Fast calibration of weak FARIMA models

Abstract

In this paper, we investigate the asymptotic properties of Le Cam’s one-step estimator for weak Fractionally AutoRegressive Integrated Moving-Average (FARIMA) models. For these models, noises are uncorrelated but neither necessarily independent nor martingale differences errors. We show under some regularity assumptions that the one-step estimator is strongly consistent and asymptotically normal with the same asymptotic variance as the least squares estimator. We show through simulations that the proposed estimator reduces computational time compared with the least squares estimator. An application for providing remotely computed indicators for time series is proposed.

keywords:

[class=AMS]keywords:

Weak FARIMA models; Le Cam’s one-step estimator; Least squares estimator; Consistency; Asymptotic NormalitySamir.BenHariz@univ-lemans.fr

Alexandre.Brouste@univ-lemans.fr

Youssef.Esstafa@univ-lemans.fr

marius.soltane@utc.fr

1 Introduction

Time series often exhibit linear and/or nonlinear dependence. When large correlations for small lags are detected, short memory processes can suffice to model the dependence structure of the series. The ARMA processes (see for example Box and Jenkins, [1970] and Francq and Zakoïan, [1998]) or VARMA for the multivariate framework (see Lütkepohl, [2007] and Boubacar Maïnassara, [2009]) are examples of short memory processes.

However, in many scientific disciplines and many applied fields, including hydrology, climatology, economics, finance and computer science, the autocorrelations of some time series decrease very slowly. This phenomenon may be due to several factors, in particular nonstationarity and/or long-range dependence.

A large audience of mathematicians has been attracted by long memory processes and their various applications (see for instance Mandelbrot, [1965], Mandelbrot and Van Ness, [1968] and Mandelbrot and Wallis, 1969a , Mandelbrot and Wallis, 1969b , Mandelbrot and Wallis, 1969c ), Granger in economics (Granger and Joyeux, [1980]), Dobrushin in physics (Dobrushin and Major, [1979]) and, even earlier, Hurst in hydrology (Hurst, [1951]). Long-range dependent processes constitute currently one of the popular areas of statistical research and occupy a central place in the time series literature (see Granger and Joyeux, [1980], Hosking, [1981], Fox and Taqqu, [1986], Dahlhaus, [1989], Palma, [2007], Beran et al., [2013], Boubacar Maïnassara et al., 2021b , among others).

The fractional autoregressive integrated moving-average (FARIMA, for short) model is widely used to model the long memory phenomenon. This model was first introduced by Granger and Joyeux, [1980] and then generalized to take into account short-term fluctuations in time series by Hosking, [1981]. FARIMA models therefore have the advantage of jointly modeling the long memory behavior of time series and their short-term dynamics through a fractional integration parameter and autoregressive and moving-average parameters respectively. Their fame is partly due to their structure similar to the one of standard ARIMA models in which the differentiation exponent is an integer. FARIMA models are generally used with strong assumptions on the noise that limit their generality. We call strong FARIMA the standard models in which the error term is assumed to be an independent and identically distributed sequence (iid for short), and we speak about weak FARIMA models when the errors are uncorrelated but neither necessarily independent nor martingale differences. It is common in the time series literature to talk about the subclass of semi-strong FARIMA models when the associated innovation process is a semi-strong white noise, that is a stationary martingale difference. An example of semi-strong white noise is the generalized autoregressive conditional heteroscedastic (GARCH) model (see Francq and Zakoïan, [2010]). The distinction between strong, semi-strong or weak FARIMA models is therefore only a matter of noise assumptions with the following inclusions:

The independence of the noise in strong FARIMA models is often considered to be very restrictive for many time series with general nonlinear dependencies111See for instance Tong, [1990], Francq and Zakoïan, [1998], Francq et al., [2005], Bauwens et al., [2006], Fan and Yao, [2008], Francq and Zakoïan, [2010], Boubacar Maïnassara, [2011], Boubacar Maïnassara and Francq, [2011], Shao, [2011], Boubacar Maïnassara et al., [2012], Shao, [2012], Boubacar Maïnassara, [2014] and Boubacar Maïnassara and Saussereau, [2018] for some references on nonlinear time series models.. Weak FARIMA models correct this problem by allowing the noise to contain very general nonlinear dependencies of often unidentified structures. They therefore have the great advantage of providing linear modeling to nonlinear processes.

The asymptotic theory of estimation is mainly limited to strong and semi-strong FARIMA models. Whittle’s estimator (see Whittle, [1953]) is commonly used to estimate the parameters of FARIMA models (see for example Fox and Taqqu, [1986], Dahlhaus, [1989], Giraitis and Surgailis, [1990] and Taqqu and Teverovsky, [1997]).

The study of the asymptotic properties of this estimator is developed in the case where the errors are assumed to be independent and identically distributed and in the framework where the noise is considered to be a martingale difference (see Beran, [1995], Baillie et al., [1996], Ling and Li, [1997], Hauser and Kunst, [1998], Palma, [2007], Beran et al., [2013], among others). All this work is limited to the case where the nonlinear dependency is absent or with a well-identified structure. For example, in financial time series modeling, in order to capture conditional heteroscedasticity, it is common that innovations in FARIMA models are assumed to have a GARCH structure (see for example Baillie et al., [1996], Hauser and Kunst, [1998]).

