Graphical tools for selecting conditional instrumental sets

Abstract

We consider the efficient estimation of total causal effects in the presence of unmeasured confounding using conditional instrumental sets. Specifically, we consider the two-stage least squares estimator in the setting of a linear structural equation model with correlated errors that is compatible with a known acyclic directed mixed graph. To set the stage for our results, we characterize the class of linearly valid conditional instrumental sets that yield consistent two-stage least squares estimators for the target total effect and derive a new asymptotic variance formula for these estimators. Equipped with these results, we provide three graphical tools for selecting more efficient linearly valid conditional instrumental sets. First, a graphical criterion that for certain pairs of linearly valid conditional instrumental sets identifies which of the two corresponding estimators has the smaller asymptotic variance. Second, an algorithm that greedily adds covariates that reduce the asymptotic variance to a given linearly valid conditional instrumental set. Third, a linearly valid conditional instrumental set for which the corresponding estimator has the smallest asymptotic variance that can be ensured with a graphical criterion.

1 Introduction

Suppose we want to estimate the total causal effect of an exposure on an outcome in the presence of latent confounding. This is often done with instrumental variable estimators. A popular instrumental variable estimator is the two-stage least squares estimator which has attractive statistical properties for linear models (Vansteelandt and Didelez,, 2018), such as being asymptotically efficient among a broad class of estimators for Gaussian linear structural equation models (Chapter 5, Wooldridge,, 2010). The two-stage least squares estimator is computed based on a tuple of covariate sets, where we call the instrumental set, the conditioning set and the conditional instrumental set. It is well-known that the two-stage least squares estimator is only consistent if we use certain tuples and we call such tuples valid conditional instrumental sets relative to . Determining which conditional instrumental sets are valid has received considerable research attention (e.g. Bowden and Turkington,, 1990; Angrist et al.,, 1996; Hernán and Robins,, 2006; Wooldridge,, 2010). In the graphical framework and for linear structural equation models, the setting we adopt in this paper, the most relevant results are by Brito and Pearl, 2002b and Pearl, (2009) who have proposed a necessary graphical criterion for a conditional instrumental set to be linearly valid, i.e., valid for linear structural equation models.

Besides validity, there is another aspect to this problem that has received less attention: the choice of the conditional instrumental set also affects the estimator’s statistical efficiency. While in some cases no linearly valid conditional instrumental set may exist, in other cases multiple linearly valid tuples may be available. In such cases, each linearly valid tuple leads to a consistent estimator of the total effect but the respective estimators may differ in terms of their asymptotic variance. This raises the following question: can we identify tuples that lead to estimators that are more efficient than others? This is an important problem, as it is well-known that the two-stage least squares estimator can suffer from low efficiency (Kinal,, 1980).

It is known that increasing the number of instruments, i.e., enlarging , can only improve the asymptotic variance (e.g. Wooldridge,, 2010, Chapter 5). However, this may also increase the finite sample bias (Bekker,, 1994). A related result that does not suffer from this drawback is given by Kuroki and Cai, (2004). They provide a graphical criterion that can identify in some cases which of two tuples and provides a more efficient estimator. However, this result is limited to singletons and with a fixed conditioning set . The selection of the conditioning set has received even less attention. The only result we are aware of is by Vansteelandt and Didelez, (2018), who establish that if a set is independent of the instrumental set then using rather than cannot harm the efficiency and may improve it. There are no results for pairs where both the instrumental set and the conditioning set differ.

There exists a similar problem in the setting without latent confounding that has received more research attention. In this setting and under a linearity assumption, it is possible to estimate the target total effect by using the ordinary least squares estimator adjusted for a valid adjustment set. There have been a series of more and more general graphical criteria to compare pairs of adjustment sets in terms of the asymptotic variance of the corresponding estimators (Kuroki and Miyakawa,, 2003; Kuroki and Cai,, 2004; Henckel et al.,, 2022). These advances have allowed Henckel et al., (2022) to graphically characterize an adjustment set guaranteed to attain the optimal asymptotic variance among all valid adjustment sets in causal linear models. Rotnitzky and Smucler, (2020) show that this result also holds for a large class of non-parametric estimators (see also Rotnitzky and Smucler,, 2022; Guo et al.,, 2022). Runge, (2021) and Smucler et al., (2022) provide conditions under which this result generalizes to settings with latent variables, although they do assume that at least one valid adjustment set is observed.

In this paper we aim to fill the gap between the growing literature on selecting adjustment sets and the more limited literature on conditional instrumental sets. We consider the setting of a linear structural equation model with correlated errors that is compatible with a known acyclic directed mixed graph. To set the stage for our results, we first derive a necessary and sufficient graphical condition for a conditional instrumental set to be linearly valid. Moreover, we derive a new formula for the asymptotic variance of the two-stage least squares estimator. This formula only holds for linearly valid conditional instrumental sets but has a simpler dependence on the conditional instrumental set and the underlying graph compared to the traditional formula.

Equipped with these two results, we provide three graphical tools to select more efficient conditional instrumental sets. The first result is a graphical criterion that for certain pairs of linearly valid conditional instrumental sets identifies which of the two corresponding estimators has the smaller asymptotic variance. This criterion includes the results by Kuroki and Cai, (2004) and Vansteelandt and Didelez, (2018) as special cases. It is also the first criterion that can compare pairs of linearly valid tuples where both the instrumental set and the conditioning set differ. This tool also forms the theoretical foundation for our other two tools. The second result is an algorithm that takes any linearly valid conditional instrumental set and greedily adds covariates that decrease the asymptotic variance, while preserving validity. We also use the basic principle underlying our algorithm to propose a simple, intuitive guideline for practitioners on how to select a more efficient tuple when the underlying causal structure is not fully known. The third result is the graphical characterization of a conditional instrumental set that, given mild constraints, is linearly valid and for which the corresponding estimator has the smallest asymptotic variance we can ensure with a graphical criterion; a property we formally define and call graphical optimality.

Lastly, we provide a simulation study to quantify the gains that can be expected from applying our results in practice. We also illustrate our results on the settler-mortality data set by Acemoglu et al., (2001) in order to more efficiently estimate the effect of a country’s institutions on its economic wealth. All proofs are provided in the Supplementary Material.

2 Preliminaries

We consider acyclic directed mixed graphs where nodes represent random variables, directed edges represent direct effects and bi-directed edges represent error correlations induced by latent variables. We now give the most important definitions. The remaining ones together with an illustrating example are given in Section A.2 of the Supplementary Material.

Notation: We generally use to denote sets but we drop the brackets around singletons to ease the notation. For the same reason we use lowercase letters in sub- and superscripts.

Linear structural equation model: Consider an acyclic directed mixed graph , with nodes and edges , where the nodes represent random variables. A random vector is said to be generated from a linear structural equation model compatible with if

| (1) |

such that the following three properties hold: First, is a matrix with for all where . Second, is a random vector of errors such that and is a matrix with for all where . Third, for any two disjoint sets such that for all and all , , the random vector is independent of .

We use the symbol in equation (1) to emphasize that it is interpreted as a generating mechanism rather than just an equality. As a result we can use it to identify the effect of an outside intervention that sets a treatment to a value uniformly for the entire population. Such interventions are typically called do-interventions and denoted (Pearl,, 1995). The edge coefficient is also called the direct effect of on with respect to . The non-zero error covariances can be interpreted as the effect of latent variables.

Causal paths and forbidden nodes: A path from to in is called a causal path from to if all edges on are directed towards . The descendants of in are all nodes such that there exists a causal path from to in and the set of descendants is denoted by . We use the convention that . Moreover, for a set we let . The causal nodes with respect to in are all nodes on causal paths from to excluding and they are denoted by . We define the forbidden nodes relative to in as .

Total effects: We define the total effect of on at as

In a linear structural equation model the function is constant, which is why we simply write . The path tracing rules by Wright, (1934) allow for the following alternative definition. Consider two nodes and in an acyclic directed mixed graph and suppose that is generated from a linear structural equation model compatible with . Then is the sum over all causal paths from to of the product of the edge coefficients along each such path.

Two-stage least squares estimator: (Basmann,, 1957) Consider two random variables and , and two random vectors and . Let and be the random matrices corresponding to i.i.d. observations from the random vectors , and , respectively. Then the two-stage least squares estimator is defined as the first entry of

| (2) |

where we omit the dependence on the sample size for simplicity and let denote the population level version of . The estimator is also commonly written as

where is the symmetric and idempotent hat matrix from an ordinary least squares regression on . This notation emphasizes that we can also obtain by regressing on obtaining the fitted values and then regressing on ; hence the name two-stage least squares estimator.

Latent projection and m-separation: (Koster,, 1999; Richardson,, 2003) Consider an acyclic directed mixed graph , with generated from a linear structural equation model compatible with . We can read off conditional independence relationships between the variables in directly from with a graphical criterion known as m-separation. A formal definition is given in the Supplementary Material. We use the notation to denote that is m-separated from given in . We use the convention that holds for any and .

Consider a subset of nodes . We can use a tool called the latent projection (Richardson,, 2003) to remove the nodes in from while preserving all m-separation statements between subsets of . We use the notation to denote the acyclic directed mixed graph with node set that is the latent projection of over . A formal definition of the latent projection is given in the Supplementary Material.

