First Price Auction is Efficient

Abstract

We prove that the PoA of First Price Auctions is , closing the gap between the best known bounds .

1 Introduction

In 1961, Vickrey [Vic61], a Nobel laureate in Economics, initiated auction theory. At the center of his work was the solution concept of Nash equilibrium [Nas50] for auctions as non-cooperative games. This game-theoretical approach has shaped modern auction theory and has a tremendous influence also on other areas in mathematical economics [HR04]. In particular, Vickrey systematically investigated the first-price auction (or its equivalent, the Dutch auction), the most common auction format in real business.

In the first-price auction, the auctioneer (seller) sells an indivisible item to potential bidders (buyers). The rule is as simple as it can be: All bidders simultaneously submit bids to the auctioneer (each of which is unknown to the other bidders); the highest bidder wins the item, paying his/her own bid. Simple as the rule is, the bidders’ optimal bidding strategies can be sophisticated. From one bidder’s own perspective, a higher bid means a higher payment on winning but also a better chance of winning. Accordingly, this bidder’s optimal bidding strategy depends on the competitive environment, which in turn is determined by the other bidders’ bidding strategies. This situation is perfectly a non-cooperative game and the standard solution concept is Bayesian Nash equilibrium. To get a better sense, let us show a warm-up example from Vickrey’s original work.

Example 1 ([Vic61]).

Consider two bidders: Alice and Bob have (independent) uniform random values and respectively bid and . The value distributions and bidding strategies determine the (independent) bid distributions of bidders. In this example, they are (independent) uniform random bids , whose CDFs are . By bidding , Alice wins with probability and gains a utility conditioned on winning. Her expected utility is , which is maximized when . Thus, her current strategy is optimal. By symmetry, Bob’s current strategy is also optimal. In sum, the above strategy profile is an equilibrium, in a sense that no bidder can gain a better utility by deviating from his/her current strategy.

For clarity, let us formalize the model. Each bidder independently draws his/her value from a distribution . Only with this knowledge and depending on his/her own strategy , bidder submits a possibly random bid . Then over the randomness of the other bidders’ values and strategies , bidder wins with probability and gains an expected utility .

Definition 1.1 (Equilibria).

A strategy profile is a Bayesian Nash Equilibrium when: For each bidder and any possible value , the current strategy is optimal, namely for any deviation bid .

Example 1 is special in that bidders have identically distributed values. This symmetric setting is well understood: The first-price auction has a unique Bayesian Nash equilibrium [CH13], which is fully efficient – The bidder with the highest value always wins the item. Instead, the current trend focuses more on the asymmetric setting, where bidders’ values are distinguished by their distributions. Again, let us get a better sense through two concrete examples.

Example 2.

Consider two bidders: Alice has a fixed value and always bids . Bob has a uniform random value and truthfully bids his value , namely the distribution . By bidding , Alice gains an expected utility , for which her current strategy is optimal. Bob cannot gain a positive utility because his value is at most Alice’s bid ; thus his current strategy is also optimal. In sum, this strategy profile is an equilibrium.

Unlike the symmetric setting, this auction game has multiple equilibria. E.g., it is easy to verify that the same strategy for Alice and a different strategy for Bob (namely the distribution for ) are another equilibrium.

Both equilibria and given in Example 2 have two features: (i) The strategies , and are pure strategies – Each of them has no randomness, just the function of a value. (ii) Both equilibria are fully efficient akin to the symmetric setting – Alice always has the highest value and always wins the item. However, these are not always the case in the asymmetric setting, such as in the following example, which only slightly modifies Example 2 by changing the fixed value of Alice from to .

Example 3.

Consider two bidders: Alice has a fixed value and bids following the distribution for . Bob has a uniform random value and bids , namely the distribution for . By bidding , Alice gains an expected utility , which is maximized anywhere between , so her current strategy is optimal. Using elementary algebra, we can check that Bob’s current strategy also is optimal. In sum, this strategy profile is an equilibrium.

In Example 3: Alice has a mixed strategy – A fixed value but a random bid . Furthermore, the equilibrium is not fully efficient. E.g., with a value , although not the highest value , Bob bids and wins with probability . Indeed, Example 3 has infinite equilibria, among which the given one has the relatively “simplest” format. But none of those equilibria is a pure equilibrium or is fully efficient, despite that Example 3 is only a minor modification of Example 2.

From the above examples, we observe that Bayesian Nash equilibria can be very complicated and sensitive to the value distributions, despite the intrinsic simple rule of the first-price auction. After an extensive study for more than 60 years, the first-price auction and its equilibria remain the centerpiece of modern auction theory and have promoted a rich literature; see [SZ90, Leb06, Leb96, Leb99, MR00a, MR00b, JSSZ02, MR03, HKMN11, CH13, ST13, Syr14, HHT14, FLN16, HTW18, WSZ20, FGH+21] etc. These efforts are justifiable since the study of the first-price auction and its equilibria is both theoretically challenging and practically important.

Among various aspects of the first-price auction, efficiency at equilibria is of primary interest. In economics, efficiency measures to what extent a resource can be allocated to the persons who value it the most, thus maximizing the social welfare, particularly in a competitive environment. As shown above (Example 3), the first-price auction generally is not fully efficient at an equilibrium: The winner has the highest bid but possibly not the highest value; this crucially depends on both (i) the instance itself and (ii) which Bayesian Nash equilibrium it falls into. Earlier works in economics focus on (generalizing) the conditions for the value distribution that guarantee the full efficiency.

However, the quality of (in)efficiency should not be all-or-nothing. E.g., when the highest value is , a value- bidder versus a value- bidder is very different, although neither of them is fully efficient. Towards a quantitative analysis, Koutsoupias and Papadimitriou introduced a new measure on the efficiency degradation under selfish behaviors, the Price of Anarchy [KP99] (which is an analog of the “approximation ratio” in theoretical computer science). For the first-price auction, denote by the expected optimal social welfare from an instance , and by the expected social welfare at an equilibrium , then the Price of Anarchy is defined to be the minimum possible ratio, as follows.

Definition 1.2 (Price of Anarchy).

Regarding First Price Auctions, the Price of Anarchy is given by

The Price of Anarchy is bounded between . Namely, a larger ratio means a higher efficiency and the ratio means the full efficiency. For the first-price auction, Syrgkanis and Tardos first proved that the PoA is at least [ST13]. Later, Hoy, Taggart and Wang derived an improved lower bound of [HTW18]. On the other hand, Hartline, Hoy and Taggart gave a concrete instance of ratio [HHT14], which remains the best known upper bound.

Despite the prevalence of the first-price auction and much effort in studying its efficiency, there has been a persistent gap in the state of the art. In the current paper, we will completely solve this long-standing open problem.

Theorem 1 (Tight PoA).

The Price of Anarchy in First Price Auctions is .

Remarkably, neither the best known lower bound nor the upper bound is tight; we close the gap by improving both of them. Our tight bound not only is a mathematically elegant result but has further implications in real business since it is fairly close to . Namely, at any equilibrium, the efficiency degradation in the first-price auction is small, no worse than 13.53%, which might be acceptable given other merits of the first-price auction.

En route to the tight PoA, we obtain many new important perspectives, characterizations, and properties of equilibria in the first-price auction. These might be of independent interest and find applications in the future study of other aspects of the first-price auction, e.g., the complexity of computing equilibria. Beyond the first-price auction, our overall approach is general enough and might help determine the Price of Anarchy in other auctions.

1.1 Technical overview

This subsection sketches our high-level proof ideas. To ease the readability, some descriptions are roughly accurate but not perfectly, and most technical details are deferred to Sections 2, 3, 4, 5 and 6. Our approach is very different from the prior works [ST13, HTW18], which mainly adopt the smoothness techniques or an extension. More concretely, we employ a first principle approach that directly characterizes the worst-case instance and the worst-case Bayesian Nash equilibrium regarding the definition of the Price of Anarchy. To this end, we step by step narrow down the search space of the worst case by proving more and more necessary conditions it must satisfy. Finally, we capture the exact worst case and thus derive the tight PoA bound.

Changing the viewpoints (Section 2)

Regarding the PoA definition, we need to prove that the auction social welfare is within a certain ratio of the optimal social welfare , given any value distribution and any equilibrium thereof .

Two difficulties emerge immediately: (i) One value distribution generally has multiple or even infinite equilibria. (ii) One equilibrium generally has no analytic solution; even an efficient algorithm for computing (approximate) equilibria from value distributions is unknown.

