ifundefinedbibfont \externaldocument[S-]SM2[SM2.pdf]

Dynamic CoVaR Modeling††thanks: The first author gratefully acknowledges support of the German Research Foundation (DFG) through grant number 502572912 and the second author through grant HO 6305/2-1. A previous version of the article circulated under the title “Dynamic Co-Quantile Regression”.

Abstract

The popular systemic risk measure CoVaR (conditional Value-at-Risk) is widely used in economics and finance.

Formally, it is defined as an (extreme) quantile of one variable (e.g., losses in the financial system) conditional on some other variable (e.g., losses in a bank’s shares) being in distress and, hence, measures the spillover of risks.

In this article, we propose joint dynamic and semiparametric models for VaR and CoVaR together with a two-step M-estimator for the model parameters drawing on recently proposed bivariate scoring functions for the pair (VaR, CoVaR).

Among others, this allows for the estimation of joint dynamic forecasting models for (VaR, CoVaR).

We prove consistency and asymptotic normality of the proposed estimator and analyze its finite-sample properties in simulations.

We apply our dynamic models to generate CoVaR forecasts for real financial data, which are shown to be superior to existing methods.

Keywords: CoVaR, Estimation, Forecasting, Modeling, Systemic Risk

JEL classification: C14 (Semiparametric and Nonparametric Methods); C22 (Time-Series Models); C58 (Financial Econometrics); G17 (Financial Forecasting and Simulation); G32 (Financial Risk and Risk Management)

1 Motivation

Since the introduction of the Value-at-Risk (VaR), risk forecasts have become a key input in financial decision making (Jorion, 2006). For instance, VaR and Expected Shortfall (ES) forecasts are now routinely used for setting capital requirements of financial institutions under the Basel framework (Liu and Stentoft, 2021). Consequently, a huge literature on forecasting VaR and ES has emerged (see, e.g., McNeil and Frey, 2000; Engle and Manganelli, 2004; Massacci, 2017; Patton et al., 2019). By definition, these measures are primarily designed to assess the riskiness of banks in isolation. Thus, these measures are well-suited to address microprudential objectives in banking regulation, that is, to limit risk taking of individual institutions.

However, in the aftermath of the financial crisis of 2007–09, macroprudential objectives have gained importance on the regulatory agenda (Acharya et al., 2012, 2017). While also attempting to limit risk taking of individual financial institutions, the macroprudential approach also takes into account the commonality of risk exposures among banks. For instance, a measure of interconnectedness of banks is now used under the Basel framework of the Basel Committee on Banking Supervision (2019, SCO40) to determine the global systemically important banks (G-SIBs), which are subjected to higher capital requirements. This new focus calls for systemic risk measures to accurately measure the interlinkages for which VaR and ES are unsuitable. Hence, a plethora of systemic risk measures is available by now (Giesecke and Kim, 2011; Chen et al., 2013; Adrian and Brunnermeier, 2016; Acharya et al., 2017).

One of the most popular systemic risk measures is the conditional VaR (CoVaR) of Adrian and Brunnermeier (2016). It is defined as a quantile of a financial loss (e.g., of an entire market), given a reference asset (e.g., a systemically important bank) is in distress, where the latter is measured as an exceedance of its VaR. Yet, while forecasting models and the asymptotic properties of forecasts are well explored for VaR and ES (Chan et al., 2007; Gao and Song, 2008; Wang and Zhao, 2016; Hoga, 2019), the models for CoVaR forecasting are hitherto rather ad-hoc and little is known about the consistency of the forecasts. In particular, DCC–GARCH models of Engle (2002) are popular due to their ability to accurately forecast conditional variance-covariance matrices (Laurent et al., 2012; Caporin and McAleer, 2014). However, as Francq and Zakoïan (2016, p. 620) point out, “[n]o formally established asymptotic results exist for the full estimation of the DCC […] models”; see also Darolles et al. (2018). This renders their use in forecasting systemic risk measures questionable. Moreover, there are additional problems associated with their use in systemic risk forecasting that stem from the non-uniqueness of the decomposition of the variance-covariance matrix (see Section 2.5). In sum, there is a need for multivariate models that can deliver accurate systemic risk forecasts with strong theoretical underpinnings.

The first main contribution of this paper is to introduce such dynamic, semiparametric models for the CoVaR, which we call CoCAViaR models, as they nest the classical CAViaR models of Engle and Manganelli (2004). In the spirit of Engle and Manganelli (2004) and Patton et al. (2019), we model the pair (VaR, CoVaR) depending on external covariates, past financial losses, and lagged (VaR, CoVaR). Our models are semiparametric in the sense that the quantities of interest (VaR and CoVaR) are modeled parametrically, yet no assumptions are placed on the remaining conditional distribution.

There are new challenges in modeling systemic risk vis-à-vis modeling univariate quantities such as VaR (Engle and Manganelli, 2004) and ES (Patton et al., 2019). Modeling VaR or (VaR, ES) requires to specify the univariate dynamics only. Yet, since CoVaR measures the interlinkage of bivariate random variables, it becomes necessary to model the co-movements as well. We explore different models for doing so, and identify several competitive performers in our empirical application.

Our second main contribution is to propose an estimator for the model parameters and derive its large sample properties. The main technical hurdle to overcome in developing asymptotic theory is that—unlike VaR and (VaR, ES)—the pair (VaR, CoVaR) fails to be elicitable, such that no real-valued scoring function exists that is uniquely minimized by the true report (Fissler and Hoga, 2022). This renders standard M-estimation—adopted by Engle and Manganelli (2004), Dimitriadis and Bayer (2019) and Patton et al. (2019)—infeasible (Dimitriadis et al., 2022, Theorem 1). Instead, we exploit the multi-objective elicitability of (VaR, CoVaR) (Fissler and Hoga, 2022). This property suggests a two-step M-estimator. In the first step, the score in the VaR component is minimized, and then the CoVaR score is minimized in the second step. We show consistency and asymptotic normality of our two-step M-estimator and propose valid inference based on consistent estimation of the asymptotic variance-covariance matrix. Our proofs show how to deal with non-smooth and discontinuous objective functions in the context of two-step M-estimation for dynamic models (based on past model values). We speculate that our proof strategy may also be used elsewhere and, therefore, may be of independent interest. We provide an open source R package (Dimitriadis and Hoga, 2022) that contains the implementation of our two-step M-estimator together with inference tools for the flexible class of dynamic CoVaR models.

Simulations confirm the good finite-sample properties of our estimator. While the parameters of the CoCAViaR models can be estimated accurately in realistic settings, reliable inference for the model parameters requires large sample sizes or moderate probability levels. However, as the main use of our CoCAViaR models is in forecasting, inference for the model parameters is of lesser importance than consistent estimates.

In the empirical application, we compare CoVaR forecasts issued from our CoCAViaR models with those from benchmark DCC–GARCH models. We do so for the four most systemically risky US banks according to the Financial Stability Board (2021), whose impact on a broader market index is assessed by CoVaR. Our various CoCAViaR model specifications tend to outperform the DCC–GARCH benchmarks, particularly in the CoVaR forecasts but also in the VaR component. Often, these differences in predictive ability are also statistically significant, as judged by the Diebold and Mariano (1995)-type comparative backtest of Fissler and Hoga (2022). The superiority of our proposals may be explained by two reasons. First, our CoCAViaR specifications are specifically tailored to model the quantities of interest (VaR and CoVaR), whereas multivariate GARCH processes focus on modeling the complete predictive distribution. Second, our estimation technique is tailored to provide an accurate description of the (VaR, CoVaR) evolution. In particular, the estimator is not too strongly influenced by center-of-the-distribution observations as, e.g., standard estimators of multivariate GARCH models.

The rest of the paper is structured as follows. Section 2 formally introduces CoVaR, our modeling framework and the appertaining parameter estimator. It also gives large sample results for our estimator, and points out the difficulties of DCC–GARCH models to predict CoVaR. We illustrate the finite-sample properties of our estimator in Section 3. Section 4 presents the empirical application. The final Section 5 concludes. The main proofs are relegated to the Appendix, and additional details are given in the Supplementary Material, which also verifies our model assumptions for CCC–GARCH models and generalizes our consistency result to arbitrary starting values.

2 Modeling and Estimation

2.1 The CoVaR

Throughout the paper, we consider a sample of size of the bivariate series . Specifically, stands for the log-losses of interest (e.g., system-wide losses in the financial system) and are the log-losses of some reference position (e.g., the losses of a bank’s shares). Here, log-losses are simply the negated log-returns. Let denote some time- information set to be specified below. Define , where with denotes the -quantile of the (absolutely continuous) distribution , and denotes the conditional distribution of given . The stress event that is considered in the definition of the CoVaR is that the loss of the reference position exceeds its VaR, i.e., . With our orientation of denoting financial losses, we commonly consider values for close to one, such as . For we define , where

for a joint distribution function with marginals and . Again, we usually consider values of close to one. If we simply write , and for we simply have . Note that our definition of CoVaR deviates from the original one of Adrian and Brunnermeier (2016), who used as the stress event. This latter choice is problematic because it often has probability zero and it does not fully incorporate all tail events of . Thus, we follow Girardi and Tolga Ergün (2013) and Nolde and Zhang (2020) in using the above alternative definition.

2.2 Dynamic Models for VaR and CoVaR

In the spirit of Engle and Manganelli (2004) and Patton et al. (2019), we consider semiparametric models for the pair (VaR, CoVaR) of the general form

| (1) |

where is some (possibly multivariate) exogenous covariate vector. Throughout the paper, we assume that the model in (1) is correctly specified in the sense that there exist true parameter values and such that

| (2) |

almost surely (a.s.), where .

A few comments on our modeling approach are in order. First, the fact that the VaR model does not depend on the CoVaR parameters renders our two-step estimator (introduced in the next subsection) feasible; see Section 2.3 for more detail. In contrast, our two-step estimator is in principle compatible with letting depend on . This would, however, come at the cost of a further explosion of technicality in the proofs, without any offsetting improvements (in terms of predictive accuracy) of the resulting models; see the empirical application in Section 4.

Second, our model is semiparametric in the sense that—while the model dynamics are governed by the parameters and —we impose no additional distributional assumption on the innovations driving the evolution of .

