Bartlett’s Delta revisited: Variance-optimal hedging in the lognormal SABR and in the rough Bergomi model

Abstract

We derive analytic expressions for the variance-optimal hedging strategy and its mean-square hedging error in the lognormal SABR and in the rough Bergomi model. In the SABR model, we show that the variance-optimal hedging strategy coincides with the Delta adjustment of Bartlett [Wilmott magazine 4/6 (2006)]. We show both mathematically and in simulation that the efficiency of the variance-optimal strategy (in comparison to simple Delta hedging) depends strongly on the leverage parameter and – in a weaker sense – also on the roughness parameter of the model, and give a precise quantification of this dependency.

1 Introduction

Delta-hedging, as the unique strategy to eliminate all hedging risk in the Black-Scholes model, has been one of the pillars of classical finance. By using the option-implied Delta, Delta-hedging is easily adapted to models beyond Black-Scholes. However, it has been well understood that other risk factors, such as changes in volatility (Vega risk), also have to be taken into account in effective hedging strategies. Within the setting of local or stochastic volatility models, the derivation of such adjustments to Delta-hedging has been repeatedly considered in the literature. Crepéy, for example, proposes in [Cré04] an adjustment of the form

| (1) |

where is the derivative of implied volatility with respect to strike. Hull and White consider in [HW17] an adjustment of the form

| (2) |

where the coefficients , and are determined by regression. Importantly, they emphasize that their regression approach corresponds to minimizing the variance of the hedging error. Here, we also follow this variance-optimality approach, which has originally been introduced and thoroughly explored in a general setting by Föllmer and Schweizer [Sch84, FS88]. We assume that a description of the dynamic evolution of the option-implied volatility is available, and we obtain a general expression for the variance-minimizing hedging strategy and its mean-square error in Section 2. We then focus on the application of these theoretical results to optimal hedging in the SABR model [HKLW02] and in its extension to ‘rough volatility’ (see [GJR18]), the rough Bergomi model introduced in [BFG16].

Already in [HKLW02], an adjusted Delta hedge for the SABR model is proposed by Hagan-Kumar-Lesniewski-Woodward (HKLW), taking the form

| (3) |

Aiming to improve the HLKW strategy, Bartlett proposes in [Bar06] the adjustment111All parameters refer to the SABR model as discussed in Section 3 below.

| (4) |

which is subsequently discussed as ‘Bartlett’s Delta’ in [HL17]. In Section 3, we show mathematically that Bartlett’s hedge corresponds exactly to the variance-optimal hedge in the SABR model. Moreover, we derive analytic expressions for the mean-square hedging errors of the classic Delta-hedge, the HLKW-hedge and the Bartlett/variance-optimal hedge, allowing us to compare the strategies on a theoretical basis, in addition to their numerical evaluation. Subsequently, we show in Section 4 that our ‘dynamic implied volatility’ framework for variance-optimal hedging can also be applied to rough stochastic volatility models, which are neither Markovian nor semi-martingales. Combining our framework with the implied-volatility approximations of Fukasawa and Gatheral [FG22] for the rough Bergomi model [BFG16], we derive analytic expressions for the variance-optimal hedging strategy and its mean-square error. In particular, we discover an interesting interplay between the leverage parameter and the roughness parameter in determining the efficiency of the variance-optimal strategy. In section 5 we report numerical results for the SABR and the rough Bergomi model, which confirm our theoretical findings.

2 Background

2.1 Variance-optimal hedging

Let be the stock price and be the price of a contingent claim with maturity . For simplicity we set interest rates to zero and we assume that there exists a risk-neutral measure under which both and are square-integrable martingales. Let be a strategy to hedge the payoff . Then we can write

