A novel approach for Fair Principal Component Analysis based on eigendecomposition

Abstract

Principal component analysis (PCA), a ubiquitous dimensionality reduction technique in signal processing, searches for a projection matrix that minimizes the mean squared error between the reduced dataset and the original one. Since classical PCA is not tailored to address concerns related to fairness, its application to actual problems may lead to disparity in the reconstruction errors of different groups (e.g., men and women, whites and blacks, etc.), with potentially harmful consequences such as the introduction of bias towards sensitive groups. Although several fair versions of PCA have been proposed recently, there still remains a fundamental gap in the search for algorithms that are simple enough to be deployed in real systems. To address this, we propose a novel PCA algorithm which tackles fairness issues by means of a simple strategy comprising a one-dimensional search which exploits the closed-form solution of PCA. As attested by numerical experiments, the proposal can significantly improve fairness with a very small loss in the overall reconstruction error and without resorting to complex optimization schemes. Moreover, our findings are consistent in several real situations as well as in scenarios with both unbalanced and balanced datasets.

1 Introduction

Dimensionality reduction techniques have been used in signal processing and machine learning problems in order to deal with high dimensional datasets and, therefore, to enhance data visualization and reduce the complexity of learning algorithms [1, 2, 3]. Among such techniques, one of the most used is the Principal Component Analysis (PCA) [4], which has been applied in several problems [5, 6, 7, 8, 9]. In summary, PCA aims at reducing the dimensionality of a dataset while preserving as much information as possible from this dataset. Besides maximizing the retained information, there is also an interest in the development of methods that avoid bias when providing dimensionality reduction. Indeed, the classical PCA formulation does not take into account different sensitive groups when projecting the data. As a consequence, the reduced dataset may contain distinct representation errors for those different groups, which in turn may lead to bias for certain sensitive groups. Therefore, unless strategies to mitigate bias are deployed, the application of PCA in machine-learning-based systems may suffer from fairness issues.

Several recent studies have addressed bias and fairness issues in real world problems [10, 11, 12, 13]. For instance, a topic of interest is the trade-off between model accuracy and fairness [14, 15, 16, 17, 18, 19]. In PCA-based dimensionality reduction, trade-offs between the quality of representation and fairness have also been studied in the literature [20, 21]. For instance, a central question is how much one is willing to lose in the overall representation error in order to decrease the disparity between the sensitive groups. Aiming at reducing such a disparity, several works in the literature proposed fair PCA-based dimensionality reduction techniques [22, 23, 24, 25, 20, 26, 21].

There are basically two main lines of reasoning in these approaches. For instance, in the algorithm FairPCA [22], as well as in other related approaches [21, 24, 25], fairness is measured by means of the loss suffered by each sensitive group with respect to their individual optimal projection. In the optimal scenario, the proposed algorithm will find a projection matrix that leads to the same average loss for each sensitive group. On the other hand, in the Multi-Objective Fair Principal Component Analysis (MOFPCA) algorithm [20], one simply measures fairness by taking the squared difference between the averaged reconstruction errors of both sensitive groups. Therefore, in this case, the fairest scenario is the one that minimizes the disparity between the groups. Moreover, the formulation in MOFPCA does not require to find projections vectors that improve fairness. One may exploit the eigenvectors provided by the classical PCA and, in a different combination (i.e., not necessarily the eigenvectors associated with the highest eigenvalues), evaluate if fairness was improved without a large loss in the overall reconstruction error. The price that MOFPCA pays is that the projection vectors are restricted to the ones provided by the classical PCA.

In this paper, we propose a novel approach to exploit fairness in PCA-based dimensionality reduction. Similarly as in the MOFPCA, we also consider the disparity between the reconstructions errors as a fairness measure. However, we exploit any projection matrix that improve fairness in the reduced space. For this purpose, we formulate an optimization problem whose cost function includes both overall reconstruction error and the adopted fairness measure. In order to cast this cost function as a mono-objective optimization problem, the objectives are weighted by a scalar factor. The interesting aspect is that, given a predefined weighted factor, the solution has a closed form based on the eigenvector/eigenvalue decomposition. Therefore, a first contribution of this paper consists in formulating an optimization problem that provides a compromise solution between the overall reconstruction error and the fairness measure, which depends on the adopted weighted factor and can be solved by an eigendecomposition.

Moreover, since a central concern is reducing the disparity between the sensitive groups, one may investigate which weighted factor lead the the fairest scenario. Therefore, the other contribution of this paper is to propose an efficient fair PCA-based dimensionality reduction algorithm that minimizes the disparity in the averaged reconstruction errors by means of a one-dimensional search in closed form solutions. Note the existing fair PCA methods either require a complex mono-optimization scheme or a multiobjective scheme which is limited to the principal components which stem from the classical PCA algorithm.

