[2]\fnmQingna\surLi

1]\orgdivSchool of Mathematics and Statistics, \orgnameBeijing Institute of Technology, \orgaddress\streetNo. 5 Zhongguancun South Street, Haidian District, \cityBeijing, \postcode100081, \countryChina

[2]\orgdivSchool of Mathematics and Statistics/ Beijing Key Laboratory on MCAACI/ Key Laboratory of Mathematical Theory and Computation in Information Security, \orgnameBeijing Institute of Technology, \orgaddress\streetNo. 5 Zhongguancun South Street, Haidian District, \cityBeijing, \postcode100081, \countryChina

A Highly Efficient Adaptive-Sieving-Based Algorithm for the High-Dimensional Rank Lasso Problem

Abstract

The high-dimensional rank lasso (hdr lasso) model is an efficient approach to deal with high-dimensional data analysis. It was proposed as a tuning-free robust approach for the high-dimensional regression and was demonstrated to enjoy several statistical advantages over other approaches. The hdr lasso problem is essentially an -regularized optimization problem whose loss function is Jaeckel’s dispersion function with Wilcoxon scores. Due to the nondifferentiability of the above loss function, many classical algorithms for lasso-type problems are unable to solve this model. In this paper, inspired by the adaptive sieving strategy for the exclusive lasso problem [1], we propose an adaptive-sieving-based algorithm to solve the hdr lasso problem. The proposed algorithm makes full use of the sparsity of the solution. In each iteration, a subproblem with the same form as the original model is solved, but in a much smaller size. We apply the proximal point algorithm to solve the subproblem, which fully takes advantage of the two nonsmooth terms. Extensive numerical results demonstrate that the proposed algorithm (AS-PPA) is robust for different types of noises, which verifies the attractive statistical property as shown in [2]. Moreover, AS-PPA is also highly efficient, especially for the case of high-dimensional features, compared with other methods.

keywords:

Adaptive sieving, proximal point algorithm, semismooth Newton’s based augmented Lagrangian method, high-dimensional rank lassopacs:

[MSC Classification]90C06, 90C25

1 Introduction

In this paper, we will design a highly efficient and robust algorithm for solving the convex composite optimization problems including the following high-dimensional rank lasso (hdr lasso) problem

| (1) |

where is a nonsmooth convex function, is a linear map whose adjoint is denoted as , and is a given data. Here and are two finite real dimensional Euclidean spaces, equipped with standard inner product and is the norm.

With the development of information technology and artificial intelligence, people face great challenges in data analysis due to the high dimensional features and the large scale of datasets. In the low-dimensional case, where the number of features is less than the number of samples, i.e. (), the rank lasso problem was investigated by Wang and Li in 2009 [3], where in (1) is given by

| (2) |

and are given data defined by

That is,

| (3) |

The rank lasso model (3) basically replaces the quadratic loss function in the traditional lasso model by the loss function as defined in (2). Minimizng the loss function in (2) is equivalent to minimizing Jaeckel’s dispersion function with Wilcoxon scores:

where denotes the rank of among . Therefore, (3) is referred to as the rank lasso model. The advantages of such rank-based methods include “better power, efficiency at heavy-tailed distributions and robustness against various model violations and pathological data” [4, Page xv]. It is well-known that heavy-tailed distribution is ubiquitous in modern statistical analysis and machine learning problems, and may be caused by chance of extreme events or by the complex data generating process [5]. Heavy-tailed errors usually arise in climate data, insurance claim data, e-commerce data and many other scenarios [2]. The traditional lasso model, though well-studied and popular used, has difficulty in dealing with heavy-tailed noises. In contrast, the hdr lasso model proposed by Wang et al. [2] deals with the data where the number of features is much larger than the number of samples and it can adapt to a variety of errors, including heavy-tailed errors. Besides the above excellent property, the hdr lasso model also enjoys the following attractive property. A tuning-free parameter was derived in [2], based on which, one does not need to solve a sequence of hdr lasso models with different ’s. Fan et al. [6] evaluated the tuning-free parameter in [2] is more interpretable, easier to select, and is independent of noise variance.

Due to the importance of problem (1), a natural question from the numerical point of view is how to solve it efficiently, particularly in the scenario of the hdr lasso problem. To address this issue, below we will briefly review the existing methods for the lasso and rank lasso problems, respectively, then we will review the recent sieving strategies for these problems.

In terms of the lasso problem, many traditional algorithms are developed, such as the least angle regression (LARS) method [7], the pathwise coordinate descent method [8, 9, 10, 11]. Since the proximal mapping of the norm is easy to calculate, algorithms such as fast iterative shrinkage-thresholding algorithm (FISTA) [12] and alternating direction method of multipliers (ADMM) [13] can also be applied to solve the lasso problem. Recently, Li et al. proposed the semismooth Newton augmented Lagrangian (Ssnal) [14] method and fully exploited the second order sparsity of the problem through the semismooth Newton’s method. Moreover, Ssnal can deal with a lasso-type of models where the loss function is smooth and convex.

For the low-dimensional rank lasso (ldr-lasso) problem, Wang and Li [3] combined the two parts of functions into an norm of a vector in the dimension of , which is then solved by transforming to the least absolute deviation (LAD) problem. Similarly, in [15], Kim et al. also transformed into LAD to deal with the low-dimensional datasets for and , which can be solved by Barrodale-Roberts modified simplex algorithm [16]. In [17], Zoubir et al. used iterative reweighted least squares (IRWLS) to solve the rank-lasso problem. IRWLS essentially approximates the norm by a sequence of the weighted regularized problems. Another way to deal with the rank lasso problem is to reformulated it as a linear programming problem, which may lead to the large scale of problems when dealing with the high-dimensional case. To summarize, the above recent efforts have been devoted to dealing with small scale cases, i.e., the ldr-lasso problem. In terms of solving the hdr lasso problem, very recently, Tang et al. [18] applied a proximal-proximal majorization-minimization algorithm. It can be seen from the numerical results that this method can efficiently solve the hdr lasso problem.

Taking the sparsity of solutions into account, there are many literatures trying to use sieving strategies to solve the lasso problems. Ghaoui et al. [19] proposed a strategy (referred to as the safe screening rule) in 2010 to eliminate features that are guaranteed not to exist after solving the learning problem. Tibshirani et al. [20] proposed the so-called strong rules that are very simple and yet screened out far more predictors than the safe rules in [19]. As explained in [20], the cost of this improvement is the possibility of mistakenly discarding active predictors. In 2014, Bonnefoy et al. [21] proposed a dynamic safe rule which speeds up many optimization algorithms by reducing the size of the dictionary during iterations, discarding elements that are not part of the lasso solution. Wang et al. [22] proposed an efficient and effective screening rule via dual polytope projections (DPP), which is mainly based on the uniqueness and nonexpansive-ness of the optimal dual solution due to the fact that the feasible set in the dual space is a convex and closed polytope. In [23], Fercoq et al. leveraged the computations of duality gaps to propose a simple strategy unifying both the safe rule [19] and the dynamic safe rules [21].

To summarize, all the above sieving algorithms aim at solving the lasso problem, and filter active variables through dual problems or dual gaps. In [1], an adaptive sieving strategy was proposed to solve the exclusive lasso problem where the regularizer is replaced by the weighted exclusive lasso regularizer. Different from the safe rules as in [20, 22, 19], the adaptive sieving strategy in [1] starts with a few nonzero components and gradually adds more nonzero components by checking the KKT conditions of the exclusive lasso problem. Very recently, based on the dual problem of (1), Shang et al. [24] applied the dual circumscribed sphere technique to build up a safe feature screening rule for the rank lasso problem in the scenario that the number of features is much larger than the number of samples . Numerical results in [24] indicate that this screening method can shorten the time by about half. In [25], Yuan et al. generalized the results of [1] to apply this adaptive sieving strategy to the case where is sparse.

To summarize, based on the above analysis, to solve (1) in the high-dimensional case, the efficient Ssnal proposed in [14] can not be applied since in (1) is nonsmooth. Meanwhile, the above sieving strategies mentioned in [19, 20, 22, 23, 1] can not be applied to the rank lasso problem directly. Therefore, a natural question is whether one can design a sieving strategy and proposes an efficient algorithm to solve the hdr lasso problem in (1). This motivates the work in this paper.

In this paper, inspired by [1], we design an adaptive sieving (AS) strategy for (1). Here we would like to highlight that for the lasso problem, there is only one nondifferentiable term (which is the norm term). It leads to only one block of constraints in the dual problem, and the variables can be screened by checking whether such block of constraint is satisfied. However, for the rank lasso problem, it contains two nondifferentiable terms. The corresponding dual problem has two blocks of constraints. Due to the above observations, there are two challenges to design the AS strategy for (1). One is the nondifferentiablity of the loss function in (1), which brings difficulty in extending the AS strategy in [1] to solving (1). The second challenge is how to solve the resulting subproblem efficiently. We tackle the first challenge by introducing an extra variable to decouple the problem. By doing this, a new efficient sieving criterion is developed. For the second challenge, we apply the proximal point algorithm (PPA) to solving the subproblem.

The contributions of the paper are mainly in three aspects. Firstly, we propose an AS strategy to reduce the scale of the hdr lasso problem, based on checking the KKT conditions of the problem. We also prove the convergence of the AS algorithm. Secondly, taking into account of the nonsmoothness of the loss function and the regularizer in the hdr lasso problem, we apply PPA for solving the subproblem. Finally, for each subproblem of PPA, we use the semismooth Newton’s based augmented Lagrangian method. Numerical results demonstrate that the proposed adaptive sieving strategy is very efficient in reducing the scale of the hdr lasso problem and the resulting AS-PPA significantly outperforms other methods.

The organization of the paper is as follows. In Sect. 2, we propose our AS strategy and prove the convergence. In Sect. 3, we propose PPA to solve the subproblems in AS and illustrate the convergence of PPA. In Sect. 4, we use the augmented Lagrange method (ALM) to solve each subproblem in PPA. In Sect. 5, we apply the semismooth Newton’s method (SSN) to solve the subproblems in ALM. Numerical results on different datasets are presented in Sect. 6, which verify the efficiency of our proposed AS-PPA for the hdr lasso problem. Final conclusions are given in Sect. 7.

Notations: Denote as the infinity norm unit ball. For , , where denotes the sign function of . Denote as the diagonal matrix whose diagonal elements are given by vector . We use as the block diagonal matrix whose -th diagonal block is the matrix , . represents the matrix formed by the corresponding columns of with as the index set. Denote the identity matrix of order by . Similarly, and denote the zero matrix and the matrix of all ones, respectively. We use to denote the Euclidean distance of to a set . That is, .

2 Adaptive Sieving Strategy (AS) for (1) and Its Convergence

In this section, we will propose an adaptive sieving (AS) strategy to solve (1) and discuss the convergence of AS.

