Robust Tests of Model Incompleteness in the Presence of Nuisance Parameters††thanks: We thank for their comments Iván Fernández-Val, Jean–Jacques Forneron, Bryan Graham, Hidehiko Ichimura, Paul Koh, Lixiong Li, Francesca Molinari, Pierre Perron, Zhongjun Qu, Marc Rysman, Katsumi Shimotsu, Kevin Song, Guang Zhang, and seminar and conference participants at Boston University, Johns Hopkins University, University of Tokyo, and the North American Meeting of the Econometric Society 2023. Kaido gratefully acknowledges financial support through NSF Grant SES-2018498.

Abstract

Economic models may exhibit incompleteness depending on whether or not they admit certain policy-relevant features such as strategic interaction, self-selection, or state dependence. We develop a novel test of model incompleteness and analyze its asymptotic properties. A key observation is that one can identify the least-favorable parametric model that represents the most challenging scenario for detecting local alternatives without knowledge of the selection mechanism. We build a robust test of incompleteness on a score function constructed from such a model. The proposed procedure remains computationally tractable even with nuisance parameters because it suffices to estimate them only under the null hypothesis of model completeness. We illustrate the test by applying it to a market entry model and a triangular model with a set-valued control function.

Keywords: Incomplete models, Discrete choice models, Strategic interaction, Score tests

1 Introduction

Discrete choice models are used widely. A common empirical strategy is to combine a theory of choice (e.g., utility maximization) that predicts a unique outcome value with distributional assumptions on latent variables (McFadden, 1981). This approach allows the researcher to derive the conditional distribution of the outcome given covariates and apply likelihood-based inference methods. However, recent economic applications often involve models that permit multiple outcome values, which we call an incomplete prediction. Such an incomplete prediction occurs when the researcher is willing to work only with weak assumptions or has limited knowledge of the data-generating process.

This paper considers a form of incompleteness summarized as follows. An observable discrete outcome satisfies

| (1.1) |

where collects all outcome values compatible with the model given observed and unobserved variables and a structural parameter . This structure arises in a variety of contexts. For example, multiple outcomes are predicted in single-agent discrete choice models when the agent’s unobservable choice set is consistent with a wide range of choice set formation processes (Barseghyan et al., 2021). Multiple equilibria may exist in discrete games such as firms’ market entry or household labor supply decisions, but one may not know how an equilibrium outcome gets selected (Bresnahan and Reiss, 1991; Ciliberto and Tamer, 2009). Recent empirical studies have applied inference methods for incomplete models in different areas; they include English auctions (Haile and Tamer, 2003), strategic voting (Kawai and Watanabe, 2013), product offerings (Eizenberg, 2014; Wollmann, 2018), network formation (de Paula et al., 2018; Sheng, 2020), school choice (Fack et al., 2019), and major choice (Henry et al., 2020).

This paper focuses on developing tests to determine if a structural model is incomplete. The completeness of a model is important when considering its policy implications. For example, in a canonical market-entry model, multiple equilibria exist only if firms strategically interact. Testing for strategic interaction effects and inferring their signs can provide valuable information for policymakers (de Paula and Tang, 2012). In a triangular model with a discrete endogenous variable, the control function approach yields an incomplete model, but it remains complete if the assignments are exogenous. Detecting self-selection can aid practitioners in selecting a proper strategy for evaluating treatment effects. Dynamic discrete choice models can make incomplete predictions when they admit state dependence, but they are complete without it. The presence of state dependence can significantly impact program evaluation and counterfactual analyses (Card and Hyslop, 2005; Handel, 2013).

In many of these examples, one can state the null hypothesis of model completeness as a restriction on the parameter’s subvector. We develop a novel score test for such a restriction. Advantages of this approach are (i) the score statistic only requires estimation of nuisance parameters in the complete restricted model; (ii) one can use package software to estimate the nuisance parameters; and (iii) simulating the score statistic’s limiting distribution is straightforward.

Our focus is on models that are complete under the null hypothesis. This structure makes score-based tests appealing. First, one can obtain a unique likelihood function for any null parameter value , thanks to the model’s completeness. For each alternative parameter value , the model implies multiple (typically infinitely-many) likelihood functions. However, the recent work of Kaido and Zhang (2019) demonstrates that one can identify a "least favorable" density that is most difficult to distinguish from . We may then consider the family as a "least favorable parametric model". Second, we can use the least favorable parametric family to calculate a score function. We then construct a score-based statistic that maximizes a measure of local discrimination. The resulting test is robust to incompleteness because it detects any local deviation from the null hypothesis regardless of how is selected from the predicted set.

The score test has another appealing feature wherein one can estimate nuisance parameters within the complete restricted model. Typically, the null hypothesis does not restrict some components of . By exploiting the model completeness, we demonstrate that one can construct a restricted maximum likelihood estimator (RMLE) of these nuisance components that is -consistent. This estimator is usually simple to calculate using package software. Next, we insert the estimator into the score formula to compute a test statistic. The suggested procedure is computationally tractable since it avoids evaluating the test statistic over a grid of nuisance parameters. Finally, we derive the score-based statistic’s limiting distribution and demonstrate that it can be easily simulated. Although there are existing methods to test restrictions on subvectors of , they can be computationally expensive since they are not designed to utilize the model completeness under the null hypothesis. This paper presents a procedure that makes use of the model structure to simplify its implementation. Through a Monte Carlo experiment, we also show that the proposed test has significantly higher power than a general subvector test that does not utilize the structure.

1.1 Relation to the Literature

Our paper belongs to the literature on inference in incomplete models pioneered by Wald (1950) in the context of simultaneous equations models and by Jovanovic (1989) in the context of models with multiple equilibria. The seminal work of Tamer (2003) shows an incomplete model induces multiple distributions and implies partially identifying restrictions on parameters. Developments in the literature (Galichon and Henry, 2011; Beresteanu et al., 2011; Chesher and Rosen, 2017) provided tools to systematically derive so-called sharp identifying restrictions, which convert all model information into a set of equality and inequality restrictions on the conditional moments of observable variables. Inference methods based on the sample analogs of moment restrictions are extensively studied (see Canay and Shaikh, 2017, and references therein). Our approach builds on recent developments in likelihood-based inference methods for incomplete models (Chen et al., 2018; Kaido and Zhang, 2019). In particular, we combine the sharp identifying restrictions with the framework of Kaido and Zhang (2019) to derive the least favorable parametric model and its score. To our knowledge, this approach is new. One can view our procedure as an analog of deriving a score function from a parametric family in a complete model.

Hypothesis testing in incomplete models is studied extensively. As discussed earlier, many of them are based on the sample analogs of conditional or unconditional moment restrictions. A challenge in making inferences is the high computational cost of implementing existing methods, as noted in Molinari (2020). There are attempts to improve the computational tractability of moment-based inference methods within specific classes of models or testing problems, such as those made by Andrews et al. (2019) and Cox and Shi (2020), who assume that moment inequality restrictions are linear conditional on observable variables. This paper focuses on another class in which the model is complete under the null hypothesis. This structure makes our test computationally tractable by combining (i) the score function associated with the least favorable parametric model and (ii) a point estimator of the nuisance components.

Practitioners can use this paper’s framework to test various hypotheses. For example, one can examine the exsitence of strategic interaction effects and multiple equilibria in static complete information games. Related problems are studied in other models. For incomplete information games, de Paula and Tang (2012) introduced a semiparametric inference procedure on the signs of strategic interaction effects. For finite-state Markov games, Otsu et al. (2016) developed techniques to test whether the conditional choice probabilities, state transition, and other features of games are homogeneous across cross-sectional units. Rejecting their null hypothesis may indicate the presence of multiple equilibria. Pelican and Graham (2021) studied a testing problem that involves determining whether agents’ preferences are interdependent in a network formation model. The problem includes nuisance parameters that account for degree heterogeneity and homophily. Using the logit structure, they constructed a sufficient statistic for the nuisance parameters and developed a conditional score test. This paper and Pelican and Graham (2021) consider testing in settings with a complete model under the null and an incomplete model under the alternative. The two papers take different approaches by exploiting the structures of the respective models. Specifically, we use the least favorable parametric model and estimate nuisance parameters using the restricted MLE. In contrast, Pelican and Graham (2021) utilized a sufficient statistic for the nuisance parameters.

One can apply our framework to triangular systems involving a binary outcome and a discrete endogenous variable. We show that taking a control function approach in such a setting leads to a model with an incomplete prediction.111A nonparametric identification analysis based on set-valued control functions is undertaken in another paper. We provide a test of endogenous treatment assignments under weak assumptions. To our knowledge, this test is new and provides an alternative to the existing proposal by Wooldridge (2014), who makes additional high-level assumptions.

