Pairwise Learning via Stagewise Training in Proximal Setting

Abstract

The pairwise objective paradigms are an important and essential aspect of machine learning. Examples of machine learning approaches that use pairwise objective functions include differential network in face recognition, metric learning, bipartite learning, multiple kernel learning, and maximizing of area under the curve (AUC). Compared to pointwise learning, pairwise learning’s sample size grows quadratically with the number of samples and thus its complexity. Researchers mostly address this challenge by utilizing an online learning system. Recent research has, however, offered adaptive sample size training for smooth loss functions as a better strategy in terms of convergence and complexity, but without a comprehensive theoretical study. In a distinct line of research, importance sampling has sparked a considerable amount of interest in finite pointwise-sum minimization. This is because of the stochastic gradient variance, which causes the convergence to be slowed considerably. In this paper, we combine adaptive sample size and importance sampling techniques for pairwise learning, with convergence guarantees for nonsmooth convex pairwise loss functions. In particular, the model is trained stochastically using an expanded training set for a predefined number of iterations derived from the stability bounds. In addition, we demonstrate that sampling opposite instances at each iteration reduces the variance of the gradient, hence accelerating convergence. Experiments on a broad variety of datasets in AUC maximization confirm the theoretical results.

1 Introduction

In machine learning, an unknown optimal classifier is sought to minimize the overall true or excess error associated with classifying all underlying distributions. Since the distribution is not completely known, sampling statistics are used to depict it, for instance, empirical loss (finite sum of pointwise losses) is proved to be an unbiased estimate of the true risk. However, in many situations, such as imbalanced data classification, where labels are not evenly distributed across the training set, continuing to approach the learning process in the classical pointwise empirical risk minimization may result in enormous computational effort. In the latter scenario and others e.g. differential network in face recognition kang2018pairwise ; song2019occlusion , metric learning kulis2012metric , bipartite learning zhang2016pairwise , multiple kernel learning zhuang2011unsupervised , and area under the curve (AUC) maximization zhao2011online , the pairwise objective paradigms is one alternative with superior statistical properties.

In contrast to pointwise learning, the sample size for pairwise learning increases quadratically as the number of samples increases. Researchers address this challenge by adopting an online learning scheme. For example Boissier et al. boissier2016fast introduced an improved online algorithm for general pairwise learning with complexity of 111The complexity is measured by gradient components evaluations where T is iteration number and d is the dimension of the data. In AUC maximization, Zhao et al. employs reservoir sampling with size , to sidestep the pairwise quadratic complexity in an online framework to enhance the complexity to zhao2011online . Recently, Ying et al. ying2016stochastic , have obtained an equivalent formulation of the AUC convex square linear loss using the saddle point problem and have optimized it in a stochastic manner to enhance the complexity to . Based on saddle point formulation of AUC objective, Natole et al.pmlr-v80-natole18a enhanced the algorithm such that extra variables introduced in ying2016stochastic are found in closed form solutions, which enhances the convergence of the original work from to under strong convexity assumption of the objective function but kept same complexity.

Moreover, many offline algorithms were proposed in the pairwise framework, for instance, Yang et al. recently investigated the offline stochastic gradient descent for pairwise learning in which at every iteration one pair is randomly selected from uniform distribution over i.e. the number of available examples. yang2021simple . Gu at al. gu2019scalable implemented doubly stochastic gradient descent to update a linear model incrementally in an stagewise offline manner, where again prior uniform distribution is assumed on the training set every stage. As with point-wise stochastic gradient descent, however, randomly picking one pair and modeling the gradient solely on one pair generates inevitable variance that slows convergence.

