Do Investors Hedge Against Green Swans?

Option-Implied Risk Aversion to Wildfires††thanks: I would like to thank Serdar Dinc, Matthew E. Kahn, Jens Jackwerth,

Mathieu Naud, Piotr Orłowski, Toan Phan, David Thesmar, Ambika Gandhi

for insightful comments on preliminary versions of this paper. The

standard disclaimers apply.

Abstract

Measuring beliefs about natural disasters is challenging. Deep out-of-the-money options allow investors to hedge at a range of strikes and time horizons, thus the 3-dimensional surface of firm-level option prices provides information on (i) skewed and fat-tailed beliefs about the impact of natural disaster risk across space and time dimensions at daily frequency; and (ii) information on the covariance of wildfire-exposed stocks with investors’ marginal utility of wealth. Each publicly-traded company’s daily surface of option prices is matched with its network of establishments and wildfire perimeters over two decades. First, wildfires affect investors’ risk neutral probabilities at short and long maturities; investors price asymmetric downward tail risk and a probability of upward jumps. The volatility smile is more pronounced. Second, comparing risk-neutral and physical distributions reveals the option-implied risk aversion with respect to wildfire-exposed stock prices. Investors’ marginal utility of wealth is correlated with wildfire shocks. Option-implied risk aversion identifies the wildfire-exposed share of portfolios. For risk aversions consistent with Barro (2012), equity options suggest (i) investors hold larger shares of wildfire-exposed stocks than the market portfolio; or (ii) investors may have more pessimistic beliefs about wildfires’ impacts than what observed returns suggest, such as pricing low-probability unrealized downward tail risk. We calibrate options with models featuring both upward and downward risk. Results are consistent a significant pricing of downward jumps.

1 Introduction

Natural disaster risk is receiving increasing attention by both academics and policymakers preparing for a potential “Green Swan” [bolton2020green, rudebusch2021climate]. What are market participants’ beliefs about the wealth impact of natural disasters? Measuring such beliefs is challenging as they may be (a) asymmetric, as firms may lose or gain; (b) fat-tailed, as natural disasters may cause large jumps and volatility shifts; (c) non-stationary, as agents learn about the probability distribution of disaster risk over time; (d) heterogeneous, as firms have different levels of adaptation to disasters; and (e) ambiguous as different forecasters provide different probability distributions. A seminal literature uses surveys to measure beliefs about assets’ risk exposure [bakkensen2017flood], and about the evolution of future disaster risk [leiserowitz2010climate, ballew2019climate]. Yet, eliciting high frequency and spatially heterogeneous beliefs about climate risk for the United States at both local and national levels, and for short- and long-run time horizons, remains challenging.

The exchange-traded market for options is a fast-growing global market with a total volume of 33.3 billion contracts in 2021111Futures Industry Association, January 19, 2022. that allows financial agents to trade hedges for firm-, time-, and maturity-specific risks. The surface of option prices by maturity and strike depends on market participants’ subjective probability distribution as well as the marginal utility of consumption or wealth, thus revealing the set of Arrow-Debreu prices for each level of each climate-exposed stock [breeden1978prices, ait2003nonparametric, beber2006effect, figlewski2018risk]. Such surface typically displays a ’smile’ or ’smirk’ that steepened significantly after the 1987 market crash [benzoni2011explaining], as market participants hedge against large downward and upward tail risks. Teasing out what, in Arrow Debreu state prices, is driven by the marginal utility of wealth and by beliefs about risks enables an estimation of investors’ aversion to natural disaster risks.

This paper measures the response of investors’ hedging to natural disaster shocks, compares this response to observed returns, and identifies investors’ option-implied risk aversion with respect to such natural disasters. It matches the universe of establishments, sales, and employment of publicly-traded firms between 2000 and 2018 to their daily surface of option prices by strike and maturity, and to the boundaries of wildfire perimeters reported by fire departments across the United States. First, the paper estimates the daily risk neutral distribution implied222Option prices are de-americanized using the procedure evaluated by \citeasnounburkovska2018calibration, which converts American option prices into European option prices using \possessivecitecox1979option binomial trees to recover implied volatilities. Alternatives involve solving partial differential equations with a boundary condition for each firm day strike maturity. by the surface of option prices333The paper uses a method close to \possessiveciteait2003nonparametric arbitrage-free prices described in Section 3.2. Other important alternatives for estimating the risk neutral distribution include \citeasnounfiglewski2009estimating and \citeasnounfiglewski2018risk. for all day-firms affected by a wildfire, and for an equal-sized set of control surfaces, at short-, medium-, and long-run time horizons. This panel approach can non-parametrically estimate the impact of wildfires on the risk neutral distribution over and above day- and firm-specific confounders. Second, over the last two decades the paper estimates a significant impact of exposure to wildfires on the price in deep out-of-the-money options, controlling for day- and firm-specific confounders. This increase in prices is over and above what a log normal distribution of stock prices would imply. Third, the paper compares such risk neutral probabilities to the physical probabilities, thus inferring investors’ marginal utility for each level of a wildfire-exposed stock. This yields a risk aversion parameter with respect to each wildfire-exposed stock. Fourth, the paper develops a continuous time \citeasnounmerton1969lifetime model with a wildfire stock and the index to tease out risk aversion with respect to the index from that with respect to the wildfire-exposed stock. Portfolio shares are typically unobserved, and this paper’s novel approach provides, ‘in reverse’, the weight of wildfire stocks implied by deep out-of-the-money option prices. Fifth, the paper calibrates investors’ marginal utility at the levels of each wildfire-exposed stock to disentangle what, in the impact of wildfires on the risk neutral distribution is due to marginal utility from what is due to change in beliefs.

The paper puts forward and implements a fast and efficient way to identify the impact of natural disasters on investors’ risk-neutral probability distributions for each firm and for each maturity at daily frequency. Using such daily probability surfaces, the paper estimates the impact of wildfires on the risk neutral distribution non-parametrically when affected by a wildfire. This enables an estimation of the impact of wildfires on beliefs’ (a) asymmetry, (b) fat tails, and (c) non-stationarity. Results suggest that when a firm’s network of establishments is exposed to a wildfire, the risk neutral probability of downward tail events increases but is heterogeneous across industries, while they have a small but precisely estimated positive impact on the risk neutral probability of upward movements. Impacts are observed for short and long maturities.

Backing out risk neutral distributions from option prices requires using arbitrage-free prices. Since such arbitrage opportunities may be observed, prices are converted into arbitrage-free prices that do not exhibit possibilities of butterfly, calendar spread, or call spread arbitrage [carr2005note]. Yet, wildfires show little correlation with the difference between arbitrage-free and observed prices, suggesting that there may be few opportunities to take advantage of ‘climate risk’ arbitrage opportunities in vanilla option markets. This also suggests that arbitrage opportunities are unlikely to drive the paper’s main findings.

Investors’ hedging against downward and upward tail risks is typically associated with a steeper implied volatility smile [bakshi2003stock]. The surface of implied volatilities is a simple transformation of the surface of option prices such that, if the firm’s stock followed a geometric diffusion process, the implied volatility would be independent of strike and maturity. In the short-run, wildfires have a greater impact on the implied volatility smile for low strikes than for strikes higher than the forward price: the impact is asymmetric, suggesting that market participants hedge more against the downside than for the upside. Over medium and long run time horizons, the lower hedging for the upside remains: markets price a lower probability of an upside. Impacts are long-lasting, with a smile that persists after the first wildfire.

Results on the risk neutral distribution and the volatility smile are obtained either in a linear panel data regression with day and firm fixed effects with daily data between 2000 and 2018; they are also obtained using a more flexible non-parametric approach pooling all day-firm surfaces after orthogonalization with respect to firm and day-specific confounders.

Option prices can also enable an identification of the correlation of investor’s wealth with wildfires. Arrow Debreu state prices are the product of the marginal utility of investors, the physical probability of each state, and the risk free discount factor. As each wildfire-exposed stock represents a small share of the S&P 500, wildfire stocks could be statistically uncorrelated with investors’ wealth, once controlling for the stock’s beta with respect to the index. If movements in wildfire-exposed stocks were uncorrelated with investors’ marginal utility of wealth or consumption, risk neutral probabilities would be proportional to the physical probabilities. We compare the Arrow Debreu state prices for each day-firm to the physical probability distribution of future returns to estimate investors’ risk aversion with respect to the wildfire stocks. This also identifies the marginal utility of investors at each level of the wildfire-exposed stock.444This paper’s results suggest that most firms exhibit pricing kernels with negative slopes consistent with decreasing marginal utilities of standard microeconomic models: between 87.4% and 90.5% of the firms have a strictly negative slope of the pricing kernel w.r.t. the log of the forward price. When considering index options, an extensive literature provides evidence of pricing kernel puzzles and methods to address them, e.g. \citeasnounlinn2018pricing. The first finding is that the ratio of risk neutral to physical probabilities significantly differs from a constant for treated stocks. This suggests that investors’ marginal utility is significantly correlated with wildfire shocks. Results provide a firm-level elasticity of state prices with respect to the level of the stock.

Such risk aversion with respect to a specific stock can reveal the weight of the stock in the investor’s portfolio. We develop a \citeasnounmerton1971optimum portfolio allocation problem with two risky assets, the index and a wildfire-exposed stock, to separately identify what, in investors’ demand for equity options, is driven by the beta of the wildfire-exposed stock w.r.t the index from what is driven by wildfires. Proposition 1 of Section 5.1 shows that the Arrow-Pratt risk aversion with respect to a single stock is proportional to the relative risk aversion with respect to wealth, where the proportionality constant is a linear function of the share of the stock in the investor’s portfolio and the beta of the stock w.r.t. the market. Using the option-implied risk aversion with respect to the stock, assuming that the investor holds the market portfolio, and using the estimated betas from CRSP, we can identify the risk aversion with respect to wealth that is consistent with the option-implied risk aversion with respect to the wildfire-exposed stock.

Assuming the market portfolio, the option-implied relative risk aversion w.r.t wealth is significantly higher than that suggested by \citeasnounbarro2006rare, \citeasnounbarro2012rare, or \citeasnounmehra1985equity. This is consistent with (i) investors holding shares of wildfire-exposed stocks larger than what the market portfolio implies, markets may be segmented as in \citeasnoungabaix2007limits; (ii) a mismeasurement of the physical probability distribution, which reflects investors’ beliefs; thus investors’ beliefs are not well captured by the realization of past or future returns; this would include investors’ expectations of rare tail risk, that does not materialize with high enough frequency in the sample of wildfire-exposed stocks, a phenomenon suggested for the index by \citeasnounbarro2012rare.

The last part of the paper parameterizes the risk neutral distribution using \possessivecitemerton1976option jump-diffusion model, and \possessivecitekou2004option double exponential jump model to be able to observe the pricing of both upward and downward shocks in the same model. Results of this calibration on the treatment group (affected by wildfires) and the control group (unaffected) suggest a small increase in the pricing of upward jumps, but a doubling in the risk-neutral magnitude of downward jumps.

merton1976option suggests that jumps are a source of market incompleteness, as riskless delta hedging is not typically feasible. A set of state-contingent parametric insurance, with a payoff tied to the occurrence of wildfires for each specific area, could allow market participants to hedge wildfire risk. The calibration of the options, by providing the risk neutral distribution, allows the pricing of such parametric insurance.

This paper contributes to at least three literatures. First, the growing literature on the impact of natural disaster on option prices. \possessivecitekruttli2021pricing important contribution provides convincing evidence of an increase in the at-the-money implied volatility of firms affected by a hurricane. The paper also finds that, for firms hit by hurricanes, the variance risk premium, i.e. the difference between the implied volatility and the realized volatility, is a significant predictor of future stock returns. This paper’s model-free approach to the recovery of the risk neutral distribution from option prices has two benefits that complement \possessivecitekruttli2021pricing key insights. First, this paper provides the entire probability distribution by stock level and by time horizon (maturity) and thus can separate symmetric uncertainty (volatility) from asymmetric expectations of gains and losses. As such, this paper’s approach reveals the response of the moments of the risk neutral distribution and the downside and upside hedging of investors: this enables an identification of downward and upward tail risks separately, as investors perceive the possibility of firms’ recovery in the short-, medium-, and long-run. This enables the identification of jump risk separately from stochastic volatility, as the calibration of option prices as in \citeasnounduffie2000transform enables the identification of the jump diffusion processes consistent with the surface of option prices. An emerging literature studies the skewness risk premium [orlowski2020nature]. Second, this paper’s approach has the benefit of identifying investors’ option-implied risk aversion, and thus reveals the importance of wildfire shocks for investors’ portfolio. Results suggest that wildfire shocks matter more than if investors held the market portfolio.

This paper also contributes to the literature on the estimation of beliefs. An important literature uses surveys to measure beliefs about the specific risk exposure of assets [bakkensen2017flood], and about the evolution of future climate risk [leiserowitz2010climate, ballew2019climate]. The economics literature has shown that stated beliefs have predictive power for individual behavior [manski2018survey], predict portfolio allocation [giglio2021five] and shape macroeconomic outcomes [fuster2010natural]. This paper suggests that option prices provide a low-cost, high-frequency, and spatially heterogeneous way of measuring beliefs in natural disaster risk at multiple time horizons. The absence of a significant correlation between arbitrage opportunities and wildfire risk suggests that this recovers well-behaved impacts on the risk neutral probability distribution.

This paper contributes to the literature on risk aversion and asset pricing. In the mortgage-backed securities (MBS) market, \citeasnoungabaix2007limits suggests that prepayment risk, which is diversified in the aggregate, is priced in MBS yields. They also find that the sign for the correlation between income and yields is the opposite of what would be expected. Their conclusion is that markets are segmented. This paper is also in the flavor of \citeasnounfroot1999pricing, which finds that the price of catastrophe reinsurance is unusually high, lending support for a segmented trading of such assets; in this paper, we find that the pricing of deep out of the money puts is significantly higher than the pricing when investors hold a diversified portfolio.

The response of option prices to transitory shocks is akin to \possessivecitedessaint2017managers finding that the managers of firms located next to hurricane-hit areas tend to express concerns about hurricanes in their 10-Ks/10-Qs, and increase cash holdings, even when actual risk remains unchanged. This paper suggests that such concerns translate into the pricing of downward tail risk in out-of-the-money options, but also in upward tail risk pricing. It is also closely related to \citeasnounorlik2014understanding on Black Swans: when people form expectations like Bayesian econometricians, and when they estimate tail risk probabilities dynamically, small changes in estimated skewness cause large changes that “whip around” the probabilities of unobserved tail events.

Finally, this paper contributes to the literature on firms’ adaptation to natural disaster risk [kahn2020climate]. This paper provides a method for identifying the option-implied price of wildfire insurance, a set of state-contingent and spatially-located Arrow Debreu assets whose price is the risk neutral price of downward tail risk. This paper’s wildfire data suggests a significant upward trend in the probability that a Zip code is in a wildfire perimeter. Results suggest long-run impacts of wildfires on the implied volatility smile, but such long-run impacts are priced in after the first exposure to a wildfire rather than cumulatively per wildfire. Hence option prices may provide an adaptation signal [kahn2021adapting]. Out of the money put and call options are part of the set of hedging devices that enable investors to weather natural disaster risks. And, in reverse, investors’ demand for such options reveals their expectations of firms’ ability to adapt to natural disasters. In this sense, this paper’s causal estimates are the reduced-form estimates of firms’ adaptation responses.

