Bayesian regularization of empirical MDPs

Abstract

In most applications of model-based Markov decision processes, the parameters for the unknown underlying model are often estimated from the empirical data. Due to noise, the policy learned from the estimated model is often far from the optimal policy of the underlying model. When applied to the environment of the underlying model, the learned policy results in suboptimal performance, thus calling for solutions with better generalization performance. In this work we take a Bayesian perspective and regularize the objective function of the Markov decision process with prior information in order to obtain more robust policies. Two approaches are proposed, one based on regularization and the other on relative entropic regularization. We evaluate our proposed algorithms on synthetic simulations and on real-world search logs of a large scale online shopping store. Our results demonstrate the robustness of regularized MDP policies against the noise present in the models.

1 Introduction

A Markov decision process (MDP) is a model . Here is the discrete state space, with each state represented by . represents the discrete action space with each action denoted by . denotes the transition probability tensor where, for each action , is the transition matrix between the states, i.e., denotes the probability of moving from state to state if action is taken at state . represents the reward tensor where, for each action , is the reward matrix between the states, i.e., denotes the reward obtained in moving from state to state if action is taken at state . The discount factor determines the importance given to rewards obtained in the future relative to those collected immediately.

A policy defines the probabilities of taking action at state . The goal in the MDP is to find a policy that maximizes the expected discounted cumulative reward for each state , given by . In what follows, , , and are considered to be fixed, and therefore, we often denote the MDP model in short with .

For most applications, the environment is modeled with an unknown underlying MDP that is not directly accessible. The empirical model is often estimated from samples of and an optimal policy is then learned from . As the two models and are different due to sampling noise, the policy learned from is different from the true optimal policy of . When applying directly to the environment modeled by the underlying MDP , one often experiences suboptimal performance.

To give a simple example, consider an MDP with only two actions and at each state and that action is always better than for all states under the true transition probability matrices and reward matrices . The transition matrices and reward matrices constructed from samples are different from and due to the noise present in the data. As a result, the policy learned from the empirical model may recommend action over for some states , thus leading to poor generalization performance.

As a more concrete example, let us consider the shopping experience of a customer at an online shopping store. A customer starts a session by typing in an initial query. Based on the given query, the store can recommend products using one of the existing search algorithms. Upon viewing the results, the customer may either make a purchase or continue the browsing session by typing a modified or new query. Such a shopping experience can be modeled as an MDP, where each query is regarded as a state and each search algorithm as an action . The reward corresponds for example to whether a purchase is made or not. The optimization problem is to decide which search algorithm should be activated given the query in order to improve the overall shopping experience. In a typical offline learning setting, the empirical MDP model is constructed based on the historical log data. Therefore, the transition tensor and purchase actions are inherently noisy. If one learns the policy directly from the noisy empirical model, it can have a poor performance when deployed in the future. While we motivate this issue using the online shopping example, it exists universally in many other applications.

In this work, we study the problem of learning a robust MDP policy from the empirical model that can perform significantly better than the naive policy from when deployed to the unknown underlying . Though this is a challenging problem stated as it is, a key observation is that in many real applications there is often prior information on the rankings of the available actions. Here, we take a Bayesian approach to incorporate such prior information as a regularizer.

Main Contributions.

The main contributions of this work are:

-

•

We propose a Bayesian approach that factors in known prior information about the actions and learns policies robust to noise in empirical MDPs. More specifically, two approaches are proposed: one based on regularization and the other on relative entropic regularization. Both can be implemented efficiently by leveraging existing algorithms for MDP optimization.

-

•

We evaluate the designed algorithms on both synthetic simulations and on the logs of a real-world online shopping store dataset. Our regularized policies significantly outperform the un-regularized MDP policies.

Related work.

When solving the MDPs, entropy regularization has proven quite useful [18, 7, 20, 14]. Commonly, Shannon entropy or negative conditional entropy is used to regularize the MDPs [18, 7, 20, 14, 4, 11]. While this results in more robust stochastic policies, they do not necessarily account for any prior information. The work of [16, 18, 15, 22] discusses relative entropic regularization in MDPs, which biases results to a reference distribution. These works focus on improving the convergence and stability of RL methods by employing entropic regularization. But, this idea has yet to be applied in the context of empirical MDPs through a Bayesian perspective.

