Explaining the root causes of unit-level changes

Abstract

Existing methods of explainable AI and interpretable ML cannot explain change in the values of an output variable for a statistical unit in terms of the change in the input values and the change in the “mechanism” (the function transforming input to output). We propose two methods based on counterfactuals for explaining unit-level changes at various input granularities using the concept of Shapley values from game theory. These methods satisfy two key axioms desirable for any unit-level change attribution method. Through simulations, we study the reliability and the scalability of the proposed methods. We get sensible results from a case study on identifying the drivers of the change in the earnings for individuals in the US.

1 Introduction

Changes in the values of an output variable for a statistical unit (e.g., individual) are common when the unit’s characteristics change or the system in which those variables are measured changes. In finance, a credit scoring model may predict a high credit worthiness score for an individual who had a very low score just a year ago. It could be that the system was upgraded with a new model or the individual simply accumulated a lot of wealth within a year. To be able to take corrective actions—if needed—when we observe a change in the observed target value for a unit, we need to understand what caused the change in the first place.

In recent years, several techniques have been developed in interpretable ML (or explainable AI) literature to explain the predicted value in the foreground for a unit relative to some background value, e.g., prediction for another unit (Lundberg & Lee, 2017b; Singal et al., 2021; Sundararajan et al., 2017; Frye et al., 2020; Ribeiro et al., 2016, 2018; Shrikumar et al., 2017; Heskes et al., 2020). These methods can explain the change in the output values in terms of the change in the values of each input variable. But they cannot explain the change in terms of the change in the models, simply because they assume that the model is fixed. The models in ML are just a special case of “mechanisms”.

Formally, our problem setup is as follows. For a unit, suppose a deterministic mechanism transforms the input vector to an output value . We observe the output value in the background, and in the foreground. We assume that deterministic mechanisms map respective input to output values , with . Our goal is to quantify how much of the output change is driven by 1/ the change in the mechanism (), and 2/ the change in the input vector () or further break it down to the change in the value of each input variable ().

Our main contributions are as follows. 1/ We first axiomatize desirable properties of an attribution method for explaining unit-level changes (section 3). 2/ We then propose two methods based on counterfactuals for attributing unit-level changes at various input granularities using the concept of Shapley values from game theory (section 4). In particular, the first method attributes a unit-level change to the change in the input vector and the change in the mechanism from the background to the foreground scenario (section 4.1). This coarse-grained attribution can be broken down to a finer detail up to the change in the value of each input variable for linear mechanisms (section 4.2). To obtain a fine-grained attribution for non-linear mechanisms, we modify the coarse-grained attribution method to include the change in the value of each input variable (section 4.3). We discuss their properties in section 4.4.

We compare related work in section 5. Through simulations, we study the reliability and scalability of the methods in section 6.1. Then we present a real-world case study identifying the drivers of the change in the average earnings of US individuals reported through surveys in 1976 and 1982, and discuss the results for an exemplar individual. Finally, we conclude with a discussion on the uncertainty quantification and the limitations of our approach in section 7. All proofs are in the appendix. We also present an attribution method when one demands explanations of unit-level changes w.r.t. causal mechanisms of variables in the real-world that are stochastic in the Appendix.

2 Problem Definition

Let denote the input variables (e.g., income, marital status) to a deterministic mechanism that produces the output variable (e.g., credit score). We will use to denote the space of input values, and for the space of output values. Typically, and . In the context of ML, the mechanism can be a prediction model. Formally, we make the following assumption:

Assumption A1/ A deterministic algorithm produces output from inputs .

The output produced by can differ from the actual variable in the real-world. In particular, the inputs cause the output w.r.t. the algorithm . In a causal language, inputs are the root nodes with outgoing arrows pointing to . The causal relationships between variables in the real-world become irrelevant here as the output results from applying the algorithm on inputs (Janzing et al., 2020). We also refer to as the mechanism that generates from .

For a statistical unit (e.g., a person), suppose that we observe the output value in the background (e.g., score in 1976) and in the foreground (e.g., score in 1982). The background and foreground scenarios can be two snapshots of time. We want to explain the drivers of the change in the output value of the unit, i.e., . Let us rewrite in terms of input values and mechanisms:

| (1) |

Observe that the changes in the input () and the mechanism () drive . Our goal is thus to attribute to 1/ the mechanism , and 2/ the inputs overall or break it down to each input variable . By working with deterministic mechanisms , we keep the framework general for a broad range of AI/ML applications. In the context of explainable AI or interpretable ML, we can explain the drivers of the change in the predicted values between two scenarios.

3 Desirable Properties

Next we discuss desirable properties of an attribution method for explaining unit-level changes.

Axiom 1/ Dummy: An attribution method for explaining unit-level changes satisfies Dummy property if the causal driver gets a zero attribution if its value does not change from the foreground scenario to the background scenario. In particular, the Dummy property implies the following: A/ the mechanism gets a zero attribution if the foreground and background mechanisms are equivalent, i.e., for all , and B/ the overall input gets a zero attribution if the foreground and background input vectors are the same, i.e., , or any input variable gets a zero attribution if the foreground and background values of are the same, i.e., .

The Dummy property reflects the semantics that a cause does not contribute to the change in the effect, if the cause did not change. For example, it is plausible that the education level of individuals is one of the causes of their wage; if the education level of an individual does not change between two years but the wage changes, then education level does not contribute to the wage-change. This axiom formalizes the Dummy axiom of Shapley values (Shapley, 1953) in the context of unit-level changes.

Axiom 2/ Completeness: An attribution method for explaining unit-level changes satisfies Completeness property if the attributions add up to the unit-level output change . Such a linear decomposition is desirable because then the attributions are interpretable to humans. This axiom formalizes the Efficiency axiom of Shapley values (Shapley, 1953) for unit-level changes.

4 Attributing unit-level changes

First we present our method to attribute the output change for a unit to the mechanism and the overall input in section 4.1. For the special case of linear mechanisms, we derive a closed-form solution in section 4.2. Through the decomposition of that closed-form solution, we also obtain a fine-grained attribution to each input variable . Finally, to obtain a fine-grained attribution for non-linear mechanisms, we introduce our second method in section 4.3. Whenever we mention the causes of , we interchangeably use the scalar placeholder for and the vector placeholder for .

