Chapter 1

Linear and Nonlinear Partial Integro-Differential Equations arising from Finance

Abstract

The purpose of this review paper is to present our recent results on nonlinear and nonlocal mathematical models arising from modern financial mathematics. It is based on our four papers written jointly by J. Cruz, M. Grossinho, D. Ševčovič, and C. Udeani [20], [19], [58], [66], as well as parts of PhD thesis by J. Cruz [18]. We investigated linear and nonlinear partial integro-differential equations (PIDEs) arising from option pricing and portfolio selection problems and studied the systematic relationships between the PIDEs with option pricing theory and Black–Scholes models. First, we relax the liquid and complete market assumptions and extend the models that study the market’s illiquidity to the case where the underlying asset price follows a Lévy stochastic process with jumps. Then, we establish the corresponding PIDE for option pricing under suitable assumptions. The qualitative properties of solutions to nonlocal linear and nonlinear PIDE are presented using the theory of abstract semilinear parabolic equation in the scale of Bessel potential spaces. The existence and uniqueness of solutions to the PIDE for a general class of the so-called admissible Lévy measures satisfying suitable growth conditions at infinity and origin are also established in the multidimensional space. Additionally, the qualitative properties of solutions to the generalized PIDE are investigated by considering a general shift function arising from nonlinear option pricing models, which takes into account a large trader stock-trading strategy with the underlying asset price following the Lévy process. For the portfolio management problem, we present the existence and uniqueness results of the fully nonlinear HBJ equation arising from the stochastic dynamic optimization problem in Sobolev spaces using the theory of monotone operator technique, which can also be viewed as PIDE in some sense. Furthermore, a stable, convergent, and consistent numerical scheme that can give an approximate solution to such PIDE is presented, and various numerical experiments are conducted to illustrate the influence of a large trader and the intensity of jumps on the option price.

Keywords: Lévy measure, Option pricing, Partial integro-differential equation, Hamilton-Jacobi-Bellman equation, Maximal monotone operator, Dynamic stochastic portfolio optimization

1. Introduction

This review paper contain our recent advances in the research focused on nonlinear and nonlocal mathematical models arising from modern financial mathematics. The major parts of this chapter are based on our four papers jointly written by J. Cruz, M. Grossinho, D. Ševčovič, and C. Udeani [20], [19], [58], [66], as well as parts of PhD thesis by J. Cruz.

The classical Black–Scholes model has been widely used in financial industry because of its simplicity and existence of analytical formula for pricing derivative securities. This model relies on the restrictive assumptions, such as completeness, frictionless of the market, and the assumption that the underlying asset price follows a geometric Brownian motion. However, the assumption that an investor can trade large amount of assets without affecting the underlying asset price is usually not satisfied, especially in illiquid markets. It is also known that the fully nonlinear Hamilton–Jacobi–Bellman equation plays an essential role in finance. For instance, it gives the necessary and sufficient condition of a control with respect to the value function. Therefore, this chapter investigates linear and nonlinear partial integro-differential equations (PIDEs) arising from option pricing and portfolio selection problem. We investigate the systematic relationships of the PIDEs with option pricing theory and Black–Scholes models. First, we relax the liquid and complete market assumptions and extend the models that study market’s illiquidity to the case where the underlying asset price follows a Lévy stochastic process with jumps. Then, we establish the corresponding PIDE for option pricing under suitable assumptions. The qualitative properties of solutions to nonlocal linear and nonlinear PIDE are presented using the theory of abstract semilinear parabolic equation in the scale of Bessel potential spaces. The existence and uniqueness of solutions to the PIDE for a general class of the so-called admissible Lévy measures satisfying suitable growth conditions at infinity and origin are also established, and the solution to the corresponding PIDE are presented in the multidimensional space. Additionally, the qualitative properties of solutions to the generalized PIDE are investigated by considering a general shift function arising from nonlinear option pricing models, which takes into account a large trader stock-trading strategy with the underlying asset price following the Lévy process. For the portfolio management problem, we present the existence and uniqueness results to the fully nonlinear HBJ equation arising from stochastic dynamic optimization problem in Sobolev spaces using the theory of monotone operator technique, which can also be viewed as PIDE in some sense. Furthermore, a stable, convergent, and consistent numerical scheme that can give an approximate solution of such PIDE is presented, and various numerical experiments are conducted to illustrate the influence of a large trader and intensity of jumps on the option price.

The Black–Scholes model and Hamilton–Jacobi–Bellman (HJB) equation have been widely used in financial markets. However, evidence from the stock market observation shows that the Black-Scholes model is not the most realistic one because it depends on some restrictive assumptions, such as the liquidity, completeness, and frictionless of the market. Additionally, the linear Black–Scholes equation provides a solution that corrsponds to a perfectly replicated portfolio, which is not a desirable property. For this reason, several attempts have been made to generalize and relax some of these assumptions. Some authors relaxed these assumptions by considering the presence of transaction costs (see Kwok [41] and Avellaneda and Paras [6]), feedback and illiquid market effects due to large traders choosing given stock-trading strategies (Schönbucher and Willmott [55], Frey and Patie [25], Frey and Stremme [26]), and risk from the unprotected portfolio (Jandačka and Ševčovič [32]). In these generalizations, the constant volatility was replaced by a nonlinear function depending on the second derivative of the option price. Frey and Stremme derived a nonlinear Black–Scholes model that plays an essential role in the class of the generalized Black–Scholes equation with such a nonlinear diffusion function [25, 32, 27]). In this model, the asset dynamics considers the presence of feedback effects due to a large trader choosing his/her stock-trading strategy [55]. Another important direction in generalizing the original Black–Scholes equation arises from the fact that the sample paths of a Brownian motion are continuous; however, the realized stock price of a typical company exhibits random jumps over the intraday scale, making the price trajectories discontinuous. In the classical Black–Scholes model, the logarithm of the price process has normal distribution. However, the empirical distribution of stock returns exhibits fat tails. Meanwhile, when calibrating the theoretical prices to the market prices, the implied volatility is not constant as a function of strike price nor a function of time to maturity, contradicting the prediction of the Black–Scholes model. However, the models with jumps and diffusion can solve the problems inherent to the Black–Scholes model. The jump models also plays an essential role in the option market. In the Black–Scholes model, the market is complete, implying that every payoff can exactly be replicated; meanwhile, there is no perfect hedge in jump models, making the way of options not redundant.

Market Illiquidity has been widely studied in the literature [33, 52, 64, 56, 28]. The first major contribution was made by Robert Jarrow, in 1994, who studied the market manipulation strategies that may arise in illiquid markets. The author also studied the option pricing theory in discrete time when there is a large trader. The pricing argument used was a condition to ensure that no market manipulation strategy is used by the large trader and large trader’s optimality conditions; thus, replacing the usual free-arbitrage argument. Then, Frey (1998) extended Jarrow’s analysis to the continuous time case and established the existence and uniqueness of solution of a nonlinear partial differential equation satisfied by the large trader’s hedging strategy. Additionally, Platten and Schweizer (1998) proposed an explanation for the smile and skewness for the implied volatilities and showed that hedging strategies followed by large traders can lead to option price bias. Sircar and Papanicolaou (1998) also proposed a model where the derivative security price is characterized by a nonlinear partial differential equation that becomes the Black–Scholes equation when there is no feedback. When the programme traders are a small fraction of the economy, numerical and analytical methods can be used to analyze the nonlinear partial differential equation through perturbation. This equation is derived using an argument similar to the one used in deriving classical Black–Scholes equation. Consequently, they obtained that this model also predict increased implied volatilities as in Platten and Schweizer. Furthermore, Schonbucher and Willmott (2000) analyzed the feedback effects from the presence of hedging strategies. They also derived a nonlinear partial differential equation for an option replication strategy and studied these effects for a put option. The effects are more pronounced in markets with low liquidity, which can induce discontinuities in the price process. However, none of these studies that investigated jump models [45, 44, 10, 14, 49, 15, 22] considered in the market’s illiquidity. Meanwhile, investors and risk managers have realized that financial models based on the assumption that an investor can trade large amounts of an asset without affecting its price is no longer true in markets that are not liquid. Therefore, in this chapter, we relax the liquid and complete market hypothesis and extend the models that study market’s illiquidity to the case where the underlying asset price follows a Lévy stochastic process with jumps to obtain a model for pricing European and American call and put options on an underlying asset characterized by a Lévy measure. In this way, it is assumed that trading strategies affects the stock price, and the possibility to account for sudden jumps that might occur when the market is under stress .