Although importance sampling is a fundamental strategy for dealing with variance created in stochastic learning systems, none of the available research has studied the importance sampling in pairwise paradigm to the best of our knowledge. On the other hand, we make advantage of the successful analysis presented in daneshmand2016starting with regard to the computational complexity in connection to the generalization and optimization errors. In particular, we tackle the quadratic complexity of finite sum minimization by employing an established yet effective adaptive sample size technique in which the problem is splitted to multi sub problems with expanding sample size. Although the method has been studied in the context of pointwise mokhtari2016adaptive smooth-pariwise recently gu2019scalable , but none of the researches tackle the non-smooth pairwise optimization. Moreover, we analyze the sub problems iteration number from different approach, namely the uniform stability and the optimization error as discussed in section 3.

| Algorithm | Reference | Problem | Loss | Sampling | Complexity |

|---|---|---|---|---|---|

| SPAM-NET | pmlr-v80-natole18a | AUC | NS-CVX | Online | |

| SOLAM | ying2016stochastic | AUC | S-CVX | Online | |

| OAM | zhao2011online | AUC | S-CVX | Online | |

| OPAUC | gao2013one | AUC | S-CVX | Online | |

| AdaDSGD | gu2019scalable | General | S-CVX | Uniform | |

| adaPSGD | Ours | Genereal | NS-CVX | Opposite |

1.1 Related work

The adaptive sample size approach is investigated in literature in different frameworks. The fundamental stochastic gradient descent (SGD) algorithm is one of the early techniques taking advantages of the identically distributed and independently drawn (i.i.d.) finite sum structure of the ERM. Followed by that the pioneer work of SAGA defazio2014saga , SVRGreddi2016stochastic , SARAHnguyen2017sarah and ADAMkingma2014adam . The primary motivation for all of the above techniques is to decrease the variance caused by randomly selecting a fixed-size subset every iteration. Recently Daneshmand et al. implemented an adaptive size scheme of training samples every iteration, and proved a better computational complexity in new algorithm (dynSAGA) to have statistical accurate solution in instead of iterationsdaneshmand2016starting . Moreover, Mokhtari et al. mokhtari2017first applied sample size methodology to first-order stochastic and deterministic algorithms, notably SVRG and accelerated gradient descent, and later to newton method mokhtari2016adaptive where better computational complexity is achieved. However in all mentioned researches, only univariate ERM or regularized ERM. Different authors are addressing pairwise learning in which full gradient needs a visit to all possible pairs i.e. , where refers to the number of training samples and thus deterministic approach serves as naive upper bound of complexity in where is iterations number. Zhao et al. presented an online approach for AUC maximization zhao2011online where buffer sampling with size is implemented to reduce computational complexity to with squared pairwise loss and Frobenius norm, with d being the dimension of data. Gau et al. gao2013one presented covariance matrix to update the gradient in , however this approach is very infeassible in high-dimensional data. Ying et al. ying2016stochastic converted the pairwise loss function with regularization to saddle point point problem, and update the primal and dual variables stochastically with complexity. The saddle point problem of AUC is also investigated in pmlr-v80-natole18a with non-smooth regularization namely, elastic net, with same computational complexity but better convergence rate under strong convexity setting. Although the work of Natole et al. pmlr-v80-natole18a handles the non-smooth regularization, it only focuess on the AUC maximization but we condiser the pairwise learning in general. Recently, Gu et al. gu2019scalable performed the adaptive sample size scheme on pairwise loss function, where experiment on AUC proved a superior results in terms of convergence and computational complexity , as shown in table 1. This research is most relevant to the last research, but with non-smooth regularized ERM and room of imporovment in the sub problem iteration number.

1.2 Contributions

We focus on pairwise learning in general, and AUC in particular, in this study, and make the following contributions:

-

•

Design new algorithm for non-smooth pairwise learning with adaptive sample size, and non-uniform sampling technique.

-

•

Analyze the sub problems iteration number from uniform stability and convergence analysis.

The remainder of the study is structured as follows: section 2 defines the problem of research, section 3 presents the methods for solving pairwise learning, section 4 illustrates the experiments, and section 5 concludes with closing remarks.