There has been work on reward shaping [17, 12, 3, 10, 9] where the idea is to obtain a new MDP model by modifying the rewards of model as , where are potential functions at state . In particular, [17] showed that such a reward shaping ensures that the optimal policy in the two models and remains the same. The focus of all these works is to design potential functions to improve the convergence of algorithms in without altering the optimal policies. As the empirical model and true model are different in our setting due to the inherent noise, we need regularization based approaches which incorporate the prior information about preference towards certain actions as the optimal policy in is not necessarily optimal under .

An alternative solution to this problem would be from a denoising perspective, where the empirical model is first denoised and then the policy is learned from the denoised model instead. This has been studied in the context of linear systems where the objective is to solve the system but the estimated model parameters and contain a significant level of noise. To tackle this, [6, 5] propose an operator augmentation approach that perturbs the inverse of the sampled operator for better approximation to . However, it is not clear how to extend this approach to the control setting in MDP.

A closely related line of work is that of model based Bayesian reinforcement learning [8], where priors are expressed over model as opposed to the policy. Imposing priors in such a way allows one to deal with imprecise models [13]. Our work on studying Bayesian regularization policies in the action space is complementary to this line of work. The choice of imposing a prior on model against a prior on policy boils down to the application domain. In several application domains, the state space is quite large as a result of which working with a Bayesian model on transition/reward tensors becomes infeasible. In contrast, the action space is relatively much smaller, as a result of which employing a Bayesian approach on the action space is much more practical.

Organization.

In Section 2, we present the optimization formulations and describe our regularization approach by incorporating prior information. Section 3 studies the performance of the proposed policy against baseline algorithms on several simulated examples. Section 4 evaluates the performance of our proposed algorithms on an application data set.

2 Problem statement and algorithms

2.1 Policy maximization

Let be the probability simplex over the action set . The set of all valid policies is

For a policy , the transition matrix under the policy is defined as , i.e., is the probability of arriving at state from state if policy is taken. Similarly, the reward under the policy is given by , where , i.e., the expected reward at state under action .

For a discounted MDP [21, 19] with , the value function under policy is a vector , where each entry represents the expected discounted cumulative reward starting from state under the policy , i.e.,

with the expectation taken over and for all . The value function satisfies the Bellman equation [2], i.e., for any

or equivalently in the matrix-vector notation

Here, the inverse of the matrix exists whenever or there exists a terminal state in the MDP such that , , and [1]. Given the MDP, the optimization problem is

| (1) |

where is an arbitrary vector with positive entries [23]. By introducing the discounted visitation count , we can rewrite Equation 1 as

| (2) |

2.2 Bayesian approaches

Given an MDP model , we can view (2) as the maximum a posteriori probability (MAP) estimate with

| (3) |

When prior knowledge about is not available, it is natural to take a uniform prior over , i.e. is constant. This implies that , leading to

| (4) |

On the other hand, if prior knowledge about is available, it makes sense to impose more informative priors on . One commonly used prior is that at state an action is often preferred over the rest of the actions. This prior information can be incorporated naturally in the following two ways.

2.2.1 -type prior

In particular, we assume a prior

| (5) |

where is defined to be the norm of outside of action , i.e., . This prior puts more probability on action relative to other actions in . Combining (4) and (5) leads to the a posteriori probability

The corresponding MAP estimate is

| (6) |

Note that individual component of can be broken down as,

where if and if . Hence, this formulation is equivalent to replacing with , i.e., the reward of all non-preferred actions is reduced by a constant . The corresponding Bellman equation is

Once is computed, the optimal action at state is given by

| (7) |

2.2.2 Relative entropy regularization

In the MDP literature, it is common to use Shannon entropy regularization, which allows for learning stochastic policies instead of deterministic ones. However, it fails to capture the prior information, such as the scenario where one of the actions in is preferred over others. To accommodate such a prior, we propose to use the relative entropy instead of Shannon entropy. By choosing the prior distribution carefully, relative to which the entropy of policy is evaluated, we obtain solutions that prefer one action over other actions in . We consider a penalty such that with , where is a distribution over that prefers , e.g.,

for some . The corresponding MAP estimate is

| (8) |

This is in fact equivalent to the standard Shannon entropy regularization with modified rewards , i.e., a penalty is added to when action is taken. The magnitude of the penalty for action is large if the prior probability of selecting action is small. By applying the Bellman equation of Shannon entropy regularization [16, 24] to (8), we obtain

Because of the Gibbs variational principle, the RHS is equal to

. Thus,

the Bellman equation can be written in the following log-sum-exp form

| (9) |

which can be solved with a value function iteration. Once is known, the optimal policy at state and action is given by

| (10) |

where is the normalization factor.