4.1 Coarse-grained attribution for any type of mechanism

Here we attribute the output change to the mechanism and the inputs . We do not break down the attribution to to each input variable . In particular, the set of causes of is . Here, we are agnostic to the type of mechanism .

Observe that we can obtain the foreground output value from the background value by gradually replacing the input vector and mechanism to their foreground values one by one. Each time we replace a cause by its foreground value, we can compute its contribution as the change in the output value relative to the output value obtained by replacements before. In particular, we can compute the contribution of a cause given that we have already replaced causes in subset to their foreground values before as

| (2) |

where is an indicator function of subset that tells whether a cause assumes its foreground value, indexed by (2), or its background value, indexed by (1), based on the causes in , i.e.,

| (3) |

But the contribution depends on the subset given as context. For any ordering of causes , we could consider the contribution of given as the context. This dependence on ordering introduces arbitrariness in the attribution procedure.

To get rid of the arbitrariness, we leverage Shapley values (Shapley, 1953) from cooperative game theory. The key idea of Shapley values is to symmetrize over all orderings, i.e., consider all possible orderings, compute the contribution for each ordering, and then take the average.

Using the concept of Shapley values, the contribution of a cause to the output change is then given by the average contribution over all possible orderings, i.e.,

| (4) |

where the second summation follows from averaging contributions for permutations of with the same value of before in the ordering.

As we only have two causes (i.e., ), we can derive a closed-form solution with a simple algebraic manipulation. In particular, the Shapley value contribution of the mechanism equals:

| (5) |

In words, the contribution of to is the average of the output changes (using vs ) for the background and foreground input vectors separately.

Similarly, the Shapley value contribution of the overall input equals:

| (6) |

In words, the contribution of inputs to is the average of the output changes for the foreground and background input vectors using the background and foreground mechanisms separately.

Counterfactual interpretation. In the expression of Shapley values and above, besides two factual terms and , we also have two counterfactual terms and . Thus, the attributions and consider two key counterfactual questions that naturally arise when explaining unit-level changes: 1/ What would have been the output value for the unit had the input vector remained the same (to its background value), but the mechanism changed (to its foreground value)? The term answers this enquiry. 2/ What would have been the output value for the unit had the mechanism remained the same (to its background value), but the input vector changed (to its foreground value)? The term answers this enquiry. These counterfactuals are predictive, and fit the predictive interpretation of counterfactuals by Pearl using a structural causal model when the unobserved noise terms remain constant (Pearl, 2009, Ch. 7.2.2).

We refer to this attribution method as COARSE-ATTRIB, to emphasize that the attribution is for the overall input variables instead of each input variable, and the procedure works with any type of mechanism (linear or non-linear). For the special case of linear mechanisms, we can derive a closed-form solution from the above procedure that provides a more fine-grained attribution at the level of each input variable and the mechanism, which we discuss next.

4.2 Breakdown of coarse-grained attribution for linear mechanisms

Consider the linear mechanisms of the form: where ’s are the linear coefficients. Then the Shapley value contribution of inputs to (Eq. 6) reduces to

| (7) |

From here, we obtain the contribution of each input variable to as

| (8) |

In words, the Shapley value contribution of each input variable captures the impact of the change in the values of the variable in the foreground and background scenarios, weighed by the average value of corresponding linear coefficients.

Analogously, the Shapley value contribution of the mechanism to (Eq. 5) reduces to

| (9) |

That is, the Shapley value contribution of captures the impact of changes in the linear coefficients of variables in the background and foreground scenarios, weighed by the average values of corresponding variables in the two scenarios.

The Shapley values and can be negative for the linear mechanisms because we consider the change in the linear coefficients as well as the change in the input values, both of which can be either positive or negative. Consider a simple case wherein the linear coefficients of the foreground and background mechanisms are positive. A negative value of then implies a decrease in the value of from the background to the foreground scenario, whereas a negative value of implies a decrease in the linear coefficients from the background to the foreground scenario. This two-step attribution procedure for fine-grained attribution only works with linear mechanisms, however. Next we present an attribution method that provides a fine-grained attribution for any type of mechanism.

4.3 Fine-grained attribution for any type of mechanism

To obtain a fine-grained attribution for any type of mechanism, we consider each input variable as a potential cause of the output change, besides the mechanism. The core idea remains the same as in the coarse-grained attribution: starting with their background values for all causes, we gradually replace the value of each cause by its foreground value to measure its contribution.

Here, the set of causes of is . We modify the contribution (Eq. 2) in the coarse-grained attribution method to account for each input variable. In particular, we define the contribution of a cause given that we have already replaced causes in to their foreground values before as

Averaging the contributions over all orderings, we get the Shapley value contribution of each cause to the output change as

| (10) |

We refer to this attribution method as FINE-ATTRIB. While this method is close in spirit to the classical Shapley value attribution proposal for explaining prediction models (Lundberg & Lee, 2017b), the key difference is that we also include the mechanism as a player in the game. For reasons similar to the previous two attribution methods, the Shapley value contributions ’s can also be negative. It is easy to see that for a single input variable, this attribution method coincides with the coarse-grained attribution; the expressions for Shapley values will be the same. When there are at least two input variables (i.e., ), we consider more than two counterfactual terms however—involving various combinations of input variables and mechanisms—in this fine-grained attribution.

4.4 Properties of proposed methods

We are now ready to discuss the properties of the proposed attribution methods.

Theorem 1.

Both attribution methods satisfy completeness and dummy axioms.

Theorem 2.

When the mechanisms are linear, i.e., , the Shapley value attributions of both methods are the same, i.e., for .

