Diversification quotients: Quantifying diversification via risk measures

Abstract

We establish the first axiomatic theory for diversification

indices using six intuitive axioms – non-negativity, location invariance, scale invariance, rationality, normalization, and continuity – together with risk measures. The unique class of indices satisfying these axioms, called the diversification quotients (DQs), are defined based on a parametric family of risk measures. DQ has many attractive properties, and it can address several theoretical and practical limitations of existing indices. In particular, for the popular risk measures Value-at-Risk and Expected Shortfall, DQ admits simple formulas, it is efficient to optimize in portfolio selection, and it can properly capture tail heaviness and common shocks which are neglected by traditional diversification indices.

When illustrated with financial data, DQ is intuitive to interpret, and its performance is competitive against other diversification indices.

Keywords: Expected Shortfall, axiomatic framework, diversification benefit, portfolios, quasi-convexity

1 Introduction

Portfolio diversification refers to investment strategies which spread out among many assets, usually with the hope to reduce the volatility or risk of the resulting portfolio. A mathematical formalization of diversification in a portfolio selection context was made by Markowitz (1952), and some early literature on diversification includes Sharpe (1964), Samuelson (1967), Levy and Sarnat (1970) and Fama and Miller (1972), amongst others.

Although diversification is conceptually simple, the question of how to measure diversification quantitatively is never well settled. An intuitive, but non-quantitative, approach is to simply count the number of distinct stocks or industries of substantial weight in the portfolio; see e.g., Green and Hollifield (1992), Denis et al. (2002) and DeMiguel et al. (2009) in different contexts. This approach is heuristic as it does not involve statistical or stochastic modeling. The second approach is to compute a quantitative index of the portfolio model, based on e.g., the volatility, variance, an expected utility or a risk measure; this idea is certainly along the direction of Markowitz (1952). In addition, one may empirically address diversification by combining both approaches; see e.g., Tu and Zhou (2011) for the performance of different diversified portfolio strategies and D’Acunto et al. (2019) in the context of robo-advising. Green and Hollifield (1992) studied conditions under which the two approaches are roughly in-line with each other.

In this paper, we take the second approach by assigning a quantifier, called a diversification index, to each modeled portfolio. Carrying the idea of Markowitz (1952), we start our journey with a simple index, the diversification ratio (DR) based on the standard deviation (SD), defined as

| (1) |

for a random vector representing future random losses and profits of individual components in a portfolio in one period;111We focus on the one-period losses to establish the theory. This is consistent with the vast majority of literature on risk measures and decision models. one can also replace SD by the variance. Intuitively, with a smaller value indicating a stronger diversification, the index quantifies the improvement of the portfolio SD over the sum of SD of its components, and it has several convenient properties. Nevertheless, it is well-known that SD is a coarse, non-monotone and symmetric measurement of risk, making it unsuitable for many risk management applications, especially in the presence of heavy-tailed and skewed loss distributions; see Embrechts et al. (2002) for thorough discussions.

Risk measures, in particular the Value-at-Risk (VaR) and the Expected Shortfall (ES), are more flexible quantitative tools, widely used in both financial institutions’ internal risk management and banking and insurance regulatory frameworks, such as Basel III/IV (BCBS (2019)) and Solvency II (EIOPA (2011)). ES has many nice theoretical properties and satisfies the four axioms of coherence (Artzner et al. (1999)), whereas VaR is not subadditive in general, but it enjoys other practically useful properties; see Embrechts et al. (2014, 2018), Emmer et al. (2015) and the references therein for more discussions on the issues of VaR versus ES.

Some indices of diversification based on various risk measures have been proposed in the literature. For a given risk measure , an example of a diversification index is DR in (1) with SD replaced by , that is,

see Tasche (2007). Other studies on DR can be found in e.g., Choueifaty and Coignard (2008), Bürgi et al. (2008), Mainik and Rüschendorf (2010) and Embrechts et al. (2015). For a review of diversification indices, see Koumou (2020).

We find several demerits of DR built on a general risk measure such as VaR or ES. First, DR is not location invariant, meaning that adding a risk-free asset changes the value of DR. Second, the value of is not necessarily non-negative. Since the risk measure may take negative values,222A negative value of a risk measure has a concrete meaning as the amount of capital to be withdrawn from a portfolio position while keeping it acceptable; see Artzner et al. (1999). it would be difficult to interpret the case where either the numerator or denominator in DR is negative, and this makes optimization of DR troublesome. This is particularly relevant if some components in the portfolio are used to hedge against other components, possibly leading to a negative or zero risk value. Another example is a portfolio of credit default losses, where VaR of individual losses are often . Third, DR is not necessarily quasi-convex in portfolio weights; this point is more subtle and will be explained later in the paper. In addition to the above drawbacks, we find that DR has wrong incentives for some simple models; for instance, it suggests that an iid portfolio of -distributed risks is less diversified than a portfolio with a common shock and the same marginals; see Section 5.2 for details.

Based on the above observations, a natural question is whether we can design a suitable index based on risk measures to quantify the magnitude of diversification, which avoids all the deficiencies above. Answering this and related questions is the main purpose of this paper.

We take an axiomatic approach to find our desirable diversification indices. Axiomatic approaches for risk and decision indices have been prolific in economic and statistical decision theories; see e.g., the recent discussions of Gilboa et al. (2019) and the axiomatization of preferences in Klibanoff et al. (2005) and Gilboa et al. (2010). Closely related to diversification indices, risk measures (Artzner et al. (1999)) and acceptability indices (Cherny and Madan (2009)) also admit sound axiomatic foundation; the particular cases of VaR and ES are studied by Chambers (2009) and Wang and Zitikis (2021). In Section 3, we establish the first axiomatic foundation of diversification indices.333A different list of desirable axioms for diversification indices is studied by Koumou and Dionne (2022). Their framework is mathematically different from ours as their diversification indices are mappings of portfolio weights, instead of mappings of portfolio random vectors. They did not provide axiomatic characterization results. This axiomatic theory leads to the class of diversification quotients (DQs), the main object of this paper. For a portfolio loss vector , a DQ is defined as

| (2) |

where is a class of risk measures decreasing in with . Our axiomatic theory starts with three simple axioms satisfied by DR based on SD in (1) – non-negativity, location invariance and scale invariance – that are arguably natural for diversification indices. We then put forward three other axioms of rationality, normalization and continuity, and discuss their interpretation and desirability. Our first main result (Theorem 1) establishes that the six axioms together uniquely identify DQ based on monetary and positive homogeneous risk measures, including VaR and ES as special cases.

In the most relevant case , we see from Figure 1 a conceptual symmetry between DQ, which measures the improvement of risk by pooling in the horizontal direction, and DR, which measures an improvement in the vertical direction.

A detailed analysis of properties of DQ based on general risk measures is discussed in Section 4, which reveals that DQ has many appealing features, both theoretically and practically. In addition to standard operational properties (Proposition 1), DQ has intuitive behaviour for several benchmark portfolio scenarios (Theorem 2). Moreover, DQ allows for consistency with stochastic dominance (Proposition 2) and a fair comparison across portfolio dimensions (Proposition 3). We proceed to focus on VaR and ES in Section 5. Alternative formulations of and are first derived (Theorem 3). It turns out that and have a natural range of and , respectively (Proposition 4). We further find that DQs based on both VaR and ES report intuitive comparisons between normal and t-models and it has the nice feature that it can capture heavy tails and common shocks.

In Section 6, we formulate DQ as a function of portfolio weights, and portfolio optimization problems are studied. It is shown that is quasi-convex in portfolio weights (Theorem 4), and efficient algorithms to optimize and based on empirical observations are obtained (Proposition 5). Our new diversification index is applied to financial data in Section 7, where several empirical observations highlight the advantages of DQ. We conclude the paper in Section 8 by discussing a number of implications and promising future directions for DQ. Some additional results, proofs, and some omitted numerical results are relegated to the technical appendices.

Notation. Throughout this paper, is an atomless probability space, on which almost surely equal random variables are treated as identical. A risk measure is a mapping from to , where is a convex cone of random variables on representing losses faced by a financial institution or an investor, and is assumed to include all constants (i.e., degenerate random variables). For , denote by the set of all random variables with where is the expectation under . Furthermore, is the space of all (essentially) bounded random variables, and is the space of all random variables. Write if the random variable has the distribution function under , and if two random variables and have the same distribution. Further, denote by and . Terms such as increasing or decreasing functions are in the non-strict sense. For , and are the essential supremum and the essential infimum of , respectively. Let be a fixed positive integer representing the number of assets in a portfolio, and let . It does not hurt to think about although our results hold also (trivially) for . The vector represents the -vector of zeros, and we always write and .

2 Preliminaries and motivation

The most important object of the paper, a diversification index is a mapping from to , which is used to quantify the magnitude of diversification of a risk vector representing portfolio losses. Our convention is that a smaller value of represents a stronger diversification in a sense specified by the design of .

As the evaluation of diversification is closely related to that of risk, diversification indices in the literature are often defined through risk measures. An example of a diversification index is the diversification ratio (DR) mentioned in the Introduction based on measures of variability such as the standard deviation () and the variance ():

with the convention . We refer to Rockafellar et al. (2006), Furman et al. (2017) and Bellini et al. (2022) for general measures of variability. DRs based on and satisfy the three simple properties below, which can be easily checked.

