Sharp hypotheses and organic fiducial

inference

Russell J. Bowater

Independent researcher,

Doblado 110, Col. Centro, City of Oaxaca, C.P. 68000, Mexico.

Email address: as given on arXiv.org. Twitter profile:

@naked_statist

Personal website:

sites.google.com/site/bowaterfospage

Abstract:

A fundamental class of inferential problems are those characterised by there having been a

substantial degree of pre-data (or prior) belief that the value of a model parameter was

equal or lay close to a specified value , which may, for example, be

the value that indicates the absence of a treatment effect or the lack of correlation between two

variables.

This paper puts forward a generally applicable ‘push-button’ solution to problems of this type that

circumvents the severe difficulties that arise when attempting to apply standard methods of

inference, including the Bayesian method, to such problems.

Usually the only input of major note that is required from the user in implementing this solution

is the assignment of a pre-data or prior probability to the hypothesis that the parameter

lies in a narrow interval that is assumed to contain the

value of interest .

On the other hand, the end result that is achieved by applying this method is, conveniently, a

joint post-data distribution over all the parameters of the

model concerned.

The proposed method is constructed by naturally combining a simple Bayesian argument with an

approach to inference called organic fiducial inference that was developed in a number of earlier

papers. To begin with, the main theoretical arguments underlying this combined Bayesian and

fiducial method are presented and discussed in detail. Various applications and useful extensions

of this methodology are then outlined in the latter part of the paper. The examples that are

considered are made relevant to the analysis of clinical trial data where appropriate.

Keywords:

Almost sharp hypothesis; Bayes factors; Bayesian analogies; Gibbs sampler; Incompatible

conditional distributions; Lack of pre-data knowledge; Model comparison; Organic fiducial

inference; Physical probability; Post-data predictive densities.

1 Introduction

The aim of this paper is to address a general type of problem in statistical inference that was also the focus of attention in Bowater (2019c). Therefore, let us begin in the same way that this earlier paper began with a definition of a sharp and almost sharp hypothesis, and an introduction to the specific problem of interest. For the moment, we will suppose that our overall aim is to make inferences about an unknown parameter on the basis of a data set that was generated by a sampling model that depends on the true value of .

Definition 1: Sharp and almost sharp hypotheses

The hypothesis that the parameter lies in an interval will be defined as a sharp hypothesis if , and as an almost sharp hypothesis if the difference is very small in the context of our general uncertainty about after the data have been observed.

Clearly, any importance attached to a hypothesis of either of these two types should not generally have a great effect on the way that we make inferences about on the basis of the data if there had been no exceptional reason to believe that it would have been true or false before the data were observed. Taking this into account, it will be assumed that we are in the following scenario.

Definition 2: Scenario of interest

This scenario is characterised by there having been a substantial degree of belief before the data were observed, i.e. a substantial pre-data belief, that a given sharp or almost sharp hypothesis about the parameter could have been true, but if, on the other hand, this hypothesis had been conditioned to be false, i.e. if had been conditioned not to lie in the interval , then there would have been very little or no pre-data knowledge about this parameter over all of its allowable values outside of this interval. In this scenario, the hypothesis in question will be referred to as the special hypothesis.

Perhaps some may try to dismiss the importance of this type of scenario, however trying to make data-based inferences about any given parameter of interest in such a scenario represents one of the most fundamental problems of statistical inference that arise in practice. Let us consider the following examples.

Example 1.1: Intervening in a system

If is a parameter of one part of a system, and an intervention is made in a second part of the system that is arguably completely disconnected from the first part, then there will be a high degree of belief that the value of will not change as a result of the intervention, i.e. there will be a strong belief in a sharp hypothesis about what will be the change in the value of .

Example 1.2: A randomised-controlled trial

Let us imagine that a sample of patients is randomly divided into a group of patients, namely the treatment group, that receive a new drug B, and a group of patients, namely the control group, that receive a standard drug A. We will assume that patients in the treatment group experience a given adverse event, e.g. a heart attack, in a certain period of time following the start of treatment, and that patients in the control group experience the same type of event in the same time period. On the basis of this sample information, it will be supposed that the aim is to make inferences about the relative risk , where and are the population proportions of patients who would experience the adverse event when given drug B and drug A respectively. Now, if the action of drug B on the body is very similar to the action of drug A, which is in fact often the case in practice when a new drug is being compared with a standard drug in this type of clinical trial, then there may well have been a strong pre-data belief that this relative risk would be close to one, or in other words, that the almost sharp hypothesis that the relative risk would lie in a narrow interval containing the value one would be true.

It would appear that a common way to deal with there having been a strong pre-data belief that a sharp or almost sharp hypothesis was true is to simply ignore the inconvenient presence of this belief. However, doing so means that inferences based on the observed data will often not be even remotely honest. On the other hand, a formal method of addressing this issue that has received some attention is the Bayesian method. We will now take a quick look at how this method would work in a simple example.

Example 1.3: Application of the Bayesian method

Let us suppose that we are interested in making inferences about the mean of a normal distribution that has a known variance on the basis of a random sample of values drawn from the distribution concerned. It will be assumed that we are in the scenario of Definition 2 with the special hypothesis of interest being the sharp hypothesis that . Under the Bayesian paradigm, it would be natural to incorporate any degree of pre-data belief that equals zero into the analysis of the data by assigning a positive prior probability to this hypothesis.

However, the only generally accepted way of expressing a lack of pre-data knowledge about a model parameter under this paradigm is the controversial strategy of placing a diffuse proper or improper prior density over the parameter concerned. Taking this into account, let us assume, without a great loss of generality, that the prior density function of conditional on is a normal density function with a mean of zero and a large variance .

The inadequacy of the strategy in question is clearly apparent in the uncertainty there would be in choosing a value for the variance , and this issue becomes very hard to conceal after appreciating that the amount of posterior probability given tothe hypothesis that is highly sensitive to changes in this variance. For example, the natural desire to allow the variance to tend to infinity results in the posterior probability of this hypothesis tending to one for any given data set and any given positive prior probability that is assigned to equalling zero.

It can be easily argued, therefore, that the application of standard Bayesian theory to the case just examined has an appalling outcome. Moreover, applying the Bayesian strategy just described leads to outcomes of a similar type in cases where the sampling density of the data given the parameter of interest is not normal, and/or the prior density of this parameter has a more general form, and also, importantly, in cases where the special hypothesis is an almost sharp rather than simply a sharp hypothesis. This clearly gives us a strong motivation to look for an alternative method for making inferences about in the scenario of interest.

One such method was proposed in Bowater and Guzmán-Pantoja (2019a) and further developed in Bowater (2019c), where it was referred to as being a special formalisation of what was called bispatial inference. In particular, this method is based on the interpretation of one-sided P values that correspond to a composite null hypothesis that incorporates the special hypothesis of the scenario outlined in Definition 2. No doubt many will find that this method has a certain degree of intuitive appeal. However, the foundational justification given in Bowater (2019c) as to why small P values should be viewed as discrediting the type of null hypothesis in question was inadequate. Also, it was not completely clear in Bowater (2019c) how, by taking into account the size of the type of one-sided P value under discussion, an appropriate post-data probability can in practice be assigned to the null hypothesis to which it corresponds, which was one of the aims of the method being referred to in this earlier paper.

In this paper, another type of method will be proposed for tackling the problem of inference in question. It is reasonable to hope that this method will be regarded as representing a natural and elegant way of addressing this problem of inference that is universally much better than the approaches based on standard Bayesian inference and on the notion of bispatial inference that were just mentioned. In particular, it is a method that is based on using a simple Bayesian argument in combination with a general approach to inference that was originally presented and named as organic fiducial inference in Bowater (2019b) and then further discussed in Bowater (2020, 2021a) before being clarified and modified in Bowater (2021b).

Let us now briefly describe the structure of the paper. In the next five sections (Sections 2.1 to 2.5), the main theoretical arguments are presented for the method of inference that will be advocated in the case where the sampling model depends on only one unknown parameter. More specifically, the Bayesian component of the line of reasoning in question is introduced and discussed in Section 2.2, while a brief summary of organic fiducial inference is given in Section 2.3. These two approaches to inference are then brought together in Sections 2.4 and 2.5 with the aim of solving the inferential problem of interest. Examples of the application of the resulting method of inference are then presented in Sections 3 and 4.

Following on from this, a methodological adjustment is put forward in Section 5 that enables undesirable discontinuities in the post-data density function of the parameter of interest to be smoothed out. An example of the application of the adjusted method in question is then given in Section 6.

