Chen, Lyu, Wang and Zhou

NRM with Demand Learning and Fair Resource-Consumption Balancing

Network Revenue Management with Demand Learning and Fair Resource-Consumption Balancing

Xi Chen111Author names listed in alphabetical order. \AFFLeonard N. Stern School of Business, New York University, New York, NY 10012, USA, \EMAILxc13@stern.nyu.edu \AUTHORJiameng Lyu111Author names listed in alphabetical order.222Corresponding authors. \AFFDepartment of Mathematical Sciences, Tsinghua University, Beijing 100084, China, \EMAILlvjm21@mails.tsinghua.edu.cn \AUTHORYining Wang111Author names listed in alphabetical order. \AFFNaveen Jindal School of Management, University of Texas at Dallas, Richardson, TX 75080, USA, \EMAILyining.wang@utdallas.edu \AUTHORYuan Zhou111Author names listed in alphabetical order.222Corresponding authors. \AFFYau Mathematical Sciences Center & Department of Mathematical Sciences, Tsinghua University, Beijing 100084, China, \EMAILyuan-zhou@tsinghua.edu.cn

In addition to maximizing the total revenue, decision-makers in lots of industries would like to guarantee balanced consumption across different resources. For instance, in the retailing industry, ensuring a balanced consumption of resources from different suppliers enhances fairness and helps maintain a healthy channel relationship; in the cloud computing industry, resource-consumption balance helps increase customer satisfaction and reduce operational costs. Motivated by these practical needs, this paper studies the price-based network revenue management (NRM) problem with both demand learning and fair resource-consumption balancing. We introduce the regularized revenue, i.e., the total revenue with a balancing regularization, as our objective to incorporate fair resource-consumption balancing into the revenue maximization goal. We propose a primal-dual-type online policy with the Upper-Confidence-Bound (UCB) demand learning method to maximize the regularized revenue. We adopt several innovative techniques to make our algorithm a unified and computationally efficient framework for the continuous price set and a wide class of balancing regularizers. Our algorithm achieves a worst-case regret of , where denotes the number of products and denotes the number of time periods. Numerical experiments in a few NRM examples demonstrate the effectiveness of our algorithm in simultaneously achieving revenue maximization and fair resource-consumption balancing.

network revenue management, demand learning, resource-consumption balancing, fairness, regret analysis, linear bandit

1 Introduction

Network revenue management, as a fundamental and important model in revenue management, has been successfully applied in lots of industries, such as online retailing, airline, hotel (Talluri et al. 2004, Klein et al. 2020). Classical research on NRM aims to maximize the total revenue over time periods under resource constraints assuming the demand function is known. See, for example, the seminal works of Gallego and Van Ryzin (1997), Jasin (2014), Maglaras and Meissner (2006).

In practice, there are two main challenges in adopting NRM models. First, the demand function in NRM is usually unknown, which needs to be learned on the fly. Second, in addition to maximizing the total revenue, many decision-makers would like to guarantee balanced consumption across different resources.

In various network revenue management applications, resource-consumption balancing may achieve multiple benefits such as fairness in channel relationships, customer satisfaction enhancement, and operational cost reduction. Let us provide two examples to illustrate the importance of resource-consumption balancing as follows.

Retailing Industry: In an NRM model for the retailing industry, a retailer decides prices for products and each product consumes several types of resources. Different resources are provided by different suppliers, and it is also possible that one supplier could provide more than one type of resource. If one supplier terminates the cooperation, certain products may no longer be able to be produced. Therefore, to maximize long-term revenue and guarantee no product is out of stock, the retailer should keep long-term good cooperation with different resource suppliers. Extensive research in the fields of economics and marketing has consistently revealed the significant role of fairness in the development and sustenance of channel relationships between suppliers and retailers (Corsten and Kumar 2005, Haitao Cui et al. 2007). To this end, it is essential for retailers to ensure profit fairness across different suppliers. Indeed, only paying attention to revenue maximization may cause an “unfair” scenario in which some suppliers earn a lot but the shares of others are small, subsequently leading to a higher probability of these under-used resource suppliers to withdraw from cooperation. Suppose the profit expectations of different suppliers are the same,111To address the issue of different profit expectations among suppliers while maintaining profit fairness, the retailer could introduce a weighting mechanism that adjusts resource-consumption balancing based on each supplier’s profit expectations or earnings per demand (please refer to the weighting mechanism in Section 2.1 for details). resource-consumption balancing could enhance profit fairness among suppliers in the channel relationship, and consequently help maintain a good collaboration between retailers and suppliers. Moreover, over-reliance on certain suppliers creates a precarious dependency, since if some of these suppliers were to withdraw from the partnership, the retailer would face severe revenue loss and supply disruptions. In this way, resource-consumption balancing ensures that the retailer is not overly reliant on a few suppliers, reducing the risk of severe revenue loss and supply disruptions due to supplier withdrawal.

Cloud Computing Industry: In an NRM model for the cloud computing industry, the firm needs to make decisions on the prices of products (e.g., Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS), or specialized services like data storage, machine learning, or database management) subject to resource constraints (e.g., the capacity constraints of servers, virtual machines, data centers, storage systems, network bandwidth, and other computing resources). Designing an algorithm solely focused on profit maximization over a specific time period, without considering the balanced consumption of different resources, can have several potential consequences. From the perspective of customer satisfaction, overutilization of certain resources can lead to saturation and bottlenecks, resulting in poor service quality, slower response times, inconsistent performance, and limited flexibility for customers. Even if the firm achieves short-term maximum profit, dissatisfied customers may seek alternative providers or express their dissatisfaction, leading to customer churn and potential long-term revenue loss. From the perspective of operational cost and efficiency, neglecting resource consumption balance can lead to some resources being heavily utilized and quickly depleted, while others remain underutilized. Overloaded resources may require more frequent maintenance or replacement due to excessive usage, resulting in higher operational costs. Additionally, managing and maintaining imbalanced resource consumption simultaneously becomes more challenging, reducing overall operational efficiency. It seems that optimizing the capacity of different resources can be another way to solve the above issues. However, frequently scaling up or down to optimize capacities to match rapid shifts in demand and resource requirements might not be feasible and practical, since adjusting capacities in could computing industries can be a time-consuming and costly process and might lead to service disruptions. In contrast, resource-consumption balancing could increase customer satisfaction and reduce operational costs, which in turn contributes to long-term profitability and business growth, in a more convenient way.

As shown in the above examples, the resource-consumption balancing objective is often measured in the sense of the whole selling season and cannot be decomposed as an additive objective at each time period. In this paper, we adopt several different metrics that are applied to the average resource consumption vector to measure its balancing level. For example, the balancing level on resource consumption could be measured by the minimum element of the average resource consumption vector, which is the famous max-min fairness metric extensively studied in economics and resource allocation literature, also included as a special case of the weighted max-min fairness metric studied in this paper. In some cases, it may also be desirable to consume the resources at similar rates, which can be incentivized by our range fairness metric. In addition to the above two examples, we propose several more practically useful balancing metrics. We further identify a wide class of balancing metrics (including all the above examples) with quite mild assumptions. All the balancing metrics in the class can be incorporated into our learning and doing framework. Please refer to Section 2.1 for more details.

The main contribution of this paper is a dynamic pricing algorithm that simultaneously learns the unknown demand function and optimizes the composite objective concerning both the NRM revenue and the balancing metric. For any balancing metric included in the class mentioned above, our algorithm achieves a regret at most (where is the number of products and is the selling horizon, see Theorem 6.1 for more details). Below we discuss the various technical challenges and our contributions that overcome them in detail.

1.1 Main technical challenges

There are several technical challenges to tackle for the NRM problem with resource-consumption balancing and demand learning. First, the balancing metrics are all applied to the average resource consumption vector, which is a global objective calculated across all time periods. There is also a global unreplenishable inventory constraint for the resources. The global objective and constraint are usually difficult for sequential decision making problems since the decisions at each time step have to be well coordinated to jointly optimize the balancing metric and satisfy the inventory constraint. Second, the problem becomes even harder when the demand function is unknown to the retailer and the retailer has to balance the exploration vs. exploitation trade-off with only learned information or estimated demand. Here, “exploration” means that the retailer needs to explore different prices in order to learn the unknown demand function on the run, and “exploitation” means that the retailer needs to exploit the near-optimal price to simultaneously gain revenue and achieve the global balancing objective. Finally, we aim at designing a computationally efficient algorithm (i.e., that runs in polynomial time) to minimize the regret (i.e., the cost of learning and sequential decision making) about the revenue and the balancing metric.

Compared with the work of Balseiro et al. (2021), the fact that demand curves are unknown in our problem leads to several specific technical hurdles that require novel solutions. In particular, we have the following challenges:

-

1.

In Balseiro et al. (2021), the dual problem is unconstrained, leading to complex dual space shapes and unbounded penalty vectors. This causes two problems: first, with dual spaces having complex shapes, the dual update steps may not have closed forms or be solved efficiently for general balancing-induced penalty functions. More importantly, with penalty vectors being unbounded the regret of the problem becomes unbounded as well because of the uncertainty exhibited in the estimated demand functions, rendering bandit learning algorithms impractical.

-

2.

With uncertainty quantified in the estimated demand functions, solving the primal update steps becomes computationally intractable as the objective functions are not necessarily concave anymore. Novel algorithms and analysis are required to solve such non-concave problems efficiently and rigorously.

1.2 Our contributions

We are able to address the above challenges with several technical innovations. At a higher level, our algorithm combines the primal-dual-type online policy proposed by Balseiro et al. (2021) with the Upper-Confidence-Bound (UCB) method, where the former solves the regularized online allocation problem with the known demand function and the latter is a widely adopted principle to balance the exploration and exploitation trade-off in many online learning algorithms. However, this combination is not black-box style and we make novel technical contributions in the design and analysis of our algorithm. Moreover, we also introduce new algorithmic ingredients to make sure that our algorithm is computationally efficient. In contrast, most of the online learning algorithms for linear demand models in the revenue management literature do not guarantee a polynomial time complexity, especially in the multi-product case. Below, we describe our main technical contributions in more detail.

First, instead of using the UCB of the objective function in the usual online learning and decision making algorithms, we make decisions according to the UCB of the specially designed adjusted revenue function. While our adjusted revenue function involves the revenue, it does not directly include the balancing metric (as it is not obvious how to decompose such a global metric to each individual time period, as discussed previously). Instead, we include a carefully designed term in the adjusted revenue function to relate it to the dual variable. This term, together with our update rule of the dual variable, helps optimize the balancing metric in a global fashion and reflects the inventory constraint at the same time.

Second, to control the estimation error of the adjusted reward during learning, we need to design a bounded domain for the dual parameter (i.e., the dual space). In contrast, Balseiro et al. (2021) adopt an unbounded dual space which is unfriendly to the analysis of our learning process, as illustrated in the first bullet point in the previous section. By adopting a bounded domain for the dual parameter, we are able to upper bound the estimation errors as well, leading to a correct regret rate. An additional benefit of our new dual space is that due to its simpler shape, we are able to employ a closed-form dual update rule (Algorithm 2, Section 5) for any balancing metric. In contrast, Balseiro et al. (2021) may only achieve this for selected balancing metrics and the dual update in our algorithm is much simplified.

Third, the regret analysis (especially the analysis related to the dual variable) greatly relies on the magnitude of our model parameter estimations. While the natural (regularized) least-squares estimator may not provide the desired bound, we employ an additional convex program to compute a set of bounded model estimates. This program is also helpful to guarantee the concavity of the estimated (adjusted) revenue function so that we may computationally efficiently find its maximum point which crucially connects to the decision we will make at each time step.

Finally, to achieve computational efficiency, we adopt an -norm confidence radius instead of the usual -norm confidence radius when computing the Upper Confidence Bounds so that we are able to maximize the UCB of the adjusted revenue function in polynomial time. Also, by reducing the program to a linear program with infinitely many constraints, we design a polynomial-time separation oracle and invoke the Ellipsoid method to efficiently solve the program. Both ingredients help our algorithm to achieve the polynomial time complexity that addresses the second bullet point of technical challenges mentioned in the previous section.

1.3 Related Works

In this section, we introduce three streams of literature related to our paper: network revenue management (NRM) with a known demand function, revenue management (RM) with demand learning, and fairness and resource-consumption balancing in operations management. And we discuss how our paper is appropriately placed into contemporary literature by giving comparisons with closely-related existing works.

NRM with known demand function. A large body of the price-based network revenue management literature focuses on the case in which the seller knows the underlying demand function in advance. And it is known that the optimal pricing policy of this case can be computed using dynamic programming (DP). However, the well-known curse of dimensionality of DP makes the optimal pricing policy computationally intractable. As a result, many works in the literature have investigated developing algorithms that are computationally efficient with a superior revenue performance. The seminal work by Gallego and Van Ryzin (1994, 1997) proposed simple but powerful heuristics. Specifically, they solve the optimal price of the fluid approximation model which is a deterministic analog of the DP and choose a static price every time. And their approach achieves an regret. Jasin (2014) introduced an improvement to the static pricing policy by resolving the static price periodically according to the remaining inventory, and attained regret bound. Recently, Wang and Wang (2022) proved that the resolving heuristics can achieve regret as compared to the optimal policy of the DP.

