A Stochastic Contraction Mapping Theorem

Abstract.

In this paper we define contractive and nonexpansive properties for adapted stochastic processes which can be used to deduce limiting properties.

In general, nonexpansive processes possess finite limits while contractive processes converge to zero Extensions to multivariate processes are given. These properties may be used to model a number of important processes, including stochastic approximation and least-squares estimation of controlled linear models, with convergence properties derivable from a single theory. The approach has the advantage of not in general requiring analytical regularity properties such as continuity and differentiability.

Keywords. 93E20 Optimal stochastic control; 93E24 Least squares and related methods; 93E35 Stochastic learning and adaptive control

1 Introduction

Let be a sequence of random variables adapted to filtration . Following the Doob decomposition theorem we may always write

| (1.1) |

where are -measurable martingale differences, and defines a predictable process, in the sense that is -measurable. We let be any suitable -measurable initial value. We can think of as a control effector, and we will sometimes have for some sequence of deterministic mappings , . In this case, we can imagine setting in Equation (1.1), obtaining a deterministic iterative process. To fix ideas, suppose each has common fixed point and that there exists positive constants such that when . In a manner similar to the Banach fixed point theorem, it can be shown that if , then . We can refer to this as a contraction property, although we need not assume is formally a contraction mapping (or even Lipschitz continuous). If we restore to Equation (1.1), the question becomes how the additional stochastic variation affects the convergence properties.

In Almudevar (2008) (see also Almudevar (2014)) a general theorem for such noisy iterative algorithms was developed, for which is defined on any Banach space (not necessarily stochastic). For example, suppose operator possesses Lipschitz constant , and is the fixed point of each . In this case the “exact algorithm” , converges to . The “approximate algorithm” , , is then a noisy version of the exact algorithm. Then if , we may claim that , and if then converges to . In fact, the convergence rate of is bounded by for any (Almudevar, 2008, 2014).

The theory extends to nonexpansive operators (), especially “weakly contractive” sequences which satisfy , while, typically, the limit also holds. In this case, stronger convergence results are obtainable when is assumed to be additionally a Hilbert space (for example, adapted stochastic processes endowed with the norm).

In this paper, we extend some of these ideas to filtered stochastic processes, with strong convergence in place of convergence in a Banach space. We will characterize precisely contractive or nonexpansive properties based on the predictable process of Equation (1.1). These force to behave like a supermartingale above 0, and a submartingale below. If is a martingale of finite variation, it follows naturally that the process will possess a finite limit. However, if we then impose sufficient contractive properties, it can be shown that converges to 0

The main result is given in Section 2 for . We introduce the nonexpansive and contractive properties, then Theorem 2.1 summarizes the important limiting properties.

In Section 3 we consider the “nonuniform contractive” case, by which we mean that the nonexpansive or contractive properties required of Theorem 2.1 are now required to hold only outside a neighborhood of zero (Theorems 3.1 and 3.2).

In Section 4, Theorem 2.1 is extended to , , by replacing the constraint with , . It is then quite straightforward to apply Theorem 2.1 to (the conditions of which permit the process to be, for example, strictly positive). The argument is given in Theorem 4.1.

We include two important applications which can be modeled using the proposed theory. The Robbins-Monro stochastic approximation algorithm is a filtered stochastic process intended to converge to the solution to for a given mapping (Robbins and Monro, 1951). The univariate case will demonstrate the main theorem of Section 2. Extension to the nonuniform contractive model will significantly expand the class of to which stochastic approximation can be applied. The multivariate extension is then developed. This may be of some interest, since regularity conditions usually imposed on for are not needed by the methods introduced here (Spall, 1992; Pham et al., 2009; Lai, 2003; Kushner and Yin, 2003; Pham et al., 2009).

In Section 5 we consider the controlled least-squares regression model introduced in Christopeit and Helmes (1980). We can directly derive the same conditions for strong convergence, while also proving that they are also necessary. In general, we can prove that the least-squares estimator always possess a finite limit, hence weak convergence implies strong convergence.

