Online Resource Allocation under Horizon Uncertainty

Abstract

We study stochastic online resource allocation: a decision maker needs to allocate limited resources to stochastically-generated sequentially-arriving requests in order to maximize reward. At each time step, requests are drawn independently from a distribution that is unknown to the decision maker. Online resource allocation and its special cases have been studied extensively in the past, but prior results crucially and universally rely on the strong assumption that the total number of requests (the horizon) is known to the decision maker in advance. In many applications, such as revenue management and online advertising, the number of requests can vary widely because of fluctuations in demand or user traffic intensity. In this work, we develop online algorithms that are robust to horizon uncertainty. In sharp contrast to the known-horizon setting, no algorithm can achieve even a constant asymptotic competitive ratio that is independent of the horizon uncertainty. We introduce a novel generalization of dual mirror descent which allows the decision maker to specify a schedule of time-varying target consumption rates, and prove corresponding performance guarantees. We go on to give a fast algorithm for computing a schedule of target consumption rates that leads to near-optimal performance in the unknown-horizon setting. In particular, our competitive ratio attains the optimal rate of growth (up to logarithmic factors) as the horizon uncertainty grows large. Finally, we also provide a way to incorporate machine-learned predictions about the horizon which interpolates between the known and unknown horizon settings.

1 Introduction

Online resource allocation is a general framework that includes as special cases various fundamental problems like network revenue management (Talluri and Van Ryzin, 2004), online advertising (Mehta, 2013), online linear/convex programming (Agrawal and Devanur, 2014; Agrawal et al., 2014; Devanur et al., 2011; Kesselheim et al., 2014), bidding in repeated auctions (Balseiro and Gur, 2019), and assortment optimization under inventory constraints (Golrezaei et al., 2014). It captures any setting in which a decision-maker endowed with a limited amount of resources faces sequentially-arriving requests, each of which consumes a certain amount of resources and generates a reward. At each time step, the decision maker observes the request and then takes an action, with the overarching aim of maximizing cumulative reward subject to resource constraints. In this work, we focus on the setting in which requests are generated by some stationary distribution unknown to the decision maker. We impose very mild assumptions on this distribution, and in particular do not require the requests to satisfy common convexity assumptions.

To the best of our knowledge, all of the previous works on stochastic online resource allocation (with the exception of the concurrent work of Brubach et al. 2019, Bai et al. 2022, and Aouad and Ma 2022) assume that the total number of requests (horizon) is known to the decision maker. Importantly, this assumption is vital for previous algorithms and performance guarantees because it allows them to compute a per-period resource budget (total amount of resources divided by total number of requests) and use it as the target consumption in each time step. However, if the total number of requests is not known to the decision maker, one can no longer compute this quantity and these previous works fail to offer any guidance.

Juxtapose this with a world in which viral trends are becoming ever more common, causing online advertising platforms, retailers and service providers to routinely experience traffic spikes. These spikes inject uncertainty into the system and make it difficult to accurately predict the total number of requests that will arrive. In fact, these spikes present lucrative opportunities for the advertiser/retailer, which makes addressing the uncertainty even more pertinent (Esfandiari et al., 2015). Moreover, it is usually difficult to predict these spikes, e.g. a news story breaks about COVID-travel bans being lifted, which results in a sudden and large uptick in the number of advertising opportunities for an airline. In fact, search-traffic spikes might be so large that they cause websites to crash111https://developers.google.com/search/blog/2012/02/preparing-your-site-for-traffic-spike. This motivates us to relax the previously-ubiquitous known-horizon assumption and address this omission in the literature by developing algorithms which are robust to horizon uncertainty. We use as our benchmark the hindsight optimal allocation that can be computed with full knowledge of all requests and the time horizon.

1.1 Main Contributions

Impossibility Results. If no assumptions are made about the horizon, it has been shown in the context of matching (Brubach et al., 2019) and prophet inequalities (Alijani et al., 2020) that no algorithm can guarantee a positive constant fraction of the hindsight optimal reward. Contrast this with the online convex optimization literature, where one can easily obtain a low-regret algorithm (i.e., asymptotic competitive ratio of one) for the unknown horizon setting by applying the doubling trick to a low-regret algorithm for the known-horizon setting (Shalev-Shwartz et al., 2012; Hazan et al., 2016)222Specifically, the doubling trick involves repeatedly running the low-regret algorithm for the known-horizon setting with increasing lengths of horizons. This is possible because the online convex optimization problem decouples across time into independent subproblems. Such decomposition is not possible in our problem because of the resource constraints: resources that have been consumed in the past restrict future actions of the algorithm.. In this paper, we prove a new impossibility result for the setting when the horizon is constrained to lie in an uncertainty window that is known to the decision maker, which is the mildest possible assumption that renders the problem interesting. In the uncertainty-window setting, we show that no online algorithm can achieve a greater than fraction of the hindsight optimal reward (Theorem 2). This upper bound holds even when (i) there is only 1 type of resource, (ii) the decision maker receives the same request at each time step, (iii) this request is known to the decision maker ahead of time, (iv) the request has a smooth concave reward function and linear resource consumption, (v) is arbitrarily large, and (vi) the initial resource endowment scales with the horizon. In particular, unlike the known-horizon setting, vanishing regret is impossible to achieve under horizon uncertainty, leading us to focus on developing algorithms with a good asymptotic competitive ratio (fraction of the hindsight optimal reward).

Variable Target Dual Mirror Descent. Dual mirror descent is a natural algorithm for the known-horizon setting introduced by Balseiro et al. (2020), who build on a long line of primal-dual algorithms for online allocation problems (Agrawal and Devanur, 2014; Devanur et al., 2011; Gupta and Molinaro, 2016). It maintains a price (i.e., dual variable) for each resource and then dynamically updates them with the goal of consuming the per-period resource budget at each step—if the resource is being over-consumed, increase its price; and vice-versa. As stated earlier, this approach fails if the horizon is not known because the per-period budget cannot be computed ahead of time. A natural approach to handle horizon uncertainty is to use dual mirror descent with some proxy horizon in the hopes of getting good performance for all . Unfortunately, as we show in Section 2.1, this approach can be extremely suboptimal, not just for dual mirror descent but for any algorithm which is optimal for the known-horizon setting. Thus, the unknown-horizon setting calls for new algorithms. Our main insight is that, even though one cannot compute the per-period resource budget and target its consumption, it is possible to compute a time-varying sequence of target consumptions which, if consumed at those rates, perform well no matter what the horizon turns out to be. To achieve this, we develop Variable Target Dual Mirror Descent (Algorithm 1), which takes a sequence of target consumptions as input and dynamically updates the prices to hit those targets. One of our primary technical contributions is generalizing the analysis of dual mirror descent to develop a fundamental bound that allows for general target consumption sequences. We leverage this bound to show that there exists a simple time-varying target consumption sequence which can be described in closed form and achieves a near-optimal asymptotic competitive ratio when deployed with Algorithm 1, matching the upper bound up to logarithmic factors.

Optimizing the Target Sequence and Incorporating Predictions. Variable Target Dual Mirror Descent reduces the complex problem of finding an algorithm which maximizes the competitive ratio to the much simpler problem of finding the optimal target consumption sequence. We develop an algorithm to solve the latter efficiently (Algorithm 2), leading to substantial gains over previous algorithms even for small values of (see Figure 1). Importantly, Algorithm 2 does not require one to solve computationally-expensive linear programs (LPs), which can be desirable in time-sensitive applications. We then use the Algorithms-with-Predictions framework (Mitzenmacher and Vassilvitskii, 2020) to study incorporating (potentially inaccurate) predictions about the horizon with the goal of performing well if the prediction comes true, while also ensuring a good competitive ratio no matter what the horizon turns out to be. We show that the problem of computing the optimal target consumption sequence for the goal of optimally incorporating predictions can also be solved efficiently using Algorithm 2. Our algorithm allows the decision maker to account for the level of confidence she has in the predictions, and smoothly interpolate between the known-horizon and uncertainty-window settings.

1.2 Additional Related Work

Online resource allocation is an extremely general framework that captures a wide range of problems, which together have received significant attention in the past. Here, we focus on works that present results which hold at the level of generality of online linear packing or higher, and refer the reader to Mehta et al. (2007) and Balseiro et al. (2021) for a discussion of other special sub-problems like Adwords, network revenue management, repeated bidding in auctions, online assortment optimization etc.

Online linear packing is a special case of online resource allocation in which the reward and consumption functions are linear. It has been studied in the random permutation model, which assumes that the requests arrive in a random order and is slightly more general than the i.i.d. stochastic arrival assumption. Most of the results on online linear packing described here hold for this more general model. Devanur and Hayes (2009) and Feldman et al. (2010) present an algorithm that uses the initial requests to learn the dual variables and then subsequently uses these to make accept/reject decisions. It can be shown to have a regret of . Agrawal et al. (2014) improved this to regret by repeatedly re-learning the dual variables by solving LPs at intervals of geometrically-increasing lengths. Devanur et al. (2011) and Kesselheim et al. (2014) provide algorithms with regret but better dependence of the constants on the number of resources. Li et al. (2020) give a dual-stochastic-gradient-based algorithm which achieves regret without solving computationally-expensive LPs, albeit with a slightly worse dependence on the number of resources. For the special case of network revenue management with finitely many types where the arrival probability of each type and the per-period budget are apriori known to the decision maker, Freund and Banerjee (2019) provided a primal resolving algorithm which attains constant regret when the exact horizon is revealed time periods before the final request. Importantly, if only the total budget is known, then their algorithm needs to know the horizon to compute the per-period budget.