The rest of this paper is organized as follows. Section 2 describes the classical PCA formulation and the possible disparities in dimensionality reduction tasks. In Section 3, we present the proposed approach for fair dimensionality reduction. The numerical experiments as well as the obtained results are discussed in Section 4. Finally, our conclusions and future perspectives are presented in Section 5.

2 Disparities in principal component analysis

Let denote a dataset with samples and attributes. For convenience, let us also assume that has zero mean (otherwise, one should center the data by extracting its mean). With the purpose of reducing the dimensionality of from to -dimensional samples, the goal in PCA is to find a projection matrix such that the projected data are uncorrelated and retain as much information from as possible. A typical solution of PCA is obtained by tackling the following optimization problem:

| (1) |

where represents the overall reconstruction error, is the Frobenius norm [27] and , where is the identity matrix, ensures that is orthogonal. It is easy to show that minimizing is equivalent to maximize (or maximize , where is the covariance matrix of , since is a constant) [28, 29, 30]. Moreover, since , minimizing the reconstruction error is also equivalent to maximize the total variance of the projected data. It is also known in the literature [4] that the solution of PCA is achieved by setting the columns of as the eigenvectors of associated with its highest eigenvalues (see Appendix Eigenvectors as a solution for PCA).

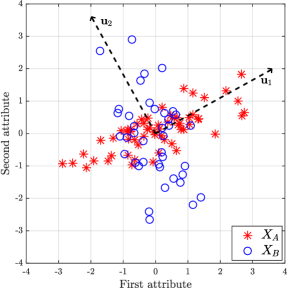

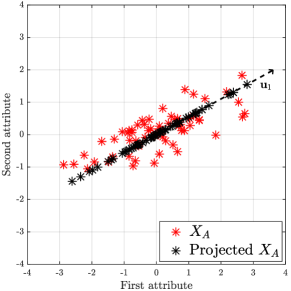

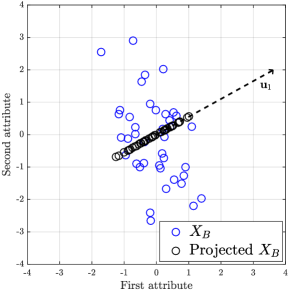

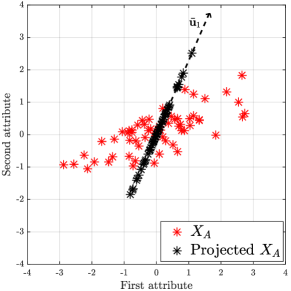

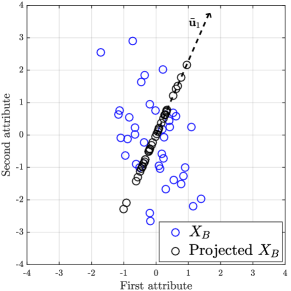

Although one expects to optimize the overall model performance (i.e., to achieve the minimum reconstruction error in PCA), there is a growing interest in the literature in the development of automatic decision systems that are also fair. We here consider that a fair algorithm should not lead to disparities between sensitive groups (e.g., males and females, whites and blacks, etc.). Therefore, a concern in the classical PCA is that it does not take into account possible disparities between different groups when projecting the dataset. For instance, assume that , where and represent different sensitive groups with and samples, respectively. Without loss of generality, let us also assume that group is privileged in comparison with group . This means that the application of the classical PCA in leads to a reduced dataset in which the average reconstruction error of group is lower in comparison with group , i.e., . Therefore, this disparity may harm the representation of group in comparison with group in the projected data. In order to illustrate this scenario, let us consider the example presented in Figures 1a, 1b and 1c. One may see that, by projecting the dataset into the first principal component, the variance of group is greater than the variance of group . Therefore, group has a worst representation in comparison with group .

In order to avoid disparities in the reconstruction errors, it is convenient to adopt a disparity measure when performing dimensionality reduction. We here propose the following one:

| (2) |

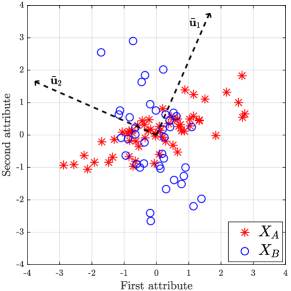

which calculates the disparity between the average reconstruction errors of the harmed group () and the privileged one (). For instance, if , we achieved the fairest scenario. If one considers the example illustrated in Figures 1d, 1e and 1f, one may see that, by assuming another projection vector, the retained information for groups and are similar, which indicates that the disparity between their representations was mitigated.

3 Proposed fair PCA-based dimensionality reduction approach

Our formulation for fair principal component analysis consists in minimizing both overall reconstruction error and . Therefore, we deal with the following optimization problem:

| (3) |

where and is the weighting factor that controls the importance given to the each objective. Note that, if , (3) is equivalent to the classical PCA formulation. However, the lower is the value of , the greater is the importance assigned to the disparity measure. Therefore, different values of lead to trade-off solutions between the fairness metric and the overall reconstruction error.

