Domain Analysis of Ethical, Social and Environmental Accounting Methods

Department of Information and Computing Sciences

Utrecht University

Princetonplein 5, 3584 CC Utrecht

v.d.ramautar@uu.nl

\And

Department of Information and Computing Sciences

Utrecht University

Princetonplein 5, 3584 CC Utrecht

s.espana@uu.nl

Abstract

Ethical, social and environmental accounting is the practice of assessing and reporting organisations’ performance on environmental, social and governance topics. There are ample methods that describe how to perform such sustainability assessments. This report presents a domain analysis of ethical, social and environmental accounting methods. Our analysis contains 21 methods. Each method is modelled as a process deliverable diagram. The diagrams have been validated by experts in the methods. The diagrams lay the foundation for further analysis and software development. In this report, we touch upon the ethical, social and environmental accounting method ontology that has been created based on the domain analysis.

1 Introduction

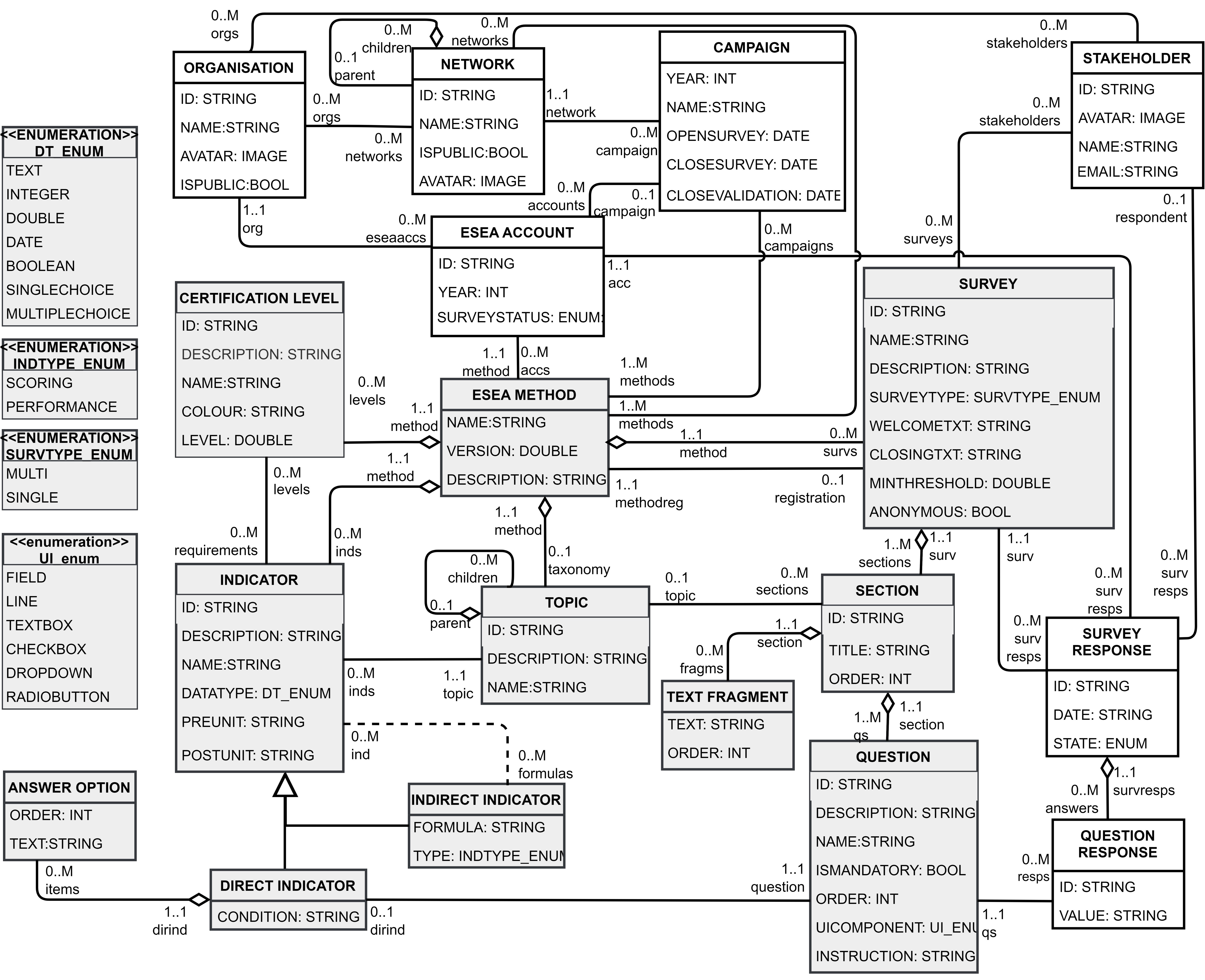

Ethical, social and environmental accounting (ESEA) methods guide responsible entities in performing sustainability assessments and reporting on the assessment results. Typically organisations report on their performance regarding ethical, social and environmental dimensions. The contributions of this report include a detailed domain analysis of 21 ESEA methods. For each, method, we propose a process deliverable diagram (PDD) that depicts the method from two perspectives: the process part focuses on the activities of the method, and the deliverable part focuses on the products used as input or produced as output by the activities (thus constituting a conceptual data model for the method) van de Weerd and Brinkkemper (2009).The diagrams are created as part of the Software for Organisation Responsibility research line. We base the models on method documentation and official information published by the entity that developed the method. The PDDs are validated with experts in the respective ESEA methods. After the validation interviews, we update and improve the PDDs if necessary. The validated PDDs are used to create activity and concept comparisons. For this, we adapt the method comparison approach (van de Weerd et al., 2007). We provide a discussion of the results and present a metamodel that abstracts the 21 ESEA methods. We name this the openESEA metamodel since it acts as a domain ontology that serves as the foundation for engineering the openESEA domain-specific language (DSL). The openESEA metamodel and the DSL are presented in a technical report (Ramautar and España, 2022a). An earlier version of the metamodel and DSL are presented in España et al. (2019).

The report structure is the following. Section 2 lists the research questions and provides an overview of the research method. Section 3 contains the domain analysis of ESEA methods, including all PDDs and brief descriptions of each of the ESEA methods. Section 4 discusses the results of the domain analysis of ESEA methods. The result includes the openESEA metamodel. In Section 5 we present the conclusions of this research.

2 Research method

2.1 Research questions

This report answers the following research questions.

-

RQ1

What is the state of the art in ethical, social and environmental accounting methods?

-

•

-

RQ1.1

Which ESEA methods exist?

-

RQ1.2

What are the commonalities and differences in ESEA methods in terms of the process and data structure?

-

RQ1.1

-

RQ2

What are requirements for engineering a be part of a domain-specific modelling language for specifying ESEA methods?

-

•

-

RQ2.1

Which method constructs should be part of a domain ontology for ESEA methods?

-

RQ2.1

2.2 Overview of the research method

Figure 1 provides an overview of the research method. We have performed a multi-vocal literature review (activity A1) to search for ESEA methods. We collected both scientific and grey literature because in this domain we find much valuable information coming from practitioners Garousi et al. (2016). Practitioners can be part of networks of social enterprises such as B Corporations BLab (2018) and institutions such as the United Nations Williams (2004).

For each ESEA method identified in the literature, we have searched for and collected as much documentation as possible (activity A2). We are interested in sources of diverse nature, such as method manuals, standards related to the methods, websites providing instructions to users, tools supporting the methods, examples of the application of the methods (e.g. sustainability reports from companies applying the method).

Based on the collected documentation in activity A2 we have created a process deliverable diagram for each ESEA method (activity A3). The PDDs are validated with experts of the methods (activity A4). In the validation interview we present experts with the PDDs and ask them whether the process activities are complete and modelled in the correct order. Additionally, we ask them to validate whether all relevant deliverables are present in the PDD. After the validation interviews we improve and redesign the PDDs (activity A5) based on the expert feedback. Based on the validated PDDs we create the openESEA metamodel Ramautar and España (2022a).

3 Domain analysis of ethical, social and environmental methods

The following sections give a brief explanation of each of the analysed ESEA method. After the explanation the PDD of the corresponding method is depicted. For each PDD we have multiple versions, since ESEA methods evolve and so does our knowledge of said methods. In this report we present the latest versions of each of the method diagrams. Most diagrams are validated with experts on the method. However, not all diagrams are yet validated. Table 1 contains a list of all analysed ESEA methods.