Covariance matrices and regression coefficients: Consider random vectors and . We denote the population level covariance matrix of by and the covariance matrix between and by , where its -th element equals . We further define . If , we write instead of . The value can be interpreted as the residual variance of the ordinary least squares regression of on . We also refer to as the conditional variance of given . Let represent the population level least squares coefficient matrix whose -th element is the regression coefficient of in the regression of on and . We denote the corresponding estimator by . Finally, for random vectors with we use the notation that and .

Adjustment sets: (Shpitser et al.,, 2010; Perković et al.,, 2018) A node set is a valid adjustment set relative to in , if for all linear structural equation models compatible with . There exists a necessary and sufficient graphical criterion for a set to be a valid adjustment set, which can be found in the Supplementary Material.

3 Linearly valid conditional instrumental sets

In this section, we graphically characterize the class of conditional instrumental sets such that the two-stage least squares estimator is consistent for the total effect in linear structural equation models.

Definition 3.1.

Consider disjoint nodes and , and node sets and in an acyclic directed mixed graph . We refer to as a linearly valid conditional instrumental set relative to in if the following hold: (i) there exists a linear structural equation model compatible with such that and (ii) for all linear structural equation models compatible with such that , the two-stage least squares estimator converges in probability to .

Condition (i) of Definition 3.1 ensures that Condition (ii) is not void. In graphical terms, it corresponds to requiring that . Condition (ii) then ensures that if , which can be checked with observational data, the two-stage least squares estimator is consistent for the total effect . If , the estimator is generally inconsistent and has non-standard asymptotic theory (Staiger and Stock,, 1997), which is why we do not consider this case. In finite samples, a non-zero but small is also problematic due to weak instrument bias (Bound et al.,, 1995; Stock et al.,, 2002) but since we only consider the asymptotic regime this is not relevant for our results. We now provide a graphical characterization for the class of linearly valid conditional instrumental sets.

Theorem 3.2.

Consider disjoint nodes and , and node sets and in an acyclic directed mixed graph . Then is a linearly valid conditional instrumental set relative to in if and only if (i) , (ii) and (iii) , where the graph is with all edges out of on causal paths from to removed.

The graphical criterion in Theorem 3.2 is similar to the well-known graphical criterion from Pearl, (2009) (see also Brito and Pearl, 2002a, ; Brito and Pearl, 2002b, ). In fact the two are equivalent for any triple with no causal path from to in except for the edge . The main contribution of Theorem 3.2 is that it gives a necessary and sufficient criterion for general graphs.

By Condition (i) of Theorem 3.2, a linearly valid conditional instrumental set may not contain nodes in . We can therefore use the latent projection and remove the nodes in from to obtain the smaller graph , without loosing any relevant information, i.e., we treat them as unobserved even if we did in fact observe them. This is an example of the forbidden projection originally proposed by Witte et al., (2020) in the context of adjustment sets. We formalize this result in the following proposition.

Proposition 3.3.

Consider nodes and in an acyclic directed mixed graph and let . Then is a linearly valid conditional instrumental set relative to in if and only if it is a linearly valid conditional instrumental set relative to in .

We now provide an additional proposition regarding the remaining descendants of .

Proposition 3.4.

Consider nodes and in an acyclic directed mixed graph and let be a linearly valid conditional instrumental set relative to in . If , then is a valid adjustment set relative to in .

Proposition 3.4 implies that whenever we may use descendants of in the conditional instrumental set, we can also use covariate adjustment to estimate , that is, use the ordinary least squares estimator. As the latter is known to be a more efficient estimator than the two-stage least squares estimator (e.g. Chapter 5.2.3 of Wooldridge,, 2010, Section D.2 of the Supplementary Material), we disregard such cases and apply the latent projection to also marginalize out any remaining variables in . We also assume that as otherwise by default. We summarize our assumptions in a remark at the end of this section.

Example 3.5 (Linearly valid conditional instrumental sets).

We now characterize all linearly valid conditional instrumental sets relative to in the graph from Figure 1a using Theorem 3.2. First, and . By Condition (i), we therefore only need to consider sets and that are subsets of .

We first consider potential instrumental sets . Since for all , no may contain or we have a violation of Condition (iii). This means we have seven candidates for and . We now consider the potential conditioning sets corresponding to each of these seven candidates.

Consider first the four candidate instrumental sets and . Letting be any of these sets, it holds that for all . Therefore Condition (ii) holds irrespective of . Further, with if and only if . Therefore, Condition (iii) holds and is a linearly valid conditional instrumental set if an only if . The conditioning sets for are therefore and , for they are and , for they are and , and for there is only .

Consider now the two candidate instrumental sets and . Letting be either of these two sets, it holds that for all and therefore Condition (ii) holds irrespective of . Further, with if and only if or . Therefore, Condition (iii) holds and is a linearly valid conditional instrumental set if and only if or . The conditioning sets for are therefore and , while for they are and .

Finally consider the case . It holds that for if and only if and therefore Condition (ii) holds if and only if . Further, given any with , if and only if or . The conditioning sets for are therefore and . In total there are therefore linearly valid conditional instrumental sets (see Table 3 in the Supplementary Material).

Consider now the graph from Figure 1b. It is the forbidden projection graph with . It is easy to verify that the arguments we gave for also apply to and therefore every linearly valid conditional instrumental set relative to in is also a linearly valid conditional instrumental set relative to in and vice versa.

Remark 3.6.

For the remainder of this paper we consider graphs such that . The graph then simply equals the graph with the edge removed.

4 Efficient and linearly valid conditional instrumental sets

4.1 Asymptotic variance formula for linearly valid conditional instrumental sets

We present a new formula for the asymptotic variance of the two-stage least squares estimator, in terms of three conditional variances, that is, terms of the form as defined in Section 2. The new formula has a simpler dependence on the tuple than the traditional formula (see Equation (4) below), but it only holds if the tuple is a linearly valid conditional instrumental set.

Theorem 4.1.

Consider nodes and in an acyclic directed mixed graph such that . Let be a linearly valid conditional instrumental set relative to in and . Then for all linear structural equation models compatible with such that , is an asymptotically normal estimator of with asymptotic variance

| (3) |

The new formula in Equation (3) differs in two ways from the traditional asymptotic variance formula which is

| (4) |

where and is the population level residual variance of the estimator defined in Section 2. The first difference is that in Equation (3) the residual variance from Equation (4) is replaced by the conditional variance of the oracle random variable on . This is possible because under the assumption that is a linearly valid conditional instrumental set, we have . The advantage of this change is that it is easier to describe how the term behaves as a function of the tuple than . For example, it is immediately clear that depends on only via . We refer to the numerator of Equation , , as the residual variance of the estimator or, when is clear, of the tuple .

The second change is that in Equation (3) the denominator from Equation (4) is replaced with the difference . The difference measures how much the residual variance of on decreases when we add to the conditioning set. Intuitively, this is the information on that contains and which was not already contained in . Based on this intuition, we refer to the denominator of Equation (3), , as the conditional instrumental strength of the estimator or, when is clear, of .

Another important contribution of Theorem 4.1 is that it also holds for linear structural equation models with non-Gaussian errors. This is a non-trivial result, because Equation (4) is usually derived under a homoscedasticity assumption on the residuals , which generally does not hold if the errors in the underlying linear structural equation model are non-Gaussian. However, in our proof we show that if is a linearly valid conditional instrumental set, Equations (3) and (4) hold, even if the residuals are heteroskedastic.

Finally, the new asymptotic variance formula elegantly mirrors the ordinary least squares asymptotic variance formula . We can use this to illustrate how the two-stage least squares estimator is less efficient than the ordinary least squares estimator. We discuss this further in Section D.2 of the Supplementary Material.

4.2 Comparing pairs of linearly valid conditional instrumental sets

We derive a graphical criterion that, for certain pairs of linearly valid conditional instrumental sets, identifies which of the two corresponding estimators has the smaller asymptotic variance.

Theorem 4.2.

Consider nodes and in an acyclic directed mixed graph such that . Let and be linearly valid conditional instrumental sets relative to in . Let and . If

| (a) | |||

| (b) | |||

| (c) | |||

| (d) |

then for all linear structural equation models compatible with such that ,

Theorem 4.2 is more general in terms of the linearly valid conditional instrumental sets it can compare, than the results by Kuroki and Cai, (2004) and Vansteelandt and Didelez, (2018). In particular, it can compare tuples and with and .

As a result, the graphical condition of Theorem 4.2 is, however, rather complex. For easier intuition, we can think of it as consisting of two separate parts. Condition (a) verifies that may not provide a smaller residual variance than , that is, . It does so by checking that the covariates in do not reduce the residual variance of the oracle random variable . Because is not a node in but can be thought of as the node in the graph , this requires checking an m-separation statement in . Conditions (b–d) jointly verify that may not provide a larger conditional instrumental strength than , that is, . This requires three conditions because we need to verify in turn that (i) the covariates in do not increase, (ii) the nodes in do not decrease and (iii) the nodes in do not increase the conditional instrumental strength.

Theorem 4.2 also simplifies whenever , or . In the first case, and therefore Conditions (a) and (b) are void. In the second case, and therefore Condition (c) is void. In the third case, and therefore Condition (d) is void. If and all four conditions are void. Therefore, the well-known result that adding covariates to the instrumental set is beneficial for the asymptotic variance (e.g. Chapter 12.17 of Hansen,, 2022) is a corollary of Theorem 4.2. We formally state it for completeness.