In the second part of the paper, two different ways of extending the originally proposed and the adjusted method of inference just mentioned to the case where all model parameters are unknown are developed. More specifically, in Section 7, a generalisation to address the case in question is presented that is based on determining a joint post-data distribution over all the model parameters by first constructing a set of full conditional post-data distributions for these parameters. An example of the application of this extended methodology is then given in Section 8. As an alternative to this approach, a way of dealing with the case where all model parameters are unknown is outlined in Section 9 that represents a more direct extension to the originally proposed method for the case where only one parameter is unknown. Examples of the application of this alternative methodology are then presented in Sections 10 and 11. The final section of the paper (Section 12) contains some discussion of related approaches to inference and an indication is given as to how the methodology that has been put forward could be generalised further.

2 Organic fiducial inference applied to the problem of interest

2.1 Overall assumptions

Attention will be focused in the rest of this paper on a general version of the problem of inference that was outlined in the Introduction. In particular, we will be interested in the problem of making inferences about a set of parameters , where each is a one-dimensional variable, on the basis of a data set that was generated by a given sampling model that is fully specified by this set of parameters. Let the joint density or mass function of the data given the true values of the parameters be denoted as .

For the moment, though, it will be assumed that the only unknown parameter on which the sampling density depends is the parameter , either because there are no other parameters in the model, or because all the other parameters are known. Under this assumption, we will again suppose that the scenario of interest is the scenario outlined in Definition 2. To clarify, the special hypothesis in this scenario will be assumed to be the hypothesis that the parameter lies in a given narrow interval, which we will now denote as the interval .

2.2 A comparison of two Bayesian arguments

As was the case in Bowater (2020, 2021a, 2022), it will be assumed that the Bayesian approach to inference is justified in any given situation by making an analogy between the uncertainty that surrounds the validity of hypotheses that are relevant to the problem of inference being studied and the uncertainty that surrounds the outcome of a well-understood physical experiment, e.g. the outcome of randomly drawing a ball out of an urn of balls or the outcome of randomly spinning a wheel. To clarify, specific outcomes of an experiment of this type and unions of these outcomes will be regarded as having physical probabilities. What we exactly mean here by a physical probability agrees with the definition of this type of probability that was given in Bowater (2022).

A full Bayesian analysis of the problem of inference outlined in Section 2.1 would require that a prior density function is placed over all values of the only unknown parameter . Here an analogy would therefore need to be made between, on the one hand, our uncertainty, before the data set is observed, both about the value of and the values that will make up this data set, and on the other hand, our uncertainty about the outcome of a physical experiment that is designed to generate a value of and the values in the data set by drawing these values from the joint density of and that is specified by:

where is the sampling density defined in Section 2.1.

However, as discussed in the analysis of Example 1.3, it would arguably be very difficult to elicit the prior density under the assumption being made that we are in the scenario of Definition 2. Moreover, it can be argued that in this scenario, the prior density conditional on not lying in the interval should be treated, in the case where pre-data knowledge about outside of this interval is most lacking, as being a completely unknown density function. Therefore, we may well be naturally led to consider dealing with the problem at hand by performing a sensitivity analysis of the posterior density of the parameter over all possible forms for the prior density that are consistent with a given prior probability being assigned to the hypothesis that lies in the interval .

If this strategy was applied to Example 1.3 then, as was shown in Berger and Sellke (1987), the lower limit on the posterior probability of the hypothesis that lies in the interval , i.e. the hypothesis that the mean equals zero in this example, would be given by the expression:

where is the prior probability that equals zero and is the sample mean. This lower limit on the posterior probability in question is achieved when the prior density of , apart from placing a probability mass of at the point , also places a probability mass of at the point . On the other hand, as was the case for the strategy outlined in Example 1.3, the upper limit on the posterior probability of the mean being equal to zero would be equal to one, and therefore it could be argued that the current strategy being considered could not, in general, be regarded as being practically viable.

Nevertheless, in searching for an alternative strategy we do not need to move completely away from the Bayesian paradigm. In particular, let us make an analogy of the type just discussed in which the prior density of conditioned on not lying in the interval is essentially treated as though it does not exist. However, the precise analogy that we need to make depends on the scenario in which we find ourselves. Therefore, let us give a more specific definition of the scenario of interest by assuming that not only are we in the scenario of Definition 2, but that if, before the data were observed, the parameter had been conditioned to lie in the interval , then very little or nothing would have been known about where in this interval the parameter would lie.

Under these assumptions, we will make an analogy between, on the one hand, our pre-data uncertainty both about the value of and the values that will make up the data set , and on the other hand, our uncertainty about the outcome of a physical experiment that will randomly select either a value or a value for the parameter , and then will generate the data by substituting this chosen value of into the formula of the sampling density . The key detail that establishes this analogy as being a generally acceptable one to make is that it will be assumed that we know that the value lies in the interval and that the value lies outside of this interval, but apart from this, the values and will be assumed to be completely unknown to us. To clarify, in conducting the physical experiment of interest, the joint density of and the values in the data set would be given by:

| (1) |

in which

| (2) |

where is a specified probability. Given our lack of information concerning the values of and , the probability is in effect our prior probability that lies in the interval , while is in effect our prior probability that lies outside of this interval.

However, in using the analogy that has just been outlined, we can not form the posterior probability of lying in the interval and the posterior probability of not lying in this interval by simply conditioning the joint density of and the data given in equation (1) on the data that is actually observed. This is because, as a consequence of the values and being unknown, the sampling densities and will also be unknown. Nevertheless, it is perfectly reasonable to contemplate estimating the densities and using all the information that is available to us. As will be detailed in Section 2.4, we will choose to estimate these densities using organic fiducial inference. Before that though, with the aim of giving an adequate background to this later section, we will present, in the next section, a brief general overview of the theory of organic fiducial inference.

2.3 An overview of organic fiducial inference

As mentioned in the Introduction, organic fiducial inference is a theory of inference that was developed in Bowater (2019b, 2020, 2021b). Also, precursory work that forms part of the basis of this theory can be found in Bowater (2017, 2018). For a complete account of this theory of inference, it is recommended that Bowater (2019b) is studied with careful attention given to the modifications to this theory that are presented in Bowater (2021b). In this section, we will simply give a brief overview of the methodology that underlies organic fiducial inference in the case where the parameter is the only unknown parameter in the sampling model, which is of course the case of current interest.

Fiducial statistics

Let be a set of univariate statistics that together form a sufficient or approximately sufficient set of statistics for the parameter . To clarify, a set of statistics will be defined as being an approximately sufficient set of statistics for if conditioning the distribution of the data set of interest on this set of statistics leads to a distribution of this data set that does not depend heavily on the value of the parameter .

Now, if a given set , as just defined, only contains one statistic that is not an ancillary statistic, then that statistic will be called the fiducial statistic of this set . Assuming that the set is of this nature, we will denote all the statistics in except for the statistic as the set of statistics , and we will refer to the statistics in this set as being the ancillary complements of . Note that often it may be possible to find a set that consists of just a single sufficient statistic for , and of course in these cases, the fiducial statistic will be this sufficient statistic and the set will be empty.

Data generating algorithm

Independent of the way in which the data set was actually generated, it will be assumed that this data set was generated by a specific algorithm called the data generating algorithm.

After generating the values of the ancillary complements , if any exist, of a given fiducial statistic , this algorithm proceeds by determining a value for this latter statistic by setting it equal to a function that depends on the parameter , the values and an already generated value of a variable that is referred to as the primary random variable (primary r.v.). The density function of , which we will denote as the density , does not depend on the parameter . In the final step of the algorithm the data set is randomly drawn from the sampling density or mass function conditioned on the statistics and being equal to their already generated values.

Types of fiducial argument

In the theory of organic fiducial inference, the fiducial argument, which is usually considered to be a single argument, is broken down into three sub-arguments referred to as the strong, moderate and weak fiducial arguments.

Strong or standard fiducial argument

This is the argument that the density function of the primary r.v. after the data have been observed, i.e. the post-data density function of , should be equal to the pre-data density function of , i.e. the density .

Moderate fiducial argument

It will be assumed that this argument is only applicable if, on observing the data , there exists some positive measure set of values of the primary r.v. over which the pre-data density function was positive, but over which the post-data density function of , which will be denoted as the density function , is necessarily zero. Under this condition, it is the argument that, over the set of values of for which the density function is necessarily positive, the relative height of this function should be equal to the relative height of the density function , i.e. the heights of these two functions should be proportional.

Weak fiducial argument

This argument will be assumed to be only applicable if neither the strong nor the moderate fiducial argument is considered to be acceptable. By using this argument, the most appropriate post-data density of , i.e. the density , can be determined in the most general type of scenario, i.e. determined with regard to the most general form of a function of specified before the data were observed that is referred to as the global pre-data function of . Let us now define this latter function.

Global pre-data (GPD) function

The global pre-data (GPD) function is used to express pre-data knowledge, or a lack of such knowledge, about the unknown parameter . More specifically, this function may be any given non-negative and upper bounded function of the parameter . It is a function that only needs to be specified up to a proportionality constant, in the sense that, if it is multiplied by a positive constant, then the value of the constant is redundant.