Computational Complexity. Assume that the mechanism in concern is an oracle that evaluates an input vector of dimension in time for some function . That is, the worst-case computational complexity of is . This is a reasonable assumption because commonly assumed mechanisms like prediction models take more steps to evaluate an input as its dimensionality increases. The coarse-grained attribution method evaluates input vectors by mechanisms four times in total, and performs basic algebraic operations on those to obtain the attributions. As such, COARSE-ATTRIB runs in . The attribution method for linear mechanisms only perform simple algebraic operation on the values of input variables and linear coefficients, and hence has a worse-case complexity of . The fine-grained attribution method for non-linear mechanisms, however, has an exponential complexity, i.e., , as the contributions—which take constant time—are computed over all subsets whose size is . Up to 30 input variables, FINE-ATTRIB finishes within minutes. For more variables, we use sampling approximations to Shapley value contributions (Strumbelj & Kononenko, 2014) where we sample a fixed number of subsets and compute the Shapley values by averaging contributions over those (in Eq. 10).

5 Related Work

Next, we compare and contrast the proposed methods to existing approaches in the explainable AI and interpretable ML literature. To this end, we group the existing literature into three scenarios.

1/ Input fixed, Mechanism fixed. The vast body of work on explainable AI focuses on explaining a fixed AI/ML model Cohen & Howe (1988); Newell & Simon (1976); Lundberg & Lee (2017c); Ribeiro et al. (2016, 2018); Lakkaraju et al. (2020); Nguyen et al. (2019); Singal et al. (2021); Lundberg & Lee (2017a); Shrikumar et al. (2017); Sundararajan & Najmi (2020). That is, most explanation methods (e.g., node-based, instance-based) explain a single prediction model at one of the following levels of details.

Unit–Input Level. Methods like LIME Ribeiro et al. (2016), SHAP Lundberg & Lee (2017c), causal Shapley value (Heskes et al., 2020), and asymmetric Shapley value Frye et al. (2020) explain some function of prediction by quantifying the importance of the value of each input variable for unit . A typical example of is the deviation of prediction from its expected value, i.e., . While we can introduce a new binary variable to a new function , which switches to either or , doing so introduces ambiguity in selecting the distribution for computing the baseline expectation .

Unit Level. Methods in this category explain some function of prediction by quantifying the importance of a subset of input vector of the unit or for other units . Counterfactual visual explanation method Goyal et al. (2019) finds regions in a given image , when changed, would produce a different classification. Koh & Liang (2017) use influence functions to identify instances in the training set that are responsible for the prediction of a given test instance . Nguyen et al. Nguyen et al. (2019) use activation maximization to identify input instances that strongly activate a function (neuron) of interest. Anchors Ribeiro et al. (2018) explain the prediction for an input vector by identifying rules (i.e., subsets ) that are sufficient for the prediction. These methods also cannot attribute to the mechanism as they also assume that the mechanism is fixed.

Aggregate Input Level. Classical proposals on ablation study Newell & Simon (1976); Cohen & Howe (1988) quantify the importance of an input variable to the prediction model, e.g., through random perturbation of the values of input variables or removing the input variables. As such, we obtain the importance of input variable to the prediction model , in contrast to the prediction for a unit . Methods that provide explanations at the unit–input level can also provide input–level explanations by aggregating unit-level explanations over all units of an input variable. Like previous methods, these also assume that the mechanism is fixed.

2/ Input changes, Mechanism fixed. Most edge-based or flow-based explanation methods Singal et al. (2021); Shrikumar et al. (2017) quantify the importance of an edge, given a graphical representation of input variables (e.g., causal graph), by propagating changes in the values of input variables along the edges. As such, these methods can handle changes in input variables. Formally, these methods attribute the deviation in the prediction for a unit from the prediction for a reference unit using a single prediction model , i.e., . We could set and to attribute the prediction change to input variables. But they cannot attribute to the mechanism as they assume that the mechanism is fixed.

3/ Input changes, Mechanism changes. A classical statistical methodology called Kitagawa-Blinder-Oaxaca decomposition Kitagawa (1955) also explains changes, but at the aggregate level (mean), and only works with linear models. In a nutshell, the decomposition of prediction change into input change and mechanism change is obtained by taking the difference between the linear regression equations of background and foreground scenarios. A recent proposal by Budhathoki et al. (2021) attributes the change in the distribution (or its property) of a variable to the conditional distribution of each variable given its direct parents in the causal graph. If an FCM is also available, by replacing the structural assignments at the unit-level (with corresponding noise values), we can attribute the unit-level output change. We operationalize this idea in Appendix B.

6 Experiments

First, through simulations, where we can establish the ground truth, we evaluate the performance of our methods for attributing output changes when we learn prediction models from data, and study the scalability of FINE-ATTRIB whose computational complexity is exponential (section 6.1). Then we assess whether results are sensible on a real-world case study (section 6.2). We ran the scalability simulations on a Macbook Pro with 8GB RAM and 1.4 GHz Quad-Core Intel Core i5 processor.

6.1 Simulated experiments

Here we empirically investigate two research questions: 1/ How reliable are the attributions when we do not know the underlying mechanisms? 2/ Does the fine-grained attribution scale?

Reliability Simulation Setup & Results. We start with ground truth background and foreground models with random parameters. Then we generate random background and foreground input/output samples of the same size. For each instance of those samples, we obtain ground truth attributions using the ground truth models. Likewise, using prediction models learned from respective samples, we obtain estimated attributions with fitted models.

In particular, we consider 2 types of ground truth models: linear and polynomial with interactions. We uniformly randomly choose between 1 to 5 number of inputs. For a polynomial model, we uniformly randomly select its degree between 2 to 4. For both models, we uniformly randomly assign between -5 to 5 to each of its linear coefficients. For each input variable (in both background and foreground scenario), we draw samples of size 2000 independently from a standard Normal distribution. Then we apply those models to obtain the background and foreground outputs.

