Parametric quantile regression for income data

Abstract

Univariate normal regression models are statistical tools widely applied in many areas of economics. Nevertheless, income data have asymmetric behavior and are best modeled by non-normal distributions. The modeling of income plays an important role in determining workers’ earnings, as well as being an important research topic in labor economics. Thus, the objective of this work is to propose parametric quantile regression models based on two important asymmetric income distributions, namely, Dagum and Singh-Maddala distributions. The proposed quantile models are based on reparameterizations of the original distributions by inserting a quantile parameter. We present the reparameterizations, some properties of the distributions, and the quantile regression models with their inferential aspects. We proceed with Monte Carlo simulation studies, considering the maximum likelihood estimation performance evaluation and an analysis of the empirical distribution of two residuals. The Monte Carlo results show that both models meet the expected outcomes. We apply the proposed quantile regression models to a household income data set provided by the National Institute of Statistics of Chile. We showed that both proposed models had a good performance both in terms of model fitting. Thus, we conclude that results were favorable to the use of Singh-Maddala and Dagum quantile regression models for positive asymmetric data, such as income data.

Keywords. Income distributions Quantile regression Income data Reparameterization.

1 Introduction

Income modeling plays an important role in determining workers’ earnings, as well as being an important research topic in labor economics. In general, income data are modeled using mean-based regression models based on the normality assumption. Nevertheless, income is often unequally distributed, hence why this type of data usually has an asymmetric behavior and then the mean is not an appropriate central tendency measure. Therefore, quantile regression models are usually more useful in this context; see Galarza et al., (2020), Sánchez et al., 2021b and Saulo et al., (2021).

Quantile regression models are robust alternatives to traditional mean-based models. That is because instead of focusing on the conditional mean, these models are based on the conditional quantile, such as median; see Koenker, (2005). The quantile approach has the advantage of providing flexibility in modeling, as it allows considering the effects of explanatory variables throughout the spectrum of the dependent variable, thus also including the effect on the median, which is a measure of central tendency better than the mean in the asymmetric context.

Income modelling begins with Pareto, (1897) propositions, establishing a law on how income distribution works. Later on, this suggested a distribution – known as Pareto distribution – and it has set a reference for other distributions, such as log-normal and gamma, to show their potential as for describing income distribution; see Shirras, (1935); Reed, (2003). Even though the Pareto, log-normal and gamma are the most frequently distributions applied to income data because of their abilities to describe this type of data, they have limitations. On the one hand, the Pareto model is appropriate to describe only the upper tail of the distribution. On the other hand, the log-normal and gamma distributions perform poor in describing both the upper and lower tails of the actual distributions. Income distributions such as Dagum and Singh-Maddala have outperformed the Pareto, log-normal and gamma distributions in terms of model fitting; see Cramer, (1971); Dagum, (2008).

Originally proposed by Dagum, (1973, 1975), the Dagum distribution has flexibility to deal with distribution changes, nil and negative income, income range with non-predetermined positive minimum income start, and strictly decreasing and unimodal density functions. This distribution also shows good goodness of fit to income data and obeys a weak version of the Pareto law, i.e. it asymptotically approaches the Pareto distribution. The Dagum model accommodates both heavy tails and an interior mode, characteristics commonly found in income data, and not found singly in well-known distributions – such as log-normal and Pareto; see Krämer and Ziebach, (2002); Dagum, (2008); Kleiber, (2008).

The Singh-Maddala distribution was derived from the concept of hazard rate, an approach widely used in the reliability literature; see Singh and Maddala, (1976). This model also obeys the weak Pareto law, and one of its advantages is to be more flexible than other income distributions. The Dagum and Singh-Maddala distributions are special cases of the generalized beta distribution of the second kind (GB2); for more details on these models, one may refer to the works by Kleiber, (1996, 2008); Kumar, 2017a ; Hajargasht et al., (2012).

This work explores a parametric quantile regression approach for the Dagum and Singh-Maddala distributions. We first introduce reparameterizations of the Dagum and Singh-Maddala model by inserting quantile parameters, and then develop the new regression models. We then demonstrate that the proposed models outperform the recently proposed Birnbaum-Saunders quantile regression model (Sánchez et al., 2021a, ) in terms of model fitting.