Corollary 4.3.

Consider nodes and in an acyclic directed mixed graph such that . Let and be linearly valid conditional instrumental sets relative to in . If and , then for all linear structural equation models compatible with such that ,

Theorem 4.2 also gives interesting new insights. We first discuss the special case with fixed and only varying. Here, the most important insight is that there exists a class of covariates that practitioners should avoid adding to because they increase the asymptotic variance. We now illustrate this class along with other consequences in a series of examples.

Example 4.4 (Harmful conditioning).

Consider the graph from Fig. 2a. We are interested in estimating with conditional instrumental sets of the form , where . Since , and for all , all tuples of this form are linearly valid conditional instrumental sets relative to in .

Let and . As and , we can apply Theorem 3 with and (Conditions (a) and (b) (ii) hold, Conditions (c) and (d) are void). We can therefore conclude that adding to any can only increase the asymptotic variance.

Conditioning on is harmful, because and but . Therefore, and but . The node is representative of a larger class of covariates that we should avoid conditioning on because they do not affect the residual variance and may reduce the conditional instrumental strength.

Example 4.5 (Beneficial conditioning).

Consider the graph from Fig. 2a and any two tuples of the form and , where and . By Example 4.4, any such tuple is a linearly valid conditional instrumental set relative to to in . Further, as we can apply Theorem 3 with and (Condition (c) (i) holds, Conditions (a), (b) and (d) are void). We can therefore conclude that adding to any can only decrease the asymptotic variance.

Conditioning on is beneficial, because and . Therefore, but (see Lemma C.11 in the Supplementary Material). Interestingly, this remains true if we add the edge to , making a confounder. The covariate is representative of a larger class of covariates that we should aim to condition on because they may reduce the residual variance and do not affect the conditional instrumental strength. This class, in particular includes confounders between and that are independent of .

Example 4.6 (Ambiguous conditioning).

Consider the graph from Fig. 1b. Consider the two tuples and . By Example 3.5, both tuples are linearly valid conditional instrumental sets relative to in . Further, as and we cannot apply Theorem 3 with and (Condition (c) does not hold). For the same reason, we cannot apply Theorem 3 with and (Condition (b) does not hold). We can therefore not use Theorem 4.2 to determine the effect of adding to the conditioning set on the asymptotic variance.

There are two additional interesting classes of covariates, one neutral and one beneficial, that we discuss in Section D.3 of the Supplementary Material.

Since Theorem 4.2 can compare tuples and with and , it also gives interesting new insights regarding covariates that we may add both to and . The following corollary is an example of such a result.

Corollary 4.7.

Consider nodes and in an acyclic directed mixed graph such that . Let be a linearly valid conditional instrumental set relative to in . If is a linearly valid conditional instrumental set relative to in , then for all linear structural equation models compatible with such that , it holds that

Intuitively, Corollary 4.7 states that covariates that may be added to both and should be added to . If we restrict ourselves to the special case that is a singleton , we can also show the following complementary result.

Proposition 4.8.

Consider nodes and in an acyclic directed mixed graph such that . Let be a linearly valid conditional instrumental sets relative to in . If is a linearly valid conditional instrumental set relative to in but is not, then for all linear structural equation models compatible with such that ,

Corollaries 4.3 and 4.7 along with Proposition 4.8 are very useful tools for identifying efficient tuples. We illustrate this by revisiting the graph from Fig. 1b and using the three results to identify a tuple guaranteed to provide the smallest asymptotic variance among all linearly valid tuples.

Example 4.9 (Asymptotically optimal tuple).

Consider the graph in Fig. 1b. By Example 3.5 there are linearly valid conditional instrumental sets relative to in , which we list in Table 3 of the Supplementary Material. Let be a linearly valid tuple such that . Then, . We can therefore apply Corollary 4.7 with and conclude that the linearly valid tuple is more efficient than . Consider now a linearly valid tuple such that . We now construct a more efficient linearly valid tuple such that . If , then with is a linearly valid tuple. Further, for all linearly valid tuples in . Therefore, we can invoke Proposition 4.8 with and conclude that is more efficient than . Let and . Since , is a linearly valid tuple and we can therefore apply Corollary 4.3 to conclude that is more efficient than . Combining the two results, we can conclude that provides the smallest attainable asymptotic variance among all linearly valid tuples.

4.3 Greedy forward procedure

As shown in the previous section, the asymptotic variance can behave in complex ways. However, in the simple case where we are given a linearly valid tuple and a covariate , we can use the results of Section 4.2 to derive the following simple rules. If we can add to , then we should do so by Corollaries 4.3 and 4.7. If we cannot add to , but may add it to , then we should add to by Proposition 4.8.

Based on these two rules, we propose the greedy two phase Algorithm 1 which given a linearly valid conditional instrumental set returns a more efficient tuple. In the first phase, Algorithm 1 moves all covariates in where this is possible to . In the second phase, it greedily adds any additional covariates to either or while minimizing the asymptotic variance. The m-separation checks in the second phase of Algorithm 1 are not necessary in the sense that we could drop them and the algorithm would still greedily minimize the asymptotic variance. We include them, nonetheless, as otherwise the algorithm would add covariates that do not affect the asymptotic variance to the tuple. This would needlessly grow the output tuple, likely negatively affecting the finite sample performance. Adding the two m-separation checks ensures that in each step the algorithm only adds nodes to the tuple that may decrease the asymptotic variance. We prove the soundness of Algorithm 1 in Section C.4 of the Supplementary Material. We emphasize that due to the second phase, the output tuple is order dependent and has no efficiency guarantee when compared to all linearly valid tuples in .

Example 4.10 (Illustrating Algorithm 1).

Consider the graph from Fig. 1b (see Table 3 in the Supplementary Material for a list of the linearly valid tuples in ). Suppose our starting linearly valid conditional instrumental set is . Since is not a linearly valid tuple, the first phase returns . Regarding the second phase, consider first the case that Algorithm 1 checks before . Because and , Algorithm 1 discards even though and are linearly valid tuples. Because is a linearly valid tuple and , it then adds to and outputs the tuple . Consider now the case that Algorithm 1 checks before . Again, is added to . However, as is a linearly valid tuple and , Algorithm 1 also adds to . The output tuple is therefore in this case. Both and are more efficient than but only provides the smallest attainable asymptotic variance among all tuples.

Based on the two rules underpinning Algorithm 1, we propose the following guidelines for practitioners. They are particularly useful in cases where we have a basic understanding of the causal structure, but not enough knowledge of the causal graph to apply Theorem 4.2 directly.

Remark 4.11 (Practical guidelines).

Covariates that can be used as instrumental variables should be used as instrumental variables. Covariates that can only be used as conditioning variables should be used as conditioning variables.

4.4 Graphically optimal linearly valid conditional instrumental sets

In Example 4.9 we identified a linearly valid conditional instrumental set that provides the smallest attainable asymptotic variance among all linearly valid tuples using only the graph. In the closely related literature on efficient valid adjustment sets Henckel et al., (2022) referred to this property as asymptotic optimality. They also provided a graphical characterization of a valid adjustment set that for linear structural equation models with independent errors is asymptotically optimal and showed that in cases with latent variables, i.e., correlated errors, no asymptotically optimal valid adjustment set may exist. The following example shows that, similarly, an asymptotically optimal linearly valid conditional instrumental set may not exist.

Example 4.12 (No asymptotically optimal tuple).

Consider the graph from Fig. 2b. There are five linearly valid tuples with respect to in : , and . We consider two linear structural equation models compatible with : for model let all error variances and edge coefficients be , where we model the bi-directed edges with a latent variable, i.e, and . For model do the same, except for setting the edge coefficient for the edge to . For both models we computed the asymptotic variance corresponding to the five linearly valid tuples. The results are given in Table 1 and they show that in the most efficient tuples are and while in the most efficient tuple is . Therefore, there is no asymptotically optimal tuple.

The reason that is more efficient than in but less efficient in , is that adjusting for reduces both the residual variance and the instrumental strength. The overall effect on the asymptotic variance depends on how large these reductions are, which depends on the strength of the edges and , respectively. Because the edge has a small edge coefficient in , adjusting for reduces the asymptotic variance here.

Example 4.12 does not contradict our results from Section 4.3, as these cover the special case of adding a single covariate to a linearly valid tuple at a time. Given that there may not be an asymptotically optimal conditional instrumental set, we now introduce the concept of a graphically optimal tuple. It is inspired by the definition of an admissible decision rule in statistical decision theory (Chapter 2, Robert et al.,, 2007).

Definition 4.13.

Let and be nodes in an acyclic directed mixed graph and let be a linearly valid conditional instrumental set relative to in . We call graphically suboptimal relative to in , if there exists a linearly valid conditional instrumental set such that for all linear structural equation models compatible with in which holds, and for at least one model this inequality is strict. We say that is graphically optimal if it is not graphically suboptimal.

Graphical optimality is a natural generalization of asymptotic optimality. In particular, there always exists a graphically optimal tuple and if an asymptotically optimal one exists, any graphically optimal tuple is asymptotically optimal. We now give a definition which we use to construct a conditional instrumental set that is linearly valid and graphically optimal under mild conditions.