Finally, we bring attention to a machine learning application proposed in Zhou and Hooker (2018), involving regularization of stochastic gradient boosted trees. This makes use of an earlier version of the methodology proposed here that appeared in an unpublished preprint written by this author. It demonstrates how the approach can be used to prove strong consistency where differentiability cannot be assumed.

Throughout the manuscript proofs and a number of technical lemmas are given in the appendix.

2 Main Result

Let be an stochastic process defined on probability space . Suppose there is a filtration defined defined by the -algebras to which X is adapted. Define residuals

| (2.1) |

and the partial sums for , with whenever . Then define the events

and the compound events , , . Define similarly , , and . We may then construct the increasing sequence of stopping times

for . Then may be interpreted as the times at which sequence X changes sign, changes from zero to a nonzero value or changes from a nonzero value to zero. We can refer to any such event as a crossing. Note that may be infinite, so it will be useful to define Then let

for . We will make use throughout the paper of the following sequence:

| (2.2) |

Our model will be based on the following assumptions:

-

(A1)

There exist nonnegative constants , , such that

and .

-

(A2)

There exist nonnegative constants , , such that

and (equivalently, for all ).

-

(A3)

-

(A4)

The partial sums possess a finite limit as .

Assumption (A1) is analogous to a nonexpansive condition on , and is related to the “almost martingale” introduced in Robbins and Siegmund (1971). Assumption (A2) is the stronger, or contractive, version of (A1). The central result of this section is that under assumptions (A3) and (A4) the process defined by (A1) converges to a finite limit, while that defined by (A2) converges to 0.

In some applications, (A3) will be a natural extension of (A1) or (A2) to the case . That is, we may be able to claim for and for . In this case (A3) holds trivially. However, we find that our theory can be extended to a broader class of interesting models by permitting somewhat more flexibility when conditioning on . Finally, since is a martingale, conditions under which (A4) holds are well known. For example, if is an martingale, by Theorem 4.5.2 of Durrett (2019), we may claim

| (2.3) |

We are now give the main results. We first consider the nonexpansive model. Given (A1), (A3) and (A4) we may claim that X possesses a finite limit. When (A2) holds as well we have convergence to zero. It will be useful, however, to consider the case for which (A3) need not hold. The results are essentially partitioned into the cases and , since the analysis differs between these cases in some important ways. For example, on the nonexpansive property (A1) is sufficient for convergence to zero.

Theorem 2.1.

Suppose X satisfies (A1) and (A4). Then the following statements hold.

-

(i)

possesses a finite limit as .

-

(ii)

If in addition (A2) holds then converges to zero

-

(iii)

The inequality holds

-

(iv)

If in addition (A3) holds, then

2.1 The Strong Law of Large Numbers as a Contractive Process

We now discuss the relationship between Theorem 2.1 and the strong law of large numbers. We suppose that there is an sequence of random variables on a probability space such that , , is a martingale with respect to some filtration .

Suppose is a nondecreasing sequence of positive real numbers such that . Then for any ,

| (2.4) |

We are interested in conditions under which We first note that, following Equation (2.4), the sequence satisfies assumption (A2), since

Then (A3) holds since The residual becomes Direct application of Theorem 2.1 gives

Theorem 2.2.

Let be an martingale with respect to filtration . If , and if is a convergent series then

But this is simply a restatement of Kronecker’s lemma, which states that if then for any sequence of real numbers the convergence of the series implies .

2.2 Stochastic Approximation

The stochastic approximation algorithm is a method used to determine the solution to

| (2.5) |

where mapping can only be evaluated with noise. In Robbins and Monro (1951) the iterative algorithm

| (2.6) |

was proposed, giving conditions under which converges in to . Here, is a sequence of positive constants, and the sequence is adapted to filtration and constructed so that .

Strong convergence has been since been established under a variety of conditions (Blum, 1954; Robbins and Siegmund, 1971; Ljung, 1978; Lai, 2003; Kushner and Yin, 2003; Benveniste et al., 2012). Our first task with respect to stochastic approximation will be to show how it may be interpreted as a stochastic contraction process.

Given a sequence X constructed by the iterations of Equation (2.6) we define the following assumptions.

-

(B1)

The mapping , possesses root .