Third, besides the full history of lagged values of , and , the model in (1) depends on the (correctly specified) initial values and . Thus, our setup allows for the inclusion of lagged (VaR, CoVaR); see Example 1 below for details. Equivalently, the model could be defined to depend on the infinite past of , and , which would be in line with the rest of the related literature developing dynamic models for quantile-related quantities (Engle and Manganelli, 2004; White et al., 2015; Patton et al., 2019; Catania and Luati, 2022). However, in contrast to the extant literature, our definition in (1) allows for a clearer discussion of the implications of starting values for estimation; see also Remark 1.

Fourth, the model in (1) generalizes classical (time-series) quantile regressions based on lagged values of , and the covariate vector . Also, the “VAR for VaR” models (of dimension two) of White et al. (2015) are nested by choosing such that the CoVaR simply becomes the VaR of .

Example 1.

The general formulation of our model class in (1) allows for dynamic models, where (VaR, CoVaR) may depend on their lags. E.g., it nests models of the form

| (3) |

with parameters , that can be collected in and . Borrowing terminology from Engle and Manganelli (2004), we call models of the form (3) Symmetric Absolute Value (SAV) CoCAViaR models. Of course, our restriction that () only depends on () implies that the matrix is diagonal (i.e., ) to facilitate two-step M-estimation.

The models of Example 1 are correctly specified under a type of Jeantheau’s (1998) extended constant conditional correlation (ECCC) process, that has been studied extensively in the literature (He and Teräsvirta, 2004; Conrad and Karanasos, 2010):

| (4) |

where , . In (4), the -measurable conditional volatilities and are independent of the independent and identically distributed (i.i.d.) innovations , where denotes a generic absolutely continuous, bivariate distribution with zero mean and covariance matrix , . We deviate from Jeantheau (1998) by using absolute (instead of squared) returns as drivers of volatility, since these have more predictive content for volatility (Forsberg and Ghysels, 2007). Model (4) implies the (VaR, CoVaR) dynamics in (3), where the true model parameters of the model in (3) arise as transformations of .111 Multiplying the rows of the volatility equation in (4) by the true VaR and CoVaR of the innovations respectively gives that and , where is the -VaR of and the -CoVaR of the pair , whose analytical form is given in Mainik and Schaanning (2014, Theorem 3.1 (b)).

In our simulations in Section 3, we use (a restricted version of) model (4) to generate data to assess how well our two-step M-estimator performs. In our empirical application, we consider various SAV CoCAViaR specifications based on zero restrictions in and as well as generalizations to so-called “asymmetric slope” models based on the positive and negative components of and instead of on their absolute values.

2.3 Parameter Estimation

We now introduce estimators of the unknown parameters and . As we consider M-estimation in this paper, we require a to-be-minimized objective (or also: scoring) function. However, as pointed out in the Motivation, there is no real-valued scoring function associated with the pair (VaR, CoVaR). Dimitriadis et al. (2022, Theorem 1) show that the existence of such a (consistent) scoring function is a necessary condition for consistent M-estimation of semiparametric models. To overcome this drawback, Fissler and Hoga (2022) propose to consider a -valued scoring function in the closely related context of forecast evaluation. To be able to compare forecasts, has to be equipped with an order, and Fissler and Hoga (2022) show that the lexicographic order is suitable for that purpose. Specifically, they show that (under some regularity conditions) the expectation of the -valued scoring function

| (5) |

is minimized by the true VaR and CoVaR with respect to the lexicographic order. That is, for all ,

where if or ( and ). Note that in (5) is the standard tick-loss function known from quantile regression. Clearly, is similar in structure to , with the only difference being the indicator that restricts the evaluation to observations with VaR exceedances in the first component. In the related literature, these scoring functions are often also called loss functions (Gneiting, 2011). To avoid confusion with financial “losses”, we adhere to the term “scoring function”.

The definition of the lexicographic order suggests the following two-step M-estimator of and . In the first step, we use

such that the parameters are chosen to minimize the average empirical score in the VaR component for some parameter space . For the VaR model , this is the quantile regression estimator of Engle and Manganelli (2004).

With the estimate at hand, the lexicographic order then suggests to minimize the average empirical score in the second component via

for some CoVaR parameter space . For this two-step estimator to be feasible, the requirement that the VaR evolution does not depend on is essential. Section 2.4.2 shows that the presence of in the minimization problem impacts the asymptotic variance of . Of course, this is usually the case for two-step estimators (Newey and McFadden, 1994, Section 6).

2.4 Asymptotic Properties of the Estimators

2.4.1 Consistency

We first show consistency of our two-step M-estimators and . To do so, we introduce several regularity conditions in Assumption 1, where is some large positive constant, and denotes the Euclidean norm when is a vector, and the Frobenius norm when is matrix-valued. The joint cumulative distribution function (c.d.f.) of is denoted by , and its Lebesgue density (which we assume exists) by . Similarly, () denotes the distribution (density) function of for . For sufficiently smooth functions , we denote the -gradient by , its transpose by and the -Hessian by .

Assumption 1.

-

(i).

The models and are correctly specified in the sense of (2). Furthermore, for all implies that , and for all implies that .

-

(ii).

is strictly stationary.

-

(iii).

For all , belongs to a class of distributions on that possesses a positive Lebesgue density for all such that . Moreover, for all .

-

(iv).

is compact, where and .

-

(v).

obeys the uniform law of large numbers (ULLN) in .

-

(vi).

For all , and are -measurable and a.s. continuous in and .

-

(vii).

For all , is continuously differentiable on .

-

(viii).

There exists a neighborhood of , such that for all elements of that neighborhood. Furthermore, for all , and for all .

-

(ix).

, , , , for some .

In Assumption 1, item (i) ensures identification of the true parameters and item (ii) is a standard stationarity condition. Item (iii) ensures—among other things—strict (multi-objective) consistency of the scoring function given in (5); see Fissler and Hoga (2022, Theorem 4.2) for details. Compactness in (iv) is a standard requirement in extremum estimation; see Newey and McFadden (1994). Assumption 1 (v) is also a standard condition, imposed for instance by Engle and Manganelli (2004, Assumption C6) and Patton et al. (2019, Assumption 1 (A)). It can be verified using, e.g., Lemma 2.8 in Newey and McFadden (1994) or Theorem 21.9 in Davidson (1994). The final items (vi)–(ix) are smoothness conditions on the model. See Remark 3 and Supplement G for a verification of these conditions for CCC–GARCH models of Bollerslev (1990).

Our first main theoretical result establishes the consistency of and :

Theorem 1.

Suppose Assumption 1 holds. Then, as , and .

The proof of Theorem 1 proceeds by verifying the conditions of Theorem 2.1 in Newey and McFadden (1994), and can be found in Appendix A. The result that is essentially a version of Theorem 1 in Engle and Manganelli (2004); the only difference being that our regularity conditions are slightly more involved, since we also show that .

Remark 1.

By imposing (2), we follow the related literature on dynamic quantile models (Engle and Manganelli, 2004; White et al., 2015; Patton et al., 2019; Catania and Luati, 2022) and assume that the true starting values and are known. We generalize the consistency result of Theorem 1 in Supplement F to arbitrary starting values for an empirically relevant model class that is linear in the lagged model values, nests the models in (3) and contains all models used in our simulations and empirical application. For this result, it essentially suffices to extend Assumption 1 by the well-known condition that the spectral radius of the parameter matrix in (3) is strictly smaller one. We mention that starting values are of concern only in autoregressive-type models. For moving average-type models (e.g., model (3) with ) they are irrelevant.

2.4.2 Asymptotic Normality

To show asymptotic normality of our estimators, we have to impose additional regularity conditions on the model. We denote the partial derivative of with respect to the -th argument by for .

Assumption 2.

-

(i).

and , where denotes the interior of a set.

-

(ii).

and are a.s. twice continuously differentiable on and , respectively.

-

(iii).

There exists a neighborhood of , such that , for all elements , of that neighborhood.

-

(iv).

There exists a neighborhood of , such that , , for all elements , of that neighborhood.

-

(v).

There exists some , such that , , , , , .

-

(vi).

, , , and for all in the support of .

-

(vii).

, , for .

-

(viii).

The matrices

are positive definite, and has full rank.

-

(ix).

and a.s., as .

-

(x).

is -mixing with mixing coefficients satisfying for some .

Item (i) of Assumption 2 is essential for asymptotic normality of extremum estimators. In fact, examples of non-normal estimators can easily be constructed when the true parameter is on the boundary (Newey and McFadden, 1994, p. 2144). Items (ii)–(v) are again smoothness conditions on the model that are similar in spirit to those of Engle and Manganelli (2004) and Patton et al. (2019). Item (vi) is a (uniform) Lipschitz condition on derivatives of the joint conditional c.d.f. and item (vii) provides convenient bounds on the densities and partial derivatives. The positive definiteness of and in item (viii) is a sufficient condition for the existence of a unique minimum of the expected population loss with respect to the lexicographic order. Item (ix) bounds the number of exact equalities of financial losses and (VaR, CoVaR) model values; see also Patton et al. (2019). Finally, item (x) is a standard mixing condition that ensures validity of a suitable central limit theorem; see Lemmas V.2 and C.2.

The proof of Theorem 2 is in Appendix B. Similarly as in Engle and Manganelli (2004) and Patton et al. (2019), the key step in the proof is to apply Lemma A.1 of Weiss (1991). However, since we consider a two-step estimator, our arguments necessarily extend those of the aforementioned authors, who only consider one-step estimators. Specifically, in showing asymptotic normality of one has to take into account the fact that it depends on the first-step estimate . This complicates the technical treatment and, in fact, increases the asymptotic variance relative to the case where is known. In more detail, our proof shows that when the true value of were known in the second step, the asymptotic variance of would be given by . Comparing this with the asymptotic variance from Theorem 2 demonstrates that, as expected, the first-stage estimation has an asymptotic effect on . More precisely, the first-stage estimation increases the asymptotic variance (in terms of the Loewner order), because

is positive semi-definite. This is akin to two-step GMM-estimation, where uncorrelated first- and second-step moment conditions imply an increased variance of the second-step estimator; see Newey and McFadden (1994, Eq. (6.9)). In our context of two-step M-estimation, the derivatives (with respect to the parameters) of the two components of the scoring functions in (5) play the role of these moment conditions. This uncorrelatedness is the reason for the off-diagonal zero blocks in the matrix . See in particular the proof of Theorem 2 in Appendix B.2.

