Foreign exchange options on Heston-CIR model under Lévy process framework

Abstract.

In this paper, we consider the Heston-CIR model with Lévy process for pricing in the foreign exchange (FX) market by providing a new formula that better fits the distribution of prices. To do that, first, we study the existence and uniqueness of the solution to this model. Second, we examine the strong convergence of the Lévy process with stochastic domestic short interest rates, foreign short interest rates and stochastic volatility. Then, we apply Least Squares Monte Carlo (LSM) method for pricing American options under our model with stochastic volatility and stochastic interest rate. Finally, by considering real-world market data, we illustrate numerical results for the four-factor Heston-CIR Lévy model.

2 Department of Applied Mathematics, Faculty of Mathematical Sciences, University of Guilan, P. O. Box: 41938-1914, Rasht, Iran,

3 Department of Economics and Finance, University of Bari “Aldo Moro”, Largo Abbazia S. Scolastica, I-70124 Bari, Italy

Keywords: Heston-CIR model, Variance Gamma process, Lévy processes, foreign short interest rates.

JEL Classification: C22, G15, F31

MSC 2010: 60G51, 60G40, 62P05

1. Introduction

In this paper, we study the problem of pricing American options in foreign exchange (FX) markets. Our purpose is to consider a Heston hybrid model, that is the Heston-CIR model. The said model correlates stochastic volatility and stochastic interest rate, under the assumption that the underlying stock returns follow a Lévy process. In FX markets, option pricing under stochastic interest rate and stochastic volatility was first introduced by Grzelak et al. [29] and Van Haastrecht et al. [75].

Let be a filtered probability space with the risk-neutral probability on which a Brownian motion is defined . Consider an asset price process following a Geometric Brownian Motion (GBM) process and satisfying the following stochastic differential equation (SDE)

| (1.1) |

where is the asset price at time and the constant parameters and are, respectively, the (domestic) risk-neutral interest rate and the volatility. This model was presented by Black-Scholes and Merton [52] and was a major step in arbitrage-free option pricing because it evaluates options at the risk-neutral rate regardless of the risk and return of the underlying. Meanwhile the model (1.1) became very popular in finance among practitioners because it takes positive values and it has simple calculations (for example, see [52], [34], [36], [67], [56], [57], [58], [59]). But along with all these advantages, this model has also some noteworthy shortcomings such as constant interest rate, constant volatility and absence of jump term.

The need for more sophisticated frameworks, to cope with the above-mentioned shortfalls, has led the ensuing literature to the development of a number of papers for pricing derivatives on risky assets based on stochastic asset price models generalizing the classical GBM paradigm ([37], [69], [38], [13], [53], [25], [74])

For example, with regard to interest rates, the most widely used model in finance is the Cox-Ingersoll-Ross (CIR) model which assumes the risk-neutral dynamics of the instantaneous interest rate to be described by a stochastic process (also known as square-root process ) driven by the SDE

where is the speed of adjustment of interest rates to the long-term mean and is the volatility.

Further, concerning volatility, one of the pioneering papers is that of Steven L. Heston [38] who derived the pricing formula of a stock European option when the dynamics of the underlying stock price are described by a model with non-constant volatility supposed to be stochastic.

Given the popularity and advantages of both the Heston and the CIR models, the hybrid version of them is the so-called Heston-CIR model [1, 29, 30, 31, 76] (see also [25] for application to the American option pricing), where the dynamics of the underlying asset price is given by

| (1.2) |

where and are, respectively, the stochastic variance and the stochastic domestic interest rate of the stock return. All processes are defined under the domestic risk-neutral measure, . is the second-order volatility, i.e. the volatility of variance (often called the volatility of volatility or, shorter, vol of vol), and denotes the volatility of the short rate . and are the mean reverting rates of the variance and short rate processes, respectively. We assume the long-run mean of the asset price is constant. The parameters and are respectively, the long-run mean of the variance and interest rate. denote the initial asset price, variance and interest rate. The standard Brownian motions , for , are supposed to be correlated. The correlation matrix is given by

1.1. Jumps in financial models

With regard to jumps, there are lots of reasons to utilize them in financial models. In the real world, asset price empirical distributions present fat tails and high peaks and are asymmetric, behaviour that deviates from normality. From a risk management perspective, jumps allow quantifying and taking into account the risk of strong stock price movements over short time intervals, which appears non-existent in models with continuous paths. Anyway, the strongest argument for using discontinuous models is simply the presence of jumps in observed prices. Thus, we want to model these phenomena with jump diffusion or Lévy processes. A jump-diffusion process is a stochastic process in which discrete movements (i.e. jumps) take place at fixed or random arrival times. Those jumps represent transitions between discrete states and the time spent on a given state is called holding time (or sojourn time). In [52], Merton introduced a jump-diffusion model for pricing derivatives as follows

where and are constants and is a jump process independent of . Since the publication of the Merton paper [52], several jump-diffusion models have been considered in the academic finance literature, such as the compound Poisson model, the Kou model, the Stochastic Volatility Jump (SVJ) model (see [44], [45] and references therein), the Bates model [11] and the Bates Hull-White model [41].

1.2. Lévy processes

In this paper, we consider Lévy processes, commonly used in mathematical finance because they are very flexible and have a simple structure. Further, they provide the appropriate tools to adequately and consistently describe the evolution of asset returns, both in the real and in the risk-neutral world. A one-dimensional Lévy process defined on , is a càdlàg, adapted process with a.s., having stationary (homogeneous) and independent increments and also, it is continuous in probability (see, for example, [55, 61, 12, 16]).

When the discounted process is a martingale under , the asset price dynamics under the Lévy process can be modeled as

where the parameter is the (domestic) risk-free interest rate and is the continuous dividend yield of the asset. Several processes of this kind have been studied. Well-known models are the Variance Gamma (VG) [48], [49] the Normal Inverse Gaussian (NIG) [8] and the Carr-Geman-Madan-Yor (CGMY).

1.3. Normal Inverse Gaussian (NIG)

The NIG process was first introduced in 1977 [8] and adopted in finance in 1997 [9] as a handy model to represent fat tails and skews. Let us denote by the location parameter, the tailedness, the skewness satisfying , the scale, and by a modified Bessel function of the third kind. The NIG distribution is defined on the whole real line having density function ([7])

The NIG process of Lévy type can be represented via random time change of a Brownian motion as follows.

Let be a Brownian motion with drift and diffusion coefficient 1, and

be the inverse Gaussian process with parameters and . For each , is a random time defined as the first passage time to level of . Further, denote by a second Brownian motion, stochastically independent of , with drift and diffusion coefficient 1. Thus the NIG process is the random time changed process

It can be interpreted as a subordination of a Brownian motion by the inverse Gaussian process ([9]). The distribution of the unit period increment follows the NIG distribution.

1.4. Variance Gamma (VG)

The VG model was first introduced by Madan et al. in [48], and then widely used to describe the behaviour of stock prices (see [49] and references therein). The goal of using the VG model for fitting stock prices is to improve, with respect to the classical GBM, the ability to replicate skewness and kurtosis of the return distribution. In fact, the VG process is an extension of the GBM aimed at solving some shortcomings of the Black and Scholes model. A gamma process is a continuous-time stochastic process with mean rate and variance rate , such that for any , the increments over non-overlapping intervals of equal length, are independent gamma distributed random variables with shape parameter and scale parameter .

