An Empirical Study on Ethereum

Private Transactions and the Security Implications

Abstract

Recently, Decentralized Finance (DeFi) platforms on Ethereum are booming, and numerous traders are trying to capitalize on the opportunity for maximizing their benefits by launching front-running attacks and extracting Miner Extractable Values (MEVs) based on information in the public mempool. To protect end users from being harmed and hide transactions from the mempool, private transactions, a special type of transactions that are sent directly to miners, were invented. Private transactions have a high probability of being packed to the front positions of a block and being added to the blockchain by the target miner, without going through the public mempool, thus reducing the risk of being attacked by malicious entities.

Despite the good intention of inventing private transactions, due to their stealthy nature, private transactions have also been used by attackers to launch attacks, which has a negative impact on the Ethereum ecosystem. However, existing works only touch upon private transactions as by-products when studying MEV, while a systematic study on private transactions is still missing. To fill this gap and paint a complete picture of private transactions, we take the first step towards investigating the private transactions on Ethereum. In particular, we collect large-scale private transaction datasets and perform analysis on their characteristics, transaction costs and miner profits, as well as security impacts. This work provides deep insights on different aspects of private transactions.

1 Introduction

Recent years have witnessed an explosive growth of DeFi [26], which provides end users with financial products and services. By June 2022, the Total Value Locked (TVL) of DeFi has reached about $114 billion [23]. Moreover, the number of DeFi wallets has increased to around $4.8 million as of May 2022 [19]. Among all blockchains, Ethereum is the second-largest blockchain by market capitalization and the first to support smart contracts, which are the foundation of DeFi. Nowadays, the majority of DeFi TVL ($91 billion) lies in Ethereum.

Due to the popularity of DeFi platforms and the large amount of money involved, the number of attacks to steal money from them is also arising. Since all transactions in Ethereum need to be broadcasted before mining, every transaction will need to stay in the public mempool for some time. Some attackers have exploited this fact and launched attacks (e.g., frontrunning [17]) targeting pending transactions in mempool. In particular, in frontrunning attacks, an attacker observes a victim transaction in the mempool and launches an attack transaction with certain features (e.g., higher gasprice) so that the attack transaction will be mined before the victim transaction, thus making profits. Another example is the Miner Extractable Value (MEV) [22], which represents the profit that miners can extract from the manipulation of transactions. For example, two MEV Bots have gained $476,000 recently by targeting the stablecoin swaps [7].

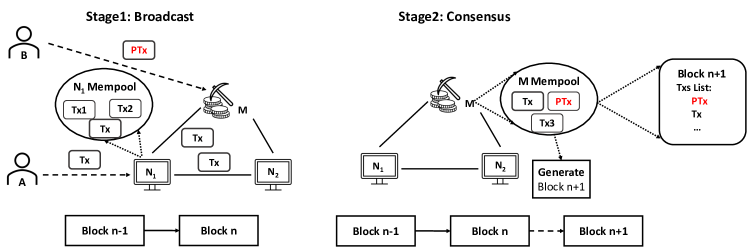

To help protect transactions from being attacked, private transactions were proposed. A private transaction is a special transaction that can be sent directly to miners, bypassing the public mempool (see Fig. 1). By doing so, such transactions remain private (i.e., only present in the target miner’s mempool) until they are posted by the target miner, and cannot be monitored by others. As a result, attackers cannot see these transactions in their mempool, thus thwarting the attacks. Besides being hidden from others, private transactions have a high probability of being packaged to the front position of a new block by the miner and then added to the blockchain. This property also motivates MEV searchers, frontrunning attackers, and arbitragers to seek profit-making opportunities.

It has been two years since private transactions were first introduced by SparkPool in August 2020 [69]. However, private transactions have not attracted much attention from the research community. There are several works that have analyzed the Ethereum blockchain and DeFi platforms, but they mainly focus on 1) detecting bugs from smart contracts [55, 58, 76, 47, 46, 73, 37, 72], 2) measuring Ethereum networks and transactions [49, 14, 88, 4, 67, 52, 86], and 3) analyzing transactions to uncover attacks [87, 83, 66, 63].

To date, however, there are only a few papers [59, 81, 62, 12] that touched upon private transactions as by-products when they study MEVs. However, the scope of private transactions goes beyond MEVs. A complete view of private transactions such as their characteristics and impacts on the Ethereum ecosystem remains unclear. Although the original intention of inventing private transactions is to protect users from attacks, how they are actually used in reality is still an open question.

In this paper, we make the first step towards understanding private transactions and their impacts on the Ethereum ecosystem. Specifically, we conduct a large-scale empirical study on private transactions from three different dimensions: 1) the basic characteristics of private transactions, 2) their economic impacts to Ethereum such as transaction cost and miner profits of private transactions, and 3) their security implications such as the real-world attacks hidden in private transactions. We collect transaction related information from customized Ethereum nodes, and we retrieve public data from Etherscan [33], TradingView [74]. In total, we collect four datasets for our analysis, containing transaction data from May 1, 2021 to April 30, 2022 (one year) and mempool observation data from May 22, 2022 to May 30, 2022 (nine days). Based on these large-scale datasets, we perform a detailed analysis of the basic characteristics of private transactions, their impacts on economics as well as on security. To the best of our knowledge, we are the first to systematically study the private transactions and their impacts on the blockchain ecosystem.

Contributions. This paper makes the following contributions:

-

Large-scale private transaction datasets (Sec. 3). We construct four datasets from public data sources and our modified Ethereum nodes. The datasets include transaction information in a one-year timespan, as well as the DeFi platforms, miners, ERC20 tokens, and MEV Bots involved in each of the transactions. We also build datasets from the local mempools of two Ethereum nodes deployed on two continents, which is used to measure private transaction leakage. To facilitate future research, all the datasets used in our paper will be open-sourced.

-

Characteristics of private transactions (Sec. 4). We study the characteristics of private transactions. We find that during the last year, the percentage of private transactions per month is increasing and rises to about 2% of the total transaction volume. We categorize the purpose of private transactions. Although private transactions were proposed to protect end users from attacks, we find that only 18.1% of them were used for that purpose, whereas 28.6% of them are actually related to MEV Bots. Besides, five of the top ten receivers of private transactions are MEV Bots.

-

Impacts of private transactions on blockchain economics (Sec. 5). We study how private transactions affect the transaction fees and miner profits. We find that the gas used for private transactions is about 737,829 on average, which is much smaller than the average gas used (16,673,757) of normal transactions. We also investigate the impact of EIP-1559 on private transactions. We find that around 50% of private transactions set the gas price at zero before EIP-1559; after EIP-1559, since basefees are mandatory, there are around 22% private transactions setting the priority fee to zero. The revenue of private transactions is an integral part of miner profits, accounting for around 5% of the total revenue.

-

Impacts of private transactions on blockchain security (Sec. 6). We study security issues related to private transactions, including MEV, attack case studies, consensus security and leakage of private transactions. We find that 2.6% private transactions senders earned more than ten ETH as profits via MEV Bots. Attackers have already utilized private transactions to launch attacks [8, 5, 18]; in these attacks, the attackers paid a large amount to the miner as a bribe to get their transactions executed. According to our evaluation, the miner earned as high as 700 ETH for mining a single private transaction. This can lead to serious consensus security issues, such as the undercutting attacks [13, 22]. We also find that private transactions are not always private. By running two Ethereum nodes in two continents for nine days, we have observed 4.3% private transactions in our mempool, which means that they are actually not private. Therefore, users should proceed with caution when sending private transactions.

2 Background

2.1 Ethereum Basics

Ethereum [11] is a public, decentralized, and permissionless blockchain platform, which supports Turing-Complete smart contracts. In Ethereum, nodes, also called Ethereum clients, are connected through a P2P network. Moreover, nodes run a discovery protocol to find other nodes [24] and a TCP-based transport protocol for data communication [25]. In particular, the nodes who have the capabilities to create new blocks are called miners. To produce a new block, a miner has to pack transactions into the block and then solve the difficult puzzle according to the Proof-of-Work (PoW) [29] consensus mechanism. Once mined, the miner broadcasts the block to other nodes for validation and execution. For each new block, miners can receive block rewards and gas fees (introduced shortly) as earned profits. There is a gas limit of the total gas used by the transactions within one block. Note that Ethereum 2.0 will use Proof-of-state (PoS) to replace PoW in the near future [28].

ERC20 tokens. Ethereum Request for Comments 20 (ERC20) [27] is a token standard for fungible tokens, which is the second most popular token type in Ethereum, in addition to ETH. Any user can own and even create such tokens by implementing the required smart contract features, such as transfer(), transferFrom() and balanceOf() functions, as well as related Events.

2.2 DeFi

ERC20 tokens are the most popular tokens created and used by DeFis. DeFis are decentralized financial applications consisting of multiple smart contracts as backends. DeFis mainly serve for borrowing and lending, token exchanging, asset management, and other similar financial functionalities. By February 2022, there are around 4.4 million unique Ethereum addresses that have interacted with DeFi contracts [65].

Stablecoin. Stablecoins are implemented based on the ERC20 token standards to ensure the price stability. For example, Tether (USDT) [70] is a stablecoin with a price pegged to 1 USD. Similarly to other types of ERC20 tokens, they are global to reach in the Ethereum network and exchangeable with any other tokens. As the time of writing, the top three stablecoins by market capitalisation [30] are Tether, USD Coin, and TerraUSD.

2.3 Gas and Fees

To pay for the computational resources to execute a transaction, every transaction is required to pay a fee that is decided by both the gas and the gas price. Specifically, the transaction fee is calculated as: TxFee = UsedGas × GasPrice, where UsedGas refers to the gas amount used for executing a transaction and GasPrice is the amount that the user would like to pay per unit of gas. As previously mentioned, a gas limit is enforced to restrict the total gas used of transactions in each block.

EIP-1559. EIP-1559 [61] is a proposal requiring transactions to pay both the base fee and the priority fee as the total gasprice. Specifically, basefee is algorithmically determined for each block in Ethereum, and the priority fee is the optional fee to motivate miners to include the transactions in new mined blocks. Before EIP-1559, there is no limitation on the gasprice. Users can set zero to the gasprice of their transactions. However, after the EIP-1559 taking effects, the gasprice is required to be equal or higher than the basefee of the mined blocks. On the other hand, the basefee is the minimum gasprice for mined transactions. Generally, miners usually choose the transactions with the higher gas price, since the higher the gasprice, the more profits miners will earn. Besides, to avoid network congestion, the gas limit of each block is doubled from 15,000,000 GWei to 30,000,000 GWei.

2.4 Private Transactions

Private transactions. Every normal transaction has to go through two stages to be mined in blockchain, as shown in Fig. 1. In particular, a user sends a transaction to Ethereum nodes in the p2p network, and all nodes will add this transaction to their local mempool. In contrast, a private transaction is sent directly to the miners and will not appear in the mempool of normal nodes. Then, miners pack these transactions into blocks and put the private transaction in front of the normal transaction. However, there is a price of being a private transaction, which is usually to pay the additional fee by directly sending money during the execution of transaction. Moreover, the private transaction can be leaked as discussed in [32]. We perform experiments to confirm the leakage and discuss the related security issues in Sec. 6.4.