The paper is structured as follows. Section 2 describes the main data set: the daily set of option implied volatilities and prices by strike and maturity, matched to each publicly-traded firm’s geocoded network of establishments and wildfire perimeters. Section 3 describes the relationship between option prices and their implied risk neutral distribution. It estimates the firm-level risk neutral distribution at daily frequency between 2000 and 2018 for listed firms using the convexity of option prices. It estimates the impact of wildfires on the risk neutral moments, the lower and upper tails, as well as the central part of the probability distribution. Section 4 estimates the model-free impact of wildfires on the volatility smile, using daily longitudinal panel data controlling for day and firm-level unobservables. Section 5 then estimates the relationship between the risk neutral distribution and the physical distribution for wildfire-exposed stocks, thus identifying a correlation between investors’ marginal utility and the value of wildfire-exposed stocks. This yields an option-implied risk aversion. Section 7 calibrates the surface of option prices to tease out whether wildfires cause in upward and downward jump intensity or magnitude. Section 8 concludes.

2 Data Sets

Estimating the impact of natural disasters on the surface of option prices, on Arrow-Debreu prices, and on investors’ beliefs requires four data sets. First, the universe of establishments of publicly-traded companies. Second, the spatial footprint of natural disasters at daily frequency. Third, option prices by maturity and strike at daily frequency. Fourth, stock prices and dividends to build physical probability distributions that can be compared to the risk-neutral distribution of Arrow-Debreu prices.

2.1 The Geography of Publicly-Traded Companies’ Establishments

The first source of data is Dun and Bradstreet’s NETS for the 50 states and the District of Columbia between 2000 and 2018. NETS provides the geographic location of establishments, with their employment, sales, and 8-digit NAICS code at annual frequency. \citeasnounbarnatchez2017assessment compares NETS data to the County Business Patterns (CBP), the Nonemployer Statistics, and the Quarterly Census of Employment and Wages (QCEW) and finds that the data set covers three quarters of U.S. private sector employment. The study finds that the county-level correlation of NETS employment and CBP employment is typically above 0.99. We follow the convention of \citeasnounecheverri2019chasing in omitting the last two years of data, which can be subject to revisions. Other studies using NETS and comparing it to administrative data counts include \citeasnounneumark2011small. Recent work using NETS includes \citeasnounsong2019firming.

A key feature of NETS is its inclusion of the ticker symbol when the establishment is the headquarters of a publicly-traded firm. It also links a parent firm with its subsidiaries. Hence the data enable the estimation of each publicly-traded firm’s geographic footprint. We compute the number of establishments, the employment, and the sales of each publicly traded firm in each 5-digit Zip code. As NETS is longitudinal, the data also enable the estimation of the relocation of a firm’s establishments over time in response to climate shocks. Thus this paper’s estimates use the firm’s latest measured geographic footprint and exposure to wildfires, which may respond to expectations or experiences of climate risk.

2.2 Wildfire Risk

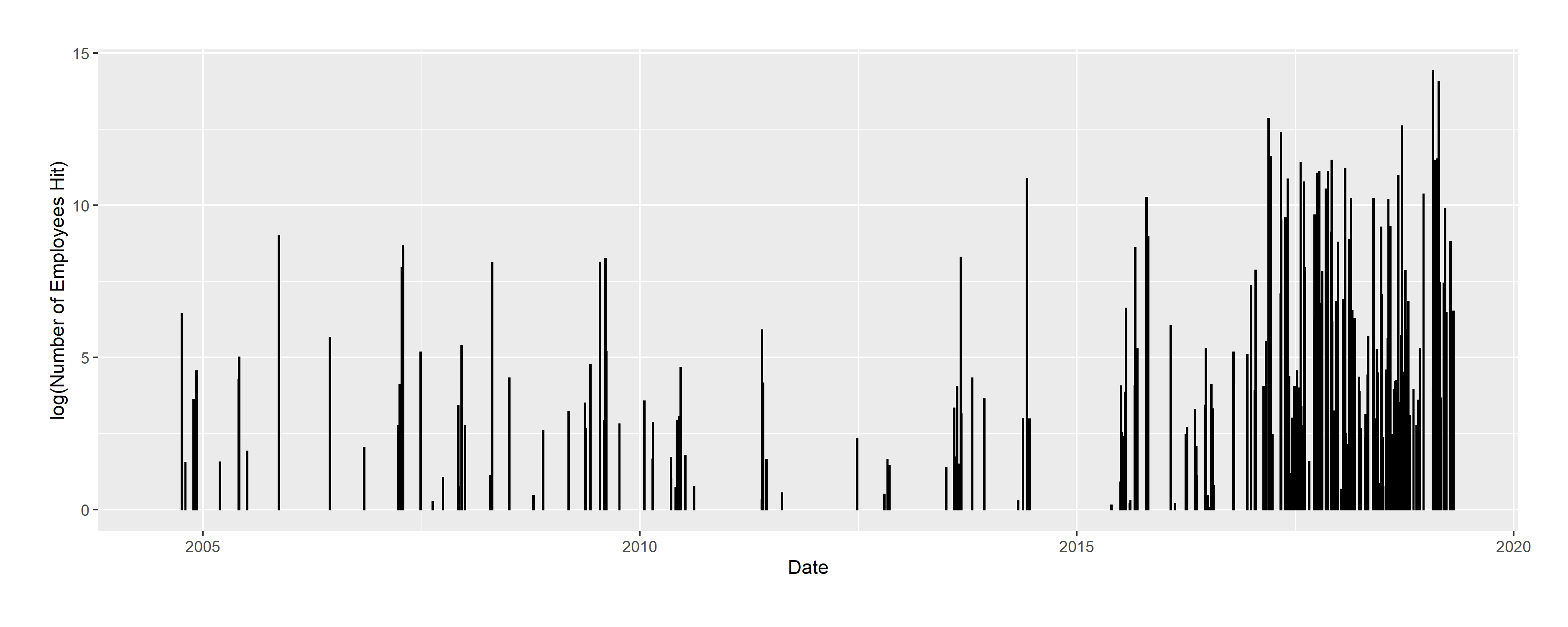

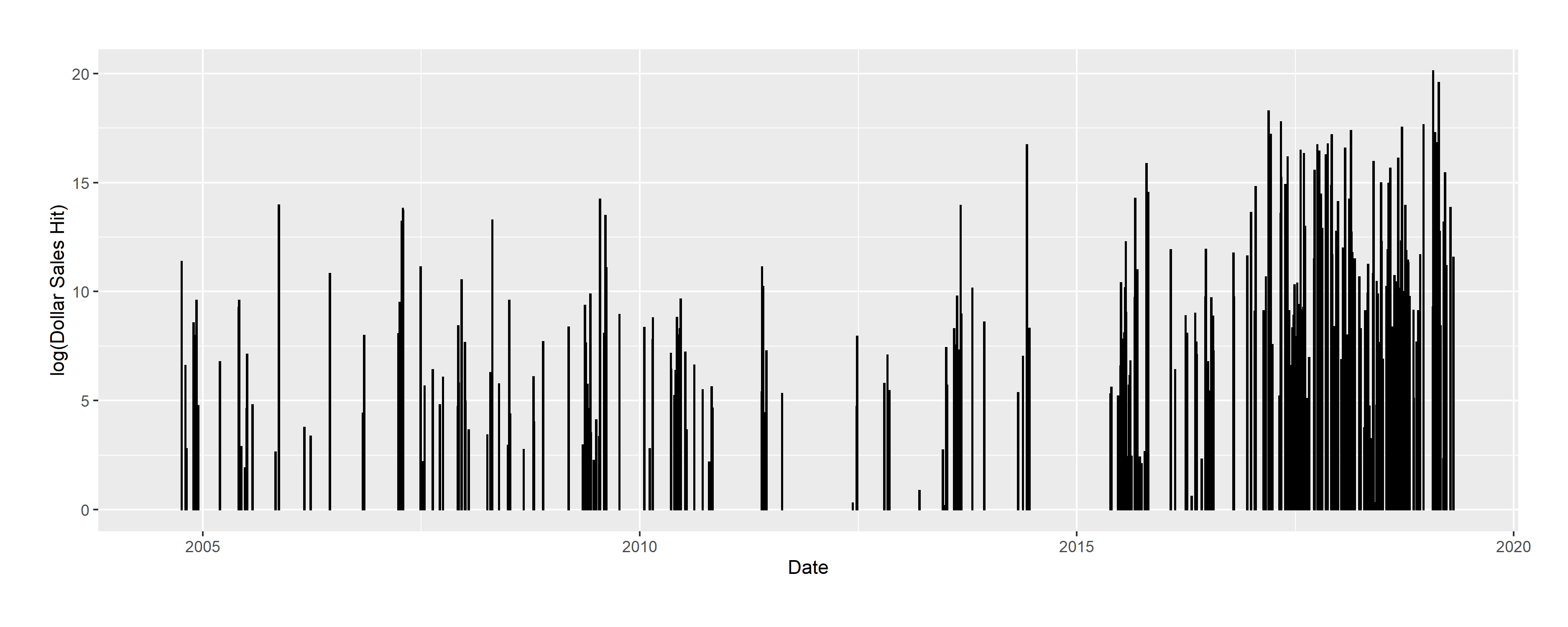

Wildfire perimeters and dates are provided by the Development and Application team of Wildland Fire Management Research at the National Interagency Fire Center. Such center coordinates the actions of local firefighting agencies and records the polygon of each fire’s perimeter, the date of the fire, the number of acres burnt, the reporting agency; for a total of 43,114 wildfire perimeters on 829 separate dates, with an average of 726 perimeters per year, 67 million acres in total, and an average of 3,771 acres per perimeter. For each 5-digit Zip Code (Census ZCTAs) we record the area of the Zip code intersecting the wildfire perimeter in the US National Atlas Equal Area coordinate reference system. Wildfires affected 1,964 5-digit Zip codes. The share of a publicly-traded firm’s establishments, sales, and employment hit by a wildfire depends on the share of its establishments in each of the US’s 33,120 ZCTAs. We use the boundaries of 2014 ZCTAs. The log number of establishments, employees, and sales hit by a wildfire according to this definition are presented on Appendix Figure A. The figures suggest a substantial increase in the number of establishments, employees, and sales hit by a wildfire over time.

2.3 Option Prices and Implied Volatility

Our option data comes from OptionMetrics’ IvyDB US, which covers all US-listed equity options. We consider data on the same time period as the Dun and Bradstreet data, i.e. from January 2000 till December 2018. The data include the strike, maturity, call/put indicator, best bid/ask prices and we use the midpoint as the option price. We estimate the moneyness of the option using ratio of the strike over the forward price. Implied volatility is obtained by OptionMetrics using binomial trees, which account for the possibility of early exercise. Option prices are de-Americanized using the methodology described by \citeasnounburkovska2018calibration, which converts binomial-tree implied volatilities into European option prices.555\citeasnounburkovska2018calibration provides numerical bounds for the absolute statistical biases in prices potentially introduced by this approach, ranging between and . In total, this comprises 2.36 billion equity option day maturity strike observations. To work with a more manageable data set amenable to a panel regression with multi-way fixed effects, we (i) include all option prices of treated (wildfire-exposed) firms, and (ii) a random sample of 500 untreated firms on a random 5% of trading days. We end up with a sample of 16,842,463 option prices.