RM with demand learning. There is a large body of literature focusing on the price-based revenue management with demand learning, which are either without inventory constraints (see, e.g., Den Boer (2014), Den Boer and Zwart (2014), Keskin and Zeevi (2014, 2017), Bu et al. (2022) and references therein) or with inventory constraints (see, e.g., Besbes and Zeevi (2009), Wang et al. (2014), Chen et al. (2014), Ferreira et al. (2018), Miao et al. (2021)). For dynamic pricing problems without inventory constraints, we refer the readers to Den Boer (2015) for a detailed review. For price-based revenue management problems with inventory constraints, there are two streams of literature, either considering the nonparametric demand model (Wang et al. 2014, Chen and Shi 2023, Chen et al. 2019, Miao and Wang 2021) or the parametric demand model (see discussion below). Since our paper considers a parametric demand function, we mainly investigate the literature on the revenue management problem with inventory constraints and the parametric model. There are three main approaches for tackling the learning-while-doing challenge.

The first approach is using the Explore-Then-Commit strategy, which separates the exploration phase and exploitation phases. This simple strategy has been widely used in online learning tasks, and Besbes and Zeevi (2009, 2012) and Chen et al. (2014) applied this strategy to the NRM problem and Chen et al. (2014) achieved regret assuming the strong concavity of the revenue function.

The second approach is using Thompson sampling to address the exploration-exploitation trade-off. Ferreira et al. (2018) introduced Thompson sampling into network revenue management and considered both the discrete price model and continuous price set with the linear demand model. They obtained a Bayesian regret instead of the worst-case regret. The most important step in their algorithm for the continuous price set is to solve a quadratic program, which is not guaranteed to be a convex problem and is not clear how to be solved efficiently.

The third approach is incorporating the Optimism in the Face of Uncertain principle into the primal-dual optimization framework. This approach is closely related to the Bandit-with-Knapsack (BwK) model (Badanidiyuru et al. 2018), which introduces global resource constraints into the multi-armed bandit. Agrawal and Devanur (2019) further generalized BwK to bandit with global convex constraints and concave objective. The work by Agrawal and Devanur (2016), which considered BwK in the linear bandit setting, can be applied to the NRM problem with the discrete price. However, in the continuous price setting, the regret and the running time will be exponentially dependent on the number of products due to the discretization procedure. Miao et al. (2021) considered the NRM problem with continuous price and generalized linear model. To tackle the high computational complexity due to the continuous price set, they designed a UCB solver to reduce the original optimization problem to the price optimization problem of an ordinary NRM problem by randomly sampling a vector on the unit sphere and using it to linearize the -norm-based UCB term. However, the price optimization problem might still be non-convex and difficult to solve despite this reduction.

Among the above three types of approaches, our work falls into the primal-dual category, which seems to be most proper to address (via the Lagrangian) both the global regularization and resource constraints in our problem. Our work is closely related to Agrawal and Devanur (2016) and Miao et al. (2021). However, there are several significant differences. First, the primal-dual framework in Agrawal and Devanur (2016) and Miao et al. (2021) do not consider the global regularization and their algorithms do not directly work in our setting. To simplify the global regularization, we introduce an auxiliary variable. With the regularization and the auxiliary variable, our algorithm adopts very different primal and dual updates, which requires a different analysis. For example, on the primal side, we need to update the auxiliary variable according to a maximization problem of the regularizer in each period and carefully handle the term of the auxiliary variable in the regret analysis. On the dual side, the update of the dual variable is also related to the auxiliary variable, which makes the choice of the stationary benchmark dual variables more involved. Second, as compared to the random sampling method in Miao et al. (2021) which sacrifices an factor as shown in Lemma EC.2.1 of their paper, we introduce the -norm-based UCB term (Section 4.2) which is not only simpler to calculate, but also only sacrifices an factor in the regret. In contrast, even without the balancing regularization, the regret of Miao et al. (2021) for the NRM problem is , about times our regret (as discussed above there is term due to the random sampling method; the another term due to their suboptimal self-normalized concentration inequality lemma). Third, we introduce a feasibility program (Section 4.1) to make sure the estimated revenue function is concave and computationally easy to optimize. We are able to combine the above new techniques to derive a computationally efficient low-regret learning-while-doing algorithm for the NRM problem with fair resource-consumption balancing.

Fairness and resource-consumption balancing in operations. With the development of data-driven algorithms in operations, there is a growing concern about discrimination and unfairness. As a result, the fairness issue has attracted a lot of attention in operations problem (Bonald et al. 2006, Ma et al. 2022b, Kallus and Zhou 2021, Kallus et al. 2022, Zhang et al. 2022, Cohen et al. 2021, 2022, Chen et al. 2021b)

There is a vast body of literature considering the fairness in online allocation problem with inventory constraints (with known demand models) (Elzayn et al. 2019, Ma et al. 2022b, Balseiro et al. 2021, Chen et al. 2021a), where the decision-maker must take an action upon each arriving request and generates a reward and the consumption of resources. Balseiro et al. (2021) and Ma et al. (2022a) considered revenue maximization and fair resource-consumption (or resource-allocation) balancing simultaneously in the online allocation problem by introducing a non-separable regularizer. Balseiro et al. (2021) emphasized the importance of resource-consumption balancing in online advertising (Miller 2015) and cloud computing industries (Al Nuaimi et al. 2012) to avoid saturation of certain resources and retain some free capacity to maintain flexibility. Zhang et al. (2023) studied the online allocation problem with two-side resource constraints, which can be seen as a novel way to achieve resource-consumption balancing. They also provided several real-life examples, such as the online orders assignment in e-commerce platforms and online advertising platforms (Zhang et al. 2020), where it is required to guarantee a certain amount of resource-consumption. Since our work is most related to (Balseiro et al. 2021), we have thoroughly discussed the technical differences in the introduction section above and we will present the comparison more concretely in Section 3. We also note that (Balseiro et al. 2021) works for the regularized NRM problem in a quantity-based setting, where the decision-maker must irrevocably accept or reject each arriving request given limited resources (a special case of the online allocation problem studied in their paper). In contrast, we study the NRM problem in the price-based setting where the decision-maker has to decide the prices that influence the demand and the demand has always to be met (as long as permitted by the resource constraints). To the best of our knowledge, our work is the first to consider the fairness objective in the price-based NRM problem.

1.4 Notations

The vectors throughout this paper are all column vectors. We denote the set by for any . For vectors , we use ( respectively) to denote ( respectively) for all . We use to denote the -th element of the vector . For and , we define the following norms: , , , and .

We use to denote the identity matrix of order . For , we define the following matrix norms: ( refers to the element in the -th row and -th column of matrix ), , and it is easy to obtain . For square matrix , we use to denote the largest eigenvalue of . For a symmetric matrix , we use to represent that is negative semi-definite. We use to denote the augmented matrix by adding to the right of the matrix as a new column.

We use the big- notation to denote that . We use to further omit the logarithmic dependency on , , and .

1.5 Organization

The remainder of this paper is organized as follows. In Section 2, we formulate our problem by introducing the model assumptions and the performance measure; we also give plenty of examples of the balancing regularizers to illustrate the potential guidance our paper might bring to the practical scenarios. In Section 3, we present our algorithm and discuss the high-level ideas of the algorithm design. Then we discuss reward and demand estimation (Section 4) and the design of the mirror descent solver (Section 5) in detail, which are two key building blocks of our algorithm. In Section 6, we present the main theorem that upper bounds the regret of our algorithm (the detailed proof of the main theorem is presented in Section 12 in E-Companion). To demonstrate the empirical performance of our policy, we conduct several numerical experiments and present the results in Section 7. In the end, we give a summary of our paper in Section 8. The proofs of most technical lemmas and the additional experimental results are included in the supplementary materials.

2 Model Description and Assumptions

In an NRM model with types of products and types of resources, a retailer sells types of products during a selling season with time periods. Each product is defined as a combination of types of unreplenishable resources by the consumption matrix , where means that selling one unit of the type- product consumes unit of the type- resource. At each time period , the retailer must determine the prices for the products, i.e., the price vector . The retailer then observes the consumer’s demand vector which is realized from an unknown underlying demand function , and finally consumes the resources according to the consumption matrix . The retailer needs to choose the prices during the selling season to accomplish the following 3 goals:

-

1.

to gradually learn the underline demand function from the observed demands,

-

2.

to maximize the total revenue based on the learned information and given the unreplenishable resource inventory,

-

3.

to balance the consumption of the different types of resources via maximizing the balancing regularizer , which will be defined soon.

More specifically, the initial inventory levels of the resources are . At the end of time , the inventory levels become for . For convenience, we also define the normalized inventory level , which is the average amount of resources that can be used at a time period.

For simplicity, we assume that the price range for each product is and the retailer has to choose in the price set at each time . The price set can either be or a discrete subset in . For brevity, we focus on the case , which is much more challenging. One can easily adapt our algorithm and analysis to the discrete price set.

The realized demand is a random variable centered at , i.e.,

where is a zero-mean noise variable (see Assumption 2.2 for the more precise statement). We consider the linear demand function (which is the most commonly analyzed demand model in literature, e.g., Keskin and Zeevi (2014) and Ferreira et al. (2018))

where and are the model parameters unknown to the retailer. For convenience, we also denote these unknown parameters by , where is the parameter space.

The revenue collected by the retailer at time is . We also denote the corresponding expected revenue by

The objective of the retailer is to design a policy with (where is the historical prices and demands before time ) to satisfy the inventory constraint for all and maximize the following expected total revenue plus the balancing regularizer on resource consumption:

Below in Section 2.1 we will discuss more about the regularizer ; in Section 2.2 we introduce some standard assumptions on the linear demand model and define the regret that our online policy aims to minimize.

2.1 Balancing Regularizer : Assumptions and Examples

The resource-consumption balance is measured by the regularizer (i.e., the regularizer function applied to the average resource consumption vector).

Throughout this paper, we impose the following assumptions on .

-

1.

is -Lipschitz continuous with respect to the -norm on its effective domain, i.e., for any .

-

2.

There exists such that for all .

-

3.

is concave.

In the following, we present several regularizers satisfying the above assumptions as examples (please refer to Section 10.2 in E-Companion for the detailed proof). We will use and refers to the average consumption of the type- resource.

Example 1: Weighted Max-min Fairness Regularizer. The first example is rooted in the famous max-min fairness guarantee (Nash Jr 1950), which has been well studied in the literature on static resources allocation (Bansal and Sviridenko 2006, Bertsimas et al. 2011). The idea behind the max-min fairness guarantee is to promote fairness by maximizing the minimum resource allocation. In our paper, we consider the following weighted max-min fairness regularizer to promote fair resource-consumption balancing. It is worth noting that the max-min regularizer in Balseiro et al. (2021) can be seen as a special case of our weighted max-min regularizer by setting the parameters correspondingly.

Formally, we define the weighted max-min fairness regularizer as , where is the parameter to balance between the total revenue goal and the balancing objective, and in the online retailing setting the parameter could be selected as the revenue of the resource supplier due to the consumption of one unit type resource and could also denote different profit expectations among suppliers.

Example 2: Group Max-min Fairness Regularizer. We may divide the different types of resources into groups and only focus on promoting the minimum consumption of each resource group. In practice, each supplier may provide several types of resources (which naturally forms a group) and the group max-min fairness would be useful if we wish to guarantee fairness among the suppliers.

Formally, we define the group max-min fairness regularizer as ,222In general, we may combine the grouping operation with any balancing regularizer satisfying the Assumption 2.1 to obtain a group version of the balancing regularizer, but for simplicity, we only present the group version of the weighted max-min regularizer here. where , is similarly defined as in Example 1, and is a - matrix describing the grouping scheme. In particular, we require that in each column there is exactly non-zero element and in each row there is at least non-zero element, where a simple example of is as follows,

In this example, there are two resource suppliers. The first supplier provides the type- and the type- resources and the second supplier provides the type- and the type- resources.

Example 3: Range Fairness Regularizer. Range is a fundamental statistical quantity that measures the difference between the highest and the lowest value of a population. The range fairness regularizer provides an incentive to minimize the range among the entries of the weighted average consumption vector .

Formally, we define the range fairness regularizer as , where is the range of and is introduced to guarantee the positiveness of the regularizer. When is chosen to be per-unit revenue of the type- resource supplier, the range fairness regularizer can be applied to promote revenue fairness across different suppliers; when , this regularizer can evaluate the evenness of resource availability and help to avoid the pre-mature saturation of a few resource types.

Example 4: Load Balancing Regularizer. We finally present the load-balancing regularizer proposed in Balseiro et al. (2021). The regularizer is defined as , which measures the minimum relative resource availability, and also helps to make sure that no resource is too demanded.

2.2 Model Assumptions and Performance Measure

Throughout this paper, we impose the following assumptions on the demand model :

-

1.

The noise is a martingale difference sequence adapted to the filtration where , i.e., .