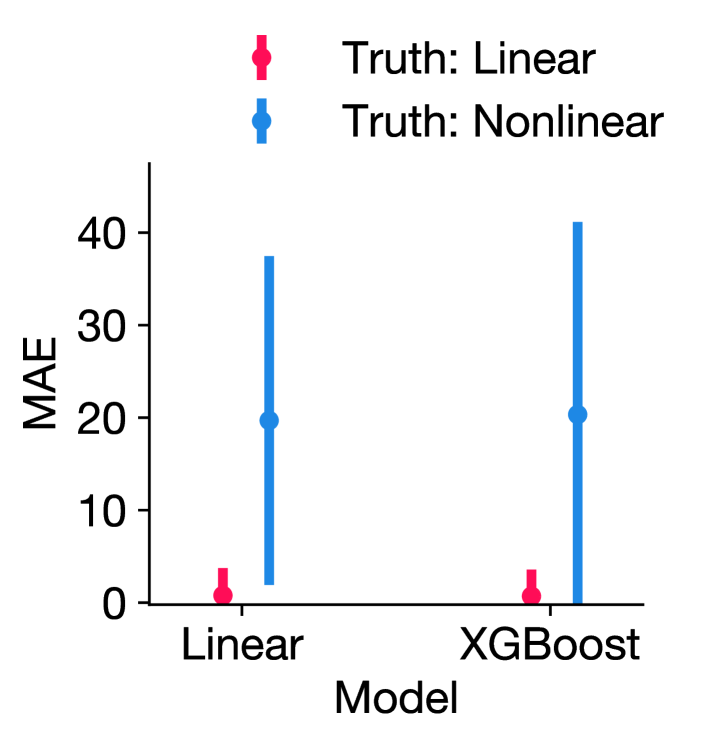

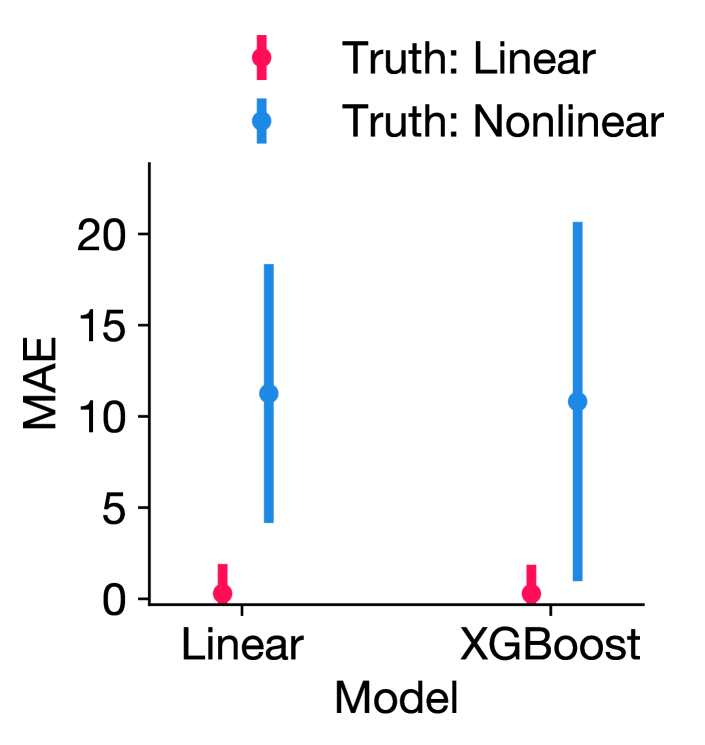

Fig. 1 (a–b) shows the mean absolute error (MAE) of estimated fine-grained and coarse-grained attributions (relative to ground truth attributions) using fitted linear and XGBoost regressions (with default hyperparameters) for 100 ground truth models. When the ground truth is linear, regardless of the type of fitted prediction models, estimated attributions are closer to the ground truth attribution. In contrast, for the non-linear ground truth, attributions show a relatively high variance.

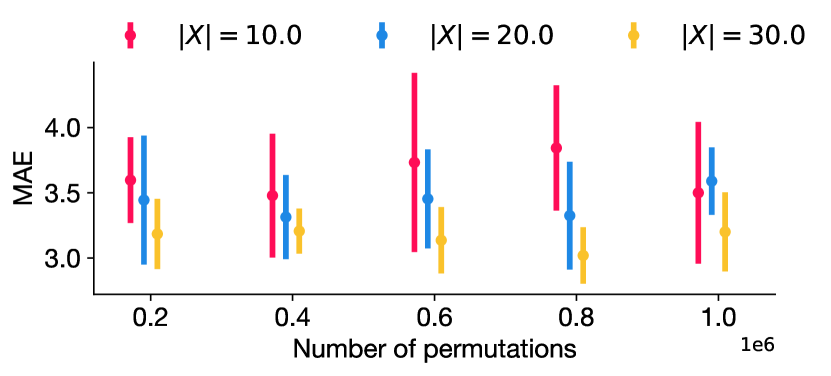

Scalability Simulation Setup & Results. We first study how well sampling-based fine-grained attributions approximates exact fine-grained attributions. We use linear ground truth models where we can compute the exact attributions using the closed form expression for any number of features. Fig. 1 (c) shows the MAE of approximated attributions for the case of 10, 20 and 30 input variables as we sample more permutations. The reported averages and standard errors are calculated over 100 ground truth models and 1000 sample sizes. As expected, if there are more input variables, with more permutations the attributions are close to the true attributions. This tells us that we can trade-off accuracy for speed to obtain fine-grained attributions when the number of input variables is large.

6.2 Real-world case study

We will use real-world earnings data to explain how our method can be used to explain the drivers of changes in earnings over time. We first explain the drivers for all individuals in the study (by aggregating over unit–level attributions), and then show the results for an exemplar individual.

Background. The Panel Study of Income Dynamics (PSID) is an ongoing survey of households launched in 1968 in the United States with the goal of providing data to assess President Lyndon Johnson’s “War on Poverty” (Johnson et al., 2018). The survey was conducted annually until 1997 and biennially thereafter. In particular, this survey collects information on income and family demographics of thousands of representative households in the US over time. We use our method to identify the drivers of change in the income of households between two surveys, 1976 and 1982.

Data. We consider a sample of 595 individuals who are heads of the households from the surveys carried out between 1976 and 1982. So, for each individual, we have 7 annual observations on 12 variables related to income. Our target is “wage” (reported in natural logarithm). We use the 9 relevant variables as input to a prediction model that predicts “wage” (clarified in Appendix A).

