Seojeong Lee

Department of Economics

Seoul National University

Seoul, Korea

s.jay.lee@snu.ac.kr

and Siha Lee

Department of Economics

McMaster University

Hamilton, Ontario, Canada

lees223@mcmaster.ca

and

Julius Owusu

Department of Economics

McMaster University

Hamilton, Ontario, Canada

owusuj4@mcmaster.ca

and

Youngki Shin

Department of Economics

McMaster University

Hamilton, Ontario, Canada

shiny11@mcmaster.ca

csa2sls: A complete subset approach for many instruments using Stata

Abstract

We develop a Stata command csa2sls that implements the complete subset averaging two-stage least squares (CSA2SLS) estimator in Lee and Shin [2021]. The CSA2SLS estimator is an alternative to the two-stage least squares estimator that remedies the bias issue caused by many correlated instruments. We conduct Monte Carlo simulations and confirm that the CSA2SLS estimator reduces both the mean squared error and the estimation bias substantially when instruments are correlated. We illustrate the usage of csa2sls in Stata by an empirical application.

keywords:

st0001, csa2sls, many instruments, complete subset averaging, two-stage least squares.1 Introduction

The two-stage least squares (2SLS) estimator is one of the most widely used methods in applied economics. Theoretically, the optimal instrument can be achieved by the conditional mean function of the first-stage regression. However, in practice, practitioners working with a finite sample face a crucial question of how many instruments one should use, especially when there are many instruments available. This is partly due to the well-known trade-off between bias and variance when the number of instruments increases. Donald and Newey (2001) shows this point clearly by a higher-order Nagar expansion and proposes to choose the optimal number of instruments that minimizes the mean squared errors. Kuersteiner and Okui (2010) proposes a model averaging approach for the first stage regression and shows that it achieves the optimal weight. These other approaches, however, either require the practitioner to know the order of importance among instruments (Donald and Newey, 2001) as the method chooses the first few important instruments, or the practitioner needs to estimate the optimal weights for the instruments (Kuersteiner and Okui, 2010).

As an alternative, Lee and Shin (2021) proposes a model averaging approach that uses all size- subsets of the set of available instruments in a cross-sectional regression model. This new approach is named as the complete subset averaging two-stage least squares (CSA2SLS) estimator. One advantage of the CSA2SLS estimator is that since it uses all subsets, it does not require knowledge of the order of importance among instruments. Furthermore, averaging models using equal weights reduces potential efficiency loss in finite samples. This is because when estimated weights (instead of equal weights) are used, these become additional parameters in the model and therefore, cause inefficiency when the number of models to be averaged is large.

We develop a Stata command csa2sls that implements the CSA2SLS estimator. It selects the optimal number of subset size that minimizes the approximate mean squared errors. Since the size of the complete subset grows at the order of , where is the total number of instruments, CSA2SLS is computationally intensive. To alleviate such a computational burden, the command csa2sls includes options for subsampling and a fast-but-memory-intensive method.

The remainder of the paper is organized as follows. In Section 2, we introduce the complete subset averaging two-stage least squares (CSA2SLS) estimator in Lee and Shin (2021). Section 3 explains the command csa2sls. Section 4 shows results from Monte Carlo experiments which numerically illustrates how the CSA2SLS estimator alleviates some of the issues that arise from many instruments. We provide an empirical application of csa2sls in Section 5. Section 6 concludes.

2 CSA2SLS Estimator

In this section, we explain the key idea of the CSA2SLS estimator in Lee and Shin (2021). Heuristically speaking, we estimate the first-stage predicted value by model averaging and apply the 2SLS estimation with those predicted values. Given a total of instruments, we consider all subsets composed of instruments. We compute a simple average of predicted values across models and the 2SLS estimator follows immediately. The optimal is selected by minimizing the approximate mean squared errors criterion, which will be explained in detail below.

To be concrete, consider the following model generated from an independent and identically distributed (i.i.d.) sample:

where is a scalar outcome variable, is a vector of endogenous variables, is a vector of included exogenous variables, and is a vector of exogenous variables (including ), is an unknown function of , and and are error terms uncorrelated with . Finally, denotes an error term when we project the endogenous regressor into the space of exogenous variable . Note that by construction.

Let , , , , and where . The set of instruments has the form , where ’s are functions of such that is the collection of instruments. Note that the total number of instruments can increase as . We suppress the dependency of on for notation simplicity. Let be the collection of .

Let be the number of subsets (or models) with instruments:

We also suppress the dependency of on and . Let be an index of each model and be a vector of instruments in model . Then, the first-stage regression of model can be written as

The average predicted value of is

where is the OLS estimator of . Then, the CSA2SLS estimator is defined as

Using the projection matrices, we can also write the CSA2SLS estimator as a one-step procedure:

where with .