2.1 AS Strategy for (1)

Due to the norm in (1), the optimal solution of (1) enjoys the sparsity property. However, different from the exclusive lasso problem that is considered in [1], the function in (1) is not differentiable. Moreover, there is a composition as the variable of rather than . Consequently, compared with the adaptive sieving strategy in [1], in order to design an adaptive sieving strategy for (1), we face the following challenges: how to deal with the composition in and how to deal with the nondifferentiability of . We leave the second challenge to the subproblem in Section 3, where the proximal point method is applied to deal with the nondifferentiability of .

To tackle the first challenge, we will introduce a new variable to decouple the problem. Let be defined by . We have the equivalent form of (1) as follows

| (4) |

To derive our AS strategy, we need the KKT conditions of (4). The Lagrangian function of (4) can be written as

| (5) |

where is the Lagrange multiplier corresponding to the equality constraints in (4). The KKT conditions of (4) are given as follows

| (6) |

Define the following two sets: Define the residual function as follows

Therefore, (6) is equivalent to

The idea of our AS strategy is as follows. In each iteration , let be the set of indices corresponding to the nonzero elements in . To estimate the set of indices in next iteration, we check whether the KKT conditions in (6) are satisfied approximately. That is,

| (7) |

where is a prescribed parameter. If (7) fails, we select the following indices based on the violation of KKT conditions:

Here, . The set of nonzero elements in next iteration is given by

The details of our AS strategy is summarized as below.

Input:

, tolerance .

Initialization:

Choose a fast algorithm to find an approximate solution to problem (1).

S0: Let Solve

where , , are error vectors such that , . Set .

S1: Create by

where . Let .

S2: Solve the following problem:

| (8) |

where are error vectors such that , .

S3: Let .

S4: If , stop; otherwise, , go to S1.

2.2 Convergence of Algorithm 1

In Algorithm 1, we check the violation of KKT conditions by , and gradually add the elements in to . As long as the required accuracy is not achieved, the set is not empty. This is demonstrated in the following theorem.

Theorem 1.

If the residual function does not satisfy (7), the set is not empty.

Proof.

For contradiction, assume that . There is

Then there exists , such that and . So we can get

| (9) |

which means

| (10) |

Remark 1.

Remark 2.

Our AS strategy is different from that in [25]. Firstly, in [25], Yuan et al. exploit the sparsity of , based on which, the AS strategy is designed. However, for problem (1), we have the sparsity of . The term in does not enjoy the sparsity property, but brings challenge in designing AS strategy. Secondly, we have one extra nonsmooth term in (1) whereas in [25], there is only one nonsmooth term.

3 Proximal Point Algorithm for Subproblem

In order to make full use of the AS strategy, we must design an efficient method to solve subproblem (8), which is the second challenge of designing an efficient sieving algorithm for (1). We will address this challenge in this section. Comparing problem (1) with subproblem (8), the differences lie in the dimension of and the corresponding coefficient matrix . That is, subproblem (8) can be regarded as solving problem (1) in a subspace indexed by . Therefore, we consider how to solve problem (1) instead.

Since the two terms in (1) are both nonsmooth, we apply PPA [26] to solve it. For any starting point , PPA generates a sequence by solving following problem [26]:

| (13) |

Here is a sequence of positive real numbers such that . Now, we present PPA in Algorithm 2.

Input:

.

Initialization: choose

S1: Find an approximate solution of (13), denoted as .

S2: If the stopping criteria of PPA are satisfied, stop; otherwise, go to S3.

S3: Update

In practice, it is difficult to directly check the stopping criteria (A) and (B). We replace them with the following criteria, which are analogous to those proposed in [26]:

where

According to the above definition of and its properties, we can get the convergence result in [26].

Theorem 2.

Let be an infinite sequence generated by Algorithm 2 under stopping criterion (A)(or (A’)) for solving (1), and is a proper convex function. The sequence converges to a solution of (1). Furthermore, if the criterion (B)(or (B’)) is also executed in Algorithm 2, there exists such that for all , there is

| (14) |

where the convergence rate is given by

Proof.

In order to obtain similar convergence results as in [26], we only need to verify three conditions: (i) the defined operator is maximal monotone; (ii) is bounded; (iii) satisfies the error bound condition at the zero point.

Notice that is the subdifferential of defined in (5), and is a continuous proper convex function. Therefore, is maximal monotone [27, Theorem A].

According to the convexity of the hdr lasso problem, we know that there is at least one solution and the corresponding and satisfy . Together with stopping criterion (A) and is maximal monotone, so the sequence is bounded [26].

By [28, Proposition 2.2.4], we know that is a polyhedral multivalued function. Therefore, the error bound condition holds at the origin with modulus [29]. That is, such that , there is

Then we can get converges to a solution of (1) by [26, Theorem 1]. If the criterion (B)(or (B’)) is also executed, the rate of convergence in (14) is established by [26, Theorem 2], the theorem is proved. ∎

4 ALM for (13)

In this part, we present ALM for (13) and discuss its convergence. Note that what we need to consider now is how to efficiently solve subproblem (13) in PPA at each iteration . By introducing , we solve the following equivalent form of (13):

| (15) |

Note that there are only equality constraints in (15). A natural choice to solve (15) is the augmented Lagrangian method. The augmented Lagrangian function of (13) is given as follows

where , and . Here are the Lagrangian multipliers corresponding to the two types of equality constraints in (15).

At -th iteration, the augmented Lagrangian method generates in the following way :

| (16a) | |||||

| (16b) |

The key point is how to solve (16a). Note that is a function of three variables . It is difficult to find the minimum value of the function with respect to the three variables simultaneously. Notice that there is no coupling term between and , and they are only related to respectively. Another fact is that with fixed, one can have closed form solutions for and respectively, by using the property of Moreau-Yosida regularization. Therefore, we first represent and by through the Moreau-Yosida regularization, denoted by , respectively. Then we solve the resulting minimization problem with respect to , that is, .

Firstly, we introduce the properties of Moreau-Yosida regularization. For any given proper closed convex function , the Moreau-Yosida regularization of is defined by

| (17) |

The proximal mapping associated with is the unique minimizer of (17) denoted by . is Lipschitz continuous with modulus 1 [30]. Moreover, is a continuously differentiable convex function [31], and its gradient is given by

Next, we show how to use Moreau-Yosida regularization to derive and . Denote and . There is

| (18) |

where is defined as in (17). The optimal solution to (18) is . Similarly, for , there is

| (19) |

where the unique minimizer of (19) is . Then, we have

Input:

Initialization:

choose , set .

S1: Solve

| (20) |

S2: Calculate

S3: If the stopping criteria are satisfied, stop; otherwise, go to S4.

S4: Update by (16b);

We will use the following stopping criteria considered by Rockafellar [26], [32] for terminating Algorithm 3:

The global convergence result of ALM has been extensively studied in [26, 32, 33, 14]. ALM is applied to solve a general form of (13), i.e., problem (D) in [14]. The convergence result is obtained therein. Therefore, as a special case of problem (D) in [14], we can get the following global convergence of Algorithm 3.

Theorem 3.

Let be the infinite sequence generated by Algorithm 3 with stopping criterion (C). The dual problem of (13) is as follows

| (21) |

where , and are the conjugate functions of and . Then, the sequence is bounded and converges to an optimal solution of (21). In addition, is also bounded and converges to the unique optimal solution of (13).

To state the local convergence rate, we need the following stopping criteria which are popular used such as in [34] and [14]:

Define the Lagrangian function of (15) as

Correspondingly, define the maximal monotone operator and by

| (22) |

By [28, Proposition 2.2.4], we know that the corresponding operator defined in (22) is a polyhedral multivalued function. Therefore, by [35, Proposition 3.8], the error bound condition holds at the origin with modulus . Similarly, defined in (22) also satisfies the error bound condition at the origin with modulus . We can get the following theorem.

Theorem 4.

Let be the infinite sequence generated by ALM with stopping criteria (D1) and (D2). The following results hold.

-

If the stopping criterion (D2) is also used, then for all sufficiently large, there is

where as .

Proof.

The proof is similar to that in [14, Theorem 3.3]. By definition 2.2.1 in [28], (21) is a convex piecewise linear quadratic programming problem. According to the optimal solution set is not empty, , so is metrically subregular at for the origin. Following Theorem 3.3 in [14], (i), (ii) holds. The proof is finished. ∎

5 The SSN Method for (20)

To solve (20), since is strongly convex and continuously differentiable, the minimization problem (20) has a unique solution which can be obtained via solving the following system of equation:

| (23) |

where

We know that and are strongly semismooth everywhere as special cases in [36, Theorem 2]. Therefore, we apply the SSN method to solve the nonsmooth equation (23).

A key point is to characterize the generalized Jacobian of . To that end, define the multivalued mapping as follows: at ,

where is a multivalued mapping defined in the following Proposition 6, which can be viewed as the generalized Jacobian of [37, Proposition 2.9], is the Clarke’s subdifferential of .

According to the chain rules in [38], there is where is the Clarke’s generalized Jacobian of .

Now we are ready to present the globalized version of SSN method for (20) which is used in [39, 40, 41, 42].

Input:

, , , and .

Initialization:

choose

S1: Select an element . Apply the conjugate gradient (CG)

method to find an approximate solution of the following system

such that

where .

S2: Let , where is the smallest nonnegative integer such that the following holds

S3: Let

S4: If , stop; otherwise, , go to S1.

To demonstrate the convergence of Algorithm 4, we need the characterization of and . It is easy to show that

The following results about come from [37].

Proposition 5.

[37, Proposition 2.3] Given , there exists a permutation matrix such that , and . Then it holds

where the vector is defined by , , and is a matrix such that . is the optimal solution of

| (24) |

Define , denote the active index set by

| (25) |

where is the -th row of . Define a collection of index subsets of as follows: , where supp() denotes the support of , is the matrix consisting of the rows of indexed by , and . Let is a diagonal matrix, where

| (26) |

Proposition 6.

To guarantee the quadratic convergence rate of the SSN method, one need to verify that each element in is positive definite. Below we confirm the result in Lemma 1 with the proof postponed in Appendix.

Lemma 1.

Any is symmetric and positive definite.

Based on Lemma 1, the convergence rate of the SSN method is given below.

Theorem 7.

Proof.

According the strong convexity of , we have

Therefore, the stopping criteria (C), (D1) and (D2) can be simplified to

That is, the stopping criteria (C), (D1), and (D2) will be satisfied as long as is sufficiently small.

6 Numerical Results

In this section, we conduct numerical experiments to evaluate the performance of AS-PPA for solving (1). It contains four parts. In the first part, we provide the test problems and the implementation of the algorithm. In the second part, we investigate the performance of Algorithm 1 based on different parameters. In the third and fourth parts, we compare Algorithm 1 with other methods for small scale and large scale of test problems. All of our results are obtained by running Matlab R2020a on a windows workstation (Intel Core i5-7200U @ 2.50GHz, 12G RAM).

