Example of a Dirichlet process whose zero energy part has finite -variation

Abstract

Let be a fractional Brownian motion on with Hurst parameter , be its pathwise antiderivative with , and let be a standard Brownian motion, independent of . We show that the zero energy part of has positive and finite -variation in a special sense for . We also present some simulation results about the zero energy part of a certain median process which suggest that its -variation is positive and finite.

keywords:

semimartingale property , semimartingale function , Dirichlet process , p-variationMSC:

60H05 60J65, 60J55,1 Introduction

In a recent paper ([5]) we showed that a certain median process lacks the semimartingale property. This median process has a decomposition into a sum of a martingale and a process with zero quadratic variation. Such a process is called a Dirichlet process in [3], and a process with zero quadratic variation is said to have zero energy. Since the median process above is not a semimartingale, the zero energy part of the decompostion can not be of finite total variation. The proof provided in the above paper is indirect, that is it does not compute the total variation of the zero energy part. This paper tries to make the first steps for this computation. We consider a simpler case where the computation can be carried out and we also present some simulation result for the above median process. These simulation results suggest that if we compute the -variation along a specially selected sequence of partitions, then it has a finite limit. The exponent is the same as in [8]. They consider a process obtained from a Brownian motion with the formula , that is is the amount of time spent so far below the current value of .

Without going into too much details, short term increments of these processes are obtained roughly by substituting a Brownian motion into a continuously differentiable random function whose first derivative has non-zero and finite quadratic variation. The increment of the zero energy part of during an upcrossing of the interval is where is the exit time of and is conditioned to . By the mean value theorem there is a such that and we get that the increment is roughly . Here the stochastic integral is simply approximated with .

Similarly, the increment of the zero energy part during a downcrossing of is roughly . Since the number of down and upcrossing upto time differs only by one and is proportional to , we get that the contribution of crossings of is roughly proportional to . Similar computation can be done for intervals of form . The fact that the quadratic variation of is finite roughly means that for most of the increments is of order so finally we arrive at the conclusion that in order to have finite variation it is needed that , that is .

This argument is far from being rigorous. The aim of this paper to make this argument precise for the simplest case when is a fractional Brownian motion. The increments of a fractional Brownian motion with Hurst index over an interval of length is of size , so the last step of the above heuristic computation is , that is .

Theorem 1.

Let be a fractional Brownian motion on with Hurst parameter and let be a standard Brownian motion independent of . Denote an antiderivative of with and

For the variation of on any exists and equals to with .

Especially, for the variation is infinite almost surely on any non degenerate interval, while for it is identically zero.

In the previous claim the variation is definied similarly to the quadratic variation, that is, for any and any (deterministic) sequence of subdivisions of whose mesh goes to zero we have that

We start with a somewhat simpler claim.

Theorem 2.

2 Proof of Theorem 2

Using the scaling property of the Brownian motion and of the fractional Brownian motion we have that

| (1) |

For details see Lemma 2 below. Since we have by the law of large numbers that

This implies that we can replace the the right hand side of (1) with

and investigate its limiting behavior as . The difference is that now the number of summands is deterministic, therefore the summands are identically distributed by their definition, although not independent. It is also clear that we can further simplify the expression; to prove Theorem 2 it is enough to show that

| (2) |

As is now fixed to 1, we drop it from the notation. In this form it is a weak law of large numbers and we prove it by showing that the variance of this sum is . For this we use the strong mixing property of the increments of the fractional Brownian motion which follows easily from the decay of the correlation (see [4]). We formulate it in Lemma 1 below.

We finish the proof of Theorem 2 by showing the next proposition.

Proposition 1.

With , , and , let . Then is strictly stationary and strong mixing in the sense that

for any measurable functional for which is a square integrable random variable.

From Proposition 1 we have the weak law of large numbers for squares integrables functionals . Indeed, using the stationarity we have the following estimation for the variance

Here , hence its arithmetic mean sequence does the same.