3.1 AA1000AS

The AA1000 Assurance Standard (AA1000AS v3) is a method used by sustainability professionals for sustainability-related assurance engagements, to assess the nature and extent to which an organisation adheres to the AccountAbility Principles AccountAbility (2020). Initially we classified this method as an ESEA method. Currently we classify the method as an assurance standard, which covers the last part of the ESEA process.

3.2 B Impact Assessment

The B Impact Assessment BLab (2018) is a method developed by the not-for profit organisation B Lab. Application of the B Impact Assessment can result in an official B Corporation certification. In order to achieve the certification, organisation should meet the legal requirements and score at least 80 of the 200 points on the assessment. It is a private certification of for-profit companies, distinct from the legal designation as a Benefit corporation. B Corp certification is conferred by B Lab, a global nonprofit organisation.

3.3 CDP

The CDP (formaly know as the Carbon Disclosure Project) is an international non-profit organisation based in the United Kingdom, Japan, India, China, Germany and the United States of America that helps companies and cities disclose their environmental impact CDP (2021). The PDD depicts the process of applying the CDP company programs. CDP (for companies) has three corporate questionnaires; climate change, forests and water security. The questionnaires provide a framework for companies to provide environmental information to their stakeholders covering governance and policy, risks and opportunity management, environmental targets and strategy and scenario analysis.

3.4 Common Good Balance Sheet

The Common Good Matrix is a framework for the evaluation of business activities and an aid for organisational development Felber et al. (2019). It describes 20 Common Good themes and gives guidance on how to evaluate based on Common Good principles. A Common Good Report is a comprehensive evaluation of a company‘s contribution to the common good, and is prepared as part of the reporting process. It should include a description of how the company‘s activities relate to each of the 20 common good themes. This will show how developed each value is within the company. Each theme describes how the individual values apply to the relevant stakeholder group. The Certificate documents an externally audited evaluation of the individual themes, gives an, and presents this in the layout of the Matrix. Together, the Common Good Report and Certificate represent the Common Good Balance Sheet.

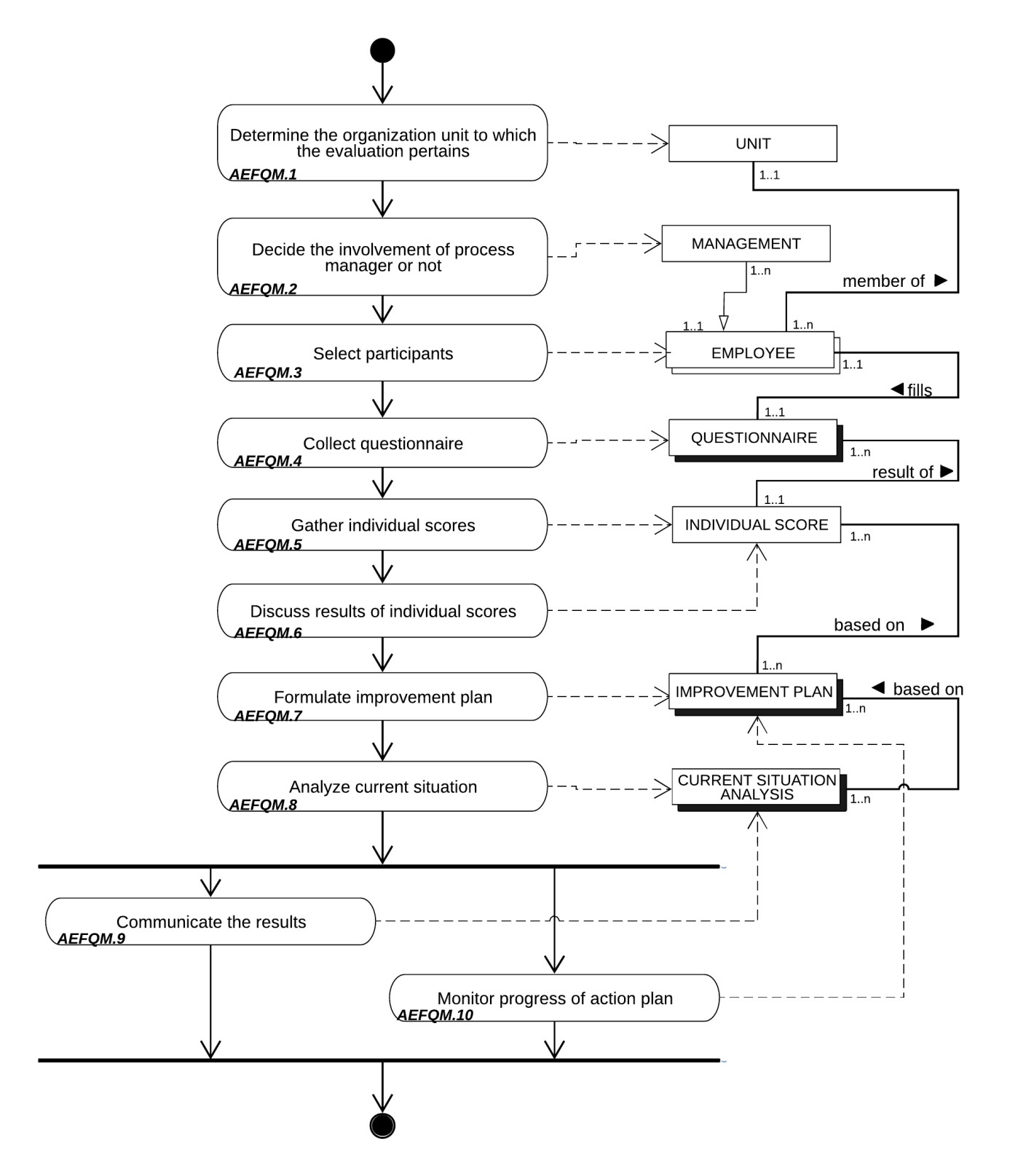

3.5 EFQM Model

The European Foundation for Quality Management (EFQM) Model, is a self-assessment framework for measuring the strengths and areas for improvement of an organisation across all of its activities Nabitz et al. (2000). Figure 6 shows the diagram of the self-assessment process and the corresponding deliverables.

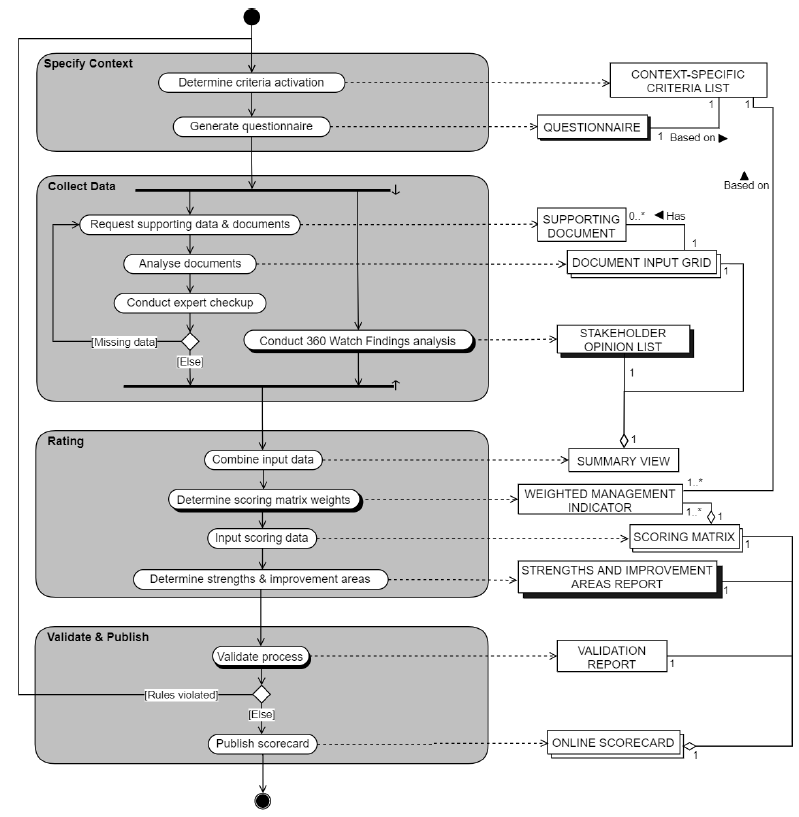

3.6 Ecovadis

Ecovadis was established in 2007. The company offers an environmental sustainability ratings platform to assess corporate social responsibility and sustainable procurement Ecovadis (2021). Figure 7 depicts the PDD of the sustainability assessment method offered by Ecovadis.

