Uncovering a two-phase dynamics from a dollar exchange model with bank and debt

Abstract

We investigate the unbiased model for money exchanges with collective debt limit: agents give at random time a dollar to one another as long as they have at least one dollar or they can borrow a dollar from a central bank if the bank is not empty. Surprisingly, this dynamics eventually leads to an asymmetric Laplace distribution of wealth (conjectured in [22] and shown formally in a recent work [18]). In this manuscript, we carry out a formal mean-field limit as the number of agents goes to infinity where we uncover a two-phase (ODE) dynamics. Convergence towards the unique equilibrium (two-sided geometric) distribution in the large time limit is also shown and the role played by the bank and debt (in terms of Gini index or wealth inequality) will be explored numerically as well.

Key words: Econophysics, Agent-based model, Mean-field, Two-phase, Bank

1 Introduction

Econophysics is a subfield of statistical physics that apply concepts and techniques from traditional physics to economics or finance [12]. One of the primary goal of this area of research is to explain how various economical phenomena could be derived from universal laws in statistical physics under certain model assumptions, and we refer to [15] for a general review.

There several motivations for the study of econophysics models: from the perspective of a policy maker, how to influence/control the emerging wealth inequality (measured by Gini index) in order to mitigate the alarming gap between rich and poor is a central issue to be dealt with. From a mathematical viewpoint, the fundamental mechanisms behind the formation of macroscopic phenomena, for instance various possible wealth distributions from different agent-based money exchange models, must be thoroughly understood. For a given (stochastic) agent-based model, we would like to identify a limit (deterministic) dynamics when we send the number of individuals to infinity, and then the deterministic system will be further analyzed with the intention of proving its convergence to equilibrium (if there is one) for large time. This paradigm has been implemented in vast amount of works across different fields of applied mathematics, see for instance [1, 6, 7, 20].

In this work, we consider a simple mechanism for money exchange involving a bank, meaning that there are a fixed number of agents (denoted by ) and one bank. We denote by the amount of dollars the agent has at time and we suppose that for some fixed so that . Moreover, we denote by the initial amount of dollars in the bank, where and represent the amount of dollars owned by the bank in the form of “cash” and in the form of “debt” (borrowed by agents), respectively. Also, we introduce another parameter so that and set .

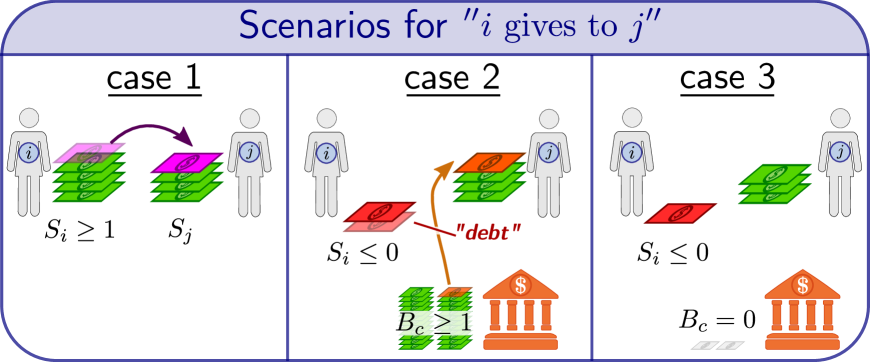

The model investigated in this work was proposed in [22] and revisited by [18]: at random time (generated by an exponential law), an agent (the “giver”) and an agent (the “receiver”) are picked uniformly at random. If the “giver” has at least one dollar (i.e. ) or if the central bank has “cash” (i.e. ), then the receiver receives a dollar. Otherwise, when the receiver has no dollar and the bank has no cash, then nothing happens. We illustrate the dynamics in figure 1 explaining the three cases when agent is picked to give one dollar to agent . From now on, we will call this model the unbiased exchange model with collective debt limit and it can be represented by (1.1).

| (1.1) |

Notice that when the bank gives a dollar to agent , there is still one dollar withdrew from the giver , i.e. the debt of agent increases (represented in red in figure 1). The debt of agent could be reduced once it will become a “receiver”. It is also important to notice that in this model the bank never losses money, it just transforms its “cash” into “debt”. Without the bank, agents can only give a dollar when they have at least one dollar (hence no debt is allowed). In this case, the model is termed as the one-coin model in [16], the unbiased exchange model in [2, 5], and the mean-field zero range process in [19].