2.2.3 Comments

Both the optimization formulations in Sections 2.2.1 and 2.2.2 add a penalty on top of the reward obtained for each action. The less preferred actions (i.e., ) are penalized and hence as a result the learned policy prefers action over the other ones. The magnitude of the penalty depends on the regularization parameter in the case and in the relative entropy case. The policy obtained in Section 2.2.1 is a deterministic policy, whereas the one learned in Section 2.2.2 is a stochastic policy due to the added entropy regularization. When in Section 2.2.2 is chosen to be small, the policy becomes more and more concentrated and is often practically equivalent to the one in Section 2.2.1. Finally, we note that both the approaches presented above can be easily extended to settings where a certain subset of the actions are preferred over the others.

3 Simulated examples

In the following simulated examples, we demonstrate numerically that an optimal policy of the empirical MDP results in sub-optimal performance on the underlying MDP model and that the regularized policies provide significantly better performance.

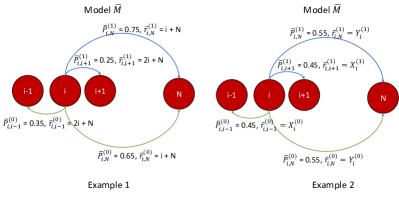

Example 1.

Consider the MDP model shown in Figure 1. This model has states and two actions . The transition and reward tensors for model are defined below

Here, state is a terminal state, where and . In our simulations, and . The empirical MDP is constructed from the true MDP by sampling the transition probabilities from a set of 100 samples for each state . Due to the sampling noise, the transition tensor of model is different from of . In this example, we assume that the underlying reward tensor is known exactly. Under the true model , action is optimal for any state , as the transition probability to states with higher reward is larger under action . However, when the model is constructed from empirical samples, the optimal policy learned on recommends action for some states, leading to a sub-optimal performance on the true model .

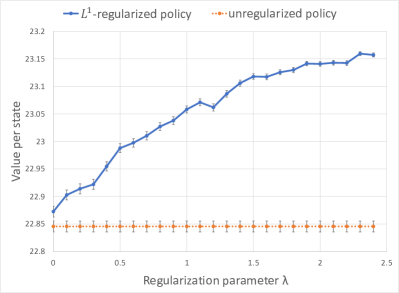

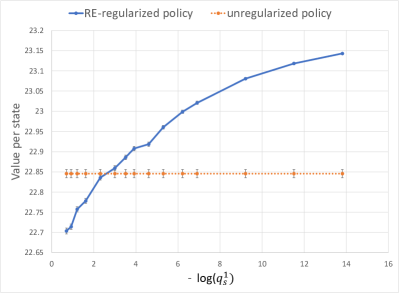

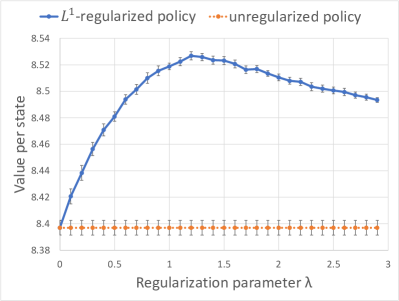

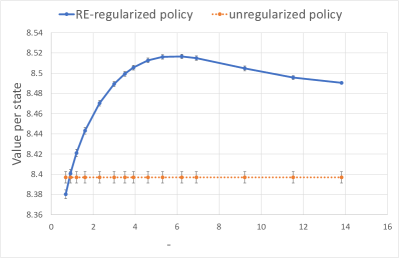

Figure 2 shows the comparison between the -regularized policy and the unregularized policy when evaluated on . As the regularization parameter increases, the learned policy prefers action over action and obtains higher value per state as a result. In Figure 3, we compare the relative entropic regularization policy (referred in short as the RE-regularized policy) with the unregularized policy on the true model . We set regularization coefficient to be and vary the value of prior on the -axis. The value corresponds to the case with Shannon entropic regularization. As the value of becomes smaller, the RE-regularized policy prefers action over action and results in a higher value per state relative to the unregularized policy.

