Optimal Estimation of Generic Dynamics by Path-Dependent Neural Jump ODEs

Abstract

This paper studies the problem of forecasting general stochastic processes using a path-dependent extension of the Neural Jump ODE (NJ-ODE) framework (Herrera et al., 2021). While NJ-ODE was the first framework to establish convergence guarantees for the prediction of irregularly observed time series, these results were limited to data stemming from Itô-diffusions with complete observations, in particular Markov processes, where all coordinates are observed simultaneously. In this work, we generalise these results to generic, possibly non-Markovian or discontinuous, stochastic processes with incomplete observations, by utilising the reconstruction properties of the signature transform. These theoretical results are supported by empirical studies, where it is shown that the path-dependent NJ-ODE outperforms the original NJ-ODE framework in the case of non-Markovian data. Moreover, we show that PD-NJ-ODE can be applied successfully to classical stochastic filtering problems and to limit order book (LOB) data.

1 Introduction

The processing and prediction of time series data is of great importance in many data-driven fields such as economics, finance, and medicine. In recent years a lot of progress was made improving the machine learning techniques and, in particular, the neural network based ones, to be able to deal with more complicated problem settings. Recurrent Neural networks (RNNs) constituted the starting point to deal with discrete time series of variable and possibly unbounded length. Their main constraint is the underlying assumption that observations occur in regular time steps. A first step in the direction of irregular observation times was made by defining the RNN’s latent variable continuously in time with some time-decay (e.g. exponential) directed to (Che et al., 2018; Cao et al., 2018). However, since this is a rather stiff framework, neural ODEs (Chen et al., 2018) set a new milestone by making the continuously-in-time defined latent dynamics trainable through a neural network. Finally, combining this trainable continuous-in-time latent framework with an RNN cell, led to a framework for irregularly sampled time series data (Rubanova et al., 2019; Brouwer et al., 2019).

In machine learning applications to time series data, we distinguish between two different problem settings. Firstly, the labelling problem, where the entire time series is processed with the goal to determine a class or value describing some feature of this time series. An example would be a time series consisting of health parameters of a hospital patient with the aim of predicting whether the patient will develop a certain disease within the next days. And secondly, the forecasting problem where the goal is to process the known past values of the time series to predict how it will develop in the future. If this is done such that the entire time series of a predefined length is processed and certain time points in the future are predicted, then this can be viewed as a special case of the labelling problem (with a possibly infinite dimensional output). Here, we will refer to this as offline forecasting. On the other hand, if the goal is to forecast continuously in time, where for every time point a prediction can be made depending only on the past observations, this is a different problem, which we refer to as online forecasting. Here, the algorithm has to dynamically predict based on the known past observations as long as no new information is available and then processes new observations (and adjust itself accordingly), whenever they become available. Coming back to our previous example, this would mean to continuously in time forecast how the health parameters will evolve, given those observations which were made up to the current time. In this work, which is the second part and generalisation of the Neural Jump ODE (NJ-ODE) framework (Herrera et al., 2021), we consider precisely this problem. In particular, our goal is to make optimal forecasts, where optimality in this work is meant in terms of the -norm.

While NJ-ODE was the first framework in which theoretical convergence guarantees of the model output to the optimal prediction were derived, relatively restrictive assumptions on the underlying dynamics of the time series data were needed. In particular, the data has to stem from an Itô diffusion with several constraints on its drift and diffusion. This implies that paths of the dataset are continuous and Markovian (no path-dependence). Moreover, it is necessary that observations are complete, i.e., that all coordinates are observed simultaneously at each observation time. In the present work, we extend the NJ-ODE such that it can be applied to a very general set of stochastic processes that satisfy only weak regularity conditions. Since some of these constraints might seem a bit abstract at first, we provide several examples for which we prove that the assumptions are satisfied. Some examples are processes with jumps, fractional Brownian motion (rough paths with path-dependence) and multidimensional correlated processes with incomplete observations. Moreover, we show how the NJ-ODE framework can be used to perform not only prediction but also uncertainty estimation and how it can be applied to the stochastic filtering problem. Our theoretical results are based on the universal approximation property of neural networks and the signature transform.

1.1 Related Work

Recurrent neural networks (Rumelhart et al., 1985; Jordan, 1997) and the neural ODE (Chen et al., 2018) are the two main ingredients for the (path-dependent) NJ-ODE model. The first works in which they were combined to a model similar to the one we use were Rubanova et al. (2019); Brouwer et al. (2019). In contrast to our framework, the latent ODE (Rubanova et al., 2019) is a model for the offline forecasting problem, where an encoder-decoder type model is used. First, the ODE-RNN encoder processes the entire time series of observations to generate an initial latent variable, which is then used as starting point for a neural ODE that produces the forecasts. In comparison to that, GRU-ODE-Bayes (Brouwer et al., 2019) uses the same model framework as we do for online forecasting. The main difference to NJ-ODE lies in the objective function and training framework. In particular, no convergence guarantees exist for GRU-ODE-Bayes, as was discussed in detail in Herrera et al. (2021).

Being the predecessor, NJ-ODE (Herrera et al., 2021) clearly is the most related work to the present one. While the main structure of the model and of the theoretical results is the same, we make many important changes to extend the theory from a class of Itô processes to a large class of generic stochastic processes. A major ingredient to do this is the signature transform (Chevyrev & Kormilitzin, 2016; Kiraly & Oberhauser, 2019; Fermanian, 2020), which allows us to approximate path dependent behaviours.

The most related work in the context of the labelling problem, besides Rubanova et al. (2019), is the neural controlled differential equation (NCDE) (Kidger et al., 2020). Similar to neural ODEs, it integrates a neural network, however, not against time but against the linear or spline interpolation of the observed time series. The NCDE can only be used for the labelling problem (including offline forecasting), but not for the online forecasting problem, since its interpolation of the observations depends on future data (cf. Morrill et al. (2022)). Hence, in general its output at an intermediate time is not measurable with respect to the information available at this time. In Morrill et al. (2022), the NCDE was extended by using the rectilinear (instead of linear or spline) interpolation of the data to circumvent this problem and make it applicable to online forecasting tasks. Nevertheless, the authors did not apply it to the type of online prediction tasks we are most interested in, where the value of a stochastic process should be predicted based on previous discrete observations of this process, but only to labelling problems (making the comment that these labelling problems can now be addressed in an online manner). In line with this, no convergence guarantees are provided for such problems.

Neural rough differential equations (NRDE) (Morrill et al., 2021) are yet another extension of NCDEs, where a neural network is piece-wisely integrated on intervals against time and multiplied with the depth- log-signature transform computed over the respective interval. The advantage of this method over NCDEs is that the intervals can be chosen larger than the intervals between consecutive observation times, since the log-signature can compress the path information on the entire interval. In particular, no information is lost, while this is the case when increasing the step size of the NCDE model, which corresponds to sub-sampling of the data. Therefore, NRDEs are well suited for labelling problems on long time series (by choosing larger integration intervals), where NCDEs experience worsening accuracy and prohibitively long training times. However, similar to the original NCDE model, the NRDE method is not suitable for online forecasting, since in general its output at an intermediate time is not measurable with respect to the information available at this time.

While all of the previously discussed frameworks are prediction models that are deterministic once they are trained, neural stochastic differential equations (NSDEs) (Tzen & Raginsky, 2019; Li et al., 2020) are rather generative models with a standardized stochastic input generating stochastic output. In particular, NSDEs produce sample paths of a stochastic process, which can be useful when either stochastic samples are needed or if the generation of samples is easier than the computation of the distribution of the process. However, usually the training of generative models is more complicated than the training of prediction models. In particular, NSDEs can be interpreted as (infinite-dimensional) GANs (Kidger et al., 2021), for which it is well known that they are difficult to train (vanishing gradients, mode collapse and failure to converge being the most common problems) (Saxena & Cao, 2021). Monte Carlo techniques can be used to apply NSDEs when the main interest is the distribution of the underlying process. The disadvantage of this approach is the comparably large computation time due to the need of a large amount of independent samples of the NSDE to get reasonably small Monte Carlo errors. In contrast to this, we explain in Section 5 how the NJ-ODE framework can be used for a more direct way (without sampling) to predict the conditional distribution.