The rest of this paper proceeds as follows. In Section 2, we describe the usual Dagum and Singh-Maddala distributions and propose reparameterizations of these distributions in terms of a quantile parameter. In this section, we also present some properties including mode, real and truncated moments. In Section 3, we introduce the quantile regression models and also describe the parameter estimation by the maximum likelihood (ML) method. In Section 4, we carry out a Monte Carlo simulation study to evaluate the performance of the estimators and generalized Cox-Snell (GCS) and random quantile (RQ) residuals. In Section 5, we apply the Dagum and Singh-Maddala quantile regression models to a household income data set provided by the National Institute of Statistics of Chile, and finally in Section 6, we provide some concluding remarks.

2 Classical and quantile-based income distributions

In this section, we describe the classical Singh-Maddala and Dagum distributions along with the proposed quantile-based reparameterizations of these distributions, which will be useful subsequently for developing the parametric quantile regression models. We also present some properties for each model, including mode, real and truncated moments.

2.1 Classical Singh-Maddala distribution

If a random variable follows a Singh-Maddala distribution with shape parameters and scale parameter , denoted by , then the corresponding probability density function (PDF) and cumulative distribution function (CDF) are given by

| (2.1) |

and

| (2.2) |

respectively. The Singh-Maddala distribution includes as special cases the Lomax distribution when , and the log-logistic distribution when . If follows a Singh-Maddala distribution, then follows a Dagum distribution, and vice-versa.

The -th quantile of is obtained by inverting Equation (2.2), which yields

| (2.3) |

2.2 Quantile-based Singh-Maddala distribution

From the quantile function (2.3), we find that the most parsimonious way of conducting the reparametrization is using the scale parameter , where we can then write

where . Then, the quantile-based Singh-Maddala PDF is given by

with notation .

If , then the following properties hold:

-

(QSM1)

Mode (Kumar, 2017b, ; Klugman et al.,, 2019):

- (QSM2)

- (QSM3)

2.3 Classical Dagum distribution

The PDF and CDF of a random variable following a classical Dagum distribution with shape parameters and scale parameter , denoted by , are given by

and

| (2.4) |

respectively. It is simple to observe that and that when both densities coincide with the log-logistic distribution.

The -th quantile of is given by

2.4 Quantile-based Dagum distribution

By observing the three parameters of the classical Dagum distribution, the isolation of the scale according to the quantile would produce the simplest form of the new quantile-based Dagum distribution; it is represented as follows:

where . Then, the quantile-based Dagum PDF can be written as

2.5 Summary table and density plots

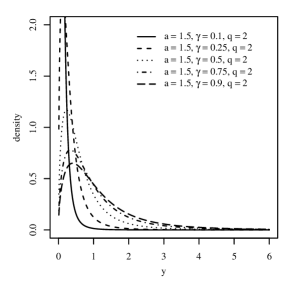

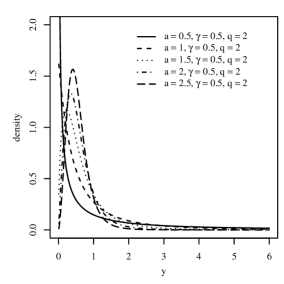

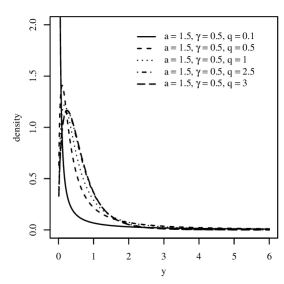

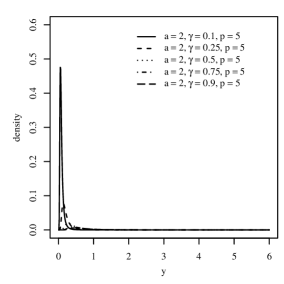

Table 1 presents the Singh-Maddala and Dagum distributions in their original and quantile-based versions. Figures 1 and 2 display different shapes of the quantile-based income distributions for different combinations of parameters, considering scenarios where , , and are fixed. For Singh-Maddala, we can see that influences the kurtosis and skewness, while changes the kurtosis, as it decreases when increases. For Dagum, we see a similar pattern for , changing both kurtosis and skewness, while affects the kurtosis.