2 Set-up

Let be a discrete outcome taking values in a finite set . Let be a vector of observable covariates and let be a vector of unobservable variables. We equip , and with their Borel -algebra. In what follows, we use upper case letters for random elements (e.g., ) and lower case letters (e.g., ) for the values they can take. Let be a finite-dimensional parameter, where is a convex parameter space with a nonempty interior.

A set-valued map summarizes the prediction of a structural model. We assume is weakly measurable for every and takes one of the values in with probability 1.222A set-valued map is weakly measurable if its weak inverse image is measurable for any open set . A random element with this property is said to be a measurable selection of the random closed set (Molchanov, 2005). The map describes how observable and unobservable characteristics translate into a set of possible outcome values. It reflects restrictions imposed by theory, such as the functional form of utility/profit functions, forms of strategic interaction, and any equilibrium or optimality concepts. Importantly, can contain multiple values. This feature allows the researchers to encode their lack of understanding of parts of the structural model.

The formulation above also nests the standard setting in which the model is characterized by a reduced form equation:

| (2.1) |

for a function . In this case, is almost surely singleton-valued, i.e., , and we say the model makes a complete prediction.

Throughout, we assume ’s law belongs to a parametric family , where, for each , is a probability distribution on . To keep notation concise, we use the same for parameters that enter and that index . Also, we focus on settings in which is independent of . However, the framework can be easily extended to settings where is correlated with , and the researcher specifies its conditional distribution . Furthermore, our framework accommodates settings in which some of the observable covariates are endogenous, and one can construct a set-valued control function (See Example 2 below).

2.1 Motivating examples

We illustrate the objects introduced above with examples. Our first example is a discrete game of complete information (Bresnahan and Reiss, 1991; Ciliberto and Tamer, 2009).

Example 1 (Discrete Games of Strategic Substitution).

There are two players (e.g., firms). Each player may either choose or . The payoff of player is

| (2.2) |

where is the opponent’s action, is player ’s observable characteristics, and is an unobservable payoff shifter. The payoff is summarized in the table below and is assumed to belong to the players’ common knowledge.

| Player | |||

|---|---|---|---|

| Player | |||

| , | |||

The key parameter is the strategic interaction effect which captures the impact of the opponent’s taking on player ’s payoff. Suppose that for both players.333This restriction is often used in models of market entry. Games with strategic complementarity (i.e., ) can be analyzed similarly. Suppose that the players play a pure strategy Nash equilibrium (PSNE). Then, one can summarize the set of PSNEs by the following correspondence:

| (2.3) |

where, , and .

Note: ; .

Left Panel: and the model is complete. Right panel: and and the model is incomplete. in (2.3) corresponds to the region in green, and similarly is the region in red. Multiple equilibria are predicted in the blue region.

The next example is a parametric version of triangular nonseparable equations with binary outcome and treatment (Chesher, 2003; Shaikh and Vytlacil, 2011). We consider a control function approach applied to the triangular system.

Example 2 (Triangular Models with a Set-valued Control Function).

Consider a triangular model, in which a binary outcome is determined by a binary treatment , a vector of exogenous covariates, and an unobserved variable . The binary treatment is determined by a vector of instrumental variables and an unobserved variable .

| (2.4) | ||||

| (2.5) |

The unobserved variables may be dependent rendering potentially endogenous. We assume that is independent of .

If one could recover from the observables (which would be possible with a continuous ), conditioning on would make independent of , i.e. . This control function approach would allow us to recover structural parameters (Blundell and Powell, 2004; Imbens and Newey, 2009; Wooldridge, 2015). With a binary endogenous variable, we cannot uniquely recover .444Alternatively, Wooldridge (2014) uses the generalized residual from the first stage MLE, where is the inverse Mills ratio. He makes additional high-level assumptions so that is a sufficient statistic for capturing the endogeneity of and proposes an estimator of the average structural function. Instead of taking this approach, we explore what can be learned from the set-valued control function. However, the model restricts to the following set-valued control function:

| (2.6) |

This set contains the actual control function as its measurable selection. Suppose that the conditional distribution belongs to a location family, in which the location parameter is . Then, one may write for some independent of . Substituting this expression into (2.4), we can summarize the model’s prediction by

| (2.7) |

where and with . When is positive, one can simplify further:

| (2.8) |

As we show below, the control function approach allows one to test the endogeneity of even if the control function is set-valued.555We take a control function approach that conditions on , which only requires specification of the conditional distribution of given . Alternatively, one could take the vector as endogenous variables and specify the joint distribution of . This alternative approach with a stronger assumption would imply a complete model (Lewbel, 2007).

The next example is a panel dynamic discrete choice model (Heckman, 1978; Chamberlain, 1985; Hyslop, 1999).

Example 3 (Panel Dynamic Discrete Choice Models).

An individual makes binary decisions across multiple periods according to

| (2.9) |

where is a binary outcome for individual in period , is a vector of observable covariates, is an unobservable individual specific effect, and is an unobserved idiosyncratic error. We use and to denote realizations of and respectively. If is nonzero, the individual’s choice in period depends on her past choice, rendering the decision state dependent.

Suppose the researcher observes for and . Without any knowledge of , the dynamic restrictions (2.9) alone do not fully determine the value of (Heckman, 1978, 1981; Honoré and Tamer, 2006).666As an alternative, one could work with the likelihood function conditional on the initial observation. However, this approach can be problematic if one wants to be internally consistent across different periods (Honoré and Tamer, 2006; Wooldridge, 2005). Consider . Suppose for the moment . For a given and , the outcome must satisfy

| (2.10) | ||||

| (2.11) |

Similarly, if , the outcome must satisfy

| (2.12) | ||||

| (2.13) |

Without further assumptions, the model permits both possibilities. Let with . One can summarize the model prediction by

| (2.14) |

If , one can express this correspondence as follows:777Appendix B.3 provides details and a graphical illustration of .

| (2.15) |

Figure 2 summarizes . The model makes a complete prediction when there is no state dependence, i.e., (left panel).

Note: The level sets of when (left) and (right). ; .

Multiple outcome values are predicted in the red, blue, and green regions.

3 Testing Hypotheses

Let denote the subvector of whose value determines whether the model is complete or not. Let collect the remaining components of . Given a sample of data , consider testing

| (3.1) |

where is a set not containing . For instance, in entry games (i.e. Example 1), the presence of strategic substitution effects can be tested by letting and .888Our framework also nests settings in which the researcher tests one of the interaction effects, e.g., and . In this case, the model is complete under both hypotheses. Our test then reduces to a conventional score test. Similarly, we may test the potential endogeneity of treatment assignments (Example 2) and the presence of state dependence (Example 3) by setting and choosing suitable alternative hypotheses. In what follows, we let and .

Let denote the set of conditional distributions of given . For each , an incomplete model admits the following set of conditional distributions:

| (3.2) |

The conditional distribution represents the unknown selection mechanism according to which an outcome gets selected from . Reflecting the lack of understanding of the selection, we allow any law supported on . Consequently, the model can admit (infinitely) many likelihood functions for a given . Let be the counting measure on For each , define

| (3.3) |

This set collects all (conditional) densities compatible with a given . In the case of discrete games (Examples 1), this set contains all densities of equilibrium outcomes that are compatible with the game’s description. Similarly, in the context of panel discrete choice (Example 3), this set collects all densities of individual choices consistent with arbitrary specifications of the initial condition. Observe that reduces to a singleton set if the model is complete, in which case with .

While the multiplicity of likelihood functions may appear challenging, can be simplified, and this property also simplifies our tests. By Artstein’s inequality, we may rewrite as follows (see e.g. Galichon and Henry, 2011; Molinari, 2020):

| (3.4) |

where

| (3.5) |

is the conditional containment functional (or belief function) associated with the random set . This function gives the sharp lower bound for the conditional probability across all ’s belonging to .999The upper bound for is given by the capacity functional . It is sufficient to use either of the lower or upper bounds in (3.4) because the bounds are related to each other through the conjugate relationship . Theoretical properties of the containment functional and numerical approximation methods are well studied.101010See Molchanov (2005) for a general treatment. For numerical approximations, see Ciliberto and Tamer (2009); Galichon and Henry (2011). We briefly review them in Appendix A. For us, it is important that the linear inequalities in (3.4) characterize . Together with an extended Neyman-Pearson lemma reviewed below, this characterization makes the score computation feasible. In the following subsection, we briefly review the existing results we will rely on.