Recently, the relationships between more general nonlocal operators and jump processes have been widely investigated. For instance, there is an actual connection between the solution to PIDE and properties of the corresponding Markov jump process (c.f., Abels and Kassmann [2]; Florescu and Mariani [24]). In the past decades, the role of PIDEs has been investigated in various fields, such as pure mathematical areas, biological sciences, and economics [3, 4, 69]. PIDE problems arising from financial mathematics, especially from option pricing models, have been of great interest to many researchers. In most cases, standard methods for solving these problems lead to the study of parabolic equations. Mikulevičius and Pragaraustas [47] investigated solutions of the Cauchy problem to the parabolic PIDE with variable coefficients in Sobolev spaces. They employed their results to obtain solutions of the corresponding martingale problem. Crandal et al. [31] employed the notion of a viscosity solution to investigate the qualitative results. Soner et al. [12] and Barles et al. [8] extended and generalized their results for the first and second order operators, respectively. Florescu and Mariani [24] employed the Schaefer fixed point argument to establish existence of a weak solution of the generalized PIDE. Amster et al. [57] used the notion of upper and lower solutions to obtain the solution to such PIDEs. They proved the existence of solutions in a general domain for multiple assets and the regime switching jump-diffusion model. Cont et al. [16] investigated the actual connection between option pricing in exponential Lévy models and the corresponding PIDEs for European options and those with single or double barriers. They discussed and established the conditions for which prices of option are classical solution of the corresponding PIDE. In this chapter, we obtain a certain partial integro-differential equation (PIDE) for option pricing in illiquid market by assuming a certain dynamics for the stock’s price. The existence of solution and localization results of the associated PIDE are also established. We investigated and established the qualitative properties of solutions to the nonlocal linear and nonlinear PIDE in the scale of Bessel potential spaces using the theory of abstract semilinear parabolic equation. Furthermore, we present the existence and uniqueness results for nonlinear parabolic equations using monotone operator technique, Fourier transform, and Banach fixed point argument. We considered the fully nonlinear HJB equation arising portfolio selection problem, where the goal of an investor is to optimize the condition expected value of the terminal utility of the portfolio. Such nonlinear parabolic equation is presented in an abstract setting, which can also be viewed as a nonlinear PIDE. Many previous studies have developed numerical methods for PIDEs, such as finite difference and finite element methods. However, the equation corresponding to the case of illiquid markets is more difficult. Therefore, this chapter also presents a stable, convergent, and consistent numerical scheme that can give an approximate solution of such PIDEs. Various numerical experiments are presented to illustrate the influence of a large trader and intensity of jumps on the option price.

2. Background and Motivation

Based on the classical theory developed by Black, Scholes, and Merton, the price of an option in a stylized market at time and the underlying asset price can be calculated as a solution to the following linear Black–Scholes parabolic equation:

| (1) |

Here, is the historical volatility of the underlying asset driven by the geometric Brownian motion, and is the risk-free interest rate of zero-coupon bond. The solution to above equation is subject to the terminal payoff condition at maturity . Meanwhile, evidence from stock markets observations indicates that the model is not the most realistic one because it assumes that the market is liquid, complete, frictionless and without transaction costs. It is also known that the linear Black–Scholes equation provides a solution corresponding to a perfectly replicated portfolio, which need not be a desirable property. To solve this issues, several attempts have been made to generalized the linear Black–Scholes equation (1) by replacing the constant volatility with a nonlinear function depending on the second derivative of the option price. In this regard, Frey and Stremme derived a nonlinear Black–Scholes model, which plays an essential role in the class of generalized Black–Scholes equation with such a nonlinear diffusion function [25, 27]). They considered that case in which the asset dynamics takes into account the presence of feedback effects due to a large trader choosing his/her stock-trading strategy (see also [55]). The diffusion coefficient is non-constant, and it is given by

| (2) |

where and are constants.

Furthermore, several researchers have attempted to generalized the original Black–Scholes equation arises from the fact that the sample paths of a Brownian motion are continuous. However, the realized stock price of a typical company exhibits random jumps over the intraday scale, making the price trajectories discontinuous. The underlying asset price process is usually assumed to follow a geometric Brownian motion in the classical Black–Scholes model. However, the empirical distribution of stock returns exhibits fat tails. The models with jumps and diffusion can solve the problems inherent to the linear Black–Scholes model and play an essential role in options pricing. It is well-known that the market is complete in the Black–Scholes model, illustrating that each payoff can be perfectly replicated; however, there is no perfect hedge in jump–diffusion models, making the options not redundant. It turns out that the option price can be computed from the solution to the following PIDE Black–Scholes equation [20]:

| (3) |

where , and is the so-called Lévy measure characterizing the underlying asset process with random jumps in time and space. It is worth noting that (3) reduces to the classical linear Black–Scholes equation (1) if .

In this chapter, we consider both directions of generalizations of the Black–Scholes equation. First, we relaxed the assumption of liquid market following the Frey–Stremme model by assuming that the underlying asset price follows a Lévy stochastic process with jumps and established the corresponding PIDEs. Then, we present the existence and uniqueness results to the linear and nonlinear nonlocal PIDE in the framework of Bessel potential spaces for the multidimensional case. A more generalized nonlinear nonlocal PIDE is also presented by considering a shift function depending on the variables . Furthermore, we derive, analyze, and perform numerical computation of the model. We also show that the corresponding PIDE nonlinear equation has the following form:

| (4) |

It is worth noting that the function may depend on the large trader strategy function and the delta of the price if .

We consider a stylized economy with two traded assets: a riskless asset (a bond with a price taken as numeraire) and a risky asset (stock with a price ). Here, we assume that the bond market is perfectly elastic since it is more liquid than stocks. Here, we consider two type of traders: reference and program traders. The program traders are also known as portfolio insurers because they use dynamic hedging strategies to hedge portfolio against jumps in stock prices. They are classified as single traders or group of traders acting together. It is assumed that their trades influence the stock price equilibrium. In contrast, the reference traders can be considered as representative traders of many small agents. We assume that they act as price takers. Generally, represents the reference trader demand function that depends on the income process or some other fundamental state variable influencing the reference trader demand. The aggregate demand of program traders is denoted by , where is the number of written identical securities that the program traders are trying to hedge, and is the demand per unit of the security being hedged. For simplicity, we assume that is the same for every program trader. For a more general case where different securities are considered, see [64]. Suppose the supply of a stock with the price is constant, and let be the quantity demanded by a reference trader per unit supply. Then, the total demand relative to the supply at time is given by , where , and is the proportion of the total supply of the stock traded by program traders. Therefore, to obtain the market equilibrium, the variables and should satisfy . Assume that the function is monotone with respect to the variables and , and it is sufficiently smooth. Then, we can solve the implicit equation to obtain , where is a sufficiently smooth function. By employing the approach in [64], we assume that the stochastic process has the following dynamics:

Then, using Itô’s lemma for the process , we have

| (5) |

It means that follows a geometric Brownian motion with a nonconstant volatility function , where . Thus, we follow the argument used in the derivation of the original Black–Scholes equation to obtain a generalization of the Black–Scholes partial differential equation with a nonconstant volatility function . We employ the Frey and Stremme’s approach (cf. [25, 27]) to prescribe a dynamics for the underlying stock price instead of deriving it using the market equilibrium and dynamics for the income process as it is done in [64]. In this way, Frey and Stremme derived the same stock price dynamics as in [64] corresponding to a situation where the demand function is of logarithmic type, , where , and the income process follows a geometric Brownian motion, i.e.,

| (6) | |||

Assuming the delta hedging strategy with and substituting the volatility function in (5), we obtain the generalized Black–Scholes equation with the nonlinear diffusion function of the form (2).

In this chapter, we first generalized the Frey–Stremme model by considering an underlying asset following a Lévy process with jumps. Then, we establish the corresponding PIDE for option pricing. Furthermore, we investigated the existence and uniqueness of solutions to such PIDE in the multidimensional spaces.

3. Preliminaries and Definitions

This section presents some basic definitions and properties of Lévy measures and notion of admissible activity Lévy measures. Here, and represent the Euclidean norm in and the norm in an infinite dimensional function space (e.g., ). HIn what follows, stands for the usual Euclidean product in with the norm .