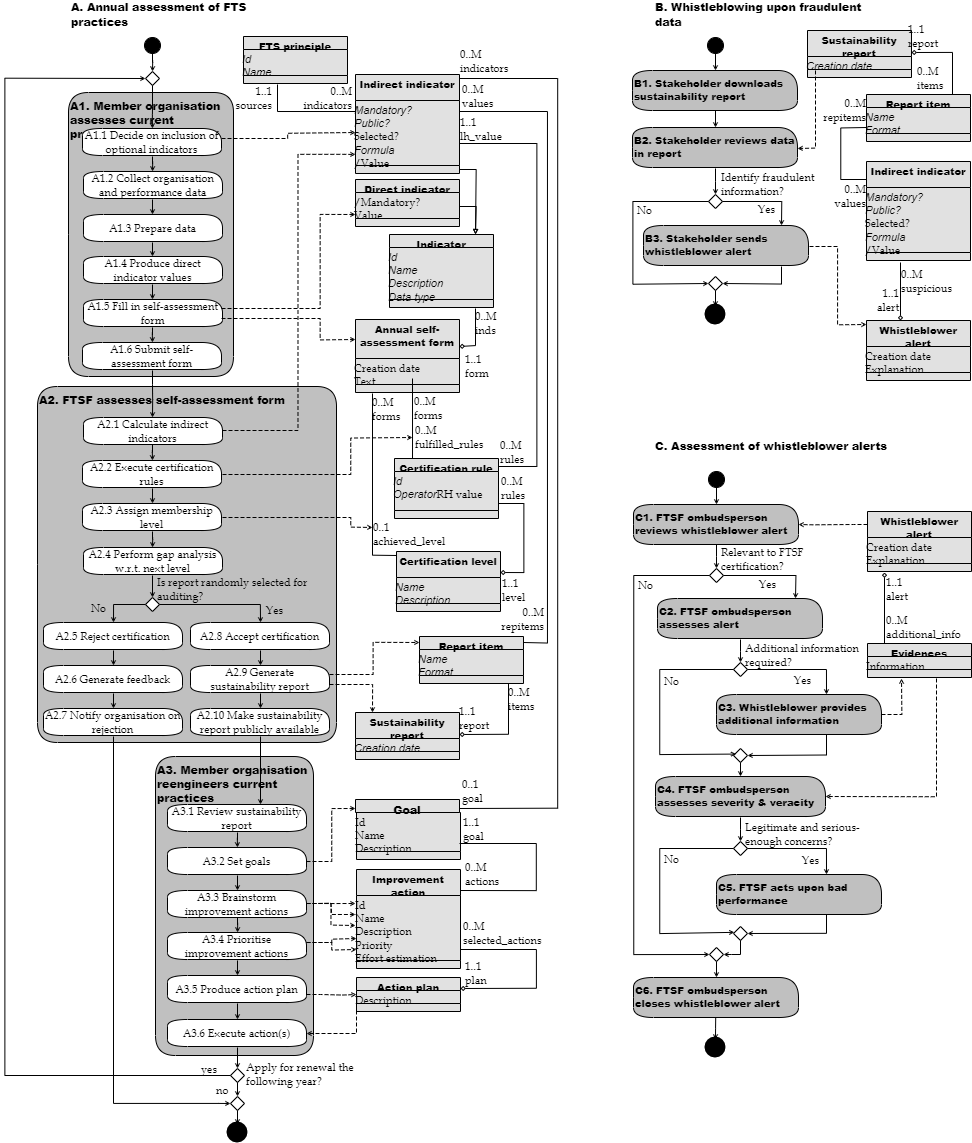

3.7 Fair Trade Software Foundation (FTSF) certification

Fair Trade is a social movement that aims to help producers in developing countries through partnerships promoting and selling their products. Fair Trade Software extends this concept into the software industry, whilst carefully adhering to the ten commonly accepted Fair Trade Principles established by the World Fair Trade Organization. A preliminary version of the FTSF certification method, that was designed in collaboration with FTSF stakeholders, is depicted in the PDD. The method has not yet been implemented.

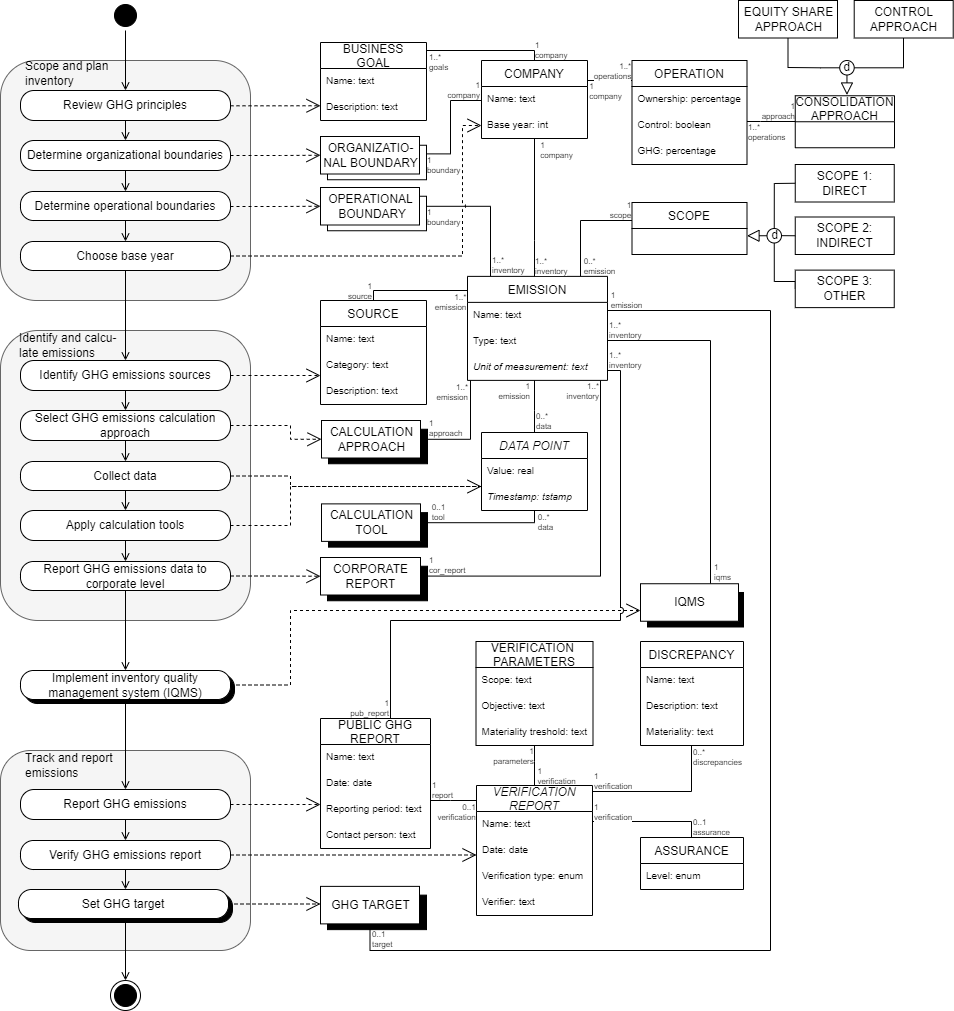

3.8 Greenhouse Gas Protocol

The Greenhouse Gas Protocol (GHG) Protocol Corporate Accounting and Reporting Standard provides requirements and guidance for companies and other organisations, such as NGOs, government agencies, and universities, that are preparing a corporate-level GHG emissions inventory Wbcsd (2004).