2.4 Descriptive Statistics

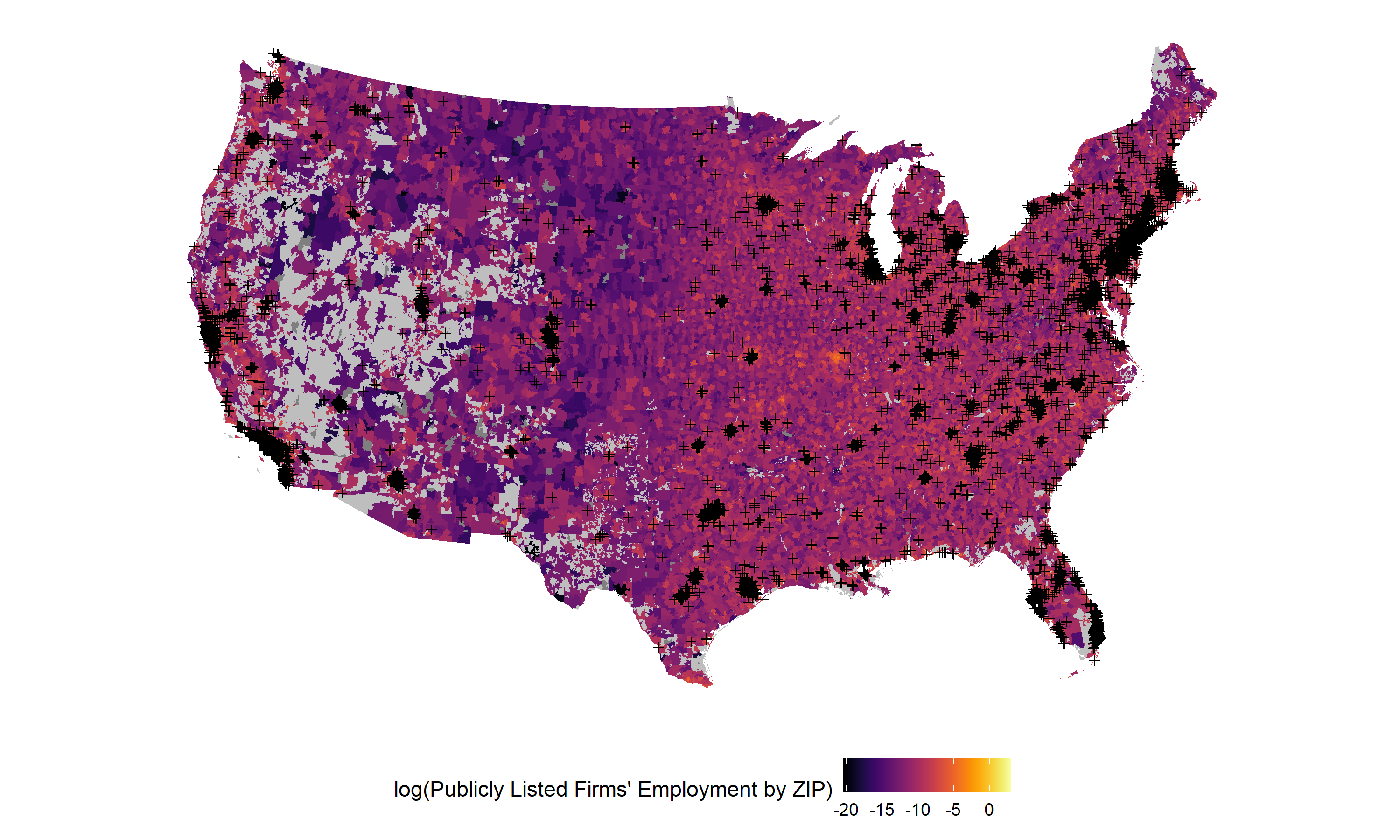

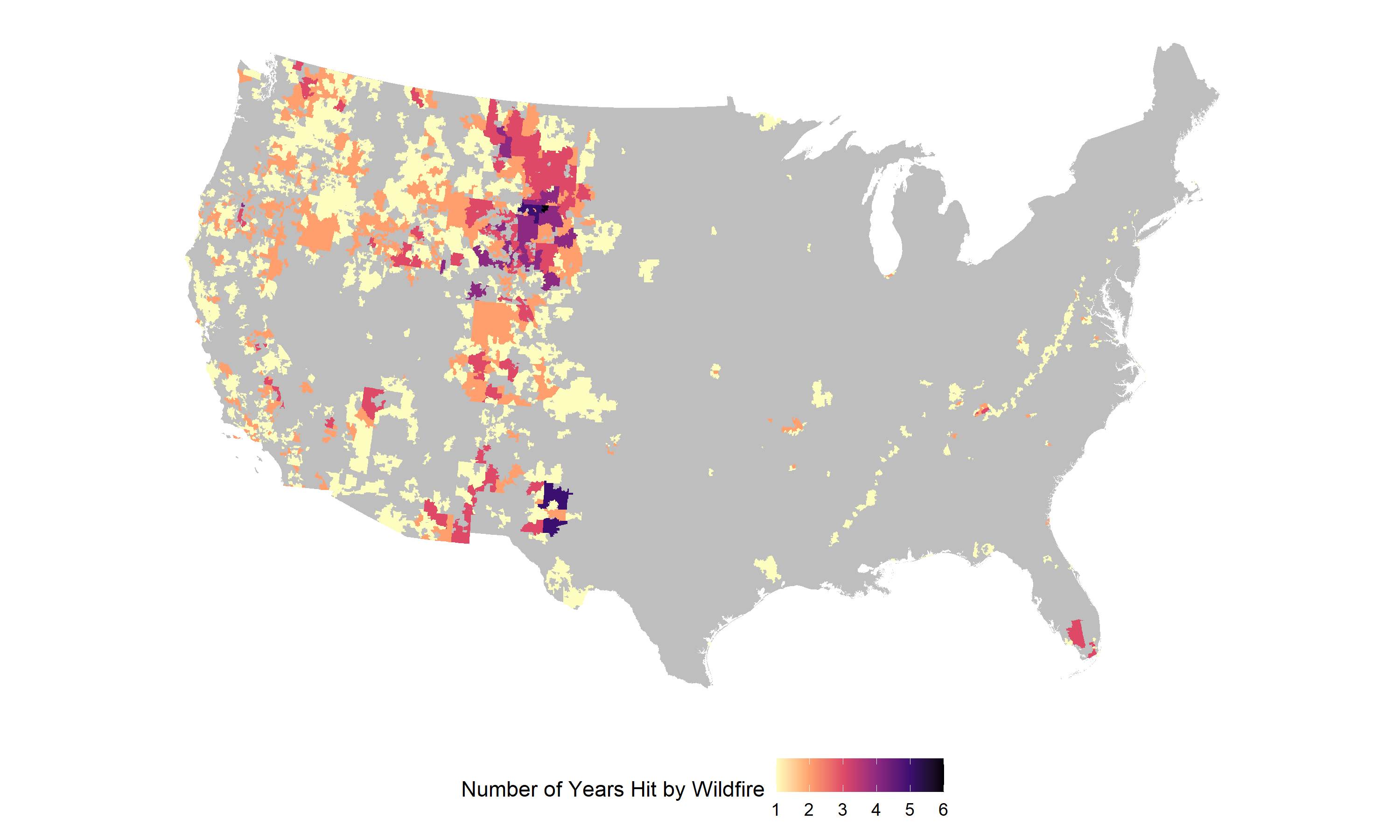

Figure 1(a) presents the spatial distribution of publicly-listed companies’ employment. For each listed company, the map estimates the number of employees in each 5-digit Zip code on average between 2000 and 2018, represented by colors from black to yellow. The black dots are for the headquarters. The map suggests that NETS data covers the coterminous United States, and that the employment captured in this paper extends beyond the location of the headquarters. Figure 1(b) presents the spatial distribution of wildfires between 2000 and 2018. The colors correspond to the number of years that a 5-digit Zip code was hit by a wildfire. The map suggests that wildfires hit most of the forests of the Western part of the United States, forests of the Pacific Northwest and Southwest, the Intermountain area, the Northern region, the Rocky Mountain region, and the Southwestern region. They also affected the George Washington and Jefferson forests in the Appalachians, the Ozark and Ouachita forests in Arkansas, Southernwestern Florida, but also the Sam Houston forest in Texas, the Tallageda forest in Alabama.

3 Option-Implied Risk Neutral Probabilities of Natural Disasters

3.1 Identifying Probability Distributions from the Surface of Option Prices

The surface of option prices by maturity and by strike reveals market participants’ set of Arrow Debreu prices at each level of the future stock price and for each maturity. This appears when considering the price of a European option, which can be exercised at maturity, before considering the case of American options.666The de-Americanization approach used in this paper is described in Section 2.3 and assessed by \citeasnounburkovska2018calibration using Monte Carlo simulations. At time , the payoff of a European call option with maturity and with strike is the expectation of the payoff at :

| (1) |

where the expectation is taken at with respect to the risk neutral distribution, whose pdf is denoted , consistent with the notations of \citeasnounait1998nonparametric. This risk neutral distribution typically differs from the physical distribution of the stock price, noted . We investigate what we learn from their differences in Section 5.1. The price of the option is thus:

| (2) |

where is the risk-free rate.

When the strike increases marginally, it has two impacts on the call price. First, the lower bound of integration changes, and second the payoff declines. \citeasnounbreeden1978prices shows that this leads to a simple relationship between the derivatives of the option price with respect to the strike and the risk neutral distribution:

| (3) |

where is the cumulative risk neutral distribution function. Hence this suggests that the convexity of option prices at the strike identifies the price of an Arrow-Debreu asset that pays off $1 when at maturity . This key result, implemented using arbitrage-free approaches of \citeasnounait2003nonparametric enables an estimation of the Arrow-Debreu prices of states in which a climate shock hits.

This approach provides the risk neutral distribution at each time , for each stock price , and for each maturity . It enables an estimation that depends on investors’ time horizon, an estimation of belief updating, and recovers a rich probability distribution parameterized by exposure to wildfires, allowing a comparison at each future level of the stock for a range of maturities.

3.2 Estimation Technique: Arbitrage Free Prices and the Convexity of Option Prices

breeden1978prices approach described in equation (3) suggests that the convexity of option prices reveals the risk neutral distribution for each maturity. Practical implementation requires arbitrage-free option prices.

Observed option prices may display arbitrage opportunities [carr2005note], and a naive approach consisting of taking the second-difference of observed prices may not yield the risk neutral distribution. First, call prices may not be convex, which may be a source of butterfly arbitrage [carr2005note]. Second, call prices may not be decreasing in the strike, which may lead to a call spread arbitrage opportunity. Third, observed call prices may not be higher than , leading to potential calendar spread arbitrage.

We address this concern by estimating arbitrage-free option prices using a method close to the approach of \citeasnounait2003nonparametric. We first de-Americanize option prices using the method described in Section 2.3. We then estimate the closest prices, in the least-squares sense, that satisfy the three no-arbitrage conditions above. This is done by a constrained linear least squares similar to \citeasnounait2003nonparametric but allowing here for an unequal grid of strikes whenever such grid is observed. Such unequal strike steps are common when considering options on individual equities. This first step yields a vector of arbitrage-free call prices for each observed strike.

Finally, we estimate the second derivative with a local polynomial regression of order 4 with a Gaussian kernel. The second-derivative of option prices is the coefficient of the second order term in the strike. In contrast with \citeasnounmalz2014simple, we allow the probabilities to be nonzero at the boundaries of the support of traded strikes and assess the impact of wildfires on the support of traded strikes in a second step.777Another choice here is to extrapolate the risk neutral distribution outside the support of observed strikes [figlewski2009estimating, birru2012anatomy], which requires distributional assumptions. This paper does not make specific distributional assumptions about probability distributions and rather estimates the impact of wildfires on the support. Both steps (arbitrage free and second derivative) rely on a constrained least squares approach with an interior point optimization algorithm.888Both steps use Matlab’s lsqlin procedure.We use a grid of 100 equally spaced strikes , with the same range as the observed strikes for . is the support. Formally, the risk neutral distribution at point is the coefficient in the optimization program:

| (4) |

with . The function is a Gaussian kernel, where the bandwidth was selected as in \citeasnounait2003nonparametric.

Important alternative methods include \citeasnounjackwerth1996recovering and \citeasnounfiglewski2009estimating. Recent reviews include \citeasnounfiglewski2018risk and \citeasnouncuesdeanu2018pricing.

3.3 Wildfires and Arbitrage Opportunities

To see whether wildfires cause the emergence or the increase in arbitrage opportunities, we compute the difference between the arbitrage-free prices of \citeasnounait2003nonparametric and the observed prices. We regress such difference on the treatment indicator variable at different maturities. Results are presented on Appendix Table C, with three different approaches for the dependent variable. Column (1) uses the dollar difference, column (2) the absolute value of the dollar difference, and column (3) the log of the absolute value of the difference. The table presents results for 5 different ranges of maturities. Results are similar when pooling all maturities. Results suggest that most coefficients on the treatment indicator are not significant, and often of small magnitude. These results also suggest that there may not be ‘climate risk’ arbitrage opportunities based on the butterfly, the calendar, and call spreads.