Private transaction relay systems. A relay system is built to provide a private channel for transactions directly being submitted from users to miners. Flashbots [36] are one of such relay systems, and around 90% of miners use Flashbots to earn such extra profits [85]. Firstly, an Ethereum user that is usually a searcher, searches for the MEV opportunities to submit private transactions and such transactions are then packed into a bundle. Secondly, relayers that are bundle propagation services forward the transactions to miners. Finally, miners mine the transactions into the front places of the new mined block as long as they are satisfied with the rewards. The workflow is similar in other relay systems, such as Eden Network [16].

2.5 MEV

Daian et al. [22] first propose the concept of MEV and introduce the potential risks brought by MEV. Although MEV is called miner extractable value, it is usually users, instead of miners, that search for MEV opportunities and share the earned profits with miners. Miners only need to put MEV related transactions to the top places of blocks and take shared profits from users. To compete for extracting MEV, MEV Bots are created to monitor the blockchain network automatically for transactions with potential MEV opportunities and immediately launch related transactions via channels (e.g., Flashbots [36]). Since being coined in 2019, MEV has been intensively studied by researchers [59, 81]. The extensive exploration on MEV might cause instabilities and re-organization on the blockchain network, since miners are incentivized to re-mine blocks. Moreover, users might suffer financial losses if they are attacked or front-run by MEV transactions.

3 Dataset

| Dataset | Timespan | Data Source | Information | Used In |

| One-year Replayed Transaction | One year | Geth Replay | Block info, Transaction info | Sec. 4; Sec. 5; Sec. 6 |

| Nine-day Mempool Transaction | Nine days | Geth Mempool | Tx info received in mempool | Sec. 6 |

| Smart Contract Label | One year | Etherscan, TradeView | Miner, MEVBot, DeFi, Token | Sec. 4; Sec. 5; Sec. 6 |

| Private Transaction Label | One year + Nine days | Etherscan | Private transactions | Sec. 4; Sec. 5; Sec. 6 |

To empirically study private transactions, we extract the necessary data from some reliable data sources including Etherscan Label Word Cloud [34] and TradingView [74], as well as our modified Ethereum nodes. In this section, we explain how we collect data in detail. The datasets and how they are used in later sections are presented in Table 1.

3.1 One-year Replayed Transaction Dataset

We collect the necessary transaction and block information from our customized Geth[31] node in full mode, which is an official Ethereum client implemented in Go language. Specifically, we replay every transaction from May 1, 2021 (block 12,344,945) to April 30, 2022 (block 14,688,626) to extract information and construct our one-year dataset, which contains 446,925,956 transactions in total. We modify the Geth node to collect the following information:

Block information. For every block, the obtained information includes block number, timestamp, miner address, block reward, gas limit, gas used, basefee, and burnt fee.

Transaction information. For each transaction, we first collect the basic information, including hash, block number, success status (0 means failure and 1 means success), sender address, receiver address, ETH value, input, gasused, gasprice, and gasfee. We also collect the following information:

1) Traces: the information of internal transactions that are the smart contract calls within the transaction. Specifically, every internal transaction should record the sender address, receiver address, ETH value, input, and the call graph information.

2) Money flows: token amount, token address, token sender, token receiver, and MFGIndex. In particular, MFGIndex records the index of the position of current money flow among all the money flows that include both ETH and ERC20 token transfers.

3) Money flow graph (MFG): To analyze the used tokens and DeFi platforms, for every DeFi-related transaction, we build a money flow graph (MFG). In MFG, nodes represent the token sender and receiver, and edges indicate the token related information, including MFGIndex, token name, and token amount.

3.2 Nine-day Mempool Transaction Dataset

To measure the leakage of private transactions and see if we can observe any of them before they are mined on blockchains, we deploy two modified Ethereum nodes in two continents from May 22, 2022, to May 30, 2022 (nine days) and collect the received transactions from the local mempool. Note that transactions in the mempool are not yet mined. Specifically, we customized the Geth node to log the hash, block number, timestamp of transactions observed from the mempool of the two nodes. We obtained 6,720,710 transactions from Node 1 and 7,854,054 transactions from Node 2 during the nine days.

3.3 Private Transaction Label Dataset

We obtain the private transactions within both the one-year dataset and the nine-day dataset by crawling Etherscan Label Cloud [34]. Specifically, we observe 7,405,835 private transactions obtained from our one-year transaction dataset and the remaining 439,520,121 are normal (non-private) transactions. We also obtain 232,729 private transactions from the nine-day dataset.

3.4 Smart Contract Label Dataset

To measure the behaviors of different entities involved in the private transactions, for each address in our one-year dataset, we check whether they have the following labels; if so, we collect the corresponding information:

1) Miner: miner address and the related label. We collect the miner address of every block in our dataset and check the address related label111e.g., 0xEA674fdDe714fd979de3EdF0F56AA9716B898ec8 is labeled as Ethermine. from the Etherscan Label Cloud.

2) MEVBot: addresses whose label are MEVBots. For every unique sender and receiver of transactions in our dataset, we check its label from Etherscan. If the label is MEVBot, we collect it.

3) DeFi: DeFi platform address and the related label. Similarly, we collect the addresses which are marked as DeFi by Etherscan, and their labels.

4) Token: For each smart contract labeled as ERC20 token, we obtain the token address and name from Etherscan, and historical price data from TradingView.

4 Characteristics

In this section, we describe the general statistics of private transactions by measuring their categories classified by their purposes, the involved DeFi tokens and platforms, and the involved entities.

4.1 Distribution

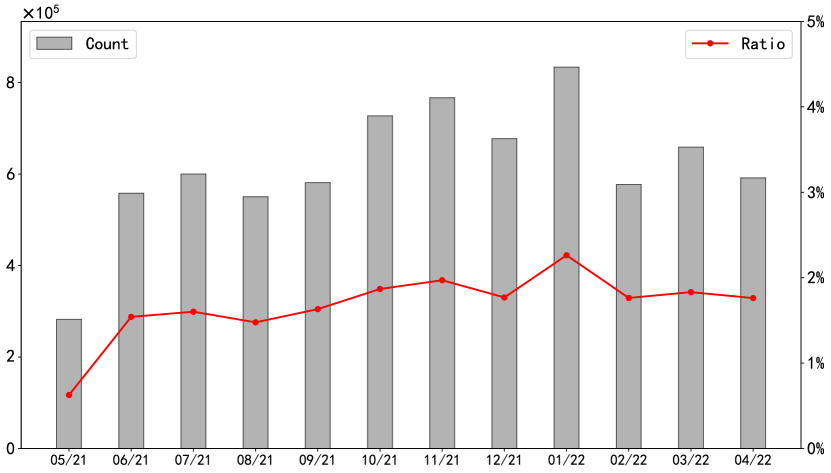

The count and percentage of private transactions. Fig. 2 shows the count of private transactions against per month. There are at least 0.28 million private transactions every month and around 0.60 million private transactions on average per month. Besides, the percentage of private transactions among all the transactions account for 2% on average per month. Overall, there are not many private transactions in the total mined transactions, while the percentage of private transactions keeps increasing slightly every month.

The distribution of private transactions.

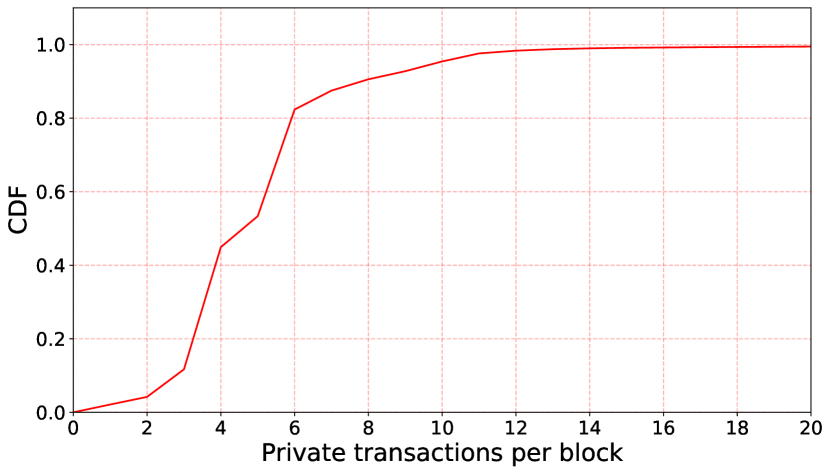

Fig. 5 plots the CDF of private transactions within a single block for the blocks that have at least one private transaction (1,259,251 blocks, 54%). 93.2% of these blocks have less than 10 private transactions, and 99.5% of these blocks have no more than 20 private transactions. Only 0.5% have the count of private transactions greater than 20. The largest count of private transactions in one block is 615.

Abnormal count of private transactions in some blocks. Fig. 3 presents the count of private transactions against per block and also the blocks in the peek periods. There are four ranges of blocks that seem to have far more private transactions than other blocks. The block ranges are [13,404,461 - 13,497,355], [13,926,965 - 13,949,430], [14,057,403 - 14,133,216], and [14,636,264 - 14,664,418], respectively. We show the details of the biggest peek in the figure. In particular, not all blocks have far more private transactions than others, and some blocks have the count of private transactions below the average. In particular, we study the blocks with more private transactions than others and find that many private transactions are used for miners transferring ETH to EOAs. Moreover, the other three peeks have similar patterns.

The positions of private transactions inside blocks. Private transactions are usually bundled together to miners and placed at the top of the block. With the collected 1,259,251 blocks who have at least one private transaction, we observe that all private transactions are located in front of normal transactions in blocks. The results are expected since private transactions are created to race for the opportunities before other transactions. Thus, they should be put in the top positions of the blocks.

4.2 Categories

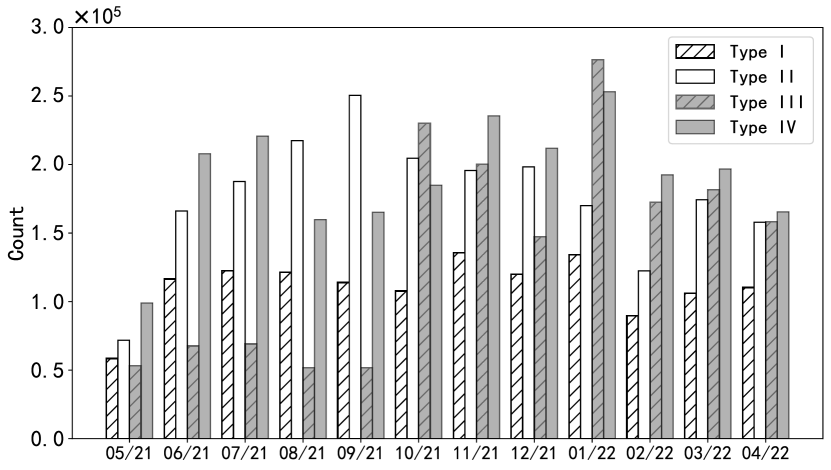

To better measure the usages and draw insights on the purposes of private transactions, we categorize them into the following four types.