Agrawal and Devanur (2014) study online resource allocation with concave rewards and a convex constraint set. They describe a dual-based algorithm which achieves regret. The work that is most closely related to ours is Balseiro et al. (2020). It studies the fully-general online resource allocation under a variety of assumptions on the request-generation process including stochastic i.i.d. They present a dual mirror descent algorithm and show that it is optimal for a variety of assumptions on the requests. In particular, their algorithm achieves a regret when requests are stochastic. In light of the lower bound of proven by Arlotto and Gurvich (2019) for the multi-secretary problem, which is a special case of online resource allocation, their result is tight in its dependence on . Jiang et al. (2020) study a more general model that allows for time-varying request distributions. They propose a dual gradient descent algorithm which works with target consumptions computed using prior information about future request distributions. When the prior information is close to being accurate (measured using Wasserstein distance), their algorithm attains regret against the hindsight optimal. Their algorithm reduces to that of Balseiro et al. (2020) with the Euclidean regularizer when the request distributions and priors are identical. Our algorithm (Algorithm 1) generalizes their algorithm to allow for arbitrary regularizers. Importantly, their guarantees for dual gradient descent with time-varying target consumptions only hold when the prior is close to being accurate, and not for general target consumption sequences like the ones we develop (Theorem 1), which lie at the heart of our results. Crucially, all of the aforementioned results rely on knowledge of the horizon (total number of requests) , and no longer hold in its absence (see Theorem 2). Moreover, naive attempts to extend them to the unknown horizon setting lead to sub-optimal algorithms (see Section 2.1).

There is also a line of work studying online allocation problems when requests are adversarially chosen. Naturally, the fully-adversarial model subsumes our input model, in which requests are drawn i.i.d. from an unknown distribution and the horizon is uncertain. Therefore, guarantees for adversarial algorithms carry over to our setting. We remark, however, that it is not possible to obtain bounded competitive ratio for the general online allocation problems we study in this paper (see, e.g., Feldman et al. 2009). Notable exceptions are online matching (Karp et al., 1990), the AdWords problem (Mehta et al., 2007), or personalized assortment optimization (Golrezaei et al., 2014), which are linear problems in which rewards are proportional to resource consumption. When rewards are not proportional to resource consumption, there is a stream of literature studying algorithms with parametric competitive ratios. These competitive ratios either depend on the range of rewards (see, e.g., Ball and Queyranne 2009; Ma and Simchi-Levi 2020) or the ratio of budget to resource consumption (see, e.g., Balseiro et al. 2020). Our work leverages the fact that requests are drawn i.i.d. from an unknown distribution to derive stronger competitive ratios that only depend on horizon uncertainty (and that are independent of all other problem parameters). In particular, our competitive ratios are bounded, while the parametric competitive ratios of the aforementioned papers can be made arbitrarily large if an adversary can choose the distribution of requests.

Finally, a few very recent papers warrant attention, all of which assume that the distribution of the horizon is known in advance. Brubach et al. (2019) study a generalization of online bipartite matching which accounts for ranked preferences over the offline vertices under a variety of input models. They show that a constant competitive ratio cannot be attained under stationary stochastic input when the horizon is completely unknown and use it to justify the known-horizon assumption. Our impossibility result (Theorem 2) establishes a parametrized upper bound on the competitive ratio in terms of the uncertainty and implies their result as a special case when . Alijani et al. (2020) study the multi-unit prophet-inequality problem in which the resource is perishable, with each unit of the resource exiting the system independently at some time whose distribution is known to the decision maker. When there is one unit of the resource, their model captures horizon uncertainty in the prophet-inequality problem, which is a special case of online resource allocation. Importantly, when there is more than one unit, our models are incomparable. For the single-unit special case, they prove a parameterized upper bound of on the competitive ratio. In contrast, our upper bound (Theorem 2) holds for the more general regime where the initial resource endowment (number of units of the resource) scales linearly with the horizon and the action space is continuous. This is crucial since the performance guarantees of algorithms for online resource allocation with known-horizon often only hold in this regime (Balseiro et al., 2020; Mehta et al., 2007; Talluri and Van Ryzin, 2004), thereby making the single-unit upper bound inapplicable.

Bai et al. (2022) develop a fluid approximation to the dynamic-programming solution for network revenue management when both the distribution of the request and the horizon are completely known. They show that the asymptotically-tight fluid approximation should attempt to respect the resource constraint for all possible horizon values and not in expectation over the horizon. Aouad and Ma (2022) consider a model for network revenue management in which the distribution of the horizon is known and each type of request follows an adversarial or random-order arrival pattern. They also show that the fluid LP relaxation based on the expected value of the horizon can be arbitrarily bad and develop tighter LP relaxations. We do not assume that the type of requests, the distribution of requests or the distribution of the horizon are known ahead of time, and use the hindsight optimal allocation as the benchmark, making our results incomparable even for the special case of network revenue management.

2 Model

Notation

We use to denote the set of non-negative real numbers and to denote the set of positive real numbers. We use to denote . For a vector and a scalar , denotes the scalar multiplication of by . For vectors and a relation , we write whenever the relation holds component wise: for all .

We consider a general online resource allocation problem with resources, in which requests arrive sequentially. At time , a request arrives, which is composed of a reward function , a resource consumption function and a compact action set . We assume that and for all . This ensures that the decision maker has the option to not spend any resources at each time step. We make no assumptions about the convexity/concavity of either , or .

Let represent the set of all possible requests. We make standard regularity assumptions: there exist constants such that, for every request , we have and for all . Furthermore, we assume that the requests are drawn i.i.d. from some distribution over , both of which are not assumed to be known to the decision maker. The decision maker has a known initial resource endowment (or budget) of , where denotes the initial amount of resource available to the decision maker. We will assume that for all .

Let denote the total number of requests that will arrive (also called the horizon). We will use to denote the per-period resource endowment that is available to the decision maker. In contrast to previous work, we do not assume that (or its distribution) is known to the decision maker. Looking ahead, this uncertainty is what makes our problem much harder than vanilla online resource allocation where the horizon is known, as evidenced by the fact that no algorithm can attain even a positive competitive ratio when nothing is known about the horizon (see Theorem 2), which is a far-cry from the no-regret property exhibited by algorithms for the known-horizon setting.

At each time step , the following sequence of events take place: (i) A request arrives and is observed by the decision maker; (ii) The decision maker selects an action from the action set based on the information seen so far; (iii) The decision maker receives a reward of and the request consumes resources. The goal of the decision maker is to take actions that maximize her total reward while keeping the total consumption of resources below the initial resource endowment. More concretely, an online algorithm (for the decision maker) chooses an action at each time step based on the current request and the history observed so far such that the resource constraints are satisfied almost surely w.r.t. . Our results continue to hold even if the actions are randomized, but we work with deterministic actions for ease of exposition. Since we assume that is not known to the decision maker, the actions of the online algorithm cannot depend on . The total reward of algorithm on a sequence of requests is denoted by .

We measure the performance of an algorithm for the decision maker by comparing it to the hindsight optimal solution computed with access to all the requests and the value of . More concretely, for a horizon and a sequence of requests , the hindsight-optimal reward is defined as the optimal value of the following hindsight optimization problem:

| (1) |

We define the performance ratio of an algorithm for horizon and request distribution as

Throughout this paper, we will assume that the horizon belongs to an uncertainty window which is known to the decision maker. This assumption is necessary because it is impossible to attain non-trivial performance guarantees in the absence of an upper bound on the horizon (see Theorem 2). Moreover, we will assume that there exists a constant such that for all . The assumption that is common in the literature on online resource allocation with bandit feedback (see Slivkins et al. 2019 for a survey). A mild sufficient condition for this assumption to hold is the existence of some mapping from request to actions which achieves positive expected reward: such that .333To see how this, define and set starting from till some resource runs out. Since , resource will last at least time steps, which in combination with implies Since for all , setting yields for all .

Next, we describe the models of horizon uncertainty we consider in this paper.

Uncertainty Window. Here, we assume that the decision maker is not aware of the exact value of and it can lie anywhere in the known uncertainty window . This approach is motivated by the literature on robust optimization, where it is often assumed that the exact value of the parameter is unknown but it is constrained to belong to some known uncertainty set (Ben-Tal and Nemirovski, 2002). Our goal here is to capture settings with large horizon uncertainty where it is difficult to predict the total number of requests with high accuracy. In such settings, it is often easier to generate confidence intervals than precise estimates. For this model of horizon uncertainty, we measure the performance of an algorithm by its competitive ratio , which we define as

We also say that an algorithm is -competitive if it has a competitive ratio of . The competitive ratio of our algorithm degrades at a near-optimal logarithmic rate as grows large, and consequently yields good performance even for conservative estimates of the uncertainty window.

Algorithms with Predictions. We also consider a model of horizon uncertainty, inspired by the Algorithms-with-Predictions framework, which interpolates between the previously studied known-horizon model and the uncertainty-window model described above. This framework assumes that the decision maker has access to a prediction about the horizon but no assumptions are made about the accuracy of this prediction. In particular, the goal is to develop algorithms that perform well when the prediction is accurate (consistency) while maintaining worst-case guarantees (competitiveness). For this setting, our algorithm allows the decision maker to smoothly trade-off consistency and competitiveness depending on her preferences.

2.1 Why do we need a new algorithm?

As discussed earlier, online resource allocation and its special cases have been extensively studied in the literature. Perhaps one of the algorithms from the literature continues to perform well under horizon uncertainty? We show below that previously-studied algorithms can be exponentially worse than our algorithm. Consider an uncertainty window , where . Consider an online algorithm which takes as input the horizon and is optimal (defined precisely later) for stochastic online resource allocation when the horizon is known. Suppose we pick some horizon before the first request arrives and run algorithm with in the hope of getting good performance for all horizons . As we show next, this approach performs much worse than our algorithm even when there is only one resource (), the same request arrives at all time steps, and the decision-maker knows this to be the case.

Let be the initial resource endowment, be the action set for all , and be the deterministic distribution that always serves the request where for a fixed and . Observe that all the requests are the same, the decision-maker knows this fact, and she takes her first action after observing the request. In particular, the decision maker completely knows the deterministic request after the first request arrives and before she takes her first action. Moreover, if she employs an algorithm for the known-horizon setting with horizon as the input and we have , then the algorithm has as much information (about the request and the horizon) available before making its first decision as it would in hindsight. This motivates us to call an algorithm optimal for the known-horizon setting if it takes the same actions as the hindsight optimal on this instance when and it is given horizon as the input. The dual-descent algorithm of Balseiro et al. (2020) (when appropriately initialized), and all of the primal methods based on solving the fluid approximation (e.g., Jasin and Kumar 2012; Agrawal et al. 2014 and Balseiro et al. 2021) satisfy this definition of optimality. Let be such an optimal algorithm.