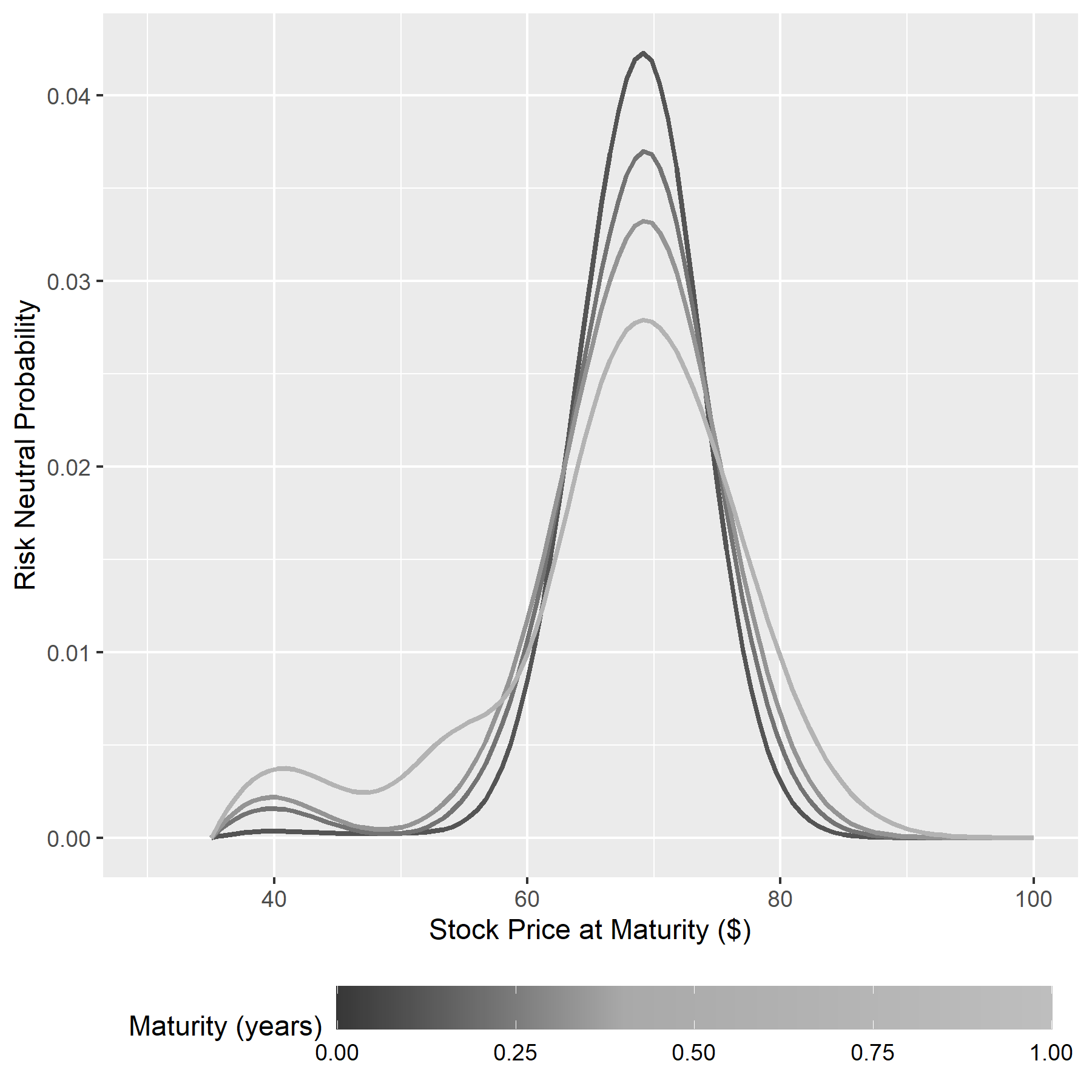

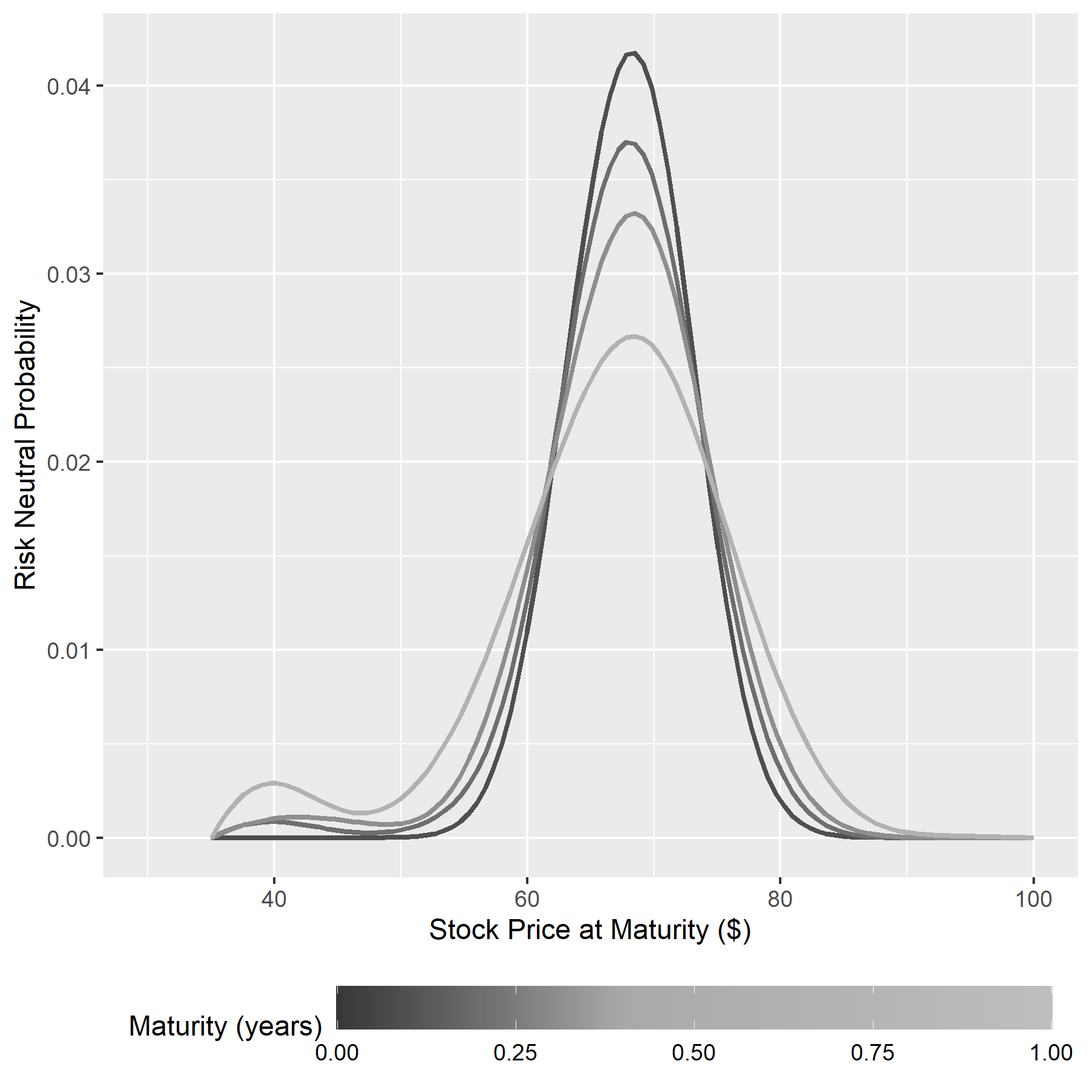

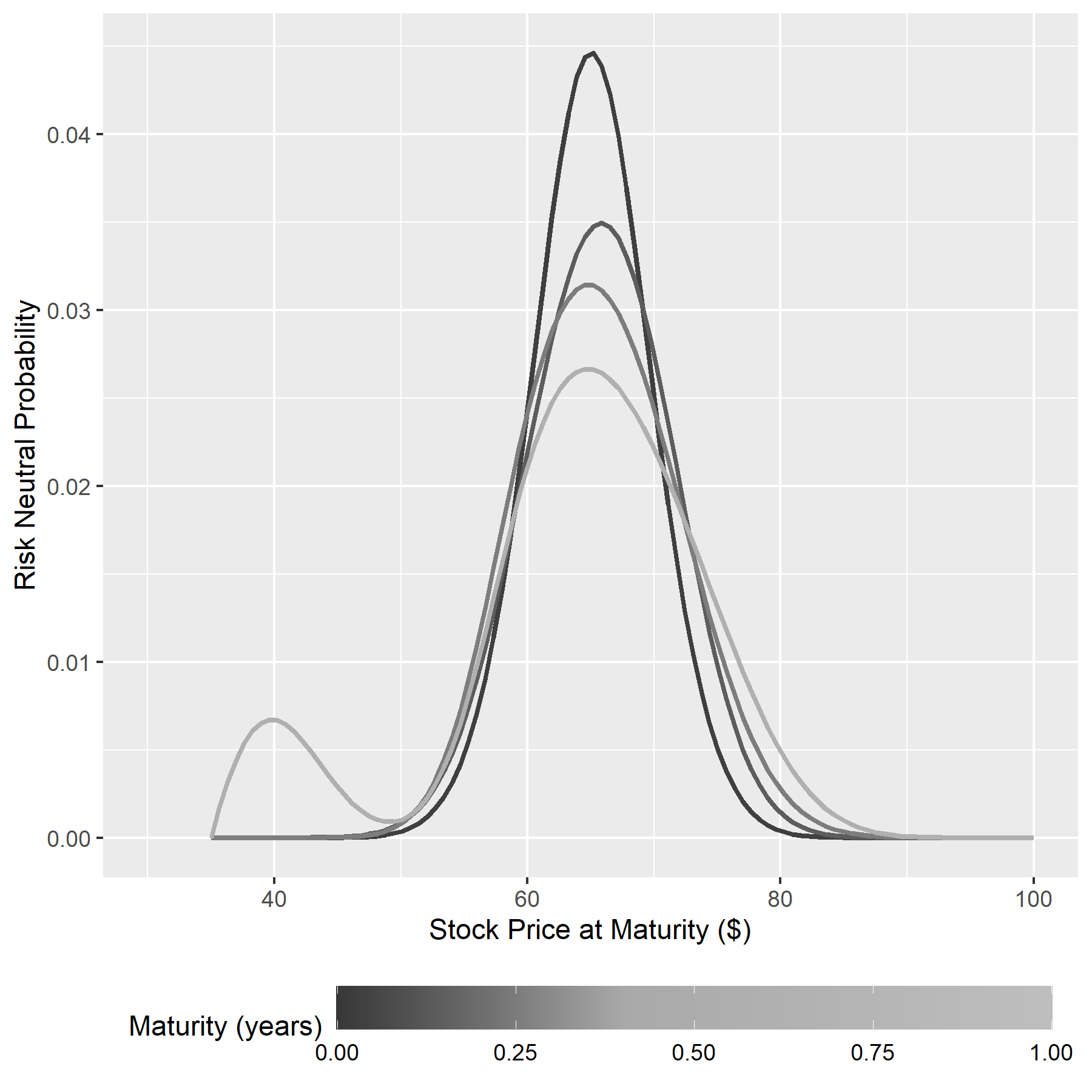

3.4 PG&E’s Risk Neutral Distribution during the October 2017 Wildfires

The Northern California wildfires broke a record as the most destructive wildfires in California’s history, with an estimated 44 deaths, 250,000 acres hit [mass2019northern], 100,000 evacuated and 8,900 structures destroyed.999California Statewide Fire Summary, Monday, October 30, 2017. The California Department of Forestry and Fire Protection released a report on June 8, 2018 stating that:101010Michael Mohler, ”CAL FIRE Investigators Determine Causes of 12 Wildfires in Mendocino, Humboldt, Butte, Sonoma, Lake, and Napa Counties”, June 8, 2018.

After extensive and thorough investigations, CAL FIRE investigators have determined that 12 Northern California wildfires in the October 2017 Fire Siege were caused by electric power and distribution lines, conductors and the failure of power poles.

The PG&E Fire Victim Trust filed a lawsuit 111111Justic John Trotter (Rer.), Trustee of the PG&E Fire Victim Trust v. Lewis Chew et al., Supreme Court of California for the County of San Francisco. https://www.cpmlegal.com/media/news/15076_2021-02-24%20Amend_Complaint__PGE_LIT_.pdf on February 24, 2021 arguing that ”The 2017 North Bay Fires Could Have Been Prevented If PG&E Had Implemented A De-Energization Program” and that ”PG&E Should Have Cut Off Power Because It Had Failed to Maintain Vegetation in Violation of Applicable Regulations.” While it took significant time for courts and CAL FIRE to describe their assessment of responsibilities, the evidence below suggests that option markets reacted quickly and provided investors with hedges against tail risk and rising, potentially stochastic, volatility.

Results are presented on Figure 2 for October 2, October 12, November 7 and November 30. The colors correspond to the traded maturities of the options. The maturity is in fraction of a year. The RND distribution suggests a clear asymmetry in investors’ risk neutral expectations. Hedges against tail risk appear as soon as October 2, and become more evident during the wildfire (figure (b)) and after the wildfire. In the aftermath of the wildfire, hedges for downside risk appear for both shorter-dated and for longer-dated options. The risk neutral distribution displays both negative skewness and negative kurtosis that become more pronounced over time.

3.5 Panel Data Impacts on the Risk Neutral Distribution: Identification Challenges

Estimating the causal impact of wildfires on listed firms’ out-of-the-money option prices, risk neutral probabilities, and implied volatility is challenging for at least four reasons. First, firms affected by wildfires may already have stock prices that are more likely to exhibit average skewness and kurtosis, asymmetric jumps and stochastic volatility, independently of wildfires. Second, wildfires may occur on days where the market is overall more likely to experience skewness and kurtosis in returns, jumps and stochastic volatility. Third, wildfires may coincide with other adverse or positive events for the firm. Fourth, option prices may exhibit arbitrage opportunities, including non-convexities.

The causal impact of wildfires on out-of-the-money option prices may also be heterogeneous across firms depending on their adaptation or expected ability to adapt to wildfire shocks. Firms that are expected to be resilient to wildfires may experience a smaller or no increase in the price of out-of-the-money puts. Firms that are expected to gain or be affected only shortly may experience increases in the price of out-of-the-money calls.

3.6 Panel Data Estimates: Wildfires and Arrow Debreu State Prices

We then turn to the estimation of the impact of wildfires on the risk neutral distribution or Arrow Debreu state prices. The approach described for PG&E is applied systematically to stocks of the treatment group, and, for computational reasons, to a random sample of the control group of the same size as the treatment group.

As in the previous sections, we wish to identify the causal impact of wildfires over and above the confounding impact of shocks specific to the day of wildfires and shocks specific to firms. The following regression estimates the impact of wildfires controlling for non-time-varying firm-level and day-specific confounders:

| (5) |

where is the risk neutral distribution obtained using the \citeasnounait2003nonparametric approach for firm on day at maturity for moneyness levels on a grid of equally-spaced moneynesses on the observed support. an indicator variable equal to 1 either when (a) firm is exposed to a wildfire on day , (b) firm has been exposed to a wildfire any time before , (c) firm has been exposed to its last recorded wildfire any time before . is the set of coefficients of interest. captures the baseline distribution. Standard errors are double-clustered as in \citeasnouncameron2011robust at the firm and date levels.

This specification is flexible as it allows an estimation of the impact of wildfire on each part of the risk neutral distribution separately. It is also demanding in terms of inference and statistical power when the grid of moneyness levels is fine-grained.

Another approach is to estimate a treatment effect at each moneyness level, weighing observations depending on how far (in a kernel weighting sense) from the moneyness level of interest. We are interested in measuring the treatment effect for moneyness level :

| (6) |

and each expectation can be approximated using local polynomial regression. This yields an estimator for the treatment effect based on a two-way fixed effects regression:

| (7) |

weighted by a smooth function of the distance between the moneyness of interest and the moneyness of the observation. This smooth function is a Gaussian kernel here. We estimate the treatment effects with different bandwidths of the kernel, to test for robustness. We also control for firm and date fixed effects as before, and cluster standard errors as before.

The sample has 630 tickers, 387 treated at least one day, 243 firms in the control group, 45.25 million observations across 539 days pre- and post-wildfires, a median maturity of 51 days. Appendix Figure A displays the evolution of treated firms over time.

Different supports of strikes across firms, time, and maturity could be a potential issue in the analysis. For instance, risk neutral probabilities may not be changing but rather be traded more often. Two additional regressions alleviate concerns about selection into the sample: 1) a regression focusing only on firms with moneyness levels that include at least the segment yields similar results, and 2) a selection regression of the probability of being quoted on the same set of covariates shows that options close to at the money are more likely to enter the sample that options deep out of the money, which is the opposite of what would be expected if tails were more likely to be traded.