Distribution Classical density : -th quantile Substitution Quantile-based density Singh-Maddala Dagum

3 Income quantile regression models

Let be independent random variables such that each , for , has PDF given by some reparameterized income distribution defined in Table 1, for a fixed (known) probability associated with the quantile of interest. Then, in the formulation of the Singh-Maddala and Dagum quantile regression models, the parameter of assumes the following functional relation:

| (3.1) |

where is the vector of the unknown regression coefficients, which are assumed to be functionally independent; , with ; and is the observations of the known regressors, for . In addition, we assume that the covariate matrices has rank . The link function in (3.1) must be strictly monotone, positive, and at least twice differentiable, with being the inverse function of . Here, we chose to work with as link since it is widely used and more flexible when it comes to simulation studies.

Consider a sample of size , say, such that . Then, the corresponding likelihood function for , is

| (3.2) |

where is as in (3.1). By applying the logarithm in (3.2), we obtain the log-likelihood function

| (3.3) |

Now, consider a sample of size , say, such that . Then, the corresponding likelihood function for , is

| (3.4) |

where is as in (3.1). By applying the logarithm in (3.4), we obtain the log-likelihood function

| (3.5) |

To obtain the ML estimate of , it is necessary to maximize the log-likelihood functions in (3.3) and (3.5). Therefore, we need to differentiate the log-likelihood functions to find the score vector and then equate it to zero, providing the likelihood equations. They are solved using the Broyden-Fletcher-Goldfarb-Shanno (BFGS) quasi-Newton method, see Mittelhammer et al., (2000). The method is implemented and applied using the R software. Under some regularity conditions (Cox and Hinkley,, 1979) and when is large, the asymptotic distribution of the ML estimator (QSM) or (QDA) follows asymptotically a multivariate normal distribution

where means ‘approximately distributed’ and is the expected Fisher information matrix, which is given by

A consistent estimator of is the estimated observed Fisher information matrix, given by

Then, we can approximate by .

Departures from regression models assumptions and goodness of fit are assessed by means of a residual analysis. Particularly, we use the generalized Cox-Snell (GCS) and randomized quantile (RQ) residuals:

where is quantile-based Singh-Maddala or Dagum CDF, and is the ML estimate of . If the model is correctly specified, the GCS is asymptotically standard exponential distributed, while the RQ is asymptotically standard normal distributed. With both residuals, graphical techquines, such as quantile-quantile (QQ) plots with simulated envelope, can be used to assess distributions assumptions.

4 Monte Carlo simulation

In this section, we present Monte Carlo simulation studies for each reparameterized quantile model, considering different scenarios of parameters and sample sizes. The first part of the study consists in evaluating ML estimation performance, while the second evaluates the empirical distribution of the GCS and RQ residuals. Both studies consider simulated data generated from each one of the Singh-Maddala and Dagum quantile regression models according to

The Monte Carlo simulation experiments were performed using the R environment; see http://www.r-project.org.