-

(B2)

for all .

-

(B3)

There exists such that for all .

-

(B4)

, .

-

(B5)

The series converges

-

(B6)

.

-

(B7)

for .

Assumption (B1) does not require that be in the interior of . Nor does it state that the root is unique, but this is forced by (B3). Then, if finite nonzero left and right derivatives of exist at , (B3) will hold on some open neighborhood of , if not the entire domain of .

It should be noted that, following Equation (2.3), if the variance of conditional on is bounded, then (B5) may be replaced by , which, with (B6), are the conditions on the sequence commonly given in the literature

We now state the main theorem of this section.

Theorem 2.3.

If (B1)-(B7) hold then the process X defined by Equation (2.6) converges to

It is interesting to note that the stochastic approximation algorithm will converge if can be perfectly evaluated (in contrast with simulated annealing, which relies on stochastic variation for convergence). In this case Equation (2.6) becomes

where is a sequence of operators with Lipschitz constant for all large enough . Given (B6) we have , so that although the Lipschitz constants are not bounded away from one, they approach one from below slowly enough to allow contraction to force convergence. Two conditions on are commonly associated with stochastic approximation, in particular, (a) ; and (b) . As can be seen, condition (a) forces sufficient contraction to ensure convergence for the noiseless algorithm, while condition (b) ensures that the cumulative effect of noise vanishes in the limit (as a consequence of contraction property). For more on this point of view, see Almudevar (2008, 2014).

3 Nonuniform Contractions

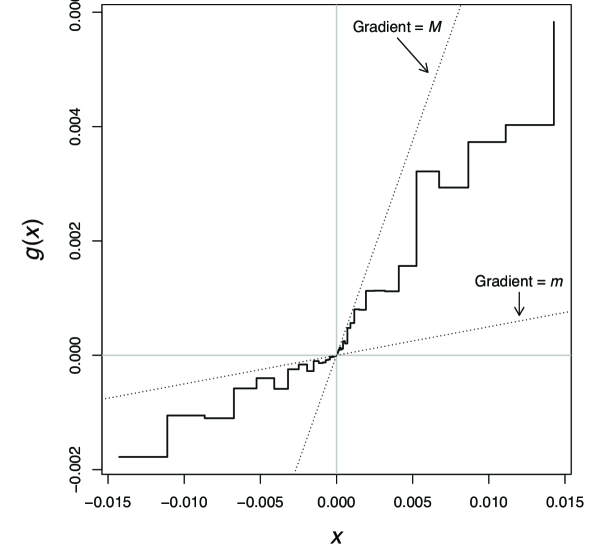

Figure 1(a) demonstrates that the conditions imposed on by Theorem 2.3 are quite general. Essentially, must be contained within a Lipschitz envelope, but otherwise need not be monotone or continuous (for convenience we will assume ).

However, a variety of conditions on have been derived in the literature. In the seminal paper Robbins and Monro (1951), alternative conditions for convergence are given, in particular, for and for , for some (Theorem 1); and , is nondecreasing and (Theorem 2). In Blum (1954), the following regularity conditions are offered:

-

(C1)

for some constants ;

-

(C2)

for and for ;

-

(C3)

for every pair of numbers for which .

While conditions (C1)-(C3) are considerably weaker than the envelope bound of Figure 1(a), they can be usefully compared. If (C1) holds, then some Lipschitz upper bound (Figure 1(a)) holds for . Then, with (C2), we can show that (A1) will hold outside a neighborhood of the origin. Then if (C3) holds we may show that (A2) holds for , for any positive constants . In this case, it will be possible to show, first, that X will be bounded in the limit. In this case, (A2) need only hold for a bounded subset of , and we will be able to show that X approaches , essentially “fattening” the origin. If the neighborhood can then be made arbitrarily small, we obtain strong convergence.

Thus, we can say that, in the context of stochastic approximation, (C1)-(C3) define models that are contractive outside any neighborhood of the origin, hence it seems reasonable to refer to such a model as “nonuniformly contractive”. Below, we formally define such a model. We again define an adapted sequence X, on which we may, as an alternative to (A1)-(A4), impose the following assumptions.