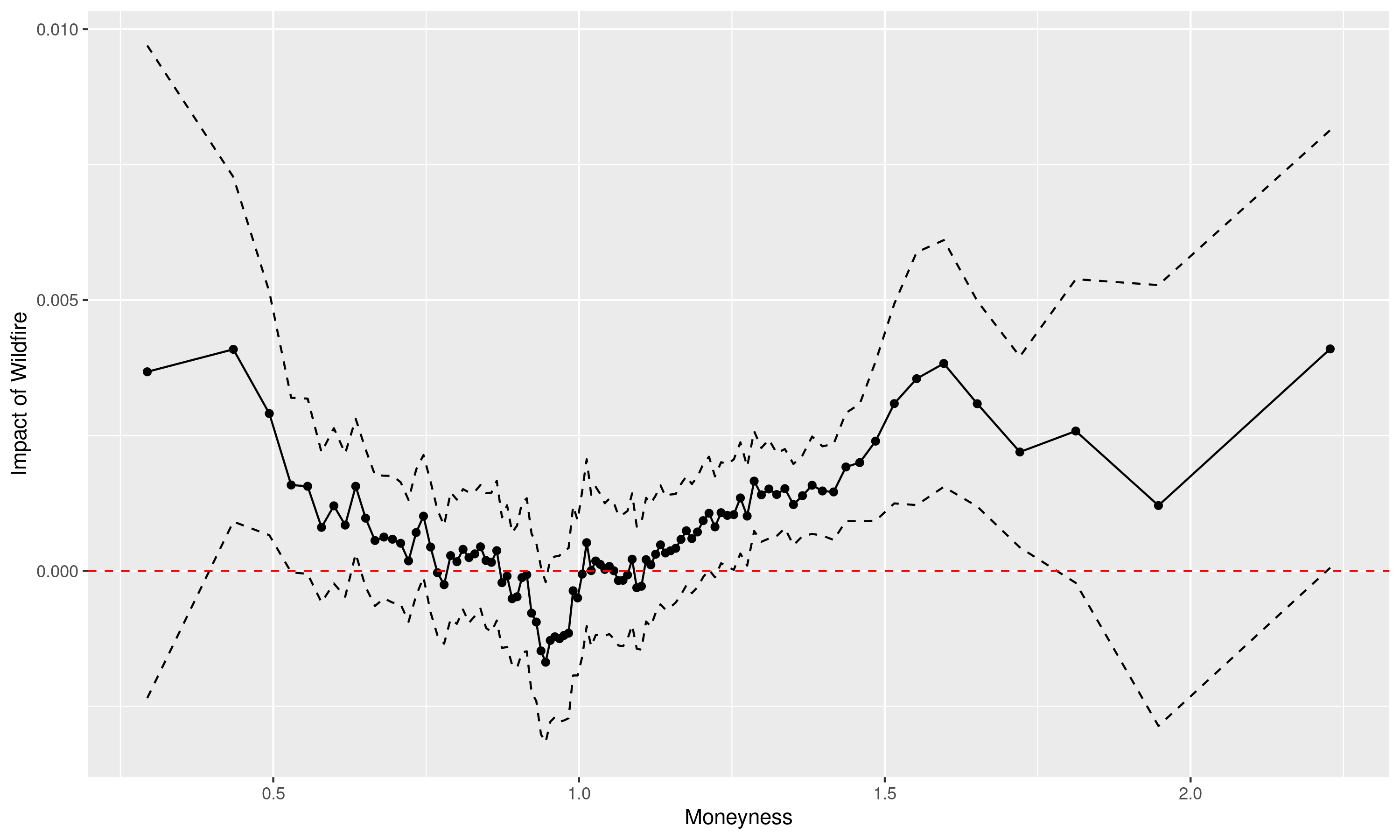

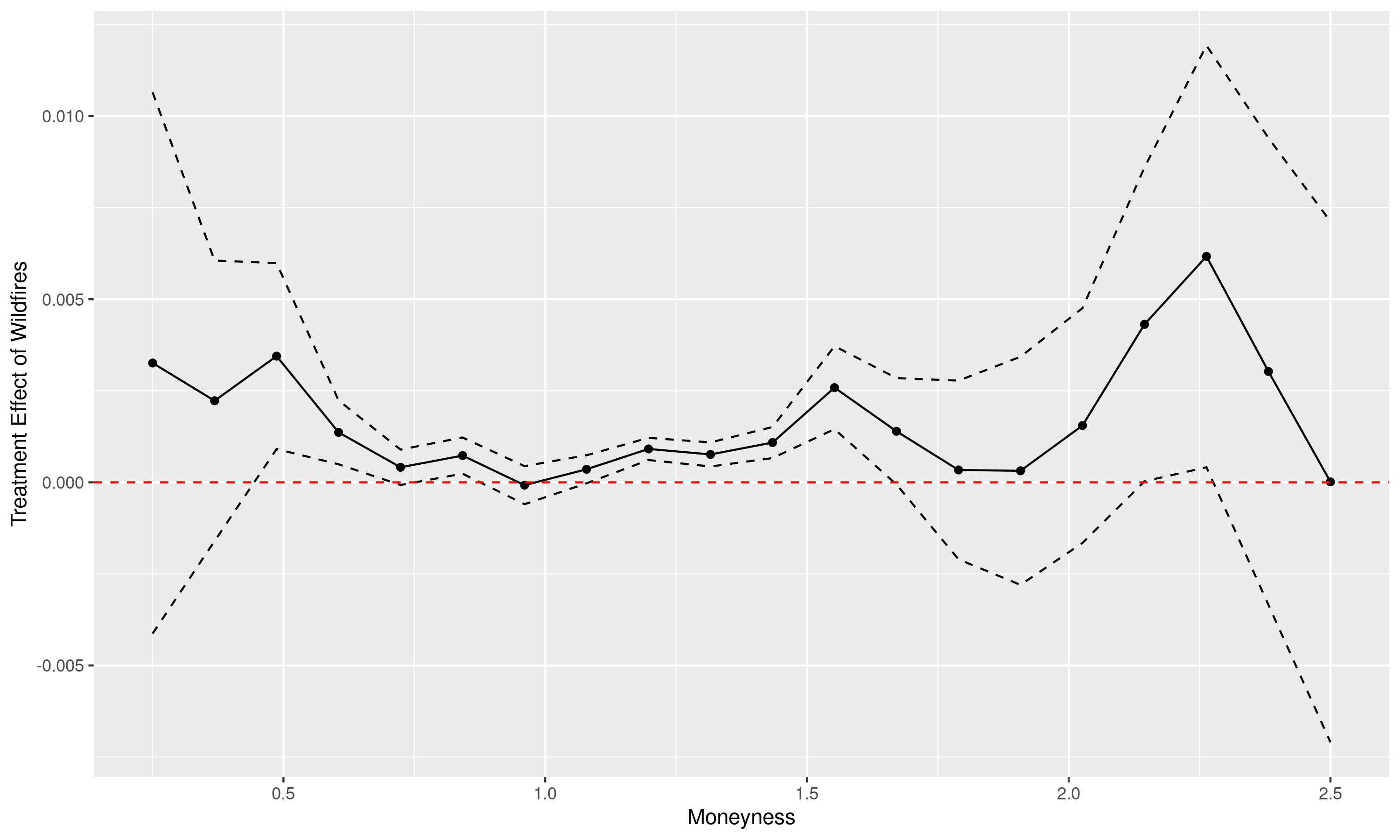

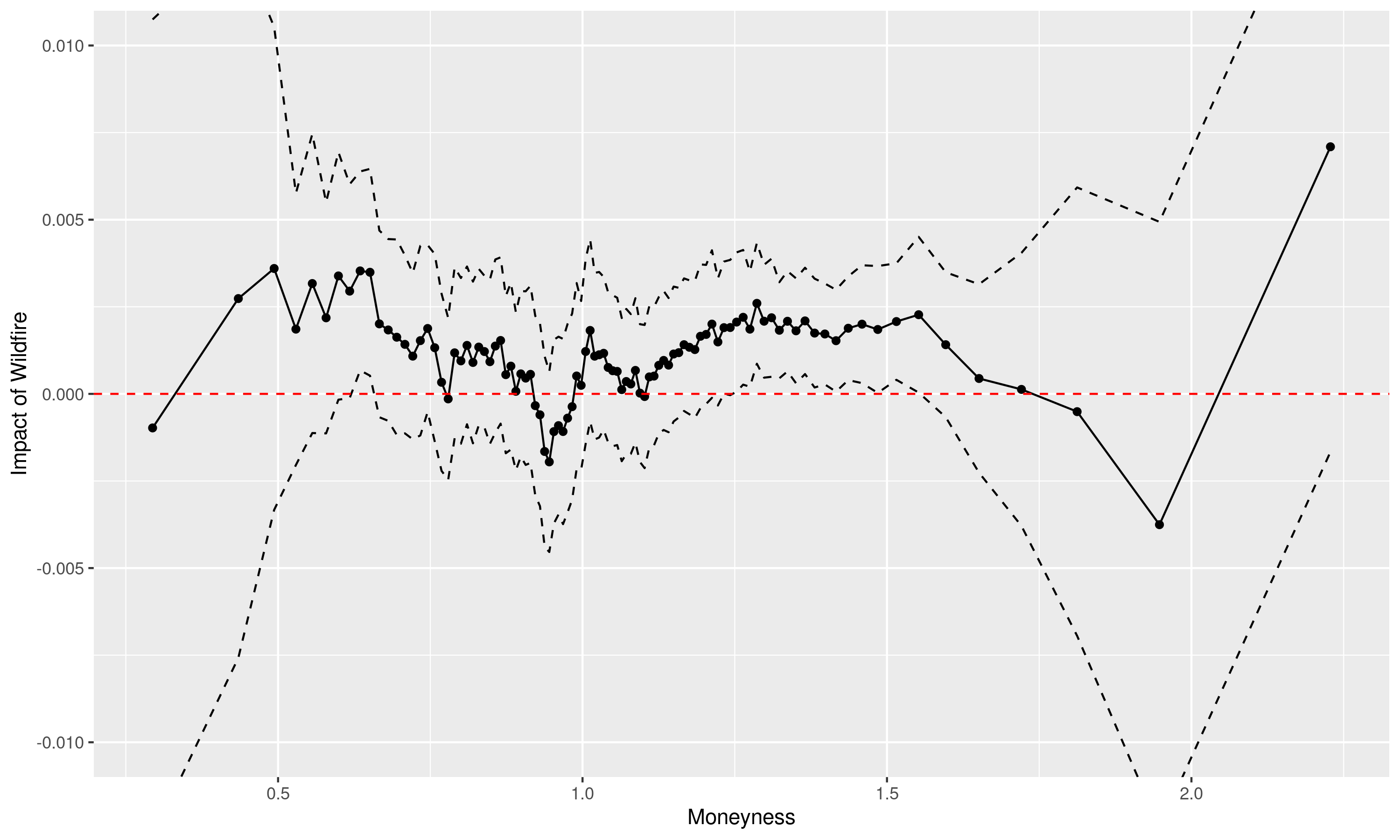

Results are presented on Figure 3. The figure and the table present estimates of the coefficients in specification (5). The segment of moneyness levels from 0.1 to 1.8 is divided into 30 quantiles of equal numbers of observations. The first column presents results for out-of-the-money puts, and the second column presents results for out-of-the-money calls.

Results are presented on Figure 3. Panel (a) presents the two-way fixed effect approach of specification (5) with 100 moneyness bins and double-clustered standard errors. Panels (b) and (c) present the local polynomial approach (7) with two different bandwidths. Both approaches suggest a positive impact of wildfires on the risk neutral probabilities at the tails.

On panel (a), in the upper tail, the impact is significant at 95% for moneyness levels above 1.208 and below 1.762. In the lower tail, the impact is significant for moneyness levels between 0.39 and 0.5132, as well as between 0.54 and 0.57, and 0.61 and 0.64. Thus the impact is more precisely estimated in the upper tail, suggesting expectations of an upside.

On panels (b) and (c), the standard errors of the local polynomial approach are less conservative. One benefit of panel (a) is that it accounts for the joint correlation of residuals across moneyness levels. Panels (b) and (c) are smoother as they use the entire panel for estimation of each treatment effect. They suggest a higher risk neutral probability at the tails, suggesting that wildfires lead to fat tails, or leptokurtic distributions.

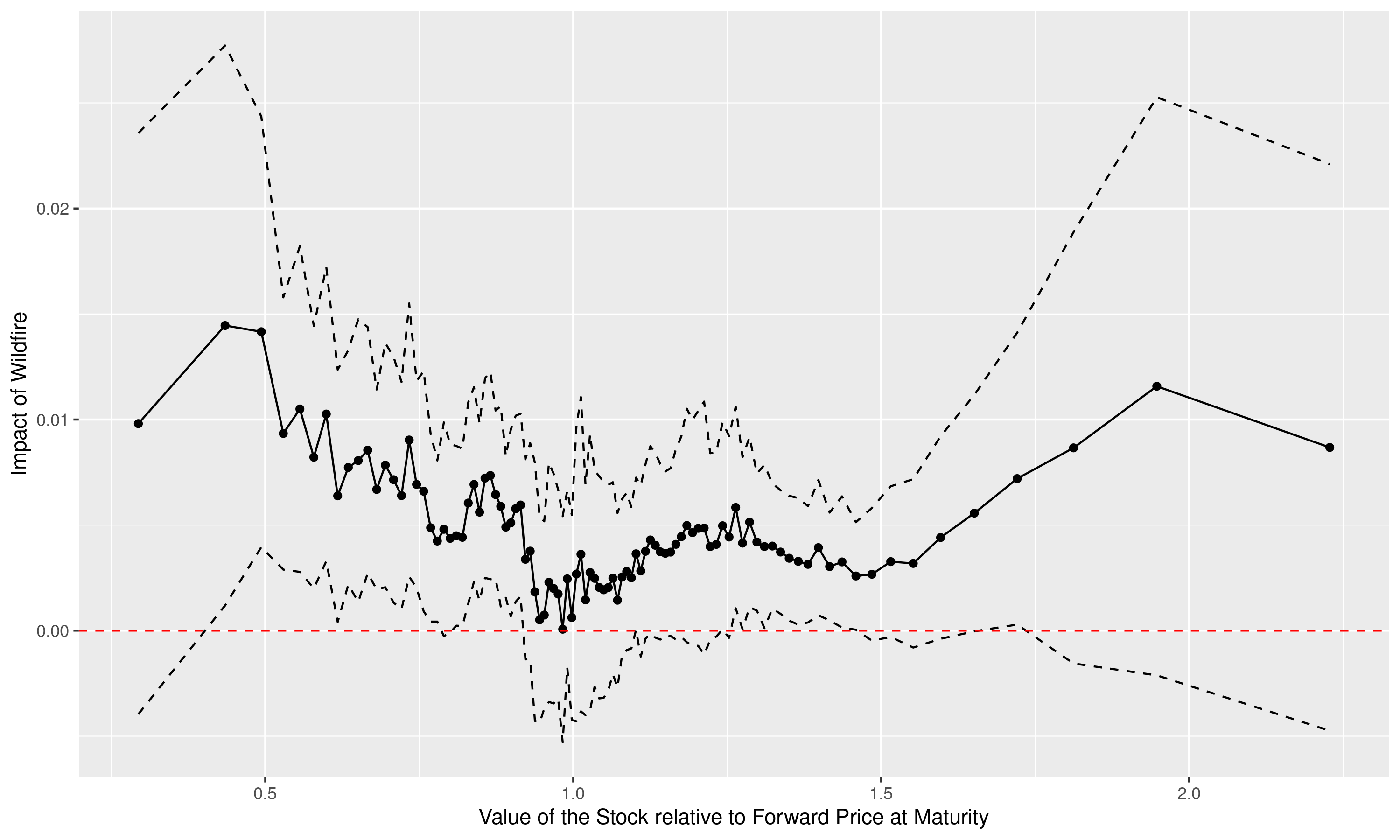

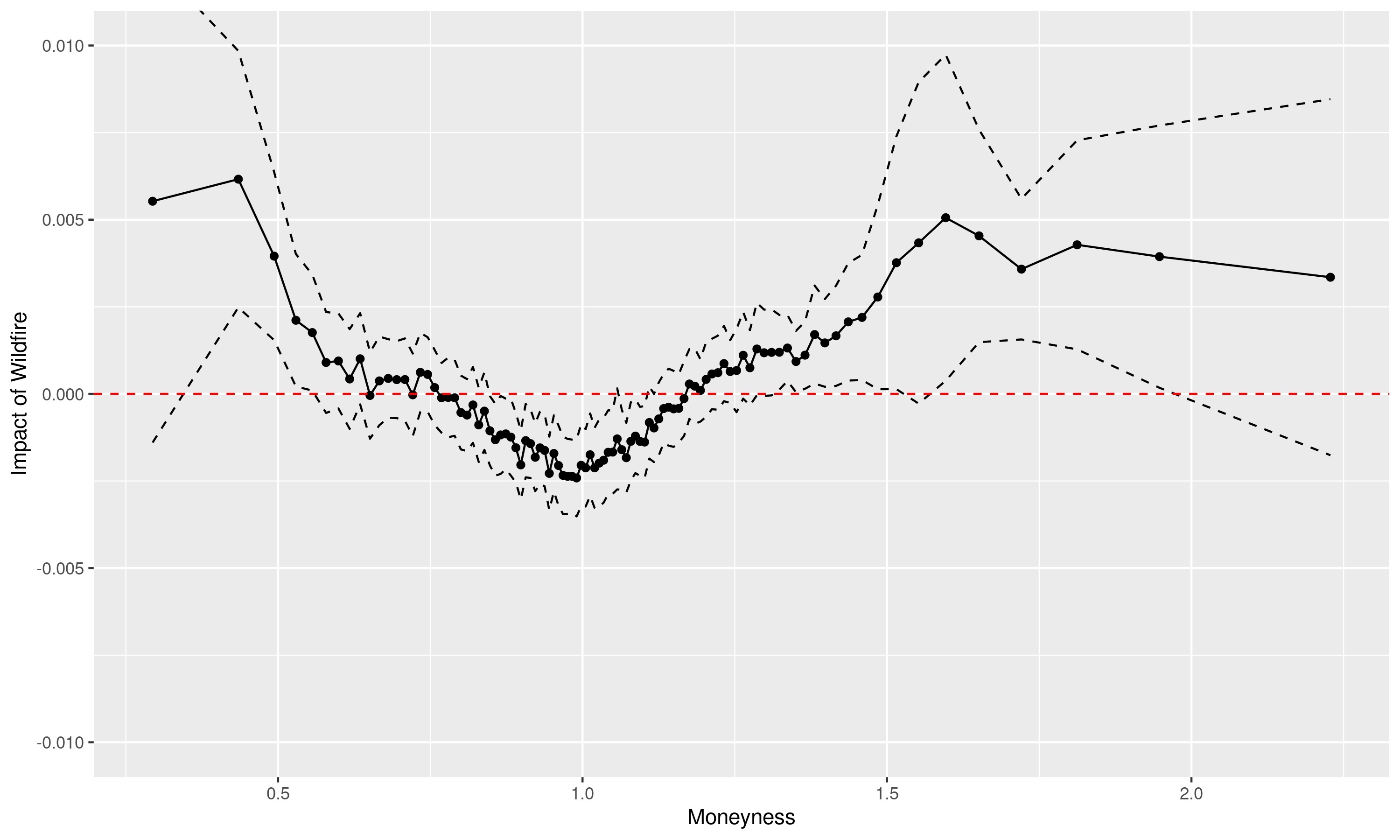

This is clearly visible on Figure 4, which estimates the treatment effect separately for each 1-digit NAICS industry. It keeps all observations of the control, but only retains those observations of the treatment group that belong to a specific 1-digit NAICS. Limiting the number of observations could lead to more imprecise estimates, but the results of panel (a), Figure 4, suggest a strongly significant impact on the risk neutral probability for low moneyness states in the trade, transportation and warehousing industry. Interestingly here the effect is asymmetric, with higher expectations of a downside than an upside. Effects are significant on both sides, but the point estimates are more than twice as large on the downside. Panel (b) shows symmetric impact in the NAICS 5 – Finance, Insurance, Real Estate, with a lower probability of almost at-the-money stock prices. This is also visible on Panel (c), for NAICS 7 – Entertainment, Recreation, Accomodation, Food Services, where there is a lower probability of being at the forward price at maturity.