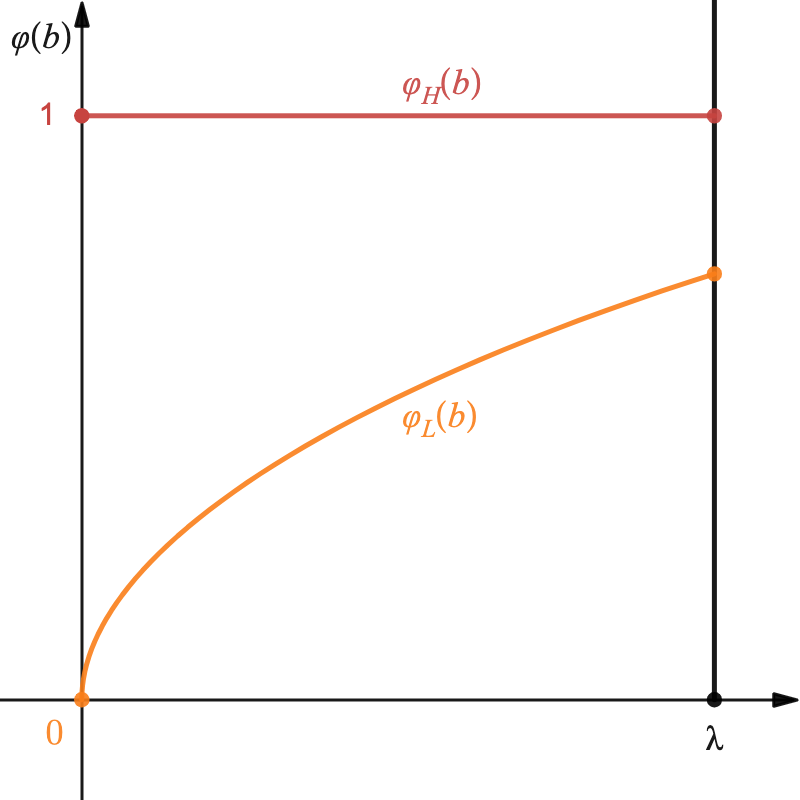

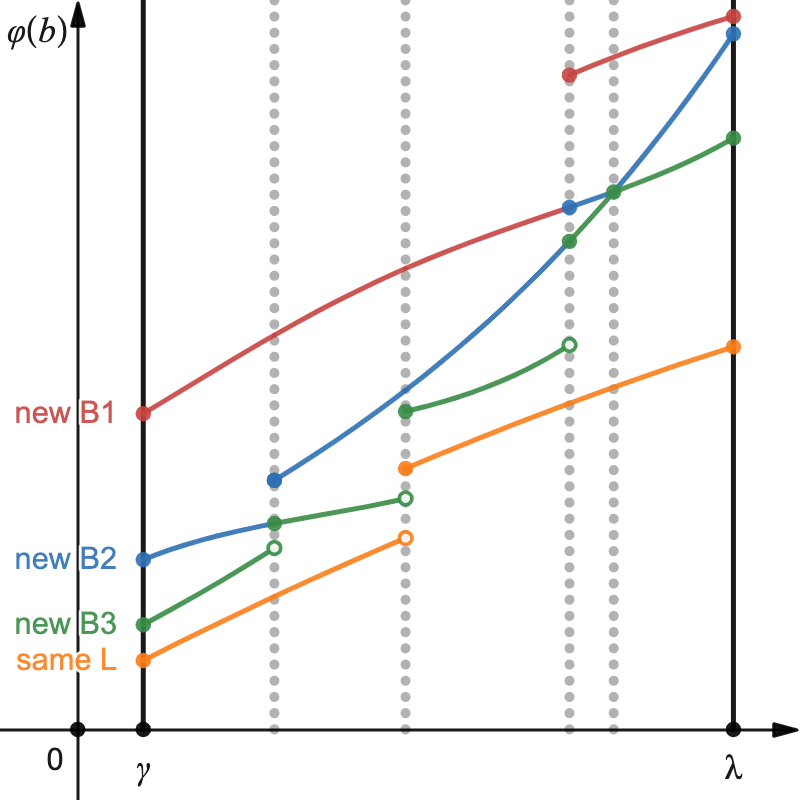

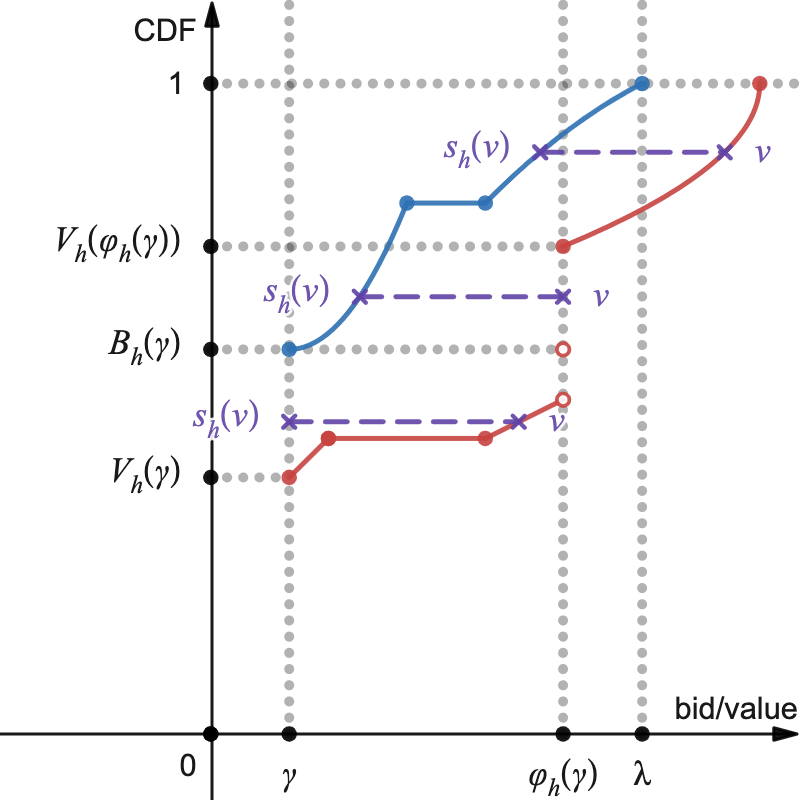

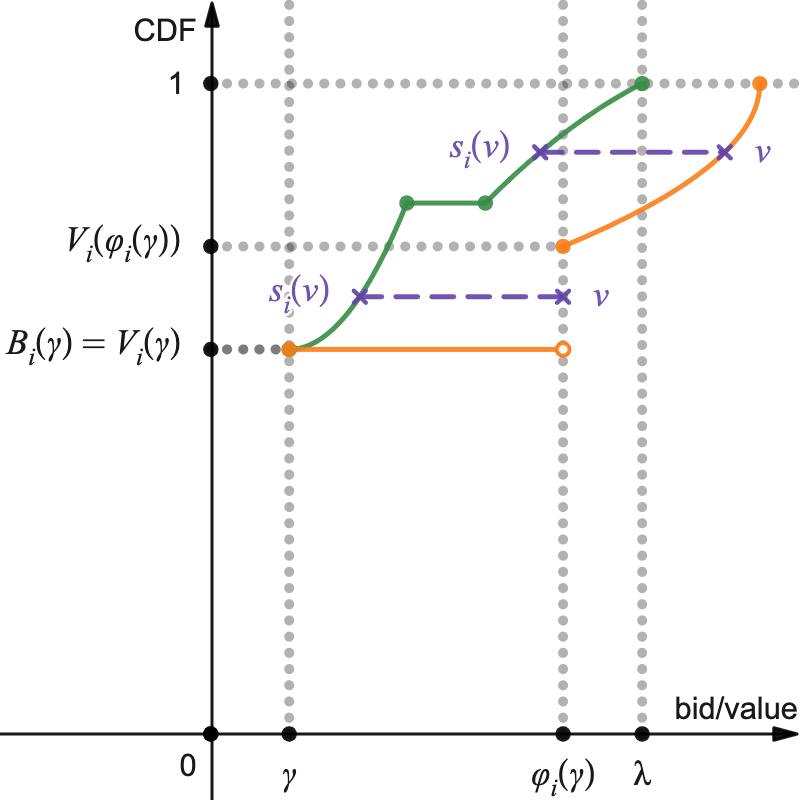

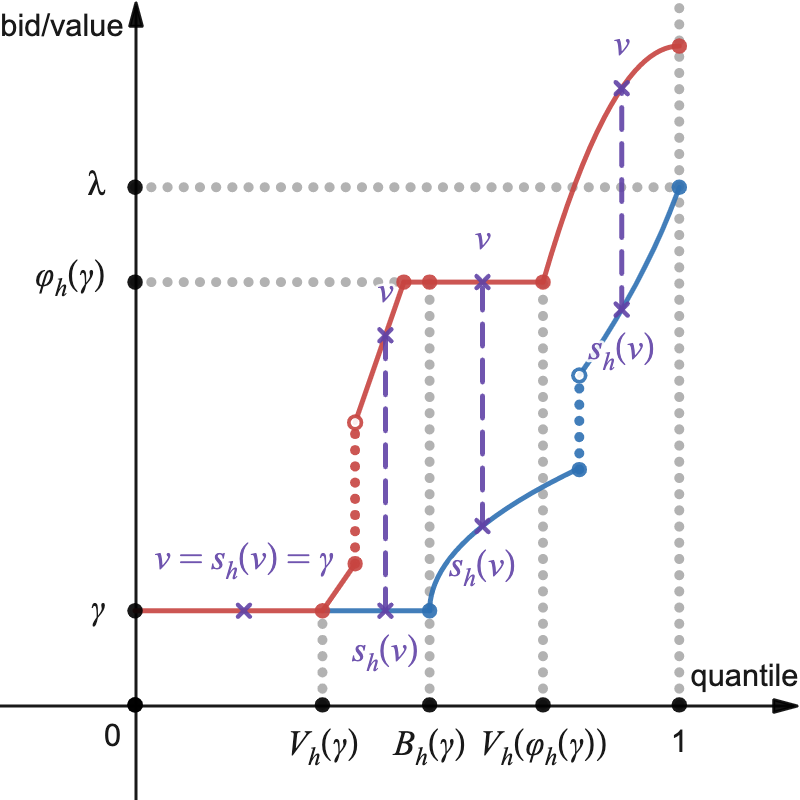

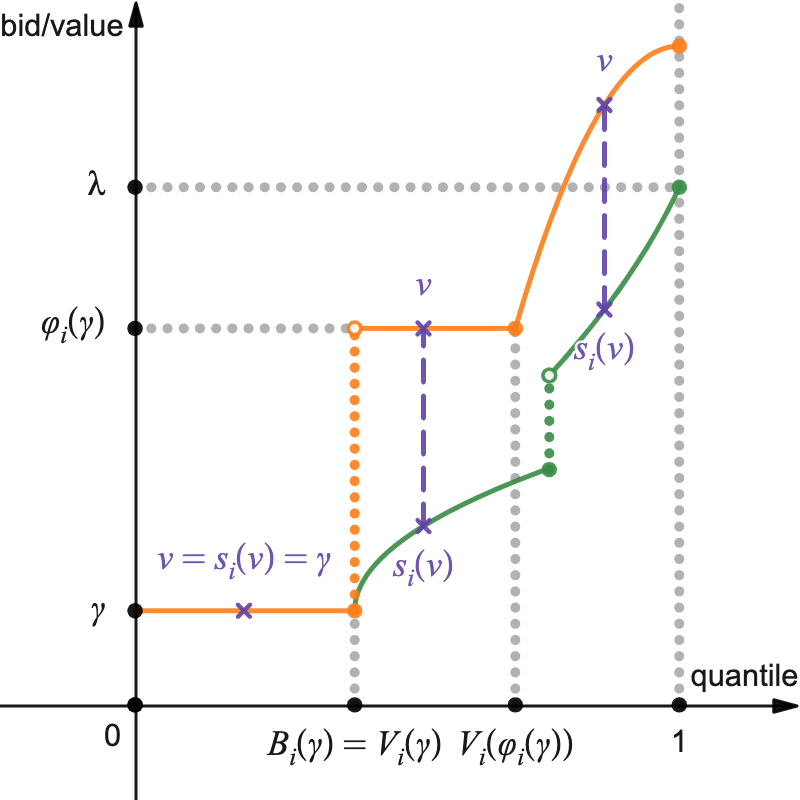

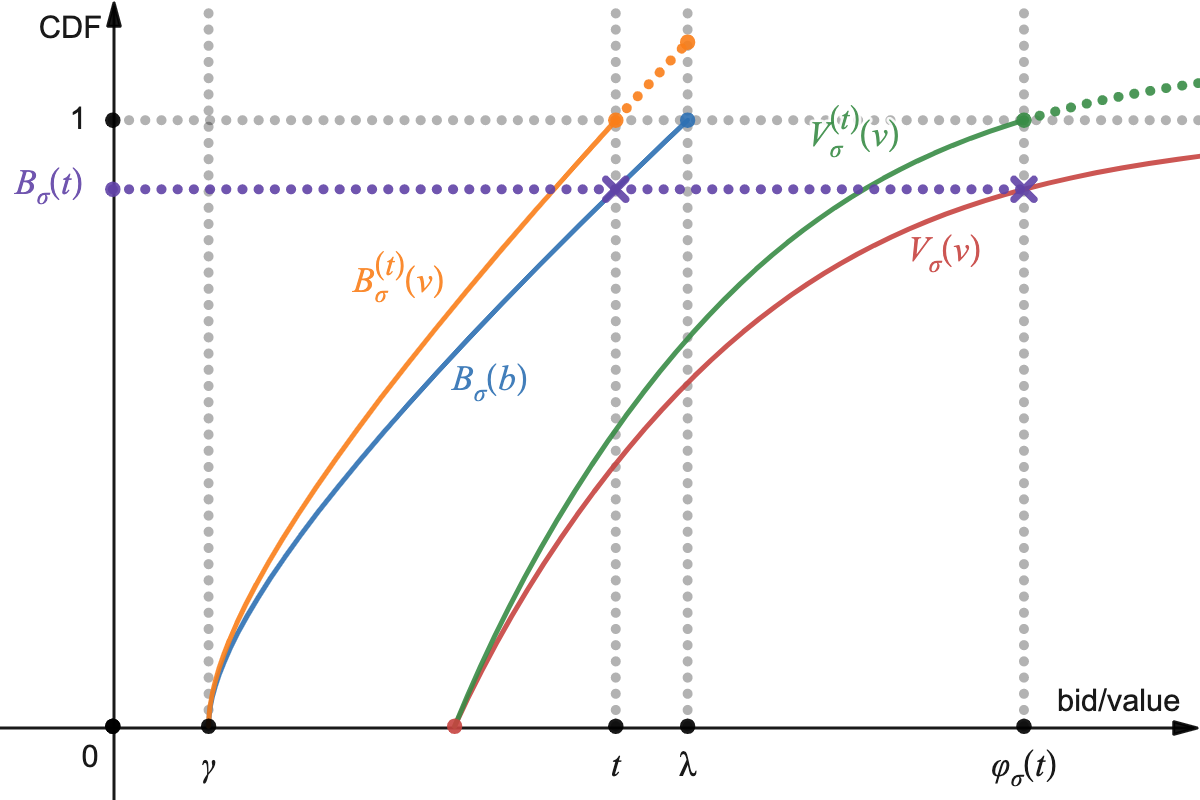

To the rescue, instead of the original value-strategy representation of equilibria, we use another representation, the bid distributions resulted from equilibria. These two representations and their relationship are demonstrated in Figure 1. Given one equilibrium bid distribution : (i) One equilibrium is uniquely determined. (ii) The reconstruction of the essentially has an analytic solution, through the bid-to-value mappings that are almost the inverse functions of the strategies .111Although the mapping formulas are previously known, NO prior work takes ANY further step. Even this structure result is unknown: “One (valid) bid distribution backward uniquely determines the underlying value-strategy tuple ”; let alone techniques towards the tight . These mitigate the above two difficulties.

In sum, there is a bijection between the space of equilibria and the space of equilibrium bid distributions . Further, the new representation is mathematically equivalent but technically easier – this is one infinite set instead of the Cartesian product of two infinite sets – showing an avenue towards the tight PoA. (Later in Sections 2, 3, 4, 5 and 6, we will see more advantages.)