It is possible to show that is square integrable, but we do not need this result. Indeed, if we know the and hence the convergence of the averages for bounded , then we have the same limiting relation for integrable functionals as well. So to finish the proof it is enough to show that is square integrable,

Here has the same law as which has a normal law, so this part is obviously square intagrable. For the Itô integral part we can use the izometry combined with the occupation time formula to obtain that

It remains to check that Proposition 1 holds. We do this using the next lemma whose proof involves only elementary computation, hence it is left for the reader.

Lemma 1.

There is a constant depending only on , such that for and for a fractional Brownian motion with Hurst index

where is the translation with , that is .

This lemma extends easily with the monotone class argument to a much wider set of functionals involving scaling as well. In what follows we need it in the following form

Corollary 1.

Let be a fractional Brownian motion with Hurst index . For let .

Then for a measurable functional ,

provided that is square integrable and

Proof.

Using the monotone class argument it is enough to prove for functionals of the form , where is a bounded continuous function on . For this case it is enough to show that the and are asymptotically independent, so eventually it is enough to check that the covariances are vanishing in the limit.

Note that

and for large enough. Then, from Lemma 1

which tends to zero by the assumption. The proof is complete. ∎

Proof of Proposition 1.

For the strict stationarity we need to show that and have the same law for each . By the special structure of the sequence is obtained from in the same way as is obtained from . So it is to show that and has the same law. It follows easily from the strong Markov property of the Brownian motion that is independent and . By the stationarity of the increments of fractional Brownian motion , has the same law as for any . Now using the value of as yields that and are independent, and has the same joint law as and .

For the strong mixing property it is enough to consider functionals of the form with bounded and then use monotone class argument. For this special case it is enough to show that

as tends to infinity. Then using the boundedness of the result easily follows.

Using the translation notation from Lemma 1, is easy to express,

So this part follows from Corollary 1 and the fact that .

Concerning , we can consider bounded functionals of the form , where and is the vector variable obtained from by sampling the values at the time points . Let , then so

and as is independent of we also have that

Lemma 2.

For let

Then

-

1.

,

-

2.

and

-

3.

.

Proof.

The first two point follows from the scaling invariance of the (fractional) Brownian motion and from the definition of the stopping time sequence.

For the last point

Here is the anti derivative of such that . Then . If denotes the antiderivative of with , then for positive

and similarly for negative . From these computations

For the stochastic integral note that , so

∎

3 Proof of Theorem 1

The proof of Theorem 1 goes along similar lines as that of Theorem 2. For a given interval let’s define

| (3) |

The key point here is again the scaling property of the (fractional) Brownian motion: for ,

If is the random function with as its derivative and , then for

and similarly for . So if we write in place of we get

Similary for the stochastic integral

So we can conclude that

with a suitable functional .

The proof of Theorem 2 is based on the next two claims which we prove below.

Proposition 2.

For a non-degenerated interval denote . Then the law of does not depends on and

provided that is square integrable.

Corollary 2.

Suppose that is a sequence of subdivisions of , such that the mesh and is a functional such that is integrable. Then

Theorem 2 follows from Corollary 2 if we apply it to

We check that is integrable by showing that . Note that so it is enough to show that the next random variable is square integrable

Since by trivial estimations we obviously have that . For the second term we apply again Itô izometry followed by the occupational time formula to get that

Proof of Proposition 2.

We start with the law of . Since the increments of the fractional Brownian motion are stationary, has the same law as for any deterministic . Then by the independence of and the conditional law of given does not depend on , that is is independent of with the same law as . But then by the scaling invariance of the same is true for . Finally, by the Markov property and scaling invariance of we get that is also a Brownian motion which is obviously independent of . So has the same law as which is by definition.

To show the asymptotics of the covariance it is enough to consider again functionals of the form where , are bounded. As in the proof of Proposition 1 it is enough to show that and that whenever is a sequence such that and .

Using the independence of and we get that

where we used the notation of Corollary 1. By assumption

Then Corollary 1 shows that .

For we can also use Corollary 1 with . ∎

Proof of Corollary 2.