where the terms on the right hand denote, respectively: the initial capital , the accumulated value of the hedging portfolio and the pathwise hedging error . Note the similarities to linear regression: We are regressing (the stochastic process) onto the hedging portfolios in , with regression coefficient , intercept , and residual . In a complete market we can find a perfect hedging strategy such that the terminal pathwise hedging error is identical to zero and the unique initial capital needed is . However, in an incomplete market model, such as the SABR model or other rough and non-rough stochastic volatility models, there is no perfect hedging strategy. Thus, we have to decide on another criterion of optimality to select a suitable strategy . Here, we focus on the principle of variance-optimality, introduced by [Sch84, FS88], which aims to find the initial capital and the variance-optimal strategy , which minimizes the risk-neutral222One can also start from a non-risk-neutral measure and minimize the MSHE under . This leads to the rich subject of mean-variance hedging, cf. [Sch92], which we do not consider here. mean-square hedging error (MSHE)

| (5) |

The proper mathematical framework is to assume that belongs to the Hilbert space (cf. [JS13, I.4a])

of square integrable continuous martingales with norm and inner product ; and to restrict the hedging strategies to

Finally, two martingales are called orthogonal in the strong sense, if their quadratic covariation vanishes, i.e., if . If , then this strong orthogonality implies orthogonality in the Hilbert-space . The key observations are that

-

•

equation (5) is minimized by the orthogonal projection in of the martingale onto the closed subspace spanned by the integrals where ranges through ; and that

-

•

the residual of this projection must be orthogonal to ; even in the strong sense of (cf. [KW67]).

Strong orthogonality of and implies that

for all . Rearranging yields the variance-optimal strategy as

where the right-hand side has to be read as the Radon-Nikodym derivative of the finite-variation processes and . Note the similarity to linear regression, where the regression coefficient is obtained as the covariance between the dependent and the independent variable, divided by the variance of the independent variable.

Above, and in what follows, we make frequent use of the following calculation rules for quadratic covariations of continuous Ito processes (see [JS13, §I.4d-e]) of dimensions and respectively:

-

Q-I.

If and , then ,

-

Q-II.

If , then

-

Q-III.

if or has finite variation.

2.2 Variance-optimal hedging and implied volatility

We restrict our attention to the case where is the price process of a call option with maturity and strike price . To the call-price we can associate its (time-) implied volatility and rewrite as

| (6) |

where is the Black-Scholes price in dependence on time-to-maturity, underlying and implied volatility. As a smooth function of the martingales and , the process must be a semi-martingale. We introduce the following notation for the Black-Scholes Greeks and related quantities, given :

Combining (6) with the variance-optimal hedging framework from above, we get a representation of the variance-optimal strategy in terms of Delta and Vega:

Theorem 2.1.

The variance-optimal hedging strategy for a call option with implied volatility process is

| (7) |

with initial capital . The mean-square hedging error of this strategy is

| (8) |

where the ‘orthogonal vol-of-vol’ process is given by

| (9) |

Remark 2.1.

We add some intuition to the nature of the orthogonal vol-of-vol process . First, define

which is the component of which is orthogonal to , i.e., we have . The process can now be written as , hence ‘orthogonal vol-of-vol’.

In addition, we can derive the following formula to evaluate the mean-square hedging error of any (not necessarily variance-optimal) hedging strategy:

Theorem 2.2.

Let be a hedging strategy for a call option with initial capital and implied volatility process . Then the mean-square-hedging error of the strategy is given by

| (10) |

.

Applying this formula to the simple Delta-hedge we obtain the following corollary:

Corollary 2.3.

The mean-square hedging error of the Delta-Hedging strategy is

| (11) |

and the difference to the error of the variance-optimal strategy (8) is equal to

| (12) |

Remark 2.2.

Proof of Thms. 2.1, 2.2 and Cor. 2.3.

Using property Q-I from above, we have

To compute the MSHE of an arbitrary strategy , note that

and calculate, using property Q-II,

| (13) |

Using property Q-I again, we obtain

which gives (10). Inserting the variance-optimal strategy yields

which gives (8). Inserting the Delta-hedging strategy, on the other hand, yields (11). ∎

To compute the variance-optimal strategy from Theorem 2.1, we need a tractable description of the dynamic implied volatility process , which is rarely available in stochastic volatility models. However, in certain models, such as the SABR and the rough Bergomi model, accurate dynamic approximations of are available, due to [HKLW02, Bal06, FG22]. This is our key to obtaining explicit approximate variance-optional strategies for these models in the following sections.

