Branching Processes in Random Environments with Thresholds

Abstract

Motivated by applications to COVID dynamics, we describe a branching process in random environments model whose characteristics change when crossing upper and lower thresholds. This introduces a cyclical path behavior involving periods of increase and decrease leading to supercritical and subcritical regimes. Even though the process is not Markov, we identify subsequences at random time points - specifically the values of the process at crossing times, viz., - along which the process retains the Markov structure. Under mild moment and regularity conditions, we establish that the subsequences possess a regenerative structure and prove that the limiting normal distribution of the growth rates of the process in supercritical and subcritical regimes decouple. For this reason, we establish limit theorems concerning the length of supercritical and subcritical regimes and the proportion of time the process spends in these regimes. As a byproduct of our analysis, we explicitly identify the limiting variances in terms of the functionals of the offspring distribution, threshold distribution, and environmental sequences.

Key Words. BPRE, COVID dynamics, Ergodicity of Markov chains, Estimators of growth rate, Length of cycles, Martingales, Random sums, Regenerative structure, Size-dependent branching process, Size-dependent branching process with a threshold, Subcritical regime, Supercritical regime.

Math Subject Classification 2020. Primary: 60J80, 60F05, 60J10; Secondary: 92D25, 92D30, 60G50, 62F10.

1 Introduction

Branching processes and their variants are used to model various biological, biochemical, and epidemic processes (see Jagers (1975); Haccou et al. (2007); Hanlon and Vidyashankar (2011); Kimmel and Axelrod (2015)). More recently, these methods have been used as a model for spreading COVID cases in a community during the early stages of the pandemic (Yanev et al.; 2020; Atanasov et al.; 2021). As the time progressed, the number of infected members in a community changed due to different containment efforts of the local communities (Falcó and Corral; 2022; Sun et al.; 2022) leading to periods of increase and decrease. In this paper, we describe a stochastic process model built on a branching process model in random environments that explicitly takes into account periods of growth and decrease in the transmission rate of the virus.

Specifically, we consider a branching process model initiated by a random number of ancestors (thought of as initiators of the pandemic within a community). During the first several generations, the process grows uncontrolled, allowing immigration into the system. This initial phase is modeled using a supercritical branching process with immigration in random environments, specifically independent and identically distributed (i.i.d.) environments. When consequences of rapid spread become significant, policymakers introduce restrictions to reduce the rate of growth, hopefully resulting in a reduced number of infected cases. The limitations are modeled using upper thresholds on the number of infected cases, and beyond the threshold the process changes its character to evolve as a subcritical branching process in random environments. During this period - due to strict controls - immigration is also not allowed. In practical terms, this period typically involves a “lockdown” and other social containment efforts, the intensity of which varies across communities.

The period of restrictions is not sustainable for various reasons, including political, social, and economic pressures leading to the easing of controls. The policymakers use multiple metrics to gradually reduce controls, leading to an “opening of communities”, resulting in increased human interactions. As a result or due to changes undergone by the virus, the number of infected cases increases again. We use lower thresholds in the number of “newly infected” to model the period of change and let the process evolve again as a supercritical BPRE in i.i.d. environments after it crosses the lower threshold. The process continues to evolve in this manner alternating between periods of increase and decrease. In this paper, we provide a rigorous probabilistic analysis of this model.

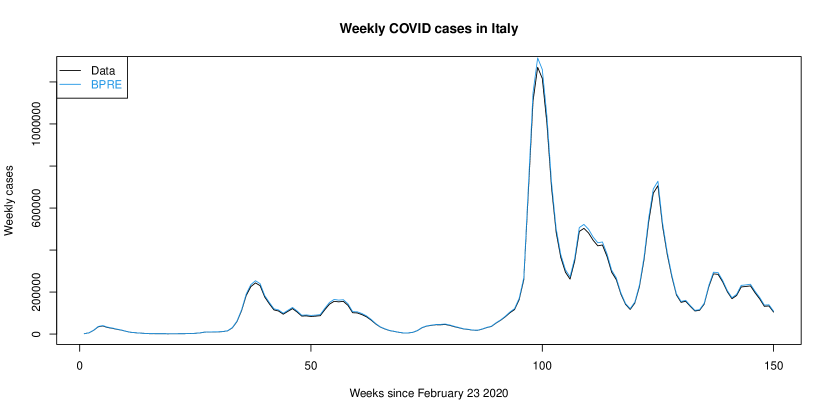

Even though we used the dynamics of COVID spread as a motivation for the proposed model, the aforementioned cyclic behavior is often observed in other biological systems, such as those modeled as a predator-prey model or the SIR model. In some biological populations, the cyclical behavior can be attributed to the decline of fecundity as the population size approaches a threshold (Klebaner; 1993). Deterministic models such as ordinary differential equations, dynamical systems, and corresponding discrete time models are used for analysis in the applications mentioned above (Teschl; 2012; Perko; 2013; Iannelli and Pugliese; 2014). While many models described above yield good qualitative descriptions, uncertainty estimates are typically unavailable. It is worthwhile to point out that previously described branching process methods also produce reasonable point estimates for the mean growth during the early stages of the pandemic. However, the above-mentioned point estimates of the growth rate are unreliable during the later stages of the pandemic. In this paper, we address statistical estimation of the mean growth and characterize the variance of the estimates. We end the discussion with a plot, Figure 1, of the total number of confirmed COVID cases per week in Italy from February 23, 2020 to July 20, 2022. The plot also includes the number of cases using the proposed model.

Other examples with similar plots include the hare-lynx predator-prey dynamics and measles cases (Tyson et al.; 2010; Iannelli and Pugliese; 2014; Hempel and Earn; 2015).

Before we provide a precise description of our model, we begin with a brief description of BPRE with immigration. Let be i.i.d. random variables taking values in , where is the space of probability distributions on ; that is, and for some non-negative integers and such that and . The process is referred to as the environmental sequence. For each realization of , we associate a population process defined recursively as follows: let take values on the positive integers and

where, given , are i.i.d. with distribution and is an independent random variable with distribution . The random variable , where , plays an important role in classification of BPRE with immigration. It is well-known that when the process diverges to infinity with probability one and if and the immigration is degenerate at zero for all environments then the process becomes extinct with probability one (Athreya and Karlin; 1971). Furthermore, in the subcritical case, that is , one can further identify three distinct regimes: (i) weakly subcritical, (ii) moderately subcritical, and (iii) strongly subcritical. (i) corresponds to when there exists a such that , while (ii) corresponds to the case when . Finally, (iii) corresponds to the case when (Kersting and Vatutin; 2017). In this paper, when working with the subcritical regime, we will assume that the process is strongly subcritical and refer to it as subcritical process in the rest of the manuscript.

