Linear Regression With Unmatched Data: A Deconvolution Perspective

Abstract

Consider the regression problem where the response and the covariate for are unmatched. Under this scenario, we do not have access to pairs of observations from the distribution of , but instead, we have separate data sets and , possibly collected from different sources. We study this problem assuming that the regression function is linear and the noise distribution is known, an assumption that we relax in the applications we consider. We introduce an estimator of the regression vector based on deconvolution and demonstrate its consistency and asymptotic normality under identifiability. Even when identifiability does not hold, we show in some cases that our estimator, the DLSE (Deconvolution Least Squared Estimator), is consistent in terms of an extended norm. Using this observation, we devise a method for semi-supervised learning, i.e., when we have access to a small sample of matched pairs . Several applications with synthetic and real data sets are considered to illustrate the theory.

Keywords: denoising, convolution, shuffled, regression, semi-supervised, unmatched data, unlinked data

1 Introduction

Consider the standard regression setting

| (1.1) |

where is the noise variable, is the vector of features and is a measurable function. Given an i.i.d. sample of , the problem of estimating has been vastly studied in the literature. The estimation problem is much harder when we do not have access to matched/linked data, i.e. the pairs from (1.1), but instead we have separate samples and such that and ’s have the same distribution as and . Under this setting, the exact equality in (1.1) is replaced by the following equality in distribution

| (1.2) |

This type of data commonly arises in applications when the data has been collected through different sources. It can also occur when the link between the covariates and the response has been deleted because of privacy concerns. This problem is known as unmatched or unlinked regression in the literature and has been studied in different variations.

Unmatched regression can be seen as a generalization of a problem known as permuted regression or unlabeled sensing. In permuted regression, one again observes only the variables and separately. The difference with unmatched regression is that in permuted regression, it is assumed that the link is lost because of the existence of some permutation such that

| (1.3) |

Clearly, permuted regression is a special case of unmatched regression. However, note that the equality (1.3) is stronger than the equality in the distribution in (1.2) for unmatched regression since, in unmatched regression, such a permutation may not exist. Permuted regression has received considerable attention, especially when is a linear transformation, e.g., Unnikrishnan et al. (2018); Pananjady et al. (2018); Abid et al. (2017); Hsu et al. (2017); Slawski and Ben-David (2019); Tsakiris et al. (2020); Slawski et al. (2020); Tsakiris and Peng (2019); Zhang et al. (2021); Slawski et al. (2021); Rigollet and Weed (2019). In permuted regression, finding the corresponding permutation has also been the focus of many research works. Note that this is a much harder problem than just estimating . If one estimates , by some estimator say, then estimating boils down to a simple estimation with matched data . For a detailed summary of the related work on permuted regression, we refer the reader to Slawski and Sen (2022).

The problem of unmatched regression is of special interest in areas such as microeconomics, where the variable of interest has not been observed jointly with some of the covariates. This problem is also known as data fusion, where multiple observational and experimental data sets exist and the links are unavailable. Popular approaches in this situation include methods based on matching, see e.g. Cohen and Richman (2002); Monge et al. (1996); Walter and Fritsch (1999). Matching-based methods rely on the access to an extra contexual variable such that they can use this variable to pair the response variable and the covariates.

In the absence of such contextual variables, there is little hope for pairing the variables. In a recent work Carpentier and Schlüter (2016), estimating in unmatched regression was studied for , assuming that the distribution of is known and is monotone without assuming any contextual variable. Note that when is monotone, this problem is also known as unmatched isotonic regression. In Carpentier and Schlüter (2016), authors have shown the close connection between unmatched isotonic regression and deconvolution. In Carpentier and Schlüter (2016) for estimating , authors have resorted to kernel deconvolution as the main estimation technique. Under some smoothness assumptions, the authors have provided the rate of convergence for the proposed kernel estimator obtained with available deconvolution methods in the literature. In Balabdaoui et al. (2021), the authors made use of the tight relationship between the unmatched isotonic regression and deconvolution and provided an estimator for under the assumption that the noise distribution is known. Their method follows the idea of estimation of the mixing distribution for a normal mean, as done by Edelman (1988). The authors provide a rate of convergence of a weighted -distance of their estimator of under several smoothness regimes of the distribution of the noise as well as some regularity conditions satisfied by . For example, in the case where the noise distribution is ordinary smooth with a smoothness parameter equal to , it follows from their Theorem 1 that the convergence rate of their monotone estimator to the truth when both are restricted on certain compacts cannot be slower than . In Rigollet and Weed (2019), a minimum Wasserstein deconvolution estimator was suggested that achieves the rate of and it was shown that for normally distributed errors, this rate is optimal. In Meis and Mammen (2021) the minimum Wasserstein deconvolution estimator achieves much better rate of for risks for discrete noise which is optimal. Later in Slawski and Sen (2022), the problem was considered for where the authors have shown that a generalized notion of monotonicity, called cyclical monotonicity, of the regression function, is sufficient for estimation of the regression function . Their method leverages ideas from the theory of optimal transport, specifically the Kiefer-Wolfowitz nonparametric maximum likelihood estimator. Slawski and Sen (2022) provide the rate of convergence of their estimator in terms of -distance under some smoothness assumption on and assuming that the noise is Gaussian.

Our Contribution: In this work, we consider the problem of estimating the regression vector in unmatched linear regression under the assumption that the noise distribution is known. Our work conceptually follows Balabdaoui et al. (2021), although there is a considerable difference between the linear model and the monotone one. Compared to Balabdaoui et al. (2021); Carpentier and Schlüter (2016), the main contribution of our work is that our theory is valid for any given dimension (though not depending on the sample size of the observations). This framework, to the best of our knowledge, has been only considered in Slawski and Sen (2022). Our proposed deconvolution least squares estimator (DLSE) is not necessarily consistent; therefore, we cannot directly compare our results to those obtained in Slawski and Sen (2022). On the other hand, when we are in a setting in which our estimator is consistent, we do have the faster rate of convergence compared to the rate of convergence in Slawski and Sen (2022), without having to assume that noise is Gaussian. Such a fast rate may come as a big surprise given the non-standard situation of lacking any knowledge of the existing link, even partial, between the responses and covariates. The explanation is that, under the identifiability of the model, the estimation problem can be cast in the usual scope of the theory of -estimators in parametric models. In the settings where the DLSE is not consistent, we show that a generalized notion of the estimator’s norm is consistent, which can be used in semi-supervised scenarios.

Outline of the paper: In Section 2 we introduce our methodology for studying the problem. In Section 3, we provide the main results of the paper by first introducing the estimator and its properties and then applying it in a semi-supervised setting. Section 4 provides simulations on synthetic and real data. We provide the proofs of all lemmas and theorems in the supplementary material.

2 Methodology

Let be a random vector in for . Consider to be a random variable such that where is the noise random variable, and is a deterministic vector of coefficients. In this work we assume that we have access to two independent data sets and such that and are i.i.d random variables which are distributed as and respectively.

For a random variable or vector , we denote by its cumulative distribution function, that is . In the case of a vector, the inequality should be considered component-wise. The equality in distribution yields

| (2.1) |

where denotes the convolution operator. Note that minimizes the function

| (2.2) |

where is an integer and is a positive measure on . In this work, we focus on the case where has a continuous distribution. Also, we assume that is known. However, we do not assume that is necessarily Gaussian. Note that the assumption that the noise distribution is known was made in all the prior works on unmatched regression. In the applications below, we relax this assumption by letting the scale parameter of the distribution of the noise unspecified. Deriving the theory for such a relaxation is still needed as the estimation procedure needs to be extended to allow for the additional estimator of the scale parameter.

A natural choice of is , the probability measure induced by the distribution of on . Given a sample we can use the empirical estimate of

By using as a surrogate of , we get the empirical version of (2.2)

| (2.3) |

Without loss of generality and for the sake of a simpler notation, we assume that . Also, we let . The main idea of this paper is to take the solution of the optimization problem as an estimate of . In Section 3, we study this optimization problem in detail.

3 Main Result

Notation and Definition. Let be the class of all functions on such that their first derivatives exist and are continuous. Let be the set of all such that the unlinked linear regression model in (2.1) holds, i.e. . Also, let us write . For , the Euclidean norm of is defined as . Let be the -sphere. For a positive-definite matrix, for is a norm.

3.1 The Deconvolution Least Squares Estimator

Given samples and let . In the following proposition, we show that when admits a continuous distribution, there exists at least a such that it minimizes .

Proposition 1

Assume that is continuous on . For a given integer , and for with probability we have .

Note that may have more than one element. For example for where are exchangeable random variables it is easy to see that we have where is any permutation on . The other interesting case is when is distributed as . In Lemma 2 we show that in this case can be characterized in terms of .

Lemma 2

Suppose the unlinked linear regression model in (2.1) holds with where is non-singular. Then, there exists a constant such that

Since is not necessarily a singleton, it is impossible to have a consistency result in the classical sense. On the other hand, with the characterization of via the norm constraint, Theorem 3 shows that is consistent in terms of such a norm constraint. From now on, we will take . This means that our deconvolution least squares estimator is any vector which minimizes the criterion (A.1) for .