-

(D1)

For (A1) holds for

-

(D2)

For (A2) holds for

-

(D3)

implies

-

(D4)

For all , (D3) holds for constants which satisfy the limit .

The key to the argument is to consider the process derived from X:

| (3.1) |

for given (it will prove to be more intuitive to introduce and separately in our notation). We denote this process . We may define the residuals in the same manner as in Equation (2.1):

| (3.2) |

Finally, following Equation (2.2) we may condition the process on :

| (3.3) |

We briefly outline the remaining strategy. Suppose we can assume that , where are the residuals of the original process X. This will be the case under (A4). Then under (D1), there exists a finite integer such that satisfies (A1) for all . Accordingly, we define the offset process , so we may claim that satisfies (A1). The remaining argument is of the same style, that is, by assuming the various conditions (D1)-(D4) hold for X, we may verify that the corresponding properties (A1)-(A4) hold for . Then the convergence properties of X follow from those of . The first theorem follows.

Theorem 3.1.

Suppose Suppose (D1) holds for some . Consider the derived process of Equation (3.1). Then

-

(i)

For all small enough , there exists finite such that satisfies (A1) for all .

-

(ii)

If in addition, X satisfies (D2) for , then satisfies (A2) whenever .

-

(iii)

If in addition (D3) holds, then

(3.4) -

(iv)

If (A4) holds for X, then it also holds for .

Theorem 3.1 allows us to deduce some convergence properties of . If (D1) and (A4) hold for X then (A1) and (A4) hold for . As a consequence, by Theorem 2.1 either converges to a finite limit, or The final step is to deduce the implications of this for the limit of X itself.

Theorem 3.2.

Suppose X satisfies (D1) for all , and in addition (D4), (A3) and (A4). Then X possesses a finite limit If in addition X satisfies (D2) for all pairs then X converges to zero

3.1 Stochastic Approximation and Nonuniform Contraction

We continue our discussion of stochastic approximation. Consider assumptions (B1)-(B7) (as before, assuming ). Then replace assumption (B3), which is placed on , with (C1)-(C3). Fix any . By (C1) . With (C2) we may conclude

Since we have, for all large enough , following Equation (A.9),

so that assumption (D1) will be satisfied. Thus, (C1)-(C2) force the nonexpansive property.

To verify (D4), note that by (C1)-(C2) for for all large enough . Thus, (D4) holds by setting .

We next show that (C3) forces the contractive property. Fix . Define the quantity

Given (C2), under (C3) , so that, for all large enough ,

Following the proof of Theorem 2.3, we may then conclude that (D2) holds for all finite pairs . Thus, by Theorem 3.2, the stochastic approximation algorithm will converge when (B3) is replaced by (C1)-(C3).

4 Multivariate Processes

We now extend Theorem 2.1 to processes in p, replacing the ratio in (A1) and (A2) with the absolute value of the ratio. Suppose is stochastic process adapted to filtration . The residual vector is , . Then , so that as before , form vectors of martingale differences. Denote the components of and by and , . Consider the following assumptions, which may be taken as multivariate extensions of (A1)-(A4) (here, is the Euclidean norm).

-

(A5)

There exist nonnegative constants , , such that

and .

-

(A6)

There exists positive constants , , such that

and (equivalently, for all ).

-

(A7)

-

(A8)

There exists a sequence of constants , such that and for all .

Assumptions (A5) and (A6) are strict generalizations of (A1) and (A2) even for , since the contraction implied by is no longer required to be of the same sign as . Assumptions (A7)-(A8) are directly comparable to (A3)-(A4), respectively.

The strategy will be to apply Theorem 2.1 directly to , .

Theorem 4.1.

Suppose is an process in p, which is adapted to filtration .