Nonetheless, there is no free lunch. The new representation has two drawbacks. (i) Unlike that any value distribution must be feasible since the existence of an equilibrium is promised [Leb96],222This existence result requires suitable tie-breaking rules in the first-price auction; see Section 2 for more details. a generic bid distribution not necessarily induces an equilibrium. To remedy this issue, we introduce the notion of validity, which almost refers to monotonicity of the bid-to-value mappings . In addition, (ii) a mapping is undefined at a singular point where the equilibrium bid distribution of that bidder has a probability mass, which must be handled separately. Luckily, such probability masses are possible only at the left endpoint of the distribution’s support. So, we further consider the conditional value distribution given one’s bid being at the left endpoint. Indeed, the concept of validity refers to a tuple of equilibrium bid distributions and a conditional value distribution.

More rigorously, our new representation considers all the valid tuples/instances . Here, the valid distributions can be replaced with the increasing bid-to-value mappings : One determines the other and vice versa (Lemma 3.4). More importantly, monotonicity of the mappings gives a strong geometric intuition, making the third representation of equilibrium more convenient for our later use. In particular, in what follows, the figures of the mappings play the role of visual demonstrations, i.e., horizontal bid axes and vertical value axes, where each mapping denotes one bidder .

The worst-case instance (Section 6)

Our overall approach is to reduce any given instance to the worst-case instance step by step. Thus, it is helpful to describe the worst case in advance, which explains why we design those reductions since our target is very specific.

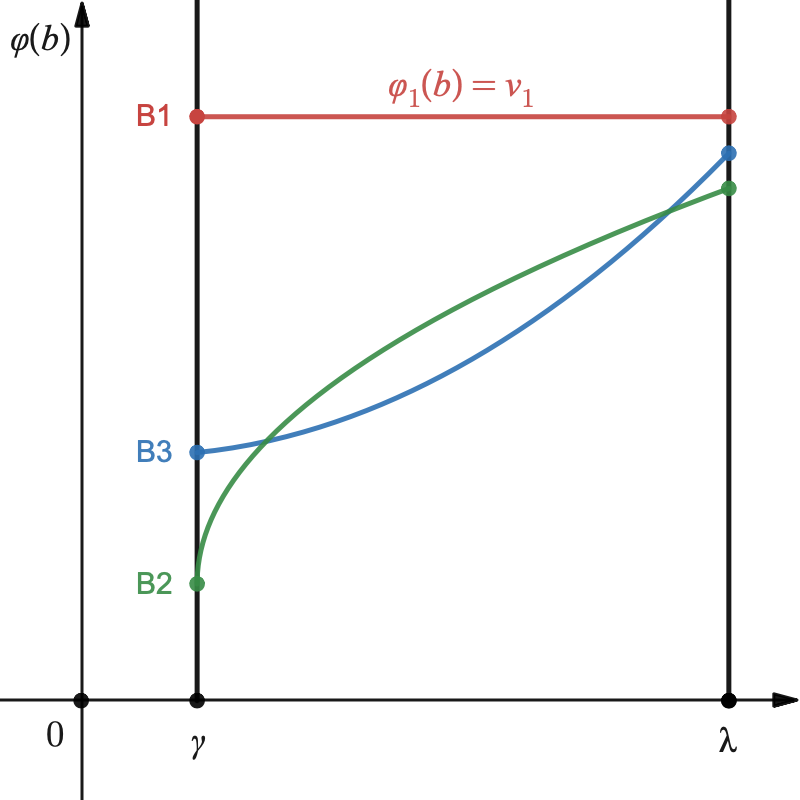

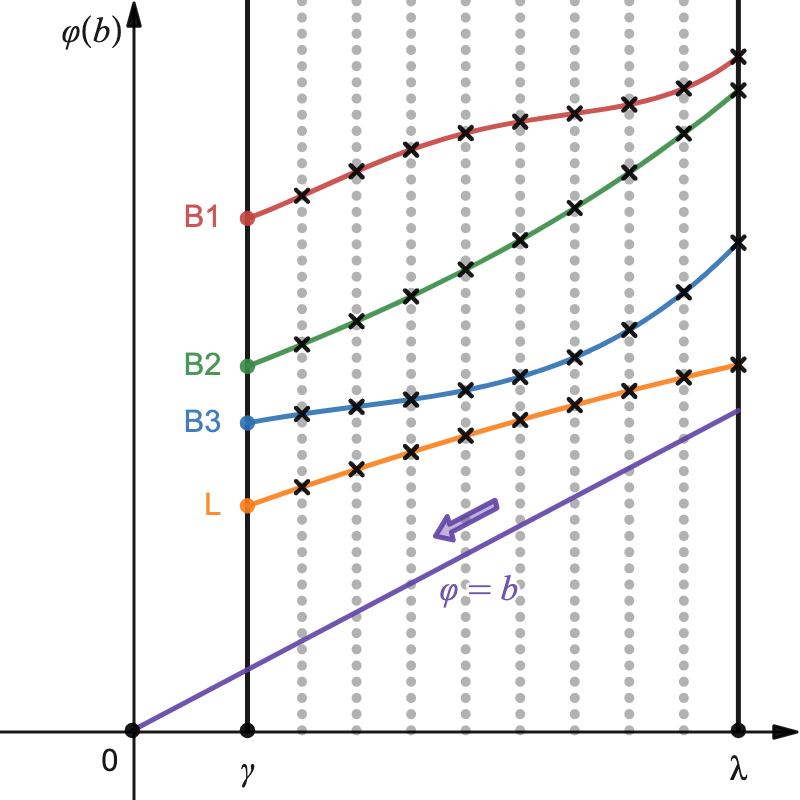

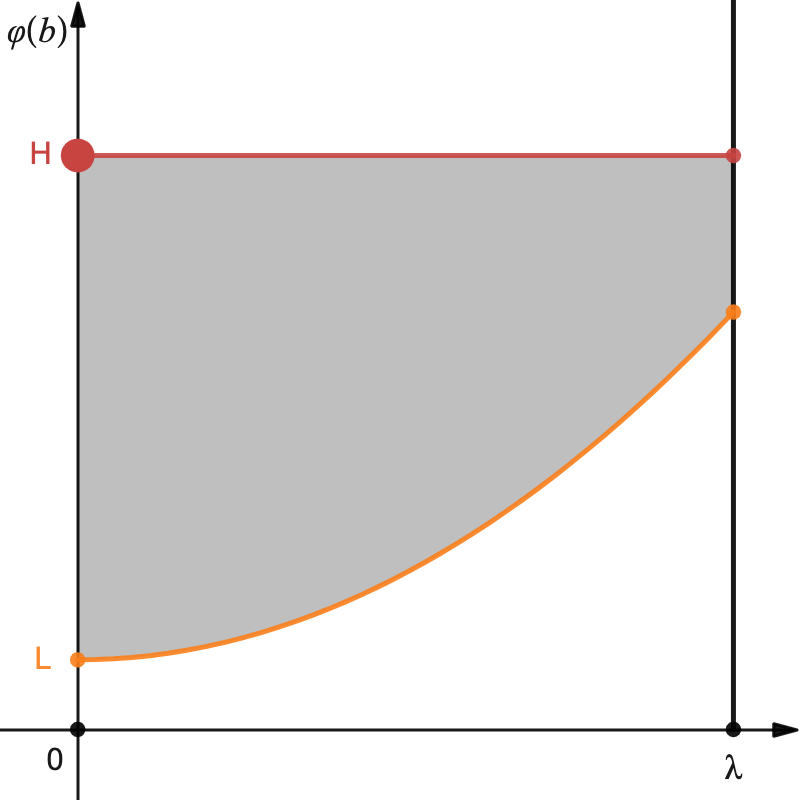

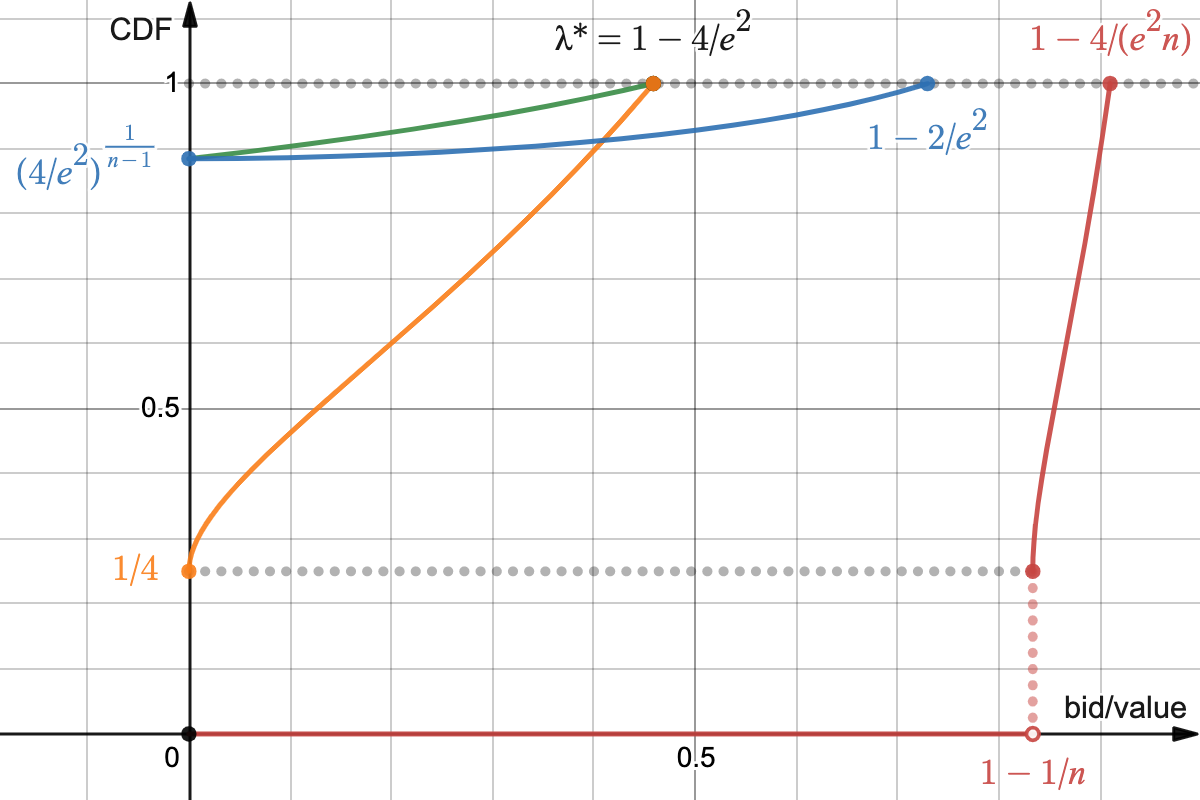

The worst case has bidders, one bidder with a fixed high value and sufficiently many identical low-value bidders . Among the low-value bidders, the highest value is distributed following the parametric equation for , over the value support . See Figure 2 for a visual aid, based on the bid-to-value mappings .

The equilibrium strategies and the bid distributions are less important for understanding our approach;333[HHT14] “just” considered a reasonable instance and for , but neither gave argument/evidence for “worstness” of the instance family , nor searched the worst case . In contrast, our contributions are twofold: (primary) “worstness” of this family; (secondary) the nontrivial worst case and for . In this family, the PoA is less sensitive to different instances, hence two numerically close bounds versus . we will show in Section 6 how to deduce them and the tight PoA . The parametric equation also is less important, being included just for completeness.

In contrast, the point is the underlying structure: The bidder always contributes the optimal social welfare . The low-value bidders individually have negligible effects (the winning probabilities etc) but collectively make the auction game less efficient.

We are inspired by the instance due to Hartline, Hoy and Taggart [HHT14], which has the same structure. Our construction differs from theirs in the concrete distributions, hence a slightly worse PoA of in comparison with their ratio of (Footnote 3).

The pseudo instances (Section 3.1) and LABEL:alg:collapse (Section 4.3)

Rigorously, the worst case for described above is not a specific instance, but a sequence of instances with the limit being the worst case. This incurs some notational inconvenience. When such issues occur in real/complex analysis, the standard method is to add the infinite point(s) to the space of the real/complex numbers, making the space more complete. In the same spirit, we introduce the notion of pseudo bidders and pseudo instances (Definition 3.1), thus including the above limit to our search space.

In our extended language, the worst case has a succinct format: one high-value bidder and one pseudo bidder , namely a two-bidder pseudo instance (Figure 2). Beyond notational brevity, the notion of pseudo bidders/instances also simplifies our proof in several places.