Local pre-data (LPD) function

The local pre-data (LPD) function is also used to express pre-data knowledge about the parameter , but in a way that is different from the way this knowledge is expressed by the GPD function. More specifically, it may be any given non-negative function of the parameter that is locally integrable over the space of this parameter. Similar to a GPD function, a LPD function only needs to be specified up to a proportionality constant.

The role of the LPD function is to facilitate the completion of the definition of the joint post-data density function of the primary r.v. and the parameter in cases where using either the strong or moderate fiducial argument alone is not sufficient to achieve this. For this reason, the LPD function is in fact redundant in many situations.

Principles for defining univariate fiducial density functions

Given the data , there are two mutually consistent principles in the theory being considered for defining the fiducial density function of the parameter conditional on all other parameters being known, i.e. the density function . Let us briefly discuss these two principles.

Principle 1 for defining the density

Loosely speaking, this principle applies if, after the data have been observed, the function that forms part of the data generating algorithm outlined earlier defines a bijective mapping between the set of all possible values of the primary r.v. , which we will denote as the set , and the set of all possible values of the parameter . Under this condition, the fiducial density is directly defined by the post-data density of , i.e. the density , which is assumed to be given by the following expression:

| (3) |

in which is the value of the parameter that maps onto the value of the variable according to the definition of the function , and where is the GPD function of defined earlier and is a normalising constant.

Principle 2 for defining the density

This principle can often be applied in situations where, after the data have been observed, various values of the parameter are consistent, according to the definition of the function , with any given value of the primary r.v. . The main step that underlies this principle is to form a joint density of and that is based on the marginal density of being the post-data density defined by equation (3) and the conditional density of given that equals a specific value being determined using the Bayesian paradigm on the basis of the pre-data information that is expressed by what was earlier defined to be a LPD function . The result of marginalising this joint density of and with respect to the variable is then quite naturally regarded as being the fiducial density .

An extension to Principle 2

In situations where neither Principle 1 nor the basic version of Principle 2 just referred to can be applied, the use of an extended version of Principle 2 was advocated in Sections 7.2 and 8 of Bowater (2019b). To calculate the fiducial density using this extension to Principle 2, we first apply the version of Principle 2 just summarised to determine a preliminary version of this fiducial density of that would be appropriate in a general scenario where nothing or very little was known about the parameter before the data were observed. Let this preliminary version of the fiducial density in question be denoted as . The fiducial density of that is actually of concern to us, i.e. the density , is then given by the expression:

| (4) |

where is the GPD function of that corresponds to the genuine scenario of interest, and is a normalising constant. Observe that if, in this definition of the fiducial density , the preliminary fiducial density was derived using Principle 1 rather than Principle 2, then the resulting density ought to be equivalent to what it would have been if it had been derived directly by using Principle 1.

2.4 Estimating the densities and

Let us return to the problem of interest that was last discussed in Section 2.2. In particular, we now will consider the question of how to estimate the densities and . First, let us recall that these two sampling densities would be known if the values of and were known. Second, since in the Bayesian analogy being used the values of and are, by contrast, assumed to be known, the door is not closed on the possibility of using the data to estimate the densities and , which to clarify, means estimating the sampling density under the assumption that lies in the interval and that does not lie in this interval, respectively. Therefore, let us explore the idea of estimating the two sampling densities and using the post-data predictive density of a future data set that is the same size as the observed data set under the assumption that and that , respectively.

We should point out, though, that it would be unwise to try to derive the post-data predictive density of the data under each of these two assumptions by using the Bayesian paradigm. The first reason for this is that, as has already been discussed, it is very difficult to use prior densities of the parameter to express the type of pre-data knowledge that we would have about in the scenario of interest under the two assumptions in question, i.e. to express that nothing or very little would have been known about before the data were observed if had either been conditioned to lie inside or outside of the interval . The second reason for not using the Bayesian paradigm to perform the current task is that the analogies that would need to be made to justify the use of this paradigm in constructing the post-data predictive densities in question would effectively imply that the overall Bayesian analogy that would be used would be the same as the first type of Bayesian analogy detailed in Section 2.2. In other words, the way being presently considered of tackling the problem of inference outlined in Section 2.1 would be effectively reduced to the type of full Bayesian analysis of this problem that was discussed in Section 2.2. In an analysis of this type, the overall prior density of that is implied by the underlying assumptions that are made would clearly need to be updated to an overall posterior density of by means of a standard application of Bayes’ theorem. The major drawbacks of conducting such a full Bayesian analysis of the problem of interest have, of course, already been carefully laid out (see the Introduction and Section 2.2).

To construct an appropriate post-data predictive density of the data either under the condition that or that , we will therefore consider using the theory of organic fiducial inference that was summarised in the previous section. This approach has the advantage that it offers a natural way in which a lack of pre-data knowledge about the parameter can be expressed when is either conditioned to lie inside or outside of the interval , and also, the use of this approach does not conflict with the Bayesian analogy that we are making as part of the overall strategy that is being adopted, i.e. the second type of Bayesian analogy detailed in Section 2.2.

The two post-data predictive densities of the data that we need to determine, which are now more specifically the fiducial predictive densities of the data that result from separately applying the condition that and that , will be denoted as being the density functions and , respectively. In broad terms, these two fiducial predictive densities are defined as follows:

| (5) |

and

| (6) | |||||

where is the general sampling density as defined in Section 2.1 and the densities and are the fiducial densities of under the condition that lies in the interval and that does not lie in this interval, respectively.

Since the sampling density is known, we only need to determine the fiducial densities and in the expressions just given to be able to obtain the predictive densities of the data that are of interest. In doing this, let us first observe that as implies that must lie in the interval , it follows that, with regard to determining the fiducial density , the GDP function must be equal to zero outside of the interval in question. On the other hand, as implies that must lie outside of the interval , it follows that, with regard to determining the fiducial density , the GDP function must be equal to zero inside the interval in question. Given that it has been assumed that nothing or very little would have been known about the parameter before the data were observed if had either been conditioned to lie inside or outside of the interval , it is quite natural to specify the two GPD functions for that are of interest so that they are equal to a positive constant over the intervals where we know that they are not equal to zero. Therefore, we will define the GPD function of as:

| (7) |

and as:

| (8) |

with regard to the construction of the fiducial densities and , respectively, where is any given positive constant. Note that the two GPD functions just defined would be regarded as being neutral GPD functions according to the terminology of Bowater (2019b).

If Principle 1 summarised in the previous section can be applied, then using this principle on the basis of the GPD functions of given in equations (7) and (8) would imply that the fiducial densities and would, in general, be derived by using the moderate fiducial argument as defined earlier. Furthermore, if Principle 1, Principle 2 or the extension to Principle 2 described in Section 2.3 can be applied, then these fiducial densities would be defined by the general expression for the fiducial density given in equation (4).

Observe that, if the fiducial densities and are determined by Principle 2 or the extension to Principle 2 in question, then a LPD function for would be required to determine the fiducial density in equation (4). However, since this latter fiducial density needs to be derived under the assumption that there was no or very little pre-data knowledge about the parameter , it may be difficult to specify a single LPD function for that is representative of our pre-data beliefs about . For this reason, it may often be of benefit to analyse how making different but nevertheless sensible choices for the LPD function of affects the form of the density , and therefore in turn, the forms of the densities and .

2.5 Returning to the Bayesian analogy of interest

Under the assumptions that define the physical experiment on which the Bayesian analogy of current interest is based, i.e. the second type of Bayesian analogy detailed in Section 2.2, the posterior distribution of the parameter is obtained by conditioning the joint distribution of and the data that is defined by equations (1) and (2) on the data that is actually observed. In particular, doing this leads to the posterior probabilities that and that being defined as:

| (9) |

and

respectively, where the notation being used here is the same as used in equations (1) and (2).

On substituting the fixed but unknown sampling densities and in equation (9) by the estimates of these densities that were put forward in the previous section, i.e. the fiducial predictive density of the future data set in the cases where and where , the posterior probabilities of the hypotheses that and that just given, which were derived purely under the Bayesian paradigm, become simply justifiable post-data probabilities of these hypotheses that are defined as:

| (10) |

and

| (11) |

respectively, where the densities and are as defined in equations (5) and (6). Observe that, according to the definitions of the values and that we have been using, the probability is, in effect, our post-data probability that lies in the interval and the probability is, in effect, our post-data probability that does not lie in this interval.

To obtain a post-data density function of over the whole of the real line it is perfectly consistent with the line of reasoning being currently adopted that the post-data densities of that result from separately applying the condition that lies in the interval and that does not lie in this interval are, respectively, the fiducial densities and defined in the previous section. Given this natural assumption, it is clear that the complete definition of the post-data density of is given by the expression:

or equivalently by the expression:

| (12) | |||||

3 First example: Inference about a normal mean with variance known

To give a first example of the application of the method of inference outlined in the previous sections, let us apply this method to the problem of inference referred to in Example 1.3 in the Introduction, i.e. the problem of making inferences about a normal mean when the population variance is known.