3 The SABR model

We consider the SABR model of [HKLW02] in its conditionally lognormal form, i.e., with , which takes the form

where with . We parameterize vol-of-vol by for consistency with the rough Bergomi model, as discussed in Section 4. An asymptotically arbitrage-free approximation of in the lognormal SABR model is given by [FG22] (see also [Bal06]) as

| (14) |

where is given by the famous SABR formula of Hagan et al. [HKLW02]:

| (15) |

We denote by , , , etc. the Black-Scholes Greeks (and related quantities) evaluated at the approximation rather than the exact implied volatility .

3.1 Bartlett’s Delta is the variance-optimal strategy

We consider and compare the following three hedging strategies for the SABR model:

-

•

The (classic) Delta hedging strategy , which uses the Black-Scholes-Delta evaluated at the SABR-implied volatility;

- •

- •

Our first result shows that Bartlett’s strategy is variance-optimal (up to the approximation error induced by the approximation ) , i.e., no other hedging strategy can obtain a smaller hedging error in the mean-square sense.

Theorem 3.1.

Remark 3.1.

Theorem 3.2.

The approximate mean-squared hedging errors for the Bartlett/variance-optimal strategy, the Hagan-Kumar-Lesniewski-Woodward strategy and the simple Delta strategy are

| (17) | ||||

| (18) | ||||

| (19) |

Remark 3.2.

-

(a)

It can be seen that in the ‘complete market limit’ , the MSHE vanishes only for the Bartlett/variance-optimal strategy. The other two strategies are not able to fully exploit the correlation of stock price and stochastic variance.

-

(b)

The formulas for the MSHE are calculated ‘within-approximation’, i.e. the approximation is used to both calculate the strategy and to evaluate its error. A more honest evaluation would be to calculate the strategy using and to evaluate the error using . We expect the error approximations to be biased towards zero (that is, a little too optimistic) compared to this honest evaluation.

Comparing the hedging errors of the strategies in Thm. 3.2, we can compute the difference of the mean-squared hedging error of the simple Delta strategy and the Bartlett/variance-optimal strategy as

| (20) |

Moreover, it is easy to see that

i.e. the error of the HKLW-strategy is always larger than the error of the Bartlett/variance-optimal strategy by a factor of , independent of all other model parameters. Finally, taking the difference of HKLW and the simple Delta strategy yields

| (21) |

For , the HKLW strategy improves upon the simple Delta hedge, which was the original intention of Hagan et al. For larger , the conclusion from (21) becomes unclear; the first-order analysis below shows that we should expect the simple Delta hedge to have the smaller error.

Proof of Thms. 3.1 and 3.2.

Applying Ito’s formula to (14) we obtain

Hence, we have

Together with

and inserting into (7) we obtain the approximate variance-optimal strategy (16); coinciding with (4). For the mean-square hedging error, we calculate

Inserting into (9) we obtain the orthogonal vol-of-vol process

from Thm. 2.1 we obtain (17). The expressions for the mean-square hedging errors of the HKLW- and the simple Delta strategy follow by applying Thm. 2.2. ∎

3.2 First-order analysis

We simplify the comparison of the different hedging strategies, using the first-order approximation

of the SABR implied volatility from [FG22]. Under this approximation

| (22) |

and the Bartlett/variance-optimal strategy is approximated by

The mean-squared hedging errors of the Bartlett/variance-optimal, the HKLW- and the Delta strategy become

| (23) | ||||

| (24) | ||||

| (25) |

such that our first-order analysis suggests

| (26) |

Note, however, that the non-asymptotic result (21) shows an advantage of the HKLW-strategy over the Delta hedge for , which gets lost in the first-order approximation.