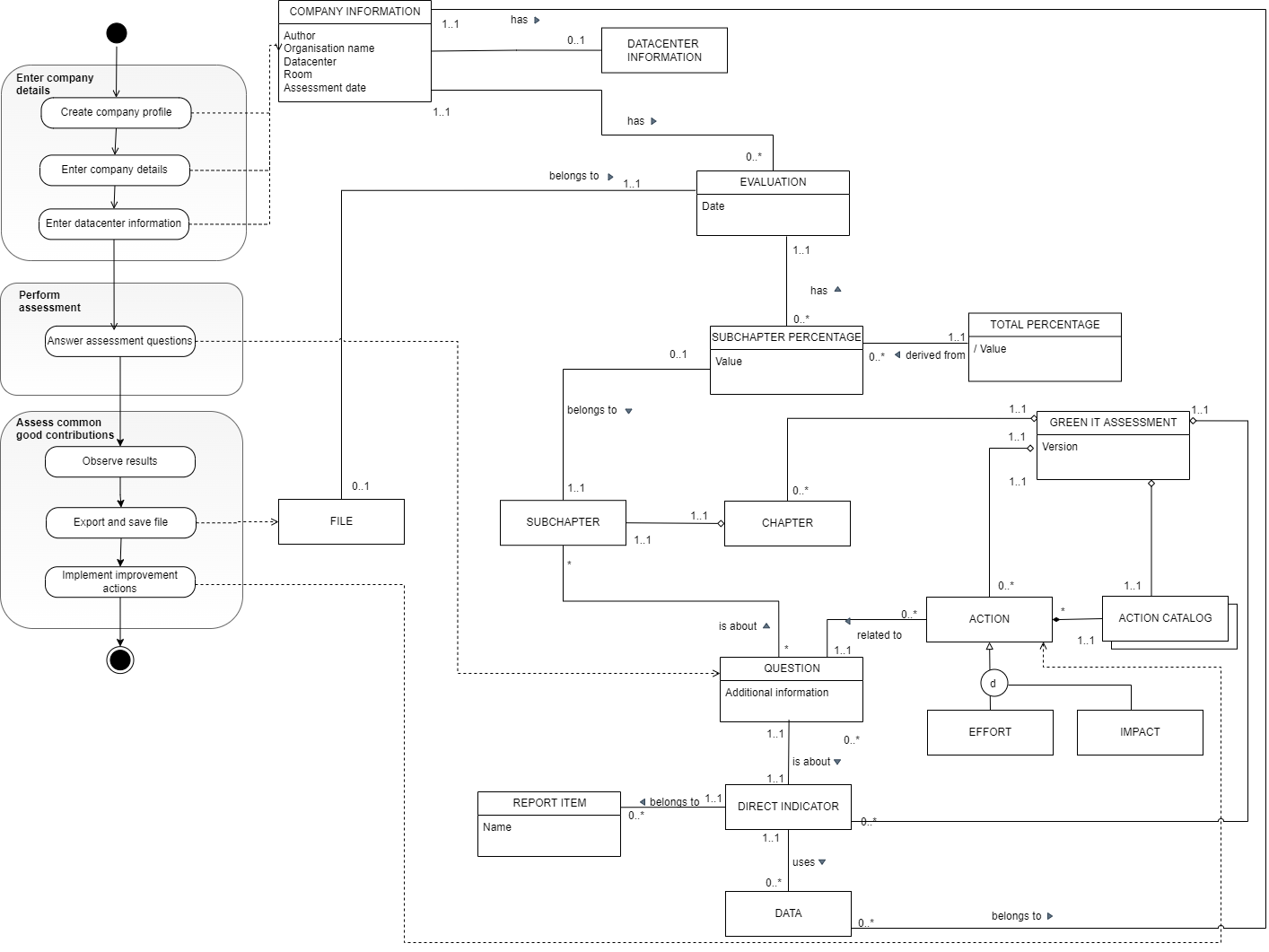

3.9 Data Centre Assessment

The Data Centre Assessment by Green IT Switzerland is a questionnaire, that assesses the maturity of data centres with regard to Green IT best practices. The questionnaire is made up of a hierarchical set of pages. Each page contains information and / or questions. Pages can be filled out in any order. The results of the assessment are available at any time, even if not all questions are answered yet.

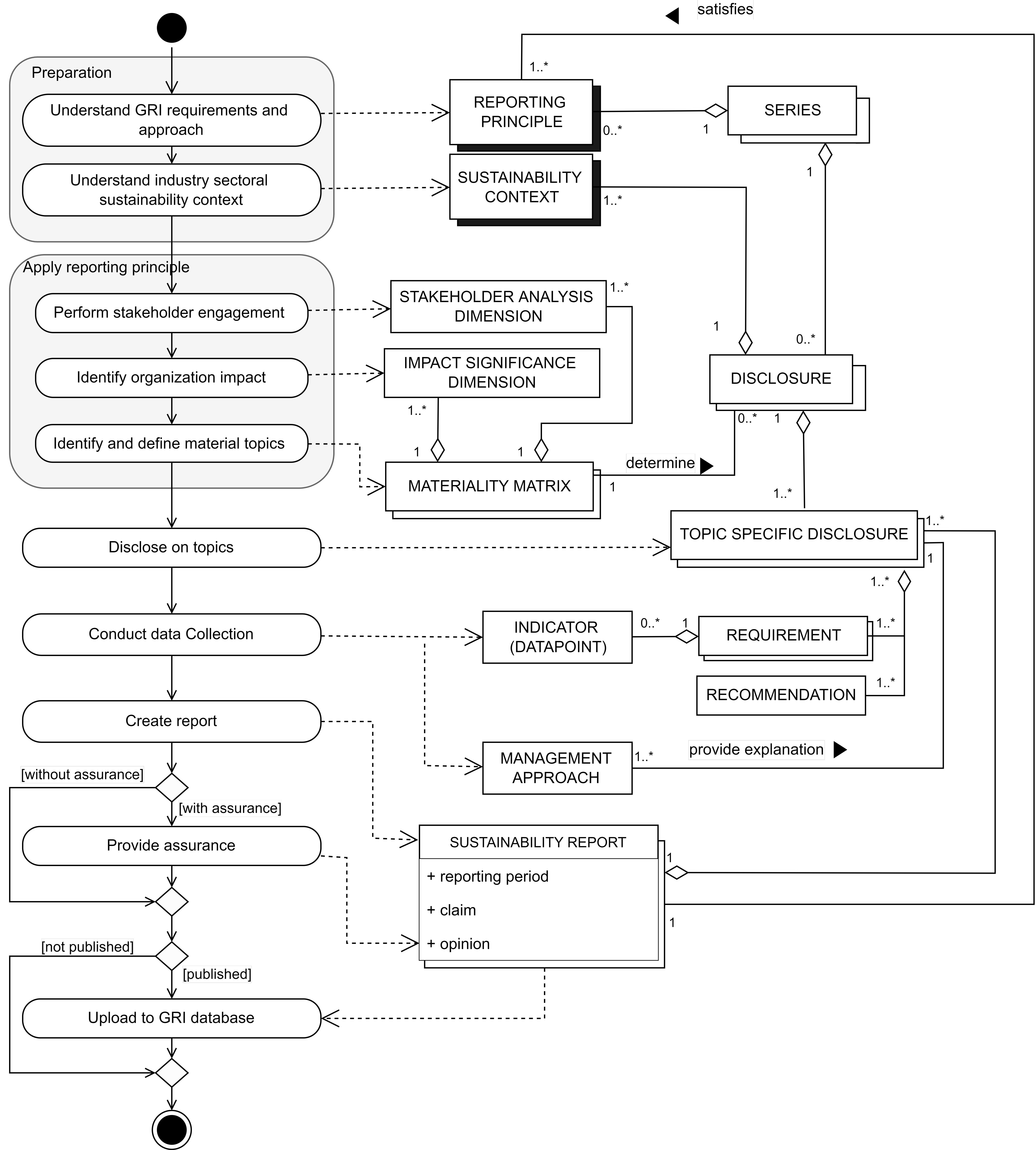

3.10 GRI Standards

The GRI Standards help organisations understand their outward impacts on the economy, environment, and society, including those on human rights GRI (2019). This increases accountability and enhances transparency on their contribution to sustainable development. The GRI Standards are a modular system comprised of three series of Standards to be used together: Universal Standards, Sector Standards, and Topic Standards. Organisations can either use the GRI Standards to prepare a sustainability report in accordance with the Standards or use selected Standards, or parts of their content, to report information for specific users or purposes, such as reporting their climate change impacts for their investors and consumers. The PDD shows an overview of constructing a sustainability report according to the GRI reporting guidelines.