-

2.

There exists such that every entry of is at most almost surely for all .

-

3.

The underlying true parameter in the linear demand model is negative definite; 333 is is negative definite (not necessarily symmetric) if for any , it holds that . there exists (with ) such that for every , where is the -th unit vector and is the -th row of .

All items in Assumption 2.2 are quite standard in the literature. The third item is usually seen in papers focusing on the linear demand model (see, e.g., Keskin and Zeevi (2014), Ferreira et al. (2018), Bu et al. (2022)). By the definition and according to Assumption 2.2, we may upper bound by .

We now discuss the performance measure for the retailer’s policy. We would like to compare the objective value achieved by the retailer with the optimal offline policy, i.e., the one that knows all the model parameters :

| (1) |

upper bounds the objective value achieved by any online policy (i.e., the one without access to ). In light of this, we define the regret of a policy up to time horizon as

| (2) |

Note that solving the exact value of is quite complicated due to the stochastic nature and adaptivity available to choose in sequence. We now introduce the following fluid model which is the deterministic and non-adaptive analog of and is easier to analyze.

| (3) |

We assert that there exists an optimal solution to such that , since otherwise, we can set for every , and the objective value of becomes no smaller due to the concavity of (since and is negative definite by Assumption 2.2) and Jenson’s inequality. Therefore we have the following equivalent definition of .

| (4) |

We denote by the optimal solution to Eq. (4).

The following proposition shows that the fluid model is an upper bound of , and its proof is deferred to the supplementary materials.

Proposition 2.1

.

By Proposition 2.1, we upper bound the regret of any policy as follows, which will serve as the starting point of the analysis of our proposed policy.

| (5) |

| (6) |

| (7) |

| (8) |

| (9) |

| (10) |

3 Primal-dual Type Algorithm with Demand Learning

The pseudo-code of our main algorithm is given in Algorithm 1. In the following, we present an intuitive and high-level idea behind the design of the algorithm.

To better introduce our algorithm design, we first imagine that the demand function was known and only explain the primal-dual framework. We then add the learning component for the demand function and address the additional challenges raised due to the unknown demand.

Given the demand function , thanks to Proposition 2.1, we may use the fluid model , which upper bounds , to calculate an upper estimation of the regret of any online policy.444Indeed, this relaxation would not ruin our aimed regret, as the difference between and is also for the network revenue management problem either without (Gallego and Van Ryzin 1997) or with the global regularization (as we will see later in this paper). We now focus on the primal formulation of the fluid model. To simplify the global regularization , we introduce an auxiliary variable . With this new variable, the original optimization problem with one primal variable and an inequality constraint is transformed into one with two primal variables and an equality constraint:

| (11) | ||||

Note that we deliberately impose a lower bound constraint in the new formulation. This does not change the optimal value of the program since is entry-wise non-negative for non-negative and .

We then transform primal formulation into an unconstrained optimization problem using the Lagrangian dual method. By the well-known weak duality, we have that

| (12) |

In light of this, we define the dual function

| (13) |

where for every we define

| (14) |

and the convex conjugate (following the convention, e.g., Chapter 3 in Boyd et al. (2004))

| (15) |

By Eq. (12), for every , we have that

| (16) |

To introduce the primal-dual framework, let us define the optimal dual solution . Suppose we had in hand, it would be natural to make a good price decision according to

which is indeed the optimal decision if strong duality holds. Since we do not know a priori, in the primal-dual framework, we alternately optimize the primal variables (Line 6)555To illustrate the intuition, we assume the demand function is known. In Algorithm 1, we need to deal with the upper confidence bounds of the estimated quantities when optimizing , which will be explained soon. based on the dual variable ,

and optimize the dual variable via calculating the subgradient of the dual function at (Line 8)666Again, here we assume the demand function is known.:

| (17) |

Here can be seen as the target resource-consumption vector related to the balancing regularization.

The optimal dual solution is also known as the shadow price in economics theory and revenue management optimization. It measures the change of the optimal revenue when given an additional unit of the constrained resource. In light of this, we refer to as the adjusted revenue function with respect to and . It represents the revenue that takes the economic value of the constrained resource into consideration. The subgradient (Eq. (17)) also offers intuitive managerial insights on how the update of the dual variable helps optimize the fair resource-consumption balancing objective: when the consumption of type- resource exceeds the resource-consumption target (), becomes negative, which in turn increases the shadow price to discourage the consumption of type- resource; similar argument applies to the opposite case when .

In Algorithm 1, when updating the dual variable at Line 9, we use the mirror descent method with the help of a mirror descent solver defined as follows.

Definition 3.1 (Mirror Descent Solver)

A mirror descent solver takes and as input and returns the updated dual variable at each time . For a sequence of input and the initial dual variable , if we repeatedly apply and produce a sequence of dual variables . The solver makes sure that for all ,

| (18) |

where and are constants that only depend on .

In other words, the mirror descent solver should generate a sequence to minimize against any stationary benchmark with the regret at most .

The above-described primal-dual framework is similar to (and inspired by) the algorithm proposed in Balseiro et al. (2021). However, the key differences are two folds explained as follows.

Demand Learning. In contrast to the known demand function in Balseiro et al. (2021), the demand function is not known to the decision-maker beforehand in our setting. Our algorithm learns the parameterized demand function from historical data via the regularized least-squares estimate (Line 3). We then solve another convex program (Line 4) to make sure the estimated parameters are bounded and is negative semi-definite. Finally, we use the Upper Confidence Bound of the adjusted revenue function (Line 6) to compute the primal update. We will explain this in more detail in Section 4.

An additional feature of our demand estimator is that the reward Upper Confidence Bound is defined based on the -norm of where the -norm is usually adopted in the linear bandit literature. Together with the convex program solved in Line 4, our definition of the reward Upper Confidence Bound renders the primal update a combination of a few convex optimization problems (Eq. (8)) that can be efficiently solved, which will be further explained in Section 4.2.777On the downside, we sacrifice an factor in the regret bound. However, we view this degradation as relatively small compared to the existing factor which seems necessary in the regret due to the parameters in to learn.

A New Dual Space. The dual space is a crucial component in the design of the mirror descent solver and affects the regret analysis. Balseiro et al. (2021) adopt a dual space which might have different shapes for different balancing regularizer . The fundamental reason that we cannot directly adopt in our problem, however, is the unboundedness of which would lead to an unbounded regret due to the unbounded estimation error of the adjusted reward during the learning process (see Eq. (26) for more details). To deal with this issue, we construct a novel, simply and uniformly shaped, and bounded dual space (Eq. (10)). We prove that our dual space encompasses all potential stationary benchmark dual variables which is necessary for the desired regret.

Thanks to the newly constructed dual space, an extra benefit enjoyed by our algorithm is that, together with a carefully chosen variant of the exponentiated gradient descent () algorithm as the mirror descent solver, we are able to obtain a uniform and closed-form update of the dual variables for all balancing regularizers. In contrast, Balseiro et al. (2021) have to design the dual update step on a case-by-case basis for the balancing regularizers. Also, the closed-form update improves the computational efficiency of the algorithm and is a desired feature in Balseiro et al. (2021) that is partially achieved for a few selected balancing regularizers.

4 Demand and Reward Estimation

The regularized least-squares estimator (Line 3 of Algorithm 1) for demand parameters is frequently used in the linear bandit literature (see, e.g., Dani et al. (2008), Rusmevichientong and Tsitsiklis (2010), Abbasi-Yadkori et al. (2011)). However, as mentioned before, we need to work with the upper confidence bound of a specially defined adjusted revenue function. Also, we employ an additional step (Line 4) to make sure the estimated parameters are bounded, which is crucial to the regret analysis (more specifically, the analysis of the mirror descent solver). Line 4 also guarantees the negative semi-definiteness of ; when computing the Upper Confidence Bound for the estimation, we use an -norm confidence radius instead of the usual -norm confidence radius – both ingredients help the algorithm to compute the upper confidence bound in polynomial time. We will show how to computationally efficiently find (Line 4) and implement the UCB-type primal update (Line 6) in Section 4.1 and Section 4.2 respectively.

To explain our Upper Confidence Bound method in more detail, we first introduce some notations. For convenience, we define the stopping time

which is the last time period when the inventory levels of all resources remain positive. Most of our analysis will be done only for time periods up to . We define

| (19) |

to be the adjusted revenue function at price and with respect to . Note that this corresponds to the optimization objective in Eq. (14) when . Our estimation for is

| (20) |

which corresponds to the first part in the optimization objective of in Eq. (8). We also define estimators with regard to as

Bounding the estimation errors. We now derive the estimation errors of and , as well as their corresponding upper confidence bounds. For any price (column) vector , we let , and then introduce the regularized information matrix at time to be

| (21) |

Let

| (22) | ||||

| (23) |

to be the confidence radii of and respectively. Note that here we use instead of the -norm confidence radius commonly seen in literature. We finally define

| (24) |

to be the confidence radius for the adjusted reward estimator . We utilize the famous Confidence Ellipsoid Lemma in Abbasi-Yadkori et al. (2011) to analyze our -type confidence region, and have the following lemma. Our lemma states that the confidence radii defined above (Eq. (23) and Eq. (24)) hold with overwhelming probability.

Lemma 4.1

With probability at least , for all and all , we have

As we will later show in Lemma 4.7, with probability at least , we are able to find a feasible in Line 4. Combining the definition of and Lemmas 4.1 and 4.7, we have the following corollary.

Corollary 4.2

With probability at least , for all and all , we have

The program . Note that by Lemma 4.1, already serve as good estimators. However, in the rest part of the algorithm (as well as the analysis), we will mainly work with , which are defined based on derived by solving the program in Line 4 of Algorithm 1. This is due to the following two requirements.

- 1.

-

2.

The primal update (Eq. (8)) involves maximizing , a quadratic form of , which can be efficiently optimized only when is negative semi-definite so that is concave.

By solving the program , we find that simultaneously satisfies the above two requirements and stays close to (in terms of the norm). In this way, we facilitate both the regret analysis and the efficient computation of the algorithm. Please refer to Sections 4.1 and 4.2 for the efficient implementations of solving and the primal update respectively.

UCB of the adjusted revenue function. When the desired event in Corollary 4.2 happens, we define

| (25) |

and have that for all and . Note that is exactly the optimization objective of (at Line 6 of Algorithm 1), which is indeed an Upper Confidence Bound (UCB) of the maximization objective in (Eq. (14), namely ).

Since for all and , we further upper bound by

| (26) |

Therefore, we set

| (27) |

to upper bound all the confidence radii , and .

Bounding the total estimation error. In our regret analysis, we will relate the regret incurred at time to the confidence radii at price at the time (which aligns with the general Upper Confidence Bound principle – bounding the regret by the confidence radii of the selected actions). And thus we will be interested in the summation of the estimation errors. The following lemma adapts the celebrated Elliptical Potential Lemma (see, e.g., Theorem 11.7 in Cesa-Bianchi and Lugosi (2006) and Lemma 9 in Dani et al. (2008)) to upper bound the total estimation error.

Lemma 4.3

With probability , we have the following upper bound for the total estimation error:

where only a universal constant is hidden in the notation.

4.1 Solving via Ellipsoid Method

In this subsection, we describe how to implement Line 4 and find a feasible solution to in polynomial time via the Ellipsoid method. The main lemma of this subsection is Lemma 4.7.

We first introduce the definition of a separation oracle for a convex set , which is closely related to the Ellipsoid method.

Definition 4.4 (Separation Oracle)

For a closed convex set , a separation oracle for , namely , is an algorithm that takes a point as input and correctly decides whether . In the case that , the separation oracle also returns a hyperplane that separates from . The hyperplane may be characterized by its norm vector such that for all .

The ellipsoid method reduces a convex program feasibility problem to the construction of an efficient separation oracle for the corresponding convex body. The following lemma characterizes such a reduction. The lemma is a simplification of Theorem 3.2.1 in Grötschel et al. (2012) modulo the numerical error due to the arithmetic operations on real numbers.888The numerical error analysis is often tedious but straightforward, which is also the case in this subsection. Therefore, we choose to omit this part and emphasize the main algorithmic idea more clearly.

Lemma 4.5

Suppose we could perform exact arithmetic operations on real numbers. Let denote the closed ball with radius and centered at . Given a closed convex set , suppose that there exist such that and for some . Given , , , and a separation oracle for , namely , the Ellipsoid method will return a point in using calls to the separation oracle and arithmetic operations.

It is easy to verify that our is a closed convex set in . To apply Lemma 4.5 to , we first upper and lower bound the shape of as follows.

Lemma 4.6

Given the desired event described in Lemma 4.1, we have that

where we treat the matrices and as -dimensional vectors.

The separation oracle. It remains to design the separation oracle . Given , we need to verify the following two types of constraints specified in the definition of (Eq. (7)).

-

•

. This condition can be verified for each by straightforward computation. When the condition is not met for some , we have that , and there exists such that

for every where , which defines the separation hyperplane.

-

•

. This condition can also be verified for each by straightforward computation. When the condition is not met for some , we have that , and there exists such that

for every where , which defines the separation hyperplane.