3.1 Least Favorable Parametric Model

Let denote the true conditional density of given . Consider distinguishing a parameter value from another value in a parametric model of conditional densities. This amounts to testing a simple null hypothesis against a simple alternative hypothesis . By the Neyman-Pearson lemma, the most powerful test is the likelihood-ratio (LR) test. In incomplete models, corresponding null and alternative hypotheses would be and rendering both hypotheses composite. Kaido and Zhang (2019) showed that it was possible to extend the Neyman-Pearson lemma to such settings, building on a general result by Huber and Strassen (1973). We briefly summarize their results below.

Let be a test and be its rejection probability, under conditional density and the marginal distribution of .111111The rejection probability can be written as . Only the conditional expectation depends on . For a given , the power guarantee of is , which is the power value certain to be obtained regardless of the unknown selection mechanism. Kaido and Zhang (2019) seeked for a level- minimax test (see e.g. Lehmann and Romano, 2005) such that

| (3.6) |

and

| (3.7) |

The minimax test is a procedure that maximizes the power guarantee among tests that meet the uniform size control requirement.

Results from Huber and Strassen (1973) imply that, when , the rejection region of a minimax test is of the form for a measurable function . Furthermore, there is a least favorable pair (LFP) of densities such that for all ,

| (3.8) |

and

| (3.9) |

where . That is, is a density consistent with and least favorable for controlling the size of a test among all elements of , and is a density consistent with and least favorable for maximizing a measure of power among all elements of . Kaido and Zhang (2019) exploited these features to show that a level- minimax test is an LR test based on the LFP:

where solves

One can also characterize the LFP as a solution to the following convex program.

| (3.10) | ||||

| (3.11) | ||||

| (3.12) |

The constraints in (3.11) and (3.12) are the sharp identifying restrictions.121212A common way to use them for identification analysis is to define the sharp identified set as That is, given the conditional probability identified from data, one collects all values of satisfying the sharp identifying restrictions. For hypothesis testing, we instead fix and ask what would be a distribution among all distributions satisfying the sharp identifying restrictions, which is least favorable for controlling the size or maximizing the power. In view of (3.4), they are equivalent to imposing the restrictions that belongs to and belongs to respectively. These restrictions are useful for computing the LFP because they are linear in . Also, the objective function is strictly convex in . One can solve the convex program above numerically in general. For the examples we discussed earlier, it is also possible to compute the LFP analytically (see Appendix B).

To illustrate, let us consider Example 1. Suppose that the latent payoff shifters follow a bivariate standard normal distribution. We may then compute for each event. Let us take as an example. Using (2.3) and (3.5), we obtain

| (3.13) |

The last expression corresponds to the probability assigned to the green region in Figure 1 (right panel) and is the sharp lower bound for the probability of .

Now consider two parameter values and , where with for . As discussed in more detail below, the model is complete when One can show that (3.11) reduces to the following equality restrictions:

| (3.14) | ||||

| (3.15) | ||||

| (3.16) | ||||

| (3.17) |

They uniquely determine the least-favorable null density as follows

| (3.18) |

where, to ease notation, we use and to denote and .

When , there are multiple densities satisfying (3.12). The least favorable alternative density can be found by minimizing (3.10) with respect to subject to (3.12). The solution can be expressed analytically. For example, when player 1’s strategic interaction effect on player 2 is relatively high, it is given by the following form:131313Appendix B.1 gives a full characterization of the LFP for Example 1.

| (3.19) |

Comparing (3.18) and (3.19), one can see that tends to as approaches its null value (i.e. 0). Hence, one may view as a “parametric” model. For each , the density corresponds to the data generating process that is least favorable in detecting ’s deviation from its null value among all densities compatible with . By varying , we may trace out a family of such densities and form a parametric model. We define a least favorable (LF) parametric model as follows.

Definition 1 (Least favorable parametric model).

Let be an open set containing . A family of densities is the least favorable (LF) parametric model indexed by if (a) is the unique element of for any ; and (b) is the density of the least-favorable alternative distribution if , i.e., constitutes a LFP with and .

Part (a) of the definition above is natural because the model is complete under the null hypothesis. Part (b) deserves discussion. We associate each alternative parameter value with a density that corresponds to the least favorable density for testing between and . In other words, for each , we focus on testing against using the least-favorable distribution for maximizing power. We construct this way because we aim at detecting local deviations in terms of . As we see below, this approach allows us to capture the sensitivity of with respect to a change in the parameter of interest through a score function.141414An alternative choice of is also possible, which we do not seek here because it does not seem to lead to a tractable score test. We provide a sufficient condition for the existence of an LF parametric model in the next section.

Let us also note the following points. First, having a complete null model is not sufficient for obtaining a score function. It also requires us to define parametric densities at local alternatives. Our approach is to select the density associated with the least favorable selection mechanism for power maximization. Second, we do not need to know the precise form of the selection mechanism that induces (for ). Solving the convex program, we “profile out” the selection mechanism and directly obtain the induced density . This is why is a function of only and does not involve any selection mechanism.

Coming back to equation (3.19), the formula suggests we may pretend as if data were generated by a parametric discrete choice model with the given density. Thanks to this feature, most of our analysis below will resemble that of standard discrete choice models.

3.2 Model Completeness under the Null Hypothesis

In this section, we start with an assumption to ensure that the LF parametric model is well-defined over a parameter set that contains the null parameter space and its neighborhood. For this, let , and let denote an open cube centered at the origin with edges of length .

Assumption 1.

(i) Under any null parameter value with , the model makes a complete prediction so that is a singleton set; (ii) There exists such that the two sets and are disjoint for any

Assumption 1 (i) holds whenever the model makes a complete prediction under the null hypothesis and is satisfied in the examples discussed in Section 2.1. The model can be incomplete under the alternative hypothesis. Assumption 1 (ii) requires does not share any element with . Under this condition, it is possible to detect local deviations from the null hypothesis regardless of the unknown selection mechanism. Such alternatives are robustly testable in the sense that there exists a test that has nontrivial power against any distribution in (Kaido and Zhang, 2019). For this condition, it suffices to have an event such that (or ) for all for some . All of the examples in Section 2.1 satisfy Assumption 1 (ii), and we demonstrate how to show this condition in Appendix B. We construct score tests that have power against robustly testable local alternatives.151515Kaido and Zhang (2019) extend the notion of local alternatives and analyze a more general setting that does not require Assumption 1 (ii). We conjecture that we may extend our framework similarly. Since all of our examples satisfy Assumption 1 (ii), we leave this extension elsewhere.

Let us revisit the examples.

Example 1 (Discrete Games of Strategic Substitution).

Consider testing the presence of strategic substitution effects by testing against . Under the null hypothesis, there is no strategic interaction between the players, which leads to the following complete prediction:

| (3.20) |

Hence, for any value of the observed and unobserved variables, contains a unique equilibrium outcome (left panel of Figure 1). Combining the complete prediction with a parametric assumption on ensures Assumption 1 (i)

We also note that Examples 2-3 reduce to complete models under the null hypothesis.161616To save space, we show Assumption 1 (ii) for these examples in Appendix B.

Example 2 (Triangular Models with a Set-valued Control Function).

Consider testing the endogeneity of the treatment by testing the hypothesis that the coefficient on the control function is 0. When the null hypothesis is true, the model’s prediction reduces to

| (3.21) |

This is a standard binary choice model with exogenous covariates. For a given , is uniquely determined. There is no need to control for because is independent of .

Example 3 (Panel Dynamic Discrete Choice Models).

Consider testing the presence of state dependence by testing whether the coefficient on the lagged dependent variable is 0. When in (2.9), the model reduces to a static panel binary choice model:

| (3.22) |

which makes (2.10)-(2.11) and (2.12)-(2.13) equivalent. Under , contains the unique outcome value satisfying (3.22).

We conclude this subsection with the following proposition.

Proposition 3.1.

Suppose Assumption 1 holds. Then, a least-favorable parametric model exists for .

3.3 Score Tests

Score-based tests such as Rao’s score (or Lagrange multiplier) test and Neyman’s test are widely used. They require the estimation of the restricted model only, which is particularly attractive in our setting. The restricted model is complete and typically admits point estimation of nuisance parameters under reasonably weak conditions. We take advantage of this property to carry out a score-based test. Below, we briefly review the core ideas behind the classic score tests and discuss extensions to handle potential model incompleteness under the alternative. For expositional purposes, we assume is differentiable with respect to for now and will weaken this assumption later.