Remark 2.

It is easy to see from the proof of Theorem 2 that joint normality of the parameter estimators also holds. Specifically, as ,

This result may be useful when testing joint restrictions on the parameters, such as the significance of some (macroeconomic or finance) variables in explaining VaR and CoVaR dynamics.

Remark 3.

The Assumptions 1 and 2 contain primitive assumptions (such as the differentiability of the functions and ) and high-level assumptions (such as the ULLN for the scores). We exemplarily verify all these assumptions for the CCC–GARCH model of Bollerslev (1990) in Supplement G. The results imply that while asymptotic normality of standard estimators in CCC–GARCH models often requires finite fourth moments of the observations, we only require finiteness of -th moments for some . This may be seen as a further advantage of our estimators, because stringent moment conditions are often empirically binding in financial applications.

2.4.3 Consistent Estimation of the Asymptotic Variance

To draw inference on the model parameters, we require consistent estimates of the asymptotic variances appearing in the limiting distributions of Theorem 2. For the VaR parameters, these are well-explored. For instance, Engle and Manganelli (2004) and Patton et al. (2019) estimate and via

respectively, where is a (possibly stochastic) bandwidth. As we are mainly interested in the CoVaR parameters, we have to estimate and . For the latter matrix, we only need to estimate via

The estimators for and are more involved and are given by

where is another (possibly stochastic) bandwidth. Footnote 2 reports the data-dependent bandwidth choices we use in the empirical parts of the paper. These estimators rely on kernel density estimates of the derivatives of the conditional c.d.f., and use a rectangular kernel. However, at the expense of some additional technicality other kernels may also be considered.

Assumption 3.

-

(i).

It holds for () that , where the non-stochastic satisfies and , as .

-

(ii).

.

-

(iii).

.

-

(iv).

.

-

(v).

, .

2.5 CoVaR Forecasting with Multivariate GARCH Models

This section points out the difficulties of multivariate volatility models in computing CoVaR. By doing so, it sheds some light on the advantages of our modeling approach.

Example 2.

Suppose that financial losses are generated by for some positive-definite, -measurable and , independent of , where is some generic distribution. Then, the conditional variance-covariance matrix is . Much like univariate GARCH processes model the conditional variance, multivariate GARCH models—such as the DCC–GARCH of Engle (2002) and the corrected DCC–GARCH of Aielli (2013)—directly model the conditional variance-covariance matrix . While for many applications—e.g., portfolio construction as in Hautsch et al. (2015)— is the object of interest, CoVaR forecasting explicitly requires to be specified. See Supplement H for details on how CoVaR forecasts can be extracted from a DCC–GARCH model.

However, for a given , there exist infinitely many choices of satisfying the decomposition , such as the symmetric square root implied by the eigenvalue decomposition () or the lower triangular matrix of the Cholesky decomposition (). The problem is that each possibility, while implying the same variance-covariance dynamics , implies different values for the CoVaR. E.g., consider

and with standardized -distributed and that are independent of each other. Then, for the model () based on the symmetric (lower triangular) decomposition, we obtain (). Thus, CoVaR forecasts depend intimately on the decomposition of , on which typical multivariate GARCH models stay silent. Thus, in principle, any GARCH-type model for may be consistent with an infinite number of CoVaR forecasts (depending on ), thus imposing an unsatisfactory ambiguity when applied to CoVaR forecasting.

We mention that the issue raised in Example 2 has not kept researchers from using standard multivariate volatility models for systemic risk forecasting. For instance, Girardi and Tolga Ergün (2013) and Nolde and Zhang (2020) use Engle’s (2002) DCC–GARCH model for CoVaR forecasting. Girardi and Tolga Ergün (2013) leave open which they use (symmetric, lower triangular etc.). Nolde and Zhang (2020) explicitly use a lower triangular . Specifically, Nolde and Zhang (2020) model the loss of the broader market and that of some individual unit , i.e., the opposite scenario as we consider in our empirical applications. They do so using the structural model

based on the lower-triangular matrix from the Cholesky decomposition of the variance-covariance matrix . In such a setting it may be acceptable to assume that the individual shock does not impact the market losses, as the individual institution is very small relative to the market. However, when comparing systemic risk contributions across a handful of business units of comparable size (e.g., different trading desks), such an assumption may be untenable, and a different modeling approach may be needed. Yet, which one exactly may be difficult to say. Our approach sidesteps these difficulties by directly modeling CoVaR (and VaR).

3 Simulations

Replication material for the simulations and the applications in Section 4 is available on Github under https://github.com/TimoDimi/replication_CoQR. It draws on the corresponding open source package CoQR (Dimitriadis and Hoga, 2022) implemented in R (R Core Team, 2022).

| VaR | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bias | M Bias | CI | Bias | M Bias | CI | Bias | M Bias | CI | |||||||||||

| 0.90 | 500 | 0.0258 | 0.0029 | 0.080 | 0.128 | 0.96 | 0.0132 | 0.0004 | 0.109 | 0.143 | 0.95 | 0.0828 | 0.0143 | 0.256 | 0.378 | 0.95 | |||

| 1000 | 0.0126 | 0.0008 | 0.050 | 0.094 | 0.98 | 0.0079 | 0.0004 | 0.080 | 0.100 | 0.94 | 0.0412 | 0.0089 | 0.167 | 0.278 | 0.97 | ||||

| 2000 | 0.0063 | 0.0004 | 0.031 | 0.067 | 0.99 | 0.0049 | 0.0017 | 0.055 | 0.072 | 0.96 | 0.0208 | 0.0049 | 0.107 | 0.200 | 0.98 | ||||

| 4000 | 0.0029 | 0.0004 | 0.019 | 0.047 | 1.00 | 0.0030 | 0.0009 | 0.039 | 0.051 | 0.96 | 0.0101 | 0.0042 | 0.067 | 0.140 | 0.99 | ||||

| 0.95 | 500 | 0.0355 | 0.0044 | 0.106 | 0.179 | 0.96 | 0.0217 | 0.0026 | 0.148 | 0.195 | 0.94 | 0.0861 | 0.0217 | 0.253 | 0.396 | 0.94 | |||

| 1000 | 0.0200 | 0.0022 | 0.074 | 0.130 | 0.98 | 0.0118 | 0.0004 | 0.108 | 0.137 | 0.93 | 0.0479 | 0.0099 | 0.181 | 0.286 | 0.96 | ||||

| 2000 | 0.0086 | 0.0004 | 0.041 | 0.092 | 0.99 | 0.0050 | 0.0002 | 0.075 | 0.098 | 0.95 | 0.0207 | 0.0044 | 0.106 | 0.205 | 0.98 | ||||

| 4000 | 0.0040 | 0.0001 | 0.026 | 0.065 | 1.00 | 0.0030 | 0.0004 | 0.055 | 0.069 | 0.95 | 0.0099 | 0.0019 | 0.070 | 0.145 | 0.99 | ||||

| CoVaR | |||||||||||||||||||

| Bias | M Bias | CI | Bias | M Bias | CI | Bias | M Bias | CI | |||||||||||

| 0.90 | 500 | 0.1766 | 0.0644 | 0.241 | 0.254 | 0.82 | 0.0573 | 0.0388 | 0.459 | 0.520 | 0.89 | 0.5344 | 0.2664 | 0.660 | 0.727 | 0.79 | |||

| 1000 | 0.1326 | 0.0255 | 0.218 | 0.206 | 0.85 | 0.0567 | 0.0289 | 0.301 | 0.351 | 0.90 | 0.4001 | 0.1266 | 0.606 | 0.598 | 0.82 | ||||

| 2000 | 0.0896 | 0.0096 | 0.183 | 0.159 | 0.89 | 0.0425 | 0.0225 | 0.206 | 0.246 | 0.91 | 0.2708 | 0.0563 | 0.512 | 0.463 | 0.86 | ||||

| 4000 | 0.0417 | 0.0006 | 0.124 | 0.122 | 0.93 | 0.0285 | 0.0114 | 0.137 | 0.176 | 0.93 | 0.1292 | 0.0140 | 0.360 | 0.359 | 0.92 | ||||

| 0.95 | 500 | 0.2651 | 0.1578 | 0.337 | 0.383 | 0.82 | 0.0809 | 0.0384 | 0.958 | 0.982 | 0.87 | 0.6146 | 0.4355 | 0.666 | 0.833 | 0.78 | |||

| 1000 | 0.2403 | 0.0956 | 0.330 | 0.330 | 0.82 | 0.0925 | 0.0371 | 0.661 | 0.689 | 0.86 | 0.5325 | 0.2868 | 0.650 | 0.709 | 0.79 | ||||

| 2000 | 0.1942 | 0.0400 | 0.307 | 0.274 | 0.83 | 0.0769 | 0.0400 | 0.454 | 0.505 | 0.87 | 0.4271 | 0.1475 | 0.615 | 0.586 | 0.81 | ||||

| 4000 | 0.1380 | 0.0165 | 0.265 | 0.228 | 0.86 | 0.0635 | 0.0235 | 0.306 | 0.361 | 0.89 | 0.3042 | 0.0666 | 0.545 | 0.480 | 0.84 | ||||

Here, we consider estimation of a dynamic SAV CoCAViaR model given in (3). For this, we simulate from the absolute value ECCC model in (4). We choose the parameter values , , and let be the multivariate (marginally standardized) -distribution with degrees of freedom and a residual correlation of . The off-diagonal zero-restrictions in and result in (more or less) the classic CCC–GARCH model of Bollerslev (1990). Recall that is essential for our two-step M-estimator, whereas just facilitates the derivation of the asymptotic theory. We estimate the SAV-diag CoCAViaR model, which arises for diagonal and in (3). (Table 2 below provides a complete nomenclature of CoCAViaR models considered in this paper.) Therefore, the to-be-estimated parameters are and , whose true values can be obtained from , and as in footnote 1.