6.1 Test Problems

We test the following examples.

-

E1

[2] We simulate random data from the regression model , where is generated from a -dimensional multivariate normal distribution and is independent of , . The correlation matrix has a compound symmetry structure: for ; and for . We consider six different distributions for : (i) normal distribution with mean 0 and variance 0.25 (denoted by ); (ii) normal distribution with mean 0 and variance 1 (denoted by ); (iii) normal distribution with mean 0 and variance 2 (denoted by ); (iv) mixture normal distribution (denoted by ); (v), where denotes the distribution with 4 degree of freedom; and (vi) Cauchy(0,1), where Cauchy(0,1) denotes the standard Cauchy distribution.

-

E2

[2] Similar as in E1, we take , where is a -dimensional vector of zeros. Comparing with E1, this is a considerably more challenging scenario with 25 active variables and a number of weak signals, such as 0.5, 0.25, etc.

-

E3

[2] is the same as in E1. We use the following three different choices of : (i) the compound symmetry correlated correlation matrix with correlation coefficient , denoted as ; (ii) the compound symmetry correlation matrix with correlation coefficient , denoted as ; and (iii) the compound symmetry correlation matrix with correlation coefficient , denoted as . For each choice of , we consider three different error distributions: , the mixture normal distribution in E1, and the Cauchy distribution in E1.

-

E4

[24] The simulation data is generated from with and . Here, elements of are randomly generated from the exponential distribution and the error . The number of nonzero coefficients of is , and the nonzero part of is generated from the standard normal distribution.

-

E5

[44] is generated from a -dimensional multivariate normal distribution . The correlation matrix is the Toeplitz correlation matrix, i.e., , .

-

E6

[44] Similar as in E5, we take .

We choose following the way in [2, Theorem 1]111 , where , and denotes the -quantile of the distribution of , , is the design matrix, the random vector , with following the uniform distribution on the permutations of the integers .. The parameters are taken as , .

Taking into account of numerical rounding errors, we define the number of nonzero elements of a vector and the index set of nonzero components of as follows (see [18, Page 17])

where is sorted, i.e., . Let .

We report the following information: the relative KKT residual () calculated by

the function value of (1) (val); the estimation error ; the estimation error ; the model error ME where is the population covariance matrix of ; the number of false positive variables FP; the number of false negative variables FN; the correct component ratio CR, where is the solution of the original problem by taking ; the running time in second (). Moreover, we additionally report the number of iterations in Algorithm 1 (It-AS), the total number of iterations in Algorithm 2 (It-PPA), the total number of iterations in Algorithm 3 (It-ALM), the total number of iterations in Algorithm 4 (It-SSN) and the total time of SSN ().