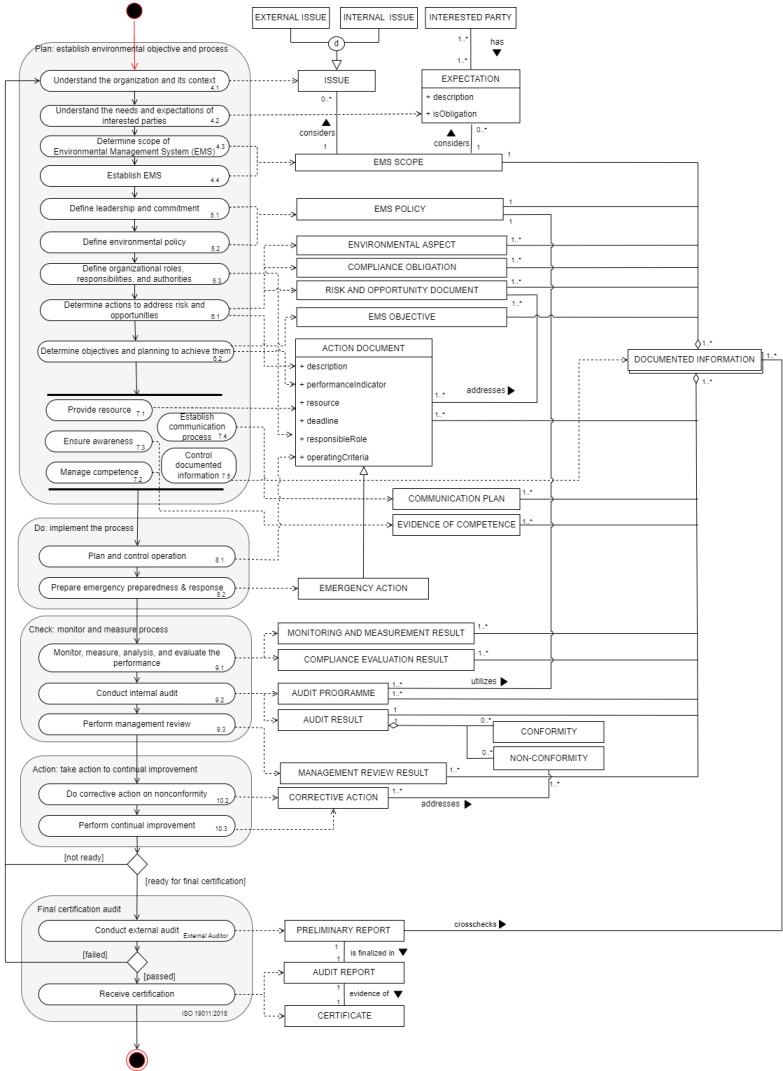

3.11 ISO14001

ISO 14001:2015 sets out the criteria for an environmental management system and can be certified to ISO (2015). Using ISO 14001:2015 can provide assurance to company management and employees as well as external stakeholders that environmental impact is being measured and improved.

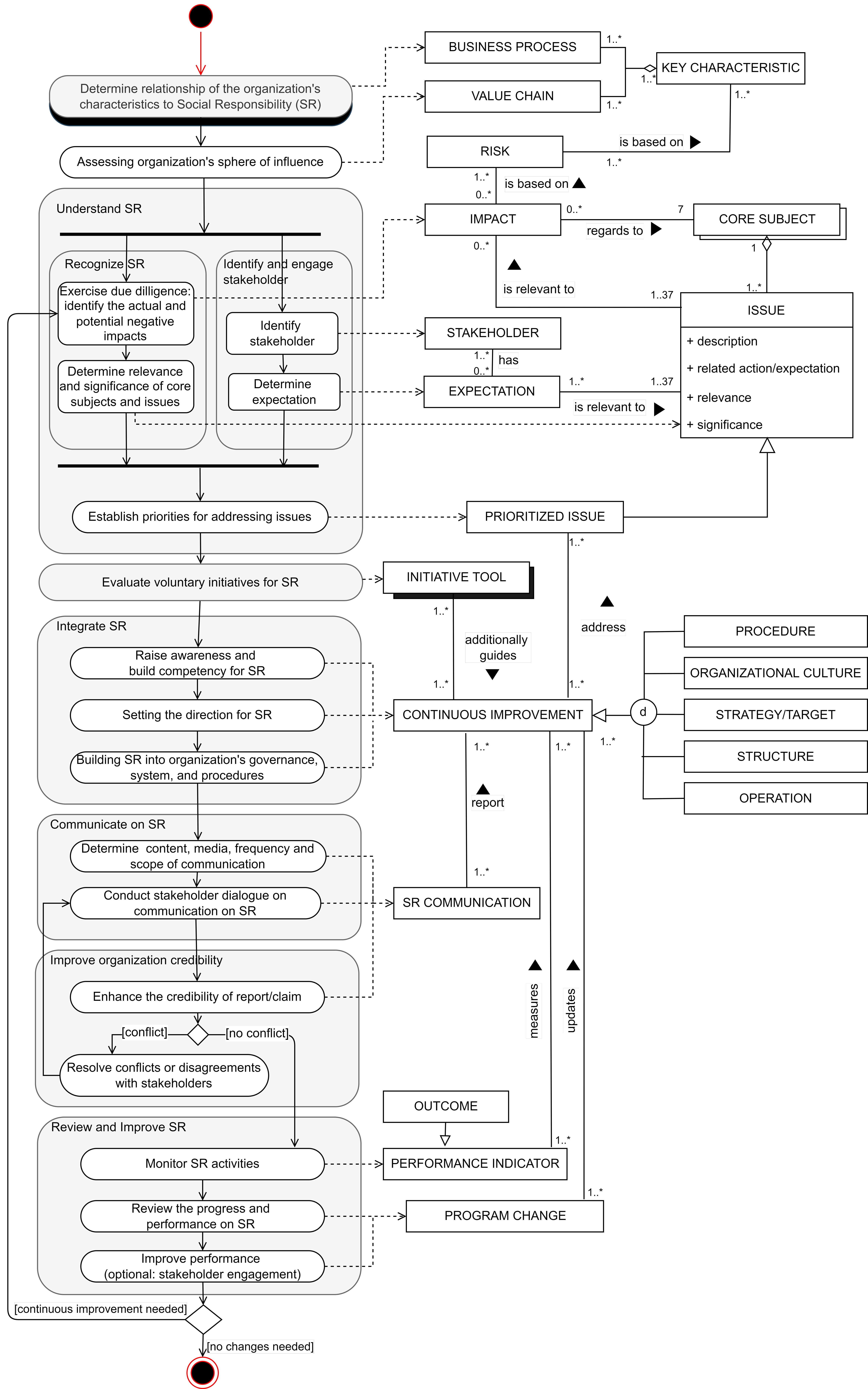

3.12 ISO26000

ISO 26000:2010 is intended to provide organisations with guidance concerning social responsibility and can be used as part of public policy activities Moratis and Cochius (2017). ISO 26000:2010 is not a management system standard. It is not intended or appropriate for certification purposes or regulatory or contractual use. As ISO 26000:2010 does not contain requirements, any such certification would not be a demonstration of conformity with ISO 26000:2010.

3.13 S-CORE

Sustainability – Competency, Opportunity, Reporting and Evaluation (S-CORE) is a web-based tool used to assess where and how sustainability lies within an organisation, while also providing insight into opportunities based on identified sustainability goals. S-CORE is not limited to a certain business type or size, and includes almost 100 practices across various sectors that span all levels and stages of sustainability implementation Hart (2016).

3.14 NCP

The Natural Capital Protocol is a decision-making framework that enables organisations to identify, measure and value their direct and indirect impacts and dependencies on natural capital Whitaker (2018). It is focused at a business decision-making level and helps organisations to understand the value of their dependence on ecosystem flows, rather than the value of natural capital stocks.

3.15 Sustainable Development Goals Compass

The Sustainable Development Goals (SDG) Compass was developed to meet the uncertainty about what actions an organisation can and should take in order to contribute to the goals, the SDG Compass is a guide that companies can use to align their strategies with the relevant SDGs, and measure and manage their impacts Briones Alonso et al. (2021).

3.16 SMETA

Sedex Members Ethical Trade Audit (SMETA) is an ethical accounting and audit method which encompasses aspects of responsible business practice. As a multi-stakeholder initiative, SMETA was designed to minimise duplication of effort and provide members and suppliers with an audit format they could easily share Medina Rodriguez (2016). SMETA reports are published in the SEDEX system, ensuring transparency and efficient information sharing.

SMETA audits use the ETI Base Code, founded on the conventions of the International Labor Organization, as well as relevant local laws. SMETA audits can be conducted against two or four auditing pillars. The two pillars mandatory for any SMETA audit are Labor Standards and Health & Safety. The two additional pillars of a 4-pillar audit are Business Ethics and Environment. They were introduced to further deepen the social responsibility aspect of SMETA audits.