Similarly as in the classical PCA, the interesting aspect of our proposal is that the optimal solution can be also achieved by means of an eigendecomposition. This finding is stated in the following theorem:

Theorem 1.

Assume a predefined weighting factor . The optimal solution of the fair principal component analysis problem expressed in (3) is given by the eigenvectors of the weighed covariance matrices associated with its highest eigenvalues.

Proof.

Since , where (and similarly for and ), it is easy to show that

| (4) |

where and . Since is a constant, the minimization of leads to the maximization of . Similarly as in the classical PCA, our proposal also turns to the maximization of a trace operator. Therefore, one may follow the iterative approach to find the columns of . We start by the first principal component:

| (5) |

This optimization problem is equivalent to the one presented in (10). Therefore, we know that is equal to the eigenvector of associated with the highest eigenvalue . For the next projection vectors, we must include the constraint that ensures that , for all and solve the following the following optimization problems:

| (6) |

However, instead of assuming that , for all , we here assume that , for all . As a consequence, we do not ensure that the projected data are uncorrelated. However, we may follow the derivation of the classical PCA and conclude that the columns of are composed, in its columns, by the eigenvectors of associated with its highest eigenvalues. ∎

In summary, given a weighting factor , we attempt to reduce the disparities by solving an optimization problem very similar to the classical PCA. However, in our approach, the eigendecomposition of matrix takes into account the disparity between sensitive groups. Clearly, for , one only minimizes the overall reconstruction error and does not reduce possible disparities (i.e., one may have ). On the other hand, may minimize the disparity measure more than the necessary, which may invert the privileged group. In other words, one may achieve a projected data in which group has a better representation in comparison with group (i.e., ). Therefore, it is possible that there is a value of that leads to , i.e., that minimizes the considered fairness measure

| (7) |

Note that (7) is the square of . Therefore, when minimizing , one reduces the disparity and avoids the inversion of the privileged group. In the sequel, we present the proposed algorithms for fair dimensionality reduction.

3.1 Unconstrained fair dimensionality reduction

Since fixed the optimization problem has a closed solution, the (unconstrained) fair PCA-based dimensionality reduction algorithm proposed in this paper (called here u-FPCA) consists in a one-dimensional search (in ) of eigenvectors/eigenvalues solutions aiming at minimizing the fairness measure (7). Mathematically, this formulation can be expressed as follows:

| (8) |

where the columns of are composed by the eigenvectors of associated with its highest eigenvalues. Therefore, it is a simple and efficient approach that can be solved, for instance, by applying a golden section search algorithm [31]. Based on the dataset divided into the sensitive groups and , the steps of u-FPCA are presented in Algorithm 1 (in this algorithm, represents the operator that returns the eigenvectors of associated with its highest eigenvalues). Recall that, without loss of generality, we assume that group is the privileged one when applying the classical PCA.

3.2 Constrained fair dimensionality reduction

Without further considerations, the optimization problem (8) will only minimize the fairness measure. In this case, there are two possible scenarios for enhancing fairness, either by degrading both and (group more than group ) or by degrading while improving . We would say that the first scenario may be an inconvenient, since we must reduce the quality of representation of both groups. However, the second scenario may be acceptable, since in order to reduce the disparities between the reconstruction errors, the privileged group will “resign” part of its quality in representation in order to improve the harmed one. Therefore, with the purpose of ensuring that one only achieves a solution in the second scenario, one should adopt a constraint in the one-dimensional search. In the second approach proposed in this paper (called here c-FPCA), the optimization problem can be formulated as follows:

| (9) |

where the columns of are the same as before and is the overall reconstruction error of group (the unprivileged one) by considering the projection matrix obtained from the solution of the classical PCA on all dataset . In order to solve (9), one may also use a one-dimensional search algorithm, such as the golden section search, and include the aforementioned constraint. For instance, one may start from (which is the solution of the classical PCA and, therefore, a feasible solution) and decrease its value until achieve the minimum of the fairness measure while preserving . Algorithm 2 presents the steps of the c-FPCA.

4 Experiments

The experiments222It is worth mentioning that all codes supporting this paper are available in the public repository https://github.com/GuilhermePelegrina/FPCA. The pre-processed data are available at https://github.com/GuilhermePelegrina/Datasets/tree/main/FPCA. benchmark our proposals against the classical PCA and the algorithms MOFPCA [20] and FairPCA [22]. We used the following datasets and sensitive attributes (the first two were also used in [22, 20]):

-

•

Taiwanese Credit Default (TCRED)333https://archive.ics.uci.edu/ml/datasets/default+of+credit+card+clients. [32]: Personal attributes and credit history information used to predict default payments in Taiwan. It consists of 30000 samples and 22 attributes. We considered as sensitive attribute the education level (higher and lower, with 24615 and 5385 samples, respectively).