-

Type I (Self protection): the private transactions that are only used for DeFi services (e.g., Uniswap trader). Specifically, such private transactions protect themselves from risks in the public mempool, such as frontrunning attacks.

-

Type II (MEV related): the private transactions that MEV Bots participate in. Private transactions of this type should have MEV Bots as their recipients and are usually used for MEV extraction.

-

Type III (Miner payout): the private transactions used to transfer money to EOAs. Private transactions of this type are normally sent from miners or other well-known services and used to transfer ETH.

-

Type IV (Normal services): the remaining private transactions whose receivers are normal smart contracts that cannot be labeled.

The categories of private transactions. We present the count of private transactions of each type against per month in Fig. 4. For type I, about 18.1% of private transactions are sent to call DeFi related services. For type II, there are 28.6% of private transactions that are sent to MEV Bots, which shows the increasing need for private transactions for MEV searchers since the competition of MEV becomes more and more fierce. For type III, 22.4% of private transactions are used for transfers. In particular, the senders of these private transactions are miners and well-known services(e.g., Crypto.com [21]). In addition, the left 30.9% of private transactions belong to type IV. Among them, about 650,000 transactions are used for transferring tokens through the smart contracts.

Finding 1: Only 18.1% of the total private transactions are used for the original purpose—protecting DeFi services from attacks. More private transactions (28.6%) are used by MEV Bots in search of MEV opportunities. The actual usage of private transactions has departed from its design purpose.

4.3 DeFi Tokens and Platforms

Most Private transactions are used to interact with the tokens for different purposes mentioned in Sec. 4.2. We first briefly describe some features of the tokens in private transactions, to give an overview of the usage of tokens. Moreover, we classify the token exchange pattern into different types according to the token exchange count and token types. Then we demonstrate the usages of DeFis among the private transactions and the related tokens, for further deep analysis.

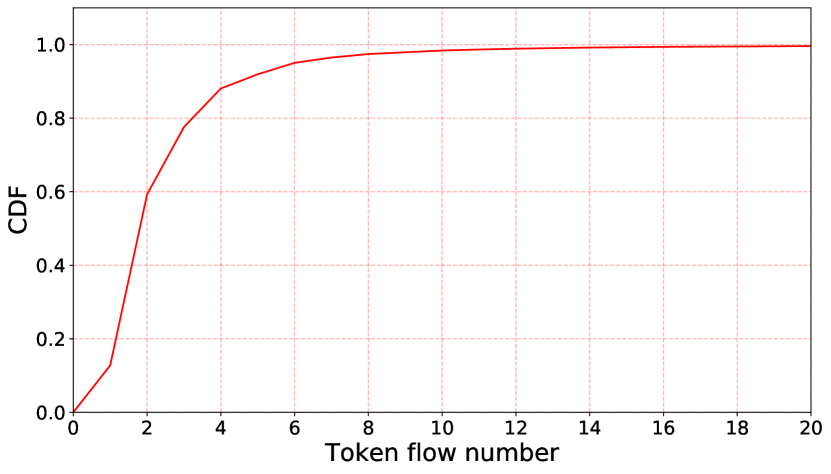

The distribution of token flow number in private transactions. We present the distribution of token flow numbers of transactions that have at least one and no more than 20 token flows (99.6% of 5,746,633 private transactions) in Fig. 6. We exclude 1,659,202 private transactions without token flow. From the figure, around 88% transactions have no more than 4 token flows. In particular, the private transaction 2220x470ceedf30f8c1c533b0911c2b37ab1c55b0cbd83d1e40c0d44cd7e9f5db1569 has the most token flows (600).

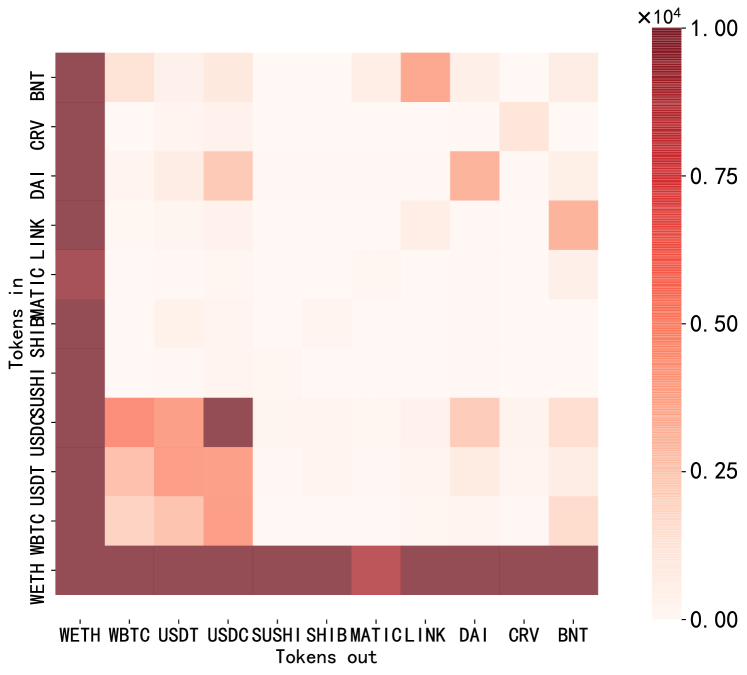

The top token exchange pairs in private transactions. We measure the most frequently used token exchange pairs of the private transactions in Fig. 7. From the figure, we observe that the exchanges from the stablecoin USDC to WETH takes the most portion. In addition, the top token exchange pairs usually contain WETH and stablecoins. It is expected that such tokens are popular on exchanges, since they are less subtle to market changes and more valuable to keep.

The token swap patterns in private transactions. To present more details of the complexity and behaviors, we classify the token swap patterns in private transactions into the following five types and measure them.

-

Type I: involving in one token type.

-

Type II: involving in two types of tokens and two token transfer edges.

-

Type III: involving in two types of tokens but more than two token transfer edges.

-

Type IV: involving in three types of tokens.

-

Type V: involving in more than three types of token.

In total, we discover 5,746,633 private transactions involved in tokens, which accounts for around 78% among all the private transactions. Specifically, the private transactions that only exchange two types of tokens (type II and type III) accounts for about 69% among all types. Moreover, the percentage of Type V is around 2.2%, which is the smallest among all types.

The top DeFi services used by private transactions. We measure the count of private transactions against every DeFi. Specifically, the top 3 DeFis are Uniswap V2 [77], Uniswap V3 [78], and SushiSwap [68], which are related to 558,919, 332,058, and 177,055 private transactions respectively. Moreover, more than 60% of the private transactions are used for tokens swap in DeFi markets.

4.4 Entities

We evaluate the entities involved in private transactions, to give an overview of the general distribution of different entities. In particular, we measure the top senders, receivers, and miners.

Sender. Senders of transactions are EOAs. To give an overview of the senders, we measure the top 10 senders and the count of sent private transactions. In total, 1,147,181 private transactions are sent from the top 10 senders, which is about 15.5% portion of the total private transactions. The miner address Ethermine:0xEA674f is the 1st largest sender creating 581,086 private transactions. It mainly uses private transactions to transfer money to other addresses for redistributing mining income. Another special sender is Fund:0x0F4ee9, which is related to investment or venture funds and ranks in the top 8 for sending out 43,995 private transactions. Such Ethereum addresses that are labeled as Fund are usually users who own lots of ETH for fund. Moreover, the rest of the top senders are all normal EOAs.

Receiver. Receivers are the target addresses of transactions, which can either be smart contracts or EOAs. We measure the top 10 receivers that are related to 2,275,695 private transactions, accounting for about 31% in total. Specifically, all the top 10 receivers are smart contracts. From Table 2, there are 5 MEV Bots involved in 1,037,924 private transactions. In addition, there are 1,237,771 private transactions involving in 4 receivers that are DeFis addresses. These DeFi addresses belong to Uniswap and SushiSwap. Morever, the left top receiver is Tether USDT stable coin address. Private transactions calling this address usually are used to transfer the Tether USDT to others.

| Label | Receiver Address | Count |

| Uniswap | 0x7a250d5630B4cF539739dF2C5dAcb4c659F2488D | 558,919 |

| MEV Bot | 0xa57Bd00134B2850B2a1c55860c9e9ea100fDd6CF | 412,563 |

| MEV Bot | 0x00000000003b3cc22aF3aE1EAc0440BcEe416B40 | 222,829 |

| Uniswap | 0xE592427A0AEce92De3Edee1F18E0157C05861564 | 216,791 |

| SushiSwap | 0xd9e1cE17f2641f24aE83637ab66a2cca9C378B9F | 177,055 |

| Token | 0xdAC17F958D2ee523a2206206994597C13D831ec7 | 169,739 |

| MEV Bot | 0x1d6E8BAC6EA3730825bde4B005ed7B2B39A2932d | 151,668 |

| MEV Bot | 0x000000000035B5e5ad9019092C665357240f594e | 138,867 |

| Uniswap | 0x68b3465833fb72A70ecDF485E0e4C7bD8665Fc45 | 115,267 |

| MEV Bot | 0x4d246bE90C2f36730bb853aD41d0a189061192d3 | 111,997 |

| Miner | Blocks with private transactions | Direct payment | As a sender | Total private transactions |

| Ethermine | 316,774 | 482,894 | 581,086 | 1,063,980 |

| F2Pool | 168,442 | 174,541 | 5,251 | 179,792 |

| Spark Pool | 143,767 | 310,958 | 969 | 311,927 |

| Hiveon Pool | 80,937 | 57,088 | 1,872 | 58,960 |

| Flexpool.io | 46,365 | 93,563 | 484 | 94,047 |

| MiningPoolHub | 41,701 | 63,691 | 28,010 | 91,701 |

| Miner:0xb7e…707 | 41,360 | 39,909 | 81 | 39,990 |

| 2Miners:PPLNS | 36,657 | 39,967 | 1089 | 41,056 |

| Nanopool | 35,541 | 25,881 | 74 | 25,955 |

| BeePool | 33,533 | 82,797 | 1,728 | 84,525 |

Miner. In total, 278 miners have been identified and 145 of them have mined blocks with private transactions. We list the top 10 miners in table Table 3, which are sorted by the number of their mined blocks containing private transactions. Specifically, the table shows the miner, the number of blocks, the number of private transactions with direct transfer to the miner, and the number of private transactions sent to the miner of the top 10 miners. Generally, the more blocks the miners have mined, the more private transactions with direct transfers will be included and the more profits the miners will earn. In addition, Ethermine and MiningPub send lots of private transactions. We conjecture that these two mining pools are required to redistribute the earned profits frequently or there are many miner nodes in the two mining pools. Moreover, Sparkpool (which first introduced private txs) and BeePool stopped mining since September and October of last year, respectively.