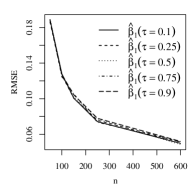

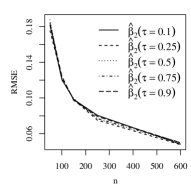

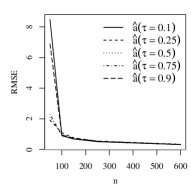

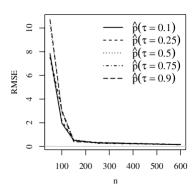

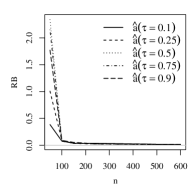

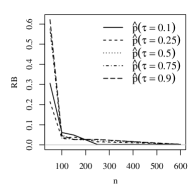

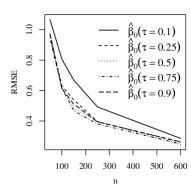

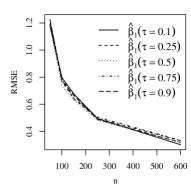

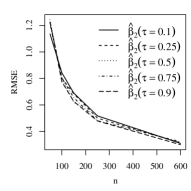

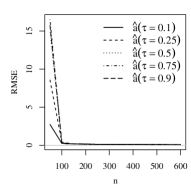

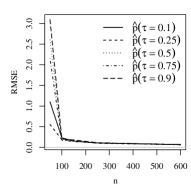

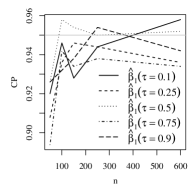

4.1 ML estimation

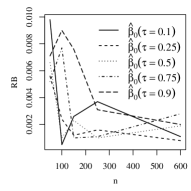

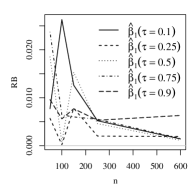

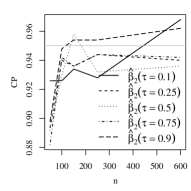

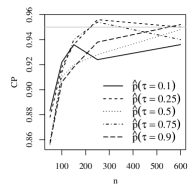

The simulation scenario considers the following settings: sample sizes , vector of betas , quantiles , (Singh-Maddala), and (Dagum), with 500 Monte Carlo replications for each sample size. Covariate values are obtained from a uniform distribution in the interval (0,1). To study the ML estimators, we use compute the relative bias (RB), root mean square error (RMSE) and the coverage probability (CP). We expect that, as sample size increases, the RB and RMSE reduces, and the CP approaches the 95% nominal level. The estimates of RB, RMSE and CP are computed from the Monte Carlo replicas as:

where and are the true parameter value and its respective -th ML estimate, is the number of Monte Carlo replicas, is an indicator function taking the value 1 if , and 0 otherwise, where and are the -th upper and lower limit estimates of the 95% confidence interval.

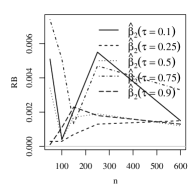

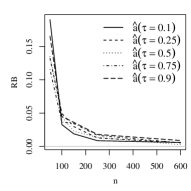

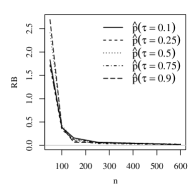

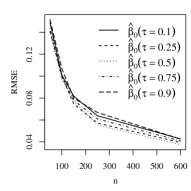

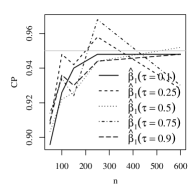

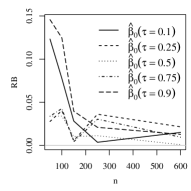

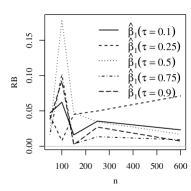

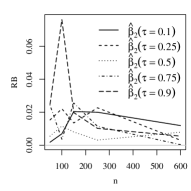

The results for Singh-Maddala models are shown in Figure 3. It is possible to see that the simulations produced the expected outcomes. As the sample size increases, the RB and RMSE both decrease, and the CP tends to 95%. The results for the Dagum model are shown in Figure 4. This figure presents results similar to those found for the Singh-Maddala model.

4.2 Empirical distribution of residuals

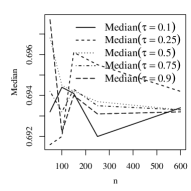

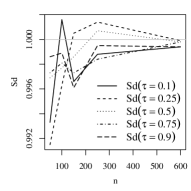

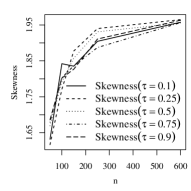

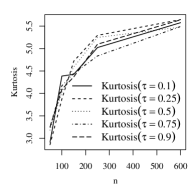

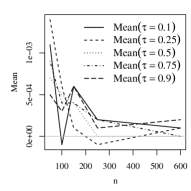

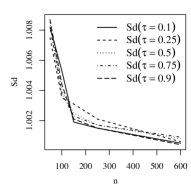

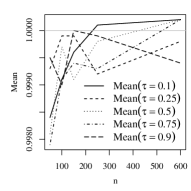

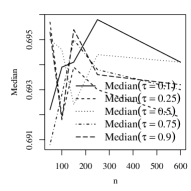

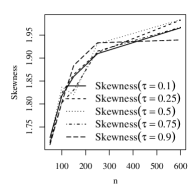

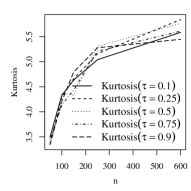

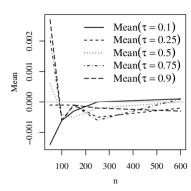

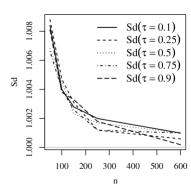

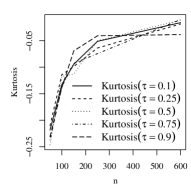

Here we show the performance of GCS and RQ residuals. We analyse the results with descriptive statistics (mean, median, standard deviation, coefficient of skewness and coefficient of kurtosis). The simulation scenario is exactly the same as in Subsection 4.1. Figures 5 and 6 show the simulation results of the Singh-Maddala and Dagum models, respectively.