-

•

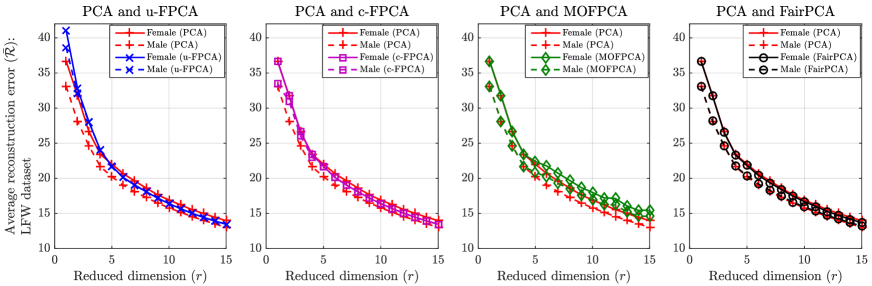

Labeled Faces in the Wild (LFW)444http://vis-www.cs.umass.edu/lfw/. [33]: Public benchmark of photographs frequently used for face recognition. It consists of 13232 samples and 1764 attributes (36x49 pixels). We considered as sensitive attribute the gender (female and male, with 2962 and 10270 samples, respectively).

-

•

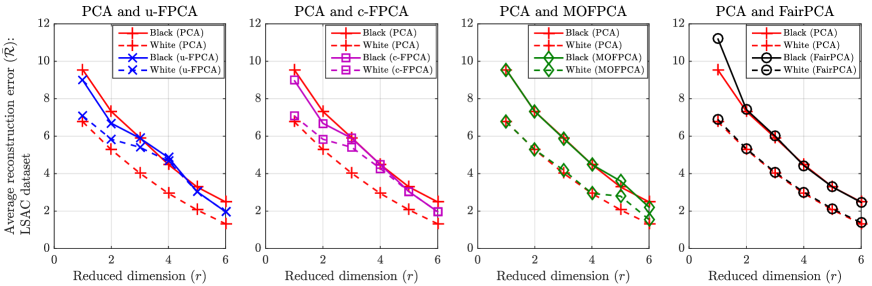

The Law School Admissions Council’s (LSAC)555http://www.seaphe.org/databases.php. [34]: A dataset collected from law school students that investigates ethical concerns in the bar passage rates. It consists of 26551 samples and 10 attributes. We considered as sensitive attribute the race (black and white + other, with 1790 and 24761 samples, respectively).

For each one, we collected the predictive attributes and defined the sensitive one, which will be only used to split the dataset into groups and . Therefore, we do not consider the sensitive attribute in the dimensionality reduction task.

We also evaluate the considered methods in scenarios in which there are unbalanced and balanced datasets with respect to the sensitive attributes. The obtained results are presented in the sequel.