Definition 1.

[58] A Lévy process on is a stochastic (right continuous) process having the left limit with independent stationary increments. It is uniquely characterized by its Lévy exponent :

The subscript in the expectation operator indicate that the process starts from a given value at the origin . The Lévy exponent has the following unique decomposition:

where is a constant vector; is a constant matrix, which is positive semidefinite; is a nonnegative measure on such that (c.f., [50]).

3.1. Exponential Lévy models

Let be a stochastic process. The Poisson random measure of a Borel set is defined by , where . This measure gives the mean number per unit time of jumps whose amplitude belongs to the set . It is worth noting that the Lévy–Itô decomposition provides a representation of interpreted as a combination of a Brownian motion with a drift and an infinite sum of independent compensated Poisson processes with variable jump sizes (see [19]), i.e.,

where is the compensation of .

Remark 1.

[19, Remark 1] Note that any Lévy process is a strong Markov process, and the associated semigroup is a convolution semigroup. Its infinitesimal generator is a nonlocal partial integro-differential operator given by

| (7) | |||||

which is well-defined for any compactly supported function .

Let be a stochastic process representing an underlying asset process under a filtered probability space . The filtration represents the price history up to the time . In an arbitrage-free market, there is an equivalent measure under which discounted prices of all traded assets are martingales, which is called the fundamental theorem of asset pricing (see, [17]). The measure is also known as the risk-neutral measure. We consider the exponential Lévy model in which the risk-neutral price process under is given by , where is a Lévy process under with the characteristic triplet . Then, the arbitrage-free market hypothesis states that is a martingale, which is equivalent to the following conditions imposed on the triplet :

| (8) |

The risk-neutral dynamics of under is given by

| (9) |

The exponential price process, , is also a Markov process with the state space . It has the following infinitesimal generator:

| (11) | |||||

(see [17]). A Lévy process with the following representation:

is called the Lévy type stochastic integral. The following variant of Itô’s lemma is an essential results, which will be needed later in this study.

Theorem 1.

[20, Therorem 2.1] Let and . Suppose is a Lévy stochastic process. Then,

3.2. Examples of Lévy processes in finance

There are two types of exponential Lévy models considered in the literature. The first types are jump-diffusion models, where the log-price is represented as a Lévy process with a nonzero diffusion part and a jump process with finite activity i.e., . The second types of models are infinite activity pure jump models, where there is no diffusion part and only a jump process with infinite activity i.e., . This section presents different types of exponential Lévy models that differ in the choice of the Lévy measure.

3.2.1. Jump-Diffusion models

A Lévy process with jump-diffusion has the following general form:

where , and is a Poisson process with intensity that counts the jumps of , and are independent and identically distributed random variables with distribution . The Lévy measure is , and the drift is given by

Merton’s model

This is the first jump-diffusion model proposed by Merton [45] in the financial application. The random variables , are normally distributed with mean and variance . It has the following Lévy density:

| (13) |

where the parameters are given. Merton’s measure is a finite activity Lévy measure, i.e., , with finite variation . Therefore, the probability density of can be obtain as a series that converges rapidly (see [17]): {IEEEeqnarray}rCl p_t(x)&=∑_j=0^∞e^-λt(λt)^je-—z-γt-jm—22(σ2t+jδ2)j!2 π(σ2t+jδ2). Thus, the price of an European call option can be expressed as a weighted sum of Black–Scholes prices:

| (14) |

where , , and is the well-known Black–Scholes formula.

3.2.2. Infinite activity pure jump models

The variance Gammma and normal inverse Gaussian (NIG) processes are obtained by a subordination of a Brownian motion and a tempered -stable process; variance Gamma and NIG processes correspond to and , respectively. These models are widely used in finance because of the existence of probability density of the subordinator in a closed form for these values of (see [17]).

Variance Gamma process

This is a pure discontinuous process of infinite activity and finite variation () that is widely used in the financial modeling. It has the following Lévy measure:

Here, and are parameters related to the volatility and drift of the Brownian motion, respectively; is the parameter related to the variance of the subordinator, which is a the Gamma process (see [17]). The probability density is given by

where is the modified Bessel function of second kind. The characteristic function of is given by

where is determined by the martingale condition, and is the characteristic function of . Moreover, we have

| (15) |

where

| (16) |

is the risk-neutral process introduced in [44]. Therefore,

Normal inverse Gaussian model

The NIG process is a process of infinite activity and infinite variation without any Brownian component. It has the following Lévy measure [17]

and

where , , and have the same meaning as in the Variance Gamma process. The probability density is given by

where is the modified Bessel function of second kind. The characteristic function is given by

| (17) |

Generalized hyperbolic model

The generalized hyperbolic model is a process of infinite variation without Gaussian part. It has the following characteristic function (see [17]):

| (18) |

where is a scale parameter, is the shift parameter, and has the same meaning as in the variance Gamma process. The parameters , , and determine the shape of the distribution. The density function

where is the modified Bessel function and

The variance Gamma process is obtained for and . The NIG process corresponds to .

3.3. Admissible activity Lévy measures

This subsection presents the notion of an admissible activity Lévy measure introduced by Cruz and Ševčovič [20, 19] for the one-dimensional case , which was later extended by Ševčovič and Udeani [58] for the multidimensional case .

Definition 2.

[58, Definition 1] A measure in is called an admissible activity Lévy measure if there exists a nonnegative Lebesgue measurable function such that with

| (19) |

for all and the shape parameters ( if , where is a positive constant.

Remark 2.

It is worth noting that the additional conditions and are satisfied provided that is an admissible Lévy measure with shape parameters , and either , or and . For the Merton model, we have and . Meanwhile, for the Kou model, we have . For the variance Gamma process, we have .

4. Multidimensional Linear and Nonlinear PIDE

This section focuses on qualitative properties of solutions to the linear and nonlinear nonlocal parabolic PIDE of the form:

where is a given sufficiently smooth function; is a positive measure on such that its Radon derivative is a nonnegative Lebesgue measurable function in , i.e., . Additionally, we will analyze the solution of the following generalization of the above PIDE, in which the shift function may depend on the variables :

| (21) |

where is the shift function. An application of such a general shift function can be found in nonlinear option pricing models considering a large trader stock-trading strategy with the underlying asset price dynamic following the Lévy process (c.f., Cruz and Ševčovič [20]). If , then (21) reduces to equation (4.). Fr example, the nonlinearity often arises from applications occurring in pricing XVA derivatives (c.f., Arregui et al. [4, 5]) or applications of the penalty method for American option pricing under a PIDE model (c.f., Cruz and Ševčovič [19]).

4.1. Existence and uniqueness results of PIDE

In this section, we present the existence and uniqueness results for the general (21) for a class of Lévy measures using the theory of abstract semilinear parabolic equation in the scale of Bessel potential spaces. First, we rewrite the PIDE (21) in high-dimensional space as follows:

| (22) |

where . The linear nonlocal operator is defined by

| (23) |

where is a given shift function. The function is assumed to be Hölder and Lipschitz continuous in the and other variables, respectively. Then, we employ the theory of abstract semilinear parabolic equations presented by Henry [29] to establish the existence, continuation, and uniqueness of a solution. A solution to the PIDE (22) is constructed in the scale of the Bessel potential spaces in high-dimensional space, . These spaces can be viewed as a natural extension of the classical Sobolev spaces for non-integer values of order . It is worth noting that nested scale of Bessel potential spaces allows for a finer formulation of existence and uniqueness results than the classical Sobolev spaces.

Definition 3.

[29, Definition 1] An analytic semigroup is a family of bounded linear operators in a Banach space satisfying the following conditions:

-

i)

, for all ;

-

ii)

when for all ;

-

iii)

is a real analytic function on for each .

The associated infinitesimal generator is defined as follows: and its domain consists of those elements for which the limit exists in the space .

Definition 4.

[29] Let be a sector of complex numbers. A closed densely defined linear operator is called a sectorial operator if there exists a constant such that for all .

Next, we briefly recall the construction and basic properties of Bessel potential spaces. It is worth noting if is a sectorial operator in a Banach space , then is a generator of an analytic semigroup acting on (c.f., [29, Chapter I]). For any , we can introduce the operator as follows: . Then, the fractional power space is the domain of the operator , i.e., . The norm is defined as follows: . Furthermore, we have continuous embedding: , for .