2 Problem Definition

In pairwise learning the ultimate goal is to learn a hypothesis over some distribution where is input space, is output space, and is a probability distribution. In cotrast to pointwise learning, in pairwise learning samples are available as pairs of samples and thus a pairwise loss function is implemented. In particular assumes a space and a pairwise loss function of hypothesis as . Some examples of pairwise loss functions are squared loss function , and hinge loss where , and is the hypothesis mapping. Moreover, the primary goal is to minimize an expected loss (risk) which is defined as or the regularized expected loss as illustrated in 1:

| (1) |

where is possibly non-smooth regularizer and is the regularization parameter. Formulation in 1 is common in machine learning e.g. AUC maximization ying2016stochastic . Since the expected loss is built on the unknown distributions , the empirical risk given a samples of data has been demonstrated to be a good estimator of the expected loss as illustrated in 2.

| (2) |

2.1 Assumptions and Notations

Given , being some input and output space, and unknown distributions and on , we first consider a training subset

where and is i.i.d of and i.e. , where

We also define a modified training subset of as follow,

| (3) |

where and independent from other examples i.e. .

We list all assumptions as follow assuming linear hypothesis e.g.

Assumption 1 (Lipschits Continuity).

For any the loss function is G-Lipschits continuous function over the feasible set i.e.

.

Assumption 2 (Convexity).

For any the loss function is -strongly convex function over the feasible set i.e.

moreover, the possibly non-smooth function is convex. Thus we have that is at least -strongly convex.

Assumption 3 (Smoothness).

For any the loss function is L-smooth i.e. there exist a constant such that

| (4) |

which is equivalent to :

| (5) |

Thus we have that is at least -smooth function.

3 Methodology

We first introduce our algorithm for solving the the problem in 2 in algorithm 1. Then, the analysis begins with the double stochastic gradient descent outlined in section 3.1 to solve the subproblems using non-uniform sampling and adatptive sample size. In sections 3.2 and 3.3, we analyze the algorithm’s convergence and uniform stability, and in section 3.4, we determine the least number of iterations required to solve any subproblem.

3.1 Doubly Stochastic gradient descent (DSGD) with adaptive sample size

Since the pair data are i.i.d., we expect to have a generalization bound on the difference between the empirical and the true risks, namely; in literature boucheron2005theory the bound is found to be function of the sample size as illustrated in (6).

| (6) |

In which corresponds to the algorithm used to solve the ERM and the expectation is set in relation to the training sample A small subset of training samples is used to solve the corresponding ERM within its statistical accuracy (based on 6). The adaptive sample size training then expands the training samples to include new samples on top of the previously solved ERM and solves the new ERM within its statistical accuracy (defined by the number total samples), where the optimization begins with an initial solution equal to the previous stage solution. The process will continue until all of the samples have been visited at least once.

In Theorem 1, an upper bound on the empire loss difference of a random stage with dataset is derived . The theorem, in particular, constrains the absolute difference between the optimal empire risk and the initial empire risk found using a subset in the prior stage. That is, if we define suboptimality of random stage empire loss with dataset with , as the difference , then the upper bound relies on the optimization accuracy of the ERM solution () of the previous stage on and other factors.

Theorem 1.

Assume that the training set is i.i.d. and we have a subset of of the size of , where is drawn from with equal probability. Define as an approximate solution of the risk in expectation, i.e., , we have that

| (7) |

Proof in appendix.

Remark 1.

The ultimate result of Theorem 1 leads to two important conclusions:

-

•

It is possible to obtain an approximate solution to the ERM by solving the ERM problem on a subset .

-

•

However, even if the most accurate ERM solution on exists, i.e. if , the succeeding ERM problem on will always have an optimal solution that is dependent on the . Theorem 1 states that this is true regardless of whether or not .

Thus, in light of the above-mentioned findings, we suggest an adaptive technique that includes expanding the training set size. In spite of the fact that the notion of dynamically growing sample size has been studied in the literature (see e.g. gu2019scalable ; mokhtari2017first ), none of the research currently accessible have dived into the implications of adaptive sample size in non-smooth pairwise learning (i.e. AUC with -norm).