1.2 Outline of the Work

First we establish the problem setting in Section 2, where we outline which information is available to learn from and what assumptions are needed. Moreover, we show that the theoretically optimal solution (cf. Section 2.4) to the online forecasting problem, which we aim to approximate, is given by the conditional expectation process (cf. Section 2.3). In Section 3, we introduce our model as a signature based extension of NJ-ODE (Herrera et al., 2021) for which we prove in Section 4 that it converges to the theoretically optimal solution. This proof is based on the respective proof for the NJ-ODE model. In Section 5 we explain how to bridge from learning only the conditional expectation to approximating the conditional distribution, using the same framework. We continue by explaining how our model can be applied to the stochastic filtering problem in Section 6.

Although the needed assumptions formulated in Section 2.3 are weak, they are a bit technical and might seem hard to be verified in concrete problems. Therefore, we provide several examples of processes for which we prove that they satisfy these assumptions in Section 7. In particular we show that the setting used in Herrera et al. (2021) is a special case that satisfies our assumptions here, justifying that we speak of a generalisation of Herrera et al. (2021). In Section 8, we provide empirical evidence that our model works well, with experiments performed on synthetic datasets based on some of the examples of Section 7 as well as experiments on real world datasets. Additional details are given in the Appendix.

2 Problem Setting

We assume to have a dataset of time series samples which are irregular, possibly incomplete, discrete-time observations of a continuous-time stochastic process, where the observation times and the observed coordinates are random. Importantly, we do not assume to have any knowledge about the underlying stochastic process or the observation times and masks, except for the data we observe and that they satisfy the assumptions formulated in Section 2.3. In particular, we do not assume to know the distribution of the stochastic process or the distribution of the observation times and masks. The goal is to use the given data to train a model such that it approximates the optimal solution of the online forecasting problem (cf. Section 1), which is shown to be given by the conditional expectation process (cf. Section 2.4). In the following we give precise definitions together with the needed assumptions to establish our theoretical guarantees, following the descriptions in Herrera et al. (2021).

2.1 Stochastic Process, Random Observation Times and Observation Mask

Let be the dimension and be the fixed time horizon. Consider a filtered probability space , on which an adapted càdlàg stochastic process111A stochastic process is a collection of random variables for . taking values in is defined. We define the running maximum process

where denotes the standard -norm for vectors. Moreover, let be the random set of discontinuity times of , defined for every as . Here, is the jump of the process at time , where denotes the left limit of at time (or equivalently, the value of the left-continuous version of at time ).

We consider another filtered probability space , on which the random observation framework of the stochastic process is defined. In particular, we define the following objects.

-

•

, an -measurable random variable, is the random number of observations.

-

•

is the maximal value of .

-

•

for are the sorted222For all , . stopping times333In particular, is a random variable s.t. for all and ., describing the random observation times, with if and only if .

-

•

is the time of the last observation before a certain time .

-

•

is the observation mask, which is a sequence of random variables on taking values in such that is -measurable. The -th coordinate of the -th element of the sequence , i.e., , signals whether , denoting the -th coordinate of the stochastic process at observation time is observed. In particular, means that it is observed, while means that it is not. By abuse of notation, we also write .

2.2 Information -algebra

is the filtered product probability space which, intuitively speaking, combines the randomness of the stochastic process with the randomness of the observations. Here, consists of the tensor-product -algebras for . On this probability space, we define the filtration of the currently available information by

where are the random observation times and denotes the generated -algebra. By the definition of we have for all . Moreover, we have for any fixed observation (stopping) time that the stopped and pre-stopped -algebras at are (Karandikar & Rao, 2018, Definitions 2.37 and 8.1)

2.3 Notation and Assumptions on the Stochastic Process

We denote the conditional expectation process of by , defined by and remark that in contrast to the setting in Herrera et al. (2021), in general, since observations are incomplete. Moreover, we define for any the process to be the interpolation of the observations of made until time . Its -th coordinate at time is given by

where

with the standard definition that the infimum of the empty set is and the additional definition that . A schematic representation of this interpolated observation path is given in Figure 1. In particular, is the rectilinear interpolation (sometimes denoted as forward-fill), except that its jumps at are replaced by linear interpolations between the previous observation time and . It is important to note that this is not solely a coordinate-wise interpolation, since the given coordinate might not have been observed at the previous observation time. In particular, in general. Moreover, by this definition, is -measurable for all , and for any and all we have . We denote the set of continuous -valued paths of bounded variation (cf. Definition 3.1) on by . By the definition of it is clear that its paths belong to .

Using and that carries all information available444More precisely, this is only true if the probability of any consecutive observations being equal is zero. If this is not the case, one can add coordinates to which describe the coordinate-wise amount of observations as paths that increases by , whenever a new observation is made for this coordinate. To get continuity of these paths, the same interpolation as for can be used. in , we know by the Doob-Dynkin Lemma (Taraldsen, 2018, Lemma 2) that there exist measurable functions such that . The following assumptions are central to establish our theoretical results. Examples where these assumptions are satisfied are given in Section 7.

Assumption 1.

For every , is independent of and of , and for all (every coordinate can be observed at any observation time and is completely observed at ) and for every -almost surely (at every observation time at least one coordinate is observed).

Assumption 2.

The probability that any two observation times are closer than converges to when does, i.e., if then .

Assumption 3.

Almost surely is not observed at a jump, i.e., for all .

Assumption 4.

are continuous and differentiable in their first coordinate such that their partial derivatives with respect to , denoted by , are again continuous and there exists a and such that for every the functions are polynomially bounded in , i.e.,

Assumption 5.

is -integrable, i.e., .

Assumption 6.

The random number of observations is integrable, i.e., .

Remark 2.1.

Assumption 2 is a technical condition that is needed to get compact subsets of . It is actually equivalent to , which is always satisfied when the observation times are strictly increasing.

Remark 2.2.

The Assumption that is observed completely, i.e., that , can be weakened (at least) in two possible ways.

-

1.

We assume instead that is not observed at all, i.e., .

-

2.

We assume instead that a fixed subset of coordinates is always observed at and the others not, i.e., .

In both cases, the definition of can easily be adjusted accordingly.

With Assumption 4 we can rewrite by the fundamental theorem of calculus as

implying that it is càdlàg. We remark that jumps of occur only at new observation times, i.e., at , for .

Remark 2.3.

In principle, the assumption that are continuous would be enough to use neural networks to approximate them. The reason why we make the stronger assumption that exist and are continuous is that by subsequently rewriting with the fundamental theorem of calculus, we can make use of additional domain knowledge which simplifies the learning task. For more details see Appendix E.

Remark 2.4.

The assumption that and are bounded by together with the assumption that is -integrable ensure that our loss function (defined later) is well defined and does not explode. In particular, they are crucial to show that the maximal distance between and our model’s approximation of it is integrable, which is needed to prove convergence of our method.

2.4 Optimal Approximation

As in Herrera et al. (2021), we are interested in the -optimal approximation of at any time given the currently available information . The following result was proven in Herrera et al. (2021, Proposition B.1) and shows that this approximation is given by the conditional expectation process .

Proposition 2.5.

The optimal (-norm minimizing) process in approximating is given by555 While we gave a pointwise definition, Cohen & Elliott (2015, Theorem 7.6.5) allows to define directly as the optional projection. By Cohen & Elliott (2015, Remark 7.2.2) this implies that the process is progressively measurable, in particular, jointly measurable in and . However, as we have seen, even from the pointwise definition, it follows that is càdlàg, hence optional (Cohen & Elliott, 2015, Theorem 7.2.7). . Moreover, this process is unique up to -null-sets.

2.5 Push-forward Measure of Known Information and Implied Metric

In our analysis the left-limit of càdlàg processes at observation times plays an important role. In the following we define (pseudo) metrics for our processes of interest. We start by constructing probability measures and define the (pseudo) metrics as their induces -norm. We note that to understand the rest of the paper it is enough to consider Definition 2.7 and Remark 2.8, while the other parts of this section can be skipped.

Let us fix any and , then we use the notation to denote it. Any -adapted process can be written as a function of and (cf. Section 2.3). By abuse of notation, we will use the same symbol to write

| (1) |

and we will simply write whenever the context is clear. Moreover, we define for any such process , such that is well defined. The available information at , i.e., just before new information becomes available, is given through . Therefore, the process at time can be written as , which is standard notation for stochastic processes. We define the joint push-forward measure

through the following limit of the joint push-forward measures for , which are probability measures on their induced image probability space with the sample space . For any bounded function for which left limits in terms of its second argument exist, we define

| (2) |

where we used Durrett (2010, Theorem 1.6.9) for the second and dominated convergence in the third equality. It is easy to show that satisfies the properties of a probability measure (i.e., that it integrates to and satisfies the additivity property) by choosing to be the appropriate indicator function. For any càdlàg -adapted process , for which is integrable, (2) holds similarly (by replacing boundedness with integrability of for dominated convergence). Moreover, by combining (1) and (2), we then have for such a that

| (3) |

In the following we are interested in the probability measure conditioned on the event that (which is equivalent to ). In particular, we define .