5 Transaction Cost and Miner Profits

In this section, we analyze the transaction cost including used gas and gas price, and measure the miner profits in terms of the distribution, detailed income, and flows.

5.1 Transaction Cost

To present the detailed cost of the transaction fee, we measure the gas used and the gasprice settings from private transactions.

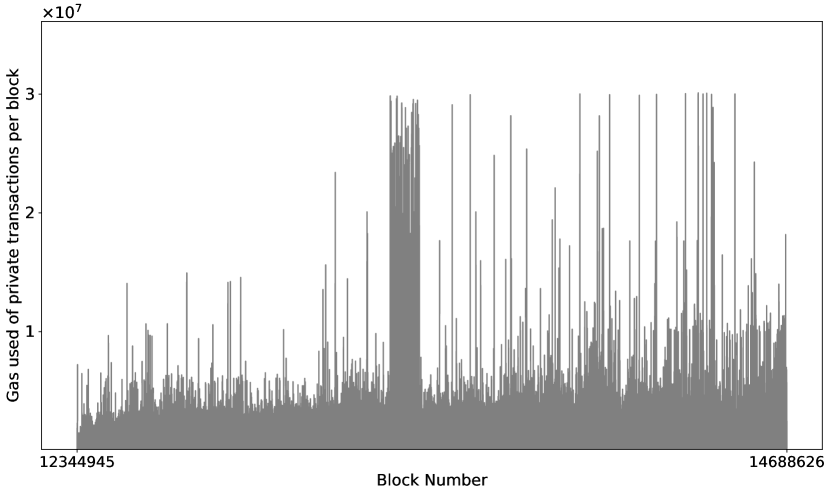

The used gas of private transactions. Fig. 8 presents the gas used of private transactions against per block. The total gas used for private transactions in each block is about 737,829 on average, which is much smaller than the average gas used (16,673,757) of normal transactions. Particularly, there are some blocks where the gas used of private transactions takes a large portion of the total gas used. It is obvious that transactions in such blocks are mostly private transactions. For example, the blocks starting from 13,403,072 to 13,497,355 have a high percentage of gas used by private transactions, which also relate to the first abnormal period in Sec. 4.1. For another example, block 14,520,420 has only one transaction and this transaction is a private transaction. Meanwhile, there are 367 blocks in total whose used gas percentage by private transactions is 100%. In particular, 361 blocks are mined after the gas limit expansion and 6 blocks are mined before the expansion.

Moreover, we observe that the expansion of the gas limit helps the growth of private transactions. Before the gas limit expansion in block 12,965,000, the used gas by total transactions is about 99% of the gas limit on average. It shows that the Ethereum network is somehow crowded and transactions are awaiting to be mined. Besides, after the gas limit is increased, miners have the ability to pack more transactions. Accordingly, the number of private transactions in blocks can be dynamically increased.

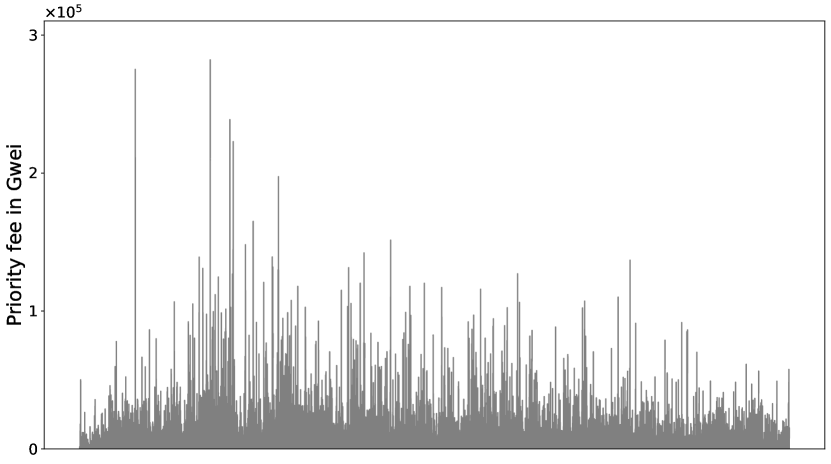

The gasprice setting in private transactions

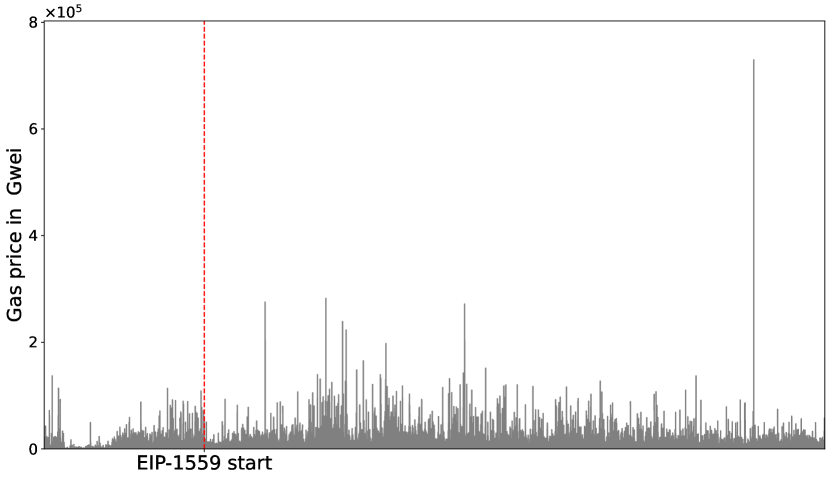

We measure the gas price against every private transaction in Fig. 9. Particularly, we study the influences of EIP-1559 to gas price of private transactions. In total, there are 1,528,843 private transactions before EIP-1559 and 5,876,992 after EIP-1559.

Before EIP-1559, the average gas price of the private transactions is around 93.3 Gwei. Moreover, the gas price of 771,979 private transactions are set to be 0 accounting for 50% of the total. Generally, miners will not pack transactions with 0 gas fee into the blocks since they are incentived to max their profits. However, such private transactions will pay the earned profits to miners via the direct transfer in the transactions. These transactions with 0 gas price are distributed in 318,375 blocks. In particular, blocks containing transactions with 0 gas price at least include one direct payment transfer from private transactions to miners, which proves that private transactions indeed bring profits to miners. Moreover, the average transfer of these private transactions is around 0.214 ETH. Detailed miner profits will be analyzed later in Sec. 5.2.

After EIP-1559, the average gas price of all private transactions is around 189 Gwei. Specifically, we observe that the transaction3330xba5a6f7970f5ff78786bb318085f2b6789488827dfec4f8ceed67e289728a7ee with the highest gas price (729,541.97 Gwei) is from a transfer to an EOA address and the total transaction fee is 15.32 ETH. As required by EIP-1159, the gas price is not allowed to be 0 due to the basefee. Private transactions should pay both basefee and priority fee that is the tip for miners, as their gas price. To further measure the transaction fee after EIP-1559, we measure the priority fee against every private transaction after EIP-1559.Some private transactions did not set the new gas properties such as priority after EIP-1559, and we got 4,105,987 private transactions with priority set in Fig. 10. Among these private transactions, the private transaction 4440xc9951933b0aef59f60b5421d39ab89c30ee48be15d80a0db69cdfbe9f72e874a pays the highest priority fee, only transfers 1 GWei from the sender to the sender itself, of which the priority fee is around 282,093 GWei. In total, the private transaction pays around 6 ETH as the transactions. To our knowledge, we doubt that the high-priority fee of this transaction is mistakenly set. In addition, there are 1,266,449 private transactions whose priority fee is 0,which takes around 22% of the total private transactions. Moreover, 96.5% of them are sent to call MEV Bots. Transactions with 0 priority fee are distributed in about 615,508 blocks and all of these blocks contain at least one direct payment from private transactions to miners. The average transfer amount is around 0.14 ETH. As we stated before, while the profits will decrease due to the 0 priority fee, miners are still willing to pack such private transactions into the blocks due to the direct transfer serving as a bribe.

Finding 2: Some private transactions (around 50% before EIP-1559 and 22% after) do not use gas fees as rewards to the miners. Instead, MEV profits are distributed to the miners via direct transfers.

5.2 Miner Profits

In this section, we investigate the mining profits and the flows of the earned profits to assess the impact of private transactions on the miners.

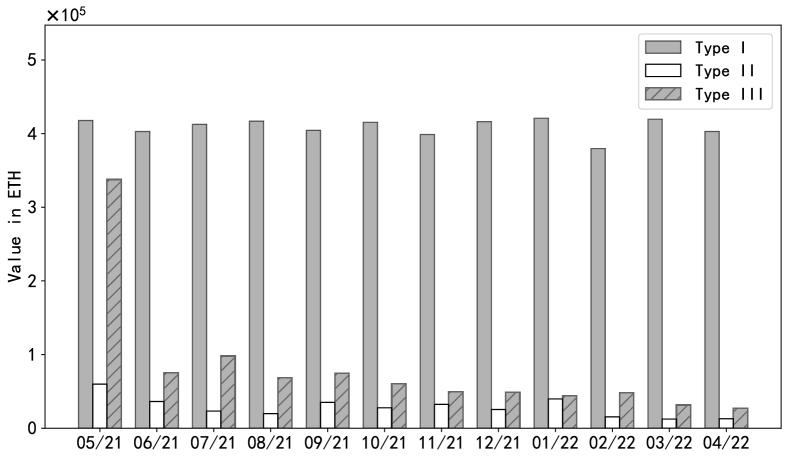

The distribution of total profits. Miners mainly gain benefits from the following three types.

-

Type I: Block reward. The reward consists of both normal and uncle blocks payouts.

-

Type II: Profits from private transactions. The profits include both transaction fee and the bribe to miners in private transactions. Specifically, basefee in private transactions will be burnt by the network and deducted from the earned transaction fee for miners.

-

Type III: Profits from normal transactions. The profits include both transaction fee and the bribe to miners in normal transactions. The same as Type II, the earned transaction fee in normal transactions will remove basefee.