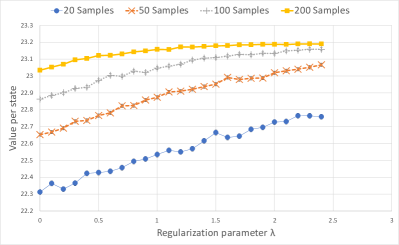

In practice, the values of (for the RE-regularized policy) and (for the -regularized policy) can be learned through evaluation on a validation set. In both the cases, the need for regularization goes down as the number of samples used to evaluate increases. This effect is demonstrated in Figure 4, where we plot the performance of the -regularized policy as a function of the samples used to estimate the transition probabilities for each state in .

Example 2.

In Example 1, only the transition tensor in is sampled from the true model . In practice, the reward tensor is also estimated empirically. To model this, in this example the reward values has a Gaussian noise added to the true unknown underlying reward . The transition and reward tensors for model are defined below (also see Figure 1)

Here, is taken to be a random realization drawn from . Similarly, , , . In our simulations, . For this MDP model , the optimal action is for about of the states in as the expected number of steps to reach the terminal state from a given state is higher in action relative to action .

The empirical MDP is obtained by averaging samples per state of , where each reward entry of is corrupted by a zero mean Gaussian noise with standard deviation . As the transition and reward tensors in contain noise, the unregularized policy from recommends action for more than of the states. As a result, the unregularized policy is sub-optimal on the underlying model .

The prior information that action is preferred over action helps the -regularized policy and RE-regularized policy to outperform the unregularized policy. Figures 5 and 6 illustrate this improvement as a function of regularization parameters and (the regularization coefficient is fixed at for this example). As the value of or increase, the regularized policies favor action over action , leading to significant improvements on model . With further increase in and , the performance dips afterwards as the regularized policies start selecting action over action for more states than necessary.

4 Experiments on real data

This section discusses large-scale experiments on logs of an online shopping store with competing search algorithms. We consider the user shopping experience discussed in Section 1 and model a shopping session with an MDP where a state corresponds to the search query typed in by the user.

For each query , the shopping store needs to decide on the search algorithm to use to display results. This corresponds to the two actions of the MDP. When an action is taken, the search results are shown to the user and the user interaction will result in a transition to a new state. We identify this new state with the new query from the user. However, before making this transition from state to , the user may make a purchase, which corresponds to the reward. The user may terminate the session at any point with/without making a purchase and this is captured by the transition to a terminal state (see Figure 7). The rewards are considered to be binary: if a user makes a purchase at state under shopping store’s action and then transitions to , . if no purchase were made. The two available search algorithms perform differently on different queries. Therefore, there is an opportunity to interleave different algorithms based on the queries, even within a single shopping session. Moreover, often it is known a priori that one search algorithm may work better than the other. As a result, it is useful to incorporate this information as a prior and design regularized policies that are robust to noise in the empirical MDP.

To conduct our experiment, we collected the search logs of an online shopping store for a time period for two different search algorithms, one deployed in period 1 and the other in period 2, with period 1 is before period 2 in time and both the time periods are non-overlapping. Therefore, the action space consists of two search algorithms, which were previously deployed in period 1 and period 2 respectively. We processed the data in a time period where ranker 1 was deployed to obtain the search logs under the ranker 1 action. Similarly, the data for another time period, in which ranker 2 was used, was collected to obtain the user logs under the ranker 2 action. We considered the set of most typed queries as the state space . For each of these time periods, we estimated the transition and reward tensors from user logs, thereby obtaining the MDP model , i.e., , , , for all .

The key challenge is to learn robust policies from the empirical model . It is known a priori that on average, ranker 2 tends to produce better results relative to ranker 1. We exploit this information to learn the -regularized and RE-regularized policies, which interleave ranker 1 and ranker 2 effectively for different queries within a single session.

The performance of different policies is judged based on the objective function , where is the value function at with discount factor and denotes the probability that is the first query in a random shopping session. This probability is evaluated based on a hold-out time period from the collected search logs.

In order to evaluate the performance in an unbiased way, we extracted the data for different time periods in which ranker 1 and ranker 2 were deployed, to construct a model with tensors denoted by and . As the true underlying model is not directly accessible, we use , a fresh unbiased estimator of , to evaluate the different policies. This essentially corresponds to evaluating the performance of the policies on a new time period.

The transition and reward tensors between models and can be quite different. In fact, comparing these two estimated models provides an idea of the existing noise in the estimated models. For example, the average norm of the rows of (also ) is about , suggesting that the average total variational distance between transition probability vectors of and is , which is empirically quite significant.

For comparison purposes, we include the performance of several baselines defined below:

-

•

unregularized MDP policy: this policy is optimal for model and is applied to without any regularization.