This extension does not hurt our proof, given that pseudo instances are only considered in the lower-bound analysis. Precisely, we show that even the worst case in the extended search space has the PoA , implying a lower bound of for the original problem. In addition, the upper-bound analysis leverages the above instance sequence . Precisely, we show that when the is sufficiently large, the PoA can be arbitrarily close to . As a combination, the tight PoA in Theorem 1 gets established.

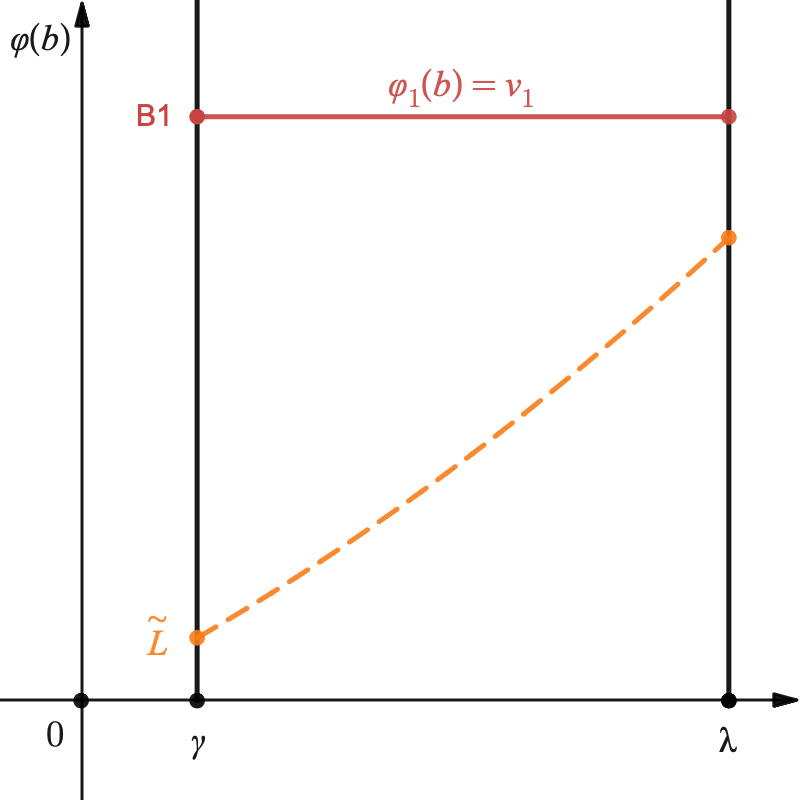

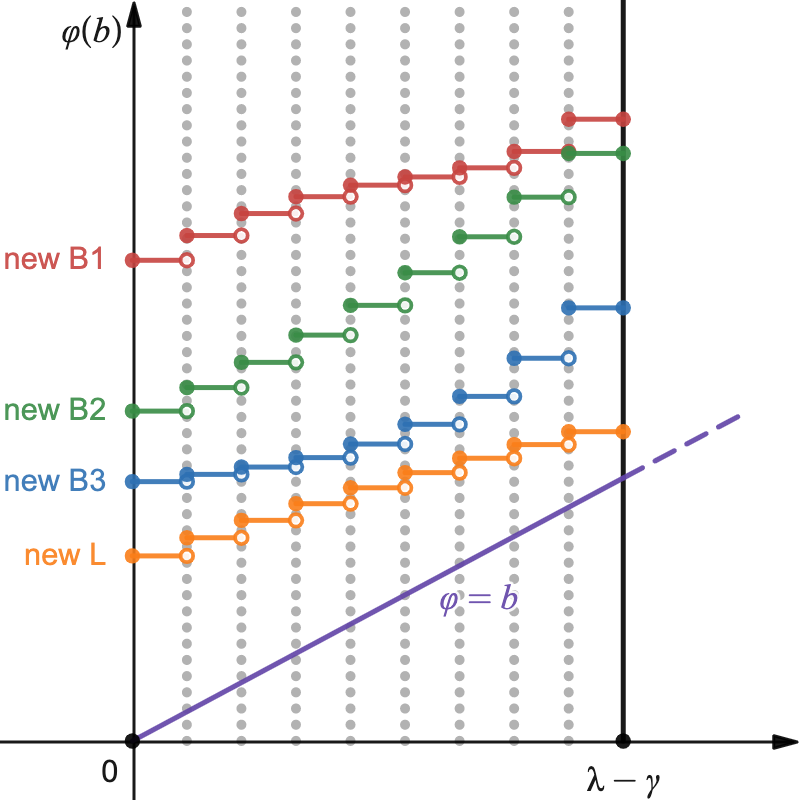

Another related thing is the LABEL:alg:collapse reduction. As Figures 3a and 3b show, when a specific bidder has a fixed high value over the bid support , the LABEL:alg:collapse reduction can replace all the other bidders by one pseudo bidder , resulting in a two-bidder pseudo instance that has a worse-or-equal PoA. (I.e, whether before or after the LABEL:alg:collapse reduction, the optimal social welfare is the bidder ’s fixed high value . Moreover, it turns out that the auction social welfare can only decrease.) Such a two-bidder pseudo instance will be easy to handle since it has the same shape as the worst case .

In sum, the remaining task is to transform every valid instance into a specific instance that the Collapse reduction can work on, i.e., an instance that has one fixed-high-value bidder.

LABEL:alg:layer (Section 3.4): Hierarchizing the bidders

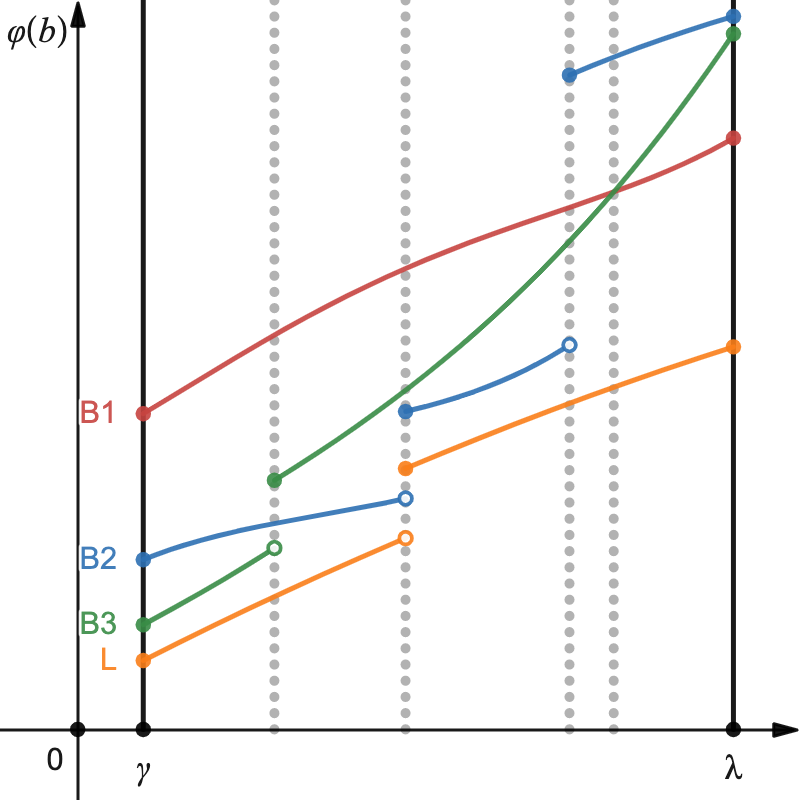

To transform a given instance into the worst case, we shall identify one special high-value bidder and “derandomize” his/her value, i.e., making the bid-to-value mapping a constant function . (If so, upon scaling, we can normalize this fixed value .) But it is even unclear which bidder should be the candidate: The highest-value bidder at different bids can be different. More concretely, consider the example in Figure 4a, the highest-value bidder is the red bidder initially for small bids, but changes to the blue bidder later for large bids.

We can segment the bid-to-value mappings into pieces and rearrange them, in a sense of Figure 4b, making them ordered point-wise . Then, the candidate high-value bidder clearly is the index- bidder (i.e., the red one in Figure 4b). We call this reduction LABEL:alg:layer.

Under the LABEL:alg:layer reduction, the auction/optimal social welfares FPA and OPT each remain the same, so the PoA is invariant. This proof is not that technically involved, once we formalize the reduction. However, without switching our viewpoint to the bid-to-value mappings , even describing this reduction seems difficult.

In sum, we narrow down the search space to the “layered” instances and the remaining task to address the candidate high-value bidder , particularly derandomizing his/her value .

LABEL:alg:discretize and LABEL:alg:translate (Sections 3.2 and 3.3): Two simplifications

Our main reduction is an iterative algorithm; thus it is convenient to work with bounded discrete instances, for which the main reduction will terminate in finite iterations. Such an idea appears in many prior works [CGL14, AHN+19, JLTX20, JLQ+19, JJLZ21], and the proof plan is twofold: (i) For any bounded discrete instance, the PoA is at least . (ii) For any valid instance, there exists a bounded discrete instance approximating the PoA, up to an arbitrary but fixed error . As a combination, the PoA for any valid instance is at least .

However, our discretization scheme is subtle. First, we cannot discretize the valid bid distributions given that they must be continuous everywhere except the left endpoint of the bid support. Second, we cannot discretize the value distributions and the strategies . Although bounded discrete value distributions that well approximate the given ones are trivial, it is unclear how to obtain desirable strategies : No algorithm for computing equilibria from value distributions is available. Also, with modified value distributions, even the existence of that is “close enough” to the given equilibrium is doubtful.

We circumvent these issues by discretizing the bid-to-value mappings instead (Figure 5), i.e., approximating them through piecewise constant functions .444In real analysis, for various purposes, piecewise constant functions (a.k.a. simple functions) are widely used as approximations to general functions. The benefits are threefold: (i) The valid bid distributions , the value distributions , and the equilibrium strategies can be reconstructed from the new mappings , through analytic expressions. (ii) The piecewise constancy of the new mappings makes the value distribution bounded and discrete. (iii) More importantly, we are able to obtain a sequence of piecewise constant mappings that pointwise converge to the given ones . The corresponding , , and can be arbitrarily close to the given , , and , approximating the PoA up to any fixed error . This exactly implements the second part of our proof plan.

Afterward, the LABEL:alg:translate reduction further vanishes the lowest bid, through shifting both the value space and the bid space by the same distance of (Figure 5). As a consequence, both the auction/optimal social welfares decrease by an amount of , giving a worse-or-equal PoA.

In sum, we can focus on piecewise constant and increasing mappings over a bounded support , together with the conditional value given the nil bid (i.e., the left endpoint).

LABEL:alg:polarize and LABEL:alg:slice (Sections 3.5 and 4.2): Dealing with the probability masses

Now we address the probability masses and the conditional value . (This is the only information that cannot be reconstructed from the bid-to-value mappings and must be handled separately.) Our main observation is (Lemma 2.16) that at most one bidder can have a nontrivial conditional value , who will be called the monopolist . (After the LABEL:alg:layer reduction, this monopolist will be the high-value bidder; cf. Figure 4.) That is why we can use a single conditional value , instead of values akin to the distributions or . Moreover, following the monotonicity, this value is supported on .

The LABEL:alg:polarize reduction derandomizes the conditional value by moving all the probabilities to either or . Namely, this is a win-win reduction, in a sense that at least one of the two possibilities and induces a worse-or-equal PoA than the given instance. Later, such win-win reductions also appear in several other places.

Further, the LABEL:alg:slice reduction totally determines the conditional value by eliminating the other possibility. This reduction modifies both the conditional value and the mappings , thus far more complicated than the LABEL:alg:polarize reduction, which only modifies the .555For very technical reasons, we should not unify LABEL:alg:polarize and LABEL:alg:slice into a single reduction (cf. Sections 3 and 4).

In conclusion, we can drop the notation hereafter: Just the piecewise constant and increasing mappings are enough to describe the entire instance and the reductions on it.

10 and LABEL:alg:AD (Sections 4.4 and 4.5): The main reductions

Our main reduction aims to reduce the number of pieces of the high-value bidder ’s mapping . (After the LABEL:alg:discretize reduction, this mapping has finite many pieces. In particular, the one in the worst-case instance has one single piece (Figure 2), namely a constant mapping.) To this end, we look at the first jump point of this mapping . Furthermore, we distinguish two types of jumps, pseudo jumps versus real jumps, and adopt two different reductions respectively.