For weak FARIMA models, the asymptotic normality has been obtained for Whittle’s estimator (Shao, [2012, 2010]) and the LSE (Boubacar Maïnassara et al., 2021b ). In this paper, we propose a new calibration of weak FARIMA models based on Le Cam’s one-step approach (see Le Cam, [1956]). In Le Cam’s one-step procedure, an initial guess estimator is corrected by a single step of Newton gradient descent method on loglikelihood function. We adapt in this work the Le Cam one-step procedure. Firstly, we propose the LSE on subsample as an initial estimator. Secondly, since we do not specify the distribution of the weak white noise, the single Newton step is done on the least squares functional. This estimator greatly reduces the computation time and preserves the same asymptotic properties as the LSE. One-step procedure has shown its efficiency in terms of computation time and precision for diffusion processes Kamatani and Uchida, [2015], Gloter and Yoshida, [2021], ergodic Markov chains Kutoyants and Motrunich, [2016], fractional Gaussian noise observed at high frequency Brouste et al., [2020] or stable noise Brouste and Masuda, [2018] and inhomogeneous Poisson processes Dabye et al., [2018].

The paper is organized as follows. In Section 2, we introduce the model and the notations used in the sequel and we give the asymptotic properties of Le Cam’s one-step estimator of the parameters of weak FARIMA models. In Section 3, we provide some numerical illustrations to show the performance of the proposed estimator on finite sample sizes. All the technical proofs are gathered in Section 4.

2 Le Cam’s one-step estimation of weak FARIMA models

In this section we present the parametrization that is used in the sequel and we study the asymptotic properties of the Le Cam one-step estimator of long memory FARIMA processes induced by uncorrelated but not independent error terms. We also recall the results on the asymptotic behavior of the least squares estimator of weak FARIMA models obtained by Boubacar Maïnassara et al., 2021b . This estimator will be used as the initial estimator in Le Cam’s one-step procedure.

2.1 Statement of the problem and notations

Let be a long memory second-order stationary process satisfying a weak FARIMA representation of the form

| (1) |

where is the long memory parameter, is a sequence of uncorrelated random variables defined on some probability space with zero mean and common variance , stands for the back-shift operator and , respectively , is the autoregressive, respectively the moving-average, operator. These operators represent the short memory part of the model and are supposed to have all their roots outside the unit disk with no zero in common to ensure the invertibility of the model and the unique identifiability of the parameters.

The fractional difference operator is defined, using the generalized binomial series, by

where for all , and is the Gamma function. It can be readily shown, see for example Beran et al., [2013], that for large , . It is therefore clear that the fractional difference operator impacts the speed of convergence to 0 of the coefficients in the AR() and MA() representations of Model (1) compared with standard short-memory ARMA models where this operator is absent. This loss of speed, compared to the exponential one of ARMA models, implies that the series of autocovariances of the process defined in (1) is not absolutely summable.

Let be the parameter space

Denote by the Cartesian product . Note that the unknown parameter of interest belongs to the parameter space .

For all , we define as the second-order stationary process which is the solution of

| (2) |

Observe that, for all , a.s. Given a realization of length , can be approximated, for , by defined recursively by

| (3) |

with if .

As shown in Proposition 2 (see Section 4), these initial values are asymptotically

negligible and in particular it holds that

almost-surely as uniformly in .

Thus the choice of the initial values has no influence on the asymptotic properties of the model parameters estimator.

Let denote the compact set

We define the set as the Cartesian product , where is a positive constant chosen such that belongs to and where .

For and , consider the function

| (4) |

where is given in (3). The Le Cam one-step estimator is defined, almost-surely, by

| (5) |

where is the least squares estimator of parameter calculated over the first , with , observations , i.e.

2.2 Asymptotic properties

The asymptotic properties of the least squares estimator of the parameters of weak FARIMA models have been established by Boubacar Maïnassara et al., 2021b . The authors have showed, under some regularity assumptions on the noise, the consistency and the asymptotic normality of the least squares estimator. In this subsection, we study the asymptotic behavior of the Le Cam one-step estimator . We show, under the same assumptions, that the estimator converges not only in probability but almost-surely to the true parameter and also satisfies a central limit theorem with a similar limit variance.

To ensure the strong consistency of the Le Cam one-step estimator , we assume that the innovation process in (1) satisfies the following condition:

-

(A1):

The process is strictly stationary and ergodic.

Our first main result is stated in the following theorem.

Theorem 1.

The proof of this theorem is given in Section 4.

For the asymptotic normality of the Le Cam one-step estimator, additional assumptions are required. It is necessary to assume

that is not on the boundary of the parameter space

.

-

(A2):

We have , where denotes the interior of .

The stationary process is not supposed to be an independent sequence. So one needs to control its dependency by means of its strong mixing coefficients defined by

where and .

We shall need an integrability assumption on the moments of the noise and a summability condition on the strong mixing coefficients .