A VG process of Lévy type, , can be represented in two different ways:

-

•

As a difference , where and are processes with i.i.d. gamma distributed increments. Notice that, as the gamma distribution assumes only positive values, the process is increasing;

-

•

As a subordination of a Brownian motion by a gamma process, i.e. is the random time changed process , where is a gamma process with unit mean and variance rate , and is a Brownian motion with zero drift and variance .

In this work, we shall consider the second representation of a VG process (see Section 2).

1.5. Stylized facts on returns, options’ dynamics and Variance Gamma (VG)

As mentioned several reasons lead us to adopt a VG model. The stylized facts about returns, options’ dynamics are documented by Fama [26], Akgiray et al. [2], Bates [11], Madan et al. [48], Campa et al. [20], etc. Namely, they are: a) “smiles” and “smirks” effects b) jumps c) finite sum of the absolute log price changes d) excess of kurtosis/long tailedness e) finite moments for at least the lower powers of returns; f) extension to multivariate processes with elliptical multivariate distributions to ensure consistency with the capital asset pricing model (CAPM).

Regarding “smiles” and “smirks”, it is well known that the Black-Scholes formula is strongly biased across both moneyness and maturity and that underprices deep out-of-the-money puts and calls. For example Rubinstein [63, 64] reports evidence that implied volatilities are higher for deeply in- or out-of-the-money options. This is because stock return distributions are negatively skewed with higher kurtosis than allowable in a BS log-normal distribution [11]. Furthermore ”pure diffusion based models have difficulties in explaining smile effects in, in particular, short-dated option prices” [49].

The so-called stochastic volatility (SV) models were one of the first solutions to the problem as they allowed a flexible distributional structure by correlating volatility shocks and underlying stock returns. The correlation in SV models controls both skewness and kurtosis. The downside of that approach is that the volatility is a diffusion process which means it can only follow a continuous sample path (thus is unable to internalize enough short-term kurtosis [5]).

To solve that concern, jump-diffusion models were introduced. In fact, they are capable to explain negative skewness and high implicit kurtosis in option prices where the random discontinuous jumps are represented by a Poisson component [5].

On the other hand, the VG process (for which the Black Scholes model is a parametric special case) is a pure jump process and there is no diffusion component. In the VG process, the returns are normally distributed, conditional on the realization of a random time with gamma density. Therefore the resulting stochastic process and associated option pricing model provide ”a robust three parameter model” [48]. Apart from the volatility of the Brownian motion the VG can control both kurtosis and skewness.

1.6. Organization of the article

This article is organized as follows. Section 2 explains the Heston-CIR Lévy model for FX market. In Section 3 we study the local existence and uniqueness of solution for the stochastic differential equations as described by the Variance Gamma process. Section 4 shows that the forward Euler-Maruyama approximation method converges almost surely to the solution of the Heston-CIR model. Section 5 illustrates the considered dataset. Section 6 displays numerical simulations obtained with the LSM method for Lévy processes on the American put and call options and compares estimated prices with real-wolrd market prices. Section 7 concludes.

2. The Heston-CIR of VG Lévy type model for FX market

This section describes a generalization of the Heston-CIR model (1.2) for evaluating options price, under the domestic risk-neutral measure , in FX markets. The resulting model is evaluated at random times given by a gamma process.

Let be a complete filtered probability space, where is the risk-neutral probability measure, and let us denote by the expected value operator. On such a space, let be a -dimensional Brownian motion with instantaneous correlation matrix

Clearly, being them correlation coefficients, it must hold and has to be positive definite (assuming that are linearly independent). Let us now consider a Gamma subordinator independent of . Precisely, as introduced in the previous section, a Gamma subordinator with mean rate and variance rate is a pure-jump increasing Lévy process such that and is a Gamma distributed random variable with shape parameter and scale parameter , where with we denote the equality in distribution. One can easily express the Lévy measure of in terms of the shape and scale parameters and , as

where and for any set and any we denote for any

Clearly, satisfies the usual integrability assumption on the Lévy measure of a subordinator, i.e.

where for any and any real numbers we denote

Let us stress that , i.e. the subordinator has infinite activity. This guarantees that we cannot reduce to the (trivial) case of a compound Poisson process (see [14, Section 1.2]). Up to a time-scaling, we could always assume . However, in the following, we will, in any case, consider any shape parameter . Now let us consider, for any , the subordinate Brownian motion . A deep study on subordinate Brownian motions is given in [43]. In particular, if , is a Variance Gamma process for any , as observed in [49]. By virtue of the previous observation, we will call a Variance Gamma process even if , as they exhibit, up to a suitable time-scaling, the same properties. In particular, let us recall that admits finite moments of any order and its sample paths are almost surely of bounded variation. Finally, we denote .

Fix now . The Heston-CIR of VG Lévy type model is defined by the following system of SDEs, for :

| (2.1) | ||||

where is the stochastic variance of the underlying asset price , and are, respectively, the domestic and foreign stochastic short interest rates. The parameters are the speeds of mean reversion, are the foreign long-run means, are the volatilities, are the drifts respectively of and . Moreover, we assume that is the correlation between a domestic asset and the foreign interest rate and is its drift. For any function , where , we denote, if it exists, . Finally, we assume that the initial data are deterministic.

In the next section, we will investigate (local) the existence and uniqueness of the solution of the system defining the Heston-CIR VG Lévy type model.

3. Existence and uniqueness of the solution of VG Lévy type model

First of all, let us consider, without loss of generality, . Let us fix some further notation. For any topological space we denote by its Borel -algebra. Moreover, for any cádlág function we denote . For any and we denote to identify its components and the action of a function will be denoted both with or depending on the necessity of highlighting the single components of the argument. For we denote the usual scalar product and the Euclidean norm. Moreover, for any fixed and any bounded function we denote . For any function we denote the support of as , where, for any , is the topological closure of . We denote by the space of continuous and bounded functions and by the space of infinitely differentiable functions with compact support. For any we denote by the space of continuous functions with continuous partial derivatives up to order and by its subspace of bounded function with bounded partial derivatives. Finally, given a sequence , we denote (resp. ) as if is non-decreasing (resp. non-increasing) and . In the proofs, we will denote by any generic constant whose value is not crucial.

To prove the local existence and uniqueness of the solutions of (2.1) we will make use of several different techniques from both the theory of stochastic differential equations with jumps and cádlág rough differential equations. In place of proving a single existence and uniqueness theorem for the whole system, we will proceed step by step, providing first the results concerning the equations of and , then the one of and finally the one of . Thus, we first want to focus on the equations

| (3.1) | |||

| (3.2) |

To do this, we need the following easy (but technical) Lemma which is demonstrated in Appendix A.

Lemma 3.1.

Let

For any , the process is a pure jump Lévy process on with Lévy measure

| (3.3) |

With this property in mind, we can prove the following existence and uniqueness theorem by combining the arguments of [77, Theorems 2.4 and 2.8] and [28, Theorem 3.1 and 3.2].

Theorem 3.2.

Now let us handle the Equation

| (3.4) | ||||

It will be convenient to consider it as coupled with (3.1). However, the processes and that constitute part of the noise are correlated, not only since they are obtained from their respective parent processes and by means of the same time-change , but also since the parent processes themselves are correlated, with instantaneous correlation matrix

Let us consider a standard -dimensional Brownian motion and let be the Cholesky factor (see [35, Corollary 7.2.9]). In particular, in this case, one can evaluate explicitly as

It is well known (see, for instance, [3, Section XI.2]) that, denoting , it holds , where with we mean the transposed of the matrix . This means that is a standard -dimensional Brownian motion ad we can directly set without loss of generality. Defining , we have . With this in mind, we can rewrite Equations (3.1) and (3.4) as

| (3.5) | |||||

| (3.6) | |||||

This time we need a slightly different technical Lemma, that is proved in the same way as Lemma 3.1.