Table 1 shows simulation results for the dynamic CoCAViaR model based on replications for the choices and sample sizes of . The asymptotic variance-covariance matrices are estimated as detailed in Section 2.4.3. Our (stochastic) bandwidth choices follow Koenker (2005) and Machado and Santos Silva (2013).222Formally, we let where refers to the sample median absolute deviation, and and denote the density and quantile functions of the standard normal distribution. The choice of is a straightforward adaptation for the density at the CoVaR, which is simply estimated as the VaR at level of only observations. A formal description of the table columns is given in the table caption.

The columns reporting the (average and median) bias and the standard deviations confirm the consistency of the estimator. In general, the VaR parameters have a smaller empirical bias than the CoVaR parameters, which is not surprising given that CoVaR is further out in the tail and, hence, subject to larger estimation uncertainty. Furthermore, the average bias is often larger than the median bias indicating that the empirical distributions of the parameter estimates are still subject to some skewness or outliers. Notice that even for the largest sample size of for our choice of , the CoVaR model is essentially estimated as a -quantile based on an effective sample size of only observations, which is an inherently difficult task. We further see that sample sizes of around 2000 days are required to reliably estimate the models for these extreme levels. This is especially true for the CoVaR parameters.

The results on the estimated standard deviations and the confidence interval coverage rates show that asymptotic variance-covariance estimation is a very difficult task for (Co)CAViaR models. The empirical standard errors are somewhat overestimated for the VaR parameters in Table 1, whereas they are interestingly more accurate for the CoVaR parameters. While the confidence intervals for the VaR parameters are rather conservative, the ones for CoVaR display some undercoverage for the extreme probability levels of , and exhibit almost correct coverage for . While this shows the need for future research on improving the estimation accuracy of the asymptotic variance-covariance matrix for dynamic (Co)CAViaR models, their main purpose lies in prediction and, hence, inference is of lesser importance.

4 Application: CoVaR Forecasting with CoCAViaR Models

For the empirical forecasting application, we use daily close-to-close log-losses from January 4, 2000 until December 31, 2021 with a total of trading days, obtained from the financial data provider Refinitiv. We use data for the S&P 500 index as our , and for the S&P 500 Financials (SPF) that represents the financial sector of the S&P 500, Bank of America (BAC), Citigroup (C), Goldman Sachs (GS) and JPMorgan Chase (JPM). The latter institutions are the four systemically most important US banks according to the Financial Stability Board (2021). With these variables, measures the spillover risk of the financial system/institution to the overall economy. We focus on the probability levels and estimate all models using a rolling window with estimation samples of length 3000 days. To reduce the computational burden, we only re-estimate the models every 100 days.

We consider 12 forecasting models in total. The first three candidate models are from the general class of SAV CoCAViaR models given in (3). The acronym SAV indicates that the driving forces of the models are the absolute values of the log-losses, and . The top panel of Table 2 summarizes which covariates are included in each of the employed SAV CoCAViaR model specifications. The suffix “diag” in the first model indicates that the off-diagonal elements of the parameter matrices and are set to zero. Similarly, “full” indicates that the full specification of (3) is used (only restricting to facilitate two-step M-estimation) and the suffix “fullA” indicates that the full matrix is considered, while is restricted to be a diagonal matrix.

Notice that the SAV-full model is not covered by our modeling framework (1), because the CoVaR model depends on lags of , such that is a function of the VaR parameters as well. Nonetheless, we include this specification here to show that the gains of this extension may be non-existent in practice.

| Covariates | ||||||||||||

| CoCAViaR Model | ||||||||||||

| SAV-diag | ||||||||||||

| SAV-fullA | ||||||||||||

| SAV-full | ||||||||||||

| AS-pos | ||||||||||||

| AS-signs | ||||||||||||

| AS-mixed | ||||||||||||

Along the lines of Engle and Manganelli (2004), we extend the CoCAViaR model class by using signed values of and to the Asymmetric Slope (AS) CoCAViaR models,

| (6) |

where are collected in the parameter vectors and . Here, we define and for . Parameter equalities in and can be used to generate absolute values and in (6). Intuitively, the positive values of and (i.e., financial losses in our orientation) are expected to contribute more to the future VaR and CoVaR than their negative values. This is much like large losses often have more predictive content for volatility than equally large gains in GJR–GARCH models of Glosten et al. (1993). The three model suffixes “pos”, “signs” and “mixed” in the bottom panel of Table 2 imply that for the first only the positive components are included, for the second both positive and negative components are used, and the latter one includes a mix of positive, negative and absolute value losses (see Table 2 for details).

| Estimated Model Parameters | |||||||||||||

| CoCAViaR Model | 1 | ||||||||||||

| SAV-diag | 0.019 | 0.096 | 0.947 | ||||||||||

| (0.169) | (0.073) | (0.056) | |||||||||||

| 0.060 | 0.751 | 0.834 | |||||||||||

| (0.775) | (0.592) | (0.163) | |||||||||||

| SAV-fullA | 0.022 | 0.096 | 0.031 | 0.939 | |||||||||

| (0.213) | (0.079) | (0.220) | (0.079) | ||||||||||

| 0.171 | 0.106 | 0.468 | 0.798 | ||||||||||

| (0.974) | (0.197) | (0.625) | (0.304) | ||||||||||

| SAV-full | 0.022 | 0.096 | 0.031 | 0.939 | |||||||||

| (0.213) | (0.079) | (0.220) | (0.079) | ||||||||||

| 0.148 | 0.073 | 0.685 | 0.827 | ||||||||||

| (0.856) | (0.136) | (0.718) | (0.163) | (0.280) | |||||||||

| AS-pos | 0.011 | 0.091 | 0.080 | 0.965 | |||||||||

| (0.176) | (0.078) | (0.175) | (0.059) | ||||||||||

| 0.149 | 0.028 | 0.627 | 0.880 | ||||||||||

| (0.569) | (0.420) | (0.524) | (0.160) | ||||||||||

| AS-signs | 0.023 | 0.132 | 0.051 | 0.950 | |||||||||

| (0.218) | (0.069) | (0.159) | (0.074) | ||||||||||

| 0.138 | 0.112 | 0.075 | 0.349 | 0.909 | |||||||||

| (0.430) | (0.494) | (0.149) | (0.492) | (0.613) | (0.150) | ||||||||

| AS-mixed | 0.027 | 0.152 | 0.071 | 0.018 | 0.935 | ||||||||

| (0.328) | (0.079) | (0.215) | (0.224) | (0.121) | |||||||||

| 0.228 | 0.110 | 0.705 | 0.027 | 0.811 | |||||||||

| (0.687) | (0.116) | (0.545) | (0.554) | (0.149) | |||||||||

Table 3 reports the estimated parameters together with their standard errors for the six CoCAViaR model specifications. The results are based on the initial estimation window of 3000 observations. The autoregressive coefficients are between 0.8 and 0.97, and highly significant. The other coefficients are all barely significant, but their direction is very reasonable. The “cross-terms” seem to be less important in general. From the SAV-full and AS-mixed models, we infer that is more important in than is for . Furthermore, in the SAV-full model, the lagged has no significant influence on , which is also reflected by the model’s poor forecasting behavior; see Table 4 below. Hence, the additional generality of the SAV-full model (where depends on ) does not seem be relevant empirically. Consistent with the idea of Glosten et al. (1993) that losses have a larger impact on volatility than do equally large gains, we find that losses are more important than gains in predicting systemic risk in the AS models; especially and in the CoVaR equation of the AS-mixed model.

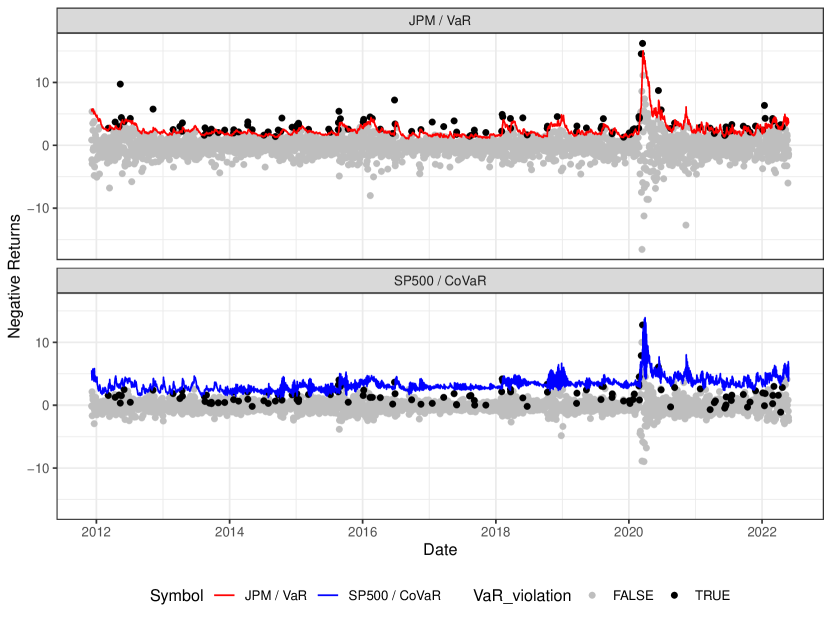

Figure 1 illustrates the rolling window forecasts from the SAV-fullA CoCAViaR model for the evaluation window ranging from December 6, 2011 until December 31, 2021. The upper panel shows the log-losses of JPMorgan Chase—the systemically most important bank according to the Financial Stability Board (2021)—together with its VaR forecasts. Losses exceeding the VaR forecasts are highlighted in black, which correspond to days with an (out-of-sample) stress event in the definition of the CoVaR in Section 2.1. The lower panel shows the log-losses of the S&P 500 together with the model’s CoVaR forecasts. There, the log-losses of days with a VaR exceedance (of JPMorgan Chase) are displayed in black, such that the CoVaR forecasts can be interpreted as quantile forecasts among these days with VaR exceedances.