-

(A3):

There exists an integer such that for some , we have and for .

In order to state our asymptotic normality result, we define the function

where the sequence is given by (2), and we consider the following information matrices

The existence of these matrices and the invertibility of are proved in Lemmas 16 and 18 in Boubacar Maïnassara et al., 2021b for weak FARIMA.

Our second main result is given in the next theorem.

Theorem 2.

(Asymptotic normality). Assume that satisfies (1). Under (A1), (A2) and (A3) with , the sequence has a limiting centered normal distribution with covariance matrix .

The detailed proof of this result is postponed to Section 4.

Remark 1.

The quantity in the definition of Le Cam’s one-step estimator (5) can be replaced by since the matrix has an explicit expression in the framework of FARIMA models (see Subsection 2.3).

It can also be replaced by

This is due to the fact that satisfies a stochastic Lipschitz condition similar to the one in Proposition 1 and that converges almost-surely to (see Lemma 1). The ergodic theorem and the uncorrelatedness of are behind the intuition of the construction of the estimator . More precisely, observe that under (A1), the matrix can be rewritten as

| (7) |

Remark 2.

Under (A1), (A2) and (A3) with , it can be shown (see Boubacar Maïnassara et al., 2021b , Lemma 18) that the sequence where, for all , , is absolutely summable. Therefore, from the stationarity of the centered process , we have

When the noise is assumed to be an iid sequence, one can use the orthogonality of with any linear combination of in particular (see Subsection 4.1) to obtain

Thus, the asymptotic covariance matrix in the strong FARIMA case is reduced to . Generally, when the noise is not an independent sequence, this simplification can not be made and we have . The true asymptotic covariance matrix obtained in the weak FARIMA framework can be very different from .

A key point allowing to establish the limit distribution of the one-step estimator of the parameters of the weak FARIMA model (1) is the fact that is a stochastic Lipschitz function.

Proposition 1.

The proof of this proposition is detailed in Section 4.

2.3 Explicit computations of

The particular structure of FARIMA models allows an explicit calculation of the matrix . Thus, the use of the closed form of the limit matrix in (5) instead of the second derivative of the function further improves the computational performance of Le Cam’s one-step estimator while maintaining the same asymptotic properties. The matrix clearly depends on the derivative of the process . This derivative can be expressed as an infinite linear combination of the past and present values of the true noise , which subsequently gives rise to a simple calculation of by exclusively exploiting the uncorrelatedness of the innovations process . Let us be more precise. Observe that from Equations (1) and (22), one has

Furthermore, for , the sequence in Equation (22) is the sequence of the coefficients in the power series of

Thus, is the th coefficient taken in . There are three cases.

-

:

Sincewe deduce that is the th coefficient of .

-

:

We haveand consequently is the th coefficient of .

-

:

In this case, and so we havewhich implies that is the th coefficient of which is equal to .

Example 1.

In this example, we illustrate the previous calculations in the case of weak FARIMA model (i.e. when in (1) and (2)). This model is widely used in practice. Since the modulus of the autoregressive parameter and the moving-average parameter are assumed to be strictly less than 1, one can easily obtain that and similarly . So, it can be shown that

and consequently, we deduce that

This explicit expression can be used in the one-step procedure to speed it up.

3 Numerical illustrations

We investigate in this section the behavior of the one-step estimator on finite sample sizes through Monte Carlo experiments. The numerical illustrations of this section are made with the open source statistical software R (R Core Team, [2021]).

3.1 Simulation studies

The behavior of Le Cam’s one-step estimator is numerically studied for FARIMA model of the form

| (8) |

where the unknown parameter takes different values. We start by comparing the asymptotic properties of the one-step estimator and the LSE in both strong and weak frameworks. For this, firstly we consider that the innovation process in (8) is an iid centered Gaussian process with common variance 1 (which corresponds to the strong FARIMA case) and secondly that it is defined by

| (9) |

where is a sequence of iid centered Gaussian random variables with variance 1. Note that the innovation process in (9) is a weak white noise which is not a martingale difference.