Theorem 3

Suppose that is continuous on . If there exists a non-singular positive-definite matrix such that for all and some , then if we have

Note that the result in Theorem 3 requires that . The following proposition shows that when this requirement is met, and therefore we have the consistency of the DLSE in terms of .

Proposition 4

Suppose that for some non-singular . Then, and

where for any for which the unlinked linear regression model in (2.1) holds, and is any consistent estimator of .

In the case where , meaning that there exists a unique such that we show that is a consistent estimator in the classical sense. In Theorem 5, we show that under this uniqueness assumption in probability.

Theorem 5

Assume that admits a density and . In addition assume that for any such that . Then for all we have

When , then depending on the distribution of , we might be able to narrow down by more than just specifying the norm of the members. In Theorem 6 below, we show that for a certain family of probability distributions, consists of all vectors that result from permuting the components of a member .

Theorem 6

Suppose that the components of the covariate , are i.i.d. with moment generating function that takes the form

where , , and is a continuous function such that

Then the set of all such that is

Note that this family includes exponential and Gamma distributions as well as any convolution thereof.

Finally, in Theorem 7, where there exists a unique regression vector for which the unmatched regression model holds we are able to show that under some smoothness assumptions the DLSE is asymptotically normal with mean and covariance matrix that depends on the distribution of , that of and the true regression vector .

Theorem 7

Suppose and there exists such that and . Also assume that there exists an integer and such that is monotone on . Furthermore, we assume that , and the matrix

is positive-definite. Then when we have

where

with , and and are two independent standard Brownian Bridges from to . The random vector is distributed as .

The conditions required for are satisfied by most of the well-known densities, including normal, Laplace, symmetric Gamma densities and any finite convolution thereof. The asymptotic covariance matrix has a complicated dependence on the parameters of the model. However, the exact knowledge of this asymptotic covariance matrix is not at all necessary to make useful inferences. In fact, the asymptotic result of Theorem 7 allows us to use re-sampling techniques to infer the true regression vector. Therefore, one can resort to bootstrap in order to find an approximation of asymptotic confidence bounds for .

Theorem 7 provides the asymptotic normality of the DLSE only under the identifiability of the unmatched linear regression model, and hence it cannot be used beyond the scope where .

When we are in the situation of Theorem 6, and if the components of are all distinct, then the model becomes identifiable if the components of are ordered from smallest to largest. In fact, the arguments in the proof of Theorem 8 can be used again to show the following result.

Theorem 8

Suppose that satisfies the same conditions as in Theorem 6. Suppose also that the assumption of Theorem 6 holds and that the components of the vector are all distinct. Denote the vector of ordered components of from smallest to largest, and the vector of ordered components of the DLSE, . Then,

where and are defined in Theorem 6.

To close this section, we would like to stress the fact that the fast rate of convergence, , is obtained under the very important condition of identifiability of , or in other words its uniqueness. When this condition is satisfied, arguments from the theory of M-estimators can be used. In this case, the -rate can be obtained since the estimation problem is fully parametric. In case identifiability is not satisfied, Theorem 6 provides a sufficient condition on the distribution of the covariates which guarantees identifiability of the ordered values of the regression vector. Although the condition given in that theorem encompasses many distributions, a unified result with more general identifiability conditions is yet to be established.

3.2 Application to Semi-supervised Learning

As established above, the estimator is not consistent in case of non-identifiability. Therefore, one cannot possibly think of as something that will be close to some unique truth since the latter does not even exist. However, there are situations where some feature of the model is unique, and in this case, one would expect that the DLSE succeeds in remaining faithful to such features.

Consider the case where with a non-singular covariance matrix . Lemma 2 describes the set in terms of a norm with respect to : There exists a constant such that for any we have . In addition, Proposition 4 guarantees that although we do not have consistency of , it holds that . In this case if we have access to a third sample of matched data, we can benefit from the result of Proposition 4 together with an estimate of from the matched sample.

Let be a set of matched data such that . Take to be an estimator of based on only . For example, one can take to be the ordinary least squared (OLS) estimator. Let be a consistent estimator of , the covariance matrix of using the sample (here, an estimate based on this sample is more accurate since is much bigger than ). Now consider the following modified estimator

| (3.1) |

When , we expect that to be a better estimate of compared to . Therefore, while the estimate based on the unlinked data fails to provide a meaningful estimate of the direction of , we can still use to modify the norm of and hence improve the performance of the latter.

Unfortunately, we do not yet have a rate of convergence for . In Section 4 we provide experimental results suggesting that for large enough one can use as an estimate of . As we do not have the right arguments which show theoretically that the modified estimator in (3.1) improves the performance , we resort to another estimator of the norm and whose convergence rate can be established. The estimator is based on the following simple observation:

Therefore, under the assumption of known distribution of , it is possible to estimate by estimating . The following remark shows that when , using the information from unmatched data improves the performance of the OLS estimator.

Remark 9

Let be the ordinary least square estimate of using the matched data . Let where is the sample mean of . Define

where is the empirical covariance matrix of . When

where expectations on the right and left sides are taken with respect to the distribution of the matched data and the product distribution of the matched and unmatched, respectively.

4 Applications to Synthetic and Real Data

In this section, we present the result of several simulations with the goal of illustrating the theoretical results derived above. In addition, we shall consider real applications using two different real data sets: The (unmatched) inter-generational mobility data set already analyzed by several authors; e.g. Olivetti and Paserman (2015) and the (matched) Power Plant data set to which we apply ideas from semi-supervised learning. Computation of the DLSE, especially for large data sets (synthetic or not) and for several runs impose numerical challenges. One major issue is that the minimization problem is generally not convex and can be multi-modal especially in the case of non-identifiability. We use the default setting of the function “optim”from the package “stats” of the open software R. The default method of optimization is the method introduced by Nelder and Mead (1965).