6.2 Role of Parameters

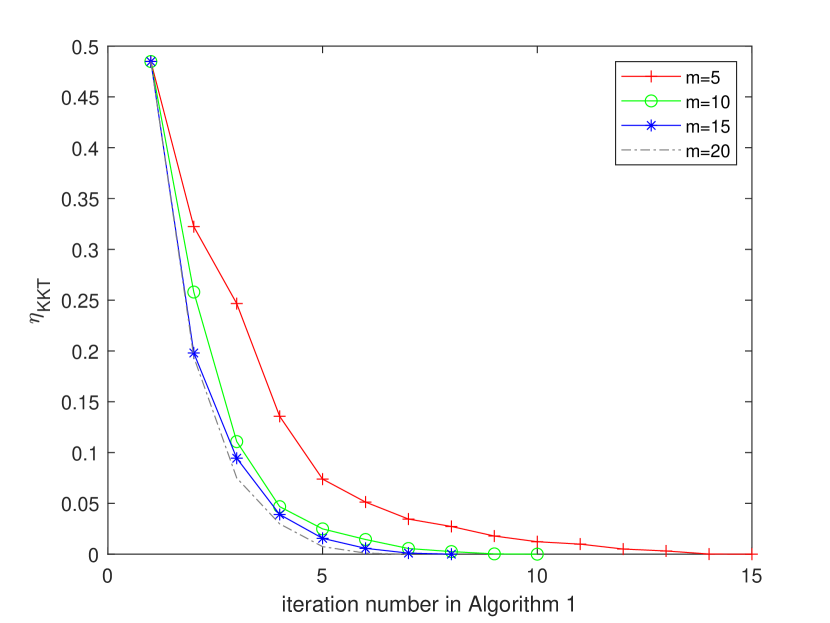

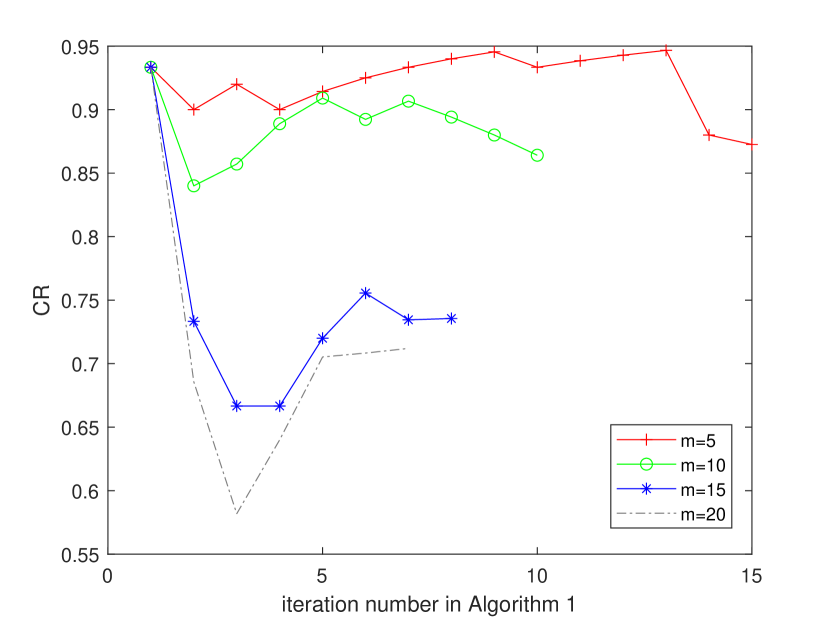

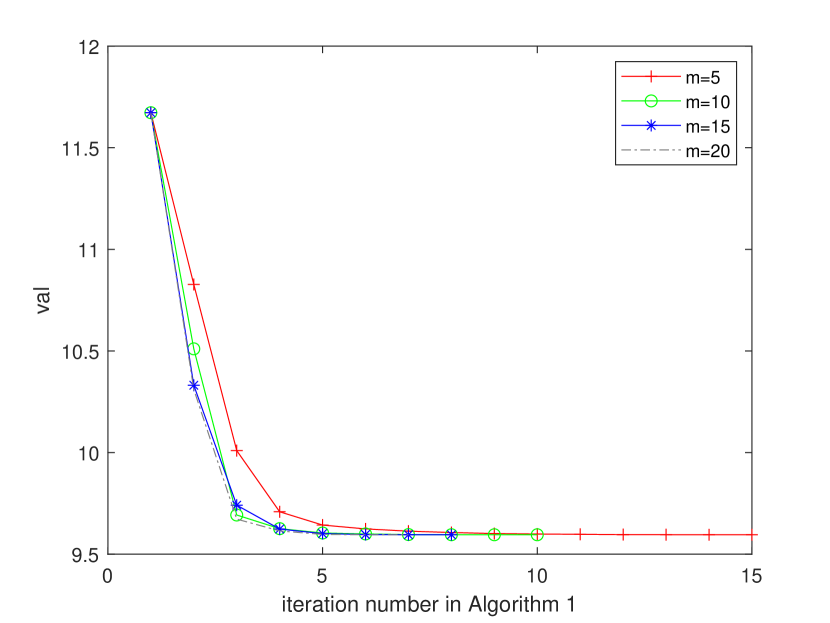

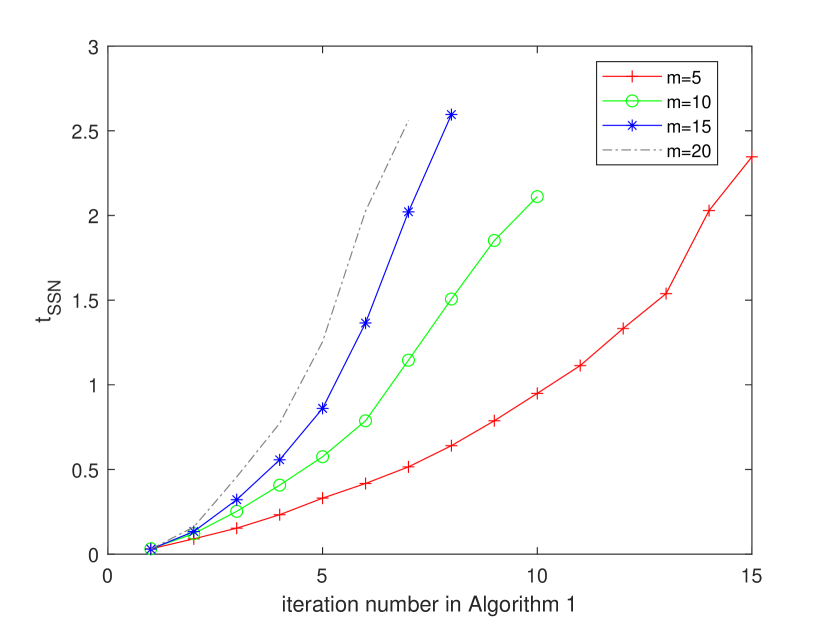

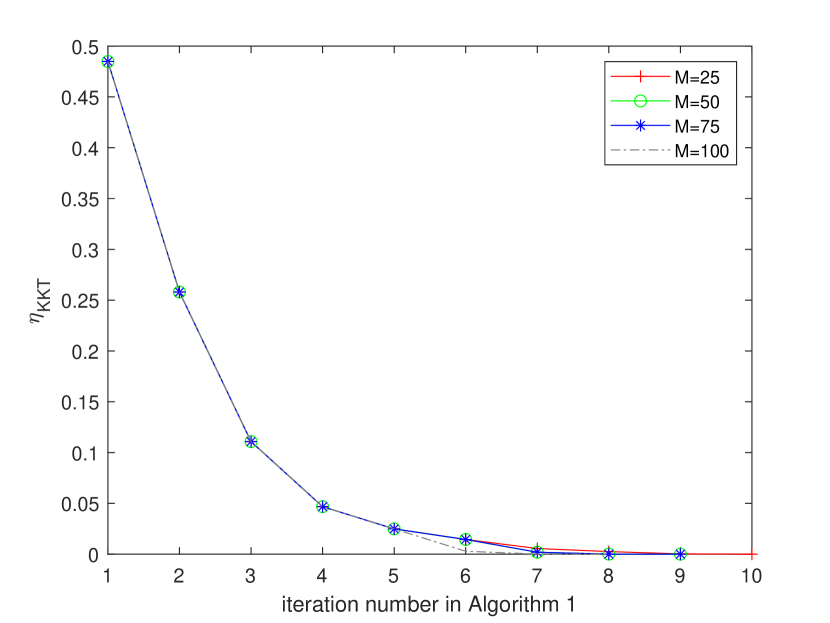

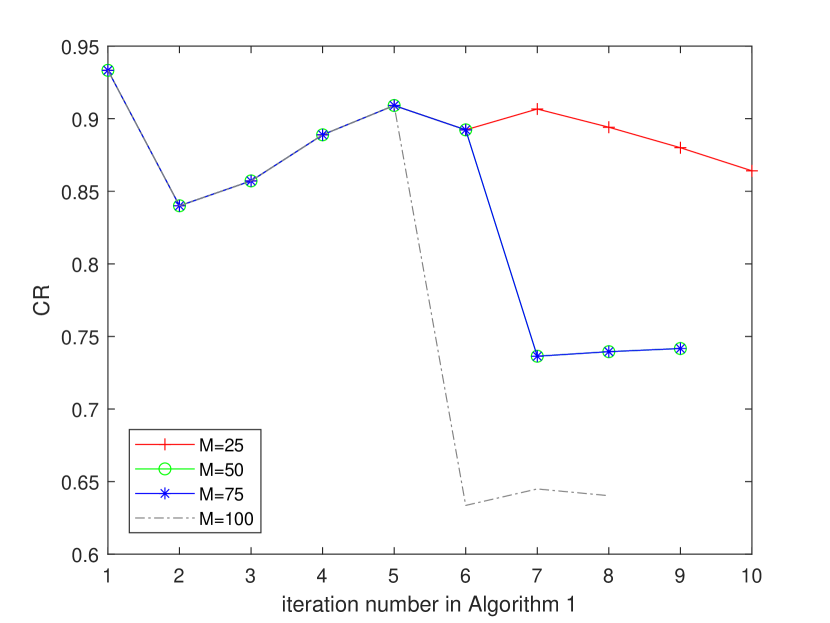

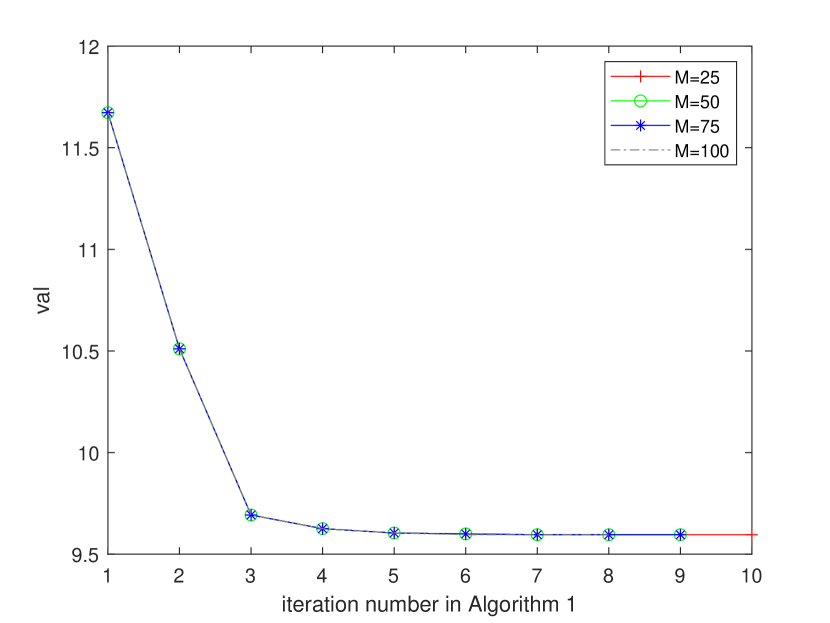

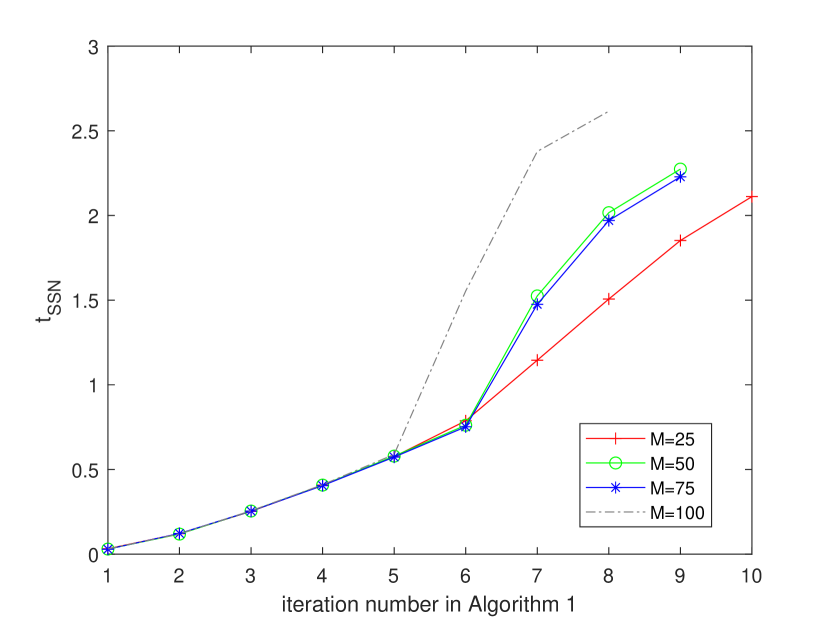

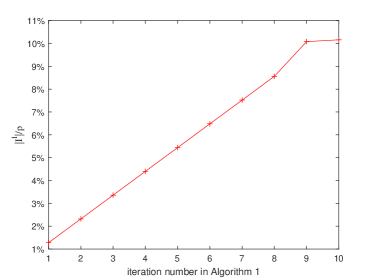

The number of components added to . In Algorithm 1, the number of components we choose to add to in each iteration may affect the performance of the algorithm. We first fix the maximum number of added components (denoted as ) as 25, that is, if the sieved components are less than or equal to 25, then all are added. We use to represent the number of components added to each time. We conduct experiments on E2 with of (i) for , that is, . The results are shown in Figure 1 and Table 1. We can see from Figure 1 that with the iteration of AS, new components are gradually added to , and the relative KKT residuals are getting smaller and smaller. Furthermore, gradually covers . For the different numbers of components added each time, the relative KKT residuals decline differently. Obviously, the larger is, the faster the decline is. For the comparison of CR, we can see that the smaller is, the higher the CR will be. From , we can see that grows in the slowest way if takes the smallest value. However, because the number of AS iterations increases, the overall time of SSN may be longer. The results in Table 1 show the overall performance for the four values of . It can be seen that four choices of lead to similar quality of output whereas leads to the smallest time. Therefore, we choose in our following test.

| ME | FP | FN | It-AS | It-PPA | It-ALM | It-SSN | |||||||

| 5 | 4.8-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.44 | 15 | 246 | 747 | 3477 | 2.35 |

| 10 | 9.9-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.18 | 10 | 188 | 555 | 2835 | 2.11 |

| 15 | 9.4-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.66 | 8 | 186 | 458 | 2887 | 2.60 |

| 20 | 6.9-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.62 | 7 | 130 | 369 | 2682 | 2.56 |

The role of the maximum number that added to (denoted as ). We still test on E2. That is, , and . The results are reported in Figure 2 and Table 2. We can see from Figure 2 that in the first five iterations of AS, the results of the four choices are almost the same. This is because the maximum number of additions is not reached. In this case, only 10 components are added each time, so the results of the four choices of are the same. From iteration , different ’s lead to different CR’s and ’s. Specifically, higher leads to lower residuals as well as lower CR’s, but more cputime in . On the other hand, different values of hardly affect the function value. From Table 2, one can see that is a reasonable choice compared with other choices since it leads to less cputime. Therefore, in our following test, we choose .

| ME | FP | FN | It-AS | It-PPA | It-ALM | It-SSN | |||||||

| 25 | 9.9-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.18 | 10 | 188 | 555 | 2835 | 2.11 |

| 50 | 9.8-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.34 | 9 | 175 | 506 | 2579 | 2.27 |

| 75 | 9.8-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.30 | 9 | 175 | 506 | 2579 | 2.23 |

| 100 | 8.0-7 | 9.60 | 4.42 | 0.68 | 0.15 | 63 | 0 | 2.67 | 8 | 119 | 406 | 2503 | 2.62 |

in the subproblem. Since needs to be smaller than , so here we test different . The results are reported in Table 3. We can see that the quality of the solutions are the same, indicate by the same values in . With the increase of , the numbers of iterations of ALM and PPA are decreasing, but the total numbers of iterations of SSN are equal. As a result for different , the difference of the cputime is very small. Considering the number of iterations of each part and the cputime, we choose to take as .

| It-AS | It-PPA | It-ALM | It-SSN | ||||

|---|---|---|---|---|---|---|---|

| 9.9-7 | 2.33 | 10 | 350 | 717 | 2835 | 2.23 | |

| 9.9-7 | 2.31 | 10 | 350 | 717 | 2835 | 2.22 | |

| 9.9-7 | 2.30 | 10 | 302 | 669 | 2835 | 2.21 | |

| 9.9-7 | 2.32 | 10 | 302 | 669 | 2835 | 2.23 | |

| 9.9-7 | 2.33 | 10 | 280 | 647 | 2835 | 2.24 | |

| 9.9-7 | 2.27 | 10 | 280 | 647 | 2835 | 2.19 | |

| 9.9-7 | 2.49 | 10 | 235 | 602 | 2835 | 2.39 | |

| 9.9-7 | 2.34 | 10 | 211 | 578 | 2835 | 2.25 | |

| 9.9-7 | 2.25 | 10 | 188 | 555 | 2835 | 2.17 |

The initial points in the subproblem. For the initial point in the subproblem, noticed that has been obtained in the last iteration, so we set . For the added index set , we compare four different options . The results for four different initial points are in Table 4. From the results, we can see that there is no big difference between the four initial points in the effect of the solution, for example, , , etc. have basically no difference. In terms of the number of iterations, although the number of ALM iterations of the last initial point selection method is slightly less, the number of internal iterations of SSN is more. For the method of taking 0 as the initial point, the number of internal iterations of SSN is the lightest, and considering the total time of SSN, it will be faster in time. Therefore, we take 0 as the initial points for the following test.