Lemma 3.3.

Let

The process is a pure jump Lévy process on with Lévy measure

| (3.7) |

Now we are ready to state the following existence and uniqueness theorem.

Theorem 3.4.

Equation (3.4) admits a pathwise unique non-negative strong solution up to a Markov time .

Remark 3.5.

It is clear that the localization argument adopted in the case is also valid in the case and for Equations (3.1) and (3.2).

Let us define a somewhat natural extension of the processes , and when they turn negative.

Up to now, we were not able to prove that a similar extension holds as .

Let us also recall that, since we are using [70, Theorem 2.2] or [4, Theorem 6.2.3], we have the processes , and are almost surely cádlág. Without loss of generality, we can assume that for any the paths , and are cádlág respectively up to , and .

Now we are finally ready to prove that Equation

| (3.8) | ||||

admits a pathwise unique strong solution up to a Markov time.

Theorem 3.6.

Equation (3.8) admits a pathwise unique non-negative cádlág strong solution up to a Markov time .

Proof.

Let and be the Markov times up to which Equations (3.1), (3.2) and (3.4) admit a pathwise unique strong solution and let . Without loss of generality, we can assume that and are of bounded variation and cádlág for any , while , and are cádlág for any . Then we define the process, for ,

where we can consider each integral as a Lebesgue-Stieltjes integral for any fixed .

Now fix and any . Then we can consider the random rough differential equation

Such an equation admits a unique cádlág solution for each , thanks to [27, Theorem 1.13], while [27, Proposition 6.9] guarantees that is the unique strong solution of Equation (3.8), concluding the proof. ∎

Remark 3.7.

By definition, . Hence we can define as the local existence time threshold for the whole Heston-CIR system (2.1).

In the next section we will focus on the convergence of the forward Euler-Maruyama scheme to the solution of our Heston-CIR model. To do this, we will use a localization argument which is similar to the one adopted in the proof of Theorem 3.4 in the case .

4. Convergence of the Euler discretization method to the Heston-CIR of VG Lévy type model

As we stated in the previous Section, we want to prove some form of a convergence of the forward Euler-Maruyama scheme for the Heston-CIR system (2.1). As we did for the proof of Theorem 3.4, we first need to recast the equations in order to handle the correlation structure between the processes , . Arguing as before, we can consider the Cholesky factorization (where ) and define a -dimensional standard Brownian motion by setting

Then we can define the process as . Again, to find the Lévy-Itô decomposition of , we need the following technical Lemma, whose proof is identical to the one of Lemma 3.1.

Lemma 4.1.

Let

Then the process is a pure jump Lévy process on with Lévy measure

We can deduce from the previous Lemma the Lévy-Itô decomposition of , by defining the Poisson random measure, for and as

and the compensated Poisson measure as and then observing that

Once we have obtained the Lévy-Itô decomposition of , we can rewrite the Heston-CIR system as follows

where ,

and

Let us also recall that recursive formulae for are known:

| (4.1) | ||||

Once this is done, we proceed with the localization of the equation. Precisely, let be such that and consider for as defined in the proof of Theorem 3.4. Let then for any and

Clearly, by definition, is Lipscthiz and bounded. Concerning , we need two technical observations.

Lemma 4.2.

For any and it holds

Proof.

Fix and let us prove the first inequality. Indeed, we have

since . To prove the second inequality, just observe that , so that, since , by the well-known formula for the absolute moments of the Gaussian distribution, it holds

∎

Lemma 4.3.

For any there exist two functions such that:

-

(i)

For any and it holds

(4.2) -

(ii)

For any and it holds

(4.3) -

(iii)

For any it holds

Proof.

To prove (i), let us first observe that whenever for some . Hence we only need to work with for all .

Recalling that for any , we have

To prove (ii), let us observe that for fixed and is a Lipschitz function, hence we only need to determine an upper bound for the gradient of . Let us also stress that as for some , hence we only need to consider the case for all . By simple but cumbersome calculations, it can be shown that

Finally, item (iii) follows directly from Lemma 4.2. ∎

Now, we consider the solution of the localized equation

| (4.4) |

which exists for any since we are under the hypotheses of [4, Theorem 6.2.3]. Moreover, if we set

by pathwise uniqueness we know that for any . We also know that such solutions are cádlág. However, we first want to prove an important property of which will turn out to be useful in the following.

Theorem 4.4.

The process is stochastically continuous, i.e. for any fixed it holds .

Proof.

Remark 4.5.

Let us stress that, since for any , up to the processes and coincide, this also proves the stochastic continuity of the process up to the Markov time . By definition, it is also clear that

Hence we can conclude that , while we are not able, up to now, to prove equality. This justifies the fact that we did not use this localization technique to prove local existence for (3.1), (3.2) and (3.4) if . Indeed, our proof guarantees a local existence time that could be possibly greater than the one obtained by localization.

Now let us introduce the forward Euler-Maruyama approximation of the localized equation (4.4). Let us consider a stepsize and let for . Let us also denote and for . Then we define and, for ,

It is clear, by induction, that

We can construct a polygonal-like continuous extension of the discrete process as follows:

where if for some non-negative integer . With the exact same arguments as in Theorem 4.4 we can prove the following Lemma.

Lemma 4.6.

For any , the process is stochastically continuous.

Now, for , let us define where for some constant . It will be clear, in the following, that all the arguments are independent of the choice of , hence we can set for simplicity. We want to prove the following theorem, along the lines of [33, Theorem 2.3].

Theorem 4.7.

For any and there exists a random variable such that and

| (4.6) |

almost surely.

Now, we are ready to prove the convergence of the forward Euler-Maruyama scheme for our Heston-CIR model.

Theorem 4.8.

Let

| (4.7) |

Then is well defined up to a Markov time such that . Moreover, for almost any and there exists such that for any and

| (4.8) |

Proof.

For any with and any , let

Then, by definition of and , as . Thus we can define . Now let

| (4.6) holds for any rational and any | |||

and observe that, clearly, . Fix and . Then there exists a rational such that . However, , hence there exists such that . By Inequality (4.6) we have

| (4.9) |

In particular, this means that for any there exists such that for any

| (4.10) |

However, since , we know that for any and thus we can choose so small that Inequality (4.10) implies for any . This clearly implies that for any it holds . Finally, (4.8) is implied by (4.9) once we observe that for it holds and . ∎

4.1. Simulation

At this point, we use Theorem 4.8 to provide a simulation algorithm for the Heston-CIR model (2.1) on a grid of equidistant time points with , assuming we assign the value . Precisely, let us set so that for . Then we define by setting and then, for ,

| (4.11) |

Let us stress that such a discrete-time process can be extended to a continuous time one as in equation (4.7), thus Theorem 4.8 guarantees that for small enough is almost surely a good approximation of the values of the process in the nodes . Let us stress that for with , the quantities and are independent of each other and the same occurs for and . To simulate , we just observe that these are Gamma-distributed random variables with scale parameter and shape parameter . To simulate , we observe that, thanks to the independence of the processes and , if we consider , where the ’s are independent standard Gaussian random variables for , then .

We can rewrite the recursive relation (4.11) in terms of the four components , , and of , using also the previous observation, as follows

where

and are the components of the Cholesky factor of , as in equation (4.1).