Consequently, if are the actions of algorithm , then is an optimal solution to the hindsight-optimization problem (see equation (1)). In Lemma 2, we will show that the concavity of implies that for all and for is the unique hindsight optimal solution of , which implies that for all . Now, recall that algorithm does not know the horizon and is non-anticipating. Consequently, it will take the actions no matter what turns out to be. This is because, if , then it does not know that is different from , and if , then it has run out of budget by time step .

The performance ratio of algorithm for is given by

and for is given by

Finally, observe that:

-

•

If , then .

-

•

If , then .

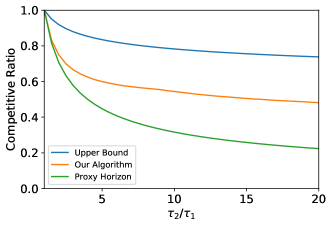

Therefore, we get that the competitive ratio of algorithm is bounded above by for all values of . In stark contrast, if is large and , we will show that our online algorithm achieves a competitive ratio greater than , which is exponentially better than algorithm . Even for small values of , our algorithm significantly outperforms previous algorithms (see Figure 1).

We have shown that a proxy horizon does not allow us to use algorithms which are optimal for the known-horizon setting to obtain good performance in the face of horizon uncertainty. Perhaps one can use the Doubling Trick instead? The Doubling Trick involves running an algorithm designed for the known-horizon setting repeatedly on time-intervals of increasing lengths. More precisely, given an optimal (or low-regret) algorithm for the known horizon setting, run it separately on the intervals for some . Unfortunately, as we alluded to in the Introduction, the Doubling Trick does not work for online resource allocation. This is because, unlike online convex optimization (Hazan et al., 2016; Shalev-Shwartz et al., 2012) where the problem decouples and the regret from the different intervals is simply added together to get total regret, the online resource allocation problem has global resource constraints and does not decouple.

In particular, if we were to run an algorithm with low-regret in the known-horizon setting on the interval , it will attempt to deplete all of the available resources by time (because unused resources have no value to after ), which in turn implies that we will not have sufficient resource capacity to even run algorithm on latter intervals . The crux of the problem is that the Doubling Trick does not take the resources capacities into account: since we only have a finite amount of resources, one cannot repeatedly run algorithm because it will consume the entire resource capacity on every run (if possible). Additionally, note that the benchmark in online resource allocation is the optimal solution in hindsight considering all requests till time , which is very different from the sum of the benchmark optimal solutions in the intervals . One can potentially come up with sophisticated versions of the Doubling Trick that allocate the resource endowment between the intervals in non-trivial ways. But the aforementioned lack of decomposability of the benchmark across intervals means that analyzing such heuristics would be far from straightforward. In fact, one of our primary contributions is a general performance guarantee for dual mirror descent with arbitrary allocation of the resource endowment across time steps (Theorem 1), which allows one to analyze such heuristics. Finally, in online convex optimization, the Doubling Trick allows one to convert an algorithm for the known-horizon setting into one for the unknown-horizon setting while maintaining the same asymptotic competitive ratio of 1. However, as we will show in Theorem 2, it is impossible to achieve the same competitive ratio in the known-horizon and unknown-horizon settings for the online resource allocation problem. Thus, the simple Doubling Trick cannot be applied to online resource allocation, necessitating the need for novel techniques beyond the ones developed for online convex optimization.

3 The Algorithm

In this section, we describe our dual-mirror-descent-based master algorithm. As the name suggests, this algorithm maintains and updates dual variables, using them to compute the action at time . Moreover, the algorithm is parameterized by a target consumption sequence.

Definition 1.

We call a sequence a target consumption sequence if for all , and .

Here, denotes the target amount of resources that one wants to consume in the -th time period. ensures that the budget never runs out if one is able to hit these target consumptions. Given a target consumption sequence , we use to denote the largest target consumption of any resource at any time step.

We will be showing performance guarantees for our algorithms in terms of the target consumption sequence, and then provide algorithms for computing the optimal target sequence in later sections.

3.1 The Dual Problem

The Lagrangian dual problem to the hindsight optimization problem (1) is obtained by moving the resource constraints to the objective using multipliers . Intuitively, the dual variable acts as the price of resource and accounts for the opportunity cost of consuming resource . This allows us to define the objective function of the dual optimization problem:

where the second equation follows because the objective is separable and , and the last by defining the opportunity-cost-adjusted reward to be . The dual problem is simply . Importantly, we get weak duality: for all dual solutions (we provide a proof in Proposition 5 of Appendix A).

Recall that, in our definition of competitive ratio (4), we are interested in the expectation of when . Weak duality allows us to bound this quantity from above as

| (2) |

This motivates us to define the following single-period dual function with target consumption as . The following lemma notes some important properties of the single-period dual objective.

Lemma 1.

is convex in for every . Moreover, for every and , the following properties hold:

-

(a)

Separability:

-

(b)

Sub-homogeneity: For , .

-

(c)

Monotonicity: If , then .

3.2 Variable Target Dual Mirror Descent

| (3) | |||

Algorithm 1 is a highly-flexible stochastic dual descent algorithm that allows the decision maker to specify the target consumption sequence , in addition to the initial dual variable , the reference function and the step-size needed to specify the mirror-descent procedure. This flexibility allows us to seamlessly analyze a variety of different algorithms using the same framework. As is standard in the literature on mirror descent (Shalev-Shwartz et al., 2012; Hazan et al., 2016), we require the reference function to be either differentiable or essentially smooth (Bauschke et al., 2001), and be -strongly convex in the norm. Moreover, Algorithm 1 is efficient when an optimal solution for the per-period optimization problem in equation (3) can be computed efficiently. This is possible for many applications, see Balseiro et al. (2020) for details.

The algorithm maintains a dual variable at each time step, which acts as the price of the resources and accounts for the opportunity cost of spending them at time . Then, for a request at time , it chooses the action that maximizes the opportunity-cost-adjusted reward . As our goal here is to build intuition, we ignore the minor difference between and which ensures that we never overspend resources. The dual variable is updated using mirror descent with reference function , step-size , and using as a subgradient. Intuitively, mirror descent seeks to make the subgradients as small as possible, which in our settings translates to making the expected resource consumption in period as close as possible to the target consumption . As a result, the target consumption sequence can be interpreted as the ideal expected consumption per period, and the algorithm seeks to track these rates of consumption.

We conclude by discussing some common choices for the reference function. If the reference function is the squared-Euclidean norm, i.e., , then the update rule is and the algorithm implements subgradient descent. If the reference function is the negative entropy, i.e., , then the update rule is and the algorithm implements multiplicative weights.

3.3 Performance Guarantees

In this section, we provide worst-case performance guarantees of our algorithm for arbitrary target consumption sequences. Before stating our result, we provide further intuition about our algorithm. Consider the single-period dual function with target consumption , given by

Then, by Danskin’s Theorem, its subgradient is given by where is an optimal decision when the request is and the dual variable is . Therefore, is a random unbiased sample of the subgradient of . Now, if we wanted to minimize the dual objective for some known , we can run mirror descent on the function by setting for all . This is exactly the approach taken by Balseiro et al. (2020). Unfortunately, this method does not extend to our setting because the horizon is unknown.

Observe that, since mirror descent guarantees vanishing regret even against adversarially generated losses, it continues to give vanishing regret in the dual space even when the single-period duals vary with time due to the changing target consumptions. However, when for some , it is no longer the case that provides an upper bound on the hindsight optimization problem. The crux of the following result involves overcoming this difficulty and comparing the time-varying single-period duals with the hindsight optimal solution for all simultaneously, leading to a performance guarantee for Algorithm 1.

Theorem 1.

Consider Algorithm 1 with initial dual solution , initial resource endowment , a target consumption sequence , reference function , and step-size . For any , if we set

| (4) |

then it holds that

| (5) |

where , , . Here is the -th unit vector and .

The proof proceeds in multiple steps. First, we write the rewards collected by Algorithm 1 as a sum of per-period duals and complementary-slackness terms. Next, we use weak duality to upper bound the expected value of the hindsight optimal reward in terms of the expected hindsight dual. These two steps are common to all primal-dual analyses, but past techniques offer no guidance beyond this point. The core difficulty is that the expected hindsight dual is equal to the sum of per-period duals with target consumption , whereas the lower bound on the performance of our algorithm is in terms of per-period duals with target consumptions . Importantly, this difficulty does not arise in past works because the target consumptions , which makes the two terms directly comparable. Our main technical insight lies in using Lemma 1 to manipulate the per-period duals and then carefully choosing the right dual solution in order to compare the two terms. Moreover, one also needs to take into account the fact that the resources may run out before the horizon is reached, and Algorithm 1 does not accumulate rewards after this point. Since the point at which the budget runs out depends on the target consumption sequence, we also establish a bound on the loss from depleting the resources too early which applies to variable target sequences. We believe that Algorithm 1 and our proof techniques distill the core tradeoffs of the problem and can be used more broadly. The full proof is in Appendix A.

Theorem 1 is the bedrock of our positive results. It allows us to drastically simplify the design of algorithms: instead of searching for the optimal algorithm, we can focus on the much simpler problem of selecting the optimal target consumption sequence. The following result provides a key step in this direction by showing that is the asymptotic performance ratio of Algorithm 1 with target sequence .

Proposition 1.

Let be Algorithm 1 with initial dual solution , initial resource endowment , a target consumption sequence , reference function , and step-size . Set and . Then, with step size , the following statement holds for all :

where

Remark 1.