As competitors for our six CoCAViaR models, we use six different DCC–GARCH specifications. DCC–GARCH models have attained benchmark status, because of their accurate variance-covariance matrix predictions (Laurent et al., 2012; Caporin and McAleer, 2014). Particularly, we use three DCC–GARCH model specifications, containing two standard DCC–GARCH(1,1) models with multivariate Gaussian and -distributed innovations respectively and a DCC specification based on a univariate GJR–GARCH(1,1) model. All models are estimated by maximum likelihood. Following Section 2.5, the VaR and CoVaR forecasts are obtained by combining all three model specifications with a symmetric and a Cholesky decomposition of the forecasted variance-covariance matrices, yielding six sets of forecasts. We refer to Supplement H for details on the CoVaR computations.

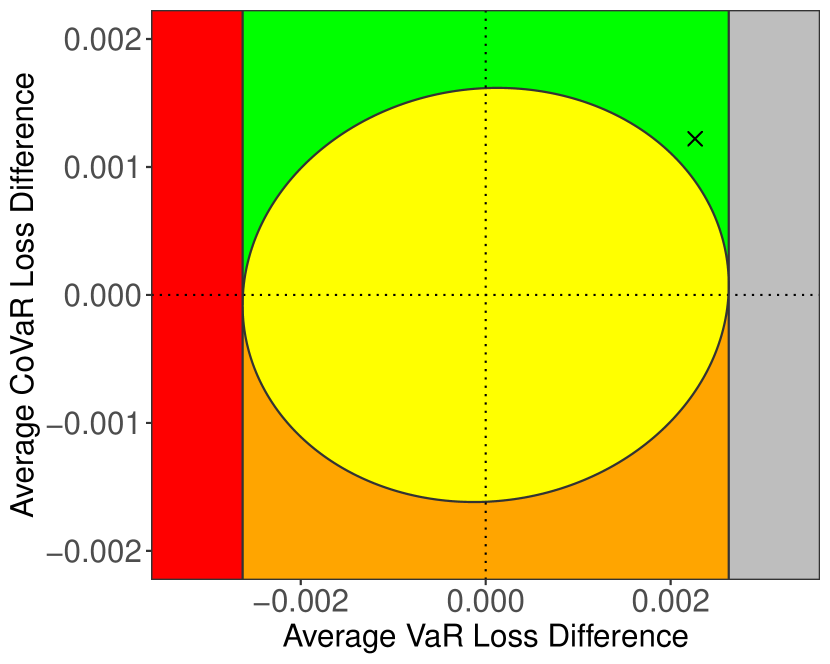

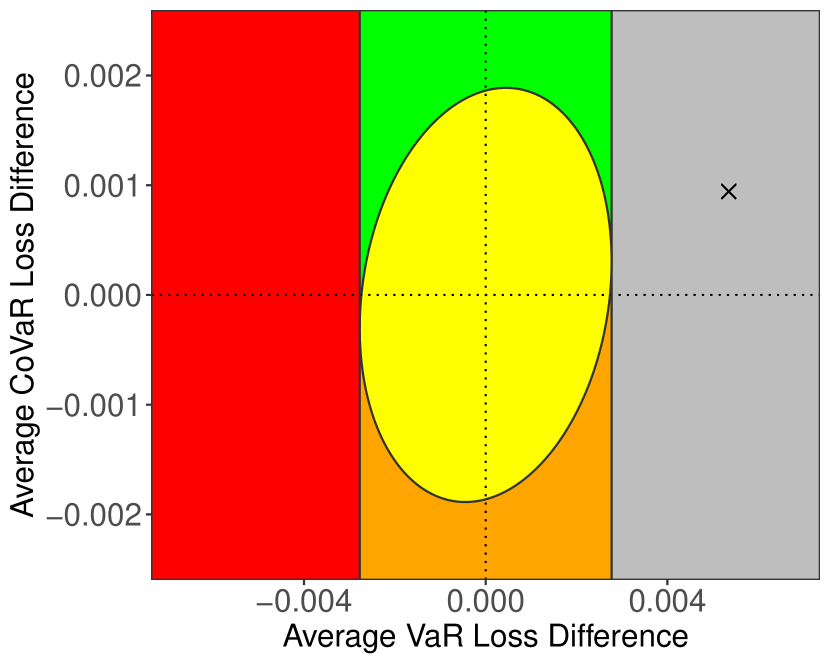

The multi-objective elicitability of (VaR, CoVaR) complicates inference on the predictive ability of forecasts, since the scoring function in (5) is bivariate such that standard Diebold and Mariano (1995) tests—based on scalar scores—cannot be applied. We follow Fissler and Hoga (2022) and their “one and a half-sided” tests together with their extended traffic light system that we illustrate exemplarily in Figure 2 for two models. These tests require to fix a baseline model, and we arbitrarily choose the “DCC-t-Chol” model for all evaluations. Such a baseline model is necessary as classical extensions to multi-model forecast comparison methods as, e.g., the model confidence set of Hansen et al. (2011) are not available in the case of bivariate (multi-objective) scoring functions.

Multi-objective elicitability implies that the scores of two competing sequences of CoVaR forecasts can only be compared if their underlying VaR forecasts perform equally well. To obtain a reasonable finite-sample counterpart, Fissler and Hoga (2022) interpret this as an insignificant score difference in the standard Diebold and Mariano (1995) test for the VaR forecasts. Hence, the null that the expected VaR score differences (calculated based on the first component in (5)) are equal to zero cannot be rejected. The red zone in Figure 2 indicates that the baseline VaR is significantly superior, and the comparison model is rejected without consideration of its CoVaR forecasts. The grey zone indicates the reverse, while the three remaining zones in the intermediary corridor imply insignificant score differences of the VaR forecasts. Here, the orange zone implies that the baseline CoVaR is significantly superior (i.e., the CoVaR score differences based on the second component of (5) are smaller than zero in expectation), the green zone that the alternative model is superior and the yellow zone represents insignificant score differences. As the baseline is the “DCC-t-Chol” model, a comparison with our CoCAViaR models should ideally yield results in the green zone (which indicates superior CoVaR forecasts and comparable VaR forecasts) or in the grey zone (which implies superior VaR forecasts).

| VaR | CoVaR | Inference | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| model | score | rank | hits | score | rank | hits | zone | -value | ||||

| BAC | CoCAViaR-SAV-fullA | 2.060 | 6 | 4.5 | 5.913 | 1 | 7.9 | green | 0.01 | |||

| CoCAViaR-AS-pos | 2.062 | 7 | 4.9 | 6.793 | 2 | 6.5 | yellow | 0.11 | ||||

| CoCAViaR-SAV-diag | 2.096 | 12 | 4.7 | 6.977 | 3 | 7.6 | yellow | 0.18 | ||||

| CoCAViaR-AS-mixed | 2.041 | 1 | 4.9 | 7.019 | 4 | 6.4 | grey | 0.01 | ||||

| CoCAViaR-AS-signs | 2.043 | 4 | 5.0 | 7.228 | 5 | 7.1 | grey | 0.01 | ||||

| CoCAViaR-SAV-full | 2.060 | 6 | 4.5 | 7.609 | 6 | 8.8 | yellow | 0.30 | ||||

| DCC-n-Chol | 2.083 | 8 | 4.4 | 7.652 | 7 | 15.3 | green | 0.01 | ||||

| DCC-t-Chol | 2.086 | 10 | 4.6 | 8.109 | 8 | 14.5 | ||||||

| DCC-n-sym | 2.084 | 9 | 4.4 | 8.139 | 9 | 15.3 | yellow | 0.95 | ||||

| DCC-t-sym | 2.086 | 11 | 4.6 | 8.460 | 10 | 16.4 | yellow | 0.71 | ||||

| DCC-gjr-t-Chol | 2.043 | 3 | 4.6 | 8.635 | 11 | 13.7 | grey | 0.00 | ||||

| DCC-gjr-t-sym | 2.042 | 2 | 4.6 | 8.869 | 12 | 11.2 | grey | 0.00 | ||||

| C | CoCAViaR-SAV-full | 2.138 | 6 | 4.9 | 6.528 | 1 | 6.4 | yellow | 0.77 | |||

| CoCAViaR-SAV-diag | 2.134 | 5 | 5.0 | 6.568 | 2 | 7.9 | yellow | 0.13 | ||||

| CoCAViaR-AS-mixed | 2.127 | 4 | 5.1 | 6.608 | 3 | 5.4 | yellow | 0.15 | ||||

| CoCAViaR-SAV-fullA | 2.138 | 6 | 4.9 | 6.689 | 4 | 6.4 | yellow | 0.12 | ||||

| CoCAViaR-AS-pos | 2.158 | 12 | 5.2 | 6.705 | 5 | 5.3 | yellow | 0.19 | ||||

| CoCAViaR-AS-signs | 2.126 | 3 | 5.1 | 6.714 | 6 | 6.2 | yellow | 0.11 | ||||

| DCC-n-Chol | 2.141 | 8 | 4.9 | 7.516 | 7 | 10.4 | green | 0.01 | ||||

| DCC-t-Chol | 2.146 | 11 | 4.9 | 7.750 | 8 | 11.2 | ||||||

| DCC-gjr-t-Chol | 2.104 | 1 | 4.9 | 7.878 | 9 | 10.6 | grey | 0.01 | ||||

| DCC-n-sym | 2.141 | 9 | 5.0 | 8.035 | 10 | 11.8 | yellow | 0.42 | ||||

| DCC-gjr-t-sym | 2.107 | 2 | 5.2 | 8.331 | 11 | 10.7 | grey | 0.00 | ||||

| DCC-t-sym | 2.144 | 10 | 5.1 | 8.347 | 12 | 11.5 | yellow | 0.88 | ||||

| GS | CoCAViaR-SAV-fullA | 1.840 | 4 | 5.0 | 6.069 | 1 | 9.5 | green | 0.01 | |||