-

[+]

Non-negativity: for all .

-

[LI]

Location invariance: for all and all .

-

[SI]

Scale invariance: for all and all .

The first property, [+], simply means that diversification is measured in non-negative values, where typically represents a fully diversified or hedged portfolio (in some sense). The property [LI] means that injecting constant losses or gains to components of a portfolio, or changing the initial price of assets in the portfolio,444Recall that represents the loss from asset . Suppose that two agents purchased the same portfolio of assets but at different prices of each asset. Denote by the portfolio loss vector of agent . The portfolio loss vector of agent is , where is the vector of differences between their purchase prices. The two agents should have the same level of diversification regardless of their purchase prices, as they hold the same portfolio. does not affect its diversification index. The property [SI] means that rescaling a portfolio does not affect its diversification index. The latter two properties are arguably natural, although they are not satisfied by some diversification indices used in the literature (see (3) below). A diversification index satisfying both [LI] and [SI] is called location-scale invariant.

Next, we define the two popular risk measures in banking and insurance practice. The VaR at level is defined as

and the ES (also called CVaR, TVaR or AVaR) at level is defined as

and which may be . The probability level above is typically very small, e.g., or in BCBS (2019); note that we use the “small ” convention. Artzner et al. (1999) introduced coherent risk measures as those satisfying the following four properties.

-

[M]

Monotonicity: for all with .555The inequality between two random variables and is point-wise.

-

Constant additivity: for all and .

-

Positive homogeneity: for all and .

-

[SA]

Subadditivity: for all .

ES satisfies all four properties above, whereas VaR does not satisfy [SA]. We say that a risk measure is monetary if it satisfies and [M], and it is MCP if it satisfies [M], [CA] and [PH]. For discussions and interpretations of these properties, we refer to Föllmer and Schied (2016).

Some diversification indices, such as DR and the diversification benefit (DB, e.g., Embrechts et al. (2009) and McNeil et al. (2015)), are defined via risk measures. For a risk measure , DR and DB based on are defined as666If the denominator in the definition of is , then we use the convention and .

| (3) |

In contrast to DR, a larger value of DB represents a stronger diversification, but this convention can be easily modified by flipping the sign. By definition, DR is the ratio of the pooled risk to the sum of the individual risks, and thus a measurement of how substantially pooling reduces risk; similarly, DB measures the difference instead of the ratio. In general, the value of is not necessarily non-negative, since may be negative for some . As such, we cannot interpret diversification from the value of DR if either the denominator or the numerator in (3) is negative or zero. In addition to violating [+], DR does not necessarily satisfy [LI] and [SI] even if the risk measure has nice properties. The index satisfies [LI] for satisfying [CA], but it does not satisfy [SI] in general and it may take both positive and negative values.

In financial applications, the risk measures VaR and ES are specified in regulatory documents such as BCBS (2019) and EIOPA (2011), and therefore it is beneficial to stick to VaR or ES as the risk measure when assessing diversification. Both and satisfy [SI], but they do not satisfy [+] or [LI].777DR and DB for a general do not satisfy some of [+], [LI] and [SI]. Moreover, an impossibility result (Proposition EC.2) is presented in Appendix C which suggests that it is not possible to construct non-trivial diversification indices like DR and DB satisfying [+], [LI] and [SI]. It remains unclear how one can define a diversification index based on VaR or ES satisfying these properties. In the remainder of the paper, we will introduce and study a new index of diversification to bridge this gap.

3 Diversification quotients: An axiomatic theory

In this section, we fix as the standard choice in the literature of axiomatic theory of risk measures. Six axioms are used to uniquely characterize a new diversification index, called diversification quotient (DQ). The first three of the six axioms , , have been introduced in Section 2, and we proceed to introduce the other three.

For a risk measure we say that two vectors are -marginally equivalent if for each , and we denote this by . In other words, if an agent evaluates risks using the risk measure , then she would view the individual components of and those of as indifferent. Similarly, denote by if for each , and by if for each . The other three desirable axioms are presented below, and they are built on a given risk measure , such as VaR or ES, typically specified exogenously by financial regulation.

-

Rationality: for satisfying and .

To interpret the axiom , consider two portfolios and satisfying , meaning that their individual components are considered as equally risky. If further holds, then the total loss from portfolio is always less or equal to that from portfolio , making the portfolio safer than . Since the individual components in and those in are equally risky, the fact that is safer in aggregation is a result of the different diversification effects in and , leading to the inequality . This axiom is called rationality because a rational agent always prefers to have smaller losses.

Next, we formulate our idea about normalizing representative values of the diversification index. First, we assign the zero portfolio the value , as it carries no risk in every sense.888Indeed, the value of may be rather arbitrary; this is the case for DR where occurs. A natural benchmark of a non-diversified portfolio is one in which all components are the same. Such a portfolio will be called a duplicate portfolio, and we may, ideally, assign the value . However, since the zero portfolio is also duplicate but , we will require the weaker assumption for duplicate portfolios. Lastly, we should understand for what portfolios needs to occur. We say that a portfolio is worse than duplicate, if there exists a duplicate portfolio such that and . Intuitively, this means that each component of is strictly less risky than , but putting them together always incurs a larger loss than ; in this case, diversification creates nothing but a penalty to the risk manager, and we assign .999Such situations may be regarded as diversification disasters; see Ibragimov et al. (2011). Putting all of the considerations above, we propose the following normalization axiom.

-

Normalization: and if is duplicate and is worse than duplicate.

Finally, we propose a continuity axiom which is mainly for technical convenience.

-

Continuity: For and satisfying for each , if as , then .

The axiom is a special form of semi-continuity. To interpret it, consider portfolios and which are marginally equivalent. If the sum of components of is not much worse than that of in , then the axiom says that the diversification of is not much worse than the diversification of . This property allows for a special form of stability or robustness101010In the literature of statistical robustness, often a different metric than the metric is used; see Huber and Ronchetti (2009) for a general treatment. Our choice of formulating continuity via the metric is standard in the axiomatic theory of risk mappings on . with respect to statistical errors when estimating the distributions of portfolio losses.

One can check that the axioms , and are satisfied and if we only consider positive portfolio vectors. The axioms are not satisfied by because is not monotone and hence the inequalities and used in and are not relevant for SD.

We now formally introduce the diversification index DQ relying on a parametric class of risk measures.

Definition 1.

Let be a class of risk measures indexed by with such that is decreasing in . For , the diversification quotient based on the class at level is defined by

| (4) |

with the convention .

DQ can be constructed from any monotonic parametric family of risk measures. All commonly used risk measures belong to a monotonic parametric family, as this includes VaR, ES, expectiles (e.g., Bellini et al. (2014)), mean-variance (e.g., Markowitz (1952) and Maccheroni et al. (2009)), and entropic risk measures (e.g., Föllmer and Schied (2016)). In addition, there are multiple ways to construct DQ from a single risk measure; see Section 4.4.

In the following result, we characterize DQ based on MCP risk measures by Axioms , , , , and .

Theorem 1.

A diversification index satisfies , , , , and for some MCP risk measure if and only if is for some decreasing families of MCP risk measures. Moreover, in both directions of the above equivalence, it can be required that .

Theorem 1 gives the first axiomatic characterization of diversification indices, to the best of our knowledge. The diversification index DQ turns out to enjoy many intuitive and practically relevant properties, which we will study in the next few sections.

The axioms , and are formulated based on an exogenously specified risk measure , usually by financial regulation. This choice can also be endogenized in the context of internal decision making. We present in Appendix A an axiomatization of DQ without specifying a risk measure via a few additional axioms on the preference of a decision maker.

4 Properties of DQ

In this section, we study properties of DQ defined in Definition 1. For the greatest generality, we do not impose any properties of risk measures in the decreasing family , i.e., the family is not limited to a class of MCP risk measures, so that our results can be applied to more flexible contexts in which some of the six axioms are relaxed.

4.1 Basic properties

We first make a few immediate observations by the definition of DQ. From (4), we can see that computing is to invert the decreasing function at . For the cases of VaR and ES, , , and DQ has simple formulas; see Theorem 3 in Section 5. For a fixed value of , DQ is larger if the curve is larger, and DQ is smaller if the curve is smaller. This is consistent with our intuition that a diversification index is large if there is little or no diversification, thus a large value of the portfolio risk, and a diversification index is small if there is strong diversification.

In Theorem 1, we have seen that DQ satisfies [SI] and [LI] if is a class of MCP risk measures. These properties of DQ can be obtained based on a more general version of properties [CA] and [PH] of risk measures, allowing us to include SD and the variance. The results are summarized in Proposition 1, which are straightforward to check by definition.

-

Constant additivity with : for all and .

-

Positive homogeneity with : for all and .

Proposition 1.

Let be a class of risk measures decreasing in . For each ,

-

(i)

if satisfies with the same , then satisfies [SI].

-

(ii)

if satisfies with the same , then satisfies [LI].

-

(iii)

if satisfies [SA], then takes value in .