-

(i)

If (A5), (A7), (A8) hold then exists and is finite

-

(ii)

If (A6), (A7), (A8) hold then

4.1 Multivariate Stochastic Approximation

In this section we extend the stochastic approximation algorithm to the multivariate case. In particular, we consider the problem of determining the solution to to where is only observable with noise. The extension to has been widely considered in the literature (Ljung, 1978; Spall, 1992; Lai, 2003; Kushner and Yin, 2003). Regularity conditions usually impose differentiability assumptions on , although in Section 2.2 and Section 3.1 it can be seen that such conditions play little role for the univariate case. We show in this section how Theorem 4.1 can be used to extend this nonsmooth case to p (we do not consider here the nonuniform contractive model, although presumably it would also apply to this application).

We keep more or less intact conditions (B1)-(B7), with (B3) becoming a type of positive definiteness assumption on . Assuming , the algorithm retains form

| (4.1) |

here interpreted as a multivariate process, where , and is a positive constant. Again, , , is adapted to some filtration . We replace (B1)-(B7) with the following assumptions (some are identical to the corresponding assumption in (B1)-(B7), but are included for convenience).

-

(B1a)

The mapping , , possesses root .

-

(B2a)

for all .

-

(B3a)

There exists such that satisfies

for all , where is the inner product on p.

-

(B4a)

, .

-

(B5a)

for all .

-

(B6a)

.

-

(B7a)

for .

Under these conditions the multivariate stochastic approximation algorithm remains strongly convergent.

Theorem 4.2.

If (B1a)-(B7a) hold then the process , , defined by Equation (4.1) converges to

5 Least Squares Regression and Control

We consider the example of multivariate linear regression, possibly controlled. We are given probability measure space on which is a filtration. Suppose is a sequence of random vectors, where is -measurable. Let be the matrix with th row equal to . Suppose is a sequence of zero mean random variables. Define vector . We assume is -measurable, and defines a sequence of martingale differences, that is, , . Let be a fixed vector. Define , and . Then consider the nested sequence of linear models

| (5.1) |

If contains linearly independent rows, does as well for any . It will therefore be reasonable to assume that there exists finite such that is nonsingular for .

The ordinary least squares estimate of based on the th model is well known to be . We then center the estimates by setting . The consistency problem involves finding conditions on the sequences and under which converges strongly to zero.

In Drygas (1976) and Anderson and Taylor (1976), conditions are given for deterministic under which is necessary and sufficient for weak convergence of to zero. Here it is assumed that the maximum eigenvalue of the covariance matrix of remains bounded as . In Lai et al. (1979) it is shown that is sufficient for strong convergence, assuming that the series converges whenever .

Thus, under quite general conditions, for the deterministic case weak convergence implies strong convergence. Our purpose in this section is to extend the same general rule to the control model. A commonly used approach is to, in essence, turn into a scalar by provisionally replacing it with a diagonal matrix , the assumption then being that is uniformly bounded over . In Anderson and Taylor (1979), this is accomplished by assuming that the eigenvalue ratio is uniformly bounded over , hence the sequence of matrices is similarly bounded. A more general condition is used in Christopeit and Helmes (1980), by assuming is uniformly bounded over , where for some function . Here we will use this model. Under regularity conditions to be given below, it is verified in Christopeit and Helmes (1980) that is sufficient for strong consistency. We will also add to this result by allowing for and for . Possibly, , in which case we will have strong consistency. Otherwise we have intermediate cases. We show that always possesses a finite limit for any . Indeed, the component is strongly consistent for when . On the other hand, if , and we define subvector , then . This means that is also necessary for strong consistency.

Interestingly, although Equation (5.1) defines a multivariate process, the main analysis will consider univariate processes, so we make use of Theorem 2.1. Conditions (E1)-(E4) will define our model. Condition (E5) then suffices for strong consistency, but, as already discussed, we will also consider intermediate cases.

-

(E1)

is a sequence of martingale differences adapted to .

-

(E2)

for some .

-

(E3)

There exists finite such that is nonsingular.

-

(E4)

is uniformly bounded over , where is a nondecreasing function satisfying for some .

-

(E5)

for .

Note that (E4) implies .

We may write , where

However, at this point we replace with , and define the process

If necessary, set . Since is -measurable we have

Fix and consider the component process . If , then , and hence . Therefore (A3) holds for . The ratio of assumption (A1) is given by

Suppose (E4) holds. Then is nonnegative and nondecreasing in and is nondecreasing in , so we may conclude that , and therefore (A1) holds for . If , then . It follows from Equation (2.4) that (A2) also holds.