To convert the guarantee in Proposition 1 to an asymptotic guarantee, one needs to consider the regime where the initial resources scale with the horizon as , which ensures that and the constants and remain bounded. In which case, if we let grow large while ensuring , we can make arbitrarily small. In particular, . The assumption that the initial resources scales linearly with the number of requests is pervasive in the literature and well-motivated in applications such as internet advertising (Mehta, 2013) and revenue management (Talluri and Van Ryzin, 2004). Moreover, an error of is unavoidable even for the case when the horizon is known, i.e., (see Arlotto and Gurvich 2019).

Remark 2.

In applications where it might be difficult to estimate the constants and , one can use the step size to get

which yields similar asymptotic rates.

Having characterized the performance of Algorithm 1 in terms of the target sequence, we next optimize it for the models of horizon uncertainty discussed in Section 2. Although we will only discuss two models of uncertainty, we would like to note that Theorem 1 and Proposition 1 are very general tools that can be applied more broadly. In particular, observe that

is a concave function of for all . This is because each term in the sum is a minimum of a finite collection of linear functions of . Consequently, any performance measure of Algorithm 1 which is a concave non-decreasing function of the performance ratios is a concave function of the target sequence in light of Proposition 1. We pause to emphasize this important transition we have made in this section: we reduced the extremely complex problem of designing an algorithm for online resource allocation under horizon uncertainty to a concave optimization problem with the power to handle a variety of constraints and objectives. In the next section, we show that this reduction is without much loss in the uncertainty-window setting—picking the optimal target consumption sequence leads to a near-optimal competitive ratio in the uncertainty-window model.

4 Uncertainty Window

Motivated by robust optimization, in this section, we take the uncertainty-set approach to modeling horizon uncertainty. In particular, we assume that the decision maker is not aware of the exact value of but knows it can lie anywhere in the known uncertainty window . Recall that we measure the performance of an algorithm in this model by its competitive ratio , which is defined as

4.1 Upper Bound on Competitive Ratio

We begin by showing that no online algorithm can attain a competitive ratio of whenever and, moreover, when is large the competitive ratio degrades at a rate of . In other words, the competitive ratio of every algorithm degrades to 0 as grows large. In fact, we prove that this upper bound on the best-possible competitive ratio holds even when (i) there is only 1 resource, (ii) the decision maker receives the same request at each time step, (iii) this request is known to the decision maker ahead of time, and (iv) the request has a smooth concave reward function and linear resource consumption.

For the purposes of this subsection, set the number of resources to . Consider an arbitrary initial resource endowment . For every , define the singleton request space , where , and , for all . Note that is concave for all . Let be the canonical distribution on that serves the request with probability one. Since all requests are identical, we abuse notation and use (similarly ) to denote the hindsight-optimal reward (total reward of algorithm ) when , i.e., for all .

Before stating the upper bound, we would like to note that randomization only makes the performance of any online algorithm worse. To see this consider any non-deterministic online algorithm and let denote the random variable which captures the action taken by at time . Define to be the online algorithm which takes the action at time . Then, due to the strict concavity of , we have , and from the linearity of expectation, we have . Therefore, the deterministic algorithm attains strictly greater reward. Consequently, we will focus only on deterministic online algorithms for the remainder of this subsection. We are now ready to state the main result of this section.

Theorem 2.

For all and , every online algorithm satisfies

In particular, when and , every online algorithm satisfies

The above bounds hold even for online algorithms that have prior knowledge of before time .

Remark 3.

Note that the upper bound on the competitive ratio established in Theorem 2 degrades to zero as grows large. In particular, a positive competitive ratio cannot be obtained if no upper-bound on the horizon is known, thereby necessitating the need for a known uncertainty window.

Figure 1 plots the value of the upper bound on the competitive ratio as a function of for .

We now discuss the main ideas behind the proof of Theorem 2. It suffices to prove the stronger statement in the theorem that holds for online algorithms with prior knowledge of before time . Consequently, we assume that online algorithms have this prior knowledge in the remainder of this section. Any algorithm without this knowledge can only do worse. We begin by utilizing the concavity of to evaluate the optimal reward, which we note in the following lemma.

Lemma 2.

For and , we have . Moreover, is the unique hindsight optimal solution.

Because the reward function is concave, it is optimal to spread resources uniformly over time and the optimal action with the benefit of hindsight is . Next, we provide an alternative characterization of the competitive ratio that is more tractable.

Lemma 3.

For and , we have

where and the is taken over all online algorithms.

We present a proof sketch of Lemma 3 here. The main step in the proof involves showing that, for a given competitive ratio , the minimum amount of resources that any online algorithm needs to be spend in order to satisfy is given by

This is because is concave for all and the resource consumption function is linear, which together imply that the marginal bang-per-buck (amount of reward per marginal unit of resource spent) decreases with . As a consequence, an online algorithm that does not have any knowledge of (other than ) and needs to satisfy for all would spend the minimum amount of resources in doing so if (i) it attains a reward of by evenly spending resources in the first steps, and (ii) it spends just enough resources to attain a reward of at each time step . Proving (ii) requires showing that decreases with an increase in , which follows from Lemma 2. In particular, this ensures that obtaining all of at time is cheaper than obtaining some of that reward at an earlier time . However, the proof requires a sophisticated water-filling argument to show that the aforementioned greedy strategy of minimizing the amount of resources at each time step leads to globally-minimal spending. Finally, combining Lemma 3 and Lemma 2 yields

for . The above equation specifies an upper bound on , which upon simplification leads to Theorem 2.

We conclude by noting that the upper bound of Theorem 2 can be extended to the popular setting of online resource allocation with random linear rewards and consumptions (see Appendix B.4 for details). Moreover, the upper bound of Theorem 2 holds even when the horizon is drawn from a distribution supported on and this distribution is known to the decision maker. A proof based on strong duality can be found in Appendix B.5.

4.2 Optimizing the Target Sequence

Having shown that no algorithm can attain a competitive ratio better than , we now show that Algorithm 1 with an appropriately chosen target consumption sequence can achieve a competitive ratio of for sufficiently large and . In light of Proposition 1, we can optimize the competitive ratio of Algorithm 1 by finding the target consumption sequence which maximizes , i.e., we need to solve the following maximin problem:

The following proposition restates the above maximin problem as an LP.

Proposition 2.

For budget and uncertainty window , we have

| s.t. | ||||

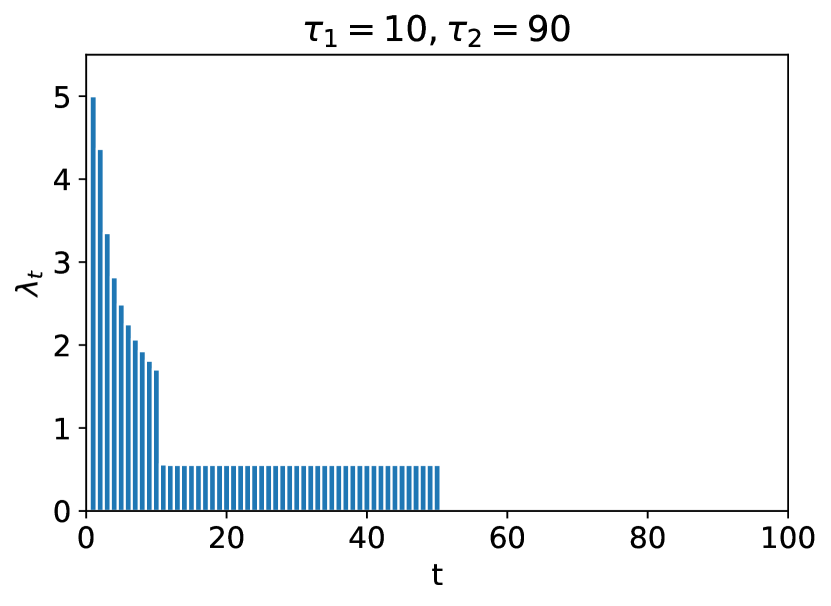

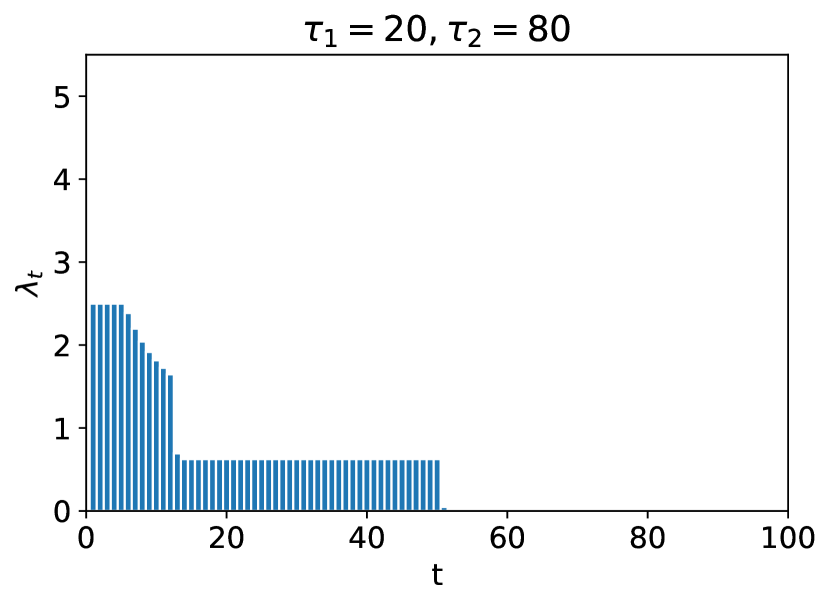

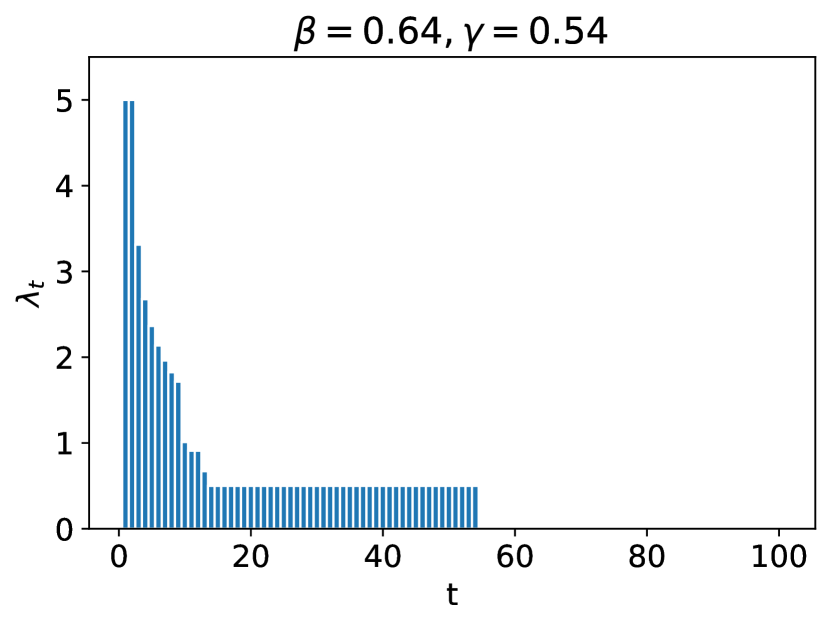

Proposition 2 states that we can efficiently compute the optimal target consumption sequence by solving an LP. Figure 2 plots the optimal target sequences from Proposition 2 for different uncertainty windows. The optimal target consumption sequences are decreasing as the algorithm consumes resources more aggressively early on to prevent having too many leftover resources if the horizon ends being short. Moreover, as the uncertainty window becomes more narrow, the consumption sequence becomes less variable.