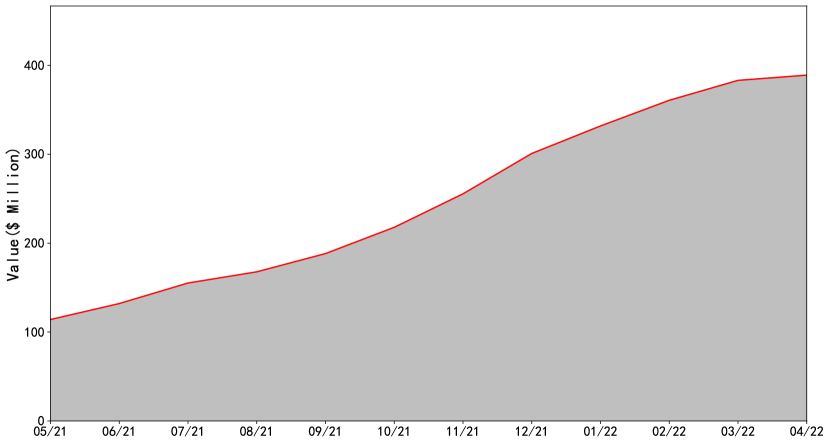

We show the profits of each type earned by the miners per month in figure Fig. 11. From the figure, most of the profits of miners come from the Type I and the amount of the profits, which are almost the same in every single month. For Type II, the average monthly profits of the miner is 28,122.8 around ETH, accounting for about 5% of the total miner profit of per month. Besides, we observe that the profits of Type III is pretty high in May 2021. The reason is that there are about 45 million transactions in that month, which is higher than the average count of 36.5 million.

| Miner | Transfer from private transactions (ETH) | Transfer from normal transactions (ETH) | Total (ETH) |

| Ethermine | 59,072.95 | 46,246.64 | 105,319.59 |

| F2Pool Old | 63,574.24 | 40,400.79 | 103,975.03 |

| Spark Pool | 20,578.58 | 164.34 | 20,742.92 |

| BeePool | 5,677.03 | 40.81 | 5,717.84 |

| Flexpool.io | 5,002.37 | 73.42 | 5,075.79 |

| Hiveon Pool | 4,631.24 | 84.45 | 4,715.69 |

| MiningPoolHub | 3,057.21 | 277.08 | 3,334.29 |

| 2Miners:PPLNS | 2,443.37 | 127.89 | 2,571.26 |

| Miner:0xb7e390 | 2,210.07 | 21.79 | 2,231.86 |

| Nanopool | 1,708.91 | 57.67 | 1,766.58 |

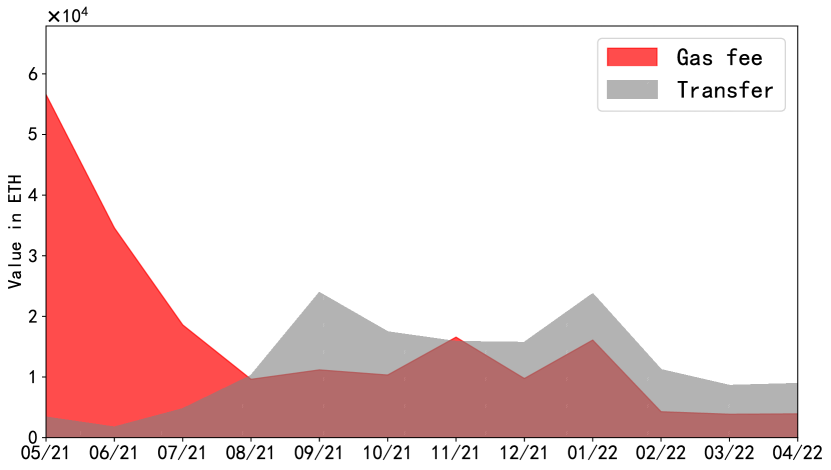

The distribution of profits from private transactions. In particular, we present the transaction fee and direct transfer to miners of private transactions against per month in Fig. 12. In total, around 23% of all private transactions transfers money to miners, and the total transferred amount is around 195,381 ETH, which accounts for around 58% among the total revenue of 337,474 ETH form private transactions. In the figure, the profits from the direct transfer exceed the transaction fee in some months. The reason is that some private transactions set low priority fee and pay the miners with the direct transfer. Additionally, we list the top 10 miners sorted by the income from direct transfers of private transactions in Table 4. Specifically, the income of the top 3 miners accounts for around 90% of the total. From the table, we notice that most of the transfers come from the private transactions, which demonstrates that private transactions bring in a lot of money for miners.

The flow of earned profits from miners. We observe that miners frequently transfer a certain amount of ETH to others. For example, some miners usually send 0.02 ETH to particular addresses. These transactions are used by miners to redistribute the income to the mining nodes 555A miner normally groups multiple mining nodes into a pool to combine the computation powers, and then splits the rewards to these mining nodes [6]. that perform the mining work. The money is to reward the computation power of these nodes. Specifically, the profit redistribution transactions is always private transactions for two reasons. The first reason is that miners are capable of sending transactions by themselves to avoid the long waiting time in blockchains. The second reason is that miners can save money since they do not have to pay the priority fee and earn the basefee they pay.

| Address | Txs Inbound | Total Miner Inbound | Private txs Inbound | Txs Outbound | Exchange Outbound |

| 0x909bFe | 509 | 509 | 58 | 152 | 152 |

| 0x18690F | 492 | 468 | 67 | 191 | 185 |

| 0xE426ec | 476 | 476 | 64 | 49 | 49 |

| 0xa4C916 | 327 | 312 | 72 | 23 | 23 |

| 0xbaAa28 | 341 | 341 | 52 | 4 | 0 |

To study the detailed flows of the profits of the miner, we performed a case study on the top miner Ethermine who sends out 581,086 private transactions. We list the top five addresses receiving the largest number of private transactions from Ethermine in Table 5. These five addresses are all EOA addresses. From the table, we observe that most of such addresses are used as the wallets of miner nodes, which normally receive the profits from Ethermine and then withdraw money. For example, the address 6660x909bfe97a6f77d2bec31b4c19e8c2810136abb90 receives 509 transactions and all are transfers from miners, in which 58 transactions are private transactions. Additionally, the address sends out 152 transactions to withdraw money from their personal wallets via DeFi platforms (e.g. Binance). The behaviors are pretty similar for the other four addresses. With the investigation, we have a better understanding of the money flows of the miner profits.

Finding 3: Miners take a major share of the profits of private transactions. Miners, in turn, re-distribute the profits to mining nodes via private transactions, rewarding their contribution in the computing power.

6 Security-related Issues

In this section, we present the measured results to quantify the related security issues, including MEV, real-world DeFi attacks, consensus security, and private transactions leakage. Moreover, we perform detection on private transactions from our one-year dataset in Appendix to study arbitrage, which is one popular type of MEVs.

6.1 MEV

The earned profits by MEV Bots. We have identified 143 MEV Bots participating in the total private transactions and they are involved in 2,116,587 private transactions. Among these private transactions, 766,640 of them are identified to gain profits. Table 6 shows the private transactions distribution of the earned profit. Specifically, 2.6% calling MEV bots gain more than 10 ETH as profits, while 92.8% earn less than 1 ETH. Furthermore, we find the average transaction cost of these private transactions is around 0.005 ETH and 60% of them share the miner with an average transfer of 0.2 ETH. Moreover, we identify about 3% of these private transactions ending up with negative pure profits after deducting transaction cost and miner profit share from the earned profits.

| Profit Range (in ETH) | [0,1) | [1,10) | [10,50) | [50,100) | |

| Count | 711,441 | 35,265 | 7,794 | 2,830 | 9,241 |

| Percentage | 92.8% | 4.6% | 1.02% | 0.37% | 1.21% |

Failed transactions. Generally, users need to pay the transaction fee even though their transactions fail, of which the fee is decided by both gas price and used gas. However, before EIP-1559, the gas price can be set to 0 and users can pay nothing for transactions, regardless of whether they fail or not. Transactions with 0 gas price are not usually mined to blockchains since they give miners no profits in terms of the transaction fee. But with the appearance of private transaction, users pay or bribe miners by directly transferring money to them. Thus, miners are willing to mine such transactions. Specifically, we observe 94 private transactions fail before EIP-1559 within our dataset and 58 of them have 0 gas price. Although EIP-1559 forces the transactions to pay at least the basefee, private transactions users can set the priority fee to 0, to reduce the potential loss if their transactions fail. We observe 19,762 failed private transactions and 577 of them have 0 priority fee after EIP-1559.

Finding 4: Allowing zero gas price before EIP-1559 in private transactions enables attacks with no economic loss, whereas the basefee introduced by EIP-1559 increases costs for failed attacks.

6.2 Attack Case Studies

We investigate three DeFi related attacks that are exploited via private transactions. Specifically, we perform case studies on PolkaBridge [60], LI.FI [51], and Multichain [56] attacks. Moreover, we measure the top 30 private transactions according to the money transferred to the miners and the top 10 blocks sorted by the amount of profits from the miners.

PolkaBridge Attack. PolkaBridge is a cross-chain DeFi and the first to decentralized bridge between Polkadot platform and other blockchains. Polkadot [82] is a blockchain protocol connecting multiple blockchains into one unified network. PolkaBridge mainly is used to support the token exchanges between multiple blockchains, which is also what the bridge aims to. PolkaBridge was attacked due to a smart contract logic error at Nov-22-2021 07:44:02 AM +UTC. In particular, an attacker can withdraw tokens that did not belong to them by simply calling the related function. Moreover, The attacker stole around $632K worth of assets via the transaction7770x36d2f3aaf7d160ea9bd072692555e6d3ff9b76139c8dfa83a475b23cc39cf8e6.

As labeled by Etherscan, this transaction is a private transaction in Ethereum blockchain and mined in block 13,663,243. Besides, the transaction was placed in the first place inside the block by miner Poolin 38880x2a20380dca5bc24d052acfbf79ba23e988ad0050. Specifically, the attacker set the priority fee at 0 and transferred 60.1012422 ETH to the miner as a bribe. This attack case shows that attackers can utilize private transactions to collude with miners and attack the exploited platforms. As far as we know, there is no related report or paper that analyzes the bribe to the miner. We are the first to investigate the relationship of attack, miner, and private transaction.

LI.Fi Attack. We studied another attack on DeFi platform LI.FI supporting cross-chain bridging, swapping, and messaging. The services provided by LI.FI are similar to the services from PolkaBridge, which are for token exchanges between multiple blockchains. According to the report [8], LI.FI was attacked due to the unchecked external call vulnerability in smart contracts. The attack happened on Mar-20-2022 02:51:44 AM +UTC via the transaction9990x4b4143cbe7f5475029cf23d6dcbb56856366d91794426f2e33819b9b1aac4e96, which caused a huge financial loss around $596K. Moreover, the transaction was mined in block 14,420,687 and the miner was MiningPoolHub. As expected, the transaction was placed in the first place inside the block.

Although the attacking transaction is label as private transaction by Etherscan, the attack did not share the earned profits with the miners. After investigating the token flow of the attacking transaction, we did not find any direct transfer to the miner and the priority fee was set to be 2.2 GWei. We suspect that the fee of launching a private transaction was paid off-chain by the attacker. From these two attacks, we can conclude that attacking transactions have the urges to not be monitored by others and placed in the front of the blocks, in case that attack competitors take the opportunity away.