4.1 Synthetic Data

Example 1

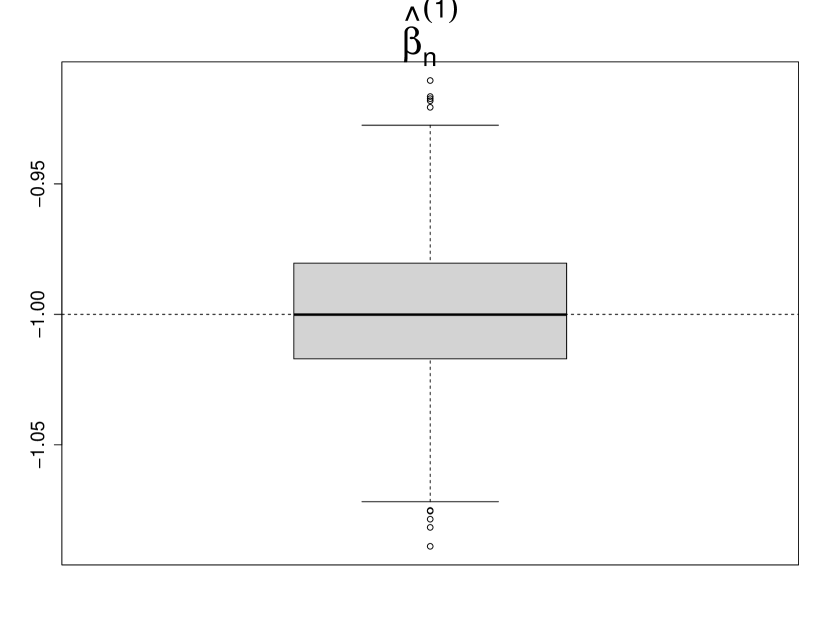

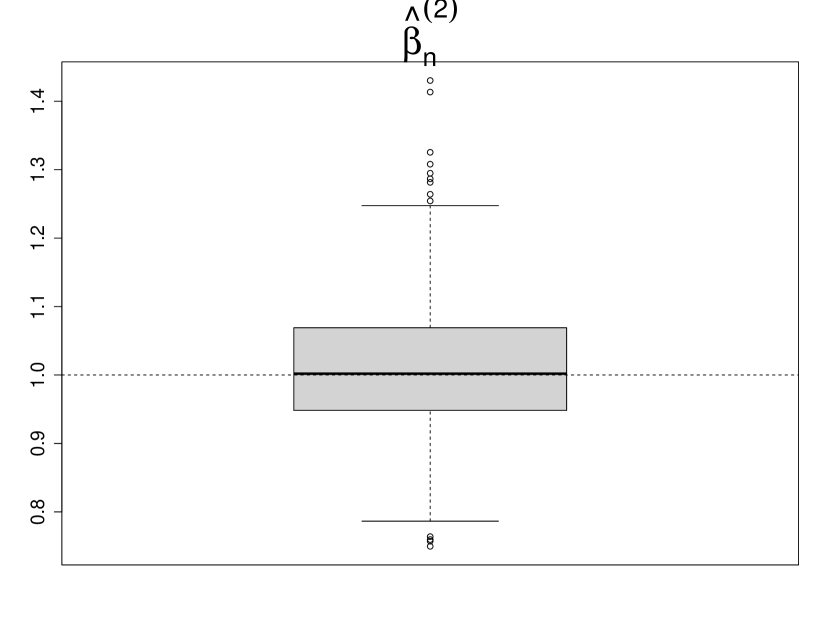

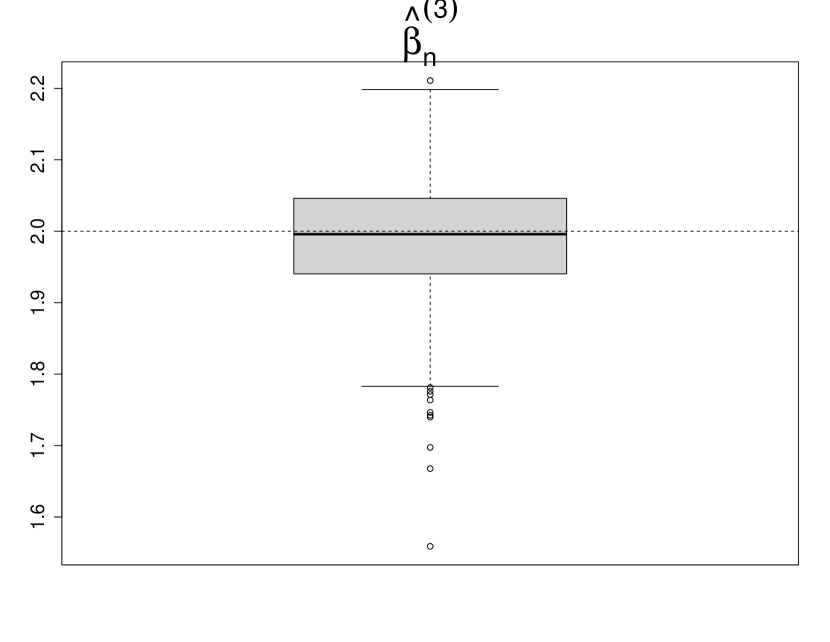

For this example, we generated 1000 independent samples of and where of size such that

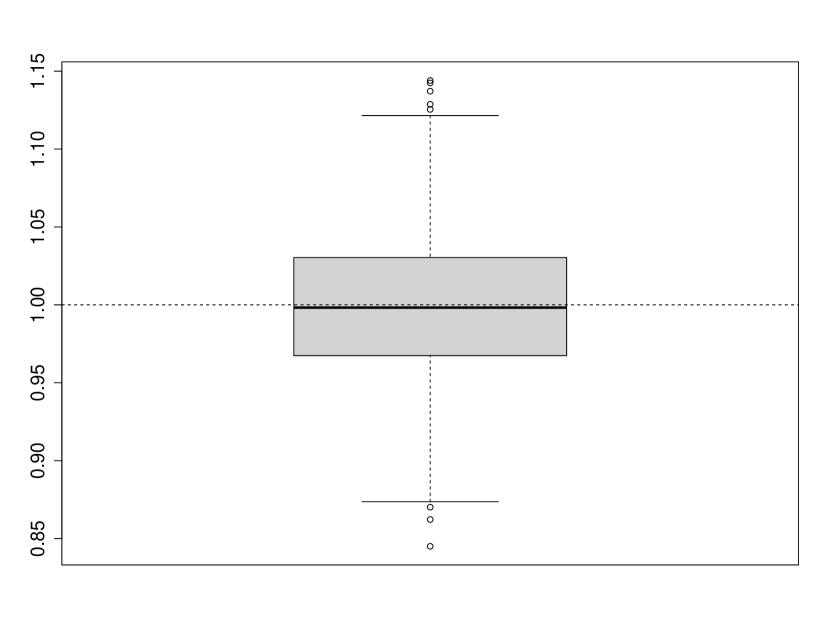

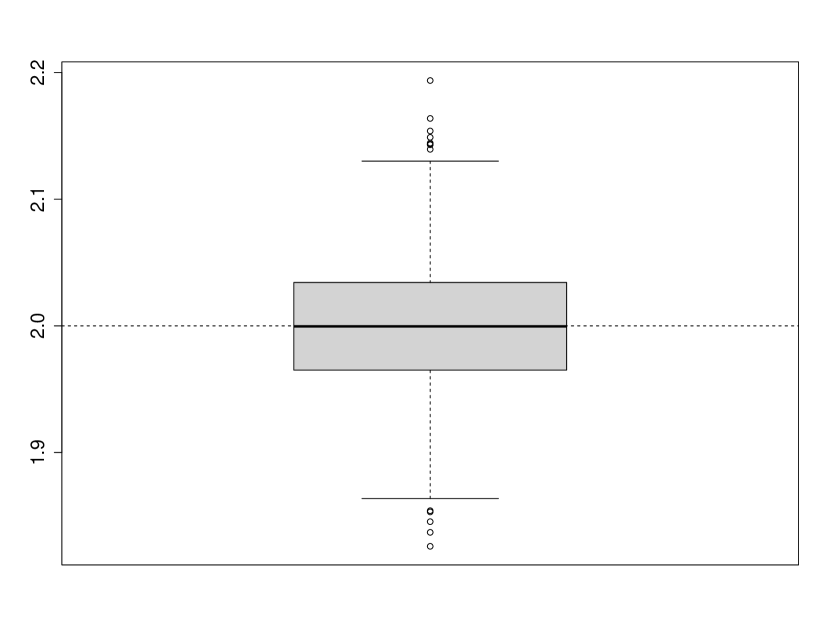

where and are independent. In this case, and as shown in the supplementary material, contains only . Therefore, we expect that is a consistent estimator of . Figure 1 shows the boxplot of and based on the 100 replications.