Since is -measurable, we have residual vector

This gives

| (5.2) |

By Lemma D.1 we may conclude that , so that (A4) holds, following Equation (2.3). Thus, by Theorem 2.1, converges to a finite limit, and if , converges to zero

The convergence properties of follow directly, by writing

| (5.3) |

Then, by (E4), is bounded uniformly as , so we have just proven that (E5) is sufficient for strong consistency, as reported in Christopeit and Helmes (1980).

If we then more precisely characterize properties of implied by (E4) we can deduce convergence properties for intermediate cases, and show that (E5) is also necessary for strong consistency.

Theorem 5.1.

Suppose the regression model of Equation (5.1) satisfies (E1)-(E4). Then the following statements hold:

-

(i)

The least-squares estimator possesses a finite limit

-

(ii)

If , then is a strongly consistent estimator of .

-

(iii)

is a strongly consistent estimator of if and only if (E5) holds.

References

- Almudevar (2008) Almudevar, A. (2008). Approximate fixed point iteration with an application to infinite horizon markov decision processes. SIAM Journal on Control and Optimization, 47(5), 2303–2347.

- Almudevar (2014) Almudevar, A. (2014). Approximate Iterative Algorithms. CRC Press.

- Anderson and Taylor (1979) Anderson, T. and Taylor, J. B. (1979). Strong consistency of least squares estimates in dynamic models. The Annals of Statistics, 7(3), 484–489.

- Anderson and Taylor (1976) Anderson, T. W. and Taylor, J. B. (1976). Strong consistency of least squares estimates in normal linear regression. The Annals of Statistics, 4(4), 788 – 790.

- Benveniste et al. (2012) Benveniste, A., Métivier, M., and Priouret, P. (2012). Adaptive Algorithms and Stochastic Approximations, volume 22. Springer Science & Business Media.

- Blum (1954) Blum, J. R. (1954). Approximation methods which converge with probability one. The Annals of Mathematical Statistics, 25(2), 382 – 386.

- Christopeit and Helmes (1980) Christopeit, N. and Helmes, K. (1980). Strong consistency of least squares estimators in linear regression models. The Annals of Statistics, 8(4), 778 – 788.

- Drygas (1976) Drygas, H. (1976). Weak and strong consistency of the least squares estimators in regression models. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 34(2), 119–127.

- Durrett (2019) Durrett, R. (2019). Probability: Theory and Examples. Cambridge University Press.

- Horn and Johnson (2012) Horn, R. A. and Johnson, C. R. (2012). Matrix Analysis. Cambridge University Press.

- Kushner and Yin (2003) Kushner, H. and Yin, G. (2003). Stochastic Approximation and Recursive Algorithms, volume 35. Springer-Verlag NY.

- Lai (2003) Lai, T. L. (2003). Stochastic approximation. The Annals of Statistics, 31(2), 391–406.

- Lai et al. (1979) Lai, T. L., Robbins, H., and Wei, C. Z. (1979). Strong consistency of least squares estimates in multiple regression II. Journal of Multivariate Analysis, 9(3), 343–361.

- Ljung (1978) Ljung, L. (1978). Strong convergence of a stochastic approximation algorithm. The Annals of Statistics, 6(3), 680–696.

- Pham et al. (2009) Pham, Q.-C., Tabareau, N., and Slotine, J.-J. (2009). A contraction theory approach to stochastic incremental stability. IEEE Transactions on Automatic Control, 54(4), 816–820.

- Robbins and Monro (1951) Robbins, H. and Monro, S. (1951). A stochastic approximation method. The Annals of Mathematical Statistics, 22(3), 400 – 407.

- Robbins and Siegmund (1971) Robbins, H. and Siegmund, D. (1971). A convergence theorem for non negative almost supermartingales and some applications. In J. S. Rustagi, editor, Optimizing Methods in Statistics, pages 233–257. Elsevier.

- Spall (1992) Spall, J. C. (1992). Multivariate stochastic approximation using a simultaneous perturbation gradient approximation. IEEE Transactions on Automatic Control, 37(3), 332–341.