Multichain Attack. Multichain is also a DeFi platform for cross-chain services. It was attacked due to the unauthorized permission, according to the report [5]. Specifically, the vulnerable smart contract function did not validate the token input parameter and the call being successful or not. Moreover, Multichain was attacked by at least three attacker groups; there were multiple attacking transactions and the total stolen amount was estimated to be around $3 million. After investigation, lots of them are labeled as private transactions.

In particular, we studied the attacking transaction 1010100xe50ed602bd916fc304d53c4fed236698b71691a95774ff0aeeb74b699c6227f7 with the highest financial loss, accounting for 308 ETH (around $950K). This transaction behaves as the attacking transaction in PolkaBridge attack. Similarly, it set the priority fee to be 0 and shared 274.686613834949640784 ETH to the miner. Moreover, the from address1111110xfa2731d0bede684993ab1109db7ecf5bf33e8051 is labeled as both Multichain Exploiter 4 (the fourth found attacker exploiting this attack) and Whitehat (who aims to rescue the attacks). The reason is that at first the address hacked the smart contracts for attacks and then agreed to return part of the earned profits after negotiation [18]. In addition, transaction is placed at the very beginning of the block 14,037,237 by the miner Ethermine1212120xea674fdde714fd979de3edf0f56aa9716b898ec8. For another example, attacking transaction 1313130x6e26e226d81563a96e6aa9423b1301ce798242b5b4387ad7b9ac5b66966c2a44 (labeled as a private transaction) was launched by another attacker address1414140xd37448ad7949c4ad8eba5aad1a0afdd3199971d8, which is labeled as Multichain Exploiter 7. The patterns between the two attacking transactions are exactly the same. From these example transactions, we observe that private transactions indeed help the attackers to take the priority for attacks.

Finding 5: Real world attacks have used private transactions to seize the fleeting attack opportunities. In some cases, the miners take a major share of the profits, making them unwitting accomplices in these attacks.

6.3 Consensus Security

We measure the most profitable private transactions from the user side and blocks for the miner side, and find that private transactions have threats on the consensus security. Specifically, the huge profits brought by private transactions increase the risks of undercutting attacks.

The top 50 private transactions. After manually checking the top 50 private transactions sorted by the transfer amount to miners, 49 of them are related to MEV and 1 is related to real-world attacks, which is the Multichain attack we mentioned above. In addition, MEV related transactions are used for arbitrage (34 among 50 private transactions) or liquidation (15 among 50 private transactions). For arbitrage, these private transactions usually interact with Uniswap, SushiSwap, and Curve. For liquidation, private transactions are usually sent to Aave, dYdX, and Compound. Specifically, the most profitable transaction 1515150x3b5fc9f804e026a23f1474218bc9d15e69a4fded405c8ffda0beb028e9d61c53 is used for arbitrage. It earns 729.6836279 ETH and shares 706.3337518 ETH with the miner. Besides, the private transaction costs 0.03407946836279 ETH as the transaction fee, while the priority fee is set to 0.

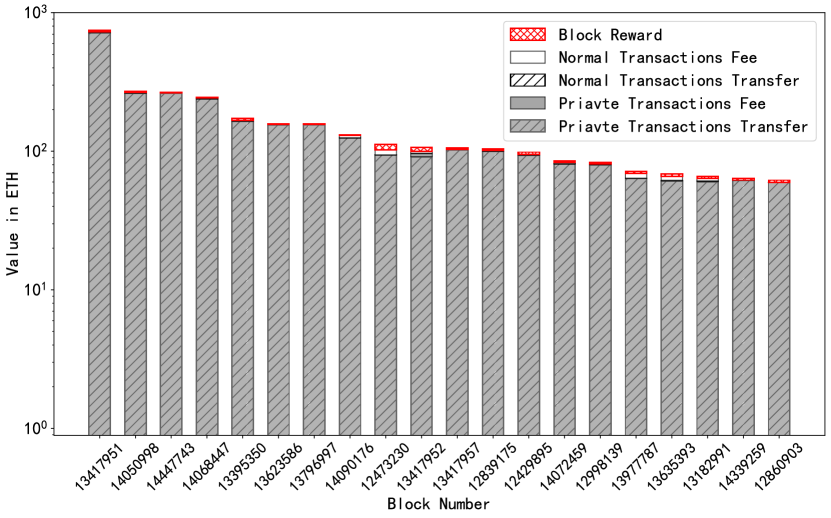

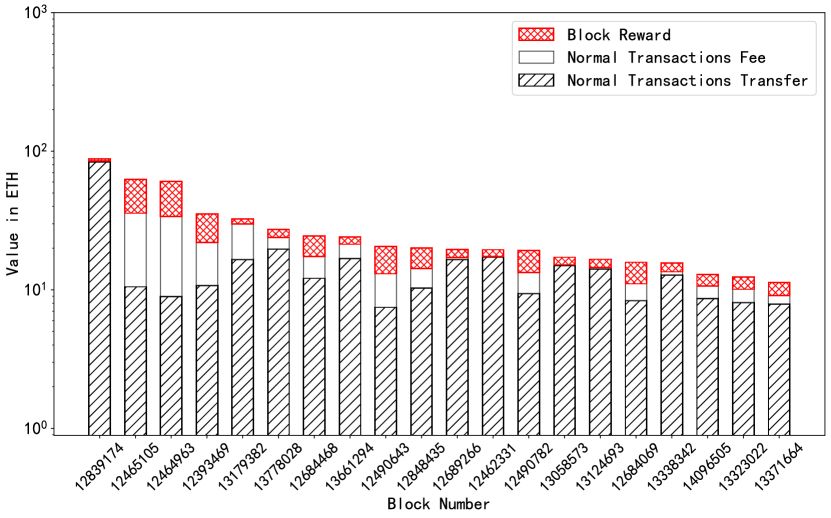

The top 20 blocks. To study the influences of private transactions, we present the top 20 blocks that earn the most profits in Fig. 13(a). From the figure, we observe that most of the profits in the top 20 blocks come from the direct transfers from private transactions to miners, which takes around 90% among the total profits in blocks. In particular, the top block is 13,417,951 and earns around 747 ETH, in which the transfer from private transactions is about 714 ETH. The most profitable private transaction we mentioned above comes from this block and transfers 706.3337518 ETH to the miner. We can learn that other profits types only take a very small portion. For comparison, we show the top 20 blocks without private transactions in Fig. 13(b), sorted by the earned profits from miners. The most profitable block 12,839,174 earns around 88 ETH, which is far less than the profits from top blocks with private transactions in Fig. 13(a). Moreover, the results shown in Fig. 13(b) are comparable with those presented by Daian et al. [22]: the most profitable block (block 7,029,147) resulted in around 100 ETH profit as well.

Undercutting attacks. An undercutting attack happens when the profits from transactions exceed the block rewards, in which miners deliberately fork the existing blockchain and leave these profitable transactions unclaimed, in order to attract other miners to create new blocks on the undercutting blockchain. To successfully launch the undercutting attacks, attackers need to give enough money incentives to the miners since the main goal of a rational miner is to maximize its profits. Previously, Carlsten et al. [13] consider the transaction fees as the only factor that causes undercutting attacks; In [22], it also takes Ordering Optimization (OO) fees (including MEV) into account. According to Gong et al. [39], before private transactions were introduced, the money deliberately left by attackers may not be enough to incentivize the miners to launch the undercutting attack. For instance, the transactions that are left for attracting miners might not be able to fit into the blocks. However, from the above experiments measuring the top 20 blocks in both private transactions and normal transactions (Fig. 13(a) and Fig. 13(b)), private transactions greatly increase the incentives for undercutting attacks; miners can easily find the most profitable private transactions and place them into the new block by squeezing out the less profitable ones. Therefore, we find that private transactions can be a potential driving factor that leads to undercutting attacks since the block rewards are far lower than other profits, especially the direct transfers from private transactions.

Finding 6: Private transactions exacerbate threats to consensus protocols. The huge profits brought by private transactions might provide the miners additional incentives to launch undercutting attacks.

6.4 Leakage of Private Transactions

We notice that there are some inaccuracies of the private transactions label from Etherscan. For example, the transaction 1616160x8d0c16210335a9ee8815d7b0dba22134f9dc722047e8f2d67399184cd92c420f is labeled as a private transaction in Etherscan, but found it in our local mempool.

| Date | Node 1 View | Node 2 View | Two Nodes Combined | Labeled by Etherscan | Found in mempool |

| May 22 | 726,225 | 935,288 | 1,015,771 | 32,831 | 1,272 (3.9%) |

| May 23 | 735,962 | 1,025,886 | 1,060,942 | 24,162 | 1,350 (5.6%) |

| May 24 | 766,517 | 1,035,457 | 1,059,803 | 33,787 | 1,381 (4.1%) |

| May 25 | 739,896 | 971,091 | 1,010,729 | 30,708 | 1,686 (5.5%) |

| May 26 | 776,464 | 1,000,375 | 1,011,134 | 21,669 | 1,109 (5.1%) |

| May 27 | 727,589 | 1,010,602 | 10,20,657 | 31,642 | 1,346 (4.3%) |

| May 28 | 760,488 | 987,575 | 1,027,682 | 26,772 | 1,047 (3.9%) |

| May 29 | 752,500 | 951,380 | 1,005,138 | 31,158 | 1,072 (3.4%) |

| May 30 | 735,069 | 971,857 | 1,041,587 | 32,831 | 1,319 (4.0%) |

To study the inaccuracies, we deploy two modified full nodes in two continents to monitor the transactions coming to the local mempool from the nine-day dataset. Then we compare the transactions collected from the mempool of two nodes with the private transactions from Etherscan and present our results in Table 7. From the table, we observe a 4.3% leakage in 9 days with the two nodes. We suspect that some private transactions are leaked due to the uncle block, block reorganization, the orphan transaction, the loss with the low gasprice, and so on. For example, when a private transaction is successfully packed into the block but is then considered as an uncle block, private transaction will be released to the local mempool of every node.

The leakage of private transactions will harm the profits of users. For example, if the user of a transaction exchanges a large amount of tokens and tries to avoid being monitored by others, he/she will submit a private transaction. However, assuming the private transaction is leaked and frontran by MEV Bots, it will cause a huge financial loss to the user. Similarly, the leakage can cause the failure of MEV opportunities. For instance, if the MEV related private transactions is leaked into the mempool and placed in the lower places of the mined blocks, the competitors are likely to take advantage of the MEV opportunity before them.

Finding 7: We observe private transaction leakage from our two local Ethereum nodes. Therefore, private transactions are not guaranteed to be absent from the public mempool; they may still be vulnerable to attacks.