Modelling. We wish to understand the drivers of change in the earnings reported in surveys from 1976 versus 1982. We observe that the earnings of roughly 98% of individuals have increased between the surveys (585 out of 595).

Let denote the growth in average earnings reported in 1982 relative to that in 1976, i.e.,

where is the earnings of individual reported in the survey conducted in year , and divisions by cancel out. We observe a relative growth of . What drove this change? It is difficult to establish the causal graph here. We thus resort to prediction models, and explain this wage gap w.r.t. the prediction model.

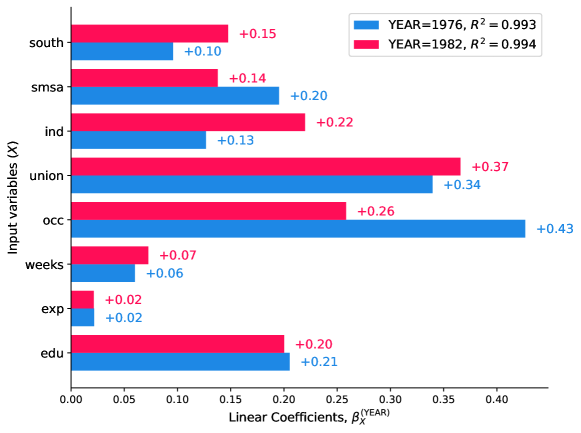

We assume a linear mechanism, which we shall probe with model fit diagnostics later. That is, we model “wage” as a linear function of input variables for each survey. We use Ordinary Least Squares (OLS) method for fitting the linear models from data. The fitted linear coefficients and model diagnostics are shown in Figure 4 in the Appendix. We observe that the R-squared fits of linear models from both data are roughly 0.99. That is, roughly 99% of the variance in “wage” is explained by each linear model. This shows that linear models are suitable for this case study.

To explain , first we compute the Shapley value attributions to input variables and mechanism for the change in earnings of each individual , i.e. . We then take the sum of Shapley value attributions to each input variable of all individuals, and repeat the same for the mechanism. The grand sum of the resulting sums then matches the numerator , by which we obtain the aggregate attributions to input variables and mechanism.

Results: Aggregate attribution.

Our method reveals that roughly 76% of is driven by mechanism change and the remaining 24% is driven by input change as shown in Figure 2 (a). If we break down the attribution to input change further, the change in the years of full-time work experience (i.e., “exp”) is the biggest driver amongst others.

The attribution to mechanism change is reasonable for the following reason. From the model fit plot in Fig. 4, we observe that the coefficient of “occ” (white-collar occupation or not), in particular, decreased by roughly 40%, from 0.43 in 1976 to 0.26 in 1982. The 70s were a tumultuous time in the US as the country was transitioning from a manufacturing to a service-based economy, manufacturing plants shut down, jobs were lost, and workers protested. Blue-collar jobs were replaced by white-collar jobs. But many blue-collar workers who got white-collar jobs still ended up in low paid white-collar occupations (Westcott, 1982). Thus, being a white-collar worker did not impact earnings greatly in the beginning of the 80s. The attribution to input “exp” change is also plausible given that there is a 6 year gap between the two surveys. It is also typical to get paid better with more years of experience. We also rightly attribute 0% to “edu” as education of the individuals did not change between the two surveys.

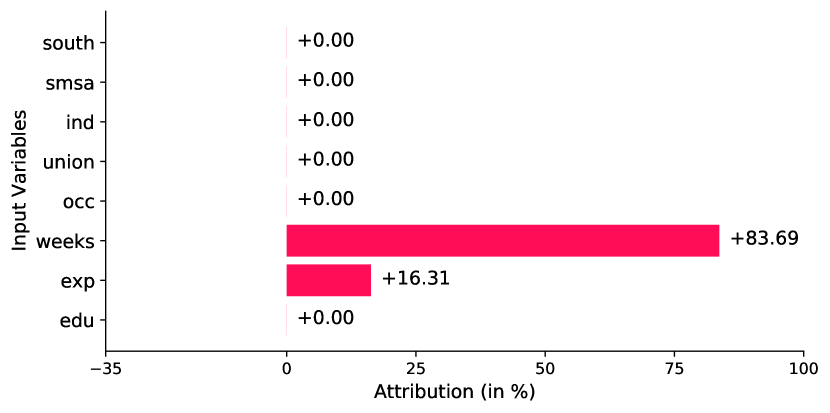

Results: Unit–level attribution anecdote.

To show how our method can be used to explain unit-level changes, we pick one anecdote from the data. In particular, we study an individual (id 167) whose reported earnings has increased the most between 1976 and 1982 (by roughly 34%) as shown in Table 2 in the Appendix. Only two input values have changed for this individual, namely that of “exp” and “weeks”. Our method attributes changes in input variables as the biggest driver (see Fig. 2 (b)). If we further break down the attribution to input, we observe that the drivers amongst input variables are the change in the number of weeks worked (“weeks”) and the work experience (“exp”). Given the gain in experience (by 6 years) and more weeks of work reported in 1982 subject to the level of education (Master’s Degree) and white-collar job, the increase in earnings is reasonable. We correctly identify the drivers that drove the increase in earnings for this individual.

7 Discussion

We proposed two methods based on counterfactuals for attributing the change in output values for a statistical unit at various granularities using Shapley values from game theory. The first method (COARSE-ATTRIB) attributes the output change to the change in the mechanism and the change in the input vector. For linear mechanisms, we obtain a closed-form solution that can also attribute to the change in the value of each input variable. To obtain this fine–grained attribution for non–linear mechanisms, we proposed FINE-ATTRIB that generalises COARSE-ATTRIB to each input variable. Both methods attribute a non-zero output change to a cause only if its value changes, and their attributions sum to the output change. As it is important for real-world applications, we studied the reliability of COARSE-ATTRIB and FINE-ATTRIB when we do not know the underlying mechanisms. When the underlying mechanisms are linear, both methods are accurate regardless of which model we pick. For non-linear ground truth, the variances in attributions are larger than that for the linear ground truth. We also showed that FINE-ATTRIB scales w.r.t. a number of input variables if we are willing to trade-off accuracy by applying sampling approximation to Shapley values. Lastly, we presented a case study identifying the drivers of average change in the earnings of individuals between two years, and discussed the drivers for one exemplar individual.