With the aim of providing a context for this problem, let us imagine that a random sample of patients are being constantly monitored with regard to the concentration of a certain chemical in their blood. In this scenario, the data value will be assumed to be simply the measurement of this concentration for the th patient at a time point minus the same type of measurement for this patient taken at a time point , where the time point is immediately before the patient is subjected to some kind of intervention and the time point is immediately after this intervention. Furthermore, we will suppose that the data values are normally distributed around a population mean , and also that the sample size is large enough such that it is acceptable to use the sample vari-ance as a substitute for the population variance .

Finally, it will be imagined that the intervention in question is not expected to affect by very much or at all the concentration of the chemical of interest for each of the patients concerned. Therefore, a substantial degree of pre-data belief would exist that the population mean change in this concentration in going from the time point to the time point will be very small. More specifically, it will be assumed that we find ourselves in the scenario of Definition 2 with the parameter of interest in this scenario now being and with the special hypothesis being that lies in the interval , where is a small non-negative constant.

As clearly the sample mean is a sufficient statistic for , it can therefore be assumed to be the fiducial statistic in applying the theory of organic fiducial inference as summarised in Section 2.3. Based on this assumption, the function that forms part of the data generating algorithm described in Section 2.3 can be expressed as:

where the primary r.v. , which means that it is being assumed that the fiducial statistic is determined by setting equal to its already generated value in the formula: .

If, with regard to the construction of the fiducial densities and, the GPD functions of are defined according to equations (7) and (8) respectively, then these fiducial densities will be derived in the present case under Principle 1 described in Section 2.3 by using the moderate fiducial argument. As a result, it turns out that the fiducial densities in question, i.e. the fiducial densities and in the present case, are obtained by conditioning the normal density of given by:

on the event that and the event that , respectively.

Taking into account that the sampling density of every value in the data set , i.e. the

density for , is a normal density with mean and variance

, the fiducial predictive densities and

, i.e. the densities

and

in the present case, are defined by the

expressions in equations (5) and (6).

On eliciting a value for the prior probability , which in the present case is the

prior probability that , we can, as a next

step, use the expression in equation (10) to determine the post-data probability

, i.e. the post-data probability that

.

Just to clarify, under the assumptions of the current example, this post-data probability is

defined as follows:

| (13) |

where is the prior probability that .

Observe that the fiducial predictive densities and will, in general, need to be computed on the basis of a numerical approximation. However, let us take a look at the simple case where , which means that the fiducial predictive densities in question are now of course the densities and . In relation to this case, it can easily be established that the fiducial predictive densities of a future sample mean that result from applying either the condition that or that , i.e. the densities and , are given by the analytical expressions:

and

respectively. On taking into account that the values that make up the future data set are independent normal random values, it can be appreciated that these expressions effectively specify the predictive densities and . We should point out that, since the predictive density is derived under the precise condition that , it is simply the sampling density with the data taking the place of the data .

As a next step, let us substitute the predictive densities and just defined into equation (13). As a result, we obtain the following analytical expression for the post-data probability that equals zero:

| (14) |

where is the prior probability that equals zero.

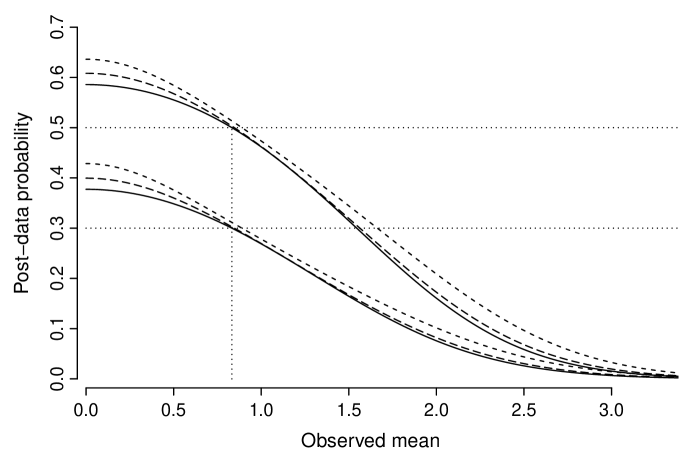

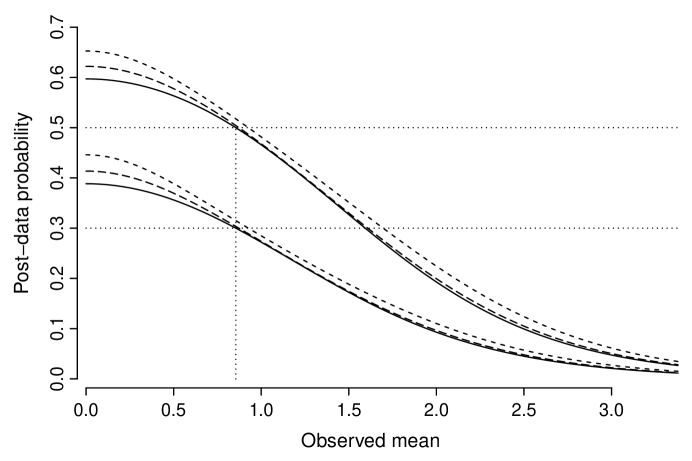

To illustrate the general use of the calculation that appears in equation (13), Figure 1 shows various plots of the post-data probability against the observed mean . This figure is based on the assumption that the variance is equal to the sample size , i.e. it is being assumed that the standard error of the sample mean is equal to one, and for the sake of convenience, this figure is only concerned with the case where , which will be assumed to also be the case of interest in the following discussion. The short-dashed, long-dashed and solid curves that form the three upper curves in Figure 1 correspond to the scenario where the prior probability is equal to 0.5, while the three lower curves in this figure correspond to the scenario where the prior probability is equal to 0.3. The two solid curves in Figure 1 represent plots of against in the case where , and are therefore, in effect, plots of the function given in equation (14) under the assumptions that are currently being made. On the other hand, the two long-dashed curves in this figure correspond to the case where , while the two short-dashed curves correspond to the case where .

Given that setting equal to 0.25 implies that the interval has half the width of the standard error of the sample mean, a realistic choice of would arguably be less than 0.25 since, according to the scenario of Definition 2, the width of the interval of values for that are permitted under the special hypothesis about should be very small in the context of our post-data uncertainty about . However, if we had set to be equal to say 0.1, the plots of the post-data probability against the observed mean would have been almost indistinguishable from the solid curves in Figure 1 for the two values of the prior probability being considered. The reason why plots of against for the case where have been included in Figure 1, i.e. the plots traced out by the short-dashed curves in this figure, is to show what happens when is chosen to be equal to a value that arguably is unrealistically large.

It can be gathered from Figure 1 that not only do large values of the sample mean lead to the post-data probability of the hypothesis that being less than the prior probability of this hypothesis, but small values of the sample mean lead to the reverse being true. For example, in the case where , the post-data probability of the hypothesis that is greater than the prior probability of this hypothesis for values of that are less than 0.8325, independent of the choice that is made for the prior probability in question. Also, in the case where , it is of interest to note that for the three values of the sample mean that correspond to the two-sided P value of the Z test of the null hypothesis that being 0.05, 0.01 and 0.001, the post-data probability would be 0.1716, 0.0488 and 0.0063, respectively, if the prior probability that was 0.5, and would be 0.0816, 0.0215 and 0.0027, respectively, if this prior probability was 0.3.

Under the assumptions that have already been made, we can not only define, for any given and any given prior probability , the post-data probability , but we can also define the post-data density function of over the whole of the real line according to the expression in equation (12). Just to clarify, under the assumptions of the present example, this post-data density function is defined as follows:

| (15) |

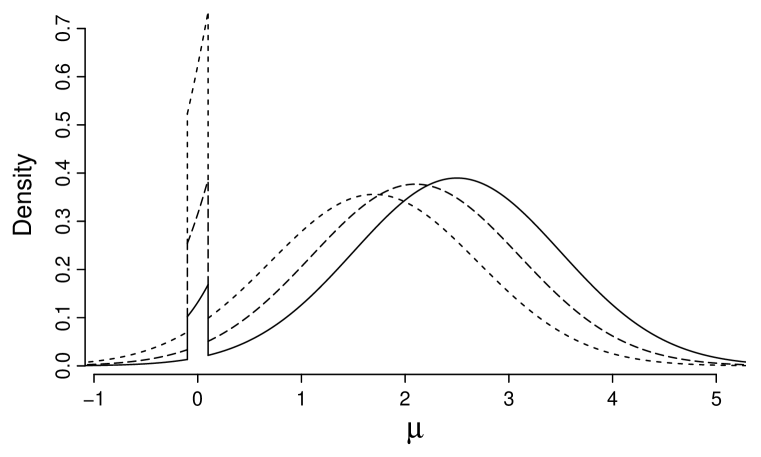

To illustrate the use of the calculation in this equation, Figure 2 shows plots of the post-data density for various values of the observed mean . All plots in this figure correspond to the case where and where the prior probability is equal to 0.3, and again it has been assumed that the variance is equal to the sample size . The short-dashed, long-dashed and solid curves in Figure 2 correspond to the observed mean being equal to 1.7, 2.1 and 2.5, respectively. In keeping with the results that were reported in Figure 1, it can be seen from the present figure that for the range of values of the sample mean being considered, the post-data probability decreases fairly sharply as increases.