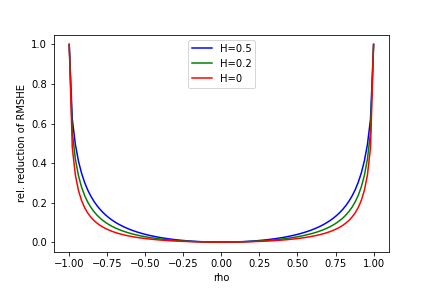

An interesting quantity to analyze is the relative reduction in root-mean-square error of the Bartlett/variance-optimal strategy in comparison to the Delta hedge. Using (23) and (25) we obtain

| (27) |

Note that this expression is independent of the option’s strike and its time-to-maturity, but loses accuracy for ITM/OTM options. The quantity is shown as a function of in Figure 1. It is flat around zero and only starts to rise steeply in vicinity of the endpoints . This suggest that the advantage of the Bartlett/variance-optimal hedge over the Delta hedge only starts to manifest in models with a leverage close to . A half-way reduction of the root-mean-squared error, for example, is achieved only at .

4 The rough Bergomi model

We consider the rough Bergomi model, introduced in [BFG16] to generalize Bergomi’s model [Ber08], with price process and forward variance given by

Here, with ; is the power-law kernel with , and . Note that the Hurst parameter controls the roughness of the volatility process and the kernel reproduces the power-law behavior of the volatility skew, cf. [GJR18]. An asymptotically arbitrage-free approximation of is given by [FG22] as

| (28) |

where

and is the solution of the ODE

| (29) |

We will also need the auxilliary process

and use the approximations

| (30) |

which become exact in the limit , see [FG22]. Note that they are also exact in the limit, i.e., in the SABR model, see Sec. 3.

4.1 Variance-Optimal Hedging

Theorem 4.1.

The approximate variance-optimal strategy for the rough Bergomi model, obtained by substituting for in (7) and using the approximations (30), is given by

| (31) |

where

and the solution of (29). The approximate mean-squared hedging error, obtained by substituting for in (8) and using the approximations (30) is given by

| (32) |

Remark 4.1.

Corollary 4.2.

Let denote the Delta-hedging strategy (using the approximate implied volatility ). The approximate mean-square hedging error of this strategy is

| (33) |

and its difference to the error of the approximate variance-optimal strategy is given by

| (34) |

Proof of Thm. 4.1 and Cor. 4.2.

From [FG22] we know that

Hence, we have

Together with

and inserting into (7) we obtain the approximate variance-optimal strategy (31). For the mean-square hedging error, we calculate

Inserting into (9) we obtain the orthogonal vol-of-vol process

Together with (8) and using the approximations (30) we obtain (32). Cor. 4.2 now follows by an application of Cor. 2.3. ∎

4.2 First-order analysis

We use the first-order approximation

of the rough Bergomi implied volatility, as given in [FG22]. Under this approximation

| (35) |

Using these approximations, the error of the approximate variance-optimal and the Delta strategy become

| (36) | ||||

| (37) |

The ratio of these quantities evaluates to

Taking derivatives, it is easy to see that this ratio is decreasing in on . Consequently, the relative reduction of the hedging error is given by

| (38) |

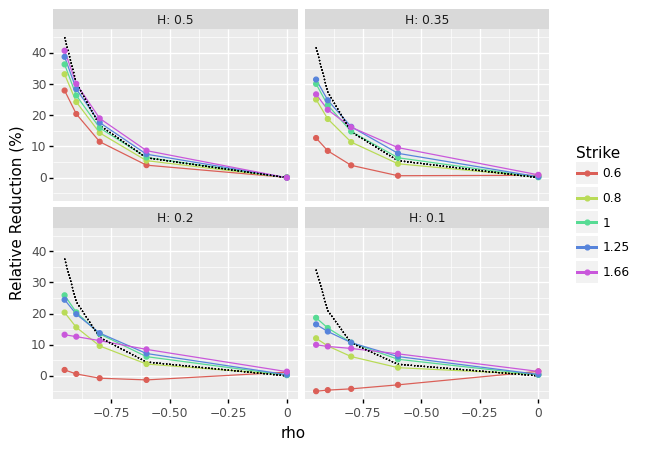

and is increasing in . We conclude that the effectiveness of variance-optimal hedging, relative to Delta hedging, is largest in the SABR case and smallest in very rough models with close to zero. A plot of in dependency of and for different is shown in Figure 1. While the effect of is visible, the influence of dominates, and is qualitatively similar for all . The boundary case can also be simplified; for the relative error reduction evaluates to

compare with (27). A half-way reduction of the root-mean-squared error in the case , is achieved only at .