Let us recall the convolution operator . According to [29, Section 1.6], is a sectorial operator in the Lebesgue space for any , and . It follows from [65, Chapter 5] that the space can be identified with the Bessel potential space , where

Here, is the Bessel potential function,

The norm of is given by . The space is continuously embedded in the fractional Sobolev–Slobodeckii space (c.f., [29, Section 1.6]).

In what follows, we denote as a generic constant, which is independent of the solution ; however, it may depend on the model parameters, e.g., .

Proposition 1.

[58, Proposition 1] Let us define the mapping as follows:

Then, there exists a constant such that, for any vector valued functions , and such that , , the following estimate holds:

Proof.

Let be such that , i.e., . Then, for some , and . Here, and . Let . Then,

Recall that the following inequality holds for convolution operator:

where and (see [29, Section 1.6]). In particular, for , we have . The following estimate holds for the modulus of continuity of the Bessel potential function :

for any (c.f., [65, Chapter 5.4, Proposition 7]). Let be bounded vector valued functions, i.e., . Then, for any , we have

Now,

By Young’s inequality, we have for any , and with (c.f., [13]). Set . Then, , and we obtain . Therefore,

Hence, the pointwise estimate holds with the constant . ∎

Applying Proposition 1 with , we obtain the following corollary.

Corollary 1.

[58, Corollary 1] Let be such that where . Then, for any , the following pointwise estimate holds:

Next, we consider the case when the nonlocal integral term depends on and variables. It is a generalization of the result [20, Lemma 3.4] due to Cruz and Ševčovič proven for the case where .

Proposition 2.

[58, Proposition 2] Suppose that the shift mapping satisfies for some constants and any . Assume is a Lévy measure with the shape parameters and either , or and . Assume , and . Then there exists a constant such that

provided that . If then , i.e., is a bounded linear operator.

Proof.

The Lévy measure is given by . Let us denote the auxiliary function . Then, . Since , where and . Applying Proposition 1 with , and using the Hölder inequality, we obtain

Assuming are such that

then, the integrals and are finite, provided that the shape parameters satisfy: either , or . As , there exists satisfying

Therefore, there exists such that . ∎

Let be the Banach space consisting of continuous functions from to with the maximum norm. The following proposition is due to Henry [29] (see also Cruz and Ševčovič [19]).

Proposition 3.

[29, Proposition 3.5] Suppose that the linear operator is a generator of an analytic semigroup in a Banach space . Assume the initial condition belongs to the space where . Suppose that the mappings and are Hölder continuous in the variable, , and is Lipschitz continuous in the variable. Then, for any , there exists a unique solution to the abstract semilinear evolution equation: such that for any . The function is a solution in the mild (integral) sense, i.e., , .

Applying Propositions 2 and 3, we can state the following result which is a nontrivial generalization of the result shown by Ševčovič and Cruz [19] for .

Theorem 2.

[58, Theorem 1] Suppose that the shift mapping satisfies , for some constants . Assume is an admissible activity Lévy measure with the shape parameters , and, either , or . Assume and , . Suppose that is Hölder continuous in the variable and Lipschitz continuous in the remaining variables, respectively. Assume , and . Then, there exists a unique mild solution to PIDE (21) satisfying .

4.2. Maximal monotone operator technique for solving nonlinear parabolic equations

This section presents the existence and uniqueness results of a fully nonlinear parabolic equation using the monotone operator technique. We consider the HJB equation arising from portfolio optimization selection, where the goal is to maximize the conditional expected value of the terminal utility of the portfolio. Such a fully nonlinear HJB equation presented in an abstract setting can be viewed as a PIDE in some sense. First, we employ the so-called Riccati transformation method to transform the fully nonlinear HJB equation into a quasilinear parabolic equation, which can be viewed as the porous media type of equation with source term. Then, we showed that the underlying operator is maximally monotone in some Sobolev spaces. Next, we employed the Banach’s fixed point theorem and Fourier transform technique to obtain the existence and uniqueness of a solution to the general form of the transformed parabolic equation in an abstract setting in high-dimensional spaces. Furthermore, as a crucial requirement for solving the Cauchy problem, we obtain that the diffusion function to the quasilinear parabolic equation is globally Lipschitz continuous under some assumptions.

We consider the Cauchy problem for the nonlinear parabolic PDE of the following form:

| (24) | |||

| (25) |

where . The solution to such a nonlinear parabolic equation is established in some Sobolev spaces in high-dimensional spaces (see, [66]). To achieve such results, we assumed that the diffusion function is globally Lipschitz continuous and strictly increasing in the -variable. An example of such a Lipschitz continuous function is the value function of the following parametric optimization problem:

| (26) |

where and are given functions, and is a compact decision set. The properties of the value function depend on the structure of the decision set . It is smooth if is a convex set; meanwhile, it can only be smooth if is not connected.

4.2.1. Existence and uniqueness of a solution to the Cauchy problem

First, we define our underlying function spaces. Let be a Gelfand triple, where

is a Hilbert space endowed with the inner product . The Banach spaces and are defined as follows:

where the Sobolev spaces are defined by means of the Fourier transform

endowed with the norm , and . Let the linear operator be defined as follows:

It is worth nothing that the operator is self-adjoint in the Hilbert space with the following Fourier transform representation:

The fractional powers of is defined by . In particular,

and is a self-adjoint operator in the Hilbert space . Moreover, .

In the sequel, we denote the duality pairing between the spaces and by , i.e., the value of a functional at is denoted by . We have the following definitions.

Definition 5.

Theorem 3.

[7, 63] Let be a separable reflexive Banach space, dense, and continuous in a Hilbert space , which is identified with its dual, so . Let and set Assume a family of operators , is given such that

-

(i)

for each , the function is measurable,

-

(ii)

for a.e , the operator is monotone, hemicontinuous, and bounded by where ,

-

(iii)

and there exists such that

Then, for each and , there exists a unique solution of the Cauchy problem

Consider the spaces , , and , i.e., . Thus, we have that these spaces satify the Gelfand triple, i.e., , where is a Hilbert space endowed with the norm

For a given value , we denote .

Theorem 4.

[66, Theorem 2] Assume that the above settings on and hold. Let be globally Lipschitz continuous functions. Suppose is such that there exist constants such that , , for a.e. and . Then, for any there exists a unique solution of the Cauchy problem

| (27) |

We remark here that the above result and its proof are contained in our recent paper [66, Theorem 2].

P r o o f: Recall that and , its dual space being . Let the scalar products in and be respectively defined by

Let us define the operator by

Therefore, we conclude that the mapping maps into under the assumption made on the function . Indeed, if and , then , and so

Thus, . Since , we have

because . Consequently, , as claimed.

Next, we show that the operator is monotone in the space . According to (76), we have , for any .

This implies that the operator is strongly monotone.

For a given , we have , where , because are globally Lipschitz continuous, , and the operator maps into . The hemicontinuity, boundedness, and coercivity of the operator follow from the assumption that the function is globally Lipschitz continuous and strictly increasing.

Applying Theorem 3, we deduce the existence of a solution such that

| (28) |

where . Next, we multiply (28) by to obtain

| (29) |

where . For , we denote . The Fourier transform of is defined by

Let be the Lipschitz constant of the mappings . Using Parseval’s identity and Lipschitz continuity of in , we obtain, for ,

where . Hence, we obtain

| (30) |

Suppose are such that and Here, the map is defined by where is a solution to the Cauchy problem

Letting , we obtain

| (31) |

Next, multiplying (31) by and taking the scalar product in the space , we obtain

| (32) | |||||

Using (30) and the fact that is self-adjoint in , then (32) gives

This implies

Then, integrating on a small time interval from to and noting that , we obtain

Taking the maximum over and using the fact that for any , we obtain

Using the Cauchy–Schwartz inequality, we obtain This implies that

Thus, for sufficiently small value of such that , the operator is a contraction on the space . Therefore, by the Banach fixed point theorem, has a unique fixed point in . It is worth noting that and are given such that they are independent of . If is arbitrary, then we can apply a simple continuation argument. In other words, if the solution exists in interval with , then starting from the initial condition , we can continue the solution from the interval over the interval . Continuing in this manner, we obtain the existence and uniqueness of a solution defined on the time interval .

Finally, the solution belongs to the space because the right-hand side, i.e., the function belongs to . Applying Theorem 3 we conclude , as claimed.