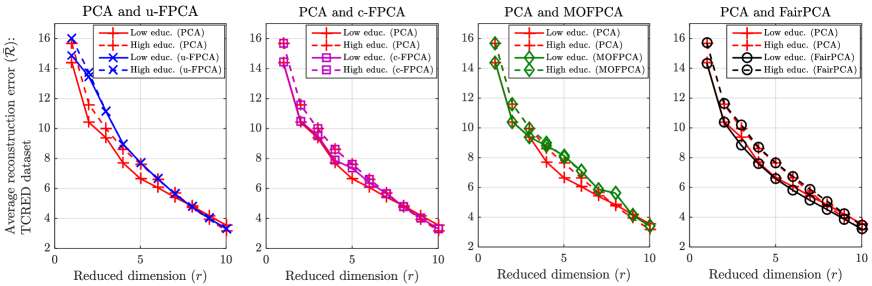

4.1 Fair dimensionality reduction: Unbalanced datasets

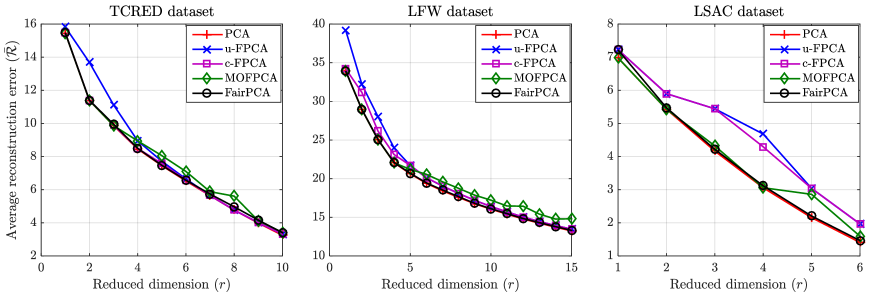

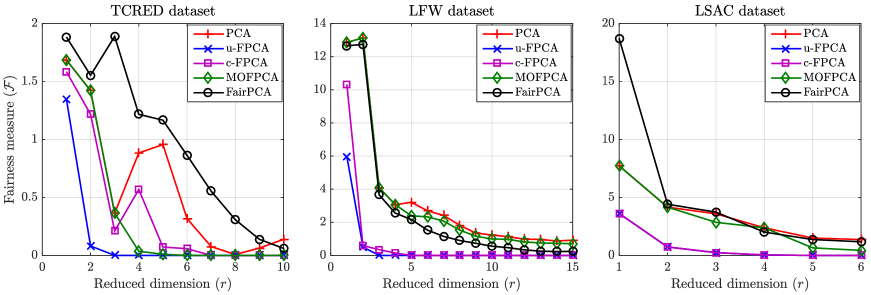

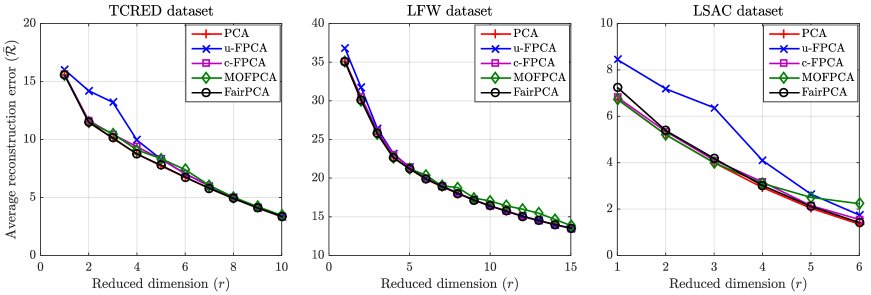

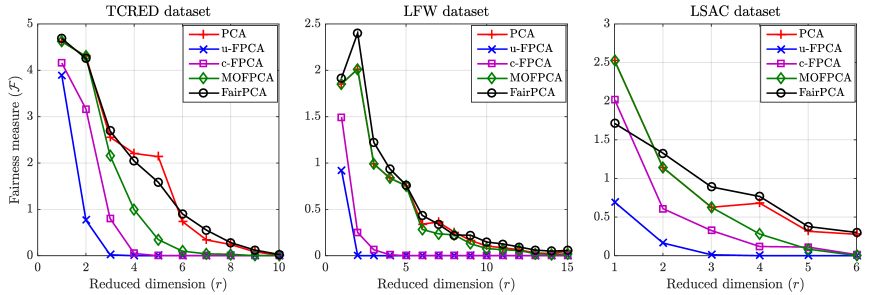

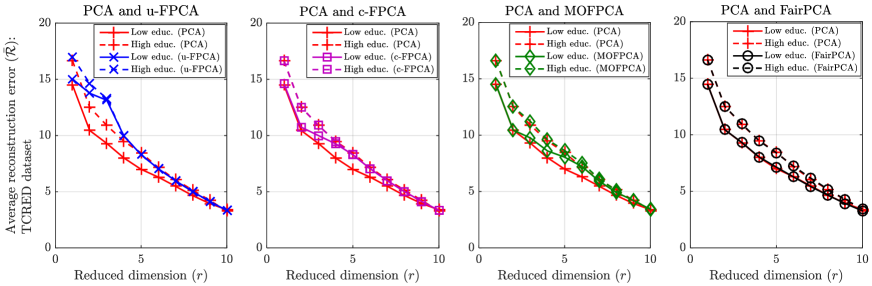

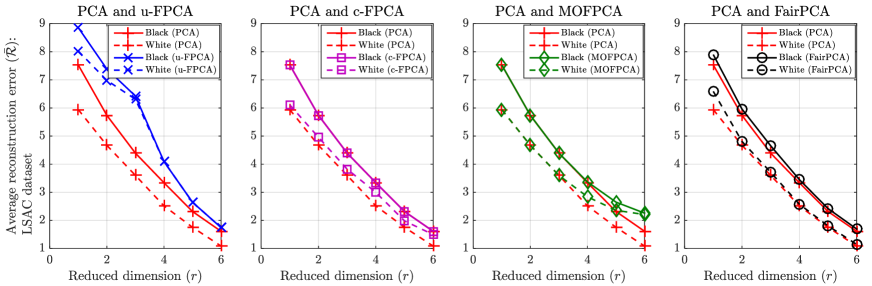

We first addressed scenarios with unbalanced datasets, i.e., when . Figure 2 presents the reconstruction errors and the fairness measures for different reduced dimensions. In all cases, the u-FPCA approach led to the lower values of fairness measure. However, since this approach allows an increase of the reconstruction error of both groups in order to achieve fairness, in some datasets we obtained higher overall reconstruction errors in comparison with MOFPCA and FairPCA (see Figure 2a). However, if we consider the c-FPCA approach, we achieve good values of fairness with a small loss in the overall reconstruction error in comparison with the u-FPCA approach. In other words, if we compare the reconstruction errors of groups and in different reduced dimensions, the c-FPCA approach could reduce the disparities between these values without damaging the overall reconstruction error. Therefore, by comparing with the classical PCA, we achieved reconstruction errors such that , where group is the unprivileged group. Note, in Figure 3, that this is not always true for the u-FPCA approach.

