The maximality principle in singular control with absorption and its applications to the dividend problem

Abstract.

Motivated by a new formulation of the classical dividend problem, we show that Peskir’s maximality principle can be transferred to singular stochastic control problems with 2-dimensional degenerate dynamics and absorption along the diagonal of the state space. We construct an optimal control as a Skorokhod reflection along a moving barrier, where the barrier can be computed analytically as the smallest solution to a certain non-linear ordinary differential equation. Contrarily to the classical 1-dimensional formulation of the dividend problem, our framework produces a non-trivial solution when the firm’s (pre-dividend) equity capital evolves as a geometric Brownian motion. Such solution is also qualitatively different from the one traditionally obtained for the arithmetic Brownian motion.

Key words and phrases:

Singular control with absorption; the maximality principle; the dividend problem; optimal stopping; free boundary problems1. Introduction

The modern formulation of De Finetti’s classical dividend problem [13] is a very popular example of a singular stochastic control (SSC) problem with absorption of the state dynamics. The absorption feature captures the default of a firm whose capital evolves randomly in time and that pays dividends to its share-holders according to a singular control strategy that must be determined via a stochastic optimisation. Another application of SSC with absorption can be found in the literature on optimal resource extraction under stochastic fluctuations. An early contribution in that area is a problem of optimal harvesting of a population formulated and solved by Alvarez and Shepp [2], where the absorption describes the extinction of the population being harvested. The basic idea in this class of problems is that exerting control may endogenously trigger absorption of the state-process, which is generally undesirable. Therefore, when constructing optimal strategies one needs to find a trade-off between exerting control (i.e., paying dividends or harvesting) and keeping a sufficiently high reserve (cash or resources) to withstand future fluctuations in the dynamics.

Mathematically, SSC problems with absorption are harder to study than their counterpart without absorption. This is due to the fact that the absorption feature introduces an inhomogeneity in the state space that translates into additional boundary conditions in the Hamilton-Jacobi-Bellman equation associated to the stochastic control problem. When the underlying dynamics is 1-dimensional, an approach based on an educated guess for the optimal strategy and a verification theorem (so-called guess-and-verify) is generally adopted to obtain solutions in closed-form. In higher dimensions, guessing-and-verifying is not always feasible. However, some two-dimensional stochastic control problems with degenerate dynamics are known to be tractable and produce solutions in closed form (yet not explicit, in general). Notably, in this class of problems we find Markovian stopping problems where the payoff upon stopping depends on the supremum process (cf. [9]). Such considerations motivate our study of SSC with two-dimensional degenerate dynamics and absorption. In this context we develop a solution method that transfers the so-called maximality principle in optimal stopping (Peskir [20]) to SSC.

For the ease of presentation we focus on a variant of the classical dividend problem; extensions beyond this model are possible and they are highlighted in Remark 3.2. A control (or dividend strategy) is a non-decreasing stochastic process that stands for the cumulative amount of dividends paid by a firm to its share-holders over time. Denoting by the firm’s default time, the dividend problem can be stated informally as

| Find that maximizes . |

A common approach in the literature is to use a diffusion approximation for the firm’s net capital. The capital may fluctuate because of gains and losses incurred by the firm over time and the traditional example is that of an insurance company that collects premia at a certain rate and pays claims as and when they occur. In fact, a benchmark in the literature is to model the (post-dividend) equity capital as a Brownian motion with drift subject to a downward push, i.e.,

In this setting the default time is the first time goes below . It has been shown (see Asmussen and Taksar [3], Jeanblanc and Shiryaev [15], Radner and Shepp [22]) that the optimal strategy is of threshold type, i.e., it is optimal to pay the minimal amount of dividends required to ensure that stays below a constant threshold , which can be determined explicitly. The constant coefficient case admits two natural interpretations:

-

(i)

represents the post-dividend equity capital of a company, i.e., the holdings after dividend payments have been deducted according to a strategy (as described above);

or

-

(ii)

an arithmetic Brownian motion models the firm’s pre-dividend equity capital, i.e., the equity capital that the firm would have if no dividends were ever paid out, while is a given dividend strategy. In this case the default time links the two processes via the relationship .

For constant coefficients, the two formulations are equivalent (set ). Instead, when generalising to an underlying process that follows a 1-dimensional diffusion with state-dependent coefficients and , the two settings are truly different: in particular, either the coefficients depend on the post-dividend equity capital, or on the pre-dividend equity capital (or, in a more refined model, on both). In the first case, the process and absorption time are defined as

| (1) |

and

respectively. In the second case instead the pre-dividend equity capital evolves as an uncontrolled process

| (2) |

and

The first formulation (1) is well-suited for problems of resource extraction, where the rate of reproduction depends on the current population size. The problem is one-dimensional in the sense that a sufficient statistics consist of only the current level of . As a consequence, the value function of the problem is characterised by a free-boundary problem in terms of an ordinary differential equation (ODE) (e.g., Shreve, Lehoczky, Gaver [23]). In contrast, the second formulation (2) has a two-dimensional sufficient statistic and the associated free-boundary problem is therefore more involved.

In the current article, we study the two-dimensional formulation (2). From a financial perspective that model assumes that the law of the firm’s (pre-dividend) equity capital at time depends on its own value at time via the coefficients in the stochastic differential equation (SDE) in (2), but it does not depend on the amount of dividends paid to share-holders. However, the actual cash reserve (the post-dividend equity capital) of the firm at any time is given by the difference and, over time, the firm cannot pay out in dividends more than its total (pre-dividend) equity capital.

We find in this paper that the conditions for non-trivial solutions in the two cases (1) and (2) differ considerably. Notably, it is well-known that the standard financial model using a geometric Brownian motion (gBm) is degenerate in the first formulation: if the drift exceeds the discount rate (in the notation of Section 7 below, ), then the value is infinite; if instead the drift is smaller than the discount rate (), then it is optimal to distribute an initial lump sum payment of size that leads to immediate default of the firm (absorption). In contrast, the second formulation gives rise to a non-degenerate problem, the details of which are provided in Section 7 below.