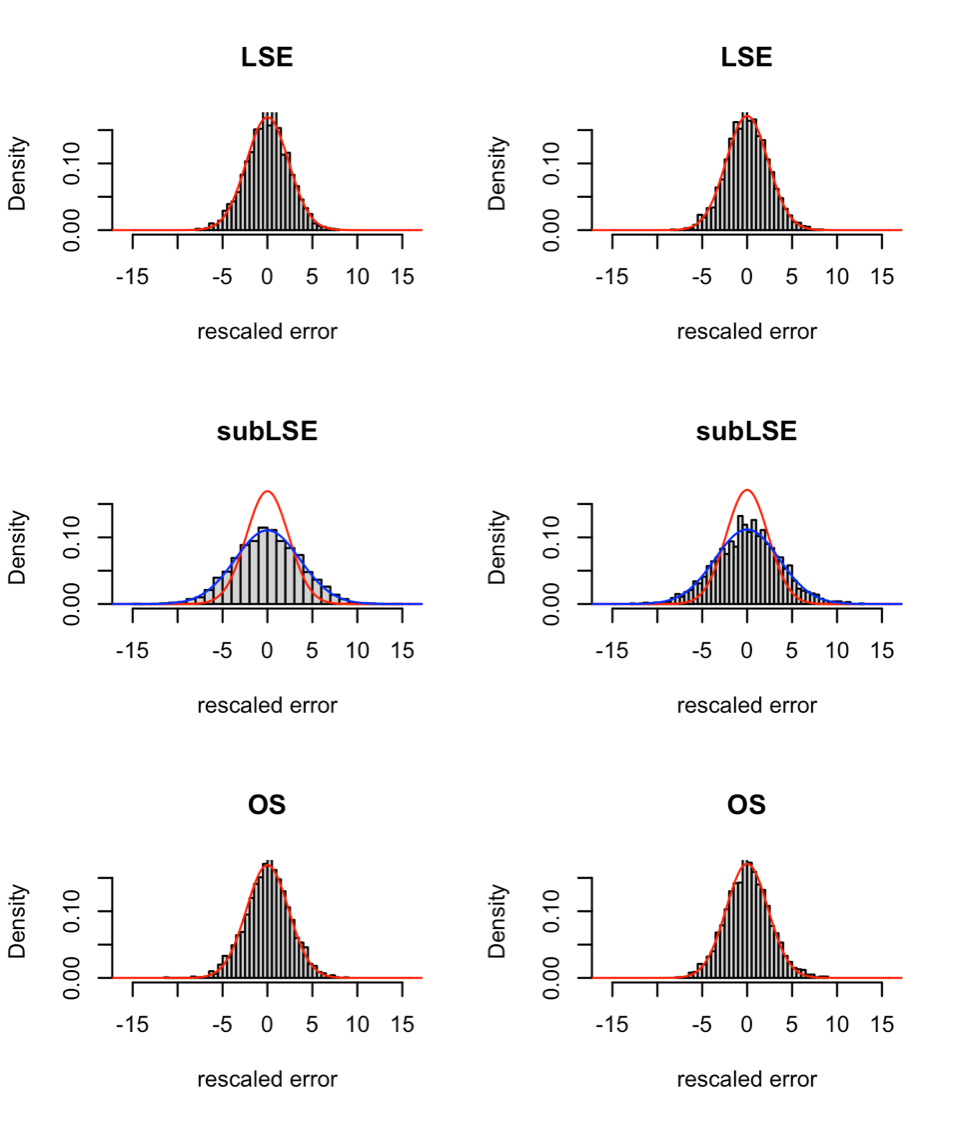

The Figure 1 compares the empirical distribution of the LSE and the Le Cam one-step estimator of the memory parameter in the strong case (first column) and the weak case (second column). We simulated independent trajectories of size of Model (8) with endowed first by the strong Gaussian noise and then by the weak noise (9). We considered that . Let us recall that the fraction defines the size of the sample on which the initial estimator is calculated.

The LSE calculated on the fraction of the data (see the two middle graphs) is computed faster than the LSE on the whole sample but is naturally less efficient. We can observe the similarity of the empirical distributions of the one-step estimator and the LSE on the whole sample. This perfectly illustrates the theoretical results presented in Subsection 2.2.

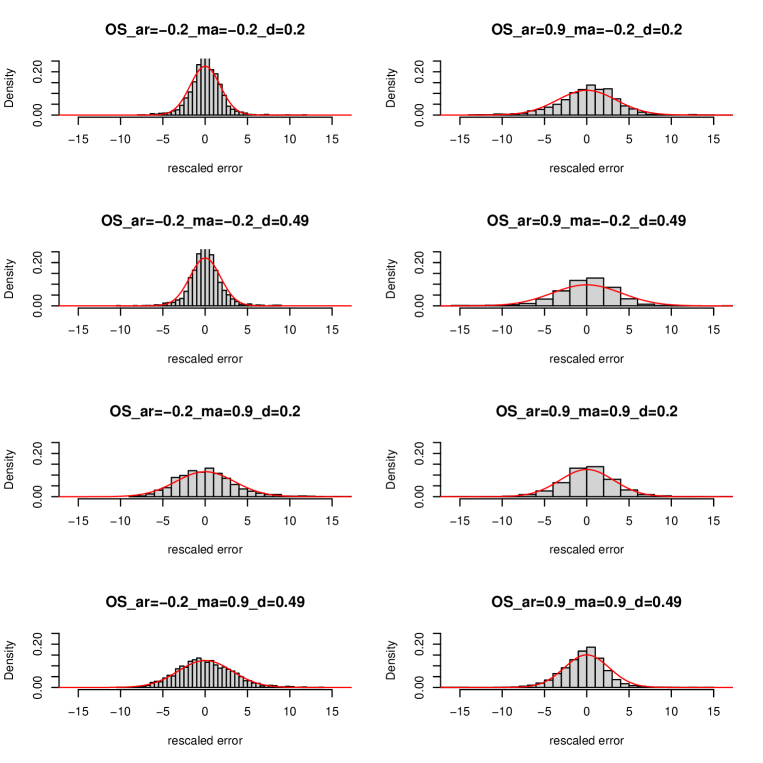

In Figure 2, we present the empirical distribution of the Le Cam one-step estimator of the memory parameter for different values of the parameters in (8) induced by the noise (9) with over the 2,000 replications. This graph highlights the adequacy of the empirical results (distributions over a finite sample size) and the theoretical results obtained in Theorem 2, even when the parameter is close to the boundary of the parameter space.