Remark. In order to have the correct asymptotic as the number of agents goes to infinity , we need to adjust the rate by normalizing by so that the rate of a typical agent giving a dollar per unit time is of order .

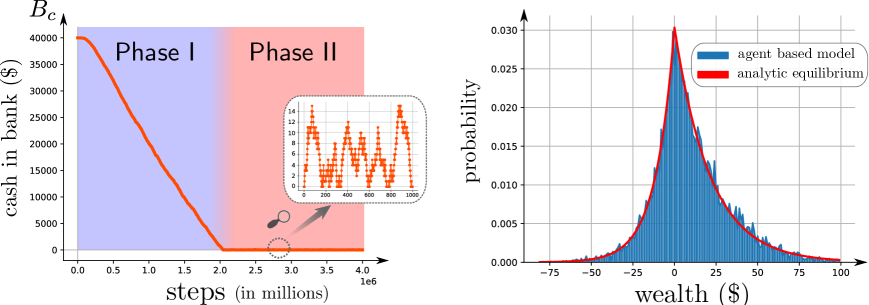

The fundamental question of interest is the exploration of the limiting money distribution among the agents as the total number of agents and time become large. To foresee the behavior of the dynamics under these limits, we perform a numerical simulation with agents over steps. In figure 2-left, we plot the evolution of the cash in the bank over time. We observe a first phase where the cash is decaying linearly until it reaches zero (after roughly millions steps). After that, there is a second phase where remains close to zero. In figure 2-right, the distribution of the wealth distribution is plotted after millions steps. This distribution is well approximated by an asymmetric Laplace distribution given in (1.4).

This numerical result will be explained by our derivation in section 2 and the following asymptotic analysis in section 3. Our approach illustrated by figure 3 consists in two steps. Our first step consists in deriving the limit dynamics as the number of agents goes to infinity (section 2). With this aim, we introduce the probability distribution of wealth:

| (1.2) |

with . The evolution of will be given by a (deterministic) nonlinear ordinary differential equations. To fully justify this transition from a stochastic interacting systems into a deterministic set of ODEs, one needs the so-called propagation of chaos [21]. We do not investigate the proof in this manuscript, the derivation has been rigorously justified in various models arising from econophysics, see for instance [2, 3, 4, 5, 13, 10, 11]. The additional difficulty here is that the evolution of is split into two phases. Indeed, the evolution changes at the first time when there is no more cash in the bank. We will denote by the time at which such event occur, i.e. at the bank is empty for the first time. The evolution equation of takes the form of:

| (1.3) |

where the exact expressions for the operator and are given by (2.5) and (2.15), respectively.

Our second step is to investigate the asymptotic behavior of the probability mass function as , more precisely its convergence toward an asymmetric Laplace distribution given in (1.4):

| (1.4) |

where the three positive parameters , and only depend on (average wealth per agent) and (the ratio between the bank and agent’s combined wealth). Our proof relies on the so-called entropy method which gives a rigorous proof of the convergence of toward the asymmetric Laplace distribution , see section 3.2. Moreover, a standard linearization analysis performed in section 3.3 allows us to obtain an exponential decay result for the linearized entropy (near equilibrium), provided that the parameters and fulfill certain criteria.

Finally, we would like explore the role played by the bank in terms of wealth inequality. In particular, we conjecture that the inclusion of the bank and possibility for agents to go into debt will lead to accentuation of wealth inequality (measured by the Gini index), compared to the usual unbiased exchange model (without the presence of a bank). This type of Gini index comparison conjecture (shown numerically in section 4) makes sense at least heuristically but we are not able to provide a rigorous proof.