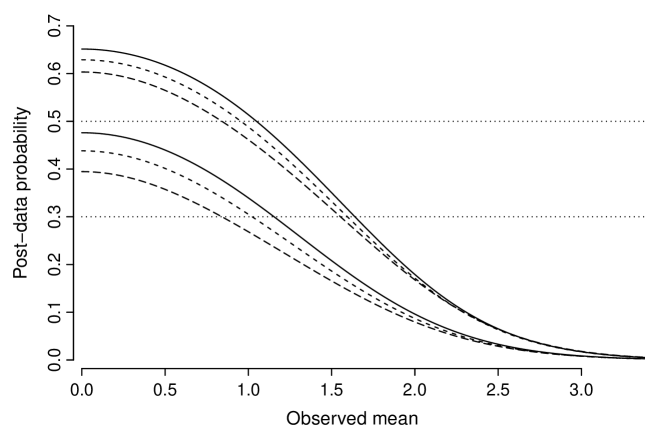

Let us now take a closer look at how sensitive the post-data density is to changes in the value of when the prior probability is held constant. In this regard, Figure 3 shows plots of the post-data probability of lying in the fixed interval , i.e. the probability , against the observed mean for three different values of . More specifically, the solid, short-dashed and long-dashed curves in this figure correspond to the cases where is equal to 0, 0.1 and 0.2, respectively. Similar to Figure 1, the three upper curves in Figure 3 correspond to the case where the prior probability is equal to 0.5, while the three lower curves in this figure correspond to the case where the prior probability is equal to 0.3. Again it has been assumed that .

Taking into account the results reported in Figure 3, we can conclude that if we are interested in determining a post-data probability for being, in some sense, ‘close’ to zero on the basis of the post-data density defined in equation (15), then there will be some degree of insensitivity to the choice made for the value of . However, in trying to achieve this particular goal, it will be generally the case that a reasonable amount of care will nevertheless need to be shown in choosing an appropriate value for . In this regard, the precise choice made for will become a more important issue as the prior probability becomes smaller.

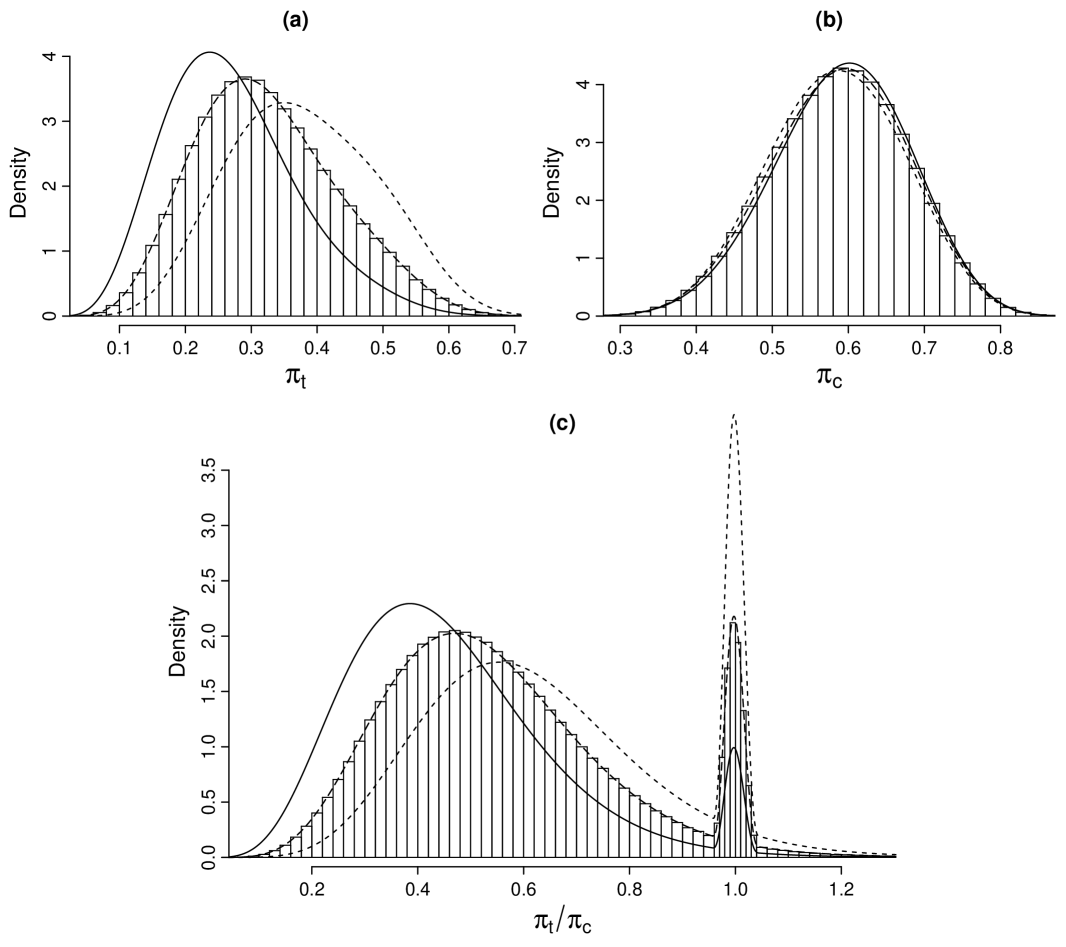

4 Second example: Inference about a binomial proportion

Let us imagine that a random sample of patients are switched from being given a standard drug A to being given a new drug B. After a period of time has passed, they are asked which out of the two drugs A and B they prefer. Let denote the number of patients who prefer drug B to drug A and let denote the number of patients left in the sample after patients who do not express a preference have been excluded. Given the sample proportion , we will suppose that the aim is to make inferences about what this proportion would be in the population, which will be denoted as the proportion , under the standard assumption that, before the experiment took place, the probability of observing any given count was specified by the binomial mass function in this case, i.e. the function:

| (16) |

For a similar reason with regard to the nature of drugs A and B as that given in Example 1.2 of the Introduction, let us also assume that the scenario of Definition 2 applies with the parameter of interest in this scenario now being the proportion and with the special hypothesis being that lies in a narrow interval centred at 0.5, which will be denoted as .

As clearly the observed count is a sufficient statistic for the proportion , it can therefore be assumed to be the fiducial statistic in this example. If it is also supposed that the primary r.v. has a uniform distribution over the interval , then the function that forms part of the data generating algorithm described in Section 2.3 can be expressed as:

| (17) |

where the mass function is as defined in equation (16), which means that it is being assumed that the sample count is determined by setting equal to its already generated value in the formula .

On defining the GPD function of according to equations (7) and (8) in the cases where and respectively, the fiducial densities and referred to in Sections 2.4 and 2.5 are then derived in the present case using the extension to Principle 2 that was outlined in Section 2.3. As explained in Section 2.4, to apply this extension to Principle 2, a LPD function of is required so that the fiducial density in equation (4) can be determined. To give an example, let us assume that this LPD function is defined as follows:

where is a positive constant.

By applying the extension to Principle 2 being referred to, we now can define the fiducial densities and , which in the present case are the densities and , in the following way:

where the conditional density function is given by:

in which is the set of values of that map onto the value for the primary r.v. according to the equation given the observed value of , and where , and are normalising constants, the latter of which clearly must depend on the value of .

Taking into account that the sampling mass function of the count is as defined in

equation (16), the fiducial predictive densities and

, i.e. the densities and in the

present case, are given by the expressions in equations (5) and (6).

On eliciting a value for the prior probability , which in the present case is the

prior probability that , we can, as a next step, use the

expression in equation (10) to determine the post-data probability , i.e. the post-data probability that .