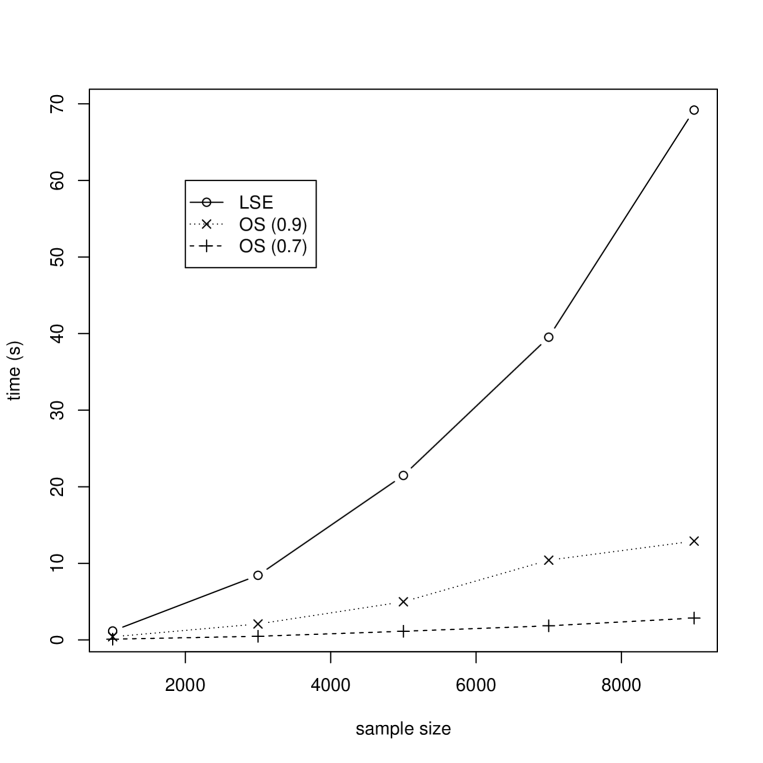

Finally, we compare in Figure 3 the computation time (in seconds), with respect to the sample size, of the LSE and the one-step estimator of all the parameters, with two different fractions ( and ) and . For each size , we simulated 10 replications to calculate the estimators. We observe that the one-step estimator outperforms the LSE in terms of computation time. It should also be noted that taking a small fraction further reduces the calculation time.

3.2 Illustrative example

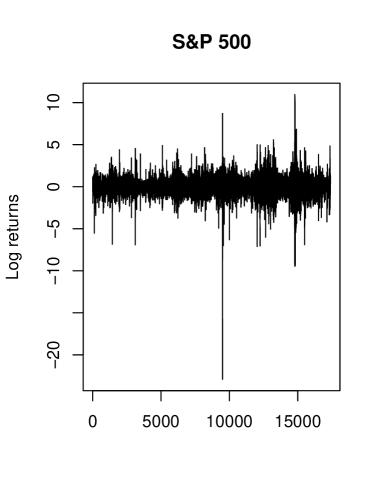

We consider in this example the daily returns of the Standard & Poor’s 500 index (S&P 500, for short). The returns (or simply returns) are defined by where is the price index of the S&P 500 at time . The observations of the S&P 500 index cover the period from January 3, 1950 to February 14, 2019. The length of the series is . The data can be downloaded with the R package quantmod.

The phenomenon of long memory has been widely studied for financial series. Ding et al., [1993] have shown that the positive powers of the absolute value of returns have more persistence than the returns themselves. We choose here the case of squared returns. The mean and the standard deviation of are and . As in Ling, [2003], we consider the centered series of the squared returns, that is, .The sample autocorrelations of the series (see Figure 5) decrease very slowly and are approximated by the function in blue (which is not integrable on ). This suggests that this series has a long memory.

It has been statistically validated in our previous work (see Boubacar Maïnassara et al., 2021a ) that the time series could be adjusted by a weak FARIMA model. It is worth emphasizing that the strong FARIMA fitting with the same orders is rejected for this series. The calibration of such models with the LSE is time consuming. Consequently, we propose a remote solution (API REST with the HTTP protocol) to provide fast and similar estimates with the same asymptotic properties as the LSE. In R, we can access to this API with the httr package using the POST command and format our data into JSON (package jsonlite). We can find an example of a program at the address https://www.effi-stats.fr/files/API_wFARIMA.R.

4 Proofs

Before starting the proofs of our main results, we introduce in the next subsection some necessary results on estimations of the coefficients of formal power series that will arise in our study.

In all our proofs, is a positive constant that may vary from line to line.

4.1 Preliminary results

We begin by recalling the following properties on power series. If for , the power series and are well defined, then is also well defined for with the sequence which is given by where denotes the convolution product between and defined by .