First assume that is square integrable, and for a sequence of partitions of let

Then

since the sequence of function is dominated by and tends to zero everywhere but the diagonal of by Proposition 2. Also by Proposition 2 the expectation does not depend on , hence we have the claim for provided that .

For general , when is integrable, we can use truncation. ∎

4 The zero energy part of the median process

Let be a Brownian motion and suppose that satisfies the following stochastic differential equation

| (4) |

This two parameter process was analyzed in [6] in detail. It was shown that the solution can be viewed as a conditional distribution function, and this justifies the (conditional) quantile name for the process , , and particularly the (conditional) median name for the process .

In [5] it was proved that the quantile process is not a semimartingale, so neither the median process is it. The following decomposition formula holds for (cf. Subsection 5.2 in [5])

This is a process of zero energy, that is, the quadratic variation of exists and . If would have finite total variation, then would be a semimartingale, so should have infinite total variation.

We will refer to the process as the zero energy part of the quantile process. In the following we prove that the local martingale part in the previous decomposition of is a true martingale and we will investigate the following main question: however the total variation of is infinite, and the quadratic variation is identically , is there any for which the -variation of is positive and finite? We are not able to give a mathematically rigorous answer to this latter question, but we formulate some heuristic arguments which are supported by some simulation results.

4.1 Space inverse of a stochastic flow

In this subsection we revise a method for obtaining the space inverse of a stochastic flow (which is given by an Itô diffusion) at a given time point. We will use this in the next subsection (in the proof of the martingale property of the local martingale part of ). We prove only for the case of the unit diffusion coefficient but with suitable transformations this result can be extended.

Let be a Brownian motion and let be a stochastic flow which satisfies the following equation

| (5) |

where is a bounded measurable function. Suppose that on an almost sure event the mapping is continuous and the mappings are homeomorphisms of for all . We now define a process which produces as its terminal value on an almost sure event the space inverse of for a certain . For this we will use the time reversion of the Brownian motion.

For a fixed time horizon let be the time reversed Brownian motion on . Let be the solution of the following equation

| (6) |

Suppose again that on an almost sure event the mapping is continuous and the mappings are homeomorphisms of for all .

Recall the following result from [1] (see also in [2]; a different approach and a generalization of this result can be found in [9] and [10])

Theorem 3.

Consider the following equation

| (7) |

where , is a standard -dimensional Brownian motion and is a bounded Borel function from to .

For almost every Brownian path , there is a unique continuous satisfying (7).

It will be pointed out in the proof of the next proposition the role of this theorem. Applying this result, we know that on an almost sure event there are unique continuous and which satisfy

and

Taking into account all rational and then using the continuity of and , we can conclude that on an almost sure event the mappings and are unique. Then we have the following

Proposition 3.

On an almost sure event, for all and for all we have the following: and .

Especially, we have and , so .

Proof.

We restrict ourselves to . Let . For let be the time reversed process of . Using (5) we obtain

Substituting in place of yields

As , we have obtained that solves the equation (6) of . However, from [11] we know that (6) has a unique strong solution, but it is not obvious that is adapted to the filtration generated by , hence we need the previously cited uniqueness result. It follows that on we have , so .

A similar argument for yields . ∎

4.2 The local martingale part of the quantile process is a true martingale

Now we turn to the case of the quantile process. Using the result of the previous subsection we derive a process which produces a transformed version of as its terminal value. In the following we do not use the exact form of from the equation (4) of , we only use that it is a Lipschitz continuous function with Lipschitz constant , but we also provide the particular results for that special case.