Our main contributions are threefold:

-

(i)

We study a new formulation of the dividend problem. We establish conditions under which its solution is given by a dividend strategy of (stochastic) moving-barrier type and we obtain the barrier level as minimal solution of an associated non-linear ODE. Our formulation covers standard financial models building upon gBm that produce optimal strategies that are qualitatively and quantitatively different from the classical models with arithmetic Brownian motion (see Remark 7.1).

-

(ii)

We show that Peskir’s maximality principle [20] for optimal stopping problems involving the supremum process finds applications in the context of our SSC problems with absorption. Although our results are presented for the dividend problem, the methods and the maximality principle can be adapted to more general situations at the cost of dealing with more involved ODEs for the optimal barrier. That, however, leads to potentially difficult questions about existence of a minimal solution of such ODEs.

-

(iii)

We are able to transfer the maximality principle from optimal stopping to SSC by extending the well-known connection between singular control and optimal stopping (see Bather and Chernoff [6], Baldursson and Karatzas [4], Boetius and Kohlmann [7], Karatzas and Shreve [16]) to the current case of two-dimensional singular control with absorption. The derivative of the value function in the dividend problem with respect to the state variable associated to the process is the value function of an optimal stopping problem for a two-dimensional degenerate diffusion with oblique reflection at the diagonal of the first quadrant in the Cartesian plane. The gain function depends on such dynamics via a state-dependent exponential factor which increases upon each reflection at a ‘rate’ depending (informally) on the ‘local-time’ of the process at the diagonal. We emphasise that the original connection between singular control and optimal stopping (see [6], [4], [7], [16]) has a different structure compared to ours. In those papers, the controlled dynamics does not undergo absorption and, as a result, the optimal stopping problem does not involve reflecting processes and local times. The mathematical arguments that provide the connection in [6], [4], [7], [16] do not apply to our setting as they rest on convexity/concavity of the expected payoff of the SSC problem with respect to the initial value of the controlled state variable. That condition breaks down in our framework because of the additional absorption (default) time . When convexity/concavity are not in place, as in our setting, a connection between SSC and optimal stopping cannot be taken for granted. Indeed, it was shown in De Angelis et al. [12, Sec. 3] that without convexity/concavity the classical connection in the spirit of Bather and Chernoff [6] fails.

The paper is organised as follows. In Section 2 we present a detailed problem formulation, and we state our main result (Theorem 2.1). The theorem derives an optimal dividend strategy transferring the maximality principle from optimal stopping problems to singular control problems with absorption. Section 3 presents the key heuristic ideas that led us to the derivation of the solution of the singular control problem. Sections 4–5 are devoted to the proof of Theorem 2.1. In Section 6 we establish a connection between our SSC problem with absorption and an optimal stopping problem, highlighting the link between the maximality principle and SSC. In Section 7 we apply our main result to solve our version of the dividend problem for gBm.

2. Setting and main results

In this section we first formulate the stochastic control problem and define its value function. Then we introduce a class of solutions of a certain ODE and we associate with it a collection of candidate value functions for the control problem. Finally, we construct suitable admissible controls (via Skorokhod reflection) and we use them to state our main result (Theorem 2.1).

2.1. Problem formulation

Throughout the paper we consider a filtered probability space equipped with a Brownian motion adapted to . The filtration is augmented with -null sets and it is right-continuous. We denote by the unique strong solution on to

| (3) |

where and , are locally Lipschitz continuous functions with at most linear growth on , with for . The process is regular in the sense that it visits each point of in finite time with positive probability (provided ). We further assume that is an absorbing boundary point in case it can be reached in finite time, and that is a natural boundary point so that does not explode in finite time.

For a fixed starting point with , alongside the process we consider the purely controlled dynamics

where is a non-decreasing, right-continuous and -adapted process with . For a fixed process and any initial point with we let

| (4) |

and say that is admissible if, in addition, (notice that this implies a.s.). In other words, the process cannot jump strictly above the process . We then denote the class of admissible controls by

| (5) | ||||

In the problem formulation we find it convenient to use the notations and . For any and an arbitrary , the objective function in our stochastic control problem reads

where the integral is in the Lebesgue-Stieltjes sense, including atoms of the (random) measure at times 0 and . The value function of our problem is then defined as

| (6) |

Remark 2.1.

Problem (6) is a two-dimensional singular stochastic control problem with absorption occurring at the first time the underlying controlled process hits the diagonal . The problem is degenerate since there is no diffusion in the direction of the controlled dynamics .

2.2. A class of solutions for an ODE

For an arbitrary the scale function of reads

| (7) |

The infinitesimal generator of the process killed at a rate is defined by its action on functions as

| (8) |

Denote by and two solutions of the ODE on such that is positive and strictly decreasing and is positive (on ) and strictly increasing with and . These functions can be chosen as the fundamental solutions of (8) and are then unique up to multiplication by a positive constant, if appropriate boundary conditions are imposed at 0 (cf. [8, Chapter II]). It is then known (see e.g. [8]), and also easy to verify using , that for some constant . For simplicity, and with no loss of generality, we assume that constants are chosen so that

Now let

| (9) |

for , with

Notice that for we have

| (10) |

by the strict monotonicity and positivity of and , so the denominator in is well-defined. Next, consider the nonlinear ODE

| (11) |

We do not specify an initial datum for the ODE but instead look at solutions from the class

| (12) |

Notice that as part of the definition of we require that it only contains solutions of (11) that do not explode for finite values of .

Given , the inverse function is well-defined and strictly increasing and when we extend the definition by setting for . Notice that with

We associate with a function defined by and for by

| (15) |

where

| (16) |

Since on then the integrals in the definition of are well-defined for with .

2.3. Solution of the stochastic control problem

We start by stating a lemma for the construction of a suitable class of admissible controls. The proof is standard and we provide it in the Appendix for completeness.

Lemma 2.1.

Let . For an arbitrary , set

| (17) |

Then . Moreover, letting and , the pair solves the Skorokhod reflection problem

| (18) |

for all , -a.s.

We now present the main result of the paper, which is the characterisation of the optimal control in our optimisation problem (6) via the maximality principle.

Theorem 2.1.

The proof of Theorem 2.1 and further properties of the value function are presented in Sections 4 and 5 below.

Remark 2.2.