Proposition 2.6.

Let . For any càdlàg -adapted process , for which is integrable, we have

Proof.

Let be measurable such that its pre-image under is -measurable and define . Then

where we used that is equivalent to . For a general the claim now follows with “measure theoretic induction” (Durrett, 2010, Case 1-4 of Proof of Theorem 1.6.9), of which the first step was presented above. ∎

We use to define a pseudo-metric on the set of càdlàg -adapted processes. In particular, for any two such processes , we define

| (4) |

By looking at the equivalence relation induced by this pseudo metric, defines a metric on the corresponding quotient space. Moreover, this equivalence relation defines indistinguishability between processes in our setting in the following sense.

Definition 2.7.

We call two càdlàg -adapted process indistinguishable, if holds for every .

Remark 2.8.

The (pseudo) metrics can also be defined directly as

however, (4) allows the interpretation of as distance induced by an -norm.

3 Extension of the Neural Jump ODE Model

After shortly revisiting the original Neural Jump ODE model (Section 3.1) and the definition of the signature transform of paths (Section 3.2) we introduce a signature based extension of NJ-ODE which we call Path-Dependent Neural Jump ODE (PD-NJ-ODE) in Section 3.3.

3.1 Recall: Neural Jump ODE

We define and to be the observation and latent spaces for . Moreover, we define three feedforward neural networks (with at least hidden layer and e.g. sigmoid activation functions)

-

•

modelling the ODE dynamics,

-

•

modelling the jumps when new observations are made, and

-

•

the readout map, mapping into the target space for ,

where are the trainable weights. We define the pure jump stochastic process

| (5) |

Then the Neural Jump ODE (NJ-ODE) is defined by the latent process and the output process which are the solution of the SDE system

| (6) |

The latent process of the NJ-ODE before and after each observation can equivalently be written as

| (7) |

3.2 Signature Transform

The variation of a path is defined as follows.

Definition 3.1.

Let be a closed interval in and . Let be a path on . The variation of on the interval is defined by

where the supremum is taken over all finite partitions of .

Definition 3.2.

We denote the set of -valued paths of bounded variation on by and endow it with the norm

For continuous paths of bounded variation we can define the signature transform.

Definition 3.3.

Let denote a closed interval in . Let be a continuous path with finite variation. The signature of is defined as

where, for each ,

is a collection of iterated integrals. The map from a path to its signature is called signature transform.

A good introduction to the signature transform with its properties and examples can be found in Chevyrev & Kormilitzin (2016); Kiraly & Oberhauser (2019); Fermanian (2020). In practice, we are not able to use the full (infinite) signature, but instead use a truncated version.

Definition 3.4.

Let denote a compact interval in . Let be a continuous path with finite variation. The truncated signature of of order is defined as

i.e., the first terms (levels) of the signature of .

Note that the size of the truncated signature depends on the dimension of , as well as the chosen truncation level. Specifically, for a path of dimension , the dimension of the truncated signature of order is given by

| (8) |

When using the truncated signature as input to a model this results in a trade-off between accurately describing the path and model complexity.

For the following universality result of the signature we have to exclude tree like paths. Essentially, a path is tree-like, if it can be reduced to a constant path by successively removing pieces of the form , where is the time-reversal of and the concatenation of paths.

Definition 3.5.

A path is tree-like if there exists a function such that and such that, for all with ,

Two paths are called tree-like equivalent if following forward the first one and concatenating with the backwards running second one leads to a tree-like path.

Remark 3.6.

By adding time as one component to a given path, the set of tree-like equivalent paths reduces to a singleton.

For a Hilbert space we denote the set of continuous, -valued paths of bounded variation starting at the origin () on by . The main reason why the signature transform is used, is its universal approximation property. It states that any continuous function invariant under tree-like equivalences of a path can be approximated arbitrarily well by a linear function of the truncated signature transform for some truncation level and is proven, e.g., in Kiraly & Oberhauser (2019, Theorem 1).

Theorem 3.7.

Let be a compact subset of of paths that are not tree-like equivalent. Let be continuous in variation norm. Then, for any , there exists and a linear functional acting on the truncated signature of degree such that

In the following proposition we show that the result of Theorem 3.7 can be extended to functions with additional inputs.

Proposition 3.8.

Let be a compact subset of of paths that are not tree-like equivalent and let for be compact. We consider the Cartesian product with the product norm given by the sum of the single norms (variation norm and -norm). Let be continuous. Then, for any , there exists and a continuous function such that

Remark 3.9.

We could with equal effort prove that there is a continuous selection of weights such that is close to uniformly on compacts . For later purposes we shall need the proposition’s assertion.

Proof.

Since is a continuous function on a compact metric space, it is uniformly continuous by Heine-Cantor theorem. Hence, there exist such that for all with we have

for all . Since is compact, there exist finitely many open balls with of radius such that they cover . Let the points be the centres of these balls. By the partition of unity, there exist continuous functions , with and such that for all . For each , Theorem 3.7 implies that there exist and such that the function is approximated well by , i.e.,

W.l.o.g. we can assume that all are the same, by concatenating with s. Then the function is continuous as sum of products of continuous functions and satisfies the claim. Indeed, for any we have

where we used that if implying that if and therefore . ∎

To apply this result, we need a tractable description of certain compact subsets of that include suitable paths for our considerations. Since is not finite dimensional, not every closed and bounded subset is compact. Bugajewski & Gulgowski (2020, Theorem 2) characterizes relatively compact subsets of , i.e., subsets such that their closure is compact. Moreover, they prove in Bugajewski & Gulgowski (2020, Example 4) that the following set of functions is relatively compact.

Proposition 3.10.

For every the family of all piecewise linear, bounded and continuous functions that can be written as

is relatively compact, where , , , for all , and .

The following remark shows that this result can be extended to -valued paths, which we will need for our considerations.

Remark 3.11.

Since the product of compact sets is compact and can be identified with , Proposition 3.10 can be extended to -valued paths. Moreover, the generalisation from to is immediate. These are the compact subsets of that we will use.

3.3 Path-Dependent Neural Jump ODE

We adapt (6) by using the signature as additional input in the neural ODE as well as the jump network . Moreover, since the process is not necessarily Markovian any more, we go back to a recurrent structure for the jump network , as in Brouwer et al. (2019); Rubanova et al. (2019). Note that we cannot use the signature of the true path of the data up to time as input, since we only have discrete observations of at the observation times (which is not sufficient to calculate the signature of ). Instead, we use the shifted interpolation up to time and compute the truncated signature . This signature together with the starting point include all available information (while the signature of would include much more then the available information, i.e., it is not -measurable). Moreover, the interpolation has bounded variation, no matter whether this is true for the original path or not. Hence, Theorem 3.7 applies if lies in some compact subset. The advantage (besides Theorem 3.7) of using the truncated signature over using the discrete observations directly is that the truncated signature cumulates information of an arbitrary number of observations in a vector of fixed size.

Our proof depends on the neural networks to be bounded such that we can derive an upper bound for the worst case difference between the true conditional expectation and our model’s approximation of it. Therefore, we introduce the following special class of neural networks with bounded outputs based on any standard class of neural networks.

Definition 3.12 (Bounded output neural networks).

For any dimension we define the bounded output activation function with trainable parameter as the Lipschitz continuous function

Then we define the class of bounded output neural networks as

where can be any set of neural networks. We use the notations and for to highlight the trainable weights and of the respective (bounded output) neural networks. If needed, one could also consider appropriately smoothened versions of .

In the following we assume that is a set of feedforward neural networks with Lipschitz continuous activation functions such that for any and any compact subset we have that is dense in the space of continuous functions (with respect to the supremum-norm). In particular, has to satisfy the standard universal approximation theorem, which is the case e.g. for the set of 1-hidden-layer neural networks with continuous, bounded and non-constant activation function (Hornik, 1991, Theorem 2). Moreover, we assume that .

Definition 3.13.

The Path-Dependent Neural Jump ODE (PD-NJ-ODE) model is given by

| (9) |

The functions are bounded output feedforward neural networks and is a feedforward neural network. They have trainable parameters , where for and is the set of all possible weights for the PD-NJ-ODE; is the signature truncation level and is the jump process counting the observations defined in (5).

Protter (2005, Thm. 7, Chap. V) implies that a unique solution of (9) exists. We write to emphasize the dependence of on and . Moreover, we present an implementable version of this model in Algorithm 1.