Definition 4.14.

Let be a node and a node set in an acyclic directed mixed graph with node set . Let . Then let denote the set .

Theorem 4.15.

Consider nodes and in an acyclic directed mixed graph such that . Let and . Then the following two statements hold: (i) if then is a linearly valid conditional instrumental set relative to in ; (ii) if then is also graphically optimal relative to in .

The tuple is constructed as follows. We first choose in order to minimize the residual variance. With fixed we then in turn choose from the remaining covariates in order to maximize the conditional instrumental strength. The conditions and ensure that the resulting is not too small. We give examples where the two conditions are violated in Section D.4 of the Supplementary Material and emphasize that may occur in cases where other tuples are linearly valid. For interested readers, we also provide an example in Section D.4 where all linearly valid tuples are graphically optimal.

Example 4.16 (Illustrating Theorem 4.15).

We revisit the graphs from Figure 1b and 2b, denoting them and , respectively. In , and . By Examples 3.5 and 4.9, is a linearly valid conditional instrumental set relative to in and in fact asymptotically optimal. In , and . By Example 4.12, is a linearly valid conditional instrumental set relative to in . There is no asymptotically optimal linearly valid conditional instrumental set relative to in . However, as is more efficient than any other tuple in it follows that it is graphically optimal.

5 Simulations

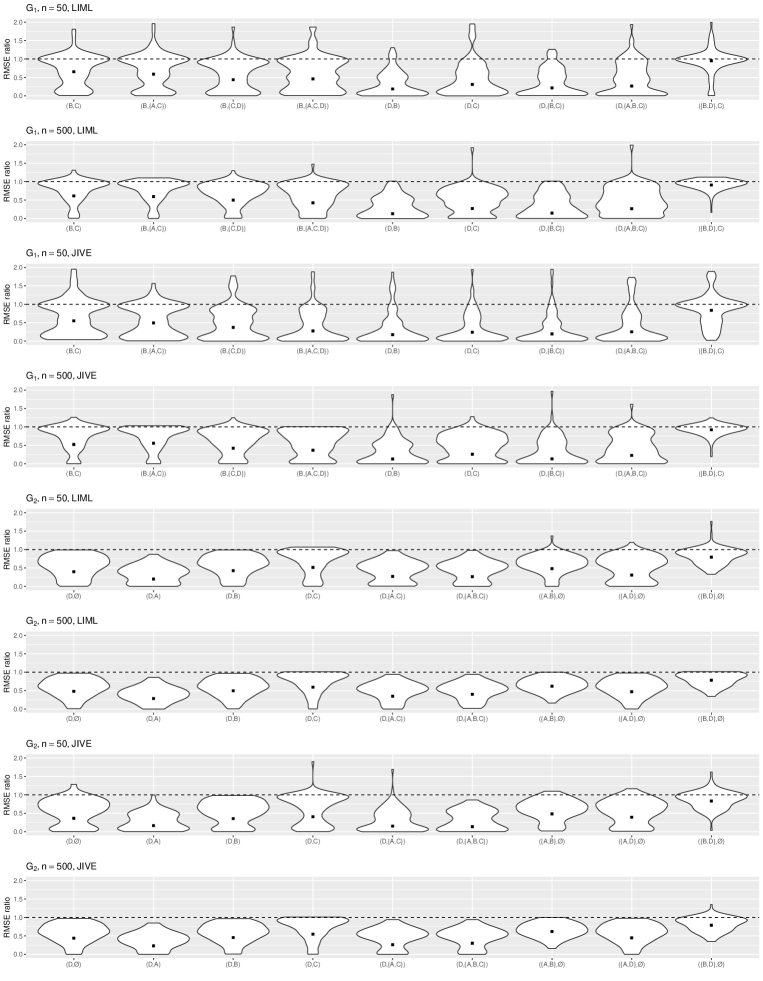

We investigated the finite sample efficiency of and how it compares to alternative linearly valid conditional instrumental sets. For further comparison, we also considered the following three alternative estimators to the two-stage least squares: (i) the limited information maximum likelihood (LIML) estimator (Anderson et al.,, 1949; Phillips and Hale,, 1977), (ii) the jackknife instrumental variables (JIVE) estimator (Angrist et al.,, 1999) and (iii) the ordinary least squares regression of on . The first two are alternative instrumental variable estimators with the same asymptotic distribution as the two-stage least squares estimator but with distinct finite sample characteristics. We include the ordinary least squares regression as a non-causal baseline. We did so in linear structural equation models compatible with the two graphs and from Figures 1a and 2a, respectively. Recall that by Example 4.16, the tuple in is asymptotically optimal. We also show that the tuple in is asymptotically optimal in Example D.5 of the Supplementary Material.