Now we come back to the power series that arise in our context. Remind that for the true value of the parameter,

| (10) |

Thanks to the assumptions on the moving average polynomials and the autoregressive polynomials , the power series and are well defined.

Thus the functions defined in (2) can be written as

| (11) | ||||

| (12) |

and if we denote the sequence of coefficients of the power series , we may write for all ,

| (13) |

In the same way, by (11) we have

and if we denote the coefficients of the power series one has

| (14) |

We strength the fact that for all .

For large , Hallin et al., [1999] have shown that uniformly in the sequences and satisfy

| (15) |

and

| (16) |

One difficulty that has to be addressed is that (13) includes the infinite past whereas only a finite number of observations are available to compute the estimators defined in (5). The simplest solution is truncation which amounts to setting all unobserved values equal to zero. Thus, for all and one defines

| (17) |

where the truncated sequence is defined by

In the following proposition, we show that the difference between and converges almost-surely to 0 as and this uniformly in . This proposition shows that the convergence of the least squares estimator in (6) studied in Boubacar Maïnassara et al., 2021b is not only in probability but it is almost-sure when . This last confirmation can be easily demonstrated by following line by line the proof of Theorem 1 in Francq and Zakoïan, [1998].

Proposition 2.

Let be the second-order stationary process given by (1). Under the standard assumptions of invertibility and identifiability on the autoregressive polynomial and the moving-average polynomial , we have almost-surely

| (18) |

Proof.

Remark 3.

Since, for large , and , this last proposition remains valid for the first and second derivatives of . Following the same arguments developed in the proof of Proposition 2, we have, almost-surely and for any ,

and

Since our assumptions are made on the noise in , it will be useful to express the random variables and its partial derivatives with respect to , as a function of .

From (12), there exists a sequence such that

| (19) |

where is given by the sequence of the coefficients of the power series . Consequently or, equivalently,

| (20) |

As in Hualde and Robinson, [2011], it can be shown using Stirling’s approximation that there exists a positive constant such that

| (21) |

Equation (19) and Inequality (21) imply that for all the random variable belongs to , that the sequence is an ergodic sequence and that for all the function is a continuous function. We proceed in the same way as regard to the derivatives of . More precisely, for any , and there exists sequences and such that

| (22) | ||||

| (23) |

Of course it holds that and .

Similarly, we have

| (24) | ||||

| (25) | ||||

| (26) |

where , and .

4.2 Proof of Theorem 1

We use (5) and a Taylor expansion of the function around to obtain

| (27) |

where the ’s are between and . In the two following lemmas, we show respectively the almost-sure convergence of to and that of to 0.

Lemma 1.

Under the assumptions of Theorem 1, we have almost-surely

Proof.

For any , let

and

It is clear that for any ,

| (28) |

So it is enough to show that the three terms in the right hand side of (4.2) converge almost-surely to when tends to infinity. The random variable is uncorrelated with and (this is due to (22) and (23) and the non correlation of the innovation process ). Thus, by the ergodicity of process assumed in (A1), we have

Let us now show that the term converges almost-surely to 0.

In view of (13) and (15), one successively has

Consequently, we obtain

| (29) |

Following the same approach used in (29), we have

| (30) |

A Taylor expansion implies that there exists a random variable between and such that

Proposition 2 (which implies the almost-sure convergence of the LSE to ), the ergodic theorem and Equations (29) and (30) imply that a.s.

To prove the almost-sure convergence of the first term of the right hand side of (4.2) it suffices to show that

and

converge almost-surely to 0. On one hand, we have

From (13) and (15), it follows that

Similar calculations can be done to obtain

Cesàro’s Lemma, Remark 3 and the ergodic theorem yield

On the other hand, one similarly may prove that

Thus

and the lemma is proved. ∎

Lemma 2.

Under the assumptions of Theorem 1, we have almost-surely

Proof.

The proof of the theorem follows from Proposition 2, Lemma 16 of [Boubacar Maïnassara et al., 2021b, ] and Lemmas 1 and 2.

4.3 Proof of Theorem 2

In view of (5) and by a Taylor expansion of the function around , we have

where the ’s are between and . Hence, it follows that

We use Lemmas 16-19 of Boubacar Maïnassara et al., 2021b , Proposition 1 and Slutsky’s theorem to complete the proof.

4.4 Proof of Proposition 1

For any , the mean value theorem gives

for some between 0 and 1.

In view of (4) and for all , a simple calculation of derivative leads to

where

and

We use Equations (17) and (15) to obtain

Thanks to Markov’s inequality, we deduce that

Similar calculation can be done to show that , and are bounded in probability uniformly in . It follows then that

This is enough to complete the proof.

Acknowledgments. This research benefited from the support of the ANR project "Efficient inference for large and high-frequency data" (ANR-21-CE40-0021), the "Chair Risques Émergents ou Atypiques en Assurance", under the aegis of Fondation du Risque, a joint initiative by Le Mans University and MMA company, member of Covea group and the "Chair Impact de la Transition Climatique en Assurance", under the aegis of Fondation du Risque, a joint initiative by Le Mans University and Groupama Centre-Manche company, member of Groupama group.