The optimal subset size is chosen by minimizing the approximate mean squared error. Let be a preliminary estimator and . The fitted value of is given as

where consists of exogenous variables plus the preliminary selection of instruments as described above. Let . The residual matrix is denoted by . Define , , , and . Then, the sample counterpart of the approximate mean squared error is given by

where

The preliminary estimator can be estimated either by using the two-step Malllows’s criterion or by adopting the one-step method. See Lee and Shin (2021) for detail.

3 The command csa2sls

3.1 Syntax

The generic syntax for the command is as follows: csa2sls depvar exogvar (endovar = instvar) [ , noprint noconstant r(integer) large onestep ]

The four arguments of the command are depvar (the dependent variable), exogvar (the list of included exogenous variables), endovar (the endogeneous variable) and instvar (the list of excluded exogenous variables, i.e. instrumental variables).

-

noprint specifies estimation without printing the results on screen. The default is to print estimation results in the result pane.

-

noconstant specifies estimation without an intercept term in the second stage regression. The default is to include a constant term.

-

r(integer) specifies a positive integer for the maximum number of randomly selected subsets when the number of subsets are bigger than integer. The default is 100.

-

large turns on the large sample estimation program. When the sample size is large, the average projection matrices may require a large memory size. The large option must be turned on to avoid an insufficient memory issue. The default is not using this option.

-

onestep specifies the preliminary estimation method using the one step approach described in Lee and Shin [2021]. The default is the preliminary two-step Mallows criterion.

3.2 Stored results

ereturn list command has the following stored information:

-

Scalars:

-

equals the residual sum of squares.

-

equals the optimal subset size of instruments.

-

equals the model degrees of freedom.

-

equals the root mean squared error.

-

equals the model sum of squares.

-

equals the R-squared.

-

equals the adjusted R-squared.

-

equals the chi-squared.

-

equals the number of observations.

-

equals the rank of

-

-

Macros:

-

describes the preliminary estimation method.

-

is the name of the command.

-

is the name of the dependent variable.

-

is the name of the exogenous variables.

-

is the name of the instruments.

-

is the name of the instrumented variables.

-

is the command line typed by the user.

-

specifies the name of the coefficient and variance-covariance matrix.

-

is the program used to implement predict

-

is noconstant or hasconstant if specified.

-

is the name of cluster variable.

-

program used to implement footnote display.

-

is the title in estimation output.

-

-

Matrices:

-

equals the coefficient matrix

-

equals the variance-covariance matrix

-

4 Monte Carlo experiments

In this section, we conduct Monte Carlo simulation studies focusing on the effect of correlated instruments. An sample is generated from the following simulation design:

where is a scalar endogenous regressor, is set to be , and is a -dimensional vector of instruments generated from a multivariate normal distribution . The diagonal elements of are set to be 1 and the off-diagonal elements are . We set each element of to be , where 0.1 is the R-squared in the first stage regression. The vector of error terms follows a bivariate normal distribution whose means are zeros and variances are ones. The covariance between and is set to be 0.9. In these simulation studies, varies in and varies in . The sample size is set to be and the results are from 1,000 replications.

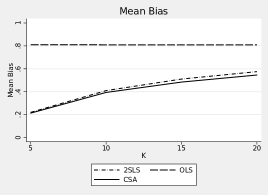

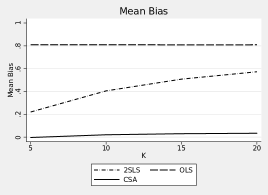

Figure 1 summarizes the simulation results. We report the mean bias and mean squared error (MSE) of CSA2SLS along with the performance of the ordinary least squares estimator (OLS) and the two-stage least squares estimator (2SLS). First, the CSA2SLS estimator reduces the bias substantially when instruments are correlated (). As predicted by theory, the bias of 2SLS increases as increases. Note that when instruments are independent (), the difference in the bias between the CSA2SLS estimator and the 2SLS estimator is small. Lee and Shin (2021) proves that the performance of CSA2SLS will be asymptotically equivalent to that of 2SLS when .

Second, the efficiency loss of CSA2SLS is modest. When instruments are correlated, CSA2SLS achieves lower mean squared errors when . Like the bias, the MSE gap between CSA2SLS and 2SLS increases as increases. It is also worthwhile to note that the MSE of CSA2SLS does not change much over different values of . Finally, the OLS estimator performs the worst in these simulation designs.

To sum, the CSA2SLS estimator shows a good finite sample performance as predicted by theory. We also observe the increased bias of 2SLS when there are many instruments. We recommend practitioners to use the CSA2SLS estimator when they have many correlated instruments.

5 Empirical illustration

In this section we illustrate the usage of csa2sls by an empirical application. In this example, we revisit Berry, Levinsohn, and Pakes (1995) and estimate a logistic demand function for automobiles based on pooled cross-sectional data over different markets.

The model is specified as

where is the market share of product with product 0 denoting the outside option, is the endogenous price variable, is a vector of included exogenous variables and is a set of 10 instruments. The parameter of interest is from which we can calculate the price elasticity of demand. Note that the optimal subset size is 9 in this empirical example.