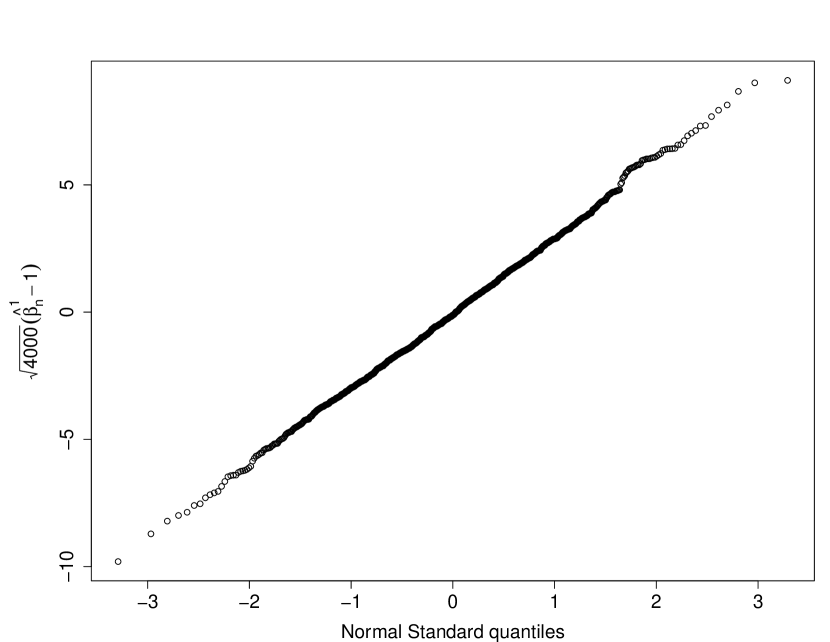

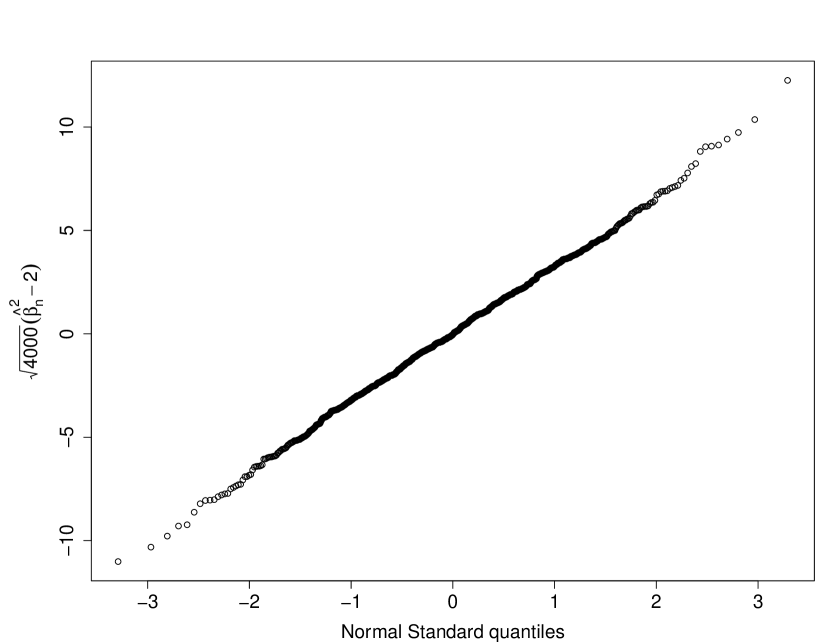

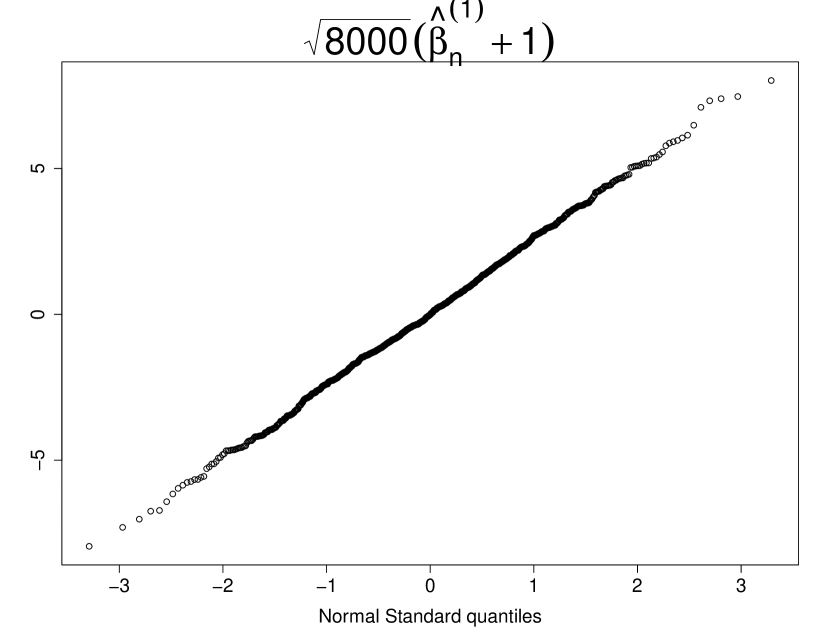

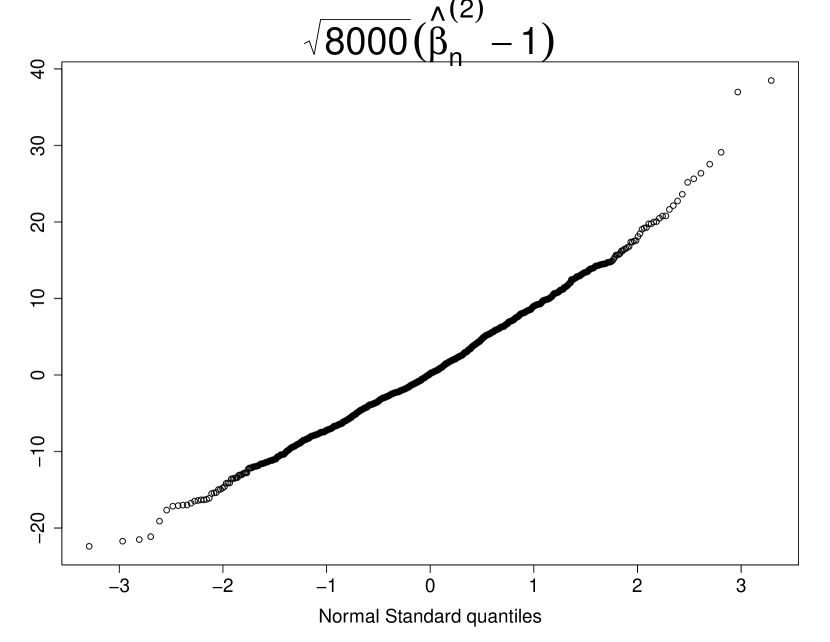

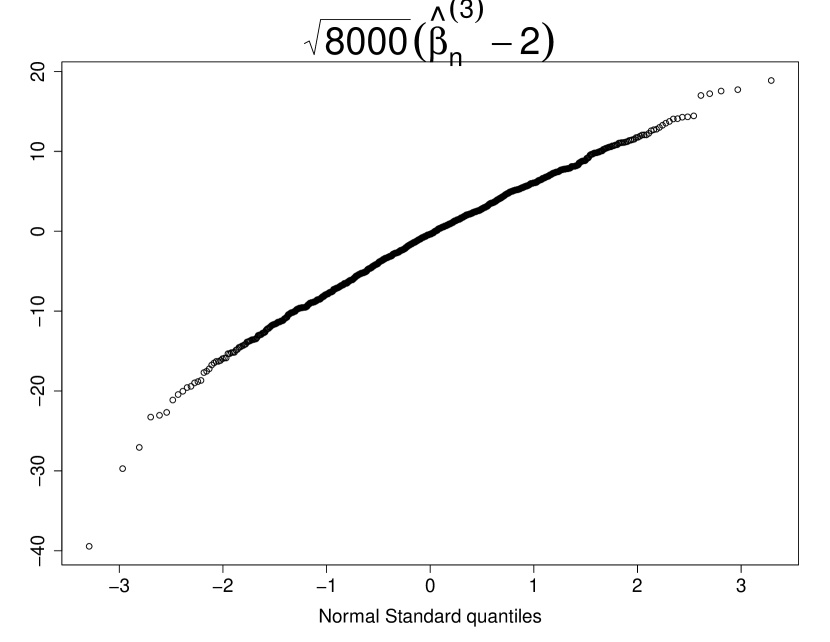

Theorem 7 shows that has asymptotically a normal distribution. This type of result can be validated by plotting the quantiles against those of a standard normal variable. Such plot is commonly known under the name of qqplot. Figure 5 shows such qqplots for the components of . Their linear shape is much aligned with the asymptotic normality of our estimator as stated in Theorem 7.

Using unmatched data, at best, means that we only have access to the generating mechanism of and without knowing the link between them. Lack of information about the link between the ’s and ’s should come with a price paid on the performance of the estimate of . To see how much our DLSE suffers from this lack of knowledge, we compare the performance of with the ordinary least square estimator using a matched sample of size over 100 independent replications. The comparison is done in terms of absolute prediction error. For this purpose we vary the noise strength level for to see how much it effects the performance. In Table 1, the result is summarized in terms of the ratio of the absolute error of the OLS estimator to the absolute error of DLSE for each value of and for each component of . Clearly, beats as it uses more information, but given the fact that is oblivious to the link between the response and covariate, its performance is rather quite satisfactory.

| 0.14 | 0.26 | 0.32 | 0.28 | 0.61 | |

| 0.18 | 0.16 | 0.18 | 0.25 | 0.55 |

Example 2

We consider the following setting

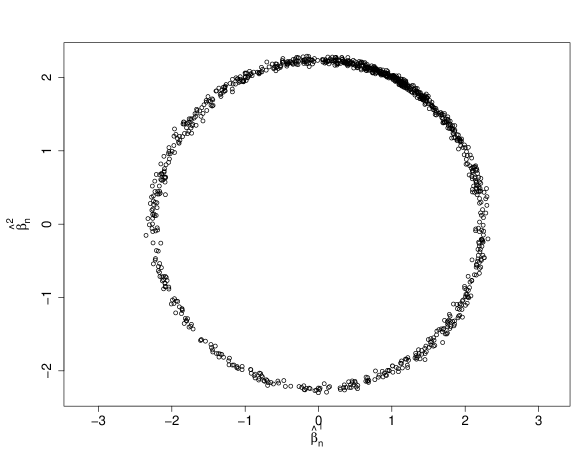

where is the identity matrix. Note that in this case, contains more than one element. In fact by Lemma 2 we know that . Proposition 4 guarantees that converges to in probability. The scatterplot of shown in Figure 3 gives a clear illustration of this fact. The mean and standard deviation of over the 1000 replications with sample size were found to be and respectively.

Example 3

In this example, we generated 1000 times independent samples of and where with size such that

where and are independent. Theorem 6 implies that , since all permutations of lead to the same distribution. Instead of we take a look at where is the -th smallest element of . As mentioned earlier, when , we do not have any asymptotic normality result but believe that is asymptotically normal under some regularity assumptions. Figure LABEL:fig:exp_dim3_8000_qqplot shows the qqplots of against the quantiles of , and which is supported by Theorem 8.

This example suggests that in cases where we do not have uniqueness, looking at the ordered version of can provide additional information. Such a piece of information can be very valuable in the presence of a small matched data set or expert knowledge. In this case, one might even be able to recover the permutation that maps to a consistent estimator of .

Example 4

For this example we generated 100 samples of size from model (1.2) such that and

We also generate 100 samples of matched data from model (1.1) for . Note that . We use the unlinked data for computing and the linked data for computing the OLS estimator of , . In Table 2, the mean and standard deviation of these estimators over the 100 replications are shown. It can be seen that is highly concentrated around compared to the OLS estimators with smaller sample sizes.

| , square norm of OLS estimate with sample size | |||||||||||

| m | 10 | 20 | 30 | 40 | 50 | 60 | 70 | 80 | 90 | 100 | |

| mean | 6.44 | 6.23 | 6.07 | 6.02 | 6.12 | 6.04 | 6.11 | 6.25 | 6.02 | 6.11 | 6.00 |

| sd | 2.03 | 1.23 | 0.87 | 0.80 | 0.66 | 0.65 | 0.58 | 0.56 | 0.52 | 0.55 | 0.16 |