At this point, we want to price American options numerically. Monte Carlo is a widespread method for option pricing as it can be used with any type of probability distribution. However, by construction, with Monte Carlo, it is difficult to derive the holding value (or the continuation value) at any time because that value depends on the unknown subsequent path. The research has dealt with the problem in several ways (see, for example,

[51, 21, 39], and references therein). Here we apply the Least Squares Monte Carlo simulation method (LSM) by Longstaff and Schwartz(([47],[40], [65]),

which consists of an algorithm for computing the price of an American option by stepping backward in time. Then, we compare the payoff from instant exercise with the expected payoff from continuation at any exercise time.

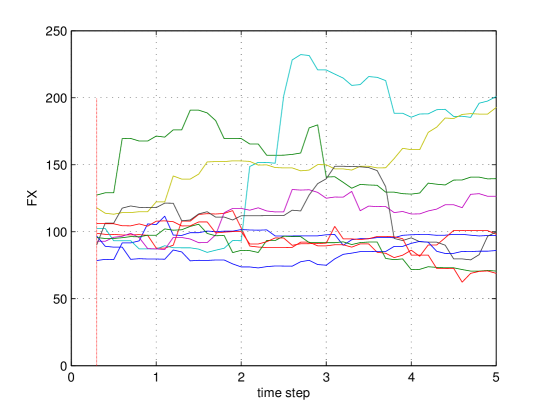

Results are displayed in Figure 1 where we show ten different paths of the asset price with parameters: , , , , time steps and .

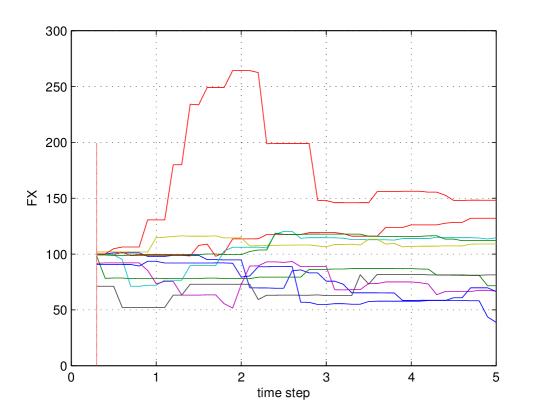

In Figure 2, we display also ten simulated paths of the asset price under Heston-CIR of VG Lévy type process for , , , , time steps.

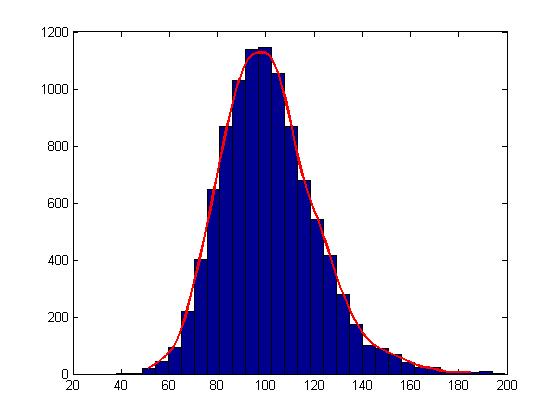

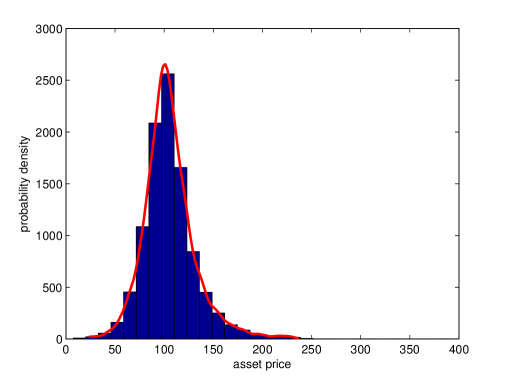

In Figures 3 and 4, we have plotted the histogram of under Heston-CIR of VG Lévy type process, with and , respectively. The scale parameter controls the kurtosis of the distribution. Therefore, raising the parameter shifts mass to the tails.

5. Dataset

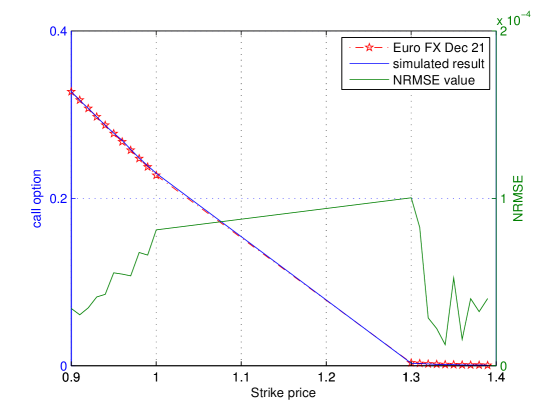

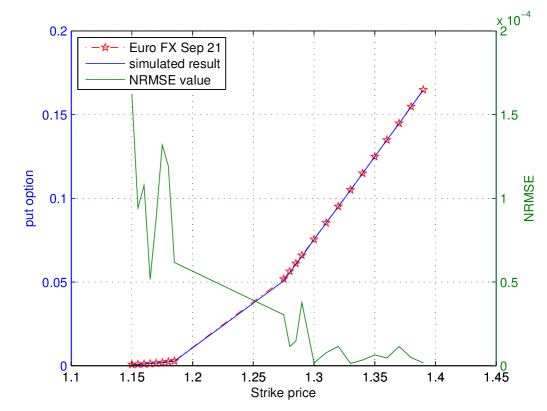

Concerning data, we retrieved interest rates and FX quotes from FRED, Federal Reserve Bank of St. Louis. In particular, the domestic rate is EURONTD156N [24] (Fig. 5), the foreign rate is USDONTD156N [73] (Fig. 6) and the FX is [22] (Fig. 7).

American options’ data were retrieved from the Chicago Mercantile Exchange (CME). Namely, on Wed, Jun 2nd, 2021, we have taken a snapshot of the following FX contracts: a) Euro FX Sep ’21 (E6U21), 36 days to expiration on 07/09/21, b) Euro FX Sep ’21 (E6U21) 92 days to expiration on 09/03/21, c) Euro FX Dec ’21 (E6Z21), 184 days to expiration on 12/03/21.

6. Results

Having discussed some stylized facts regarding returns and options’ dynamics in Section 1.5 concerning the VG models, in the following we report the results of our simulations on American options.

Note that, while the proper risk-neutral simulations can be found in Madan et al. [49, 48], here we test our approach on real data.

To demonstrate the efficiency of the LSM method, we present some tests on American put options (see also [65, 18, 23] and references therein) under Heston-CIR Lévy model. We assign the following values, , , , , , , , , , , , , , , , , and . The number of simulations is 10,000, the number of steps is and we have repeated these calculations 100 times. Tables 1, 2 and 3 present the results, where put option price, kurtosis and skewness are listed in columns and varies across rows. Note that a VG process has fat tails. As shown, the parameter is linked to the kurtosis and skewness. Therefore, allows us to control skewness and kurtosis, to obtain the peak of the distribution. Moreover, according to the simulations, the higher the strike price, the higher the price of the American put options.