It is clear that [CA] is with and [PH] is with . Proposition 1 implies that if is a class of risk measures satisfying [CA], [PH] and [SA] such as ES, then is location-scale invariant and takes value in . More properties of DQs on the important families of VaR and ES will be discussed in Section 5. In particular, we will see that the ranges of and are and , respectively.

Example 1 (Liquidity and temporal consistency).

In risk management practice, liquidity and time-horizon of potential losses need to be taken into account; see BCBS (2019, p.89). If liquidity risk is of concern, one may use a risk measure with with to penalize large exposures of losses. For such risk measures, remains scale invariant, as shown by Proposition 1. On the other hand, if the risk associated to the loss at different time spots are scalable by a function (usually of the order in standard models such as the Black-Scholes), then DQ is consistent across different horizons in the sense that for two time spots , given that for , and .

Remark 1.

Cherny and Madan (2009) proposed acceptability indices defined via a class of risk measures. More precisely, an acceptability index is defined by for a decreasing class of coherent risk measures , which has visible similarity to in (4); see Kováčová et al. (2020) for optimization of acceptability indices. If is a class of risk measures satisfying [CA], then

For Dhaene et al. (2012) studied several methods for capital allocation, among which the quantile allocation principle computes a capital allocation such that and for some . The constant appearing as a nuisance parameter in the above rule has a visible mathematical similarity to . Mafusalov and Uryasev (2018) studied the so-called buffered probability of exceedance, which is the inverse of the ES curve at a specific point ; note that in (4) is obtained by inverting the ES curve at .

4.2 Interpreting DQ from portfolio models

To use DQ as a diversification index, we need to make sure that it coincides with our usual perceptions of portfolio diversification. For a given risk measure and a portfolio risk vector , we consider the following three situations which yield intuitive values of DQ.

-

(i)

There is no insolvency risk with pooled individual capital, i.e., a.s.;

-

(ii)

diversification benefit exists, i.e., ;

-

(iii)

the portfolio relies on a single asset, i.e., for some and .

The above three situations receive special attention because they intuitively correspond to very strong diversification, some diversification, and no diversification, respectively. Naturally, we would expect DQ to be very small for (i), DQ to be smaller than for (ii), and DQ to be for (iii). It turns out that the above intuitions all check out under very weak conditions that are satisfied by commonly used classes of risk measures.

Before presenting this result, we fix some technical terms. For a class of risk measures decreasing in , we say that is non-flat from the left at if for all , and is left continuous at if is left continuous. A random vector is comonotonic if there exists a random variable and increasing functions on such that a.s. for every . A risk measure is comonotonic-additive if for comonotonic . Each of ES and VaR satisfies comonotonic-additivity, as well as any distortion risk measures (Yaari (1987), Kusuoka (2001)) and signed Choquet integrals (Wang et al. (2020)). We denote by . Note that for common classes such as VaR, ES, expectiles, and entropic risk measures.

Theorem 2.

For given and , if is left continuous and non-flat from the left at , the following hold.

-

(i)

Suppose that . If for there is no insolvency risk with pooled individual capital, then . The converse holds true if .

-

(ii)

Diversification benefit exists if and only if .

-

(iii)

If satisfies and relies on a single asset, then .

-

(iv)

If is comonotonic-additive and is comonotonic, then .

In (i), we see that if there is no insolvency risk with pooled individual capital, then . In typical models, such as some elliptical models in Section 5.2, is unbounded from above unless it is a constant. Hence, for such models and satisfying , if and only if is a constant, thus full hedging is achieved. This is also consistent with our intuition of full hedging as the strongest form of diversification.

Remark 2.

We require to be left continuous and non-flat from the left to make the inequality in (ii) holds strictly. This requirement excludes, in particular, trivial cases like which gives by definition. In case the conditions fail to hold, may not guarantee , but it implies the non-strict inequality , and thus the portfolio risk is not worse than the sum of the individual risks.

With the help of Theorem 2 (ii), we can show that DQ and DR are equivalent when it comes to the existence of the diversification benefit. Under the conditions of Theorem 2, for a given , if and are positive, then it is straightforward to check that the following three statements are equivalent: (i) Diversification benefit exists, i.e., ; (ii) ; (iii) . The above equivalence only says that and agree on whether they are smaller than , but they do not have to agree in other situations, and they are not meant to be compared on the same scale.

4.3 Constructing DQ from a single risk measure

In this section, we discuss how to construct DQ from only a single risk measure . For commonly used risk measures like VaR and ES, a natural family with exists. If in some applications one needs to use a different which does not belong to an existing family, we will need to construct a family of risk measures for .

First, suppose that is MCP. A simple approach is to take for . Clearly, . As is MCP, we have for all . Hence, is a decreasing class of MCP risk measures. Therefore, satisfies the six axioms in Theorem 1. Moreover, by checking the definition, this DQ has an explicit formula

If , we have and ; this is also reflected by Theorem 2 when .

For any arbitrary risk measure , we can always define the decreasing family for constructing DQ; here is the positive part of . This approach leads to DQs which are also DRs. Assuming that is non-negative (such as SD), in Proposition EC.3 in Appendix D.1, we will see that DQ based on the class is precisely DR based on ; thus, DR with a non-negative is a special case of DQ. For the interested reader, we further show that any satisfying [+], [LI] and [SI] belongs to the DQ class; see Proposition EC.4 in Appendix D.1.

4.4 Stochastic dominance and dependence

In this section, we discuss the consistency of DQ with respect to stochastic dominance, as well as the best and worst cases for DQ among all dependence structures with given marginal distributions of the risk vector.

For a diversification index, monotonicity with respect to stochastic dominance yields consistency with common decision making criteria such as the expected utility model and the rank-dependent utility model. A random variable (representing random loss) is dominated by a random variable in second-order stochastic dominance (SSD) if for all decreasing concave functions provided that the expectations exist, and we denote this by .111111If and represents gains instead of losses, then SSD is typically defined via increasing concave functions. A risk measure is SSD-consistent if for all whenever . SSD consistency is known as strong risk aversion in the classic decision theory literature (Rothschild and Stiglitz (1970)). SSD-consistent monetary risk measures, which include all law-invariant convex risk measures such as ES, admit an ES-based characterization (Mao and Wang (2020)).

Proposition 2.

Assume that is a decreasing class of SSD-consistent risk measures. For and , if and , then .

Assume is a class of SSD-consistent risk measures (e.g., law-invariant convex risk measures). Proposition 2 implies that if the sum of marginal risks is the same for and (this holds in particular if and have the same marginal distributions), then DQ is decreasing in SSD of the total risk. The dependence structures which maximize or minimize DQ for with specified marginal distributions are discussed in Appendix D.2. For instance, a comonotonic portfolio has the largest DQ (thus the smallest diversification) among all portfolios with the same marginal distributions; this observation is related to Proposition 1 (iii) and Theorem 2 (iv).

4.5 Consistency across dimensions

All properties in the previous sections are discussed under the assumption that the dimension is fixed. Letting vary allows for comparison of diversification between portfolios with different dimensions. In this section, we slightly generalize our framework by considering a diversification index as a mapping on ; note that the input vector of DQ and DR can naturally have any dimension . We present two more useful properties of DQ in this setting. For and , is the -dimensional random vector obtained by pasting and , and is the -dimensional random vector obtained by pasting and .

-

[RI]

Riskless invariance: for all , and .

-

[RC]

Replication consistency: for all and .

Riskless invariance means that adding a risk-free asset into the portfolio does not affect its diversification. For instance, the Sharpe ratio of the portfolio does not change under such an operation. Replication consistency means that replicating the same portfolio composition does not affect . Both properties are arguably desirable in most applications due to their natural interpretations.

Proposition 3.

Let be a class of risk measures decreasing in and be a continuous and law-invariant risk measure. For ,

-

(i)

If satisfies with and then satisfies [RI].

-

(ii)

If satisfies , then satisfies .

We further show in Proposition EC.5 that if [RI] is assumed, then the only option for DR is to use a non-negative . Thus, if [RI] is considered as desirable, then DQ becomes useful compared to DR as it offers more choices, and in particular, it works for any classes of monetary risk measures with including VaR and ES. Both DQ and DR satisfy [RC] and [RI] for MCP risk measures.

Example 2.

Let be a risk measure satisfying , such as or . Suppose that and , and thus . If a non-random payoff of is added to the portfolio, then , which turns to as , and it becomes negative as soon as . Hence, is improved or made negative by including constant payoffs (either as a new asset or added to an existing asset). This creates problematic incentives in optimization. On the other hand, does not suffer from this problem due to [LI] and [RI].

5 DQ based on VaR and ES

Since VaR and ES are the two most common classes of risk measures in practice, we focus on the theoretical properties of and in this section. We fix the parameter range , and we choose to be when we discuss and when we discuss , but all results hold true if we fix .

5.1 General properties

We first provide alternative formulations of and . The formulations offer clear interpretations and simple ways to compute the values of DQs. The formula (7) below can be derived from the optimization formulation for the buffered probability of exceedance in Proposition 2.2 of Mafusalov and Uryasev (2018).

Theorem 3.

For a given , and have the alternative formulas

| (5) |

and

| (6) |

where and . Furthermore, if , then

| (7) |

and otherwise

As a first observation from Theorem 3, it is straightforward to compute and on real or simulated data by applying (5) and (6) to the empirical distribution of the data.