Consider testing the null parameter value against a local alternative hypothesis , where . As discussed earlier, the optimal test in terms of guaranteed power is the likelihood-ratio test based on the LFP. The test is also robust in that, under Assumption 1 (ii), the log-likelihood ratio can detect any deviation from the null hypothesis with non-trivial power regardless of the selection mechanism.

One can locally approximate the log-likelihood ratio by , where is the score function. Let . For i.i.d. data, where . For a fixed , the normalized quantity

| (3.23) |

serves as a robust measure of discrimination between and . It locally approximates the log-likelihood ratio . The direction that maximizes (3.23) is , which motivates Rao’s score statistic:171717See Bera and Bilias (2001) for a more detailed argument for complete models. The same argument can be applied to incomplete models by replacing the standard likelihood function with the LF density .

| (3.24) |

Suppose that the nuisance parameter can be estimated by a point estimator . Evaluating the sample mean of the score at and imposing the null hypothesis yields

| (3.25) |

A feasible version of (3.24) is

| (3.26) |

where is an estimator of the asymptotic variance . For example, one can use the sample analog or its regularized version.181818For example, the following estimator proposed by Andrews and Barwick (2012) ensures that it is always nonsingular and is equivariant to scale changes (3.27) where , , and . Under regularity conditions, converges in distribution to a -distribution with degrees of freedom under the null hypothesis.

The analysis so far presumed that was differentiable, and was unrestricted. These assumptions may be restrictive in our context. For example, in discrete games of complete information, the least favorable parametric model and its score can take different functional forms depending on whether the alternative hypothesis admits strategic substitution (i.e. as in Example 1) or strategic complementarity (i.e. ). It is then natural to analyze these two cases separately. Below, we weaken differentiability requirements to accommodate these features and allow the alternative hypothesis to be restricted (e.g., one-sided).

Recall that a set is said to be locally equal to set if for some (Andrews, 1999).

Assumption 2 (-directional differentiability).

(i) is locally equal to a convex cone ; (ii) For any , there exists a square integrable function such that

| (3.28) |

as .

Assumption 2 (i) requires the set of deviations (from ) can be locally approximated by a convex cone. In Example 1, consider testing against . Then, is locally equal to

| (3.29) |

Assumption 2 (ii) uses the notion of differentiability in quadratic mean (see, e.g. van der Vaart, 2000), but it only requires that a unique score, in the sense of the -derivative of the square-root density, exists for the set of local deviations from the null hypothesis. This weaker assumption is appropriate for incomplete models, and can be derived from the least favorable parametric model similar to the standard parametric models (see Appendix B).

To accommodate the one-sided nature of the alternative hypothesis, we define a test statistic by

| (3.30) |

This test statistic is a modification of (3.26) and follows the construction in Silvapulle and Silvapulle (1995). It requires the same functions of data as , but it is designed to direct power against the local alternatives in . If the alternative hypothesis is locally unrestricted, i.e., , the test statistic reduces to .

The asymptotic distribution of is no longer a -distribution. However, its critical value is easy to compute using simulations. Let

| (3.31) |

where

| (3.32) |

which can be simulated by drawing repeatedly from a zero mean multivariate normal distribution with estimated variance

3.4 Restricted Maximum Likelihood Estimator

Let be the conditional density of given . By Assumption 1 (i), this density is unique. A natural estimator of is the restricted maximum likelihood estimator (RMLE) , which maximizes the log-likelihood function

| (3.33) |

The complete model (under ) is often a standard discrete choice problem. Hence, one can use package software (e.g., R, Stata) to compute the RMLE. Let us revisit the examples.

Example 1 (Discrete Games of Strategic Substitution).

Under , the model has a unique likelihood function as discussed in Section 3.1. The RMLE maximizes

where .

Example 2 (Triangular Models with a Set-valued Control Function).

When , there is no correlation between the errors in the outcome and selection equations. The outcome equation reduces to a binary choice model with exogenous covariates. If we assume , we obtain a probit model with

| (3.34) |

One can compute the RMLE of using package software. Similarly, the selection equation is another binary choice model. One can estimate the coefficients on the instruments similarly.

Example 3 (Panel Dynamic Discrete Choice Models).

A random effects probit model assumes is independent of and follows , and are independent standard normal random variables. This specification yields the following conditional density function:

| (3.35) |

One can construct a simulated likelihood function based on (3.35) to obtain a restricted MLE of (Train, 2009).

3.5 Asymptotic Properties

This section collects results on the asymptotic properties of the score test. The proofs of all theoretical results are in Appendix C. Throughout, we assume that is an independent and identically distributed (i.i.d.) sample drawn from , and is also an i.i.d. sample following . The joint distribution of the outcome sequence conditional on is not uniquely determined due to the potential incompleteness of the model. For , the distribution belongs to the following set:

| (3.36) |

where denotes the joint law of , and is the Cartesian product of the set-valued predictions. We let collect joint laws of ; each element of is such that the conditional law of given belongs to , and the law of is . Assuming and are i.i.d. does not imply is i.i.d. The set , in general, contains dependent and heterogeneous laws because the behavior of the selection mechanism across experiments is unrestricted (see Epstein et al., 2016). This feature does not create an issue for the size properties of our test because reduces to a single i.i.d. law under the null hypothesis.

For the asymptotic properties of the RMLE, we also allow to be in a local neighborhood of . For such settings, we provide conditions under which is -consistent. Let and . We assume data are generated from . The null hypothesis corresponds to the setting with .

Fixing , one can view as the conditional density of in a regular parametric model, in which is the only unknown parameter. For each , let , where expectation is taken with respect to the conditional density and the distribution of Let be the sample counterpart of defined in (3.33).

Assumption 3.

(i-a) There is a continuous function such that

(i-b) The map is Lipschitz continuous uniformly in . That is,

| (3.37) |

(i-c) with positive probability;

(ii) is a nonempty compact subset of Euclidean space;

(iii) The restricted MLE satisfies , for some sequence . For any and in a neighborhood of , .

Assumption 3 imposes sufficient conditions for identification and uniform law of large numbers standard in the literature. We also assume the density of depends on smoothly. For this, for any integrable function defined on a measure space , let be the -norm of .

Assumption 4.

For each , is absolutely continuous with respect to a -finite measure on . The Radon-Nikodym density satisfies

| (3.38) |

for some

Finally, the following condition ensures the population objective function is locally well behaved so that its value is informative about .

Assumption 5.

(i) is twice continuously differentiable at ;

(ii) The Hessian matrix

| (3.39) |

is negative definite.

Under these assumptions, the restricted MLE is -consistent.

Below, let be the joint law of under the null hypothesis. Let be the -th component of . Let

| (3.41) |

and let Next, we add a condition for the asymptotic distribution of and consistent estimation of the asymptotic variance .

Assumption 6.

(i) exists on a neighborhood of ;

(ii) and is continuous for any .

(iii) is nonsingular.

Here we assume the expected score can be linearized and the elements of obey a uniform law of large numbers. Suppose as defined in (3.30). The following theorem shows that the test controls its asymptotic size.

3.6 Inference on Parameters

In some applications, the ultimate goal may be to make inference on the underlying parameter, for example, to construct confidence intervals for components of . While we defer a formal analysis to future work, we suggest a hybrid procedure that aims at controlling the potential distortion of the model selection step, borrowing insights from the moment selection literature (Andrews and Soares, 2010; Romano et al., 2014).

Consider constructing confidence intervals for a component or linear combination of .191919Since the null hypothesis pins ’s value down, it is natural to consider inference on the parameters that are estimated under both null and alternative hypotheses. Due to Proposition 3.2, is a -consistent estimator of as long as the true value of is in a neighborhood of whose radius is of order . It would be natural to use such an estimator to construct a confidence interval for if the complete model is selected. A well-known challenge for such post-model selection inference is that a naive asymptotic approximation that disregards the model selection step may not be valid uniformly over a large class of data generating processes (Leeb and Pötscher, 2005; Andrews and Guggenberger, 2009). Given this, we consider the following hybrid method.

Step 1: Compute and , where is a sequence of shrinkage factors that tends to 0 slowly, e.g. ;

Step 2:

- •

-

•

Do not reject if . Construct the Wald confidence interval , where is the (estimated) standard error of its argument, and is the quantile of the standard normal distribution.

The heuristic behind this procedure is as follows. First, we compare to a critical value that tends to 0 slowly. For DGPs whose is outside local neighborhoods of , we cannot ensure the asymptotic validity of the Wald confidence interval. In such settings, the procedure above uses a robust confidence interval asymptotically, which controls the asymptotic coverage probability. Since the critical value tends to 0, we use the Wald confidence interval only if is in a local neighborhood of . The shrinkage factor , therefore, introduces a conservative distortion, which is expected to make the resulting confidence interval’s coverage probability above its nominal over a wide range of values.