| option price | kurtosis | skewness | |

|---|---|---|---|

| 2.5392 | 3.3980 | 0.5009 | |

| 2.8064 | 4.2689 | 0.6127 | |

| 4.5454 | 6.3111 | 0.8331 | |

| 4.3301 | 9.5439 | 1.0831 | |

| 4.7478 | 8.6184 | 0.9495 | |

| 4.0028 | 12.7592 | 0.8370 |

| option price | kurtosis | skewness | |

|---|---|---|---|

| 2.3797 | 3.9047 | 0.5049 | |

| 3.0896 | 4.2724 | 0.6310 | |

| 6.5128 | 7.1719 | 0.9343 | |

| 6.3791 | 10.3365 | 1.1680 | |

| 6.0814 | 11.1584 | 1.0038 | |

| 5.5649 | 17.0802 | 1.0214 |

| option price | kurtosis | skewness | |

|---|---|---|---|

| 6.7369 | 4.0933 | 0.6317 | |

| 5.3028 | 4.6504 | 0.6902 | |

| 9.4756 | 6.0042 | 0.7517 | |

| 9.2740 | 7.9159 | 0.8873 | |

| 8.6605 | 11.7784 | 0.9051 | |

| 8.7161 | 34.1771 | 2.3745 |

In Table 4, we outlined the comparison of American put option prices in the FX market estimated by the Heston-CIR model and the Heston-CIR of VG Lévy type model for different strike values . As displayed, the Lévy process has kurtosis.

| option price | kurtosis | |||

|---|---|---|---|---|

| Heston-CIR | Lévy | Heston-CIR | Lévy | |

| 2.3559 | 4.5454 | 3.9467 | 6.2111 | |

| 3.7776 | 6.5128 | 4.1502 | 10.3365 | |

| 6.7438 | 9.4756 | 3.7244 | 6.0042 |

We employ and option prices to estimate the structure parameter of the Heston-CIR of VG Lévy type model by indirect inference. In Figures 8, 9, 10, and 11 and Tables 6, 7, 8, 9, 10, 11, 12, 13 and 14 we compare the price of American put and call options written on the and with the corresponding estimated prices of the Heston-CIR of VG Lévy type model, with maturity and . The corresponding NRMSE (normalized root mean square error) has been also reported.

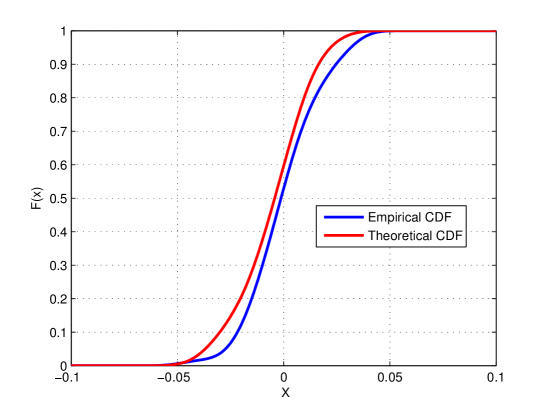

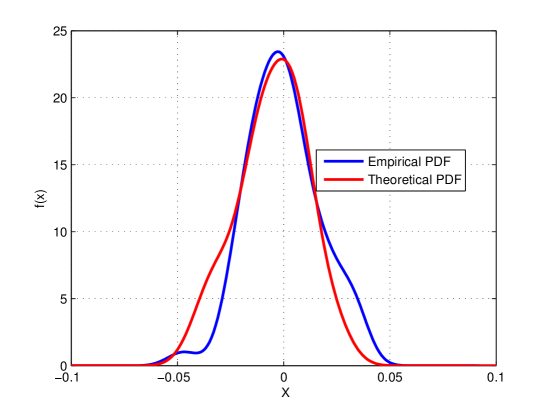

Madan and Seneta (1987) indicated a satisfactory fit of the VG process, using a Chi-square goodness-of-fit test [50, 68]. The Chi-square goodness-of-fit test is a statistical tool used to evaluate whether data are suited to the considered model. We calculate the value of the Chi-square goodness of fit test using the following formula

where is the sample size, are the observed counts and are the expected counts. We apply the Chi-square goodness-of-fit test to the FX market.

| Chi-square Lévy | Chi-square Normal | |||

|---|---|---|---|---|

| 1/12 | 2021-6-4 | 1.0245 | 0.1704 | 0.2321 |

| 1 | 9-6-2019 | 1.183 | 0.039 | 0.6803 |

| 2 | 9-6-2019 | 1.183 | 0.0141 | 1.132 |

| 5 | 4-9-2016 | 1.239 | 0.4693 | 3.218 |

In Table 5 goodness-of-fit test statistics are stated. The Heston-CIR of VG Lévy model fits the data for FX markets with low Chi-square test statistics, meaning that the distance between theoretical and empirical distributions is small.