The reference values of mean, median, Sd, skewness and kurtosis are 1, 0.69, 1, 2 and 6, respectively, for GCS residual, and 0, 0, 1, 0 and 0, respectively, for RQ residual. From Figures 5 and 6, it is possible to verify that, as the sample size increases, the values tend to the expected results for each . Therefore, we can use the both residuals to verify the fit of the proposed models.

5 Application to income data

In this section, we use the 2016 Chilean household income data set, provided by the National Institute of Statistics in Chile111Available at https://www.ine.cl/estadisticas/sociales/ingresos-y-gastos/encuesta-suplementaria-de-ingresos. to illustrate the proposed parametric quantile regression models. This data set was also used by Sánchez et al., 2021a , who introduced the Birnbaum-Saunders quantile regression model. While the Birnbaum-Saunders is not a distribution commonly used for income data, Singh-Maddala and Dagum are, so we assess if these models can produce better fits than the BS model.

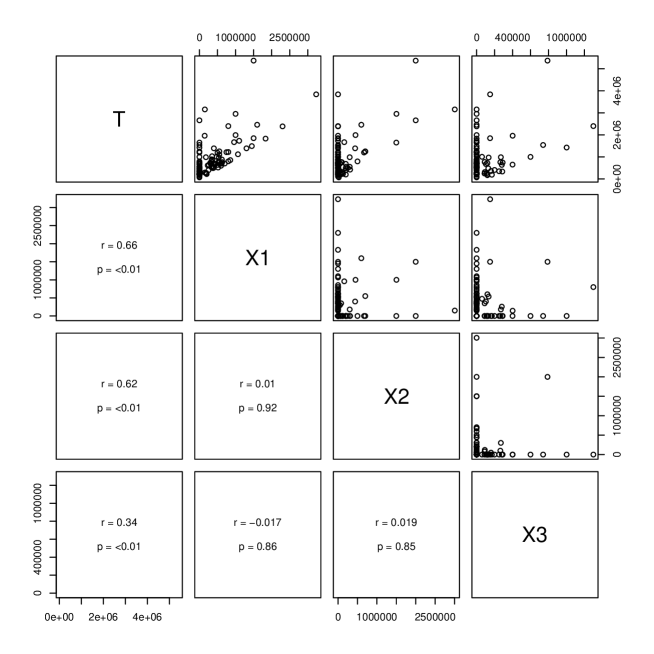

The household income is the response variable (), whereas the covariates are the total income due to salaries (), the total income due to independent work () and the total income due to retirements (). The original dataset contains 107 variables, including the aforementioned, but these were selected based on economic and statistical criteria in relation to the response variable and descriptive analysis conducted by Sánchez et al., 2021a . Moreover, all incomes are expressed in thousands of Chilean pesos222 See http://www.bancocentral.cl for their equivalence in American dollars..