Theorem 3 also gives a clear economic interpretation as the improvement of insolvency probability when risks are pooled. Suppose that are continuously distributed and they represent losses from assets. The total pooled capital is , which is determined by the marginals of but not the dependence structure. An agent investing only in asset with capital computed by has an insolvency probability On the other hand, by Theorem 3, is the probability that the pooled loss exceeds the pooled capital . The improvement from to , computed by , is precisely . From here, it is also clear that is equivalent to .

To compare with , recall that the two diversification indices can be rewritten as

| (8) |

From (8), we can see a clear symmetry between DQ, which measures the probability improvement, and DR, which measures the quantile improvement. DQ and DR based on ES have a similar comparison.

Next, we compare the range of DQs based on VaR and ES.

Proposition 4.

For and , and .

By Proposition 4, both and take values on a bounded interval. In contrast, the diversification ratio is unbounded, and is bounded above by only when the ES of the total risk is non-negative. Moreover, similarly to the continuity axiom of preferences (e.g., Föllmer and Schied (2016)), a bounded interval can provide mathematical convenience for applications.

Remark 3.

It is a coincidence that for and both have a maximum value . The latter maximum value is attained by a risk vector for any .

5.2 Capturing heavy tails and common shocks

In this section, we analyze three simple normal and t-models to illustrate some features of DQ regarding heavy tails and common shocks in the portfolio models. A separate paper Han et al. (2023) contains a detailed study of DQs based on VaR and ES for elliptical distributions and multivariate regularly varying models, including explicit formulas to compute DQ for these models. Here, we only present some key observations.

Let be an -dimensional standard normal random vector, and let have an inverse gamma distribution independent of . Denote by the joint distribution with independent t-marginals , where the parameter represents the degrees of freedom; see McNeil et al. (2015) for t-models. The model can be stochastically represented by

| (9) |

where are iid following the same distribution as , and independent of . In contrast, a joint t-distributed random vector has a stochastic representation that is,

| (10) |

In other words, is a standard normal random vector multiplied by a heavy-tailed common shock . All three models have the same correlation matrix, the identity matrix .

Because of the common shock in (10), large losses from components of are more likely to occur simultaneously, compared to in (9) which does not have a common shock. Indeed, is tail dependent (Example 7.39 of McNeil et al. (2015)) whereas is tail independent. As such, at least intuitively (if not rigorously), diversification for portfolio should be considered as weaker than , although both models are uncorrelated and have the same marginals.121212On a related note, as discussed by Embrechts et al. (2002), correlation is not a good measure of diversification in the presence of heavy-tailed and skewed distributions. By the central limit theorem, for , the component-wise average of (scaled by its variance) is asymptotically normal as increases, whereas the component-wise average of is always t-distributed. Hence, one may intuitively expect the order to hold.

| 0.3162 | 0.3162 | 0.3162 | 1 | |||

| 0.0235 | 0.0124 | 0.3569 | 0.2903 | 0.3162 | 1 | |

| 0.0502 | 0.0340 | 0.3162 | 0.3162 | 0.3162 | 1 | |

| Yes | Yes | Yes | No | No | No | |

| Yes | Yes | No | Yes | No | No |

| 0.3162 | 0.3162 | 0.3162 | 1 | |||

| 0.0050 | 0.0017 | 0.3415 | 0.2828 | 0.3162 | 1 | |

| 0.0252 | 0.0138 | 0.3162 | 0.3162 | 0.3162 | 1 | |

| Yes | Yes | Yes | No | No | No | |

| Yes | Yes | No | Yes | No | No |

In Tables 1 and 2, we present DQ and DR for a few different models based on , , and . We choose and or ,131313Most financial asset log-loss data have a tail-index between , which corresponds to ; see e.g., Jansen and De Vries (1991). and thus we have five models in total. As we see from Tables 1 and 2, DQs based on both VaR and ES report a lower value for and a larger value for , meaning that diversification is weaker for the common shock t-model (10) than the iid t-model (9). For the iid normal model, the diversification is the strongest according to DQ. In contrast, DR sometimes reports that the iid t-model has a larger diversification than the common shock t-model, which is counter-intuitive. In the setting of both Tables 1 and 2, a risk manager governed by would prefer the iid portfolio over the common shock portfolio, but the preference is flipped if the risk manager uses . A more detailed analysis on this phenomenon for varying is presented in Figure EC.1 in Appendix E, and consistent results are observed.

6 DQ as a function of the portfolio weight

In this section, we analyze portfolio diversification for a random vector representing losses from assets and a vector of portfolio weights, where

The total loss of the portfolio is . We write which is the portfolio loss vector with the weight . For a portfolio selection problem, we need to treat as a function of the portfolio weight . Denote by which is a known vector that does not depend on the decision variable

6.1 Convexity and quasi-convexity

We first analyze convexity and quasi-convexity of the mapping on . Recall that for any real-valued mapping on a space , is convex (resp. quasi-convex) if

for all and , where is the maximum operator. When formulated on monetary risk measures, convexity naturally represents the idea that diversification reduces the risk; see Föllmer and Schied (2016). For risk measures that are not constant additive, Cerreia-Vioglio et al. (2011) argued that quasi-convexity is more suitable than convexity to reflect the consideration of diversification; moreover, convexity and quasi-convexity are equivalent if holds for .

We first note that, for a diversification index , convexity or quasi-convexity on should not hold, as illustrated in Example 3 below.

Example 3 (Convexity or quasi-convexity on is not desirable).

Let represent any diversified portfolio (e.g., with iid normal components), and assume that is not a constant. Since the portfolio relies only on one asset and has no diversification benefit, for a good diversification index we naturally want to be larger than both and ; recall that in the setting of Theorem 2 (iii). This argument shows that it is unnatural to require to be convex or quasi-convex on ; the case of is similar. Indeed, if a real-valued satisfies and convexity on , then it is a constant (see Proposition EC.6 in Appendix E).

Despite that quasi-convexity of is unnatural on , quasi-convexity may hold for for each given ; this property will be called quasi-convexity in for short. Quasi-convexity in means that combining a portfolio with a better-diversified one on the same set of assets does not reduce the diversification of the original portfolio; this interpretation is different from quasi-convexity on which means that combining a portfolio with an arbitrary better-diversified portfolio does not reduce diversification (this is not desirable as discussed in Example 3).

In the next result, we see that DQ is quasi-convex in for convex risk measures satisfying [PH], such as ES. In contrast, DR may not be quasi-convex in for a convex risk measure since the denominator in (3) may be negative.

Theorem 4.

Let be a class of convex risk measures satisfying and decreasing in . For every and , is quasi-convex.

Theorem 4 implies, in particular, that DQ based on SD, ES, or other coherent risk measures is quasi-convex in . In contrast, the stronger condition of convexity in generally fails to hold. Indeed, we discuss in the next example that convexity in is not desirable for a good diversification index.

Example 4 (Convexity in is not desirable).

Consider a risk vector where is standard normal and is a small constant. Let and . Note that and . The portfolio is not diversified since it has only one non-zero component, and the portfolio is perfectly hedged since the sum of its components is . Hence, for a good diversification index , it should hold that and ; Theorem 2 confirms this. On the other hand, the portfolio

is not well diversified since its second component is very small compared to its first component. Intuitively, for , we expect . This shows that is not convex. One can verify that this is indeed true if is DQ or DR based on commonly used risk measures such as SD, VaR and ES.

6.2 Portfolio optimization

Next, we focus on the following optimal diversification problem

| (11) |

recall that a smaller value of DQ means better diversification.141414A possible alternative formulation to (11) is to use DQ as a constraint instead of an objective in the optimization. This is mathematically similar to a risk measure constraint (e.g., Rockafellar and Uryasev (2002) and Mafusalov and Uryasev (2018)), but it is perhaps less intuitive, as DQ is not designed to measure or control risk. We do not say that optimizing a diversification index has a decision-theoretic benefit; here we simply illustrate the advantage of DQ in computation and optimization. Whether optimizing diversification is desirable for individual or institutional investors is an open-ended question which goes beyond the current paper; we refer to Van Nieuwerburgh and Veldkamp (2010), Boyle et al. (2012) and Choi et al. (2017) for relevant discussions.

For the portfolio weight , DQ based on VaR at level is given by

and DQ based on ES is similar. In what follows, we fix and , where is for VaR and for ES, as in Section 5. Write

Proposition 5.

Proposition 5 offers efficient algorithms to optimize and in real-data applications. The values of and can be computed by many existing estimators of the individual losses (see e.g., McNeil et al. (2015)). In particular, a popular way to estimate these risk measures is to use an empirical estimator. More specifically, if we have data sampled from satisfying some ergodicity condition (being iid would be sufficient), then the empirical version of the problem (12) is

| (14) |

where is the empirical estimator of based on sample ; see McNeil et al. (2015). Write and for . Problem (14) involves a chance constraint (see e.g., Luedtke (2014) and Liu et al. (2016)). By using the big-M method (see e.g., Shen et al. (2010)) via choosing a sufficient large (e.g., it is sufficient if is larger than the components of for all ), (14) can be converted into the following linear integer program:

| (15) |

Similarly, the optimization problem (13) for can be solved the empirical version of the problem (13), which is a convex program:

| (16) |

where is the empirical estimator of based on sample . Both problems (15) and (16) can be efficiently solved by modern optimization programs, such as CVX programming (see e.g., Matmoura and Penev (2013)).