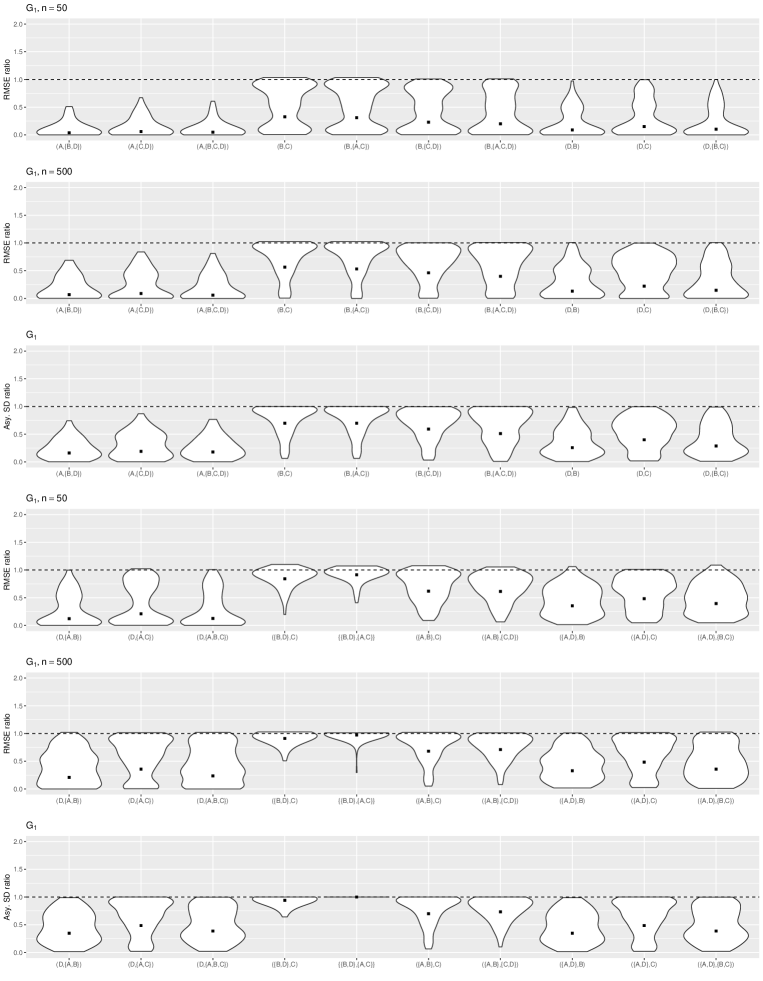

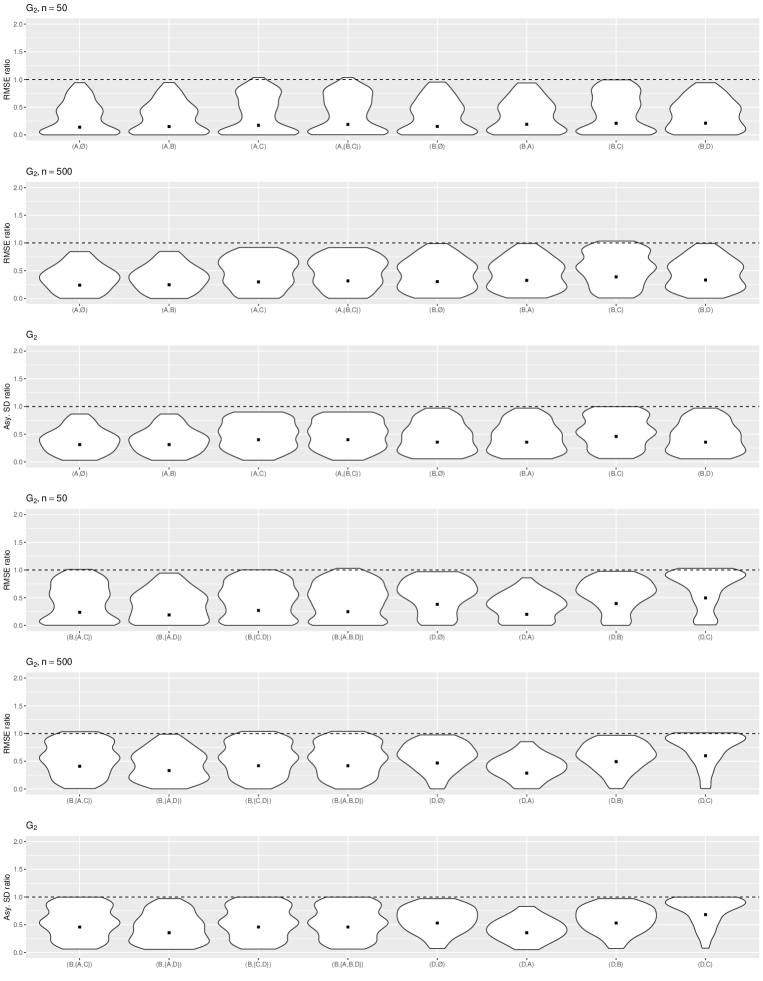

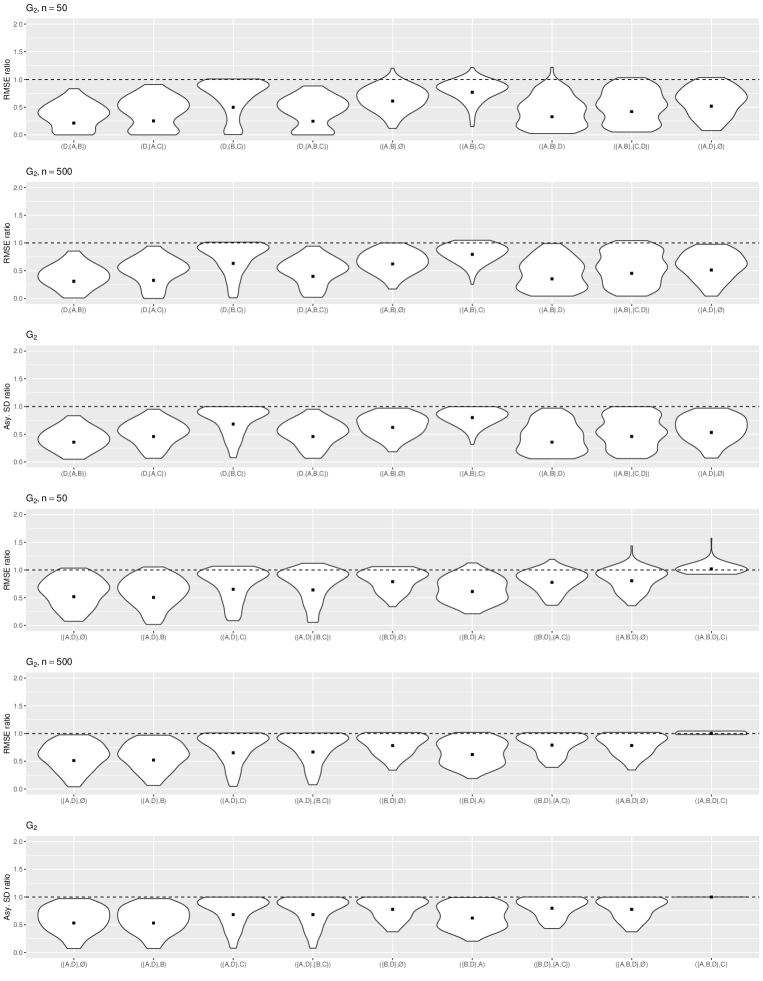

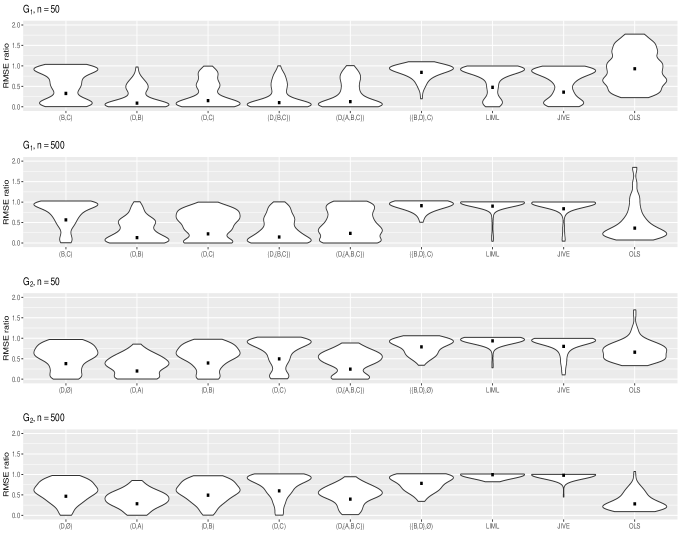

For each graph, we randomly generated compatible linear structural equation models as follows. We considered models with either all Gaussian or all uniform errors, each with probability . For each node we sampled an error variance uniformly on and for each edge an edge coefficient uniformly on . Any bi-directed edge was modelled as a latent variable , with the error variances and edge coefficients generated as for the other nodes and edges. From each linear structural equation model we generated data sets with sample size and used these to compute the two-stage least squares, the limited information maximum likelihood and the jackknife instrumental variables estimators corresponding to all available linearly valid conditional instrumental sets relative to in the respective graph as well as the ordinary least squares regression of on . For each of these estimators, we computed Monte-Carlo root mean squared errors with respect to the known true total effect over the simulated data sets. We did this separately for the sample sizes and . To compare the performances, we computed the ratio of the root mean squared error for the two-stage least squares with to the one for each of the alternative linearly valid tuples and estimators. A ratio smaller than indicates that two-stage least squares with was more efficient than the other estimator. A ratio larger than indicates the opposite. Fig. 3 shows violin plots of these ratios over the linear structural equation models. As there are linearly valid conditional instrumental sets relative to in and in , we only show the violin plots for a representative subset for the two-stage least squares estimator and only consider the optimal tuple for the alternative instrumental variable estimators. Please see Section E of the Supplementary Material for further plots.

The violin plots corroborate our theoretical results. The optimal two-stage least squares outperforms all other estimators, with few of the ratios larger than . This is also true for the sample size even though our results only hold asymptotically and the alternative estimators which our results do not cover. Interestingly, the most competitive estimator in and for is the inconsistent ordinary least squares estimator. This illustrates that using the two-stage least squares estimator rather than the ordinary least squares estimator represents a bias-variance trade-off. Our simulation indicates that it is important to consider statistical efficiency when selecting the conditional instrumental set to ensure that this bias-variance trade-off is favourable in small samples. The fact that the optimal limited information maximum likelihood and the optimal jackknife instrumental variables estimator perform worse than the ordinary least squares for and indicates that this bias-variance trade-off is not just a characteristic of the two-stage least squares but rather of instrumental variable estimators in general, which further emphasizes the importance of carefully selecting the conditional instrumental set in practice.

6 Estimating the causal effect of institutions on wealth

| estimate | standard error | ||

| 0.94 | 0.16 | ||

| 1.00 | 0.22 | ||

| 0.96 | 0.28 | ||

| 0.74 | 0.13 | ||

| 0.94 | 0.14 | ||

| 0.74 | 0.11 |

We revisit the analysis by Acemoglu et al., (2001) of the effect of institutions on economic wealth with the mortality of European settlers as an instrument. In their analysis Acemoglu et al., (2001) consider a variety of different conditioning sets. They diligently check that all of them yield a coherent estimate of the total effect of institutions on economic wealth. This serves as a robustness check for their analysis. The authors do not, however, consider how the standard errors differ depending on the conditioning set. We investigate this for three of the available covariates: latitude, ethnolinguistic fragmentation, and percentage of population of European ancestry. We summarize our results in Table 2. Even though we do not have a causal graph, we can follow arguments by Acemoglu et al., to approximately check the conditions of Theorem 4.2.

According to the authors, latitude and percentage of population with European ancestry are correlated with settler mortality, because (i) tropical diseases were a major cause of settler mortality and (ii) low settler mortality led to a larger settler population. Accepting this, we classify both as covariates of the same type as variable in Figure 2a. By the argument of harmful conditioning from Example 4.4 we expect that conditioning on them leads to a larger standard error and we indeed observe this in our calculations. Adding percentage of population with European ancestry to the instrumental set, on the other hand, leads to a smaller standard error, as expected per Corollary 4.7. Similarly, the variable ethnolinguistic fragmentation belongs to the same class of covariates as variable in Figure 2a. This is because cultural barriers are often also market barriers and as a result, ethnolinguistic fragmentation is predictive of economic wealth. This time, by the argument of beneficial conditioning from Example 4.5, adjusting for ethnolinguistic fragmentation should lead to a smaller standard error and we indeed observe this in our calculations.

In our analysis the smallest standard error (0.11) is less than half the size of the largest (0.28), illustrating the potential advantages of applying our results to select the best linearly valid tuple. We emphasize that identifying an efficient tuple by computing the standard errors for many tuples and selecting the one with the smallest standard error leads to invalid standard errors due to post-selection inference (Berk et al.,, 2013). Using qualitative causal background knowledge, ideally in form of a graph, to apply our results does not suffer from this drawback.

7 Discussion

There are many instrumental variable estimators other than the two-stage least squares estimator, such as the limited information maximum likelihood and the jackknife instrumental variables estimator we considered in our simulation study, which were developed for settings with many weak instruments. It would be interesting to try to generalize our results to a broad class of alternative instrumental variable estimators and beyond the linear setting with a fixed number of instruments.