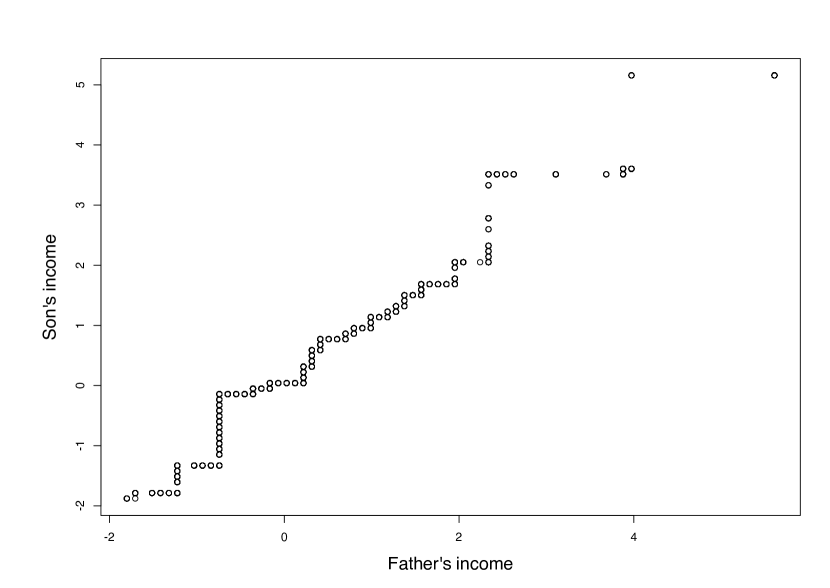

4.2 Intergenerational Mobility in the United States, 1850-1930

The degree to which the economic status is passed along generations is an important factor in quantifying the inequality in a society. Researchers have approached this problem by studying the relationship between the father/father-in-law’s income and the son/son-in-law’s income. It is intuitive to assume that there is an increasing relationship between the son’s income and that of the father. If we assume that this relationship is linear, the magnitude of the coefficient can quantify the existing inequality: the stronger the relationship, the more inequality. For this purpose, we apply our method to data from 1850 to 1930 decennial censuses of the United States studied in Olivetti and Paserman (2015); D’Haultfoeuille et al. (2022) using the 1 percent IPUMS samples (Ruggles et al., 2010). We follow Olivetti and Paserman (2015) and focus only on white father/father-in-law and son/son-in-law relationships. In this available historical data on father-son income in the United States, the link between the father/father-in-law and son/son-in-law is not available. Other studies on this data have used information on the first name to reconstruct the link between the father/father-in-law and son/son-in-law, but we only use the unmatched data and do not look at these partially reconstructed links.

Since the exact value of the income in this data set is not available, we use the provided OCCSCORE. OCCSCORE assigns each occupation in all years a value representing the median total income (in hundreds of 1950 dollars) of all persons with that particular occupation in 1950. Therefore, using this score, we lose the within-occupation variation of the income.

We let be the son/son-in-law’s OCCSCORE and to be the father/father-in-law’s OCCSCORE and assume that . The sample sizes in the data sets are quite large () and therefore, for computational reasons, we select a subset of size of and at random. We centered and normalized each sub-sample such that they have a mean of 0 and a variance of 1 but kept the same names ( and ) for the transformed variables. In Figure 6, we show the sorted values of (Son’s income) plotted against those of (Father’s income) for a sub-sample of size .

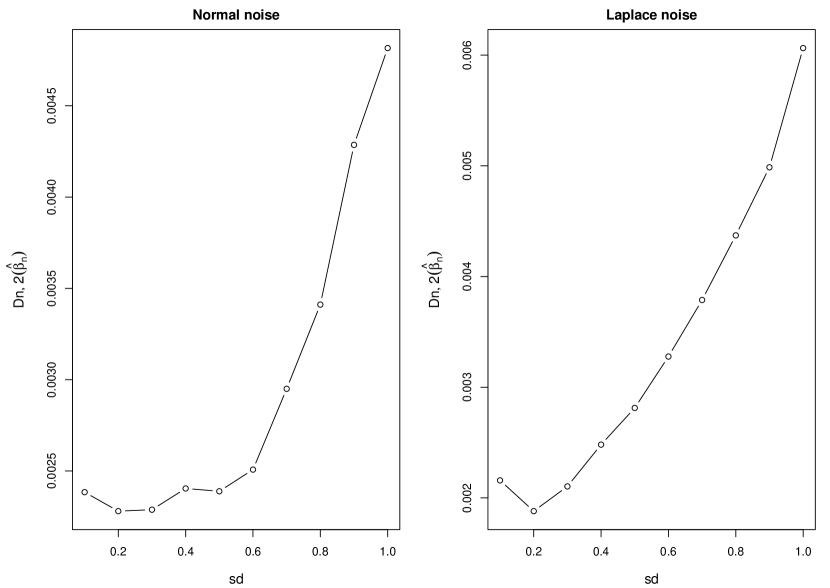

Since the true distribution of the noise variable is unknown in this problem, we consider two different families of centred distributions, Normal and Laplace. We consider different possible values for their scale parameters, so that the standard deviation (sd) of the noise varies in the set . Recall that the standard deviation of a random variable distributed as is and as is . Therefore, we choose the parameters and accordingly.

Note that the data is discrete as there are many repeated values for each of and .

Varying and , the respective parameters of the distributions and , such that the standard deviation takes its value in the set allows us to plot the values of in Figure 7. Assuming that the noise is Gaussian, we observe that takes its minimum over the grid of values of at and the optimization procedure yields . Similarly assuming that the noise follows with parameter such that we find the minimum to be attained for and .

Relying on the observation that is minimized for for both the Normal and Laplace distributions over 100 iterations we take independent sub-samples of size and calculate using Normal and Laplace distribution for the noise with standard deviation equal . For both distributions, the estimate shows a bi-modal behaviour with positive and negative modes with the same magnitude. This is to be expected in case the covariate has a zero expectation. However, as we know that the relationship between and should be non-decreasing, we can consider the absolute value of in all cases. Table 3 shows the values of mean and standard deviation for using the Normal and Laplace distributions for the noise. Note that Theorem 7 guarantees asymptotic normality of when under some regularity assumptions. Such assumptions do not seem to be fulfilled in this dataset because of its discreteness. However, one may use sub-sampling ideas to create confidence intervals based on , hoping that some asymptotic normality holds.

| Normal (sd = 0.2) | Laplace (sd = 0.2) | |

| mean | 1.17 | 1.14 |

| sd | 0.06 | 0.09 |

| Bootstrap confidence interval |

In this example, the covariate is 1-dimensional, and the distribution of data is far from continuous. Still, we found this example interesting as it is the only real data problem with unmatched data that we could access to.

4.3 Power Plant Data Set

We consider the Power Plant data set from UCI Machine Learning Repository111https://archive.ics.uci.edu/. The data set contains 9568 matched data points collected from a combined cycle power plant. Features consist of hourly average ambient variables Temperature (T), Ambient Pressure (AP), Relative Humidity (RH) and Exhaust Vacuum (V) to predict the net hourly electrical energy output (EP) of the plant. Assuming that EP is a linear function of T, AP, RH, and V, we run ordinary least squares using all the data points. We get , which supports the linearity of the relationship. We perform 100 independent simulations in the following manner: For each simulation, we select a sub-sample of matched data of size . We use this subsample of matched data for both and estimate the distribution of . Then, from the remainder of the data, we select a sub-sample of unmatched data of size . This is done by selecting a sample of size from the remaining ’s and independently selecting a sample of size from the remaining ’s. Since we do not have access to the population density in this case, we take the OLS estimate using all the data points as the ground truth.

For the DLSE estimator , we need an estimate of the noise distribution, and for this, we use a Kernel density estimator based on the residuals of OLS obtained using the matched data. We use a Gaussian kernel and select the bandwidth according to Sheather and Jones (1991).222We use function density from R package “stats” with hyper-parameter “SJ” for the bandwidth and Gaussian kernel.

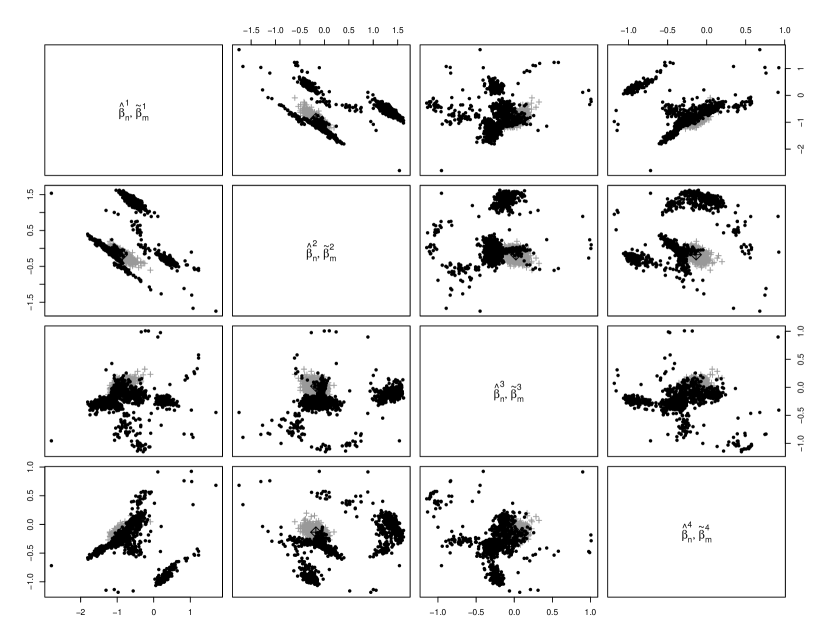

Figure 8 depicts the scatterplots of pairs of components of the obtained DLSE over 1000 sub-samples of size together with the projection of onto the corresponding sub-spaces. The grey points in the scatterplots correspond to components of . For example, the plot in the first row and the second column is the scatter plot of vs (and vs ) which shows that the first two components of form 3 main clusters. Therefore, the scatterplots suggest that is not converging to a unique value. On the other hand, they show that the vectors ’s are concentrated around multiple modes similar to the phenomena described in Theorem 6. Note that in each scatterplot, one of the clusters can be represented by the projection of and therefore can be recognized as the “true cluster”. As in reality we do not have access to the whole matched data set, one can use as a “guide” to pin down the right cluster. We intend to formalize this idea more concretely in the scope of future work.