We now turn to a description of the model. Let , where , denote a collection of supercritical environmental sequences. Here, indicates the offspring distribution and represents the immigration distribution. Also, let , where , denote a collection of subcritical environmental sequences. We now provide an evolutionary description of the process: at time zero the process starts with a random number of ancestors . Each of them live one unit of time and reproduce according to the distribution . Thus, the size of the first generation population is

where, given , are i.i.d. random variables with offspring distribution and independent of the immigration random variable with distribution . The random variable is interpreted as the number of children produced by the parent in the generation and is interpreted as the number of immigrants whose distribution is generated by the same environmental random variable .

Let denote the random variable representing the upper threshold. If , each of the first generation population live one unit of time and evolve, conditionally on the environment, as the ancestors independent of the population size at time one. That is,

As before, given , are i.i.d. with distribution and has distribution . The random variables are independent of , , and , . If , then

where, given , are i.i.d. with distribution . Thus, the size of the second generation population is

The process is defined recursively as before. As an example, if , or , , for a random lower threshold , then the process will evolve like a supercritical BPRE with offspring distribution and immigration distribution . Otherwise (that is, and or and ), the process will evolve like a subcritical BPRE with offspring distribution . This dynamics continues with different thresholds yielding the process which we refer to as branching process in random environments with thresholds (BPRET). The consecutive set of generations where the reproduction is governed by a supercritical BPRE is referred to as the supercritical regime, while the other is referred to as the subcritical regime. As we will see below, non-trivial immigration in the supercritical regime is required to obtain alternating periods of increase and decrease.

The model described above is related to size dependent branching processes with a threshold as studied by Klebaner (1993) and more recently by Athreya and Schuh (2016). Specifically, in that model the offspring distribution depends on a fixed threshold and the size of the previous generation. As observed in these papers, these Markov processes either explode to infinity or are absorbed at zero. In our model the thresholds are random and dynamic resulting in a non-Markov process; however, the offspring distribution does not depend on the size of the previous generation as long as they belong to the same regime. Indeed, when for all , the immigration distribution is degenerate at zero, and the environment is fixed, one obtains as a special case the density dependent branching process (see for example Klebaner (1984, 1993); Jagers and Klebaner (2011); Athreya and Schuh (2016)). Additionally, while the model of Klebaner (1993) uses Galton-Watson process as a building block, our model uses branching processes in i.i.d. environments.

Continuing with our discussion on the literature, Athreya and Schuh (2016) show that in the fixed environment case the special case of size-dependent process with a single threshold becomes extinct with probability one. We show that this is also the case for the BPRE when there is no immigration, and the details are in Theorem 2.1. Similar phenomenon have been observed in slightly different contexts in Jagers and Zuyev (2020, 2021). Incorporation of immigration component ensures that the process is not absorbed at zero and hence may be useful for modeling stable populations at equilibrium as done in deterministic models. For an additional discussion see Section 7.

For the ease of further discussions we introduce a few notations. Let and , where

that is, and represent the offspring means conditional on the environment and , respectively. Also, let denote the immigration mean conditional on the environment; and

denote the conditional variance of the offspring distributions given the environment.

From the description, it is clear that the crossing times at the thresholds of , namely and will play a significant role in the analysis. It will turn out that and will form a time homogeneous Markov chain with state space and , respectively, where we take and for all . Under additional conditions on the offspring distribution and the environment sequence, the processes and will be uniformly ergodic. These results are established in Section 3.

The amount of time the process spends in the supercritical and subcritical regimes, beyond its mathematical and scientific interest, will also arise when studying the central limit theorem for the estimates of and . Using the uniformly ergodicity alluded to above, we will establish that the time averages of and converge to finite positive constants, and . Additionally, we establish a central limit theorem (CLT) related to this convergence under a finite second moment hypothesis after an appropriate centering and scaling; that is,

and we characterize in terms of the stationary distribution of the Markov chain. A similar result also holds for . This, in turn, provides qualitative information regarding the proportion of time the process spends in these regimes. That is, if is the amount of time the process spends in the supercritical regime up to time we show that converges to ; a related central limit theorem is also established and in the process we also characterize the limiting variance. Interestingly, we show that the CLT prevails even for the joint distribution of the length of time and the proportion of time the process spends in supercritical and subcritical regimes. These results are described in Sections 4 and 5.

An interesting question concerns the rate of growth of the BPRET in the supercritical and subcritical regimes described by the corresponding expectations, namely and . Specifically, we establish that the limiting joint distribution of the estimators is bivariate normal with a diagonal covariance matrix yielding asymptotic independence of the mean estimators derived using data from supercritical and subcritical regimes. In the classical setting of a supercritical BPRE without immigration this problem has received some attention (see for instance Dion and Esty (1979)). The problem considered here is different in the following four ways: (i) the population size does not converge to infinity, (ii) the lengths of the regimes are random, (iii) in the supercritical regime the population size may be zero, and (iv) there is an additional immigration term. While (iii) and (iv) can be accounted for in the classical settings as well, their effect on the point estimates is minimized due to the exponential growth of the population size. Here, while the exponential growth is ruled out, perhaps as anticipated, the Markov property of the process at crossing times, namely and and their associated regeneration times play a central role in the proof. It is important to note that, it is possible that both regimes occur between regeneration times. Hence, also the proportion of time the process spends in the supercritical and subcritical regime plays a vital role in deriving the asymptotic limit distribution. The limiting variance of the estimators depend additionally on and , beyond , , , and . In the special case of fixed environments, the limit behavior of the estimators takes a different form compared to the traditional results as described for example in Heyde (1971). These results are in Section 6.

Finally, in Appendix B we provide some numerical experiments illustrating the behavior of the model. Specifically, we illustrate the effects of different distributions on the path behavior of the process and describe how they change when the thresholds increase. The experiments also suggests that if different regimes are not taken into account the true growth rate of the virus may be underestimated. We now turn to Section 2 where we develop additional notations and provide a precise statement of the main results.

2 Main results

Branching process in random environments with thresholds (BPRET) is a supercritical BPRE with immigration until it reaches an upper threshold after which it transitions to a subcritical BPRE until it crosses a lower threshold. Beyond this time the process reverts to a supercritical BPRE with immigration and the above cycle continues. Specifically, let denote a collection of thresholds (assumed to be i.i.d.). Then, the BPRET evolves like a supercritical BPRE with immigration until it reaches the upper threshold at which time it becomes a subcritical BPRE. The process remains subcritical until it crosses the threshold ; after that it evolves again as a supercritical BPRE with immigration, and so on. We now provide a precise description of BPRET.

Let be i.i.d. random vectors with support , where , , and are fixed integers. We denote by and the supercritical and subcritical environmental sequences; that is,

We use the notations and for probability statements with respect to (w.r.t.) the supercritical and subcritical environmental sequences. As in the introduction, given the environment, are i.i.d. random variables with distribution and are independent of the immigration random variable . Similarly, conditionally on the environment, are i.i.d. random variables with offspring distribution . Finally, let be an independent random variable with support included in . We emphasize that the thresholds are independent of the environmental sequences, offspring random variables, immigration random variables, and . For technical details regarding the construction of the probability space we refer to Appendix A.1. We denote by , , and the annealed (averaged over the environment) offspring mean and the annealed immigration mean respectively. Throughout the manuscript, we make the following assumptions on the environmental sequences.