Although we will only investigate a specific binary exchange models in the present work, other exchange rules can also be imposed and studied, leading to different models. To name a few, the so-called immediate exchange model introduced in [14] assumes that pairs of agents are randomly and uniformly picked at each random time, and each of the agents transfer a random fraction of its money to the other agents, where these fractions are independent and uniformly distributed in . The so-called uniform reshuffling model investigated in [12, 17, 3] suggests that the total amount of money of two randomly and uniformly picked agents possess before interaction is uniformly redistributed among the two agents after interaction. For closely related variants of the unbiased exchange model we refer to the recent work [2]. For other models arising from econophysics, see [8, 9, 18, 4].

2 Formal mean-field limit

In this section, we carry out a formal mean-field argument of the stochastic agent-based dynamics (1.1) as the number of agents goes to infinity. Even our analysis is not completely rigorous, the resulting system of ODEs (i.e., (2.4)-(2.5) in Phase I and (2.14)-(2.15) in Phase II) admits a unique equilibrium distribution as , which is a two-sided geometric distribution and can be well-approximated by an asymmetric Laplace distribution when (i.e., when the initial average amount of dollars per agent becomes large). As our predication of the limiting distribution of money based on the large time behavior of the ODE system (2.14)-(2.15) coincides with the conjecture in [22] and the work in [18], it strongly indicates that our heuristic mean-field analysis actually captures the correct deterministic behavior of the underlying stochastic dynamics when we send .

The unbiased exchange model with collective debt limit can be written in terms of a system of stochastic differential equations, thanks to the framework set up in [2] for the study of the basic unbiased exchange model as well as some of its variants. Introducing , which represents a collection of independent Poisson processes with constant intensity , the evolution of each is given by:

| (2.1) |

where we use the notation . By the obvious symmetry, we can focus on the case when and notice that whenever , the SDE for simplifies to

| (2.2) |

If we introduce

then the two Poisson processes and are of intensity . Motivated by (2.2), we give the following definition of the limiting dynamics of as from the process point of view, providing that .

Definition 1 (Mean-field equation — Phase I)

We define to be the compound Poisson process satisfying the following SDE:

| (2.3) |

in which and are independent Poisson processes with unit intensity.

We denote by the law of the process , i.e. . Its time evolution is given by the following dynamics:

| (2.4) |

with

| (2.5) |

Remark. It is readily seen that is exactly the law of a continuous-time symmetric simple random walk on defined via

| (2.6) |

with being a sequence of independent Rademacher random signs and being a Poisson clock running at unit rate.

The distribution naturally preserves its mass (since it is a probability mass function) and the mean value (as the total amount of money in the whole system is preserved), thus if we introduce the affine subspaces:

| (2.7) |

and

then it is clear that the unique solution of (2.4)-(2.5) with satisfies for all . Moreover, if we define the average amount of “debt” per agent as

| (2.8) |

this quantity will be non-decreasing: . Since the average amount of debt each agent can sustain in the underlying stochastic -agents system is at most , we therefore terminate the evolution of Phase I (2.4)-(2.5) until , where

| (2.9) |

Remark. Thanks to the previous remark, . By the identity and the obvious symmetry, we deduce that is also unbounded as . This observation ensures the finiteness of the .

At the level of the agent-based system, after the first time when there is no cash in the bank, i.e., when , the analysis is much more involved so heuristic reasoning plays a major role in this manuscript. We notice that we have the following basic relations for all time :

| (2.10) |

and . Therefore, the evolution of is much faster than the evolution of each of the ’s, indicating that (2.10) is really a “fast” dynamics compared to (2.1). These observations motivate the next definition:

Definition 2 (Mean-field equation — Phase II)

We define (for ) to be the compound Poisson process satisfying the following SDE:

| (2.11) |

in which and are independent Poisson processes running at the unit intensity. Moreover, and are independent Bernoulli random variables with parameters

| (2.12) |

and

| (2.13) |

respectively.