-

•

. This condition is equivalent to which can be efficiently verified. If the condition is not satisfied, we can efficiently find a vector such that

for every , which defines the separation hyperplane.

The above separation oracle can be implemented using arithmetic operations (required by both the first and the third steps). Combining Lemma 4.6, and the separation oracle constructed above, we may invoke Lemma 4.5 with , (therefore ) and , and conclude this subsection with the following lemma.

Lemma 4.7

With probability at least , for all , is feasible, and we can find via the Ellipsoid method using calls to the separation oracle and arithmetic operations on real numbers.

4.2 Efficient Primal Update

We now show that thanks to the new -norm-based confidence region, we may efficiently implement the primal update (Line 6) by solving convex optimization problems. We focus on the optimization problem for as the one for is already convex. Note that

where ( is the -th canonical basis vector in . For any , define the convex program (which is convex due to the negative semi-definiteness of guaranteed in Line 4)

It is easy to verify that . Therefore, to compute the primal update for , we only need to first solve convex programs to identify for every , and then select

| (28) |

5 Mirror Descent Solver and its Closed-form Dual Update

In this section, we design the mirror descent solver to satisfy Definition 3.1. Given the dual space , for any reference function that is -strongly convex with respect to over , the online mirror descent (OMD) algorithm operates in the following way to update the dual variable:

| (29) |

where is the Bregman divergence. It is well-known (see, e.g., Hazan et al. (2016)) that if for all , then if we start with any given , the sequence produced by Eq. (29) guarantees that for any stationary benchmark ,

which matches the requirement of Definition 3.1.

The popular choices of the reference functions are the negative entropy function (so that , and the OMD algorithm becomes the exponentiated gradient algorithm) and the Euclidean norm (so that and the OMD algorithm becomes the projected gradient descent algorithm). However, based on the different shapes of the dual space , one has to carefully choose to guarantee its strong convexity and proper definition (e.g., the negative entropy function is not properly defined when any of the coordinates becomes negative). Due to this reason, Balseiro et al. (2021) have to design the reference function on a case-by-case basis for various balancing regularizers which shape their dual space . When designing , Balseiro et al. (2021) also aim to simplify the update rule (Eq. (29)) with the hope of a closed-form update, so as to reduce the computational cost. However, they are only able to achieve this goal for selected balancing regularizers.

In our work, thanks to the simplicity of newly designed dual space (Eq. (10)), we are able to use a uniform mirror descent solver that enjoys the closed-form update for all balancing regularizers. Our is similar to the OMD algorithm with the negative entropy function. The only issue, however, is that the negative entropy function does not apply to negative coordinates covered by our dual space . To this end, we employ the special variant of the algorithm that separately deals with the positive weights and negative weights in . The algorithm was proposed by Kivinen and Warmuth (1997) and called (Exponentiated Gradient Algorithm with Positive and Negative Weights).

The algorithms is formally described in Algorithm 2. Note that instead of a single vector , the algorithm keeps two vectors and , and the update of the two vectors are in simple closed forms. While both vectors are in , they respectively represent (the absolute values of) the positive and negative weights in (see Eq. (31)). Due to this technical reason, to use as our mirror descent solver, we need to slightly modify the description of our main Algorithm 1. First, we initialize the two vectors as

| (30) |

which replaces the initialization (Line 1) of Algorithm 1. We also replace the dual update (Eq. (9)) of Algorithm 1 by

| (31) |

It remains to choose as the upper bound of . To this end, we set

Since for all we have and , which is guaranteed in Line 4, it is easy to obtain . And thus we could have the following upper bound of

| (32) |

Therefore, we may upper bound by :

| (33) |

By directly applying Theorem 2 in Hoeven et al. (2018), we have the following lemma showing that satisfies our requirement of the mirror descent solver.

Lemma 5.1

By adopting as our mirror descent solver , Definition 3.1 is satisfied with

| (34) |

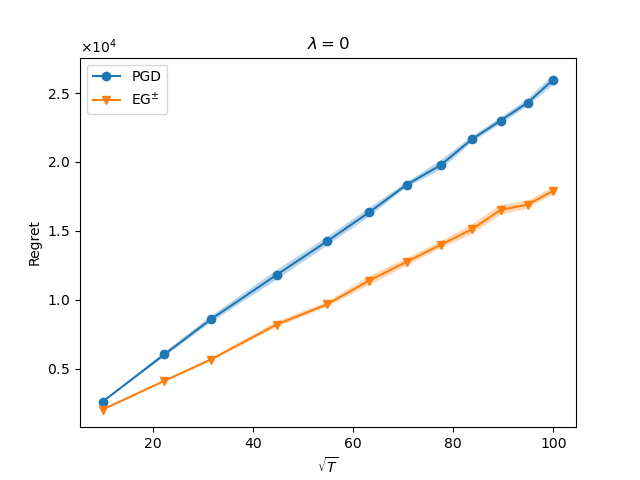

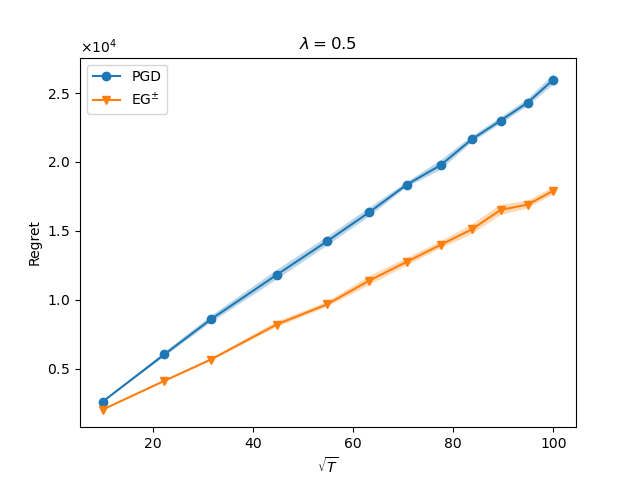

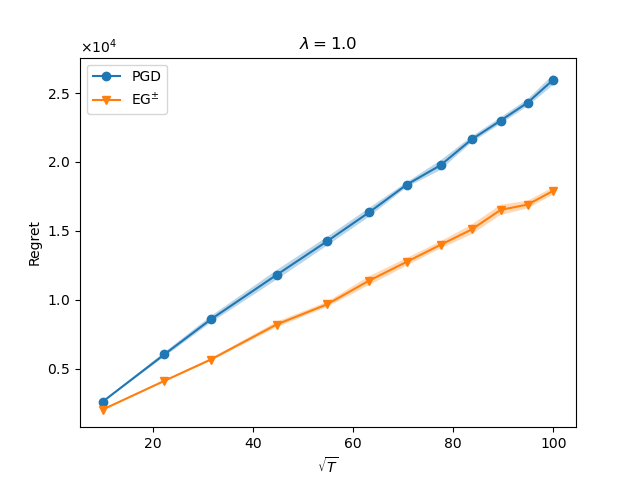

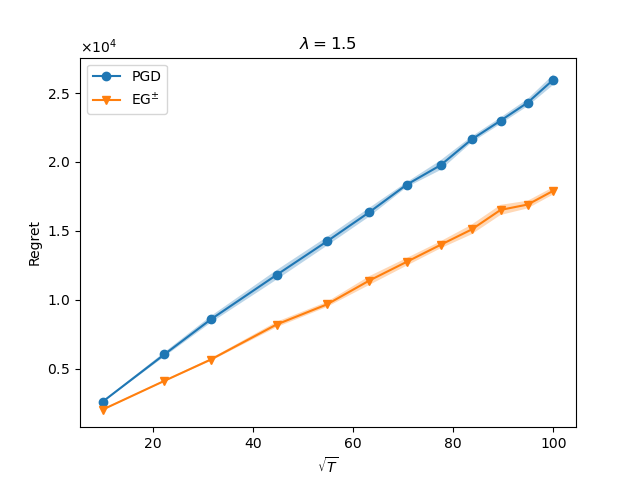

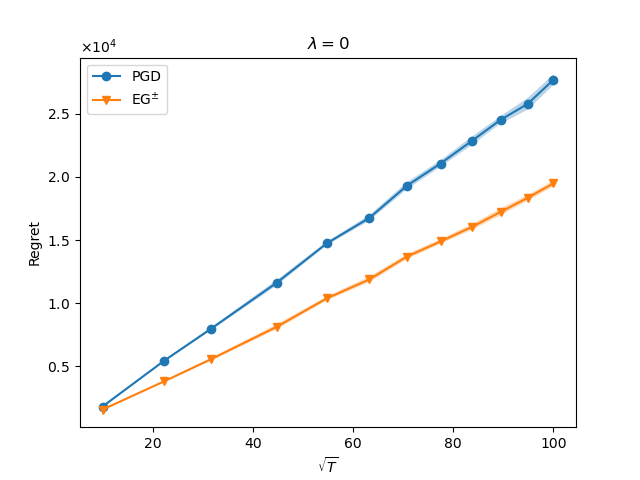

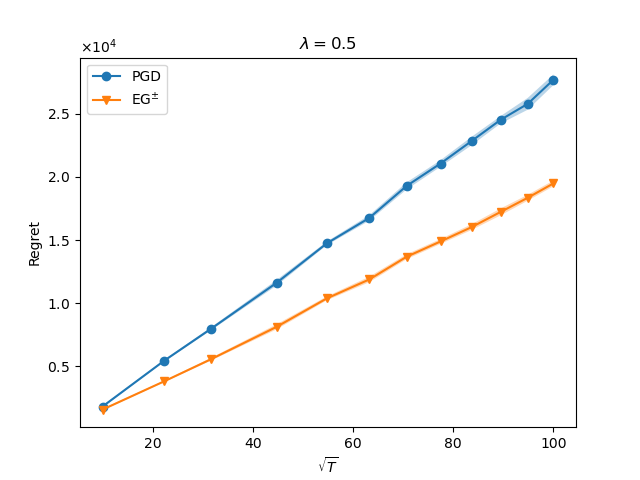

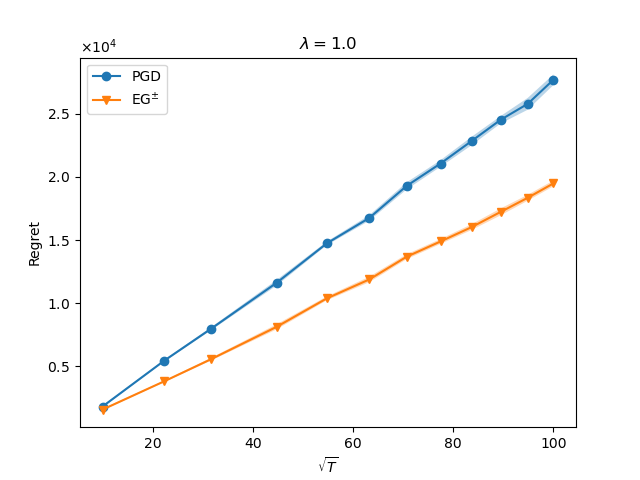

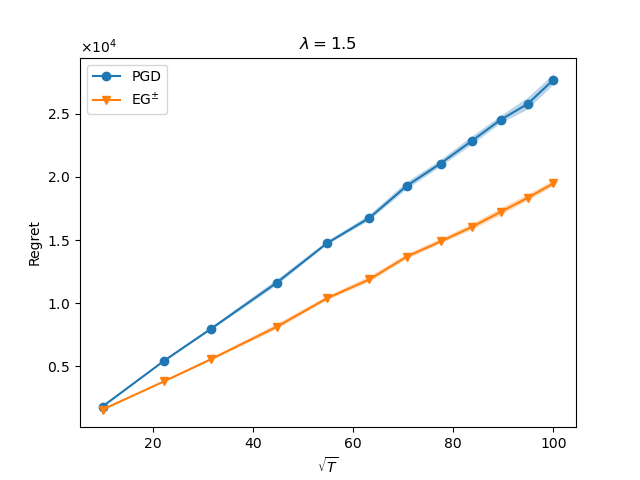

It is worth noting that when , the online mirror descent algorithm (29) is known as the projected gradient descent method (PGD). Since is -strongly convex over with respect to , the PGD solver also satisfies Definition 3.1. However, the updating step of the PGD solver has no closed form due to the projection onto the ball in each update. Numerical results in Section 14 demonstrate that has better empirical performance than the PGD solver.

6 Main Result

With the main technical tools ready in hand, we now prove the following main theorem which upper bounds the regret of our Algorithm 1.

Theorem 6.1

Remark 6.2

Recall that , , and is defined in Eq. (22). Assuming the problem parameters and , we have that , , , and .

The proof of our main theorem, which is presented in Section 12 in E-Companion, follows the general framework of the primal-dual analysis of online optimization problems (e.g., Beck and Teboulle (2003), Hazan et al. (2016), Balseiro et al. (2023, 2021)), and will be detailed in 5 steps. The main differences from Balseiro et al. (2021) is that in Step II, we need to deal with the estimation error in the dual expression that relates to the balancing regularizer (note the term in ). We bound this part in Steps III and IV. This error can be upper bounded by estimation error of multiplied by the -norm of the dual variables. Our definition of the dual space again kicks in to help upper bound the error.