If the empire loss in (2) has a differentiable loss function, then as is the case with univariate loss functions, double stochastic gradient descent seeks to employ an unbiased stochastic gradient.using pair of data. In other words given a sequences of i.i.d. training data in which , we define stochastic gradient of the ERM in 2 as:

| (8) |

where . Assume that variance of is defined as follow:

| (9) |

Before we prove the stochastic gradient used in algorithm 1 have reduced variance compared to uniform distribution we redefine the empirical risk to be unbiased of the true expected risk inspired by gopal2016adaptive as illustrated in 10.

| (10) |

where and . Moreover is a set of pairs defined on such that . This concept was developed for the first time by Gopal et al. gopal2016adaptive in an effort to reduce variance in pointwise stochastic gradient using class labels. In our pairwise framework, there are four natural sets: two sets with identical classes of the size and and two symmetric sets with distinct classes of the size , where and are the number of positive and negative examples in .

We define new distribution over our samples such that and zero otherwise , by forcing for k=3 and k=4 (sets with opposite labels) and zero for k=1 and k=2. The new gradient is now defined as

| (11) |

In proposition 1 we prove that the variance using the new static distribution is less than the uniform distribution gradient.

Proposition 1.

Using only opposite pairs to generate the stochastic gradient would results in reduced variance compared to uniform distribution over i.e.:

| (12) |

Proof in appendix.

3.2 Uniform Stability

Solving the optimization problem in adaptive sample size requires crucial definition of the iteration number in every subproblem (or inner loop). We investigate the minimal number of iteration needed in every innep loop using uniform stability and convergence rate of the DSGD, after we define the uniform stability and its relation to generalization error in definitions 1 and 2 (bousquet2002stability ; shen2020stability ; agarwal2009generalization ).

Definition 1 (Algorithmic Stability).

An iterative algorithm is called -stable w.r.t. the loss function if:

| (13) |

where the expectation is w.r.t. the algorithm randomness, , and defined in (3).

Definition 2 (Generalization Bound).

Given -stable algorithm , the generalization error of the same algorithm given dataset is bounded above as:

| (14) |

which is equivalent to

| (15) |

where the expectations is w.r.t. the randomness of algorithm and choice of S.

In proposition 2 we introduce the stability bound of our algorithm 1 as a function of the step size and the Lipschits continuity constant.

Proposition 2 (Stability).

Let w be the output of algorithm 1 on training datasets and . Let assumption 2 hold with and , then the algorithm 1 is -uniformly stable and further the generalization bound of is bounded above as:

| (16) |

Proof in appendix.

The bound of the stability in proposition 1 depends on the sequence of the step size . In corollary 1 we assumes the standard fixed step size, to have a bound that is dependent on the iteration number .

Corollary 1.

If the step size is chosen to be constant i.e. , then the bound in proposition 2 is :

| (17) |

In the next section we derive the convergence rate for algorithm 1 and together with the stability bound we can arrive at the optimal iteration number needed in the inner loop to have a solution that is statistically accurate.

3.3 Convergence Analysis

Theorem 2.

The DSGD algorithm under assumptions 2,3 and bounded variance of gradient e.g.:

| (18) |

have sublinear convergence rate given the proximal operator of is cheaply computed, i.e. given an initial solution such that we have for any stage in DSGD algorithm 1:

| (19) |

where depends on the setting of the loss function.

Remark 2.

The convergence and stability bound of DSGD indicates the following:

-

1.

Variance of the gradient could slow the convergence.

-

2.

The generalization bound indicates the iteration number expand the bound .

3.4 Computational Complexity

Based on proposition 2 and theorem 2, we chose the number of iteration in every inner loop by minimizng both bounds in as follow:

| (20) |

The solution can be found easily as .

Theorem 3 states the computational complexity of our algorithm 1 is where n is the number of examples, and the complexity is expressed in terms of gradient components to reach -optimal solution of the ERM.

Theorem 3.

| Dataset | Examples | Features | Reference | |

|---|---|---|---|---|

| 1 | a9a | 32,561 | 123 | Dua:2019 |

| 2 | rcv1 | 20,242 | 47,236 | lewis2004rcv1 |

| 3 | fourclass | 862 | 2 | ho1996building |

| 4 | diabetes | 768 | 8 | Dua:2019 |

| 5 | covtype | 581,012 | 54 | Dua:2019 |

| 6 | ijcnn1 | 49,990 | 22 | CC01a |

4 Experiments

The experiments in this part are focused on pairwise learning in AUC maximization, which is the approach that attempts to maximize the area under the receiver operating characteristic curve (ROC) through a variety of ways but not including the pointwise learning.