| simulated result | market price | NRMSE | |

|---|---|---|---|

| 4.2 | 5 | 2.719 | |

| 4.0801 | 5 | 2.908 | |

| 4.782 | 5 | 2.9267 | |

| 6.31 | 5 | 4.3435 | |

| 1.0052 | 1 | 1.6836 | |

| 1.6176 | 1.5 | 2.0751 | |

| 1.83 | 2 | 2.8377 | |

| 2.5126 | 2.5 | 4.1396 |

| simulated result | market price | NRMSE | |

|---|---|---|---|

| 0.0015 | 0.0015 | 2.225 | |

| 0.0017 | 0.0017 | 1.0581 | |

| 0.002 | 0.0019 | 2.7412 | |

| 0.0024 | 0.0021 | 1.6858 | |

| 0.0025 | 0.0024 | 1.4501 | |

| 0.0027 | 0.0028 | 1.6588 | |

| 0.0031 | 0.0032 | 1.3906 | |

| 0.0032 | 0.0035 | 1.902 |

| simulated result | market price | NRMSE | |

|---|---|---|---|

| 0.1634 | 0.1631 | 1.0619 | |

| 0.1533 | 0.1532 | 1.2562 | |

| 0.1432 | 0.1433 | 3.0054 | |

| 0.1333 | 0.1335 | 2.414 | |

| 0.1234 | 0.1237 | 1.2835 | |

| 0.1136 | 0.114 | 1.4544 | |

| 0.1036 | 0.1043 | 1.4414 | |

| 0.0937 | 0.0947 | 4.632 |

| simulated result | market price | NRMSE | |

|---|---|---|---|

| 0.0853 | 0.0853 | 7.7691 | |

| 0.0754 | 0.0755 | 1.6754 | |

| 0.0651 | 0.0659 | 3.7741 | |

| 0.0606 | 0.0611 | 1.4728 | |

| 0.0557 | 0.0564 | 1.1434 | |

| 0.0507 | 0.0518 | 3.0421 | |

| 0.0023 | 0.0023 | 1.9313 | |

| 0.0027 | 0.0028 | 6.1121 |

| simulated result | market price | NRMSE | |

|---|---|---|---|

| 0.1647 | 0.1648 | 1.7288 | |

| 0.1547 | 0.1548 | 4.8363 | |

| 0.1446 | 0.1448 | 1.1436 | |

| 0.1348 | 0.1347 | 4.6565 | |

| 0.1249 | 0.1249 | 6.4369 | |

| 0.1148 | 0.1149 | 3.411 | |

| 0.1049 | 0.105 | 1.3209 | |

| 0.0949 | 0.0951 | 1.1516 |

| simulated result | market price | NRMSE | |

|---|---|---|---|

| 0.3278 | 0.3274 | 3.4218 | |

| 0.3170 | 0.3174 | 3.042 | |

| 0.3074 | 0.3074 | 3.4581 | |

| 0.2972 | 0.2974 | 4.1098 | |

| 0.2871 | 0.2874 | 4.262 | |

| 0.2778 | 0.2774 | 5.5471 | |

| 0.2691 | 0.2675 | 5.4698 | |

| 0.2584 | 0.2575 | 5.3664 |

| simulated result | market price | NRMSE | |

|---|---|---|---|

| 5.5704 | 5 | 4.0065 | |

| 7.8713 | 7 | 3.2333 | |

| 8.5784 | 8 | 4.005 | |

| 9.9123 | 0.001 | 1.5721 | |

| 0.0012 | 0.0012 | 5.2441 | |

| 0.0014 | 0.0014 | 1.2596 | |

| 0.0016 | 0.0018 | 2.2165 | |

| 0.0021 | 0.0022 | 2.8563 |

| simulated result | market price | NRMSE | |

|---|---|---|---|

| 0.3259 | 0.3253 | 1.6764 | |

| 0.3159 | 0.3153 | 7.9192 | |

| 0.3054 | 0.3053 | 4.9681 | |

| 0.2956 | 0.2953 | 8.3867 | |

| 0.2854 | 0.2853 | 1.0489 | |

| 0.2752 | 0.2753 | 5.935 | |

| 0.2653 | 0.2653 | 8.2524 | |

| 0.2553 | 0.2553 | 1.2934 |

| simulated result | market price | NRMSE | |

|---|---|---|---|

| 1.1868 | 1 | 2.4010 | |

| 1.7458 | 1 | 6.3155 | |

| 1.8853 | 1 | 9.7082 | |

| 1.5572 | 1.5 | 9.7195 | |

| 1.8542 | 2 | 2.7133 | |

| 2.2579 | 2.5 | 1.0322 | |

| 2.8955 | 3 | 1.868 | |

| 5.6845 | 4.5 | 2.9546 |

7. Conclusions

This paper, first, introduced Heston-CIR Lévy model for the FX market. The model has many positive features, for instance, through the parameters we can control tails, peaks and asymmetry.

The proof of the strong convergence of the Lévy process with stochastic domestic short interest rates, foreign short interest rates and stochastic volatility was provided.

Then the Euler-Maruyama discretization scheme was used to estimate the paths for this model. Finally, American put option for FX market under Heston-CIR Lévy process with the LSM method were priced and a test on real data was performed. The simulations prove that the chosen model fits well real-world data.

Appendix A Proof of Lemma 3.1

Proof.

Let us observe that the process is a Lévy process and is a subordinator independent of it. Then, by Phillips subordination theorem (see [66, Theorem 30.1]), is still a Lévy process. Still by [66, Theorem 30.1], we know that for any Borel set it holds

| (A.1) |

Now let us consider any couple of Borel set and and let . It is clear that

hence, without loss of generality, we can assume . Observe that

Thus, Equation (A.1) becomes

concluding the proof. ∎

Appendix B Proof of Theorem 3.2

Proof.

Let us just prove the existence and uniqueness statement for (3.1), as the other one can be proven with the same rationale. First, we need to obtain the Lévy-Itô decomposition of . To do this, let us consider the Poisson random measure of the process , defined on as

where the summation makes sense since in any interval a Lévy process admits countable (but possibly dense) jumps. Let also be the compensated Poisson random measure, where has been identified in Lemma 3.1. Recalling that , we get the Lévy-Itô decomposition (see for instance [55, Theorems 1.7-1.8])

This means that we can recast Equation (3.1) as follows.

| (B.1) |

Now let us set, for ,

and let us consider the auxiliary Equation

| (B.2) |

By direct evaluation, one can check that for any

for some constant . Indeed,

On the other hand

and then

| (B.3) | ||||

This guarantees that any solution of Equation (B.2) is non-explosive by means of Theorem [77, Theorem 2.2], since and satisfy [77, Assumption 2.1]. One can also check, still by direct evaluation, that for any it holds

| (B.4) |

for a constant . Now let us consider a sequence such that , for any and for any . Set, for any , and . It is clear that it still holds

| (B.5) |

for some constant . Let us also stress that, by Inequality (B.3),

| (B.6) |

for a suitable constant . In particular, Inequality (B.5) implies that if we consider the Equation

| (B.7) |

its strong solutions are non-explosive. Now let us show that Equation (B.2) admits at least a weak solution. For any function , we can consider the operator

Let us consider, for any and any Borel set ,

so that, by the change of variable formula (see [15, Theorem 3.6.1]),

Now let and observe that, by the change of variables formula and Inequality (B.6), we have

for some constant . Thus we are under the hypotheses of [70, Theorem 2.2] and we know that the martingale problem associated with admits a solution, which guarantees the existence of at least a weak solution of (B.7) through [46, Theorem 2.3]. Now we need to show that strong solutions of (B.7) are pathwise unique. To do this, let us first observe that for any , and any such that and it holds

| (B.8) |

where is a suitable constant independent of . Now consider a sequence such that , , as and

For such a sequence , there exists a sequence of continuous functions such that , and

Let us further define the sequence of functions

One can easily check that , , for any and, for any , and as . Now let us suppose we have two strong solutions and of Equation (B.7) and let

Then it is clear that

By the Itô formula for Lévy-Itô processes (see [4, Theorem 4.4.7]) we have

Fix any and and define

Taking the expectation and using the optional stopping theorem we get

| (B.9) | ||||

Now let us recall that while

hence

| (B.10) |

On the other hand, by Taylor’s formula with integral remainder and recalling that , it holds

Taking the integral in and recalling that we have

| (B.11) | ||||

where we also used Inequality (B.8). Thus, applying Inequalities (B.10) and (B.11) to (B.9), we get

Taking the limit as , recalling that , by the monotone convergence theorem we achieve

Now let us take , recalling that since both and are non-explosive, so that

and thus . Being both and arbitrary, we achieve the desired pathwise uniqueness. By [6, Theorem 2], this guarantees the existence of a strong solution to (B.7). Now let us define . By definition of and by the pathwise uniqueness of (B.7), it is clear that is the first exit time from of any such that . Hence we can define the following process

Again, by definition of and , such a process solves (B.2) up to for any . Let us stress that we can use the same arguments as before to guarantee pathwise uniqueness for the strong solutions of Equation (B.2) and . However, we already proved that the solutions of Equation (B.2) are non-explosive, thus as , implying that is the pathwise unique global strong solution of (B.2). Now let and observe that, for , we can rewrite (B.2) as (B.1). Recalling that is a cádlág process, it is clear that . Hence is a strong solution of (B.1) up to . Finally, to guarantee pathwise uniqueness of , let us consider any other strong solution of (B.1) up to a stoppin time with , let us consider the global solution of (B.2). Then, both and are solutions of (B.2) up to and thus, by pathwise uniqueness, they coincide. This also implies that , concluding the proof. ∎

Appendix C Proof of Theorem 3.4

Proof.

If , then existence and uniqueness is proven analogously as in Theorem 3.2.

Let us consider the case . As in Theorem 3.2, let us find the Lévy-Itô decomposition of . Indeed, if we consider its Poisson random measure, defined for and as

and its compensated version , where is the Lévy measure of identified by Lemma 3.3, it holds

and then we can rewrite Equations (3.5) and (3.6) as

| (C.1) | |||||

| (C.2) | |||||

Now let and be as in the proof of Theorem 3.2 and define, for and ,

Consider the auxiliary equations

| (C.3) | |||||

| (C.4) | |||||

As in Theorem 3.2, one can prove by direct evaluation (and by means of Young’s inequality with exponents and to handle ) that for any it holds

where is a suitable constant, which guarantees, by means of [77, Theorem 2.2], that the strong solutions of (C.3) and (C.4) (and thus also the strong solutions of (C.1) and (C.2)) are non-explosive.

Now we need to distinguish among the two cases and .