Just to clarify, under the assumptions of the current example, this post-data probability is

defined as follows:

where is the prior probability that . Finally, using this result, the post-data density function of over all allowable values for , i.e. over the interval , can be determined according to the expression in equation (12), which means that, under the assumptions of the present example, this density function is defined as follows:

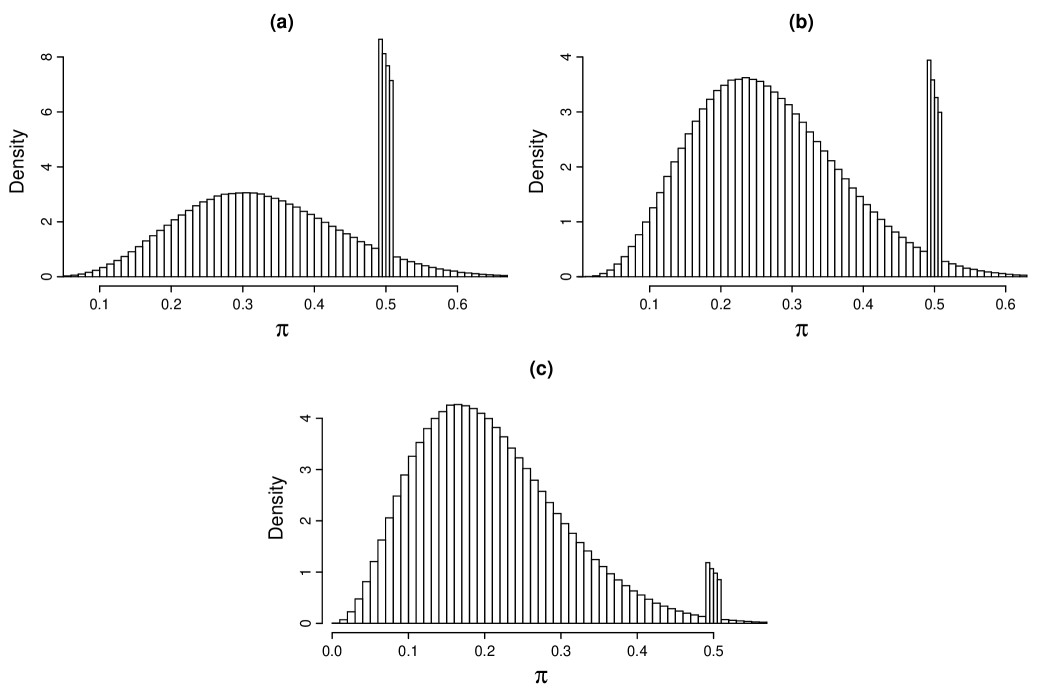

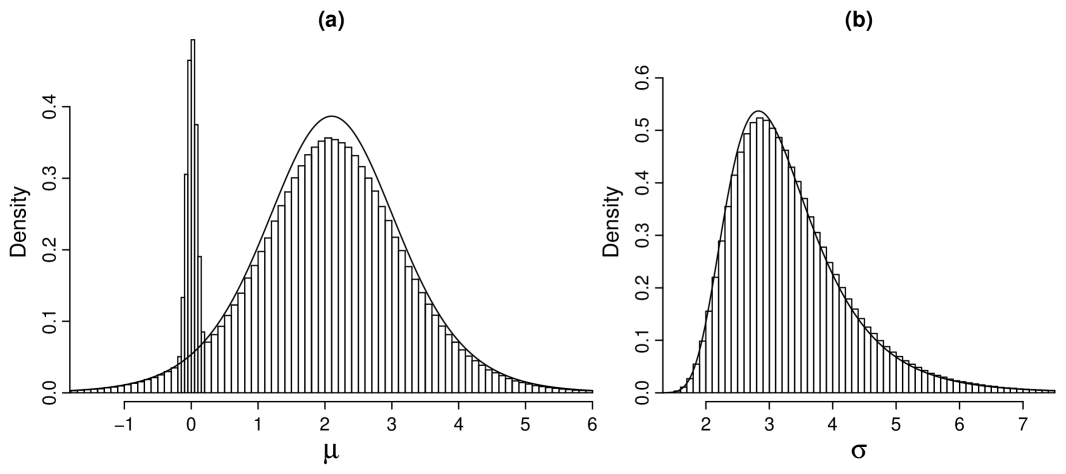

To illustrate the use of the calculations just outlined, Figures 4(a) to 4(c) show some results from generating values from the post-data density defined by the equation just given in three different scenarios. In particular, the histograms in these figures represent the density in these three scenarios. The general assumptions that were made to perform the calculations that underlie the figures in question were that , the sample size is equal to 16 and the prior probability of lying in the interval is equal to 0.3. More specifically, the histogram in Figure 4(a) represents results that were obtained in the case where the observed count was set equal to 5, while the histograms in Figures 4(b) and 4(c) represent results that were obtained when was set equal to 4 and 3, respectively. The numerical output on which these histograms are based was generated by the method of importance sampling, more specifically by appropriately weighting, in each case, a sample of two million independent random values drawn from the fiducial density or, more precisely, the density referred to in the above discussion that corresponded to the particular case concerned.

It can be seen from Figure 4(a) that when the sample proportion is 0.3125, a substantial amount of the probability mass of the post-data density can be found in the interval , but from Figures 4(b) and 4(c) it can be seen that the probability mass of this density that lies in this interval decreases sharply as the sample proportion moves further away from 0.5. To give some more detail here, the post-data probability is equal to 0.1580, 0.0689 and 0.0204 when the sample count is equal to 5, 4 and 3, respectively.

5 A more sophisticated method

Although the methodology outlined in Sections 2.1 to 2.5 allows us to adequately determine the post-data probability of lying inside the narrow interval , i.e. the probability , and also the post-data density of conditional on lying outside the interval , i.e. the fiducial density , it does have two slight disadvantages. First, it will generally be the case that the post-data density defined by equation (12) will have two large and unrealistic discontinuities at the points and of the type that can be clearly seen in Figure 2 and Figures 4(a) to 4(c). Second, the methodology in question does not take into account that usually there will be more pre-data belief that lies towards the centre of the interval rather than towards its lower and upper limits. With the aim of remedying these two drawbacks, we now will put forward a small modification to the methodology detailed in Sections 2.4 and 2.5.

In particular, let us replace the simple GPD function for in the case where , i.e. where , that was specified in equation (7) by the following more sophisticated GPD function for :

| (18) |

where is a given constant and is a continuous unimodal density function on the interval that is equal to zero at the limits of this interval. Although, on the basis of this GPD function, we can not determine the fiducial density , i.e. the density , using Principle 2 summarised in Section 2.3, Principle 1 and the extension to Principle 2 discussed in this earlier section are nevertheless available for this purpose. If Principle 1 can be applied to the present case, then using this principle would imply that the fiducial density would, in general, be derived by using the weak fiducial argument. Furthermore, if Principle 1 or the extension to Principle 2 being referred to can be applied, then the fiducial density of in question would again be defined by the general expression for the fiducial density given in equation (4). After determining the fiducial density that corresponds to the GPD function of current interest, the post-data density of over the whole of the real line, i.e. the density , can then be derived in the usual way by using the expression in equation (12).

However, there is a critical final issue that needs to be resolved, which is how the value of the constant in equation (18) is chosen. In this regard, let us make the assumption that the value of is chosen in a way that implies that the post-data density will be continuous in the vicinity of the points and . In general, a unique value of will exist that satisfies this condition. Therefore, taking into account also the general form of the proposed GPD function of given in equation (18), the slight drawbacks can be avoided that were identified at the start of this section as being associated with the methodology outlined in Sections 2.4 and 2.5.

Furthermore, there are two reasons why placing the condition in question on the choice of the constant can be viewed as not placing a substantial restriction on the way we are allowed to express our pre-data knowledge about the parameter . First, since breaking this condition will generally lead to the post-data density of having undesirable discontinuities, it can be regarded as being a useful guideline in choosing a suitable GPD function for in the case where it is assumed that lies in the interval . Second, any detrimental effect caused by obliging the value of to obey the condition under discussion may not be that apparent given the great deal of imprecision there will usually be in the specification of the GPD function of in the case in question.

6 Third example: Revisiting the simple normal case

To give an example of the application of the method proposed in the previous section, let us return to the problem of making inferences about the mean of a normal distribution that was last considered in Section 3.

We will assume that the density function that appears in equation (18), i.e. the density in the present case, is defined by:

| (19) |

i.e. it is a beta density function for on the interval with both its shape parameters equal to 4. This density function clearly satisfies the conditions that were placed on the function in the last section. Observe that choosing the GPD function of to be as specified by equation (18) implies that the fiducial density will be derived in the current example under Principle 1 described in Section 2.3 by using the weak fiducial argument. As a result, it turns out that this fiducial density, which in the present case is the fiducial density , is defined by:

| (20) |

where is a normalising constant, is the standard normal density function and is as defined in equation (19). On the basis of this fiducial density, the post-data density of over the whole of the real line, i.e. the density , can be derived in the usual way by using the expression in equation (12).