As the first step, to be able to apply Proposition 3, consider the Lamperti transform of , so let be such that , where is a connected component of . In the special case of and we can use . Let . Then evolves as

| (8) |

Let be the solution of

| (9) |

In the special case the equations are

| (8′) |

and

| (9′) |

In order to be able to calculate easily, let be a scale function (or Zvonkin transform, [12]) for . This transform removes the drift, and satisfies

For such a function we have with some , and the transformed process satisfies

| (10) |

In the special case of the quantile process a possible can be , and with this choice

| (10′) |

To calculate , we can use Lemma 16 from [6]. Since

we know that is a Lipschitz continuous function (with the same Lipschitz constant as ), so is differentiable in its space variable, and the space derivative satisfies

From this we obtain that

| (11) |

and this yields the following estimation

where is the Lipschitz constant for .

To be able to apply Proposition 3, we need to guarantee that on an almost sure event and are continuous, and are homeomorphisms of for all and its drifts are bounded. The latter property follows from the Lipschitz continuity of . Moreover, since also is a Lipschitz continuous function, we know that (Theorems 37 and 46 from Chapter V in [7]) the above properties hold for and , and hence hold for and (as they are transformations). So by Proposition 3 we know that almost surely , so

hence

Using these results we can prove that the local martingale part of is a true martingale.

Lemma 3.

If on , then

for every and .

Proof.

Using the previous results we have

hence

∎

Corollary 3.

In the case of and it follows that the local martingale part of the quantile process is a true martingale.

4.3 Simulation framework and results

In this subsection we will restrict ourselves to the case , so is the median process, and with the previous notations we have

| (12) |

In the next we present the simulation framework and the results which supports the following

Conjecture.

With the above notations, for , the stochastic limit of

| (13) |

is positive and finite (where denotes, with simplified indices, a sequence of partitions of which have grid size tending to ).

Instead of the sum in the above conjecture, we investigate the following sum

| (14) |

where is the natural filtration of the Brownian motion . If for the -adic variation (13) tends to in expectation, then so does the conditional version (14), so if the conditional version has a positive and finite limit, then (13) can not tend to . Moreover, in this way the martingale term in the definition of can be eliminated

4.3.1 Calculating the median and calculating the conditional expectation

For calculating the value of the median we can use (12), since for it is enough to calculate (and transform its value). In order to do this, we want to use the discretised version of the equation (10′)

| (15) |

where is an equidistant grid of with mesh size , and are correspondingly rescaled independent Rademacher variables (with expectation and variance , so ). We restrict ourselves to the interval , so . For the calculation of the median we use the sequence for some suitable values of (typically powers of ).

Between the time reversed Brownian motions we have the following relationship: for and , we have

| (16) |

which easily follows from the definition of . Since can be calculated from the increments of in the interval , and is an increment of in , they are independent.

Suppose that we want to calculate the values of the median in two consecutive time points, in and , on the same trajectory (until ). Suppose that we use a sequence for ; in order to calculate , we append one independent rescaled Rademacher variable to the beginning of the sequence , and we calculate along this extended sequence. In this way we can guarantee that we remain on the same trajectory.

Now we describe how to estimate the conditional expectation of . Let and be again two consecutive time points. We want to calculate one realization of on the same trajectory as we did in the case of .

Since for and we have , we obtain that , and from (16) we know that is independent of .

Suppose that is calculated using the sequence . To calculate the conditional expectation along this trajectory, we can do the following. We use the discretised equation (15) of with the same driving sequence , but with different initial values: we approximate the distribution of using a finer grid of (using (15) of course, with independent random increments), and we calculate the values of from these points as initial values. Finally, we take the average of ’s.