In the case , once we observe that there exists a constant such that for any

we can proceed as in Theorem 3.2 by defining for any

where for any it holds . The only real difference concerns the proof of the pathwise uniqueness for Equations

| (C.5) | ||||

| (C.6) |

Indeed, once we consider two pairs and of strong solutions of Equations (C.5) and (C.6) and we define

we can observe that Equation (C.5) coincides with Equation (B.7) and then almost surely by the pathwise uniqueness proved in Theorem 3.2. Thus, being almost surely, one can easily check that, defining

it holds

Once this is clear, the same arguments as in Theorem 3.2 conclude the proof in the case .

Now let us handle the case . Fix big enough to have . For any consider a function such that for any , for any and . Let us also denote for any .

This time we define

and the auxiliary SDEs

| (C.7) | ||||

| (C.8) |

By direct evaluation, one can check that there exists a constant such that for any it holds.

Moreover, by definition, it is clear that is Lipschitz (since it belongs to and its gradient is bounded by the definition of ). For the same reason, for any and , also is a a Lipschitz function and one can prove, by direct evaluation of the supremum of the gradient, that there exists a constant such that for any and it holds

Hence, we know that there exists a constant such that for any it holds

Hence we are under the classical Lipschitz and sublinear growth hypotheses and by [4, Theorem 6.2.3] there exists a pathwise unique strong solution to Equations (C.7) and (C.8). Now let us define the sequence of Markov times

and observe that, as , solves Equation (C.1) and thus it coincides with by pathwise uniqueness. On the other hand, let us also observe that for and solve the same equation up to , where

By pathwise uniqueness, we know that up to and thus, as a consequence, . This implies that is an increasing sequence of Markov times and then we can define the Markov time . Moreover, for any , one can define

However, since for , actually solves Equation (C.2). Moreover, if is another strong solution of (C.2) and we consider

then solves also (C.8) up to . This implies that up to and thus . Thus, in particular, and we have that is the unique pathwise solution of (C.2) up to . ∎

Appendix D Proof of Theorem 4.7

Proof.

Let us observe that for any and any it holds

By the Itô formula for Lévy-Itô processes and some simple algebraic manipulations we have

where we set

Let us observe that, by the fact that is Lipschitz and bounded and by Lemma 4.3, it holds

where we also used Cauchy-Schwartz and Young’s inequality. Now let and observe that, by applying Jensen’s inequality, taking the supremum and then the expectation and finally applying Kunita’s first inequality and Lemma 4.3, it holds

| (D.1) | ||||

Now let us estimate . By stochastic continuity of , we know that and almost surely. Moreover, we have

and then, by using the fact that is bounded, Lemma 4.3 and Jensen’s inequality, we achieve

Again, by Kunita’s first inequality, Lemma 4.3 and Jensen’s inequality holds

Using the latter inequality into Inequality (D.1) we have

which, in turn, by Grönwall’s inequality implies

Now consider any and use Markov’s inequality to remark that

Recalling that , we can always choose so that . With such a choice, it holds

The Borel-Cantelli Lemma concludes the proof. ∎

References

- [1] Ahlip, R. and Rutkowski, M. (2013). Pricing of foreign exchange options under the Heston stochastic volatility model and CIR interest rates. J. Quantitative Finance, 13(6):955-966.

- [2] Akgiray, V. Booth, G. G. (1988). Mixed diffusion-jump process modeling of exchange rate movements. J. Economics and Statistics.

- [3] Asmussen, S., Glynn P. W. (2007). Stochastic simulation: algorithms and analysis. Vol. 57. New York: Springer.

- [4] Applebaum, D. (2009). Lévy processes and stochastic calculus. Cambridge University Press.

- [5] 1997, Bakshi, G., Cao, C., Chen, Z. (1997). Empirical performance of alternative option pricing models. J. finance.

- [6] Barczy, M., Li Z., Pap G. (2015). Yamada-Watanabe results for stochastic differential equations with jumps. International Journal of Stochastic Analysis 2015.

- [7] Barndorff-Nielsen, O. E. and Shephard, N. (2001). Non-Gaussian Ornstein-Uhlenbeck based models and some of their uses in financial economics (with discussion). J. Roy. Statist. Soc., Ser. B. 63 167-241.

- [8] Barndorff-Nielsen, Ole. (1977). Exponentially decreasing distributions for the logarithm of particle size. J. Mathematical and Physical Sciences.

- [9] Barndorff-Nielsen, O. (1997). Normal Inverse Gaussian Distributions and Stochastic Volatility Modelling, Scandinavian. Statistics.

- [10] Barone-Adesi, G. (2005). The saga of the American put. J. Banking & Finance.

- [11] Bates, D. S. (1996). Jumps and stochastic volatility: The exchange rate processes implicit in deutsche mark options, Rev. Financ. Stud. 9, 69-107.

- [12] Barndorff-Nielsen, O. E., Mikosch, T. Resnick, S. I. (2013). Lévy Processes, Theory and Applications, Birkhauser.

- [13] Benhamou, E., Gobet, E. and Miri, M. (2010). Time dependent Heston model, SIAM J. Financ. Math. 1, 289-325.

- [14] Bertoin, J. (1999) Subordinators: examples and applications. Lectures on probability theory and statistics. Springer, Berlin, Heidelberg. 1-91.

- [15] Bogachev, V. I. (2007) Measure theory. Vol. 1. Berlin: Springer.

- [16] Boyarchenko, S. I. and Levendorskii, S. Z. (2002). Perpetual American options under Lévy processes. SIAM J. Control Optim.401663–1696

- [17] Braunstein, A. (2008). American Option Approximations. [Online; accessed 5. Aug. 2019].

- [18] Broadie, M. Glasserman, P. (1997). Pricing American-style securities using simulation. Economic Dynamics and Control.

- [19] Bunch, D.S., Johnson, H. (1992). A Simple and Numerically Efficient Valuation Method for American Puts Using a Modified Geske-Johnson Approach. J. Finance.

- [20] Campa, JM., Chang, PHK., Reide,r RL. (1998). Implied exchange rate distributions: evidence from OTC option markets. J. international Money and Finance.

- [21] Carriere, Jacques F. (1996). Valuation of the early-exercise price for options using simulations and nonparametric regression. Mathematics and Economics.

- [22] Board of Governors of the Federal Reserve System (US). (2021). U.S./ Euro Foreign Exchange Rate [DEXUSEU]. https://fred.stlouisfed.org/series/DEXUSEU. Online; accessed 7 June 2021.

- [23] Dorbov, B. (2015). Monte Carlo Simulation with Machine Learning for Pricing American Options and Convertible Bonds. SSRN Electronic.

- [24] ICE Benchmark Administration Limited. (2021). Overnight London Interbank Offered Rate (LIBOR), based on Euro [EURONTD156N]. https://fred.stlouisfed.org/series/EURONTD156N , Online; accessed 7 June 2021.

- [25] Fallah, L. Najafi, A. R. Mehrdoust, F. (2018). A fractional version of the Cox-Ingersoll-Ross interest rate model and pricing double barrier option with Hurst index , Communications in Statistics. Theory and Methods

- [26] Fama, F. Eugene,. (1965). The behavior of stock-market prices. journal of Business.

- [27] Friz, P. K., Zhang H. (2018). Differential equations driven by rough paths with jumps. Journal of Differential Equations 264.10: 6226-6301.

- [28] Fu, Z., Li Z. (2010). Stochastic equations of non-negative processes with jumps. Stochastic Processes and their Applications 120.3: 306-330.

- [29] Grzelak, L. A. Oosterlee, C. W. (2011). On the Heston model with stochastic interestrates. SIAM Journal on Financial Mathematics, 2:255-286.

- [30] Grzelak, L. A.Oosterlee, C. W. (2012). An Equity-Interest Rate hybrid model with Stochastic Volatility and the interest rate smile. Computational Finance.