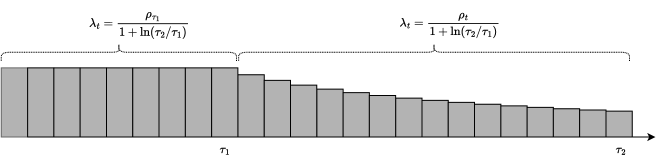

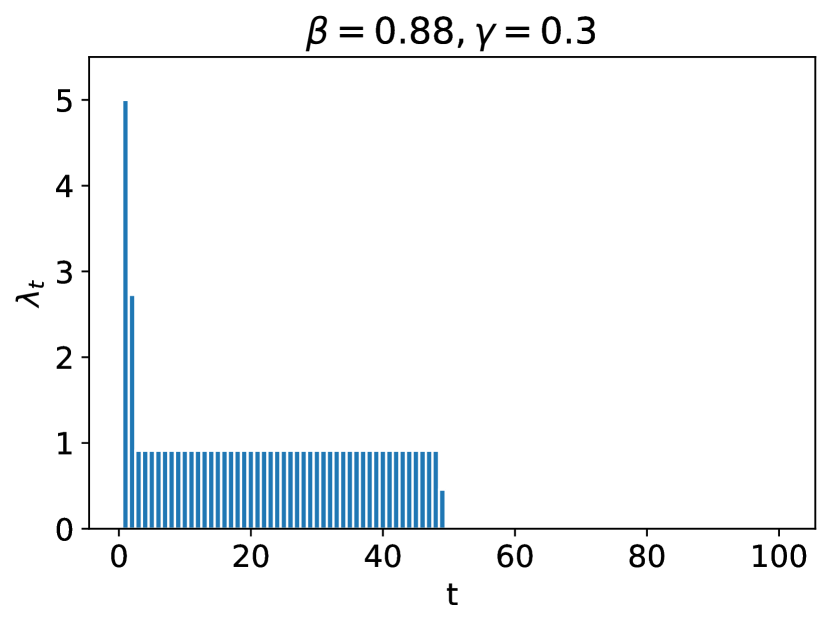

To see that Algorithm 1 with the optimal target consumption sequence from the above LP has an asymptotic competitive ratio of , consider the following target consumption sequence (depicted in Figure 3):

| (6) |

It is easy to see that it satisfies the budget constraint:

Moreover, since for all and , we get

where the inequality follows from the fact that for all and the definition of as given in (6).

Since from (6) is just one possible choice of the target consumption sequence, we have

Therefore, we get that Algorithm 1 in combination with the target consumption sequence returned by the LP in Proposition 2 achieves a degradation of in the competitive ratio as a function of the multiplicative uncertainty , which is optimal up to constants and a factor. In fact, as Figure 4 shows, the target consumption sequence from the LP performs much better than , even for small values of . In Section 6, we will give a faster algorithm which leverages the structure of the problem to optimize the target sequence and does not require solving an LP.

We conclude with a discussion on the structural similarity of the results of this subsection with those of Besbes and Sauré (2014), who studied the dynamic pricing problem (special case of online resource allocation) under demand shifts. They worked under the assumption that the request distribution is perfectly known, and showed that the optimal dynamic programming solution has a non-decreasing resource consumption sequence when the horizon is uncertain. The target consumption sequences described in this section are also non-increasing, leading to a similar structural insight for the more general online resource allocation problem with unknown request distribution.

5 Incorporating Predictions about the Horizon

In the previous section, we did not assume that we had any information about the horizon other than the fact that it belonged to the uncertainty window . This may be too pessimistic in settings where the environment is well behaved and machine learning algorithms can be deployed to make predictions about the horizon. In this section, we show that our Variable Target Dual Descent algorithm allows us to easily incorporate predictions by optimizing the target sequences. We formulate an LP to optimize the target sequence which allows the decision-maker to smoothly interpolate between the uncertainty-window setting and the known-horizon setting, thereby catering to different levels of confidence in the prediction.

First, we define the performance metrics we will use to measure the performance of an online algorithm capable of incorporating predictions. These metrics are pervasive in the Algorithms-with-Predictions literature (see Mitzenmacher and Vassilvitskii 2020 for an excellent survey) and are aimed at capturing the performance of the algorithm both when the prediction is accurate and in the worst case when the instance bears no resemblance to the prediction. To this end, in addition to the competitive-ratio metric defined in Section 2, which captures the worst-case performance, we introduce the notion of consistency to capture the performance of the algorithm when the prediction is accurate. Let denote the predicted value of the horizon and let denote algorithm when provided with the prediction . We say that an algorithm is -consistent on prediction and -competitive if it satisfies

and

for all request distributions . In other words, an algorithm which is -consistent on prediction and -competitive is guaranteed to get a fraction of the hindsight optimal reward in expectation if the prediction comes true and it is guaranteed to attain a fraction of the hindsight optimal reward for every horizon (whether or not it conforms to the prediction). Consistency and competitiveness are conflicting objectives and different decision makers might have different preferences over them. In particular, increasing consistency usually leads to lower competitiveness. Consequently, our goal is to find an algorithm which can trade off the two quantities, allowing us to interpolate between the known-horizon and the uncertainty-window settings.

Once again, the versatility of Algorithm 1 and its ability to reduce the problem of finding the optimal algorithm to that of finding the optimal target consumption sequence comes to the fore. In particular, Proposition 1 implies that Algorithm 1 with target consumption sequence for prediction is -consistent for prediction and -competitive with

Therefore, given a prediction and a required level of competitiveness , we need to solve the following optimization problem in order to maximize consistency while achieving -competitiveness:

As in the uncertainty-window setting, we can rewrite this as an LP.

Proposition 3.

For budget , uncertainty window , predicted horizon and required level of competitiveness , we have

| s.t. | s.t. | ||||||

Remark 4.

Our framework can also accommodate distributional predictions about the horizon, leading to a similar LP with the only difference being an additional expectation over the predicted horizon in the objective.