Although the c-FPCA approach led to interesting results in fair dimension reduction problems, there was a specific scenario in which the MOFPCA achieved better results in terms of fairness. In the TCRED dataset and for a dimensionality reduction into 4, 5 and 6-dimensional samples, the MOFPCA practically eliminated the disparity between the sensitive groups. However, as can be seen in Figure 3a, it payed the same price as the u-FPCA: the reconstruction error of both groups increased. As we have already mentioned, this can be a problem in practical applications, and a projection with a better compromise between the objectives, such as the one provided by the c-FPCA proposed approach, could be a good solution for the dimensionality reduction problem. With respect to the FairPCA algorithm, most results are close (or even worst) to the classical PCA (see Figure 2 ). However, it is important to recall that the fairness measure in FairPCA is different from the one adopted in this paper.

4.2 Fair dimensionality reduction: Balanced datasets

In the previous experiment, we considered unbalanced datasets and showed the interesting results provided by the proposed c-FPCA approach. However, since some bias in machine learning comes from unbalanced datasets, there may be a concern if our proposals only works on such scenarios. Motivated by this question, in this experiment, we verify the consistency of our proposals in balanced scenarios for each dataset. For this purpose, we considered the same datasets and selected a subset of samples666We selected the first samples of each group, where is the minimum between and . such that . Therefore, there will not be an interference of unbalanced data in the dimension reduction problem.

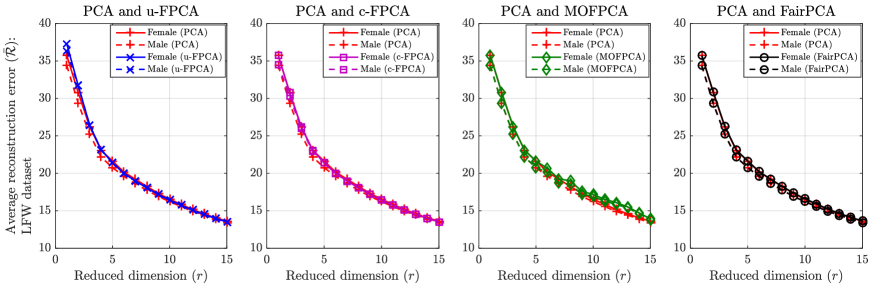

Figures 4 and 5 present the obtained results. Similarly as in the previous experiment, the u-FPCA approach achieved very good results in terms of fairness. However, there were some considerable loss in the overall reconstruction error. Although it reduced the disparity, the reconstruction error of both groups increased (see the u-FPCA results in Figure 5). Conversely, for all datasets, the c-FPCA approach could improve fairness with a very small loss in the overall reconstruction error. Therefore, it was consistent with the previous experiment.

If one analyzes the results provided by the MOFPCA, there was a slightly improvement in some reduced dimensions (see Figure 4b). However, the c-FPCA could further improve fairness with a lower loss in the overall reconstruction error. With respect to the FairPCA, the achievements were consistent with the previous experiment, with results very similar to the classical PCA, or even worst in some scenarios (see the TCRED and the LSAC datasets in Figure 4). We note such a similarity in the reconstruction errors of both sensitive groups, which are practically the same as in the application of the classical PCA (see the FairPCA results in Figure 5).

5 Conclusion

In this paper, we addressed the problem of fair dimensionality reduction based on principal component analysis. Since the classical PCA only minimizes the overall reconstruction error of a dataset, it was not conceived in order to avoid possible disparities between sensitive groups. As a consequence, the application of such a technique may lead to a reduced dataset in which a specific group is underrepresented with respect to another one. This may create (or even increase) social bias.

In order to maximize the information retained in the dimensionality reduction while mitigating disparities between sensitive groups, we formulate an optimization problem that exploits both overall reconstruction error and fairness measure when searching for the projection matrix. We also proved that the solution of such a formulation is as simple as the solution of the classical PCA, which consists of an eigendecomposition. Moreover, we proposed two one-dimensional algorithms, which exploit eigendecomposition solutions, to achieve a fair dimensionality reduction. Therefore, our proposal can be easily deployed in any already running systems.

The experimental results in several real datasets attested that our proposal can find a projection matrix that minimizes the disparity between the sensitive groups without a large loss in the overall reconstruction error. Moreover, in contrast with other existing methods, our results were consistent in scenarios with both unbalanced and balanced data.

It is worth highlighting that this article addresses the fairness issue in unsupervised dimensionality reduction. However, ongoing works extend our proposal in supervised principal component analysis. In this context, the fair dimensionality reduction technique can find a projection matrix that improve the classification accuracy while reducing the disparity between the true/false positive/negative rates of sensitive groups.