In Section 5 we specify general conditions under which solutions of (11) in exist and are ordered, so that is the minimal element of as stated in (21). We notice that Peskir [20] works with boundaries that are below the diagonal, so ‘maximal’ in his setting and ‘minimal’ in our setting are equivalent notions.

3. Heuristic derivation of the variational problem

The construction of our solution to the singular control problem via the maximality principle in Theorem 2.1 can be derived from heuristic ideas that we illustrate in this section.

In line with the literature on the dividend problem, it is intuitively clear that control should be exerted when is sufficiently bigger than , so that the risk of bankruptcy remains small. At the same time, waiting is penalised by discounting the future payoff, so that it would not be optimal to wait indefinitely for ever larger values of . In contrast with the classical set-up, where dividend payments affect directly the diffusive dynamics of the firm’s equity capital, here the decision to make a dividend payment should depend on the amount of dividends that have already been paid. So, letting denote the total amount of dividends paid so far, we expect that there should exist a critical value such that no further dividends are paid at times such that .

As long as it is optimal to pay no dividends, the discounted value of the problem should remain constant on average, i.e., should be a martingale for as long as . Moreover, if an amount of control is used at time zero, the resulting payoff is at most and, in general, one has . Dividing by and letting , we expect that if then , because exerting control is strictly sub-optimal (of course assuming that is smooth). On the contrary, we expect that for exerting control be optimal, hence . Finally, it is clear by the problem formulation that if , then , -a.s., and .

The informal discussion above translates into the following free boundary problem: find a pair that satisfies

| (27) |

The first equation corresponds to the martingale property of when . The second equation is the absorption condition, whereas and identify the optimal boundary in terms of the so-called marginal cost of exerting control. Finally, condition relates to the super-martingale property of the value process. Common wisdom on singular control problems with dynamics similar to ours (e.g., [14, 19]) suggests that we should additionally impose a so-called smooth-fit condition at the boundary of the form

| (28) |

First, plugging the boundary condition into of (27) we get

| (29) |

Second, formally differentiating twice with respect to , we get

| (30) |

From (29) and the first equation in (30) we get

Substituting in the second equation of (30) we arrive at

| (31) |

At this point we notice that it is possible to reduce the free boundary problem for to a somewhat easier one for . Such simplification leads us to the particular choice of candidate solutions of the form described in (15) and to the connection with problems of optimal stopping. This can be viewed as the extension of the original ideas in [6] to the current case of two-dimensional degenerate dynamics with absorption. Indeed, setting and differentiating with respect to equation in (27) we obtain a boundary value problem

| (35) |

The condition (28) translates into the classical smooth-fit condition for :

| (36) |

Moreover, the boundary condition (31) on the diagonal translates into a reflection/creation equation

| (37) |

A solution of in (35) must be of the form

by definition of functions and introduced in Section 2. Continuous-fit ( in (35)) gives

and the smooth-fit (36) implies

Solving for and we obtain

| (38) |

where we recall that . The ansatz gives

| (39) |

by simply taking so that . Thus we have obtained exactly the expression of in (15).

Next, we make use of (31) (or equivalently of (37)) to determine the equation for . Computing the derivatives , and directly from (39) and imposing (31) we find that must solve (11) (these calculations are performed below in (49), (50) and (52)). That completes a heuristic derivation of (15) and (11).

It can be checked with tedious but straightforward algebra that if solves (11), then

| (40) |

If in addition to in (35), also a.e., then (40) implies that in (27) is fulfilled. It turns out that the condition can be obtained by defining the function as the value function of a suitable optimal stopping problem for a carefully specified, two-dimensional degenerate diffusion that gives rise to the reflection/creation condition (37) (see Section 6 for details).

Remark 3.1.

Conditions in (27) and a.e. hold simultaneously only if the function solving (11) is non-decreasing. In general (11) could exhibit non-monotonic solutions and the set in (12) could be empty. In that case there seems to be no connection between the derivative of our singular control problem and the value of a stopping problem.

Remark 3.2.

It is clear at this point that an analogous heuristic procedure could be applied to problems with a more general structure of the payoff as, e.g.,

Some changes are required in the free boundary problem in Eq. (27). In particular, in and one has on the right-hand side of the expressions and in one has . Then, making the appropriate changes in the derivation above we can obtain the candidate expression for and the ODE for . Of course, it is a difficult task to determine whether the ODE for the boundary admits a minimal solution that stays above the diagonal and, in general, this should not be expected. Nevertheless, it is an interesting question to find sufficient conditions for the applicability of the maximality principle in such more general setting. We leave it for future study.

4. Proof of Eq. (20) in Theorem 2.1

In this section we prove the first result in Theorem 2.1: for . We thus enforce throughout that the assumptions of the theorem are fulfilled, i.e.,

One may notice that a.s. finiteness of and the integrability condition for are not needed to prove Proposition 4.1. Instead those conditions will be used in the proof of the subsequent Proposition 4.2.

We denote and recall that as in (15).

Proposition 4.1.

We have and the function satisfies

| (46) |

where acts on the second variable in (i) and (v). Moreover, the additional boundary conditions

| (47) |

hold for .

Proof.

Throughout the proof we use the notation as in (16). Conditions and in (46) follow from (15). The continuity of is immediate using -regularity of and of its inverse and recalling that (notice in particular that , which will be used next). For the continuity of take (i.e., ), so that it follows from (15)

| (48) | ||||

where the final equality uses . Since it is easy to check that is continuous separately in the sets and , then (48) also guarantees continuity across the boundary .

Next we prove that (47) holds. We have

| (49) |

and

| (50) |

Then, for we have and for we have . Hence, we conclude that by taking limits in (50) for converging to the boundary (i.e., ) where .

In order to check the second condition in (47) we must compute . Since close to the diagonal , differentiating (49) and then setting we obtain

| (51) | ||||

The latter expression can be substantially simplified by using that

combined with the fact that . Then we get

| (52) |

Putting together (49), (50) and (52) and using that we obtain the second equation in (47).

Since we have already proven that and are continuous in , it remains to show that is also continuous to conclude that . Since it is easy to check that . In order to show that is also continuous across the boundary, we differentiate (48) once more and use the first condition in (47) to get

| (53) |

Since for we have the desired regularity across the boundary.