| CoCAViaR-AS-mixed | 1.818 | 1 | 5.0 | 6.460 | 2 | 4.0 | grey | 0.00 | ||||

| CoCAViaR-AS-pos | 1.820 | 2 | 4.9 | 6.572 | 3 | 7.2 | grey | 0.00 | ||||

| CoCAViaR-AS-signs | 1.838 | 3 | 5.1 | 6.855 | 4 | 3.9 | grey | 0.00 | ||||

| CoCAViaR-SAV-full | 1.840 | 4 | 5.0 | 7.313 | 5 | 12.7 | green | 0.05 | ||||

| CoCAViaR-SAV-diag | 1.879 | 8 | 4.9 | 7.338 | 6 | 8.1 | green | 0.02 | ||||

| DCC-n-sym | 1.888 | 9 | 4.7 | 8.485 | 7 | 14.3 | yellow | 0.14 | ||||

| DCC-t-sym | 1.890 | 10 | 4.9 | 9.081 | 8 | 13.8 | yellow | 0.31 | ||||

| DCC-n-Chol | 1.891 | 11 | 4.7 | 9.165 | 9 | 17.6 | yellow | 0.27 | ||||

| DCC-gjr-t-sym | 1.857 | 6 | 4.7 | 9.249 | 10 | 13.3 | grey | 0.00 | ||||

| DCC-t-Chol | 1.895 | 12 | 4.7 | 9.288 | 11 | 18.3 | ||||||

| DCC-gjr-t-Chol | 1.857 | 7 | 4.9 | 9.536 | 12 | 16.0 | grey | 0.00 | ||||

| JPM | CoCAViaR-SAV-fullA | 1.718 | 6 | 4.5 | 6.008 | 1 | 12.4 | green | 0.06 | |||

| CoCAViaR-AS-mixed | 1.686 | 2 | 4.5 | 6.402 | 2 | 7.0 | grey | 0.00 | ||||

| CoCAViaR-AS-signs | 1.685 | 1 | 4.6 | 6.628 | 3 | 6.8 | grey | 0.00 | ||||

| DCC-n-sym | 1.735 | 9 | 3.8 | 6.751 | 4 | 14.4 | green | 0.07 | ||||

| DCC-t-sym | 1.741 | 12 | 3.9 | 6.987 | 5 | 17.2 | yellow | 0.50 | ||||

| DCC-n-Chol | 1.733 | 8 | 3.9 | 7.034 | 6 | 18.2 | grey | 0.01 | ||||

| CoCAViaR-AS-pos | 1.708 | 5 | 5.2 | 7.209 | 7 | 6.9 | yellow | 0.15 | ||||

| DCC-t-Chol | 1.741 | 11 | 4.0 | 7.396 | 8 | 19.8 | ||||||

| CoCAViaR-SAV-diag | 1.737 | 10 | 4.7 | 7.443 | 9 | 8.5 | yellow | 0.98 | ||||

| DCC-gjr-t-Chol | 1.705 | 4 | 4.0 | 7.466 | 10 | 14.7 | grey | 0.02 | ||||

| DCC-gjr-t-sym | 1.704 | 3 | 4.0 | 7.666 | 11 | 11.9 | grey | 0.01 | ||||

| CoCAViaR-SAV-full | 1.718 | 6 | 4.5 | 9.250 | 12 | 14.2 | yellow | 0.15 | ||||

| SPF | CoCAViaR-SAV-fullA | 1.416 | 12 | 4.5 | 5.488 | 1 | 9.6 | green | 0.09 | |||

| CoCAViaR-AS-mixed | 1.389 | 4 | 4.9 | 5.865 | 2 | 7.2 | yellow | 0.26 | ||||

| CoCAViaR-AS-signs | 1.379 | 3 | 4.9 | 5.927 | 3 | 8.9 | grey | 0.03 | ||||

| CoCAViaR-SAV-diag | 1.409 | 10 | 4.7 | 6.078 | 4 | 7.6 | yellow | 0.22 | ||||

| CoCAViaR-AS-pos | 1.401 | 9 | 4.9 | 6.314 | 5 | 7.2 | yellow | 0.60 | ||||

| DCC-n-Chol | 1.395 | 6 | 4.4 | 6.514 | 6 | 15.3 | grey | 0.01 | ||||

| DCC-t-Chol | 1.400 | 8 | 4.4 | 6.830 | 7 | 17.9 | ||||||

| DCC-n-sym | 1.394 | 5 | 4.6 | 6.900 | 8 | 15.4 | yellow | 0.15 | ||||

| DCC-t-sym | 1.400 | 7 | 4.7 | 7.207 | 9 | 17.6 | yellow | 0.93 | ||||

| DCC-gjr-t-sym | 1.354 | 1 | 4.7 | 7.593 | 10 | 9.2 | grey | 0.00 | ||||

| DCC-gjr-t-Chol | 1.357 | 2 | 4.8 | 7.613 | 11 | 11.5 | grey | 0.00 | ||||

| CoCAViaR-SAV-full | 1.416 | 12 | 4.5 | 10.261 | 12 | 12.2 | yellow | 0.14 | ||||

Table 4 presents results on the forecast performance of all 12 models. For the VaR, we report the average VaR score (multiplied by 10 for better readability) using the first component of (5), its rank among the different models, and the “hits” as the percentage of days where the loss is larger than the VaR forecast, . For the CoVaR, we report the average CoVaR score using the second component (5) (multiplied by 1000 for better readability), the corresponding rank, and the CoVaR hits defined as the percentage of days where among all days with a VaR hit, i.e., the where . The VaR forecast should ideally be exceeded with probability , and on those days the CoVaR forecast should be exceeded with probability . The last two columns of Table 4 report results for the previously described one and a half-sided test of Fissler and Hoga (2022). There we use “DCC-t-Chol” as the baseline model, and report the test’s -value together with the resulting zone of their extended traffic light system. For each considered asset , we sort the table rows (i.e., the models) according to their CoVaR loss, as the CoVaR forecasts are of main interest in this section.

Overall, we find a superior forecasting performance of the CoCAViaR models for all five employed assets for compared to the DCC models. While the rankings of the VaR scores vary over the different assets, their superior forecasting performance is more substantial for the CoVaR. This is supported by CoVaR hits (corresponding to unconditional forecast calibration) much closer to the nominal level of than the DCC models, whose hit frequencies are almost all above . While none of the CoCAViaR models are significantly outperformed by being in the red or orange zones, some significantly outperform the baseline DCC model and are located in the green and grey zones. Also notice that among the CoCAViaR models, the SAV-full specification (not covered by our framework) often performs the poorest. Therefore, our modeling framework (1) seems to be sufficiently general to capture the salient features of (systemic) risk evolution through time.

The favorable performance of our CoCAViaR models may be explained as follows. First, DCC–GARCH forecasts of CoVaR intimately rely on the somewhat arbitrary decomposition of the conditional variance-covariance matrix, which is a problem that is sidestepped by our modeling approach; see Section 2.5. Second, our CoCAViaR specifications directly model the quantities of interest (VaR and CoVaR), whereas multivariate GARCH processes model the whole predictive density. Third, our estimators are tailored to accurately capture the (VaR, CoVaR) evolution and, hence, do not place undue emphasis on center-of-the-distribution observations. In contrast, estimators of DCC–GARCH models may trade off a better fit in the body of the distribution for a worse fit in the tails.

Among the CoCAViaR models, we find a better performance of the AS than the SAV models for the VaR, but a relatively comparable performance for CoVaR forecasting. A reason for this may be that the additional VaR parameters in the AS models are estimated with more precision and, hence, the predictive content of the positive/negative parts emerges more clearly than for CoVaR, where the effective sample size is much reduced. It is further noteworthy that the SAV-full CoCAViaR model, that includes the lagged VaR in the CoVaR model equation performs relatively poorly. This might be caused by a high co-linearity of the VaR and CoVaR models, and also shows that the restriction which we have to impose for our two-step M-estimator is likely to be unproblematic in practice.

5 Conclusion

Our first main contribution is to propose a flexible, semiparametric approach for modeling (VaR, CoVaR). To the extent that we only model (VaR, CoVaR) and not the full predictive distribution, we ‘let the tails speak for themselves’ (DuMouchel, 1983). As we find in an empirical application on the systemic riskiness of US financial institutions, this yields models that improve upon benchmark DCC–GARCH models in terms of predictive accuracy. As a second main contribution, we propose a two-step M-estimator for the model parameters and derive its large sample properties. From an econometric perspective, our proofs are non-standard since the loss function that has to be used for the CoVaR is not only non-smooth, but also discontinuous in the VaR model (parameter).

We expect our modeling framework to have applications beyond the one considered here, for instance in predictive CoVaR regressions as in Adrian and Brunnermeier (2016). Furthermore, in macroeconomics, Adrian et al. (2019, 2022) have recently drawn attention to tail risks and their interconnections by popularizing the Growth-at-Risk, which is simply the VaR of GDP growth. Hence, the modeling approach developed in this paper could be relevant for studying interconnections of macroeconomic risks. Much like Brownlees and Souza (2021) compared the predictive accuracy of Growth-at-Risk model, our model may be used as a competitor in Co-Growth-at-Risk comparisons.

Appendix A Proof of Theorem 1

-

Proof of Theorem 1::

Throughout the proof, denotes some large constant that may change from place to place. We prove both convergences by verifying conditions (i)–(iv) of Theorem 2.1 in Newey and McFadden (1994).

First, we prove . For condition (i), we have to show that

is uniquely minimized at . By Assumption 1 (iii) and from Fissler and Hoga (2022, Theorem 4.4) it follows that is uniquely minimized at , which equals under correct specification. By Assumptions 1 (i) and (vi), is then the unique minimizer of . By the law of the iterated expectations (LIE) we have that

which implies that is also the unique minimizer of , as desired.

The compactness requirement of condition (ii) of Theorem 2.1 in Newey and McFadden (1994) is immediate from Assumption 1 (iv). Condition (iii), i.e., the continuity of , holds because for any ,

where the second step follows from the dominated convergence theorem (DCT), and the third step from the continuity of the map together with continuity of (by Assumption 1 (vi)). Thus, is continuous. Note that we may apply the DCT, because is dominated by

where the final term is integrable due to Assumption 1 (ix). The ULLN required by condition (iv) follows directly from our Assumption 1 (v).