5 Discussion and Future Research Directions

In this paper, we have proposed an approach for making inference in a regression model in the case where the link between responses and covariates is not known. Here, our main goal is to estimate the regression vector. Note that the model we consider includes the permuted regression model studied by in Pananjady et al. (2018), where the principal focus is to recover the permutation under which the covariates are shuffled and which is responsible for the loss of the link. The main idea that we pursued in this work is to view the responses as random variables generated from the convolution of and and find the vector which minimizes over all possible an -distance between the sample distribution of the responses and a natural estimator of the distribution of the convolution of and . As it becomes clear at the end of Section 3, the problem boils down to a deconvolution. It may come as very surprising that one is able to recover, under some identifiability conditions, the true regression vector or an ordered version thereof at the -rate. In fact, the convergence rates in deconvolution problems are known to be slow to very slow for smooth noise distributions. For example, if the noise is Gaussian and under minimal smoothness assumptions, then it follows from the seminal paper of Fan (1991) that is the optimal rate of convergence for deconvoluting the distribution of from the noise based on observations from the model . How do we reconcile this slow rate with the obtained in our Theorem 7? The answer is that our problem is completely parametric, and the distribution to be deconvoluted is in a much smaller class than the one considered in Fan (1991).

The estimation method that is chosen and implemented in this work is partially motivated by convenience to some degree. In fact, the arguments from the theory of empirical process, although technical, seem to be less cumbersome as they are, for example, for the Maximum Likelihood estimator (MLE). Finding the MLE in this problem would have been a very appealing approach, and the estimator might be even more efficient. In this case, one would find a regression vector which maximizes the log-likelihood

over . Optimization, in this case, presents harder numerical challenges because of the logarithm. Nevertheless, we believe that this estimator should be implemented. We leave this task to future research work, where we also plan to study the asymptotic properties of this estimator and compare its performance to the DLSE studied here. If the noise distribution is assumed to be known, we would like to stress the fact that it is possible to relax such an assumption. This can be done either by (1) estimating this distribution from a matched sample as done above for the Power Plant data set or (2) assuming that it belongs to some scaled parametric family and estimating the scale parameter, say, together with the unknown regression vector. This approach was followed for the inter-generational mobility data set. We conjecture that under identifiability, the resulting estimators of and are asymptotically Gaussian. A referee noted that it is possible to consider the case where the response is multivariate, of dimension , in which case one needs to estimate a whole regression matrix. If the components of are independent, then the asymptotic theory developed here can be easily extended. However, the optimization problem, already difficult for , will impose additional numerical challenges. In case the components are not independent, we do not think that extending our estimator to this case would be straightforward. Computation of the empirical distribution of the observed responses becomes very tedious as well as the criterion, which now involves multivariate integration.

The great potential of the method described in this work was clearly seen in the semi-supervised learning situation, where some matched data is available. We view this scenario as the best and most realistic application for two reasons: (1) One is able to estimate the distribution of the noise from the matched proportion and not simply impose it. (2) The OLS found with the matched data can be used in combination with re-sampling from the unmatched data to “guide” the deconvolution least square method in finding the closest DLSE to the OLS. The point in (2) is particularly useful in case the re-sampled data do not seem to agree on the DLSE.

Finally, we would like to point out that the linear regression model can be, of course, extended to other models, such as logistic regression for example. An extension is the high-dimensional setting, although we believe that many theoretical challenges will have to be tackled, both from theoretical and numerical perspectives.

Acknowledgments

The authors thank Professor Charles H. Doss for very interesting discussions on the methodology used in the paper. The authors thank Professor Wendelin Werner for some very useful hints, which allowed us to finish the proof of Theorem 7, Professor Ashwin Pananjady and Professor Martin Wainwright for helpful comments.

Appendix A Supplementary Material

We present proofs of all the theorems and lemmas in the following.

A.1 Proof of Proposition 1

Proof Our goal is to show that with probability one, there exists a vector such that it minimizes .

For consider the compact set . We show that our choice of depends only on . Let be a fixed vector. Then we have

with and . Note that and depend on the vector . Since has a continuous distribution, with probability one. If , then for some distinct , are not linearly independent, which is of probability zero.

Suppose that . Using , it follows that

Since we have . By taking , and following from , with probability one we have

This implies that for

Now, for any small and large enough

Let . Then, there exists such that for

| (A.1) |

with probability provided that . Note that for , similar reasoning can be applied by summing over . Now, consider the set

| (A.2) |

where is the same constant defined above. Since the lower bound shown in (A.1) does not depend on the vector , we conclude that for all

| (A.3) |

On the other hand, and by using the equality ,

Convexity of gives us

where denotes the supremum norm, and is the empirical distribution based on . By Glivenko-Cantelli we have

| (A.4) |

Therefore by combining (A.3) and (A.4) we have

Since defined in (A.2) is compact and is Lebesgue-a.e continuous we have

A.2 A Useful Proposition and Its Proof

We will use the following proposition in the rest of the proofs.

Proposition 10

For any we have

Proof By definition of we have

By adding and subtracting we have

By Dvoretzky–Kiefer–Wolfowitz inequality; Dvoretzky et al. (1956) we have

Using it follows that

Therefore . Since by definition we conclude that

| (A.5) |

which implies that

which completes the proof.

A.3 Proof of Theorem 3

Proof For positive semi-definite matrix and , define . Note that is equivalent to . It follows from (van der Vaart, 1998, Theorem 5.14) that for any compact set and

Assuming that , for any we can find such that

for all . Take to be the closed Euclidean ball in with centre and radius . Then,

Hence

Since can be arbitrarily small, this implies

By the assumption of Theorem for any we have . This, together with triangle inequality, implies

hence

as . This completes the proof.

A.4 Proof of Lemma 2

Proof For a random variable denote the characteristic function of by ; i.e.,

Then, for all . Let be a small interval containing 0 such that for all we have . Then and if and only if for all . Since we have

Therefore . Note that is positive definite which implies for .

A.5 Proof of Proposition 4

Proof Let us start with the case where . Using (A.9) we have

where

This implies that

For any fixed and

Fix a small . Since is a cumulative distribution function, there exists such that if . This implies that for and such

Let . Since converges almost surely to , we have that

Now, note that for such that we have

Therefore

Now,

Note that since the event is included in the complement of the event

On the other hand, (A.5) implies that . Since

Thus

this implies that . Now, consider the general case where with positive definite. Then, the model in (2.1) can be written as

where , independent of , and . Thus, as and , with the least squares estimator based on and , it follows that . By Lemma 2 and Proposition 3, we have

where for all for this model. For a consistent estimator of , we have

where the second term on the right is bounded by since . This concludes the proof.

A.6 Proof of Theorem 5

Proof Recall that

For define

the convolution density and its empirical estimator. Then, we have that

Let us consider .

Functions , , and are all non-negative, monotone and bounded above by . Denote the class of real monotone functions such that by . We have

where . By Theorem 2.7.5 of van der Vaart and Wellner (1996) there exists a universal constant such that for all

where denotes the bracketing covering number. Now, by Lemma 3.4.2 of van der Vaart and Wellner (1996) and using the fact that all functions in are bounded above by , we have that

where for small

It follows that for all . Using Markov’s inequality, we conclude that

| (A.6) |

Now, we focus on the term . We have

Hence

Note that

implying that . Also, for all

where

using the change of variable , and integration by parts. Thus, it follows that

| (A.7) | |||||

Next, we show that the supremum in (A.7) is independently of . Consider the class

Note that is a dimensional vector space. By Lemma 2.6.15 of van der Vaart and Wellner (1996), is a VC-subgraph of index smaller than . Now, note that

with and . Since is monotone, by Lemma 2.6.18(viii) of van der Vaart and Wellner (1996), we conclude that the class is a VC-subgraph. Since all elements in are bounded by , the latter can be taken as its envelope. Thus, it follows from Theorem 2.6.7 in van der Vaart and Wellner (1996) that there exists such that (taking ) for all and all probability measures

where is some universal constant. Hence, there exists a constant such that

using the fact that

| (A.8) |

using . It follows from Theorem 2.14.1 in van der Vaart and Wellner (1996) that

where

Using Markov’s inequality, it follows that

from which we conclude that

| (A.9) |

Since for all it follows that

By the Cauchy-Schwarz inequality, we have that

since . Therefore

Similarly, we have

Also,

It follows that

In the following, we show that

| (A.10) |

for open set such that . Note that , therefore

Let be the open Euclidean Ball of center and radius . Suppose that . This means that we can find a sequence such that

| (A.11) |

Assume there exists a subsequence such that . Let . Since the unit sphere is compact, there exists a subsequence of , which without loss of generality we denote by , such that where . Note that for a fixed

Since does not belong to any affine space with probability one, we have

and therefore . Also, for all such that , we have and hence as . Similarly, for all such that , . By the Dominated Convergence Theorem, it follows that

Using the Dominated Convergence Theorem again, we conclude that

which implies with (A.11) that for all , which is impossible. We conclude that it is impossible that the sequence has an Euclidean norm that tends to . This means that it is bounded by some constant . Then, there exists a subsequence, w.o.l.g. we denote it by , converging to some vector . Using similar arguments as above, we have

and hence . Since is the unique vector such that , we must have . However, this is impossible because this would mean that . Since any open set containing contains for some , we conclude that the separability condition in (A.10) must hold. As minimizes , it follows that all the conditions of (i) in (van der Vaart and Wellner, 1996, Corollary 3.2.3) are fulfilled. Therefore

This concludes the proof.