We next show in (46). By direct calculations on (15) and we obtain for

Comparing with the expressions on the right-hand side of (49), (50) and (51) we obtain

| (54) |

where the final equality is from (47).

We now show that satisfies also in (46). For a fixed , and it solves (in the classical sense)

| (58) |

The claim is thus trivial for . Let us consider . Plugging the second and third equation of (58) into the first one we get

Thus on for some and consequently is increasing on that neighbourhood. Then in due to the second equation in (58). Next, we want to show that

| (59) |

so that we can conclude that

| (60) |

By arbitrariness of , we would then have the desired inequality in .

With as above let

with . For notational simplicity we drop the dependence on in . Arguing by contradiction, assume that so that . At the same time , because on by construction. Plugging the latter two expressions into the first equation of (58) gives

That implies on for some , which is a contradiction with the definition of .

Remark 4.1.

Proposition 4.1 does not use any specific property of other than the fact that . Therefore, all the results in that proposition continue to hold for any associated to (with replaced by everywhere).

Proposition 4.2.

We have on .

Proof.

Fix , let be an arbitrary control and denote

where

is a local martingale. Set and apply Itô’s formula to get

where denotes the continuous part of . Now, using that and on , and that

we have

| (61) |

Taking expectation and using that we arrive at

Now, letting and then we obtain

by monotone convergence. Since was arbitrary, it follows that .

For the other inequality, let and recall and from Theorem 2.1. Set

Apply the same arguments as above to arrive at

since is continuous for . By construction is bound to evolve in the set by Lemma 2.1, so we have that , for all -a.s. by Proposition 4.1. Taking also expectations in the expression above and re-arranging terms we arrive at

where we used the fact that since only increases when by (18). The function is decreasing thanks to in (46). So, thanks to the integrability condition (19), letting and go to infinity and using that , -a.s. we obtain

Since we already have the reverse inequality , the claim and the optimality of follow. ∎

5. The maximality principle

In this section we prove (21) in Theorem 2.1. In particular, solutions of (11) are ordered, and we show that a large gives a large . This leads to the characterisation of in Theorem 2.1 as the minimal element of and, consequently, the only one for which (19) holds (notice that is the maximal inverse of an element of ).

First note that we have existence and uniqueness up to a possible explosion of the solution to (11) for any initial point in the interior of . Indeed, since and are locally Lipschitz continuous on , one finds that

-

•

the map is continuous for all ;

-

•

is locally Lipschitz on .

Thus a unique solution of (11) can be constructed by standard Picard-Lindelöf type of arguments. Clearly this does not guarantee , for which we will show sufficient conditions in Proposition 5.2. Since is not defined on the diagonal, due to , then solutions of (11) may approach the diagonal with an infinite slope. More precisely, let , and consider an initial point with . Then, for any , there exists a unique solution of (11), with , on the interval , where

| (62) |

Moreover, the solution can be extended continuously to , with . Furthermore, for , two solutions with initial points and , respectively, satisfy .

In order to properly define the minimal element of , for let us denote by a solution of (11) such that . It is convenient to introduce the set of initial values for which . That is, for a fixed we let

| (63) |

Then, for any in we must have by uniqueness of the solution. We will say that solutions are ordered and we refer to ‘larger’ or ‘smaller’ solution as appropriate.

Proposition 5.1.

Fix and assume that belong to so that satisfy . Then, on .

Proof.

Let us start by recalling that all the results in Proposition 4.1 also hold for and provided that we replace therein by and , respectively (see Remark 4.1). In particular, and by (46). Moreover, arguing as in the proof of of Eq. (46) we can analogously show that

| (64) |

That implies, in particular,

which will be used in the next part of the proof.

Next we prove that . To simplify notation we set , for . It is sufficient to prove

| (65) |

with strict inequality at the diagonal, so that for each and all we have

where we also use that by (15). As in (58), for a fixed and for , we have by construction that and it solves

| (69) |

Since , then we have for and for (we adopt the convention that if ). Now, for we have , so (65) holds with equality in that set. Instead, we have

| (70) |

and (65) holds with strict inequality.

It remains to prove that such strict inequality also holds on . This is equivalent to proving it on for each given and fixed. Set . Then by (70) evaluated at the boundary . Moreover by the third equation in (69) applied to , and (64) applied to (along with the fact that ). Thus, there is such that on and, setting

we must have . Indeed for . In particular, at it holds , where the strict inequality is by which holds because on . This leads to a contradiction, since should be a minimum of . Hence, on , as needed. ∎

Corollary 5.1 (Uniqueness and minimality).

Proof.

Assume by way of contradiction that there are and in that satisfy the integrability conditions (19). Then, with no loss of generality but , which contradicts Proposition 5.1. As for the minimality of , assume that there is with and satisfies the integrability conditions in (19). Then, by Proposition 5.1, so that satisfies the second condition in (19). Moreover, by construction for all , -a.s. Hence, , -a.s. and also the first condition in (19) holds for . Thus, we reach again a contradiction as would satisfy (19) and it would be . ∎

We now address the question of whether is non-empty. We first have the following lemma.

Lemma 5.1.

For any sequence with such that as we have as .

Proof.

First observe that as , letting we have the asymptotic expansion

Likewise, for the first term in the square brackets in the definition of we have (see (9))

where the final expression follows from the fact that both and solve the ODE . So for the first term in (9) we have

| (71) |

For the second term inside the square brackets in (9) we have

so the desired result follows easily since as and . ∎

For let

and note that by Lemma 5.1. For , denote by the solution of (11) with initial point . Let us also recall that is the smallest for which touches the diagonal (see (62)). We can now provide easy sufficient conditions under which , its minimal element exists and the map is strictly increasing.

Proposition 5.2.

Assume that , for all , and

| (72) |

Then, is strictly increasing and is increasing on and decreasing on . Moreover,

is the minimal element in .

Proof.

Let us fix and simplify the notation for this initial part of the proof by setting . First we show that is the unique stationary point of on and that it is a global maximum.

Assume there exists such that so that (a priori and potentially ). Then by Lemma 5.1 and, by (9), we have

| (73) |

Differentiating (11) we obtain

so that

| (74) |

Recalling the expression for in (9) and performing straightforward calculations we obtain

Evaluating the above at we see that the first term vanishes. We can evaluate the second term substituting and therein with

which are due to . Rearranging terms and using also (73) we thus obtain

with defined as in (72). Since and on and (see (10)), we can conclude .