References

- Baillie et al., [1996] Baillie, R. T., Chung, C.-F., and Tieslau, M. A. (1996). Analysing inflation by the fractionally integrated ARFIMA-GARCH model. Journal of applied econometrics, 11(1):23–40.

- Bauwens et al., [2006] Bauwens, L., Laurent, S., and Rombouts, J. V. K. (2006). Multivariate GARCH models: a survey. J. Appl. Econometrics, 21(1):79–109.

- Beran, [1995] Beran, J. (1995). Maximum likelihood estimation of the differencing parameter for invertible short and long memory autoregressive integrated moving average models. J. Roy. Statist. Soc. Ser. B, 57(4):659–672.

- Beran et al., [2013] Beran, J., Feng, Y., Ghosh, S., and Kulik, R. (2013). Long-memory processes. Springer, Heidelberg. Probabilistic properties and statistical methods.

- Boubacar Maïnassara, [2009] Boubacar Maïnassara, Y. (2009). Estimation, validation et identification des modèles ARMA faibles multivariés. PHD thesis of Université Lille 3.

- Boubacar Maïnassara, [2011] Boubacar Maïnassara, Y. (2011). Multivariate portmanteau test for structural VARMA models with uncorrelated but non-independent error terms. J. Statist. Plann. Inference, 141(8):2961–2975.

- Boubacar Maïnassara, [2014] Boubacar Maïnassara, Y. (2014). Estimation of the variance of the quasi-maximum likelihood estimator of weak VARMA models. Electron. J. Stat., 8(2):2701–2740.

- Boubacar Maïnassara et al., [2012] Boubacar Maïnassara, Y., Carbon, M., and Francq, C. (2012). Computing and estimating information matrices of weak ARMA models. Comput. Statist. Data Anal., 56(2):345–361.

- [9] Boubacar Maïnassara, Y., Esstafa, Y., and Saussereau, B. (2021a). Diagnostic checking in FARIMA models with uncorrelated but non-independent error terms.

- [10] Boubacar Maïnassara, Y., Esstafa, Y., and Saussereau, B. (2021b). Estimating FARIMA models with uncorrelated but non-independent error terms. Stat. Inference Stoch. Process., 24:549–608.

- Boubacar Maïnassara and Francq, [2011] Boubacar Maïnassara, Y. and Francq, C. (2011). Estimating structural VARMA models with uncorrelated but non-independent error terms. J. Multivariate Anal., 102(3):496–505.

- Boubacar Maïnassara and Saussereau, [2018] Boubacar Maïnassara, Y. and Saussereau, B. (2018). Diagnostic checking in multivariate arma models with dependent errors using normalized residual autocorrelations. J. Amer. Statist. Assoc., 113(524):1813–1827.

- Box and Jenkins, [1970] Box, G. E. P. and Jenkins, G. M. (1970). Times series analysis. Forecasting and control. Holden-Day, San Francisco, Calif.-London-Amsterdam.

- Brouste and Masuda, [2018] Brouste, A. and Masuda, H. (2018). Efficient estimation of stable Lévy process with symmetric jumps. Stat. Inference Stoch. Process., 21:289–307.

- Brouste et al., [2020] Brouste, A., Soltane, M., and Votsi, E. (2020). One-step estimation for the fractional Gaussian noise model at high-frequency. ESAIM Probability and Statistics, 24:827–841.

- Dabye et al., [2018] Dabye, A., Gounoung, A., and Kutoyants, Y. (2018). Method of moments estimators and multi-step MLE for Poisson processes. Journal of Contemporary Mathematical Analysis, 53(4):187–196.

- Dahlhaus, [1989] Dahlhaus, R. (1989). Efficient parameter estimation for self-similar processes. Ann. Statist., 17(4):1749–1766.

- Ding et al., [1993] Ding, Z., Granger, C. W., and Engle, R. F. (1993). A long memory property of stock market returns and a new model. Journal of empirical finance, 1:83–106.

- Dobrushin and Major, [1979] Dobrushin, R. L. and Major, P. (1979). Non-central limit theorems for non-linear functional of gaussian fields. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 50(1):27–52.

- Fan and Yao, [2008] Fan, J. and Yao, Q. (2008). Nonlinear time series: nonparametric and parametric methods. Springer Science & Business Media.

- Fox and Taqqu, [1986] Fox, R. and Taqqu, M. S. (1986). Large-sample properties of parameter estimates for strongly dependent stationary Gaussian time series. Ann. Statist., 14(2):517–532.

- Francq et al., [2005] Francq, C., Roy, R., and Zakoïan, J.-M. (2005). Diagnostic checking in ARMA models with uncorrelated errors. J. Amer. Statist. Assoc., 100(470):532–544.

- Francq and Zakoïan, [1998] Francq, C. and Zakoïan, J.-M. (1998). Estimating linear representations of nonlinear processes. J. Statist. Plann. Inference, 68(1):145–165.

- Francq and Zakoïan, [2010] Francq, C. and Zakoïan, J.-M. (2010). GARCH Models: Structure, Statistical Inference and Financial Applications. Wiley.