For a 4.4 (LABEL:fig:intro:halve:input), the after-jump parts of all mappings are universally higher than the before-jump parts, so the entire instance naturally divides into the left-lower part versus the right-upper part (LABEL:fig:intro:halve:left and LABEL:fig:intro:halve:right). We prove that at least one part induces a worse-or-equal PoA than the given instance.666In particular, for the right-upper part, we reapply the LABEL:alg:translate reduction to make the bid space start from . This is another win-win reduction and will be called 10.

For a 4.5 (LABEL:fig:intro:AD:input), the after-jump parts (of some mappings) still interlace with the before-jump parts. We would modify the first two pieces of the high-value mapping to reduce the number of pieces by one. I.e., we either ascend the first piece to the value of the second piece (LABEL:fig:intro:AD:ascend) or descend the second piece to the value of the first piece (LABEL:fig:intro:AD:descend). We show that at least one modification gives a worse-or-equal PoA than the given instance. This is again a win-win reduction and will be called LABEL:alg:AD.

To conclude, whether a 4.4 or a 4.5, we obtain a new instance that (i) has a worse-or-equal PoA and (ii) the high-value mapping has one fewer piece. Clearly, we can iterate the entire process until a constant mapping , i.e., one single piece. Then, the LABEL:alg:collapse reduction can replace all the other bidders by one pseudo bidder , hence a two-bidder pseudo instance that has the same shape as the worst case (Figure 3), as desired.

We stress again that the above description is greatly simplified and thus just roughly accurate – The high-level idea is delivered, but most technical details are hidden.

Solving the functional optimization (Section 5)

After the above reductions, we get a nice-looking instance: (i) one bidder with a fixed high value and (ii) infinite identical low-value bidders , or one pseudo bidder in our extended language. Towards the worst case, it remains to determine the pseudo mapping , or essentially, the high-value bidder ’s bid distribution.

This is accomplished by standard tools from the calculus of variations. Via the Euler-Lagrange equation [GS+00], we formulate the worst-case bid distribution as the solution to an ordinary differential equation (ODE). Luckily, this ODE admits a closed-form solution, and “coincidentally” the tight bound is pretty nice-looking.

Comparison with previous techniques

On the Price of Anarchy in auctions, the canonical approach is the smoothness framework proposed by Roughgarden [Rou15] and developed by Syrgkanis and Tardos [ST13]. The past decade has seen an abundance of its applications and extensions (cf. the survey [RST17]).

However, the smoothness framework has an intrinsic restriction – It focuses on the structure of an auction game BUT ignores the independence, i.e., both the independence of value distributions and the independence of strategies . Thus, although giving an arsenal of tools for proving lower bounds, this approach seems hard to access tight bounds for some auctions. In particular for the first-price auction, the smoothness-based bound of obtained by Syrgkanis and Tardos [ST13] is tight when correlated distributions are allowed. Hence, this bound cannot be improved without taking the independence into account.

The work by Hoy, Taggart, and Wang [HTW18] is one of the very few follow-ups that transcend the smoothness framework.777To the best of our knowledge, [HTW18] is the only work for Bayesian single-item auctions that transcends the smoothness framework. Other such works for multi-item auctions are thoroughly discussed in [RST17, Section 8.3]. For the first-price auction, they show an improved lower bound of , but this bound is still not tight. Technically, the improvement stems from an extension of the smoothness framework that leverages the independence.

In sum, towards tight bounds for the first-price auction and the beyond, the primary consideration is: What is the consequence of the independence of values and strategies ? Our answer is, the bids are also independent and follow a product distribution . This is the starting point of our overall approach.

In the literature, ALL prior works (within/beyond the smoothness framework) follow the proof paradigm: “searching over value distributions and equilibrium strategies plus deviation strategies thereof ” [RST17, Section 8.3]. Instead, we present the FIRST different proof paradigm: “searching over (valid) bid distributions that are resulted from certain value-strategy tuples ”.

In our main proof, we step by step narrow down the search space of the worst-case instance, by showing stronger and stronger conditions it must satisfy, and completely capture the worst-case instance eventually. En route, an abundance of tools is developed, which may find applications in the future. It is conceivable that our approach can be adapted to other auctions. So, we hope that this would develop into a complement to the smoothness framework, especially in the setting of independent distributions.

2 Structural Results

This section shows a number of structural results on First Price Auction and Bayesian Nash Equilibrium. Some results or their analogs may already appear in the literature [SZ90, Leb96, MR00a, MR00b, JSSZ02, MR03, HKMN11, CH13]. However, we still formalize and reprove them for completeness. Provided these structural results, we can reformulate the Price of Anarchy problem in terms of bid distributions rather than value distributions.

To sell a single indivisible item to one of bidders, each bidder is asked to submit a non-negative bid . A generic auction is given by its allocation rule and payment rule , both of which can be randomized. Concretely, the item is allocated to the bidder , and ’s are the payments of bidders .

Rigorously, First Price Auction is not a single auction but a family of auctions, each of which has a specific allocation rule that obeys the • ‣ 2.1/• ‣ 2.1 principles.

Definition 2.1 (First Price Auctions).

An -bidder single-item auction is called a First Price Auction when its allocation rule and payment rule satisfy that:

-

•

first price allocation: Let be the set of first-order bidders. When such bidders are not unique , allocate the item to one of them , through a (randomized) tie-breaking rule given by the auction itself on this bid profile . When such a bidder is unique , allocate the item to him/her .

-

•

first price payment: The allocated bidder pays his/her own bid, while non-allocated bidders each pay nothing. Formally, for .

Without ambiguity, the allocation rule itself will be called the considered First Price Auction, since it controls the payment rule . Denote by the space of all First Price Auctions.

The only undetermined part of a First Price Auction is the tie-breaking rule, which is subtle and plays an important role in our analysis. To clarify it, let us rigorously define the interim allocation/ utility formulas (Definition 2.2) and Bayesian Nash Equilibrium (Definition 2.3).

Definition 2.2 (Interim allocations/utilities).

Given a First Price Auction , value distributions , and a strategy profile :

-

•

Each interim allocation formula for , over the randomness of the others’ bids and the considered First Price Auction itself.

-

•

Each interim utility formula for and .

Definition 2.3 (Bayesian Nash Equilibria).

Following Definition 2.2, the strategy profile reaches a Bayesian Nash Equilibrium for this distribution-auction tuple, namely , when: For each bidder , any possible value , and any deviation bid ,

Definition 2.3 means for any value , nearly all the equilibrium bids EACH maximize the interim utility formula , except a zero-measure set. By excluding these zero-measure sets from the bid supports , for , the modified strategy profile still satisfies the definition of Bayesian Nash Equilibrium. Hereafter, without loss of generality, we assume that EVERY equilibrium bid maximizes the formula .

The following existence result can be concluded from [Leb96].

Theorem 2 (Bayesian Nash Equilibrium [Leb96]).

Given any value distribution , there exists at least one First Price Auction that admits an equilibrium .

2.1 The forward direction: Bayesian Nash Equilibria

This subsection presents a bunch of lemmas that characterize an equilibrium . To this end, let us introduce some helpful notations, which will be adopted throughout this paper.

-

•

denotes the equilibrium bid distributions .

-

•

denotes the first-order bid distribution .

-

•

denotes the competing bid distribution of each bidder .

-

•

and denote the “infimum”/“supremum” first-order bids, respectively. Without ambiguity, we call the low values/bids, the boundary values/bids, and the normal values/bids. As their names suggest: (i) low bids each gives a zero winning probability, so these bids are less important; (ii) normal bids are the most common ones and we will show that they behave nicely; and (iii) boundary bids are tricky and we will deal with them separately.

-

•

denotes the optimal utility formula of each bidder . This is well defined on the value support , because (Definition 2.3) every equilibrium bid does optimize the interim utility formula .

Each bidder’s interim allocation relies on his/her competing bid distribution , plus the tie-breaking rule of the considered auction . When is a continuous distribution, they are identical , because the probability of being ONE of the first-order bidders is exactly the probability of being the ONLY one . In general, we can at least obtain (Lemma 2.4) the following properties for an interim allocation .

Lemma 2.4 (Interim allocations).

For each interim allocation formula :

-

1.

is weakly increasing for .

-

2.

It is point-wise lower/upper bounded as for .

-

3.

for any low bid , AND for any normal bid .

Proof.

Items 1 and 2 directly follows from the • ‣ 2.1 principle (Definition 2.1). Especially for Item 2, suppose that (with a nonzero probability) bidder ties with someone else for this first-order bid , then the auction always favors this bidder when “”, or always disfavor him/her when “”. Item 3 holds because is the infimum first-order bid . ∎

Lemma 2.5 shows that both of the value space and the bid space of each bidder , are almost separated by the infimum first-order bid .

Lemma 2.5 (Bidding dichotomy).

For each bidder :

-

1.

For a low/boundary value , the optimal utility is zero and, almost surely over random strategy , the equilibrium bid is low/boundary .

-

2.

For a normal value , the optimal utility is nonzero and, almost surely over random strategy , the equilibrium bid is boundary/normal .

Proof.

Recall Definition 2.2 for the interim utility formula .

Item 1. A low/boundary value induces EITHER a low (under)bid and a zero interim allocation/utility , OR a truthful/over bid and a negative interim utility . Especially, a normal bid induces a nonzero interim allocation and a strictly negative interim utility . Therefore, the optimal utility is zero and the equilibrium bid must be low/boundary . Item 1 follows then.

Item 2. A normal value is able to gain a positive utility ; for example, underbidding gives a nonzero allocation/utility . So, the equilibrium bid neither can be truthful/over (hence a negative utility ), nor can be low (hence a zero allocation/utility ). That is, the optimal utility is nonzero and the equilibrium (under)bid must be boundary/normal . Item 2 follows then. ∎

Lemma 2.6 shows, in the normal value regime , the optimal utility formula and the equilibrium strategy are monotonic (cf. [CH13, Lemma 3.9] for a similar result).

Lemma 2.6 (Bidding monotonicity).

For any two normal values that of a bidder :

-

1.

The two optimal utilities are strictly monotonic .

-

2.

The two random bids are weakly monotonic , almost surely over the random strategy .

Proof.

Lemma 2.5 already shows that the utilities are nonzero and the equilibrium bids are boundary/normal . It remains to verify the utility/bidding monotonicity.

Item 1. The utility monotonicity . We deduce that

The first step: Under the value , the optimal utility is at least the interim utility resulted from bidding , namely the equilibrium bid at the (lower) value .

The second step: Apply the interim utility formula to and .

The third step: The random bid optimizes the interim utility formula at the value .

The fourth step: (Lemma 2.5) and .

Item 1 follows then.

Item 2. The bidding monotonicity . This result also appears in [CH13, Lemma 3.9]; we would recap their proof for completeness. Assume to the opposite that . Following the interim utility formula (Definition 2.2),

We have (i) , since the equilibrium bid optimizes the interim utility formula for this value . Similarly, we have (ii) . Also, under the assumption , we know from Item 1 of Lemma 2.4 that (iii) . Given the above two equations (note that ), each of 2.1, 2.1, and 2.1 must achieve the equality. However, this means888In particular, the equality of 2.1 gives ; notice that . And the equality of 2.1 gives . For these reasons, we must have . all interim allocations/utilities are zero , which contradicts Item 1. Rejecting our assumption gives Item 2. ∎

Remark 3 (Quantiles).

Due to Lemma 2.6, the normal value space and normal/boundary bid space each identify the other in terms of quantiles. From this perspective, the stochastic process of the auction game runs as follows: Draw a uniform random quantile , and then realize the value/bid and accordingly. The two stochastic processes are equivalent conditioned on the realized value being normal .

Lemma 2.7 shows that, on the whole interval , all of the equilibrium/competing/first-order bid distributions , , and are well structured. The earlier works [MR00a, MR00b, MR03] derive similar results (under additional assumptions).

Lemma 2.7 (Bid distributions).

Each of the following holds:

-

1.

The competing/first-order bid distributions for and each have probability densities almost everywhere on , therefore being strictly increasing CDF’s on the CLOSED interval .

-

2.

The equilibrium/competing/first-order bid distributions for , for and , each have no probability mass on , excluding the boundary , therefore being continuous CDF’s on the CLOSED interval .

Proof.

We safely assume . (Otherwise, Lemma 2.7 is vacuously true since the unique bidder always bids zero in any First Price Auction.) The proof relies on Fact A.

Fact A.

Any two equilibrium bid distributions and for cannot both have probability masses at a normal bid .

Proof.