This means that any stationary point of on must be a maximum. Hence, there can only be one stationary point on and therefore it must coincide with , where . So, is strictly increasing on and strictly decreasing on (with in both intervals). Thus for , because if it were for some then it would be in a right-neighbourhood of , which contradicts that is strictly increasing there. Analogously, it must be for .

Notice also that by definition of and, by the same calculations as above, . Since , it follows that is strictly increasing. Moreover, noticing that for all the limit exists and it is infinite.

Clearly is also increasing (for each and any ) by uniqueness of the solution to (11) and the construction above. Hence

is well-defined, and it satisfies the ODE (11). By construction since for all , which implies for all . Moreover, it is also the minimal element of because for any it must be for all and any . ∎

Let as in Proposition 5.2 and and as in Lemma 2.1. Take as in (15) and recall Corollary 5.1. Then the next result follows.

Corollary 5.2.

Remark 5.1.

Proposition 5.2 above gives conditions under which is non-empty and allows to construct its minimal element . Corollary 5.2 then says that if such minimal element satisfies the integrability conditions as in Theorem 2.1 then and it is the optimal boundary. While we do not know of general conditions under which the integrability conditions for are satisfied, the following observation can be useful in certain situations.

Assume that two sets of model specifications and are given, and assume that and for . Further assume that satisfies the integrability conditions for the first set of parameters so that reflection along is optimal. Construct by setting for , and by solving (11) for with boundary condition . Then is optimal for .

6. An optimal stopping problem with oblique reflection

The link between Peskir’s maximality principle and our singular control problem passes through a special connection between problems of singular stochastic control with absorption and optimal stopping problems for reflecting diffusions with discounting at the ‘rate’ of local time (see, e.g., [10] and [11]).

Letting , with as in Theorem 2.1, and using the explicit expression (15) we obtain

| (79) |

Notice that all but the final equation above can also be obtained by simply differentiating (46) with respect to . Moreover, the boundary condition in (47) reads

| (80) |

Since for by definition of and (60), we see that appears to be the value function of an optimal stopping problem whose underlying process has a peculiar behaviour along the diagonal due to (80).

First we construct the process , then we state the optimal stopping problem and finally we make a precise claim on the connection between and . For , let be defined by the system

| (81) |

where is a continuous and increasing process and all equations hold -a.s. The pair is the solution of a two-dimensional degenerate reflecting SDE, with reflection occurring at the diagonal but in the direction . The next lemma states that such a process is uniquely determined. We postpone its proof to the appendix so that we instead can continue with the construction of our optimal stopping problem.

Lemma 6.1.

There exists a pathwise unique -adapted solution to (81). Moreover, the process is strong Markov.

Let us define the process

and the optimal stopping problem with value

| (82) |

where the supremum is taken over -a.s. finite -stopping times. In essence, (82) is an optimal stopping problem for the reflected strong Markov process , which pays for immediate stopping and which gains value when the process is reflected in the diagonal . The next result confirms that .

Theorem 6.1.

Proof.

The proof consists of a standard verification argument. Set and denote and .

Thanks to the regularity of in Proposition 4.1 we know that . Then, from and in (79) we also obtain that is locally bounded on and it is continuous separately in the sets and , because

and on . (Notice that is not continuous across the boundary.)

For any initial points we can apply the change-of-variable formula derived in [1] to . In particular, for any stopping time we obtain

| (84) | ||||

where is the local martingale

and

is the usual localising sequence. Now we recall the minimality condition in the final line of (81) that guarantees

Plugging this into (84) and recalling also (80), we see that the integral in vanishes. Then, taking expectations and rearranging terms we have

where the first inequality comes from in (79) (notice that is constant off the diagonal and admits a transition density with respect to the Lebesgue measure) and the second one from . Using Fatou’s lemma, we can take limits inside the expectation, as and . Thus, by arbitrariness of the stopping time we have

| (85) |

7. The Case of Geometric Brownian motion

In this section we consider the case when is a geometric Brownian motion, i.e. we assume that and where and are positive constants so that

To ensure the integrability condition (19), we further assume that . Notice that condition (72) in Proposition 5.2 holds.

The fundamental solutions of the equation are given by and , where are solutions of the quadratic equation

The function is given by

so is constant along rays , . Thus , and the function is independent of the choice of .

Lemma 7.1.

The function is strictly increasing, with . Moreover, for

and for

Furthermore, is negative on and positive on .

Proof.

The claims that , and are straightforward to verify. For the last claim, note that the function

is strictly increasing since and satisfies . Consequently, is negative on and positive on , and so is also because for all . ∎