7 Discussion

Limitations. In this paper, we use the labels from Etherscan as our ground truth, similar to previous works [48, 79, 3]. Etherscan is trusted by the community that it has a clear and comprehensive view of the labels, since Etherscan has reliable data sources. For private transaction labels, Etherscan deploys Ethereum nodes deployed over the world to capture private transactions. Besides, they fetch the data from private transaction service providers (e.g., Flashbots [36]) to label these transactions. For instance, there is a label called Flashbots in Etherscan Label World, which provides all the private transactions coming from Flashbots. However, Etherscan might still have mis-labeled data on private transactions. To enhance the authenticity of the private transactions labels, we may consult other third-party mempool services (e.g., BLOXROUTE [9]) and cross-check their labels with Etherscan’s labels. We leave this as our future work.

Future extensions. As stated in Sec. 6.4, there is private transaction leakage at around 4.3% percentage. The leaked private transactions against their intentions and may harm the profits of their users. We can analyze the purposes and usages of these private transactions and study the potential risks. Besides, there are 299 private transactions are leaked not due to the uncle blocks. It might bring some interesting insights to measure how they are leaked. Moreover, in this paper, we perform analysis on arbitrage in private transactions in the Appendix. It would be interesting to measure other attacks such as sandwich attacks and flashloans in the private transaction pool. We leave these to the future work.

Ethereum 2.0. Ethereum will move from PoW to PoS and replace miners with validators. Users can become validators as long as they stake 32 ETH as collateral that encourages them to behave well. Specifically, validators are either chosen to create blocks or responsible for validating blocks. With the upgrade of the consensus layer, private transactions will not disappear. Instead, MEV opportunities will attract more users to stake Ether and become validators since validators can earn huge profits from the private transactions. However, the difference of income between validators who are responsible to attest the blocks and the validators who are randomly selected to create blocks will increase significantly. In particular, users that have a large validator stake are likely to have more blocks to create and obtain more rewards from the MEV related private transactions. Thus, they earn more and have more to stake. Therefore, the impact of private transactions on Ethereum 2.0 is worth investigating, and Ethereum 2.0 will also affect the private transactions.

Private transactions on other blockchains. Similar as Ethereum, Binance Smart Chain (BSC) is built based on Ethereum Virtual Machine (EVM) and smart contracts. However, BSC uses a consensus of Proof of Staked Authority (PoSA) [2]. In BSC, there are only 21 validators that are similar as miners in Ethereum. Although the validators are re-elected daily based on the top 21 nodes that meet the requirements to be validators, the number is always 21. To the best of our knowledge, there is no official private transaction concept in the BSC while there are MEV Bots. We believe the reason is that it is hard to become validators in BSC than Ethereum miners since the there only be 21 validators. Besides, there are no special channels in BSC (e.g., FlashBots [36] in Ethereum) for private transactions. For other blockchains, Polygon that can be considered as a fork of Ethereum uses a Proof-of-Stake (PoS) consensus mechanism. In order to participate in the blockchain, validators need to stake money and take the resposiblities as miners in Ethereum. Similarly, there are no general channels used for private transactions, although the MEV related transactions are popular in Polygan. We believe that there are more to observe and examine in such blockchains about MEV and private transactions.

8 Related Work

In this section, we discuss existing works that are related to this paper. In particular, we first discuss existing works that cover private transactions, then present the measurement papers on blockchains. We also briefly discuss works that focus on finding bugs in smart contracts.

8.1 Private Transactions

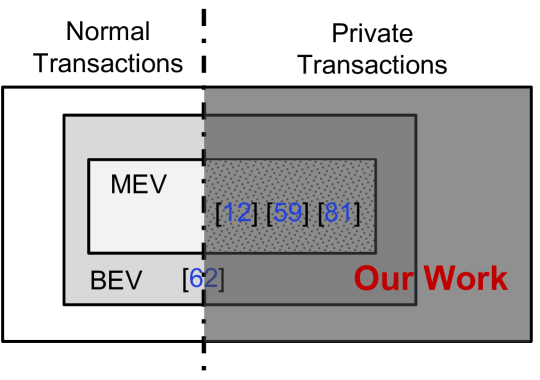

Private transactions are still very new and have not received much attention in the research community. To date, there are only a few works [59, 81, 12, 62] that touch upon private transactions as by-products when investigating MEVs. We compare the scope of our work and these papers in Fig. 14. In particular, our work mainly study the landscape of private transactions, while they focus on MEVs.

Piet et al. [59] measured private transactions in transaction pools from four sources for about 1 day, and found that most of the private transactions are used for miner profit redistribution and MEV extraction. In particular, 91.5% of MEV extraction is done via private transactions. They also analyzed the miner profits among private transactions and the top five miners earned most profits. Besides, 40% of miners had not mined any private transaction. We are different in the focuses of analysis. For example, they measure the inconsistency of private transactions in miners, while our work focuses on the profits flows earned by miners. Besides, we have a much larger dataset (one year) and we present a study on the security impacts of private transactions.

Weintraub et al. [81] mainly measure and analyze the impact of Flashbots with focusing on MEV, which provides a private channel between Ethereum users and miners. Weintraub et al. also measures other private services providers (e.g., Eden Network [16]) and shows that most of the MEV extraction comes from private service providers, especially Flashbots. They discover the unfairness of Flashbots, in which miners have profited much more than MEV searchers. Their work studies private transactions mainly from the perspective of MEV extraction, while our work gives a more complete view on private transactions in other aspects.

Qin et al. [62] measure the Blockchain Extraction Value (BEV) by detecting sandwich attacks, liquidation, and arbitrage in transactions. Specifically, they consider the transaction with zero gas price as private transactions and measure the percentage and its value in each BEV category. Moreover, their paper formalizes BEV relay systems and analyzes the impacts on P2P network and consensus layer. their paper mainly studies BEV, while our work highlights private transactions.

Capponi et al. [12] propose a game theoretical model to analyze the economic incentives behind the venues from the private transactions. In particular, their paper collected and investigated the transactions summited via the private channel from the Flashbots. The results show that the implications on different entities, including the increasement of users and miners payoffs. Their work highlights the economic incentives of private transactions, while our work focuses on analyzing the behavior of private transactions and their impacts.

8.2 Measurement of Blockchains

Measurement of Ethereum interaction networks. To study the behaviors of different entities and their interactions, many works study Ethereum networks between users and smart contracts. Particularly, Lee et al. [49], Chen et al. [14], Lin et al. [88], and Bai et al. [4] perform a measurement study on these interaction networks to observe the activities of Ethereum and propose some insights, All of these works measure the general features of the Ethereum interaction networks between users and contracts from graph analysis, while our paper focuses on the purposes and usages of private transactions from the interaction networks.

Measurement of Ethereum transactions. Besides, some works [67, 52, 86] study transactions via graph analysis to investigate the transactions behaviors. Specifically, Said et al. [67] analyze transaction behaviors, community structure and link prediction. Lin et al. [52] model the transactions records as temporal weighted multi-digraphs. Zanelatto et al. [86] conduct a large-scale study based on 3-year Ethereum transactions with cryptocurrency. These works measure the overall features of transactions, while we focus on investigating the influences of private transactions and the related security issues.

Measurement and analysis of Ethereum EIP-1559. Moreover, works [54, 50, 64] conduct an empirical study on the effects of the EIP-1559 protocol. Liu et al. [54] lead an empirical study the effects of EIP-1559 protocol on transaction fee dynamics, transaction waiting time, and security exploits. Stefanos et al. [50] study both theoretical and experimental analysis of the dynamics and stability properties of the EIP-1559 protocol. Daniel et al. [64] study the fee market upgrade by leveraging the data from first month after the EIP-1559 protocol. They also propose an alternative rule to replace EIP-1559 and prove the effectiveness from the experimental results.

Measurement and analysis of MEV. In addition, MEV is gaining attentions recently. Daian et al. [22] is the first to propose the concept of MEV and empirically shows the risks posed by MEV. Qin et al. [62] is the first to introduce the concept of Blockchain Extractable Value (BEV) and measure the dangers of BEV. Specifically, this paper quantifies the value threshold at which BEV would encourage miners to fork the blockchain. Wang et al. [80] conduct a measurement study on cyclic arbitrages which is one type of the arbitrages on the Uniswap platform. Moreover, arbitrage is also measure in some works. Zhou et al. [89] propose a framework to automatically construct profitable arbitrage transactions. They analyze the MEV or in terms of its risks to the Ethereum consensus layer, while our article measures the impact of the MEV from the related private transactions. Also, these papers detect or simulate the arbitrage in normal transactions while our work detects arbitrage in private transactions.

8.3 Bug Detection on Smart Contracts

Due to the immunity of smart contracts and their various applications, attacks happen consistently and frequently on Ethreum blockchain, which can cause huge financial losses. To mitigate such attacks, many works [42, 55, 58, 76, 47, 20, 75, 35, 46, 10, 73, 37, 71] study the vulnerabilities of smart contracts and on Ethereum. They usually use static analysis approaches, such as symbolic execution, to uncover vulnerabilities and bugs in smart contracts. Some other works [44, 40, 84, 57, 15, 41, 43, 53, 72, 38] make use of fuzzing techniques to discover bugs in smart contracts. In contrast, our work analyzes private transactions to understand their mechanisms, incentives, and security risks.

9 Conclusion

In this paper, we conduct the first empirical study on Ethereum private transactions. First, we study the general characteristics of private transactions, including the distribution, categories, DeFi tokens and platforms, and the involved entities. Contrary to the original intention of protecting users, many private transactions are used for MEV opportunities by MEV searchers. Second, we study the transaction cost and miner profits of private transactions. Private transactions use less gas and bring huge profits to miners. Finally, we evaluate security-related issues, including MEV, real-world attacks, consensus security, and the leakage of private transactions. The huge profits of private transactions might lead to undercutting attacks, and private transactions have about 4.3% chance of being leaked to the public mempool. This work sheds light on the private transaction ecosystem, and calls for more actions to protect users from private transactions.

References

- [1] 1inch, “1inch network,” https://app.1inch.io/#/1/swap/ETH/DAI, 2022.

- [2] B. ACADEMY, “An introduction to binance smart chain (bsc),” https://academy.binance.com/en/articles/an-introduction-to-binance-smart-chain-bsc, 2021.

- [3] R. Agarwal, T. Thapliyal, and S. K. Shukla, “Vulnerability and transaction behavior based detection of malicious smart contracts,” in International Symposium on Cyberspace Safety and Security. Springer, 2021, pp. 79–96.

- [4] Q. Bai, C. Zhang, Y. Xu, X. Chen, and X. Wang, “Evolution of ethereum: A temporal graph perspective,” 2020. [Online]. Available: https://arxiv.org/abs/2001.05251

- [5] T. Be’ery, “Without permit: Multichain’s exploit explained,” https://medium.com/zengo/without-permit-multichains-exploit-explained-8417e8c1639b, 2022.

- [6] beincrypto, “Eth pools: Best mining pools for ethereum mining,” https://beincrypto.com/learn/eth-pools-mining/, 2021.

- [7] T. Block, “Mev bots earn $476,000 by targeting large stablecoin swaps,” https://www.theblockcrypto.com/post/139155/mev-bots-earn-476000-by-targeting-large-stablecoin-swaps/, 2022.