We again denote by the law of the process for , i.e. for . Its time evolution is given by the following dynamics:

| (2.14) |

with

| (2.15) |

where

| (2.16) |

represent the proportion of “rich” and “debt” agents, respectively.

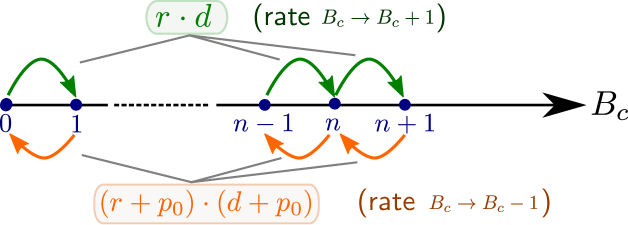

Remark. We will illustrate the basic intuition behind Definition 2. Under the large population limit , we denote by the law of . It is easily seen that the transition rates of can be described by figure 4 below.

That is, the transition occurs when a “rich” agent is being picked () and gives a dollar to an agent in “debt” (). Similarly, the transition happens when an agent without dollar is being picked () and gives a dollar to an agent with debt () and moreover . As the evolution of is a “fast” dynamics, we assume its distribution will relax to its ergodic invariant distribution within a time-scale that is negligible compared to the evolution of each of the ’s. Thus, from the following detailed balance equation at equilibrium

one arrives at for all . Taking into account that , we end up with

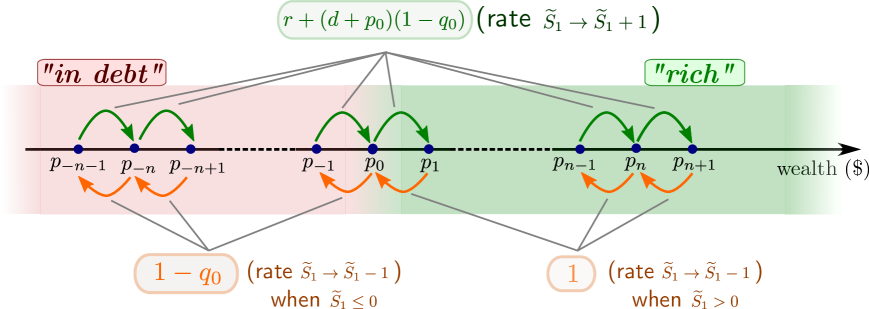

which is exactly (2.13). On the other hand, the transition rates of can be described by figure 5 below.

3 Large time behavior

Although our mean-field analysis is not completely rigorous, we will soon see that our system of ODEs (i.e., (2.4)-(2.5) for and (2.14)-(2.15) for ) converges to a double-geometric distribution as , which resembles an asymmetric Laplace distribution when becomes large. Taking into account the conjecture in [22] and the work of [18], as well as several numerical experiments, we believe that the two phase dynamics (1.3) accurately captures the mean-field behavior of the stochastic -agents dynamics as .

3.1 Elementary properties of the limit equation

In Phase II, the collective debt (2.16) is preserved, therefore we can further restrict the affine space where the solution of (2.14)-(2.15) lives:

| (3.1) |

it is straightforward to check that if then for all . Now, we identify the unique equilibrium solution associated with (2.14)-(2.15) in this space.

Proposition 3.1

Proof.

From the evolution equation in Phase II (2.14)-(2.15), it is straightforward to check that the equilibrium distribution takes the ascertained form (3.2). As we also have , we impose that

These constraints lead us to

Combining these relations with the elementary identity , we obtain the desired result.