| ME | FP | FN | It-AS | It-PPA | It-ALM | It-SSN | |||||||

| 9.9-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.31 | 10 | 188 | 555 | 2835 | 2.23 | |

| 9.4-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.46 | 10 | 234 | 605 | 2844 | 2.37 | |

| 9.1-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.41 | 10 | 190 | 557 | 2817 | 2.30 | |

| 9.8-7 | 9.60 | 4.42 | 0.68 | 0.15 | 64 | 0 | 2.82 | 10 | 188 | 515 | 3256 | 2.75 |

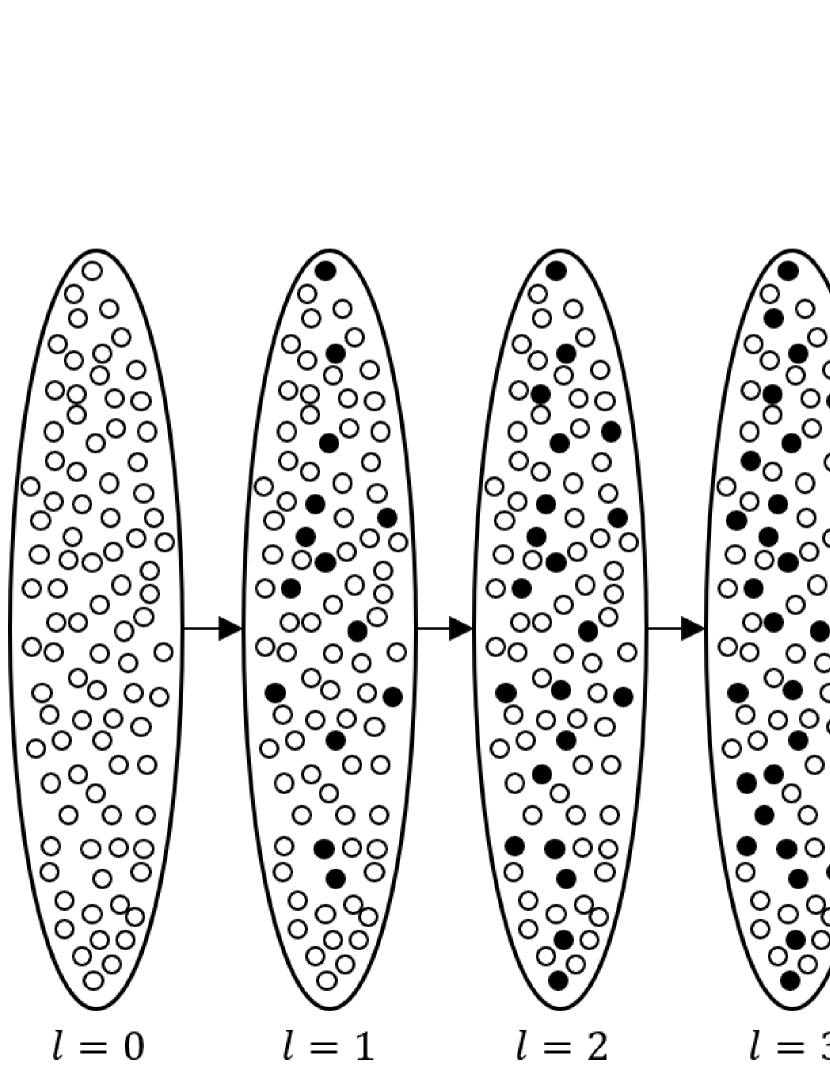

In order to visualize the effect of our sieving strategy, we draw the following diagram for on E2. In this way, we can observe whether the added components gradually cover after each iteration of AS. In Figure 3, the white circles represent the nonzero components of the true solution , and the black circles represent the components selected in each sieving. We can find that as the number of iterations increases, the white circles are gradually covered. This indicates that AS gradually selects the real nonzero components. It verifies that our AS strategy can effectively sieve the components that are not zeros after adding new components each time.

6.3 Comparison with Other Methods

In this part, we compare Algorithm 1 with other methods for (1), including Gurobi for the linear programming formulation of (1), Barrodale-Roberts modified simplex algorithm [16] (BR) for LAD formulation of (1) and the iteratively reweighted least squares (IRWLS). The following linear programming formulation is used to solve (1) [2, Page 1709]:

| (27) |

We use the Gurobi 9.5.1 package111https://www.gurobi.com/ to solve (27)222The ’deterministic concurrent’ method is used in Gurobi.. There are equality constraints, box constraints, inequality constraints, and the dimension of variables is . For LAD, we use the Fortran code in [45]. For IRWLS, we use IRWLS provided in the RobustSP toolbox333https://github.com/RobustSP/toolbox by Zoubir et al. [17].

Table 5 and 6 summarizes the results for small scale of test problems with . All the results are taken average over 50 random runs. From Table 5, we can see that AS-PPA, BP and Gurobi return almost the same solutions due to almost the same function values in , ME, FP and FN. For IRWLS, FN is significantly different from those given by AS-PPA and Gurobi, indicating that the returned solutions by IRWLS may provide extra false negative components. In terms of cputime, both AS-PPA and Gurobi are much faster than IRWLS and BR, whereas AS-PPA is the fastest one. This can be explained by the fact that BR, Gurobi and IRWLS do not explore the sparsity of solutions. Furthermore, the linear programming problem contains 4950 equality constraints, 9900 box constraints, 800 inequality constraints, and variable dimension is 10700. In BR algorithm, the LAD problem is an minimization problem on a 5350-dimensional vector. For our AS-PPA, there are 900 variables and 500 equality constraints. This also explains why AS-PPA is faster than Gurobi and BR.