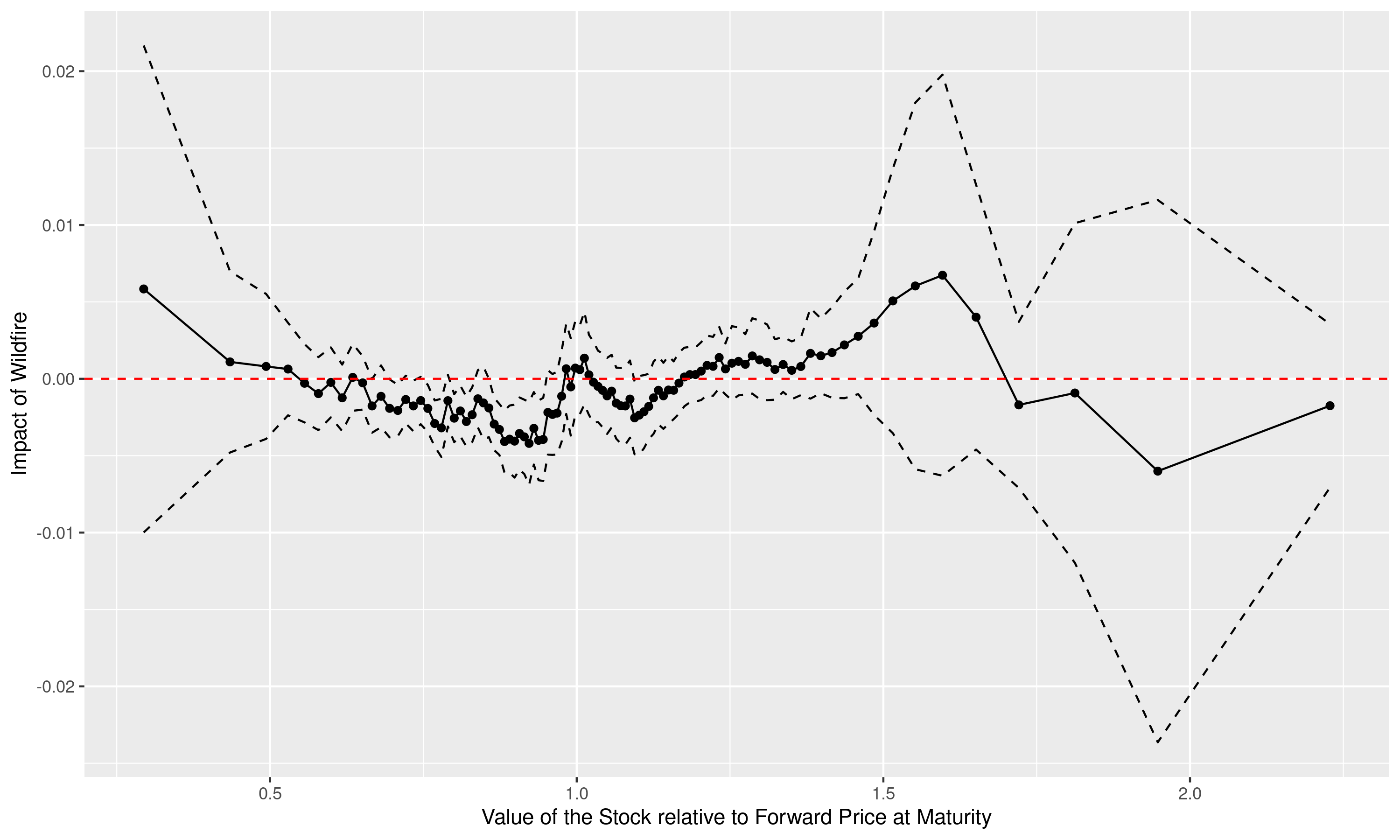

Figure 5 performs an analysis by splitting the sample in two, for maturity levels below the median of 51 days, and above the median. Results are significant for both samples, but the impact on the downside is mostly visible for higher maturity levels, suggesting that investors hedge on the downside.

Overall, in a specification saturated with firm moneyness and day fixed effects and conservative double-clustered standard errors with risk neutral probabilities obtained using \citeasnounbreeden1978prices, results suggest that wildfires have significant impacts on the risk neutral probability distribution at the tails. While the effects seem to price the upside more precisely than the downside on average for the entire sample, the market hedges against the downside in the trade, transportation, warehousing industry.

4 Natural Disaster Risk and the Volatility Smile

The volatility is a deviation from the standard Black and Scholes approach whose first appearance in the aftermath of the 1987 Black Monday is well-documented [ait1998nonparametric, derman2016volatility]. \citeasnounbirru2012anatomy suggests that such implied volatility smile became more pronounced during the 2008 crisis. \citeasnounyan2011jump suggests that the slope of the smile is a significant predictor of jump risk and future stock returns.

Whether the physical risk exposure to wildfires leads to a steepening of such smile is an empirical question.

This section provides evidence of a steepening volatility smile and skew for firms exposed to wildfires by a systematic panel data approach on the daily implied volatility surface of listed equity options between 2000 and 2018. Estimating the impact of wildfires has an advantage over the use of the risk neutral distribution, as it requires less processing and relies solely on the binomial tree approach readily available in OptionMetrics [cox1979option]. The smile or skew focuses on the tails, which provides information on the pricing of large deviations, complementary to the volatility information at the money [kruttli2021pricing].

4.1 The Risk Neutral Distribution and the Implied Volatility Smile

We model below the relationship between the implied volatility surface and the risk neutral probability distribution.

black1973pricing approach indeed parameterizes underlying stock price dynamics using a single parameter, the volatility , when this stock follows a diffusion process, where the risk-neutral trend of the stock is the risk-free rate, and is a Brownian motion. In this world, option prices at different strikes and maturities are redundant, as the price of one option, typically the at-the-money (ATM) call option, provides the price of options of all maturities and strikes.

The implied volatility is the volatility that makes the observed price at maturity and strike consistent with the Black and Scholes price. While stocks do not follow geometric Brownian motions, the market price of an option is typically quoted through its Black-Scholes implied volatility. If is the observed option price, and is the Black and Scholes price of an option with volatility , the implied volatility is:

| (8) |

where is the risk-free rate. is independent of the strike and maturity if the stock follows a geometric Brownian motion.

A more pronounced volatility smile is typically associated with a corresponding shift in the underlying risk-neutral distribution, or Arrow Debreu state prices [bakshi2003stock]. However \citeasnounbakshi2003stock documents that the moments of the risk neutral distribution are typically different from the distribution of implied volatilities. This is visible by noticing that the first and second derivatives of the implied volatility with respect to the strike is a weighted average of the risk neutral cdf and the risk neutral pdf, with non-linear weights. In general, applying the chain rule:

| (9) |

where the implied volatility function is a deterministic function of the strike and the price of the call, the inverse of the Black and Scholes pricing function w.r.t. to the volatility.

Thus the slope in implied volatility along the range of out-of-the-money strikes is related to a shift in the cumulative distribution function, weighted by and with a constant . An increasing slope of the implied volatility surface at the tails is related higher values of the cumulative distribution function.121212The convexity of the implied volatility smile is weighted average of the cdf and the pdf. (10) Thus, in general the relationship between the implied volatility surface and the risk neutral probability distribution is non-linear.

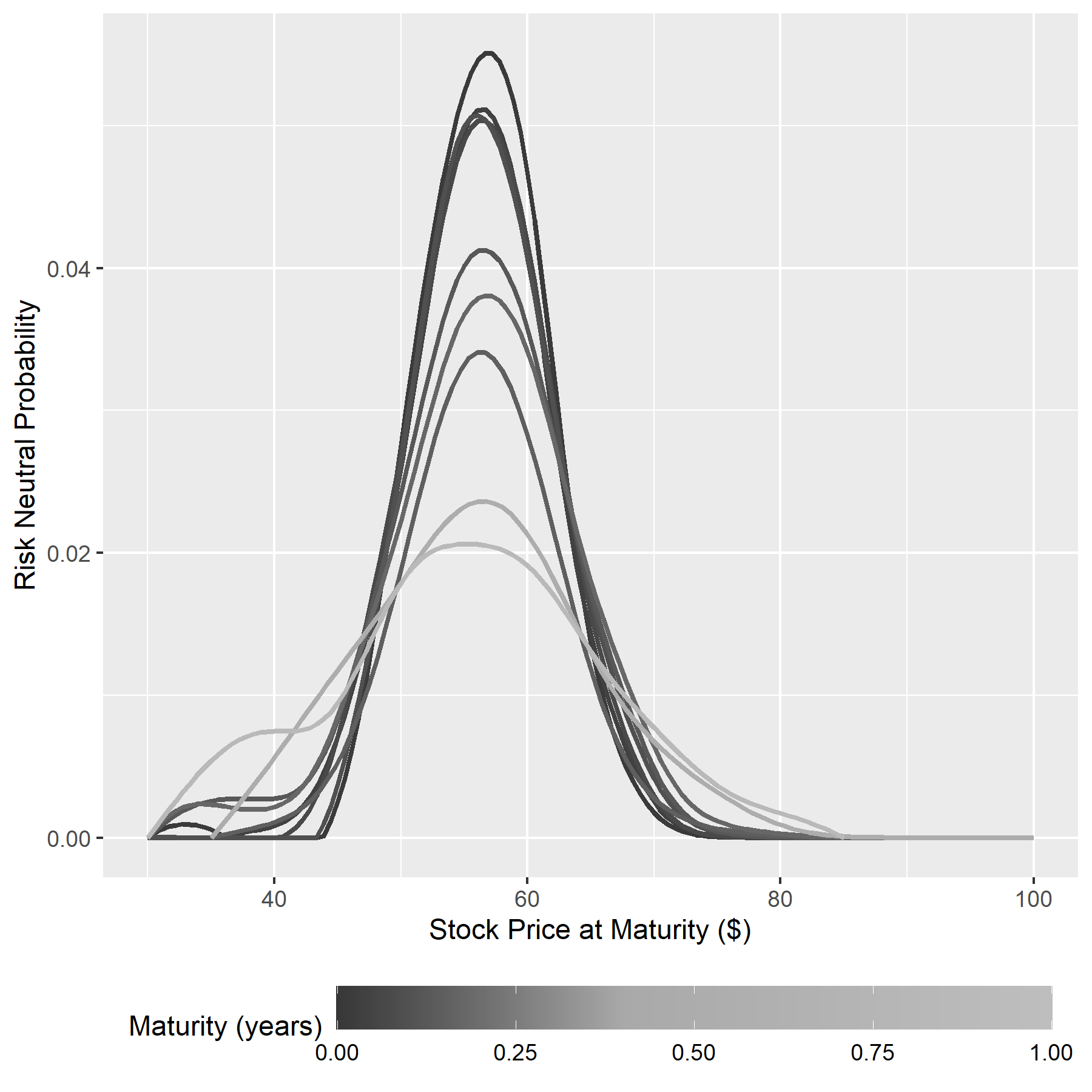

4.2 PG&E’s Volatility Smile During the October 2017 Wildfires

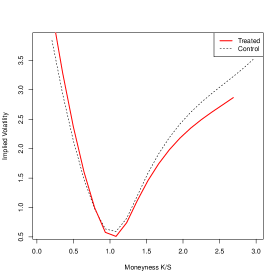

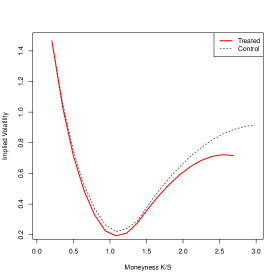

Figure 6 presents the evolution of the implied volatility smile for the PG&E stock (ticker: PCG) during the October 2017 wildfires. Maturity is in days, and is the ratio of the strike over the forward price. Axis scales are constant across figures. The figures consider out-of-the-money calls and puts only. Hence, when , the data is that of calls, while is the implied volatility data for puts.

The wildfires started on the evening of 8 October 2017, and lasted until October 31, 2017. Figures 1(a) and 1(b) are thus estimated prior to the beginning of the wildfires; Figure 1(c) is the set of implied volatilities during the wildfire and 1(d) is drawn after the wildfires. The graphs suggest two phenomena. First, the trading and pricing of shorted-dated options. On September 22, 2017, options with maturities of 28, 56, 84, and 175 are quoted. On October 12, options with maturities of 8, 36, 64, 155 days are traded. On November 7, there are 9 maturities traded: 3, 10, 17, 24, 31, 38, 45, 129, 220 days. This thicker market is also visible in the number of traded strikes: from 14 strikes until October 12, to 46 smiles on November 7. The minimum traded strike also decreases, from $35 to $30. The second phenomenon is the increase in implied volatilities that is larger for out-of-the-money options than for at-the-money options: on September 22, the ATM implied volatility ranges between 0.13 and 0.148 from short-dated to long-dated options. The smile is already visible on September 22, with implied volatilities for deep out of the money ranging between 0.96 and 0.42. The smile becomes substantially more pronounced during the wildfires, with deep OTM IVs for puts ranging between 2.19 (short-dated) and 0.45, while ATM calls and puts have IVs ranging between 0.28 and 0.19. This smile becomes significantly more pronounced in November. Hence, while ATM implied volatilities increase during the wildfire, most of the volatility is at the tails, for deep out-of-the-money calls and puts.

While the PG&E smile suggests that information is contained in deep out of the money options, it also suggests controlling for sources of endogeneity, such as pre-existing trends in deep OTM implied volatility and for market-level volatility. These endogeneity concerns and the identification strategy conditioning for unobservables are addressed in Section 3.5.

4.3 The Out-of-the-Money Volatility Smile: Linear Fixed Effect Panel Regression

A ‘model-free’ linear specification addresses the first three identification concerns. The effect of exposure to a wildfire on the volatility surface by strike and maturity is estimated controlling for firm-specific and time-specific unobservables with a specification similar to \citeasnoundumas1998implied.

| (11) | |||||

A separate regression is estimated for calls and for puts. is the implied volatility of option on day obtained using binomial trees. It is regressed on the moneyness of the option , i.e the ratio of the strike over the forward price. The coefficient on this first covariate captures the volatility skew. is the square root of maturity. measures a phenomenon observed in the case of PG&E on Figure 6: it measures how the volatility skew depends on the maturity of the option. is an indicator variable for the treatment status.

The coefficients of interests are , , and . measures the impact of wildfires on volatility skew. measures the impact of the wildfire on the term structure of implied volatilities. captures the impact of wildfires on the variation in the skew along maturities.

captures non-time-varying firm-specific differences in implied volatilities. controls for increases or declines in implied volatility specific to each day. Standard errors are double-clustered at the firm and date levels, as in \citeasnouncameron2011robust.

A firm is treated if either 10% of its establishments, its employment or its sales are in a ZIP code affected by a wildfire on day . Table 3, panels (a) and (b) presents industry-level statistics on the share of treated firm date observations. 74.4% of 6-digit NAICS industries have at least one treated firm date observation, the median industry has 1.2% of treated observations, and the industry with the largest share has 8% of treated observations. The top 3 is Home Health Care Services, Ammunition Manufacturing, Petroleum and Petroleum Productions Merchant Wholesalers. These panels suggest that the share of treated firm date observations is quite homogeneous across industries, and that this paper’s results are therefore unlikely to be due to a single or a few industries.

4.4 The Out-of-the-Money Volatility Smile: Non-Parametric Analysis

While the linear panel fixed effect provides a model-free set of estimators that are arguably independent of the specific parametric assumptions of option pricing models, the functional form of the implied volatility is better captured by a non-parametric approach relying on flexible function forms. Option pricing that feature stochastic volatility [heston1993closed], jumps \citeasnounkou2004option, or combine both stochastic volatility and jumps \citeasnounduffie2000transform predict more general functional forms for the implied volatility. Two models are identified in Section 7.

An alternative approach regresses the implied volatility of the set of options on a flexible functional form that differs between the control and the treatment groups.

| (12) |

where is a two-dimensional function of moneyness and maturity for the control group. is the impact of the treatment on the functional form. As before, the regression includes firm and day fixed effects. These functional forms are estimated using a Frisch-Waugh-Lovell approach by first orthogonalizing the implied volatilities with respect to the firm and day fixed effects. This yields . The functional forms and are then estimated using a local polynomial regression [cleveland1979robust] of order 2 of on the surface of .