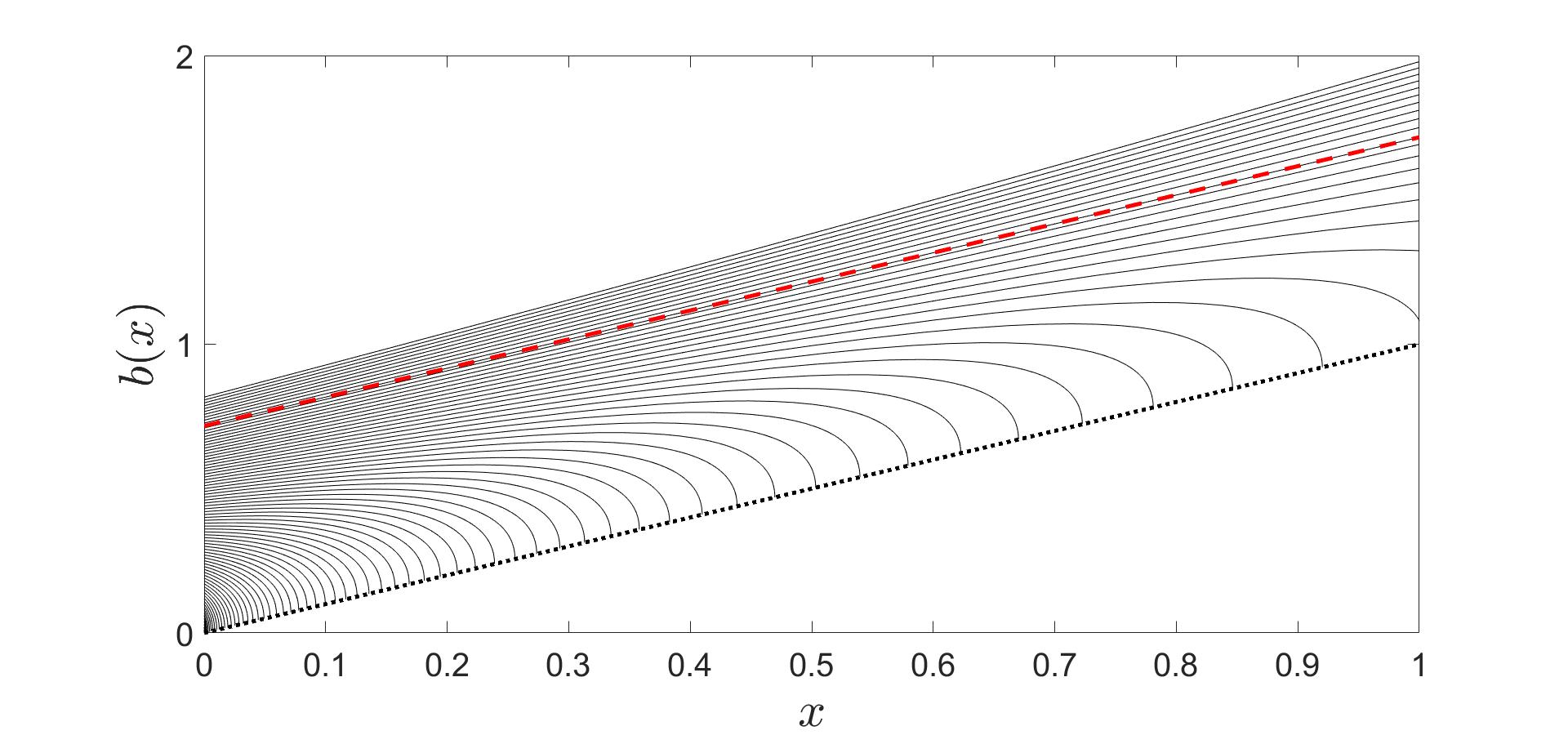

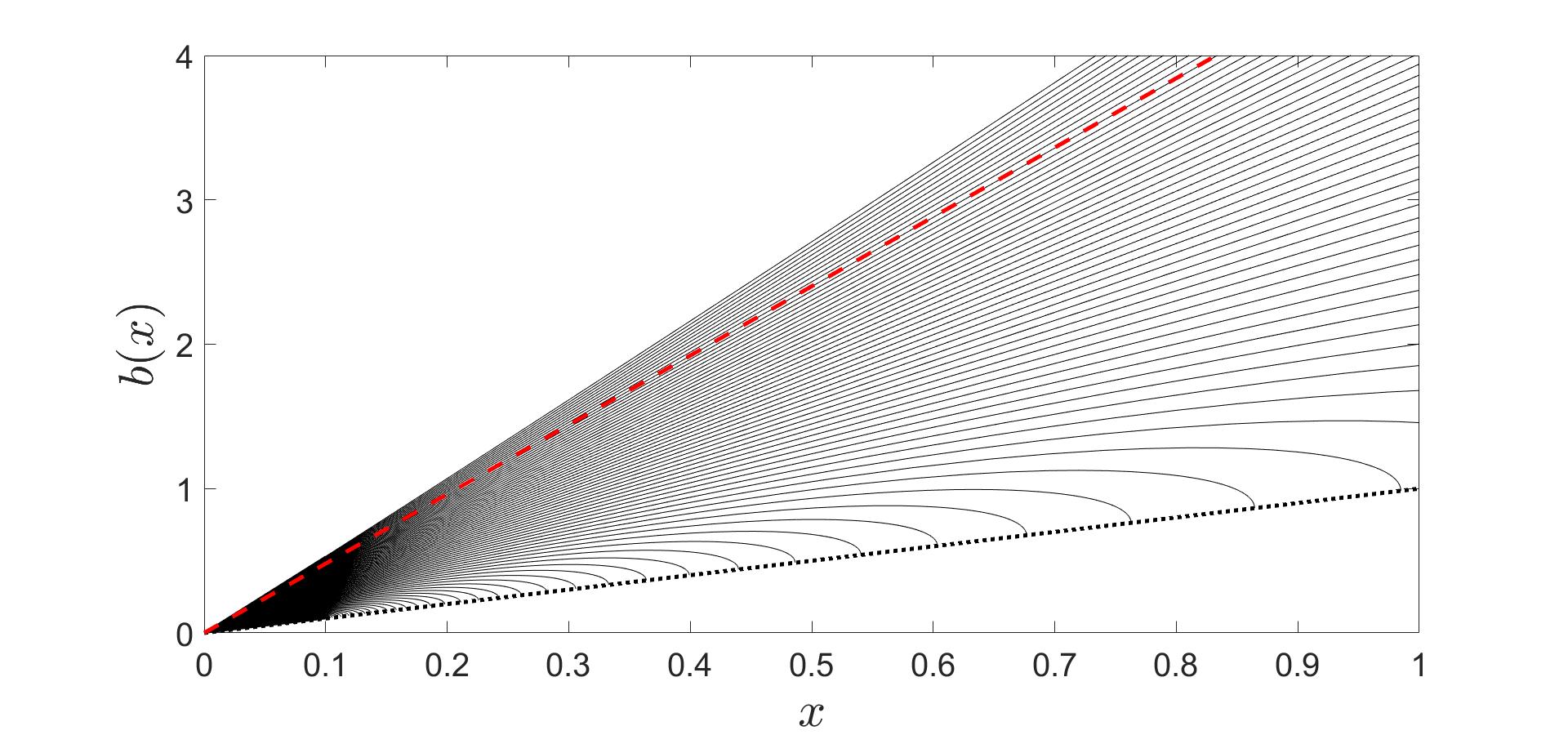

Solutions of the ODE (11) In this setting, the optimal dividend strategy is described by an affine boundary (dashed line).