The following result demonstrates the absolute continuity and a-priori energy estimate property of the solution. Based on the assumption of the previous theorem, we have . Here, the space is endowed with the norm

Again, the following result and its are contained in our recent paper [66, Theorem 3].

Theorem 5.

Proof.

Since , where and , then . Therefore, for each , we have , where is the Banach space . According to [63, Proposition 1.2], we have . Hence, the unique solution to the Cauchy problem (4) belongs to the space , as claimed.

Next, we show that the unique solution satisfies a-priori energy estimate (33). Let be a unique solution to the Cauchy problem (27). Multiply (29) by and take the scalar product in to obtain

| (34) |

Using the Lipschitz continuity of , and strong monotonicity of , we obtain

Hence, there exist constants such that

Solving the differential inequality , where and , we obtain

and the proof of the Theorem follows. ∎

5. Applications to Option Pricing

The classical linear Black–Scholes model and its multidimensional generalizations have been widely used in the financial market analysis. It is well-known that the price of an option on an underlying asset price at time can be obtained as a solution to the linear Black–Scholes parabolic equation of the form (1). Generally, th underlying asset price is assumed to follow the geometric Brownian motion . Here, is the standard Wiener process. The terminal condition represents the payoff diagram at maturity , (call option case) or (put option case).

For the multidimensional case, where the option price depends on the vector of underlying stochastic assets with the volatilities and mutual correlations , the Black–Scholes pricing equation can be expressed as follows:

| (35) |

Equations (1) and (35) can be transformed into equation (4.) defined on the whole space (c.f., Ševčovič, Stehlíková, Mikula [59, Chapter 4, Section 5]).

According to stock markets observations, the models (1) and (35) were derived under some restrictive assumptions, e.g., completeness and frictionless of the financial market, perfect replication of a portfolio and its liquidity, and absence of transaction costs. However, these assumptions are often violated in financial markets. In the past few decades, several attempts have been made to investigate the effects of nontrivial transaction costs [41, 6, 42, 60]. For instance, Schönbucher and Willmott [55], Frey and Patie [25], Frey and Stremme [26] investigated the feedback and illiquid market effects due to large traders choosing given stock-trading strategies. Jandačka and Ševčovič recently investigated the effects of the risk arising from an unprotected portfolio. Barles and Soner [9] analyzed the option pricing models based on utility maximization. The common feature of these generalizations of the linear Black–Scholes equation (1) is that the constant volatility is replaced by a nonlinear function depending on the second derivative of the option price . Among these generalizations, Frey and Stremme [32] derived a nonlinear Black–Scholes model by assuming that the underlying asset dynamics takes into account the presence of feedback effects due to the influence of a large trader choosing particular stock-trading strategy (see also [55, 25, 27]).

Recently, Cruz and Ševčovič [20] generalized the Black–Scholes equation in two important directions. First, they employed the ideas of Frey and Stremme [32] to incorporate the effect of a large trader into the model. Second, they relaxed the assumption on liquidity of market by assuming that the underlying asset price follows a Lévy stochastic process with jumps to obtain the following nonlinear PIDE:

| (36) | |||||

where the shift function depends on the large investor stock-trading strategy function . Moreover, this shift function is a solution to the following implicit algebraic equation:

| (37) |

The large trader strategy function may depend on the derivative of the option price , e.g., . However, in our application, we assume the trading strategy function is prescribed and globally Hölder continuous. Next, we present the analysis of this equation depending the behavior of the parameter .

If , then . Thus, equation (36) can be reduced to a linear PIDE of the form (4.) in the one-dimensional space (). This is obtained using the standard transformation and setting .

However, if , then (36) can be transformed into a nonlinear parabolic PIDE. Indeed, suppose that the transformed large trader stock-trading strategy . Then, solves equation (36) if and only if the transformed function is a solution to the following nonlinear parabolic equation:

| (38) | |||||

. The shift function is a solution to the following algebraic equation:

| (39) |

and .

For small values of , we can construct the first order asymptotic expansion . For , we obtain . Hence,

Taking the first derivative of the above implicit equation with respect to and evaluating it at the origin , we obtain , i.e.,

| (40) |

Consequently, we obtain the following lemma.

Lemma 6.

[58, Lemma 1] Assume that the stock-trading strategy is a globally -Hölder continuous function, . Then, the transformed function is -Hölder continuous, and the first order asymptotic expansion of the nonlinear algebraic equation (39) is -Hölder continuous in all variables. Furthermore, there exists a constant such that for any .

5.1. Linearization of PIDE

In what follows, we consider a simplified linear approximation of (36) by setting in the diffusion function, but we keep the shift function depending on the parameter . Then, the transformed Cauchy problem for the solution with the first order approximation of the shift function is given as follows:

| (41) | |||||

, where .

Note that the call/put option payoff functions / do not belong to the Banach space . According to [19], the procedure on how to overcome this problem and formulate existence and uniqueness of a solution to the PIDE (41) is based on shifting the solution by . Here, is an explicitly given solution to the linear Black–Scholes equation without the PIDE part. In other words, solves the following linear parabolic equation:

| (42) |

Recall that (call option case), where (c.f., [41, 59]). Here, is the cumulative density function of the normal distribution. The next result and its proof are based on the recent paper by Ševčovič and Udeani [58]

Theorem 7.

[58, Theorem 2] Assume the transformed stock-trading strategy function is globally -Hölder continuous in both variables. Suppose that is a Lévy measure with the shape parameters , where either , or and . Let be the space of Bessel potentials space , where and . Let . Then, the linear PIDE (41) has a unique mild solution with the property that the difference belongs to the space .

Proof.

We first outline the idea of the proof. The initial condition because of two reasons. It is not smooth for , and it grows exponentially for (call option) or (put option). The shift function satisfies , and so the initial condition belongs to . However, the shift function enters the governing PIDE as it includes the term in the right-hand side. Since is not sufficiently smooth for , the shift term is singular for . Following the ideas of [19], for the shift term , we can provide Hölder estimates, which are sufficient for proving the main result of this theorem (c.f., [19, Lemma 4.1]). Furthermore, the exponential growth of the function will be overcome since , where , i.e.,

Next, we present more details of the proof. The function solves the linear PDE (42). Thus, the difference of the solution to (41) and satisfies the PIDE with the right-hand side:

. Here , and . According to Proposition 2, is a bounded linear mapping. Consequently, it is Lipschitz continuous, provided that and . Clearly, . Hence,

Now, it follows from [19, Lemma 4.1] that the following estimate holds true:

for any . The function is -Hölder continuous because . Moreover,

because . Recall that the crucial part of the proof of [19, Lemma 4.1] was based on the estimates:

where . This estimate is satisfied because of Proposition 2 under the assumptions made on . The proof for the case of a put option is similar. The final estimate on the Hölder continuity of the mapping follows from careful estimates of the solution derived in the proof of [19, Lemma 4.1]. Now, the proof follows from Theorem 2 and Proposition 3. ∎

6. Feedback effects under jump-diffusion asset price dynamics

Suppose that a large trader uses a stock-holding strategy and is a cadlag process (right continuous with limits to the left). In what follows, we will identify with . We assume has the following dynamics:

| (43) |

which can seen as a perturbation of the classical jump-diffusion model. For instance, if a large trader does not trade, then or the market liquidity parameter is set to zero, then the stock price follows the classical jump-diffusion model.

We will assume the following structural hypothesis in this chapter:

Assumption 1.

[, Assumption 1] Assume the trading strategy and the parameter satisfy , where .

Next, we show an explicit formula for the dynamics of satisfying (43) under certain regularity assumptions made on the stock-holding function .

Proposition 4.

Proof.

First, the SDE (44) can be expressed for as follows:

Since the function is smooth, by applying Itô formula (1) to the process , we obtain

Substituting the differential into (43), we obtain

Next, rearrange terms in (6.) to obtain

| (50) | |||

By comparing terms in (44) and (50), we obtain the expressions (45), (46), and the implicit equation for the function :

| (51) | |||||

Simplifying this expression for , we establish (47), as claimed. ∎

Since the function is given implicitly by equation (47), we can expand its solution in terms of a small parameter as follows:

to deduce the following proposition:

Proposition 5.

Assume is sufficiently small. Then, the first-order approximation of the function is given as follows:

| (52) |

The next proposition and its proof is based on the recent paper by Cruz and Ševčovič [20].

Proposition 6.