Additional linear constraints, such as those on budget or expected return, can be easily included in (12)-(16), and the corresponding optimization problems can be solved similarly.

Tie-breaking needs to be addressed when working with (14) since its objective function takes integer values. In dynamic portfolio selection, it is desirable to avoid adjusting positions too drastically or frequently. Therefore, in the real-data analysis in Section 7.3, among tied optimizers, we pick the closest one (in -norm on ) to a given benchmark , the portfolio weight of the previous trading period. With this tie-breaking rule, we solve

| (17) |

where is the optimum of (14). A tie-breaking for (16) may need to be addressed similarly since (16) is not strictly convex.

7 Numerical illustrations

To illustrate the performance of DQ, we collect the stocks’ historical data from Yahoo Finance and conduct three sets of numerical experiments based on financial data. We use the period from January 3, 2012, to December 31, 2021, with a total of 2518 observations of daily losses and 500 trading days for the initial training. In Section 7.1, we first compare DQs and DRs based on and . In Section 7.2, we calculate the values of and under different selections of stocks. Finally, we construct portfolios by minimizing , and and by the mean-variance criterion in Section 7.3.

7.1 Comparing DQ and DR

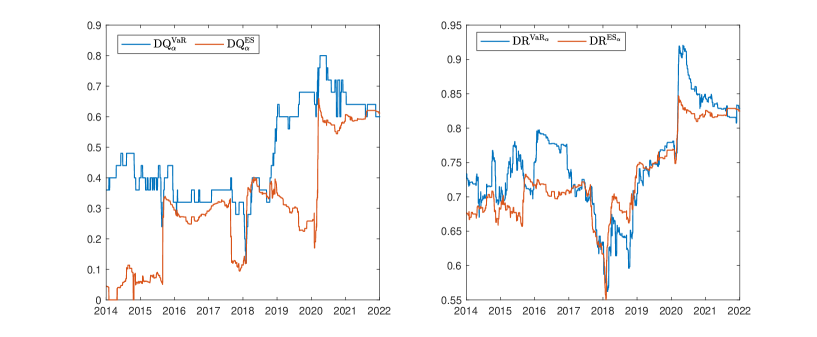

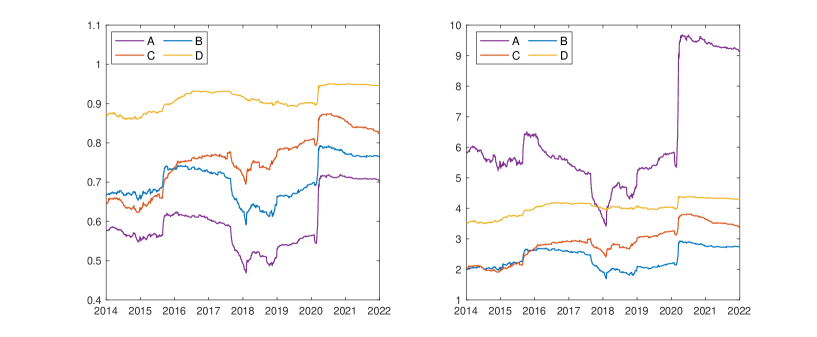

We first identify the largest stock in each of the S&P 500 sectors ranked by market cap in 2012. Among these stocks, we select the 5 largest stocks (XOM from ENR, AAPL from IT, BRK/B from FINL, WMT from CONS, and GE from INDU) to build our portfolio. We compute , , and on each day using the empirical distribution in a rolling window of 500 days, where we set .

Figure 2 shows that the values of DQ and DR are between 0 and 1. This corresponds to the observation in Section 4.2 that is equivalent to . DQ has a similar temporal pattern to DR in the above period of time, with a large jump when COVID-19 exploded, which is more visible for DQ than for DR. We remind the reader that DQ and DR are not meant to be compared on the same scale, and hence the fact that DQ has a larger range than DR should be taken lightly. We also note that the values of are in discrete grids. This is because the empirical distribution function takes value in multiples of there is the sample size (500 in this experiment) and hence takes the values for an integer ; see (5). If a smooth curve is preferred, then one can employ a smoothed VaR through linear interpolation. This is a standard technique for handling VaR; see McNeil et al. (2015, Section 9.2.6) and Li and Wang (2022, Remark 8 and Appendix B).

7.2 DQ for different portfolios

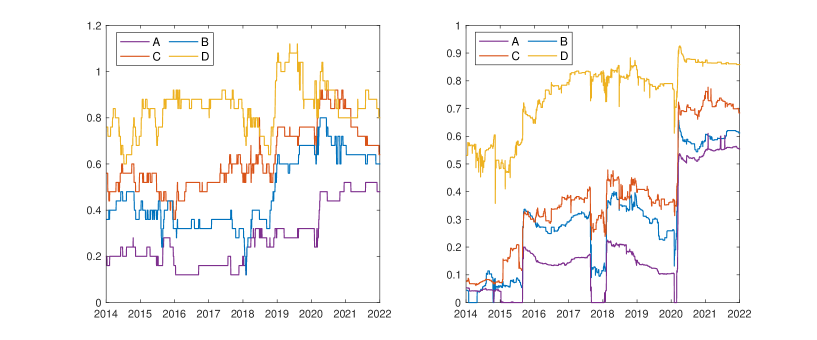

In this section, we fix and calculate the values of and under different portfolio compositions of stocks. We consider portfolios with the following stock compositions:

-

(A)

the two largest stocks from each of the 10 different sectors of S&P 500;

-

(B)

the largest stock from each of 5 different sectors of S&P 500 (as in Section 7.1);

-

(C)

the 5 largest stocks, AAPL, MSFT, IBM, GOOGL and ORCL, from the Information Technology (IT) sector;

-

(D)

the 5 largest stocks, BRK/B, WFC, JPM, C and BAC, from the Financials (FINL) sector.

We make a few observations from Figure 3. Both and provide similar comparative results. The order (A)(B)(C)(D) is consistent with our intuition.151515The observations here are consistent with those from applying (which is also a DQ) in the same setting; see Appendix F. First, portfolio (A) of 20 stocks has the strongest diversification effect among the four compositions. Second, portfolio (B) across 5 sectors has stronger diversification than (C) and (D) within one sector. Third, portfolio (C) of 5 stocks within the IT sector has a stronger diversification than portfolio (D) of 5 stocks within the FINL sector, consistent with the fact that the stocks in the IT sector are less correlated. Moreover, for the FINL sector is larger than 1 during some period of time, which means that there is no diversification benefit if risk is evaluated by VaR. All DQ curves based on ES show a large up-ward jump around the COVID-19 outbreak; such a jump also exists for curves based on VaR but it is less pronounced.

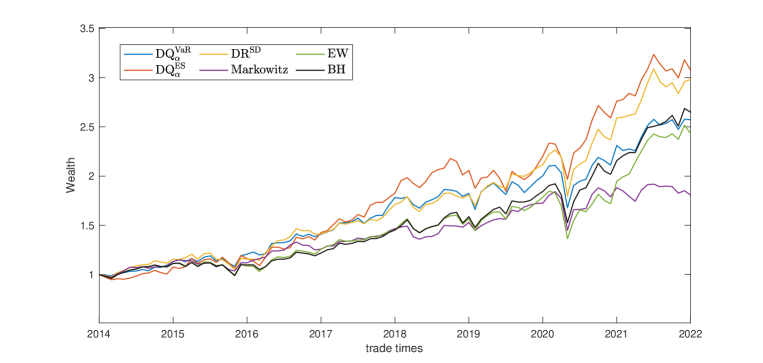

7.3 Optimal diversified portfolios

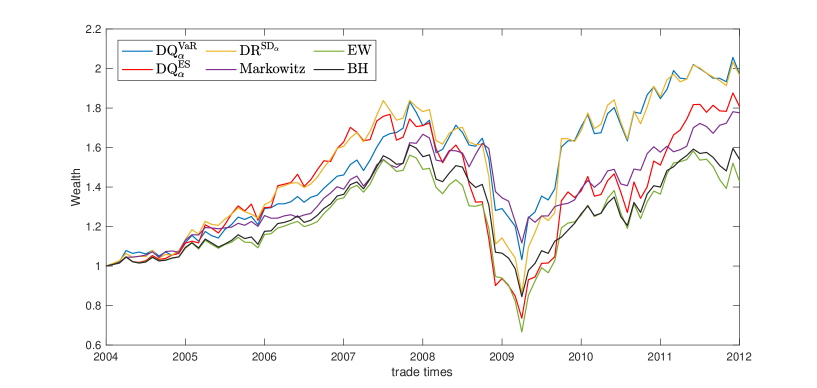

In this section, we fix and build portfolios via , , , and the mean-variance criterion in the Markowitz (1952) model.161616One may try other portfolio criteria other than mean-variance. For instance, Levy and Levy (2004) found that portfolio strategies based on prospect theory perform similarly to the mean-variance strategies. The optimal portfolio problems using and the Markowitz model are well studied in literature; see e.g. Choueifaty and Coignard (2008). We compare these portfolio wealth with the equal weighted (EW) portfolio and the simple buy-and-hold (BH) portfolio. For an analysis on the EW strategy, see DeMiguel et al. (2009).