| Error | Method | val | ME | FP | FN | ||||

| AS-PPA | 2.7125 | 0.77 | 0.34 | 0.08 | 8.4 | 0.0 | 0.1 | ||

| Gurobi | 2.7125 | 0.77 | 0.34 | 0.08 | 8.4 | 0.0 | 4.2 | ||

| IRWLS | 2.7125 | 0.77 | 0.34 | 0.08 | 27.3 | 0.0 | 67.1 | ||

| BR | 2.7125 | 0.77 | 0.34 | 0.08 | 8.4 | 0.0 | 21.5 | ||

| AS-PPA | 3.1889 | 1.53 | 0.68 | 0.32 | 8.5 | 0.0 | 0.1 | ||

| Gurobi | 3.1889 | 1.53 | 0.68 | 0.32 | 8.5 | 0.0 | 4.1 | ||

| IRWLS | 3.1890 | 1.53 | 0.68 | 0.32 | 39.9 | 0.0 | 66.7 | ||

| BR | 3.1889 | 1.53 | 0.68 | 0.32 | 8.5 | 0.0 | 20.6 | ||

| AS-PPA | 3.5836 | 2.17 | 0.97 | 0.65 | 8.5 | 0.0 | 0.1 | ||

| Gurobi | 3.5836 | 2.17 | 0.97 | 0.65 | 8.5 | 0.0 | 4.4 | ||

| IRWLS | 3.5837 | 2.17 | 0.97 | 0.65 | 51.6 | 0.0 | 72.9 | ||

| BR | 3.5836 | 2.17 | 0.97 | 0.65 | 8.5 | 0.0 | 20.1 | ||

| AS-PPA | 3.2537 | 1.64 | 0.74 | 0.38 | 8.2 | 0.0 | 0.1 | ||

| Gurobi | 3.2537 | 1.64 | 0.74 | 0.38 | 8.2 | 0.0 | 4.3 | ||

| IRWLS | 3.2538 | 1.64 | 0.74 | 0.38 | 44.9 | 0.0 | 72.1 | ||

| BR | 3.2537 | 1.64 | 0.74 | 0.38 | 8.2 | 0.0 | 20.4 | ||

| AS-PPA | 4.0392 | 2.62 | 1.17 | 0.95 | 8.6 | 0.0 | 0.1 | ||

| Gurobi | 4.0392 | 2.62 | 1.17 | 0.95 | 8.6 | 0.0 | 4.3 | ||

| IRWLS | 4.0393 | 2.62 | 1.17 | 0.95 | 61.5 | 0.0 | 73.3 | ||

| BR | 4.0392 | 2.62 | 1.17 | 0.95 | 8.6 | 0.0 | 20.3 | ||

| Cauthy | AS-PPA | 14.1917 | 3.44 | 1.53 | 1.84 | 7.5 | 0.1 | 0.2 | |

| Gurobi | 14.1917 | 3.44 | 1.53 | 1.84 | 7.5 | 0.1 | 4.5 | ||

| IRWLS | 14.1918 | 3.44 | 1.53 | 1.84 | 81.7 | 0.0 | 72.5 | ||

| BR | 14.1917 | 3.44 | 1.53 | 1.84 | 7.5 | 0.1 | 18.8 |

| Error | Method | val | ME | FP | FN | ||||

| E2 | |||||||||

| AS-PPA | 12.5636 | 15.79 | 2.49 | 0.60 | 45.4 | 3.2 | 3.1 | ||

| Gurobi | 12.5636 | 15.79 | 2.49 | 0.60 | 45.4 | 3.2 | 5.8 | ||

| IRWLS | 12.5638 | 15.80 | 2.49 | 0.60 | 45.4 | 3.2 | 71.4 | ||

| BR | 12.5636 | 15.79 | 2.49 | 0.60 | 45.4 | 3.2 | 583.9 | ||

| AS-PPA | 12.7503 | 20.87 | 3.33 | 1.43 | 44.5 | 5.1 | 2.8 | ||

| Gurobi | 12.7503 | 20.87 | 3.32 | 1.43 | 44.5 | 5.1 | 5.4 | ||

| IRWLS | 12.7504 | 20.89 | 3.33 | 1.43 | 44.8 | 5.1 | 71.3 | ||

| BR | 12.7503 | 20.87 | 3.32 | 1.43 | 44.5 | 5.1 | 430.6 | ||

| AS-PPA | 12.9379 | 24.09 | 3.86 | 2.33 | 42.8 | 6.4 | 2.6 | ||

| Gurobi | 12.9379 | 24.09 | 3.86 | 2.33 | 42.9 | 6.4 | 5.4 | ||

| IRWLS | 12.9380 | 24.10 | 3.87 | 2.34 | 43.0 | 6.4 | 71.5 | ||

| BR | 12.9379 | 24.09 | 3.86 | 2.33 | 42.9 | 6.4 | 381.4 | ||

| AS-PPA | 12.7426 | 21.51 | 3.41 | 1.62 | 44.6 | 5.4 | 2.8 | ||

| Gurobi | 12.7426 | 21.51 | 3.41 | 1.62 | 44.6 | 5.4 | 5.6 | ||

| IRWLS | 12.7427 | 21.52 | 3.42 | 1.62 | 44.8 | 5.4 | 71.5 | ||

| BR | 12.7426 | 21.51 | 3.41 | 1.62 | 44.6 | 5.4 | 441.1 | ||

| AS-PPA | 13.2316 | 26.61 | 4.31 | 3.40 | 41.1 | 7.8 | 2.3 | ||

| Gurobi | 13.2316 | 26.61 | 4.31 | 3.40 | 41.0 | 7.8 | 5.1 | ||

| IRWLS | 13.2317 | 26.61 | 4.31 | 3.40 | 41.1 | 7.8 | 70.9 | ||

| BR | 13.2316 | 26.61 | 4.31 | 3.40 | 41.0 | 7.8 | 281.8 | ||

| Cauthy | AS-PPA | 22.9788 | 34.29 | 5.66 | 9.30 | 35.8 | 12.1 | 1.8 | |

| Gurobi | 22.9788 | 34.29 | 5.66 | 9.30 | 35.8 | 12.1 | 4.9 | ||

| IRWLS | 22.9789 | 34.30 | 5.66 | 9.30 | 35.7 | 12.1 | 71.3 | ||

| BR | 22.9788 | 34.29 | 5.66 | 9.30 | 35.8 | 12.1 | 161.5 | ||

| E3 | |||||||||

| AS-PPA | 2.8645 | 2.59 | 1.01 | 0.24 | 11.2 | 0.0 | 0.2 | ||

| Gurobi | 2.8645 | 2.59 | 1.01 | 0.24 | 11.2 | 0.0 | 4.4 | ||

| IRWLS | 2.8646 | 2.59 | 1.01 | 0.24 | 122.9 | 0.0 | 70.9 | ||

| BR | 2.8645 | 2.59 | 1.01 | 0.24 | 11.2 | 0.0 | 24.7 | ||

| MN | AS-PPA | 2.9327 | 2.76 | 1.09 | 0.29 | 11.5 | 0.0 | 0.2 | |

| Gurobi | 2.9327 | 2.76 | 1.09 | 0.29 | 11.5 | 0.0 | 4.4 | ||

| IRWLS | 2.9328 | 2.76 | 1.09 | 0.29 | 127.4 | 0.0 | 70.7 | ||

| BR | 2.9327 | 2.76 | 1.09 | 0.29 | 11.5 | 0.0 | 24.7 | ||

| Cauthy | AS-PPA | 13.9108 | 5.33 | 2.06 | 1.10 | 11.0 | 0.3 | 0.2 | |

| Gurobi | 13.9108 | 5.33 | 2.06 | 1.10 | 11.0 | 0.3 | 4.5 | ||

| IRWLS | 13.9109 | 5.33 | 2.06 | 1.10 | 141.1 | 0.0 | 70.9 | ||

| BR | 13.9108 | 5.33 | 2.06 | 1.10 | 11.0 | 0.3 | 21.9 | ||

| AS-PPA | 3.2881 | 1.24 | 0.71 | 0.58 | 2.1 | 0.0 | 0.1 | ||

| Gurobi | 3.2881 | 1.24 | 0.71 | 0.58 | 2.1 | 0.0 | 4.8 | ||

| IRWLS | 3.2881 | 1.24 | 0.71 | 0.58 | 4.8 | 0.0 | 72.0 | ||

| BR | 3.2881 | 1.24 | 0.71 | 0.58 | 2.1 | 0.0 | 15.8 | ||

| MN | AS-PPA | 3.3529 | 1.34 | 0.76 | 0.67 | 2.0 | 0.0 | 0.1 | |

| Gurobi | 3.3529 | 1.34 | 0.76 | 0.67 | 2.0 | 0.0 | 4.8 | ||

| IRWLS | 3.3530 | 1.34 | 0.76 | 0.67 | 5.4 | 0.0 | 72.5 | ||

| BR | 3.3529 | 1.34 | 0.76 | 0.67 | 2.0 | 0.0 | 15.6 | ||

| Cauthy | AS-PPA | 14.1796 | 3.15 | 1.78 | 3.98 | 1.8 | 0.3 | 0.1 | |

| Gurobi | 14.1796 | 3.15 | 1.78 | 3.98 | 1.8 | 0.3 | 4.8 | ||

| IRWLS | 14.1797 | 3.15 | 1.78 | 3.98 | 80.0 | 0.0 | 70.9 | ||

| BR | 14.1796 | 3.15 | 1.78 | 3.98 | 1.8 | 0.3 | 14.9 | ||

| AS-PPA | 3.1889 | 1.53 | 0.68 | 0.32 | 8.5 | 0.0 | 0.1 | ||

| Gurobi | 3.1889 | 1.53 | 0.68 | 0.32 | 8.5 | 0.0 | 4.3 | ||

| IRWLS | 3.1890 | 1.53 | 0.68 | 0.32 | 39.9 | 0.0 | 72.0 | ||

| BR | 3.1889 | 1.53 | 0.68 | 0.32 | 8.5 | 0.0 | 20.7 | ||

| MN | AS-PPA | 3.2537 | 1.64 | 0.74 | 0.38 | 8.2 | 0.0 | 0.1 | |

| Gurobi | 3.2537 | 1.64 | 0.74 | 0.38 | 8.2 | 0.0 | 4.4 | ||

| IRWLS | 3.2538 | 1.64 | 0.74 | 0.38 | 44.9 | 0.0 | 76.7 | ||

| BR | 3.2537 | 1.64 | 0.74 | 0.38 | 8.2 | 0.0 | 21.1 | ||

| Cauthy | AS-PPA | 14.1917 | 3.44 | 1.53 | 1.84 | 7.5 | 0.1 | 0.2 | |

| Gurobi | 14.1917 | 3.44 | 1.53 | 1.84 | 7.5 | 0.1 | 4.5 | ||

| IRWLS | 14.1918 | 3.44 | 1.53 | 1.84 | 81.7 | 0.0 | 72.6 | ||

| BR | 14.1917 | 3.44 | 1.53 | 1.84 | 7.5 | 0.1 | 18.7 | ||

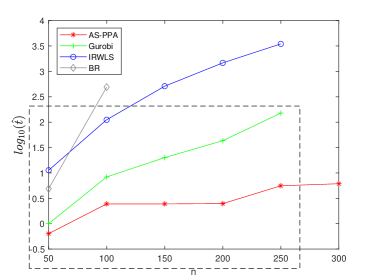

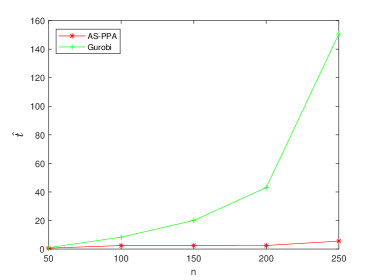

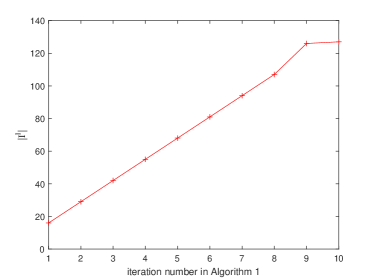

To further investigate the cputime consumed by each method, we choose E2 as a typical example with error for different ’s and . As we can see from Figure 4, the cputime taken by BR and IRWLS increases dramatically whereas Gurobi increases in a slower trend than the above two. In order to see the time comparison more clearly, we show the results of Figure 4 in the Table 7. In Table 7, ’–’ indicates the cputime is more than one hour, that is after reaches 150, the cputime taken by BR exceeds one hour, while Gurobi and IRWLS exceed one hour after reaches 300. For those results that take more than an hour, we do not show them in Figure 4. In contrast, the time taken by AS-PPA increases the slowest as grows. Figure 4 further zooms in to demonstrate the cputime taken by AS-PPA and Gurobi. As grows, it can be seen that the cputime by AS-PPA grows slowly whereas the cputime by Gurobi increases dramatically. For , AS-PPA takes less than 10 seconds which is much smaller than 140 seconds by Gurobi. The fast speed of AS-PPA can be further explained by the smaller scale of subproblems due to the efficient adaptive sieving strategy, as shown in Figure 5. In Figure 5, the size of each subproblem is much smaller (less than ), compared with the scale of the original problem. Due to the above observations, below we only compare with Gurobi.

| BR | IRWLS | Gurobi | AS-PPA | |

|---|---|---|---|---|

| 4.88 | 11.27 | 1.00 | 0.64 | |

| 490.28 | 111.39 | 8.32 | 2.45 | |

| – | 510.40 | 20.01 | 2.45 | |

| – | 1470.19 | 43.07 | 2.48 | |

| – | 3480.74 | 150.63 | 5.58 | |

| – | – | – | 6.12 |

Next, we test E1 - E3 in larger scale. That is, . As we can see from Table 8, the quality of solutions provided by AS-PPA and Gurobi are the same, indicate by the same values in val, , ME, FP and FN. However, AS-PPA is much faster than Gurobi. Even for E2, which is a difficult case, the cputime consumed by AS-PPA is ten times faster than Gurobi. The reason is that the linear programming problem has 41800 variables with 19900 equality constraints, 39800 box constraints and 2000 inequality constraints. In contrast, for AS-PPA, there are only 2200 variables and 1200 equality constraints and the subproblem in AS algorithm is even in a much smaller scale.

| Error | val | ME | FP | FN | ||||

| AS-PPA Gurobi | ||||||||

| E1 | ||||||||

| 2.1744 | 0.59 | 0.25 | 0.04 | 10.78 | 0 | 0.2 34.5 | ||

| 2.6893 | 1.18 | 0.50 | 0.18 | 10.84 | 0 | 0.2 34.4 | ||

| 3.1158 | 1.66 | 0.71 | 0.35 | 10.90 | 0 | 0.2 33.4 | ||

| MN | 2.7576 | 1.24 | 0.53 | 0.20 | 10.96 | 0 | 0.2 34.5 | |

| 3.5774 | 2.00 | 0.85 | 0.51 | 10.80 | 0 | 0.2 33.9 | ||

| Cauthy | 11.3205 | 2.63 | 1.09 | 0.86 | 12.14 | 0 | 0.2 33.6 | |

| E2 | ||||||||

| 9.5967 | 6.12 | 0.88 | 0.18 | 69.96 | 0.16 | 3.8 48.1 | ||

| 9.9378 | 11.48 | 1.66 | 0.69 | 68.42 | 1.84 | 4.3 47.0 | ||

| 10.2303 | 15.37 | 2.24 | 1.32 | 68.06 | 3.04 | 4.4 46.4 | ||

| MN | 9.9725 | 12.16 | 1.76 | 0.78 | 68.04 | 1.98 | 4.3 47.6 | |

| 10.5935 | 18.58 | 2.71 | 2.07 | 65.68 | 4.16 | 4.0 45.9 | ||

| Cauthy | 18.1334 | 26.03 | 3.81 | 5.03 | 62.80 | 7.12 | 5.1 44.0 | |

| E3 | ||||||||

| 2.4285 | 2.04 | 0.77 | 0.15 | 15.12 | 0 | 0.2 33.6 | ||

| MN | 2.4994 | 2.15 | 0.82 | 0.16 | 15.10 | 0 | 0.2 34.1 | |

| Cauthy | 11.0742 | 4.45 | 1.64 | 0.70 | 15.92 | 0.04 | 0.3 33.7 | |

| 2.7884 | 0.84 | 0.47 | 0.26 | 2.84 | 0 | 0.1 33.1 | ||

| MN | 2.8546 | 0.89 | 0.50 | 0.30 | 2.96 | 0 | 0.1 33.5 | |

| Cauthy | 11.3876 | 1.92 | 1.04 | 1.32 | 3.26 | 0 | 0.1 33.6 | |

| 2.6893 | 1.18 | 0.50 | 0.18 | 10.84 | 0 | 0.2 34.3 | ||

| MN | 2.7576 | 1.24 | 0.53 | 0.20 | 10.96 | 0 | 0.1 34.4 | |

| Cauthy | 11.3205 | 2.63 | 1.09 | 0.86 | 12.14 | 0 | 0.2 33.4 | |

To further demonstrate the performance of AS-PPA, we expand the data scale to . This scale is already beyond the reach of Gurobi, because it needs to generate a matrix of 199900010000, occupying nearly 150G of memory which is out of the reach for our laptop. So we only show the results of AS-PPA in Table 9. It can be seen that AS-PPA is quite efficient, even for the difficult example E2. In particular, for the Cauchy distribution of in E2, it takes less than one minute to return a solution.