[20, Proposition 3.4] Assume that the asset price process satisfies SDE (44), where the Lévy measure is such that . Let the price of a derivative security be define by

| (53) |

Suppose that the payoff function is Lipschitz continuous and the function has a bounded derivative. Then, is a solution to the PIDE of the form:

| (54) |

where and are given by and , respectively.

Proof.

Recall that the asset price dynamics of under the measure is given by

| (55) |

Applying the Itô’s lemma to , we obtain , where

and

Our aim is to show that is a martingale. Consequently, we have a.s., and is a solution to (54) ([17, Proposition 8.9]). To show that the term is a martingale, it is suffices to show that

| (56) |

Since , and the payoff function is Lipschitz continuous, is Lipschitz continuous with the Lipschitz constant . Moreover, since the function has bounded derivatives, we have

(see Assumption 1). Since , we obtain . Again, since is Lipschitz continuous with the Lipschitz constant , we have

since . Here, because of the assumptions made on the measure . Next, we show that is a martingale. Since is bounded, we have

Therefore, because is a martingale. Thus, is also a martingale, and . Hence, is a solution to PIDE (54), as claimed. ∎

Remark 3.

If , then . Moreover, equation (54) becomes

| (57) |

which is the well-known classical PIDE. If there are no jumps () and a trader follows the delta hedging strategy, i.e., , then equation (54) reduces to the Frey–Stremme option pricing model:

| (58) |

(c.f. [27]). Finally, if and , equation (54) reduces to the classical linear Black–Scholes equation.

For simplicity, we assume the interest rate is zero, i.e., . Then, the function is a solution to the following PIDE:

| (59) | |||||

Next, let the tracking error of a trading strategy be . By applying Itô’s formula to and using , we obtain

Using expression (55) for the dynamics of the asset price (with ), the tracking error can be expressed as follows:

Remark 4.

For the delta hedging strategy , the tracking error function can be expressed as follows:

It is obvious that the tracking error for the delta hedging strategy need not be zero for .

The next proposition presents a criterion that can be used to find the optimal hedging strategy. The proposition and its proof is based on the recent paper by Cruz and Ševčovič [20].

Proposition 7.

[20, Proposition 3.5] The trading strategy of a large trader minimizing the variance of the tracking error is given by the implicit equation:

| (61) | |||||

where and .

Proof.

Remark 5.

It is worth noting that the optimal trading strategy minimizing the variance of the tracking error need not satisfy the structural Assumption 1. For instance, if , then the tracking error minimizer is the delta hedging strategy . For a call or put option, its gamma, i.e., , becomes infinite as and . However, given a level , we can minimize the tracking error under the additional constraint . In other words, we can solve the following convex constrained nonlinear optimization problem

instead of the unconstrained minimization problem proposed in Proposition 7.

Remark 6.

Note that if and , the trading strategy reduces to the Black–Scholes delta hedging strategy, i.e., . Meanwhile, if and , then the optimal trading strategy becomes , where

where .

We conclude this section with the following proposition providing the first-order approximation of the tracking error minimizing trading strategy for small values of the parameter . In what follows, we derive the first-order approximation of as as . Clearly, the first-order Taylor expansion of the volatility function is given by

According to Proposition 5 (see (52)), we have , where

| (62) |

The function can be expanded as follows: ,

| (63) | |||||

Using the first-order expansions of the functions , and , we obtain the following results.

Proposition 8.

6.1. Numerical simulation for the underlying PIDE

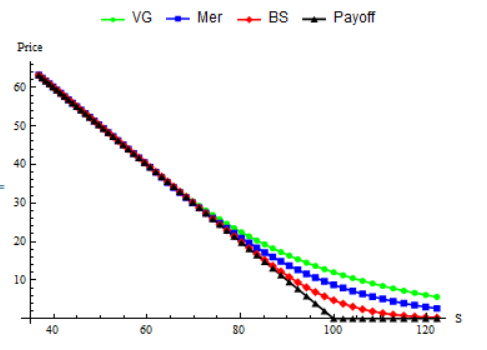

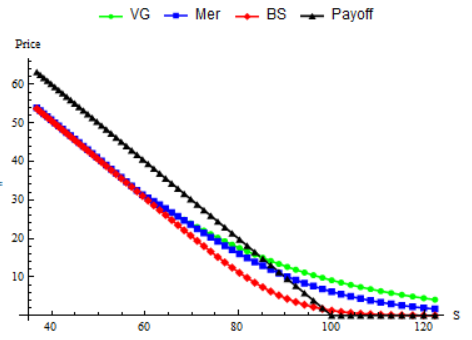

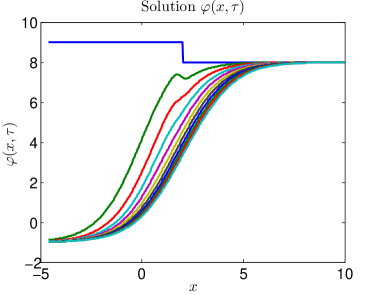

In this section, we illustrate the behavior of the solutions to the linear PIDE with various Lévy measures. Specifically, we consider European put options, i.e., . The goal of the numerical simulation is to compare the solution to the linear Black–Scholes equation with solutions to the Merton and variance gamma PIDE models. The common model parameters were chosen as follows: , and . For the underlying Lévy process, we consider the variance gamma process with parameters and the Merton processes with parameters , , and . First, we employ the finite difference discretization scheme proposed and analyzed by Cruz and Ševčovič [20] to calculate the numerical solution to the equation. Their scheme is based on a uniform spatial finite difference discretization with a spatial step , and implicit time discretization with a step . Then, we set the total number of spatial discretization steps as and the number of time discretization steps as . We restricted the spatial computational domain to , where . For more details about the discretization scheme, see the recent paper by Cruz and Ševčovič [20].

Figure 6.1. shows the comparison of European put option prices between PIDE and linear Black–Scholes models. Figures 6.1. (a) and (b) show the plots of put option prices for for the interest rates and , respectively. Table 6.1. summarizes the numerical values of option prices for two different values of the interest rate and . The option price for the Merton and variance gamma models are higher than that of the classical Black-Scholes model. This is based on the idea prices of put or call options should be higher on underlying assets following stochastic processes with jumps than those following a continuous geometric Brownian motion.

a) b)

| BS | PIDE-VG | PIDE-Merton | Payoff | ||||

|---|---|---|---|---|---|---|---|

| 85.2144 | 15.2547 | 7.35166 | 19.2687 | 14.9855 | 17.1692 | 12.9056 | 14.7856 |

| 88.692 | 12.2484 | 5.24145 | 17.2948 | 13.3899 | 14.8335 | 10.9901 | 11.308 |

| 92.3116 | 9.42895 | 3.51944 | 15.428 | 11.8822 | 12.6423 | 9.21922 | 7.68837 |

| 96.0789 | 6.90902 | 2.21106 | 13.674 | 10.4691 | 10.6201 | 7.61307 | 3.92106 |

| 100. | 4.78444 | 1.29196 | 12.0372 | 9.15576 | 8.78655 | 6.18483 | 0. |

| 104.081 | 3.1099 | 0.69843 | 10.52 | 7.94499 | 7.155 | 4.94044 | 0. |

| 108.329 | 1.88555 | 0.34773 | 9.12343 | 6.83762 | 5.73137 | 3.87864 | 0. |

| 112.75 | 1.0604 | 0.15881 | 7.84623 | 4.51403 | 5.83246 | 2.99166 | 0. |

7. Hamilton-Jacobi-Bellman equation

In this section, we present the motivation for studying the fully nonlinear parabolic equation (24), which can be viewed as a parabolic PIDE in some sense. We also present the relationship between the nonlinear parabolic equation and the transformed equation using the so-called Ricatti transform.

The motivation for studying the nonlinear parabolic equation of the form (24) arises from dynamic stochastic programming for . The fully nonlinear HJB equation describing optimal portfolio selection strategy is represented by the following nonlinear parabolic equation:

| (65) | |||

| (66) |

where . A solution to the parabolic equation (65) is subject to the terminal condition . According to Kilianová and Ševčovič [35, 34, 36], such HJB equation of the form (65) arises from the dynamic stochastic programming, where the goal of an investor is to maximize the conditional expected value of the terminal utility of the portfolio:

| (67) |

on a finite time horizon . Here, is an increasing terminal utility function, and is a given initial state condition of the process at . The underlying stochastic process with a drift and volatility is assumed to satisfy the following Itô’s SDE:

| (68) |

where the control process is adapted to the process , and is the standard one-dimensional Wiener process. The control parameter belongs to a given compact subset in . An example of such a subset is the compact convex simplex , where .