4.1 Problem Formulation

AUC metric maximization is defined as in equation (22) as first introduced in hanley1982meaning that measures the probability of obtaining higher weight on the positive label. Given a space with unknown distribution and . A function that takes a sample,e.g. drawn independently according to and predicts the classes have AUC score given by:

| (22) |

where the expectation is w.r.t. the samples. However given the fact that the formulation in (22) is neither convex nor differentiable, researchers have approximated the AUC by using surrogate convex functions, such as the square function and hinge loss. In addition to the fact that data are often limited and the distribution is unidentifiable, it is impossible to calculate the expectation directly; as a result, we present the empirical AUC score in (23) with linear model and regularized squared loss function.

| DS | adaDSGD |

|

SOLAM | B-LS-SVM | OPAUC | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 |

|

|

|

|

|

|

|

||||||||||||||

| 2 |

|

|

- | - | - | - | - | ||||||||||||||

| 3 |

|

|

|

|

|

|

|

||||||||||||||

| 4 |

|

|

|

|

|

|

|

||||||||||||||

| 5 |

|

|

|

|

|

|

|

||||||||||||||

| 6 |

|

|

|

|

|

|

|

||||||||||||||

| Reg | |||||||||||||||||||||

| Ref | Ours | pmlr-v80-natole18a | ying2016stochastic | zhao2011online | zhao2011online | joachims2006training | gao2013one |

| (23) |

where , denote the positive and negative examples respectively, is d-dimensional linear model weight and is non-smooth but convex regularization. The elastic net is considered i.e. , to have fair compassion with AUC maximization algorithms in literature. However, (lasso) or mixture of both and (group lasso) can be applied. The proximal step (part 8) in algorithm 1 for elastic net can be easily computed given the stochastic gradient step 7, as follow:

| (24) |

where , are the regularization weights, and is the step size.