4.5 Linear Panel Data Results

Estimates of the impact of a wildfire on the volatility skew are presented in Table 2. The upper panel is for puts, and the lower panel for calls. Column (1) is an OLS regression with double-clustered standard errors. Column (2) includes firm fixed effects. Column (3) includes day fixed effects. Column (4) is a two-way fixed effect regression with double-clustered standard errors.

Baseline coefficients suggest a volatility skew for both puts () and for calls (), inconsistent with the Black and Scholes geometric Brownian motion. Coefficients also suggest that implied volatility is a decreasing function of the square root of maturity, for both puts and calls (). The skew is less pronounced for longer-dated options () in the control group.

In the treatment group, results suggest that the volatility skew is significantly steeper for both puts and for calls. In the regression including both fixed effects, the coefficient is significant at 5% for both puts and calls. For puts, its magnitude is approximately of the baseline skew. For calls, its magnitude is times the magnitude of the baseline skew. For calls, the effect is statistically significant in columns (1)–(3). Thus the impact on puts is more precisely estimated than on calls, even though the magnitude of the impact on calls is larger. This suggests an asymmetry and a heterogeneity in the impact of wildfires: wildfires may lead to significant increases in the prices of out-of-the-money puts, which insure investors against downside risk. And more heterogeneity in the impact on the price of out-of-the-money calls, which allow investor to sell the upside.

Table 3, panel (c), presents results estimated separately for each 3-digit NAICS industry. For puts, results suggest that the steepening of the volatility smile of out-of-the-money puts is present in a majority of industries (66%), and that 57% of industries exhibit a steepening significant at 99%. For calls, 26% of industries exhibit a steepening of the volatility smile, suggesting an asymmetry between downward risk (observable with puts) and upward risk (observable with calls). For calls, 24.3% of industries exhibit an effect significant at 99%.

4.6 Non-Parametric Treatment Effect Along the Volatility Surface

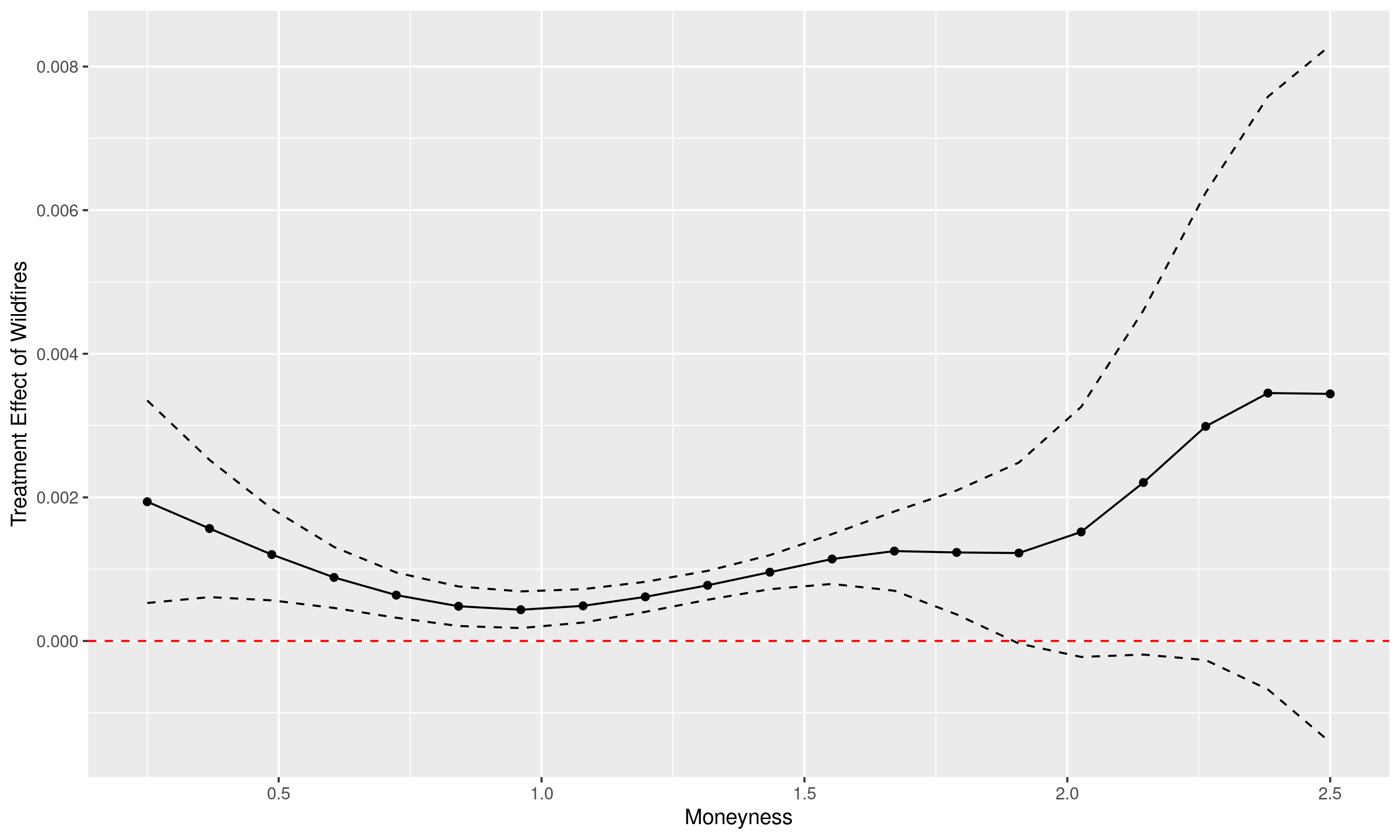

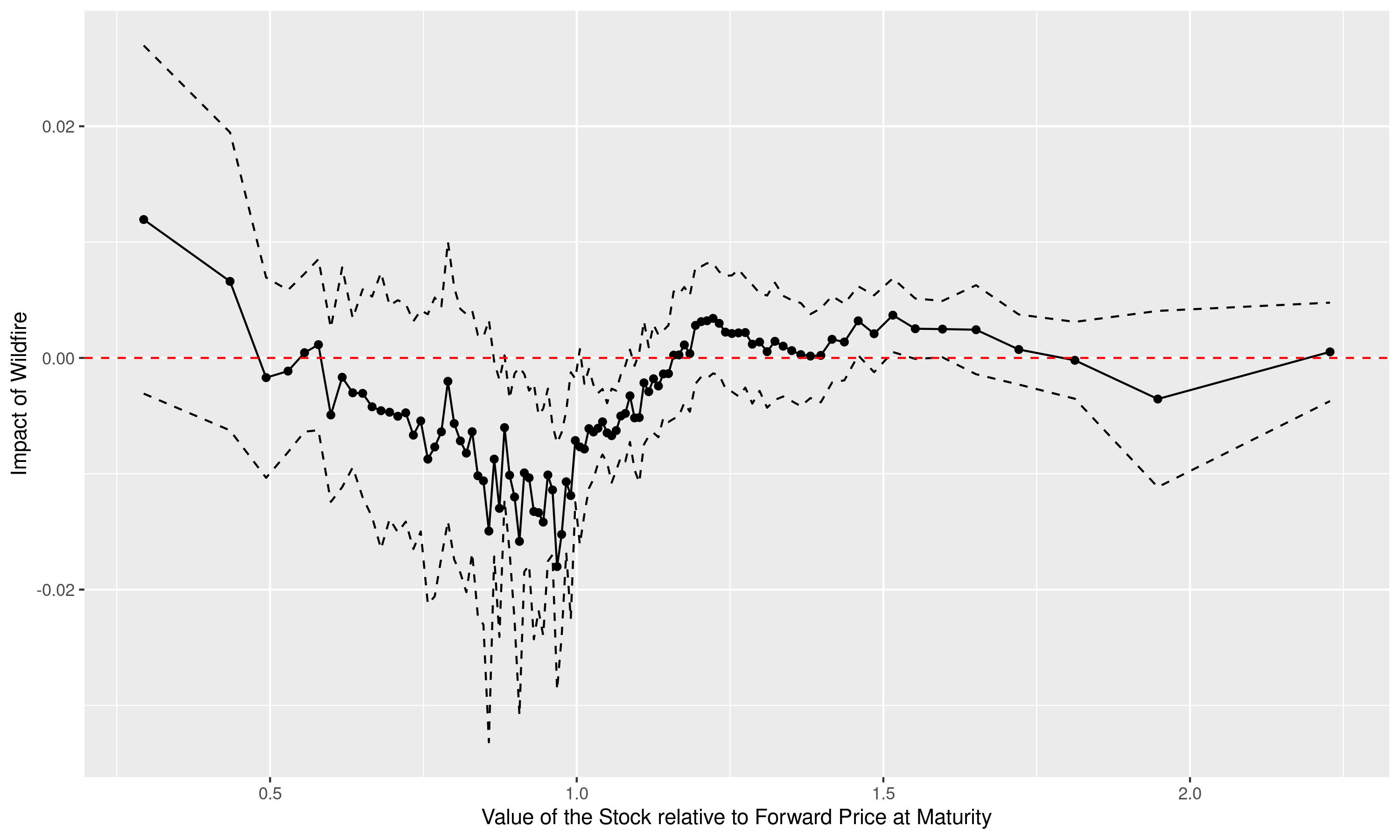

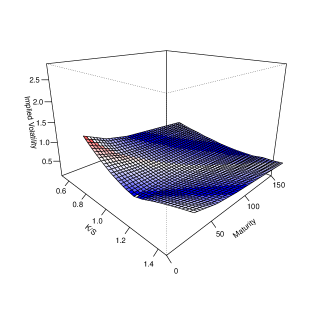

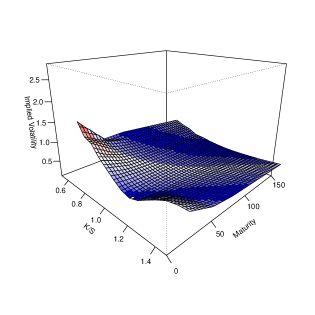

The non-parametric enables an estimation of the treatment effect that is specific to each strike and maturity. As such, it also reassures us that the linear specification used previously is not driving results. The non-parametric results are presented on Figure 7. Figure (a) presents the shape of the IV surface in the control group, while (b) presents the shape of the treatment effect , as defined in specification (12). Figures (c) and (d) present cross sections at two different maturities. This analysis is performed only on calls, both in-the-money and out-of-the-money.

Figure (a) suggests that the average IV surface in the control displays a smile: as documented in past literature, option IVs are higher at low and high moneyness levels, and the smile is steeper for shorter-dated options. Figure (b) suggests that the IV of wildfire-exposed stocks is higher for moneyness less than 1, and higher for moneyness levels higher than 1. This is consistent with investors pricing in a higher risk-neutral probability of downward shocks and a lower probability of an upward shock. Figures (c) and (d) show that the pricing of the downward shock happens for short-dated options. For longer maturities, investors are less likely to price upward shocks, but there is no difference in the pricing of downward shocks.

4.7 Long-Run: Linear Panel Data Approach

The previous approach focuses on effects on the days of the wildfire. This section estimates the permanent impact of wildfire exposure on the skews of calls and puts. Wildfires may have a permanent impact on puts and calls if wildfires affect expected stock price dynamics or the dividend flow.

To do so, we estimate two sets of regressions, where the Treatment variable is replaced by either an ‘After the first wildfire’ indicator variable, or an ‘After the last wildfire’ indicator variables. Other covariates are kept as in the baseline regression.

The results are presented on Table 4. All fours specifications include day and firm fixed effects, and double-cluster standard errors by firm and by day. Columns (1) and (3) are for puts, and columns (3) and (4) are for calls. Columns (1) and (2) are for the permanent impact after the first wildfire, and columns (3) and (4) for the permanent impact after the last wildfire. The results suggest that the permanent effects are on calls. This is consistent with the previous non-parametric evidence that suggested that long-dated options priced a lower probability of upward stock price movements. This is consistent with this evidence, that call options respond permanently to wildfire exposure. The impact on the slope of calls’ implied volatility is after the first wildfire: a call with strike at 1.5 times the forward price of the stock has a lower implied volatility in the treatment group than in the control group. The impact () is similar after the last wildfire: a call with strike at 1.5 times the forward price of the stock has a lower implied volatility in the treatment group than in the control group. The impact is stronger for short-dated options than for long-dated options: there is no permanent impact on call options with a 136-day maturity () after the first wildfire, and with a 144-day maturity after the last wildfire.

5 Wildfires and Investors’ Marginal Utility

A key question is whether the results presented in the previous section are small, diversifiable shocks on a single stock in the market portfolio or whether they are correlated with investors’ wealth and its marginal utility. This would occur if, for instance, investors hold higher shares of wildfire-exposed stocks than what the market portfolio would suggest.

By comparing the risk neutral distribution to the physical distribution of wildfire-exposed stock returns, we can identify investors’ marginal utility at each level of the wildfire-exposed stock. This allows an estimation of the correlation between the investors’ marginal utility of wealth and the value of a wildfire stock. A simple proposition, derived from a Merton portfolio model with a wildfire stock and the index, provides a relationship between the Arrow Pratt risk aversion with respect to a wildfire-exposed stock and the risk aversion with respect to wealth.

Results suggest a risk aversion w.r.t. wealth that is arguably inconsistent with a representative agent investing in the market portfolio. Multiple hypothesis are consistent with this result. Wildfire stocks could be held by heterogeneous investors who hold significantly more shares exposed to natural disaster risk than what the market portfolio suggests. Investors may be hedging against rare tail risk, that is not observed in realized returns, and thus not captured in the physical distribution measured in this paper. This latter explanation is consistent with the option hedging on the index.

5.1 Pricing Kernel and Investors’ Marginal Utility of Wealth

This section (i) estimates state prices and the pricing kernel for all wildfire-exposed stocks, (ii) shows that the relationship between the state prices of wildfire-exposed stocks and the value of such stocks depends on the weight of wildfire-exposed stocks in the portfolio, the stocks’ beta, and investors’ risk aversion; thus (iii) we provide an empirical method to estimate a stock-specific Arrow-Pratt aversion and a statistical test of this null hypothesis of independence.

As a testable benchmark, consider a continuous-time investment problem over the time period where the investor maximizes the expected utility of terminal wealth. At each time , the investor can invest a share in the potentially wildfire-exposed stock and a share of wealth in a diversified portfolio with price :

| (13) | |||||

| (14) |

where are two independent Brownian motions, and (resp. ) are functions from to (resp., to ). The portfolio follows a diffusion process whose trend and volatility are general functional forms that depend on both the price and time. The wildfire exposed stock follows a similar diffusion process with general functional forms but with a beta on the portfolio .131313We introduce later jumps where the magnitude of the jump and the intensity depend on the stock price and time.

The investor picks and to maximize the utility of terminal wealth:

| (15) | |||||

If is the investor’s value function, the Euler equation becomes:

| (16) |

where is the pricing kernel, a random variable at time that depends both on the value of the diversified portfolio and the value of the wildfire-exposed stock.