- [31] Grzelak, L. A. and C. W. Oosterlee. (2012). On Cross-Currency Models with StochasticVolatility and Correlated Interest Rates. Applied Mathematical Finance.

- [32] Grant, D. Vora, G. Weeks, D. (1997). Simulation and the Early Exercise Option Problem. J. Financial Engineering.

- [33] Gyöngy, I. (1998) A note on Euler’s approximations. Potential Analysis 8.3: 205-216.

- [34] Higham, D. J., (2004). An introduction to financial option valuation. United States of America by Cambridge University Press, New York.

- [35] Horn, R. A., Johnson, C. R., (2012). Matrix analysis. Cambridge University Press.

- [36] Higham,D. J. Mao, X. Stuart, A. M., (2003). Exponential mean square stability of numericalsolutions to stochastic differential equations, London Mathematical Society J. Comput. and Math.

- [37] Hull, J., White, A. (1987). The pricing of options on assets with stochastic volatilities. J. Finance 42 281-300.

- [38] Heston, S. L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options, Rev. Financ. Stud. 6, 327-343.

- [39] Huang, J. Subrahmanyam, M. G., George, Y. G. (1996). Pricing and Hedging American Options: A Recursive Integration Method. J. Financial Studies.

- [40] Kavacs, B., (2012). American option pricing with LSM algorithm and analytic bias correction, 12-13.

- [41] Kienitz, J., Wetteran, D., (2012). Financial modelling, Springer.

- [42] Kim, B. J., Ma, YK., Choe, HJ. (2013). A Simple Numerical Method for Pricing an American Put Option. J. Appl. Math.

- [43] Kim, P., Song ,R., Vondraček, Z. (2012). Potential theory of subordinate Brownian motions revisited. Stochastic analysis and applications to finance: Essays in honour of Jia-an Yan. 243-290.

- [44] Kou, S. G. (2002). A Jump-Diffusion Model for Option Pricing. Management Science, 48, 1086-1101.

- [45] Kou, S. G. (2008). Jump Diffusion Models for Asset Pricing in Financial Engineering. In Handbooks in OR and MS, Vol, 15, Ch. 2, edited by J. Birge and V. Linetsky, Elsevier.

- [46] Kurtz, T. G. (2011) Equivalence of stochastic equations and martingale problems, Stochastic analysis 2010. Springer, Berlin, Heidelberg: 113-130.

- [47] Longstaff, F. A.,Schwartz, E. S., (2001). Valuing American options by simulation: a simple least-squares approach, Rev. Financ. Stud. 14 (1). 113-147.

- [48] Madan, D. B., Seneta, E., (1990). The V. G. Model for Share Market Returns. J. Business. 63, 511-524.

- [49] Madan, D. B., Carr, P., Chang, E. C., (1998) The Variance Gamma Process and Option Pricing. Review of Finance, 79–105.

- [50] Madan. D. B. Seneta. E., (1987). Chebyshev Polynomial Approximations and Characteristic Function Estimation. J. Royal Statistical Society B, 49: 163-169.

- [51] Margrabe, W. (1978). The value of an option to exchange one asset for another. J. Finance.

- [52] Merton, R. C. (1976). Option pricing when underlying stock returns are discontinuous. J. of Financial Economics. Vol. 3, 125-144.

- [53] Mikhailov, S. and Nogel, U. (2003). Heston’s stochastic volatility model: Implementation, calibration and some extensions, Wilmott J. 7, 74-79.

- [54] Muthuraman, K., Kuma, S. (2008). Solving Free-boundary Problems with Applications in Finance. J. Found. Trends. Stoch. Sys.

- [55] Oksendal, B. and Sulem,A. (2004). Applied Stochastic Control of Jump Diffusions.

- [56] Orlando, G. Mininni, R. Bufalo, M. (2018). A New Approach to CIR Short Term Rates Modelling. New Methods in Fixed Income Modeling.

- [57] Orlando, G. Mininni, R. Bufalo, M. (2019). Interest rates calibration with a CIR model. Journal of Risk Finance.

- [58] Orlando, G. Mininni, R. Bufalo, M. (2019). A New Approach to Forecast Market Interest Rates Through the CIR Model. Studies in Economics and Finance.

- [59] Orlando, G. Mininni, R. Bufalo, M. (2019). Forecasting interest rates through Vasicek and CIR models: a partitioning approach. Journal of Forecasting.

- [60] Owen, J. Ramon, R. (1983). On the class of elliptical distributions and their applications to the theory of portfolio choice. The Journal of Finance.

- [61] Nunno, D, G. Oksendal, and B. Proske, F. (2008). Malliavin Calculus for Lévy Processes with Applications to Finance.

- [62] Robert, A., van de Geijn, (2011). Notes on Cholesky Factorization. The University of Texas, Austin.

- [63] Rubinstein,M. (1978). Nonparametric tests of alternative option pricing models using all reported trades and quotes on the 30 most active CBOE option classes from August 23, 1976 through August 31, 1978. J. Finance.

- [64] 1994, Rubinstein,M. (1994). Implied binomial trees. J. finance.

- [65] Samimi, O., Mardani, Z., Sharafpour, S., Mehrdoust, F. (2016). LSM Algorithm for Pricing American Option Under Heston-Hull-White’s Stochastic Volatility Model. Computational Economics.

- [66] Sato, K.-I. (1999). Lévy processes and infinitely divisible distributions. Cambridge University Press.

- [67] Steven, E. (2000). Shreve, Stochastic Calculus for Finance, Springer finance series.

- [68] Stephens, M.A., (1974). EDF Statistics for Goodness of Fit and Some Comparisons. J. American Statistical Association, 69: 730-737

- [69] Stein, E., & Stein, J. (1991). Stock Price Distributions with Stochastic Volatility: an Analytic Approach. Review of financial studies.

- [70] Stroock, D. W. (1975). Diffusion processes associated with Lévy generators. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete 32.3: 209-244.

- [71] Teng, L., Ehrhardt, M. and Gunther, M. (2014). The dynamic Correlation model and its application to the Heston model, Preprint 14/09, University of Wuppertal.

- [72] Tsitsiklis, J. N. Fellow, Van, R. B . (2001). Regression Methods for Pricing Complex American-Style Options. IEEE.

- [73] ICE Benchmark Administration Limited (IBA).(2021). Overnight London Interbank Offered Rate (LIBOR), based on U.S. Dollar [USDONTD156N]. https://fred.stlouisfed.org/series/USDONTD156N. Online; accessed 7 June 2021.

- [74] Teng, L., Ehrhardt, M. and Gunther, M. (2014). The dynamic Correlation model and its application to the Heston model, Preprint 14/09, University of Wuppertal.

- [75] van Haastrecht, A., and Pelsser, A. (2011). Generic pricing of FX, inflation and stock options under stochastic interest rates and stochastic volatility. Quantitative Finance, 11(5), 665–691. doi: 10.1080/14697688.2010.504734

- [76] Van, H., Pelsser, A. (2011). Generic pricing of FX, inflation and stock options under stochastic interest rates and stochastic volatility. Quantitative Finance, 11(5):665-691.

- [77] Xi, F., Zhu C. (2019). Jump type stochastic differential equations with non-Lipschitz coefficients: non-confluence, Feller and strong Feller properties, and exponential ergodicity. Journal of Differential Equations 266.8: 4668-4711.

- [78] We, L. Kwok, Y. K. (1997). A front-fixing finite difference method for the valuation of American options. J. Financial Engineering.