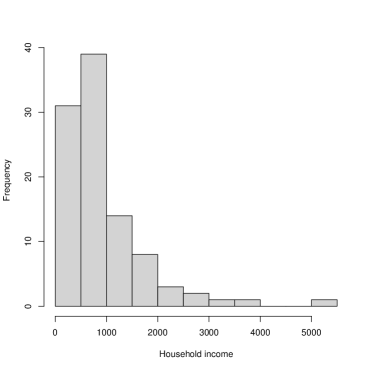

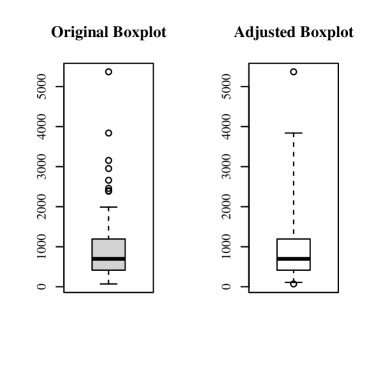

We report in Table 2 descriptive statistics for the household income (). Figure 7 shows the histogram along with usual and adjusted box plots (Rousseeuw et al.,, 2016). We observe that the household income data have a unimodal and right-skewed behavior, which i the precise needed scenario to uphold the usage of asymmetric distribution. Figure 8 shows scatterplots (with correlation) between the household income () and the covariates (, and ). We observe that correlations are reasonable and significant, meanwhile the covariates have almost no linear correlation between each other.

| Mean | Median | Sd | Coef. Variation | Coef. Skewness | Coef. Kurtosis | minimum | maximum | |

|---|---|---|---|---|---|---|---|---|

| 698.80 | 938.10 | 837.52 | 0.89 | 2.45 | 11.03 | 70 | 5369.90 | 100 |

We then analyze the household income data using the Singh-Maddala and Dagum quantile regression models, with regression structure expressed as333We use this specification in order to compare the results of the proposed models with those of the Birnbaum-Saunders quantile regression model.

for . The proposed models are fitted using the function IncomeReg.fit, implemented in the R software (R Core Team,, 2019) by the authors. The codes are available upon request.

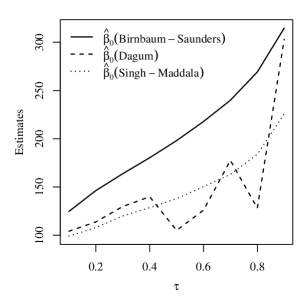

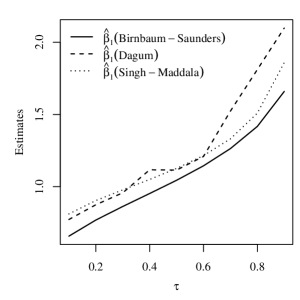

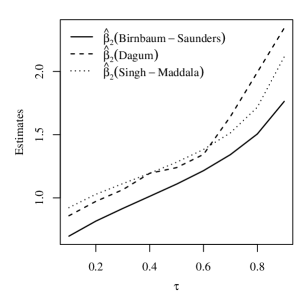

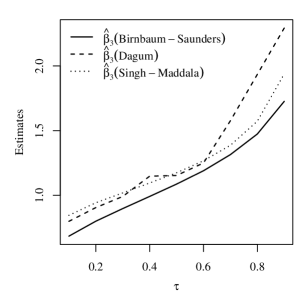

Table 3 presents the ML estimates, computed by the BFGS quasi-Newton method, standard errors (SEs) and Akaike (AIC) and Bayesian information (BIC) criteria values, for the Singh-Maddala and Dagum quantile regression models with . As mentioned earlier, the results of the Birnbaum-Saunders quantile regression are presented as well. The results of Table 3 reveal that the proposed Singh-Maddala and Dagum models provide better adjustments than the Birnbaum-Saunders model based on the values of log-likelihood, AIC and BIC. Particularly, the Singh-Maddala model has the lowest AIC and BIC values. The estimated parameters of the Birnbaum-Saunders, Dagum and Singh-Maddala models across are shown in Figure 9. From this figure, we observe that the estimates associated with all the covariates tend to increase as increases, as expected.