Remark 3.14 (Continuation of Remark 2.2).

In the case that is not observed completely, we have to slightly extend the model architecture (9) by another bounded output neural network , where we distinguish between the two cases.

-

1.

If , then and .

-

2.

If , then and , where is the projection to the coordinates in .

3.3.1 Objective Function

Let be the set of all càdlàg -valued -adapted processes on the probability space . Then we define our objective functions

| (10) | ||||

| (11) |

where is the element-wise multiplication (Hadamard product) and will be our (theoretical) loss function. Remark that from the definition of it directly follows that it is an element of , hence is well-defined.

Let us assume that we observe independent realisations of the path together with independent realizations of the observation mask at times , , which are themselves independent realisations of the random vector . In particular, let us assume that , and are i.i.d. random processes (respectively variables) for and that our training data is one realisation of them. We write . Then the Monte Carlo approximation of our loss function

| (12) |

converges -a.s. to as , by the law of large numbers (cf. Theorem 4.4).

4 Convergence Guarantees

As in Herrera et al. (2021), we first give the convergence result for the objective function and then show that its Monte Carlo approximation converges to it. The proofs mainly follow the proofs therein, with extensions for the more general setting. Let be the set of possible weights with for , for the (bounded output) neural networks of the PD-NJ-ODE (6), such that their widths and depths666The width of a neural network is the maximal number of nodes in any of its hidden layers and the depth is the number of hidden layers. are at most and such that the truncated signature of level or smaller is used as input. We define the compact subset . Furthermore, we use the notation , and if we speak of the projections of the sets on the weights and respectively.

4.1 Convergence of Theoretical loss function

Theorem 4.1.

Before proving the theorem, we derive the following useful result, which is an extension of a result in Herrera et al. (2021).

Lemma 4.2.

For any -adapted process it holds that

Proof.

Proof of Theorem 4.1.

We start by showing that is the unique minimizer of up to indistinguishability (as defined in Definition 2.7). First, note that for every we have and that if , hence with probability 1. Therefore,

where we use Lemma 4.2 for the second line and the triangle inequality for the third line. Hence, is a minimizer of .

Before we can show uniqueness of , we need some additional results. For those, let . Let , then the Hölder inequality, together with the fact that , yields

| (13) |

By Assumption 1 we know that . Hence, we have for any by the independence of from , and that

and by the the equivalence of - and -norm, we therefore have for some constant

| (14) |

To see that is the unique minimiser up to indistinguishability, let be a process which is not indistinguishable from . Hence, there exists some such that . We have

where we used triangle-inequality for the second and Lemma 4.2 in the third line. Hence, it is enough to note that the second term is greater than . Indeed,

| (15) |

where we used (13) for the 3rd, (14) for the 4th and Proposition 2.6 together with (4) for the last line. Hence, .

Next we show that (9) can approximate arbitrarily well. Since the dimension can be chosen freely, let us fix it to . Furthermore, let us fix such that , which is possible since we assumed that . Let , (implying that ) and be the closure of the set of Remark 3.11, which is compact. For any , the function is continuous by Assumption 4 and can (by abuse of notation) equivalently be written as (continuous) function . Therefore, Proposition 3.8 implies that there exists an and a continuous function such that

Since the variation of functions in is uniformly bounded by a finite constant, the set of their truncated signatures is a bounded subset in for some (depending on and ), hence its closure, denoted by , is compact. Therefore, the universal approximation theorem for neural networks (Hornik et al., 1989, Theorem 2.4) implies that there exists an and neural network weights such that for every the function is approximated up to by the -th coordinate of the neural network (denoted by ) on the compact set . Hence, combining the two approximations we get (by triangle inequality)

Obviously, extending the input of the neural network does not make the approximation worse, by simply setting the corresponding weights to , hence, also can be used as additional input. Similarly we get that there exists an and neural network weights such that for every

As before, can be used as additional input without worsening the approximation.

Next we define the bounded output neural networks based on these neural networks. For this let us define

and equivalently for . Since the neural networks are continuous functions they take a finite maximum on the compact sets, hence are finite. Then we define the bounded output neural networks with . Clearly, these bounded output neural networks coincide with the neural networks on the compact sets. Therefore, they satisfy the same -approximation and since are bounded by (Assumption 4), it follows that are bounded by . In particular, we have for the global bounds and . Setting , it follows that .

Now we can bound the distance between and . Whenever , the number of observations satisfies and the minimal difference between any two consecutive observation times , we know that the corresponding path is an element of and therefore the neural network approximations up to hold. Otherwise, one of those conditions is not satisfied and the global upper bound can be used. Hence, if , we have for and

and if ,

Moreover, by equivalence of the - and -norm, there exists a constant such that for all

So far, we have fixed an and argued that there exists some such that the neural network approximation bounds hold with -error. However, what we actually need to show is that this error converges to when increasing the truncation level and network size . Therefore, we define to be the smallest number such that the above bounds hold with error when using an architecture with signature truncation level and weights in . Since increasing can only make the approximations better (by setting the new weights to , the same approximation error as before is achieved, but potentially there exists a better choice), we have for any . In particular is a a decreasing sequence, hence, our derivations before prove that . In the following we denote by the best choice for the weights within the set to approximate the functions .

Note that Assumptions 4 and 5 imply that there exists such that and that . Since (note that at least one minimum exists in the compact set since is continuous), we get

| (16) |

where we used the triangle inequality for the -norm in the th line, Jensen’s inequality (for concave functions) in the last line and define as a suitable constant. Integrability of and (Assumptions 5 and 6) together with Assumption 2 on imply that

Therefore, we have for a suitable constant (not depending on and ),

by dominated convergence, since is -integrable by Assumption 5 (and using the inequality for ). Using this and , we get from (16)

Remark 4.3 (Continuation of Remark 2.2 and Remark 3.14).

In the case that is not observed completely, we only need to check that is still satisfied, which amounts to showing that . We distinguish again between the two cases.

-

1.

If , we have

using that the constant can be approximated arbitrarily well by the bounded output neural network on the compact subset .

-

2.

If , then is a continuous function in the input (by Assumption 4) and can therefore by approximated arbitrarily well by on any compact subset. It is enough to note that implies that lies in a compact set to conclude that

4.2 Convergence of the Monte Carlo Approximation

We now assume the size of the neural network and of the signature truncation level is fixed and we study the convergence of the Monte Carlo approximation when the number of samples increases. Moreover, we show that both types of convergence can be combined. The convergence analysis is based on Lapeyre & Lelong (2021, Chapter 4.3) and follows Herrera et al. (2021, Theorem E.13).

Theorem 4.4.

Let for every . Then, for every , -a.s.

Moreover, for every ,

In particular, one can define an increasing sequence in such that for every we have that converges to in the metric as .

We define the separable Banach space for a suitable (see below) with the norm , the function

and , where and , and (with entries for coordinates which are not observed) are random variables describing the -th realization of the training data, as defined in Section 3.3.1. Let , , and . By this definition we have -almost-surely. Moreover, we have that are i.i.d. random variables taking values in . Let us write to make the dependence of on the input and the weight explicit. Then we define

Lemma 4.5.

Almost-surely the random function is uniformly continuous for every .

Proof.

Since the activation functions of the neural networks are continuous, also the neural networks are continuous with respect to their weights , which implies that also is continuous. Since is compact, this automatically yields uniform continuity. ∎

The following lemma is a consequence of (Ledoux & Talagrand, 1991, Corollary 7.10) and (Rubinstein & Shapiro, 1993, Sec. 2.6, Lemma A1 & Theorem A1 and discussion thereafter).

Lemma 4.6.

Let be a sequence of random variables with values in and be a measurable function. Assume that a.s., the function is continuous and for all , . Then, a.s. converges locally uniformly to the continuous function , i.e.,

Moreover, let be compact and define the random variables . We consider a minimizing sequence of random variables , given by and let and . Then and a.s.

Proof of Theorem 4.4..

First we note that, is the (integration over the) output of (bounded output) neural networks and therefore bounded in terms of the input, the weights (which are bounded by ), and some constant depending on the architecture and the activation functions of the neural network. In particular we have that for all and for some constant (possibly depending on ), where corresponds to the input . Hence,

Hence,

| (19) |

by Assumption 5. By Lemma 4.5, the function is continuous, hence, we can apply Lemma 4.6, yielding that almost-surely for the function

| (20) |

converges uniformly on to

| (21) |

Moreover, Lemma 4.6 yields that a.s. when . Then there exists a sequence in such that a.s. for . The uniform continuity of the random functions on implies that

By continuity of this yields a.s. as . With (19) we can apply dominated convergence which yields

Since for every integrable random variable we have and since we can deduce

| (22) |

Now by triangle inequality,

| (23) |

(20), (21) and (22) imply that both terms on the right hand side converge to 0 a.s. when , which finishes the proof of the first part of the Theorem.