We apply the algorithms in Proposition 5 to optimize and , which are extremely fast. A tie-breaking is addressed for each objective as in (17). Minimization of and the Markowitz model can be solved by existing algorithms. The initial wealth is set to , and the risk-free rate is , which is the 10-year yield of the US treasury bill in Jan 2014. The target annual expected return for the Markowitz portfolio is set to . We optimize the portfolio weights in each month with a rolling window of 500 days. That is, in each month, roughly 21 trading days, starting from January 2, 2014, we use the preceding 500 trading days to compute the optimal portfolio weights using the method described above. The portfolio is rebalanced every month. We choose the 4 largest stocks from each of the 10 different sectors of S&P 500 ranked by market cap in 2012 as the portfolio compositions (40 stocks in total). The portfolio performance is reported in Figure 4 with some summary statistics in Table 3.

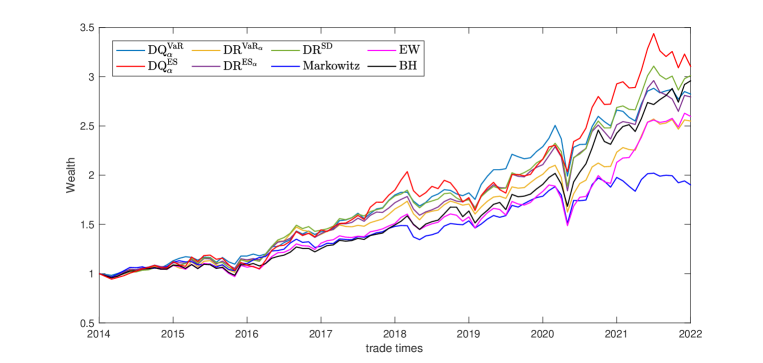

From these results, we can see that the portfolio optimization strategies based on minimizing DQ perform on par with other strategies such as the EW, BH strategies and those by minimizing or mean-variance. We remark that it is not our intention to analyze which diversification strategy performs the best, which is a challenging question that needs a separate study; also, we do not suggest diversification should or should not be optimized in practice. The empirical results here are presented to illustrate how our proposed diversification indices work in the context of portfolio selection. More empirical results with some other datasets and portfolio strategies are given in Appendix F, and the results show similar observations.

| Markowitz | EW | BH | ||||

|---|---|---|---|---|---|---|

| AR | 12.56 | 14.59 | 14.36 | 7.93 | 11.91 | 12.88 |

| AV | 14.64 | 15.74 | 14.99 | 12.98 | 15.92 | 14.34 |

| SR | 66.40 | 74.66 | 76.85 | 39.22 | 56.95 | 70.02 |

8 Concluding remarks

In this paper, we propose putting forward six axioms to jointly characterize a new index of diversification. The new diversification index DQ has favourable features both theoretically and practically, and it is contrasted with its competitors, in particular DR. At a high level, because of the symmetry in Figure 1 (see also (8)), we expect both DQ and DR to have advantages and disadvantages in different applications, and none should fully dominate the other. Nevertheless, we find many attractive features of DQ through the results in this paper, which suggest that DQ may be a better choice in many situations.

We summarize these features below. Certainly, some of these features are shared by DR, but many are not. (i) DQ defined on a class of MCP risk measures can be uniquely characterized by six intuitive axioms (Theorem 1), laying an axiomatic foundation for using DQ as a diversification index. (ii) DQ further satisfies many properties for common risk measures (Propositions 1-3). These properties are not shared by the corresponding DR. (iii) DQ is intuitive and interpretable with respect to dependence and common perceptions of diversification (Theorem 2). (iv) DQ can be applied to a wide range of risk measures, such as the regulatory risk measures VaR and ES, as well as entropic risk measures. In cases of VaR and ES, DQ has simple formulas and convenient properties (Theorem 3 and Proposition 4). (v) DQ based on a class of convex risk measures is quasi-convex in portfolio weights (Theorem 4). (vi) Portfolio optimization of DQs based on VaR and ES can be computed very efficiently (Proposition 5). (vii) DQ can be easily applied to real data and it produces results that are consistent with our usual perception of diversification (Section 7).

We also mention a few interesting questions on DQ, which call for thorough future study. (i) DQ is defined through a class of risk measures. It would be interesting to formulate DQ using expected utility or behavioral decision models, to analyze the decision-theoretic implications of DQ. For instance, DQ based on entropic risk measures can be equivalently formulated using exponential utility functions. Alternatively, one may also build DQ directly from acceptability indices (see Remark 1). (ii) To compute DQ, one needs to invert the decreasing function . In the case of VaR and ES, the formula for this inversion is simple (Theorem 3). For more complicated classes of risk measures, this computation may be complicated and requires detailed analysis. (iii) For general distributions and risk measures other than VaR and ES, finding analytical formulas or efficient algorithms for optimal diversification using either DQ or DR is a challenging task, and it is unclear which diversification index is easier to work within a specific application.

Acknowledgements. The authors thank Fabio Bellini, Aleš Černý, An Chen, Jan Dhaene, Paul Embrechts, Paul Glasserman, Pablo Koch-Medina, Dimitrios Konstantinides, Henry Lam, Jean-Gabriel Lauzier, Fabio Macherroni, Massimo Marinacci, Cosimo Munari, Alexander Schied, Qihe Tang, Stan Uryasev, Peter Wakker, and Zuoquan Xu for helpful comments and discussions on an earlier version of the paper. Liyuan Lin is supported by the Hickman Scholarship from the Society of Actuaries. Ruodu Wang is supported by the Natural Sciences and Engineering Research Council of Canada (RGPIN-2018-03823, RGPAS-2018-522590) and the Sun Life Research Fellowship.

References

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J.-M. and Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9(3), 203–228.

- BCBS (2019) BCBS (2019). Minimum Capital Requirements for Market Risk. February 2019. Basel Committee on Banking Supervision. Basel: Bank for International Settlements, Document d457.

- Bellini et al. (2022) Bellini, F., Fadina, T., Wang, R. and Wei, Y. (2022). Parametric measures of variability induced by risk measures. Insurance: Mathematics and Economics, 106, 270–284.

- Bellini et al. (2014) Bellini, F., Klar, B., Müller, A. and Rosazza Gianin, E. (2014). Generalized quantiles as risk measures. Insurance: Mathematics and Economics, 54(1), 41–48.

- Bernard et al. (2014) Bernard, C., Jiang, X. and Wang, R. (2014). Risk aggregation with dependence uncertainty. Insurance: Mathematics and Economics, 54, 93–108.

- Boyle et al. (2012) Boyle, P., Garlappi, L., Uppal, R. and Wang, T. (2012). Keynes meets Markowitz: The trade-off between familiarity and diversification. Management Science, 58(2), 253–272.

- Bürgi et al. (2008) Bürgi, R., Dacorogna, M. M. and Iles, R. (2008). Risk aggregation, dependence structure and diversification benefit. In: Stress testing for financial institutions, Riskbooks, Incisive Media, London, 265–306.

- Cerreia-Vioglio et al. (2011) Cerreia-Vioglio, S., Maccheroni, F., Marinacci, M. and Montrucchio, L. (2011). Risk measures: Rationality and diversification. Mathematical Finance, 21(4), 743–774.

- Chambers (2009) Chambers, C. P. (2009). An axiomatization of quantiles on the domain of distribution functions. Mathematical Finance, 19(2), 335–342.

- Cherny and Madan (2009) Cherny, A. and Madan, D. (2009). New measures for performance evaluation. The Review of Financial Studies, 22(7), 2571–2606.

- Choi et al. (2017) Choi, N., Fedenia, M., Skiba, H. and Sokolyk, T. (2017). Portfolio concentration and performance of institutional investors worldwide. Journal of Financial Economics, 123(1), 189–208.

- Choueifaty and Coignard (2008) Choueifaty, Y. and Coignard, Y. (2008). Toward maximum diversification. The Journal of Portfolio Management, 35(1), 40–51.

- Corbett and Rajaram (2006) Corbett, C. J. and Rajaram, K. (2006). A generalization of the inventory pooling effect to non-normal dependent demand. Manufacturing and Service Operations Management, 8(4), 351–358.

- D’Acunto et al. (2019) D’Acunto, F., Prabhala, N. and Rossi, A. G. (2019). The promises and pitfalls of robo-advising. The Review of Financial Studies, 32(5), 1983–2020.

- Debreu (1954) Debreu, G. (1954). Representation of a preference ordering by a numerical function. Thrall, R.M., Coombs, C.H. and Davis, R.L., Editors, pp. 159–165.

- DeMiguel et al. (2009) DeMiguel, V., Garlappi, L. and Uppal, R. (2009). Optimal versus naive diversification: How inefficient is the 1/N portfolio strategy? The Review of Financial Studies, 22(5), 1915–1953.