Remark. Under the settings of Proposition 3.1, if we take while keeping fixed, the two-sided geometric distribution (3.2) can be well-approximated by the asymmetric Laplace distribution given by (1.4) and conjectured in [18, 22]. Furthermore, we have an estimation of the parameters of this distribution with

| (3.5) |

Indeed, by taking in (3.3), we can perform the following simple asymptotic analysis for :

Similarly, the asymptotic behavior of can be seem from the asymptotic analysis for . Thanks to (3.3), (3.4) and the asymptotic argument for above, we have

The argument for is pretty similar and hence will be omitted here.

3.2 Convergence to asymmetric Laplace distribution

The main goal of this section is to prove the convergence of the solution in Phase II (2.14)-(2.15) to its two-sided geometric equilibrium solution as . The essence of the method consists in studying the (relative) entropy dissipation between the two distributions. We remind the formula for estimating the relative entropy:

| (3.6) |

Theorem 1

Proof.

We split the computation of

into two parts. On the one hand, we have

where

| I | (3.8) | |||

| (3.9) |

and

| III | (3.10) | |||

Assembling (3.8)-(3.10), we end up with

| (3.11) |

On the other hand, straightforward computations lead us to

| (3.12) | ||||

Combining (3.11) and (3.12) gives rise to the advertised entropy dissipation result (3.7). The last statement of Theorem 1 can be handled in a pretty similar way as in the case for the basic unbiased exchange model (without the presence of a bank), see for instance [2] or [19].

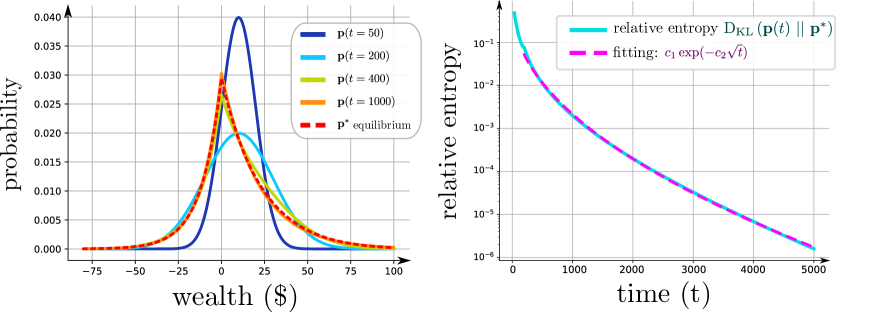

To illustrate the convergence of toward the equilibrium , we run a simulation and plot the evolution of at different times (see figure 6-left) as well as the evolution of the relative entropy over time (see figure 6-right). Notice that the decay of the relative entropy changes abruptly around which corresponds to the transition of the dynamics from phase I to phase II. During the phase II, the decay of the relative entropy is well-approximated by a decay of the form:

| (3.13) |

where the coefficients and are estimated using mean-square error criteria. We emphasize here that the ansatz for the decay of the relative entropy (3.13) is inspired from a very recent work on the vanilla unbiased exchange model [5], which corresponds to the special case of the model at hand where .

3.3 Linearization analysis

We perform a standard linearization analysis near the two-sided geometric equilibrium distribution . The hope is that for some ranges of parameter choices for and , the linearized entropy will decay exponentially fast in time. As we will soon realize, to enlarge the parameter choices of and for which the linearized entropy decreases exponentially fast, one has to find the best possible constants for certain Poincaré-type inequalities.

We linearize the ODE system (2.14)-(2.15) near its equilibrium , i.e., we set for for all to obtain the following linearized system around :

| (3.14) |

with

and

where we set

It is straightforward to check that

for all . Moreover, if we denote the linearized entropy associated with the linearized system (3.14) by

| (3.15) |

a direct computation yields

| (3.16) | ||||

We can bound as follows. Introduce by defining for and for . Similarly, let be defined by for and for , where and are constants whose choices will be optimized later. The definition of , together with the fact that , allows us to deduce that