It follows from Lemma 7.1 that one solution of the ODE

| (86) |

for the boundary is given by . Since , we have . Moreover, if is another solution with , then by Lemma 7.1, so

at all points since . Consequently, any such is concave and, in the next paragraph, we will use such concavity to show that is the smallest solution that stays above the diagonal (Figure 2).

Assume that satisfies and for . First note that if for some , then for , so would not stay above the diagonal. Therefore we must have that for all . By concavity, it then has an asymptote as , say for some constants and , with . However, then

as . Since the last inequality is strict if , we must have , and then also for the inequality to hold. This shows that , so is the smallest element of .

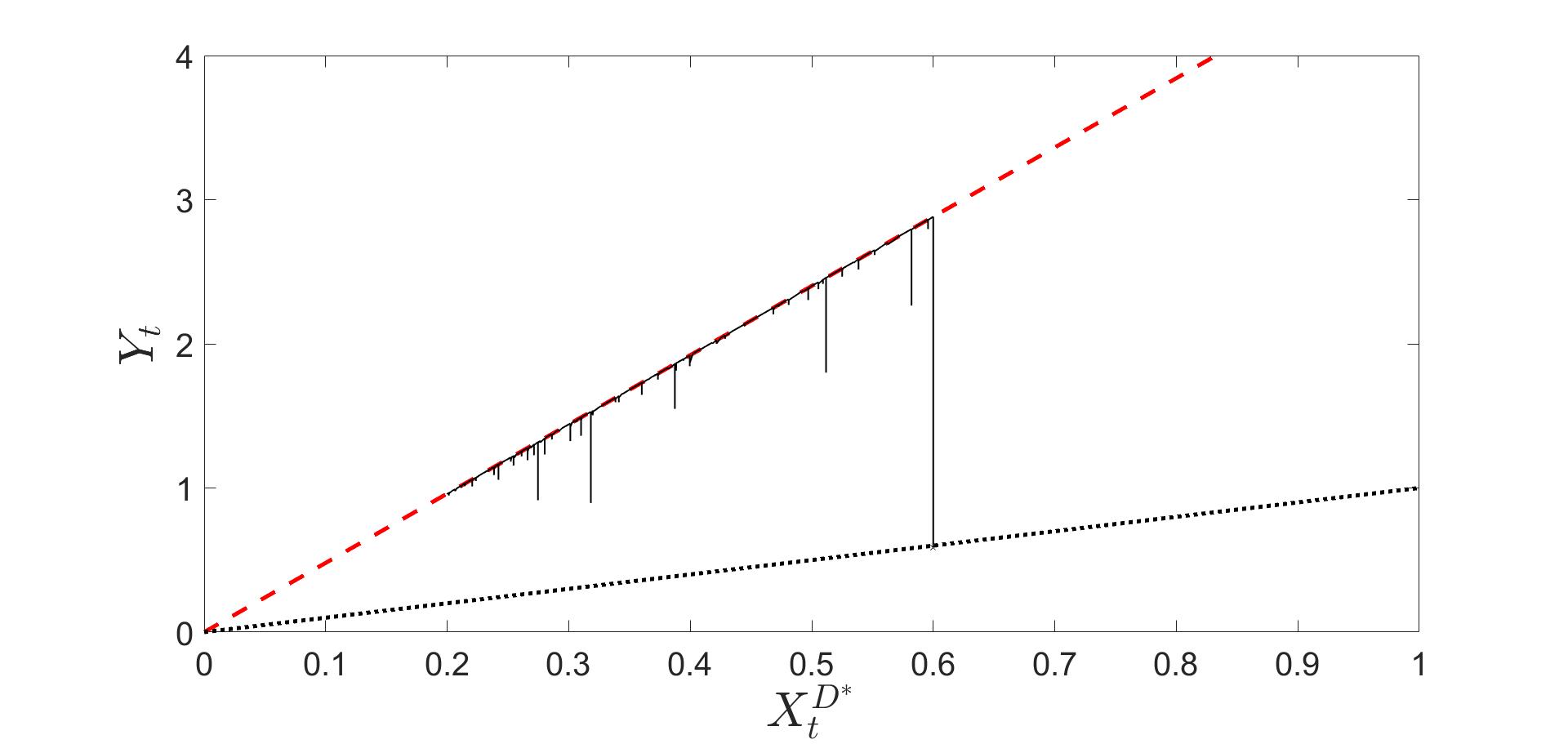

The maximality principle thus suggests that the optimal dividend boundary is given by , where is as above. Consequently, , where is the maximum process. Clearly, , -a.s. Moreover,

and in particular, for some constant . Consequently,

since is a geometric Brownian motion with (strictly) negative drift.

It follows that the conditions of Theorem 2.1 are fulfilled, so an optimal dividend boundary is given by the straight line . More specifically, the dividend strategy

is optimal in (6). For an illustration of the optimally controlled path , see Figure 3.

Remark 7.1.

The structure of the optimal strategy we found here is different from the classical example with arithmetic Brownian motion studied in, e.g., [3, 15, 22]. In that case dividends are paid optimally when the distance between the pre-dividend equity capital, , and the total amount of dividends already paid out, , is equal to a fixed constant (the optimal boundary), i.e., when . So, in that case, the optimal distance between and is constant throughout the optimisation. In our problem formulation instead, the decision to pay dividends is determined based on a constant ratio between the process and the process . That is, dividends are paid out when . This scaling may be only partially read out of the logarithmic transformation that links geometric and arithmetic Brownian motion. Indeed, for the state variables and we retrieve the optimality condition

and the absorption condition . However, the logarithmic transformation of the expected payoff leads to

where we notice that in the first expression and, for simplicity, we take with continuous trajectories in the change of variable formula. Therefore, after the logarithmic transformation the objective function is not the usual one from the classical dividend problem with arithmetic Brownian motion.

Appendix

Proof of Lemma 2.1

Since then is strictly increasing and continuous. Then the process is by definition continuous for and it has a single jump at time zero if . Moreover it is -adapted and non-decreasing and by continuity of paths on . Therefore .