Acknowledgements

The authors would like to thank the grants #2020/01089-9, #2020/09838-0, #2020/10572-5 and #2021/11086-0, São Paulo Research Foundation (FAPESP), and the grant #311357/2017-2, National Council for Scientific and Technological Development (CNPq), for the financial support.

Eigenvectors as a solution for PCA

In this section, we demonstrate that the solution of PCA consists of the eigenvectors associated with the highest eigenvalues of the covariance matrix of . We follow an iterative approach [4], which starts by searching for an unitary projection vector that maximizes the variance of the projected data . This variacne is given by , where is the covariance of . The optimization problem is the following:

| (10) |

This optimization problem can be easily solved by using the Lagrange multipliers [35], which leads to:

| (11) |

By taking the gradient of this cost function, one obtains that

| (12) |

where one recognizes that is an eigenvector of and is the associated eigenvalue. Therefore, the first projection vector is the eigenvector associated with the highest eigenvalue of the covariance matrix . Moreover, since , , i.e., the variance in is given by the highest eigenvalue of .

Once one has found the first principal component, one may move to the second one. Other than the constraint that ensures a unitary vector, one also needs to guarantee that the second principal component is orthogonal to the first one, i.e., . This leads to the following optimization problem:

| (13) |

One may also deal with (13) by means of the Lagrange multipliers:

| (14) |

By taking the gradient of this cost function, one obtains that

| (15) |

If one multiplies the aforementioned equation on the left by and since one assumed that , one obtains that

| (16) |

Since we want that the projections and are uncorrelated, i.e., , this implies that and, therefore, must be equal to zero. One may also verify this condition on by taking (15) and, since , . This leads to the following expression:

| (17) |

where one also recognizes that is an eigenvector of and is the associated eigenvalue. In other words, the second principal component coefficients are the eigenvector associated with the second highest eigenvalue of . Moreover, the variance in the projected data is also equivalent to the second highest eigenvalue of .

For the next principal components, the aforementioned technique can be iteratively used to find the projection matrix whose columns are composed by the eigenvectors of .

References

- [1] S. Kaski and J. Peltonen. Dimensionality reduction for data visualization [Applications Corner]. IEEE Signal Processing Magazine, 28(2):100–104, 2011.

- [2] X. Huang, L. Wu, and Y. Ye. A review on dimensionality reduction techniques. International Journal of Pattern Recognition and Artificial Intelligence, 33(10):1950017, 2019.

- [3] G. T. Reddy, M. P. K. Reddy, K. Lakshmanna, R. Kaluri, D. S. Rajput, G. Srivastava, and T. Baker. Analysis of dimensionality reduction techniques on big data. IEEE Access, 8:54776–54788, 2020.

- [4] I. T. Jolliffe. Principal component analysis. Springer-Verlag, New York, 2 edition, 2002.

- [5] M.-S. Kang, J.-H. Bae, B.-S. Kang, and K.-T. Kim. ISAR Cross-Range Scaling Using Iterative Processing via Principal Component Analysis and Bisection Algorithm. IEEE Transactions on Signal Processing, 64(15):3909–3918, 2016.

- [6] H. Zhao, J. Zheng, J. Xu, and W. Deng. Fault diagnosis method based on principal component analysis and broad learning system. IEEE Access, 7:99263–99272, 2019.

- [7] C.-M. Feng, Y. Xu, J.-X. Liu, Y.-L. Gao, and C.-H. Zheng. Supervised Discriminative Sparse PCA for Com-Characteristic Gene Selection and Tumor Classification on Multiview Biological Data. IEEE Transactions on Neural Networks and Learning Systems, 30(10):2926–2937, 2019.

- [8] I. Chakraborty, D. Roy, I. Garg, A. Ankit, and K. Roy. Constructing energy-efficient mixed-precision neural networks through principal component analysis for edge intelligence. Nature Machine Intelligence, 2(1):43–55, 2020.

- [9] D. Rajani and P. R. Kumar. An optimized blind watermarking scheme based on principal component analysis in redundant discrete wavelet domain. Signal Processing, 172:107556, 2020.

- [10] S. Barocas, M. Hardt, and A. Narayanan. Fairness in machine learning. fairmlbook.org, 2019.

- [11] V. Mhasawade, Y. Zhao, and R. Chunara. Machine learning and algorithmic fairness in public and population health. Nature Machine Intelligence, 3:659–666, 2021.

- [12] B. M Booth, L. Hickman, S. K. Subburaj, L. Tay, S. E. Woo, and S. K. D’Mello. Integrating Psychometrics and Computing Perspectives on Bias and Fairness in Affective Computing: A case study of automated video interviews. IEEE Signal Processing Magazine, 38(6):84–95, 2021.