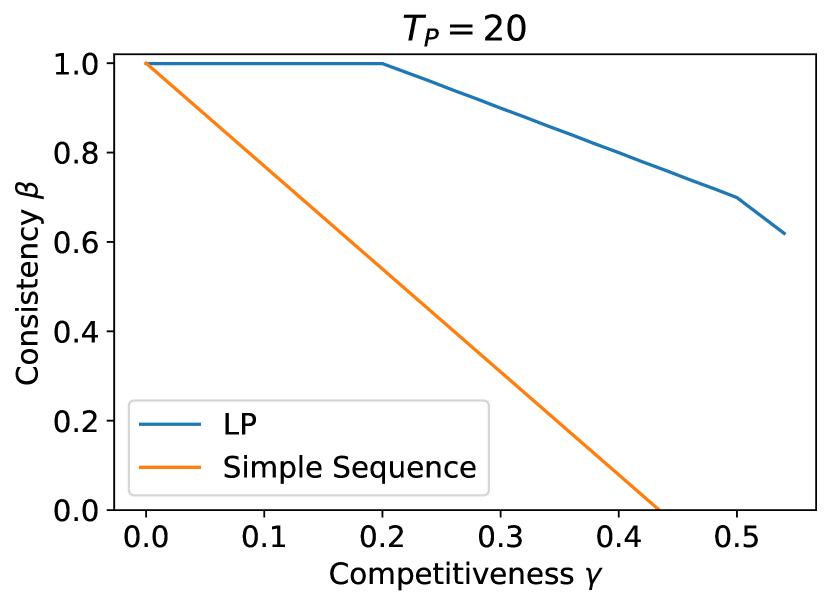

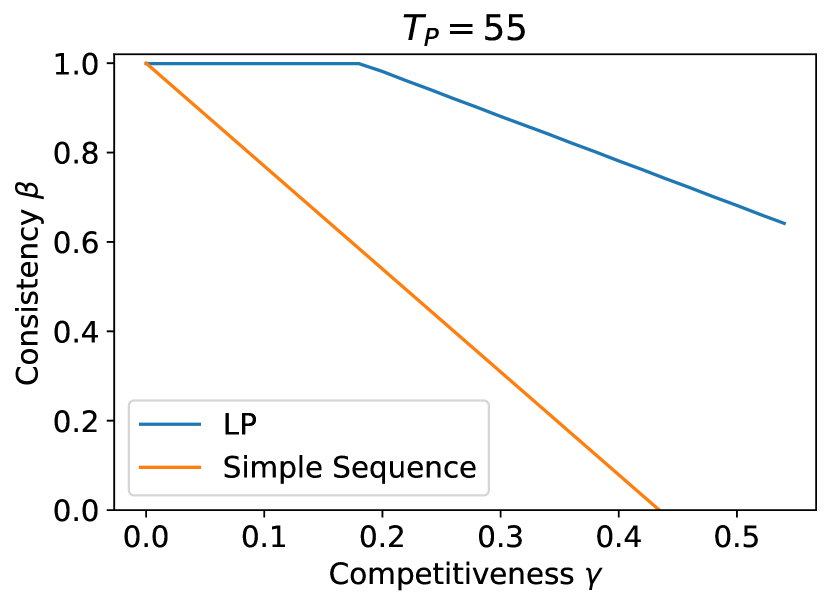

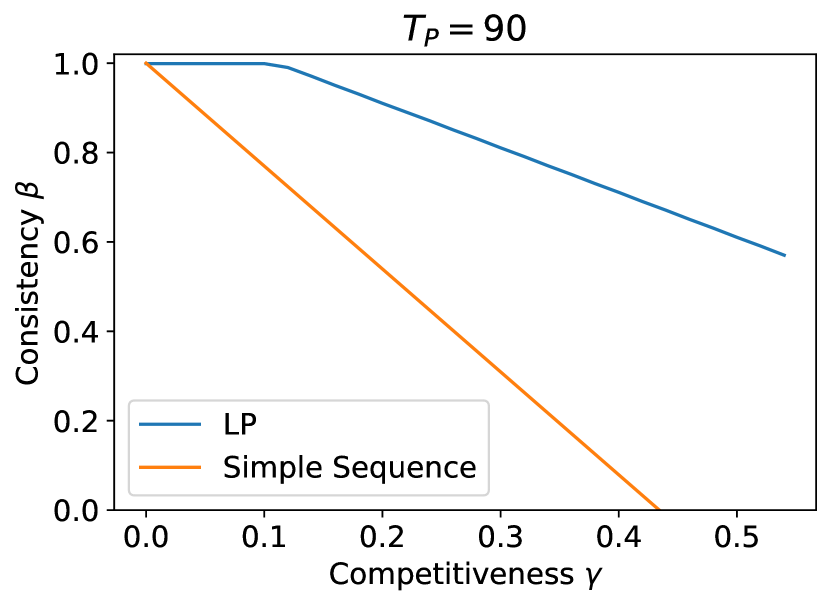

Observe that, when and the decision maker does not desire robustness, the LP in Proposition 3 would output with for and otherwise. Algorithm 1 with this target consumption sequence is exactly the algorithm of Balseiro et al. (2020), which yields a consistency of . On the other extreme is being equal to the output of the LP in Proposition 2, in which case the LP in Proposition 3 would output a target sequence which maximizes the competitive ratio . For values of in between the two extremes, the LP in Proposition 3 outputs a target consumption sequence which attempts to balance the two objectives, as can be seen in Figure 5. This allows the decision maker to interpolate between the known-horizon and the uncertainty-window settings (see Figure 6).

Now, suppose the required level of competitiveness is such that for some . Then, for predicted horizon , consider the following simple target consumption sequence

| (7) |

The target sequence is simply a sum of two target sequences: (i) The first part is an -scaled-down version of the simple target sequence from (6), which ensures competitiveness; (ii) The second is a -scaled-down version of the target sequence which spends evenly and is optimal when the prediction were true. , as defined in (7), is a feasible solution to the optimization of Proposition 3, which allows us to establish the following closed-form guarantee.

Proposition 4.

Note that the target sequence in (7) is just one particular target sequence and the LP in Proposition 3 computes the optimal target sequence, and consequently the latter always performs better. This domination in performance is depicted in Figure 6, where the consistency-competitiveness curve the simple sequence (in orange) lies entirely below the curve from Proposition 3 (blue curve).

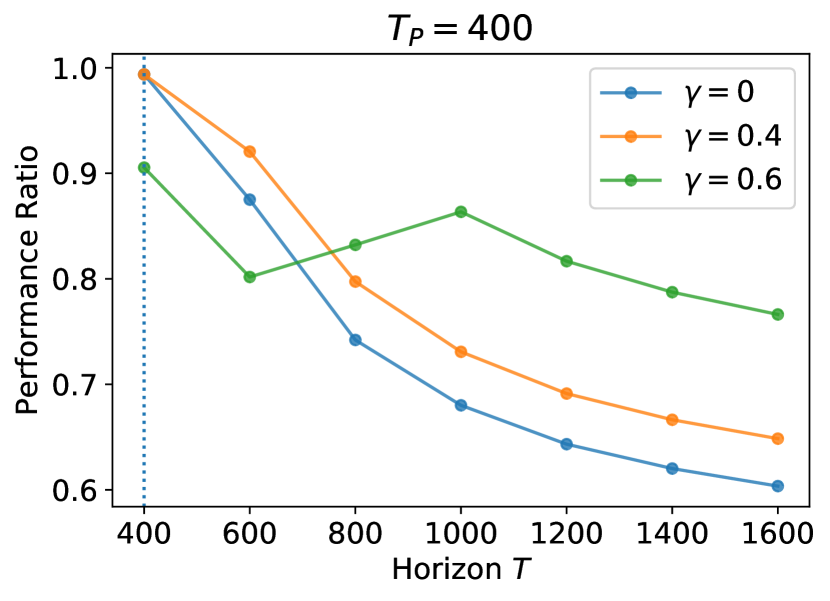

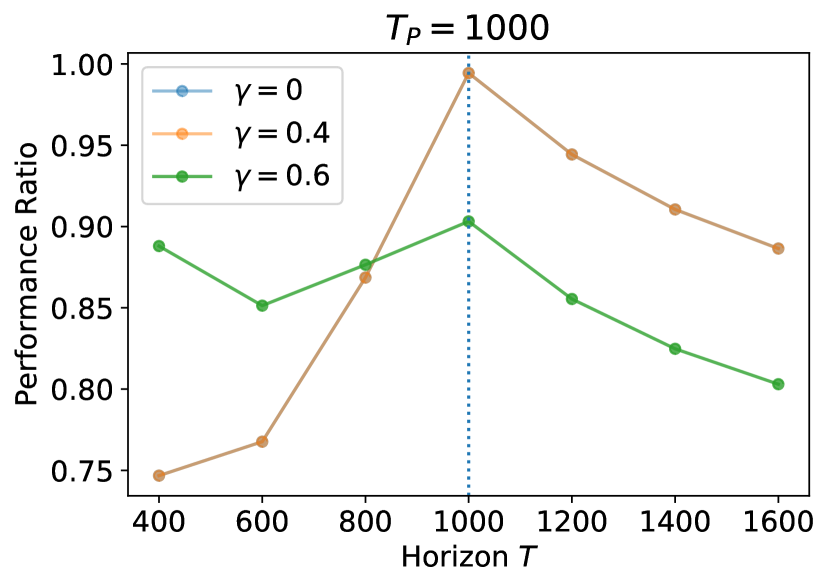

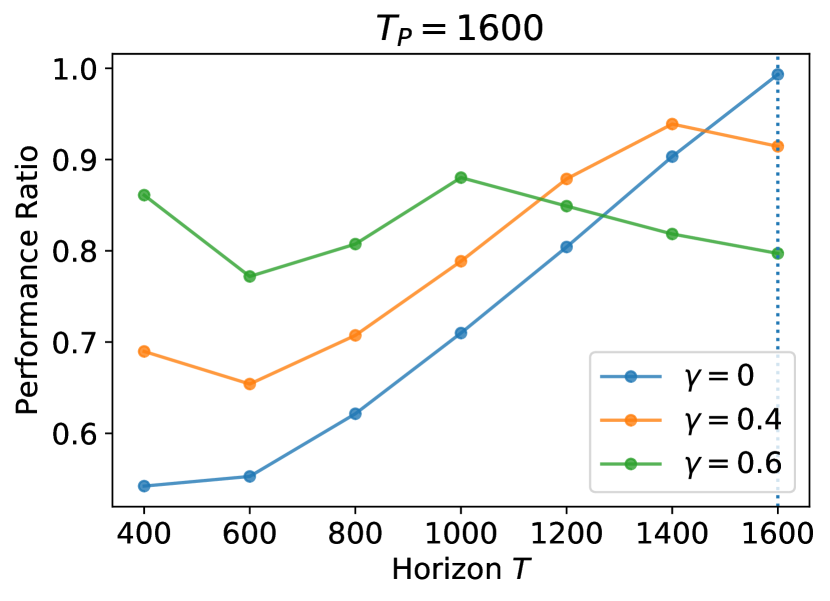

Numerical Experiment. We evaluated our algorithm (Algorithm 1 with target sequence from Proposition 3) on the multi-secretary problem with uniform rewards and the results are summarized in Figure 7. In this experiment, the request distribution captures the uniform multi-secretary problem: each request has reward for , consumption and an accept/reject action space . Moreover, , , , , and . As expected, smaller values of lead to better performance when the true horizon is close to the prediction , but this comes at the expense of lower worst-case reward (minimum competitive ratio over all possible values of the horizon ). Recall that represents the algorithm of Balseiro et al. (2020) with horizon . Our experiment demonstrates its fragility to traffic spikes: if the number of requests turns out to be 3 times the predicted traffic of , the algorithm of Balseiro et al. (2020) achieves a drastically lower performance ratio than our algorithm with .

6 Bypassing the LP: A Faster Algorithm

Even though the LPs of Proposition 2 and Proposition 3 compute the optimal target consumption sequence in polynomial time, they do not exploit the structure of the problem and are not desirable in large-scale domains like internet advertising where speed is of the essence. To remedy this, we next develop a faster algorithm to compute the optimal target consumption sequence; this algorithm more directly exploits the structure of the problem. The algorithm (Algorithm 2) will rely on the following observation about :

| (8) |

where the last equality follows from multiplying and diving by . Moreover, note that the above inequality is tight when for all

Therefore, any target sequence which is -consistent for prediction , i.e., , and -competitive, i.e. , satisfies the following inequalities for all :

Algorithm 2 minimizes while maintaining the above property. And as a consequence, we can show that consistency on and competitiveness are attainable if and only if Algorithm 2 returns TRUE. Given this property, it is a straightforward exercise to use binary search in conjunction with Algorithm 2 to compute the optimal solution to the LPs in Proposition 2 and Proposition 3 up to arbitrary precision (For completeness, we provide details in Appendix E).

| (9) |

Theorem 3.