4.2 Datasets

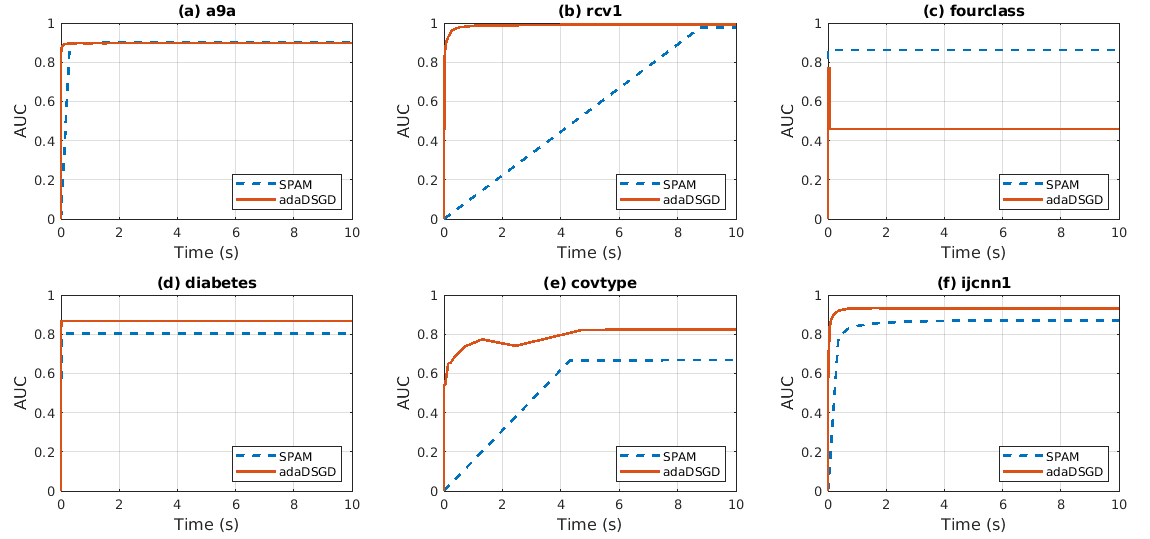

The datasets names used in this experiments are listed in table LABEL:datasets along with their features, sample size, and source reference. Since AUC maximization approach is based on binary classification, where nonbinary datasets are converted to binary by randomly dividing the labels into two groups. Every dataset is divided into two parts: 80 percent training and 20 percent testing; in addition, the experiments on each dataset are repeated 25 times with different random seeds, and the standard error and mean are calculated for each experiment. The experiments are conducted in MATLAB on intel 2.4 GHz machine with 4 GBs RAM.

Experiment findings are separated into two parts: first, we compare the complexity of the algorithm as measured by its running time to SPAM-NET since, as shown in its experiment section, it is the superior algorithm pmlr-v80-natole18a . In the second part of this analysis, we evaluate the outcomes of the AUC in terms of the arithmetic mean and the standard error of each method displayed in table 3. Both aspects of the study demonstrate that our algorithm is better in terms of the AUC findings and the length of time it takes to execute (except for dataset number 3 fourclass).

5 Conclusions

In this study, a new approach for pairwise objective paradigms was investigated. A double stochastic gradient descent (DSGD) in stagewise phase is presented as a workable solution of sample size, which increases quadratically with the number of samples. In particular , the training set is divided into finite number of smaller sets, and every outerloop the algorithm expand the training set to include new set. Moreover, we used convergence bound and uniform stability of DSGD to calculate the lowest number of iterations required for each stage. Concurrently, we presented a new distribution over the different sample space in order to lower the gradient variance induced in DSGD, by sampling opposite instances at each iteration. AUC maximization experiments conducted on a wide range of datasets confirm the theoretical predictions. It is possible to do further investigation in order to develop a more sophisticated, non-static importance sampling strategy.

References

- [1] Bong-Nam Kang, Yonghyun Kim, and Daijin Kim. Pairwise relational networks for face recognition. In Proceedings of the European Conference on Computer Vision (ECCV), pages 628–645, 2018.

- [2] Lingxue Song, Dihong Gong, Zhifeng Li, Changsong Liu, and Wei Liu. Occlusion robust face recognition based on mask learning with pairwise differential siamese network. In Proceedings of the IEEE/CVF International Conference on Computer Vision, pages 773–782, 2019.

- [3] Brian Kulis et al. Metric learning: A survey. Foundations and trends in machine learning, 5(4):287–364, 2012.

- [4] Zhen Zhang, Qinfeng Shi, Julian McAuley, Wei Wei, Yanning Zhang, and Anton Van Den Hengel. Pairwise matching through max-weight bipartite belief propagation. In Proceedings of the IEEE conference on computer vision and pattern recognition, pages 1202–1210, 2016.

- [5] Jinfeng Zhuang, Jialei Wang, Steven CH Hoi, and Xiangyang Lan. Unsupervised multiple kernel learning. In Asian Conference on Machine Learning, pages 129–144. PMLR, 2011.

- [6] Peilin Zhao, Steven CH Hoi, Rong Jin, and Tianbo YANG. Online auc maximization. 2011.

- [7] Martin Boissier, Siwei Lyu, Yiming Ying, and Ding-Xuan Zhou. Fast convergence of online pairwise learning algorithms. In Artificial Intelligence and Statistics, pages 204–212. PMLR, 2016.

- [8] Yiming Ying, Longyin Wen, and Siwei Lyu. Stochastic online auc maximization. Advances in neural information processing systems, 29:451–459, 2016.

- [9] Michael Natole, Jr., Yiming Ying, and Siwei Lyu. Stochastic proximal algorithms for AUC maximization. In Jennifer Dy and Andreas Krause, editors, Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 3710–3719. PMLR, 10–15 Jul 2018.