- [8] BlockSec, “Li.fi attack: a cross-chain bridge vulnerability? no, it’s due to unchecked external call!” https://blocksecteam.medium.com/li-fi-attack-a-cross-chain-bridge-vulnerability-no-its-due-to-unchecked-external-call-c31e7dadf60f, 2022.

- [9] BLOXROUTE, “Fastest mempool data,” https://bloxroute.com/mempool-data/, 2022.

- [10] L. Brent, A. Jurisevic, M. Kong, E. Liu, F. Gauthier, V. Gramoli, R. Holz, and B. Scholz, “Vandal: A scalable security analysis framework for smart contracts,” arXiv preprint arXiv:1809.03981, 2018.

- [11] V. Buterin, “Ethereum white paper: A next generation smart contract & decentralized application platform,” 2013. [Online]. Available: https://github.com/ethereum/wiki/wiki/White-Paper

- [12] A. Capponi, R. Jia, and Y. Wang, “The evolution of blockchain: from lit to dark,” arXiv preprint arXiv:2202.05779, 2022.

- [13] M. Carlsten, H. Kalodner, S. M. Weinberg, and A. Narayanan, “On the instability of bitcoin without the block reward,” in Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security, 2016, pp. 154–167.

- [14] T. Chen, Z. Li, Y. Zhu, J. Chen, X. Luo, J. C.-S. Lui, X. Lin, and X. Zhang, “Understanding ethereum via graph analysis,” ACM Transactions on Internet Technology (TOIT), vol. 20, no. 2, pp. 1–32, 2020.

- [15] J. Choi, D. Kim, S. Kim, G. Grieco, A. Groce, and S. K. Cha, “Smartian: Enhancing smart contract fuzzing with static and dynamic data-flow analyses,” in 2021 36th IEEE/ACM International Conference on Automated Software Engineering (ASE). IEEE, 2021, pp. 227–239.

- [16] P. Chris, Q. Jeffrey, and S. Caleb, “Eden network,” https://edennetwork.io/EDEN_Network___Whitepaper___2021_07.pdf, 2021.

- [17] Coinmarketcap, “Front running,” https://coinmarketcap.com/alexandria/glossary/front-running, 2022.

- [18] COINTELEGRAPH, “Multichain hacker returns 322 eth, keeps hefty finders fee,” https://cointelegraph.com/news/multichain-hacker-returns-322-eth-keeps-hefty-finders-fee, 2022.

- [19] CONSENSYS, “Defi market commentary | may 2022,” https://consensys.net/blog/cryptoeconomic-research/defi-market-commentary-may-2022/, 2022.

- [20] ConsenSys, “Mythril classic,” https://github.com/ConsenSys/mythril-classic, 2022.

- [21] Crypto.com, “Crypto.com: The world’s fastest growing crypto app,” https://crypto.com, 2022.

- [22] P. Daian, S. Goldfeder, T. Kell, Y. Li, X. Zhao, I. Bentov, L. Breidenbach, and A. Juels, “Flash boys 2.0: Frontrunning, transaction reordering, and consensus instability in decentralized exchanges,” 2019. [Online]. Available: https://arxiv.org/abs/1904.05234

- [23] DappRadar, “Defi overview,” https://dappradar.com/defi, 2022.

- [24] Ethereum, “Node discovery protocol v5,” https://github.com/ethereum/devp2p/blob/master/discv5/discv5.md, 2021.

- [25] ——, “The rlpx transport protocol,” https://github.com/ethereum/devp2p/blob/master/rlpx.md, 2021.

- [26] ——, “Decentralized finance (defi) | ethereum.org,” https://ethereum.org/en/defi/, 2022.

- [27] ——, “Erc-20 token standard | ethereum.org,” https://ethereum.org/en/developers/docs/standards/tokens/erc-20/, 2022.

- [28] ——, “Proof-of-stake (pos) | ethereum.org,” https://ethereum.org/en/developers/docs/consensus-mechanisms/pos/, 2022.

- [29] ——, “Proof-of-work (pow) | ethereum.org,” https://ethereum.org/en/developers/docs/consensus-mechanisms/pow/, 2022.

- [30] ——, “Stablecoins: Digital money for everyday use | ethereum.org,” https://ethereum.org/en/stablecoins/, 2022.

- [31] G. Ethereum, “Official go implementation of the ethereum protocol,” https://github.com/ethereum/go-ethereum, 2022.

- [32] Ethermine, “Want to keep your dex trades away from the public mempool?” https://twitter.com/ethermine_org/status/1443502516604477445, 2022.

- [33] Etherscan, “Etherscan,” https://etherscan.io/, 2022.

- [34] ——, “Label word cloud,” https://etherscan.io/labelcloud, 2022.

- [35] J. Feist, G. Grieco, and A. Groce, “Slither: a static analysis framework for smart contracts,” in 2019 IEEE/ACM 2nd International Workshop on Emerging Trends in Software Engineering for Blockchain (WETSEB). IEEE, 2019.

- [36] Flashbot, “Flashbots docs,” https://docs.flashbots.net/flashbots-auction/overview/, 2022.

- [37] J. Frank, C. Aschermann, and T. Holz, “ETHBMC: A bounded model checker for smart contracts,” in 29th USENIX Security Symposium (USENIX Security 20), 2020, pp. 2757–2774.

- [38] Y. Fu, M. Ren, F. Ma, H. Shi, X. Yang, Y. Jiang, H. Li, and X. Shi, “Evmfuzzer: detect evm vulnerabilities via fuzz testing,” in Proceedings of the 2019 27th ACM joint meeting on european software engineering conference and symposium on the foundations of software engineering, 2019, pp. 1110–1114.

- [39] T. Gong, M. Minaei, W. Sun, and A. Kate, “Towards overcoming the undercutting problem,” arXiv preprint arXiv:2007.11480, 2020.

- [40] G. Grieco, W. Song, A. Cygan, J. Feist, and A. Groce, “Echidna: effective, usable, and fast fuzzing for smart contracts,” in Proceedings of the 29th ACM SIGSOFT International Symposium on Software Testing and Analysis, 2020.

- [41] A. Groce and G. Grieco, “echidna-parade: a tool for diverse multicore smart contract fuzzing,” in Proceedings of the 30th ACM SIGSOFT International Symposium on Software Testing and Analysis, 2021, pp. 658–661.

- [42] S. Grossman, I. Abraham, G. Golan-Gueta, Y. Michalevsky, N. Rinetzky, M. Sagiv, and Y. Zohar, “Online detection of effectively callback free objects with applications to smart contracts,” Proceedings of the ACM on Programming Languages, 2017.

- [43] J. He, M. Balunović, N. Ambroladze, P. Tsankov, and M. Vechev, “Learning to fuzz from symbolic execution with application to smart contracts,” in Proceedings of the 2019 ACM SIGSAC Conference on Computer and Communications Security, 2019, pp. 531–548.

- [44] B. Jiang, Y. Liu, and W. Chan, “Contractfuzzer: Fuzzing smart contracts for vulnerability detection,” in 2018 33rd IEEE/ACM International Conference on Automated Software Engineering (ASE). IEEE, 2018, pp. 259–269.

- [45] D. B. Johnson, “Finding all the elementary circuits of a directed graph,” SIAM J. Comput., vol. 4, pp. 77–84, 1975.

- [46] S. Kalra, S. Goel, M. Dhawan, and S. Sharma, “Zeus: Analyzing safety of smart contracts,” in Proceedings of the 25th Annual Network and Distributed System Security Symposium, 2018.

- [47] J. Krupp and C. Rossow, “teether: Gnawing at ethereum to automatically exploit smart contracts,” in 27th USENIX Security Symposium, 2018.

- [48] N. Kumar, A. Singh, A. Handa, and S. K. Shukla, “Detecting malicious accounts on the ethereum blockchain with supervised learning,” in International Symposium on Cyber Security Cryptography and Machine Learning. Springer, 2020, pp. 94–109.

- [49] X. T. Lee, A. Khan, S. Sen Gupta, Y. H. Ong, and X. Liu, “Measurements, analyses, and insights on the entire ethereum blockchain network,” in Proceedings of The Web Conference 2020, 2020, pp. 155–166.

- [50] S. Leonardos, B. Monnot, D. Reijsbergen, E. Skoulakis, and G. Piliouras, “Dynamical analysis of the eip-1559 ethereum fee market,” in Proceedings of the 3rd ACM Conference on Advances in Financial Technologies, 2021, pp. 114–126.

- [51] LI.FI, “Advanced Bridge & DEX Aggregation,” https://li.fi, 2022.

- [52] D. Lin, J. Wu, Q. Yuan, and Z. Zheng, “Modeling and understanding ethereum transaction records via a complex network approach,” IEEE Transactions on Circuits and Systems II: Express Briefs, vol. 67, no. 11, pp. 2737–2741, 2020.

- [53] C. Liu, H. Liu, Z. Cao, Z. Chen, B. Chen, and B. Roscoe, “Reguard: finding reentrancy bugs in smart contracts,” in IEEE/ACM 40th International Conference on Software Engineering: Companion (ICSE-Companion). IEEE, 2018.

- [54] Y. Liu, Y. Lu, K. Nayak, F. Zhang, L. Zhang, and Y. Zhao, “Empirical analysis of eip-1559: Transaction fees, waiting time, and consensus security,” arXiv preprint arXiv:2201.05574, 2022.

- [55] L. Luu, D.-H. Chu, H. Olickel, P. Saxena, and A. Hobor, “Making smart contracts smarter,” in Proceedings of the 2016 ACM SIGSAC conference on computer and communications security. ACM, 2016.

- [56] Multichain, “Cross-chain router protocol,” https://multichain.xyz, 2022.

- [57] T. D. Nguyen, L. H. Pham, J. Sun, Y. Lin, and Q. T. Minh, “sfuzz: An efficient adaptive fuzzer for solidity smart contracts,” in Proceedings of the ACM/IEEE 42nd International Conference on Software Engineering, 2020, pp. 778–788.

- [58] I. Nikolić, A. Kolluri, I. Sergey, P. Saxena, and A. Hobor, “Finding the greedy, prodigal, and suicidal contracts at scale,” in Proceedings of the 34th Annual Computer Security Applications Conference. ACM, 2018.

- [59] J. Piet, J. Fairoze, and N. Weaver, “Extracting godl [sic] from the salt mines: Ethereum miners extracting value,” arXiv preprint arXiv:2203.15930, 2022.

- [60] PolkaBridge, “First Cross-Chain & MultiChain AMM,” https://polkabridge.org, 2022.

- [61] E. I. Proposals, “Eip-1559: Fee market change for eth 1.0 chain,” https://eips.ethereum.org/EIPS/eip-1559, 2022.

- [62] K. Qin, L. Zhou, and A. Gervais, “Quantifying blockchain extractable value: How dark is the forest?” arXiv preprint arXiv:2101.05511, 2021.