Given budget , uncertainty window , prediction , required level of consistency and required level of competitiveness as input, let be the sequence computed by Algorithm 2. Then,

-

1.

and

-

2.

if and only if there exists a target consumption sequence (with ) which satisfies and

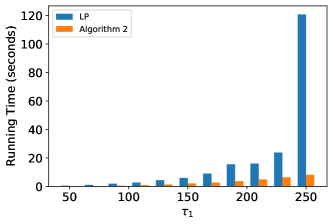

Observe that there can be at most updates of the target sequence (as given in (9)) during the run of Algorithm 2. One can maintain and iteratively update after the completion of each iteration of the inner and outer For loops to perform the update in constant time. Therefore, the runtime complexity of Algorithm 2 is , which is faster than any known general-purpose LP solver applied to the LP in Proposition 2 or Proposition 3. We also empirically observed this difference in running times between the LP of Proposition 2 and Algorithm 2 (see Figure 8).

7 Conclusion

We develop and analyze a generalized version of dual descent which can incorporate variable target consumption sequences (Algorithm 1), thereby reducing the complicated problem of finding an algorithm for online resource allocation under horizon uncertainty to the much simpler (and convex) problem of optimizing the target sequence. We then demonstrate the power of this reduction by showing that, with the optimal target sequence, Algorithm 1 achieves a near-optimal competitive ratio when only upper and lower bounds on the horizon are known. We also provide a way to smoothly interpolate between the previously-studied known-horizon setting and the uncertainty-window setting through the Algorithms-with-Predictions framework, thereby providing a robust approach to online allocation which allows the decision-maker to tailor the degree to robustness to their requirements. Our algorithms have the added advantage of simplicity and speed because they do not require the decision-maker to solve any large linear programs.

We leave open the problem of closing the gap between our lower and upper bounds on the competitive ratio by accounting for the discrepancy. Although this gap is not large asymptotically, closing it will likely result in a deeper understanding of the problem. It would also be interesting to explore whether algorithms which operate in the primal space can similarly benefit from employing a variable target consumption sequence. Finally, when both the distribution of requests and the distribution of the horizon are known in advance, it is worth studying if it is possible to achieve a constant/logarithmic regret against an appropriately defined benchmark (see for example Bumpensanti and Wang 2020; Vera and Banerjee 2019 for similar results when the horizon is known).

References

- Agrawal and Devanur (2014) Shipra Agrawal and Nikhil R Devanur. Fast algorithms for online stochastic convex programming. In Proceedings of the twenty-sixth annual ACM-SIAM symposium on Discrete algorithms, pages 1405–1424. SIAM, 2014.

- Agrawal et al. (2014) Shipra Agrawal, Zizhuo Wang, and Yinyu Ye. A dynamic near-optimal algorithm for online linear programming. Operations Research, 62(4):876–890, 2014.

- Alijani et al. (2020) Reza Alijani, Siddhartha Banerjee, Sreenivas Gollapudi, Kamesh Munagala, and Kangning Wang. Predict and match: Prophet inequalities with uncertain supply. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 4(1):1–23, 2020.

- Aouad and Ma (2022) Ali Aouad and Will Ma. A nonparametric framework for online stochastic matching with correlated arrivals. arXiv preprint arXiv:2208.02229, 2022.

- Arlotto and Gurvich (2019) Alessandro Arlotto and Itai Gurvich. Uniformly bounded regret in the multisecretary problem. Stochastic Systems, 9(3):231–260, 2019.

- Bai et al. (2022) Yicheng Bai, Omar El Housni, Billy Jin, Paat Rusmevichientong, Huseyin Topaloglu, and David Williamson. Fluid approximations for revenue management under high-variance demand: Good and bad formulations. Available at SSRN, 2022.

- Ball and Queyranne (2009) Michael O Ball and Maurice Queyranne. Toward robust revenue management: Competitive analysis of online booking. Operations Research, 57(4):950–963, 2009.

- Balseiro et al. (2020) Santiago Balseiro, Haihao Lu, and Vahab Mirrokni. The best of many worlds: Dual mirror descent for online allocation problems. arXiv preprint arXiv:2011.10124, 2020.

- Balseiro et al. (2021) Santiago Balseiro, Omar Besbes, and Dana Pizarro. Survey of dynamic resource constrained reward collection problems: Unified model and analysis. Available at SSRN 3963265, 2021.

- Balseiro and Gur (2019) Santiago R Balseiro and Yonatan Gur. Learning in repeated auctions with budgets: Regret minimization and equilibrium. Management Science, 65(9):3952–3968, 2019.

- Bauschke et al. (2001) Heinz H Bauschke, Jonathan M Borwein, and Patrick L Combettes. Essential smoothness, essential strict convexity, and legendre functions in banach spaces. Communications in Contemporary Mathematics, 3(04):615–647, 2001.

- Ben-Tal and Nemirovski (2002) Aharon Ben-Tal and Arkadi Nemirovski. Robust optimization–methodology and applications. Mathematical programming, 92(3):453–480, 2002.

- Bertsekas et al. (1998) Dimitri P Bertsekas, WW Hager, and OL Mangasarian. Nonlinear programming. Athena Scientific Belmont, MA, 1998.

- Besbes and Sauré (2014) Omar Besbes and Denis Sauré. Dynamic pricing strategies in the presence of demand shifts. Manufacturing & Service Operations Management, 16(4):513–528, 2014.

- Brubach et al. (2019) Brian Brubach, Nathaniel Grammel, Will Ma, and Aravind Srinivasan. Online matching frameworks under stochastic rewards, product ranking, and unknown patience. arXiv preprint arXiv:1907.03963, 2019.

- Bumpensanti and Wang (2020) Pornpawee Bumpensanti and He Wang. A re-solving heuristic with uniformly bounded loss for network revenue management. Management Science, 66(7):2993–3009, 2020.

- Devanur and Hayes (2009) Nikhil R Devanur and Thomas P Hayes. The adwords problem: online keyword matching with budgeted bidders under random permutations. In Proceedings of the 10th ACM conference on Electronic commerce, pages 71–78, 2009.

- Devanur et al. (2011) Nikhil R Devanur, Kamal Jain, Balasubramanian Sivan, and Christopher A Wilkens. Near optimal online algorithms and fast approximation algorithms for resource allocation problems. In Proceedings of the 12th ACM conference on Electronic commerce, pages 29–38, 2011.

- Esfandiari et al. (2015) Hossein Esfandiari, Nitish Korula, and Vahab Mirrokni. Online allocation with traffic spikes: Mixing adversarial and stochastic models. In Proceedings of the Sixteenth ACM Conference on Economics and Computation, pages 169–186, 2015.

- Feldman et al. (2009) Jon Feldman, Nitish Korula, Vahab Mirrokni, Shanmugavelayutham Muthukrishnan, and Martin Pál. Online ad assignment with free disposal. In International workshop on internet and network economics, pages 374–385. Springer, 2009.

- Feldman et al. (2010) Jon Feldman, Monika Henzinger, Nitish Korula, Vahab S Mirrokni, and Cliff Stein. Online stochastic packing applied to display ad allocation. In European Symposium on Algorithms, pages 182–194. Springer, 2010.

- Freund and Banerjee (2019) Daniel Freund and Siddhartha Banerjee. Good prophets know when the end is near. Available at SSRN 3479189, 2019.

- Golrezaei et al. (2014) Negin Golrezaei, Hamid Nazerzadeh, and Paat Rusmevichientong. Real-time optimization of personalized assortments. Management Science, 60(6):1532–1551, 2014.

- Gupta and Molinaro (2016) Anupam Gupta and Marco Molinaro. How the experts algorithm can help solve lps online. Mathematics of Operations Research, 41(4):1404–1431, 2016.

- Hazan et al. (2016) Elad Hazan et al. Introduction to online convex optimization. Foundations and Trends® in Optimization, 2(3-4):157–325, 2016.

- Jasin and Kumar (2012) Stefanus Jasin and Sunil Kumar. A re-solving heuristic with bounded revenue loss for network revenue management with customer choice. Mathematics of Operations Research, 37(2):313–345, 2012.

- Jiang et al. (2020) Jiashuo Jiang, Xiaocheng Li, and Jiawei Zhang. Online stochastic optimization with wasserstein based non-stationarity. arXiv preprint arXiv:2012.06961, 2020.

- Karp et al. (1990) Richard M Karp, Umesh V Vazirani, and Vijay V Vazirani. An optimal algorithm for on-line bipartite matching. In Proceedings of the twenty-second annual ACM symposium on Theory of computing, pages 352–358, 1990.

- Kesselheim et al. (2014) Thomas Kesselheim, Andreas Tönnis, Klaus Radke, and Berthold Vöcking. Primal beats dual on online packing lps in the random-order model. In Proceedings of the forty-sixth annual ACM symposium on Theory of computing, pages 303–312, 2014.

- Li et al. (2020) Xiaocheng Li, Chunlin Sun, and Yinyu Ye. Simple and fast algorithm for binary integer and online linear programming. Advances in Neural Information Processing Systems, 33:9412–9421, 2020.

- Ma and Simchi-Levi (2020) Will Ma and David Simchi-Levi. Algorithms for online matching, assortment, and pricing with tight weight-dependent competitive ratios. Operations Research, 68(6):1787–1803, 2020.

- Mehta (2013) Aranyak Mehta. Online matching and ad allocation. 2013.

- Mehta et al. (2007) Aranyak Mehta, Amin Saberi, Umesh Vazirani, and Vijay Vazirani. Adwords and generalized online matching. Journal of the ACM (JACM), 54(5):22–es, 2007.