- Denis et al. (2002) Denis, D. J., Denis, D. K. and Yost, K. (2002). Global diversification, industrial diversification, and firm value. The Journal of Finance, 57(5), 1951–1979.

- Denneberg (1990) Denneberg, D. (1990). Premium calculation: Why standard deviation should be replaced by absolute deviation. ASTIN Bulletin, 20, 181–190.

- Dhaene et al. (2012) Dhaene, J., Tsanakas, A., Valdez, E. A. and Vanduffel, S. (2012). Optimal capital allocation principles. Journal of Risk and Insurance, 79(1), 1–28.

- Drapeau and Kupper (2013) Drapeau, S. and Kupper, M. (2013). Risk preferences and their robust representation. Mathematics of Operations Research, 38(1), 28–62.

- EIOPA (2011) EIOPA (2011). Equivalence assessment of the Swiss supervisory system in relation to articles 172, 227 and 260 of the Solvency II Directive, EIOPA-BoS-11-028.

- Embrechts et al. (2009) Embrechts, P., Furrer, H. and Kaufmann, R. (2009). Different kinds of risk. In Handbook of financial time series (pp. 729–751). Springer, Berlin, Heidelberg.

- Embrechts et al. (2018) Embrechts, P., Liu, H. and Wang, R. (2018). Quantile-based risk sharing. Operations Research, 66(4), 936–949.

- Embrechts et al. (2002) Embrechts, P., McNeil, A. and Straumann, D. (2002). Correlation and dependence in risk management: properties and pitfalls. In Risk Management: Value at Risk and Beyond (Ed. Dempster, M. A. H.), 176–223, Cambridge University Press.

- Embrechts et al. (2014) Embrechts, P., Puccetti, G., Rüschendorf, L., Wang, R. and Beleraj, A. (2014). An academic response to Basel 3.5. Risks, 2(1), 25-48.

- Embrechts et al. (2015) Embrechts, P., Wang, B. and Wang, R. (2015). Aggregation-robustness and model uncertainty of regulatory risk measures. Finance and Stochastics, 19(4), 763–790.

- Emmer et al. (2015) Emmer, S., Kratz, M. and Tasche, D. (2015). What is the best risk measure in practice? A comparison of standard measures. Journal of Risk, 18(2), 31–60.

- Fama and Miller (1972) Fama, E. F. and Miller, M. H. (1972). The Theory of Finance. Holt, Rinehart, and Winston, New York.

- Föllmer and Schied (2016) Föllmer, H. and Schied, A. (2016). Stochastic Finance. An Introduction in Discrete Time. Fourth Edition. Walter de Gruyter, Berlin.

- Furman et al. (2017) Furman, E., Wang, R. and Zitikis, R. (2017). Gini-type measures of risk and variability: Gini shortfall, capital allocation and heavy-tailed risks. Journal of Banking and Finance, 83, 70–84.

- Gilboa et al. (2010) Gilboa, I. Maccheroni, F., Marinacci, M. and Schmeidler, D. (2010). Objective and subjective rationality in a multiple prior model. Econometrica, 78(2), 755–770.

- Gilboa et al. (2019) Gilboa, I., Postlewaite, A. and Samuelson, L. (2019). What are axiomatizations good for? Theory and Decision, 86(3–4), 339–359.

- Green and Hollifield (1992) Green, R. C. and Hollifield, B. (1992). When will mean-variance efficient portfolios be well diversified? The Journal of Finance, 47(5), 1785–1809.

- Guan et al. (2022) Guan, Y., Jiao, Z. and Wang, R. (2022). A reverse Expected Shortfall optimization formula. arXiv: 2203.02599.

- Han et al. (2023) Han, X., Lin, L. and Wang, R. (2023). Diversification quotients based on VaR and ES. arXiv: 2301.03517.

- Huber and Ronchetti (2009) Huber, P. J. and Ronchetti E. M. (2009). Robust Statistics. Second ed., Wiley Series in Probability and Statistics. Wiley, New Jersey. First ed.: Huber, P. (1980).

- Ibragimov et al. (2011) Ibragimov, R., Jaffee, D. and Walden, J. (2011). Diversification disasters. Journal of Financial Economics, 99(2), 333–348.

- Jakobsons et al. (2016) Jakobsons, E., Han, X. and Wang, R. (2016). General convex order on risk aggregation. Scandinavian Actuarial Journal, 2016(8), 713-740.

- Jansen and De Vries (1991) Jansen, D. W. and De Vries, C. G. (1991). On the frequency of large stock returns: Putting booms and busts into perspective. The Review of Economics and Statistics, 73(1), 18–24.

- Klibanoff et al. (2005) Klibanoff, P., Marinacci, M. and Mukerji, S. (2005). A smooth model of decision making under ambiguity. Econometrica, 73(6), 1849–1892.

- Koumou (2020) Koumou, G. B. (2020). Diversification and portfolio theory: A review. Financial Markets and Portfolio Management, 34(3), 267–312.

- Koumou and Dionne (2022) Koumou, G. B. and Dionne, G. (2022). Coherent diversification measures in portfolio theory: An axiomatic foundation. Risks, 10(11), 205.

- Kováčová et al. (2020) Kováčová, G., Rudloff, B. and Cialenco, I. (2020). Acceptability maximization. arXiv: 2012.11972.

- Kusuoka (2001) Kusuoka, S. (2001). On law invariant coherent risk measures. Advances in Mathematical Economics, 3, 83–95.

- Levy and Levy (2004) Levy, H. and Levy, M. (2004). Prospect theory and mean-variance analysis. The Review of Financial Studies, 17(4), 1015–1041.

- Levy and Sarnat (1970) Levy, H. and Sarnat, M. (1970). International diversification of investment portfolios. The American Economic Review, 60(4), 668–675.

- Li and Wang (2022) Li, H. and Wang, R. (2022). PELVE: Probability equivalent level of VaR and ES. Journal of Econometrics, published online, doi.org/10.1016/j.jeconom.2021.12.012.

- Liu et al. (2016) Liu, X., Küçükyavuz, S. and Luedtke, J. (2016). Decomposition algorithms for two-stage chance-constrained programs. Mathematical Programming, 157(1), 219–243.

- Luedtke (2014) Luedtke, J. (2014). A branch-and-cut decomposition algorithm for solving chance-constrained mathematical programs with finite support. Mathematical Programming, 146(1), 219–244.

- Maccheroni et al. (2009) Maccheroni, F., Marinacci, M., Rustichini, A. and Taboga, M. (2009). Portfolio selection with monotone mean-variance preferences. Mathematical Finance, 19(3), 487–521.

- Mafusalov and Uryasev (2018) Mafusalov A. and Uryasev S. (2018). Buffered probability of exceedance: Mathematical properties and optimization. SIAM Journal on Optimization, 28(2), 1077–1103.

- Mainik and Rüschendorf (2010) Mainik, G. and Rüschendorf, L (2010). On optimal portfolio diversification with respect to extreme risks. Finance and Stochastics, 14(4), 593–623.

- Mao and Wang (2020) Mao, T. and Wang, R. (2020). Risk aversion in regulatory capital calculation. SIAM Journal on Financial Mathematics, 11(1), 169–200.

- Markowitz (1952) Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1), 77–91.

- Matmoura and Penev (2013) Matmoura, Y. and Penev, S. (2013). Multistage optimization of option portfolio using higher order coherent risk measures. European Journal of Operational Research, 227(1), 190–198.

- McNeil et al. (2015) McNeil, A. J., Frey, R. and Embrechts, P. (2015). Quantitative Risk Management: Concepts, Techniques and Tools. Revised Edition. Princeton, NJ: Princeton University Press.

- Puccetti and Wang (2015) Puccetti, G. and Wang R. (2015). Extremal dependence concepts. Statistical Science, 30(4), 485–517.

- Rockafellar and Uryasev (2002) Rockafellar, R. T. and Uryasev, S. (2002). Conditional value-at-risk for general loss distributions. Journal of Banking and Finance, 26(7), 1443–1471.

- Rockafellar et al. (2006) Rockafellar, R. T., Uryasev, S. and Zabarankin, M. (2006). Generalized deviations in risk analysis. Finance and Stochastics, 10(1), 51–74.

- Rothschild and Stiglitz (1970) Rothschild, M. and Stiglitz, J. E. (1970). Increasing risk: I. A definition. Journal of Economic Theory, 2(3), 225–243.

- Rüschendorf (2013) Rüschendorf, L. (2013).Mathematical Risk Analysis. Dependence, Risk Bounds, Optimal Allocations and Portfolios. Springer, Heidelberg.

- Samuelson (1967) Samuelson, P. A. (1967). General proof that diversification pays. Journal of Financial and Quantitative Analysis, 2(1), 1–13.

- Shaked and Shanthikumar (2007) Shaked, M. and Shanthikumar, J. G. (2007). Stochastic Orders. Springer Series in Statistics.

- Sharpe (1964) Sharpe, (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance, 19(3), 425–442.

- Shen et al. (2010) Shen, S., Smith, J. C. and Ahmed, S. (2010). Expectation and chance-constrained models and algorithms for insuring critical paths. Management Science, 56(10), 1794–1814.