Now, we prove . To this end, we again verify conditions (i)–(iv) of Theorem 2.1 in Newey and McFadden (1994). Condition (i) for

follows from similar arguments used in the proof of . Condition (ii) is in force, due to Assumption 1 (iv). Condition (iii), i.e., the continuity of , follows because for any ,

where the second step follows from the DCT, and the third step from the continuity of the map together with the continuity of (by Assumption 1 (vi)). Thus, is continuous. Note that we may apply the DCT, because is dominated by

where the final term is integrable due to Assumption 1 (ix). For condition (iv), let

where we absorb the fact that is estimated into . We then have to show that

is . The term in the second line can be bounded by

We show in turn that and . By the ULLN from Assumption 1 (v) it holds that

It remains to show . For any and (with chosen sufficiently small, such that Assumption 1 (viii) is satisfied) it holds that

| (A.1) |

Define the -measurable quantities

which exist by continuity of (see Assumption 1 (vi)). Write

Therefore,

For , we obtain using the LIE (in the first step), Assumption 1 (iii) (in the third step), the mean value theorem (in the fourth step) and Assumptions 1 (viii)–(ix) (in the fifth and sixth step) that

where is some mean value between and . Hence, choosing sufficiently small, we can ensure that .

For , we obtain from Hölder’s inequality that for and ,

| (A.2) |

By the LIE,

where (which may change from line to line) lies between and , and the penultimate step follows from Assumption 1 (viii). Plugging this into (A.2) gives

Now, Assumption 1 (ix) allows us to conclude that by choosing sufficiently small. Therefore, for a suitable choice of , the first right-hand side term in (A.1) can be shown to equal zero, such that follows. This establishes condition (iv). The desired result that now follows from Theorem 2.1 in Newey and McFadden (1994). ∎

Appendix B Proof of Theorem 2

We split the proof of Theorem 2 into two parts. In Section B.1, we prove the asymptotic normality of , and in Section B.2 that of .

B.1 Asymptotic Normality of the VaR Parameter Estimator

The proof follows closely that of Theorem 2 in Engle and Manganelli (2004), although some of our assumptions differ from theirs. Our main motivation for detailing the proof is that some of the subsequent results are needed to prove the asymptotic normality of in Section B.2.

Before giving the formal proof, we collect some results that will be used in the sequel. For , it holds that

Thus, by the chain rule, it holds a.s. that

| (B.1) |

B.2 Asymptotic Normality of the CoVaR Parameter Estimator

The proof of the asymptotic normality of requires some further preliminary notation and lemmas. To see the analogy to the proof of the asymptotic normality of clearer, we label the lemmas as Lemma C.1, C.2, etc.

For , it holds that

Thus, by the chain rule, it holds a.s. that

| (B.2) |

The crucial step in the proof is once again to apply a mean value expansion and Lemma A.1 of Weiss (1991) to prove

-

Proof of Theorem 2 (continued)::

We can now show asymptotic normality of . From Lemma C.1, we have the decomposition

From simple adaptations of the proofs of Lemmas V.2 and C.2, we have that, as ,

where

is positive definite by Assumption 2 (viii). For the above display recall (B.22) and (B.40) (from Supplement C and D, respectively), and note that

and, similarly, . We then obtain from the continuous mapping theorem that, as ,

where

This, however, is just the conclusion. ∎

References

- Acharya et al. (2012) Acharya V, Engle R, Richardson M. 2012. Capital shortfall: A new approach to ranking and regulating systemic risks. American Economic Review: Papers and Proceedings 102: 59–64.

- Acharya et al. (2017) Acharya VV, Pedersen LH, Philippon T, Richardson M. 2017. Measuring systemic risk. The Review of Financial Studies 30: 2–47.

- Adrian et al. (2019) Adrian T, Boyarchenko N, Giannone D. 2019. Vulnerable growth. American Economic Review 109: 1263–1289.

- Adrian and Brunnermeier (2016) Adrian T, Brunnermeier MK. 2016. CoVaR. American Economic Review 106: 1705–1741.

- Adrian et al. (2022) Adrian T, Grinberg F, Liang N, Malik S, Yu J. 2022. The term structure of Growth-at-Risk. American Economic Journal: Macroeconomics 11: 283–323.

- Aielli (2013) Aielli GP. 2013. Dynamic conditional correlation: On properties and estimation. Journal of Business & Economic Statistics 31: 282–299.

- Andrews (1992) Andrews DWK. 1992. Generic uniform convergence. Econometric Theory 8: 241–257.

- Basel Committee on Banking Supervision (2019) Basel Committee on Banking Supervision. 2019. Basel framework. Tech. rep., Bank for International Settlements, Basel, http://www.bis.org/basel_framework/index.htm?export=pdf, accessed May 2022.

- Blasques et al. (2018) Blasques F, Gorgi P, Koopman SJ, Wintenberger O. 2018. Feasible invertibility conditions and maximum likelihood estimation for observation-driven models. Electronic Journal of Statistics 12: 1019–1052.

- Bollerslev (1990) Bollerslev T. 1990. Modelling the coherence in short-run nominal exchange rates: A multivariate generalized ARCH model. The Review of Economics and Statistics 74: 498–505.

- Bradley (2007) Bradley R. 2007. Introduction to Strong Mixing Conditions Vol. I. Heber City: Kendrick Press.

- Brownlees and Souza (2021) Brownlees C, Souza ABM. 2021. Backtesting global Growth-at-Risk. Journal of Monetary Economics 118: 312–330.

- Caporin and McAleer (2014) Caporin M, McAleer M. 2014. Robust ranking of multivariate GARCH models by problem dimension. Computational Statistics & Data Analysis 76: 172–185.

- Carrasco and Chen (2002) Carrasco M, Chen X. 2002. Mixing and moment properties of various GARCH and stochastic volatility models. Econometric Theory 18: 17–39.

- Catania and Luati (2022) Catania L, Luati A. 2022. Semiparametric modeling of multiple quantiles. Forthcoming in Journal of Econometrics https://doi.org/10.1016/j.jeconom.2022.11.002.

- Chan et al. (2007) Chan NH, Deng SJ, Peng L, Xia Z. 2007. Interval estimation of value-at-risk based on GARCH models with heavy-tailed innovations. Journal of Econometrics 137: 556–576.

- Chen et al. (2013) Chen C, Iyengar G, Moallemi CC. 2013. An axiomatic approach to systemic risk. Management Science 59: 1373–1388.

- Conrad and Karanasos (2010) Conrad C, Karanasos M. 2010. Negative volatility spillovers in the unrestricted ECCC–GARCH model. Econometric Theory 26: 838–862.

- Darolles et al. (2018) Darolles S, Francq C, Laurent S. 2018. Asymptotics of Cholesky GARCH models and time-varying conditional betas. Journal of Econometrics 204: 223–247.

- Davidson (1994) Davidson J. 1994. Stochastic Limit Theory. Oxford: Oxford University Press.

- Diebold and Mariano (1995) Diebold FX, Mariano RS. 1995. Comparing predictive accuracy. Journal of Business & Economic Statistics 13: 253–263.

- Dimitriadis and Bayer (2019) Dimitriadis T, Bayer S. 2019. A joint quantile and expected shortfall regression framework. Electronic Journal of Statistics 13: 1823–1871.

- Dimitriadis et al. (2022) Dimitriadis T, Fissler T, Ziegel J. 2022. Characterizing M-estimators. Preprint https://arxiv.org/abs/2208.08108.

- Dimitriadis and Hoga (2022) Dimitriadis T, Hoga Y. 2022. CoQR. R package version 0.0.0.9000, available at https://github.com/TimoDimi/CoQR.

- DuMouchel (1983) DuMouchel WH. 1983. Estimating the stable index in order to measure tail thickness: A critique. The Annals of Statistics 11: 1019–1031.

- Engle (2002) Engle RF. 2002. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics 20: 339–350.

- Engle and Manganelli (2004) Engle RF, Manganelli S. 2004. CAViaR: Conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics 22: 367–381.

- Feng et al. (2013) Feng C, Wang H, Han Y, Xia Y, Tu XM. 2013. The mean value theorem and Taylor’s expansion in statistics. The American Statistician 67: 245–248.

- Financial Stability Board (2021) Financial Stability Board. 2021. 2021 list of global systemically important banks (G-SIBs). Tech. rep., Bank for International Settlements, Basel, https://www.fsb.org/wp-content/uploads/P231121.pdf, accessed May 2022.

- Fissler and Hoga (2022) Fissler T, Hoga Y. 2022. Backtesting systemic risk forecasts using multi-objective elicitability. Preprint https://arxiv.org/pdf/2104.10673.pdf.

- Forsberg and Ghysels (2007) Forsberg L, Ghysels E. 2007. Why do absolute returns predict volatility so well? Journal of Financial Econometrics 5: 31–67.

- Francq and Zakoïan (2010) Francq C, Zakoïan JM. 2010. GARCH Models: Structure, Statistical Inference and Financial Applications. Chichester: Wiley.

- Francq and Zakoïan (2016) Francq C, Zakoïan JM. 2016. Estimating multivariate GARCH models equation by equation. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 78: 613–635.

- Gao and Song (2008) Gao F, Song F. 2008. Estimation risk in GARCH VaR and ES estimates. Econometric Theory 24: 1404–1424.

- Giesecke and Kim (2011) Giesecke K, Kim B. 2011. Systemic risk: What defaults are telling us. Management Science 57: 1387–1405.

- Girardi and Tolga Ergün (2013) Girardi G, Tolga Ergün A. 2013. Systemic risk measurement: Multivariate GARCH estimation of CoVaR. Journal of Banking & Finance 37: 3169–3180.

- Glosten et al. (1993) Glosten LR, Jagannathan R, Runkle DE. 1993. On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance 48: 1779–1801.

- Gneiting (2011) Gneiting T. 2011. Making and evaluating point forecasts. Journal of the American Statistical Association 106: 746–762.

- Hansen et al. (2011) Hansen PR, Lunde A, Nason JM. 2011. The Model Confidence Set. Econometrica 79: 453–497.

- Hautsch et al. (2015) Hautsch N, Kyj LM, Malec P. 2015. Do high-frequency data improve high-dimensional portfolio allocations? Journal of Applied Econometrics 30: 263–290.

- He and Teräsvirta (2004) He C, Teräsvirta T. 2004. An extended constant conditional correlation GARCH model and its fourth-moment structure. Econometric Theory 20: 904–926.

- Hoga (2019) Hoga Y. 2019. Confidence intervals for conditional tail risk measures in ARMA–GARCH models. Journal of Business & Economic Statistics 37: 613–624.