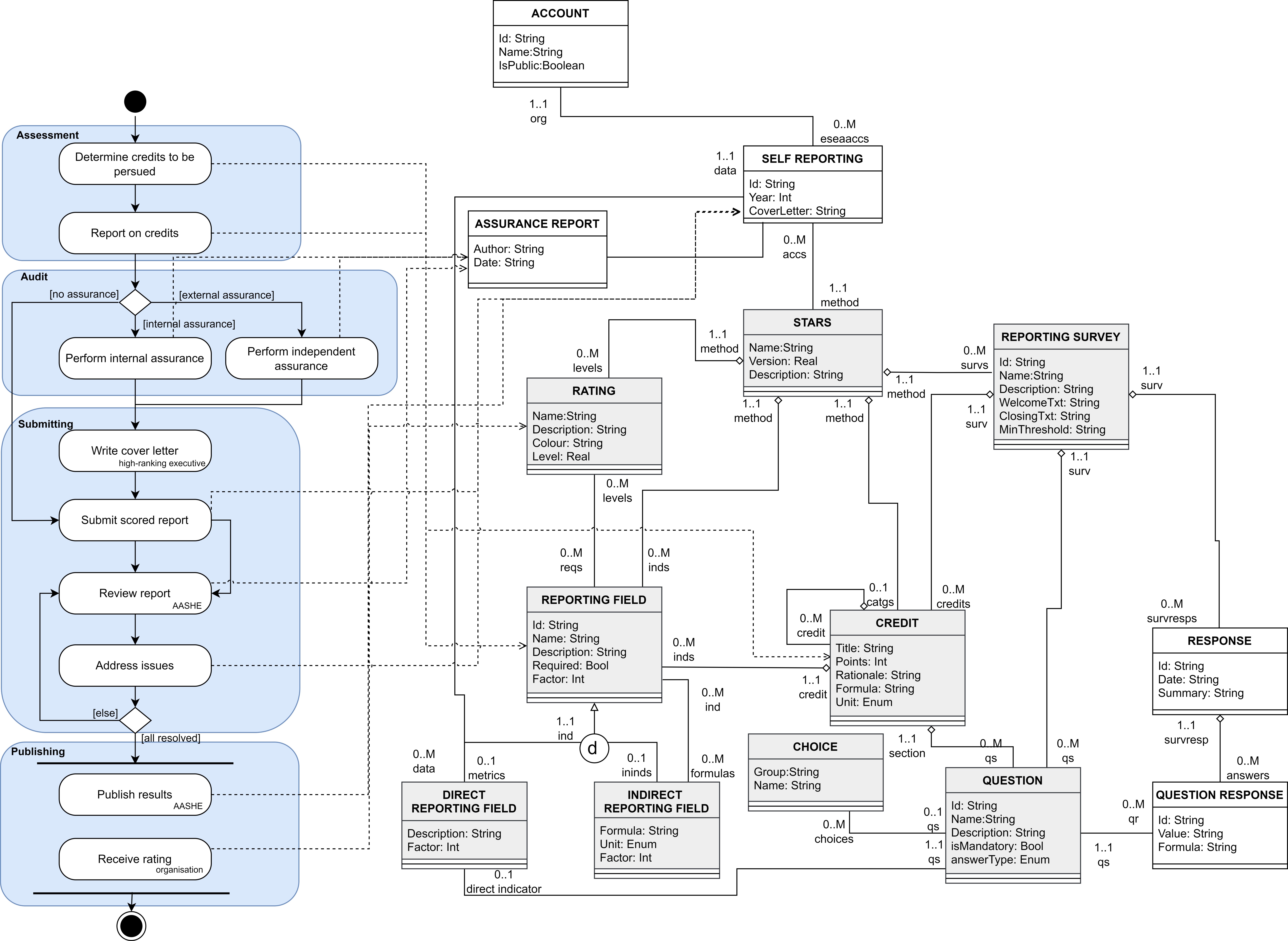

3.17 STARS

The Sustainability Tracking, Assessment & Rating System (STARS) is a transparent, self-reporting framework for colleges and universities to measure their sustainability performance Urbanski et al. (2015). STARS is intended to engage and recognise the full spectrum of higher education institutions, from community colleges to research universities. It encompasses long-term sustainability goals for already high-achieving institutions, as well as entry points of recognition for institutions that are taking first steps toward sustainability.

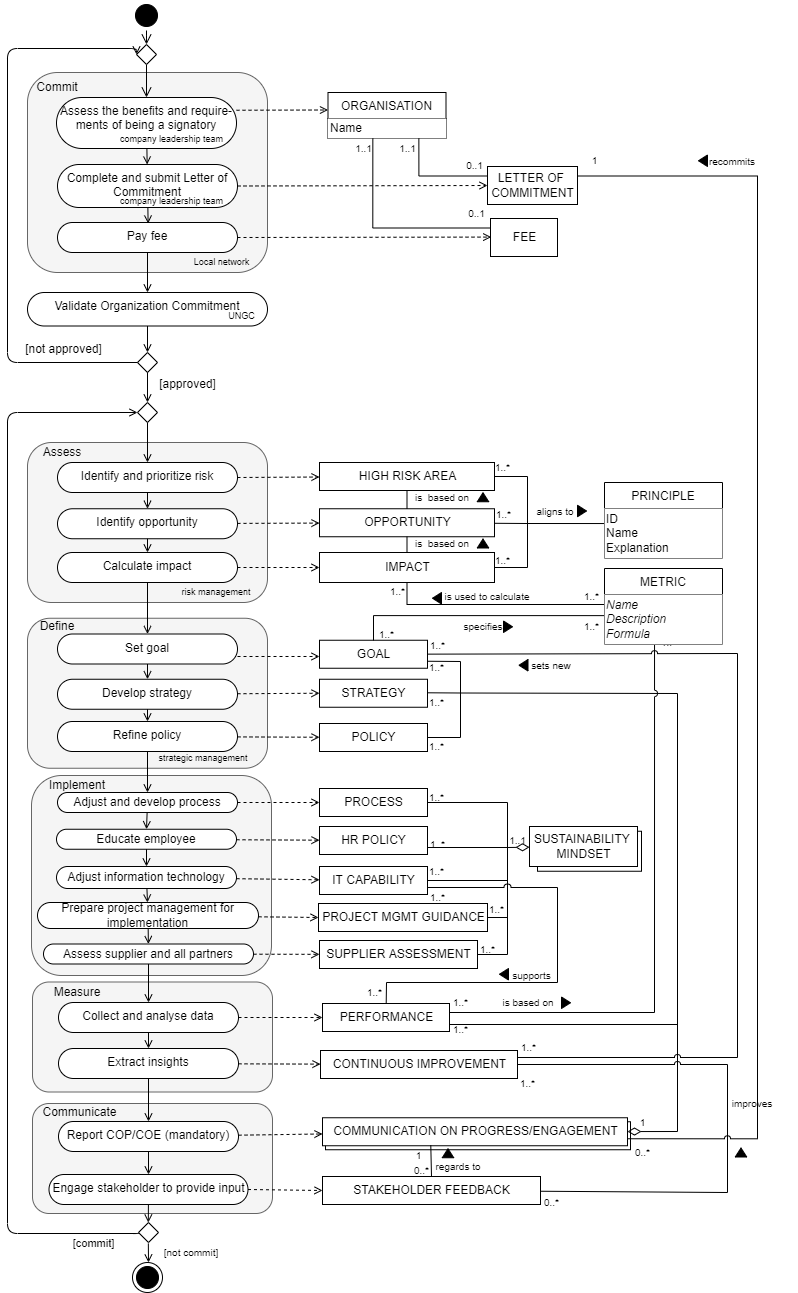

3.18 UNGC

The United Nations Global Compact is a non-binding United Nations pact to encourage businesses and firms worldwide to adopt sustainable and socially responsible policies, and to report on their implementation Williams (2004). The PDD of the ESEA method that ensures that companies adhere to the UNGC principles is shown in Figure19