- Tasche (2007) Tasche, D. (2007). Capital allocation to business units and sub-portfolios: The Euler principle. arXiv: 0708.2542.

- Tu and Zhou (2011) Tu, J. and Zhou, G. (2011). Markowitz meets Talmud: A combination of sophisticated and naive diversification strategies. Journal of Financial Economics, 99(1), 204–215.

- Van Nieuwerburgh and Veldkamp (2010) Van Nieuwerburgh, S. and Veldkamp, L. (2010). Information acquisition and under-diversification. The Review of Economic Studies, 77(2), 779–805.

- Wang and Wang (2016) Wang, B. and Wang, R. (2016). Joint mixability. Mathematics of Operations Research, 41(3), 808–826.

- Wang et al. (2020) Wang, R., Wei, Y. and Willmot, G. E. (2020). Characterization, robustness and aggregation of signed Choquet integrals. Mathematics of Operations Research, 45(3), 993–1015.

- Wang and Wu (2020) Wang, R. and Wu, Q. (2020). Dependence and risk attitudes: An equivalence. SSRN: 3707709.

- Wang and Zitikis (2021) Wang, R. and Zitikis, R. (2021). An axiomatic foundation for the Expected Shortfall. Management Science, 67(3), 1413–1429.

- Yaari (1987) Yaari, M. E. (1987). The dual theory of choice under risk. Econometrica, 55(1), 95–115.

Technical appendices

Outline of the appendices

We organize the technical appendices as follows. In Appendix A, we provide an axiomatization result of DQ via the relation of preference. The proofs of the main results, Theorems 1–4, are presented in Appendix B. Additional results, discussions, and proofs of propositions are presented in Appendices C (for Section 2), D (for Section 4), E (for Section 5), F (for Section 6). Finally, in Appendix G, we present other examples for the optimal portfolio problem which complement the empirical studies in Section 7.3.

Appendix A Axiomatization of DQ using preferences

In this section, we provide an axiomatization of DQ as in Theorem 1 without specifying a risk measure . We first define the preference of a decision maker over risks. A preference relation is defined by a non-trivial total preorder171717A preorder is a binary relation on , which is reflexive and transitive. A binary relation is reflexive if for all , and transitive if and imply . A non-trivial total preorder is a preorder which in addition is complete, that is, or for all , and there exist at least two alternatives , such that is preferred over strictly. on . As usual, and correspond to the antisymmetric and equivalence relations, respectively. On the preference of risk, the relation means the agent prefers to for any . We will use the following axioms.

-

[A1]

.

-

[A2]

for any .

-

[A3]

for any .

-

[A4]

For any , there exists such that .

The four axioms are rather standard and we only briefly explain them. The axiom [A1] means that the agent always prefers a smaller loss. The axioms [A2] and [A3] mean that if the agent prefers one random loss over another, then this is preserved under any strictly increasing linear transformations. The axiom [A4] implies that any random losses can be equally favourable as a constant loss which is commonly referred to as a certainty equivalence.

A numerical representation of a preference is a mapping , such that for all . In other words, is the preference of an agent favouring less risk evaluated via . There is a simple relationship between preferences satisfying [A1]-[A4] and MCP risk measures.

Lemma EC.1.

A preference satisfies – if and only if it can be represented by an MCP risk measure .

Proof.

The “if” statement is straightforward to check, and we will show the “only if” statement. The preference can be represented by a risk measure through for all since is separable by [A1] and [A4]; see Debreu (1954) and Drapeau and Kupper (2013). If , then by using [A1]–[A3], the preference is trivial, contradicting our assumption on . Hence, using [A1], , we can further let and . It is then straightforward to verify that is MCP from [A1]-[A3]. ∎

Similarly to Section 3, but with the preference replacing the risk measure , we denote by if for each , by if for each , and by if for each . With this new formulation and everything else unchanged, the axioms of rationality, normalization and continuity are now denoted by , and .

Proposition EC.1.

A diversification index satisfies , , , , and for some preference satisfying – if and only if is for some decreasing families of MCP risk measures. Moreover, in both directions of the above equivalence, it can be required that represents .

Appendix B Proofs of Theorems 1–4

Proof of Theorem 1.

For and a risk measure , denote by and .

We first verify the “if” statement. By definition, it is straightforward to see that is non-negative. For all , if satisfies and , then the properties of [LI] and [SI] hold for . To show [LI], for , we have

Hence, satisfy [LI]. For , we have

Thus, satisfies [SI].

To show , for such that and , we have and for all . Hence,

To show , for , we have . If , it is clear that and holds as for any . Now, we assume that . For any , we have . Since for each and as , for any , there exists such that for all . For any , let . It is clear that for all . Hence, for all , there exists such that for all , which implies . Therefore, .

To show , it is straightforward that Let for any . We have

If and , then . Hence, .

Next, we will show the “only if” statement. Assume that satisfies , , , , and . Note that for all since for any . Hence, by using , we know that implies . Using [LI], we have if . This means that is determined by . Define the mapping

| (EC.1) |

with the convention . Next, we will verify several properties of .

- (a)

-

(b)

for all and . This follows directly from (EC.1), [SI] of and positive homogeneity of which gives .

-

(c)

for all with . This follows directly from (EC.1).

-

(d)

. This follows directly from (EC.1) and in .

-

(e)

for . Let . By (c), we have . Assume ; that is, there exists such that for all . Let for . By (EC.1), there exists a sequence such that and . For , we have , which implies as . By , we have ; that is, for any , there exists such that for all , which is a contradiction. Therefore, we have .

Let . For each , let . Since is monotone, is a decreasing set; i.e., implies for all . Moreover, is conic; i.e., implies for all . Moreover, we have for , and since .

Let for . Since is defined via a conic acceptance set, is a class of MCP risk measures; see Föllmer and Schied (2016). It is also clear that is decreasing in . Note that implies . Hence,

For , using (e), we have for all implies . Then we have

Therefore, for all . Using (a), we get, for all ,

Let . Together with [PH] of , implies that

and it is equivalent to for . For any and , we have . For any , let such that . For , we have and . By [LI] and , we have , which implies that and . Hence, the value of does not change by replacing with . Therefore,

for any . For any , let . We can show that

and . ∎

Proof of Theorem 2.

(i) As a.s. and , it is clear that in (4), which implies . Conversely, if , then . By definition of and , this implies , and hence a.s.

(ii) We first show the “only if” statement. As is left continuous and non-flat from the left at ) and there exists such that

for all . Hence, we have , which leads to .

Next, we show the “if” statement. As , we have . By (4), there exists such that

Because is non-flat from the left at , we have

(iii) If satisfies , for where , we have

It is clear that . Together with the non-flat condition and for all , we have , and thus .

(iv) If is comonotonic-additive and is comonotonic, then

which, together with the non-flat condition, implies that , and thus . ∎

Proof of Theorem 3.

We first show (5). For any , and , by Lemma 1 of Guan et al. (2022), if and only if . Hence,

and (5) follows. The formula (6) for follows from a similar argument to (5) by noting that is a random variable with .

Next, we show the last statement of the theorem. If , then by Theorem 2 (i).

Below, we assume . The formula (7) is very similar to Proposition 2.2 of Mafusalov and Uryasev (2018), where we additionally show that the minimizer to (7) is not . Here we present a self-contained proof based on the well-known formula of ES (Rockafellar and Uryasev (2002)),

Using this formula, we obtain, by writing for ,

Let . It is clear that . Moreover,

By Theorem 1 (iii), we have , and hence . The continuity of yields that and thus (7) holds. ∎

Proof of Theorem 4.

Fixed . Let be given by for . From of , we have Convexity of implies convexity of . Hence, for the portfolio weight , DQ based on at level is given by

which gives us quasi-convexity. ∎

Appendix C Additional results for Section 2

In this appendix, we present an impossibility result showing a conflicting nature of the three natural properties [+], [LI] and [SI] for diversification indices defined via risk measures. As mentioned in Section 2, the most commonly used diversification indices depend on through its values assessed by some risk measure . That is, given a risk measures and a portfolio , the diversification index can be written as

| (EC.2) |

We will say that is -determined if (EC.2) holds. Often, one may further choose so that decreases in and increases in for each , for a proper interpretation of measuring diversification.

We show that a diversification index based on an MCP risk measure, such as VaR or ES satisfying all three properties [+], [LI] and [SI] can take at most different values. In this case, we will say that the diversification index is degenerate. In fact, this result can be extended to more general properties and with and of the risk measure , with definitions given at the beginning of Section 4.

Proposition EC.2.

Fix . Suppose that a risk measure satisfies and with and . A diversification index is -determined and satisfies [+], [LI] and [SI] if and only if for all ,

| (EC.3) |

where for some .

We first present a lemma to prepare for the proof of Proposition EC.2.

Lemma EC.2.

A function satisfies, for all , , and , (i) and (ii) , if and only if there exist such that

| (EC.4) |

where , for all and .

Proof.

First, we show that in (EC.4) satisfies (i) and (ii). Assume that . For any and , it is clear that and . Therefore, (i) and (ii) are satisfied. The cases of and follow by the same argument.

Next, we verify the “only if” part. Given and satisfying , let . For any , we have . Therefore,