7 Numerical Experiments

In this section, we present the numerical experiments on the synthetic data sets to illustrate the effectiveness of our algorithm. We use an NRM example, in which the retailer sells five products () using ten resources (), and the (transpose of the) resource consumption matrix is defined as

| (35) |

The underlying linear demand function is defined as

In addition, we choose the weighted min-max fairness regularizer

with for all . We generate the demand noise from the truncated Gaussian distribution

We set the time horizon as and the price range for each product as . We test two initial inventory levels ( and ) and four regularization level () using two mirror descent solvers ( and PGD). We conduct trials independently for each case and plot the average result of these trials in all figures. We also use the shaded region around each curve to indicate the confidence interval across the trials.999 For normal distribution, the - value for confidence is . Slightly abusing the terminology, we define the confidence interval here as .

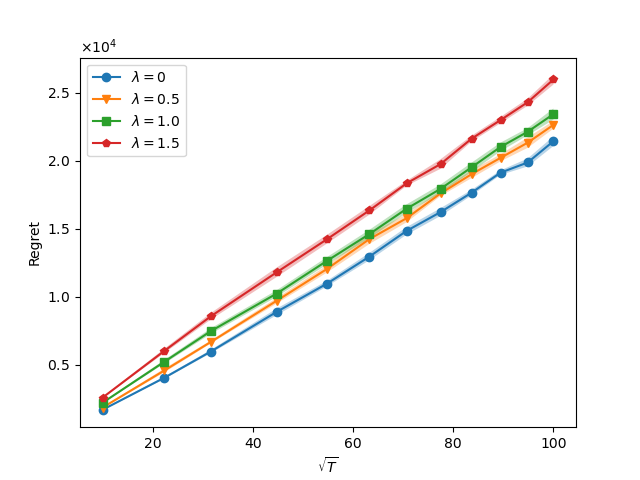

For brevity, we present the numerical results of in this section and leave the numerical results of initial inventory level to Section 14 in the supplementary materials.