Corollary 4.7.

Proof.

4.3 Dependence between the Process and the Observation Framework & Noisy Observations

So far we have focused on the case where the observation times and masks are independent of the underlying process . This was modelled by using the product space of two independent probability spaces. While this still allows for a quite high generality, it keeps the derivations of the results relatively easy, since Fubini’s theorem can be used to split expressions into the components of the one and the other probability space. Additionally, we only considered noise-free observations in our framework. Even though the process itself is stochastic and therefore might have some noisy components, we always assumed that we observe the process without any measurement noise and that we want to predict the process itself, without filtering out any noise. One way to tackle the problem of noisy observations is via stochastic filtering, which is described in Section 6. However, this approach requires stronger assumptions, in particular, that the distribution of the underlying process and of the noise are known or equivalently that training samples split up into the noise-free observation and the noise term are available.

In the companion paper (Andersson et al., 2023), we prove the equivalent theoretical results when there is dependence between the process and the observation framework and when observations are noisy under mild additional assumptions. In particular, we show that both of these generalisations do not pose a problem for our PD-NJ-ODE framework.

5 Conditional Variance, Moments and Moment Generating Function

5.1 Uncertainty Estimation: Conditional Variance

Let be a -dimensional process satisfying Assumptions 1 to 6. If satisfies Assumption 4 and 5, then also the joint process satisfies all assumptions. Therefore, the conditional expectation of can be used to get an uncertainty estimate for the prediction of the process (not to be confused with an uncertainty estimate of our model output) by computing its conditional variance

| (24) |

In particular, when using the -dimensional input for PD-NJ-ODE (where the observation mask is the same for and ), (24) yields a way to compute the conditional variance of .

An example of a process for which also its conditional variance can be estimated in our framework is given below.

5.2 Towards the Conditional Distribution: Moments and the Moment Generating Function

In the following we assume for simplicity that the process is -dimensional, although the considerations generalize to higher dimensions. If the process is such that all its moments for satisfy Assumptions 4 and 5, then, in principle, PD-NJ-ODE can be used to compute all conditional moments of . Theorem 3.3.11 and the Remark afterwards of Durrett (2010) give two conditions on the moments under which they uniquely characterize the corresponding distribution. Hence, if one of these conditions is satisfied, PD-NJ-ODE can, in principle, characterize the conditional distribution of given for any .

Under the stronger assumption that there exists some such that for all the process satisfies Assumptions 4 and 5, PD-NJ-ODE can in principle be used to compute the conditional moment generating function of , for , for any . Since the moment generating function on any open interval including uniquely characterizes the corresponding distribution (Billingsley, 1995, Section 30), PD-NJ-ODE then, in principle, characterizes the conditional distribution.

In practice, only finitely many moments can be computed and the moment generating function can only be approximated by computing it for finitely many values of . However, the two methods described above give rise to a way how PD-NJ-ODE can approximately characterize the conditional distribution of .

6 Stochastic Filtering with PD-NJ-ODE

In this section we show that the PD-NJ-ODE can be use to approximate solutions to the stochastic filtering problem with discrete observations. In Section 6.1 we first shortly introduce the stochastic filtering problem following Bain & Crisan (2009) and then we explain how PD-NJ-ODE can be used to solve it in Section 6.2. Moreover, in Appendix A we discuss solving a generalized version of the stochastic filtering problem.

6.1 Stochastic Filtering Problem

In the filtering framework, one is interested in a signal process , defined as in Section 2.1. However, this signal process is never observed. Instead one observes the observation (or sensor) process defined as

where is a measurable function and is a standard -adapted -dimensional Brownian motion independent of . Defining the available information at time as , the filtering problem consists in determining the conditional distribution of given the currently available information . In particular, this means computing the conditional expectations

for any measurable function for which the integral is well defined (Bain & Crisan, 2009, Definition 3.2). A typical assumption in the filtering problem is that the distribution of is known (e.g. in the sense that is given as the solution of an Itô-diffusion with known coefficients (Bain & Crisan, 2009, Section 3.2.1)) and that the function is known. In particular, this implies that the joint law of is known.

Remark 6.1.

There are more general formulations of the filtering problem, as for example in Cohen & Elliott (2015, Section 22). The following applications of PD-NJ-ODE work identically in these settings as long as we have access to the joint law of .

In real world filtering tasks, the observation process can only be observed at finitely many observation times , which we can model again as described in Section 2.1. In particular, we assume here that is always observed, although the framework could easily be extended to the setting where this is not the case. The available information at any time can be described similarly as in Section 2.2 by

Hence, the resulting filtering problem is to compute for any integrable measurable function the conditional expectation

6.2 Applying PD-NJ-ODE to the Filtering Problem

At first sight, one might think that our model framework is not compatible with the filtering problem, since our results depend on the assumption that every coordinate is observed with positive probability at any observation time, while obviously, in the filtering task, the signal process is never observed. However, the important subtlety is that this is only true for the samples on which we want to evaluate the trained PD-NJ-ODE model, while for the training of the model we can make use of the knowledge of the law of to generate a suitable training set.

In particular, we generate i.i.d. samples of together with i.i.d. samples of the amount of observations and observation times . Moreover, we generate observation masks , where the coordinates corresponding to are always and the coordinates corresponding to are either all or all simultaneously, with the probability to be given by and for . It is crucial that , since otherwise this would contradict Assumption 1, and that for the following reason. If was , the signal process would always be observed at the -th observation time, implying that the probability of having a sample with at least observations where only the -coordinates are observed is in the distribution of the training set777Importantly, the expectations in our theoretical results are taken with respect to the (theoretical) distribution of the training set. In particular, for samples that do not lie in a subset with positive probability in the distribution of the training set, these results do not apply.. On the other hand, any choice of leads for any fixed (and finite) amount of observations to the probability that the signal process is never observed at the observation times. Hence, those samples that we have to consider in the evaluation of the model for solving the filtering task, where only the -coordinates are observed, show up in the training set with positive probability, yielding that the theoretical results apply.

To make this precise, let be the projection on the -coordinates and let us define the probability measure similar to as

| (25) |

where we note that can equivalently be expressed in terms of and we recall that is equivalent to . Independence of and together with the arguments above imply that

Hence, (25) is a well defined probability measure for . Similarly to the pseudo-metric we define the pseudo metric on the set of càdlàg -adapted processes by

| (26) |

To prevent confusion, we will call the PD-NJ-ODE output instead of . Then the following result is a consequence of Theorem 4.4.

Corollary 6.2.

Assume that the training samples are generated as described above and that satisfies Assumptions 4 and 5. Let for every . Then, one can define an increasing sequence in such that for every the following statements hold.

-

1.

converges to in the metric as .

-

2.

converges to in the metric as .

-

3.

We write and to emphasise whether the and -coordinates or only the -coordinates are provided as input. Similarly we distinguish between the conditional expectation given the and -coordinates of the observations and the one given only the -coordinates . It holds that

Proof.

With the given assumptions on and on the training samples, Assumptions 1 to 6 are satisfied (with the Case 2 of Remark 2.2). Therefore, the first item follows directly from Theorem 4.4.

For the second item, we first note that similar to Proposition 2.6, for any càdlàg -adapted process , for which is integrable, we have

Therefore (similar to (18)), we have

from which item 2 follows.

For the last item we have

since on the subset where for , the PD-NJ-ODE model only gets the -coordinates as input up to time . The second equality holds for the same reason. ∎

Remark 6.3.

It follows from Corollary 6.2 that converges to in the metric as . In particular, the output888More precisely, the part of the output representing the approximations of the -coordinates of the trained model, when applied to input samples of the filtering task, where only the -coordinates are observed, converges to the conditional expectation .

7 Examples of Processes Satisfying the Assumptions

We summarise several processes that satisfy Assumptions 4 and 5 (the other assumptions need to be satisfied by the observation framework, i.e., they are not process specific). The examples in Sections 7.1 and 7.2 are from Herrera et al. (2021) and recalled here, to show that the new setting truly is a generalization of the old one. In Section 7.3 we present a process with jumps, in Sections 7.4 a path-dependent process, in Section 7.5 a multivariate process with correlated coordinates and incomplete observations, and in Section 7.6 a process in the setting of a stochastic filtering problem. Additional processes satisfying these assumptions are discussed in Appendix B.