- Mitzenmacher and Vassilvitskii (2020) Michael Mitzenmacher and Sergei Vassilvitskii. Algorithms with predictions, 2020.

- Shalev-Shwartz et al. (2012) Shai Shalev-Shwartz et al. Online learning and online convex optimization. Foundations and Trends® in Machine Learning, 4(2):107–194, 2012.

- Slivkins et al. (2019) Aleksandrs Slivkins et al. Introduction to multi-armed bandits. Foundations and Trends® in Machine Learning, 12(1-2):1–286, 2019.

- Talluri and Van Ryzin (2004) Kalyan T Talluri and Garrett Van Ryzin. The theory and practice of revenue management, volume 1. Springer, 2004.

- Vera and Banerjee (2019) Alberto Vera and Siddhartha Banerjee. The bayesian prophet: A low-regret framework for online decision making. ACM SIGMETRICS Performance Evaluation Review, 47(1):81–82, 2019.

Appendix A Proofs for Section 3

We begin by formally stating and proving weak duality

Proposition 5.

For every , and , we have .

Proof.

Consider any such that . Then, for , we have

Since satisfied was otherwise arbitrary, we have shown . ∎

A.1 Proof of Lemma 1

Proof of Lemma 1.

The convexity of follows from part (a) and the fact that the dual objective is always convex since it is a supremum of a collection of linear functions.

-

(a)

Shown in equation 2.

-

(b)

For , we have

where we have used the fact that for all , which holds because .

-

(c)

For , we have

where the inequality follows from the fact that .∎

A.2 Proof of Theorem 1

Proof of Theorem 1.

Fix an arbitrary . To simplify notation, define

We split the proof into four steps: (1) The first step involves lower bounding the performance of our algorithm in terms of single-period duals and the complementary slackness term; (2) The second step involves bounding the complementary slackness term using standard regret analysis of mirror descent; (3) The third step involves bounding the optimal from above using the single-period dual; (4) The final step puts it all it all together. Our proof significantly generalizes the proof of Balseiro et al. (2020), who established this result for the special case of a constant target consumption rate for all . The main technical contribution of the current proof is establishing a general performance guarantee for dual-mirror descent for all target consumption sequences, which will prove critical in getting an asymptotically-near-optimal competitive ratio for our model. This involves establishing a novel target-rate-dependent lower bound on the algorithm’s reward (Step 1), a novel target-rate-dependent upper bound on the optimal reward (Step 3), and a new way to put these bounds together (Step 4).

Step 1: Lower bound on algorithm’s reward.

Consider the filtration , where is the set of all requests seen till time and is the sigma algebra generated by it. Note that Algorithm 1 only collects rewards when there are enough resources left. Let be first time less than for which there exists a resource such that . Here, if this inequality is never satisfied. Observe that is a stopping time w.r.t. and it is defined so that we cannot violate the resource constraints before . In particular, for all . Therefore, we get

Observe that is measurable w.r.t. and is independent of , which allows us to take conditional expectation w.r.t. to write

| (A-10) |

where the second equality follows the definition of the single-period dual function.

Define . Then, is a martingale w.r.t. the filtration because and . As is a bounded stopping time w.r.t. , the Optional Stopping Theorem yields . Therefore,

A similar argument yields

Hence, summing over (A.2) and taking expectations, we get

| (A-11) |

where

The first inequality follows from part (c) of Lemma 1, the second inequality follows from part (b) of Lemma 1 and the third inequality follows from the convexity of the single-period dual function (Lemma 1).

Step 2: Complementary slackness.

Define . Then, Algorithm 1 can be seen as running online mirror descent on the choice of the dual variables with linear losses . The gradients of these loss functions are given by , which satisfy . Therefore, Proposition 5 of Balseiro et al. (2020) implies that for all :

| (A-12) |

where is the regret bound of the online mirror descent algorithm after iterations, and the second inequality follows because and the error term is increasing in .

Step 3: Upper bound on the optimal reward.

Step 4: Putting it all together.

Combining the results from steps 1-3 yields:

for all . All that remains to complete the proof is choosing the right . If (no resource was completely depleted), set . If , then there exists a resource that nearly got depleted, i.e., . Moreover, recall that the definition of a target consumption sequence implies . Thus, . Therefore, setting , where is the -th unit vector, yields:

Here we use that . This follows because . Finally, if we put everything together, we get

where we have used the definition of . The theorem follows from observing that all of our choices of in the above discussion lie in the set . ∎

A.3 Proof of Proposition 1

Appendix B Proofs and Extensions for Section 4.1

To prove Theorem 2, it suffices to prove the stronger statement which holds for online algorithms with prior knowledge of before time . Consequently, we assume that online algorithms have this prior knowledge in the remainder of this section. Any algorithm without this knowledge can only do worse.

B.1 Proof of Lemma 2

Proof of Lemma 2.

Fix . As the resource consumption function is given by , we get that

Let be a feasible solution of the above optimization problem. Then,

| (B-14) |

where the first inequality follows from the concavity of and the second inequality follows from the resource constraint . Hence, we get that for all is an optimal solution to the above optimization problem and as a consequence, . Moreover, we have that is the unique optimal solution because is strictly concave and increasing for , and therefore (i) The first inequality in (B-14) is strict whenever for some ; (ii) whenever . ∎

B.2 Proof of Lemma 3

Proof of Lemma 3.

We begin by noting that our use of instead of is justified in the right-hand side of the equality in Lemma 3 because is continuous for all . Now, fix and . Let

and define

| (B-15) |

Then, by definition of , we have . Moreover, observe that and

for all . To see why the second-last inequality holds, note that the Intermediate Value Theorem applied to the function between the points and yields the existence of an such that , which implies .

As a consequence, we get

| (B-16) |

Combining the above inequalities with the definition of yields . Hence, we have for all .

Consider the algorithm that selects action at time . Then, in time steps, it receives a reward of

Therefore, we have shown that

Next, we prove the above inequality in the opposite direction. Consider an online algorithm such that

for some constant . Let represent the action taken by at time . Since the action of an online algorithm cannot depend on future information, represents the action taken by algorithm for all horizons . Let represent the sequence obtained by sorting in decreasing order, and let represent the algorithm that takes action at time . Then, we have

which allows us to assume that is sorted in decreasing order without loss of generality.

Since , to complete the proof it suffices to show that

where the equality follows from the definition of (B-15). We will prove this via induction by inductively proving the following statement for all :

To do so, we will maintain variables that we initialize to be 0 and update inductively. At a high level, they capture a water-filling procedure. Suppose there is a container corresponding to each time step with a capacity of . We assume that these containers can be connected to each other so that water always goes to the lowest level, which corresponds to the highest marginal reward since is concave. Moreover, we will assume that container becomes available at time and is connected to containers at that point. Finally, we also freeze the newly-added water at the end of each time step to inductively use the properties of the water level from the previous time step. We would like to caution the reader that this water-filling interpretation is just a tool that guided our intuition, and the mathematical quantities defined below may not match it exactly.

Base Case :

Let be a decreasing sequence that satisfies the following properties:

-

I.

.

-

II.

for all .

-

III’.

.

Such a sequence is guaranteed to exist because satisfies properties (II - III’) trivially, and (I) can be satisfied as and is a continuous increasing function. If is a constant sequence, then property (I) implies

Suppose is not a constant sequence. Then, the strict concavity of implies that

which implies

| (B-17) |

Therefore, we have established:

-

III.

.

-

IV.

.

where (III) follows follows trivially when is a constant sequence and follows from (III’) and otherwise, and (IV) also follows trivially when is a constant sequence and follows from (B-17) otherwise.

Induction Hypothesis :

Suppose there exists a decreasing sequence that satisfies the following properties:

-

I.

.

-

II.

for all .

-

III.

.

-

IV.

.

Induction Step :

If , then set and for all . In this case, it is easy to see that conditions (I-IV) hold for . Next, assume . In this case, set . Moreover, let be a decreasing sequence that satisfies the following properties:

-

I.

.

-

II.

for all .

-

III’.

for all .

Such a sequence is guaranteed to exist because satisfies property (II) trivially, (III’) as a consequence of the inductive hypothesis, and (I) can be satisfied because is a continuous increasing function and

Observe that (III’) and implies

-

III.

Now, only (IV) remains. First, note that the Intermediate Value Theorem applied to implies

and as a consequence, we get . This further implies

where the first inequality follows from the concavity of and the fact that ; the second inequality follows from concavity of and the observation that the induction hypothesis and (III’) imply whenever , i.e., implies ; the third and the fourth inequalities follow from the Intermediate Value Theorem applied to ; and the equality follows from (I). Therefore, we get (IV) by using the inductive hypothesis and :

This concludes the induction step and thereby the proof, since (II) and (IV) together imply . ∎

B.3 Proof of Theorem 2

Proof of Theorem 2.

Combining Lemma 3 and Lemma 2 yields

| (B-18) |

where . First, note that the Intermediate Value Theorem applied to implies

which allows us to derive the following inequality from (B-18):

Using and , we get the first half of Theorem 2:

To get the second half, note that , which allows us to write:

Finally, define as . Then,

Hence, for , is concave and is maximized at . Plugging in yields

which completes the proof. ∎

B.4 Randomized Upper Bound with Linear Rewards and Consumptions

The upper bound of Theorem 2 can be extended to the popular special case of linear rewards and linear consumption. Fix and . We show that there exists a request distribution, with linear rewards and random linear resource consumption functions, that behaves like in expectation. Define a consumption rate CDF as

Consider the following request distribution: the reward of every request is , the linear resource-consumption rate is drawn randomly from , and the action set is (to represent the fraction of the request accepted), i.e., for request and action , the reward is and the amount of resource consumed is . It is relatively straightforward to see that the optimal action at each time-step is to set a threshold and accept a request (set ) if and only if the consumption rate is less than or equal to the threshold . For such a threshold , the expected cost is given by

and the expected reward is given by . Therefore, the expected reward is equal to the expected cost raised to the power , and consequently this request distribution behaves like in expectation.

B.5 Upper Bound with Distributional Knowledge of Horizon