Assumptions:

-

(H1)

are i.i.d. environments such that and -a.s.

-

(H2)

, , , and .

-

(H3)

and .

-

(H4)

are i.i.d. and have support , where and .

The above assumptions rule out degenerate behavior of the process and are commonly used in the literature on BPRE (see Assumption R and Theorem 2.2 of Kersting and Vatutin (2017)). Assumption (H2) states that is a supercritical environment and is a (strongly) subcritical environment. Additionally, using Jensen’s inequality it follows that and . Assumption (H3) states that immigration is positive with positive probability and has finite expectation , while (H4) states that the upper thresholds have finite expectation.

We are now ready to give a precise definition of the BPRET. Let . Starting from , the BPRET is defined recursively over as follows.

-

1j.

For and until

(1) Next, let .

-

2j.

For and until

(2) Next, let .

It is clear from the definition that and are stopping times w.r.t. the -algebra generated by and the thresholds . Thus, , , , , and are well-defined random variables.

It is also clear from the above definition that the intervals and represent supercritical and subcritical intervals, respectively. We show below that the process exits and enters the above intervals infinitely often. Let and denote the length of these intervals. Since a supercritical BPRE with immigration diverges with probability one (see Theorem 2.2 of Kersting and Vatutin (2017)), it follows that is finite whenever is finite:

| (3) |

We emphasize that Assumption (H3) is required since, otherwise, if the process may fail to cross the upper threshold and becomes extinct (see Theorem 2.1 below). On the other hand, since strongly subcritical BPRE becomes extinct with probability one, whenever , that is,

| (4) |

Using and induction over we see that , , , and are finite almost surely. We emphases that (4) holds whenever is a subcritical or critical (but not strongly critical) environmental sequence (see Definition 2.3 in Kersting and Vatutin (2017)). That is, it remains valid if the assumption in (H2) is weakened to and , which leads to the following assumption:

-

(

, , and .

The next theorem shows that if immigration is zero the process becomes extinct almost surely.

Theorem 1 of Athreya and Schuh (2016) follows from the above theorem by taking , , , where is a finite positive integer, and assuming that the environments are fixed in both regimes.

2.1 Path properties of BPRET

We now turn to transience and recurrence of the BPRET . Notice that even though is not Markov the concepts of recurrence and transience can be studied using the definition given below (due to Lamperti (1960, 1963)).

Definition 1.

A non-negative stochastic process satisfying is said to be recurrent if there exists an such that and transient if .

Our next result is concerned with the path behavior of and the stopped sequences and .

Theorem 2.2.

We now turn to the ergodicity properties of and . These rely on conditions on the offspring distribution that ensures the Markov chains and are irreducible and aperiodic. While several sufficient conditions are possible, we provide below some possible conditions.

-

(H5)

.

-

(H6)

and for some .

-

(H7)

.

(H5) requires that on a set of positive probability an individual can produce zero and one offspring while (H6) requires that on a set of positive probability for all and . Also, on a set of positive probability, for some . Finally, (H7) states that on a set of positive probability and for all . These are weak conditions on the environment sequences and are part of standard BPRE literature. We recall that is the set of non-negative integers not larger than and is the set of integers larger than .

Theorem 2.3.

When the assumptions (H1)-(H6) (or (H7)) hold, we denote by and the stationary distributions of the ergodic Markov chains and , respectively. While has moments of all orders, we show in Proposition A.1 below, that has a finite first moment. These distributions will play a significant role when studying the length of supercritical and subcritical regime which we now undertake.

2.2 Length of supercritical and subcritical regime

We now turn to the law of large numbers and central limit theorem for the differences and . We denote by , , , and probability, expectation, variance, and covariance conditionally on . Similarly, when is replaced by in the above quantities, we understand that they are conditioned on . We define , ,

| (5) | ||||

| (6) |

In the supercritical regime, we impose an additional assumption (H8) below, so as to not qualify our statements with the phrase “on the set of non-extinction”. Assumption (H9) below ensures that the immigration distribution stochastically dominates the upper threshold.

-

(H8)

-a.s.

-

(H9)

.

Let and . We now state the main result of this subsection.

2.3 Proportion of time spent in supercritical and subcritical regime

We now consider the proportion of time the process spends in the subcritical and supercritical regimes. To this end for , let be the indicator function assuming value if at time the process is in the supercritical regime and otherwise. Similarly, let take value if at time the process is in the subcritical regime and otherwise. Furthermore, let and be the total time that the process spends in the supercritical and subcritical regime, respectively, up to time . Let

denote the proportion of time the process spends in the supercritical and subcritical regimes. Our main result in this section is concerned with the central limit theorem for and . To this end, let

Theorem 2.5.

We use these results to now describe the growth rate of the process, as defined by their expectations, in the supercritical and subcritical regime; that is, and .

2.4 Offspring mean estimation

We begin by noticing that and are positive for all . However, there may be instances where could be zero. To avoid division by zero in (7) below, we let , , and use the convention that . The generalized method of moments estimators of and are given by

| (7) |

where the last term is non-trivial whenever , that is . Our assumptions will involve first and second moments assumptions on the centered offspring means and the centered offspring random variables . To this end, we define the quantities and . Next, let , , and be the diagonal matrix with elements

where is the average length of supercritical regime not taking into account the times in which the process is zero, is the average proportion of time the process spends in the supercritical regime and is positive, is the average sum of over a supercritical regime discarding the times in which is zero, and is the average sum of over a subcritical regime. Obviously, . Finally, we recall that is the variance of the random offspring mean and is the expectation of the random offspring variance .

Theorem 2.6.

Remark 2.1.

In the fixed environment case and are deterministic constants. Therefore, and is the diagonal matrix with elements

3 Path properties of BPRET

In this section we provide the proofs of Theorems 2.1, 2.2, and 2.3 along with the required probability estimates. The proofs rely on the fact that both the environmental sequence and the thresholds are i.i.d. It follows that probability statements like and do not depend on the index . This idea is made precise in Lemma A.1 in Appendix A.2 and will lead to time homogeneity of and . Expectedly, this property does not depend on the process being strongly subcritical: Assumptions (H1) and ( are more than enough. We denote by , , , and probability, expectation, variance, and covariance conditionally on , where is the restriction of the Dirac delta to . Similarly, when is replaced by in the above quantities, we understand that they are conditioned on , where is the restriction of the Dirac delta to .

3.1 Extinction when immigration is zero

In this subsection, we provide the proof of Theorem 2.1, which is an adaptation of Theorem 1 of Athreya and Schuh (2016) for BPRE. Recall that for this theorem there is no immigration in the supercritical regime and hence the extinction time is finite with probability one.