Assume the opposite. Then both bidders and (and possibly someone else) tie for this first-order bid with a nonzero probability . Conditioned on this, with a nonzero probability , at least one bidder between and cannot be allocated. Hence, either or or both can gain a nonzero extra allocation by raising his/her (equilibrium) bid . More formally, for some nonzero probabilities , we have EITHER for any , OR for any , OR both.

Without loss of generality, let us consider the case that for any . However, this means some deviation bid, such as , can benefit. Namely, because this bidder has a normal equilibrium bid , (Item 2 of Lemma 2.5) he/she must have a higher value . This implies that (by construction) and thus, that the deviated utility is lower bounded as

| the “WLOG” | ||||

| construction of | ||||

| and | ||||

To conclude, the deviation bid strictly surpasses the equilibrium bid , which contradicts (Definition 2.3) the optimality of . Rejecting our assumption gives Fact A. ∎

Remark 4.

In the proof of Fact A, the concrete construction of the deviation bid is less important. Instead, the point is that we are able to find two bids that can be arbitrarily close BUT admit a nonzero interim allocation gap . Suppose so, bidder strictly benefits from the deviation bid when it is close enough to the equilibrium bid , hence a contradiction to the optimality of .

Also, suppose there are two bids that yield two arbitrarily close nonzero interim allocations BUT themselves are bounded away , then bidder again benefits from the deviation bid , hence a contradiction to the optimality of .

We will apply such arguments in many places, WITHOUT specifying the deviation bids as the explicit constructions are less informative. For clarity, such arguments will be called the Neighborhood Deviation Arguments.

Below let us prove Item 1 and Item 2. We reason about the first-order bid distribution and the competing bid distributions separately.

Item 1: . Assume the opposite to the ’s strong monotonicity: The first-order bid distribution has no probability density/mass on an OPEN interval .

Indeed, because and , we can find a maximal such interval such that, the has probability densities or probability masses within both of the left/right neighborhoods and , for whatever . This gives . Let us do case analysis:

-

•

Case 1: . Then the must have ONE probability mass at the .

(Fact A) Exactly one equilibrium bid distribution, for a specific , has a probability mass at the ; his/her competing bid distribution has no probability mass there, thus being continuous at the . This competing bid distribution has no probability density/mass on the open interval , à la the first-order bid distribution .

Hence, (Item 1 of Lemma 2.4) bidder has a constant interim allocation on the left-open right-closed interval . But this means, conditioned on this bidder’s equilibrium bid being at the probability mass , any lower deviation bid yields a better deviated utility . This contradicts (Definition 2.3) the optimality of this equilibrium bid .

-

•

Case 2: . Then the must have NO probability mass at the .

À la the , at least one bidder for some , has probability densities within the right neighborhood , for whatever . No matter how close , we can find an equilibrium bid , for some , that gives a positive utility .

À la Case 1, this bidder has a constant interim allocation on the left-open right-closed interval ; let us consider a particular bid . This deviation bid is bounded away from the above equilibrium bid BUT, because there is no probability mass at , gives an arbitrarily close interim allocation . Therefore, we can apply the 4 to get a contradiction.

To conclude, we get a contradiction in either case. Reject our assumption: The first-order bid distribution is strictly increasing on .

Item 1: . Assume the opposite to the ’s strong monotonicity: At least one competing bid distribution has no probability density/mass on an OPEN interval .

In contrast, the remaining bidder has probability densities/masses almost everywhere on , since the first-order bid distribution is strongly increasing. Consider such an equilibrium bid . However, any lower deviation bid results in the same nonzero allocation and thus a better deviated utility . This contradicts (Definition 2.3) the optimality of the equilibrium bid . Reject our assumption: Each competing bid distribution is strictly increasing on . Item 1 follows then.

Item 2. We only need to verify continuity of the first-order bid distribution , which implies continuity of the equilibrium/competing bid distributions and .

Assume the opposite: has a probability mass at some normal bid . According to Fact A, exactly one bidder , for a specific , has a probability mass at this . Further, following Item 1, his/her competing bid distribution has probability densities within the OPEN left neighborhood , for whatever ; therefore at least one OTHER bidder has probability densities there.

This other bidder ’s interim allocation formula is discontinuous at the , because of ’s probability mass at the . Formally (Lemma 2.4), there exists a nonzero interim allocation gap around the . Hence, for some bids and that are arbitrary close , we can use the 4 to get a contradiction. Rejecting our assumption gives Item 2.

This finishes the proof of Lemma 2.7. ∎

An important and direct implication of the continuity is that for any . This is formalized as Corollary 2.8 and will be used in many places in the paper.

Corollary 2.8 (Interim allocations).

The interim allocation formula of each bidder is identical to his/her competing bid distribution , for any normal bid .

According to the Lebesgue differentiation theorem [Leb04], a monotonic function is differentiable almost everywhere, except a set of a zero measure.999Rigorously, the set has a zero Lebesgue measure. Yet since the bid distributions , , and are continuous on , we need not to distinguish the Lebesgue/probabilistic measures. We thus conclude Corollary 2.9 directly from Lemma 2.7.

Corollary 2.9 (Bid distributions).

Each of the equilibrium/competing/first-order bid distributions, , , and is differentiable almost everywhere on the OPEN interval , except a set on which this bid distribution, , , or , has a zero measure.

Remark 5 (Bid distributions).

The continuity/monotonicity/differentiability shown in Lemmas 2.7 and 2.9 are the basics of our later discussions; all subsequent bid distributions will satisfy them. So for brevity, we often omit a formal clarification. Also, we often simply write the derivatives etc by omitting (Corollary 2.9) the zero-measure indifferentiable points ; we can use standard tools from real analysis to deal with those points separately.

2.2 The inverse direction: Bid-to-value mappings

In this subsection, we study the inverse mappings of strategies and try to reconstruct the value distributions from (equilibrium) bid distributions.

Definition 2.10 (Inverses of strategies).

Consider bid distributions given by value distributions and a strategy profile . Each random inverse for is defined as the conditional distribution . So, each random inverse for is identically distributed as the random value .

Lemma 2.11 shows two basic properties of the random inverses .

Lemma 2.11 (Inverses of strategies).

Almost surely over each random inverse :

-

1.

dichotomy: for any low bid .

dichotomy: for any normal bid . -

2.

monotonicity: for two boundary/normal bids that .

Proof.

Below, we characterize (Lemma 2.13) the inverses of equilibrium strategies for normal bids , using (Definition 2.12) the concept of bid-to-value mappings . We prove that the inverse at a normal bid is essentially a deterministic value. (The inverses at the boundary bid are tricky and will be studied later.)

Definition 2.12 (Bid-to-value mappings).

Given equilibrium bid distributions (cf. Lemmas 2.7 and 2.9), define each bid-to-value mapping for as follows:

It turns out that (Item 2 of Lemma 2.13) each is an increasing function, so the domain can be extended to include the both endpoints and .

The above bid-to-value mapping is known in the literature ([HHT14] etc). However, it is usually defined only on the support of . We define it and study its properties on the entire interval , which is very important to our argument.

Lemma 2.13 (Normal bids).

For each bid-to-value mapping , the following hold:

-

1.

invertibility: almost surely over the random inverse , for any normal bid .101010More rigorously, (Corollaries 2.9 and 5) we shall exclude a zero-measure set , namely the indifferentiable points of the ’s

-

2.

monotonicity: is weakly increasing on the closed interval .

-

3.

rationality: on the left-open right-closed interval . Further, .

Proof.

We safely assume . (Otherwise, Lemma 2.13 is vacuously true since the unique bidder always bids zero in any First Price Auction.)

Item 1. Consider a specific inverse/value resulted from a normal bid . Regarding a normal bid , we can rewrite (Lemma 2.4 (Item 2) and Corollary 2.8) the interim utility formula and deduce the partial derivative

Hence, to make (Definition 2.3) the equilibrium bid optimize the formula , we must have . Here we use the fact that since is strictly increasing (Lemma 2.7). Thus, Item 1 follows then.

Item 2. For brevity, we consider a twice differentiable111111In general, following the Lebesgue differentiation theorem [Leb04], the is twice differentiable almost everywhere on , except a zero-measure set that can be handled by standard tools from real analysis. first-order bid CDF . Thus for , each competing bid CDF is also twice differentiable and each bid-to-value mapping is continuous on .

Following a combination of Item 1 and Lemma 2.11 (Item 2), each mapping is increasing on this equilibrium bid distribution ’s normal bid support , so the task is to extend this monotonicity to the whole interval . The proof relies on Facts A and B.

Fact A.

A mapping is increasing iff the reciprocal function is convex.

Proof.

Once again, we assume that the underlying CDF is twice differentiable. The reciprocal function has the second derivative . So we can rewrite the first derivative of the mapping . Precisely, the mapping is increasing iff the reciprocal function is convex . Fact A follows then. ∎

Fact B.

The first-order mapping is increasing on .

Proof.

Based on Fact A, it suffices to show that the first-order reciprocal function is convex. For brevity, we denote the equilibrium/competing reciprocal functions and for . Also, we may simply write etc.

By elementary algebra, each competing reciprocal function has the second derivative

We thus deduce that

| combine the like terms |

Moreover, the first-order reciprocal function has the second derivative

| à la the formulas | ||||

| substitute |

The first summation: for , so the product .

The second summation: for . At the considered bid , each mapping is increasing (Item 1) and thus each reciprocal is convex (Fact A).

Hence, the first-order reciprocal function is convex on . Fact B follows. ∎

Item 2 follows directly: On the normal bid support , the mapping must be increasing (Item 2 of Lemma 2.11). Outside the support , we have , so the mapping is still increasing (Fact B).

As an implication of Lemma 2.13, the value distributions can partially be reconstructed from the equilibrium bid distributions . (See Remark 3.)

Corollary 2.14 (Reconstructions).

For each , the part of the value distribution can be reconstructed from the equilibrium bid distributions as follows.

In the statement of Corollary 2.14, a mapping is undefined when , but since the first condition already holds, we think of the disjunction as being satisfied.

(i) A normal value induces a normal bid .

(ii) The normal value induces a normal bid or the boundary bid , both of which are possible especially when there is a probability mass .

(iii) A normal value induces the boundary bid .

(iv) The boundary value induces a low bid or the boundary bid , both of which are possible especially when there is a probability mass .

(v) A low value induces a bid that yields the optimal zero utility but is otherwise arbitrary; even an overbid is fine.

Corollary 2.14 enables us to reconstruct the part of each value distribution . Then how about the part? We shall consider two subparts separately. (i) The low value subpart of a value distribution cannot be reconstructed from the bid distributions . That is, an equilibrium strategy for a low value is arbitrary as long as it yields the optimal zero utility . Luckily, these low value subparts (Lemmas 2.20 and 2.21) turn out to have no contribution to neither of the auction/optimal Social Welfares, so we can ignore them. (ii) The subpart of a value distribution has contributions to the auction/optimal Social Welfares but also cannot be reconstructed. This subpart always induces to the boundary bid , following 2 (Lemmas 2.5 and 2.13).