- Taylor (1974) Taylor, J. B. (1974). Asymptotic properties of multiperiod control rules in the linear regression model. International Economic Review, 15(2), 472–484.

- Zhou and Hooker (2018) Zhou, Y. and Hooker, G. (2018). Boulevard: Regularized stochastic gradient boosted trees and their limiting distribution. Preprint https://arxiv.org/abs/1806.09762.

Appendix Appendix A Proof of Theorem 2.1, with Technical Lemmas

Lemma A.1.

If (A1) holds then for any

Proof.

We have by (A1), which completes the proof. ∎

The following lemma allows us to bound the process X in terms of the partial sums of the form . Define the kernel , , , and . Under (A1), . Then set .

The lemma also relies on the following device. Let be the extended integers. For any define .

Lemma A.2.

If (A1) holds then for

Proof.

Fix integers where is finite but, possibly, . For now, assume , and select , . Then

| (A.2) |

after applying (A1). Applying Equation (A.2) iteratively gives

| (A.3) |

Note that Equation (A.3) holds also for , using the standard summation convention, so we now permit . With Lemma A.1 this leads to

| (A.4) |

for . It follows from (A.4) that

| (A.5) |

Then on we have . This gives

| (A.6) | ||||

Summing Equation (A.6) over and yields

Then note that assumption (A1) also applies to , hence we may similarly conclude

Also, by construction we have for so that we may conclude

completing the proof. ∎

We are now in a position to prove the main results. We first consider the nonexpansive model. Given (A1), (A3) and (A4) we may claim that X possesses a finite limit. It will be useful, however, to consider the case for which (A3) need not hold.

Appendix A.1 Proof of Theorem 2.1

Proof.

We first consider Statement (i), that is, the case . Fix , and define stopping time

Then construct the sequence

then

Following Lemma A.1 we have for all .

Then for all and when for all , noting that we may have . This leads to

By assumption and , so that the almost martingale conditions of Theorem 1 of Robbins and Siegmund (1971) hold. We may then conclude that possesses a finite limit . This in turn implies that possesses a finite limit.

We next consider Statement (ii). Since (A2) implies (A1), the conclusions of Statement (i) hold. By assumption (A2), for ,

| (A.7) |

If does not converge to 0 then there exists such that for large enough , a.e. on when . Applying Equation (A.7) gives

But following the proof of Statement (i) must possess a finite limit, hence must converge to 0 on . The remaining proof is essentially the same as for Statement (i).

We next consider Statement (iii), the case . Since has a limit a.e., by the Cauchy criterion as . which implies

since for all , and . Statement (iii) follows by applying Lemma A.2. Given (A3), Statement (iv) follows from a direct application of Statement (ii). ∎

Appendix A.2 Proof of Theorem 2.3

Proof.

Assumption (B2) ensures that the process (2.6) is always defined. By (B4), , so we may assume without loss of generality that for all . Subtracting from both sides of (2.6) gives the equivalent process

| (A.8) |

with initial value . We then apply Theorem 2.1 to the process (A.8). Accordingly, by (B7), we have

Since we have so that (A3) holds. Then by (B3)

| (A.9) |

which gives

| (A.10) |

Then note that and . Also, (B6) implies so that (A2) holds. Then (B5) is equivalent to (A4), so that by Theorem 2.1. ∎

Appendix Appendix B Proofs of Theorems 3.1 and 3.2

Appendix B.1 Proof of Theorem 3.1

Proof.

Let be the filtration for the process . For any there exists finite such that for all . Select , then consider the offset process , . Suppose . Since and we must have . By (D1) we have . We may then write

A similar argument holds for the case , hence it follows that (A1) holds for , .

The proof of Statement (ii) is similar to that of Statement (i).

To prove Statement (iii), suppose . First consider the case . We may write

| (B.1) |

where . Otherwise, suppose but . We must then have . Suppose . Then by (A1) . Hence, for this case

| (B.2) |

Finally, suppose . By (D3) , hence

| (B.3) |

Then Equation (3.4) follows from Equations (B.1), (B.2) and (B.3).