The risk neutral density of the wildfire stock is related to the physical density by the expectation of the pricing kernel condition on the value of the wildfire stock:

| (17) |

This has multiple implications. First, the ratio of the risk neutral distribution to the physical density identifies the stochastic discount factor . The risk neutral distribution for wildfire-exposed stocks was estimated in the previous section. Second, the pricing kernel is the marginal utility of wealth, up to a multiplicative constant. As marginal utility is decreasing in wealth, the estimated should be decreasing in wealth.141414An extensive literature describes and explains apparent paradoxes in the non-monotonic shape of the pricing kernel. See for instance \citeasnounbeare2016empirical, \citeasnounlinn2018pricing, \citeasnouncuesdeanu2018pricing. Third, the beta of the wildfire-exposed stock matters, as the expectation of the pricing kernel is taken conditional on the wildfire-exposed stock, and thus depends on the joint distribution of the value diversified portfolio and the value of the wildfire-exposed stock. Intuitively, if the beta is large, declines in are correlated with declines in , and thus a high Arrow Debreu state price for low values of may be an indication of the .151515The panel data regressions of Sections 4 (Wildfires and the Volatility Smile) and 3 control for a day fixed effect, and thus for the value of the index.

Since the pricing kernel is equal to the marginal utility up to a multiplicative constant, its relationship with wealth identifies risk aversion. \citeasnounrosenberg2002empirical suggests the Arrow-Pratt measure [arrow1964role, pratt1964risk]. 161616An important alternative is to use absolute risk aversion, as in \citeasnounjackwerth2000recovering. Both approaches yield a similar set of stylized facts.

| (18) |

where is the derivative of the state price w.r.t. the value of the wildfire-exposed stock. When terminal utility is CRRA, this is equal to the constant relative risk aversion.

Here, as suggested by \citeasnounrosenberg2002empirical, we can obtain the Arrow-Pratt measure projected on to the value of a wildfire-exposed stock to estimate the sensitivity of investors’ marginal utility of wealth to the value of such stock.

| (19) |

which is the elasticity of the pricing kernel w.r.t. the value of the wildfire-exposed stock. This quantity can be estimated for all of this paper’s treated firms following the method outlined in the next subsections.

(19) can be estimated and it provides key information on the sensitivity of wealth to changes in wildfire-exposed stocks and on investors’ risk aversion.

Proposition 1.

Sensitivity of State Prices with Respect to the Wildfire-Exposed Stock Assume the stocks’ parameters are non-time-varying, the investor has CRRA preferences where is risk aversion with respect to wealth. Then a closed form ties the sensitivity of state prices w.r.t. to the wildfire stock at maturity to the investor’s risk aversion with respect to wealth and the share of the wealth invested in the wildfire-exposed stock:

| (20) |

where is the share of wealth invested in the diversified portfolio; is the correlation between the returns on the wildfire stock and the diversified portfolio, ; and the volatilities of the stock and the wildfire-exposed stock respectively.

The proof is presented in Appendix Section 9. The intuition of the proof of Proposition 1 is simple. The proof first expresses the marginal utility of terminal wealth as a function of both and . is a joint bivariate normal distribution whose correlation depends on the beta of the wildfire stock and the variances. Since depends on the conditional expectation of a bivariate normal, the classic bivariate normal expectation formula applies, conditional on the value of , which gives the coefficient . Details are provided on page 9.

Monte Carlo simulations with more complex stochastic processes for suggest the result holds for Brownian motions with jumps and stochastic volatility.

5.2 Estimating and Forecasting the Physical Distribution of

Estimation of a Firm-Specific GARCH-Wildfire Process

The pricing kernel w.r.t. to the wildfire-exposed stock price is the ratio of the risk neutral and the physical distribution. First, we use the previous section’s daily and stock-specific risk neutral distributions for each stock of a treated firm. Second, the so-called physical distribution of the future level of the stock price is estimated using a time series GARCH-Wildfire model that accounts for jumps in returns and in volatility caused by wildfires. Such physical distribution reflects investors’ beliefs and thus our approach requires using different assumptions for investors’ expectations: myopic (based on the previous history of returns), foresight (based on the post-wildfire series of returns), and stationary (assuming that the GARCH model has similar autoregressive parameters before and after the wildfire).

The GARCH-Wildfire model allows returns to have time-varying volatility and wildfire jumps:

| (21) |

where notations are similar to the important \citeasnounbarone2008garch, with a number of additions.

First, when a wildfire hit the firm either in the current period or in previous periods (in this case we include lags ). Wildfires cause jumps in the stock’s return, denoted and in volatility, denoted .

Second, the model accounts for the beta of the stock w.r.t. to the index, which is potentially correlated with the occurence of the wildfire. This controls for shifts in the index return in the estimation of . The market return is modeled as with an autoregressive structure for the variance .

Third, the model allows the volatility of the stock to depend on market volatility.

When indexed by , parameters are estimated separatelty for each stock.

Forward-Looking Physical Distribution of Wildfire-Exposed Stocks at Time

The physical distribution of a wildfire-exposed stock at given the history of observations of the stock and the index at is modelled as the distribution of the GARCH-Wildfire stock with estimated parameters conditional on the initial volatility and prior wildfire exposure. The physical distribution of market returns is also estimated using the parameters of the estimated GARCH process. Forward-looking wildfire probabilities are estimated using the history of wildfire probabilities for each firm. We discuss further in the paper how the risk neutral distribution can be used to identify the forward-looking wildfire probability.

5.3 Panel Data Estimation of Firm-Level Arrow-Pratt Risk Aversions

When investors have CRRA preferences, there is a linear relationship between the log risk neutral distribution for stock , the log of the physical distribution and the risk free return, on the log of the forward stock price. For each stock ,

| (22) |

Hence firm-specific Arrow-Pratt risk aversion is obtained by regressing the left-hand side on the right-hand side for a grid of forward prices , for equally spaced forward prices ranging from the lower bound of the support of option strikes to the upper bound of such support:

| (23) |

where we can control for firm, date, and maturity fixed effects. For maturity we control for 10 bins of maturities, and the choice of the number of maturity bins does not affect the estimation. We restrict the estimation to the range of forward prices on the support of both the risk neutral and physical distributions as Euler condition 17 implies that their supports should coincide. is the risk-free rate, obtained by calibrating the LIBOR time series at the option’s maturity using the Intercontinental Exchange (ICE) time series. Ordinary least squares regression 23 performed for each firm separately provides a firm-specific risk aversion index and an associated standard error .

In regression 23, the risk neutral distribution, the physical distribution and the risk-free rate are estimates rather than the true values. \citeasnounhausman2001mismeasured suggests that such left-hand side measurement error leads to larger standard errors, smaller statistics, and more imprecise estimators of , but does not affect the unbiased nature of the OLS estimator of .

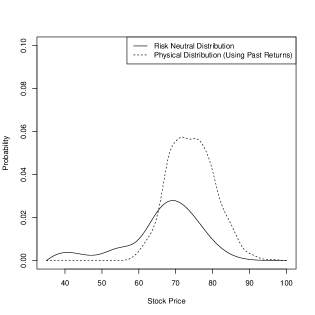

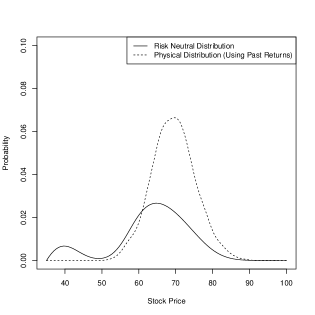

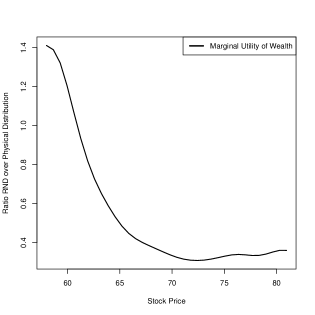

5.4 Empirical Results: PG&E

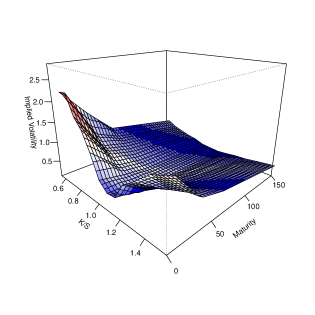

Figure 8 gives a visual intuition of the test and its results for PG&E. It presents the risk neutral distribution estimated using option prices and the physical distribution estimated using past returns. The lower panels present the ratio of the two probability distributions. The ratio is taken for stock prices in the support of the physical distribution of future prices. As before, the RND is obtained using arbitrage-free prices and a local polynomial regression using the \citeasnounbreeden1978prices butterfly spread method.

The upper panels of Figure 8 suggest that the risk neutral distribution is above the physical distribution for low values of the stock, consistent with higher values of Arrow-Debreu state-contingent assets for lower values of the stock. Similarly, the panels suggest that, for higher stock prices, the physical probabilities are higher the risk neutral probabilities, consistent with lower values of Arrow-Debreu state-contingent prices for higher wildfire-exposed stock prices.

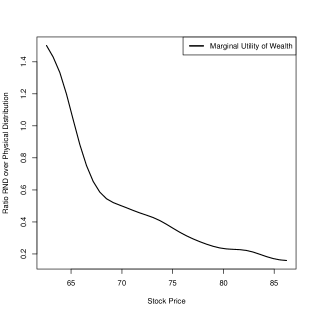

The lower panels of Figure 8 take the ratio of the two distributions, to present an estimate of the pricing kernel. Up to a constant equal to the risk-free discount factor, this is the marginal utility of the investor in model (15) if the physical distribution is correctly specified. An extant literature estimates this pricing kernel for the S&P500 index [chernov2000study, figlewski2009estimating, birru2012anatomy, figlewski2018risk, reinke2020risk] and highlights the potential pricing kernel puzzles that emerge. We address this systematically for all of the stocks in our sample in the next section.

An estimation of the elasticity of state prices w.r.t. to the PG&E stock for these two dates, September 22, 2017, and October 12, 2017, provides estimates of and . Proposition 1 can be used to identify risk aversion from such elasticity of state prices w.r.t PG&E. Given that the PG&E stock represents 0.157% of the S&P 500 on October 1, 2017, the beta of the stock is , this would suggest investors’ risk aversion equal to on September 22, 2017 and 178.8 on October 12, 2017. These are far higher than conventional measures of relative risk aversion [mehra1985equity, meyer2005relative, guiso2018time].

5.5 Empirical Results: Panel Data

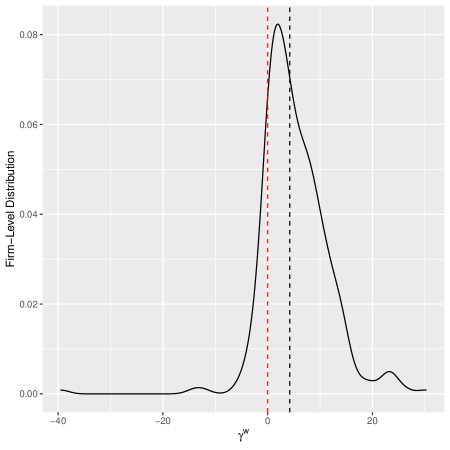

Firm-specific risk aversion is estimated stock by stock for each wildfire event of the treatment group. For each stock, and for each day that a listed firm is exposed to a wildfire, the risk neutral distribution is estimated using \possessiveciteait2003nonparametric approach of applying the \citeasnounbreeden1978prices approach using a local polynomial regression on arbitrage-free prices. The physical distribution is estimated using the GARCH-Wildfire model, estimated separately for each firm. The day- and maturity-specific risk-free rate is obtained using the LIBOR. The physical distribution is estimated on the same grid as the risk neutral distribution. This yields 1,481,076 observations for 361 firms across 233 days.

Results are presented on Figure 9. Panel (i) presents the distribution of firm-level risk aversions. Panel (ii) suggests that the average relative risk aversion is 0.292. The 75th percentile is between 0.497 and 0.571. The lower part of panel (ii) presents the t statistics, of an average of 23.0, 20.2, and 31.4 respectively.

On panel (i), observations left of the vertical line are for negative risk aversions, for which a pricing kernel puzzle is present. An extensive literature describes the presence of non-monotonic parts of the pricing kernel for specific subsets of the range of forward prices [beare2016empirical, cuesdeanu2018pricing, linn2018pricing, figlewski2018risk]. The evidence here is on the overall monotonicity of the pricing kernel. Panel (ii) suggests that 87% of firms do not exhibit a pricing kernel puzzle (1-0.13=0.87). This pricing kernel puzzle is significant at 95% for only 8% of firms (second row of estimates). This suggests that a substantial majority of pricing kernels are downward sloping. Any upward sloping segment of the state prices would lead to downward biased estimates of . Our estimates should thus be interpreted as lower bounds on the elasticity of state prices w.r.t. the wildfire-exposed stock.

We then turn to the result of proposition 1 to estimate investors’ risk aversion w.r.t. wealth. The proposition states that, for a geometric brownian motion with wildfire jumps, the . Such calculation is performed for each firm exposed to a wildfire separately. is estimated assuming the investor holds the S&P 500. The share of stocks in the investor’s portfolio is obtained using the Survey of Consumer Finances (SCF). The correlation is a function of each stock’s , the variance of returns, and the variance of market returns. The table below displays the risk aversion parameters thus estimated using each firm-level data, using the forecast physical distribution . If the model (including beliefs) are correctly specified, estimating relative risk aversion using different stocks should yield similar estimates . Hence below, and again in the case of a well-specified model, should only differ across s due to differences in the share of the stock in the market portfolio and differences in the and volatility of the stock.

| Parameter | Mean | P25 | Median | P75 |

|---|---|---|---|---|

| 114.41 | 38.56 | 91.44 | 181.79 |

Risk aversion w.r.t wealth under the assumption that: the share of the asset in the investor’s portfolio is equal to its share in the S&P 500 times the share of stocks in the investor’s portfolio; correlations and variances using the observed returns of the stock and the index; share of stocks in the investor’s portfolio using the Survey of Consumer Finances.

Results suggest a median risk aversion parameter of 38.56 (P25) to 181.79 (P75), with a median of 91.44 and mean of 114.41. The distribution is as expected right-skewed given the demand for hedges for stocks with little impact of wildfires on their physical distribution. \citeasnounbarro2006rare states that the usual view of the literature is that should be between 2 and 5. In the wildfire-exposed sample, using firm-level s , 88% of the estimates suggest a risk aversion w.r.t wealth above 5. This is the case even as our estimates of are lower bounds due to the use of estimates and of and .

These higher than expected levels of risk aversion could be consistent by at least two mechanisms:

-

1.

Investors holding larger amounts of wildfire-exposed stocks than the market portfolio.

-

2.

A difference between the observed physical distribution of returns (which was estimated using a GARCH-Wildfire model) and that used by investors to price options. Investors hold beliefs, and this probability distribution may significantly differ from the as estimated using the observed time series. Investors may hedge against large and rare downward jumps, or they may hedge against stochastic volatility. Options on wildfire-exposed stocks may price disasters, the micro counterpart of the market-level approach of \citeasnounbarro2006rare.

This second mechanism is a version of what \citeasnouncuesdeanu2018pricing coins the Peso problem, when observed historical returns do not include an event, but subjective distributions incorporate investors’ fears.

We implement an empirical approach for these two points below.

6 Discussion

6.1 Identification of Option-Implied Portfolio Shares Exposed to Wildfires

Proposition 1 can be used to calibrate the portfolio shares held by investors given literature-driven choices of the risk aversion parameter with respect to wealth. Following relationship (20), the portfolio share in the wildfire-exposed stock is:

| (24) |

where is the elasticity of state prices with respect to the wildfire stock, is the correlation of the stock and the index is the standard deviation of the diffusion of the index, is the standard deviation of the diffusion of the wildfire-exposed stock. Numerical simulations suggest this relationship holds for other types of stochastic processes than geometric brownian motions, including with stochastic volatility and jumps.