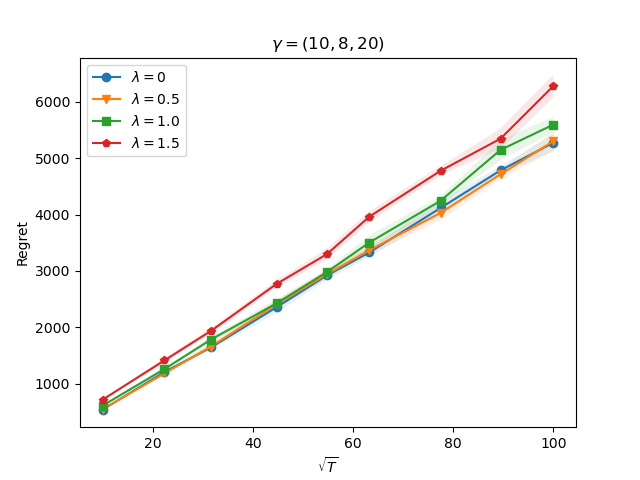

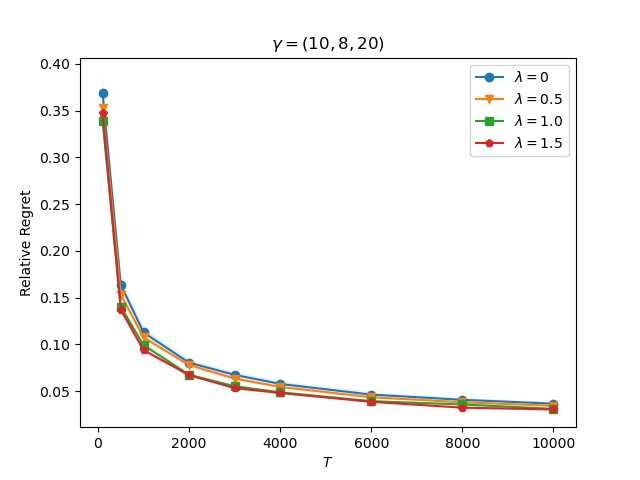

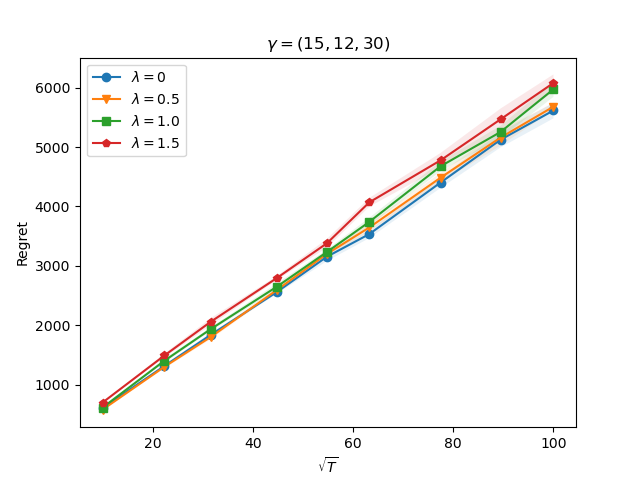

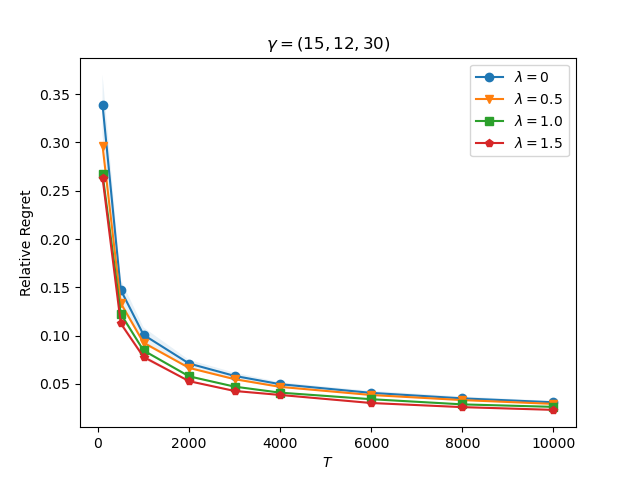

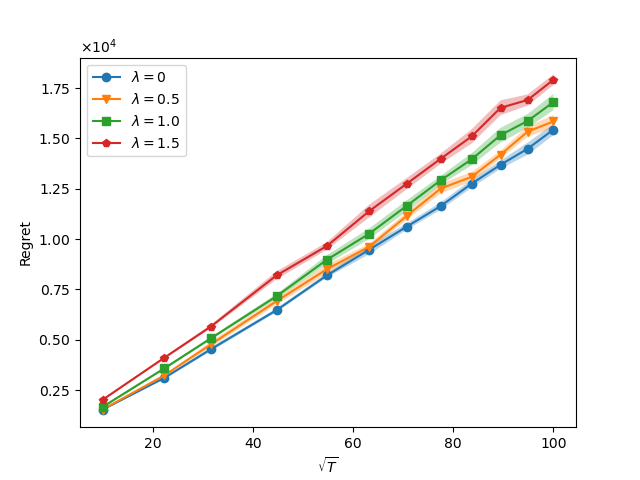

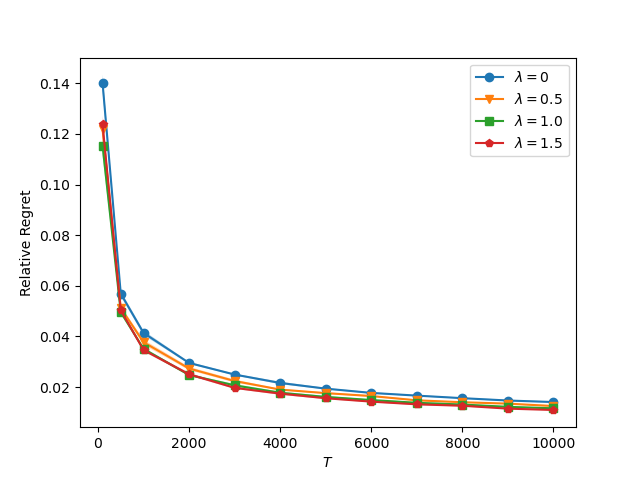

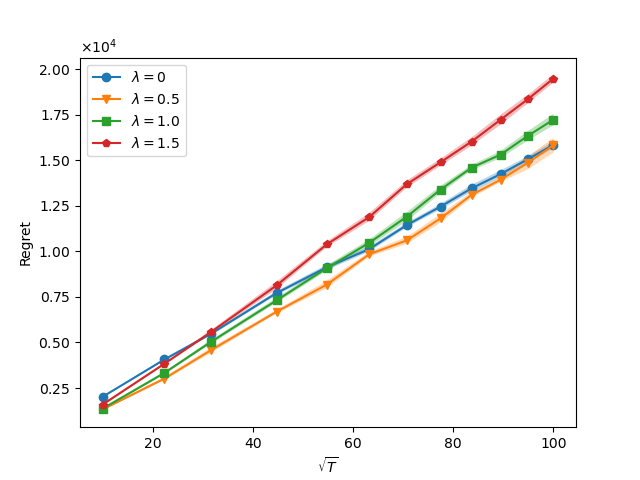

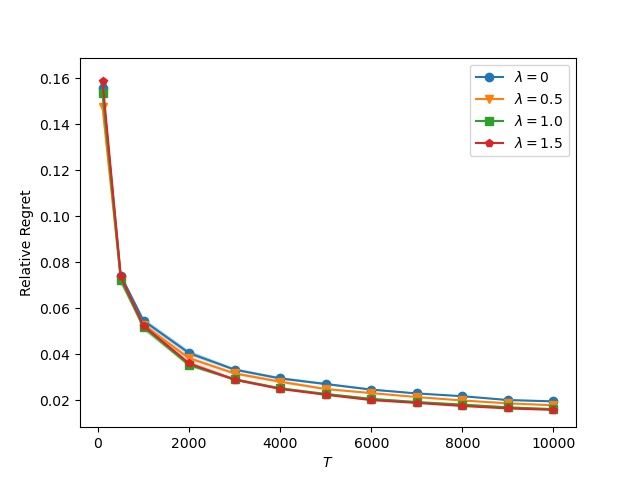

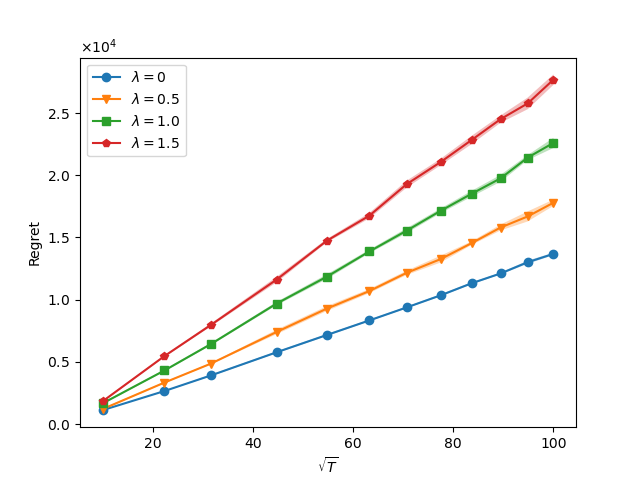

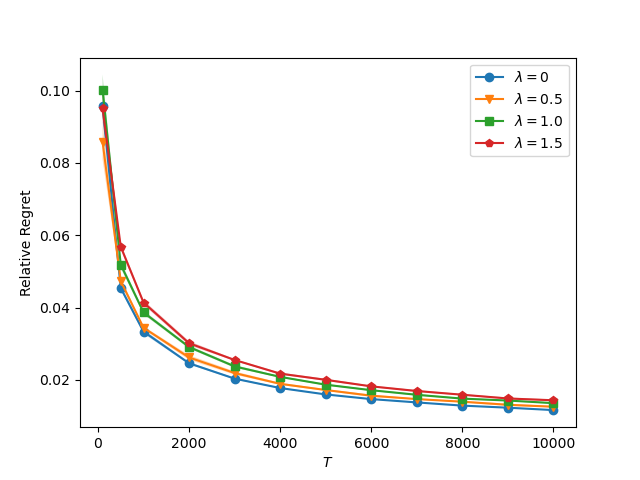

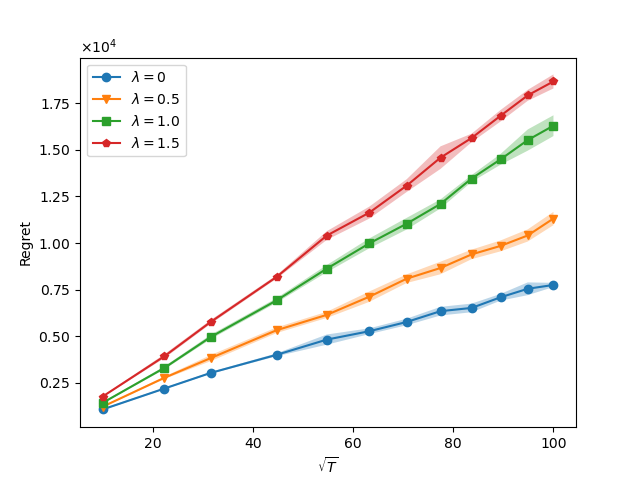

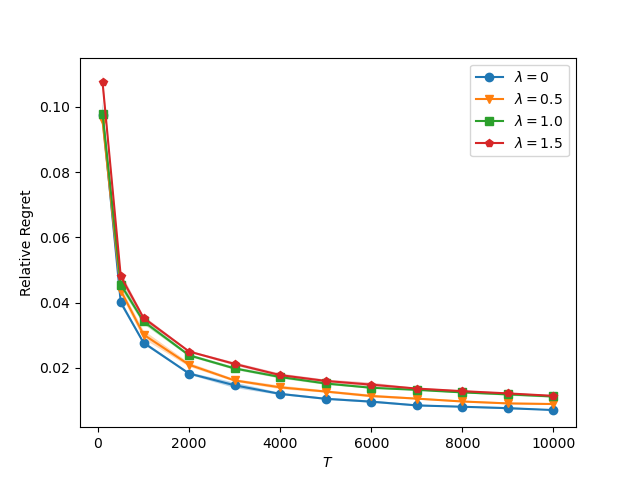

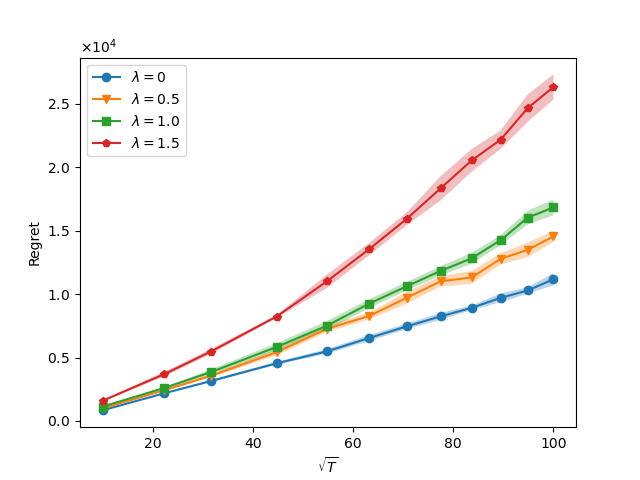

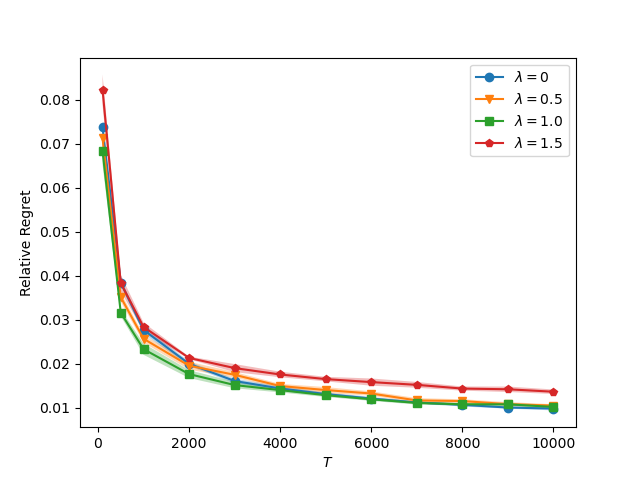

Numerical results of Algorithm 1+ under inventory level . In the left of Figure 2 is the plot of the regret of Algorithm 1 with the inventory level and versus the square root of the total time periods . This figure clearly demonstrates the regret of our algorithm grows at rate for all regularization levels , which is consistent with the theoretical guarantee of Theorem 6.1. In the right of Figure 2 we plot the relative regret of Algorithm 1 versus the total time periods , where the relative regret is defined as

| (36) |

Note that the narrow confidence intervals indicate the stability and robustness of our algorithm.