- Jeantheau (1998) Jeantheau T. 1998. Strong consistency of estimators for multivariate ARCH models. Econometric Theory 14: 70–86.

- Jorion (2006) Jorion P. 2006. Value at Risk: the New Benchmark for Managing Financial Risk. Chicago: McGraw–Hill, 3rd edn.

- Koenker (2005) Koenker R. 2005. Quantile Regression. Econometric Society Monographs, Cambridge: Cambridge University Press.

- Laurent et al. (2012) Laurent S, Rombouts JVK, Violante F. 2012. On the forecasting accuracy of multivariate GARCH models. Journal of Applied Econometrics 27: 934–955.

- Liu and Stentoft (2021) Liu F, Stentoft L. 2021. Regulatory capital and incentives for risk model choice under Basel 3. Journal of Financial Econometrics 19: 53–96.

- Machado and Santos Silva (2013) Machado J, Santos Silva J. 2013. Quantile regression and heteroskedasticity. Preprint. https://jmcss.som.surrey.ac.uk/JM_JSS.pdf.

- Mainik and Schaanning (2014) Mainik G, Schaanning E. 2014. On dependence consistency of CoVaR and some other systemic risk measures. Statistics & Risk Modeling 31: 49–77.

- Massacci (2017) Massacci D. 2017. Tail risk dynamics in stock returns: Links to the macroeconomy and global markets connectedness. Management Science 63: 3072–3089.

- McNeil and Frey (2000) McNeil AJ, Frey R. 2000. Estimation of tail-related risk measures for heteroscedastic financial time series: An extreme value approach. Journal of Empirical Finance 7: 271–300.

- Newey and McFadden (1994) Newey WK, McFadden D. 1994. Large sample estimation and hypothesis testing. In Engle RF, McFadden D (eds.) Handbook of Econometrics, vol. 4, chap. 36, Elsevier, pages 2111–2245.

- Nolde and Zhang (2020) Nolde N, Zhang J. 2020. Conditional extremes in asymmetric financial markets. Journal of Business & Economic Statistics 38: 201–213.

- Patton et al. (2019) Patton AJ, Ziegel JF, Chen R. 2019. Dynamic semiparametric models for expected shortfall (and value-at-risk). Journal of Econometrics 211: 388–413.

- R Core Team (2022) R Core Team. 2022. R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria.

- Straumann and Mikosch (2006) Straumann D, Mikosch T. 2006. Quasi-maximum-likelihood estimation in conditionally heteroscedastic time series: A stochastic recurrence equations approach. The Annals of Statistics 34: 2449–2495.

- Wang and Zhao (2016) Wang CS, Zhao Z. 2016. Conditional value-at-risk: Semiparametric estimation and inference. Journal of Econometrics 195: 86–103.

- Weiss (1991) Weiss AA. 1991. Estimating nonlinear dynamic models using least absolute error estimation. Econometric Theory 7: 46–68.

- White (2001) White H. 2001. Asymptotic Theory for Econometricians. San Diego: Academic Press, First edn.

- White et al. (2015) White H, Kim TH, Manganelli S. 2015. VAR for VaR: Measuring tail dependence using multivariate regression quantiles. Journal of Econometrics 187: 169–188.

Supplementary Material for

Dynamic CoVaR Modeling

Timo Dimitriadis and Yannick Hoga

Continuing the labeling of Sections A and B in the Appendix of the main paper, this supplement contains Sections C–H. Specifically, Section C proves Lemmas V.1 and V.2, while Section D contains the proofs of Lemmas C.1 and C.2. Section E establishes Theorem 3. Section F shows consistency of our estimator under arbitrary starting values. In Section G, we verify Assumptions 1 and 2 for a CCC–GARCH model. We also give some details on the computation of VaR and CoVaR from DCC–GARCH models in Section H. A joint reference list is given at the end of the main paper.

Notation

We use the following notational conventions throughout this appendix. The probability space that we work on is . We denote by a large positive constant that may change from line to line. If not specified otherwise, all convergences are to be understood with respect to . We also write and for short. We exploit without further mention that the Frobenius norm is submultiplicative, i.e., that for conformable matrices and . For a real-valued, differentiable function , we denote the -th element of the gradient by .

Appendix C Proof of Lemmas V.1 and V.2

Before proving Lemmas V.1 and V.2, we introduce some convenient notation. Recall from (B.3) that

| (B.3) |

This implies by the LIE and Assumption 1 (vi) that

Assumption 2 and the dominated convergence theorem allow us to interchange differentiation and expectation to yield that

| (B.4) |

Evaluating this quantity at the true parameters gives

| (B.5) |

By virtue of Assumption 1 (ii), does not depend on . Finally, define

and note that .

-

Proof of Lemma V.1::

The mean value theorem (MVT) implies that for all ,

where , denotes the -th row of and lies on the line connecting and . To economize on notation, we shall slightly abuse notation (here and elsewhere) by writing this as

(B.6) for some between and ; keeping in mind that the value of is in fact different from row to row in . However, this does not change any of the subsequent arguments. Interpreted verbatim, (B.6) would be an instance of what Feng et al. (2013) call the non-existent mean value theorem, which is widely applied in statistics; e.g., by Engle and Manganelli (2004) and Patton et al. (2019).

We have that

(B.7) since by correct specification. Plugging this into (B.6) gives

To establish the claim, we therefore only have to show that

-

(i)

;

-

(ii)

.

-

(i)

Claim (i) is verified in Lemma V.3. For this, note that since is a mean value between and , and (from Theorem 1), it also follows that .

To prove (ii), by Lemma A.1 in Weiss (1991), we only have to show that

-

(ii.a)

conditions (N1)–(N5) in the notation of Weiss (1991) hold;

-

(ii.b)

;

-

(ii.c)

.

For (ii.a), note that (N1) is immediate and (N2) follows from (B.7). The mixing condition (N5) is implied by our Assumption 2 (x). Condition (N3) is verified in Lemmas V.5–V.7 below and the remaining condition (N4) in Lemma V.8. The result in (ii.b) follows from Lemma V.4 and (ii.c) follows from Theorem 1. In sum, the desired result follows. ∎

- Proof:

Use (B.4) to write

| (B.8) |

By Assumption 2 (iii), we have that

| (B.9) |

The other two terms in (B.8) can be dealt with as follows. First, using a mean value expansion around and Assumption 2, we obtain that

| (B.10) |

where is some value on the line connecting and , and the penultimate step uses Hölder’s inequality.

Second, using a mean value expansion around to obtain for some between and (where may vary from line to line) that

| (B.11) |

where we used Assumption 2.

Plugging (B.9)–(B.11) into (B.8), we obtain that

| (B.12) |

Using this, we obtain for with that

where the final line additionally requires . This shows that . By Assumption 2 (viii) and continuity of (recall (B.12)), is non-singular in a neighborhood of . Therefore, the continuous mapping theorem (CMT) applied to implies that , as desired.∎

-

Proof:

Recall from Assumption 1 (iv) that , such that is a -dimensional parameter vector. Let denote the standard basis of . Define

where . Let be the right partial derivative of , such that (see (B.3))

where is the -th component of . Then, is the right partial derivative of

at in the direction , where . Correspondingly, is the left partial derivative. Because achieves its minimum at , the left derivative must be non-positive and the right derivative must be non-negative. Thus,

By continuity of (see Assumption 2 (ii)) it follows upon letting that

(B.13) We have that, by subadditivity, Markov’s inequality and Assumption 2 (v),

Combining this with Assumption 2 (ix), we obtain from (B.13) that

As this holds for every , we get that

which is just the conclusion. ∎

Lemma V.5.

-

Proof:

Choose sufficiently small, such that is a subset of the neighborhoods of Assumptions 1 (viii) and 2 (iii). The MVT and (B.7) imply that

for some between and . (Again, to be precise we should allow for the mean value to vary across rows of ; however, for the subsequent argument this does not matter.) Use (B.4) to write

Recall that

We first show that

by decomposing into two terms, each bounded by a -term. We have the following decomposition:

First term: Following similar steps as for (B.10), we obtain that

Second term: Again following similar steps as for (B.11), we get that

Thus, we have shown that for some large enough. By Assumption 2 (viii), has eigenvalues bounded below by some constant . Therefore,

where the second-to-last inequality holds by the triangle inequality. The conclusion follows upon choosing small enough, such that . ∎

Lemma V.6.

-

Proof:

Choose sufficiently small, such that is a subset of the neighborhoods of Assumptions 1 (viii) and 2 (iii). Recalling the definition of from (B.3), we decompose

Similarly as in the proof of Theorem 1, we define the -measurable quantities

which exist by continuity of .

We first consider . To take the indicators out of the supremum, we distinguish two cases:

Case 1:

We further distinguish two cases (a)–(b):

(a) If , then both indicators are one, such that

(b) If , then

(B.14) (Note that the third case that cannot occur, because already .)

Case 2:

(B.15) Before combining the two cases, note that our assumptions and together imply that and are in a -neighborhood of . (For this is immediate, and for this follows from .) Hence, for the final terms in (B.14) and (B.15), we have

Therefore, combining the results from Cases 1 and 2,

(B.16) By Assumptions 1 (iii) and (viii) we have

(B.17) and, similarly,

(B.18) Moreover, we have by the MVT that for some on the line connecting and ,

(B.19) Therefore,

Lemma V.7.

-

Proof:

The arguments in this proof are similar to that of Lemma V.6. We again pick sufficiently small, such that is a subset of the neighborhoods of Assumptions 1 (viii) and 2 (iii). We also work with (), and as defined in the proof of Lemma V.6.

By the -inequality (e.g., Davidson, 1994, Theorem 9.28) and the fact that , we get that

Hence, to prove the claim, it suffices to show that for (from Assumption 2 (v)) and some .

First term: Following the same arguments that led to (B.16), we obtain that

By the LIE,

(B.20) and from (B.19)

(B.21) Inserting the above three relations into (B.20), we obtain (using Assumption 2 (v)) that

where the penultimate step follows from Hölder’s inequality.

Second term: By definition of and exploiting (B.21), we have that

Combining the results for the first and second term, the conclusion follows. ∎

Lemma V.8.

- Proof:

-

Proof of Lemma V.2::

By a Cramér–Wold device, it suffices to show the univariate convergence