Optimizing the values of and gives rise to and . Thus, we obtain

| (3.17) |

In a similar fashion, we also get

| (3.18) |

as well as

| (3.19) |

Thus, we have the following upper bound:

| (3.20) | ||||

On the other hand, we have the following simple lower bound on :

| (3.21) |

Indeed, we have

from which the advertised lower bound (3.21) follows. By a parallel reasoning, we also obtain

| (3.22) |

Combining (3.21) and (3.22) leads us to the following lower bound:

| (3.23) | ||||

To alleviate the writing, we define

| (3.24) | ||||

| (3.25) |

| (3.26) | ||||

| (3.27) |

and

| (3.28) |

Then we arrive at the following differential inequality for the linearized entropy :

| (3.29) |

If we recall the upper bound (3.19) on , in order to have an exponential decay result for the linearized entropy, it suffices to ensure that

| (3.30) |

For convenience, we denote by the collection of the parameter values for which the condition (3.30) is satisfied. We claim that this set is non-empty, whence the linearized entropy will decay exponentially fast in time for all .

Theorem 2

The set is not empty. Consequently, the linearized entropy defined by (3.15) decreases exponentially fast in time if .

Proof.

To demonstrate the non-emptiness of the set it suffices to present a specific example. For this purpose, we can take to obtain . The second part of the proposition follows immediately from the definition of and the differential inequality (3.29).

Remark. The lower bounds (3.21) and (3.22) are far from being optimal as their arguments rely sole on some elementary Cauchy-Schwarz inequalities and the constraint that has not been exploited at all. We speculate that these lower bounds (Poincaré-type inequalities) can somehow be significantly sharpened, leading to a refined version of Theorem 2.

4 Debt induced wealth inequality

We would like to conclude our analysis of the model by investigating the effect of the bank on the inequality of the wealth distribution, i.e. does the bank increase or decrease inequality? To measure inequality, we use the Gini index which is usually an indicator between (no inequality) and (maximum inequality) and measures the inequality in the wealth distribution, and a higher Gini index indicates worse equality in the society (in terms of the distribution of wealth).

Definition 3 (Gini index)

For a given probability mass function with mean , the Gini index of is defined by

| (4.1) |

Equivalently, a probabilistic definition of is given by

| (4.2) |

where has as its probability mass function and is an independent copy of .

Remark. Without debt, i.e. if for or , one can show that the Gini index is always between (no inequality) and (maximum inequality). Indeed, using triangular inequality:

| (4.3) |

However, the Gini index is no longer bounded if the wealth distribution includes debts. For instance, taking a Gaussian distribution with mean and variance , i.e. , we obtain:

| (4.4) | |||||

| (4.5) |

Thus, if , the Gini index could be arbitrary large.

We would like to compare the evolution of Gini index for the basic unbiased exchange model and the model at hand (with bank and debt) at the level of the deterministic ODE system, starting from the same initial distribution. First, we recall that the unbiased exchange model investigated in [2, 13, 16, 19] is a special case of the model studied in this work with , meaning that the bank does not exist and agents are not allowed to go into debt. The rigorous mean-field analysis shown in [2, 13, 19] implies that, if we denote by the law of the amount of dollars a typical agent has as , its time evolution will be given by:

| (4.6) |

with

| (4.7) |

where .

Intuitively, the model with bank investigated in this manuscript permits agents without dollars in their pocket or agents in debt to be picked to give, thus we speculate that the Gini index of the distribution solution of (1.3) is always larger than the corresponding Gini index of the distribution (if they start from the same initial condition).