7.1 Itô Diffusion with Regularity Assumptions

Let be an -dimensional Brownian motion on , for . Let be defined as the solution of the stochastic differential equation (SDE)

| (27) |

for all , where is the starting point and the measurable functions and are the drift and the diffusion respectively. By definition this process is continuous. Moreover, we impose the following assumptions.

-

•

and are both globally Lipschitz continuous in their second component, i.e., for there exists a constant such that for all

In particular, their growth is at most linear in the second component.

-

•

is bounded, and continuous in its first component () uniformly in its second component (), i.e., for every and there exists a such that for all with and all we have .

-

•

is càdlàg (right-continuous with existing left-limit) in the first component and integrable with respect to , , i.e.,

(28) where denotes the Frobenius matrix norm. This is in particular implied if is bounded.

-

•

We always observe all coordinates of simultaneously (no incomplete observations).

Remark 7.1.

In Herrera et al. (2021) there was the additional assumption that is continuous and square integrable, which we left out here, since this is already implied by the other assumptions.

Under these assumptions a unique continuous solution of (27) exists, once an initial value is fixed (Protter, 2005, Thm. 7, Chap. V). Herrera et al. (2021, Lemma E.7) shows that is -integrable. Moreover, the results of Herrera et al. (2021, Propositions B.1 and B.4) imply that Assumption 4 is satisfied.

Remark 7.2.

The assumption that is bounded and the integrability assumption on can be weakened, as will be shown in Section B.1. In particular, the boundedness of is only needed to apply the Markov property, which is not needed in our more general setting now, where we have access to the entire past information.

7.2 Other Itô Diffusions: Black-Scholes, Ornstein-Uhlenbeck, Heston

The Black-Scholes (geometric Brownian Motion), Ornstein-Uhlenbeck and Heston processes are Itô diffusions which do not satisfy the assumptions in Section 7.1. In particular, their drifts are not bounded and the Heston process does not satisfy the Lipschitz assumptions. If the Feller condition is satisfied, the Heston process is Lipschitz with high probability, otherwise not. Nevertheless, Assumptions 4 and 5 are still satisfied for these three processes as shown below. Experiments on these processes were performed in Herrera et al. (2021).

Example 7.3 (Black-Scholes).

The SDE describing this model is

where is a 1-dimensional Brownian motion and . The conditional expectation of the solution process is given by . Hence, .

Cohen & Elliott (2015, Lemma 16.1.4) implies that for every and therefore by Hölder’s inequality for all .

Example 7.4 (Ornstein-Uhlenbeck).

This model is described by the SDE

where is a 1-dimensional Brownian motion and . The conditional expectation of the solution process is given by . Hence, .

Again, Cohen & Elliott (2015, Lemma 16.1.4) implies that for every and therefore by Hölder’s inequality for all .

Example 7.5 (Heston).

The Heston model is described by the SDE

where and are 1-dimensional Brownian motions with correlation , and . The conditional expectation of the solution process is given by . Hence, . Moreover, if also the stochastic variance should be predicted coincidently, its conditional expectation is given by . Hence, .

-integrability of the Heston model is more delicate. While Cohen & Elliott (2015, Lemma 16.1.4) implies that for every and therefore by Hölder’s inequality for all , the moments of can explode (Andersen & Piterbarg, 2007, Proposition 3.1). In particular, the moment explosion time

of is infinite if and only if and . By Itô’s lemma we can write , where is the discounted log-price process satisfying

According to Keller-Ressel (2011, Corollary 2.7 and Equation 6.1), is a martingale, hence Doob’s Maximal inequality implies that for any

Therefore, is -integrable if , where a closed form for is given in Andersen & Piterbarg (2007, Proposition 3.1), in case it is finite. Again, Hölder’s inequality implies that is -integrable if it is -integrable for some .

Remark 7.6.

if

Note that , therefore the second term is an element of .

In the standard Heston example of Herrera et al. (2021), the used parameters are , , , , and therefore for all .

In the second example of Herrera et al. (2021) of a Heston model where the Feller condition is not satisfied, the used parameters are

, , , , and therefore for all . Moreover, for we have .

7.3 Stochastic Process with Jumps: Homogeneous Poisson Point Process

A homogeneous Poisson point process , for , is defined to be the increasing stochastic process in such that and its increments are independent Poisson distributed, i.e., for any . It follows that its conditional expectation is . Therefore, .

By its definition as an increasing process, , and since all moments exists, hence for all .

7.4 Fractional Brownian Motion

Definition 7.7.

A random vector is a centered Gaussian vector if any linear combination of the is a centered Gaussian random variable.

Definition 7.8.

A stochastic process is a centered Gaussian process if any finite-dimensional vector is a centered Gaussian vector.

Since the law of a centered Gaussian vector is completely determined by its covariance function, it suffices to specify the covariance to obtain a unique Gaussian process. In fact, one can prove that for each function such that for all in and for all in ,

we can construct a centered Gaussian process with the given covariance function , using Kolmogorov’s extension theorem.

Definition 7.9.

The fractional Brownian motion with Hurst index is the centered Gaussian process with covariance function

Note that the case results in a covariance of , which is precisely the covariance of a standard Brownian motion. The case corresponds to positively correlated increments, which is a common phenomenon in financial mathematics. Meanwhile, the case corresponds to negatively correlated increments.

If , the paths are non-Markovian, hence, the conditional expectation does not only include the information of the last measurement, as we have seen for the Black-Scholes, Heston and Ornstein-Uhlenbeck model. Instead, the conditional process (of which the mean is the conditional expectation) of the fractional Brownian motion depends on the entire past trajectory. In Sottinen & Viitasaari (2017, page 3), the law of this conditional process is described explicitly. It requires knowledge of the whole trajectory of the fractional Brownian motion up to the current time. Since, in our setting, we only have a finite number of discrete observations (at random times) available to train our model, it is unreasonable to expect the model to correctly approximate the conditional expectation implied by this conditional process. However, we can also compute the true conditional expectation given our discrete observations, making use of the fact that is a Gaussian process, implying that the vector of observations is a Gaussian vector (Norros et al., 1999). Assume we have observed the values of at times and we want to compute the conditional expectation for . For any fixed , the vector is centred Gaussian with covariance

Then a simple calculation shows that

implying that is independent of , since it is a Gaussian vector. Hence,

This function is differentiable in and we get

where under the assumptions above.

The following result, which is a consequence of the upper bounds on Pickands constant (Shao, 1996; Debicki & Kisowski, 2008), shows that the running maximum process of fractional Brownian motion is -integrable for all .

Proposition 7.10.

Let and a fractional Brownian motion with Hurst parameter . Let and . Then .

Proof.

Pickands constant is defined as

According to Debicki & Kisowski (2008), is finitely bounded from above for every , therefore, there exists some such that for all , is finite and bounded from above by some constant. If , we can use that , hence we can assume without loss of generality that . We have

and since is symmetric around , implying that ,

Together, this implies that ., which means that the moment generating function of is finite. A well known property of the moment generating function implies that

since is non-negative. ∎

7.5 Multivariate Process with Incomplete Observations: Correlated Brownian Motions

Let be three i.i.d. 1-dimensional Brownian motions and let with . Then we define the process . are again Brownian motions, but they are correlated. First we remark that for every (cf. Cohen & Elliott (2015, Lemma 16.1.4)).

In this example we assume to have incomplete observations. In particular, we allow for observation times at which only or only is observed. Therefore, let us define the (ordered) observations of as for and those of as for , where are random variables similar to , representing the total number of observations of and respectively. As before, for are the times at which observations are made, i.e., the times at which at least one of is observed. Due to the correlation of the coordinates, observing (only) one coordinate, generally also impacts the conditional expectation of the other one. To compute the true conditional expectations given the discrete (possibly incomplete) previous observations, we use the fact that the increments of are independent Gaussian random variables. Remember that and let for all and similar for . Then we define

which is multivariate normally distributed with , where

Let be the lower triangular matrix with all ones and define the matrix

Then . Let be the current time and let be such that , where . Moreover, let be such that and . In the following we compute conditional expectations of . Those of follow equivalently. First we notice that the independent increments of Brownian motion imply

and therefore, . If , i.e., if was observed, then . Otherwise, and we define

where and , as well as as the submatrix of with all rows with only -entries removed. For we therefore have

where we used a well known fact about affine transformations of multivariate normal distributions (see e.g. Eaton (2007, Chapter 3.1)). Let

where , and . Then, the conditional distribution of is again normal with mean and variance (Eaton, 2007, Proposition 3.13). In particular, we have .