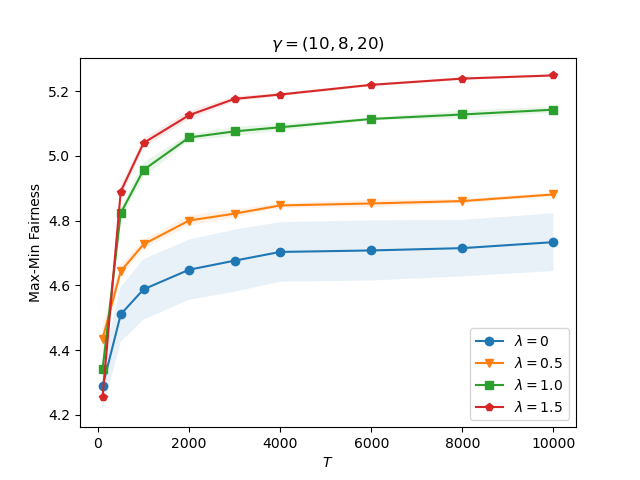

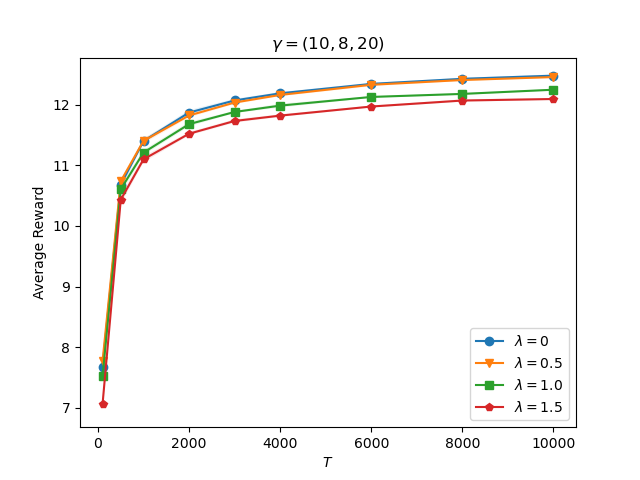

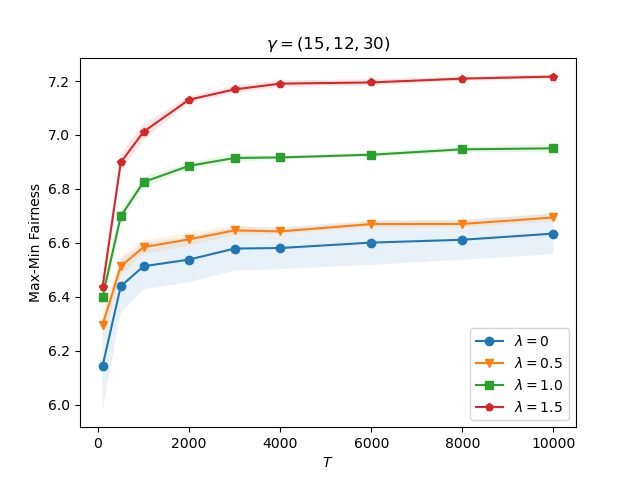

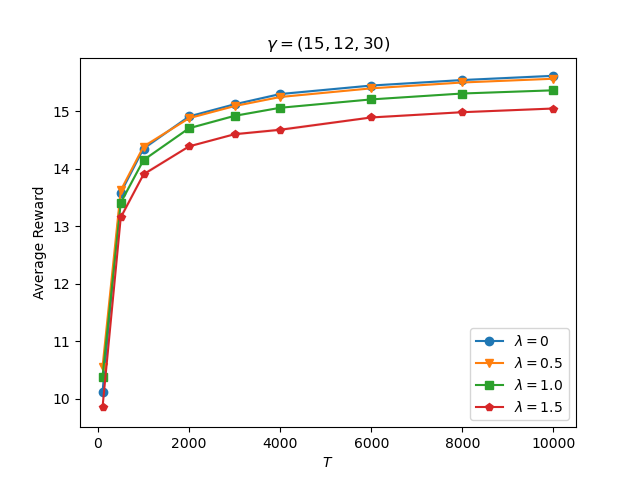

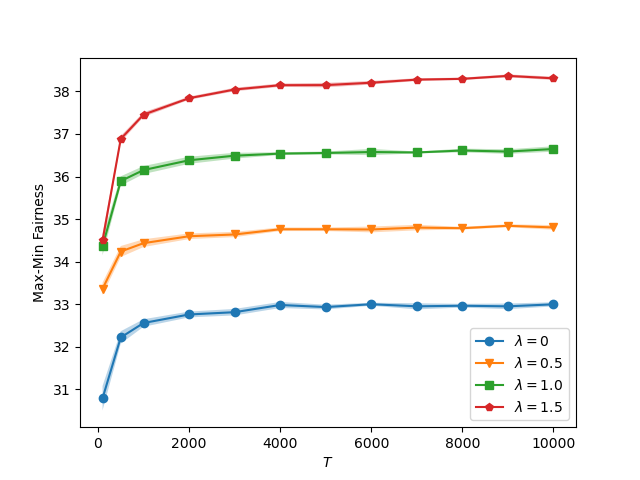

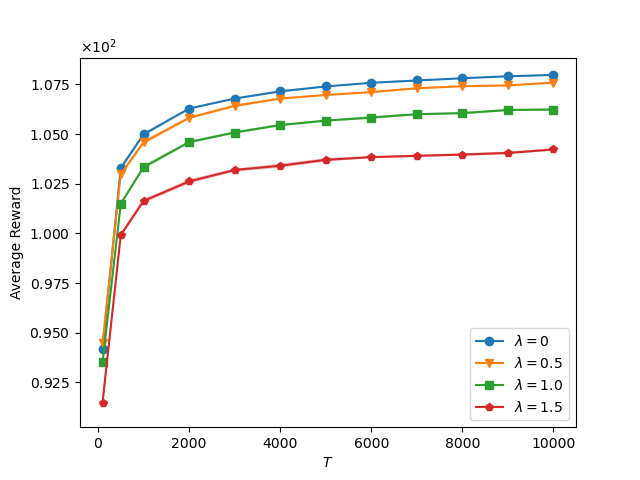

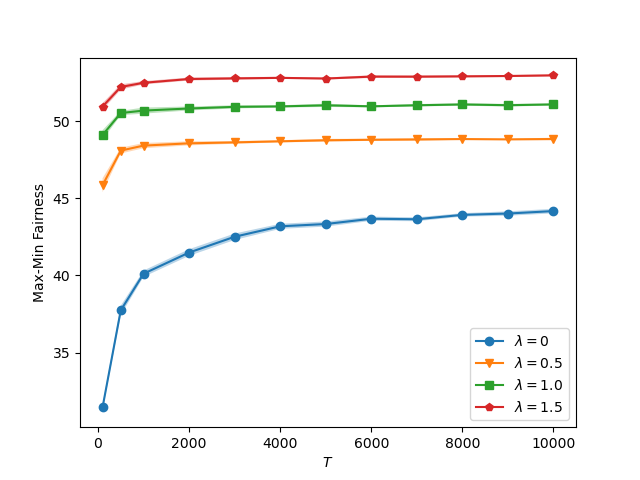

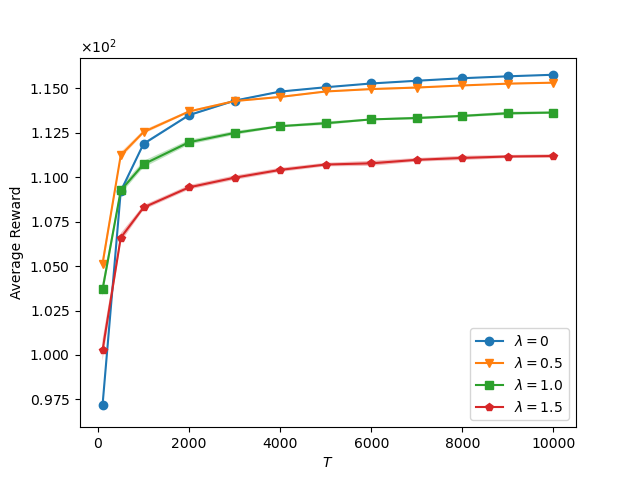

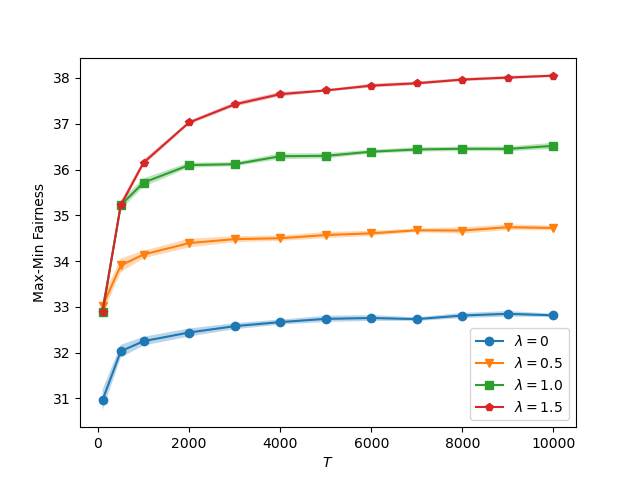

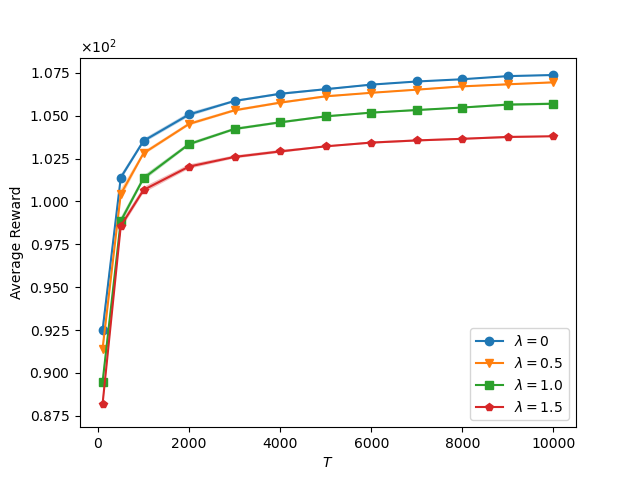

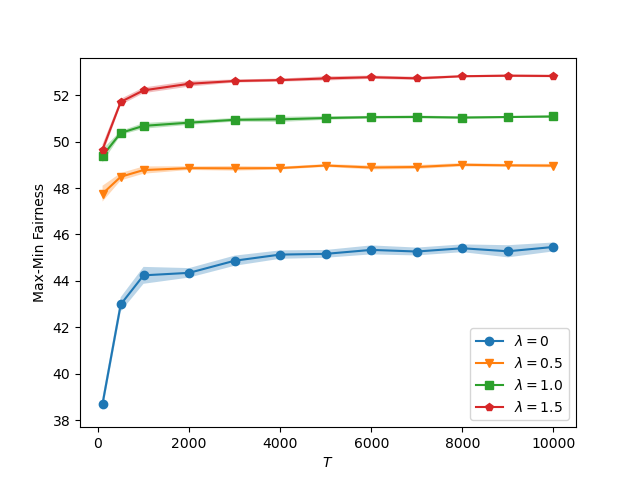

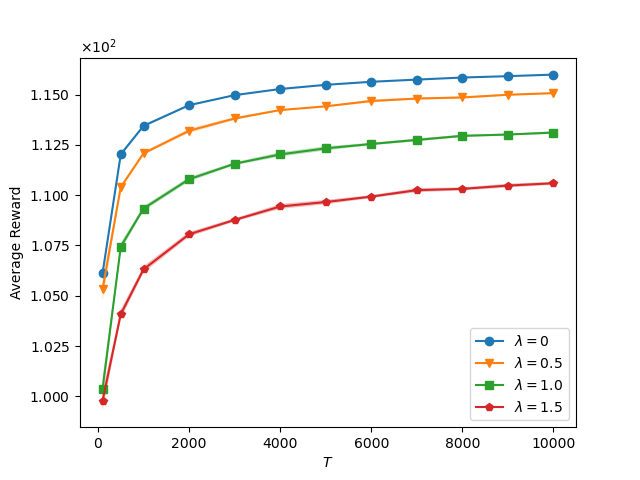

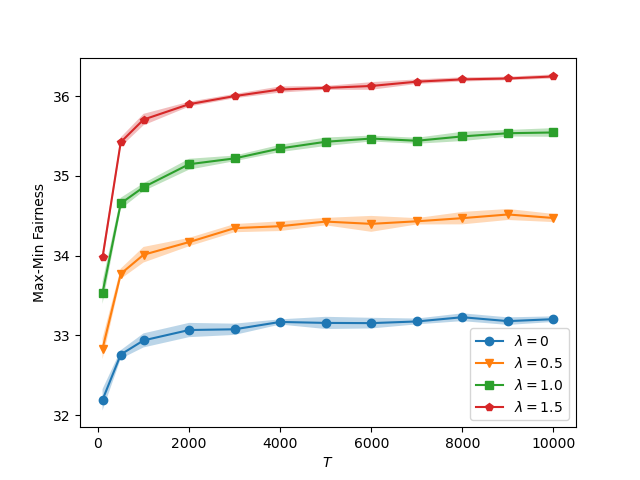

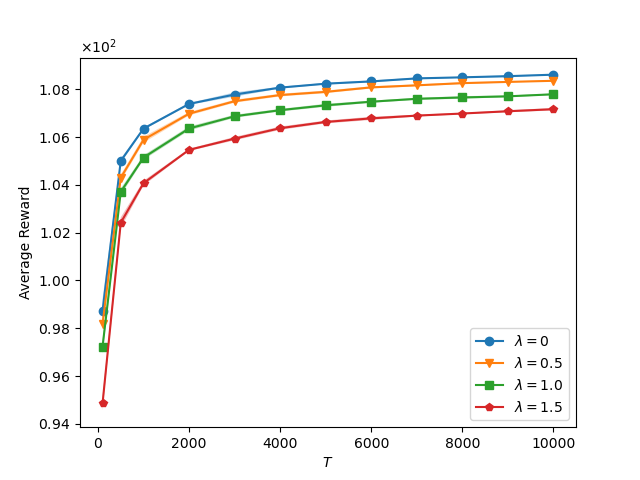

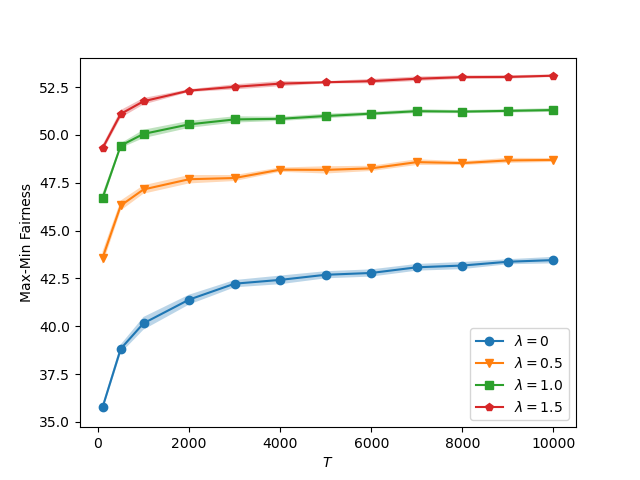

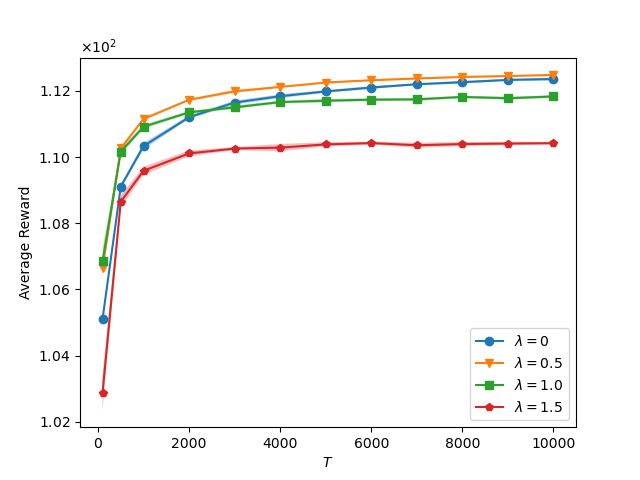

We further empirically study the impact of the regularization level to the utilization of the resources. In the left of Figure 2 is the plot of the max-min fairness versus the total time periods with the inventory level and , where the max-min fairness is defined as the minimum element of the average resource consumption vector . In the right of Figure 2 we plot the average reward versus the total time periods , where the average reward is defined as . These figures show the max-min fairness increases and the average reward decreases as grows, indicating the natural trade-off between fairness and the average reward. We also find that the max-min fairness could be enhanced greatly with a small sacrifice of the average reward reduction.

In Section 14 of the supplementary materials, we present additional numerical results, which include 1) computational time report; 2) numerical results of Algorithm 1+ under the inventory level ; 3) numerical results of Algorithm 1+; 4) performance Comparison of and ; 5) numerical results of Algorithm 1+ in a model misspecified setting; 6) numerical results on a classic NRM example studied in Besbes and Zeevi (2012), Ferreira et al. (2018).

8 Conclusion

This paper studies the price-based network revenue management with both fair resource-consumption balancing and demand learning, which is motivated by the practical needs of industries such as online retailing and airline applications. To tackle the challenges of this task, we make several innovative technical contributions, which have the potential to be applied to other operations management problems. We propose a primal-dual-type online policy with Upper-Confidence-Bound (UCB) learning method to simultaneously learn the unknown demand function and optimize the composite objective concerning both the NRM revenue and the balancing metric. Both theoretical analysis and numerical results show the effectiveness and the ability in simultaneously achieving revenue maximization and fair resource-consumption balancing.

For future directions, one can consider adapting the framework in this paper to other revenue management applications with both resource-consumption balancing and demand learning. One could also study the demand learning of non-parametric demand functions and consider adapting our framework to other global ancillary objectives beyond balanced consumption across resources. As discussed in the introduction section, in some scenarios resource-consumption balancing could enhance the customer satisfactions. Addressing customer dissatisfaction through the inclusion of customer dissatisfaction costs into revenue maximization objective is also a noteworthy consideration. While modeling and formulating customer dissatisfaction costs comes with its own set of complexities and involves intricate challenges, we believe it’s a promising avenue to explore for future research.

References

- Abbasi-Yadkori et al. (2011) Abbasi-Yadkori, Yasin, Dávid Pál, Csaba Szepesvári. 2011. Improved algorithms for linear stochastic bandits. Advances in Neural Information Processing Systems, 24 2312-2320.

- Agrawal and Devanur (2016) Agrawal, Shipra, Nikhil Devanur. 2016. Linear contextual bandits with knapsacks. Advances in Neural Information Processing Systems, 29 3458-3467.

- Agrawal and Devanur (2019) Agrawal, Shipra, Nikhil R Devanur. 2019. Bandits with global convex constraints and objective. Operations Research, 67 (5), 1486-1502.

- Al Nuaimi et al. (2012) Al Nuaimi, Klaithem, Nader Mohamed, Mariam Al Nuaimi, Jameela Al-Jaroodi. 2012. A survey of load balancing in cloud computing: Challenges and algorithms. Network Cloud Computing and Applications, International Symposium on. IEEE Computer Society, 137-142.

- Badanidiyuru et al. (2018) Badanidiyuru, Ashwinkumar, Robert Kleinberg, Aleksandrs Slivkins. 2018. Bandits with knapsacks. Journal of the ACM (JACM), 65 (3), 1-55.

- Balseiro et al. (2021) Balseiro, Santiago, Haihao Lu, Vahab Mirrokni. 2021. Regularized online allocation problems: Fairness and beyond. International Conference on Machine Learning. PMLR, 630-639.

- Balseiro et al. (2023) Balseiro, Santiago R, Haihao Lu, Vahab Mirrokni. 2023. The best of many worlds: Dual mirror descent for online allocation problems. Operations Research, 71 (1), 101-119.

- Bansal and Sviridenko (2006) Bansal, Nikhil, Maxim Sviridenko. 2006. The santa claus problem. Proceedings of the 38th Annual ACM Symposium on Theory of Computing. 31-40.

- Beck and Teboulle (2003) Beck, Amir, Marc Teboulle. 2003. Mirror descent and nonlinear projected subgradient methods for convex optimization. Operations Research Letters, 31 (3), 167-175.

- Bertsimas et al. (2011) Bertsimas, Dimitris, Vivek F Farias, Nikolaos Trichakis. 2011. The price of fairness. Operations Research, 59 (1), 17-31.

- Besbes and Zeevi (2009) Besbes, Omar, Assaf Zeevi. 2009. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research, 57 (6), 1407-1420.

- Besbes and Zeevi (2012) Besbes, Omar, Assaf Zeevi. 2012. Blind network revenue management. Operations Research, 60 (6), 1537-1550.

- Bonald et al. (2006) Bonald, Thomas, Laurent Massoulié, Alexandre Proutiere, Jorma Virtamo. 2006. A queueing analysis of max-min fairness, proportional fairness and balanced fairness. Queueing systems, 53 (1), 65-84.

- Boyd et al. (2004) Boyd, Stephen, Stephen P Boyd, Lieven Vandenberghe. 2004. Convex optimization. Cambridge university press.

- Bu et al. (2022) Bu, Jinzhi, David Simchi-Levi, Yunzong Xu. 2022. Online pricing with offline data: Phase transition and inverse square law. Management Science, Forthcoming.

- Cesa-Bianchi and Lugosi (2006) Cesa-Bianchi, Nicolo, Gábor Lugosi. 2006. Prediction, learning, and games. Cambridge university press.

- Chen et al. (2021a) Chen, Guanting, Xiaocheng Li, Yinyu Ye. 2021a. Fairer LP-based online allocation via analytic center, Preprint, submitted October 27, https://arxiv.org/abs/2110.14621.