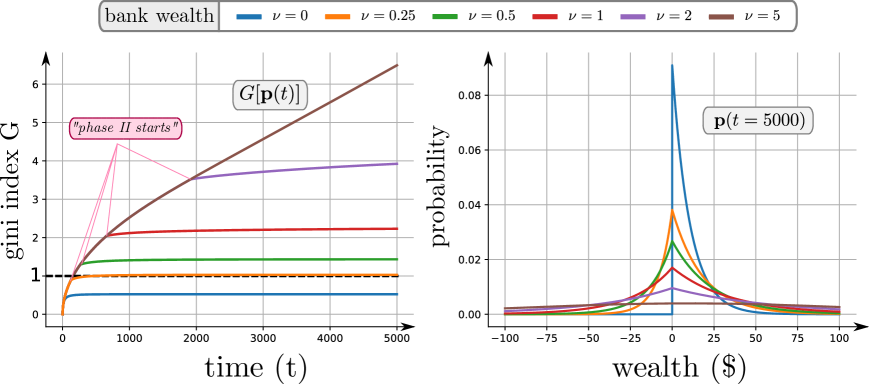

We provide in figure 7-left the evolution of the Gini index for different values of (which measures the ratio of the initial total amount of cash in the bank to the agents’ combined initial wealth). Without the bank, i.e., when , the Gini index quickly reaches its maximum around . However, when the bank comes into play (), the Gini index could eventually exceed . Moreover, the phases I and II are clearly seen in the evolution of the Gini index. In phase I, the Gini index grows like which is due to the diffusive nature of the dynamics coupled with formula (4.5). In phase II, the growth of the Gini index starts to saturate and the curve converges to its maximum. In figure 7-right, we provide the corresponding wealth distribution at the final time of the computation, i.e. , depending on the wealth of the bank . Without bank (), the distribution is exponential but it becomes an asymmetric two-sided exponential for . Notice that in the case where (which means that the bank has times more resources than the agents), the dynamics has not reached yet phase II at time as we observe in the evolution of the Gini index in figure 7-left. As a result, the distribution for is still far away from equilibrium and the characteristic cusp at zero dollar has not yet appeared.

Although we are not able to provide a complete proof of this natural and compelling conjecture based on heuristic reasoning and numerical simulations. The following simple observation is elementary:

Proposition 4.1

Proof.

We resort to the probabilistic representation of the Gini index (4.2), so we introduce independent random variables and having as their common probability mass function. If we set and let to be law of , it is trivial to see that the evolution of satisfies

| (4.8) |

from which we deduce that

In other words, the phase I evolution tends to accentuate the wealth inequality and the proof of Proposition 4.1 is completed.

5 Conclusion

In this manuscript, the so-called unbiased exchange model with collective debt limit is investigated, which can be viewed as an extension of the vanilla unbiased exchange model proposed in [12] and revisited in [2, 16, 19]. Although the inclusion of bank creates additional difficulty in the analysis and only a formal mean-field argument is presented, we found that the prediction of the asymptotic distribution of wealth as and based on our two-phase dynamics (1.3) agrees with the results reported/conjectured in earlier work [18, 22]. To the best our of knowledge, there are no (even formal) mean-field analysis for the model at hand prior to the present work and we believe that our work leaves many open and challenging questions to be investigated on a more rigorous ground. For instance, is it possible to provide a rigorous proof of the propagation of chaos as to arrive at the two-phase dynamics (1.3) ? How can we extend the recent work [4] to justify the ansatz for the decay of the relative entropy conjectured in (3.13) (for a fairly generic initial datum) ? Is it possible to show rigorously the monotonicity of the Gini index of (solution of (1.3)) with respect to during phase II ? The answer to these questions will enable us to have a better understanding of the role played by the bank and debt.

Lastly, we emphasize that econophysics models involving bank and debt have not received enough attention in the past few years, and the model investigated in this manuscript can be viewed as the representative of a promising and intriguing direction for further research in the area of econophysics. For instance, it would be interesting to introduce a bank in other closely related variants of the basic unbiased exchange model, such as the so-called poor-biased or rich-biased exchange model proposed in [2].

References

- [1] Didier Bresch, Pierre-Emmanuel Jabin, and Zhenfu Wang. On mean-field limits and quantitative estimates with a large class of singular kernels: application to the Patlak–Keller–Segel model. Comptes Rendus Mathematique, 357(9):708–720, 2019.

- [2] Fei Cao, and Sebastien Motsch. Derivation of wealth distributions from biased exchange of money. arXiv preprint arXiv:2105.07341, 2021.