- [10] Zhenhuan Yang, Yunwen Lei, Puyu Wang, Tianbao Yang, and Yiming Ying. Simple stochastic and online gradient descent algorithms for pairwise learning. Advances in Neural Information Processing Systems, 34, 2021.

- [11] Bin Gu, Zhouyuan Huo, and Heng Huang. Scalable and efficient pairwise learning to achieve statistical accuracy. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 3697–3704, 2019.

- [12] Hadi Daneshmand, Aurelien Lucchi, and Thomas Hofmann. Starting small-learning with adaptive sample sizes. In International conference on machine learning, pages 1463–1471. PMLR, 2016.

- [13] Aryan Mokhtari, Hadi Daneshmand, Aurelien Lucchi, Thomas Hofmann, and Alejandro Ribeiro. Adaptive newton method for empirical risk minimization to statistical accuracy. Advances in Neural Information Processing Systems, 29, 2016.

- [14] Wei Gao, Rong Jin, Shenghuo Zhu, and Zhi-Hua Zhou. One-pass auc optimization. In International conference on machine learning, pages 906–914. PMLR, 2013.

- [15] Aaron Defazio, Francis Bach, and Simon Lacoste-Julien. Saga: A fast incremental gradient method with support for non-strongly convex composite objectives. Advances in neural information processing systems, 27, 2014.

- [16] Sashank J Reddi, Ahmed Hefny, Suvrit Sra, Barnabas Poczos, and Alex Smola. Stochastic variance reduction for nonconvex optimization. In International conference on machine learning, pages 314–323. PMLR, 2016.

- [17] Lam M Nguyen, Jie Liu, Katya Scheinberg, and Martin Takáč. Sarah: A novel method for machine learning problems using stochastic recursive gradient. In International Conference on Machine Learning, pages 2613–2621. PMLR, 2017.

- [18] Diederik P Kingma and Jimmy Ba. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980, 2014.

- [19] Aryan Mokhtari and Alejandro Ribeiro. First-order adaptive sample size methods to reduce complexity of empirical risk minimization. Advances in Neural Information Processing Systems, 30, 2017.

- [20] Stéphane Boucheron, Olivier Bousquet, and Gábor Lugosi. Theory of classification: A survey of some recent advances. ESAIM: probability and statistics, 9:323–375, 2005.

- [21] Siddharth Gopal. Adaptive sampling for sgd by exploiting side information. In International Conference on Machine Learning, pages 364–372. PMLR, 2016.

- [22] Olivier Bousquet and André Elisseeff. Stability and generalization. The Journal of Machine Learning Research, 2:499–526, 2002.

- [23] Wei Shen, Zhenhuan Yang, Yiming Ying, and Xiaoming Yuan. Stability and optimization error of stochastic gradient descent for pairwise learning. Analysis and Applications, 18(05):887–927, 2020.

- [24] Shivani Agarwal and Partha Niyogi. Generalization bounds for ranking algorithms via algorithmic stability. Journal of Machine Learning Research, 10(2), 2009.

- [25] Dheeru Dua and Casey Graff. UCI machine learning repository, 2017.

- [26] David D Lewis, Yiming Yang, Tony Russell-Rose, and Fan Li. Rcv1: A new benchmark collection for text categorization research. Journal of machine learning research, 5(Apr):361–397, 2004.

- [27] Tin Kam Ho and Eugene M Kleinberg. Building projectable classifiers of arbitrary complexity. In Proceedings of 13th International Conference on Pattern Recognition, volume 2, pages 880–885. IEEE, 1996.

- [28] Chih-Chung Chang and Chih-Jen Lin. LIBSVM: A library for support vector machines. ACM Transactions on Intelligent Systems and Technology, 2:27:1–27:27, 2011. Software available at http://www.csie.ntu.edu.tw/~cjlin/libsvm.

- [29] James A Hanley and Barbara J McNeil. The meaning and use of the area under a receiver operating characteristic (roc) curve. Radiology, 143(1):29–36, 1982.

- [30] Thorsten Joachims. Training linear svms in linear time. In Proceedings of the 12th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 217–226, 2006.