Proof of Theorem 2.1.

Set, for simplicity, . We partition the sample space as

and show that (i) for all and (ii) . First, we notice that if then, using Theorem 2.1 of Kersting and Vatutin (2017), . Thus,

where is a supercritical BPRE until is reached. Since for all , (2.6) of Kersting and Vatutin (2017) yields that a.s. and . Turning to (ii), since the events are nonincreasing, and . Since , if , it follows that

Lemma A.1 yields that for all

| (8) |

Also, for all

Multiplying by and and summing over in (8), we obtain that

Set , where . Since and for some , we have that and . Hence, . Iterating the above argument it follows that yielding . ∎

3.2 Markov property at crossing times

Proof of Theorem 2.2.

We begin by proving (i). We first notice that since are i.i.d. random variables with unbounded support , with probability one. Next, observe that along the subsequence , . Hence, . On the other hand, along the subsequence . Thus, . It follows that is recurrent in the sense of Definition 1. Turning to (ii), we first notice that, since , and for all , the state spaces of and of are included in and , respectively. We now establish the Markov property of . For all , , and , we consider the probability . By the law of total expectation this is equal to

Now, setting , , we have that

where in the second line we have used that is a supercritical BPRE with immigration until it crosses the threshold at time , and similarly is a subcritical BPRE until it crosses the threshold at time . By taking expectation on both sides, we obtain that

Turning to the time homogeneity property, we obtain from Lemma A.1 (iii) that

The proof for is similar. ∎

3.3 Uniform ergodicity of and

In this subsection we prove Theorem 2.3. The proof relies on the following lemma. We denote by , , and , , the -step transition probability of the (time homogeneous) Markov chains and . For , we also write and . Finally, let and be the -step transition probability of the Markov chains and from state (resp. ).

Lemma 3.1.

Proof of Lemma 3.1.

The idea of proof is to establish a lower bound on and using (9) and (10) below, respectively. We begin by proving (i). Using Assumptions (H5), let be a measurable subset of satisfying and for and . By the law of total expectation

| (9) |

Since on the event , it follows that

Now, notice that on the event the term is bounded below by the probability of reaching state from in one step; that is,

The RHS of the above inequality is bounded below by the probability that the first individuals have exactly one offspring and the remaining have no offspring, that is,

Once again, using that conditional on the environment , are i.i.d., this is equal to

Since and because , the last term is bounded below by

Finally, again using that are i.i.d. and taking the expectation as in (9), we obtain that , where

Notice that is positive because , , for and , and the environments are i.i.d. Finally, since is finite, .

We now turn to the proof of (ii), which is similar to the proof of (i). Using (H6), let and be measurable subsets of satisfying:

-

(a)

and , for all and ; and

-

(b)

and for (a fixed) and .

Again using the law of total expectation, we obtain

| (10) |

Since on the event , it follows that

| (11) |

If and , then is bounded below by the probability that individuals have a total of exactly offspring and no immigration occurs; that is,

The RHS of the above inequality is bounded below by the probability that the first individuals have offspring and the last individuals have offspring (indeed ) and no immigration occurs; that is,

Using that conditional on the environment , are i.i.d., the above is equal to

| (12) |

Next, if and then is bounded below by the probability . Now, this probability is bounded below by the probability that there are immigrants at time , these immigrants have a total of exactly offspring, and no immigration occurs at time ; that is,

As before, this last probability is bounded below by probability that individuals have offspring and individuals have offspring. Thus, the above probability is bounded below by

| (13) |

Combing (11), (12), and (13) and using that , we obtain that is bounded below by

Using that are i.i.d. and taking the expectation as in (10), we obtain that

where is given by

Since , we conclude that , where

This concludes the proof of (ii). If instead of (H6), (H7) holds the proof is similar by noticing that for all , on the event , there’s a positive probability that at time there are immigrants and the individuals have no offspring. A detailed proof can be obtained in the same manner. ∎

Before we turn to the proof of Theorem 2.3 we introduce few notations. Let and , , be the random times in which the Markov chain enters state when the initial state is . Similarly, we let and , , be the random times in which the Markov chain enters state when the initial state is . The expected times to visit state starting from is denoted by and , respectively.

Proof of Theorem 2.3.

Lemma 3.1 implies that the state spaces of and are and , respectively. Next, to establish ergodicity of these Markov chains, it is sufficient to verify irreducibility, aperiodicity, and positive recurrence. Irreducibility and aperiodicity follow from Lemma 3.1 in both cases. Now, turning to positive recurrence let for . Then, using Markov property and (i) of Lemma 3.1, it follows that

Now by the finiteness of it follows that is uniformly ergodic. Next, as above for all

To complete the proof of uniform ergodicity of , we will verify the Doeblin’s condition for one-step transition: that is, for a probability distribution and every set satisfying

Now, taking , it follows from Lemma 3.1 (ii) that

Choosing uniform ergodicity of follows. ∎

Remark 3.1.

An immediate consequence of the above theorem is that possesses a proper stationary distribution , where and satisfies for all . Furthermore, where denotes the total variation norm. Furthermore, under a finite second moment hypothesis the central limit theorem holds for functions of . Similar comment also holds for with replaced by .

Remark 3.2.

It is worth noticing that the stationary distributions and are connected using for all since by time homogeneity (Lemma A.1) . Now, taking the limit as in

the above expression follows. Similarly, for all .

4 Regenerative property of crossing times

In this section, we establish the law of large numbers and central limit theorem for the length of the supercritical and subcritical regimes and . To this end, we will show that and are regenerative over the times and , respectively. In our analysis we will also encounter the random variables and . For and let , where

The triple consists of the random time required by to return for the time to state , the lengths of all supercritical regimes between the return and the return, and the lengths of both regimes in the same time interval. Similarly, for and we let , where

The proof of the following lemma is included in Appendix A.4.

Lemma 4.1.

The proof of the following lemma, which is required in the proof of the Theorem 2.4, is also included in Appendix A.4. We need the following additional notations: , ,

Lemma 4.2.

Under the assumptions of Theorem 2.4, for all the following hold:

The above statements also hold with replaced by .

Proposition A.2 in Appendix A.5 shows that and are positive and finite, and . We are now ready to prove Theorem 2.4. The proof relies on decomposing and into i.i.d. cycles using Lemma 4.1. Specifically, conditionally on (resp. ), the random variables (resp. ) are i.i.d.

Proof of Theorem 2.4.