4 Empirical Illustrations

We illustrate the score test through two empirical applications.

4.1 Testing Strategic Interaction Effects

The first application revisits the analysis of the airline industry by Kline and Tamer (2016). We test the presence of strategic interaction effects between two types of firms: low-cost carriers (LCC) and other airlines (OA). Below, we briefly summarize the setup and refer to Kline and Tamer (2016) for details. A market is defined as trips between airports regardless of intermediate stops. The two types of firms, LCC and OA, decide whether or not to serve each market. The binary variable takes value 1 if airline serves market . Airline ’s payoff in market equals

where captures the impact of the competitor’s entry decision, . The airline-specific intercepts and observable covariates determine each firm’s payoff. The covariates include the market size and the market presence . The market size is defined as the population at the endpoints of each trip. The latter variable measures the presence of firm in market (see Kline and Tamer (2016) p.356 for its definition). This airline-and-market-specific variable shows up only in firm ’s payoff. The data come from the second quarter of the 2010 Airline Origin and Destination Survey (DB1B) and contain 7882 markets.202020The data are available on Brendan Kline’s website.

Our hypothesis of interest is whether the LCCs and OAs compete strategically, which can be formulated as a one-sided test. The null hypothesis is , and the alternative hypothesis is . Finally, the vector of coefficients is the nuisance parameter in this model. We estimate by the restricted MLE under the null hypothesis.

The value of the test statistic is 24.668. The 5% critical value is 5.050. Hence, we reject the null hypothesis at the 5% level. This result is consistent with the finding of Kline and Tamer (2016) whose credible sets for the strategic interaction effects do not contain the origin. Table 1 reports the RMLE of the index coefficients. The estimates suggest that the effect of market presence is larger for LCCs than other airlines, and the monopoly profits (captured by the constant terms) in a market with below-median size and below-median market presence are smaller for the LCCs. These observations are also consistent with Kline and Tamer (2016)’s findings, although we note that these estimates are obtained by imposing the restriction rejected by the score test.

| 1.643 | 0.795 | -2.084 | 0.388 | 0.440 | 0.338 |

Note: and are treated as continuous variables on the unit interval when they are not discretized; and are binary indicators of whether the original variables are above their median or not when they are discretized.

4.2 Testing the Endogeneity of Catholic School Attendance

The second application concerns the causal effect of Catholic school attendance on academic achievements studied by Altonji et al. (2005). Whether Catholic schools provide a better education than public ones is important for education policies, but the analysis is complicated by the concern that selection into Catholic schools is nonrandom. Using the framework in Example 2, we examine the endogeneity of Catholic school attendance by testing if the coefficient on the control function is zero.

The data source is a subset of the National Educational Longitudinal Survey of 1988 (NELS:88). We use a version of the data available from Wooldridge (2019). We refer to Altonji et al. (2005) for a detailed discussion of the data. The dependent variable is a binary variable indicating whether the student graduated from high school by the year 1994. The binary treatment indicates whether the student attended a Catholic high school. The vector of exogenous control variables includes each parent’s years of education and log family income. The instrument variable is a dummy variable indicating whether a parent was reported to be Catholic. The sample size is 5970 after we remove missing observations on .

Table 2 reports the point estimates of nuisance parameters under the null hypothesis . The value of the test statistic is 154.848. The 5% critical value is 2.755. We, therefore, reject the null hypothesis at the 5% level. Our test provides strong evidence supporting the students’ selection into Catholic schools based on their unobservable characteristics. This result is in line with the concern expressed in Altonji et al. (2005).

| 0.630 | 0.029 | 0.062 | 0.028 | 1.220 | 0.003 | 0.082 | -0.319 |

Note: Constants are not included in either equations (2.5) or (2.6). The variables listed in the table denote the mother’s years of education, the father’s years of education, the log family income, and whether one of the parents is reported to be Catholic. The estimation was conducted using the glmfit in MATLAB.

5 Monte Carlo Experiments

5.1 Size and Power of the Score Test

We examine the size and power properties of the score test through simulations. The data generating process is based on Example 1 and is motivated by the empirical illustration in the previous section. There are player-specific covariates , each of which is generated as an independent Rademacher random variable taking values on . We then generate from the bivariate standard normal distribution. For each and , we determine the predicted set of outcomes based on the payoff functions with . We then test

| (5.1) |

As discussed earlier, the model is complete under . We estimate using the restricted MLE. The sample size is set to 2500, 5000, or 7500. This choice is motivated by the sample size used in the empirical application.

The size of the score test is reported in Table 3. The size of the test is controlled properly across all sample sizes, while it tends to be slightly conservative when is small.

| Sample size | 2500 | 5000 | 7500 |

|---|---|---|---|

| Size | 0.028 | 0.036 | 0.041 |

Under alternative hypotheses, multiple equilibria may be predicted. If this is the case, we select an outcome according to one of the following selection mechanisms. The first design uses a selection mechanism, which selects out of if an i.i.d. Bernoulli random variable takes 1. In the second design, we generate data from the least favorable distribution, which draws an independent outcome sequence from the least favorable distribution .

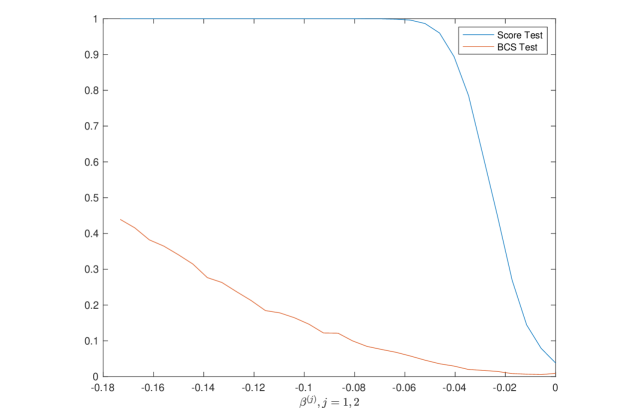

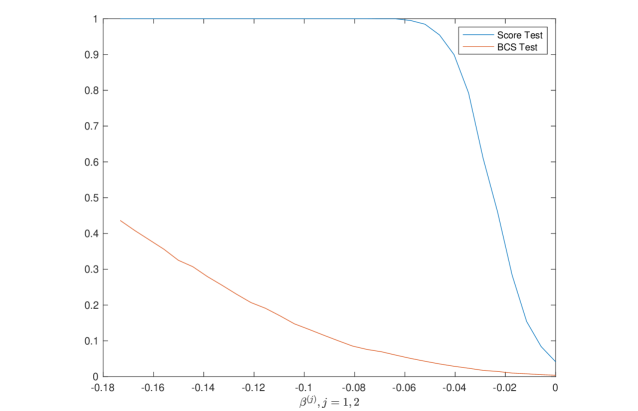

The power of the score test is calculated against local alternatives with for For this exercise, we introduce a grid of values for and generate the data described above. We then compare the rejection frequency of our test to that of the moment-based testing procedure by Bugni et al. (2017). Their test checks if a hypothesized value is compatible with a set of moment restrictions. Their statistic and bootstrap critical value are calculated using a sample analog of the following moment inequality and equality restrictions

which are the sharp identifying restrictions that characterize in (3.4).212121Since the example resembles the specification used in their Monte Carlo experiments, we added minimal changes to their replication code posted on the repository of Quantitative Economics to implement their procedure.

Figures 4-5 show the rejection frequencies of the score and moment-based tests. The results are similar across the two designs. In each design, the score test outperforms the moment-based test in terms of power by a significant margin. This difference in performance may potentially be due to the proposed score test’s exploitation of completeness under the null to estimate the nuisance parameter and direct power against . The moment-based test is designed for general subvector inference and does not necessarily exploit the model completeness.222222The procedure by Bugni et al. (2017) tests if the null parameter value is consistent with the model restrictions and deals with nuisance parameters by a profiling method combined with regularization to ensure its uniform validity. The simulation results suggest that taking advantage of the model structure may provide considerable benefits in terms of power.

6 Concluding Remarks

Economic models exhibit incompleteness for various reasons. They are, for example, consequences of strategic interaction, state dependence, or self-selection. This paper shows that one can test these important features using a score statistic even if the model is incomplete under the alternative hypothesis. The proposed test exploits the model completeness under the null hypothesis to simplify its computation. An avenue for future research includes a theory for the uniform validity of inference for post-model selection procedures based on the score test.