On Symmetrization. Although using the concept of Shapley values, we symmetrized over all ways of replacing causes from their background to foreground values, in practice, one may prefer a natural ordering of replacements, if available. In such cases, symmetrization is not necessary; it suffices to compute only the marginal contribution of a cause given the replacements of causes before following the natural ordering.

On Uncertainty Quantification. If we believe that the mechanisms have no uncertainties associated with them (e.g., among models in a class), then we get point estimates with zero uncertainties from these methods. But if we learn the mechanisms from data, uncertainties are inherent. Then it might be desirable to quantify the uncertainties of the attributions. To this end, we can compute the bootstrap confidence intervals for estimated attributions—by learning mechanisms from random subsets of data and computing the attributions using them.

Paradox 1/ Destructive Changes. We note that paradoxical results are possible in special cases where the change in the mechanism and the change in the input render no change in the output. Consider the following linear mechanisms, with a single input variable , where the coefficient flips its sign from positive to negative going from the background to the foreground scenario:

Now suppose we have the following input values for a unit, whose absolute values are the same, but sign flips similarly as in case of the mechanism:

The output does not change for this unit, i.e., . But both the mechanism and the input have changed. As such, one might expect both the mechanism and the input to get non-zero attributions. Is this the case though? Let us compute the attributions using the closed-form solutions for the linear mechanisms (section 4.2):

Contrary to our expectation, both causal drivers get zero attributions. As contributions can be negative, and we take the average of contributions over all orderings, such scenarios seem almost unavoidable. While such scenarios are possible, they are contrived. We present another paradox in the Appendix.

References

- Balke & Pearl (1994) Balke, A. and Pearl, J. Counterfactual probabilities: Computational methods, bounds and applications. In Proceedings of the Tenth International Conference on Uncertainty in Artificial Intelligence, UAI’94, pp. 46–54, San Francisco, CA, USA, 1994. Morgan Kaufmann Publishers Inc.

- Budhathoki et al. (2021) Budhathoki, K., Janzing, D., Bloebaum, P., and Ng, H. Why did the distribution change? In Proceedings of The 24th International Conference on Artificial Intelligence and Statistics, volume 130 of Proceedings of Machine Learning Research, pp. 1666–1674. PMLR, 13–15 Apr 2021.

- Cohen & Howe (1988) Cohen, P. R. and Howe, A. E. How evaluation guides ai research: The message still counts more than the medium. AI Magazine, 9(4):35, Dec. 1988.

- Frye et al. (2020) Frye, C., Rowat, C., and Feige, I. Asymmetric shapley values: incorporating causal knowledge into model-agnostic explainability. In Advances in Neural Information Processing Systems 33: Annual Conference on Neural Information Processing Systems 2020, NeurIPS 2020, December 6-12, 2020, virtual, 2020.

- Goyal et al. (2019) Goyal, Y., Wu, Z., Ernst, J., Batra, D., Parikh, D., and Lee, S. Counterfactual visual explanations. In Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pp. 2376–2384. PMLR, 09–15 Jun 2019.

- Heskes et al. (2020) Heskes, T., Sijben, E., Bucur, I. G., and Claassen, T. Causal shapley values: Exploiting causal knowledge to explain individual predictions of complex models. In Advances in Neural Information Processing Systems, volume 33, pp. 4778–4789. Curran Associates, Inc., 2020.

- Janzing et al. (2020) Janzing, D., Minorics, L., and Bloebaum, P. Feature relevance quantification in explainable ai: A causal problem. In Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics, volume 108 of Proceedings of Machine Learning Research, pp. 2907–2916, Online, 26–28 Aug 2020. PMLR.

- Johnson et al. (2018) Johnson, D. S., McGonagle, K. A., Freedman, V. A., and Sastry, N. Fifty years of the panel study of income dynamics: Past, present, and future. The ANNALS of the American Academy of Political and Social Science, 680(1):9–28, 2018.

- Kitagawa (1955) Kitagawa, E. M. Components of a difference between two rates*. Journal of the American Statistical Association, 50(272):1168–1194, 1955.

- Koh & Liang (2017) Koh, P. W. and Liang, P. Understanding black-box predictions via influence functions. In Proceedings of the 34th International Conference on Machine Learning - Volume 70, ICML’17, pp. 1885–1894. JMLR.org, 2017.

- Lakkaraju et al. (2020) Lakkaraju, H., Arsov, N., and Bastani, O. Robust and stable black box explanations. In Proceedings of the 37th International Conference on Machine Learning, ICML 2020, 13-18 July 2020, Virtual Event, volume 119 of Proceedings of Machine Learning Research, pp. 5628–5638. PMLR, 2020.

- Lundberg & Lee (2017a) Lundberg, S. M. and Lee, S. A unified approach to interpreting model predictions. In Advances in Neural Information Processing Systems 30: Annual Conference on Neural Information Processing Systems 2017, December 4-9, 2017, Long Beach, CA, USA, pp. 4765–4774, 2017a.

- Lundberg & Lee (2017b) Lundberg, S. M. and Lee, S.-I. A unified approach to interpreting model predictions. In Advances in Neural Information Processing Systems, volume 30. Curran Associates, Inc., 2017b.

- Lundberg & Lee (2017c) Lundberg, S. M. and Lee, S.-I. A unified approach to interpreting model predictions. In Advances in Neural Information Processing Systems, volume 30. Curran Associates, Inc., 2017c.

- Newell & Simon (1976) Newell, A. and Simon, H. A. Computer science as empirical inquiry: Symbols and search. Commun. ACM, 19(3):113–126, mar 1976.