-

. set seed 2022 . insheet using "BLP.csv", comma clear (54 vars, 2,217 obs) . csa2sls y hpwt air mpd space (price = sumother1 sumotherhpwt sumotherair /// > sumothermpd sumotherspace sumrival1 sumrivalhpwt sumrivalair sumrivalmpd /// > sumrivalspace) Complete Subset Model Averaging 2SLS Regression Number of obs = 2,217 Wald chi2(5) = 820.64 Prob > chi2 = 0.0000 R-squared = 0.3373 Root MSE = 1.1245 y Coef. Std. Err. z P>|z| [95% Conf. Interval] price -.142563 .0117095 -12.18 0.000 -.1655131 -.1196128 hpwt 1.422452 .414676 3.43 0.001 .6097024 2.235202 air .5620958 .1379201 4.08 0.000 .2917772 .8324143 mpd .1579617 .0471821 3.35 0.001 .0654864 .2504369 space 2.284253 .1289588 17.71 0.000 2.031499 2.537008 _cons -2.342198 .2673599 -8.76 0.000 -2.866214 -1.818182 Instrumented: price Instruments: hpwt air mpd space sumother1 sumotherhpwt sumotherair sumothermpd sumotherspace sumrival1 sumrivalhpwt sumrivalair sumrivalmpd sumrivalspace . correlate sumother1 sumotherhpwt sumotherair sumothermpd sumotherspace /// > sumrival1 sumrivalhpwt sumrivalair sumrivalmpd sumrivalspace (obs=2,217) sumoth~1 sumoth~t sumoth~r sumoth~d sumoth~e sumriv~1 sumriv~t sumriv~r sumriv~d sumriv~e sumother1 1.0000 sumotherhpwt 0.9791 1.0000 sumotherair 0.6948 0.7039 1.0000 sumothermpd 0.9309 0.9341 0.7914 1.0000 sumothersp~e 0.9902 0.9747 0.6335 0.8862 1.0000 sumrival1 -0.3873 -0.3552 0.0832 -0.1527 -0.4667 1.0000 sumrivalhpwt -0.2744 -0.2163 0.1680 -0.0271 -0.3487 0.9532 1.0000 sumrivalair -0.0227 0.0089 0.3275 0.2013 -0.1035 0.8830 0.9168 1.0000 sumrivalmpd -0.1400 -0.0923 0.2531 0.1132 -0.2131 0.9053 0.9456 0.9281 1.0000 sumrivalsp~e -0.5178 -0.4797 -0.0277 -0.2790 -0.5909 0.9823 0.9356 0.8144 0.8576 1.0000

We also report correlation coefficients among the instruments. We can confirm that the instruments are divided into two groups and that each group’s instruments are highly correlated with each other. The correlation coefficient varies from 0.69 to 0.99.

6 Conclusion

In this article, we present the complete subset averaging two-stage least squares estimator and develop the corresponding Stata command csa2sls. The usage of csa2sls is illustrated by an empirical application. The Monte Carlo experiments show that 2SLS is biased when there are many instruments and that CSA2SLS outperforms 2SLS when instruments are correlated with each other. Since CSA2SLS is computationally intensive, an interesting future research question would be to develop a more efficient computation algorithm. An approach based on the stochastic gradient descent (see, for example, Lee et al. (2022)) can be a possible solution.

7 Acknowledgement

We would like to thank the editor and an anonymous reviewer for their valuable comments on this article and for their helpful feedback on the program code. Shin is grateful for partial support by the Social Sciences and Humanities Research Council of Canada (SSHRC-435-2021-0244).

References

- Berry et al. (1995) Berry, S., J. Levinsohn, and A. Pakes. 1995. Automobile prices in market equilibrium. Econometrica 63(4): 841–890.

- Donald and Newey (2001) Donald, S. G., and W. K. Newey. 2001. Choosing the number of instruments. Econometrica 69(5): 1161–1191.

- Kuersteiner and Okui (2010) Kuersteiner, G., and R. Okui. 2010. Constructing optimal instruments by first-stage prediction averaging. Econometrica 78(2): 697–718.

- Lee et al. (2022) Lee, S., Y. Liao, M. H. Seo, and Y. Shin. 2022. Fast and robust online inference with stochastic gradient descent via random scaling. In Proceedings of the AAAI Conference on Artificial Intelligence, vol. 36, 7381–7389.

- Lee and Shin (2021) Lee, S., and Y. Shin. 2021. Complete subset averaging with many instruments. The Econometrics Journal 24(2): 290–314.

About the authors

Seojeong Lee is an associate professor of Economics at Seoul National University

Siha Lee is an assistant professor of Economics at McMaster University

Julius Owusu is a doctoral candidate in Economics at McMaster University.

Youngki Shin is a professor of Economics at McMaster University