzo Bertini and Nicoletta Cancrini. The stochastic heat equation: Feynman-kac formula and intermittence. Journal of Statistical Physics, March 1995.

- [BC17] Guillaume Barraquand and Ivan Corwin. Random-walk in beta-distributed random environment. Probability Theory and Related Fields, 167(3):1057–1116, Apr 2017.

- [BD20] Guillaume Barraquand and Pierre Le Doussal. Moderate deviations for diffusion in time dependent random media. Journal of Physics A: Mathematical and Theoretical, 53(21):215002, may 2020.

- [BG97] Lorenzo Bertini and Giambattista Giacomin. Stochastic Burgers and KPZ equations from particle systems. Communications in Mathematical Physics, 183(3):571 – 607, 1997.

- [Bor17] A.N. Borodin. Stochastic Processes. Probability and Its Applications. Springer International Publishing, 2017.

- [BR20] Guillaume Barraquand and Mark Rychnovsky. Large deviations for sticky Brownian motions. Electronic Journal of Probability, 25(none):1 – 52, 2020.

- [Bro22] Dominic Brockington. Brownian Motions in Random Environments. PhD thesis, University of Warwick, 2022.

- [CG16] Ivan Corwin and Yu Gu. Kardar parisi zhang equation and large deviations for random walks in weak random environments. Journal of Statistical Physics, 166, 06 2016.

- [CGST20] Ivan Corwin, Promit Ghosal, Hao Shen, and Li-Cheng Tsai. Stochastic pde limit of the six vertex model. Communications in Mathematical Physics, 375, 05 2020.

- [Com17] Francis Comets. Directed Polymers in Random Environments, volume 2175. Springer, 01 2017.

- [CST18] Ivan Corwin, Hao Shen, and Li-Cheng Tsai. converges to the KPZ equation. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 54(2):995 – 1012, 2018.

- [CSY03] Francis Comets, Tokuzo Shiga, and Nobuo Yoshida. Directed polymers in a random environment: path localization and strong disorder. Bernoulli, 9(4):705 – 723, 2003.

- [CT17] Ivan Corwin and Li-Cheng Tsai. KPZ equation limit of higher-spin exclusion processes. The Annals of Probability, 45(3):1771 – 1798, 2017.

- [DG21] Alexander Dunlap and Yu Gu. A quenched local limit theorem for stochastic flows, 2021.

- [DT16] Amir Dembo and Li-Cheng Tsai. Weakly asymmetric non-simple exclusion process and the kardar–parisi–zhang equation. Communications in Mathematical Physics, 341(1):219–261, 2016.

- [EK09] S.N. Ethier and T.G. Kurtz. Markov Processes: Characterization and Convergence. Wiley Series in Probability and Statistics. Wiley, 2009.

- [FGmcV01] G. Falkovich, K. Gawȩdzki, and M. Vergassola. Particles and fields in fluid turbulence. Rev. Mod. Phys., 73:913–975, Nov 2001.

- [GH04] Krzysztof Gawedzki and Péter Horvai. Sticky behavior of fluid particles in the compressible kraichnan model. Journal of Statistical Physics, 116(5):1247–1300, Sep 2004.

- [HQ18] Martin Hairer and Jeremy Quastel. A class of growth models rescaling to kpz. Forum of Mathematics, Pi, 6:e3, 2018.

- [HW09] Chris Howitt and Jon Warren. Consistent families of brownian motions and stochastic flows of kernels. Ann. Probab., 37(4):1237–1272, 07 2009.

- [KPZ86] Mehran Kardar, Giorgio Parisi, and Yi-Cheng Zhang. Dynamic scaling of growing interfaces. Phys. Rev. Lett., 56:889–892, Mar 1986.

- [Kun94a] H. Kunita. Generalized solutions of a stochastic partial differential equation. Journal of Theoretical Probability, 7(2):279–308, Apr 1994.

- [Kun94b] H Kunita. Stochastic flows and stochastic differential equations. Stochastics and Stochastic Reports, 51(1-2):155–158, 1994.

- [Lig04] T.M. Liggett. Interacting Particle Systems. Classics in Mathematics. Springer Berlin Heidelberg, 2004.

- [LJR02] Yves Le Jan and Olivier Raimond. Integration of Brownian vector fields. The Annals of Probability, 30(2):826 – 873, 2002.

- [LJR04] Yves Le Jan and Olivier Raimond. Flows, coalescence and noise. Ann. Probab., 32(2):1247–1315, 04 2004.

- [Str88] Daniel W. Stroock. Diffusion semigroups corresponding to uniformly elliptic divergence form operators, pages 316–347. Springer Berlin Heidelberg, Berlin, Heidelberg, 1988.

- [TLD16] Thimothé Thiery and Pierre Le Doussal. Exact solution for a random walk in a time-dependent 1d random environment: The point-to-point beta polymer. Journal of Physics A: Mathematical and Theoretical, 50, 05 2016.

- [War15] Jon Warren. Sticky Particles and Stochastic Flows, pages 17–35. Springer International Publishing, Cham, 2015.