7.6 Filtering Problem with Brownian Motions

Let be two i.i.d. 1-dimensional Brownian motions and let with which we define . We use as the (unobserved) signal process and define the observation process (although this differs slightly from the description in Section 6.1, it is justified by Remark 6.1). As described in Section 6, we assume that and the distribution of and are known to generate training data from it. Moreover, evaluation samples only have observations of .

is a Gaussian process with for every (cf. Cohen & Elliott (2015, Lemma 16.1.4)) and we can derive the analytic expressions of the conditional expectations similarly as in Section 7.5. Let be the observation times and define for and similarly for . Moreover, (for the samples of the training set) let us define the (ordered) observations of as for . Then

is multivariate normally distributed with , where

Let be the lower triangular matrix with all ones and define the matrix

Then . Let be the current time and let be such that , where . Moreover, let be such that . In the following we compute the conditional expectation of , since the one of is trivially given by the last observation of , as is observed at every observation time (cf. Section 7.5). The independent increments of Brownian motion imply

and therefore, . If , i.e., if was observed, then . Otherwise, and we define

where and , as well as as the submatrix of with all rows with only -entries removed. For we therefore have

where we used a well known fact about affine transformations of multivariate normal distributions (see e.g. Eaton (2007, Chapter 3.1)). Let

where , and . Then, the conditional distribution of is again normal with mean and variance (Eaton, 2007, Proposition 3.13)). In particular, we have .

8 Experiments

The code with all new experiments and those from Herrera et al. (2021) is available at https://github.com/FlorianKrach/PD-NJODE. Additional experiments are provided in Appendix C. Moreover, further details about the experiments can be found in Appendix D. Since our practical implementation slightly deviates from the theoretical description, we list all differences in Appendix D.1.1.

First we use synthetic datasets to confirm our theoretical results for all generalizations of the problem settings over those in Herrera et al. (2021). In particular, we show that the path-dependent NJ-ODE can be applied successfully when the underlying process has jumps (Section 8.1) or is path dependent (Section 8.3), when observations are incomplete (Section 8.4). Moreover, we verify that the (path-dependent) NJ-ODE can be used for uncertainty estimation (Section 8.2) and and for solving stochastic filtering problems (Section 8.5) as was suggested in Sections 5 and 6, respectively. The model performance is measured by the evaluation metric that was introduced in Herrera et al. (2021, Sec. 6.1). This metric computes the MSE on a discretization time grid between the optimal prediction (given by the conditional expectation, which can be computed in these synthetic examples because the law of the underlying process is known) and the predictions of the model on the samples of the test set. It is given by

where the outer sum runs over the test set of size and the inner sum runs over the equidistant grid points on the time interval .

In Section 8.1 and 8.2 we show results using the standard NJ-ODE model, since the respective datasets do not exhibit any of the complications that would (numerically) require the PD-NJ-ODE. However, we remark that PD-NJ-ODE leads (at least) to the same quality of results.

Our empirical results on more complicated datasets suggest that using the equivalent objective function as described in Remark 4.8 is preferable, since the training is more stable. With the original loss function, the training more easily ends up in local optima which are not global optima. However, these local optima do not exist for the equivalent loss function due to its slightly different structure, hence the training does not end up there. For more details see Appendix D.1.5.

Finally, in Section 8.6 and Section 8.7 we apply the PD-NJ-ODE model to real world datasets. First, to the PhysioNet dataset of patient health parameters, where the results of PD-NJ-ODE are compare to those of NJ-ODE. And then to 3 datasets of limit order book (LOB) data, where the architecture of the PD-NJ-ODE is adapted to additionally address a classification task.

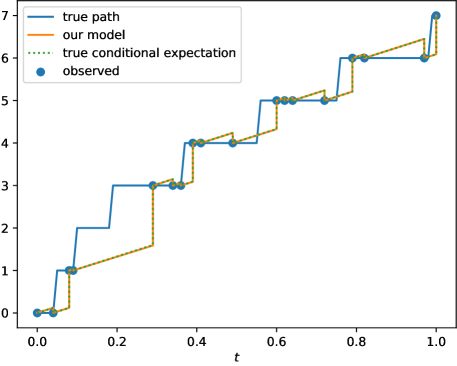

8.1 Process with Jumps – Poisson Point Process

In this experiment we use a Poisson point process, which was described in Section 7.3, to show that NJ-ODE can successfully be applied to processes with jumps. Already the standard NJ-ODE model without extensions leads to an evaluation metric smaller than after only 30 epochs of training (Figure 2). Hence, we conclude that this is another problem setting, where no extension of NJ-ODE model is needed although the setting is not covered by the theoretical framework in Herrera et al. (2021) (as is the case for Black–Scholes, Ornstein-Uhlenbeck and Heston processes as well).

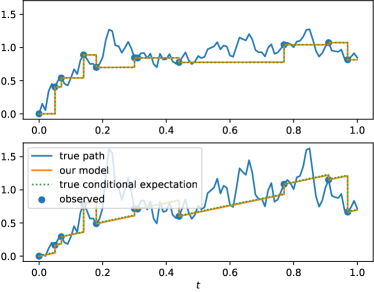

8.2 Uncertainty Estimation – Brownian Motion and its Square

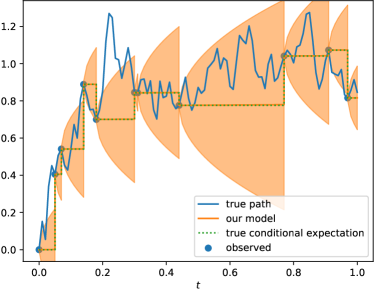

We apply NJ-ODE to a Brownian motion and its square , as described in Example 5.1, to show that our model can be used to compute the conditional variance, which gives rise to an uncertainty estimate of the prediction. In Figure 3, we show the predictions of the 2-dim process as well as the prediction of together with a confidence region defined as , where is NJ-ODE’s predicted conditional expectation and is its predicted conditional variance at time . The evaluation metric on the 2-dimensional dataset becomes smaller than .

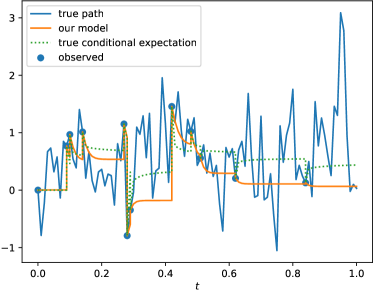

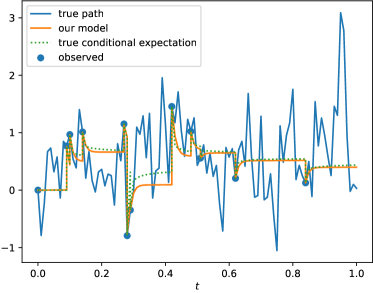

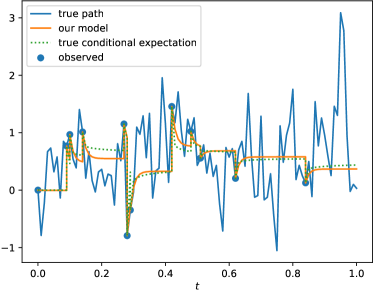

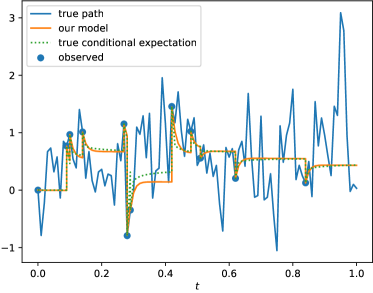

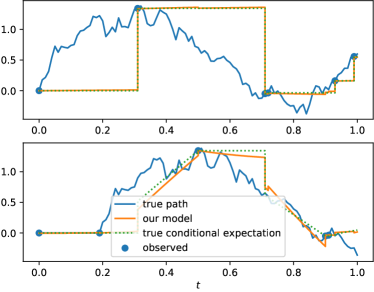

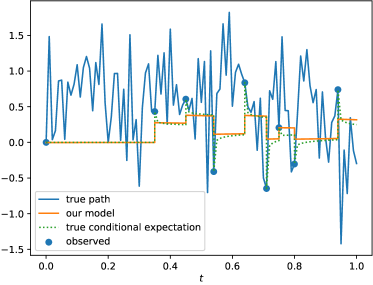

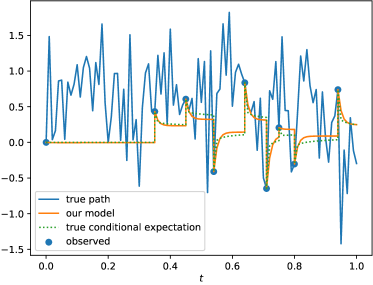

8.3 Path Dependent Process – Fractional Brownian Motion

| NJ-ODE | NJ-ODE (with sig.) | NJ-ODE (with RNN) | PD-NJ-ODE | |

|---|---|---|---|---|

| min. evaluation metric |

Path dependent processes are one of the main application areas for the extension of NJ-ODE. Here we use a fractional Brownian motion (FBM) with Hurst parameter , which yields a rough process with high negative auto-correlation (cf. Section 7.4).