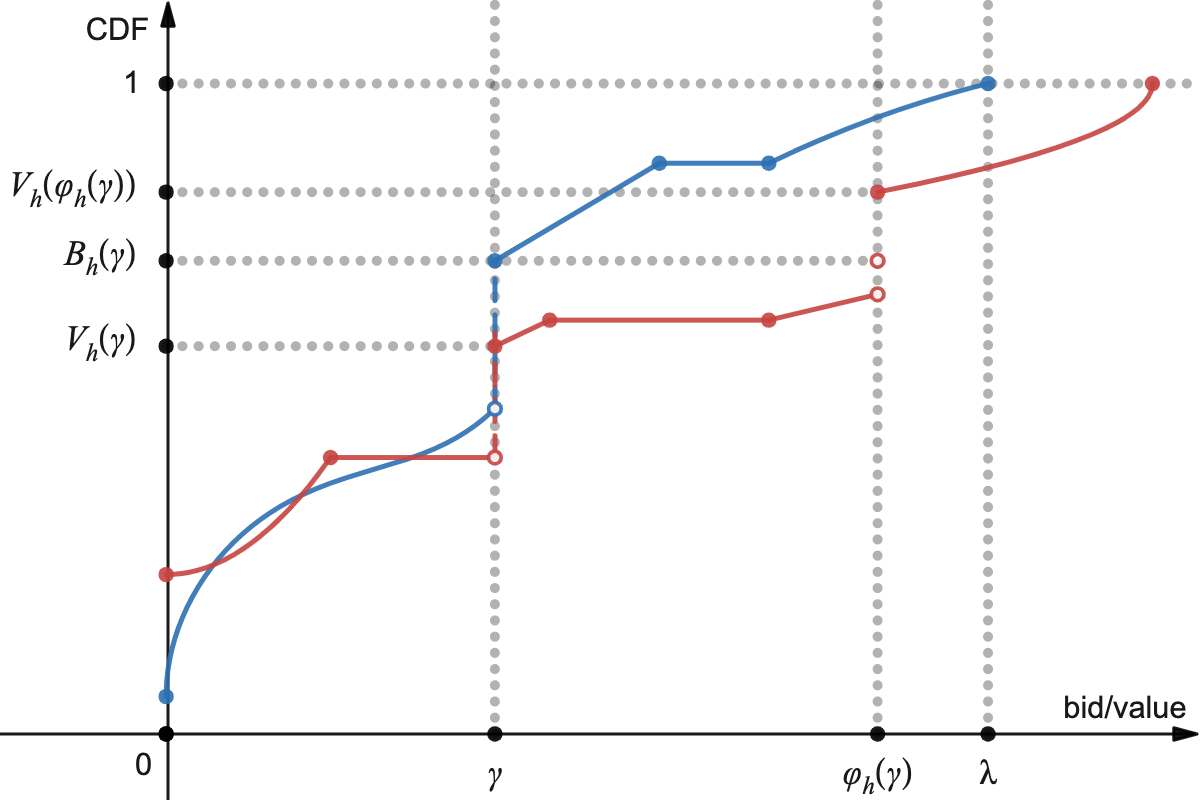

As a remedy, we introduce the concept of monopolists (Definition 2.15); cf. Figure 6 for a visual aid. Here we notice that . I.e., the first inequality holds since (Lemma 2.5) a normal bid induces a higher normal value . The second inequality directly follows from Corollary 2.14.

Definition 2.15 (Monopolists).

A bidder is called a monopolist when the probabilities of taking normal bids/values are unequal or equivalently, when the probability of taking the boundary bid yet a normal value is nonzero .

It is easier to understand this definition from the perspective of quantiles (Remark 3): A bidder is a monopolist when there are some quantiles such that but .

Lemma 2.16 presents the properties about the monopolists. (From the statement of Lemma 2.16, we can infer that there is NO monopolist when the first-order bid has no probability mass at the boundary bid .)

Lemma 2.16 (Monopolists).

There exists at most one monopolist . If existential:

-

•

monopoly: The probability of a boundary first-order bid is nonzero . Conditioned on the tiebreaker , the monopolist wins almost surely over the random allocation .

-

•

boundedness: A boundary bid induces a bounded random value .

Proof.

Suppose there is a monopolist . We first verify • ‣ 2.16 and • ‣ 2.16, and then prove that there is no other monopolist.

For some normal value , (Definitions 2.15 and 2.5) the boundary bid yields the optimal utility , so the interim allocation is nonzero . The boundary first-order bid occurs with probability . Assume for contradiction that this monopolist loses the tiebreaker with a nonzero probability . Based on the 4, some (infinitesimally) higher deviation bid gives a strictly better utility , which contradicts (Definition 2.3) the optimality of this equilibrium bid . Reject our assumption: This monopolist always wins the tiebreaker (• ‣ 2.16).

A boundary bid induces a bounded random value (• ‣ 2.16). (i) This monopolist can never take a low value . The tiebreaker occurs with a nonzero probability and, suppose so, the monopolist wins almost surely over the random allocation . Hence, a low value together with a boundary bid yields a negative utility , which is impossible. (ii) The value is also upper bounded , given bidding monotonicity (Item 2 of Lemma 2.6) and 1 (Item 1 of Lemma 2.13).

This monopolist is the unique one. Otherwise, (Definition 2.15 and • ‣ 2.16) at least two monopolists tie for the boundary first-order bid with a nonzero probability and, suppose so, BOTH win almost surely over the random allocation . However, this is impossible because we are auctioning ONE item. Lemma 2.16 follows then. ∎

Conceivably, we shall reconstruct the subpart just for the value distribution of the unique monopolist (if existential) – We will show this later in Lemma 2.18. To reconstruct the , we introduce (Definition 2.17) the concept of conditional value distributions.

Definition 2.17 (Conditional value distributions).

Regarding the monopolist ’s truncated random value for , define the conditional value distribution as follows.

In the case of no monopolist , the always takes the boundary value .

Remark 6 (Conditional value distributions).

The random value for exactly follows the distribution . With the help of Figure 6, we can see that the CDF is given by

In general, the can be any -supported distribution. Given this extra information, we can reconstruct the value distributions (Lemma 2.18) except the unimportant low value parts.

Lemma 2.18 (Reconstructions).

For each , the part of the value distribution can be reconstructed from the equilibrium bid distributions plus the conditional value distribution as follows.

-

•

in the case of a non-monopoly bidder .

-

•

in the case of the monopolist .

Proof.

See Figure 7 for a visual aid. Regarding a non-monopoly bidder , (Lemmas 2.5 and 2.15; cf. Figure 7b) a normal bid induces a normal value and vice versa. By 2, such a normal value for is at least . Hence, on the OPEN interval , the value distribution has no density and keeps a constant function . Given these, the reconstruction in Corollary 2.14 can be generalized naively: For , we have .

Lemma 2.19 will be useful for formulating the expected auction/optimal Social Welfares.

Lemma 2.19 (Social Welfares).

Conditioned on the boundary first-order bid , each of the following exactly follows the conditional value distribution :

-

•

The conditional auction Social Welfare .

-

•

The conditional optimal Social Welfare .

Proof.

The random events and are identical, regarding the infimum first-order bid . Conditioned on this, (i) a non-monopoly bidder has a low/boundary bid and (Lemmas 2.5 and 2.15) a low/boundary value ; while (ii) the monopolist has EITHER a low bid and a low/boundary value , OR the boundary bid and (Lemma 2.16) a boundary/normal value .

The allocated bidder always take the boundary bid and, to make the utility nonnegative, a boundary/normal value ; the case of a normal value occurs only if the monopolist is allocated . Hence, the conditional optimal Social Welfare is identically distributed as each of the following:

| for | ||||

| independence |

That is, the conditional optimal Social Welfare follows (Definition 2.17) the distribution . Further, since the monopolist (as the only possible bidder that has a normal value ) always wins the tiebreaker (Lemma 2.16), the conditional auction/optimal Social Welfares are identically distributed , which again follow the distribution . This finishes the proof. ∎

2.3 Reformulation for the Price of Anarchy problem

To address the Price of Anarchy problem, we shall formulate the expected auction/optimal Social Welfares and . Indeed, these can be written in terms of the equilibrium bid distributions plus the conditional value distribution (Definition 2.17).

First, Lemma 2.20 formulates the expected auction Social Welfare .

Lemma 2.20 (Auction Social Welfare).

The expected auction Social Welfare can be formulated based on the conditional value distribution and the equilibrium bid distributions :

where the first-order bid distribution and the bid-to-value mappings can be computed from the bid distributions (Definition 2.12).

Proof.

In any realization, the outcome auction Social Welfare is the allocated bidder’s value . Over the randomness of the values , the equilibrium strategies , and the allocation rule , the expected auction Social Welfare is given by

| (B) | ||||

| (N) |

Here we used the fact that the first-order bid is at least .

For Term (B), we deduce that

| Term (B) | |||

The last equality uses the fact that conditioned on the boundary first-order bid , the allocated bidder ’s value follows the distribution (Lemma 2.19).

For Term (N), we deduce that

| Term (N) | ||||

| (N1) | ||||

| (N2) | ||||

| (N3) | ||||

| (N4) | ||||

| (N5) |

(N1): Redenote for . Recall Definition 2.10 that each random inverse for is identically distributed as the random value .

(N2): Divide the event into subevents for .

(N3): Lemma 2.13 (Item 1) that for any normal bid

and Definition 2.2 that .

(N4): Corollary 2.8 that for any normal bid .

(N5): The first-order bid distribution .

Combining Terms (B) and (N) together finishes the proof of Lemma 2.20. ∎

Moreover, Lemma 2.21 formulates the expected optimal Social Welfare .

Lemma 2.21 (Optimal Social Welfare).

The expected optimal Social Welfare can be formulated based on the conditional value distribution and the equilibrium bid distributions :

Proof.

This proof simply follows from Lemma 2.18, i.e., we essentially reconstruct the value distributions from the tuple .

In any realization, the outcome optimal Social Welfare is the first-order value . Over the randomness of the values , the expected optimal Social Welfare is given by

| (O1) | ||||

| (O2) | ||||

| (O3) | ||||

(O1): The first-order value for is always boundary/normal .

(O2): The expectation of a nonnegative distribution is given by .

(O3): Apply Lemma 2.18. It also holds in case that no monopolist exists since, suppose so, we have for .

This finishes the proof of Lemma 2.21.

∎

The above -based Social Welfare formulas and , together with the characterizations of and , are the foundation of the whole paper. From all these discussions, we notice that the below- parts of bid distributions and value distributions are less important. To stress this observation, we have the key definition of valid instances .

Definition 2.22 (Valid instances).

A valid instance , where and , is given by independent distributions and satisfies the following.

-

•

The bid distributions have a common infimum bid and a universal supremum bid .

-

•

The bid CDF’s for are continuous functions on , while the competing bid CDF’s for and the first-order bid CDF are continuous and strictly increasing functions on .

-

•

monotonicity: The bid-to-value mappings for are weakly increasing functions on .

-

•

monopoly: The index- bidder without loss of generality is the unique monopolist.121212This accommodates the “no monopolist” case of Lemma 2.16, by taking as a deterministic value of . I.e., this bidder always wins in the all-infimum tiebreaker .

-

•

boundedness: Under the infimum bid , the monopolist ’s conditional value is bounded as , while the other bidders’ conditional values are truthful, for .

The valid instances capture nearly all Bayesian Nash Equilibria . Essentially, there is a bijection between these two spaces (without considering some less important details about Bayesian Nash Equilibria), especially in a sense of the Social Welfare invariant. This is formalized into Theorem 7.

Theorem 7 (Valid instances).

(I) For any valid instance , there is some equilibrium , for some value distribution , whose conditional value distribution and bid distribution are exactly the . (II) For any value distribution and any equilibrium , there is some valid instance that yields the same auction/optimal Social Welfares and .

Proof.

See Figure 8 for a visual aid. We prove Items (I) and (II) separately.

(I) Given a valid instance , we can construct the boundary/normal value part of some value distribution , following Lemma 2.18. For the low value part, we simply let on , namely putting all the undecided probabilities to the boundary value . Then the value distribution is well defined.

Since we zero-out everything below , the equivalence in Remark 3 can be extend to the entire quantile space . Hence, we can construct the equilibrium by identifying the quantiles for value distributions and bid distributions. Consider the quantile bid/value functions and . As Figure 8 shows, we construct the strategy profile as follows: For and , let be a uniform random quantile, then

We conclude Item (I) with verifying the equilibrium conditions (Definition 2.3).

Fact A.

almost surely over the random strategy , for each bidder , any value , and any deviation bid .

Proof.

First, the monopolist (Corollaries 2.8, 2.15 and 2.16) has the allocation for a boundary/normal bid and for a low .

(i) A Normal Bid .

The underlying value , by construction and Lemmas 2.18 and 2.13.

Accordingly, the current allocation/utility are positive .

Then a low deviation bid is suboptimal, because the deviated allocation/utility are zero .

Moreover, a boundary/normal deviation bid is suboptimal – The current bid maximizes the utility formula , because the partial derivative , the underlying value , and the mapping is increasing (Item 2 of Lemma 2.13).

(ii) A Boundary Bid .

The underlying value exactly follows the conditional value distribution and ranges within , by construction and Definitions 2.17 and 2.22.

Reusing the above arguments (i.e., the utility formula is decreasing for ),

we can easily see that the current bid is optimal.

In sum, the monopolist meets the equilibrium conditions.

Each non-monopoly bidder (Corollaries 2.8, 2.15 and 2.16) has the allocation for a normal bid and for a low/boundary bid .

(i) A Normal Bid .

Reusing the above arguments for the monopolist ,

we can easily see that the current normal bid is optimal.

(ii) A Boundary Bid .

The underlying value must be the boundary value , by construction and Definitions 2.17 and 2.22.

Obviously, the current zero utility and the current boundary bid are optimal.