-

•

one-shot policy (OSP): this policy selects action ranker 1 for a particular keyword if immediate reward from ranker 1 is larger, i.e.,

-

•

regularized one-shot policy (): this policy selects ranker 1 for a particular keyword only if

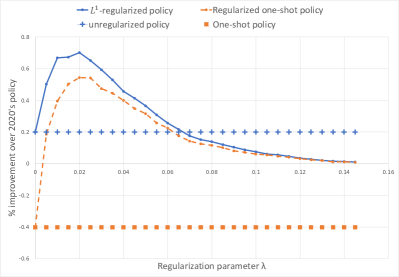

Figure 8 shows the performance of -regularized MDP policy, the unregularized MDP policy, OSP, and on model , where all these policies are learned from model . We observe that (a) the -regularized MDP policy shows about improvement over the ranker 2 policy, and the improvement over the ranker 1 policy is in the range of -, (b) the -regularized policy outperforms both OSP and , suggesting that the MDP model is beneficial as the OSP and do not factor in delayed rewards, and (c) the -regularized policy outperforms the unregularized MDP policy by accounting for prior information in the form of regularization parameter . The best performance is obtained with . As the value of increases, the regularized policies prefer ranker 2 over ranker 1. When is increased further, the learned policy ends up selecting ranker 2 for all the states. This is why its performance becomes similar to ranker 2 in Figure 8 for large values of .

The same experiment is repeated for the RE-regularized policy and we observe a performance similar to that of the regularized policy with the best improvement of coming at and .

The above experiments suggest that hyperparameters and perform the best for the -regularized policy and the RE-regularized policy, respectively. To validate our results, we performed another experiment with these hyperparameters, where we learned the model with a new action space by collecting user logs for two different non-overlapping time periods in which ranker 2 and ranker 3 were deployed. In this scenario, ranker 3 was more recently deployed relative to ranker 2. The test data is also generated by collecting user logs on a hold-out time period where ranker 2 and ranker 3 were previously deployed. In this situation, the prior is that the ranker 3 is on average better than ranker 2 and it has been incorporated in the computation of the -regularized and RE-regularized policies. The results are reported below in Table 1.

| Algorithm | improvement |

|---|---|

| over ranker 3 | |

| unregularized policy | |

| -regularized policy | 0.214 |

| RE-regularized policy | 0.207 |

| One-shot Policy | |

| Regularized one-shot Policy |

We make several observations from the results listed in Table 1. First, there is a significant difference between the performance of the regularized one-shot policy and the regularized MDP policies, as the sessions were of longer range in the collected data. For example, a typical query improved using older search algorithm is "mens gifts". As this query leads to sessions of larger length on the shopping store, the regularized MDP policies allow us to factor in the delayed rewards and suggest the appropriate search algorithm for the query. An empirical approach such as fails to evaluate the quality of search results in this case as it focuses only on the immediate rewards. Second, the regularized MDP policies outperform both ranker 2 and ranker 3, whereas all other policies are worse of than the simple strategy of selecting ranker 3 for all queries. This is because the -regularized and RE-regularized MDP policies account for the noise present in the model and incorporate the known prior information appropriately.

5 Conclusions

In this paper, we study the problem of learning policies where the parameters of the underlying MDP are not known but instead estimated from empirical data. Simply learning policies on the estimated model may lead to poor generalization performance on the underlying MDP . To address this issue, we propose a Bayesian approach, which regularizes the objective function of the MDP to learn policies that are robust to noise. Our learned policies are based on norm regularization and relative entropic regularization on the objective function of MDP. We show that our proposed regularized MDP approaches end up penalizing the reward of less preferred actions, thereby giving preference to certain actions in over others.

To validate the performance of proposed algorithms, we evaluate the performance on both synthetic examples and on the logs of real-world online shopping store data set. We demonstrate that a policy learned optimally on without any regularization can even do worse than a simple policy that always selects one of the actions for all the states. Our experiments reveal that the un-regularized policies are not robust to noise in probability and reward tensors. On the other hand, the regularized MDP policies significantly outperform other baseline algorithms both on synthetic and real-world numerical experiments.

References

- Bell, [1965] Bell, H. E. (1965). Gershgorin’s theorem and the zeros of polynomials. The American Mathematical Monthly, 72(3):292–295.

- Bellman, [1966] Bellman, R. (1966). Dynamic programming. Science, 153(3731):34–37.