4.3.2 One single increment and -variation for some values of

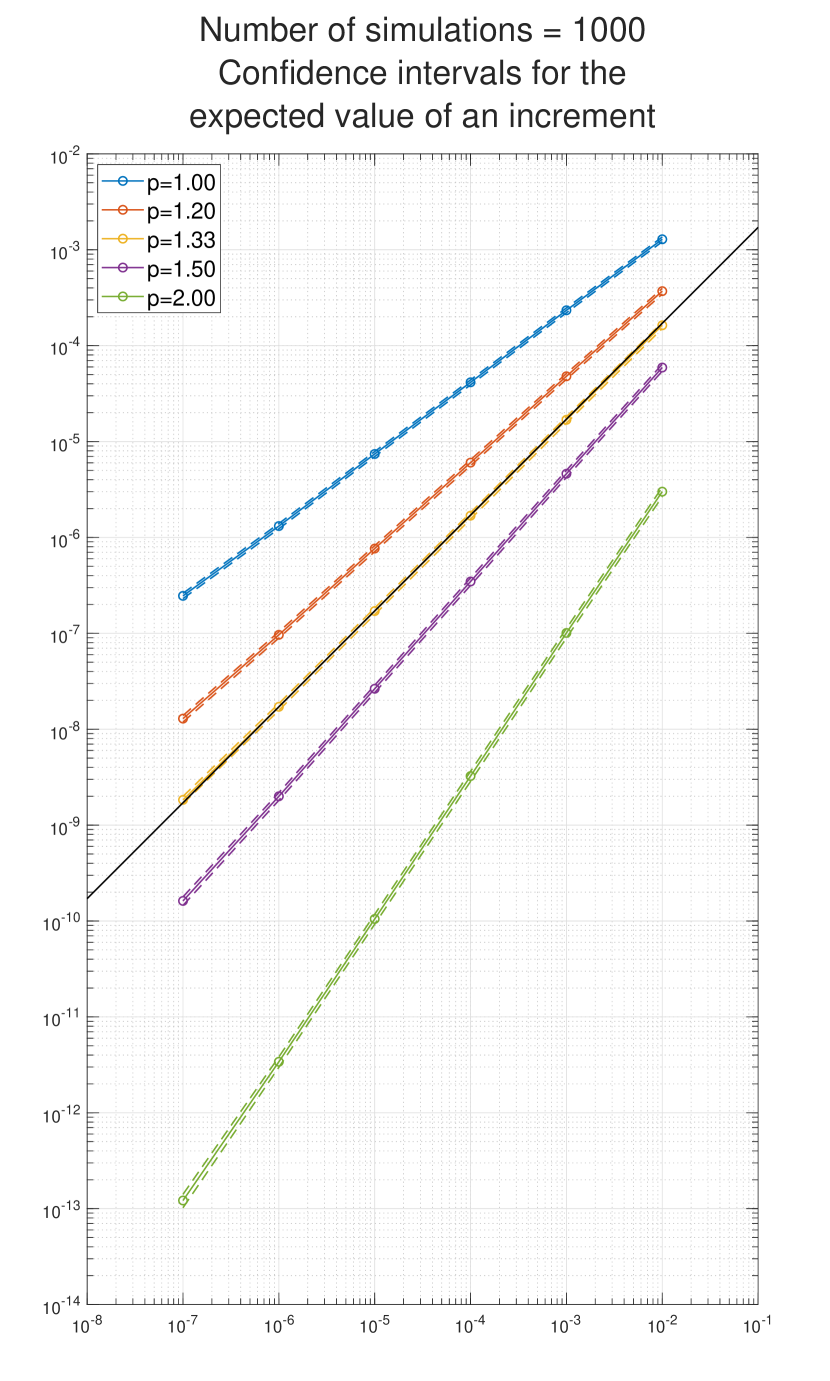

Next we summarize the simulation results. First, we present the results regarding one single increment on the time interval for different values of , so we investigate

The values of range from to . To approximate the values of and we set the grid mesh to ( gridpoints).

We have simulated realizations, and the results can be seen on the figure below. This is a log-log (base ) plot. On the -axis we indicated , while on the -axis we marked the average of the above mentioned increments. Around the mean we can also see the confidence interval of the expected value. We also give the slope and intercept values for the fitted lines, and the sum of squared residuals (SSR).

| p | slope | intercept | SSR |

|---|---|---|---|

| 1.00 | 0.7455 | -1.3994 | 0.0002 |

| 1.20 | 0.8935 | -1.6443 | 0.0002 |

| 1.33 | 0.9920 | -1.8034 | 0.0003 |

| 1.50 | 1.1149 | -1.9980 | 0.0004 |

| 2.00 | 1.4820 | -2.5593 | 0.0008 |

This figure (Figure 1) and the fitted lines (Table 1) suggest the following: there is a linear relationship between the logarithm of and the logarithm of the expected value of one single increment:

By a scaling argument we can suppose that this relationship is valid not only on the interval but also on other intervals. The slope of the thick line is , and is very close to the points which belong to the case . As the number of intervals in with length is roughly , this has the following consequences:

-

1.

for , the sum has a positive and finite limit;

-

2.

for , the above sum is unbounded from above;

-

3.

for , the above sum tends to .