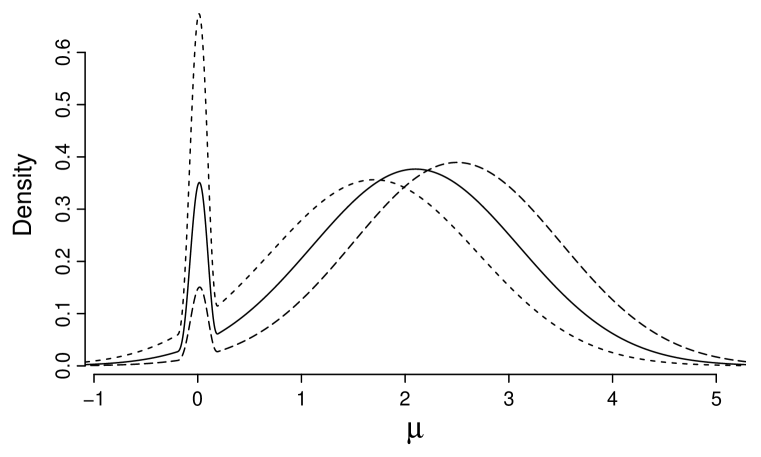

To illustrate the use of the calculations just referred to, Figure 5 shows plots of the post-data density of present interest for various values of the observed mean . As was the case in the construction of Figures 1 to 3, it has been assumed that the variance is equal to the sample size . However, unlike what was the case in the construction of the density functions in Figure 2, it has been assumed that instead of , and as a result, to maintain a useful comparison with this earlier figure, it has been assumed that the prior probability is equal to 0.33 rather than 0.30. Finally, as was the case in Figure 2, the three post-data densities of plotted in Figure 5 correspond to the observed mean being equal to 1.7, 2.1 and 2.5. In particular, the short-dashed, solid and long-dashed curves in this figure correspond to being equal to 1.7, 2.1 and 2.5, respectively. (The line types used have been switched around in comparison to Figure 2 to improve visualisation.)

By comparing Figure 5 with Figure 2, it can be appreciated that the application of the method that was outlined in the previous section will generally allow us to obtain a post-data density that more realistically represents our post-data knowledge about for values of both inside and at the limits of the interval than is possible using the original method for deriving the post-data density in question that was outlined in Sections 2.4 and 2.5.

7 Extending the methodology to multi-parameter problems

7.1 General assumptions

It was assumed in Section 2.1 that the parameter is the only unknown parameter in the sampling model. Let us now assume that all the parameters on which the sampling density depends are unknown.

More specifically, we will assume that the subset of parameters is such that what would have been believed, before the data were observed, about each parameter in this set if all other parameters in the model, i.e. , had been known, would have satisfied the requirements of the scenario of Definition 2 with being the parameter of interest . Furthermore, it will be assumed that the set of all the remaining parameters in the sampling model, i.e. the set , is such that, before the data were observed, nothing or very little would have been known about each parameter in this set over all allowable values of the parameter if all other parameters in the model, i.e. the parameters , had been known.

It is clear that we can determine the post-data density of any given parameter in the set conditional on all the parameters in the set being known by applying either the method outlined in Sections 2.4 and 2.5 or the adjusted version of this method outlined in Section 5, meaning that the general definition of this density function would be as given in equation (12). The set of full conditional post-data densities that result from doing this for each parameter in the set would therefore be denoted as:

| (21) |

Also, we can clearly justify specifying the post-data density of any given parameter in the set conditional on all the parameters in the set being known as being the fiducial density that was referred to at the end of Section 2.3 and which appears in equation (4). Doing this for each parameter in the set would therefore give rise to the following set of full conditional post-data densities:

| (22) |

7.2 Post-data densities of various parameters

If the complete set of full conditional densities of the parameters that results from combining the sets of full conditional densities in equations (21) and (22) determine a unique joint density for these parameters, then this density function will be defined as being the post-data density function of . However, this complete set of full conditional densities may not be consistent with any joint density of the parameters concerned, i.e. these full conditional densities may be incompatible among themselves.

To check whether the full conditional densities of being referred to are compatible, it may be possible to use an analytical method. An example of an analytical method that could be used to try to achieve this goal was outlined in relation to full conditional densities of a similar type in Bowater (2018).

By contrast, in situations that will undoubtedly often arise where it is not easy to establish whether or not the full conditional densities defined by equations (21) and (22) are compatible, let us imagine that we make the pessimistic assumption that they are in fact incompatible. Nevertheless, even though these full conditional densities could be incompatible, they could be reasonably assumed to represent the best information that is available for constructing a joint density function for the parameters that most accurately represents what is known about these parameters after the data have been observed, i.e. constructing, what could be referred to as, the most suitable post-data density for these parameters. Therefore, it would seem appropriate to try to find the joint density of the parameters that has full conditional densities that most closely approximate those given in equations (21) and (22).

To achieve this objective, let us focus attention on the use of a method that was advocated in a similar context in Bowater (2018), in particular the method that simply consists in making the assumption that the joint density of the parameters that most closely corresponds to the full conditional densities in equations (21) and (22) is equal to the limiting density function of a Gibbs sampling algorithm (Geman and Geman 1984, Gelfand and Smith 1990) that is based on these conditional densities with some given fixed or random scanning order of the parameters in question. Under a fixed scanning order of the model parameters, we will define a single transition of this type of algorithm as being one that results from randomly drawing a value (only once) from each of the full conditional densities in equations (21) and (22) according to some given fixed ordering of these densities, replacing each time the previous value of the parameter concerned by the value that is generated. Let us clarify that it is being assumed that only the set of values for the parameters that are obtained on completing a transition of this kind are recorded as being a newly generated sample, i.e. the intermediate sets of parameter values that are used in the process of making such a transition do not form part of the output of the algorithm.

To measure how close the full conditional densities of the limiting density function of the general type of Gibbs sampler being presently considered are to the full conditional densities in equations (21) and (22), we can make use of a method that, in relation to its use in a similar context, was discussed in Bowater (2018). To be able to put this method into effect it is required that the Gibbs sampling algorithm that is based on the full conditional densities in equations (21) and (22) would be irreducible, aperiodic and positive recurrent under all possible fixed scanning orders of the parameters . Assuming that this condition holds, it was explained in Bowater (2018), how it may be useful to analyse how the limiting density function of the Gibbs sampler in question varies over a reasonable number of very distinct fixed scanning orders of the parameters concerned, remembering that each of these scanning orders has to be implemented in the way that was just specified. In particular, it was concluded that if within such an analysis, the variation of this limiting density with respect to the scanning order of the parameters can be classified as small, negligible or undetectable, then this should give us reassurance that the full conditional densities in equations (21) and (22) are, respectively according to such classifications, close, very close or at least very close, to the full conditional densities of the limiting density of a Gibbs sampler of the type that is of main interest, i.e. a Gibbs sampler that is based on any given fixed or random scanning order of the parameters concerned. See Bowater (2018) for the line of reasoning that justifies this conclusion.

In trying to choose the scanning order of the parameters such that the type of Gibbs sampler under discussion has a limiting density function that corresponds to a set of full conditional densities that most accurately approximate the density functions in equations (21) and (22), we should always take into account the precise context of the problem of inference being analysed. Nevertheless, a good general choice for this scanning order could arguably be, what will be referred to as, a uniform random scanning order. Under this type of scanning order, a transition of the Gibbs sampling algorithm in question will be defined as being one that results from generating a value from one of the full conditional densities in equations (21) and (22) that is chosen at random, with the same probability of being given to any one of these densities being selected, and then treating the generated value as the updated value of the parameter concerned.

It is clear that being able to obtain a large random sample from a suitable post-data density of the parameters using a Gibbs sampler in the way that has been described in the present section will usually allow us to obtain good approximations to expected values of given functions of these parameters over the post-data density concerned, and thereby allow us to make useful and sensible inferences about the parameters on the basis of the data set of interest.

8 Fourth example: Normal case with variance unknown

To demonstrate the application of the approach to multi-parameter problems that has just been outlined, let us return to the example that was the focus of our attention in Section 4, however let us now assume that the difference in the performance of the two drugs of interest is measured by the difference in the concentration of a certain chemical (e.g. cholesterol) in the blood, in particular the level observed for drug A minus the level observed for drug B, rather than the preferences of the patients concerned. The set of these differences for all of the patients in the sample will be the data set . This example therefore also has a good deal in common with the example that was considered in Section 3. Moreover, similar to this earlier example, it will be assumed that each value in the data set follows a normal distribution with an unknown mean , however, by contrast to this previous example, the standard deviation of this distribution will now also be treated as being unknown.

For the same type of reason to that used in Example 1.2 in the Introduction, let us in addition suppose that, for any given value of , the scenario of Definition 2 would apply in relation to the parameter with the special hypothesis being the hypothesis that lies in the narrow interval . On the other hand, it will be assumed, as could often be done in practice, that nothing or very little would have been known about the standard deviation before the data were observed given any value for . Therefore, in terms of the notation of Section 7.1, the set of parameters will only contain , and the set will only contain .