We finally consider Statement (iv). Assume (A4) holds for . Then for the residuals are given by

Thus, , hence (A4) extends to . ∎

Appendix B.2 Proof of Theorem 3.2

Proof.

For the first (nonexpansive) case, we may conclude by Theorem 3.1 that there exists finite such that satisfies (A1) and (A4) for all small enough . We then note that

| (B.4) |

Applying (D4) and (A3) we conclude by Theorem 3.1 (iii) that . That X possesses a finite limit follows by applying Theorem 2.1 to , allowing to approach zero, and noting Equation (B.4).

For the contractive case, note that under the given assumptions may be bounded by some finite constant . If (D2) holds for all pairs then it follows from Theorem 3.1 (ii) that (A2) holds for , which therefore satisfies the hypothesis of Theorem 2.1 (ii). The remaining argument follows that of the nonexpansive case. ∎

Appendix Appendix C Proofs of Theorems 4.1 and 4.2

Appendix C.1 Proof of Theorem 4.1

Proof.

Conditions (A5), (A6) and (A7) directly imply conditions (A1), (A2) and (A3) for . It remains to verify that (A8) implies (A4) for . We have residual process

Then

| (C.1) |

However, Euclidean norm is convex, so by Jensen’s inequality we have which, when combined with Equation (C.1), gives

| (C.2) |

which, with (A8), implies that satisfies (A4). The proof is completed by a direct application of Theorem 2.1. ∎

Appendix C.2 Proof of Theorem 4.2

Proof.

The main task is to verify condition (A6) for all large enough . By construction we have so that, by (B3a),

It follows that

Since , we must have for all large enough . Suppose we have function . It is easily verified that , and that is convex for . Furthermore, there exists finite and finite index such that for all we have . We then have so that (A6) holds. That (A7) and (A8) hold follow from arguments similar to those of Theorem 4.2. The theorem is then proved following an application of Theorem 4.1 (ii). ∎

Appendix Appendix D Proof of Theorem 5.1 with Technical Lemmas

The following lemma is a generalization of Lemma 1 of Taylor (1974), which states that for any sequence of real numbers with we must have for all . A recursive argument is used in Taylor (1974), but we may also interpret as an approximation of the integral . Doing so will allow us to expand the class of models to be studied.

Lemma D.1.

Let be a sequence of nonnegative real numbers, not uniformly equal to zero. Assume (otherwise delete from the sequence). Let Suppose we are given a nondecreasing function for which for any . Then

| (D.1) |

for all .

Proof.

Let . Construct a step function on with discontinuities at , . Set the left limit of at to be . If set for . Then

Equation (D.1) follows from the fact that for . ∎

Appendix D.1 Proof of Theorem 5.1

For we have norm . Then let C be a matrix with elements . We will make use of the matrix norm . Note that is a true matrix norm, in particular, Horn and Johnson (2012).

Proof.

Suppose for model (5.1) conditions (E1)-(E4) hold. Then assume for some index , we have for and for . Set , and let be the elements of . By (E4) we have for all for some finite . It follows that

Thus, for we must have , and, since is symmetric, for as well. Then consider the matrix partitions

where , are square matrices. We then have

| (D.2) |

where is the identity matrix. Under our given assumptions, the finite limit exists and is positive definite. Let and let be the elements of . Then (noting that )

| (D.3) |

By assumption for . Furthermore, if (E4) holds we must have , where . By assumption for , so by Equation (D.3) it follows that . After applying Equation (D.2) we have .

We then have . Define the partition , where contains the first elements of . For it is easily verified that is a finite variance martingale, and hence possesses limit with . It follows that . Suppose . We then have the limit

noting that the elements of vanish as . Since is nonsingular, implies , so that . Next, we evaluate

However, in Section 5 it was shown that the components of index of converge to zero Since is uniformly bounded over , it follows that We then have, , the finite limit

| (D.4) |

Equation (D.4) can clearly be extended to the case , in which case the finite limit exists This is true also for condition (E5) (that is, ), in which case Hence, always possesses a finite limit, and that limit is zero if and only if . Otherwise converges to if . ∎