We begin by proving (i). For and , let be the number of times is in . Conditionally on , notice that is a renewal process (recall that ). We recall that and let , , and . Using the decomposition

| (14) |

are i.i.d. and a.s., we obtain using the law of large numbers for random sums and Lemma 4.2 (i) that

| (15) |

Also,

Finally, using the key renewal theorem (Corollary 2.11 of Serfozo (2009)) and Remark 3.1

| (16) |

Using (15) and (16) in (14), we obtain the SLLN for . Turning to the central limit theorem, we let and . Conditionally on , using the decomposition in (14) and centering, we obtain

where are i.i.d. with mean and variance which using Lemma 4.2 is

| (17) |

Finally, using the central limit theorem for i.i.d. random sums and (16), it follows that

To complete the proof notice that

The proof for is similar. ∎

When studying the proportion of time the process spends in supercritical and subcritical regimes we will need the above theorem with replaced by a random time .

Remark 4.1.

Theorem 2.4 holds if is replaced by a random time , where a.s.

5 Proportion of time spent in supercritical and subcritical regimes

We recall that is if the process is in the supercritical regime and otherwise and similarly . Also is the proportion of time the process spends in the supercritical regime up to time . is defined similarly. The limit theorems for and will invoke the i.i.d. blocks developed in Section 4. Let , , , and

We note that while represents the length of the first supercritical regimes is the total time taken for the process to complete the first cycles.

Lemma 5.1.

Under the conditions of Theorem 2.5, , and .

Proof of Lemma 5.1.

Remark 5.1.

Lemma 5.1 holds also with replaced by a random time such that a.s.

The next lemma concerns the number of crossings of upper and lower thresholds, namely, and where .

Lemma 5.2.

Under the conditions of Theorem 2.5,

(i) and a.s.

(ii) and a.s.

Proof Lemma 5.2.

We begin by proving (i). We recall that and a.s. for all yielding that

Since and are finite almost surely, we obtain that and a.s. (i) follows if we show that a.s. To this end, we notice that and for

Clearly, a.s. Remark 4.1 with yields that

Thus, we obtain

| (18) |

Turning to (ii), we notice that

where for . Remark 4.1 with yield that

Thus, we obtain that a.s. Similarly, a.s. ∎

Our next result is concerned with the joint distribution of the last time the process is in a specific regime and the proportion of time the process spends in that regime under the assumptions of Theorem 2.5. Let

Lemma 5.3.

Under the conditions of Theorem 2.5,

Proof of Lemma 5.3.

We are now ready to prove Theorem 2.5. Recall that , , , and ; and let and be the power of and , respectively.

Proof of Theorem 2.5.

Corollary 5.1.

Under the conditions of Theorem 2.4, for

6 Estimating the mean of the offspring distribution

We recall that , and set for the subcritical regime and . We also recall the offspring mean estimate of the BPRET in the supercritical and subcritical regimes are given by

The decomposition

| (20) |

will be used in the proof of Theorem 2.6 and involves the martingale structure of , where

| (21) |

Specifically, let be the -algebra generated by the random environments , the -algebra generated by and ; and the -algebra generated by , , and the offspring distributions , . Hence, , , and are -measurable, whereas is not -measurable. We also denote by the -algebra generated by and and the -algebra generated by , , and , . Hence, , , and are all -measurable but not -measurable. We establish in Proposition A.3 in Appendix A.6 that

are mean zero martingale sequences. Additionally, and , where is the sum of over supercritical time steps up to time discarding times in which is zero and is the sum of over subcritical time steps up to time . Proposition A.3 contains other two martingales involving the terms and in (21) and related moment bounds, which will be used in the proof of Theorem 2.6. As a first step, we derive the limit of the variances and when rescaled by . By Proposition A.3, this entails studying the limit behavior of the quantities and . To this end, we build i.i.d. blocks as in Section 4. For and let , where

, and . The triple consists of the random time required by to return for the time to state , the lengths of all supercritical regimes between the return and the return, and the sum of inverse over supercritical regimes, disregarding the times when the process hits zero. Similarly, for and we let , where

and . Notice that, since , Theorem 2.5 already yields that . We need the following slight modification of Lemma 4.1, whose proof is similar and hence omitted.

Lemma 6.1.

Proposition 6.1.

Since and are non-negative and bounded by one, Proposition 6.1 implies convergence in mean of these quantities.

Proof of Proposition 6.1.

By Lemma 5.2 (i) it is enough to show the first part of the statements (i)-(iii). Since the proof of the other cases is similar we only prove (i). We recall that for and , is the number of times is in and define , , and . Conditionally on , and we write

Lemma6.1 implies that are i.i.d. with expectation that using Proposition 1.69 of Serfozo (2009) is given by . Since a.s., we obtain that

since . Finally, it holds that a.s. ∎

We next establish that, when rescaled by their standard deviations, the terms , where and , are jointly asymptotically normal. To this end, let

Lemma 6.2.

Under the assumption of Theorem 2.6 (ii), .

Proof of Lemma 6.2.

By Cramér–Wold theorem (see Theorem 29.4 of Billingsley (2013)), it is enough to show that for , where and ,

| (22) |

Using Proposition A.3, we see that

is a mean zero martingale sequence. In particular,

is a mean zero martingale array. We will apply Theorem 3.2 of Hall and Heyde (1980) with , , , , and ; and obtain (22). To this end, we need to verify the following conditions: (i) , (ii) , (iii) , and (iv) . Using Proposition A.3 (iv) if either or and since are non-decreasing in , we obtain that

yielding Condition (i). Using again that if either or and , we obtain that

yielding Condition (iv). Turning to Condition (ii), assuming w.lo.g. that and using that

we obtain that for all

For , we use that and obtain that

It follows from Proposition A.3 (i) and Proposition 6.1 (i) that

| (23) |

where for , and since

yielding that

For , we use that if then and obtain that

Next, using Proposition A.3 (ii) and Proposition 6.1 (ii)-(iii), we have that

| (24) |

where . Since by Jensen’s inequality

using Markov inequality, we obtain that

which yields that

For (iii), we decompose

as

| (25) |

and show that each of the above terms converges to zero with probability one. Since , we use Proposition A.3 (iii) and obtain that are mean zero martingale sequences and for

We use (23) and (24), and apply Theorem 2.18 of Hall and Heyde (1980) with , , , , and , where , and obtain the convergence of the first term in (25). For the second term we proceed similarly. Specifically, using Proposition A.3 (iv) and Cauchy-Schwartz inequality we obtain that is a mean zero martingale sequence and for

Finally, we apply Theorem 2.18 of Hall and Heyde (1980) with , , , , and ; and obtain convergence of the second term in (25). ∎

We are now ready to prove the main result of the section.

Proof of Theorem 2.6.