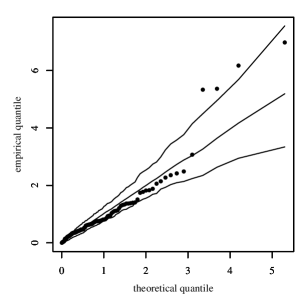

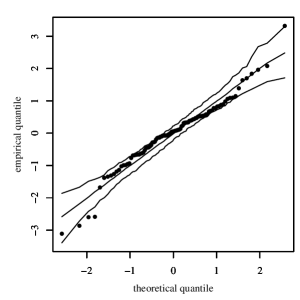

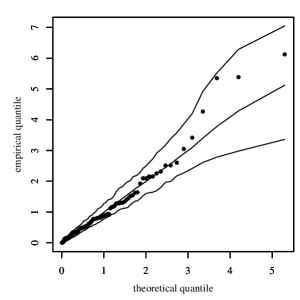

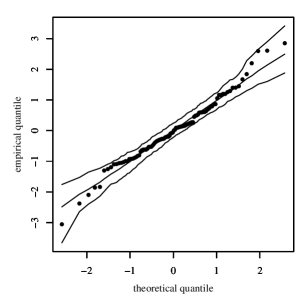

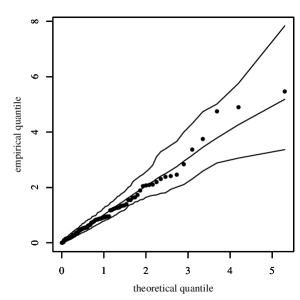

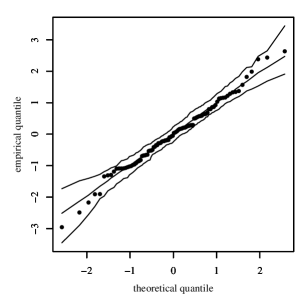

The QQ plots with simulated envelope of the GCS and RQ residuals for the models considered in Table 3 confirm the results presented in Table 3; see Figure 10. Similar results are obtained when considering .

| Birnbaum-Saunders () | Dagum () | Singh-Maddala () | |

|---|---|---|---|

| 198.0903* | 150.8307* | 137.8478* | |

| (22.3166) | (3.0771) | ( 3.2826) | |

| 1.0440* | 1.1173* | 1.1252* | |

| (0.0870) | (0.0636) | (0.0569) | |

| 1.1090* | 1.2424* | 1.2805* | |

| (0.1502) | (0.1172) | (0.1103) | |

| 1.0865* | 1.1562* | 1.1730* | |

| (0.1759) | (0.1395) | (0.1382) | |

| 0.3646* | |||

| (0.0087) | |||

| 4.3720 | 8.3380 | ||

| (0.5692) | (1.4720) | ||

| 2.2100 | 0.4034 | ||

| (1.0290) | (0.1144) | ||

| Log-lik. | 692.8373 | 686.9182 | 685.2337 |

| AIC | 1395.675 | 1385.836 | 1382.467 |

| BIC | 1408.701 | 1386.740 | 1383.371 |

* significant at 5% level. ** significant at 10% level.

Figure 11 shows 95% prediction intervals from the Birnbaum-Saunders, Dagum and Singh-Maddala quantile regression models for the household income data. The predictions were performed -steps-ahead, namely, -observations were not included in the estimation. From Figure 11, we observe that 95%, 95% and 95% of the observations are within the limits of the prediction interval for the Birnbaum-Saunders, Dagum and Singh-Maddala models, respectively. Therefore, all the models provide values closer to the nominal 95% level.

6 Concluding remarks

In this paper, we have proposed parametric quantile regression models based on the Singh-Maddala and Dagum distributions. The proposed models are based on reparametrizations of the original distributions, by including the quantile as a parameter. The maximum likelihood method was used to estimate model parameters and Monte Carlo simulation studies were conducted in order to evaluate the performance of the estimators and the empirical distribution of the generalized Cox-Snell and random quantile residuals. Results showed that the estimates had good performance, and the residuals presented good agreement with their reference distributions. We applied the proposed models to a real data set, where we have modeled the household income as a function of the following covariates: total income due to salaries, total income due to independent work and total income due to retirements. The results were compared to those obtained by Sánchez et al., 2021a , who proposed the Birnbaum-Saunders quantile regression model. We showed that both Singh-Maddala and Dagum models have better fit to data than Birnbaum-Saunders model, with Singh-Maddala also showing a slight superior performance than Dagum. Therefore, results were favorable to the usage of Singh-Maddala and Dagum quantile regression models. As part of future research, influence diagnostic tools can be investigated and also multivariate models can be studied.

References

- Cox and Hinkley, (1979) Cox, D. R. and Hinkley, D. V. (1979). Theoretical Statistics. CRC Press.

- Cramer, (1971) Cramer, J. S. (1971). Empirical econometrics. North-Holland Amsterdam.

- Dagum, (1973) Dagum, C. (1973). Un modèle nonlinéaire de répartition fonctionnelle du revenu. Faculté des sciences sociales. Dép. de science économique, Université d’Ottawa.