Taking into account our pre-data knowledge about conditional on any given value of , we may choose to define the post-data density of conditional on using either the method outlined in Sections 2.4 and 2.5 or the adjusted version of this method outlined in Section 5. Let us choose the latter option. In particular, we will assume that this post-data density is specified in the same way as the post-data density was specified in the example outlined in Section 6. To clarify, the fiducial density that is required by equation (12) will be assumed to be a normal density with mean and variance conditioned on lying outside of the interval , and the fiducial density , which also needs to enter into equation (12), will be assumed to be defined as the fiducial density of was defined in equation (20). It can be seen that we are not making any distinction here between deriving a post-data density of in a situation where is known and deriving a post-data density of conditional on taking a given value.

Furthermore, given our lack of any substantial pre-data knowledge about conditional on any particular value of , it would seem natural to derive the fiducial density of conditional on on the basis of a GPD function of that is defined as follows: if and zero otherwise, where . Observe that since the variance estimator is a sufficient statistic for if is known, it can therefore be assumed to be the fiducial statistic in deriving the fiducial density of in question. Based on this assumption, the function that forms part of the data generating algo-rithm described in Section 2.3 can be expressed as:

where the primary r.v. has a distribution with degrees of freedom, which means that it is being assumed that the fiducial statistic is determined by setting equal to its already generated value in the formula: .

Taking into account the way the GPD function of was just specified, we may then derive the fiducial density of conditional on under Principle 1 described in Section 2.3 by using the strong fiducial argument. As a result, it turns out that this fiducial density, which to be consistent with the notation used earlier will be denoted as the density , can be expressed as:

| (23) |

i.e. it is an inverse gamma density function with shape parameter equal to and scale parameter equal to . In accordance with what was discussed in Section 7.1, this density function will therefore be regarded as being the post-data density of conditional on in the example being considered.

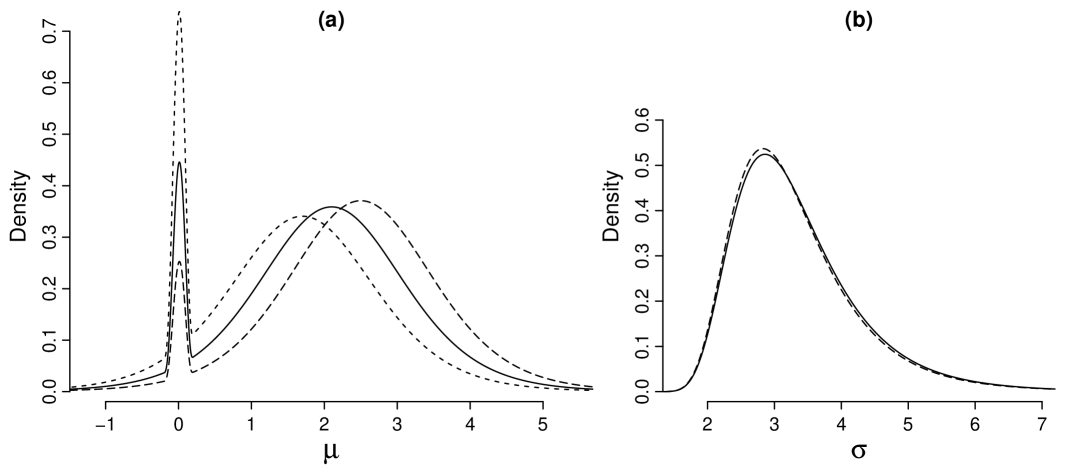

To develop the analysis of this example further, Figure 6 shows some results from running a Gibbs sampler on the basis of the full conditional post-data densities of and that have just been defined, i.e. the densities and , with a uniform random scanning order of the parameters and , as such a scanning order was defined in Section 7.2. In particular, the histograms in Figures 6(a) and 6(b) represent the distributions of the values of and , respectively, over a single run of five million samples of these parameters generated by the Gibbs sampler after a preceding run of one thousand samples, which were classified as belonging to its burn-in phase, had been discarded. This analysis is based on the assumption that the sample size is equal to 9, the sample mean is equal to 2.1 and the sample standard deviation is equal to 3, meaning of course that the usual estimator of the standard error of the sample mean, i.e. , is equal to one. Also, similar to the example discussed in Section 6, it was assumed, in specifying the post-data density , that and that the prior probability in equation (10), which in the present case is the prior probability that , is equal to 0.33.

In accordance with conventional recommendations for evaluating the convergence of Monte Carlo Markov chains outlined, for example, in Gelman and Rubin (1992) and Brooks and Roberts (1998), an additional analysis was carried out in which the Gibbs sampler was run various times from different starting points and the output of these runs was carefully assessed for convergence using suitable diagnostics. This analysis provided no evidence to indicate that the sampler does not have a limiting distribution, and showed, at the same time, that it would appear to generally converge quickly to this distribution.

Furthermore, the Gibbs sampling algorithm was run separately with each of the two possible fixed scanning orders of the parameters and , i.e. the one in which is updated first and then is updated, and the one that has the reverse order, in accordance with how a single transition of such an algorithm was defined in Section 7.2, i.e. single transitions of the algorithm incorporated updates of both parameters. In doing this, the sample correlations between and were 0.075 and 0.120 over the runs of the sampler that were based on the first scanning order just mentioned and the reverse scanning order, respectively, after excluding the burn-in phase of the sampler, and the difference between these two correlations was statistically significant (meaning simply that the difference was beyond random chance). Taking into account results referred to in Section 7.2, it can therefore be concluded that the two full conditional densities on which the Gibbs sampler is based, i.e. the post-data densities and , are incompatible. However, as discussed in Section 7.2, even though these post-data conditional densities are incompatible they could be reasonably assumed to represent the best information that is available for constructing a joint density function for the parameters and that most accurately represents what is known about these parameters after the data have been observed.

To investigate further the issue of how close the full conditional densities of the limiting density function of the type of Gibbs sampler being considered are to the full conditional densities and , another supplementary study was conducted in which the values of and generated by the Gibbs sampler in question were used to approximate the former type of full conditional densities of and . The results of this study showed that, independent of the scanning order of the parameters concerned, the full conditional densities of the limiting density function under discussion may be arguably regarded as being adequate approximations to the full conditional densities and . Also, in cases such as the present example where the sample size is small, it can be argued that we should be a little less strict in how we judge the adequacy of the approximations in question. To clarify, the results of using three different types of scanning order of and were analysed in this study and these, in particular, were the uniform random scanning order of these parameters and the two fixed scanning orders of and that were just described.

Let us point out that, although the limiting density function of the Gibbs sampler being considered is affected to some extent by what choice is made for the scanning order of and , the marginal densities of and over this joint limiting density of and will be the same whatever scanning order of and is used. If the aim is to only obtain marginal post-data densities of and , then this property is clearly convenient as it means we can avoid needing to explicitly determine the scanning order of and that corresponds to the limiting density of the Gibbs sampler having full conditional densities that, in some way, optimally approximate the conditional post-data densities and .

With regard to analysing the data set of current interest, the curves overlaid on the histograms in Figures 6(a) and 6(b) are plots of the marginal fiducial densities of the parameters and , respectively, in the case where the joint fiducial density of these parameters is defined by the conditional fiducial density that is specified by equation (23) and by the fiducial density of conditional on that, similar to how we derived the density , is derived by using the strong fiducial argument, meaning that this conditional density of is defined by the following expression:

Observe that this latter conditional fiducial density, which we will naturally denote as the density , is compatible with the conditional density and that the joint fiducial density of and that they directly define is unique. To clarify, it would be reasonable to regard the fiducial density as representing our post-data knowledge about conditional on if nothing or very little was known about before the data were observed. Here we are therefore treating both the parameters and as belonging to the set referred to in Section 7.1.

The joint fiducial density of and just referred to, which we will naturally denote as the density , can be expressed as follows:

| (24) |

where is a normalising constant. Given this is the joint fiducial density of and , the marginal fiducial density of , which we will naturally denote as the density , and which, for the data of current interest, is represented by the curve in Figure 6(a), can be expressed as follows:

| (25) |

i.e. it is a non-standardised Student density function with degrees of freedom, location parameter equal to and scaling parameter equal to . Finally, the corresponding marginal fiducial density of , which we will naturally denote as the density , and which, for the data of current interest, is represented by the curve in Figure 6(b), is given by the expression:

| (26) |

Observe that the accumulation of probability mass around the value of zero in the marginal post-data density of that is represented by the histogram in Figure 6(a), and the fact that the upper tail of the marginal post-data density of that is represented by the histogram in Figure 6(b) tapers down to zero slightly more slowly than the marginal fiducial density for that is represented by the curve in Figure 6(b) are both consequences that would be expected of the strong pre-data opinion about that was incorporated into the derivation of the conditional post-data density .

9 Direct extension of the univariate method to the multivariate case