Finally, we would like to point out four other interesting avenues for future research: First, to graphically characterize when an asymptotically optimal linearly valid conditional instrumental set exists (cf. Runge,, 2021). Second, to graphically characterize a linearly valid conditional instrumental set that is graphically optimal and has maximal conditional instrumental strength. As the finite sample efficiency of our estimators appears to be more vulnerable to a small conditional instrumental strength than a large residual variance (see Section 5), such a tuple might be a good alternative to , especially in small samples. Third, to generalize Theorem 4.2 such that it covers all cases where we can use the graph to decide which of two linearly valid conditional instrumental sets provides the smaller asymptotic variance, that is, derive a necessary and sufficient graphical criterion. Fourth, to generalize the paper’s results and in particular Theorem 3.2 to the setting where and are sets.

Acknowledgement

We thank Nicola Gnecco and Jonas Peters for valuable comments.

References

- Acemoglu et al., (2001) Acemoglu, D., Johnson, S., and Robinson, J. A. (2001). The colonial origins of comparative development: An empirical investigation. American Economic Review, 91(5):1369–1401.

- Anderson et al., (1949) Anderson, T. W., Rubin, H., et al. (1949). Estimation of the parameters of a single equation in a complete system of stochastic equations. Ann. Math. Statistics, 20(1):46–63.

- Angrist et al., (1999) Angrist, J. D., Imbens, G. W., and Krueger, A. B. (1999). Jackknife instrumental variables estimation. J. Appl. Econometrics, 14(1):57–67.

- Angrist et al., (1996) Angrist, J. D., Imbens, G. W., and Rubin, D. B. (1996). Identification of causal effects using instrumental variables. J. Amer. Statist. Assoc., 91(434):444–455.

- Basmann, (1957) Basmann, R. L. (1957). A generalized classical method of linear estimation of coefficients in a structural equation. Econometrica, 25:77–83.

- Bekker, (1994) Bekker, P. A. (1994). Alternative approximations to the distributions of instrumental variable estimators. Econometrica, 62:657–681.

- Berk et al., (2013) Berk, R., Brown, L., Buja, A., Zhang, K., and Zhao, L. (2013). Valid post-selection inference. Ann. Statist., 41:802–837.

- Bound et al., (1995) Bound, J., Jaeger, D. A., and Baker, R. M. (1995). Problems with instrumental variables estimation when the correlation between the instruments and the endogenous explanatory variable is weak. J. Amer. Statist. Assoc., 90(430):443–450.

- Bowden and Turkington, (1990) Bowden, R. J. and Turkington, D. A. (1990). Instrumental variables. Cambridge University Press, Cambridge.

- (10) Brito, C. and Pearl, J. (2002a). Generalized instrumental variables. In Proceedings of the Eighteenth Annual Conference on Uncertainty in Artificial Intelligence (UAI-02), pages 85–93, San Francisco, CA. Morgan Kaufmann.

- (11) Brito, C. and Pearl, J. (2002b). A new identification condition for recursive models with correlated errors. Struct. Equ. Model., 9(4):459–474.

- Buja et al., (2014) Buja, A., Berk, R., Brown, L., George, E., Pitkin, E., Traskin, M., Zhan, K., and Zhao, L. (2014). Models as approximations, part I: A conspiracy of nonlinearity and random regressors in linear regression. arXiv:1404.1578.

- Guo et al., (2022) Guo, F. R., Perković, E., and Rotnitzky, A. (2022). Variable elimination, graph reduction and efficient g-formula. arXiv:2202.11994.

- Hansen, (2022) Hansen, B. E. (2022). Econometrics. Princeton University Press.

- Henckel et al., (2022) Henckel, L., Perković, E., and Maathuis, M. H. (2022). Graphical criteria for efficient total effect estimation via adjustment in causal linear models. J. R. Statist. Soc. B, 84(2):579–599.

- Hernán and Robins, (2006) Hernán, M. A. and Robins, J. M. (2006). Instruments for causal inference: an epidemiologist’s dream? Epidemiology, 17:360–372.

- Kinal, (1980) Kinal, T. W. (1980). The existence of moments of k-class estimators. Econometrica, 48:241–249.

- Koster, (1999) Koster, J. T. (1999). On the validity of the markov interpretation of path diagrams of gaussian structural equations systems with correlated errors. Scand. J. Statist., 26(3):413–431.

- Kuroki and Cai, (2004) Kuroki, M. and Cai, Z. (2004). Selection of identifiability criteria for total effects by using path diagrams. In Proceedings of the Twentieth Annual Conference on Uncertainty in Artificial Intelligence (UAI-04), pages 333–340, Arlington, Virginia. AUAI Press.

- Kuroki and Miyakawa, (2003) Kuroki, M. and Miyakawa, M. (2003). Covariate selection for estimating the causal effect of control plans by using causal diagrams. J. R. Statist. Soc. B, 65(1):209–222.

- Pearl, (1995) Pearl, J. (1995). Causal diagrams for empirical research. Biometrika, 82(4):669–688.

- Pearl, (2009) Pearl, J. (2009). Causality. Cambridge University Press, Cambridge, second edition.

- Perković et al., (2018) Perković, E., Textor, J., Kalisch, M., and Maathuis, M. H. (2018). Complete graphical characterization and construction of adjustment sets in Markov equivalence classes of ancestral graphs. J. Mach. Learn. Res., 18(220):1–62.

- Phillips and Hale, (1977) Phillips, G. D. A. and Hale, C. (1977). The bias of instrumental variable estimators of simultaneous equation systems. Internat. Econom. Rev., 18(1):219–228.

- Richardson, (2003) Richardson, T. (2003). Markov properties for acyclic directed mixed graphs. Scand. J. Statist., 30(1):145–157.

- Richardson et al., (2017) Richardson, T. S., Evans, R. J., Robins, J. M., and Shpitser, I. (2017). Nested markov properties for acyclic directed mixed graphs. arXiv:1701.06686.

- Robert et al., (2007) Robert, C. P. et al. (2007). The Bayesian choice: from decision-theoretic foundations to computational implementation, volume 2. Springer.

- Rotnitzky and Smucler, (2020) Rotnitzky, A. and Smucler, E. (2020). Efficient adjustment sets for population average causal treatment effect estimation in graphical models. J. Mach. Learn. Res., 21(188):1–86.

- Rotnitzky and Smucler, (2022) Rotnitzky, A. and Smucler, E. (2022). A note on efficient minimum cost adjustment sets in causal graphical models. J. Causal Inference, 10(1):174–189.

- Runge, (2021) Runge, J. (2021). Necessary and sufficient graphical conditions for optimal adjustment sets in causal graphical models with hidden variables. Advances in Neural Information Processing Systems, 34:15762–15773.

- Shpitser et al., (2010) Shpitser, I., VanderWeele, T., and Robins, J. (2010). On the validity of covariate adjustment for estimating causal effects. In Proceedings of the Twenty-Sixth Annual Conference on Uncertainty in Artificial Intelligence (UAI-10), pages 527–536, Corvallis, Oregon. AUAI Press.

- Smucler et al., (2022) Smucler, E., Sapienza, F., and Rotnitzky, A. (2022). Efficient adjustment sets in causal graphical models with hidden variables. Biometrika, 109(1):49–65.

- Spirtes et al., (2000) Spirtes, P., Glymour, C., and Scheines, R. (2000). Causation, Prediction, and Search. MIT Press, Cambridge, MA, second edition.

- Staiger and Stock, (1997) Staiger, D. and Stock, J. H. (1997). Instrumental variables regression with weak instruments. Econometrica, 65:557–586.

- Stock et al., (2002) Stock, J. H., Wright, J. H., and Yogo, M. (2002). A survey of weak instruments and weak identification in generalized method of moments. J. Bus. Econom. Statist., 20(4):518–529.

- Vansteelandt and Didelez, (2018) Vansteelandt, S. and Didelez, V. (2018). Improving the robustness and efficiency of covariate-adjusted linear instrumental variable estimators. Scand. J. Statist., 45(4):941–961.

- Wermuth, (1989) Wermuth, N. (1989). Moderating effects in multivariate normal distributions. Methodika, 3:74–93.

- Witte et al., (2020) Witte, J., Henckel, L., Maathuis, M. H., and Didelez, V. (2020). On efficient adjustment in causal graphs. J. Mach. Learn. Res., 21(246):1–45.

- Wooldridge, (2010) Wooldridge, J. M. (2010). Econometric analysis of cross section and panel data. MIT press.

- Wright, (1934) Wright, S. (1934). The method of path coefficients. Ann. Math. Statistics, 5(3):161–215.

Appendix A Preliminaries and known results

A.1 General preliminaries

Covariance matrices and regression coefficients: Consider random vectors and . We denote the covariance matrix of by and the covariance matrix between and by , where its -th element equals . We further define . If , we write instead of . The value can be interpreted as the residual variance of the ordinary least squares regression of on . We also refer to as the conditional variance of given . Let represent the population level least squares coefficient matrix whose -th element is the regression coefficient of in the regression of on and . We denote the corresponding estimator as . Finally, for random vectors with we use the notation that and .

Two stage least squares estimator: (Basmann,, 1957) Consider two random variables and , and two random vectors and . Let and be the random matrices corresponding to taking i.i.d. observations from the random vectors , and , respectively. Then the two stage least squares estimator is defined as the first entry of the larger estimator

where we repress the dependence on the sample size for simplicity. We refer to the tuple as the conditional instrumental set, to as the instrumental set and to as the conditioning set. We also let denote the population level two-stage least squares estimator of on with instrumental set , which exists whenver is invertible.