Using Proposition A.3 (i)-(ii) and , we obtain that for are martingales and

We apply Theorem 2.18 of Hall and Heyde (1980) with , , where and , , , and for and for and obtain that a.s. From this, Theorem 2.5, and Proposition 6.1 (i), we obtain that a.s. Using (20) we conclude that a.s. Turning to the central limit theorem, Lemma 6.2 (iii) yields that

is asymptotically normal with mean zero and identity covariance matrix. Let be the diagonal matrix

By Proposition A.3 (i)-(ii) and Proposition 6.1, is asymptotically normal with mean zero and covariance matrix

Using the continuous mapping theorem, it follows that

∎

7 Discussion and concluding remarks

In this paper we developed BPRE with Thresholds to describe periods of growth and decrease in the population size arising in several applications including COVID dynamics. Even though the model is non-Markov, we identify Markov subsequences and use them to understand the length of time the process spends in the supercritical and subcritical regimes. Furthermore, using the regeneration technique we also study the rate of growth (or decline) of the process in the supercritical (subcritical) regime. It is possible to start the process using the subcritical BPRE and then move to the supercritical regime; this introduces only minor changes and the qualitative results remain the same. Finally, we note that without incorporating immigration in the supercritical regime the process will become extinct with probability one and hence the cyclical path behavior may not be observed.

An interesting question concerns the choice of strongly subcritical BPRE for the subcritical regime. It is folklore that the generation sizes of moderately and weakly subcritical processes can increase for long periods of time and in that case the time to cross the lower threshold will have a heavier tail. This could lead to lack of identifiability of supercritical and subcritical regimes. Similar issues arise when a subcritical BPRE is replaced by a critical BPRE or when immigration is allowed in both regimes. Since a subcritical BPRE with immigration converges in distribution to a proper limit law (Roitershtein; 2007), we may fail to observe a clear period of decrease. The path properties of these alternatives could be useful for modeling other dynamics observed (see Klebaner (1993); Iannelli and Pugliese (2014)). Mathematical issues arising from these alternatives would involve different techniques than used in this paper. We end this section with a brief discussion concerning the moment conditions in Theorem 2.6. It is possible to reduce the conditions to finite second moment hypothesis. This requires an extension of Lemma 4.1 to joint independence of blocks in , , offspring random variables, environments, immigration over cycles. The proof will need the Markov property of the pair and its uniform ergodicity. Also, the joint Markov property will also yield joint central limit theorem for the length and proportion of time spent in the supercritical and subcritical regimes. The proof is similar to that of Theorem 2.3 and Lemma 4.1 but is more cumbersome with an increased notational burden. The numerical experiments suggest that the estimators of the mean parameters of the supercritical and subcritical regime are not affected by the choice of various distributions. A thorough statistical analysis of the robustness of the estimators and analysis of the datasets are beyond the scope of this paper and will be investigated elsewhere.

References

- (1)

- Atanasov et al. (2021) Atanasov, D., Stoimenova, V. and Yanev, N. M. (2021). Branching process modelling of COVID-19 pandemic including immunity and vaccination, Stochastics and Quality Control 36: 157–164.

- Athreya and Karlin (1971) Athreya, K. B. and Karlin, S. (1971). On branching processes with random environments: I: Extinction probabilities, The Annals of Mathematical Statistics 42: 1499–1520.

- Athreya and Schuh (2016) Athreya, K. B. and Schuh, H.-J. (2016). A Galton-Watson process with a threshold, Journal of Applied Probability 53: 614–621.

- Billingsley (2013) Billingsley, P. (2013). Convergence of probability measures, John Wiley & Sons.

- Dion and Esty (1979) Dion, J. P. and Esty, W. W. (1979). Estimation problems in branching processes with random environments, The Annals of Statistics pp. 680–685.

- Falcó and Corral (2022) Falcó, C. and Corral, Á. (2022). Finite-time scaling for epidemic processes with power-law superspreading event, Physical Review E 105: Paper No. 064122, 8.

- Haccou et al. (2007) Haccou, P., Jagers, P. and Vatutin, V. A. (2007). Branching processes: variation, growth, and extinction of populations, Cambridge University Press.

- Hall and Heyde (1980) Hall, P. and Heyde, C. C. (1980). Martingale limit theory and its application, Academic press.

- Hanlon and Vidyashankar (2011) Hanlon, B. and Vidyashankar, A. N. (2011). Inference for quantitation parameters in polymerase chain reactions via branching processes with random effects, Journal of the American Statistical Association 106: 525–533.

- Hempel and Earn (2015) Hempel, K. and Earn, D. J. D. (2015). A century of transitions in new york city’s measles dynamics, Journal of the Royal Society Interface 12.

- Heyde (1971) Heyde, C. C. (1971). Some central limit analogues for supercritical Galton-Watson processes, Journal of Applied Probability 8: 52–59.

- Iannelli and Pugliese (2014) Iannelli, M. and Pugliese, A. (2014). An introduction to mathematical population dynamics, Springer.

- Ibragimov and Linnik (1971) Ibragimov, I. A. and Linnik, Y. V. (1971). Independent and stationary sequences of random variables, Wolters-Noordhoff Publishing, Groningen.

- Jagers (1975) Jagers, P. (1975). Branching processes with biological applications, Wiley.

- Jagers and Klebaner (2011) Jagers, P. and Klebaner, F. C. (2011). Population-size-dependent, age-structured branching processes linger around their carrying capacity, Journal of Applied Probability 48: 249–260.

- Jagers and Zuyev (2020) Jagers, P. and Zuyev, S. (2020). Populations in environments with a soft carrying capacity are eventually extinct, Journal of Mathematical Biology 81: 845–851.

- Jagers and Zuyev (2021) Jagers, P. and Zuyev, S. (2021). Amendment to: populations in environments with a soft carrying capacity are eventually extinct, Journal of Mathematical Biology 83.

- Kersting and Vatutin (2017) Kersting, G. and Vatutin, V. A. (2017). Discrete time branching processes in random environment, John Wiley & Sons.

- Kimmel and Axelrod (2015) Kimmel, M. and Axelrod, D. E. (2015). Branching processes in biology, Springer, New York.

- Klebaner (1984) Klebaner, F. C. (1984). On population-size-dependent branching processes, Advances in Applied Probability 16: 30–55.

- Klebaner (1993) Klebaner, F. C. (1993). Population-dependent branching processes with a threshold, Stochastic processes and their applications 46: 115–127.

- Lamperti (1960) Lamperti, J. (1960). Criteria for the recurrence or transience of stochastic process. I, Journal of Mathematical Analysis and applications 1: 314–330.

- Lamperti (1963) Lamperti, J. (1963). Criteria for stochastic processes II: passage-time moments, Journal of Mathematical Analysis and Applications 7: 127–145.

- Perko (2013) Perko, L. (2013). Differential equations and dynamical systems, Springer.

- Roitershtein (2007) Roitershtein, A. (2007). A note on multitype branching processes with immigration in a random environment, The Annals of Probability 4: 1573–1592.

- Serfozo (2009) Serfozo, R. (2009). Basics of applied stochastic processes, Springer.

- Sun et al. (2022) Sun, H., Kryven, I. and Bianconi, G. (2022). Critical time-dependent branching process modelling epidemic spreading with containment measures, Journal of Physics A: Mathematical and Theoretical 55.