Next, we present some results regarding the -variation processes for different values of . On the figure below (Figure 2) we investigate the behavior of the -variations at time . We have simulated trajectories with different step values (the mesh of the grid ranges from to , which corresponds to gridpoints).

The results are in line with the previous ones. We can observe that in the case of the distributions of the -variation at get more contcentrated around the same value as decreases, while for and they get contcentrated around increasing, respectively decreasing values.

![[Uncaptioned image]](/html/2206.11980/assets/x2.png)

References

- Davie [2007] Davie, A.M., 2007. Uniqueness of solutions of stochastic differential equations. Int. Math. Res. Not. IMRN , 26doi:10.1093/imrn/rnm124, arXiv:0709.4147.

- Flandoli [2011] Flandoli, F., 2011. Regularizing properties of Brownian paths and a result of Davie. Stoch. Dyn. 11, 323–331. URL: https://doi.org/10.1142/S0219493711003310, doi:10.1142/S0219493711003310.

- Föllmer [1981] Föllmer, H., 1981. Dirichlet processes, in: Williams, D. (Ed.), Stochastic Integrals, Springer Berlin Heidelberg, Berlin, Heidelberg. pp. 476–478.

- Maruyama [1970] Maruyama, G., 1970. Infinitely divisible processes. Theory of Probability & Its Applications 15, 1–22. doi:10.1137/1115001.

- Prokaj and Bondici [2022] Prokaj, V., Bondici, L., 2022. On the lack of semimartingale property. Stochastic Processes and their Applications 146, 335–359. doi:10.1016/j.spa.2022.01.009.

- Prokaj et al. [2011] Prokaj, V., Rásonyi, M., Schachermayer, W., 2011. Hiding a constant drift. Annales de l Institut Henri Poincaré Probabilités et Statistiques 47. doi:10.1214/10-AIHP363.

- Protter [2005] Protter, P., 2005. Stochastic Integration and Differential Equations. Stochastic Modelling and Applied Probability, Springer, Berlin, Heidelberg.

- Rogers and Walsh [1991] Rogers, L.C.G., Walsh, J.B., 1991. is not a semimartingale, in: Çinlar, E., Fitzsimmons, P., Williams, R. (Eds.), Seminar on Stochastic Processes, 1990 (Vancouver, BC, 1990). Birkhäuser Boston, Boston, MA. volume 24 of Progr. Probab., pp. 275–283. doi:10.1007/978-1-4684-0562-0_15.

- Shaposhnikov [2016] Shaposhnikov, A.V., 2016. Some remarks on Davie’s uniqueness theorem. Proc. Edinb. Math. Soc. (2) 59, 1019–1035. URL: https://doi.org/10.1017/S0013091515000589, doi:10.1017/S0013091515000589.

- Shaposhnikov [2017] Shaposhnikov, A.V., 2017. Correction to the paper ”some remarks on Davie’s uniqueness theorem” doi:10.48550/arXiv.1703.06598, arXiv:1703.06598v1.

- Veretennikov [1980] Veretennikov, A.J., 1980. Strong solutions and explicit formulas for solutions of stochastic integral equations. Mat. Sb. (N.S.) 111(153), 434–452, 480.

- Zvonkin [1974] Zvonkin, A.K., 1974. A transformation of the phase space of a diffusion process that will remove the drift. Mat. Sb. (N.S.) 93(135), 129–149, 152. doi:10.1070/sm1974v022n01abeh001689.