Consider the value function

| (69) |

Then, according to Bertsekas [11], the value function solves the fully nonlinear HJB parabolic equation (65) and .

Several attempts have been made for solving the HJB equation (65). Macová and Ševčovič [43] analyzed solutions to a fully nonlinear parabolic equation modeling the problem of optimal portfolio construction. Consequently, they formulated the problem of optimal stock to bond proportion in the management of a pension fund portfolio could be formulated in terms of the solutions to the HJB equation. Federicol et al. [23] investigated the utility maximization problem for an investment-consumption portfolio when the current utility depends on the wealth process, regularity of solutions to the HJB equation. They defined a dual problem and treated it by means of dynamic programming to show that the viscosity solutions of the associated HJB equation belong to a class of smooth function. Recently, Ishimura and Ševčovič [30] constructed and analyzed solutions to the class of HJB equation (65) with range bounds on the optimal response variable. They constructed monotone traveling wave solutions and identified parametric regions for which the traveling wave solutions have positive or negative wave speed. Abe and Ishimura [1] employed the Riccati transformation method for solving the full nonlinear HJB equations, which was later studied and generalized by Kilianová and Ševčovič [35]. They investigated solutions of a fully nonlinear HJB equation for a constrained dynamic stochastic optimal allocation problem. However, no attempt has been made in solving the fully nonlinear HJB parabolic equation arising from portfolio optimization in high-dimensional space using the monotone operator technique. The monotone operator method is essential because it does not only give constructive proof for existence theorems, but it also leads to various comparison results, which are effective tools for studying qualitative properties of solutions. In this chapter, we consider the case when the utility function is increasing, as a consequence, .

7.1. Static Markowitz model for portfolio optimization

This subsection presents the motivation for studying such nonlinear parabolic equation (65). It describes the mathematical formulation of the classical Markowitz model for portfolio optimization. In the static portfolio optimization, this model aims to maximize the mean return of the set of stochastic returns , under the constraint that variance of the portfolio is bounded by a given constant . Given a vector of weights, we construct a portfolio . Let be the vector of mean returns of stochastic asset returns and be their covariance matrix, , then , and the variance . The Markowitz optimal portfolio optimization problem can be formulated as the following convex optimization problem:

The corresponding Lagrange function for the minimization of has the following form:

| (70) |

where , and are Lagrange multipliers. It is worth noting that the same Lagrange function corresponds to the minimization problem:

provided the Lagrange multiplier is known and fixed. Figure 7.1. shows the optimal asset selection for German DAX30 stock index for various values of . The optimal value is denoted by . The value of the Lagrange multiplier can be viewed as a measure of investor’s risk-aversion (see Fig. 7.1.). Therefore, the higher the value of the risk aversion, the more portfolio is diversified among less risky assets with smaller mean returns.

7.2. Riccati transformation of the HJB equation and application to optimal portfolio selection problem

7.2.1. Riccati transformation

This section presents how the HJB equation (65) can be transformed into a quasilinear PDE using the so-called Ricatti transformation techniques. Such transformed parabolic equation correspond to the Cauchy problem (24), which is obtained after some pertubation in the main operator.

The Riccati transformation of the value function can be defined based on the approached introduced by Abe and Ishimura [1], Ishimura and Ševčovič [30], Ševčovič and Macová [43], and Kilianová and Ševčovič [35] as follows:

| (71) |

Suppose the value function is increasing in the -variable. In other words, assume that the terminal utility function is increasing. Then, the HJB equation (65) can be rewritten as follows:

| (72) |

where is the value function of the following parametric optimization problem:

| (73) |

Remark 7.

It is worth noting that the optimization problem (73) is related to the classical Markowitz model on optimal portfolio selection problem formulated as maximization of the mean return under the volatility constraint , i.e.,

where the decision set is the simplex . The Lagrange multiplier for the volatility constraint can be viewed as the parameter entering the parametric optimization problem (73).

Next, let be the total differential of the function , where , i.e.,

Here, and are partial derivatives of with respect to - and - variables, respectively.

Kilianová and Ševčovič [34, Theorem 4.2] recently established the relationship between the transformed function and the value function . The reported that an increasing value function in the -variable is a solution to the HJB equation (65) if and only if the transformed function , is a solution to the Cauchy problem for the quasilinear parabolic PDE:

| (74) | |||

| (75) |

Note that the Cauchy problem for the quasilinear parabolic PDE (74) is equivalent to the nonlinear parabolic equation (24) in one-dimensional space. This is obtainable after some shift/perturbation in the main operator of the transformed equation (74). This nonlinear parabolic equation (24) presented in an abstract setting can be viewed as nonlinear PIDE in some sense.

7.2.2. Properties of the value function as a diffusion function

In this subsection, we presents the qualitative properties of the value function and sufficient conditions on the decision set and functions and that guarantee higher smoothness of the value function . Let be the space consisting of all -differentiable functions defined on the domain , whose -th derivative is globally Lipschitz continuous. The next proposition shows (under certain assumptions) that the value function belongs to , where . The following proposition and its proof are contained in our recent paper ([66, Theorem 3]).

Proposition 9.

[66, Proposition 1] Let be a given compact decision set. Assume that the functions and are globally Lipschitz continuous in and variables and there exist positive constants such that for any , and .

Then, . Moreover, the function is strictly increasing, and

| (76) |

i.e., , and

| (77) |

for a.e., , where and , where .

Proof.

First, let , where . Then,

For any given , the function is globally Lipschitz continuous in all variables. Therefore, the minimal function is globally Lipschitz continuous. Moreover, the function satisfies the inequality (76) for any , and so does the minimal function .

Next, we prove inequality (77). Let such that , where is the standard normal vector, i.e., . Then, we have

Hence,

We note that so that . Taking minimum over , we obtain

By exchanging the role of and and taking the limit as , i.e., , we obtain inequality (77), as stated.

∎

According to Proposition 9, the value function given in (73) satisfies the assumptions of Theorem 4 provided that the functions

belong to the Banach space .

The next result was proved in [36]. It gives sufficient conditions imposed on the decision set and functions and that guarantee higher smoothness of the value function . Its proof is based on the classical envelope theorem due to Milgrom and Segal [48] and the result on the Lipschitz continuity of the minimizer belonging to a convex compact set according to Klatte [39].

Theorem 8.

[36, Theorem 1] Suppose that is a convex compact set and the functions and are smooth such that the objective function is strictly convex in the variable for any . Then, the function belongs to the space .

7.2.3. Point-wise a-priori estimates of solution with their existence and uniqueness

In this section, we present a-priori estimates on a solution to the Cauchy problem (74). We will assume that the function is independent of time , and is independent of and , i.e.,

Then, the value function is also independent of the variable. Next, we prove a-priori estimates for the transformed function defined as . Since the function is strictly increasing in the variable, there exists an inverse function such that . Therefore, the function is a solution to (74) if and only if the function is a solution to the following linear parabolic PDE:

where

Note that . Next, suppose that the function is bounded from above by a constant . Then, the function is a solution to the linear PDE:

where is nonpositive, i.e., for all . Let be a constant. Then, . We employ the maximum principle for parabolic equations on unbounded domains according to Meyer and Needham [46, Theorem 3.4] to obtain for all , provided that for all . In other words, is a subsolution. Similarly, if is a given constant, then and for all , provided that for all , i.e., is a supersolution. Consequently, we have the following implication:

In terms of the solution to the Cauchy problem (74)–(75), we obtain the following a-priori estimate:

| (78) |

where

| (79) |

Now, we can apply the general Theorem 4 on existence and uniqueness of a solution.

Theorem 9.

[66, Theorem 5] Let the decision set be compact and be an increasing utility function such that belongs to the space . Suppose that the drift and volatility function are continuous in the and variables and the value function given in (73) satisfies , where

Then, for any , there exists a unique solution to the Cauchy problem

| (80) |

satisfying .

Proof.

Since and is a compact set, there exist constants such that for all . It follows from Proposition 9 that

| (81) |

Since and , we obtain .

Now, let us define the shift diffusion function by . Note that . Then, equation (80) is equivalent to

where .