A.2 Graphical and causal preliminaries

Graphs: We consider graphs with node set and edge set , where edges can be either directed () or bidirected (). If all edges in are directed, then is a directed graph. If all edges in are directed or bidirected, then is a directed mixed graph.

Paths: Two edges are adjacent if they have a common node. A walk is a sequence of adjacent edges. A path is a sequence of adjacent edges without repetition of a node and may consist of just a single node. The first node and the last node on a path are called endpoints of and we say that is a path from to . Given two nodes and on a path , we use to denote the subpath of from to . A path from a set of nodes to a set of nodes is a path from a node to some node . A path from a set to a set is proper if only the first node is in (cf. Shpitser et al.,, 2010). A path is called directed or causal from to if all edges on are directed and point towards . We use to denote the concatenation of paths. For example, for any path from to with intermediary node .

Ancestry: If , then is a parent of and is a child of . If there is a causal path from to , then is an ancestor of and a descendant of . If , then and are siblings. We use the convention that every node is an ancestor, descendant and sibling of itself. The sets of parents, ancestors, descendants and siblings of in are denoted by , , and , respectively. For sets , we let , with analogous definitions for , and .

Colliders: A node is a collider on a path if contains a subpath of the form or . A node on a path is called a non-collider on if it is neither a collider on nor an endpoint node of .

Directed cycles, directed acyclic graphs and acyclic directed mixed graphs: A directed path from a node to a node , together with the edge forms a directed cycle. A directed graph without directed cycles is called a directed acyclic graph and a directed mixed graph without directed cycles is called a acyclic directed mixed graph.

Blocking, d-separation and m-separation: (Definition 1.2.3 in Pearl, (2009) and Section 2.1 in Richardson, (2003)). Let be a set of nodes in an acyclic directed mixed graph . A path in is blocked by if (i) contains a non-collider that is in , or (ii) contains a collider such that no descendant of is in . A path that is not blocked by a set is open given . If and are three pairwise disjoint sets of nodes in , then m-separates from in if blocks every path between and in . We then write . Otherwise, we write . We use the convention that for any two disjoint node sets and it holds that .

Alternatively and equivalently, we can define m-separation using walks instead of paths as follows. A walk is blocked by if (i) contains a non-collider that is in , or (ii) contains a collider such that is not in . A walk that is not blocked by a set is open given . Further, m-separates from in if blocks every walk between and in .

Markov property and faithfulness: (Definition 1.2.2 Pearl,, 2009) Let , and be disjoint sets of random variables. We use the notation to denote that is conditionally independent of given . A density is called Markov with respect to an acyclic directed mixed graph if implies in . If this implication holds in the other direction, then is faithful with respect to .

Causal paths and forbidden nodes: (Perković et al.,, 2018) Let and be nodes in an acyclic directed mixed graph . A path from to in is called a causal path from to if all edges on are directed and point towards . We define the causal nodes with respect to in as all nodes on causal paths from to excluding and denote them . We define the forbidden nodes relative to in as .

Linear structural equation model: Consider an acyclic directed mixed graph , with nodes and edges , where the nodes represent random variables. The random vector is generated from a linear structural equation model compatible with if

| (5) |

such that the following three properties hold: First, is a matrix with for all where . Second, is a random vector of errors such that and is a matrix with for all where . Third, for any two disjoint sets such that for all and all , , the random vector is independent of .

Given the matrices and it holds that

that is, the covariance matrix of a linear causal model is completely determined by the tuple of matrices .

Gaussian linear structural equation model: If the errors in a linear structural equation model are jointly normal we refer to the linear structural equation model as a Gaussian linear structural equation model. Such a model is completely determined by the tuple of matrices which is why we will use to denote the corresponding Gaussian linear structural equation model.

Latent projections and causal acyclic directed mixed graphs: (Richardson et al.,, 2017) Let be an acyclic directed mixed graph with node set and let . We can use a tool called the latent projection (Richardson,, 2003) to remove the nodes in from while preserving all m-separation statements between subsets of . We use the notation to denote the acyclic directed mixed graph with node set that is the latent projection of over . The latent projection of over is an acyclic directed mixed graph with node set and edges in accordance with the following rules: First, contains a directed edge if and only if there exists a causal path in with all non-endpoint nodes in . Second, contains a bi-directed edge if and only if there exists a path between and , such that all non-endpoint nodes are in and non-colliders on , and the edges adjacent to and have arrowheads pointing towards and , respectively.

The following is an important property of the latent projection for acyclic directed mixed graphs: if is generated from a linear structural equation model compatible with the acyclic directed mixed graph than is generated from a linear structural equation model compatible with .

Total effects: We define the total effect of on as

In a linear structural equation model the function is constant, which is why we simply write . The path tracing rules by (Wright,, 1934) allow for the following alternative definition. Consider two nodes and in an acyclic directed mixed graph and suppose that is generated from a linear structural equation model compatible with . Then is the sum over all causal paths from to of the product of the edge coefficients along each such path.

Given a set of random variables we also define to be the stacked column vector with th entry . Finally, let be the sum over all causal paths from to that do not contain nodes in of the product of the edge coefficients along each such path.

Valid adjustment sets: (Shpitser et al.,, 2010; Perković et al.,, 2018) We refer to as a valid adjustment set relative to in , if for all linear structural equation models compatible with . The set is a valid adjustment set relative to in if and only if (i) and (ii) blocks all non-causal paths from to .

Example A.1 (Linear structural equation models and total effects).

Consider the graph from Fig. 4a. Then the following generating mechanism is an example of a linear structural equation model compatible with :

with , where and if , and , or and . Suppose we are interested in the total effect of on . The path is the only causal path between the two nodes and therefore . The causal nodes are and the forbidden nodes are .

Since , any valid adjustment set relative to in has to consist of nodes in . The two non-causal paths from to in are and . The former path is blocked by if is non-empty, since all three nodes are non-colliders on the path. The latter path cannot be blocked by and as a result there is no valid adjustment set relative to in . If we remove the edge from , then any would be a valid adjustment set.

Let . The acyclic directed mixed graph in Fig. 4b is the latent projection graph . Replacing the variables in with their generating equation we obtain the linear structural equation model

with , where and if , and , or and . Letting and we can rewrite this model as

which is a linear structural equation model compatible with from which is generated.

A.3 Existing and preparatory results on covariance matrices

Lemma A.2.

(e.g. Henckel et al.,, 2022) Let and be mean random vectors with finite variance, with possibly of length zero. Then

Lemma A.3.

(e.g. Henckel et al.,, 2022) Let and be mean random vectors with finite variance, with possibly of length zero. Then

Lemma A.4.

(Wermuth,, 1989) Let and be mean Gaussian vectors, with possibly of length zero. If or , then Furthermore, if , then

Lemma A.5.

Consider an acyclic directed mixed graph and let be a Gaussian linear structural equation model compatible with with a strictly diagonally dominant matrix. Let and let denote the Gaussian linear structural equation model where the edge coefficients and error covariances corresponding to the edges in are replaced with some value . Then

for any .

Proof.

The proof is based on the fact that as continuous functions in , and , and as we will show, is a continuous function at . We show this in two steps by first showing that is a continuous function at and second showing that is a continuous function at

Regarding the first step,

is a continuous function in and . It therefore remains to check that is invertible to show it is continuous at . To see this we us that is compatible with the graph , which is the graph with the edges in removed. As is acyclic, so is and as a result is invertible (see Neumann series). Therefore,

by continuity.

Regarding the second step, to show that

is a continuous function at we need to show that the minor is invertible at . We do so by showing that is invertible. By the fact that is a diagonally dominant matrix, so is . Therefore, is invertible by the Levy-Desplanques theorem and as a result, is invertible. ∎

Appendix B Proofs for Section 3

Theorem B.1.

Consider mutually disjoint nodes and , and node sets and in an acyclic directed mixed graph . Then is a linearly valid conditional instrumental set relative to in if and only if (i) , (ii) and (iii) , where the graph is with all edges out of on causal paths from to removed.

Proof.

We first show that under the three conditions of Theorem 3.2, there exists a linear structural equation model compatible with such that and for any such model consistently estimates . By Condition (ii) of Theorem 3.2, that is, , it follows that there exist linear structural equation model compatible with such that .

We now show that for any model such that , Condition (i) and (iii) of Theorem 3.2 ensure that converges in distribution to . To do so consider any model compatible with such that and let and . Consider the whole vector valued two-stage least squares estimator , whose first entry defines our estimator . Let , with and let . Then

where and are the random matrices corresponding to taking i.i.d. observations from and , respectively. By assumption and we can therefore conclude with Lemma B.2 that is invertible. With the continuous mapping theorem it follows that that the limit in probability of is . It is thus sufficient to show that , i.e., and , to prove that converges in probability to which implies that converges to .

Consider first . Clearly, by the fact that . Consider now .

We now show that under Conditions (i) and (iii), for all linear structural equation models compatible with before arguing why this suffices to conclude that . Fix any linear structural equation model with edge coefficient matrix and error covariance matrix compatible with . By condition (i), and therefore and are also nodes in the latent projection graph over . By the fact that the latent projection preserves m-separation statements implies . By Lemma B.5, implies that , where is the graph with the edge removed. But implies by Lemma B.4 that . If the model we consider is Gaussian this suffices to conclude that . If the model is not Gaussian, on the other hand, then by the fact that depends on the linear structural equation model only via the tuple it follows that must have the same value as in the Gaussian model, i.e., be . Combined this shows that if the three conditions of Theorem 3.2 hold, then .