5 Numerical Results

5.1 Method

To verify our results by simulation, we have implemented the SABR model and the calculation of the variance-optimal strategies in Python. For the simulation of the rough Bergomi model, we use the turbocharged Monte-Carlo scheme of [MP18], publicly available at http://https://github.com/ryanmccrickerd/rough_bergomi. As parameters for the SABR/rough Bergomi model we use

and a flat term structure of initial forward variance is assumed in the rough Bergomi case. The parameters and are varied over a grid of

We have also explored positive values of , with results that are similar (up to symmetry) to the results for negative and therefore not reported here. For the call options we use a time-to-maturity of one year and set today’s stock price to . The strike price is varied over a grid of

For each parameter combination we simulate paths on a time grid of steps. We evaluate the pathwise hedging error for both the variance-optimal and the Delta strategy and then calculate all relevant summary statistics, such as the mean-square hedging error or the relative error reduction.

5.2 Observations

We first focus on the empirical reduction in hedging error, which is shown in Figure 2, together with the first-order approximation (38). For the SABR model () and for the rough Bergomi model with large , the first-order approximation matches well with the empirically observed error reduction. For smaller , the approximation and the empirical error start to diverge, in particular for

ITM options. Overall, the approximate variance-optimal hedge consistently leads to a reduction of the hedging error (in comparison to the Delta hedge), in particular for models with large and not too close to . This is in line with our theoretical results from Sections 3 and 4. Only for and for far ITM options a slightly negative reduction (i.e. an increase) of the empirical hedging error can be observed.