In order to prove that solves the Skorokhod reflection problem we start by observing that, by construction,

Fix and consider such that . Then by definition of we have

Therefore, by continuity of there exists such that for all , which implies as needed.

Proof of Lemma 6.1

We first prove uniqueness. Recall that we have locally Lipschitz coefficients with linear growth. In the notation of Bass [5, Sec. 12] we have , and . Then, [5, Thm. 12.4] (see also the remark after the theorem) yields uniqueness and the strong Markov property of for and any . Linear growth of the coefficients implies a.s. as . Then we can obtain global uniqueness of a strong Markov solution by a standard limiting argument.

The proof of existence in Bass [5] is given under an assumption of non-degeneracy of the reflecting diffusion which clearly fails in our case. For more general results Bass points to the classical paper by Lions and Sznitman [18]. Thanks to the special setting of our problem we can produce a simpler proof, which we include for completeness.

The main idea is to reduce the reflection problem to a classical problem for a reflecting Brownian motion. This can be achieved by a transformation via the scale function and a time-change. While this line of argument is canonical in the theory of one-dimensional diffusions, we believe the full proof might be difficult to find in the literature, hence we provide it here.

Let be the scale function associated to the coefficients in the SDE for (see (7)). Then, letting and and denoting and , the dynamics of these two processes read

where and

using that is supported on . Notice in particular that since is one-to-one, then (81) admits an -adapted solution if and only if the problem

| (87) |

admits one. Notice also that by construction.

The next step removes the diffusion coefficient by a canonical time change. Indeed, the process

is a continuous (local) martingale with quadratic variation

Since for , then we have for and the process is strictly increasing. Letting be the continuous inverse of we have that defines a continuous martingale with quadratic variation , hence is a Brownian motion for the time-changed filtration [17, Thm. 3.3.16]. Now, set , and . Then

where the final equality holds by a simple change of variable, and (87) admits an -adapted solution if and only if the problem below admits an -adapted one:

| (88) |

Finally, letting and we have that (88) admits an -adapted solution if and only if

| (89) |

The latter is just the classical Skorokhod reflection problem, whose solution is constructed explicitly by taking

References

- [1] Alsmeyer, G. and Jaeger, M. A useful extension of Itô’s formula with applications to optimal stopping. Acta Math. Sin., 21 (2005), no. 4, 779-786.

- [2] Alvarez, L. and Shepp, L. Optimal harvesting of stochastically fluctuating populations. J. Math. Biol., 37 (1998), no. 2, 155-177.

- [3] Asmussen, S. and Taksar, M. Controlled diffusion models for optimal dividend pay-out. Insurance Math. Econom., 20 (1997), no. 1, 1-15.

- [4] Baldursson, F., Karatzas, I. Irreversible investment and industry equilibrium. Finance Stoch., 1 (1996), 69-89.

- [5] Bass, R.F. Diffusions and elliptic operators. Probability and its Applications. Springer-Verlag, New York, 1998.

- [6] Bather, J. and Chernoff, H. Sequential decisions in the control of a spaceship, in Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability (Berkeley, California, 1965/66), Vol. III: Physical Sciences, University of California Press, Berkeley, CA, 1967, pp. 181-207.

- [7] Boetius, F. and Kohlmann, M. Connections between optimal stopping and singular stochastic control. Stochastic Process. Appl., 77 (1998), no. 2, 253-281.

- [8] Borodin, A. and Salminen, P. Handbook of Brownian motion – facts and formulae. Second edition. Probability and its Applications. Birkhäuser Verlag, Basel, 2002.

- [9] Dubins, L., Shepp, L. and Shiryaev, A. Optimal stopping rules and maximal inequalities for Bessel processes. Teor. Veroyatnost. i Primenen. 38 (1993), no. 2, 288-330; translation in Theory Probab. Appl. 38 (1993), no. 2, 226-261.

- [10] De Angelis, T. Optimal dividends with partial information and stopping of a degenerate reflecting diffusion. Finance Stoch., 24 (2020), no. 1, 71-123.

- [11] De Angelis, T. and Ekström, E. The dividend problem with a finite horizon. Ann. Appl. Probab., 27 (2017), no. 6, 3525-3546.

- [12] De Angelis, T. Ferrari, G. and Moriarty, J. A nonconvex singular stochastic control problem and its related optimal stopping boundaries. SIAM J. Control. Optim., 53 (2015), no. 3, 1199-1223.

- [13] De Finetti, B. Su un’impostazione alternativa dell teoria colletiva del rischio. Transactions of the 15th International Congress of Actuaries 2 (1957), 433-443.

- [14] Guo, X. and Tomecek, P. Connections between singular control and optimal switching. SIAM J. Control Optim., 47 (2008), no. 1, 421-443.

- [15] Jeanblanc-Picque, M. and Shiryaev, A.N., Optimization of the flow of dividends, Russian Math. Surveys, 50 (1995), 257-277.

- [16] Karatzas, I. and Shreve, S. Connections between optimal stopping and singular stochastic control. I. Monotone follower problems. SIAM J. Control Optim., 22 (1984), no. 6, 856-877.

- [17] Karatzas, I. and Shreve, S. Brownian motion and stochastic calculus. Springer-Verlag, New York, 1988.

- [18] Lions, P.L. and Sznitman, A.S. Stochastic differential equations with reflecting boundary conditions. Comm. Pure Appl. Math., 37 (1984), 511-537.

- [19] Merhi, A. and Zervos, M. A model for reversible investment capacity expansion. SIAM J. Control Optim., 46 (2007), no. 3, 839-876.

- [20] Peskir, G. Optimal stopping of the maximum process: The maximality principle. Ann. Probab., 26 (1998), no. 4, 1614-1640.

- [21] Peskir, G. and Shiryaev, A. Optimal stopping and free-boundary problems. Lectures in Mathematics ETH Zürich. Birkhäuser Verlag, Basel, 2006.

- [22] Radner, R. and Shepp, L. Risk vs. profit potential: A model for corporate strategy. J. Econom. Dynam. Control 20 (1996), no. 8, 1373-1393.

- [23] Shreve, S., Lehoczky, J. and Gaver, D. Optimal consumption for general diffusions with absorbing and reflecting barriers. SIAM J. Control Optim. 22 (1984), no. 1, 55-75.