- Dagum, (1975) Dagum, C. (1975). A model of income distribution and the conditions of existence of moments of finite order. Bulletin of the International Statistical Institute, 46(1):199–205.

- Dagum, (2008) Dagum, C. (2008). Modeling income distributions and Lorenz curves, volume 5, chapter A New Model of Personal Income Distribution: Specificationand Estimation. Springer Science & Business Media.

- Galarza et al., (2020) Galarza, C. E., Zhang, P., and Lachos, V. H. (2020). Logistic quantile regression for bounded outcomes using a family of heavy-tailed distributions. Sankhya B, pages 1–25.

- Gradshteyn and Ryzhik, (2015) Gradshteyn, I. and Ryzhik, I. (2015). Table of Integrals, Series and Products Eighth Edition. Elsevier, Academic Press, San Diego.

- Hajargasht et al., (2012) Hajargasht, G., Griffiths, W. E., Brice, J., Rao, D. P., and Chotikapanich, D. (2012). Inference for income distributions using grouped data. Journal of Business & Economic Statistics, 30(4):563–575.

- Kleiber, (1996) Kleiber, C. (1996). Dagum vs. Singh-Maddala income distributions. Economics Letters, 53(3):265–268.

- Kleiber, (2008) Kleiber, C. (2008). A guide to the Dagum distributions. In Modeling income distributions and Lorenz curves, pages 97–117. Springer.

- Klugman et al., (2019) Klugman, S. A., Panjer, H. H., and Willmot, G. E. (2019). Loss models : from data to decisions, volume Fifth edition. Wiley, Wiley Series in Probability and Statistics.

- Koenker, (2005) Koenker, R. (2005). Quantile Regression. Cambridge University Press, Cambridge.

- Krämer and Ziebach, (2002) Krämer, W. and Ziebach, T. (2002). The weak Pareto law and regular variation in the tails. Technical report, Universität Dortmund.

- (14) Kumar, D. (2017a). The Singh–Maddala distribution: properties and estimation. International Journal of System Assurance Engineering and Management, 8(2):1297–1311.

- (15) Kumar, D. (2017b). The Singh–Maddala distribution: properties and estimation. International Journal of System Assurance Engineering and Management, 8:1297–1311.

- Mittelhammer et al., (2000) Mittelhammer, R. C., Judge, G. G., and Miller, D. J. (2000). Econometric foundations pack with CD-ROM. Cambridge University Press.

- Pareto, (1897) Pareto, V. (1897). Cours d’économie politique, volume 1. F. Pichou.

- R Core Team, (2019) R Core Team (2019). R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria.

- Reed, (2003) Reed, W. J. (2003). The Pareto law of incomes—an explanation and an extension. Physica A: Statistical Mechanics and its Applications, 319:469–486.

- Rousseeuw et al., (2016) Rousseeuw, P., Croux, C., Todorov, V., Ruckstuhl, A., Salibian-Barrera, M., Verbeke, T., Koller, M., and Maechler, M. (2016). Robustbase: basic robust statistics. R package version 0.92-6.

- (21) Sánchez, L., Leiva, V., Galea, M., and Saulo, H. (2021a). Birnbaum-saunders quantile regression and its diagnostics with application to economic data. Applied Stochastic Models in Business and Industry, 37(1):53–73.

- (22) Sánchez, L., Leiva, V., Saulo, H., Marchant, C., and Sarabia, J. M. (2021b). A new quantile regression model and its diagnostic analytics for a Weibull distributed response with applications. Mathematics, 9:276.

- Saulo et al., (2021) Saulo, H., Dasilva, A., Leiva, V., Sánchez, L., and Fuente-Mella, H. L. (2021). Log-symmetric quantile regression models. Statistica Neerlandica, 76:124–163.

- Shirras, (1935) Shirras, G. F. (1935). The Pareto law and the distribution of income. The Economic Journal, 45(180):663–681.

- Singh and Maddala, (1976) Singh, S. and Maddala, G. S. (1976). A model of income distribution and the conditions of existence of moments of finite order. Econometrica, 44:963–970.

Appendix A Proof

Proof of Property (QDA3).

If then

Taking the change of variables and we get

By using the identity: , ; see Eq. (3.194.2) in Gradshteyn and Ryzhik, (2015); the last integral is

Then the proof follows. ∎