- Teschl (2012) Teschl, G. (2012). Ordinary differential equations and dynamical systems, American Mathematical Society.

- Tyson et al. (2010) Tyson, R., Haines, S. and Hodges, K. E. (2010). Modelling the canada lynx and snowshoe hare population cycle: the role of specialist predators, Theoretical Ecology 3: 97–111.

- Yanev et al. (2020) Yanev, N. M., Stoimenova, V. K. and Atanasov, D. V. (2020). Stochastic modeling and estimation of COVID-19 population dynamics, arXiv preprint arXiv:2004.00941 .

Appendix A Auxiliary results

This section contains detailed descriptions and proofs of auxiliary results used in the paper. We begin with a detailed description of probability space for BPRET.

A.1 Probability space

In this subsection we describe in detail the random variables used to define BPRET as well as the underlying probability space. The thresholds are i.i.d. random vectors with support , where , , and are fixed integers, defined on the probability space . Next, and are subcritical and supercritical environmental sequences that are defined on probability spaces and . Specifically, and , where , , and are probability distributions in . Let and denote probability spaces corresponding to supercritical BPRE with immigration and subcritical BPRE. Hence, the environment sequence , the offspring sequence , and the immigration sequence are random variables on . Similarly, and , , are random variables on . We point out here that the probability spaces and are linked; that is, for all integrable functions

Similar comments also holds with replaced by in the above. All the above described random variables are defined on the probability space .

A.2 Time homogeneity of and

Lemma A.1.

Proof of Lemma A.1.

We only prove (i) and (iii). Since is equal to

it is enough to show that for all and

| (26) | ||||

To this end, we condition on and , where . Since, given and , both the sequences , and the random variables , are i.i.d., we obtain from (1) that

By taking expectation w.r.t. and using that are i.i.d., we obtain (26). Next, we notice that

is positive because . It follows from part (i) that . Finally, (iii) follows from (i) and (ii) using (3) and (4). ∎

A.3 Finiteness of

We show that the stationary distribution of the Markov chain has a finite first moment .

Proof of Proposition A.1.

Using that is the stationary distribution of the Markov chain , we write for all . Next, we notice that

Now, using that the event is same as , the RHS of the above inequality is bounded above by

Since BPRE is a time-homogeneous Markov chain, it follows that

where we also use the fact that the process starts in the supercritical regime. Now, using and are i.i.d., it follows that

Since

using Fubini-Tonelli theorem, we obtain that

Now, for all , we have that

Finally, using the Assumptions (H2), (H3), and (H9), we conclude that

∎

A.4 Proofs of Lemma 4.1 and Lemma 4.2

Proof of Lemma 4.1.

We begin by proving (i). It is sufficient to show that for and

| (27) |

where , , and . For simplicity set . We recall that and notice

We now compute the last term of the above equation. Specifically, by proceeding as in the proof of Lemma A.1 (involving conditioning on the environments), we obtain that for , , and

Now, by summing over and , we obtain that

The last term in the above is

We thus obtain (27). The proof of (ii) is similar. ∎

Proof of Lemma 4.2.

The first part of (i) follows from Proposition 1.69 of Serfozo (2009) with , , and . For the second part of (i) we use the above proposition with and obtain that

Remark (3.2) yields that

We now prove the fist part of (ii). Since, conditionally on , and have the same distribution, using (i) we have that

Next, we apply Proposition 1.69 of Serfozo (2009) with , and and obtain that

Then, we compute

where is given by

Using Theorem 1.54 of Serfozo (2009), we obtain , which yields

Now, using Lemma 4.1, we see that, conditionally on , is independent of . If , then using stationarity (see Remark 3.1)

Therefore,

Adding the above to we conclude that

The second part of (ii) and (iii) are obtained similarly. ∎

A.5 Finiteness of , and

We establish positivity and finiteness of and where . Lemma A.2 below is used to control the covariance terms in and . We recall that uniform ergodicity of the Markov chains and is equivalent to the existence of constants and such that .

Lemma A.2.

The proof of the above lemma can be constructed along the lines of Theorem 17.2.3 of Ibragimov and Linnik (1971) with and it involves a repeated use of Cauchy-Schwarz inequality and stationarity in Remark 3.1.

Proof of Lemma A.2.

Since the proof of (ii) is similar we only prove (i). We proceed along the lines of the proof of Theorem 17.2.3 of Ibragimov and Linnik (1971). Using Cauchy-Schwarz inequality, we have that

Using Cauchy-Schwarz inequality again, we obtain that

Since by Remark 3.1, we deduce that

Using that , we obtain that

We have thus shown that

which yields that

∎

We are now ready to study the finiteness of means and variances , , and , where .

Proposition A.2.

It is easy to see that Proposition A.2 implies that and are finite.

Proof of Proposition A.2.

We begin by proving (i). For all it holds that

where is a supercritical BPRE with immigration having environmental sequence and, conditionally on , offspring distributions and immigration distribution . Using a.s. and , we see that a.s. Since , we obtain a.s., which yields . Therefore, there exists such that

| (28) |

Now, using is finite and it follows that

Turning to the finiteness of , replacing by in (28), one obtains that

This together with the finiteness of yields . Turning to the covariance terms in , we apply Lemma A.2 (i) with and using , we obtain that

We conclude that is finite. For , it holds that

where the inequality follows from the upper bound on the extinction time of the process in the subcritical regime. Hence, using Proposition A.1 it follows that .

Next, we show that is finite. As before, we obtain that for all

| (29) |

yielding that

| (30) |

This and the finiteness of implies that . Turning to covariances we apply Lemma A.2 (ii) with and using , we obtain that

yielding the finiteness of . Turning to (iii), we compute

where using Part (i) and using Remark 3.2

Turning to the covariance, we again apply Lemma A.2 (i) with and conclude that also

and the finiteness of the RHS yields . The proof of is similar.

We finally establish that , , , and are positive. We first show that, conditionally on and , and are non-degenerate. To this end, suppose by contradiction that

Since has support , we obtain that for all . In particular,

By taking both and in the above equation we obtain that both and . Similarly, if

then using that has support , we obtain that

In particular,

By taking both and we obtain that , which contradicts (H4). We deduce that is non-degenerate and, similarly,

are non-degenerate. Using Lemma 4.2 below, we conclude that

and similarly , , and . ∎

A.6 Martingale structure of

We recall that , where

Also, and for and .

Proposition A.3.

The following holds:

(i) For is a mean zero martingale sequence and for all a.s. In particular,

(ii) is a mean zero martingale sequence satisfying

Additionally, for all a.s.

(iii) For are mean zero martingale sequences and for all

(iv) For all and such that either or it holds that for all and . In particular, is a mean zero martingale sequence and for all

Proof of Proposition A.3.