To show that PD-NJ-ODE performs better than the standard NJ-ODE, we compare them as well as 2 intermediate versions, where once the signature is added as input to NJ-ODE and once a recurrent jump network is used in NJ-ODE.

For all 4 models the same architecture is used.

The optimal evaluation metric for each of the models is given in Table 1. PD-NJ-ODE achieves the best evaluation metric, for the two intermediate models it is approximately doubled and for NJ-ODE it is about times larger.

Although our theoretical results imply that the NJ-ODE with signature should be enough, the performance can depend on the truncation level used for the signature input.

All truncation levels between were tested. For and the minimal evaluation metric was and . For all , it was .

The computation time grows with increasing truncation level , since it depends on the input dimension of the neural networks which increases according to (8) for growing .

Therefore, we choose to use a truncation level of or for all of our experiments, since this seems to be a good trade-off between model performance and computation time. Here we report results with .

Since truncation levels up to are still rather small, it is not surprising that using the recurrent structure can carry on additional path information that is not covered by the truncated signature and therefore leads to improved quality.

On the other hand these results also show that the recurrent structure alone does not carry all necessary path information.

These differences in the quality of the predictions can also be seen in Figure 4.

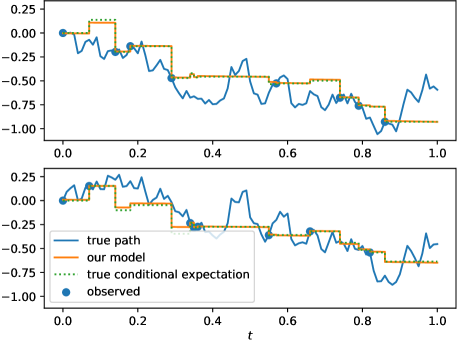

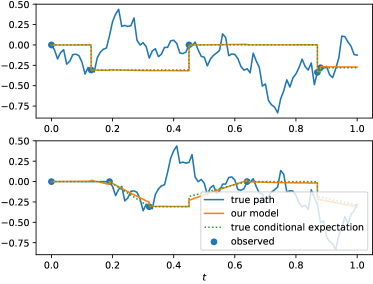

8.4 Incomplete Observations – Correlated 2-Dimension Brownian Motion

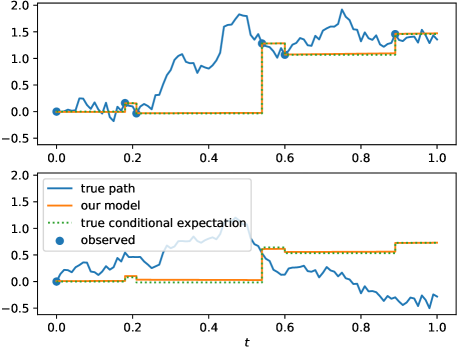

To test the model on a synthetic dataset with incomplete observations, we consider the example of a 2-dimensional correlated Brownian motion, as described in Section 7.5, with . From the discretization grid, we first sample observation times as usual and for each observation time one of the two coordinates is picked at random to be observed (cf. Appendix D.1.3, where is used). The derivations in Section 7.5 show that the incomplete observations also introduce some path dependence. The path-dependent NJ-ODE model achieves a minimal evaluation metric of and we see that it reacts well with its prediction of the one coordinate when the other coordinate is observed, even for multiple consecutive observations of the same coordinate (Figure 5).

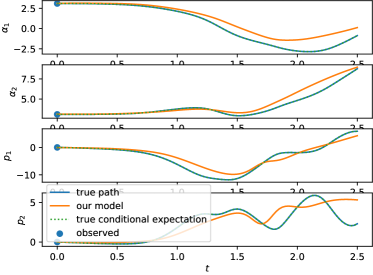

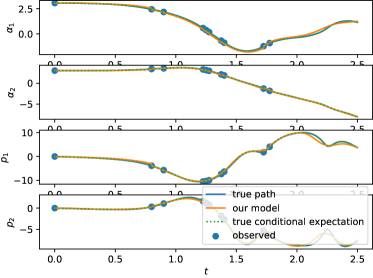

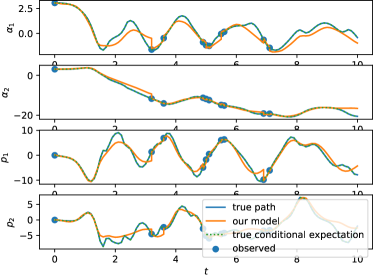

8.5 Stochastic Filtering of a Brownian Motion with Brownian Noise

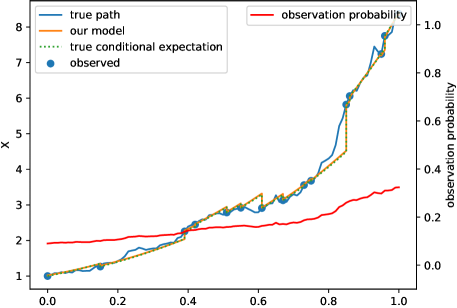

PD-NJ-ODE is applied to the stochastic filtering problem that was described in Section 7.6, where and observation probabilities , for the -coordinates of the training set, are used. The model achieves a minimal evaluation metric of and we see that it learns to use new observations of to update the predictions of (Figure 6).

8.6 Physionet

We test the PD-NJ-ODE model on the extrapolation task of Rubanova et al. (2019) on the PhysioNet Challenge 2012 dataset (Goldberger et al., 2000) and compare it to the results of NJ-ODE. In Table 2 we see that the PD-NJ-ODE outperforms the NJ-ODE. While the results for the PD-NJ-ODE are computed with -hidden layer neural networks with hidden nodes, compared to -hidden layer networks with hidden nodes for NJ-ODE, the amount of parameters is much larger, since the signature truncated at level is used as additional input (for the -dimensional underlying process, this amounts to additional inputs). These results suggest that there is some (small) path-dependence in the PhysioNet dataset, which could be dealt with by the PD-NJ-ODE model.

| Physionet – MSE | # params | |

| RNN-VAE | - | |

| Latent ODE (RNN enc.) | - | |

| Latent ODE (ODE enc) | ||

| Latent ODE + Poisson | ||

| NJ-ODE | 1.945 0.007 | |

| PD-NJ-ODE | 1.930 0.006 |

8.7 Limit Order Book Datasets

Stock and crypto-currency exchanges use a limit order book (LOB) to track all limit orders999A limit order is the order to buy (sell) a certain amount of an asset for some maximum (minimum) price or below (above). of agents who want to buy or sell any of the assets that are traded at the exchange. For each asset, the LOB has a buy and a sell side and for each side lists all the price levels together with the respective order volumes at which the agents would like to buy or sell. The midprice is defined as the mean between the best bid (buy order) and ask (sell order) price. The LOB of level is a truncated version of the LOB which only includes the best (highest) bid and the best (lowest) ask prices. In the following we always work with LOBs of level . Whenever a new order is made or an order is cancelled, the LOB is updated. New limit orders are added to the book, while new market orders are directly executed against the best available limit orders. Hence, LOBs are updated irregularly in time, making them a natural example to apply the PD-NJ-ODE.

We test our model on crypto-currency LOB data. The first dataset (denoted “BTC”) is based on one day of data of the LOB of Bitcoin, which was gratefully provided to us by Covario. The other datasets (denoted “BTC1sec” and “ETH1sec”) are based on roughly 12 days of snapshots of the LOB of Bitcoin (BTC) and Ethereum (ETH) at a frequency of 1 second (once every second the state of the LOB is saved instead of saving it at every update of the book). Using snapshots of the LOB at a predefined frequency usually leads to a loss of information compared to the full LOB. However, these datasets are publicly available (Nielsen, 2021), which is the reason why we include them here. For all datasets, any data point at which the first 10 levels of the LOB did not change compared to the previous one is deleted. The datasets are split into non-overlapping samples, which have consecutive data points as input and the data point steps ahead as label to be predicted.

| BTC | BTC1sec | ETH1sec | |