- Giraitis and Surgailis, [1990] Giraitis, L. and Surgailis, D. (1990). A central limit theorem for quadratic forms in strongly dependent linear variables and its application to asymptotical normality of Whittle’s estimate. Probab. Theory Related Fields, 86(1):87–104.

- Gloter and Yoshida, [2021] Gloter, A. and Yoshida, N. (2021). Adaptive estimation for degenerate diffusion processes. Electronic Journal of Statistics, 15(1):1424–1472.

- Granger and Joyeux, [1980] Granger, C. W. J. and Joyeux, R. (1980). An introduction to long-memory time series models and fractional differencing. J. Time Ser. Anal., 1(1):15–29.

- Hallin et al., [1999] Hallin, M., Taniguchi, M., Serroukh, A., and Choy, K. (1999). Local asymptotic normality for regression models with long-memory disturbance. Ann. Statist., 27(6):2054–2080.

- Hauser and Kunst, [1998] Hauser, M. and Kunst, R. (1998). Fractionally integrated models with arch errors: with an application to the swiss 1-month euromarket interest rate. Review of Quantitative Finance and Accounting, 10(1):95–113.

- Hosking, [1981] Hosking, J. R. M. (1981). Fractional differencing. Biometrika, 68(1):165–176.

- Hualde and Robinson, [2011] Hualde, J. and Robinson, P. M. (2011). Gaussian pseudo-maximum likelihood estimation of fractional time series models. Ann. Statist., 39(6):3152–3181.

- Hurst, [1951] Hurst, H. E. (1951). Long-term storage capacity of reservoirs. Trans. Amer. Soc. Civil Eng., 116:770–799.

- Kamatani and Uchida, [2015] Kamatani, K. and Uchida, M. (2015). Hybrid multi-step estimators for stochastic differential equations based on sampled data. Stat. Inference Stoch. Process., 18:177–204.

- Kutoyants and Motrunich, [2016] Kutoyants, Y. and Motrunich, A. (2016). On multi-step MLE-process for Markov sequences. Metrika, 79:705–724.

- Le Cam, [1956] Le Cam, L. (1956). On the asymptotic theory of estimation and testing hypothesis. Proc. 3rd Berkeley Sympos. Math. Statist. Probability 1, 129-156 (1956).

- Ling, [2003] Ling, S. (2003). Adaptive estimators and tests of stationary and nonstationary short- and long-memory ARFIMA-GARCH models. J. Amer. Statist. Assoc., 98(464):955–967.

- Ling and Li, [1997] Ling, S. and Li, W. K. (1997). On fractionally integrated autoregressive moving-average time series models with conditional heteroscedasticity. J. Amer. Statist. Assoc., 92(439):1184–1194.

- Lütkepohl, [2007] Lütkepohl, H. (2007). New Introduction to Multiple Time Series Analysis. Springer Berlin Heidelberg.

- Mandelbrot, [1965] Mandelbrot, B. B. (1965). Une classe de processus stochastiques homothétiques à soi; application à la loi climatologique de H. E. Hurst. 260:3274–3277.

- Mandelbrot and Van Ness, [1968] Mandelbrot, B. B. and Van Ness, J. W. (1968). Fractional Brownian motions, fractional noises and applications. SIAM Rev., 10:422–437.

- [41] Mandelbrot, B. B. and Wallis, J. R. (1969a). Computer experiments with fractional gaussian noises: Part 1, averages and variances. Water Resources Research, 5(1):228–241.

- [42] Mandelbrot, B. B. and Wallis, J. R. (1969b). Computer experiments with fractional gaussian noises: Part 2, rescaled ranges and spectra. Water Resources Research, 5(1):242–259.

- [43] Mandelbrot, B. B. and Wallis, J. R. (1969c). Computer experiments with fractional gaussian noises: Part 3, mathematical appendix. Water Resources Research, 5(1):260–267.

- Palma, [2007] Palma, W. (2007). Long-memory time series. Wiley Series in Probability and Statistics. Wiley-Interscience [John Wiley & Sons], Hoboken, NJ. Theory and methods.

- R Core Team, [2021] R Core Team (2021). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Shao, [2010] Shao, X. (2010). Nonstationarity-extended Whittle estimation. Econometric Theory, 26(4):1060–1087.

- Shao, [2011] Shao, X. (2011). Testing for white noise under unknown dependence and its applications to diagnostic checking for time series models. Econometric Theory, 27(2):312–343.

- Shao, [2012] Shao, X. (2012). Parametric inference in stationary time series models with dependent errors. Scand. J. Stat., 39(4):772–783.

- Taqqu and Teverovsky, [1997] Taqqu, M. S. and Teverovsky, V. (1997). Robustness of Whittle-type estimators for time series with long-range dependence. Comm. Statist. Stochastic Models, 13(4):723–757. Heavy tails and highly volatile phenomena.

- Tong, [1990] Tong, H. (1990). Non-linear time series: a dynamical system approach. Oxford University Press.

- Whittle, [1953] Whittle, P. (1953). Estimation and information in stationary time series. Ark. Mat., 2:423–434.