References

- Aliprantis and Border (2006) Aliprantis, C. D. and K. C. Border (2006): Infinite Dimensional Analysis: A Hitchhiker’s Guide, Springer.

- Altonji et al. (2005) Altonji, J. G., T. E. Elder, and C. R. Taber (2005): “An Evaluation of Instrumental Variable Strategies for Estimating the Effects of Catholic Schooling,” Journal of Human Resources, 40, 791–821.

- Andrews (1999) Andrews, D. W. K. (1999): “Estimation When a Parameter is on a Boundary,” Econometrica, 67, 1341–1383.

- Andrews and Barwick (2012) Andrews, D. W. K. and P. J. Barwick (2012): “Inference for Parameters Defined by Moment Inequalities: A Recommended Moment Selection Procedure,” Econometrica, 80, 2805–2826.

- Andrews and Guggenberger (2009) Andrews, D. W. K. and P. Guggenberger (2009): “Hybrid and size-corrected subsampling methods,” Econometrica, 77, 721–762.

- Andrews and Soares (2010) Andrews, D. W. K. and G. Soares (2010): “Inference for Parameters Defined by Moment Inequalities Using Generalized Moment Selection,” Econometrica, 78, 119–157.

- Andrews et al. (2019) Andrews, I., J. Roth, and A. Pakes (2019): “Inference for Linear Conditional Moment Inequalities,” Discussion Paper, Harvard University.

- Barseghyan et al. (2021) Barseghyan, L., M. Coughlin, F. Molinari, and J. C. Teitelbaum (2021): “Heterogeneous Choice Sets and Preferences,” Econometrica, 89, 2015–2048.

- Bera and Bilias (2001) Bera, A. K. and Y. Bilias (2001): “Rao’s Score, Neyman’s and Silvey’s LM tests: An Essay on Historical Developments and Some New Results,” Journal of Statistical Planning and Inference, 97, 9–44.

- Beresteanu et al. (2011) Beresteanu, A., I. Molchanov, and F. Molinari (2011): “Sharp Identification Regions in Models with Convex Moment Predictions,” Econometrica, 79, 1785–1821.

- Blundell and Powell (2004) Blundell, R. W. and J. L. Powell (2004): “Endogeneity in Semiparametric Binary Response Models,” The Review of Economic Studies, 71, 655–679.

- Bresnahan and Reiss (1991) Bresnahan, T. F. and P. C. Reiss (1991): “Empirical models of discrete games,” Journal of Econometrics, 48, 57–81.

- Bugni et al. (2017) Bugni, F., I. Canay, and X. Shi (2017): “Inference for Subvectors and Other Functions of Partially Identified Parameters in Moment Inequality Models,” Quantitative Economics, 8, 1–38.

- Canay and Shaikh (2017) Canay, I. A. and A. M. Shaikh (2017): “Practical and Theoretical Advances in Inference for Partially Identified Models,” in Advances in Economics and Econometrics: Eleventh World Congress, ed. by B. Honoré, A. Pakes, M. Piazzesi, and L. Samuelson, Cambridge University Press, vol. 2 of Econometric Society Monographs, 271–306.

- Card and Hyslop (2005) Card, D. and D. R. Hyslop (2005): “Estimating the effects of a time-limited earnings subsidy for welfare-leavers,” Econometrica, 73, 1723–1770.

- Chamberlain (1985) Chamberlain, G. (1985): Heterogeneity, omitted variable bias, and duration dependence, Cambridge University Press, 3–38, Econometric Society Monographs.

- Chen et al. (2018) Chen, X., T. M. Christensen, and E. Tamer (2018): “Monte Carlo confidence sets for identified sets,” Econometrica, 86, 1965–2018.

- Chesher (2003) Chesher, A. (2003): “Identification in Nonseparable Models,” Econometrica, 71, 1405–1441.

- Chesher and Rosen (2017) Chesher, A. and A. M. Rosen (2017): “Generalized Instrumental Variable Models,” Econometrica, 85, 959–989.

- Ciliberto and Tamer (2009) Ciliberto, F. and E. Tamer (2009): “Market Structure and Multiple Equilibria in Airline Markets,” Econometrica, 77, 1791–1828.

- Cox and Shi (2020) Cox, G. and X. Shi (2020): “Simple Adaptive Size-Exact Testing for Full-Vector and Subvector Inference in Moment Inequality Models,” Working Paper.

- de Paula et al. (2018) de Paula, Á., S. Richards-Shubik, and E. Tamer (2018): “Identifying Preferences in Networks With Bounded Degree,” Econometrica, 86, 263–288.

- de Paula and Tang (2012) de Paula, Á. and X. Tang (2012): “Inference of Signs of Interaction Effects in Simultaneous Games With Incomplete Information,” Econometrica, 80, 143–172.

- Dempster (1967) Dempster, A. (1967): “Upper and Lower Probabilities Induced by a Multivalued Mapping,” The Annals of Mathematical Statistics, 38, 325–339.

- Eizenberg (2014) Eizenberg, A. (2014): “Upstream Innovation and Product Variety in the U.S. Home PC Market,” The Review of Economic Studies, 81, 1003–1045.

- Epstein et al. (2016) Epstein, L., H. Kaido, and K. Seo (2016): “Robust Confidence Regions for Incomplete Models,” Econometrica, 84, 1799–1838.

- Fack et al. (2019) Fack, G., J. Grenet, and Y. He (2019): “Beyond Truth-Telling: Preference Estimation with Centralized School Choice and College Admissions,” American Economic Review, 109, 1486–1529.

- Galichon and Henry (2011) Galichon, A. and M. Henry (2011): “Set identification in models with multiple equilibria,” The Review of Economic Studies, 78, 1264–1298.

- Gilboa and Schmeidler (1989) Gilboa, I. and D. Schmeidler (1989): “Maxmin Expected Utility with Non-Unique Prior,” Journal of Mathematical Economics, 18, 141–153.

- Haile and Tamer (2003) Haile, P. A. and E. Tamer (2003): “Inference with an Incomplete Model of English Auctions,” Journal of Political Economy, 111, 1–51.

- Handel (2013) Handel, B. R. (2013): “Adverse selection and inertia in health insurance markets: When nudging hurts,” American Economic Review, 103, 2643–82.

- Heckman (1978) Heckman, J. J. (1978): “Simple Statistical Models for Discrete Panel Data Developed and Applied to Test the Hypothesis of True State Dependence Against The Hypothesis of Spurious State Dependence,” Annales de INSEE, 227–269.

- Heckman (1981) ——— (1981): “The Incidental Parameters Problem and the Problem of Initial Conditions in Estimating a Discrete Time-Discrete Data Stochastic Process,” in Structural Analysis of Discrete Data With Econometric Applications, ed. by C. Manski and D. McFadden, MIT Press.

- Henry et al. (2020) Henry, M., R. Meango, and I. Mourifié (2020): “Revealing Gender-Specific Costs of STEM in an Extended Roy Model of Major Choice,” Working Paper.

- Honoré and Tamer (2006) Honoré, B. E. and E. Tamer (2006): “Bounds on Parameters in Panel Dynamic Discrete Choice Models,” Econometrica, 74, 611–629.

- Huber and Strassen (1973) Huber, P. and V. Strassen (1973): “Minimax Tests and Neyman–Pearson Lemma for Capacities,” The Annals of Statistics, 1, 251–263.

- Hyslop (1999) Hyslop, D. R. (1999): “State Dependence, Serial Correlation and Heterogeneity in Intertemporal Labor Force Participation of Married Women,” Econometrica, 67, 1255–1294.

- Imbens and Newey (2009) Imbens, G. W. and W. K. Newey (2009): “Identification and Estimation of Triangular Simultaneous Equations Models Without Additivity,” Econometrica, 77, 1481–1512.

- Jovanovic (1989) Jovanovic, B. (1989): “Observable Implications of Models with Multiple Equilibria,” Econometrica, 57, 1431–1437.

- Kaido et al. (2019) Kaido, H., F. Molinari, and J. Stoye (2019): “Confidence Intervals for Projections of Partially Identified Parameters,” Econometrica, 87, 1397–1432.

- Kaido and Zhang (2019) Kaido, H. and Y. Zhang (2019): “Robust Likelihood-Ratio Tests for Incomplete Economic Models,” Working Paper.

- Kawai and Watanabe (2013) Kawai, K. and Y. Watanabe (2013): “Inferring Strategic Voting,” American Economic Review, 103, 624–62.

- Kline and Tamer (2016) Kline, B. and E. Tamer (2016): “Bayesian inference in a class of partially identified models,” Quantitative Economics, 7, 329–366.