Next, let and . Here, is a suitable cutoff function

where . Then, the functions are globally Lipschitz continuous.

Note that the diffusion function satisfies the assumptions of Theorem 4 with . Now, applying Theorems 4 and 5, we obtain the existence and uniqueness of a solution to the Cauchy problem (27). The solution satisfies the point-wise estimate (78). Thus, , and is a solution to the Cauchy problem (80).

Finally, from (81), we deduce the estimate for the solution since , where . Moreover, , and

∎

7.2.4. Application to stochastic dynamic optimal portfolio selection problem

This subsection presents examples of the stochastic process (68). We also present examples of the corresponding utility function. For the the stochastic process (68), we can consider a portfolio optimization problem with regular cash inflow ()/outflow () to a portfolio representing pension funds savings. Here, we consider Slovak pension fund savings according to Kilianová and Ševčovič [35]). It is well-known that in a stylized financial market, the stochastic process driven by the stochastic differential equation

| (82) |

represents a stochastic evolution of the value of a synthetized portfolio consisting of -assets with weights , mean returns , and an positive definite covariance matrix , i.e., .

In this study, we assume that the value of the inflow/outflow rate also depends on the such that it is characterized by the following

where is a constant. It represents a realistic pension saving model in which there is no inflow/outflow provided that the value of the portfolio is very small. Based on the logarithmic transformation and Itô’s lemma, the stochastic process satisfies (68), where .

Recently, Kilianová and Trnovská [37] established a further generalization of the drift and volatility functions arising from the so-called worst-case portfolio optimization problem. In such case, the volatility function is given by

where is a bounded uncertainty convex set of positive definite covariance matrices. In general, only a part of the covariance matrix can be calculated precisely, whereas entries are not precisely determined. For instance, if only the diagonal is known, we have . Furthermore, the drift function is given by

where is a given bounded uncertainty convex set of mean returns.

Remark 8.

Consider a class of utility function characterized by a pair of exponential functions:

| (83) |

where and are given constants. Here, is a point at which the risk aversion changes. We observe that is an increasing function with a jump in the second derivative at the point .

If , then the utility function is called the decreasing absolute risk aversion (DARA) function, representing an investor with a non-constant decreasing risk aversion. It means that the higher the wealth of investors, the lower their risk aversion, and hence the higher exposition of the portfolio to more risky assets. According to Post, Fang and Kopa [53], the piece-wise exponential DARA utility function plays an essential role in the analysis of decreasing absolute risk aversion stochastic dominance introduced by Vickson [67] (see also [34]). It is worth noting that the coefficients of absolute risk aversion of the above utility functions is equal to if or to if .

The piece-wise constant function should be truncated outside of some interval , where is large enough. Then, . Therefore, the underlying utility function is modified by linear functions for and .

Another simple example of a convex-concave utility function is the function . Then, . Clearly, . It is worth noting that the individual’s reduction in marginal utility arising from a loss is absolutely greater than the marginal utility from a financial gain. In the domain of gain (), the utility function is concave, indicating that investors show risk aversion in this domain. In contrast, investors become risk-seeker when dealing with losses, i.e., the utility function is convex for .

7.2.5. Numerical examples

This subsection presents examples of the value function to the parametric optimization problem with different decision sets. First, we consider a simple decision set , where is a positive definite covariance matrix, and is a positive vector of mean return. The value function can be explicitly expressed as follows:

Here, is the maximal interval where the optimal value of the function is strictly positive () for , and , , are constants explicitly depending on the covariance matrix and the vector of mean return such that the function is continuous at , i.e., and . It is clear that is only continuous function with two points of discontinuity of the second derivative .

Furthermore, consider a decision set consisting of finite number of points. Then, the value function corresponding to such decision set is only piece-wise linear. In other words, if , then , where is a linear function with the slope and intercept .

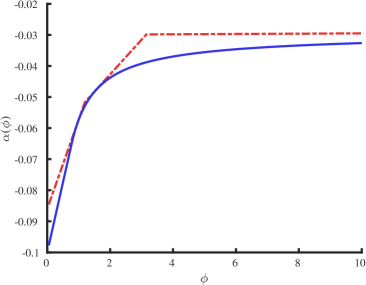

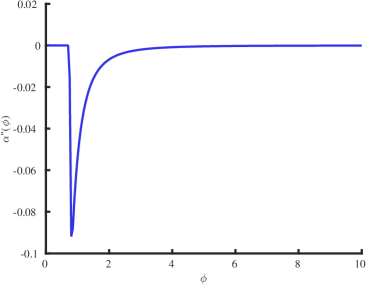

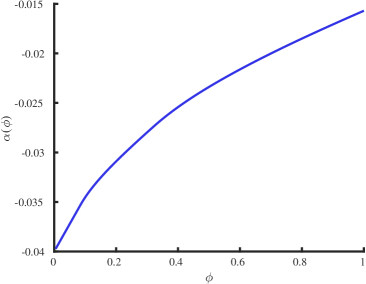

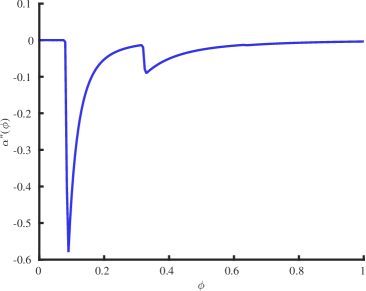

Figure 7.2.5. a) shows the graph of the value function corresponding to the Slovak pension fund system with the two types of decision sets. According to the data-set obtained from [38], the portfolio consists of the stock index (with a high mean return and high volatility ) and bonds (with mean return and very low volatility ). The returns on stocks index and bonds are negatively correlated . . Then . As shown in Figure 7.2.5. a), the solid blue line corresponds to the convex compact decision set . The piece-wise linear value function (dotted red line) corresponds to the discrete decision set . It represents the Slovak pension fund system consisting of three funds: growth funds with (80% of stocks and 20% of bonds), balanced funds with (equal proportion of stocks and bonds), and conservative funds with (only bonds) (c.f. [38]). Figure 7.2.5. b) shows the graph of the second derivative of the value function corresponding to the convex compact decision set . It has the first point of discontinuity close to the value 2. For , the number of discontinuities of increases (c.f. [35]). Figure 7.2.5. shows another example of the value function and its second derivative for the portfolio consisting of five stocks (BASF, Bayer, Degussa-Huls, FMC, and Schering) entering DAX30 German stocks index. The covariance matrix is taken from [21]. We set the vector of yields .

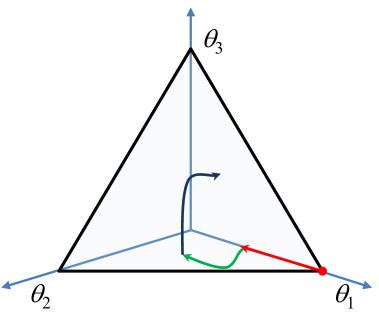

The minimizer of the convex optimization problem

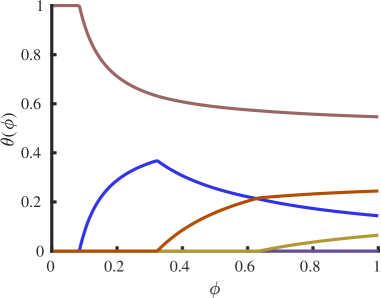

when considered as a function of the risk aversion parameter is only Lipschitz continuous in . According to Millgrom–Segal envelope theorem, the derivative is given by . Figure 7.2.5. shows the path as a function of when increasing from to . For small values of , only one asset with maximal mean return is active, i.e., . For intermediate values of , two assets are active . Moreover, for larger values of , all three assets are active, i.e., . The path has a discontinuity in the first derivative when it leaves lower dimensional object (vertex, edge) enter a higher-dimensional object volume.

a) b)

a) b)

The advantage of the Riccati transformation of the original HJB is twofold. First, the diffusion function can be computed in advance as a result of quadratic optimization problem when the vector and the covariance matrix are given or semidefinite programming problem when they belong to a uncertainity set of returns and covariance matrices (c.f. [37]). Figure 7.2.5. shows the vector of optimal weights , as a function of the parameter , obtained as the optimal solution to the quadratic optimization problem with the covariance matrix from [21] corresponding to the five assets (BASF, Bayer, Degussa–Huls, FMC, Scheringfrom) entering DAX30 index from 2008. There are more nontrivial weights when the parameter increases.