- [3] Fei Cao, Pierre-Emannuel Jabin, and Sebastien Motsch. Entropy dissipation and propagation of chaos for the uniform reshuffling model. arXiv preprint arXiv:2104.01302, 2021.

- [4] Fei Cao. Explicit decay rate for the Gini index in the repeated averaging model. arXiv preprint arXiv:2108.07904, 2021.

- [5] Fei Cao, and Pierre-Emannuel Jabin. From interacting agents to Boltzmann-Gibbs distribution of money. arXiv preprint arXiv:2208.05629, 2022.

- [6] Fei Cao. -averaging agent-based model: propagation of chaos and convergence to equilibrium. Journal of Statistical Physics, 184(2):1–19, 2021.

- [7] Eric Carlen, Pierre Degond, and Bernt Wennberg. Kinetic limits for pair-interaction driven master equations and biological swarm models. Mathematical Models and Methods in Applied Sciences, 23(07):1339–1376, 2013.

- [8] Anirban Chakraborti, and Bikas K. Chakrabarti. Statistical mechanics of money: how saving propensity affects its distribution. The European Physical Journal B-Condensed Matter and Complex Systems, 17(1):167–170, 2000.

- [9] Arnab Chatterjee, Bikas K. Chakrabarti, and Subhrangshu Sekhar Manna. Pareto law in a kinetic model of market with random saving propensity. Physica A: Statistical Mechanics and its Applications, 335(1-2):155–163, 2004.

- [10] Roberto Cortez, and Joaquin Fontbona. Quantitative propagation of chaos for generalized Kac particle systems. The Annals of Applied Probability, 26(2):892–916, 2016.

- [11] Roberto Cortez. Particle system approach to wealth redistribution. arXiv preprint arXiv:1809.05372, 2018.

- [12] Adrian Dragulescu, and Victor M. Yakovenko. Statistical mechanics of money. The European Physical Journal B-Condensed Matter and Complex Systems, 17(4):723–729, 2000.

- [13] Benjamin T. Graham. Rate of relaxation for a mean-field zero-range process. The Annals of Applied Probability, 19(2):497–520, 2009.

- [14] Els Heinsalu, and Patriarca Marco. Kinetic models of immediate exchange. The European Physical Journal B, 87(8):1–10, 2014.

- [15] Ryszard Kutner, Marcel Ausloos, Dariusz Grech, Tiziana Di Matteo, Christophe Schinckus, and H. Eugene Stanley. Econophysics and sociophysics: Their milestones & challenges. Physica A: Statistical Mechanics and its Applications, 516:240–253, 2019.

- [16] Nicolas Lanchier. Rigorous proof of the Boltzmann–Gibbs distribution of money on connected graphs. Journal of Statistical Physics, 167(1):160–172, 2017.

- [17] Nicolas Lanchier, and Stephanie Reed. Rigorous results for the distribution of money on connected graphs. Journal of Statistical Physics, 171(4):727–743, 2018.

- [18] Nicolas Lanchier, and Stephanie Reed. Rigorous results for the distribution of money on connected graphs (models with debts). Journal of Statistical Physics, 176(5):1115–1137, 2019.

- [19] Mathieu Merle, and Justin Salez. Cutoff for the mean-field zero-range process. Annals of Probability, 47(5):3170–3201, 2019. Publisher: Institute of Mathematical Statistics.

- [20] Sebastien Motsch, and Diane Peurichard. From short-range repulsion to Hele-Shaw problem in a model of tumor growth. Journal of mathematical biology, 76(1):205–234, 2018.

- [21] Alain-Sol Sznitman. Topics in propagation of chaos. In Ecole d’été de probabilités de Saint-Flour XIX—1989, pages 165–251. Springer, 1991.

- [22] Ning Xi, Ning Ding, and Yougui Wang. How required reserve ratio affects distribution and velocity of money. Physica A: Statistical Mechanics and its Applications, 357(3-4):543–555, 2005. Publisher: Elsevier.