- Nguyen et al. (2019) Nguyen, A., Yosinski, J., and Clune, J. Understanding neural networks via feature visualization: A survey. In Explainable AI: Interpreting, Explaining and Visualizing Deep Learning, volume 11700 of Lecture Notes in Computer Science, pp. 55–76. Springer, 2019.

- Pearl (2009) Pearl, J. Causality: Models, Reasoning and Inference. Cambridge University Press, New York, NY, USA, 2nd edition, 2009.

- Ribeiro et al. (2016) Ribeiro, M. T., Singh, S., and Guestrin, C. "why should i trust you?": Explaining the predictions of any classifier. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pp. 1135–1144, New York, NY, USA, 2016. Association for Computing Machinery.

- Ribeiro et al. (2018) Ribeiro, M. T., Singh, S., and Guestrin, C. Anchors: High-precision model-agnostic explanations. Proceedings of the AAAI Conference on Artificial Intelligence, 32(1), 2018.

- Shapley (1953) Shapley, L. S. A value for n-person games. Technical report, Rand Corporation, 1953.

- Shrikumar et al. (2017) Shrikumar, A., Greenside, P., and Kundaje, A. Learning important features through propagating activation differences. In Proceedings of the 34th International Conference on Machine Learning - Volume 70, ICML’17, pp. 3145––3153. JMLR.org, 2017.

- Singal et al. (2021) Singal, R., Michailidis, G., and Ng, H. Flow-based attribution in graphical models: A recursive shapley approach. In Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pp. 9733–9743. PMLR, 18–24 Jul 2021.

- Strumbelj & Kononenko (2014) Strumbelj, E. and Kononenko, I. Explaining prediction models and individual predictions with feature contributions. Knowl. Inf. Syst., 41(3):647––665, 2014.

- Sundararajan & Najmi (2020) Sundararajan, M. and Najmi, A. The many shapley values for model explanation. In Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pp. 9269–9278. PMLR, 13–18 Jul 2020.

- Sundararajan et al. (2017) Sundararajan, M., Taly, A., and Yan, Q. Axiomatic attribution for deep networks. In Precup, D. and Teh, Y. W. (eds.), Proceedings of the 34th International Conference on Machine Learning, volume 70 of Proceedings of Machine Learning Research, pp. 3319–3328. PMLR, 06–11 Aug 2017.

- Westcott (1982) Westcott, D. N. Blacks in the 1970’s: Did they scale the job ladder?. Monthly Labor Review, 105:29–38, 1982.

- Zhang et al. (2015) Zhang, K., Wang, Z., Zhang, J., and Schölkopf, B. On estimation of functional causal models: General results and application to the post-nonlinear causal model. ACM Trans. Intell. Syst. Technol., 7(2), 2015.

Appendix A Experiment Details

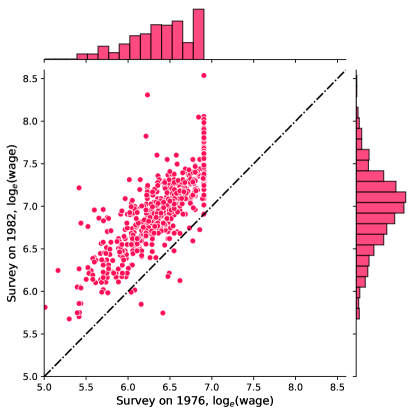

The data from the Panel Study of Income Dynamics is available online as the dataset “PSID7682” from the R package “AER” with the GPLv3 license. We describe the variables used for this case study in Table 1. From the original data, we exclude sensitive attributes like sex and race, and irrelevant attributes like marital status. Although they do not affect our analysis, learning fair models is not the main point of this case study. In Fig. 3, we show the scatter plot between earnings reported in those two surveys, along with their univariate histograms.

| Variable | Description | Type |

|---|---|---|

| wage | Natural logarithm of earnings in past year | target |

| edu | Years of education | input |

| exp | Years of full-time work experience | input |

| occ | Is the individual a white-collar worker? | input |

| weeks | Weeks worked past year | input |

| union | Is the individual a member of a union? | input |

| ind | Does the individual work in a manufacturing industry? | input |

| smsa | Does the individual reside in a standard metropolitan statistical area? | input |

| south | Does the individual live in the South? | input |

| year | edu | exp | weeks | occ | union | ind | smsa | south | wage |

|---|---|---|---|---|---|---|---|---|---|

| 1976 | 17.0 | 3.0 | 40.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 6.2 |

| 1982 | 17.0 | 9.0 | 50.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 8.3 |

Appendix B Unit-level changes with stochastic causal mechanisms

So far, we considered deterministic algorithmic mechanisms that output from inputs . The inputs are the causes of w.r.t. the algorithm . But they are not necessarily the causal ancestors of output in the real world. If our objective is to explain the change in the real output value accounting for causal mechanisms in real-world, we need to consider the causal relationships between variables and their causal mechanisms.

Suppose that the “mechanisms” by which the output is generated from its causes in the real world is stochastic. In particular, we make three assumptions here:

Assumption C1/ We have access to the causal graph of variables .

Assumption C2/ We have access to the associated functional causal model (FCM) (Pearl, 2009).

Assumption C3/ The FCM is invertible (Zhang et al., 2015).

Without loss of generality, let be the sink node, i.e., does not have any children. In an FCM, each variable is a function of its parents in the causal graph and an unobserved noise variable , i.e.,

| (11) |

where are independent (Pearl, 2009). The root nodes do not have any observed parents, only unobserved noise terms. Therefore, the stochastic properties of observables are derived from the joint distribution of unobserved noise variables . By recursively applying Eq. (11) until we reach the root nodes (which do not have any observed parents), we can write as a deterministic function of all noise variables instead of observed variables , i.e.,

| (12) |

where with being the space of values of noise variable . In other words, the unobserved variables determine the observed output . But the role of the composite function is rather subtle as it is tied to the noise variables. We can make it more explicit through the response-function based formulation of FCMs (Balke & Pearl, 1994).