- Leeb and Pötscher (2005) Leeb, H. and B. M. Pötscher (2005): “Model selection and inference: Facts and fiction,” Econometric Theory, 21, 21–59.

- Lehmann and Romano (2005) Lehmann, E. L. and J. P. Romano (2005): Testing statistical hypotheses, vol. 3, Springer.

- Lewbel (2007) Lewbel, A. (2007): “Coherency and Completeness of Structural Models Containing a Dummy Endogenous Variable,” International Economic Review, 48, 1379–1392.

- McFadden (1981) McFadden, D. (1981): “Econometric Models of Probabilistic Choice,” in Structural Analysis of Discrete Data With Econometric Applications, ed. by C. Manski and D. McFadden, MIT Press.

- Molchanov (2005) Molchanov, I. S. (2005): Theory of random sets, vol. 19, Springer.

- Molinari (2020) Molinari, F. (2020): “Microeconometrics with Partial Identification,” in Handbook of Econometrics, ed. by S. N. Durlauf, L. P. Hansen, J. J. Heckman, and R. L. Matzkin, Elsevier, vol. 7, 355–486.

- Newey (1994) Newey, W. K. (1994): “The asymptotic variance of semiparametric estimators,” Econometrica: Journal of the Econometric Society, 1349–1382.

- Newey and McFadden (1994) Newey, W. K. and D. McFadden (1994): “Large Sample Estimation and Hypothesis Testing,” in Handbook of Econometrics, ed. by J. J. Heckman and E. Leamer, Elsevier, vol. 4, chap. 36, 2111–2245.

- Otsu et al. (2016) Otsu, T., M. Pesendorfer, and Y. Takahashi (2016): “Pooling Data Across Markets in Dynamic Markov Games,” Quantitative Economics, 7, 523–559.

- Pelican and Graham (2021) Pelican, A. and B. S. Graham (2021): “An Optimal Test for Strategic Interaction in Social and Economic Network Formation Between Heterogeneous Agents,” Working Paper.

- Philippe et al. (1999) Philippe, F., G. Debs, and J.-Y. Jaffray (1999): “Decision Making with Monotone Lower Probabilities of Infinite Order,” Mathematics of Operations Research, 24, 767–784.

- Romano et al. (2014) Romano, J. P., A. M. Shaikh, and M. Wolf (2014): “A Practical Two-Step Method for Testing Moment Inequalities,” Econometrica, 82, 1979–2002.

- Shafer (1976) Shafer, G. (1976): A Mathematical Theory of Evidence, Princeton University Press.

- Shaikh and Vytlacil (2011) Shaikh, A. M. and E. J. Vytlacil (2011): “Partial Identification in Triangular Systems of Equations With Binary Dependent Variables,” Econometrica, 79, 949–955.

- Sheng (2020) Sheng, S. (2020): “A Structural Econometric Analysis of Network Formation Games Through Subnetworks,” Econometrica, 88, 1829–1858.

- Silvapulle and Silvapulle (1995) Silvapulle, M. J. and P. Silvapulle (1995): “A Score Test Against One-Sided Alternatives,” Journal of the American Statistical Association, 90, 342–349.

- Talagrand (1994) Talagrand, M. (1994): “Sharper Bounds for Gaussian and Empirical Processes,” The Annals of Probability, 22, 28–76.

- Tamer (2003) Tamer, E. (2003): “Incomplete Simultaneous Discrete Response Model with Multiple Equilibria,” The Review of Economic Studies, 70, 147–165.

- Train (2009) Train, K. (2009): Discrete Choice Methods with Simulation, Cambridge University Press, 2 ed.

- van der Vaart (2000) van der Vaart, A. (2000): Asymptotic Statistics, Cambridge University Press.

- van der Vaart and Wellner (1996) van der Vaart, A. and J. A. Wellner (1996): Weak Convergence and Empirical Processes: With Applications to Statistics., Springer, New York.

- Wald (1950) Wald, A. (1950): “Remarks on the estimation of unknown parameters in incomplete systems of equations,” Statistical Inference in Dynamic Economic Models, ed. TC Koopmans. John Wiley, New York, 305–310.

- Wasserman (1990) Wasserman, L. A. (1990): “Belief Functions and Statistical Inference,” Canadian Journal of Statistics, 18, 183–196.

- Wollmann (2018) Wollmann, T. G. (2018): “Trucks Without Bailouts: Equilibrium Product Characteristics for Commercial Vehicles,” American Economic Review, 108, 1364–1406.

- Wooldridge (2005) Wooldridge, J. M. (2005): “Simple Solutions to the Initial Conditions Problem in Dynamic, Nonlinear Panel Data Models with Unobserved Heterogeneity,” Journal of Applied Econometrics, 20, 39–54.

- Wooldridge (2014) ——— (2014): “Quasi-Maximum Likelihood Estimation and Testing for Nonlinear Models with Endogenous Explanatory Variables,” Journal of Econometrics, 182, 226–234.

- Wooldridge (2015) ——— (2015): “Control Function Methods in Applied Econometrics,” Journal of Human Resources, 50, 420–445.

- Wooldridge (2019) ——— (2019): Introductory Econometrics: A Modern Approach, Cengage Learning, 7 ed.

Appendix A Notation and Preliminaries

The following list includes notation and definitions that will be used throughout the Appendices:

| for some constant . | |

| the -norm for square-integrable functions. | |

| the supremum norm over . | |

| covering number of size for under norm . | |

| bracketing number of size for under norm . | |

| weakly converges to under |

Let be a compact metric space and let denote its Borel -algebra. Let be the set of compact subsets of endowed with the Hausdorff metric . Let be the set of continuous functions on . Let be the set of Borel probability measures on endowed with the weak topology.

A.1 Capacity functionals

We briefly summarize the definition and properties of capacities. A set function is said to be a capacity if satisfies the following conditions:

-

(i)

,

-

(ii)

, for all .

-

(iii)

, for all and .

-

(iv)

closed .

One may define integral operations with respect to capacities as follows. Let be a measurable function. The Choquet integral of with respect to is defined by

| (A.1) |

where the integrals on the right-hand side are Riemann integrals. A capacity is said to be monotone of order or, for short, k-monotone if for any ,

| (A.2) |

Conjugate is then called a -alternating capacity. A capacity that satisfies (A.2) is called an infinitely monotone capacity or a belief function. Capacities are used in various areas of statistics (Dempster, 1967; Shafer, 1976; Wasserman, 1990) and economics (Gilboa and Schmeidler, 1989).

The following result, known as Choquet’s theorem, states that a random closed set following a distribution induces a belief function, and it follows from Theorems 1-3 in Philippe et al. (1999).

Lemma A.1.

Let be a Polish space. Let be a probability measure on . Let . Then, is a belief function and satisfies

| (A.3) |

Appendix B Details on the Examples

This section provides details on each of the examples discussed in the text. We present the sharp identifying restrictions, the least favorable parametric models, and primitive conditions for Assumption 1.

B.1 Discrete Games of Complete Information

B.1.1 Sharp Identifying Restrictions and Assumption 1

Recall that . The upper and lower probabilities of all singleton events are tabulated in Table 5. In this example, they constitute the sharp identifying restrictions (Galichon and Henry, 2011).

| {(0, 0)} | ||

|---|---|---|

| {(1, 1)} | ||

| {(1, 0)} | ||

| {(0, 1)} |

As argued in Section 3.2, the model’s prediction reduces to (3.20) when , which implies a unique density in (3.18). Therefore, Assumption 1 (i) holds. For Assumption 1 (ii), it suffices to show that and are disjoint. For this, consider the event . Table 5 suggests

| (B.1) |

whereas

| (B.2) |

This means whenever . Hence, and are disjoint.

B.1.2 Least Favorable Parametric Model

The least favorable parametric model is given by

| (B.3) | ||||

| (B.4) | ||||

| (B.5) |

and is determined by . The parameter subsets, , are given by

| (B.6) | ||||

| (B.7) | ||||

| (B.8) |

where

Below, we outline how to obtain this density from the convex program in (3.10)-(3.12).

As discussed in the text, is determined by the four equality restrictions (3.14)-(3.17). Therefore, it remains to solve the convex program in (3.10)-(3.12) for . For this, we can reduce the number of control variables. First, Table 5 implies

| (B.9) | ||||

| (B.10) |

Hence, the remaining free components of are and . Let . We may then express the other component as

Hence, to solve (3.10)-(3.12), it suffices to choose optimally in the following problem:

| (B.11) | ||||

Let the Lagrangian be

The Karush-Kuhn-Tucker (KKT) conditions are

| (B.12) | |||

| (B.13) | |||

| (B.14) | |||

| (B.15) |

Below, we consider three subcases depending on the value of the Lagrange multipliers.