- Chen et al. (2014) Chen, Qi, Stefanus Jasin, Izak Duenyas. 2014. Adaptive parametric and nonparametric multi-product pricing via self-adjusting controls. Technical Report, University of Michigan, Ann Arbor, Ml.

- Chen et al. (2019) Chen, Qi, Stefanus Jasin, Izak Duenyas. 2019. Nonparametric self-adjusting control for joint learning and optimization of multiproduct pricing with finite resource capacity. Mathematics of Operations Research, 44 (2), 601-631.

- Chen et al. (2021b) Chen, Xi, Jiameng Lyu, Xuan Zhang, Yuan Zhou. 2021b. Fairness-aware online price discrimination with nonparametric demand models. Preprint, submitted November 11, https://arxiv.org/abs/2111.08221.

- Chen and Shi (2023) Chen, Yiwei, Cong Shi. 2023. Network revenue management with online inverse batch gradient descent method. Production and Operations Management, Forthcoming.

- Cohen et al. (2022) Cohen, Maxime C, Adam N Elmachtoub, Xiao Lei. 2022. Price discrimination with fairness constraints. Management Science, 68 (12), 8536-8552.

- Cohen et al. (2021) Cohen, Maxime C, Sentao Miao, Yining Wang. 2021. Dynamic pricing with fairness constraints, Preprint, submitted September 28, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3930622.

- Corsten and Kumar (2005) Corsten, Daniel, Nirmalya Kumar. 2005. Do suppliers benefit from collaborative relationships with large retailers? an empirical investigation of efficient consumer response adoption. Journal of Marketing, 69 (3), 80-94.

- Dani et al. (2008) Dani, Varsha, Thomas P Hayes, Sham M Kakade. 2008. Stochastic linear optimization under bandit feedback. Conference on Learning Theory, 355-366.

- Den Boer (2014) Den Boer, Arnoud V. 2014. Dynamic pricing with multiple products and partially specified demand distribution. Mathematics of Operations Research, 39 (3), 863-888.

- Den Boer (2015) Den Boer, Arnoud V. 2015. Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in Operations Research and Management Science, 20 (1), 1-18.

- Den Boer and Zwart (2014) Den Boer, Arnoud V, Bert Zwart. 2014. Simultaneously learning and optimizing using controlled variance pricing. Management Science, 60 (3), 770-783.

- Elzayn et al. (2019) Elzayn, Hadi, Shahin Jabbari, Christopher Jung, Michael Kearns, Seth Neel, Aaron Roth, Zachary Schutzman. 2019. Fair algorithms for learning in allocation problems. Proceedings of the Conference on Fairness, Accountability, and Transparency. 170-179.

- Ferreira et al. (2018) Ferreira, Kris Johnson, David Simchi-Levi, He Wang. 2018. Online network revenue management using thompson sampling. Operations Research, 66 (6), 1586-1602.

- Gallego and Van Ryzin (1994) Gallego, Guillermo, Garrett Van Ryzin. 1994. Optimal dynamic pricing of inventories with stochastic demand over finite horizons. Management Science, 40 (8), 999-1020.

- Gallego and Van Ryzin (1997) Gallego, Guillermo, Garrett Van Ryzin. 1997. A multiproduct dynamic pricing problem and its applications to network yield management. Operations Research, 45 (1), 24-41.

- Grötschel et al. (2012) Grötschel, Martin, László Lovász, Alexander Schrijver. 2012. Geometric algorithms and combinatorial optimization, vol. 2. Springer Science & Business Media.

- Haitao Cui et al. (2007) Haitao Cui, Tony, Jagmohan S Raju, Z John Zhang. 2007. Fairness and channel coordination. Management Science, 53 (8), 1303-1314.

- Hazan et al. (2016) Hazan, Elad, et al. 2016. Introduction to online convex optimization. Foundations and Trends in Optimization, 2 (3-4), 157-325.

- Hoeven et al. (2018) Hoeven, Dirk, Tim Erven, Wojciech Kotłowski. 2018. The many faces of exponential weights in online learning. Conference On Learning Theory. 2067-2092.

- Jasin (2014) Jasin, Stefanus. 2014. Reoptimization and self-adjusting price control for network revenue management. Operations Research, 62 (5), 1168-1178.

- Kallus et al. (2022) Kallus, Nathan, Xiaojie Mao, Angela Zhou. 2022. Assessing algorithmic fairness with unobserved protected class using data combination. Management Science, 68 (3), 1959-1981.

- Kallus and Zhou (2021) Kallus, Nathan, Angela Zhou. 2021. Fairness, welfare, and equity in personalized pricing. Proceedings of the 2021 ACM Conference on Fairness, Accountability, and Transparency. 296-314.

- Keskin and Zeevi (2014) Keskin, N Bora, Assaf Zeevi. 2014. Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies. Operations Research, 62 (5), 1142-1167.

- Keskin and Zeevi (2017) Keskin, N Bora, Assaf Zeevi. 2017. Chasing demand: Learning and earning in a changing environment. Mathematics of Operations Research, 42 (2), 277-307.

- Kivinen and Warmuth (1997) Kivinen, Jyrki, Manfred K Warmuth. 1997. Exponentiated gradient versus gradient descent for linear predictors. Information and Computation, 132 (1), 1-63.

- Klein et al. (2020) Klein, Robert, Sebastian Koch, Claudius Steinhardt, Arne K Strauss. 2020. A review of revenue management: Recent generalizations and advances in industry applications. European journal of operational research, 284 (2), 397-412.

- Ma et al. (2022a) Ma, Wanteng, Ying Cao, Danny HK Tsang, Dong Xia. 2022a. Optimal regularized online convex allocation by adaptive re-solving, Preprint, submitted September 1, https://arxiv.org/abs/2209.00399.

- Ma et al. (2022b) Ma, Will, Pan Xu, Yifan Xu. 2022b. Group-level fairness maximization in online bipartite matching. Proceedings of the 21st International Conference on Autonomous Agents and Multiagent Systems. 1687-1689.

- Maglaras and Meissner (2006) Maglaras, Constantinos, Joern Meissner. 2006. Dynamic pricing strategies for multiproduct revenue management problems. Manufacturing & Service Operations Management, 8 (2), 136-148.

- Miao and Wang (2021) Miao, Sentao, Yining Wang. 2021. Network revenue management with nonparametric demand learning: -regret and polynomial dimension dependency, Preprint, submitted October 25, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3948140.

- Miao et al. (2021) Miao, Sentao, Yining Wang, Jiawei Zhang. 2021. A general framework for resource constrained revenue management with demand learning and large action space, Preprint, submitted May 10, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3841273.

- Miller (2015) Miller, Claire Cain. 2015. When algorithms discriminate. The New York Times, 9 (7), 1.

- Nash Jr (1950) Nash Jr, John F. 1950. The bargaining problem. Econometrica: Journal of the econometric society, 155-162.

- Rusmevichientong and Tsitsiklis (2010) Rusmevichientong, Paat, John N Tsitsiklis. 2010. Linearly parameterized bandits. Mathematics of Operations Research, 35 (2), 395-411.

- Talluri et al. (2004) Talluri, Kalyan T, Garrett Van Ryzin, Garrett Van Ryzin. 2004. The theory and practice of revenue management. Springer.

- Wang and Wang (2022) Wang, Yining, He Wang. 2022. Constant regret resolving heuristics for price-based revenue management. Operations Research, 70 (6), 3538-3557.

- Wang et al. (2014) Wang, Zizhuo, Shiming Deng, Yinyu Ye. 2014. Close the gaps: A learning-while-doing algorithm for single-product revenue management problems. Operations Research, 62 (2), 318-331.

- Zhang et al. (2020) Zhang, Hong, Lan Zhang, Lan Xu, Xiaoyang Ma, Zhengtao Wu, Cong Tang, Wei Xu, Yiguo Yang. 2020. A request-level guaranteed delivery advertising planning: Forecasting and allocation. Proceedings of the 26th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining. 2980-2988.

- Zhang et al. (2023) Zhang, Qixin, Wenbing Ye, Zaiyi Chen, Haoyuan Hu, Enhong Chen, Yu Yang. 2023. Nearly optimal competitive ratio for online allocation problems with two-sided resource constraints and finite requests. Proceedings of the 40th International Conference on Machine Learning, vol. 202. 41786-41818.

- Zhang et al. (2022) Zhang, Zhiqiang, Pengyi Shi, Amy R. Ward. 2022. Routing for fairness and efficiency in a queueing model with reentry and continuous customer classes. Proceedings of the American Control Conference (ACC).

E-Companion to “ Network Revenue Management with Demand Learning and Fair Resource-Consumption Balancing”

9 Some useful technical lemmas

Lemma 9.1 (Azuma-Hoeffding Inequality)

Let be a martingale difference sequence for which there are constants such that almost surely for all . Then, for all ,

Recall that , and . Thus we have . Noting , and and applying the Theorem 2 in Abbasi-Yadkori et al. (2011), we have the following confidence ellipsoid lemma.

Lemma 9.2

Recall that , for any , with probability at least , for all we have

| (37) |

10 Proofs Omitted in Section 2

10.1 Proof of Proposition 2.1

Proof 10.1

Proof of Proposition 2.1. By the constraint of Eq. (1) , it is easy to obtain . Therefore,

With the concavity of by Jenson’s inequality we obtain

Therefore, we have

With the concavity of and , using Jenson’s inequality again, we have

where the last inequality is due to Eq. (4). Combining the above inequalities, we complete the proof.\Halmos

10.2 Assumptions Validation of the Balancing Regularizers

We will prove the balancing regularizers proposed in Section 2.1 satisfy Assumption 2.1 (we only validate Assumption 1.1 and Assumption 1.3, since Assumption 1.2 can be easily validated).

Example 1: Weighted Max-min Fairness Regularizer: .

We first show is -Lipschitz continuous with respect to the -norm in the following way,

Next, we will show the concavity of . For any and , we have

Example 2: Group Max-min Fairness Regularizer: , where .

We first show is -Lipschitz continuous with respect to the -norm in the following way,

Next, we will show the concavity of . For any and , we have

Example 3: Range Fairness Regularizer:. Example 4: Load Balancing Regularizer:.

We have shown is -Lipschitz continuous with respect to the -norm and concave. By this fact, it is easy to note that Example 3 and Example 4 also satisfy Assumption 2.1. \Halmos

11 Proofs Omitted in Section 3

11.1 Proof of Lemma 4.1

11.2 Proof of Corollary 4.2

Proof 11.2

Proof of Corollary 4.2. The proof will be conditioned on when we find a feasible for all (which happens with probability by Lemma 4.7) and the desired event of Lemma 4.1.

For each and , we first upper bound . Note that

Therefore, we only need to show that to prove that . For every , let , and we verify that

Here, the first inequality is due to Cauchy-Schwarz, and the second inequality is due to that .

We now upper bound as follows.

where in the inequality, we upper bound by due to the paragraph above.

We finally upper bound . Note that

where the second inequality is by the definitions of and , and the third inequality uses the upper bounds for and derived in the previous parts of this proof. \Halmos

11.3 Proof of Lemma 4.3

Proof 11.3

Proof of Lemma 4.3. Since , for every , . By this fact, we have

| (46) |

Note and recall the definition of and we have

| (47) | |||

| (48) |

Since , we have

| (50) |

where the first equility is due to and the last inequality is due to when .

Therefore , with Eq. (50) we have

| (51) |

where the first inequality is due to Cauchy-Schwarz inequality, the third inequality is due to the AM-GM inequality, and the last inequality is due to .

11.4 Proof of Lemma 4.6

Lemma 11.4

With probability at least , for all , we have , where is the underlying true parameter and .

Proof 11.5

Lemma 11.6

When the desired event in Lemma 11.4 happens , for any .

Proof 11.7

Proof of Lemma 11.6

Note that by the triangle inequality, for all and we have

| (57) |

When the desired event in Lemma 11.4 happens, by Eq. (55), for any and it holds that

| (58) |

And for any , we can upper bound as follows

| (59) |

where the first inequality is due to for any symmetric matrix , the second inequality is due to , and the last inequality is due to .

Now we need to prove the third constraint is satisfied by . To facilitate our discussion let be the square matrix after deleting the last column of .

Since we have the assumption that , we only need to show to prove that .

By the fact that and if is symmetric, we have

where the last inequality is due to .

Proof 11.8

Proof of Lemma 4.6. Note that , For all , we have

And thus, for , it holds that

Therefore, we have , i.e., when treating the matrix as an -dimensional vector.

12 Proof of Theorem 6.1

This section is devoted to the proof of Theorem 6.1, which is detailed in 5 steps. Recall that is the stopping time till when the inventory levels of all resources remain positive. For convenience, for , we define

| (62) |

For , we set all relevant quantities to zeros:101010We will treat as a symbol rather than a function of for .

By Eq. (5), we have that

| (63) |

12.1 Step I: Replacing with and Introducing

The first step is to replace the real demand on the Right-Hand-Side of Eq. (63) with the expected demand so that the resulting expression is easier to deal with. By applying the Azuma-Hoeffding inequality and a union bound, we have the following lemma.

Lemma 12.1

With probability at least , it holds that