- Cooper and Rangarajan, [2012] Cooper, W. L. and Rangarajan, B. (2012). Performance guarantees for empirical markov decision processes with applications to multiperiod inventory models. Operations Research, 60(5):1267–1281.

- Dai et al., [2018] Dai, B., Shaw, A., Li, L., Xiao, L., He, N., Liu, Z., Chen, J., and Song, L. (2018). Sbeed: Convergent reinforcement learning with nonlinear function approximation. In International Conference on Machine Learning, pages 1125–1134. PMLR.

- Etter and Ying, [2021] Etter, P. and Ying, L. (2021). Operator augmentation for general noisy matrix systems. arXiv preprint arXiv:2104.11294.

- Etter and Ying, [2020] Etter, P. A. and Ying, L. (2020). Operator augmentation for noisy elliptic systems. arXiv preprint arXiv:2010.09656.

- Fox et al., [2015] Fox, R., Pakman, A., and Tishby, N. (2015). Taming the noise in reinforcement learning via soft updates. arXiv preprint arXiv:1512.08562.

- Ghavamzadeh et al., [2016] Ghavamzadeh, M., Mannor, S., Pineau, J., and Tamar, A. (2016). Bayesian reinforcement learning: A survey. arXiv preprint arXiv:1609.04436.

- Gimelfarb et al., [2018] Gimelfarb, M., Sanner, S., and Lee, C.-G. (2018). Reinforcement learning with multiple experts: A bayesian model combination approach. Advances in Neural Information Processing Systems, 31:9528–9538.

- Grzes, [2017] Grzes, M. (2017). Reward shaping in episodic reinforcement learning.

- Haarnoja et al., [2018] Haarnoja, T., Zhou, A., Abbeel, P., and Levine, S. (2018). Soft actor-critic: Off-policy maximum entropy deep reinforcement learning with a stochastic actor. In International conference on machine learning, pages 1861–1870. PMLR.

- Harutyunyan et al., [2015] Harutyunyan, A., Brys, T., Vrancx, P., and Nowé, A. (2015). Shaping mario with human advice. In AAMAS, pages 1913–1914.

- Levine et al., [2020] Levine, S., Kumar, A., Tucker, G., and Fu, J. (2020). Offline reinforcement learning: Tutorial, review, and perspectives on open problems. arXiv preprint arXiv:2005.01643.

- Mnih et al., [2016] Mnih, V., Badia, A. P., Mirza, M., Graves, A., Lillicrap, T., Harley, T., Silver, D., and Kavukcuoglu, K. (2016). Asynchronous methods for deep reinforcement learning. In International conference on machine learning, pages 1928–1937. PMLR.

- Nachum et al., [2017] Nachum, O., Norouzi, M., Xu, K., and Schuurmans, D. (2017). Trust-pcl: An off-policy trust region method for continuous control. arXiv preprint arXiv:1707.01891.

- Neu et al., [2017] Neu, G., Jonsson, A., and Gómez, V. (2017). A unified view of entropy-regularized markov decision processes. arXiv preprint arXiv:1705.07798.

- Ng et al., [1999] Ng, A. Y., Harada, D., and Russell, S. (1999). Policy invariance under reward transformations: Theory and application to reward shaping. In Icml, volume 99, pages 278–287.

- Peters et al., [2010] Peters, J., Mulling, K., and Altun, Y. (2010). Relative entropy policy search. In Twenty-Fourth AAAI Conference on Artificial Intelligence.

- Puterman, [2014] Puterman, M. L. (2014). Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons.

- Schulman et al., [2015] Schulman, J., Levine, S., Abbeel, P., Jordan, M., and Moritz, P. (2015). Trust region policy optimization. In International conference on machine learning, pages 1889–1897. PMLR.

- Sutton and Barto, [2018] Sutton, R. S. and Barto, A. G. (2018). Reinforcement learning: An introduction. MIT press.

- Wu et al., [2019] Wu, Y., Tucker, G., and Nachum, O. (2019). Behavior regularized offline reinforcement learning. arXiv preprint arXiv:1911.11361.

- Ye, [2011] Ye, Y. (2011). The simplex and policy-iteration methods are strongly polynomial for the markov decision problem with a fixed discount rate. Mathematics of Operations Research, 36(4):593–603.

- Ying and Zhu, [2020] Ying, L. and Zhu, Y. (2020). A note on optimization formulations of markov decision processes. arXiv preprint arXiv:2012.09417.