In sum, each non-monopoly bidder meets the equilibrium conditions.

Fact A follows then.

∎

(II) Given an equilibrium , as before, consider the bid distribution , the conditional value distribution , and the infimum/supremum first-order bids and . Following Lemmas 2.7, 2.13, 2.16 and 2.17, this instance is almost valid, except that the distribution can be supported on low bids . (Recall that the distribution is just supported on boundary/high values .) By truncating the bid distribution for and reusing the conditional value distribution , we obtain a valid instance . In particular, the truncation does not modify the auction/optimal Social Welfares (cf. Lemmas 2.20 and 2.21). This finishes the proof of Item (II). ∎

We conclude this section with (Corollary 2.23) an equivalent definition for Price of Anarchy in First Price Auctions, as an implication of Theorem 7.

Corollary 2.23 (Price of Anarchy).

Regarding First Price Auctions, the Price of Anarchy is given by

3 Preprocessing Valid Instances

This section presents several preparatory reductions towards the potential worst-case instances. In Section 3.1, we introduce the concept of valid pseudo instances, which generalizes valid instances and eases the presentation. In Section 3.2, we discretize an instance up to any PoA-error , simplifying the bid-to-value mappings to a (finite-size) bid-to-value table . In Section 3.3, we translate the instances, making the infimum bids zero . In Section 3.4, we layer the bid-to-value mappings , making the table decreasing bidder-by-bidder. In Section 3.5, we derandomize the conditional value to either the floor value or the ceiling value .

To conclude (Section 3.6), we restrict the space of the worst cases to the floor/ceiling pseudo instances, which can be represented just by the table . These materials serve as the basis for the more complicated reductions later in Section 4.

3.1 The concept of valid pseudo instances

This subsection introduces the concept of valid pseudo instances , a natural extension of valid real instances from Definition 2.22. Given a valid real instance , we can always (Lemma 3.5) construct a valid pseudo instance that yields the same auction/optimal Social Welfares. Thus towards a lower bound on the Price of Anarchy, we can consider valid pseudo instances instead (Corollary 3.6).

Roughly speaking, a pseudo instance includes one more pseudo bidder to a real instance . To clarify this difference, we often use the letter and its variants for real bidders, and the Greek letter and its variants for real or pseudo bidders. Without ambiguity, we redenote by the space of valid pseudo instances. The formal definition of valid pseudo instances is given below; cf. Definition 2.22 for comparison.

Definition 3.1 (Valid pseudo instances).

A valid instance , where and , is given by independent distributions and satisfies the following.

-

•

The real bidders for each compete with other bidders , while the pseudo bidder competes with all bidders , including him/herself .

-

•

The bid distributions have a common infimum bid and a universal supremum bid .

-

•

The bid CDF’s for are continuous functions on , while the competing bid CDF’s for and the first-order bid CDF are continuous and strictly increasing functions on .

(The is exactly the pseudo bidder ’s competing bid CDF.) -

•

monotonicity: The bid-to-value mappings for are weakly increasing functions on .

-

•

monopoly: The index- bidder without loss of generality is the unique monopolist. I.e., this bidder always wins in the all-infimum tiebreaker .

-

•

boundedness: Under the infimum bid , the monopolist ’s conditional value is bounded as , while the other bidders’ conditional values are truthful, for .

Remark 8 (Pseudo instances).

The concept of pseudo instances greatly eases the presentation and similar ideas also appear in the previous works [AHN+19, JLTX20, JLQ+19, JJLZ21].

Essentially, a pseudo instance can be viewed as the limit of a sequence of real instances. I.e., the pseudo bidder can be viewed as, in the limit , a collection of low-impact bidders . All these low-impact bidders have the common competing bid distribution , so the highest bid among them leads to the highest value and we just need to keep track of the collective information .

On the other hand, in the limit , the common competing bid distribution pointwise converges to the first-order bid distribution . This accounts for the pseudo mapping .

Because valid pseudo instances differ from the valid real instances ONLY in the definition of the pseudo mapping , most results in Section 2 still hold. In particular, Lemma 3.2 formulates their Social Welfares (which restates Lemmas 2.20 and 2.21 basically).

Lemma 3.2 (Social Welfares).

For a valid pseudo instance , the expected auction/ optimal Social Welfares and are given by

where the first-order bid distribution and the quasi first-order value distribution can be reconstructed from .

Lemma 3.3 shows that given a pseudo instance , the pseudo bidder always has a dominated bid-to-value mapping , compared with other real bidders .

Lemma 3.3 (Bid-to-value mappings).

For a valid pseudo instance , the bid-to-value mappings satisfy the following:

-

1.

for . Further, .

-

2.

for .

Proof.

Item 1 is an immediate consequence of (Definition 3.1) the bid-to-value mappings for . In particular, in the proof of Lemma 2.13 (Fact 3), we already show that the pseudo mapping for and . Moreover, we have . Rearranging this equation gives Item 2. ∎

Lemma 3.4 shows that the bid distributions can be reconstructed from the bid-to-value mappings . This lemma is important in that many subsequent reductions will construct new bid distributions in terms of the mappings . Therefore, the correctness of such construction reduces to checking Items 1 and 2 of Lemma 3.3 and monotonicity of the mappings .

Lemma 3.4 (Bid distributions).

Proof.

The construction of intrinsically ensures that below the infimum bid and at the supremum bid , for . Moreover, Items 1 and 2 of Lemma 3.3 together make each an increasing function on , hence a well-defined -supported bid distribution. It remains to verify over the bid support , for , namely the functions are exactly (Definition 3.1) the bid-to-value mappings stemmed from the . These identities for can be easily seen via elementary algebra; we omit the details for brevity. Lemma 3.4 follows then. ∎

Lemma 3.5 suggests that any valid real instance can be reinterpreted as a valid pseudo instance , by employing a specific pseudo bidder . As a consequence (Corollary 3.6): Towards a lower bound on the Price of Anarchy in First Price Auctions, we can consider valid pseudo instances instead; cf. Corollary 2.23 for comparison.

Lemma 3.5 (Pseudo instances).

For a valid instance , the following hold:

-

1.

The pseudo bidder induces a valid pseudo instance .

-

2.

and .

Proof.

As mentioned in Remark 8, to see the validity , we only need to verify • ‣ 3.1 of mappings and • ‣ 3.1 of the conditional value .

Item 1. We have and for . Thus, each real bidder keeps the same mapping after including the pseudo bidder (Definitions 2.22 and 3.1), preserving • ‣ 3.1. Also, the pseudo mapping can be written as for , based on the first-order bid distribution . In the proof of Lemma 2.13 (Fact B), we already verify • ‣ 3.1 of this mapping. Moreover, the unmodified conditional value must preserve • ‣ 3.1.

Item 2. This can be easily inferred from (Lemmas 2.20 and 2.21 versus Lemma 3.2) the Social Welfare formulas for valid real versus pseudo instances; thus we omit details for brevity. Roughly speaking, the point is that the pseudo bidder for has no effect on Social Welfares. ∎

Due to the above lemma, we know that the PoA of pseudo instances is a lower bound of the real PoA. (On the other hand, we know that a pseudo instance can be viewed as the limit of a sequence of real instances. As a result, any PoA ratio obtained by a pseudo instance can be approximated by real instances arbitrarily well.) Thus, we have the following corollary.

Corollary 3.6 (Lower bound).

Regarding First Price Auctions, the Price of Anarchy is at least

3.2 Discretize: Towards (approximate) discrete pseudo instances

In this subsection, we introduce the concept of discretized pseudo instances ; see Definitions 3.7 and LABEL:fig:discretize for its formal definition and a visual aid.

Definition 3.7 (Discretized pseudo instances).

A valid pseudo instance from Definition 3.1 is further called discretized when it satisfies • ‣ 3.7 and • ‣ 3.7.

-

•

finiteness: The supremum bid/value are bounded away from infinite .

-

•

piecewise constancy: Given some bounded integer and some -piece partition of the bid support , each bid-to-value mapping for is a piecewise constant function under this partition.

Notice that the partition relies on the bid distributions but is irrelevant to the monopolist ’s conditional value .

Remark 9 (Discretized pseudo instances).

The value distributions for reconstructed from a discretized pseudo instance are almost discrete, except the conditional value of the monopolist (which ranges between but otherwise is arbitrary). Namely, each index piece of a bid-to-value mapping induces a probability mass of the value distribution .

Lemma 3.8 shows that the PoA bound of a (generic) valid pseudo instance can be approximated arbitrarily close by a discretized pseudo instance .

Intuition.

For the Price of Anarchy problem, we only consider (Corollary 3.6) the pseudo instances that have bounded Social Welfares . In the sense of Lebesgue integrability, we can carefully truncate131313We will use a special truncation scheme. The usual truncation scheme often induces probability masses at the truncation threshold, but we require that the bid CDF’s are continuous over the bid support . the bid distributions to meet the • ‣ 3.7 condition, by which the auction/optimal Social Welfares change by negligible amounts.

Then, we replace the bid-to-value mappings by their interpolation functions (• ‣ 3.7). The mappings determine the bid distributions (Lemma 3.4) and the auction/optimal Social Welfares (Lemma 3.2) in terms of integral formulas, which are insensitive to the (local) changes of the interpolation functions . Thus as usual, when the interpolation scheme is accurate enough, everything (including the PoA-bound) can be approximated arbitrarily well. To make the arguments rigorous, we use the continuous mapping theorem [Bil13] in measure theory.

Theorem 10 (The continuous mapping theorem [Bil13]).

Let and be random elements defined on a metric space . Regarding a function (where is another metric space), suppose its set of discontinuity points has a zero measure , then this function perseveres the property of convergence in distribution. Formally,

Lemma 3.8 (Discretization).

Given a valid pseudo instance that has bounded expected auction/optimal Social Welfares , for any error , there is a discretized pseudo instance such that .

Proof.

For ease of presentation, we first assume that the given pseudo instance itself satisfies • ‣ 3.7 ; this assumption will be removed later.

Given an integer , we would divide the bounded bid support into uniform pieces , via the partition points for . Regarding this partition , the LABEL:alg:discretize reduction (see LABEL:fig:alg:discretize and LABEL:fig:discretize for its description and a visual aid) transforms the given pseudo instance into another discretized pseudo instance . This is formalized into Fact A.

Fact A.

Under reduction , the output is a discretized pseudo instance; the conditional value is unmodified.

Proof.

The Discretize reduction (Line LABEL:alg:discretize:distribution) reconstructs the output bid distributions from the output mappings ; (Line LABEL:alg:discretize:mapping) each output mapping is the -piece interpolation of the input mapping under the partition . In particular (see LABEL:fig:discretize for a visual aid), the output mappings interpolate the right endpoint of each index- piece of the partition .

Obviously, each interpolation is a piecewise constant function on the same bounded domain (• ‣ 3.7 and • ‣ 3.7) and is an increasing function à la the input mapping (• ‣ 3.1). Also, the extended range restricts the unmodified conditional value (• ‣ 3.1).

We thus obtain a sequence of discretized pseudo instances , for . Below we study the bound for each of them. To this end, consider a specific profile . Following Definition 3.1, depending on whether the bids each take the infimum or not :

-

•

The monopolist takes a value .

-

•

Each other bidder takes a value .

Over the randomness of the allocation rule , this index- pseudo instance yields an interim auction Social Welfare .

Likewise, under the same profile , the input pseudo instance yields a counterpart formula .

Facts B and C show certain properties of the input/index- mappings and and the input/index- formulas and .

Fact B.

On the domain , the mappings and are bounded everywhere, and continuous almost everywhere except a zero-measure set . Also, on the domain , the formulas and are bounded everywhere, and continuous almost everywhere except a zero-measure set .

Proof.

Each input mapping as an increasing function (• ‣ 3.1) is continuous almost everywhere, except countably many discontinuities that in total have a zero measure. Also, each input mapping is bounded (• ‣ 3.7). Such continuity and boundedness extend to the input formula , since tiebreakers occur with a zero probability.141414That is, conditioned on the all-infimum bid profile , the monopolist always gets allocated (• ‣ 3.1). Otherwise , tiebreakers occur with a zero probability because the underlying bid CDF’s are continuous functions (Definition 3.1).

For the same reasons, the index- mappings and the index- formula are also bounded and continuous almost everywhere. Fact B follows then. ∎

Fact C.

The sequence pointwise converges to almost everywhere.

Proof.

Now we would consider a random profile from the input pseudo instance rather than a specific profile .