It remains to show that the two conditions of Definition 3.1 also imply Conditions (i), (ii) and (iii) of Theorem 3.2. Condition (i) of Definition 3.1 implies that , which is Condition (ii) of Theorem 3.2, by contraposition. We now show that if converges to for all models compatible with , such that then Condition (i) and (iii) of Theorem 3.2 hold.

By the same argument as given in the first half of this proof, suffices to conclude that the estimator converges to some unique limit , that is characterized by the fact that with . We now show that if this limit vector has as the first entry for all models compatible with such that , Conditions (i) and (iii) of Theorem 3.2 must hold. We have shown already that if the first entry of is then the remaining entries have to form the vector as otherwise . We can therefore assume that . This implies as we have also shown previously that . For a Gaussian model this is only true if . It therefore suffices to show that if for all linear structural equation models compatible with then Conditions (i) and (iii) of Theorem 3.2 hold. We do so by contraposition.

If Condition (i) of Theorem 4.2 does not hold, there exists a Gaussian model violating that by Lemma B.3. Suppose that Condition (i) holds but Condition (iii) does not. By Lemma B.5, Condition (i) holding and Condition (iii) not holding for implies that . Therefore, we can invoke Lemma B.4 to conclude that there exists a Gaussian linear structural equation model such that in this case as well. We can therefore conclude that if for all linear structural equation model compatible then Conditions (i) and (iii) of Theorem 3.2 hold. ∎

Lemma B.2.

Consider two random variables and , and two random vectors and . Let and . Then is invertible if and only if .

Proof.

Using it follows that . As and it follows that

Here we use that and for any random variable and random vector . As , it follows that is of full row rank if and only if . As is a positive-definite matrix, is positive-definite if and only if has full row rank. ∎

Lemma B.3.

Consider mutually disjoint nodes and , and node sets and in an acyclic directed mixed graph such that and . Then there exists a linear structural equation model compatible with , such that

where .

Proof.

The statement is void for . As implies that we can therefore assume that . We now construct a Gaussian linear structural equation model in which . This suffices to prove our claim since if and only if and we consider Gaussian linear structural equation models. To do so we first derive an equation for that does not depend on .

Consider any Gaussian linear structural equation model compatible with . We augment as well as the underlying linear structural equation model by adding to as well as the edges and with edge coefficients and , respectively, to . We denote the augmented graph with . Clearly the augmented model is still a linear structural equation model. In particular

| (i) | |||

| (ii) | |||

| (iii) |

where we use that and that as a result is an adjustment set relative to since there are no forbidden nodes and no non-causal paths relative to along with Lemma A.3. Plugging the latter two equations into the first one we obtain

where the right hand side does not depend in .

In the remainder of this proof we will show that there exists a linear structural equation model compatible with , such that

We now construct a graph where we drop some edges from to ensure additional structure required for our proof. As any linear structural equation model compatible with is also compatible with it suffices to show that there exists a linear structural equation model compatible with , such that

to complete our proof.

To construct , consider a proper path from to open given in . Such a path exists by assumption. For any such path if it contains a collider , then , that is, there exists a causal path from to some node in . Let denote a shortest such path. This ensures that only contains one node in . Starting from we now construct a proper path from to that is open given in and for any collider on , intersects with only at .

If has this property already we are done, so suppose it does not and let be the collider closest to on such that and intersect at some node that is not . We will now construct a path that is a proper path from to open given , with not a collider on and for any collider on that is not a collider on , intersects with only at . By iterative application of this construction we can therefore obtain a path with the required no-intersection but at the colliders property.

To construct this path, let be all nodes on where and intersect, ordered by how close to they appear on . By assumption there are at least two such nodes. Let . We assume for simplicity that points from to . The other case follows by the same arguments.

We first show that is open given . The paths and are open given . We therefore only need to consider the intersection points and . By assumption, may not be a collider on and by the fact that the only node in on is the endpoint node . The node , on the other hand, may or may not be a collider on and may or may not be . If , then by the fact that is open given , must be a collider on . Because points towards , this implies that is also a collider on and therefore is also open given . If and it is a collider on , then by the existence of , and is open given . If is a non-collider, then again is open. We can therefore conclude that is open given .

We now show that has at least one less collider violating the no-intersection but at the collider property. The path either does not contain or . In either case is not a collider on . Further, the only potential collider on that is not necessarily also a collider on , is . But the path does not intersect with but at .

While may or may not be a proper path from to , it must contain a proper subpath that inherits the other two properties we require from , so let denote this subpath. The path is a proper path from to that is open given with not a collider on and no new collider such that intersects with at a node that is not .

We can therefore let be a proper path from to open given , such that for all colliders on there exists a causal path from to , such that and intersect only at . Let a collection of such casual paths corresponding to all colliders on . Set all edge coefficients and error covariances not corresponding to edges either on or on causal paths from to nodes in to . Consider the graph with the coefficient edges dropped. The graph has the following properties: , there exists at most one edge (stemming from ) into in and is also open given in .

We now construct a linear SEM compatible with such that

where we proceed differently in the following cases. First, we assume there exists a path from to in that is open given and that does not contain . Second, we assume that no such path exists.

First, suppose that there exists a path from to in that is open given and that does not contain . We show that there then exists a walk from to open given that does not contain , where we recall that the definitions of an open path and open walk differ. We first show by contradiction that for any collider on , , irrespective of whether is open or not. So suppose there exists a collider such that and consider the causal path from to . The path consists of nodes in and therefore must consist of edges on and the ’s by construction of . As ends with an edge into , the only possible such edge in lies specifically on . Further the node adjacent to may not be a collider on and hence may not lie on any of the paths . Therefore the next edge on is also on . By iterative application we can conclude the same for all other edges on and thus is a subpath of . But then cannot be a collider on and the same argument therefore holds for the two edges into on , but as is a path it cannot contain three edges adjacent to and we get a contradiction. Therefore, we have for any collider on . As is open given it holds that for any collider . Combining with the causal paths from any collider to the node in and back we obtain a walk in from to that is open given and that does not contain . We can therefore conclude that a walk from to that is open given and does not contain exists.

We now use the existence of this walk to construct a Gaussian linear structural equation such that

Consider a Gaussian linear structural equation model compatible with and faithful to , with a diagonally dominant . Set all edge coefficients and error covariances for the edges adjacent to to some value . Then as goes to so do and by Lemma A.5 and by Wright’s path tracing rule. This is not the case for as by the walk we assume to exist, , where is the graph with the edges adjacent to dropped. Choosing sufficiently small we therefore obtain Gaussian linear structural equation such that

We now suppose that all paths from to that are open given contain . As there exists only one edge into in , must be a non-collider on any such path and they are therefore blocked given and . Further, by the fact that for all colliders on any path from to , as shown previously, the addition of to the conditioning set also does not open any new paths from to . It thus follows that and we can conclude that for all models compatible with . The fact that also implies jointly with A.3 that and jointly with that . The latter is true because for any node there exists a path of the form , with possibly . This path consists entirely of nodes in and is only blocked by if one of the nodes on is in . It therefore suffices to construct a Gaussian linear structural equation model compatible with such that and to conclude our claim. By Theorem 57 of Perković et al., (2018), for all Gaussian linear structural equation model compatible with if and only if is a valid adjustment set relative to in . Since this is not the case and therefore there exists a model such that . This implies that the equation is non-trivial in the non-zero entries of the tuple . By the same arguments as given in the proof of Lemma 3.2.1 from Spirtes et al., (2000) the function is equivalent to a polynomial in the non-zero entries of . If we generate the entries according a distribution absolutely continuous with respect to the Lebesgue measure it follows that -a.s. . Similarly, since by the construction of , it follows that -a.s. . Jointly this implies that -a.s., which concludes our proof. ∎

Lemma B.4.

Consider two nodes and , and two node sets and in an acyclic directed mixed graph such that and is generated from a linear structural equation model compatible with . Let . Then implies , where is the graph with the edge removed. Further, if there exists a linear structural equation model compatible with such that .

Proof.

Consider first the special case that , i.e., . In this case and . Therefore the claims follow from the fact that a linear structural equation model is Markov to the graph it is generated according to and that there exists a linear structural equation model faithful to .

Suppose for the remainder of the proof that . We first prove that implies . By the assumption that ,

as and , where we use that the only causal path between and is the edge and Wright’s path tracing rule. As this suffices to show that the distribution of , which is with replaced by , is generated according to a linear structural equation model compatible with . By the fact that linear structural equation models are Markov with respect to the graphs they are compatible with, the claim follows.

For the converse claim we just need to choose a model that is faithful to and after setting , is faithful to . ∎

Lemma B.5.

Consider nodes and in an acyclic directed mixed graph . Let and let denote the graph with all edges out of on causal paths from to removed. Further let be the graph with the edge removed. Then and are the same graph.

Proof.

Clearly, and contain the same nodes. We will now show that and also contain the same edges.

Assume first that . Then and there are also no edges to remove. Therefore, both and are equal to .