A.7 Proof of Theorem 6

Proof Note that if and only if

for all such that the expectations on the left and right are defined. To use a simpler notation, we write now for . By the i.i.d. assumption, we can write that

for all such that

| (A.12) |

By ordering the components of and we will assume without generality that and . Suppose that . By symmetry, we can assume without loss of generality that . There are 3 cases to consider.

-

•

. Then, let such that . Then, belongs to the permissible region in (A.12) and

for some function such that for such . This implies that

which is impossible. Hence, .

-

•

. Then, this implies that and . We show that we have . Indeed, suppose that . Take now such that . This means that . Then, for implying that . Also, . Thus, belongs to the permissible region in (A.12). Then, we have that

which implies that

which is impossible. Using a similar argument, we can show that we cannot have . Hence, . Also, one can show successively that for and finally that .

-

•

. Suppose that for all . Then,

for all such that . It is easy to see that this implies that , which can be shown by assuming that this does not hold. Now, suppose one of the coefficients . Consider then the integer such that and . Note that we necessarily have . Recall also that we are in the case where . Then, using the same argument as in the second case, we can successively show that

These equalities will enable us to show that .

Thus, in all the cases considered, the assumption leads to a contradiction. Using a recursive reasoning, we conclude that we should have for all . Therefore, in general, and without assuming that the elements of and are ordered, consists of all vectors such that for some permutation we have . Consequently and hence .

A.8 Auxiliary results for the proof of Theorem 7

In the sequel, we would need the following definition. For a given class of functions with envelope we define

| (A.13) |

where is the -covering number of with respect to . The supremum in (A.13) is taken over probability measure such that .

To make the notation used below more compact, we shall use the classical empirical process notation

For random vector we define its norm in as

Additionally, we use the fact that

together with the inequality in (A.8) shown above

Proposition 11

Consider the classes of functions , , and defined as

with , and

Then, we have

Proof (Proposition 11). We begin with the class . This class is a VC-class with index equal to ; see Example 2.6.1 in van der Vaart and Wellner (1996). Since is an envelope for the class, it follows from Theorem 2.6.7 of van der Vaart and Wellner (1996) that for any probability measure and

for some universal constant . With the definition given in (A.13) and inequality for any , it follows that

by (A.8). By Theorem 2.4.1 in van der Vaart and Wellner (1996), we have that

For the class , we use a small adaptation of Lemma 2.6.16 in van der Vaart and Wellner (1996) with to claim that it is a VC-class with index . The main difference between our setting and the one in that lemma is that we have instead of a univariate . However, the main argument in the proof of this lemma remains the same. Since is an envelope, we conclude using arguments similar to those above to show that

Now, we turn to the class , and we start by showing that it is contained in a VC-hull. Without loss of generality, suppose that . Then,

| (A.14) |

where

Now, consider the class of functions

Then, is a finite-dimensional space with dimension . Lemma 2.6.15 of van der Vaart and Wellner (1996) implies that this class is a VC-subgraph of index smaller than . Let be the class defined as

Let us denote and . The key observation is that

where denotes the minimum. The equality above is true since and are indicator functions which implies that for any pair we have that . Now, It follows by (i) of Lemma 2.6.18 in van der Vaart and Wellner (1996) that is VC. This implies that is VC. Given the definition of in (A.14), it follows that the class is a subset of the convex hull of . By the mean value Theorem, we can find some real number (depending on , , and ) such that

Thus, using the assumption that and the Cauchy-Schwarz inequality, it follows that

is an envelope of . By Theorem 2.6.9 of van der Vaart and Wellner (1996), we can find an integer and a universal constant such that we have for any probability measure satisfying , i.e.,

Hence, with

since . Under the assumption that , we are allowed to use Theorem 2.4.1 in van der Vaart and Wellner (1996) to conclude that

which completes the proof.

Proposition 12

Let be the class of monotone functions such that . Consider the class

Then, there exists a universal constant such that for all

where denotes the -bracketing number for with respect to .

Proof (Proposition 12). Fix and let . For , we can find and brackets , and such that

and and . Then,

and

using the fact that . Hence, implying that

where the last inequality follows from Theorem 2.7.5 of van der Vaart and Wellner (1996). It follows that

with .

Proposition 13

Let be a real function such that for some constant . Suppose, there exist real numbers such that is non-decreasing , non-increasing on and non-increasing on . Let be a random vector such that . Let be the empirical distribution of that are independent and identically distributed as . Then

Proof (Proposition 13). Consider the function class and note that it is dimensional. By Lemma 2.6.15 of van der Vaart and Wellner (1996), is a VC class with index . Define the functions

Fix such that . Then, we can write

Functions , , , and are all bounded monotone functions. Following from Lemma 2.6.18 (viii) and (vi), Theorem 2.6.7, Theorem 2.14.1 of van der Vaart and Wellner (1996) for we have

Application of Chebychev’s inequality yields the claim.

Proposition 14

There exists a constant depending only on such that for small enough we have that

Proof (Proposition 14). We begin with rewriting and for a given . For and define the function

Then,

Since for all , we have

Therefore,

with

These together with gives

Since , the triangle inequality gives us

Then by Cauchy-Schwarz inequality

We also have that

since implies . This implies that

Now,

and hence

We have that

which implies

Finally, to bound , note that

where

More explicitly,

Functions are non-decreasing and for . Thus, defined in Proposition 12. For define

Since and , it follows from Lemma 3.4.2 of van der Vaart and Wellner (1996) that

Now, by Proposition 12 and for small enough we have

Thus,

Taking , there exists a constant such that

which completes the proof.

Proposition 15

Assume that admits a density such that , and are bounded by some constant , and . Also, assume that matrix

is positive definite. Then, there exists a small neighborhood of and a constant such that for all in this neighborhood

Proof (Proposition 15). We need to show that

is twice continuously differentiable in a small neighbourhood of such that

| (A.15) |

and the Hessian matrix is positive definite. We can write

where

By assumption, the distribution function is continuously differentiable on , and hence

Furthermore, and by the assumption of the proposition, we have and . Hence, for any fixed , which is integrable. Thus, by the Dominated Convergence Theorem, it follows that for any fixed

and hence

Since , it follows that for all . Thus,

From the Dominated Convergence Theorem, it follows that for any

In particular, (A.15) holds. Now, we show that the multivariate

is continuously differentiable on with a positive definite Hessian at . Since we have already shown that is differentiable, we need to show differentiability of

| (A.16) |

Using the assumption that is continuously differentiable such that , we can use arguments that are very similar to those above to show that the function in (A.17) is indeed differentiable with gradient

| (A.17) |

Thus, for a fixed

For , we have that

| (A.18) |

using the Cauchy-Schwarz inequality and the fact that . The term on the right of (A.8) is a constant and hence integrable with respect to . Using the Dominated convergence Theorem again, it follows that is twice continuously differentiable and

Therefore we have

which is positive definite by assumption. Using Taylor expansion of up to the second order, and using and (A.15) we can write

If is the smallest eigenvalue of , then and also . Also, there exist a small enough neighborhood of such that when is in this neighborhood we have . This implies that for in this neighbourhood

which completes the proof.

Theorem 16

Let , , and two independent standard Brownian Bridges from to . Assume that admits a density which is continuously differentiable and that , and are bounded by . There exist an integer and such that is monotone on , and non-increasing on and . Let

Then,

in , where

with . Furthermore, if the matrix

is positive definite then is the unique minimizer of the process where

Proof (Therem 16). Let for a fixed . Using Taylor expansion, we have

for some between and . Furthermore, we shall use the well-known fact that if are i.i.d. then there exists a Brownian Bridge defined on the same probability space as such that

almost surely, where is defined such that for all for all we have

Now,

where

Using again

where , and , and .