Case 1 (): The FOC in (B.12) with identifies the solution as follows:

| (B.16) |

This implies

| (B.17) | ||||

| (B.18) |

Substituting the value of into its bounds, we obtain the following restrictions:

| (B.19) | |||

| (B.20) |

We let denote the set of parameter values that satisfy (B.19)-(B.20).

B.1.3 Score Function

We let Each component of takes the following form:

| (B.23) |

where is the partial derivative of with respect to , which is well-defined if is in , , or in the interior of . Let

| (B.24) |

Suppose . By (B.7), for small enough. Then, pointwise, because . The same argument applies when or . The only case this argument does not apply is when is on the boundary between and (or between and ). For example, suppose is on the boundary between and . Then, we may have for all with but . Then, the pointwise argument above does not apply. However, being on the boundary between the two sets means

If contains a continuous component (e.g. distance from headquarters/distribution center), the set of ’s satisfying above has measure 0, is bounded on the set. Hence, it does not affect the integral in Assumption 2. Hence, Assumption 2 holds.

For completeness, the functional form of is derived below for each and Across all subcases analyzed in the previous section, the form of and remains the same. We calculate score functions first by taking the pointwise derivative of and . This yields

where .

Next, we derive and .

Case 1: Suppose . By taking the pointwise derivative of in (B.5), one can obtain

Similarly,

Case 2: Suppose . Similarly to the analysis in Case 1, we may obtain

and

Case 3: Suppose . Similarly to the previous two cases, we may obtain

and

B.2 Triangular Model with an Incomplete Control Function

B.2.1 Sharp Identifying Restrictions and Assumption 1

Let us simplify in Example 2 first. Let We assume throughout, but a similar analysis can be done by assuming Suppose first. By (2.4)-(2.5), if

| (B.25) |

Then, by , we can write this event as . By (2.4)-(2.5) again, if

| (B.26) |

This means that is consistent with the model whenever . These predictions can be summarized as

| (B.27) |

Now suppose implying . Repeating a similar analysis yields the following correspondence

| (B.28) |

These predictions are summarized in Figure 3.

Assumption 1 (i) holds because, as argued in Section 3.2, the model’s prediction under the null hypothesis is complete and is characterized by the reduced form function:

| (B.29) |

This structure induces a unique conditional density for . Suppose .232323Here, we normalize the scale by setting the variance of to 1. Other choices of normalization are also possible. Assumption 1 (ii) holds as long as with positive probability. For this, we demonstrate that there exists an event such that for some value of . For this, take and suppose . Under the null hypothesis, the conditional probability of is uniquely determined as . When , (B.27) implies

| (B.30) |

which is greater than for values of such that . Hence, and are disjoint.

B.2.2 Least Favorable Parametric Model

For any with , the set of densities compatible with is then characterized by the following inequalities

| (B.31) | ||||

| (B.32) |

and

| (B.33) | ||||

| (B.34) |

Suppose . Let . Then, the convex program in (3.10)-(3.12) can be written as

| (B.35) | ||||

| (B.36) | ||||

| (B.37) | ||||

| (B.38) |

where (B.36) is due to the completeness of the model under the null hypothesis (see (3.34)) and . Note that (B.38) is redundant since being in the probability simplex is implicitly assumed. The KKT conditions associated with the program are, therefore

| (B.39) | |||

| (B.40) | |||

| (B.41) |

where . There are two cases to consider.

Case 1 (): When , (B.39) implies . This holds when .

B.2.3 Score Function

The corresponding score function with respect to is

| (B.50) | ||||

| (B.51) |

and

| (B.52) | ||||

| (B.53) |

B.3 Panel Dynamic Discrete Choice Models

For each , let . We explicitly derive a form of below. Note that, occurs if

| (B.54) |

which follows from (2.10)-(2.11) or

| (B.55) |

which follows from (2.12)-(2.13). When , the union of the two events reduces to (B.54).

The outcome occurs if

| (B.60) |

or

| (B.61) |

When , the union of the two events reduces to (B.61). These predictions are summarized in Figure 2.

The correspondence can therefore be written as

| (B.62) |

A similar analysis can be done for the setting with , which we omit for brevity.

B.3.1 Sharp Identifying Restrictions and Assumption 1

Assumption 1 (i) holds because, as argued in (3.22), the model makes a complete prediction with the following reduced-form function when :

| (B.63) |

Assumption 1 (ii) holds if follows a distribution that is absolutely continuous with respect to the Lebesgue measure on . We show below, when , there exists an event such that for all For example, take . As shown on the left panel of Figure 2, the probability of is uniquely determined when . Therefore, the upper bound on the probability of is

| (B.64) |

When , the lower bound on the probability of the same event is

| (B.65) |

which exceeds as long as is absolutely continuous. This means and are disjoint.

B.3.2 Least Favorable Parametric Model

The analysis of the LFP and score is similar to that of discrete games. For brevity, we give the LFP below and omit its derivation.

For each , let and . Define the following parameter sets.

| (B.66) | ||||

| (B.67) |

where

| (B.68) | ||||

| (B.69) | ||||

| (B.70) |

When , the least favorable parametric model is characterized by the following density:

| (B.71) | ||||

| (B.72) | ||||

| (B.73) | ||||

| (B.74) |

When , the least favorable parametric model is characterized by the following density:

| (B.75) | ||||

| (B.76) | ||||

| (B.77) | ||||

| (B.78) |

Appendix C Lemmas and Proofs

This section is organized as follows. Section C.1 contains the proof of Proposition 3.1. In Section C.2, we show -consistency of by extending standard arguments for extremum estimators to locally incomplete models. In Section C.3, we use the results in C.2 to show results on the asymptotic size of our score test.

C.1 Least favorable parametric model

Proof of Proposition 3.1.

By Assumption 1 (i), the model makes a complete prediction for any Then, for each , is the unique density in satisfying , where Hence, the LF parametric model is well-defined for Now, let . By Assumption 1 (ii), for any . Also,

| (C.1) |

where is the set of probability measures on such that for all . Note that is a belief function. Hence, there exists a least favorable pair by Theorem 3.1 in Kaido and Zhang (2019) applied with . We then let . Recall that . Hence, we also defined for . This completes the proof. ∎

C.2 -consistency of

Lemma C.1.

Proof.

The following proposition shows the sample log-likelihood converges to its population counterpart uniformly over a set of distributions consistent with the null or local alternative hypotheses. Recall that the set of conditional laws is defined as in (3.36), and collects joint laws of .

Proposition C.1 (ULLN).

Proof.

Below, let and be a belief function and its conjugate induced by the correspondence on . That is, they are set functions such that

| (C.7) | ||||

| (C.8) |

A key observation is that, for any ,

| (C.9) |

This is because the model is complete under by Assumption 1 and the fact that the Choquet integrals with respect to and coincide with each other in such a setting.

Note that one may write the event (i.e., the argument of ) in (C.6) as the union of the following two events:

| (C.10) | ||||

| (C.11) |

Let be a random set whose distribution follows the law induced by . Below, we simply write Note that

| (C.12) | ||||

| (C.13) | ||||

| (C.14) | ||||

| (C.15) |

By Assumption 3 and Lemma C.1,

| (C.16) |

implying there exists and such that for all . Hence, for all , (C.14) is bounded by

| (C.17) |

As shown below, we may apply Lemma C.2 to this quantity. Similarly, by Assumption 3 and Lemma C.1, (C.15) is bounded by

| (C.18) |

Now, let . Then, by Lemma C.3, the induced family of functions defined in (C.21) consists of uniformly bounded and Lipschitz functions. By Theorem 2.7.11 in van der Vaart and Wellner (1996), it follows that

| (C.19) |

Therefore, satisfies the condition of Lemma C.2. Applying the lemma ensures that (C.17) is bounded by

| (C.20) |

which tends to 0 as . (C.18) can be handled similarly. This completes the proof. ∎

Let be a Euclidean space. Given a family of measurable functions on and a random closed set , define a family of measurable functions on by

| (C.21) |

We denote the envelope function of by . A class of uniformly bounded functions is covered by at most brackets if for positive constants and ,

| (C.22) |

The following lemma gives concentration inequalities for the suprema (and infima) of empirical processes under plausibility functions.

Lemma C.2.

Let be a belief function such that for any . Let be a family of uniformly bounded measurable functions on such that in (C.21) is covered by at most brackets. Then, for all

| (C.23) | |||

| (C.24) |

for some that depends on only.

Proof.