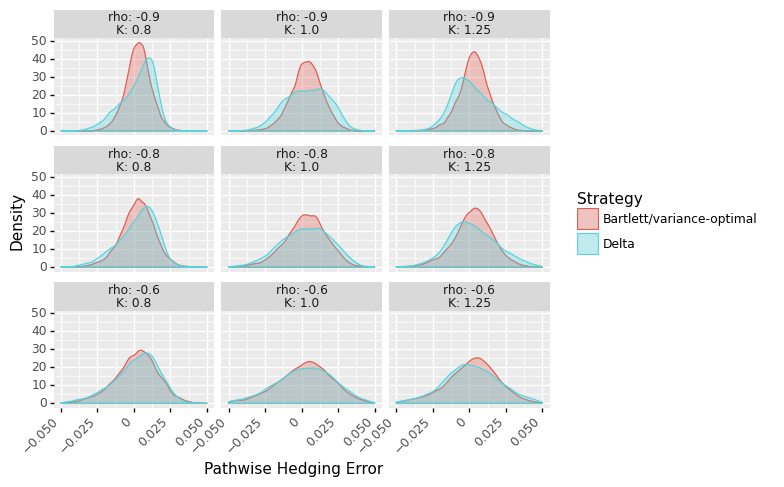

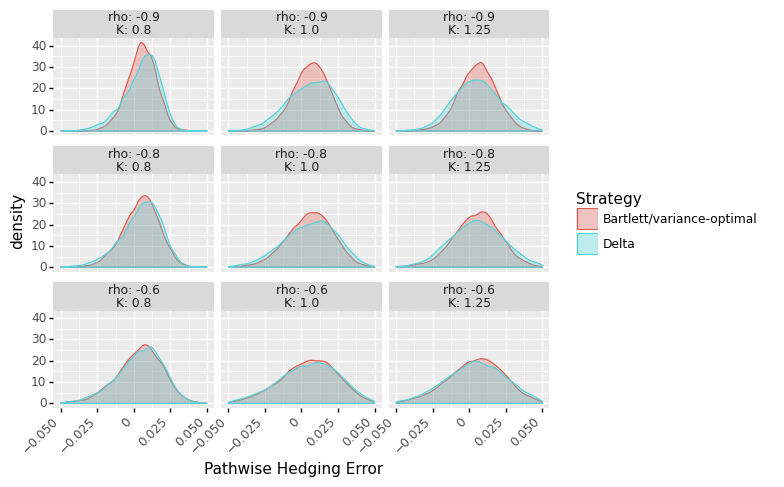

An even more detailed picture is painted by Figures 3 and 4, where we show estimated densities of the empirical pathwise hedging error for different combinations of and . In particular for large it can be seen that the density of the variance-optimal strategies’ error is narrower, more symmetric, and lighter-tailed then the density of the Delta strategies’ error. The density of the Delta strategy error exhibits a skew that varies with strike and has heavier and asymmetric tails. However, already for the moderate values of the effect is much diminished, in line with the theoretical results of Sections 3 and 4, see also Figure 1. Comparing Figures 3 and 4 it can also be seen that the described differences are more pronounces in the (non-rough) SABR case than in the rough Bergomi case with . Again, this observation confirms our theoretical results.

6 Conclusions

In this article, we have derived analytic expressions for the variance-optimal hedging strategy and its mean-square error in the lognormal SABR and in the rough Bergomi model. For the SABR model, we find that the variance-optimal strategy coincides with Bartlett’s Delta strategy from [Bar06]. Both theoretical results and simulations show that the variance-optimal strategy has lower hedging error than the implied Delta strategy, but this advantage only becomes substantial for strongly correlated models with large . The relative efficiency of variance-optimal hedging is also affected by the roughness parameter , with smaller (that is, increasing roughness) diminishing the advantage over the simple Delta hedge.

The general results of Section 2 on variance-optimal hedging in the ‘dynamic implied-volatilty’ setting can likely be applied to other models beyond the lognormal SABR/rough Bergomi model, whenever a tractable expression for the evolution of implied volatility is available. In particular, in future work, we aim to generalize results to the SABR/rough Bergomi model with variable , shedding further light on the stability of Bartlett’s Delta with respect to variations in , as discussed in [HL17].

References

- [Bal06] Philippe Balland. Forward smile. Presentation at Global Derivatives, 2006.

- [Bar06] Bruce Bartlett. Hedging under SABR model. Wilmott magazine, 4(06):2–4, 2006.

- [Ber08] L. Bergomi. Smile dynamics III. Risk 21, 21:90–96, 2008.

- [BFG16] Christian Bayer, Peter Friz, and Jim Gatheral. Pricing under rough volatility. Quantitative Finance, 16(6):887–904, 2016.

- [Cré04] Stéphane Crépey. Delta-hedging vega risk? Quantitative Finance, 4(5):559–579, 2004.

- [FG22] Masaaki Fukasawa and Jim Gatheral. A rough SABR formula. Frontiers of Mathematical Finance, 1(1):81, 2022.

- [FS88] Hans Föllmer and Martin Schweizer. Hedging by sequential regression: An introduction to the mathematics of option trading. ASTIN Bulletin: The Journal of the IAA, 18(2):147–160, 1988.

- [GJR18] Jim Gatheral, Thibault Jaisson, and Mathieu Rosenbaum. Volatility is rough. Quantitative finance, 18(6):933–949, 2018.

- [HKLW02] P Hagan, D Kumar, A Lesniewski, and D Woodward. Managing smile risk. Wilmott magazine, pages 84–108, 2002.

- [HL17] Patrick S Hagan and Andrew Lesniewski. Bartlett’s delta in the SABR model. arXiv:1704.03110, 2017.

- [HW17] John Hull and Alan White. Optimal delta hedging for options. Journal of Banking & Finance, 82:180–190, 2017.

- [JS13] Jean Jacod and Albert Shiryaev. Limit theorems for stochastic processes, volume 288. Springer Science & Business Media, 2013.

- [KW67] Hiroshi Kunita and Shinzo Watanabe. On square integrable martingales. Nagoya Mathematical Journal, 30:209–245, 1967.

- [MP18] Ryan McCrickerd and Mikko S Pakkanen. Turbocharging Monte Carlo pricing for the rough Bergomi model. Quantitative Finance, 18(11):1877–1886, 2018.

- [Sch84] Martin Schweizer. Varianten der Black-Scholes-Formel. Master’s thesis, ETH Zurich, 1984.

- [Sch92] Martin Schweizer. Mean-variance hedging for general claims. The Annals of Applied Probability, pages 171–179, 1992.