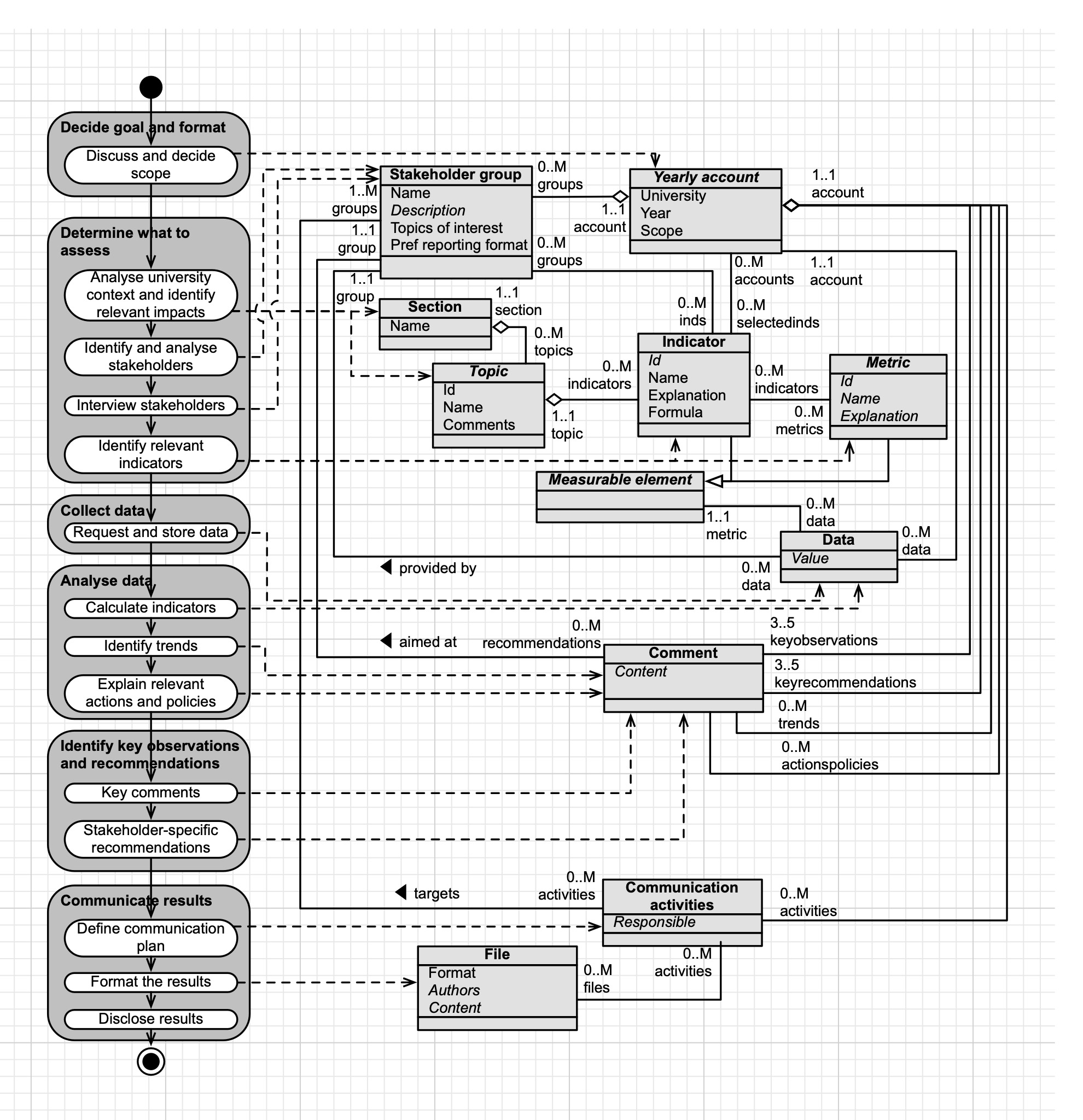

3.19 UniSAF

The University Sustainability Assessment Framework (UniSAF) is developed by rootAbility, a non-profit social business that promotes sustainability projects and initiatives in higher education. The method provides a set of indicators and methodology that can be used to gather and analyse data on the sustainability performance of university RootAbility (2017).

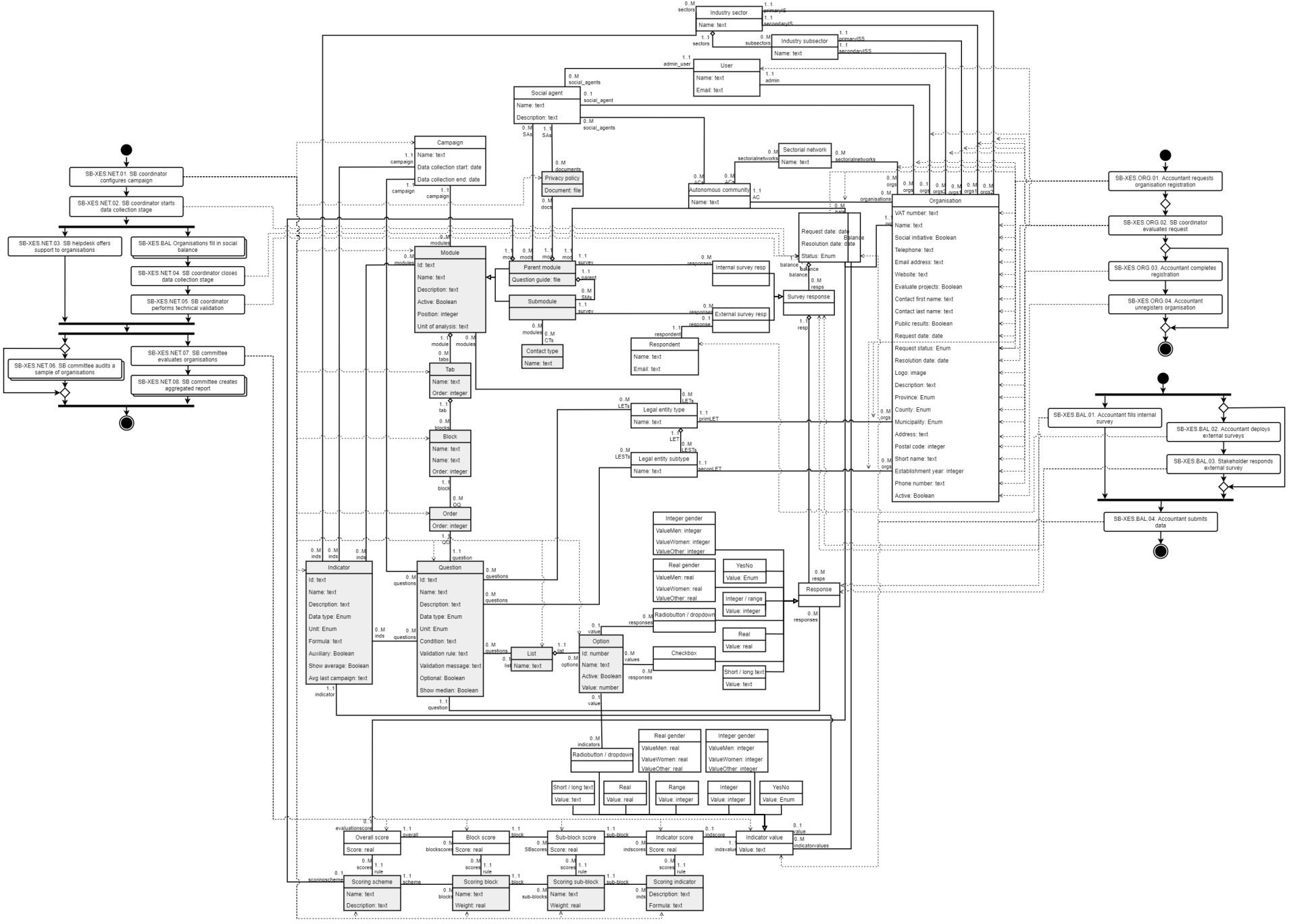

3.20 XES Social Balance

The XES Social Balance is used by the Catalan Network of Solidarity Economy (XES) to assess the performance of their members. The method has two variants: Basic Social Balance, Complete Social Balance. The complete one has more direct indicators (questions) and indirect indicators (indicators), and it also deploys multi-respondent surveys to several stakeholder groups (depending on the context of the organisation): workers/members, clients/suppliers, volunteers Crusellas et al. (2019).

4 Discussion of results

The openESEA metamodel is created based on the PDDs of ESEA methods. The PDDs are compared using the method comparison approach. This approach yields the metamodel depicted in Figure 22. An earlier version of the metamodel is presented in España et al. (2019). Based on the current version we have engineered an Xtext grammar. Using the Xtext grammar method engineers can create models of ESEA methods. Such models can be interpreted by our open-source model-driven tool, likewise called openESEA111https://github.com/sergioespana/openESEA. To test the comprehensibility and usability of the openESEA metamodel and grammar we ran an experiment. The results of the experiment are presented in Ramautar and España (2022b).