| Error | val | ME | FP | FN | It-AS | It-PPA | It-ALM | It-SSN | ||||

| E1 | ||||||||||||

| 1.1296 | 0.2370 | 0.1005 | 0.0091 | 12 | 0 | 1.4 | 2 | 45 | 99 | 641 | ||

| 1.6812 | 0.4739 | 0.2011 | 0.0363 | 12 | 0 | 1.1 | 2 | 20 | 73 | 605 | ||

| 2.1381 | 0.6702 | 0.2843 | 0.0725 | 13 | 0 | 1.1 | 2 | 21 | 81 | 656 | ||

| 1.7751 | 0.5140 | 0.2171 | 0.0422 | 13 | 0 | 1.0 | 2 | 19 | 69 | 605 | ||

| 2.6189 | 0.8312 | 0.3502 | 0.1136 | 18 | 0 | 2.1 | 2 | 21 | 80 | 927 | ||

| Cauthy | 7.9566 | 0.9608 | 0.3558 | 0.0764 | 15 | 0 | 2.4 | 3 | 34 | 127 | 1575 | |

| E2 | ||||||||||||

| 3.7605 | 1.5889 | 0.2059 | 0.0234 | 120 | 0 | 22.3 | 5 | 76 | 191 | 4789 | ||

| 4.2951 | 3.1778 | 0.4117 | 0.0935 | 123 | 0 | 19.7 | 4 | 70 | 176 | 4416 | ||

| 4.7380 | 4.4941 | 0.5823 | 0.1869 | 124 | 0 | 23.8 | 4 | 49 | 163 | 4764 | ||

| 4.4651 | 3.5411 | 0.4533 | 0.1136 | 129 | 0 | 28.3 | 5 | 52 | 189 | 5625 | ||

| 5.1816 | 5.4715 | 0.7208 | 0.2955 | 127 | 0 | 30.2 | 5 | 58 | 198 | 5936 | ||

| Cauthy | 10.4809 | 8.7929 | 1.0621 | 0.5330 | 159 | 0 | 46.2 | 5 | 86 | 226 | 8241 | |

| E3 | ||||||||||||

| 1.5808 | 0.7844 | 0.2955 | 0.0291 | 25 | 0 | 1.5 | 2 | 24 | 90 | 901 | ||

| MN | 1.6807 | 0.8331 | 0.3156 | 0.0338 | 18 | 0 | 1.3 | 2 | 23 | 84 | 888 | |

| Cauthy | 7.8553 | 1.5885 | 0.5455 | 0.0691 | 24 | 0 | 3.4 | 3 | 38 | 151 | 2031 | |

| 1.7335 | 0.3403 | 0.1907 | 0.0485 | 3 | 0 | 0.4 | 2 | 44 | 89 | 250 | ||

| MN | 1.8145 | 0.3648 | 0.2033 | 0.0550 | 4 | 0 | 0.5 | 2 | 17 | 64 | 302 | |

| Cauthy | 8.0068 | 0.6816 | 0.3032 | 0.0922 | 13 | 0 | 1.4 | 3 | 55 | 142 | 837 | |

| 1.6812 | 0.4739 | 0.2011 | 0.0363 | 12 | 0 | 1.0 | 2 | 20 | 73 | 605 | ||

| MN | 1.7751 | 0.5140 | 0.2171 | 0.0422 | 13 | 0 | 0.9 | 2 | 19 | 69 | 605 | |

| Cauthy | 7.9566 | 0.9608 | 0.3558 | 0.0764 | 15 | 0 | 2.5 | 3 | 34 | 127 | 1575 | |

6.4 Comparison with the Safe Feature Screening Method

In this part, we compare AS-PPA with the safe feature screening method proposed in [24]. The method is denoted as Safe-PPA, where PPA is also used to solve the subproblem. We test a sequence of with , where is derived in [24]. We report the following information as in [24]. The rejection ratio (RR) is the ratio between the number of discarded features by the screening rules and the actual inactive features corresponding to , that is, RR, where is for the solution obtained for the original problem, and is the set of components that are removed after screening, that is, the components that the screening rule takes zeros. The ratio of speed up (Rsp) is defined as , where is the time of solving the original problem before screening, is the time of solving the subproblem after screening.

Table 1 shows the results under different dimensions, where is the total time of taking 10 values for . From Table 1, we can see that AS-PPA is the winner in every way. It takes the smallest cputime after using our sieving strategy, and Rsp by AS strategy is more than 80 times. For , Rsp indicates that the ratio of speeding up even reaches about 1593 times, which verifies that AS strategy is indeed very efficient. For the data sets with larger , the sieving efficiency of Safe-PPA decreases. Especially on and data sets, Safe-PPA can hardly remove the components which is reflected in the RR value of 0. AS-PPA can still remove more than 99% of nonzero components.

| Method | RR | Rsp | |||

|---|---|---|---|---|---|

| (10,5000) | AS-PPA | 0.9908 | 7.897 | 0.020 | 396.05 |

| Safe-PPA | 0.9345 | 0.244 | 32.41 | ||

| (10,10000) | AS-PPA | 0.9997 | 14.865 | 0.017 | 854.13 |

| Safe-PPA | 0.9958 | 0.343 | 43.30 | ||

| (10,15000) | AS-PPA | 0.9998 | 33.715 | 0.021 | 1593.00 |

| Safe-PPA | 0.9830 | 0.709 | 47.56 | ||

| (50,5000) | AS-PPA | 0.9986 | 74.968 | 0.464 | 161.44 |

| Safe-PPA | 0.2565 | 3.668 | 20.44 | ||

| (50,10000) | AS-PPA | 0.9993 | 275.855 | 0.503 | 548.92 |

| Safe-PPA | 0.0489 | 9.586 | 28.78 | ||

| (50,15000) | AS-PPA | 0.9995 | 612.481 | 1.142 | 536.48 |

| Safe-PPA | 0.1382 | 31.216 | 19.62 | ||

| (100,5000) | AS-PPA | 0.9982 | 377.698 | 4.320 | 87.43 |

| Safe-PPA | 0.0000 | 19.158 | 19.72 | ||

| (100,10000) | AS-PPA | 0.9991 | 1442.261 | 6.299 | 228.95 |

| Safe-PPA | 0.0000 | 67.501 | 21.37 | ||

| (100,15000) | AS-PPA | 0.9994 | 1970.681 | 4.013 | 491.13 |

| Safe-PPA | 0.0007 | 87.001 | 22.65 |

6.5 Comparison on Square-Root Lasso Model

In addition to the hdr model, a model named square-root lasso is also of the form (1). The square-root lasso model has the form of

| (28) |

In [44], the authors transformed the square-root lasso problem into a cone programming problem (CCP) to solve. In [46], Tang et al. proposed proximal majorization-minimization (PMM) algorithm to solve the square-root lasso problem. In this subsection, we contrast our method with these two methods of square-root lasso model. PMM can solve the square-root lasso model with proper nonconvex regularizations. For comparison, we only fix its loss function as norm and do not compare with non-convex regularizations. We choose following the way in [44]222 is set to with being the cumulative normal distribution function..

We report the numerical results in Tables 11 for different scales of test problems. We report the primal objective value (val), and the computation time () in seconds. All the results are taken average over 50 random runs. On the small scales test problems, we can see that AS-PPA and PMM return the same solutions due to the same objective value. For CCP, the value is slightly larger than the other two. Nevertheless, CCP still takes more time to solve the problem, 20 times as long as AS-PPA. In contrast, the performance of PMM is much better, although it also takes more than 0.05s. For the problems with , the solutions obtained by AS-PPA and PMM are still basically the same, and the quality is higher than that of CCP. It can be seen that the time consuming of CCP is still the longest, and that of PMM is also longer than that of AS-PPA. This may be because PMM also exploits the sparsity of the model, so although the scale increases, the time increase is not particularly large.

| Dataset | Error | Method | val | Method | val | ||||

|---|---|---|---|---|---|---|---|---|---|

| E5 | AS-PPA | 26.8793 | 0.0077 | AS-PPA | 26.8793 | 0.0077 | |||

| CCP | 26.9093 | 0.1648 | CCP | 26.9093 | 0.1648 | ||||

| PMM | 26.8793 | 0.0788 | PMM | 26.8793 | 0.0788 | ||||

| E6 | AS-PPA | 34.3528 | 0.0084 | AS-PPA | 34.3528 | 0.0084 | |||

| CCP | 34.4057 | 0.1666 | CCP | 34.4057 | 0.1666 | ||||

| PMM | 34.3528 | 0.0546 | PMM | 34.3528 | 0.0546 |

7 Conclusion

In this paper, we designed an adaptive sieving algorithm for the hdr lasso problem, which takes full advantage of the sparsity of the solution. When solving the subproblem with the same form as the original model but with a small scale, we used PPA to solve it, which take full use of the nondifferentiability of the loss function. Extensive numerical results demonstrate that AS-PPA is robust for different types of noises, which verifies the attractive statistical property as shown in [2]. Moreover, AS-PPA is also highly efficient, especially for the case of high-dimensional features, compared with other methods.

Acknowledgments We would like to thank the team of Prof. Lingchen Kong from Beijing Jiaotong University who provided the code for the safe screening rule in [24]. Without their code, our comparison with Safe-PPA would be impossible. \bmheadData availability statement For the simulated data, they can be regenerated according to the instructions in the paper or obtained from the corresponding author.