We begin by proving (i) with . We notice that is a martingale since is -measurable and

It follows that . Next, notice that for

In particular, if then a.s. and the martingale property yields that

Finally, we notice that, since do not depend on the offspring distributions , part (i) holds with replaced by . We now turn to the proof of (ii). We notice that is -measurable and using that we obtain that

yielding the martingale property. It follows that as

We now compute

Using that, conditionally on the environment , are i.i.d. with variance , we obtain that

We conclude that

and

Additionally, Jensen’s inequality yields that for

For (iii) we notice that is -measurable and since , , , and are not -measurable we have that and

Again using the convexity of the function for , we get that

If , then by conditioning on we have that . If , then we apply Jensen’s inequality and obtain that

Turning to (iv), we show that for all and such that either or it holds that for all . This also yields that

First, if and , then because . Next, if and (say or ), then by conditioning on and and using that

and , , , and are -measurable, we obtain that

Finally, if (say ), then by conditioning on and using that is -measurable and , we obtain that

is a mean zero martingale sequence since is -measurable and if either or . If then both and . Finally, if and (say and ) then by Jensen’s inequality

which yields that

and

∎

Appendix B Numerical experiments

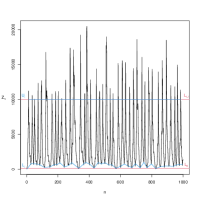

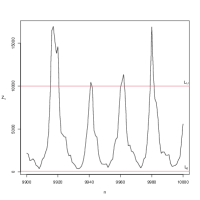

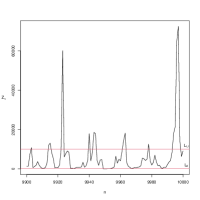

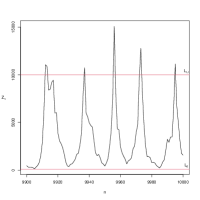

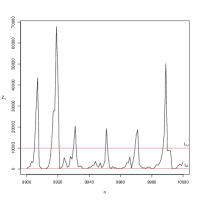

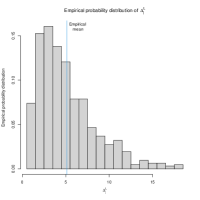

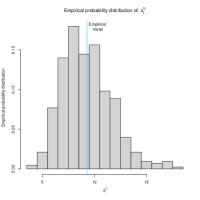

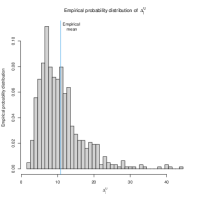

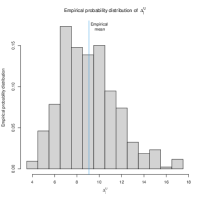

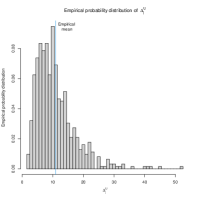

In this section we describe numerical experiments to illustrate the evolution of the process under different distributional assumptions. We also study the empirical distribution of the lengths of supercritical and subcritical regimes and illustrate how the process changes when and exhibit an increasing trend. We emphasize that these experiments illustrate the behavior of the estimates of the parameters of the BPRET when using a finite number of generations in a single synthetic dataset. In the numerical Experiments 1-4 below, we set , , , , , and different distributions for , , , and as follows:

| Exp. 1 |

,

|

,

|

,

|

|

| Exp. 2 |

,

|

,

|

,

|

|

| Exp. 3 |

,

, |

,

, |

,

, |

|

| Exp. 4 |

,

, |

,

, |

,

, |

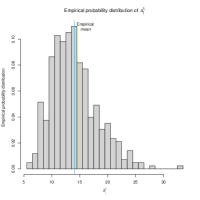

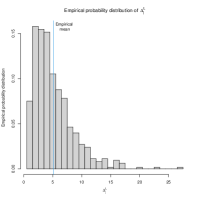

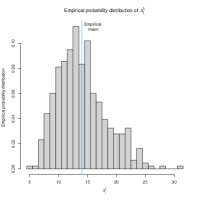

In the above description, we have used the notation for the uniform distribution over the interval and for the uniform distribution over integers between and . is the zeta distribution with exponent . is the Poisson distribution with parameter while is the Poisson distribution truncated to values not larger than . Similarly, is the negative binomial distribution with predefined number of successful trials and mean while is the negative binomial distribution truncated to values not larger than . Finally, is the Gamma distribution with shape parameter and rate parameter . In these experiments, there were between to crossing of the thresholds depending on the distributional assumptions. The results of the numerical Experiments 1-4 are shown in Figure 2.

We next turn our attention to construction of confidence intervals for the means in the supercritical and subcritical regimes. Values of , , and in Exp. 1-4 can be deduced from the underlying distributions and are summarized below. The values of and in Exp. 3-4 are rounded to 3 decimal digits.

| Exp. 1 | ||||||

| Exp. 2 | ||||||

| Exp. 3 | ||||||

| Exp. 4 |

In the next table, we provide the estimators , , , and of , , , and , respectively. Notice that

are used to estimate and . Similar to the proof of Theorem 2.6 it is easy to see that and are consistent estimators of and . Similar comments hold when is replaced by .

| Exp. 1 | ||||||

| Exp. 2 | ||||||

| Exp. 3 | ||||||

| Exp. 4 | ||||||

| Exp. 1 | ||||||

| Exp. 2 | ||||||

| Exp. 3 | ||||||

| Exp. 4 |

Using the above estimators in Theorem 2.6 we obtain the following confidence intervals for and . We also provide confidence intervals for the estimator defined below, which does not take into account different regimes. Specifically,

where is equal to if and otherwise.

| CI using | CI using | CI using | |

|---|---|---|---|

| Exp. 1 | |||

| Exp. 2 | |||

| Exp. 3 | |||

| Exp. 4 |

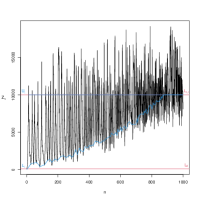

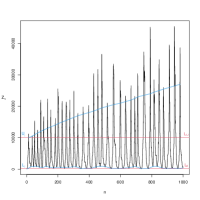

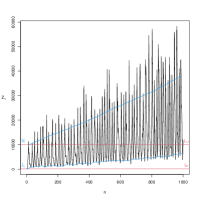

Next, we investigate the behavior of the process when the thresholds and increase with . To this end, we let , , and and take initial distribution , immigration distribution , and offspring distributions and as in the numerical Experiment 1. We consider four different distributions for and as follows:

| Exp. 5 | ||

| Exp. 6 |

, where

, |

|

| Exp. 7 | ||

| Exp. 8 |

, where

, |

The results of the numerical Experiment 5-8 are shown in Figure 3. From the plots, we see that the number of cases after crossing the upper thresholds are between and , whereas when the thresholds increase they almost reach the mark. Also, the number of regimes up to time reduces as it takes more time to reach a larger threshold. As a consequence the overall number of cases also increases.