Now let and . Then,

Define now the function

for , where and are two independent standard Brownian Bridges from to defined on the same probability space as and such that and almost surely. We show now that

Let and . Then,

where

Since we have

where

We show now that . As it is easy to adapt the proof of Proposition 13 for any integer , we have that

Now, for any we have that

where the last inequality follows from Cauchy-Schwarz. It follows that

To handle the last term, we apply the SLLN to show that

since by assumption. It follows that

in probability. Now, we show that

in . Here, we will apply Theorem 1.5.4 of van der Vaart and Wellner (1996). First, we show that the process

is asymptotically tight. We have that for all

Using a classical result about Brownian Bridge, it follows that for any we can find such that

This implies that with

Next, denote . We will show that for any finite integer , and ,

as . We will show the stronger result that the convergence above occurs almost surely. Let . The distribution function is continuous on and hence

| (A.19) |

is continuous. In fact, it is known that the Brownian Bridge is continuous on . Also, the function

is continuous at every point by the dominated convergence Theorem: The function is continuous and

is integrable. By the same theorem, we show that the function is continuous: is continuous and is integrable with respect to . Also, the function in (A.8) is bounded by

Since converges weakly to almost surely and the continuity of the function, it follows that

Since are arbitrary it follows that

as . This completes the proof that

in . Lastly, let us put

Then, we can write

which is a quadratic form. It admits a unique minimum if the matrix

is positive definite, in which case the unique minimizer solves the equation

or equivalently .

A.9 Proof of Theorem 7

A.10 Proof of Theorem 8

Proof

The arguments are the same as those used in the proof of Theorem 7 except that we replace by as defined in the statement of the theorem.

A.11 Proof of Proposition 9

Proof Let . Note that with probability one, we have

We can rewrite as

We have

where

and

To complete the proof, it is enough to show that there exist constants , and such that

| (A.20) |

and

| (A.21) |

With (A.20), and (A.21) we have

and

and therefore, we can conclude that there exists such that

Therefore for we have

To complete the proof, we need to prove (A.20), and (A.21). Let’s start by proving (A.20). First note that

where is a matrix such that its rows are from the matched data. Also with . Let then it follows that

where in the above equality, we are using the fact about trace that . Now let , then we have

Note that is based on the matched sample and is computed using the unmatched sample and . Therefore, and are independent of each other. This gives us

According to Kleinman and Athans (1968) we have

where and are respectively the smallest and largest eigenvalues of . To bound , let and and note that

Therefore

By Weyl’s theorem, we have

On the other hand, with high probability, we have

for all . Putting these together gives us a high probability

where are constants which depends on and . This gives us

and this conclude (A.20).

A.12 Uniqueness in Example 1

We show that for such that

we have . We prove this by contradiction.

Proof Assume . Take . Let and . Note that in this case both and lead to the same distribution for and hence using the moment generating function of we have

| (A.22) |

for all such that and . First suppose . By rewriting (A.22), we have

for all such that . This equality holds if and only if and . By symmetry, we reach the same conclusion assuming . Now assume and . Without loss of generality assume . Then we rewrite (A.22) as

| (A.23) |

for all such that and . We study this within the following cases:

Case 1: . In this case we have and hence the equality in (A.23) holds for . Now note that

which is contradiction with (A.23).

Case 2: . In this case (A.23) must hold for . Taking the limit again we reach contradiction.

Case 3: . In this case (A.23) must hold for . Taking the implies

which is again a contradiction. Therefore we must have which implies

for all which means

Since this implies .

References

- Abid et al. (2017) Abubakar Abid, Ada Poon, and James Zou. Linear regression with shuffled labels. arXiv preprint arXiv:1705.01342, 2017.

- Balabdaoui et al. (2021) Fadoua Balabdaoui, Charles R Doss, and Cécile Durot. Unlinked monotone regression. The Journal of Machine Learning Research, 22(1):7766–7825, 2021.

- Carpentier and Schlüter (2016) Alexandra Carpentier and Teresa Schlüter. Learning relationships between data obtained independently. In Proceedings of the 19th International Conference on Artificial Intelligence and Statistics, pages 658–666, 2016.

- Casella and Berger (1990) George Casella and Roger L. Berger. Statistical inference. The Wadsworth & Brooks/Cole Statistics/Probability Series. Wadsworth & Brooks/Cole Advanced Books & Software, Pacific Grove, CA, 1990.

- Cohen and Richman (2002) William W Cohen and Jacob Richman. Learning to match and cluster large high-dimensional data sets for data integration. In Proceedings of the eighth ACM SIGKDD international conference on Knowledge discovery and data mining, pages 475–480, 2002.

- D’Haultfoeuille et al. (2022) Xavier D’Haultfoeuille, Christophe Gaillac, and Arnaud Maurel. Partially linear models under data combination. Technical report, National Bureau of Economic Research, 2022.

- Dvoretzky et al. (1956) A. Dvoretzky, J. Kiefer, and J. Wolfowitz. Asymptotic minimax character of the sample distribution function and of the classical multinomial estimator. Ann. Math. Statist., 27:642–669, 1956.

- Edelman (1988) David Edelman. Estimation of the mixing distribution for a normal mean with applications to the compound decision problem. Ann. Statist., 16(4):1609–1622, 1988.

- Fan (1991) Jianqing Fan. On the optimal rates of convergence for nonparametric deconvolution problems. Ann. Statist., 19(3):1257–1272, 1991.

- Hsu et al. (2017) Daniel J Hsu, Kevin Shi, and Xiaorui Sun. Linear regression without correspondence. Advances in Neural Information Processing Systems, 30, 2017.

- Kleinman and Athans (1968) David L. Kleinman and Michael Athans. The design of suboptimal linear time-varying systems. IEEE Trans. Automatic Control, AC-13:150–159, 1968.

- Meis and Mammen (2021) Jan Meis and Enno Mammen. Uncoupled isotonic regression with discrete errors. In Advances in Contemporary Statistics and Econometrics, pages 123–135. Springer, 2021.

- Monge et al. (1996) Alvaro E Monge, Charles Elkan, et al. The field matching problem: algorithms and applications. In Kdd, volume 2, pages 267–270, 1996.

- Nelder and Mead (1965) John A Nelder and RA Mead. Simplex method for function minimization, the computer journal, 7. 1965.

- Olivetti and Paserman (2015) Claudia Olivetti and M Daniele Paserman. In the name of the son (and the daughter): Intergenerational mobility in the united states, 1850-1940. American Economic Review, 105(8):2695–2724, 2015.

- Pananjady et al. (2018) Ashwin Pananjady, Martin J Wainwright, and Thomas A Courtade. Linear regression with shuffled data: statistical and computational limits of permutation recovery. IEEE Trans. Inform. Theory, 64(5):3286–3300, 2018.

- Rigollet and Weed (2019) Philippe Rigollet and Jonathan Weed. Uncoupled isotonic regression via minimum Wasserstein deconvolution. Inf. Inference, 8(4):691–717, 2019.

- Ruggles et al. (2010) Steven Ruggles, J Trent Alexander, Katie Genadek, Ronald Goeken, Matthew B Schroeder, Matthew Sobek, et al. Integrated public use microdata series: Version 5.0 [machine-readable database]. Minneapolis: University of Minnesota, 42, 2010.

- Sheather and Jones (1991) S. J. Sheather and M. C. Jones. A reliable data-based bandwidth selection method for kernel density estimation. J. Roy. Statist. Soc. Ser. B, 53(3):683–690, 1991.

- Slawski and Ben-David (2019) Martin Slawski and Emanuel Ben-David. Linear regression with sparsely permuted data. Electron. J. Stat., 13(1):1–36, 2019.

- Slawski and Sen (2022) Martin Slawski and Bodhisattva Sen. Permuted and unlinked monotone regression in : an approach based on mixture modeling and optimal transport. arXiv preprint arXiv:2201.03528, 2022.

- Slawski et al. (2020) Martin Slawski, Emanuel Ben-David, and Ping Li. A two-stage approach to multivariate linear regression with sparsely mismatched data. J. Mach. Learn. Res., 21(204):1–42, 2020.

- Slawski et al. (2021) Martin Slawski, Guoqing Diao, and Emanuel Ben-David. A pseudo-likelihood approach to linear regression with partially shuffled data. Journal of Computational and Graphical Statistics, 30(4):991–1003, 2021.

- Tsakiris and Peng (2019) Manolis C. Tsakiris and Liangzu Peng. Homomorphic sensing. Proceedings of the 36th International Conference on Machine Learning, pages 6335–6344, 2019.

- Tsakiris et al. (2020) Manolis C. Tsakiris, Liangzu Peng, Aldo Conca, Laurent Kneip, Yuanming Shi, and Hayoung Choi. An algebraic-geometric approach for linear regression without correspondences. IEEE Transactions on Information Theory, 66(8):5130–5144, 2020.

- Unnikrishnan et al. (2018) Jayakrishnan Unnikrishnan, Saeid Haghighatshoar, and Martin Vetterli. Unlabeled sensing with random linear measurements. IEEE Trans. Inform. Theory, 64(5):3237–3253, 2018.

- van der Vaart (1998) A. W. van der Vaart. Asymptotic statistics, volume 3 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 1998.

- van der Vaart and Wellner (1996) Aad W. van der Vaart and Jon A. Wellner. Weak convergence and empirical processes. Springer Series in Statistics. Springer-Verlag, 1996.

- Walter and Fritsch (1999) Volker Walter and Dieter Fritsch. Matching spatial data sets: a statistical approach. International Journal of geographical information science, 13(5):445–473, 1999.

- Zhang et al. (2021) Hang Zhang, Martin Slawski, and Ping Li. The benefits of diversity: Permutation recovery in unlabeled sensing from multiple measurement vectors. IEEE Transactions on Information Theory, 2021.