- [13] J. Cheong, S. Kalkan, and H. Gunes. The Hitchhiker’s Guide to Bias and Fairness in Facial Affective Signal Processing: Overview and techniques. IEEE Signal Processing Magazine, 38(6):39–49, 2021.

- [14] J. Kleinberg, S. Mullainathan, and M. Raghavan. Inherent trade-offs in the fair determination of risk scores. In C. H. Papadimitriou, editor, 8th Innovations in Theoretical Computer Science Conference (ITCS 2017). Leibniz International Proceedings in Informatics (LIPIcs), volume 67, pages 43:1–23, Dagstuhl, Germany, 2017. Schloss Dagstuhl–Leibniz-Zentrum fuer Informatik.

- [15] J. Dressel and H. Farid. The accuracy, fairness, and limits of predicting recidivism. Science Advances, 4(eaao5580):1–5, 2018.

- [16] Christian Haas. The price of fairness - A framework to explore trade-offs in algorithmic fairness. In 40th International Conference on Information Systems (ICIS 2019), Munich, Germany, 2019.

- [17] T. Zhang, T. Zhu, J. Li, M. Han, W. Zhou, and P. Yu. Fairness in semi-supervised learning: Unlabeled data help to reduce discrimination. IEEE Transactions on Knowledge and Data Engineering, pages 1–1, 2020.

- [18] K. T. Rodolfa, H. Lamba, and R. Ghani. Empirical observation of negligible fairness–accuracy trade-offs in machine learning for public policy. Nature Machine Intelligence, 3(10):896–904, 2021.

- [19] T. Zhang, T. Zhu, K. Gao, W. Zhou, and P. S. Yu. Balancing Learning Model Privacy, Fairness, and Accuracy With Early Stopping Criteria. IEEE Transactions on Neural Networks and Learning Systems, pages 1–13, 2021.

- [20] G. D. Pelegrina, R. D. B. Brotto, L. T. Duarte, R. Attux, and J. M. T. Romano. A novel multi-objective-based approach to analyze trade-offs in Fair Principal Component Analysis. ArXiv ID: 2006.06137v2, 2021.

- [21] M. M. Kamani, F. Haddadpour, R. Forsati, and M. Mahdavi. Efficient fair principal component analysis. Machine Learning, pages 1–32, 2022.

- [22] S. Samadi, U. Tantipongpipat, J. Morgenstern, M. Singh, and S. Vempala. The price of fair PCA: One extra dimension. In Advances in Neural Information Processing Systems, pages 10976–10987, 2018.

- [23] M. Olfat and A. Aswani. Convex formulations for fair principal component analysis. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 663–670, 2019.

- [24] U. Tantipongpipat, S. Samadi, M. Singh, J. Morgenstern, and S. Vempala. Multi-criteria dimensionality reduction with applications to fairness. In Advances in Neural Information Processing Systems 32 (NIPS 2019), pages 15161–15171, Vancouver, Canada, 2019.

- [25] J. Morgenstern, S. Samadi, M. Singh, U. Tantipongpipat, and S. Vempala. Fair dimensionality reduction and iterative rounding for SDPs. ArXiv ID: 1902.11281, 2019.

- [26] G. Zalcberg and A. Wiesel. Fair principal component analysis and filter design. IEEE Transactions on Signal Processing, 69:4835–4842, 2021.

- [27] G. H. Golub and C. F. Van Loan. Matrix computations. Johns Hopkins University Press, Baltimore, Maryland, 4 edition, 2013.

- [28] R. Bro and A. K. Smilde. Principal component analysis. Analytical Methods, 6(9):2812–2831, 2014.

- [29] Q. Wang, Q. Gao, X. Gao, and F. Nie. -norm based PCA for image recognition. IEEE Transactions on Image Processing, 27(3):1336–1346, 2018.

- [30] P. Huang, Q. Ye, F. Zhang, G. Yang, W. Zhu, and Z. Yang. Double L2,p-norm based PCA for feature extraction. Information Sciences, 573:345–359, 2021.

- [31] S. Vajda. Fibonacci and Lucas numbers, and the golden section: Theory and applications. Ellis Horword Limited, Chichester, UK, 1989.

- [32] I.-C. Yeh and C.-H Lien. The comparisons of data mining techniques for the predictive accuracy of probability of default of credit card clients. Expert Systems with Applications, 36:2473–2480, 2009.

- [33] G. B. Huang, M. Mattar, T. Berg, and E. Learned-Miller. Labeled faces in the wild: A database for studying face recognition in unconstrained environments. In Workshop on Faces in ’Real-Life’ Images: Detection, Alignment, and Recognition, Marseille, France, 2008.

- [34] L. F. Wightman. LSAC national longitudinal bar passage study. Technical report, 1998.

- [35] R. J. Vanderbei. Linear programming: Foundations and extensions. Springer Science+Business Media, New York, 4 edition, 2014.