Statements and Declarations

Funding The research of Qingna Li is supported by the National Science Foundation of China (NSFC) 12071032. \bmheadConflict of interest All authors certify that they have no affiliations with or involvement in any organization or entity with any financial interest or non-financial interest in the subject matter or materials discussed in this manuscript.

Appendix A Appendix

To prove Lemma 1, we need the following proposition.

Proposition 8.

[37, Proposition 2.8] and have the same definitions as above, can be expressed as , where is either the zero matrix or the identity matrix , and any two consecutive blocks cannot be of the same type. Denote . Then it holds that

where

Proof of Lemma 1. For any , there is

where and . For any , , there is

Notice that by (25), , where . We can see that is also a diagonal matrix with diagonal elements in . Therefore, we have .

On the other hand, by Proposition 6 and Proposition 8, we have

where , is a permutation matrix such that . and are defined as in Proposition 8. Therefore, for , define

| (29) |

It is easy to verify that

| (30) |

where and represents the components of corresponding to .

Obviously, for , . If , we only need to show that for any , . Here . Indeed, note that

Together with (30), we have for any . Consequently, for any there is . That is, is positive definite. The proof is finished. ∎

References

- \bibcommenthead

- Lin et al. [2020] Lin, M., Yuan, Y., Sun, D., Toh, K.-C.: Adaptive sieving with PPDNA: Generating solution paths of exclusive lasso models. arXiv preprint arXiv:2009.08719 (2020)

- Wang et al. [2020] Wang, L., Peng, B., Bradic, J., Li, R., Wu, Y.: A tuning-free robust and efficient approach to high-dimensional regression. Journal of the American Statistical Association 115(532), 1700–1714 (2020)

- Wang and Li [2009] Wang, L., Li, R.: Weighted wilcoxon-type smoothly clipped absolute deviation method. Biometrics 65(2), 564–571 (2009)

- Hettmansperger and McKean [2010] Hettmansperger, T.P., McKean, J.W.: Robust Nonparametric Statistical Methods. CRC Press, Boca Raton (2010)

- Fan et al. [2021] Fan, J., Wang, W., Zhu, Z.: A shrinkage principle for heavy-tailed data: High-dimensional robust low-rank matrix recovery. The Annals of Statistics 49(3), 1239–1266 (2021)

- Fan et al. [2020] Fan, J., Ma, C., Wang, K.: Comment on “a tuning-free robust and efficient approach to high-dimensional regression". Journal of the American Statistical Association 115(532), 1720–1725 (2020)

- Efron [2004] Efron, B.: The estimation of prediction error: Covariance penalties and cross-validation. Journal of the American Statistical Association 99(467), 619–632 (2004)

- Tseng [2001] Tseng, P.: Convergence of a block coordinate descent method for nondifferentiable minimization. Journal of Optimization Theory and Applications 109(3), 475–494 (2001)

- Tseng and Yun [2009] Tseng, P., Yun, S.: A coordinate gradient descent method for nonsmooth separable minimization. Mathematical Programming 117, 387–423 (2009)

- Friedman et al. [2007] Friedman, J., Hastie, T., Höfling, H., Tibshirani, R.: Pathwise coordinate optimization. The Annals of Applied Statistics 1(2), 302–332 (2007)

- Wu and Lange [2008] Wu, T.T., Lange, K.: Coordinate descent algorithms for lasso penalized regression. The Annals of Applied Statistics 2(1), 224–244 (2008)

- Beck and Teboulle [2009] Beck, A., Teboulle, M.: A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences 2(1), 183–202 (2009)

- Li et al. [2015] Li, X., Zhao, T., Yuan, X., Liu, H.: The flare package for high dimensional linear regression and precision matrix estimation in R. Journal of Machine Learning Research 16(18), 553–557 (2015)

- Li et al. [2018] Li, X., Sun, D., Toh, K.-C.: A highly efficient semismooth newton augmented Lagrangian method for solving lasso problems. SIAM Journal on Optimization 28(1), 433–458 (2018)

- Kim et al. [2015] Kim, H.-J., Ollila, E., Koivunen, V.: New robust LASSO method based on ranks. In: 2015 23rd European Signal Processing Conference (EUSIPCO), Nice, pp. 699–703 (2015). IEEE

- Barrodale and Roberts [1973] Barrodale, I., Roberts, F.D.: An improved algorithm for discrete linear approximation. SIAM Journal on Numerical Analysis 10(5), 839–848 (1973)

- Zoubir et al. [2018] Zoubir, A.M., Koivunen, V., Ollila, E., Muma, M.: Robust Statistics for Signal Processing. Cambridge University Press, Cambridge (2018)

- Tang et al. [2021] Tang, P., Wang, C., Jiang, B.: A proximal-proximal majorization-minimization algorithm for nonconvex tuning-free robust regression problems. arXiv preprint arXiv:2106.13683 (2021)

- El Ghaoui et al. [2010] El Ghaoui, L., Viallon, V., Rabbani, T.: Safe feature elimination in sparse supervised learning. Technical Report Technical Report UC/EECS-2010-126, Electrical Engineering and Computer Sciences Department, University of California at Berkeley, Berkeley (2010)

- Tibshirani [1996] Tibshirani, R.: Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 58(1), 267–288 (1996)

- Bonnefoy et al. [2014] Bonnefoy, A., Emiya, V., Ralaivola, L., Gribonval, R.: A dynamic screening principle for the Lasso. In: European Signal Processing Conference EUSIPCO 2014, pp. 1–5. IEEE, Lisboa (2014)

- Wang et al. [2013] Wang, J., Zhou, J., Wonka, P., Ye, J.: Lasso screening rules via dual polytope projection. In: Proceedings of the 26th International Conference on Neural Information Processing Systems, pp. 1070–1078. Curran Associates Inc., New York (2013)

- Fercoq et al. [2015] Fercoq, O., Gramfort, A., Salmon, J.: Mind the duality gap: Safer rules for the lasso. In: International Conference on Machine Learning, Lille, pp. 333–342 (2015). PMLR

- Shang et al. [2022] Shang, P., Kong, L., Liu, D.: A safe feature screening rule for rank lasso. IEEE Signal Processing Letters 29, 1062–1066 (2022)

- Yuan et al. [2022] Yuan, Y., Chang, T.-H., Sun, D., Toh, K.-C.: A dimension reduction technique for large-scale structured sparse optimization problems with application to convex clustering. SIAM Journal on Optimization 32(3), 2294–2318 (2022)

- Rockafellar [1976] Rockafellar, R.T.: Monotone operators and the proximal point algorithm. SIAM Journal on Control and Optimization 14(5), 877–898 (1976)

- Rockafellar [1970] Rockafellar, R.: On the maximal monotonicity of subdifferential mappings. Pacific Journal of Mathematics 33(1), 209–216 (1970)

- Sun [1986] Sun, J.: On monotropic piecewise quadratic programming (network, algorithm, convex programming, decomposition method). PhD thesis, Computer Science Department, University of Washington, Seattle (1986)

- Robinson [1981] Robinson, S.M.: In: König, H., Korte, B., Ritter, K. (eds.) Some continuity properties of polyhedral multifunctions, pp. 206–214. Springer, Berlin, Heidelberg (1981)

- Moreau [1965] Moreau, J.-J.: Proximité et dualité dans un espace hilbertien. Bulletin de la Société mathématique de France 93, 273–299 (1965)

- Lemaréchal and Sagastizábal [1997] Lemaréchal, C., Sagastizábal, C.: Practical aspects of the Moreau–Yosida regularization: Theoretical preliminaries. SIAM Journal on Optimization 7(2), 367–385 (1997)

- Rockafellar [1976] Rockafellar, R.T.: Augmented Lagrangians and applications of the proximal point algorithm in convex programming. Mathematics of Operations Research 1(2), 97–116 (1976)

- Luque [1984] Luque, F.J.: Asymptotic convergence analysis of the proximal point algorithm. SIAM Journal on Control and Optimization 22(2), 277–293 (1984)

- Sun et al. [2021] Sun, D., Toh, K.-C., Yuan, Y.: Convex clustering: Model, theoretical guarantee and efficient algorithm. Journal of Machine Learning Research 22(1), 427–458 (2021)

- Yan and Li [2020] Yan, Y., Li, Q.: An efficient augmented Lagrangian method for support vector machine. Optimization Methods and Software 35(4), 855–883 (2020)

- Li et al. [2018] Li, X., Sun, D., Toh, K.-C.: On efficiently solving the subproblems of a level-set method for fused lasso problems. SIAM Journal on Optimization 28(2), 1842–1866 (2018)

- Lin et al. [2019] Lin, M., Liu, Y.-J., Sun, D., Toh, K.-C.: Efficient sparse semismooth newton methods for the clustered lasso problem. SIAM Journal on Optimization 29(3), 2026–2052 (2019)

- Hiriart-Urruty et al. [1984] Hiriart-Urruty, J.-B., Strodiot, J.-J., Nguyen, V.H.: Generalized hessian matrix and second-order optimality conditions for problems with data. Applied Mathematics and Optimization 11(1), 43–56 (1984)

- Qi and Sun [2006] Qi, H., Sun, D.: A quadratically convergent newton method for computing the nearest correlation matrix. SIAM Journal on Matrix Analysis and Applications 28(2), 360–385 (2006)

- Qi [2013] Qi, H.-D.: A semismooth newton method for the nearest euclidean distance matrix problem. SIAM Journal on Matrix Analysis and Applications 34(1), 67–93 (2013)

- Yin and Li [2019] Yin, J., Li, Q.: A semismooth newton method for support vector classification and regression. Computational Optimization and Applications 73(2), 477–508 (2019)

- Li et al. [2010] Li, Q., Li, D., Qi, H.: Newton’s method for computing the nearest correlation matrix with a simple upper bound. Journal of Optimization Theory and Applications 147(3), 546–568 (2010)

- Qi and Sun [1993] Qi, L., Sun, J.: A nonsmooth version of newton’s method. Mathematical Programming 58(1-3), 353–367 (1993)

- Belloni et al. [2011] Belloni, A., Chernozhukov, V., Wang, L.: Square-root lasso: Pivotal recovery of sparse signals via conic programming. Biometrika 98(4), 791–806 (2011)

- Barrodale and Roberts [1974] Barrodale, I., Roberts, F.: Solution of an overdetermined system of equations in the norm [F4]. Communications of the ACM 17(6), 319–320 (1974)

- Tang et al. [2020] Tang, P., Wang, C., Sun, D., Toh, K.-C.: A sparse semismooth newton based proximal majorization-minimization algorithm for nonconvex square-root-loss regression problem. Journal of Machine Learning Research 21(1), 9253–9290 (2020)