5 Conclusion

Over the course of the years our collection of ESEA method diagrams has grown rapidly. The models have helped us better understand ESEA methods and they have laid foundations for further analysis and software design and development. The domain analysis presented in this report has enabled several project already. We have created the first version of model-driven ESEA method interpreter España et al. (2019), an extension of the tool that generates infographics automatically España et al. (2022), the investigation of ESEA method selection criteria Ramautar and España (2022c), the engineering of the openESEA DSL Ramautar and España (2022b). In the future we plan to publish information on ESEA methods, as well as the PDDs in an online repository.

6 Acknowledgements

We thank all the students of Utrecht University’s Business Informatics master’s programme who modelled, validated, or improved PDDs as part of their graduation projects. Moreover, we express our gratitude to all the ESEA method experts who helped modelling and validating the diagrams. Without the contributions of all collaborations we would not have been able to present such a detailed collection of ESEA method models.

References

- van de Weerd and Brinkkemper [2009] Inge van de Weerd and Sjaak Brinkkemper. Meta-modeling for situational analysis and design methods. In Handbook of research on modern systems analysis and design technologies and applications, pages 35–54. IGI Global, 2009.

- van de Weerd et al. [2007] Inge van de Weerd, Stefan de Weerd, and Sjaak Brinkkemper. Developing a reference method for game production by method comparison. In Working Conference on Method Engineering, pages 313–327. Springer, 2007.

- Ramautar and España [2022a] Vijanti Ramautar and Sergio España. The openESEA Modelling Language for Specifying Ethical, Social and Environmental Accounting Methods. Technical report, January 2022a. URL https://doi.org/10.48550/arXiv.2205.15279.

- España et al. [2019] Sergio España, Niels Bik, and Sietse Overbeek. Model-driven engineering support for social and environmental accounting. In 2019 13th International Conference on Research Challenges in Information Science (RCIS), pages 1–12. IEEE, 2019.

- Garousi et al. [2016] Vahid Garousi, Michael Felderer, and Mika V Mäntylä. The need for multivocal literature reviews in software engineering: complementing systematic literature reviews with grey literature. In Proceedings of the 20th international conference on evaluation and assessment in software engineering, pages 1–6, 2016.

- BLab [2018] BLab. B Impact Assessment. https://bimpactassessment.net/, 2018. Accessed: 2021-11-24.

- Williams [2004] Oliver F Williams. The UN Global Compact: The challenge and the promise. Business Ethics Quarterly, 14(4):755–774, 2004.

- AccountAbility [2020] AccountAbility. AA1000. https://www.accountability.org/standards/aa1000-assurance-standard/, 2020. Accessed: 2022-06-16.

- CDP [2021] CDP. https://www.cdp.net/en, 2021. Accessed: 2022-06-16.

- Felber et al. [2019] Christian Felber, Vanessa Campos, and Joan R Sanchis. The common good balance sheet, an adequate tool to capture non-financials? Sustainability, 11(14):3791, 2019.

- Nabitz et al. [2000] Udo Nabitz, Niek Klazinga, and Jan Walburg. The EFQM excellence model: European and Dutch experiences with the EFQM approach in health care. International journal for quality in health care, 12(3):191–202, 2000.

- Ecovadis [2021] Ecovadis. Ecovadis Sustainability Assessment. https://ecovadis.com/suppliers/, 2021. Accessed: 2022-06-16.

- Wbcsd [2004] WRI Wbcsd. The greenhouse gas protocol. A corporate accounting and reporting standard, 2004.

- GRI [2019] GRI Standards. https://globalreporting.org/standards/, 2019. Accessed: 2021-11-24.

- ISO [2015] ISO 14001:2015 standard. https://www.iso.org/iso-14001-environmental-management.html, 2015. Accessed: 2021-11-24.

- Moratis and Cochius [2017] Lars Moratis and Timo Cochius. ISO 26000: The business guide to the new standard on social responsibility. Routledge, 2017.

- Hart [2016] Maureen Hart. Is your organization on the right path for sustainability? using s-core to evaluate sustainability efforts. In Brown Bag Archive. Ngwa, 2016.

- Whitaker [2018] Samir Whitaker. The natural capital protocol. In Debating Nature’s Value, pages 25–38. Springer, 2018.

- Briones Alonso et al. [2021] Elena Briones Alonso, Jan Van Ongevalle, Nadia Molenaers, and Saartje Vandenbroucke. Sdg compass guide: Practical frameworks and tools to operationalise agenda 2030, 2021.

- Medina Rodriguez [2016] Alicia Medina Rodriguez. The application of the smeta audit protocol on the management of the csr of peruvian companies: a case study of standardization via smeta in manufacturing companies. 2016.

- Urbanski et al. [2015] Monika Urbanski et al. Measuring sustainability at universities by means of the sustainability tracking, assessment and rating system (stars): early findings from stars data. Environment, Development and Sustainability, 17(2):209–220, 2015.

- RootAbility [2017] RootAbility. University sustainability assessment framework (uniSAF). http://rootability.com/greenoffices/assessment/, 2017.

- Crusellas et al. [2019] Raquel Alquézar Crusellas, Ruben Suriñach Padilla, and Xarxa d’Economia Solidaria. El balance social de la xes: 10 años midiendo el impacto de la ess en cataluña. In Conferência Genebra 2019. UNTFSSE, 2019.

- Ramautar and España [2022b] Vijanti Ramautar and Sergio España. Engineering a Modelling Language for Ethical, Social and Environmental Accounting. In Submitted to the 21st International Conference on Perspectives in Business Informatics Research, 2022b.

- España et al. [2022] Sergio España, Vijanti Ramautar, Sietse Overbeek, Tijmen Derikx, et al. A domain specific language for data-centric infographics. 2022.

- Ramautar and España [2022c] Vijanti Ramautar and Sergio España. Decision-Making Criteria for Ethical, Social and Environmental Accounting Selection. In Submitted to the 1st International Conference of the Economy for the Common Good, 2022c.

Appendix A: List of analysed ESEA method

| Method | Release year | Organisation | URL |

|---|---|---|---|

| AA1000AS | 1999 | AccountAbility | https://www.accountability.org/standards/aa1000-assurance-standard/ |

| B Impact Assessment | 2007 | B Lab | https://bimpactassessment.net/ |

| CDP | 2016 | CDP | https://www.cdp.net/en/companies |

| Common Good Balance Sheet | 2010 | Economy for the Common Good | https://www.ecogood.org/apply-ecg/companies/#balance-sheet-resources |

| EcoVadis | 2007 | EcoVadis | https://ecovadis.com/ |

| EFQM Model | 1992 | European Foundation for Quality Management (EFQM) | https://www.efqm.org/efqm-model/ |

| FTSF Certification | 2010 | Fair Trade Software Foundation | https://ftsf.eu/about-us |

| Greenhouse Gas Protocol | 2001 | Greenhouse Gas Protocol | https://ghgprotocol.org/standards |

| Data Center Assessment | 2017 | Green IT Switzerland | https://greenit-switzerland.ch/app/dca/en/dc-assessment |

| GRI Standards | 2000 | Global Reporting Initiative | https://www.globalreporting.org/how-to-use-the-gri-standards/ |

| ISO14001 | 2004 | International Organization of Strandardization | https://www.iso.org/iso-14001-environmental-management.html |

| ISO26000 | 2010 | International Organization of Strandardization | https://www.iso.org/iso-26000-social-responsibility.html |

| Natural Capital Protocol | 2016 | Capitals Coalition | https://capitalscoalition.org/capitals-approach/natural-capital-protocol/?fwp_filter_tabs=training_material |

| S-CORE | 2005 | International Society of Sustainability Professionals | https://sustainablemeasures.com/ |

| Sustainable Development Goals Compass | 2015 | GRI, the UN Global Compact and the World Business Council for Sustainable Development (WBCSD) | https://sdgcompass.org/download-guide/ |

| SMETA | 2017 | Sedex | https://www.sedex.com/our-services/smeta-audit/ |

| STARS | 2007 | Association for the Advancement of Sustainability in Higher Education (AASHE) | stars.aashe.org |

| UN Global Compact | 2000 | United Nations | https://www.unglobalcompact.org/what-is-gc/mission/principles |

| UniSAF | 2017 | Student Organization for Sustainability International | https://www.greenofficemovement.org/sustainability-assessment/ |

| WFTO certification | 2013 | World Fair Trade Organization | https://wfto.com/what-we-do#our-guarantee-system |

| XES Social Balance | - | Catalan Network of Solidarity Economy | https://xes.cat/ |