To motivate the response-function based formulation, let us consider a simple case where the causal graph is . The structural equation of is a stochastic function: , which reduces to a deterministic function of for a fixed value of noise : . That is, if and take values in and respectively, then noise acts as a random switch that selects different functions from to . Without loss of generality, we can therefore assume that takes values in the set of functions from to , denoted by . Then we can rewrite the structural equation of as . The FCM has now turned into a probability distribution on the set of deterministic functions . For example, if and are binary, i.e., and , then there are four possible functions from to , i.e., , where and denote constant functions that always map to 0 and 1 respectively, and ID and NOT denote identity and negation respectively. Note that as root node does not have any observed parents, its noise value selects a trivial identity function that simply maps the noise.

Generalising this idea to variables, we obtain the value of (i.e., ) through a series of transformations at each causal ancestor, starting from root nodes following the causal ordering:

| (13) |

where is the -th parent of , and lower case represents the value of noise corresponding to the observable . That is, the value of is determined by the functions selected by noise values . Since the FCM is invertible, we can uniquely recover the unobserved noise values from the observed values , where . Therefore, the candidates for “root causes” of the output change are the deterministic mechanisms at each node selected by the noise values.

Let denote the set of causes of . To attribute to its “root causes”, we can define the contribution of a cause as in section 4.3: quantify how much would change if we change the noise value corresponding to the cause to its foreground value (i.e., replace the background mechanism at by the foreground mechanism) given that we have already changed background mechanisms in to foreground mechanisms:

To avoid arbitrariness introduced by the order in which we replace mechanisms, we symmetrize by taking the average of contributions over all orderings of to get the Shapley value contribution. This technique operationalises the proposal for attributing distributional changes to causal mechanisms of nodes in the causal graph (Budhathoki et al., 2021) to unit-level.

Appendix C Paradox 2/ Non-additivity for multiple changes when collapsing changes

As systems may undergo change multiple times, one may wonder whether the attributions add up when we "collapse" changes. More formally, given three time points , does the sum of the attributions for two consecutive changes (i.e., and ) equal the attributions for a single change obtained by collapsing the two changes (i.e., )?

Consider a mechanism connecting a single input variable to the output . Let denote the value of for a unit from the time point . Likewise, define and . Clearly the output changes are additive when we collapse changes, i.e., . What about the attributions? As we have a single input variable, both FINE-ATTRIB and COARSE-ATTRIB yield the same Shapley values. In particular, for the change from to , the Shapley value for the mechanism is given by

and that for the change from to is given by

Their sum is given by

where is given by

This shows that attributions are non-additive when we collapse the intermediate changes. This phenomenon can be explained by the inclusion of counterfactuals in our attribution methods. When we attribute a single change (i.e. ) obtained by the collapsing the intermediate changes ( and ), we do not consider the counterfactuals involving intermediate states any more (e.g., , ). This conclusion also holds for the Shapley values of the input , following similar algebraic calculation.

Appendix D Proofs

Theorem 3.

Both attribution methods satisfy completeness and dummy axioms.

Proof.

The completeness property follows directly from the property of Shapley values (Shapley, 1953). That is, the Shapley values of players in a “coalition game” sum up to the value of the game. In our case, the players are the causal drivers of . In all the attribution techniques, we start with background values only (e.g., or )—the worth of an empty coalition of players. As we gradually replace the causal drivers to their foreground values, we end up with foreground values only (e.g., or or )—the worth of the grand coalition where all players join. Therefore, the players add a total value of .

We show the dummy property for the coarse-grained attribution first. The causal drivers of are in the set . Let us recap the contribution of a causal driver given that we have replaced the causal drivers in the subset to their foreground values:

Suppose that the mechanism does not change, i.e. for all . Then the contribution of the mechanism to given any subset reduces to

where indicator functions and as any subset does not contain ; is either an empty set or . That is, the contribution of the mechanism to is zero regardless of the ordering in which we make replacements. As a result, the Shapley value of the mechanism , which is an average of contributions over all orderings , is also zero.

Now suppose that the input vector does not change, i.e. . Then the contribution of the inputs to given any subset reduces to

where indicator functions and as any subset does not contain ; is either an empty set or . That is, the contribution of the input to is zero regardless of the ordering in which we make replacements. As a result, the Shapley value of the input , which is an average of contributions over all orderings , is also zero.

For the fine-grained attribution, we can follow similar arguments. But for the sake of completeness, we show the proof regardless. The causal drivers of are in the set . Let us recap the contribution of a causal driver given that we have replaced the causal drivers in the subset to their foreground values:

Suppose that the mechanism does not change, i.e. for all . Then the contribution of the mechanism to given any subset reduces to

where indicator functions and as any subset does not contain ; is an element of the powerset . That is, the contribution of the mechanism to is zero regardless of the ordering in which we make replacements. As a result, the Shapley value of the mechanism , which is an average of contributions over all orderings , is also zero.

Now suppose that the value of an input variable does not change, i.e. . Then the contribution of the input variable to given any subset reduces to

where indicators functions , , and as any subset does not contain ; is an element of the powerset . That is, the contribution of the input variable to is zero regardless of the ordering in which we make replacements. As a result, the Shapley value of the input , which is an average of contributions over all orderings , is also zero. ∎

Theorem 4.

When the mechanisms are linear, i.e., , the Shapley value attributions of both methods are the same, i.e., for .

Proof.

Consider linear mechanisms of the form:

where ’s are the linear coefficients. The causal drivers are in the set . Let us write down the contribution of the input variable given a subset with FINE-ATTRIB assuming the aforementioned linear mechanisms:

In particular, the coefficient can assume either a foreground or a background value depending on whether contains . As such, we have

Note that is an element of the powerset which contains elements. Each set in the powerset containing can be paired with another set that does not contain . Therefore, half of the sets in the powerset contain , half do not. Thus the average contribution of , over all subsets , which is also its Shapley value, is given by

Similarly the contribution of the mechanism given a subset with FINE-ATTRIB assuming the aforementioned linear mechanisms is given by:

Following a similar argument as before, half of the sets in the powerset contain , half do not. Using the linearity of expectation property, the average contribution of , over all subsets , which is also its Shapley value, is given by

∎